kajaria ceramics ltd - sifyim.sify.com/sifycmsimg/jul2012/finance/15003121_kajariacements.pdfkajaria...

TRANSCRIPT

1

SYNOPSIS

Kajaria Ceramics is the second largest player in the Indian ceramic tile market. The company has a manufacturing capacity of 38.30 mn sq mtrs across its units.

Kajaria Ceramics has increased its capacity from 1 mn. sq. mtrs to 30.60 mn. sq. mtrs in last 23 years.

Kajaria Ceramics Ltd has acquired 51% shareholding in M/s. Vennar Ceramics Limited for a total consideration of Rs. 136.50 Million.

During the quarter, the robust growth of Net Profit is increased by 31.85% to Rs. 221.90 million.

Kajaria Ceramics Ltd has recommended a Dividend of 125% (Rs. 2.50 per equity share of Rs. 2 each.

Kajaria Ceramics exports to more than 20 countries round the Globe & set to emerge as a leader in the international ceramic tiles market.

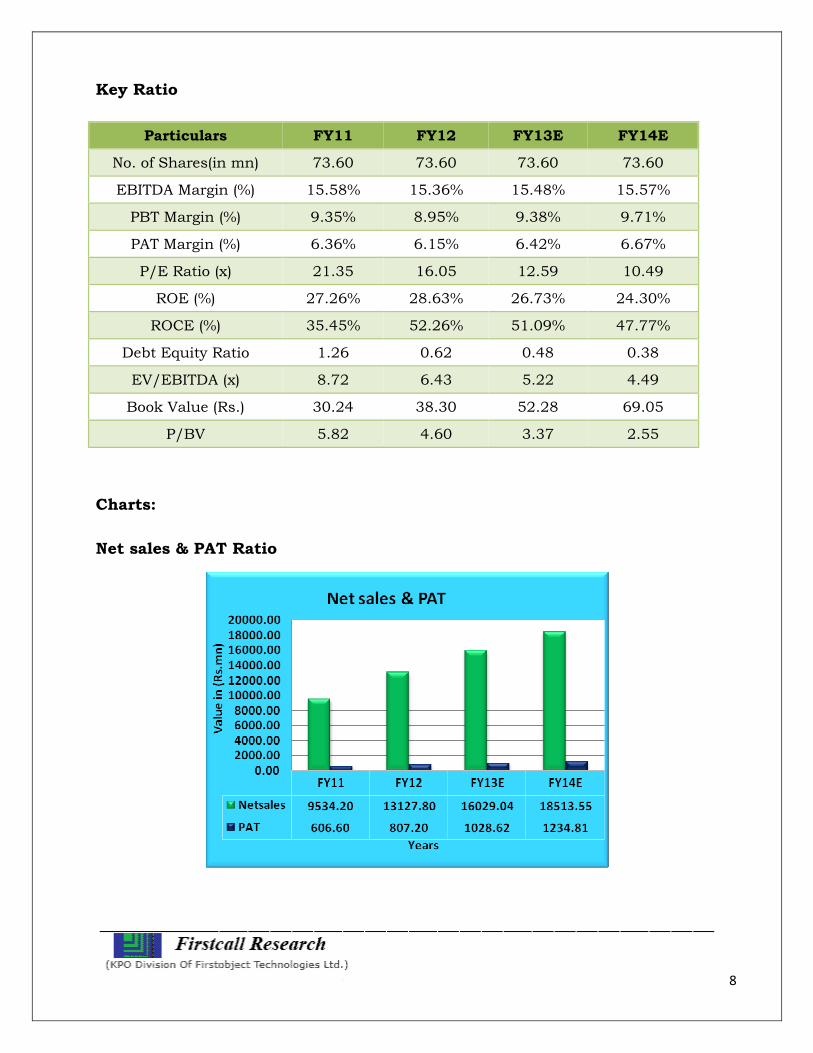

Net Sales and PAT of the company are expected to grow at a CAGR of 25% and 27% over 2011 to 2014E respectively.

