kate sayer 16 october 2017 - seafarers.uk · •‘beyond reserves’ published by sector bodies...

TRANSCRIPT

Kate Sayer

16 October 2017

Financial sustainability

• Doing the most we can

• For our beneficiaries

• And keep doing it

What do we mean by financially sustainable?

2

Financially sustainable impact

Good outcomes for beneficiaries

Impact = outcomes resources put in

QUALITY

What are reserves?

Unspent unrestricted reserves

What are reserves?

Restricted

Endowment Restricted

income

Unrestricted

Designated General

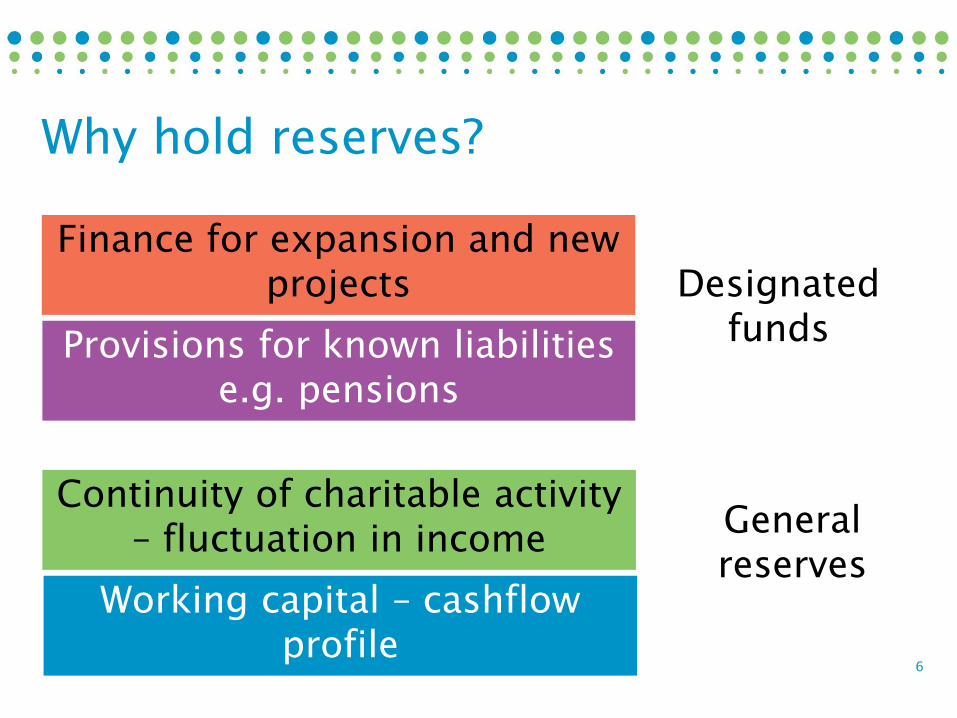

Why hold reserves?

6

Finance for expansion and new projects

Provisions for known liabilities e.g. pensions

Continuity of charitable activity – fluctuation in income

Working capital – cashflow profile

Designated

funds

General reserves

What level do we need?

7

Provisions for known liabilities e.g.

pensions

Continuity of charitable activity –

fluctuation in income

Working capital – cashflow profile

How well have we defined the risk or liability? Do we know the probability, timing and

amount needed?

How good is our income forecasting? How diverse is our

income? Reliability?

