keppel land in vietnam content - keppel corporation in vietnam - apr...2 3 keppel land’s overseas...

TRANSCRIPT

1

KLL

Keppel Land in Vietnam Investor Meetings

April 2008

2

Keppel Land’s Overseas Strategy

Introduction to Vietnam

Market Review and Outlook

Keppel Land’s Investments in Vietnam

Going Forward

Content

2

3

Keppel Land’s Overseas Strategy

4

Embarked on internationalisation drive in early 1990s to broaden earnings growth geographically

– China and Vietnam among the first countries that Keppel Land invested in

Focus on property development for sale to tap on demand for quality housing in Asia

Develop premier landmarks in the region to grow sustainable earnings

International Strategy

3

5

Continue focus on China, Vietnam, India and Indonesia

Launch 18,000 township and integrated lifestyle homes to tap on demand for quality housing across Asia and the Middle East

Two-pronged efforts focusing on :

(a) Residential projects and large-scale townships

(b) Integrated lifestyle developments

International Strategy

6

First-mover advantage : Forayed into Vietnam in early 1990s

– Jul 1991 : Entered Hanoi to develop International Centre

– Feb 1992 : Entered HCMC to develop Saigon Centre

Pioneer property developer with strong brand name and expertise

– Largest foreign developer in Vietnam

– Developed good networks and reputation

Early Head-start in Vietnam

4

7

Total asset value : S$360.7m

– 16.4% of Group’s overseas assets @ end-2007

– 6% of Group’s total assets @ end-2007

Profit contribution

– 13.8% of Group’s PATMI from overseas @ end-2007

– 5.5% of Group’s PATMI @ end-2007

Asset Value and Profit Contribution

8

Built up portfolio of prime residential developments, townships,Grade A commercial buildings, and serviced apartments in HCMC, Hanoi, Dong Nai and Vung Tau

Sixfold increase in residential landbank to 53 mil sf

– Acquired 8 residential sites in 2007

– Pipeline of more than 25,000 homes

– Lifestyle waterfront developments fronting Saigon River, Ca Cam River, Rach Chiec River and Dong Nai River

Strong Presence in Vietnam

5

9

Introduction to Vietnam

10

Area : 329,560 sq km

Coastline : 3,444 km

Capital : Hanoi

Commercial hub : Ho Chi Minh City

Total population : 86 mil

- 13th most populous country in the world

- 70% below 35 years old- HCMC : 8 mil- Hanoi : 4 mil

Literacy rate : 96%

Key Facts

6

11

Economic Transformation

Doi Moi : Shift from centrally-planned to market-oriented economy

– About 230,000 private enterprises currently– Housing Law (2000) opened up real estate market– Deregulation of banking industry (2007)