Years Net sales (Rs mn)

EBITDA (Rs mn)

Net Profit (Rs mn) EPS P/E

FY 12 13127.80 2015.80 807.20 10.97 16.05

FY 13E 16029.04 2480.90 1028.62 13.98 12.59

FY 14E 18513.55 2883.27 1234.81 16.78 10.49

Stock Data:

Sector: Ceramic

Face Value Rs. Rs.2.00

52 wk. High/Low (Rs.) 190.80/84.00

Volume (2 wk. Avg.) 14000.00

BSE Code 500233

Market Cap (Rs.In mn) 12953.60

Share Holding Pattern

1 Year Comparative Graph

KAJARIA CERAMICS BSE SENSEX

C.M.P : Rs.176.00 Target Price : Rs.198.00 Date : July 14th 2012 BUY

KAJARIA CERAMICS LTD

Result Update: Q1 FY 13

2

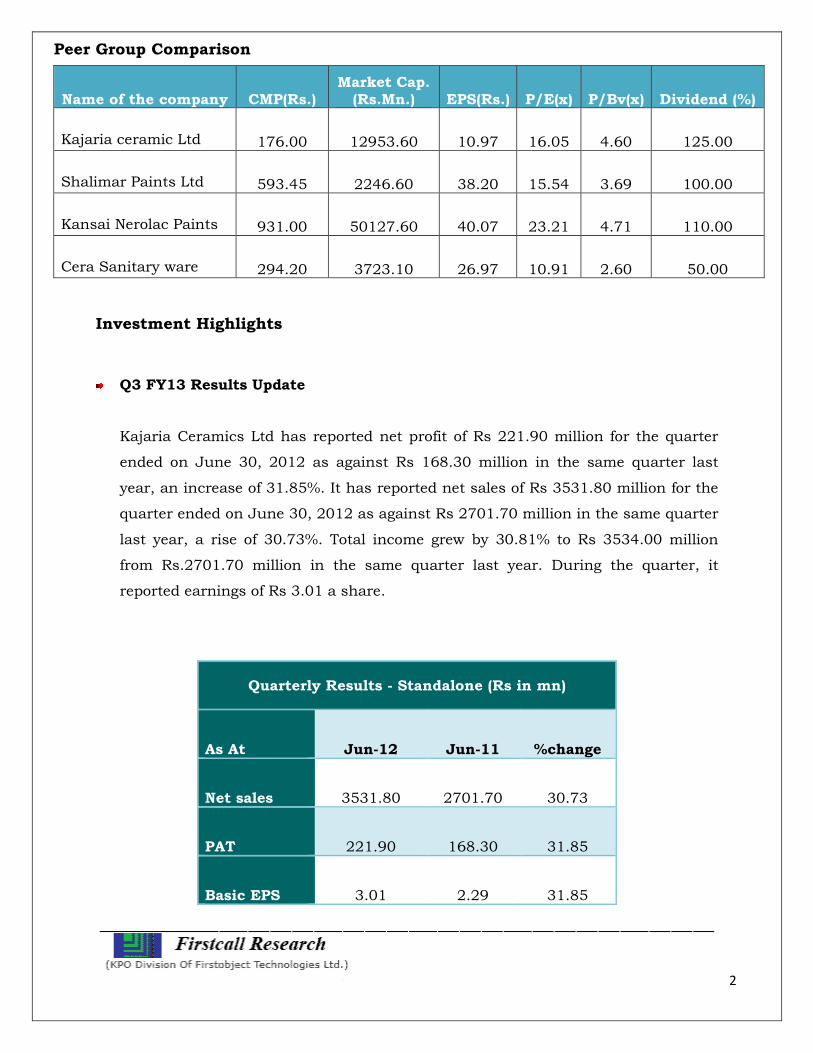

Peer Group Comparison

Name of the company CMP(Rs.) Market Cap. (Rs.Mn.) EPS(Rs.) P/E(x) P/Bv(x) Dividend (%)

