karan singh, cfa, frmstatic-news.moneycontrol.com/static-mcnews/2018/01/oct-2017-bank... ·...

TRANSCRIPT

JM Financial Institutional Securities Limited

JM Financial Research is also available on: Bloomberg - JMFR <GO>,

Thomson Publisher & Reuters S&P Capital IQ and FactSet Please see Appendix I at the end of this report for Important Disclosures and Disclaimers and Research Analyst Certification.

NBFC

The recently announced PSU Banks (PSBs) recap should lead to faster resolution of NPAs and

provide some amount of growth capital, which could lead to higher competitive intensity in

segments such as mortgages, LAP, SME and infra (while staying away from transactional

intensive and low ticket products). However, PSBs suffer from structural issues such as i) poor

underwriting, technology infrastructure and collection capabilities, ii) poor compensation

structure and iii) directed lending by the Govt. for social welfare schemes, making PSBs

inefficient. The agile nature of NBFCs ensures that they are able to navigate such competition

due to i) focus on profitability over growth, ii) focus on niche customer segments and

customised product offering, iii) faster turnaround time, iv) superior collections abilities and v)

use of data analytics and technology for better underwriting and cross-selling. We believe 1)

rural focused NBFCs such as MMFS will not be significantly impacted given a) different

customer segments vs. PSBs, b) relationship with various OEMs c) significant investment in

the distribution network (doubling of branches over the last 5 years from nearly 600 in FY12

to 1180 currently; 2) NBFCs with large Infra exposure such as LTFH would benefit from the

increase in the down selling opportunities; 3) diversified and well-managed NBFCs such as

Bajaj Finance are well placed to navigate the increasing competition in the LAP segment and

should continue to outperform its peers; and 4) competition in home loan(HL) and LAP

segments could increase. We prefer HFCs with a balanced product mix – HDFC Ltd and PNB

Housing Finance.

Structural advantages of NBFCs to lead to better growth prospects: In the last 5 years, the

market share of NBFCs has increased by more than 100bps to 15% in the overall system

credit. We believe NBFCs have structural competitive strengths that are difficult to

replicate, such as 1) superior underwriting capabilities, 2) customised product offerings, 3)

faster turnaround times, 4) strategic presence in lending segments as well as geographies,

5) extensive use of technology and analytics to improve their underwriting skills and 6)

management compensation and incentives, which help attract significantly better talent.

Some of the benefits that could accrue due to PSBs recap are as follows: i) Opportunities

for sell down of infra/mortgage loans by NBFCs to PSBs would increase, thereby boosting

fee income and growth opportunities; ii) Credit availability for NBFCs from PSBs will go up

which will benefit NBFCs; iii) Resolution of NPAs could led to better economic growth

prospects, thereby boosting lending opportunities for the entire sector.

PSBs unlikely to challenge NBFCs due to inherent structural issues: While PSBs recap will

help them resolve NPAs by taking hair-cuts and start competing for loans, we believe PSBs

would be constrained by their structural issues which are as follows: 1) focus on growth

over profitability; 2) poor underwriting and collection capabilities; 3) rigid appraisal

processes and higher turnaround times; 4) poor technology infrastructure, risk

infrastructure and monitoring mechanisms and 5) poor management compensation and

incentive structure and absence of ESOPs– the average salary for MD/CEO of top

NBFCs/private banks is 20-30x of PSBs.

However, we expect competitive intensity to increase in segments such as Home Loans,

LAP, LRD (Lease rental discounting) and auto loans: We expect PSBs to focus on larger

ticket size infrastructure loan, refinancing opportunities in corporate segment; MSME

loans, LAP/LRD and home/auto loans post this recap. At the peak of the last credit cycle,

PSBs retail portfolio comprised primarily of mortgage and car segments which constituted

40-55% and 10% of the overall book. We do not believe PSBs have the skill set to focus

on segments such as consumer durables, used vehicle, developer financing etc.

Housing Finance – High ticket LAP, LRD and home loans to witness increase in

competitive intensity, prefer HFCs with balanced product mix: We expect competitive

intensity to increase in Home Loans (HL) and LAP. Home Loan: Despite strong competitive

intensity, HFCs have gained/maintained market share due to faster turnaround times,

better service levels and their ability to raise money at competitive rates. However, given

that the current spread of home loans rates over MCLR is only 15-35 bps vs 60 bps

earlier, we believe there is limited room to cut home loan rates. We forecast pressure on

Karan Singh, CFA, FRM [email protected] | Tel: (91 22) 66303082

Nikhil Walecha [email protected] | Tel: (91 22) 66303027

Bunny Babjee [email protected] | (+91 22) 6630 3263

Sameer Bhise [email protected] | Tel: (91 22) 66303489

Jayant Kharote [email protected] | Tel: (91 22) 66303099

S Parameswaran [email protected] | +91 22 66303075

Exhibit 1. Valuation (INR)

NBFC Target

Multiple (FY20E)

Multiple

based value

Subs

Value

Target

Price

HDFC Ltd 2.8x 1015 875 1,890

LICHF 2.0x 700 - 700

REPCO 2.5x 725 - 725

BAF 5.1x 2,050 - 2,050

CIFC 2.6x 1,170 - 1,170

MMFS 2.4x 448 52 500

PNB Housing 3.3x 1,680 - 1,680

L&T Finance 3.4x 235 - 235

SHTF 1.9x 1,300 - 1,300

SCUF 2.3x 2,400 - 2,400

Source: Company, JM Financial

Exhibit 2. Earnings table

NBFC EPS CAGR (%) ROA (%) ROE (%)

FY17-20e FY19e FY20e FY19e FY20e

HDFC 16.0% 2.2% 2.2% 19.3% 20.0%

LICHF 13.8% 1.3% 1.3% 17.7% 17.8%

REPCO 16.4% 2.2% 2.2% 17.2% 17.2%

BAF 32.8% 3.6% 3.6% 19.6% 21.8%

CIFC 19.0% 2.6% 2.6% 18.7% 18.9%

MMFS 54.5% 2.2% 2.4% 13.2% 14.9%

PNB Housing 39.1% 1.5% 1.5% 16.1% 18.1%

L&T Finance 37.2% 2.0% 2.1% 18.8% 20.9%

SHTF 22.7% 2.2% 2.3% 14.5% 15.4%

SCUF 21.1% 2.6% 2.6% 13.7% 15.0%

Source: Company, JM Financial

30 October 2017 India | NBFC | Sector Report

Structurally on a strong footing

NBFC 30 October 2017

JM Financial Institutional Securities Limited Page 2

home loan yields for HFCs under over coverage. LAP: We expect competition to intensify

further in this segment as PSBs reduce rates and offer higher LTVs to become more

competitive. NBFCs were already seeing increasing competitive intensity and well-

managed NBFCs started to focus on lower ticket size LAPs and changed their distribution

strategy to reduce their dependence on DSAs. We expect PSBs to target DSA-led higher

ticket size LAP/LRD as this would help PSBs deploy their capital faster. However, NBFCs

could also benefit from increased opportunities of assignments transaction in LAP

segment and increased credit flow from PSBs to NBFCs. We favour HFCs with a balanced

product mix such as HDFC (HL: 69%, Corporate: 30%, others: 1.5%) and PNB Housing

(HL: 59%, LAP: 16.5%, CF: 12%, others: 13%); these will be able to withstand this

increasing competitive intensity and deliver strong return ratios. Other HFCs such as

Repco which is primarily present in rural/semi-urban market, focuses on lower ticket

home loans will be less impacted as PSBs are unlikely to target such segment. Companies

like LICHF, which have a very high share of retail home loans (of which most are salaried

customers), would be most impacted. We conservatively forecast a margin decline for

HFCs under our coverage.

Rural/Niche NBFCs would continue to maintain an edge: In the past 5 years, auto

financiers have increased their market share from 43% in FY12 to 47% as NBFCs that

operated in this segment focused on niche segments and have developed a deep

understanding of the market, customer profiles and products, and developed expertise in

valuation and credit appraisal. We expect market share gains to continue for NBFCs

present in i) Used vehicles – Given the expertise required and transaction intensive nature

of this business, especially with respect to collection, we do not expect significant

competition from PSB in both used and New CV segments ii) Two-wheelers - PSBs do not

participate in two-wheeler loans in a focused manner due to the transactional intensive

nature of this business due to the small ticket size of the product, lack of collection ability

and scalability issues. iii) Given the difference in customer profile, Rural-NBFCs such as

MMFS would continue to maintain their market share due to significant investment in

distribution network, faster turnaround times, different customer segments vs. PSBs and

existing relationships with OEMs. Credit assessment of farm cash flows requires a lot of

expertise and collection capabilities, which PSBs do not possess.

Diversified financiers - Bajaj Finance best positioned: BAF has the most diversified loan

book with a full suite of lending products (LAP, Small business loans, consumer durables,

digital financing, lifestyle financing, rural financing, 2/3 wheelers and vendor financing)

which coupled with superior underwriting skill, best in class technology and focus on

cross-selling should enable it to navigate increasing competitive intensity in LAP segment.

In fact, in order to mitigate risks in the LAP portfolio, BAF has been consolidating this

book for the past three years through direct sourcing and has curtailed its exposure in the

high ticket LAP segment with ticket size of INR 9-10mn (vs. 2.25mn in FY15). We believe

Bajaj Finance, with diversified loan book, strong risk management practices and top class

management at the helm, is best positioned to deliver sustainable profitable growth

ahead.

Infra financiers – LTFH best placed to capture down selling opportunities: Given the larger

ticket size of infra loans and Govt. focus towards infra, we believe PSBs would focus on

this segment after the recap. However, we expect NBFCs such as LTFH that have excellent

structuring capabilities and superior underwriting skills to benefit given a) opportunities

for sell downs to increase and will boost their fee income and b) increased availability of

banks’ credit.

MSME financiers In the MSME segment, formal channel accounts for only 15-20% of the

credit requirement of the MSMEs. We do not expect any meaningful decline in market

share for NBFCs in this segment due to i) greater market penetration and better operating

efficiency; ii) Niche focus and customised product offerings; and iii) shorter turnaround

times. We believe there would be minimal impact on players such as Shriram City Union

Finance, which deal with micro SMEs.

Top picks - Bajaj Finance, MMFS, and LTFH: Our top picks are Bajaj Finance/MMFS/LTFH

and preferred picks in HFC space are HDFC Ltd. and PNB Housing. For our top picks (Bajaj

Finance/MMFS/LTFH) we expect earnings CAGR of 33%/55%/37% respectively over

FY17-FY20E with healthy ROE of 22%/15%/21% by FY20E.

NBFC 30 October 2017

JM Financial Institutional Securities Limited Page 3

NBFCs share in systemic credit is growing steadily… Exhibit 1.

Source: CRISIL

…while maintaining lower NPLs than PSBs Exhibit 2.

