kenmare resources plc/media/files/k/kenmare... · 3 . moma titanium minerals mine in mozambique one...

TRANSCRIPT

1

Kenmare Resources plc

June 2013

2

This Confidential Presentation (the “Presentation”) has been prepared and issued by Kenmare Resources plc (the “Company” or “Kenmare”). While this Presentation has been prepared in good faith, the Company and its respective officers, employees, agents and representatives expressly disclaim any and all liability for the contents of, or omissions from, this Presentation, and for any other written or oral communication transmitted or made available to the recipient or any of its officers, employees, agents or representatives. No representations or warranties are or will be expressed or are to be implied on the part of the Company, or any of its respective officers, employees, agents or representatives in or from this Presentation or any other written or oral communication from the Company, or any of its respective officers, employees, agents or representatives concerning the Company or any other factors relevant to any transaction involving the Company or as to the accuracy, completeness or fairness of this Presentation, the information or opinions on which it is based, or any other written or oral information made available in connection with the Company.

This Presentation does not constitute or form part of, and should not be construed as, an offer, invitation or inducement to purchase or subscribe for any securities of the Company nor shall it or any part of it form the basis of, or be relied upon in connection with, any contract or investment decision relating to such securities, nor does it constitute a recommendation regarding the securities of the Company.

This Presentation is as of the date hereof. This Presentation includes certain statements, estimates and projections provided by the Company with respect to the anticipated future performance of the Company or the industry in which it operates. Such statements, estimates and projections reflect various assumptions and subjective judgments by the Company’s management concerning anticipated results, certain of which assumptions and judgments may be significant in the context of the statements, estimates and projections made. These assumptions and judgments may or may not prove to be correct and there can be no assurance that any projected results are attainable or will be realised. In particular, certain statements in this Presentation relating to future financials, results, plans and expectations regarding the Company’s business, growth and profitability, as well as the general economic conditions to which the Company is exposed, are forward looking by nature and may be affected by a variety of factors. The Company is under no obligation to update or keep current the information contained in this Presentation, to correct any inaccuracies which may become apparent, or to publicly announce the result of any revision to the statements made herein and any opinions expressed in the Presentation or in any related materials are subject to change without notice.

Disclaimer

2

3

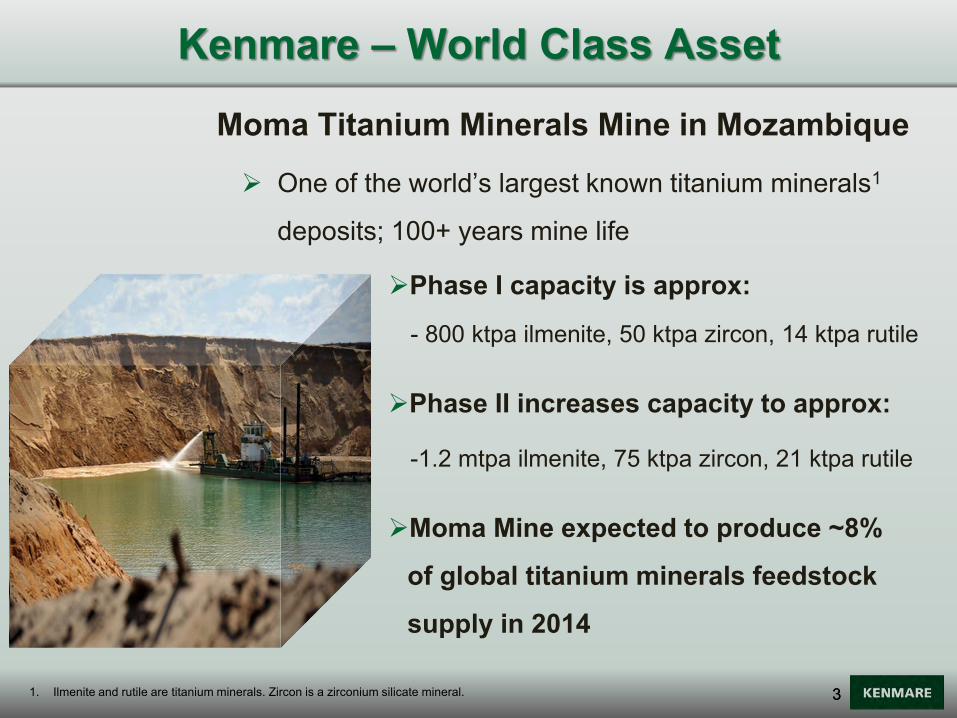

Moma Titanium Minerals Mine in Mozambique

One of the world’s largest known titanium minerals1

deposits; 100+ years mine life

Phase I capacity is approx:

- 800 ktpa ilmenite, 50 ktpa zircon, 14 ktpa rutile

Phase II increases capacity to approx:

-1.2 mtpa ilmenite, 75 ktpa zircon, 21 ktpa rutile

Moma Mine expected to produce ~8%

of global titanium minerals feedstock

supply in 2014

Kenmare – World Class Asset

3 1. Ilmenite and rutile are titanium minerals. Zircon is a zirconium silicate mineral.

4

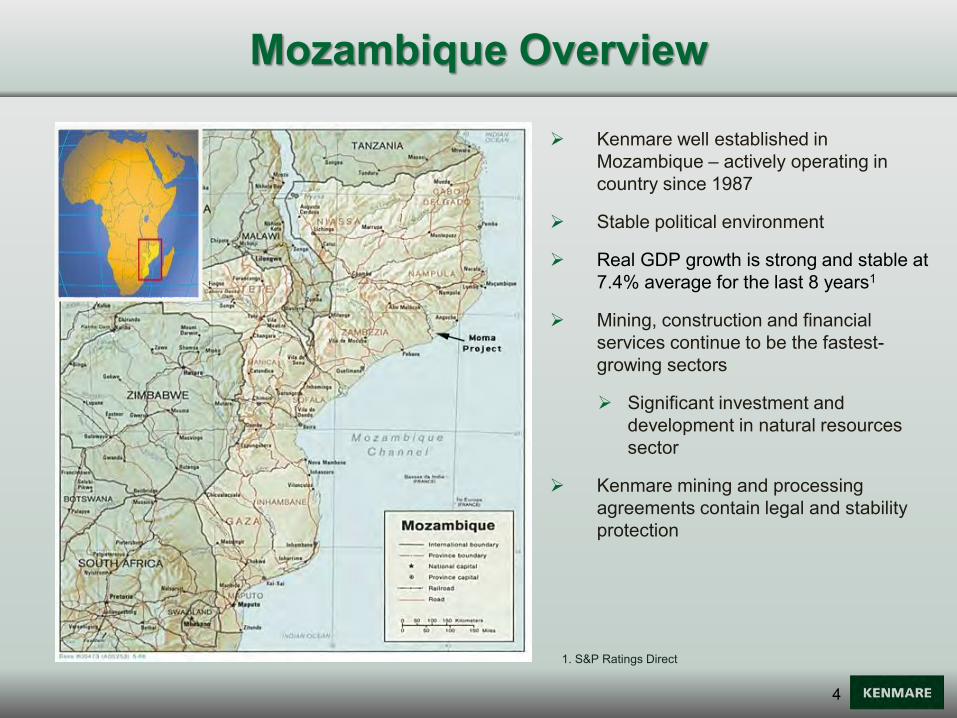

Mozambique Overview

Kenmare well established in Mozambique – actively operating in country since 1987

Stable political environment

Real GDP growth is strong and stable at 7.4% average for the last 8 years1

Mining, construction and financial services continue to be the fastest-growing sectors