Integration with global economies

Launch of Doi Moireforms

Member of ASEAN

Signed US-Vietnam Bilateral Trade Agreement

Established Permanent Normal Trade Relations with the US

Member of WTO

Member of APEC

Non-permanent member of UN Security Council for two years

1998 2001 2006 2007 200819951986

12

Third largest economy in Asia after China and India

– Sustained economic growth of 8% p.a. for past five years

– Record GDP growth of 8.5% in 2007

– Size of GDP : US$69.9b

FDI surged about 70% to US$20.3b in 2007

– Fuelled by economic reforms and pro-investor policies

Robust Economic Growth

7

13

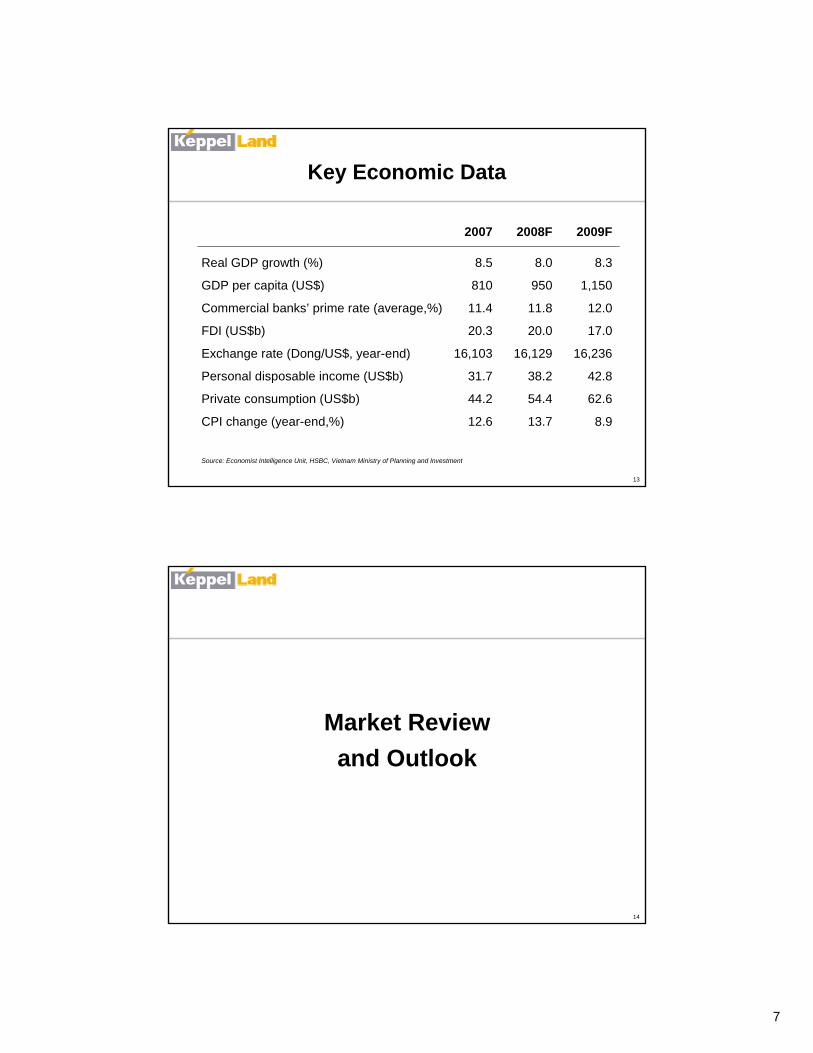

2007 2008F 2009F

Real GDP growth (%) 8.5 8.0 8.3

GDP per capita (US$) 810 950 1,150

Commercial banks’ prime rate (average,%) 11.4 11.8 12.0

FDI (US$b) 20.3 20.0 17.0

Exchange rate (Dong/US$, year-end) 16,103 16,129 16,236

Personal disposable income (US$b) 31.7 38.2 42.8

Private consumption (US$b) 44.2 54.4 62.6

CPI change (year-end,%) 12.6 13.7 8.9

Source: Economist Intelligence Unit, HSBC, Vietnam Ministry of Planning and Investment

Key Economic Data

14

Market Review and Outlook

8

15

Prices still relatively affordable compared to other Asian markets

Limited supply to meet strong demand

Housing demand drivers :-

Growing affluence and fast-growing middle class

– Strong homeownership aspirations especially in well-planned residential enclaves

– Average per capita income in HCMC : US$2,180

Increasing affordability

– Availability of mortgages of up to 50-70% of value of property

– Mortgage rates of 12% pa

– Loan quantum : 10-15 years

Residential Market

16

Housing demand drivers (con’t) :-

Buoyant Stock Market

– Firms listed on stock market up from 40 in 2005 to 280 currently

Liberalisation of government policies

– Housing Law (Jul 06) : Viet Kieus allowed to buy houses in Vietnam

– Real Estate Trading Law (Jan 07) : Transparency in property transactions

Rapid urbanisation rate

– Forecast to reach 33% by 2010 and 45% by 2020, from 27% currently

– Additional 103 mil sm of housing needed to reach 14.2 sm per capita average housing target by 2010