0%

5%

10%

15%

20%

25%

Mar-13 Mar-14 Mar-15 Mar-16 Mar-17

PSBs - GNPA NBFC - GNPA

Source: RBI

PSBs have historically focused on mortgage and auto loans Exhibit 3.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

SBI PNB BOB SBI PNB BOB

Home loans Auto loans Education loans Mortgages Others

FY 2012 FY 2017

Source: Company data, Others includes CC, personal loans, # Mortgages data not available for FY12

Avg. salary for MD/CEO of top NBFCs/Pvt Bank is 20-30x of Exhibit 4.PSBs

FY 2017 Salary -

MD & CEO (INR mn)

Employee shareholding

in the company (%)

PSU

SBI 2.9

PNB 3.0

BOB 3.1

Canara Bank 3.0

Private banks

ICICI Bank 55.4 3.42%

HDFC Bank 100.6 3.47%

IndusInd Bank 63.2 1.92%

YES 68.7 3.61%

NBFCs

BAF 69.7 1.43%

PNB Housing 17.7 1.91%

L&T Finance 47.3 1.27%

Mahindra Finance 38.1 1.20%

Source: Company data

Housing Finance – Stable Market share trends Exhibit 5.

Source: CRISIL

Stable asset quality trends Exhibit 6.

1.30%1.20%1.18%

1.08%

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

FY14 FY15

PSBs Individual Housing HFCs

Source: RBI

NBFCs have higher Market share in LAP Exhibit 7.

12%

24%27%

31%

0%

5%

10%

15%

20%

25%

30%

35%

Public SectorBanks

Private Banks NBFC HFC

Dec'16 market share (%)

Source: CIBIL

NPLs trends in LAP Exhibit 8.

7.67%

4.57%

1.45% 1.23%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

Public SectorBanks

NBFC HFC Private Banks

90DPD (%)

Source: CIBIL

69% 65% 65%

14% 14% 15%

17% 18% 20%

0%

20%

40%

60%

80%

100%

FY 2012 FY 2014 FY 2016

Capital market borrowing and ECB NBFCs credit Bank Credit

61% 61% 60% 60% 60%

39% 39% 40% 40% 40%

0%

20%

40%

60%

80%

100%

FY13 FY14 FY15 FY16 FY17

Banks NBFCs

NBFC 30 October 2017

JM Financial Institutional Securities Limited Page 4

Spreads between HL and MCLR have narrowed implying Exhibit 9.little room for further rate cuts

As of Oct-17 SBI PNB BOB ICICI

Home Loan rates (Min) 8.35% 8.35% 8.35% 8.35%

MCLR 8.00% 8.15% 8.30% 8.20%

HL spread over MCLR 35bps 20bps 5bps 15bps

Source: Company, JM Financial

We prefer HFCs with balanced product mix Exhibit 10.

73%59%

84% 80%

17%

13% 20%

12% 11%

4%15% 13%

0%

20%

40%

60%

80%

100%

HDFC PNB Housing LIC Housing Repco

Individuals LAP Construction Finance Others

Source: Company, JM Financial

LTFH – Infra has gained market share in Infra segment Exhibit 11.

27% 26% 31% 31% 35% 35% 33%

42.4% 41.9% 35.9% 36.2% 31.7% 32.9% 32.3%

13% 14% 15% 15% 16% 17% 17%

10.9% 11.0% 11.7% 11.9% 12.9% 14.0% 14.5%

1.0% 1.2% 1.4% 1.4% 1.6% 1.9% 2.4%

0%

20%

40%

60%

80%

100%

FY11 FY12 FY13 FY14 FY15 FY16 FY17

Top 5 PSBs Other SCBs PFC REC LTFH - Infra Finance

Source: Company, RBI, JM Financial

While maintaining lower stressed assets Exhibit 12.

Source: Company, RBI, JM Financial

NBFCs have just 5% share in MSME financing Exhibit 13.

Source: CRISIL

* MSME comprises of Manufacturing companies with less than INR 100mn and Services companies with less than INR 50mn turnover

Gross NPL among NBFCs and SCBs (MSME) Exhibit 14.

Source: Company data

18.3%

32.9%

11.6% 11.9%

0%

5%

10%

15%

20%

25%

30%

35%

SCBs PFC REC LTIF

FY15 FY16 FY17

72% 71% 71% 70% 67%

20% 22% 23% 23% 25%

4% 4% 3% 3% 2%2.1% 2.9% 3.3% 4.0% 5.3%

0%

20%

40%

60%

80%

100%

2011-12 2012-13 2013-14 2014-15 2015-16

Public Sector Banks Private Sector Banks Foreign Banks NBFCs

4.5-5.0%

6.0-6.5%

NBFC Banks

NBFC Banks

NBFC 26 October 2017

JM Financial Institutional Securities Limited Page 5

Sector wise impact of PSB recap Exhibit 15.

Segment Competitive

intensity Rationale

Car Loans/UVs Moderate

Rural focused NBFCs such as MMFS would continue to maintain their market share led by faster disbursements, collection abilities and existing

relationship with OEMs.

However, we expect competitive intensity to increase in urban areas as PSBs would focus on salaried customers in this segment

Consumer Finance Low

We see negligible impact on consumer durable financing which are low ticket items as both the customer acquisitions and credit underwriting

requires lot of expertise. It is the most difficult segment to target given large investment in technology infrastructure, lending expertise which player

like Bajaj Finance have taken years to build. Further, given lower duration and small ticket size, PSBs would stay away from it.

CV Low

In New CVs, Banks largely lend to large fleet operators whereas NBFCs lend to customers with a weaker credit profile such as small road transport

operators, and first time users. Auto finance NBFCs that operate in this segment have developed a deep understanding of the market, customer

profile, product and developed expertise in valuation, credit appraisal and efficient management of operations and have, thus, have been able to

maintain asset quality. Continuous monitoring of the disbursed loans by field officers who had originated the loans through frequent visits to the

borrower helps keep delinquencies under control. Given the expertise required and transaction intensive nature of this business, especially with

respect to collection, we do not expect significant competition from PSBs in both used and new CV segments.

Developer Loans Low We believe PSBs do not possess adequate underwriting skills and structuring capabilities to do developer loans. Consequent, we do not expect

significant increase in competitive intensity in this segment.

Gold Financing Low This segment is dominated by private banks and NBFCs. We believe NBFCs would continue to have an edge due to faster turnaround time, adequate

risk assessment and niche focus on gold financing loans over the past 3 decades.

Home Loans High

We expect competitive intensity to further intensify in the highly competitive Housing Finance space. We expect PSBs could only compete on rates;

however, there is limited room for further rate cuts due to compression in HL spreads over MCLR (which is currently at 30-35bps). We believe HFCs

would be able to maintain steady loan growth driven by competitive rates and faster turnaround time.

Infra Loans High

Given larger ticket size of the Infra segment and Govt. focus towards Infra, we believe PSBs would focus on this segment post recap. However, we

expect NBFCs like LTFH which have excellent structuring capability and superior underwriting skills to benefit given a) opportunities for sell downs will

increase and will boost their fee income and b) increased availability of Banks’ credit.

PSBs could also become aggressive when it comes to refinancing of Infra assets/projects. Therefore competition in refinancing opportunities could

increase.

LAP/LRD High

- LAP/LRD segment could witness an increase in competitive intensity post PSB recap. We expect PSBs to focus on larger ticket size LAP and they

would try and gain market share through following measures a) by charging lower interest rates to customers b) offering higher LTVs.

- Well managed NBFCs started focusing on lower ticket size LAP, changed their distribution strategy to reduce their dependence on DSAs. We expect

PSBs to target DSA led higher ticket size LAP/LRD as this would help PSBs deploy their capital faster

- Some customer still prefer NBFCs over Banks for LAP on self-occupied properties as Banks processes makes it difficult to release its property even

after full repayment if the customer has more than one loan arrangement with the Bank.

MFI Low PSB focus on SHGs model. Therefore there is no impact on JLG focused MFI business. On the other hand, Bank loans to MFI may get cheaper as

availability of bank finance increases

SME Moderate

- PSBs held the dominant share in the MSME lending space, funding almost two-thirds of the total MSME loan outstanding. However, their share has

contracted over the past four to five years as private banks and NBFCs have increased their presence in tier II and smaller regions. PSBs are losing out

due to their stricter appraisal process and higher turnaround time. We do not expect any meaningful decline in market share for NBFCs in this

segment due to i) Greater market penetration and better operating efficiency; ii) Niche focus and customised product offerings; and iii) Shorter

turnaround time.

Two Wheelers Low

This segment is also transaction intensive which requires significant efforts due to lower ticket size. PSBs don't participate much in two-wheelers

finance business in a focused manner due to lack of collection ability and scalability issues. Further, it requires active involvement with the

OEMs/dealers to generate business which makes it difficult segment to operate for the PSBs.

Tractors Low

- Given the difference in customer profile, Rural-NBFCs would continue to maintain their market share led by faster disbursements, collection abilities

and existing relationship with OEMs.

- We see limited on tractor financing business as PSBs would continue to focus on crop loans which are backed by land collateral. Credit assessment

of farm cash flows requires lot of expertise and collection capabilities which PSBs do not possess.

Source: Company, JM Financial

NBFC 26 October 2017

JM Financial Institutional Securities Limited Page 6

Feedback from Management Exhibit 16.

Company Feedback

Bajaj Finance

- PSBs would focus on growth than profitability and would stay away from unsecured business. Their primary target will be i) Mortgages – Higher focus on

LAP and LRD than Home loans and ii) Project Financing which would help them to deploy their capital faster.

- LAP/SME: Here, PSBs would focus on higher ticket LAP (INR 20mn to 50mn) though currently they are also doing business of INR 5mn to 10mn. There could

be some yield pressure on the SME side as PSBs may give additional exposure to its existing customers who have CASA relationship with them resulting in

higher LTV.

- NBFCs could also benefit from increased assignments transaction in LAP segment and increased credit flow from PSBs to NBFCs.

Capital First - NBFCS will continue with their current growth rate due to different pocketing of financing. NBFCs that are specialized in financing particular segments like

tractor, CV, SME, gold financing will continue to maintain their niche and it’s not easy to replicate the skill sets required to finance at micro level. Therefore

these NBFCs will continue to grow at 15-20% because there are very unique pockets for them which they have developed over the last 15-30 years.

Cholamandalam PSBs will prefer to do chunkier loans as they don’t have Infrastructure, manpower and inclination to do lower ticket retail loans which requires lot of collection

efforts. They will i) focus on chunkier SME working capital loans and ii) LAP loans (with ticket size of more than INR 10mn)

Edelweiss

- While the competition for credit will increase because both the private banks and NBFCs did not face as much competition from the PSBs up till now,

however economic recovery will also help in expanding the overall credit pool in the economy. Therefore, NBFCs, especially housing finance companies, and

the private sector banks will face some pressure on yields.

- Company believes that the housing finance companies will get aggressive, however PSBs like SBI and Bank of Baroda has always been aggressive and their

capital adequacy has remained healthy. PNB and Canara Bank on the other hand have their own housing finance companies; therefore, large PSU players

were already aggressive in the housing finance space up till now.

- Company expects higher competition in the auto loans and rural finance but not in consumer durable financing, personal loan, credit card loans, structured

credit and distressed credit.

LTFH

Currently, PSUs are present in the same market where NBFCs operates. However, niche NBFCs have maintained their dominance over PSBs due to their

nimbleness, reach and niche customer profile. Company believes that NBFCs will continue to maintain their superiority in most of the categories. As per

company, NBFC could face competition in three segments including i) Working capital loans ii) Infrastructure financing and iii) Housing loans. In the other

segments, PSBs cannot operate in a focused manner.