Kajaria ceramic Ltd 176.00 12953.60 10.97 16.05 4.60 125.00

Shalimar Paints Ltd 593.45 2246.60 38.20 15.54 3.69 100.00

Kansai Nerolac Paints 931.00 50127.60 40.07 23.21 4.71 110.00

Cera Sanitary ware 294.20 3723.10 26.97 10.91 2.60 50.00

Investment Highlights

Q3 FY13 Results Update

Kajaria Ceramics Ltd has reported net profit of Rs 221.90 million for the quarter

ended on June 30, 2012 as against Rs 168.30 million in the same quarter last

year, an increase of 31.85%. It has reported net sales of Rs 3531.80 million for the

quarter ended on June 30, 2012 as against Rs 2701.70 million in the same quarter

last year, a rise of 30.73%. Total income grew by 30.81% to Rs 3534.00 million

from Rs.2701.70 million in the same quarter last year. During the quarter, it

reported earnings of Rs 3.01 a share.

Quarterly Results - Standalone (Rs in mn)

As At Jun-12 Jun-11 %change

Net sales 3531.80 2701.70 30.73

PAT 221.90 168.30 31.85

Basic EPS 3.01 2.29 31.85

3

Break Up of Expenditure

Recommended Dividend

Kajaria Ceramics Ltd has recommended a Dividend of 125% (Rs. 2.50 per equity

share of Rs. 2 each) for the financial year ended March 31, 2012.

Acquisition

Kajaria Ceramics Ltd has acquired 51% shareholding in M/s. Vennar Ceramics

Limited for a total consideration of Rs. 136.50 Million. Pursuant to Section 4 and

other applicable provisions of the Companies Act, 1956, M/s. Vennar Ceramics

Limited has become the subsidiary of the Company.

Future Outlook

� Kajaria Ceramics Ltd is planning to expand distribution network to locations with

significant demand potential areas.

� The company manufacturing plants are maintaining high-end digitally printed wall

tiles for sales exclusively through the Kajaria World network.

4

� Kajaria Ceramics Ltd strengthen the Tier-I distribution network and the company

planning to establish a Tier-II network.

� Kajaria Ceramics Ltd is planning to expand channel network from 30 to 70.

Company Profile

Kajaria Ceramics, incorporated in 1985, is the largest ceramic floor and wall tile

manufacturer in India. It has an annual aggregate capacity of 38.30 mn. sq. meters,

distributed across Five plants-Sikandrabad in Uttar Pradesh, Gailpur in Rajasthan,

two plants in Morbi in Gujarat and one at Vijayawada in Andhra Pradesh.

The company has an in-house research and development facility that focuses on

developing new designs and creating cost effective products.

Kajaria Ceramics has received various certifications such as ISO 9001 (for quality

management), ISO 14001 (environment management), OHSAS 18001 (for safety and

health management) and SA-8000 (for commitment to society). Kajaria Ceramics has

pan-India presence with a strong distribution network of about 600 dealers and over

6000 sub-dealers. Equipped with eight stock points, the company has Kajaria World

showrooms and owns 19 offices-cum-display centres.

Exports

KAJARIA Ceramics exports to more than 20 countries round the Globe. The

International Marketing operations are organized by a specialist export division that

manages a network of international agents and distributors supported by exclusive

office/showroom in UAE. Now in international markets they enjoy a similar brand

Recall as that of Domestic.

Company Brand "Kajaria" has today become synonym of Quality, service and

innovation not only in the domestic market but even in the international market.

"Kajaria" products are also well accepted in European market. With increased

capacity, increase in turnover and a growing domestic and exports market, Kajaria

Ceramics is set to emerge as a leader in the international ceramic tiles market.

5

Products

The company manufactures more than 400 options of flooring solutions such as wall

tiles, Floor tiles, vitrified tiles, Wooden Flooring, Sanitaryware & Fittings, Wellness,

Tile Adhesives & Grout and European tiles.

The tiles major market these products under the brand name such as Kajaria,

Kerrogres, Eternity, Aparici, Saloni ceramica, Ergon and GRESPANIA Ceramica.