How well do we match incoming to outgoing

resources? Timing of funding

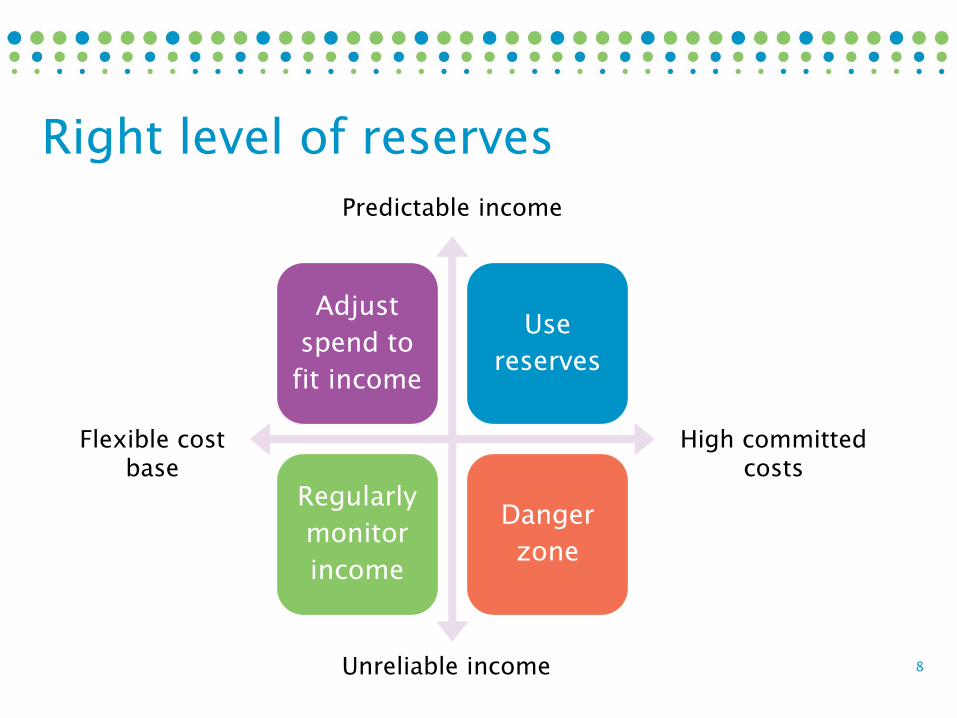

Right level of reserves

8

Adjust

spend to

fit income

Use

reserves

Regularly

monitor

income

Danger

zone

High committed costs

Predictable income

Flexible cost base

Unreliable income

• Where is your organisation on the reserves quadrant?

• What are the risks you need to cover with reserves?

• If you spend more to help more beneficiaries, what is the risk?

• If you hold more in investments, what is the risk?

Spend or save?

• Take into account reliability of funding and risk profile on income

• Consider the level of commitments and how long you are committed for

• Think about moral obligations as well as contractual commitments

• Plan cashflow

Level of reserves needed

• Base on an assessment of the risks

• Describe as a range

• Take a longer term view – you can use reserves and replace

Reserves - action

11

Investment strategies

12

• Maximise the return

• For least risk possible

• Beat inflation

• Keep the capital safe

What’s a good investment strategy?

13

Capital and revenue

14

Capital

Gains

Income Spend

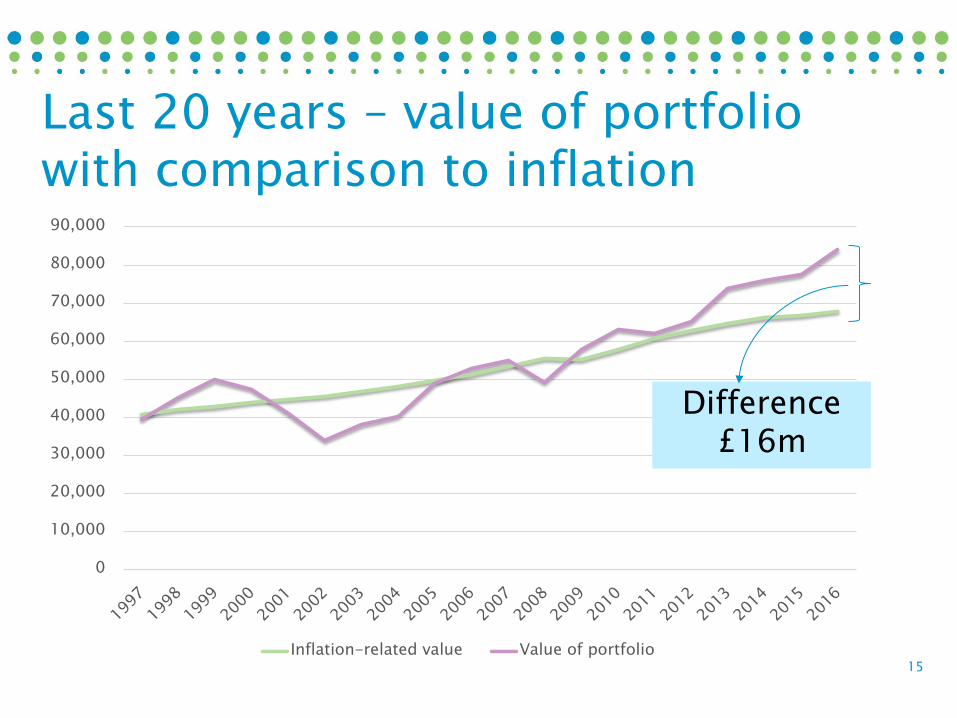

Last 20 years – value of portfolio with comparison to inflation

15

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Inflation-related value Value of portfolio