- In the Infra space, LTFH has clearly benefited from lower competition intensity of PSBs. However, as witnessed in the recent NPL cycle, PSBs do not have

adequate skills to assess Infra loans. This would create more opportunities for LTFH aided by its strong credit assessment and loan syndication skills. Therefore,

LTFH would benefit from increase in down selling opportunities. NBFCs can also expect better terms from PSBs on lending rates as they look to expand their

loan books.

- Similar to the Infra loans, PSBs do not have skills to assess developer loans. LTFH structure developer loans based on sales velocity and stage of construction

cycle. PSBs also fall behind in terms of sophisticated product structuring and underwriting skills of Developer loans compared to NBFCs.

- In the Housing Finance, company expects competition intensity to increase both for the salaried and self-employed customers. Therefore, competitive

intensity is expected to increase leading to the decline in lending rates and possible increase in LTVs. In the case of LAP, PSBs would become aggressive by

increasing LTVs.

Magma Sector that would see more credit disbursements in the coming months were government infrastructure projects, affordable housing and the MSME segment.

NBFCs may face some competition in the MSME segment. But with formal channels accounting for only 15-20% of the credit requirement of the MSMEs, the

MSMEs business of NBFCs is unlikely to be affected.

MMFS Company expects PSBs would focus on Corporates/Infra loans/Home Loans and LAP once they are adequately capitalized. Rural financing customer segments

are different and given PSBs do not have larger on the ground collection team; MMFS does not expect significant competition in this segment.

Repco

- Company expects positive impact for its SME customers due to the increase in Bank credit which would help its customers operating in stressed sectors such

as textile. Additionally, interest rates which are at its lows have a very limited room for further reduction.

- Repco which primarily operates in the rural/semi-urban areas does not see increase in competition in low ticket size home loans. Additionally, Branch

managers of PSBs do not possess enough skills required and authority to assess and sanction Home loans.

- In the LAP segment, company expects PSBs to focus on higher ticket LAP (ticket size of INR 10mn and above). However, company is incrementally focusing

on lower ticket LAP (less than INR 5mn) and would not be much impacted.

Source: Company, JM Financial

NBFC 26 October 2017

JM Financial Institutional Securities Limited Page 7

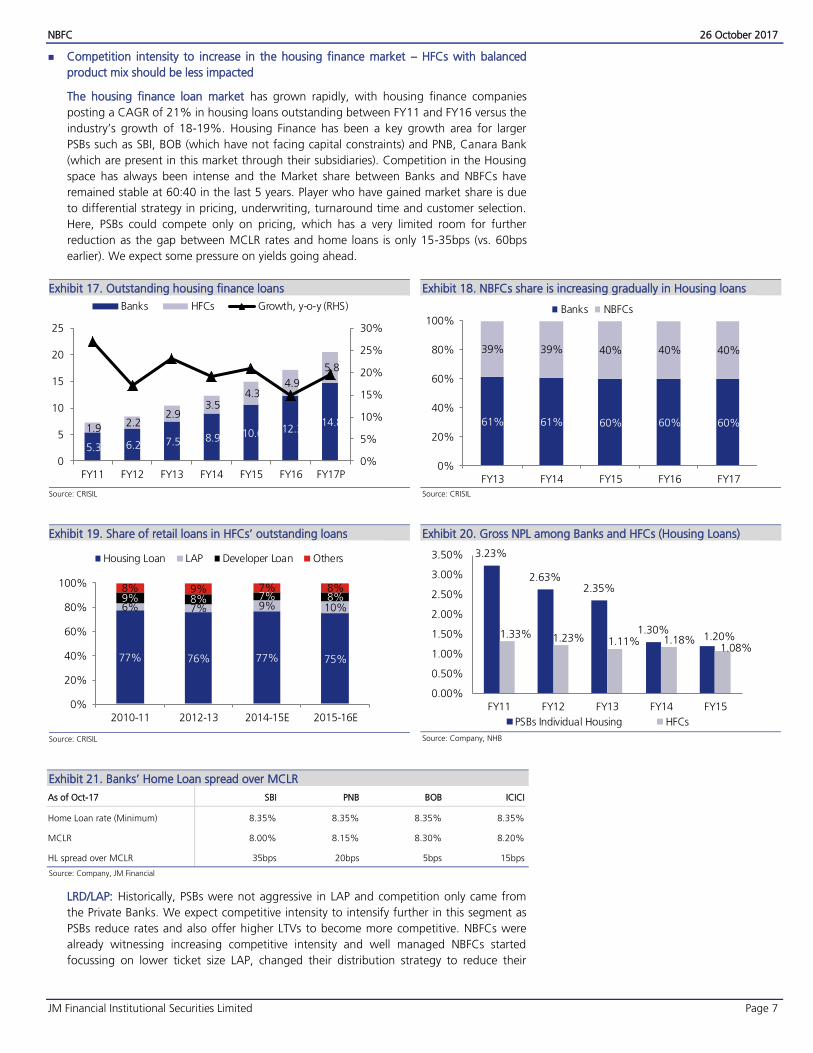

Competition intensity to increase in the housing finance market – HFCs with balanced

product mix should be less impacted

The housing finance loan market has grown rapidly, with housing finance companies

posting a CAGR of 21% in housing loans outstanding between FY11 and FY16 versus the

industry’s growth of 18-19%. Housing Finance has been a key growth area for larger

PSBs such as SBI, BOB (which have not facing capital constraints) and PNB, Canara Bank

(which are present in this market through their subsidiaries). Competition in the Housing

space has always been intense and the Market share between Banks and NBFCs have

remained stable at 60:40 in the last 5 years. Player who have gained market share is due

to differential strategy in pricing, underwriting, turnaround time and customer selection.

Here, PSBs could compete only on pricing, which has a very limited room for further

reduction as the gap between MCLR rates and home loans is only 15-35bps (vs. 60bps

earlier). We expect some pressure on yields going ahead.

Outstanding housing finance loans Exhibit 17.

Source: CRISIL

NBFCs share is increasing gradually in Housing loans Exhibit 18.

Source: CRISIL

Share of retail loans in HFCs’ outstanding loans Exhibit 19.

Source: CRISIL

Gross NPL among Banks and HFCs (Housing Loans) Exhibit 20.

3.23%

2.63%2.35%

1.30%1.20%1.33% 1.23% 1.11% 1.18%

1.08%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

FY11 FY12 FY13 FY14 FY15

PSBs Individual Housing HFCs

Source: Company, NHB

Banks’ Home Loan spread over MCLR Exhibit 21.

As of Oct-17 SBI PNB BOB ICICI

Home Loan rate (Minimum) 8.35% 8.35% 8.35% 8.35%

MCLR 8.00% 8.15% 8.30% 8.20%

HL spread over MCLR 35bps 20bps 5bps 15bps

Source: Company, JM Financial

LRD/LAP: Historically, PSBs were not aggressive in LAP and competition only came from

the Private Banks. We expect competitive intensity to intensify further in this segment as

PSBs reduce rates and also offer higher LTVs to become more competitive. NBFCs were

already witnessing increasing competitive intensity and well managed NBFCs started

focussing on lower ticket size LAP, changed their distribution strategy to reduce their

5.3 6.2 7.5 8.9 10.6 12.3 14.8

1.9 2.2

2.9 3.5

4.3 4.9

5.8

0%

5%

10%

15%

20%

25%

30%

0

5

10

15

20

25

FY11 FY12 FY13 FY14 FY15 FY16 FY17P

Banks HFCs Growth, y-o-y (RHS)

61% 61% 60% 60% 60%

39% 39% 40% 40% 40%

0%

20%

40%

60%

80%

100%

FY13 FY14 FY15 FY16 FY17

Banks NBFCs

77% 76% 77% 75%

6% 7% 9% 10%9% 8% 7% 8%8% 9% 7% 8%

0%

20%

40%

60%

80%

100%

2010-11 2012-13 2014-15E 2015-16E

Housing Loan LAP Developer Loan Others

NBFC 26 October 2017

JM Financial Institutional Securities Limited Page 8

dependence on DSAs. We expect PSBs to target DSA led higher ticket size LAP/LRD as this

would help PSBs deploy their capital faster.

NBFCs have higher market share in LAP Exhibit 22.

Source: ICRA

Gross NPL among NBFCs and Banks (LAP) Exhibit 23.

7.67%

4.57%

1.45% 1.23%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

Public SectorBanks

NBFC HFC (includesIBHFL)

Private Banks

90DPD (%)

Source: CIBIL

Developer Loan: Recently, NBFCs become aggressive in providing developer loans and the

share of developer loans in the overall portfolio increased to 7.5% in FY16 (vs. 6.7% in

FY15). We believe PSBs does not possess adequate underwriting skills and structuring

capabilities to do developer loans. Consequent, we do not expect significant increase in

competitive intensity in this segment.

We favour HFCs with balanced product mix such as HDFC and PNB Housing which would

be less impacted. Other HFCs such as Repco which is primarily present in rural/semi-urban

market, focuses on lower ticket home loans and some of its customers do not have

proper documents. With PSBs unlikely to target such segment, company would face very

less competition from the PSBs. Companies like LICHF, which have a very high share of

retail home loans (of which most are salaried customers), would be most impacted.

12%

24%27%

31%

0%

5%

10%

15%

20%

25%

30%

35%

Public SectorBanks

Private Banks NBFC HFC

Dec'16 market share (%)

NBFC 26 October 2017

JM Financial Institutional Securities Limited Page 9

Rural/Niche NBFC will continue to maintain their market share

NBFCs have increased their market share in the auto finance from about 43% in FY12 to

47% in FY17 due to factors such as i) wider and effective reach, ii) strong risk

management capabilities, iii) better understanding of their customers and iv) controlled

operating cost. Further, stress on the books of PSBs has helped NBFCs to gain share in the

auto finance market. The latent credit demand allowed NBFCs to fill the gap, especially

where PSBs do not have the appetite for risk and capabilities to serve.

NBFCs have gained share by catering to customers with a relatively weaker credit profile,

focusing on used vehicle financing (PSBs have a very limited presence in this space) and

ensuring faster processing, lower documentation and greater flexibility in borrower

appraisal.

NBFC’s share in auto-finance market Exhibit 24.

Source: CRISIL

Competition in Auto-finance Segment Exhibit 25.