Returning Viet Kieus as investors

– Remittances in 2007 : US$5.6b, up 7.7% y-o-y

Residential Market

9

17

Strong economic growth and rising FDI fuel expansion and upgrading

– Additional demand for CBD space from entry of international banks

Grade A space : Fully occupied

– Limited Grade A space, with no new supply in near-term

Grade A office rentals up 97% y-o-y

– US$63 psm per month in HCMC @ end-2007

Office Market

18

Growing number of expatriates with the country’s integration with global markets

Limited supply of quality serviced apartments and rental apartments

Average 98% occupancy for Grade A serviced apartments in HCMC and Hanoi

Current rates

– US$40 - $45 psm per month in HCMC

– US$35 - $40 psm per month in Hanoi

Serviced Apartments

10

19

Keppel Land’s Investments in Vietnam

20

Residential Developments

11

21

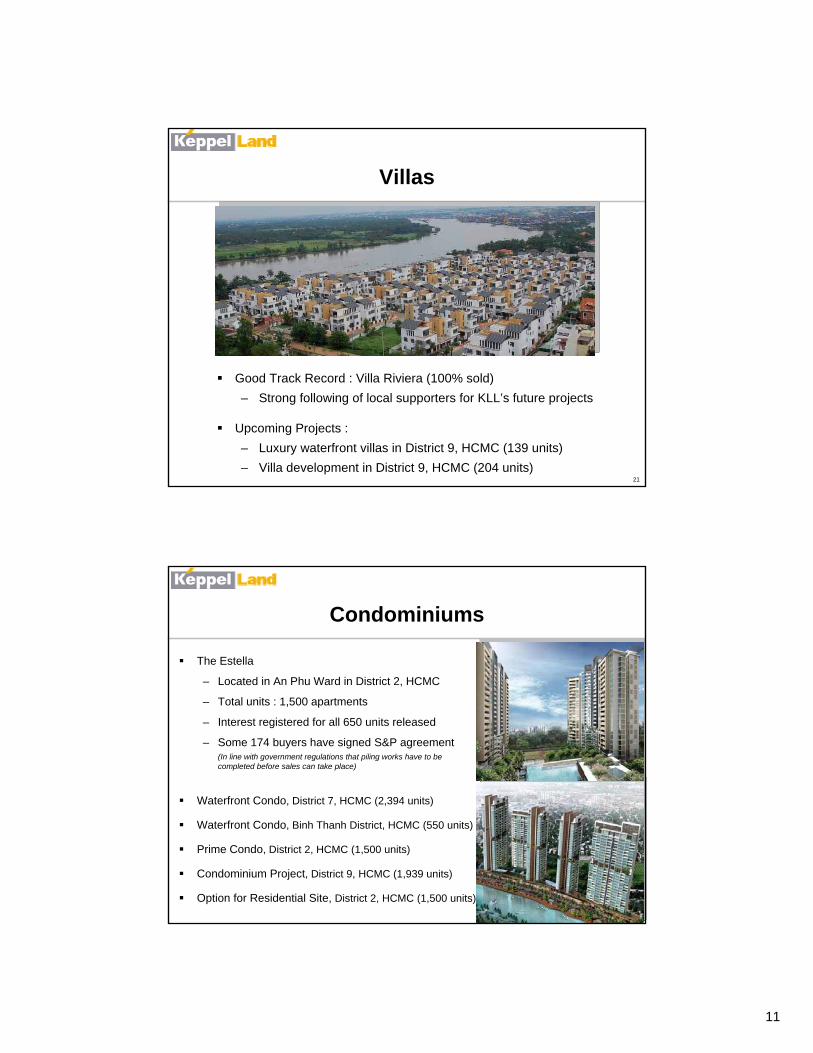

Villas

Good Track Record : Villa Riviera (100% sold)– Strong following of local supporters for KLL’s future projects

Upcoming Projects :– Luxury waterfront villas in District 9, HCMC (139 units)– Villa development in District 9, HCMC (204 units)

22

The Estella

– Located in An Phu Ward in District 2, HCMC

– Total units : 1,500 apartments

– Interest registered for all 650 units released

– Some 174 buyers have signed S&P agreement (In line with government regulations that piling works have to be completed before sales can take place)

Condominiums

Waterfront Condo, District 7, HCMC (2,394 units)

Waterfront Condo, Binh Thanh District, HCMC (550 units)

Prime Condo, District 2, HCMC (1,500 units)

Condominium Project, District 9, HCMC (1,939 units)

Option for Residential Site, District 2, HCMC (1,500 units)