Difference £16m

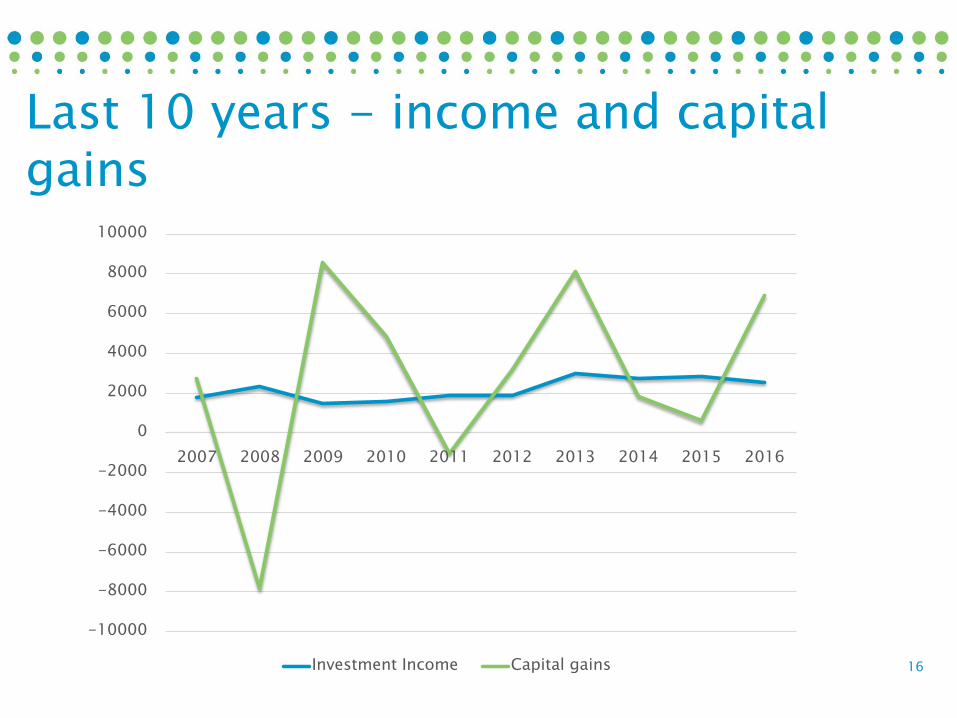

Last 10 years - income and capital gains

16

-10000

-8000

-6000

-4000

-2000

0

2000

4000

6000

8000

10000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Investment Income Capital gains

• Income-only approach Only the income (dividends, interest) produced and

paid over is withdrawn on a regular basis

• Total return Either income or capital growth is withdrawn from

the portfolio on a regular basis

Two approaches

17

• Need to understand your expenditure plans

• Cashflow forecast

• Do you have permanent endowment?

• Follow CC 2013 regulations and guidance

Adopting total return

18

• Set a spending policy as % of portfolio

• Average portfolio value over three years using quarter-end values

• Sustain spending

• And

• Maintain real value of the investment fund

Total return policies

19

Other investments

20

• Still a financial investment

• Need to have a policy Avoid specific investments because of conflict with

charity’s objects

Avoid specific investments because you may lose

supporters or beneficiaries

Can make positive choices on same grounds

• No significant financial detriment

Ethical investment

21

• May be held as part of investment portfolio (property funds) Generate dividends or interest