27%

16%

11%10%

7%

7%

6%

16%

Shriram Transport Finance Mahindra Finance

Cholamandalam Finance Kotak Mahindra Bank

Magma Fincorp TMF

Sundaram Finance Others Source: CRISIL

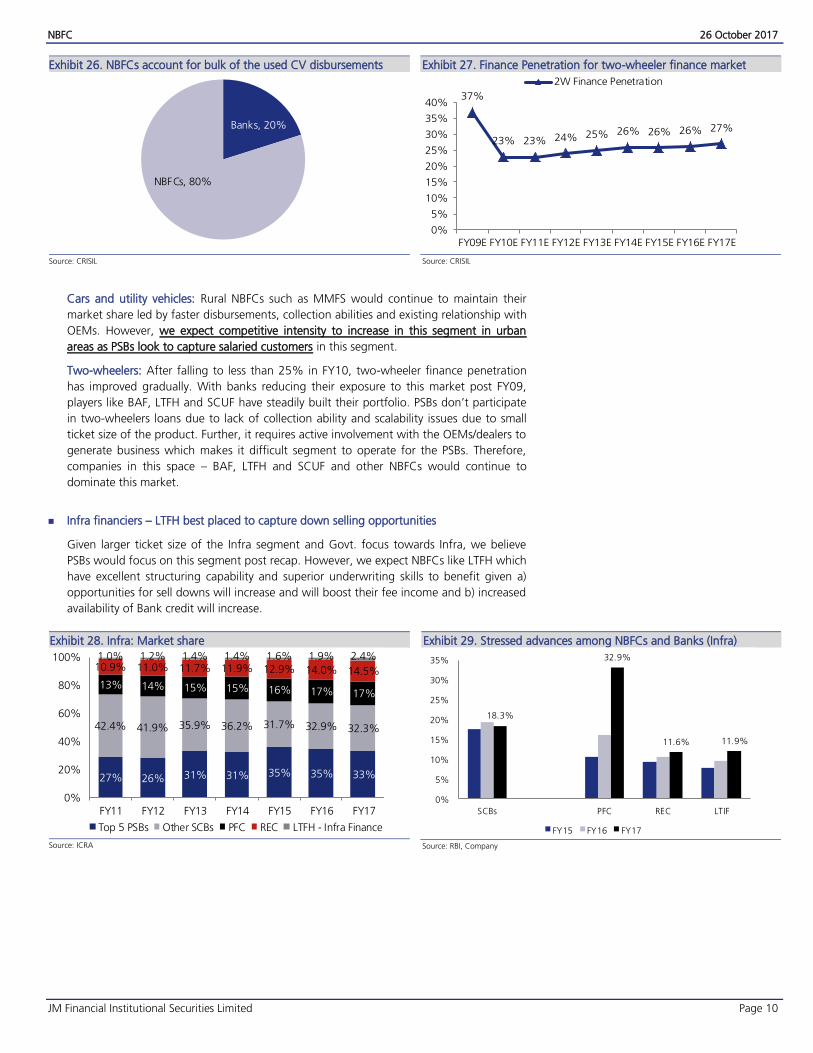

In commercial vehicles, NBFCs have a significant presence in the CVs which accounts for

almost half of NBFCs’ total auto finance outstanding while cars and UVs account for over

a third of the total portfolio. Used-vehicle financing constitutes almost two-thirds of

NBFCs’ total CV finance outstanding. NBFCs that operate in this segment are focused on

niche segments and have developed a deep understanding of the market, customer

profile, product and developed expertise in valuation, credit appraisal and efficient

management of operations and have, thus, have been able to maintain asset quality. They

have capitalised on the enormous opportunity offered by the segment through

investment in processes and manpower. NBFCs also accept payments in cash, given that a

large part of their customer segment earns in cash. Continuous monitoring of the

disbursed loans by field officers who had originated the loans through frequent visits to

the borrower helps keep delinquencies under control. NBFCs dominate the used CV

disbursement market with around 80% share. Given the high risk associated with the

used CV segment, PSBs have had minimal exposure to the segment. Therefore players like

SHTF would face no competition from the PSBs.

43% 46% 48% 47% 47%

57% 54% 52% 53% 53%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012-13 2013-14 2014-15 2015-16 2016-17P

NBFCs Banks

NBFC 26 October 2017

JM Financial Institutional Securities Limited Page 10

NBFCs account for bulk of the used CV disbursements Exhibit 26.

Source: CRISIL

Finance Penetration for two-wheeler finance market Exhibit 27.

Source: CRISIL

Cars and utility vehicles: Rural NBFCs such as MMFS would continue to maintain their

market share led by faster disbursements, collection abilities and existing relationship with

OEMs. However, we expect competitive intensity to increase in this segment in urban

areas as PSBs look to capture salaried customers in this segment.

Two-wheelers: After falling to less than 25% in FY10, two-wheeler finance penetration

has improved gradually. With banks reducing their exposure to this market post FY09,

players like BAF, LTFH and SCUF have steadily built their portfolio. PSBs don’t participate

in two-wheelers loans due to lack of collection ability and scalability issues due to small

ticket size of the product. Further, it requires active involvement with the OEMs/dealers to

generate business which makes it difficult segment to operate for the PSBs. Therefore,

companies in this space – BAF, LTFH and SCUF and other NBFCs would continue to

dominate this market.

Infra financiers – LTFH best placed to capture down selling opportunities

Given larger ticket size of the Infra segment and Govt. focus towards Infra, we believe

PSBs would focus on this segment post recap. However, we expect NBFCs like LTFH which

have excellent structuring capability and superior underwriting skills to benefit given a)

opportunities for sell downs will increase and will boost their fee income and b) increased

availability of Bank credit will increase.

Infra: Market share Exhibit 28.

27% 26% 31% 31% 35% 35% 33%

42.4% 41.9% 35.9% 36.2% 31.7% 32.9% 32.3%

13% 14% 15% 15% 16% 17% 17%

10.9% 11.0% 11.7% 11.9% 12.9% 14.0% 14.5%

1.0% 1.2% 1.4% 1.4% 1.6% 1.9% 2.4%

0%

20%

40%

60%

80%

100%

FY11 FY12 FY13 FY14 FY15 FY16 FY17

Top 5 PSBs Other SCBs PFC REC LTFH - Infra Finance

Source: ICRA

Stressed advances among NBFCs and Banks (Infra) Exhibit 29.

Source: RBI, Company

Banks, 20%

NBFCs, 80%

37%

23% 23% 24% 25% 26% 26% 26% 27%

0%

5%

10%

15%

20%

25%

30%

35%

40%

FY09E FY10E FY11E FY12E FY13E FY14E FY15E FY16E FY17E

2W Finance Penetration

18.3%

32.9%

11.6% 11.9%

0%

5%

10%

15%

20%

25%

30%

35%

SCBs PFC REC LTIF

FY15 FY16 FY17

NBFC 26 October 2017

JM Financial Institutional Securities Limited Page 11

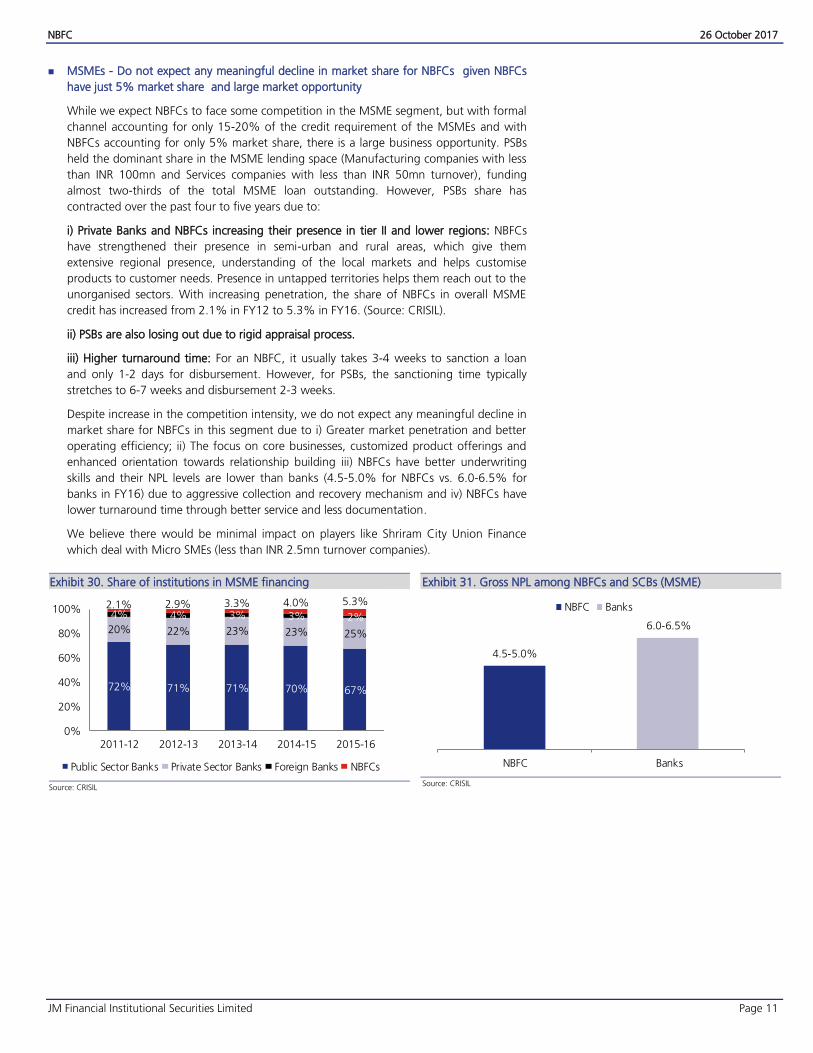

MSMEs - Do not expect any meaningful decline in market share for NBFCs given NBFCs

have just 5% market share and large market opportunity

While we expect NBFCs to face some competition in the MSME segment, but with formal

channel accounting for only 15-20% of the credit requirement of the MSMEs and with

NBFCs accounting for only 5% market share, there is a large business opportunity. PSBs

held the dominant share in the MSME lending space (Manufacturing companies with less

than INR 100mn and Services companies with less than INR 50mn turnover), funding

almost two-thirds of the total MSME loan outstanding. However, PSBs share has

contracted over the past four to five years due to:

i) Private Banks and NBFCs increasing their presence in tier II and lower regions: NBFCs

have strengthened their presence in semi-urban and rural areas, which give them

extensive regional presence, understanding of the local markets and helps customise

products to customer needs. Presence in untapped territories helps them reach out to the

unorganised sectors. With increasing penetration, the share of NBFCs in overall MSME

credit has increased from 2.1% in FY12 to 5.3% in FY16. (Source: CRISIL).

ii) PSBs are also losing out due to rigid appraisal process.

iii) Higher turnaround time: For an NBFC, it usually takes 3-4 weeks to sanction a loan

and only 1-2 days for disbursement. However, for PSBs, the sanctioning time typically

stretches to 6-7 weeks and disbursement 2-3 weeks.

Despite increase in the competition intensity, we do not expect any meaningful decline in

market share for NBFCs in this segment due to i) Greater market penetration and better

operating efficiency; ii) The focus on core businesses, customized product offerings and

enhanced orientation towards relationship building iii) NBFCs have better underwriting

skills and their NPL levels are lower than banks (4.5-5.0% for NBFCs vs. 6.0-6.5% for

banks in FY16) due to aggressive collection and recovery mechanism and iv) NBFCs have

lower turnaround time through better service and less documentation.

We believe there would be minimal impact on players like Shriram City Union Finance

which deal with Micro SMEs (less than INR 2.5mn turnover companies).

Share of institutions in MSME financing Exhibit 30.

Source: CRISIL

Gross NPL among NBFCs and SCBs (MSME) Exhibit 31.