Significant investment and development in natural resources sector

Kenmare mining and processing agreements contain legal and stability protection

1. S&P Ratings Direct

5

Key Company Highlights

Long life ore body producing high quality products

Low cost mining, efficient materials handling, well-established producer

50% expansion in commissioning, with vast majority of capex spent

Significant share of global feedstock supply of titanium minerals

Favourable mineral sands supply/demand dynamics

Important asset for Mozambique

5

6

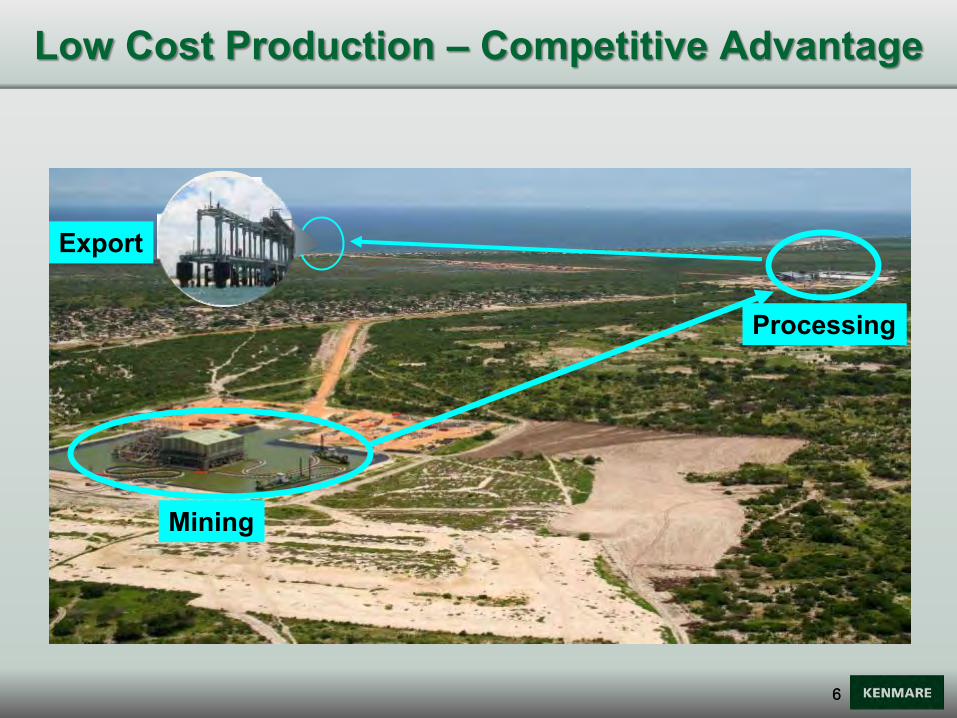

Low Cost Production – Competitive Advantage

Export

Mining

Processing

6

7

Dredge Mining & Wet Concentrator Plant

7

8

Mineral Separation Plant

8 Mineral Separation Plant before Expansion

9

Significant Increase in Loading Capacity & Availability

Export Facilities

Northern Wharf Upgraded 2nd Wharf Added to Jetty

9

10

Current mine area WCP A to 2024 WCP B to 2020

100+ year life at Phase II expanded production level1

Dredge Path WCP A

Dredge Path WCP B

Namalope dredge path plan

Moma Mine – Resource Base Map

10 1. Based on mining reserves and resources under licence.

11

Monthly Production 2013

-

20,000

40,000

60,000

80,000

100,000

120,000

Jan-13 Feb-13 Mar-13 Apr-13 May-13

tonn

es

HMC Monthly Production

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Jan-13 Feb-13 Mar-13 Apr-13 May-13

tonn

es

Ilmenite Monthly Production

- 500

1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500

Jan-13 Feb-13 Mar-13 Apr-13 May-13

tonn

es

Zircon Monthly Production Secondary Zircon

Primary Zircon

12

Transition onto Dunal Plateau – April/May 2013

Raised natural topography

Side berm completed

Dunal plateau

WCP B

13

Transition onto Dunal Plateau – April/May 2013

Side berm completed

Dunal plateau

Raised natural topography

WCP B

14

Power Reliability Electrical Supply Stability

SVC at Mocuba – now commissioned, improved stability

SVC upgrade at Alto Molocue – now commissioned

Voltage Stabilisation Equipment (Dip Doctor) – expected to be completed mid-2013

Improved Network Voltage Support

Installation of network capacitors at Nampula – now commissioned

Installation of network capacitors at Moma – completed and ready for commissioning as Expansion load increases

Installation of network capacitors at Alto Molocue – completed and commissioned

15

Health & Safety

Kenmare LTIFR 0.25 Compares favourably with South African Mineral Sands Peers

15

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13

12 Month Rolling Lost Time Injury Frequency Rate

16

Kenmare Moma Development Association

Five-Year Plan being Implemented

Support from First Class Partners:

WWF, FMO, Clusa, Mozmed & MIGA

Community Projects:

Health Projects: Health Clinic at Moma

in construction phase, Malaria

Eradication

Income Generation: Savings & Credit,

Horticulture, Poultry, Sewing, Animal

Husbandry, Salt

Socio-Cultural: Schools, Sports,

Scholarships

17

Phase II Expansion

18

Existing Wet Concentrator Plant A (WCP A)

Upgrade WCP A expected to increase spiral feed capacity from 3,000 to 3,500 tph

New Wet Concentrator Plant B (WCP B)

Installation of 2nd mining plant consisting of:

WCP with spiral feed capacity of 2,000 tph

Starter pond

3rd dredge

WCP spirals modular design allows for easier future capacity increases

Addition of WCP B will not interfere with existing operations

Planned WCP B move to the Nataka deposit in 2020 and WCP A in 2024

Phase II Expansion – Mining

New facilities

Existing facilities

2,000 tph of mineral sands

ore

2,000 tph of mineral sands

ore

>2,000 tph of mineral sands

ore

Dredge 2 Dredge 3 Dredge 1

WCP A 3,000 tph

Existing capacity

Heavy minerals concentrate to the processing plant

+ 500 tph additional capacity

WCP B 2,000 tph capacity

Dredge Path WCP A

Dredge Path WCP B

Enhanced HMC production design

Namalope dredge path plan

19

Phase II Expansion – Processing

Mineral Separation Plant (MSP)

Expanding capacity from 135 tph to an expected 225 tph

New Wet High Intensity Magnetic Separation (WHIMS) circuit More efficient upfront separation of

Magnetic and Non-magnetic minerals Enhanced efficiency of existing

operation

Modular approach to construction to avoid disruption to existing operations

Enhanced non-magnetic circuit with additional driers

Upgrade of associated infrastructure and equipment, particularly electricity and water supply

New Wet High Intensity Magnet

Separation (WHIMS)

105 tph magnetic stream

80 tph magnetic stream

40 tph of non-magnetic stream

225 tph of heavy minerals concentrate (HMC) feed

Enhanced processing plant design

Zircon & rutile Ilmenite Ilmenite

New facilities Existing facilities

Enhanced non-magnetic circuit

Existing ilmenite circuit New Auxiliary

Ilmenite circuit

20

Expansion Progress – Dredge

3rd Dredge fully commissioned and mining ore

21

Expansion Progress – WCP B

WCP B Processing ore

22

Moma Mine – Processing

New WHIMS

Existing MSP

Extended Storage

New Aux Ilmenite

New Storage

New Belt filter

23

Expansion Progress – WHIMS

Processing HMC

24

Expansion Progress

WHIMS concentrate coming through

25

Expansion Progress – Auxiliary Ilmenite Plant

Ready to process concentrate

26

Expansion Progress – Product Storage

Storage shed complete

27

Industry Overview

28

Pigment90%

Metal5%

Other5%

Paint58%Plastics

22%

Paper9%

Inks4%

Fibres2%

Others5%Kronos 8%

Huntsman 9%

Tronox 7%

Sachtleben 6%

ISK 3%Others 9%

DuPont 19%

China 27%

Cristal Global 12%

Description End uses

Demand For TiO2 Feedstock Is Primarily Driven By Pigment Consumption

TiO2 Feedstock consumption 20111 Pigment producers 20112 Pigment consumption by end-use sector 20112

Ilmenite and rutile are naturally occurring minerals containing TiO2

Ilmenite contains between 45% and 62% of TiO2 while rutile contains between 94% and 96%

Ilmenite and rutile occur predominantly in the form of heavy mineral sands. However, hard rock deposits are also found mainly in Norway and Canada

The main ilmenite producing countries are South Africa, Australia and Canada. Together, they account for the majority of global ilmenite production most of which is beneficiated

Titanium feedstocks are used predominantly to produce titanium dioxide pigment that is favoured for its brilliant whiteness, excellent opacity, non-toxicity and inertness

Rutile and beneficiated ilmenite are the main raw materials used to make titanium metal. Titanium metal’s unique properties including its high strength to weight ratio, high melting point and its resistance to corrosion make it the preferred metal for a number of demanding applications such as the manufacture of airframes and jet engines for the aerospace industry