12

23

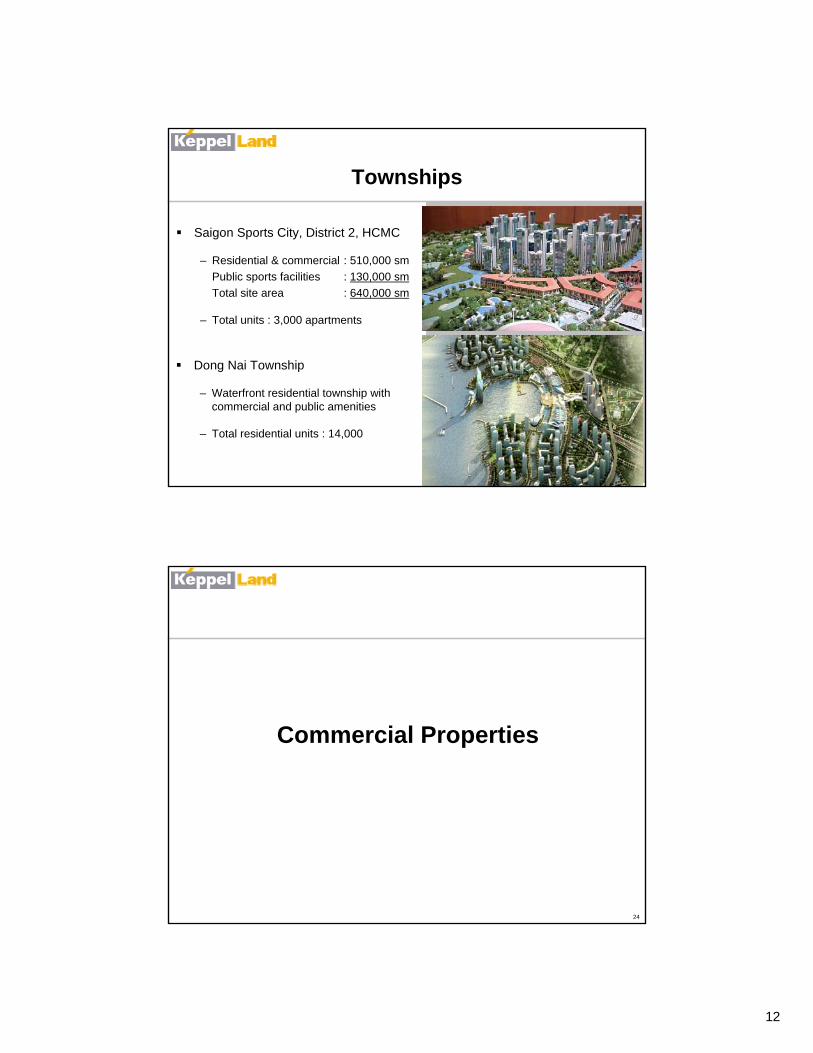

Saigon Sports City, District 2, HCMC

– Residential & commercial : 510,000 smPublic sports facilities : 130,000 smTotal site area : 640,000 sm

– Total units : 3,000 apartments

Townships

Dong Nai Township

– Waterfront residential township with commercial and public amenities

– Total residential units : 14,000

24

Commercial Properties

13

25

Landmark building located at prime Le LoiBoulevard in HCMC’s CBD

Phase 1 completed in 1996Office - 10,433 smRetail - 3,663 smServiced Apartments - 89 units

100% occupancy

Tenants include:

Office : Deutsche Bank, GE, Motorola, Mitsubishi, AIG, Temasek Holdings, Consular offices of Singapore and Poland, and US Commercial Services