Source: CRISIL

72% 71% 71% 70% 67%

20% 22% 23% 23% 25%

4% 4% 3% 3% 2%2.1% 2.9% 3.3% 4.0% 5.3%

0%

20%

40%

60%

80%

100%

2011-12 2012-13 2013-14 2014-15 2015-16

Public Sector Banks Private Sector Banks Foreign Banks NBFCs

4.5-5.0%

6.0-6.5%

NBFC Banks

NBFC Banks

NBFC 26 October 2017

JM Financial Institutional Securities Limited Page 12

Top picks – Bajaj Finance, Mahindra Finance, L&T Finance

Bajaj Finance – Superior growth with improving profitability

Bajaj Finance has the most diversified loan book with a full suite of lending products (LAP,

Small business loans, consumer durables, digital financing, lifestyle financing, rural

financing, 2/3 wheelers and vendor financing) which coupled with superior underwriting

skill, best in class technology and focus on cross-selling should enable it to navigate

increasing competitive intensity in LAP segment. In fact, in order to mitigate risks in the

LAP portfolio, BAF has been consolidating this book for the past three years through

direct sourcing and has curtailed its exposure in the high ticket LAP segment with ticket

size of INR 9-10mn (vs. 2.25mn in FY15). We believe Bajaj Finance, with diversified loan

book, strong risk management practices and top class management at the helm, is best

positioned to deliver sustainable profitable growth ahead. We expect earnings CAGR of

33% over FY17–FY20E, driven by robust AUM growth (33% CAGR). We expect healthy

return ratios with RoA/RoE of 3.6%/22% by FY20E; we value BAF at 5.1x Mar’20E book,

implying a Mar’19 TP of INR 2,050.

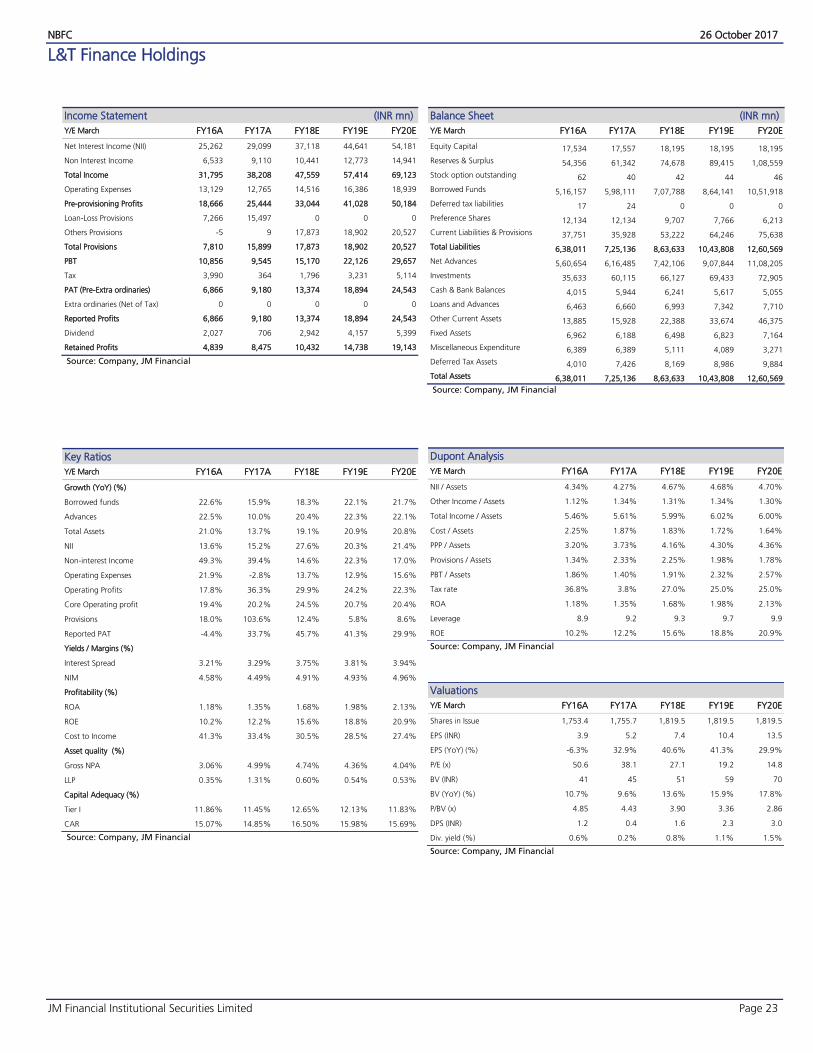

L&T Finance – Getting better with strong execution

Execution under the leadership of Mr. Dinanath Dubhashi continues to gather steam with

2QFY18 witnessing 47% YoY growth in PAT – this has seen continuous improvement

over the last 6 quarters. Profitability over the last 6 quarters has improved with reported

ROE improving from 9.7% in 1Q17 to 15.2% despite company providing for voluntary

provisioning of INR 8.9bn and accelerated provisioning of Rs 5.3bn. We believe LTFH on

track to achieve top quartile (18%+) ROE by FY19E driven by i) increasing share of

focused profitable business ii) improving capital allocation by exiting/partial sell down of

its non-core assets/unprofitable businesses and redeploying it to RoE accretive businesses;

iii) focus on fee income through sell down and DCM operations iv) focus on cost

efficiencies by streamlining businesses and digitizing operations and increase in

profitability contribution by investment management business. v) Given excellent

structuring capabilities and superior underwriting skills, we expect LTFH to benefit from

PSBs recap given increase in sell downs opportunities which will boost their fee income

and increased availability of banks’ credit. We forecast earnings CAGR of 37% over FY17-

20E with RoA/RoE improving from 1.35%/12% in FY17 to 2.1%/21% in FY20E. We

value LTFH at 3.4x Mar’20, implying Mar’19 TP of Rs 235.

Mahindra Finance – Asset quality improvement to boost RoA going forward

We expect RoA to improve going ahead due to 1) Improved crop outlook, increased

budget allocation and good monsoon for two consecutive years will boost farm income

and accelerate recoveries for MMFS; 2) With incremental NPLs coming down and

migration to 90DPD already completed, we factor credit costs of 230/200bps in FY18-19E

(vs. 306bps in FY17); 3) Management expects RoA to improve to 2% at end-FY18 (vs.

1.1% in FY17) on a like-to-like basis (120DPD); 4) Management expects the housing

subsidiary to continue its growth momentum of 40-50% and its book size to increase to

INR 100bn (vs. INR 48bn) by FY20; 5) Given the difference in customer profile, Rural-

NBFCs such as MMFS would continue to maintain their market share due to significant

investment in distribution network, faster turnaround times, different customer segments

vs. PSBs and existing relationships with OEMs. Credit assessment of farm cash flows

requires a lot of expertise and collection capabilities, which PSBs do not possess. We

expect earnings CAGR of c.60% (on a lower base) over FY17–20E and with RoA

improving to 2.4% and RoE of 15% by FY20E. We are factoring in a dilution of 9.4% in

FY18E. We value MMFS standalone at 2.4x Mar’20 BV, implying value of INR 448. We

value MRHF at INR 34 per share, while MIBL at INR 22 per share, implying Mar’19 TP of

Rs500.

NBFC 26 October 2017

JM Financial Institutional Securities Limited Page 13

Valuation charts

BAF P/B Exhibit 32.

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Oct

-15

Oct

-16

Oct

-17

BAF Fwd. P/BV (x) SD+1 SD-1 Average

Source: Company, JM Financial

BAF P/E Exhibit 33.

0

5

10

15

20

25

30

35

40

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Oct

-15

Oct

-16

Oct

-17

BAF Fwd. P/E (x) SD+1 SD-1 Average

Source: Company, JM Financial

HDFC P/B Exhibit 34.

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Oct

-05

Oct

-06

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Oct

-15

Oct

-16

Oct

-17

HDFC Fwd. Adj P/BV (x) SD+1 SD-1 Average

Source: Company, JM Financial

HDFC P/E Exhibit 35.

6

11

16

21

26

Oct

-05

Oct

-06

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Oct

-15

Oct

-16

Oct

-17

HDFC Fwd. Adj P/E (x) SD+1 SD-1 Average

Source: Company, JM Financial

MMFS P/B Exhibit 36.

0.00

1.00

2.00

3.00

4.00

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Oct

-15

Oct

-16

Oct

-17

MMFS Fwd. P/BV (x) SD+1 SD-1 Average

Source: Company, JM Financial

MMFS P/E Exhibit 37.

0

10

20

30

40

50

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Oct

-15

Oct

-16

Oct

-17

MMFS Fwd. P/E (x) SD+1 SD-1 Average

Source: Company, JM Financial

NBFC 26 October 2017

JM Financial Institutional Securities Limited Page 14

L&T Finance P/B Exhibit 38.

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

4.5x

Oct

-12

Feb-1

3

Jun-1

3

Oct

-13

Feb-1

4

Jun-1

4

Oct

-14

Feb-1

5

Jun-1

5

Oct

-15

Feb-1

6

Jun-1

6

Oct

-16

Feb-1

7

Jun-1

7

Oct

-17

LTFH Fwd. P/BV (x) SD+1 SD-1 Average

Source: Company, JM Financial

L&T Finance P/E Exhibit 39.

0

5

10

15

20

25

30

35

Oct

-12

Feb-1

3

Jun-1

3

Oct

-13

Feb-1

4

Jun-1

4

Oct

-14

Feb-1

5

Jun-1

5

Oct

-15

Feb-1

6

Jun-1

6

Oct

-16

Feb-1

7

Jun-1

7

Oct

-17

LTFH Fwd. P/E (x) SD+1 SD-1 Average

Source: Company, JM Financial

PNB Housing P/B Exhibit 40.

0.00

1.00

2.00

3.00

4.00

5.00

Nov-

16

Dec

-16

Jan-1

7

Jan-1

7

Feb-1

7

Mar-

17

Mar-

17

Apr-

17

May-

17

May-

17

Jun-1

7

Jul-17

Jul-17

Aug-1

7

Sep-1

7

Oct

-17

Oct

-17

PNB HousingFwd. P/BV (x) SD+1 SD-1 Average

Source: Company, JM Financial

PNB Housing P/E Exhibit 41.

0

5

10

15

20

25

30

35

Nov-

16

Dec

-16

Jan-1

7

Jan-1

7

Feb-1

7

Mar-

17

Mar-

17

Apr-

17

May-

17

May-

17

Jun-1

7

Jul-17

Jul-17

Aug-1

7

Sep-1

7

Oct

-17

Oct

-17

PNB Housing Fwd. P/E (x) SD+1 SD-1 Average

Source: Company, JM Financial

LIC Housing P/B Exhibit 42.

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Oct

-05

Oct

-06

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Oct

-15

Oct

-16

Oct

-17

LICHF Fwd. P/BV (x) SD+1 SD-1 Average

Source: Company, JM Financial

LIC Housing P/E Exhibit 43.

0

5

10

15

20

Oct

-05

Oct

-06

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Oct

-15

Oct

-16

Oct

-17

LICHF Fwd. P/E (x) SD+1 SD-1 Average

Source: Company, JM Financial

NBFC 26 October 2017

JM Financial Institutional Securities Limited Page 15

SCUF P/B Exhibit 44.

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50O

ct-0

5

Oct

-06

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Oct

-15

Oct

-16

Oct

-17

SCUF Fwd. P/BV (x) SD+1 SD-1 Average

Source: Company, JM Financial

SCUF P/E Exhibit 45.

0

5

10

15

20

25

30

Oct

-05

Oct

-06

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Oct

-15

Oct

-16

Oct

-17

SCUF Fwd. P/E (x) SD+1 SD-1 Average

Source: Company, JM Financial

SHTF P/B Exhibit 46.

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

Oct

-05

Oct

-06

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Oct

-15

Oct

-16

Oct

-17

SHTF Fwd. P/BV (x) SD+1 SD-1 Average

Source: Company, JM Financial

SHTF P/E Exhibit 47.