Other end-uses include fluxes and welding rod coatings

Source: 1 Kenmare estimate 2 TZMI TiO2 Pigment Annual Review June 2012

29

Description End uses

Zircon consumption by end use sector 20111

Zircon millers 20111 Geographical zircon consumption 20111

Demand For Zircon Is Primarily Driven By The Ceramics Industry

Other 2%

Zirconia & Zr

chemicals

18%

TV Glass 2%

Foundry 11%

Refractory 11%

Ceramics 56%

China40%

Europe25%

North America

8%

Japan3%

Rest of World

24%Bitossi21%

Endeka11%

Mario Pilato Blat7%Trebol

7%Kreutz

5%

Others49%

Zircon is a zirconium silicate mineral produced as a co-product of titanium minerals mining

Most zircon production is located in Australia and Southern Africa

In the ceramics industry for the production of opacifier and frit compounds for decorative wall and floor tiles and sanitary ware

Foundry and refractory applications for steel and glass industries Fused zirconia, zirconium chemicals used for ceramics

pigments, wear materials and various chemical applications Zirconium metal used primarily in the nuclear industry

Source: 1 Kenmare estimates

30

0

1,000

2,000

3,000

4,000

5,000

6,000

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

Global Pigment Demand (1991 - 2011)('000 tonnes)

China WORLD

3.0% CAGR

17.0% CAGR

China - Key Source Of Growth In Pigment Demand For 20 Years Pigment Demand Growth for 20 Years

31

Source: Kenmare pigment demand forecast based on consensus GDP growth (Economist Intelligence Unit / IHS Global Insight / IMF)

Future Pigment Demand Expected To Grow At Above Historical Growth Rate

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Global Pigment Demand 1991- 2020('000 tonnes)

BASE DOWN UPSIDE ACTUAL 3% trend

Historical 3.0% CAGR from 1991 to 2011

Growth 2011 to 2020

UPSIDE CASE 3.9% CAGRBASE CASE 3.1% CAGR

DOWNSIDE CASE 2.8% CAGR

32

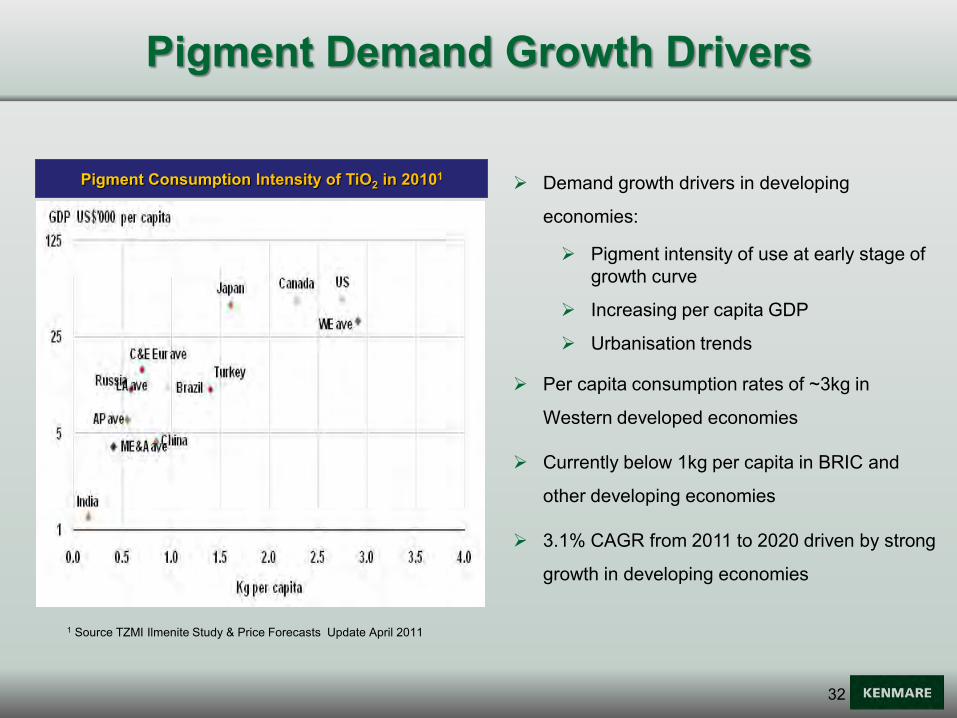

Pigment Demand Growth Drivers

Pigment Consumption Intensity of TiO2 in 20101

1 Source TZMI Ilmenite Study & Price Forecasts Update April 2011

Demand growth drivers in developing

economies:

Pigment intensity of use at early stage of growth curve

Increasing per capita GDP

Urbanisation trends

Per capita consumption rates of ~3kg in

Western developed economies

Currently below 1kg per capita in BRIC and

other developing economies

3.1% CAGR from 2011 to 2020 driven by strong

growth in developing economies

33

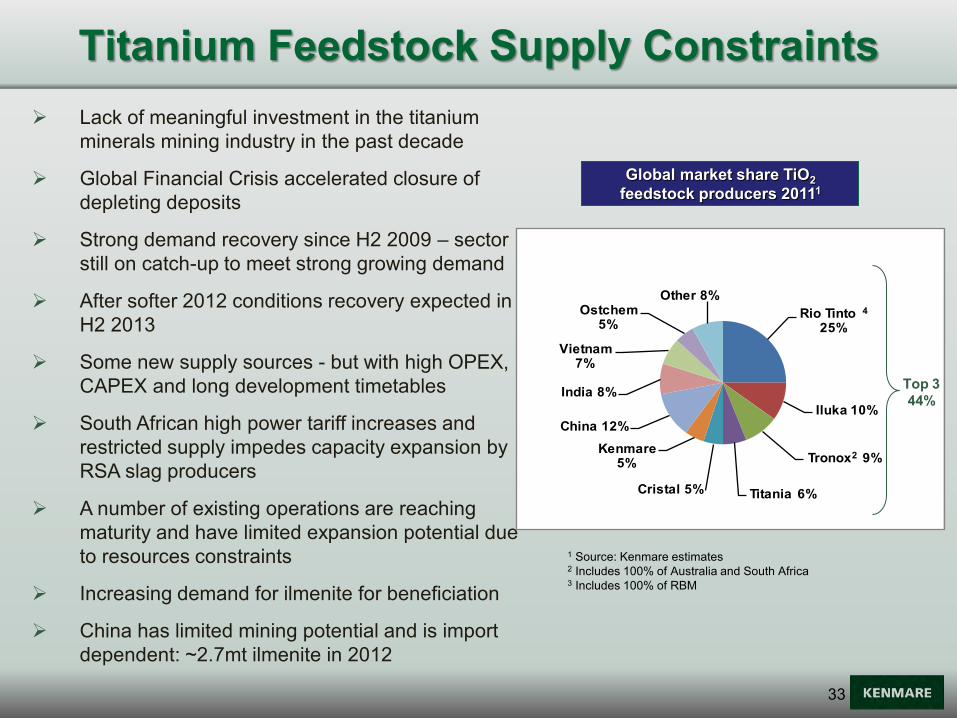

Lack of meaningful investment in the titanium minerals mining industry in the past decade

Global Financial Crisis accelerated closure of depleting deposits

Strong demand recovery since H2 2009 – sector still on catch-up to meet strong growing demand

After softer 2012 conditions recovery expected in H2 2013

Some new supply sources - but with high OPEX, CAPEX and long development timetables

South African high power tariff increases and restricted supply impedes capacity expansion by RSA slag producers

A number of existing operations are reaching maturity and have limited expansion potential due to resources constraints

Increasing demand for ilmenite for beneficiation

China has limited mining potential and is import dependent: ~2.7mt ilmenite in 2012