Retail : Mango, Highlands Coffee

Serviced apartments : Managed by Sedona Hotels International

Saigon Centre – Phase 1

26

Saigon Centre – Future Phases

Subsequent phases to be developed into integrated development

Appointed Skidmore, Ownings and Merrill (SOM) to design new concept plans

– Contribute to enhancing position of HCMC as a global city

– Revise masterplan to develop world-class iconic development

Construction of Phase 2 scheduled to commence in end-2009

State-of-the-art green technology in building design

14

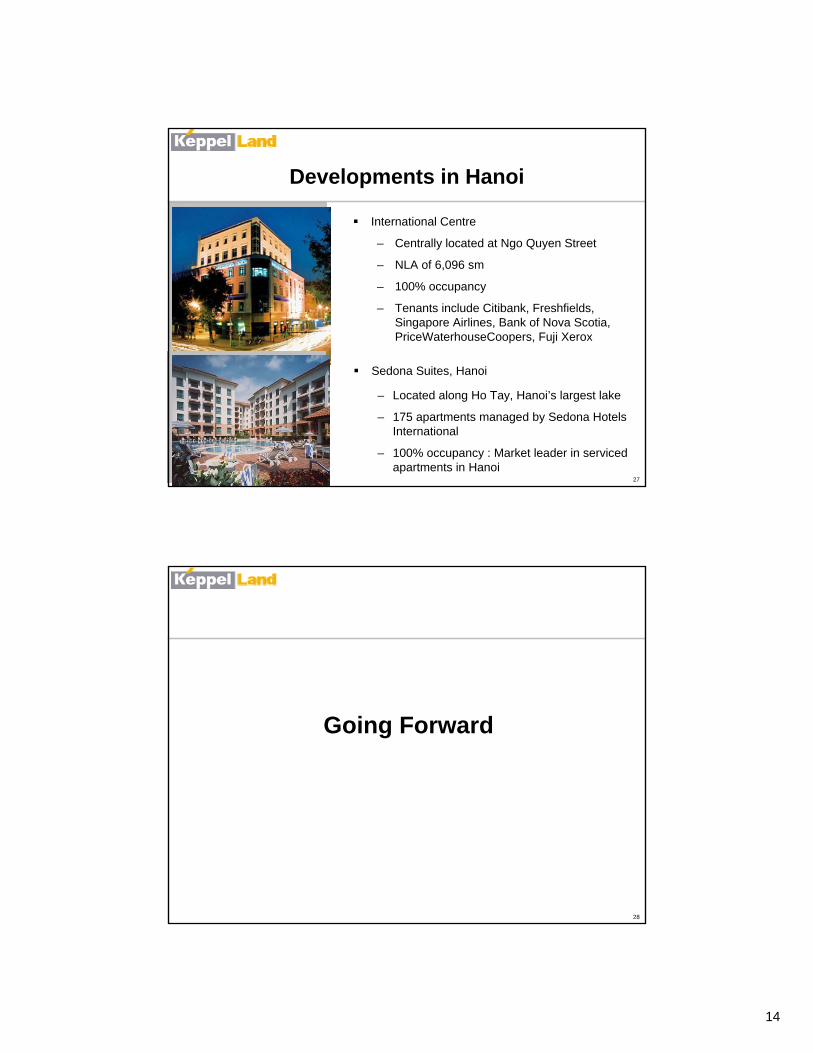

27

International Centre

– Centrally located at Ngo Quyen Street

– NLA of 6,096 sm

– 100% occupancy

– Tenants include Citibank, Freshfields, Singapore Airlines, Bank of Nova Scotia, PriceWaterhouseCoopers, Fuji Xerox

Developments in Hanoi

Sedona Suites, Hanoi

– Located along Ho Tay, Hanoi’s largest lake

– 175 apartments managed by Sedona Hotels International

– 100% occupancy : Market leader in serviced apartments in Hanoi

28

Going Forward

15

29

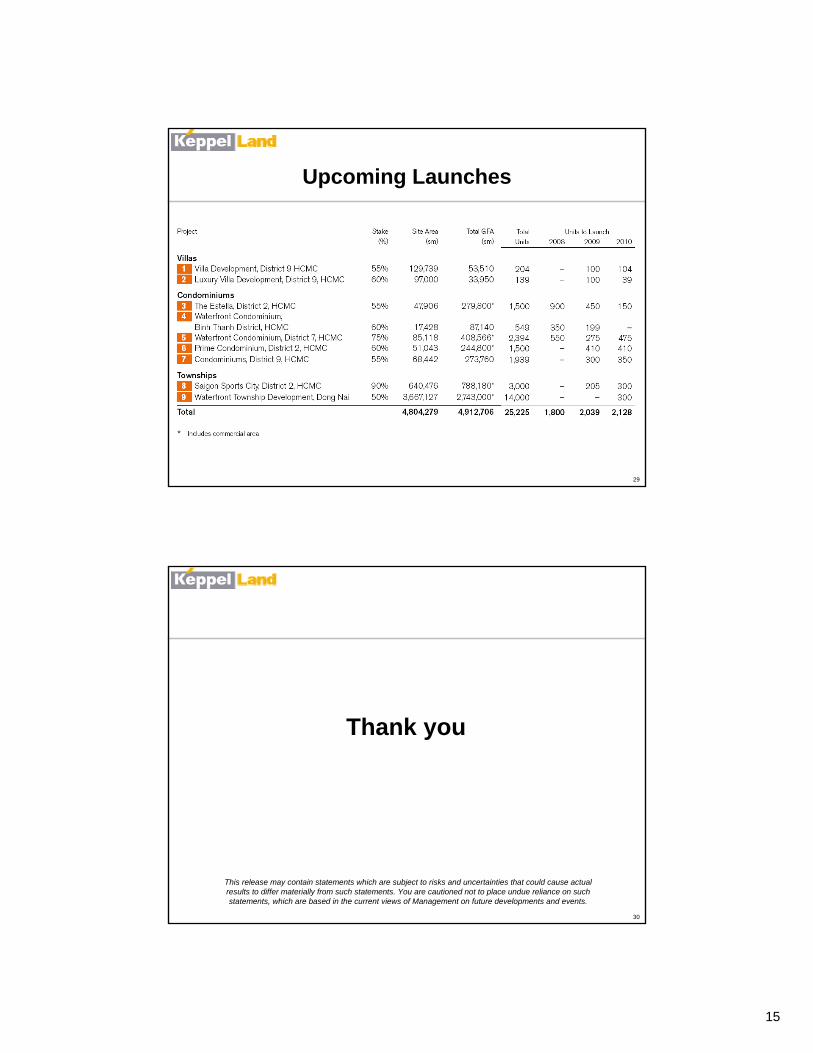

Upcoming Launches

30

Thank you

This release may contain statements which are subject to risks and uncertainties that could cause actual results to differ materially from such statements. You are cautioned not to place undue reliance on such statements, which are based in the current views of Management on future developments and events.