0

5

10

15

20

25

30

Oct

-05

Oct

-06

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Oct

-15

Oct

-16

Oct

-17

SHTF Fwd. P/E (x) SD+1 SD-1 Average

Source: Company, JM Financial

CIFC P/B Exhibit 48.

0.00

1.00

2.00

3.00

4.00

5.00

Oct

-05

Oct

-06

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Oct

-15

Oct

-16

Oct

-17

CIFC Fwd. P/BV (x) SD+1 SD-1 Average

Source: Company, JM Financial

CIFC P/E Exhibit 49.

0

10

20

30

40

50

Oct

-05

Oct

-06

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Oct

-15

Oct

-16

Oct

-17

CIFC Fwd. P/E (x) SD+1 SD-1 Average

Source: Company, JM Financial

REPCO P/B Exhibit 50.

2.0x

2.5x

3.0x

3.5x

4.0x

4.5x

5.0x

Oct

-14

Dec

-14

Feb-1

5

Apr-

15

Jun-1

5

Aug-1

5

Oct

-15

Dec

-15

Feb-1

6

Apr-

16

Jun-1

6

Aug-1

6

Oct

-16

Dec

-16

Feb-1

7

Apr-

17

Jun-1

7

Aug-1

7

Oct

-17

Repco Fwd. P/BV (x) Average SD+1 SD-1

Source: JM Financial, Company

REPCO P/E Exhibit 51.

12x

16x

20x

24x

28x

32x

Oct

-14

Dec

-14

Feb-1

5

Apr-

15

Jun-1

5

Aug-1

5

Oct

-15

Dec

-15

Feb-1

6

Apr-

16

Jun-1

6

Aug-1

6

Oct

-16

Dec

-16

Feb-1

7

Apr-

17

Jun-1

7

Aug-1

7

Oct

-17

Repco Fwd. P/E (x) Average SD+1 SD-1

Source: JM Financial, Company

NBFC 26 October 2017

JM Financial Institutional Securities Limited Page 16

HDFC Ltd.

Income Statement (INR mn)

Y/E March FY16A FY17A FY18E FY19E FY20E

Net Interest Income (NII) 79,784 92,024 1,10,886 1,26,761 1,50,429

Non Interest Income 28,867 23,092 18,489 20,585 22,438

Total Income 1,08,651 1,15,116 1,29,375 1,47,346 1,72,866

Operating Expenses 7,590 8,368 9,180 10,061 11,090

Pre-provisioning Profits 1,01,061 1,06,748 1,20,195 1,37,285 1,61,776

Loan-Loss Provisions 2,555 4,366 3,727 4,313 4,904

Others Provisions 4,425 2,158 0 0 0

Total Provisions 7,150 7,000 4,228 4,914 5,555

PBT 93,911 99,748 1,15,967 1,32,371 1,56,221

Tax 27,672 30,285 34,739 40,102 47,734

PAT (Pre-Extra ordinaries) 66,240 69,464 81,228 92,269 1,08,487

Extra ordinaries (Net of Tax) 4,683 4,960 4,602 4,381 4,381

Reported Profits 70,922 74,424 85,830 96,649 1,12,868

Dividend 31,380 28,681 29,740 33,457 39,033

Retained Profits 39,543 45,742 56,091 63,192 73,835

Source: Company, JM Financial

Key Ratios

Y/E March FY16A FY17A FY18E FY19E FY20E

Growth (YoY) (%)

Borrowed funds 13.9% 17.7% 16.5% 15.8% 15.8%

Advances 13.6% 14.6% 16.0% 17.0% 17.5%

Total Assets 13.7% 16.5% 15.8% 16.5% 17.0%

NII 8.3% 15.3% 20.5% 14.3% 18.7%

Non-interest Income 92.4% -20.0% -19.9% 11.3% 9.0%

Operating Expenses 7.4% 10.3% 9.7% 9.6% 10.2%

Operating Profits 23.8% 5.6% 12.6% 14.2% 17.8%

Core Operating profit 9.6% 14.4% 20.6% 14.6% 18.3%

Provisions 333.3% -2.1% -39.6% 16.2% 13.0%

Reported PAT 18.4% 4.9% 15.3% 12.6% 16.8%

Yields / Margins (%)

Interest Spread 1.67% 1.84% 2.11% 2.03% 1.99%

NIM 2.94% 2.94% 3.05% 2.98% 3.01%

Profitability (%)

ROA 2.44% 2.22% 2.24% 2.19% 2.20%

ROE 20.4% 18.8% 19.2% 19.3% 20.0%

Cost to Income 7.0% 7.3% 7.1% 6.8% 6.4%

Asset quality (%)

Gross NPA 0.71% 0.80% 1.29% 1.18% 1.08%

LLP 0.29% 0.25% 0.13% 0.13% 0.13%

Capital Adequacy (%)

Tier I 13.20% 13.08% 13.05% 12.92% 12.77%

CAR 16.60% 15.79% 15.39% 14.93% 14.49%

Source: Company, JM Financial

Balance Sheet (INR mn)

Y/E March FY16A FY17A FY18E FY19E FY20E

Equity Capital 3,160 3,177 3,177 3,177 3,177

Reserves & Surplus 3,38,051 3,93,277 4,44,765 5,03,577 5,73,031

Stock option outstanding 0 0 0 0 0

Borrowed Funds 23,76,392 27,97,322 32,58,880 37,73,783 43,70,040

Deferred tax liabilities 0 0 0 0 0

Current Liabilities & Provisions 1,69,926 1,69,804 1,87,653 2,56,412 3,62,717

Total Liabilities 28,87,528 33,63,579 38,94,475 45,36,949 53,08,966

Net Advances 25,86,582 29,64,720 34,39,075 40,23,718 47,27,869

Investments 1,53,454 2,04,101 2,29,757 2,50,229 2,73,521

Cash & Bank Balances 54,765 64,617 76,675 91,722 1,10,137

Loans and Advances 58,198 59,294 68,782 80,474 94,557

Other Current Assets 27,883 64,423 73,443 83,725 95,446

Fixed Assets 6,645 6,423 6,745 7,082 7,436

Miscellaneous Expenditure 0 0 0 0 0

Deferred Tax Assets 0 0 0 0 0

Total Assets 28,87,528 33,63,579 38,94,475 45,36,949 53,08,966

Source: Company, JM Financial

Dupont Analysis

Y/E March FY16A FY17A FY18E FY19E FY20E

NII / Assets 2.94% 2.94% 3.06% 3.01% 3.06%

Other Income / Assets 1.06% 0.74% 0.51% 0.49% 0.46%

Total Income / Assets 4.00% 3.68% 3.57% 3.50% 3.51%

Cost / Assets 0.28% 0.27% 0.25% 0.24% 0.23%

PPP / Assets 3.72% 3.42% 3.31% 3.26% 3.29%

Provisions / Assets 0.26% 0.22% 0.12% 0.12% 0.11%

PBT / Assets 3.46% 3.19% 3.20% 3.14% 3.17%

Tax rate 29.5% 30.4% 32.0% 32.0% 32.0%

ROA 2.44% 2.22% 2.24% 2.19% 2.20%

Leverage 8.5 8.5 8.7 9.0 9.2

ROE 20.4% 18.8% 19.2% 19.3% 20.0%

Source: Company, JM Financial

Valuations

Y/E March FY16A FY17A FY18E FY19E FY20E

Shares in Issue 1,579.9 1,595.1 1,588.7 1,588.7 1,588.7

EPS (INR) 41.9 43.5 51.1 58.1 68.3

EPS (YoY) (%) 18.4% 3.9% 17.4% 13.6% 17.6%

P/E (x) 40.5 39.0 33.2 29.3 24.9

BV (INR) 216 249 282 319 363

BV (YoY) (%) 9.8% 15.1% 13.4% 13.1% 13.7%

P/BV (x) 7.87 6.84 6.03 5.33 4.68

DPS (INR) 19.9 18.0 18.7 21.1 24.6

Div. yield (%) 1.2% 1.1% 1.1% 1.2% 1.4%

Source: Company, JM Financial

NBFC 26 October 2017

JM Financial Institutional Securities Limited Page 17

LIC Housing Finance

Income Statement (INR mn)

Y/E March FY15A FY16A FY17A FY18E FY19E

Net Interest Income (NII) 22,658 29,724 36,862 40,289 45,104

Non Interest Income 2,226 2,063 1,627 2,177 2,569

Total Income 24,884 31,787 38,489 42,467 47,673

Operating Expenses 3,792 4,687 6,118 7,495 8,745

Pre-provisioning Profits 21,092 27,100 32,371 34,971 38,928

Loan-Loss Provisions 568 1,851 3,197 2,451 1,927

Others Provisions -465 -398 -572 -50 -50

Total Provisions 73 1,465 2,813 2,401 1,877

PBT 21,019 25,636 29,558 32,571 37,051

Tax 7,158 9,028 10,247 11,074 12,597

PAT (Pre-Extra ordinaries) 13,862 16,608 19,311 21,497 24,453

Extra ordinaries (Net of Tax) 0 0 0 0 0

Reported Profits 13,862 16,608 19,311 21,497 24,453

Dividend 3,028 3,333 3,759 3,869 4,402

Retained Profits 10,834 13,275 15,552 17,627 20,052

Source: Company, JM Financial

Key Ratios

Y/E March FY15A FY16A FY17A FY18E FY19E

Growth (YoY) (%)

Borrowed funds 17.7% 14.9% 13.9% 16.0% 15.2%

Advances 18.6% 15.5% 15.5% 14.1% 15.3%

Total Assets 17.5% 16.0% 15.6% 13.5% 15.2%

NII 18.3% 31.2% 24.0% 9.3% 12.0%

Non-interest Income -8.9% -7.3% -21.1% 33.9% 18.0%

Operating Expenses 21.1% 23.6% 30.5% 22.5% 16.7%

Operating Profits 14.2% 28.5% 19.4% 8.0% 11.3%

Core Operating profit 14.2% 28.5% 19.4% 8.0% 11.3%

Provisions -66.2% 1,920.0% 92.1% -14.7% -21.8%

Reported PAT 5.2% 19.8% 16.3% 11.3% 13.8%

Yields / Margins (%)

Interest Spread 0.94% 1.21% 1.34% 1.29% 1.31%

NIM 2.20% 2.46% 2.64% 2.52% 2.46%

Profitability (%)

ROA 1.33% 1.37% 1.37% 1.33% 1.33%

ROE 18.1% 19.6% 19.1% 18.0% 17.7%

Cost to Income 15.2% 14.7% 15.9% 17.7% 18.3%

Asset quality (%)

Gross NPA 0.46% 0.45% 0.43% 0.52% 0.58%

LLP 0.05% 0.08% 0.18% 0.10% 0.04%

Capital Adequacy (%)

Tier I 11.82% 12.46% 13.35% 13.41% 13.23%

CAR 15.30% 15.50% 15.64% 15.91% 15.81%

Source: Company, JM Financial

Balance Sheet (INR mn)