Global market share TiO2 feedstock producers 20111

51%

Titanium Feedstock Supply Constraints

Rio Tinto 4

25%

Iluka 10%

Tronox2 9%

Titania 6%Cristal 5%

Kenmare 5%

China 12%

India 8%

Vietnam 7%

Ostchem 5%

Other 8%

Top 3 44%

1 Source: Kenmare estimates 2 Includes 100% of Australia and South Africa 3 Includes 100% of RBM

34

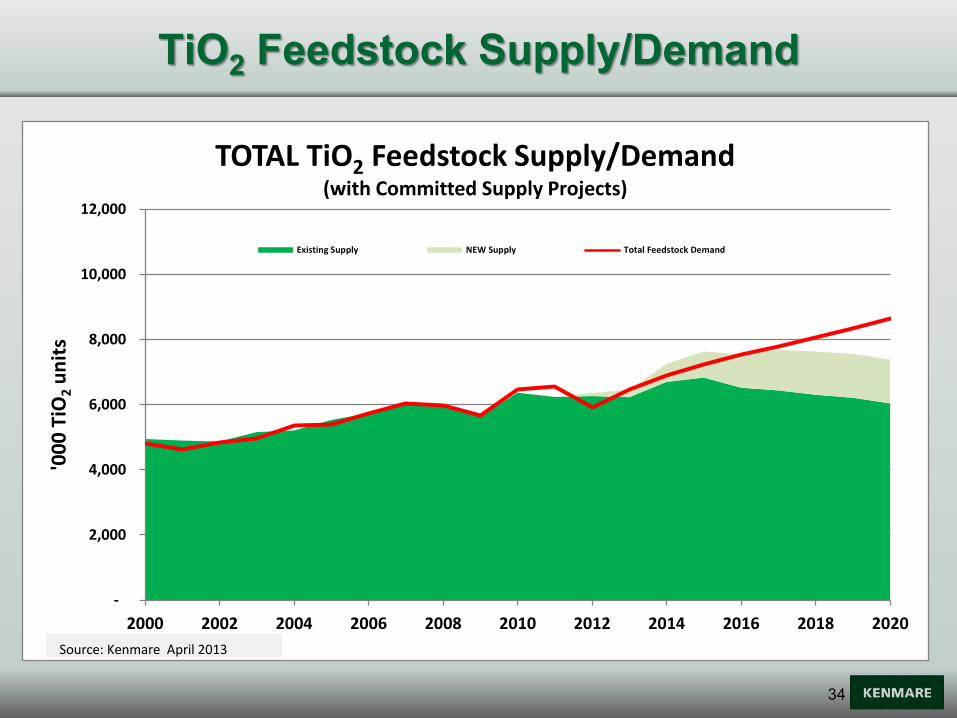

TiO2 Feedstock Supply/Demand

-

2,000

4,000

6,000

8,000

10,000

12,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

'00

0 T

iO2

un

its

TOTAL TiO2 Feedstock Supply/Demand(with Committed Supply Projects)

Existing Supply NEW Supply Total Feedstock Demand

Source: Kenmare April 2013

35

Financials

36

Revenue & EBITDA 2010 – 2012

0

20

40

60

80

100

120

0

50

100

150

200

250

2010 2011 2012

EBIT

DA

US$

m

Rev

enue

US$

m

Revenue EBITDA

37

Income Statement 2012 Review

2012 2011 Comment on 2012 & movement

US$m US$m

Revenue 234.6 167.5 Sales up 40% on 2011

CoS & Opex (154.2) (114.6) Costs up 35% on 2011

Operating profit 80.4 52.9

Net finance costs (27.0) (28.4) $7.0m paid & balance accrued

Foreign exchange loss (0.6) (6.3) On Euro debt & SA Rand cash

Profit before tax 52.8 18.2

Tax (charge) / credit (3.3) 5.5 Deferred tax - applied losses

Profit after tax 49.5 23.7

Blended product prices achieved up 50%, compared with 2011

EPS: USD 2.01c/share (2011: USD 0.99 c/share)

38

Balance Sheet 2012 Review

Significant Balance Sheet movements are expansion related

2012 2011 Comment on 2012 & movement

US$m US$m

Property, plant & equipment 887.5 714.1 Largely expansion investment

Deferred tax asset 2.2 5.5 Used with increasing profitability

Inventories 22.4 25.8 Lower product stocks & higher spares

Trade & other receivables 35.7 38.8 No bad debts

Cash 46.1 77.3 Reduced due to expansion investment

Total assets 993.9 861.5

Equity & reserves 605.6 495.4 2012 profit & share placing July ’12

Bank loans 324.4 327.1 Repaying senior & roll-up Sub debt

Creditors & provisions 63.9 39.0 Increase in expansion creditors

Total equity & liabilities 993.9 861.5

39

Key Company Highlights

Long life ore body producing high quality products

Low cost mining, efficient materials handling, well-established producer

50% expansion in commissioning, with vast majority of capex spent

Significant share of global feedstock supply of titanium minerals

Favourable mineral sands supply/demand dynamics

Important asset for Mozambique

40

Kenmare Resources plc

Chatham House , Chatham Street

Dublin 2, Ireland

www.kenmareresources.com