• May be held directly Generate rental income

Property management costs

• Balance sheet – current market value

• Gains or losses are part of income and expenditure

Investment property

22

• Charitable expenditure

• Motivated by charitable purpose

• No requirement for a financial return

• Includes: Loans to charities

Investment in property for charitable activities

Underwriting a loan or commitment for another

charity

Programme related investment

23

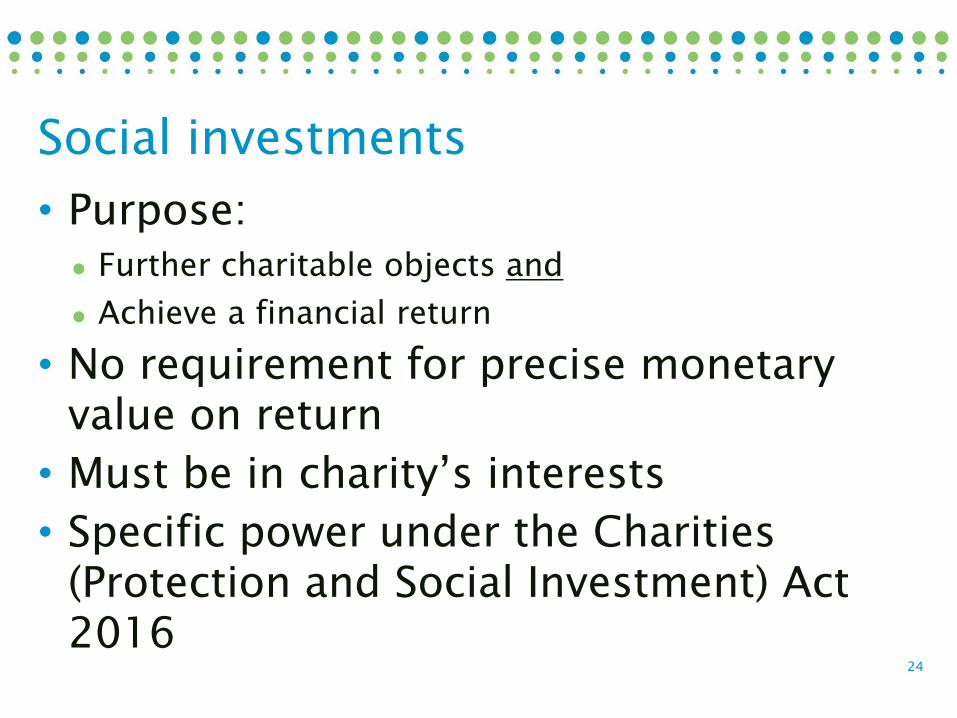

• Purpose: Further charitable objects and

Achieve a financial return

• No requirement for precise monetary value on return

• Must be in charity’s interests

• Specific power under the Charities (Protection and Social Investment) Act 2016

Social investments

24

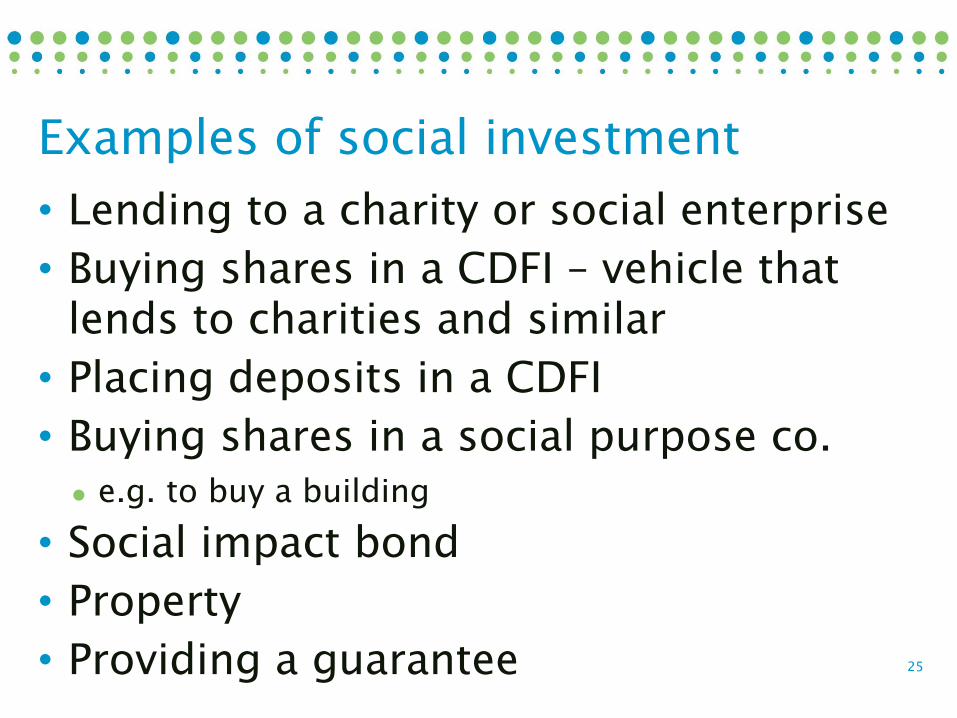

• Lending to a charity or social enterprise

• Buying shares in a CDFI – vehicle that lends to charities and similar