Y/E March FY15A FY16A FY17A FY18E FY19E

Equity Capital 1,010 1,010 1,010 1,010 1,010

Reserves & Surplus 77,174 90,450 1,09,760 1,27,387 1,47,439

Stock option outstanding 0 0 0 0 0

Borrowed Funds 9,65,319 11,09,312 12,63,371 14,65,510 16,88,267

Deferred tax liabilities 6,690 8,109 9,173 10,549 12,131

Current Liabilities & Provisions 75,258 96,097 1,25,692 1,07,877 1,24,309

Total Liabilities 11,25,451 13,04,978 15,09,006 17,12,333 19,73,156

Net Advances 10,83,607 12,51,732 14,45,340 16,48,695 19,01,251

Investments 21,408 27,748 30,249 4,946 5,704

Cash & Bank Balances 10,294 14,289 20,314 44,515 51,334

Loans and Advances 1,509 1,483 2,225 2,538 2,927

Other Current Assets 7,835 8,807 9,912 10,544 10,679

Fixed Assets 797 920 965 1,095 1,262

Miscellaneous Expenditure 0 0 0 0 0

Deferred Tax Assets 0 0 0 0 0

Total Assets 11,25,451 13,04,978 15,09,006 17,12,333 19,73,156

Source: Company, JM Financial

Dupont Analysis

Y/E March FY15A FY16A FY17A FY18E FY19E

NII / Assets 2.18% 2.45% 2.62% 2.50% 2.45%

Other Income / Assets 0.21% 0.17% 0.12% 0.14% 0.14%

Total Income / Assets 2.39% 2.62% 2.74% 2.64% 2.59%

Cost / Assets 0.36% 0.39% 0.43% 0.47% 0.47%

PPP / Assets 2.02% 2.23% 2.30% 2.17% 2.11%

Provisions / Assets 0.01% 0.12% 0.20% 0.15% 0.10%

PBT / Assets 2.02% 2.11% 2.10% 2.02% 2.01%

Tax rate 34.1% 35.2% 34.7% 34.0% 34.0%

ROA 1.33% 1.37% 1.37% 1.33% 1.33%

Leverage 14.4 14.3 13.6 13.3 13.3

ROE 18.1% 19.6% 19.1% 18.0% 17.7%

Source: Company, JM Financial

Valuations

Y/E March FY15A FY16A FY17A FY18E FY19E

Shares in Issue 505.0 505.0 505.0 505.0 505.0

EPS (INR) 27.5 32.9 38.2 42.6 48.4

EPS (YoY) (%) 5.2% 19.8% 16.3% 11.3% 13.8%

P/E (x) 22.4 18.7 16.1 14.4 12.7

BV (INR) 155 181 219 254 294

BV (YoY) (%) 3.8% 17.0% 21.1% 15.9% 15.6%

P/BV (x) 3.97 3.39 2.80 2.41 2.09

DPS (INR) 6.0 6.6 7.4 7.7 8.7

Div. yield (%) 1.0% 1.1% 1.2% 1.2% 1.4%

Source: Company, JM Financial

NBFC 26 October 2017

JM Financial Institutional Securities Limited Page 18

REPCO Home Finance

Income Statement (INR mn)

Y/E March FY16A FY17A FY18E FY19E FY20E

Net Interest Income (NII) 3,043 3,682 4,079 4,626 5,310

Non Interest Income 293 314 359 419 499

Total Income 3,336 3,996 4,438 5,045 5,809

Operating Expenses 643 676 754 862 977

Pre-provisioning Profits 2,693 3,320 3,684 4,183 4,832

Loan-Loss Provisions 388 513 588 444 473

Others Provisions 3 5 0 0 0

Total Provisions 392 518 588 444 473

PBT 2,301 2,802 3,096 3,739 4,359

Tax 800 979 1,053 1,271 1,482

PAT (Pre-Extra ordinaries) 1,501 1,823 2,043 2,467 2,877

Extra ordinaries (Net of Tax) 0 0 0 0 0

Reported Profits 1,501 1,823 2,043 2,467 2,877

Dividend 135 151 184 234 288

Retained Profits 1,365 1,672 1,859 2,233 2,589

Source: Company, JM Financial

Key Ratios

Y/E March FY16A FY17A FY18E FY19E FY20E

Growth (YoY) (%)

Borrowed funds 28.1% 15.6% 14.6% 16.0% 17.8%

Advances 27.9% 16.3% 14.5% 16.2% 17.6%

Total Assets 27.8% 16.5% 14.6% 16.2% 17.5%

NII 28.0% 21.0% 10.8% 13.4% 14.8%

Non-interest Income 24.7% 7.0% 14.3% 17.0% 18.9%

Operating Expenses 17.5% 5.1% 11.6% 14.3% 13.3%

Operating Profits 30.4% 23.3% 10.9% 13.6% 15.5%

Core Operating profit 30.4% 23.3% 10.9% 13.6% 15.5%

Provisions 92.7% 32.3% 13.4% -24.4% 6.4%

Reported PAT 22.0% 21.4% 12.1% 20.8% 16.6%

Yields / Margins (%)

Interest Spread 2.95% 2.96% 2.81% 2.75% 2.69%

NIM 4.41% 4.40% 4.23% 4.15% 4.08%

Profitability (%)

ROA 2.17% 2.17% 2.11% 2.20% 2.20%

ROE 17.0% 17.4% 16.6% 17.2% 17.2%

Cost to Income 2.2% 2.2% 2.1% 2.2% 2.2%

Asset quality (%)

Gross NPA 1.30% 2.57% 2.56% 2.23% 2.12%

LLP 0.57% 0.62% 0.61% 0.40% 0.36%

Capital Adequacy (%)

Tier I 20.77% 21.25% 20.90% 20.35% 19.60%

CAR 20.77% 21.25% 20.90% 20.35% 19.60%

Source: Company, JM Financial

Balance Sheet (INR mn)

Y/E March FY16A FY17A FY18E FY19E FY20E

Equity Capital 625 626 626 626 626

Reserves & Surplus 8,923 10,747 12,606 14,839 17,428

Stock option outstanding 0 0 0 0 0

Borrowed Funds 65,379 75,604 86,643 1,00,505 1,18,395

Deferred tax liabilities 0 0 0 0 0

Preference Shares 0 0 0 0 0

Current Liabilities & Provisions 2,705 3,457 3,730 4,456 5,096

Total Liabilities 77,632 90,433 1,03,604 1,20,426 1,41,545

Net Advances 77,049 89,578 1,02,586 1,19,175 1,40,114

Investments 124 156 179 208 244

Cash & Bank Balances 200 225 308 358 420

Loans and Advances 0 0 0 0 0

Other Current Assets 166 384 427 564 624

Fixed Assets 93 91 104 121 143

Miscellaneous Expenditure 0 0 0 0 0

Deferred Tax Assets 0 0 0 0 0

Total Assets 77,632 90,433 1,03,604 1,20,426 1,41,545

Source: Company, JM Financial

Dupont Analysis

Y/E March FY16A FY17A FY18E FY19E FY20E

NII / Assets 4.40% 4.38% 4.20% 4.13% 4.05%

Other Income / Assets 0.42% 0.37% 0.37% 0.37% 0.38%

Total Income / Assets 4.82% 4.76% 4.57% 4.50% 4.43%

Cost / Assets 0.93% 0.80% 0.78% 0.77% 0.75%

PPP / Assets 3.89% 3.95% 3.80% 3.73% 3.69%

Provisions / Assets 0.57% 0.62% 0.61% 0.40% 0.36%

PBT / Assets 3.33% 3.33% 3.19% 3.34% 3.33%

Tax rate 34.8% 34.9% 34.0% 34.0% 34.0%

ROA 2.17% 2.17% 2.11% 2.20% 2.20%

Leverage 8.1 8.0 7.8 7.8 7.8

ROE 17.0% 17.4% 16.6% 17.2% 17.2%

Source: Company, JM Financial

Valuations

Y/E March FY16A FY17A FY18E FY19E FY20E

Shares in Issue 62.5 62.6 62.6 62.6 62.6

EPS (INR) 24.0 29.1 32.7 39.4 46.0

EPS (YoY) (%) 21.6% 21.4% 12.1% 20.8% 16.6%

P/E (x) 25.0 20.6 18.4 15.2 13.0

BV (INR) 153 182 211 247 289

BV (YoY) (%) 17.2% 19.1% 16.3% 16.9% 16.7%

P/BV (x) 3.93 3.30 2.84 2.43 2.08

DPS (INR) 2.2 2.4 2.9 3.7 4.6

Div. yield (%) 0.4% 0.4% 0.5% 0.6% 0.8%

Source: Company, JM Financial

NBFC 26 October 2017

JM Financial Institutional Securities Limited Page 19

Bajaj Finance

Income Statement (INR mn)

Y/E March FY16A FY17A FY18E FY19E FY20E

Net Interest Income (NII) 38,423 52,435 74,634 98,470 1,27,755

Non Interest Income 5,826 9,440 8,796 10,956 13,549

Total Income 44,249 61,875 83,430 1,09,426 1,41,304

Operating Expenses 19,492 25,642 34,838 44,868 56,519

Pre-provisioning Profits 24,757 36,233 48,592 64,559 84,785

Loan-Loss Provisions 1,635 3,908 8,884 11,741 15,622

Others Provisions 3,476 3,908 0 0 0

Total Provisions 5,111 8,058 8,884 11,741 15,622

PBT 19,646 28,175 39,708 52,818 69,163

Tax 6,861 9,810 13,818 18,381 24,069

PAT (Pre-Extra ordinaries) 12,785 18,366 25,890 34,437 45,094

Extra ordinaries (Net of Tax) 0 0 0 0 0

Reported Profits 12,785 18,366 25,890 34,437 45,094

Dividend 1,693 2,383 5,178 6,887 9,019

Retained Profits 11,093 15,983 20,712 27,550 36,075

Source: Company, JM Financial

Key Ratios

Y/E March FY16A FY17A FY18E FY19E FY20E

Growth (YoY) (%)

Borrowed funds 38.7% 33.0% 29.5% 36.0% 32.3%

Advances 37.0% 32.9% 35.9% 32.5% 30.3%

Total Assets 41.6% 37.2% 30.0% 32.2% 29.9%

NII 36.6% 36.5% 42.3% 31.9% 29.7%

Non-interest Income 67.0% 62.0% -6.8% 24.6% 23.7%

Operating Expenses 36.5% 31.6% 35.9% 28.8% 26.0%

Operating Profits 42.8% 46.4% 34.1% 32.9% 31.3%

Core Operating profit 41.9% 44.3% 38.1% 33.4% 32.0%

Provisions 35.7% 57.7% 10.3% 32.2% 33.1%

Reported PAT 42.4% 43.6% 41.0% 33.0% 30.9%

Yields / Margins (%)

Interest Spread 8.20% 8.01% 8.75% 8.90% 8.92%

NIM 9.87% 9.76% 10.48% 10.51% 10.39%

Profitability (%)

ROA 3.23% 3.33% 3.53% 3.58% 3.58%

ROE 20.9% 21.6% 20.1% 19.6% 21.8%

Cost to Income 44.1% 41.4% 41.8% 41.0% 40.0%

Asset quality (%)

Gross NPA 1.25% 1.71% 1.99% 2.12% 2.21%

LLP 1.17% 1.37% 1.33% 1.31% 1.33%

Capital Adequacy (%)

Tier I 16.06% 14.56% 18.91% 16.75% 15.36%

CAR 19.50% 20.30% 24.21% 21.56% 19.80%

Source: Company, JM Financial

Balance Sheet (INR mn)