Clientele

� Unitech

� DLF

� Parsvnath

� Magarpatta

� Sobha Developers

� DSK

� Mantri Group

� Prestige Group

� Ansals

� Hiranandani

� Raheja Developers

� Omaxe

� EMAAR-MGF

Subsidiary companies

� Soriso Ceramic Private Limited

� Jaxx Vitrified Private Limited

� Kajaria Ceramics Addis Plc

� Vennar Ceramics Limited

6

Financial Results

12 Months Ended Profit & Loss Account (Standalone)

Value(Rs.in.mn) FY11 FY12 FY13E FY14E

Description 12m 12m 12m 12m

Net Sales 9534.20 13127.80 16029.04 18513.55

Other Income 0.00 11.30 12.43 13.67

Total Income 9534.20 13139.10 16041.47 18527.22

Expenditure -8048.80 -11123.30 -13560.57 -15643.95

Operating Profit 1485.40 2015.80 2480.90 2883.27

Interest -298.60 -469.80 -554.36 -620.89

Gross profit 1186.80 1546.00 1926.54 2262.38

Depreciation -295.00 -370.80 -422.71 -464.98

Profit Before Tax 891.80 1175.20 1503.83 1797.40

Tax -285.20 -368.00 -475.21 -562.59

Profit After Tax 606.60 807.20 1028.62 1234.81

Equity capital 147.20 147.20 147.20 147.20

Reserves 2078.40 2671.80 3700.42 4935.23

Face value 2.00 2.00 2.00 2.00

EPS 8.24 10.97 13.98 16.78

7

Quarterly Ended Profit & Loss Account (Standalone)

Value(Rs.in.mn) 31-Dec-11 31-Mar-12 30-Jun-12 30-Sep-12E

Description 3m 3m 3m 3m

Net sales 3483.80 3774.70 3531.80 3990.93

Other income 0.00 11.30 2.20 0.00

Total Income 3483.80 3786.00 3534.00 3990.93

Expenditure -2936.10 -3208.80 -2995.10 -3392.29

Operating profit 547.70 577.20 538.90 598.64

Interest -150.80 -121.30 -120.60 -135.07

Gross profit 396.90 455.90 418.30 463.57

Depreciation -100.10 -95.20 -96.70 -97.67

Profit Before Tax 296.80 360.70 321.60 365.90

Tax -89.00 -118.60 -99.70 -114.16

Profit After Tax 207.80 242.10 221.90 251.74

Equity capital 147.80 147.20 147.20 147.20

Face value 2.00 2.00 2.00 2.00

EPS 2.81 3.29 3.01 3.42

8

Key Ratio

Particulars FY11 FY12 FY13E FY14E

No. of Shares(in mn) 73.60 73.60 73.60 73.60

EBITDA Margin (%) 15.58% 15.36% 15.48% 15.57%

PBT Margin (%) 9.35% 8.95% 9.38% 9.71%

PAT Margin (%) 6.36% 6.15% 6.42% 6.67%

P/E Ratio (x) 21.35 16.05 12.59 10.49

ROE (%) 27.26% 28.63% 26.73% 24.30%

ROCE (%) 35.45% 52.26% 51.09% 47.77%

Debt Equity Ratio 1.26 0.62 0.48 0.38

EV/EBITDA (x) 8.72 6.43 5.22 4.49

Book Value (Rs.) 30.24 38.30 52.28 69.05

P/BV 5.82 4.60 3.37 2.55

Charts:

Net sales & PAT Ratio

9

P/E Ratio

Debt Equity Ratio

10

EV/EBITDA Ratio

P/BV Ratio

11

Outlook and Conclusion

At the current market price of Rs.176.00, the stock is trading at 12.59 x FY13E

and 10.49 x FY14E respectively.

Earning per share (EPS) of the company for the earnings for FY13E and FY14E

is seen at Rs.13.98 and Rs.16.78 respectively.

Net Sales and PAT of the company are expected to grow at a CAGR of 25% and

27% over 2011to 2014E respectively.

On the basis of EV/EBITDA, the stock trades at 5.22 x for FY13E and 4.49 x

for FY14E.

Price to Book Value of the stock is expected to be at 3.37 x and 2.55 x

respectively for FY13E and FY14E.

We expect that the company will keep its growth story in the coming quarters

also. We recommend ‘BUY’ in this particular scrip with a target price of

Rs.198.00 for Medium to Long term investment.