• Placing deposits in a CDFI

• Buying shares in a social purpose co. e.g. to buy a building

• Social impact bond

• Property

• Providing a guarantee

Examples of social investment

25

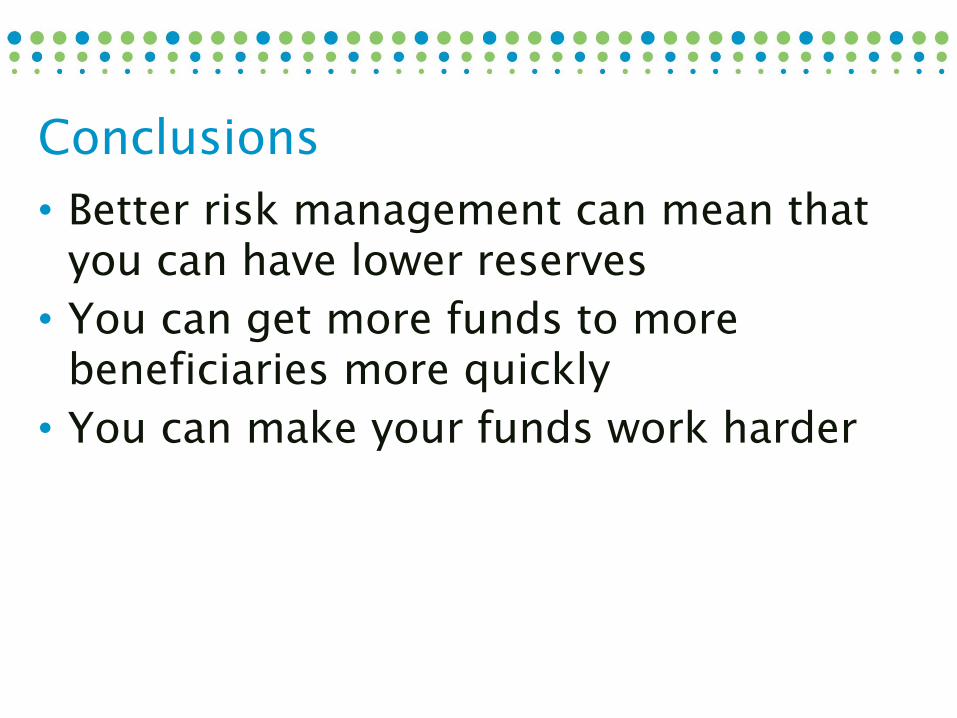

Conclusions

• Better risk management can mean that you can have lower reserves

• You can get more funds to more beneficiaries more quickly

• You can make your funds work harder

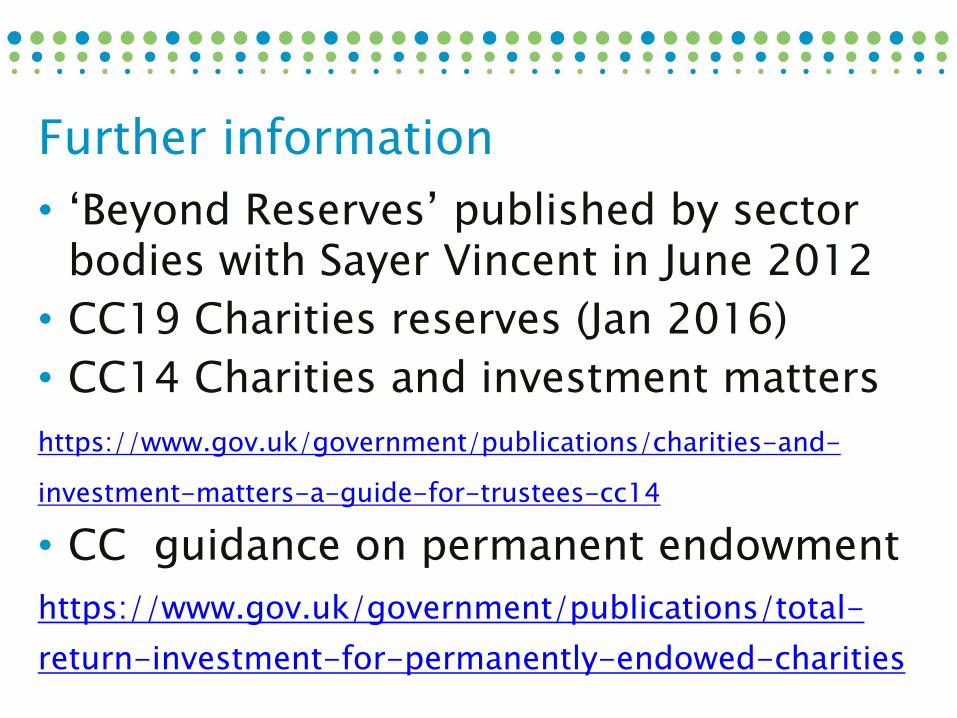

• ‘Beyond Reserves’ published by sector bodies with Sayer Vincent in June 2012

• CC19 Charities reserves (Jan 2016)

• CC14 Charities and investment matters

https://www.gov.uk/government/publications/charities-and-

investment-matters-a-guide-for-trustees-cc14

• CC guidance on permanent endowment

https://www.gov.uk/government/publications/total-

return-investment-for-permanently-endowed-charities

Further information