Y/E March FY16A FY17A FY18E FY19E FY20E

Equity Capital 536 1,094 1,147 1,147 1,147

Reserves & Surplus 73,731 94,909 1,60,568 1,88,118 2,24,193

Stock option outstanding 0 0 0 0 0

Borrowed Funds 3,70,247 4,92,497 6,37,783 8,67,385 11,47,550

Deferred tax liabilities 0 0 0 0 0

Preference Shares 0 0 0 0 0

Current Liabilities & Provisions 20,052 48,746 28,997 38,324 49,794

Total Liabilities 4,64,565 6,37,246 8,28,495 10,94,974 14,22,684

Net Advances 4,27,560 5,68,320 7,72,398 10,23,137 13,32,741

Investments 10,341 40,747 18,538 24,555 31,986

Cash & Bank Balances 13,459 3,799 6,952 9,208 11,995

Loans and Advances 5,420 5,333 8,496 11,255 14,660

Other Current Assets 2,116 11,745 13,032 15,914 18,557

Fixed Assets 2,870 3,611 4,695 5,658 6,640

Miscellaneous Expenditure 0 0 0 0 0

Deferred Tax Assets 2,800 3,691 4,384 5,247 6,106

Total Assets 4,64,565 6,37,246 8,28,495 10,94,974 14,22,684

Source: Company, JM Financial

Dupont Analysis

Y/E March FY16A FY17A FY18E FY19E FY20E

NII / Assets 9.69% 9.52% 10.18% 10.24% 10.15%

Other Income / Assets 1.47% 1.71% 1.20% 1.14% 1.08%

Total Income / Assets 11.16% 11.23% 11.38% 11.38% 11.23%

Cost / Assets 1.59% 1.69% 1.95% 1.93% 1.87%

PPP / Assets 6.25% 6.58% 6.63% 6.71% 6.74%

Provisions / Assets 1.29% 1.46% 1.21% 1.22% 1.24%

PBT / Assets 4.96% 5.11% 5.42% 5.49% 5.49%

Tax rate 34.9% 34.8% 34.8% 34.8% 34.8%

ROA 3.23% 3.33% 3.53% 3.58% 3.58%

Leverage 6.3 6.6 5.1 5.8 6.3

ROE 20.9% 21.6% 20.1% 19.6% 21.8%

Source: Company, JM Financial

Valuations

Y/E March FY16A FY17A FY18E FY19E FY20E

Shares in Issue 535.5 546.9 573.5 573.5 573.5

EPS (INR) 23.9 33.6 45.1 60.1 78.6

EPS (YoY) (%) 33.0% 40.7% 34.4% 33.0% 30.9%

P/E (x) 76.2 54.2 40.3 30.3 23.1

BV (INR) 139 176 282 330 393

BV (YoY) (%) 44.5% 26.6% 60.6% 17.0% 19.1%

P/BV (x) 13.12 10.36 6.45 5.51 4.63

DPS (INR) 3.2 4.4 9.0 12.0 15.7

Div. yield (%) 0.2% 0.2% 0.5% 0.7% 0.9%

Source: Company, JM Financial

NBFC 26 October 2017

JM Financial Institutional Securities Limited Page 20

Cholamandalam Investment and Finance Co. Ltd.

Income Statement (INR mn)

Y/E March FY15A FY16A FY17E FY18E FY19E

Net Interest Income (NII) 17,039 21,267 24,033 28,455 33,378

Non Interest Income 269 163 262 379 413

Total Income 17,308 21,429 24,295 28,834 33,791

Operating Expenses 7,489 8,449 10,133 12,454 14,599

Pre-provisioning Profits 9,819 12,980 14,162 16,380 19,192

Loan-Loss Provisions 2,174 3,492 2,515 3,392 3,703

Others Provisions 1,073 780 641 0 0

Total Provisions 3,247 4,272 3,106 3,392 3,703

PBT 6,572 8,708 11,056 12,989 15,489

Tax 2,221 3,023 3,868 4,416 5,266

PAT (Pre-Extra ordinaries) 4,352 5,685 7,187 8,572 10,223

Extra ordinaries (Net of Tax) 0 0 0 0 0

Reported Profits 4,352 5,685 7,187 8,572 10,223

Dividend 589 850 658 1,286 1,533

Retained Profits 3,763 4,835 6,529 7,287 8,689

Source: Company, JM Financial

Key Ratios

Y/E March FY15A FY16A FY17E FY18E FY19E

Growth (YoY) (%)

Borrowed funds 7.6% 15.9% 7.2% 22.0% 18.6%

Advances 14.2% 16.8% 9.7% 18.7% 18.2%

Total Assets 10.8% 16.8% 10.2% 17.2% 18.4%

NII 16.7% 24.8% 13.0% 18.4% 17.3%

Non-interest Income -13.8% -39.5% 61.2% 44.4% 8.9%

Operating Expenses 13.8% 12.8% 19.9% 22.9% 17.2%

Operating Profits 17.8% 32.2% 9.1% 15.7% 17.2%

Core Operating profit 18.9% 34.4% 8.7% 15.1% 17.3%

Provisions 14.6% 31.6% -27.3% 9.2% 9.2%

Reported PAT 19.5% 30.6% 26.4% 19.3% 19.3%

Yields / Margins (%)

Interest Spread 6.18% 6.90% 6.93% 7.39% 7.46%

NIM 7.73% 8.48% 8.54% 8.89% 8.81%

Profitability (%)

ROA 1.92% 2.20% 2.45% 2.57% 2.60%

ROE 17.5% 18.0% 18.0% 18.3% 18.7%

Cost to Income 43.3% 39.4% 41.7% 43.2% 43.2%

Asset quality (%)

Gross NPA 3.57% 3.88% 5.34% 4.71% 4.17%

LLP 0.61% 2.17% 1.31% 1.09% 1.01%

Capital Adequacy (%)

Tier I 13.02% 13.26% 13.61% 13.91% 13.89%

CAR 21.24% 19.68% 18.64% 18.70% 18.34%

Source: Company, JM Financial

Balance Sheet (INR mn)

Y/E March FY15A FY16A FY17E FY18E FY19E

Equity Capital 1,437 1,562 1,563 1,563 1,563

Reserves & Surplus 25,289 35,012 41,563 48,850 57,539

Stock option outstanding 0 0 0 0 0

Borrowed Funds 1,94,752 2,25,762 2,42,067 2,95,322 3,50,252

Deferred tax liabilities 0 0 0 0 0

Preference Shares 0 0 0 0 0

Current Liabilities & Provisions 12,253 16,547 22,018 14,406 17,056

Total Liabilities 2,33,732 2,78,883 3,07,211 3,60,141 4,26,411

Net Advances 2,21,835 2,59,101 2,84,152 3,37,230 3,98,700

Investments 675 666 2,385 2,361 2,990

Cash & Bank Balances 8,610 9,003 4,870 5,396 6,977

Loans and Advances 823 1,045 1,683 2,023 2,312

Other Current Assets 4,270 5,140 9,568 8,779 10,703

Fixed Assets 683 1,113 1,401 1,438 1,702

Miscellaneous Expenditure 0 0 0 0 0

Deferred Tax Assets 1,836 2,815 3,152 2,915 3,025

Total Assets 2,38,732 2,78,883 3,07,211 3,60,141 4,26,411

Source: Company, JM Financial

Dupont Analysis

Y/E March FY15A FY16A FY17E FY18E FY19E

NII / Assets 7.50% 8.22% 8.20% 8.53% 8.49%

Other Income / Assets 0.12% 0.06% 0.09% 0.11% 0.10%

Total Income / Assets 7.62% 8.28% 8.29% 8.64% 8.59%

Cost / Assets 0.98% 0.98% 1.37% 1.49% 1.52%

PPP / Assets 4.32% 5.02% 4.83% 4.91% 4.88%

Provisions / Assets 1.43% 1.65% 1.06% 1.02% 0.94%

PBT / Assets 2.89% 3.36% 3.77% 3.89% 3.94%

Tax rate 33.8% 34.7% 35.0% 34.0% 34.0%

ROA 1.92% 2.20% 2.45% 2.57% 2.60%

Leverage 8.9 7.6 7.1 7.1 7.2

ROE 17.5% 18.0% 18.0% 18.3% 18.7%

Source: Company, JM Financial

Valuations

Y/E March FY15A FY16A FY17E FY18E FY19E

Shares in Issue 143.7 156.2 156.3 156.3 156.3

EPS (INR) 30.3 36.4 46.0 54.8 65.4

EPS (YoY) (%) 19.1% 20.2% 26.3% 19.3% 19.3%

P/E (x) 37.1 30.9 24.4 20.5 17.2

BV (INR) 186 234 276 322 378

BV (YoY) (%) 16.1% 25.9% 17.8% 16.9% 17.2%

P/BV (x) 6.04 4.80 4.07 3.49 2.97

DPS (INR) 4.1 5.4 4.2 8.2 9.8

Div. yield (%) 0.4% 0.5% 0.4% 0.7% 0.9%

Source: Company, JM Financial

NBFC 26 October 2017

JM Financial Institutional Securities Limited Page 21

MMFS

Profit & Loss (INR mn)

Y/E March FY16A FY17A FY18E FY19E FY20E

Net Interest Income 32,246 33,299 41,492 50,261 59,353

Profit on Investments 11 10 750 130 150

Exchange Income 0 0 0 0 0

Fee & Other Income 402 492 565 650 748

Non-Interest Income 412 502 1,315 780 898

Total Income 32,658 33,801 42,808 51,041 60,250

Operating Expenses 11,781 14,509 17,064 19,557 22,375

Pre-provisioning Profits 20,877 19,292 25,744 31,484 37,875

Loan-Loss Provisions 10,495 13,091 11,588 11,639 13,244

Provisions on Investments 0 0 0 0 0

Others Provisions 0 0 0 0 0

Total Provisions 10,495 13,091 11,588 11,639 13,244

PBT 10,382 6,201 14,156 19,844 24,631

Tax 3,656 2,198 4,955 6,946 8,498

PAT (Pre-Extraordinaries) 6,726 4,002 9,201 12,899 16,134

Extra ordinaries (Net of Tax) 0 0 0 0 0

Reported Profits 6,726 4,002 9,201 12,899 16,134

Dividend paid 2,713 1,610 2,760 3,870 4,840

Retained Profits 4,013 2,392 6,441 9,029 11,293

Source: Company, JM Financial

Key Ratios

Y/E March FY16A FY17A FY18E FY19E FY20E

Growth (YoY) (%)

Deposits 0.0% 0.0% 0.0% 0.0% 0.0%

Advances 11.3% 16.0% 15.1% 16.4% 17.1%

Total Assets 12.8% 16.2% 16.0% 16.4% 17.1%

NII 5.8% 3.3% 24.6% 21.1% 18.1%

Non-interest Income 2.5% 21.7% 162.0% -40.7% 15.1%

Operating Expenses 17.0% 23.2% 17.6% 14.6% 14.4%

Operating Profits 0.3% -7.6% 33.4% 22.3% 20.3%

Core Operating profit -13.3% -39.9% 125.4% 40.2% 22.3%

Provisions 26.8% 24.7% -11.5% 0.4% 13.8%

Reported PAT -19.1% -40.5% 129.9% 40.2% 25.1%

Yields / Margins (%)

Interest Spread 6.54% 5.86% 6.38% 6.67% 6.86%