Industry Overview

Indian ceramic industry

The Indian Tile industry ranks third in terms of production and consumption

(estimated at Rs 140 billion as of March 2011). The industry reported strong growth

owing to the emergence of tiles as durable, cost-effective and convenient solutions

over natural stone.

India’s consumption grew 12.95% CAGR between 2006-07 and 2010-11 to 557 MSM,

which were about 2x the global average. Its production grew at a 13.04% CAGR over

the same period to 550 MSM in FY11.

The tiles industry largely comprises ceramic wall and floor tiles and polished and

glazed vitrified tiles. The competitive intensity is less in the vitrified tiles segment; the

country imports vitrified tiles (especially glazed). Tiles are largely consumed by

residential, commercial, retail, hospitality and aviation segments.

12

The industry is fragmented with organized players accounting for 50% of the industry

turnover; the balance was represented by small unorganized/unbranded players,

primarily in Gujarat.

Rapid capacity addition increased home ownership and rising brand aspirations

resulted in a gradual shift of consumer preference towards value-added products.

Global tile industry

Following the 2008 and 2009 slowdowns, production and consumption rebounded

with double-digit growth in CY2010. Global production rose 11.7%, which was higher

than the annual historical average (6-7% up to 2007).

Production: The most remarkable production increase came out of Asia, increasing

its share to more than 66% of the global production due to sizeable volume increases

by all leading tile manufactures – China (+600 MSM), Vietnam (+80 MSM), India (+60

MSM) and Iran (+50 MSM).

Consumption: Global ceramic tile consumption increased from 8,460 billion sq. m to

9,350 billion sq. m (10.5% up from 2009) while it declined only in the EU from 991

MSM to 941 MSM (-5%). Asia reported the biggest consumption growth, up 14% to

6.026 billion sq. m, 64.4% of the global consumption. China, India, Iran, Vietnam,

Saudi Arabia, Thailand, the UAE and Malaysia reported large capacity increases.

Tiles tend to be produced near their consumption areas. Asia accounted for 66.9% of

production and 64.4% of world consumption, Europe (EU+ non-EU) 16.6% and 15%

respectively, the US 12.6% and 14.7% and Africa 4% and 5.5%.

The Urban growth

Increase in earning family members: The dependency ratio among Indian families

declined from 58% in 2005 to 55% in 2010 and is expected to decline to 52% in 2015

and 49% in 2020 (Source: ENAM).

India gets younger: In India, the working age declined sharply, providing high

disposable incomes. Close to 65% of Indians between 20-60 years are working,

leading to higher disposable incomes and lifestyle aspirations. Among BRIC nations,

13

India is expected to remain the youngest with its working-age population estimated to

rise to 70% of the total demographic by 2030 – the largest in the world. Some

estimates suggest that India will see 70 million new entrants into its workforce over

five years.

Increasing earnings and disposable income: The salary of the average Indian grew

12.6% in 2011, higher than most other global nations. India’s per capita income is

estimated to rise 14.3% to Rs 60,972 in 2011-12 (Source: Deccan Herald).

In line with economic growth, estimates suggest that PFCE is expected to scale from

US$790 billion in 2010 to US$3.6 trillion by 2020.

Semi-urban markets

Bharat Nirman: The Build India government initiative expects to build world-class

infrastructure across rural land areas.

Preferred locations: Increasing corporate are shifting focus to Tier-II and III cities,

accounting for over 61% of the total job creation in India in 2010-11. IT/ITeS sector

is expected to add 14 million direct and 55 million indirect job opportunities pan-

India

Housing demand growth

Population growth: India’s population rose to 1.21 billion in the last 10 years, an

increase by 181 million; overall growth is pegged at 1.76% in 2011, which will

catalyze residential demand.

Urbanization:

India is the fastest urbanizing country; UN estimates that 40% of India’s population

will be living in urban areas by 2030 (Source: Forbes India). Rising disposable income

(FY08-11 CAGR of ~15%), growing middle-class and increasing urbanization

(currently ~30% of the population) will boost the demand for improved flooring

solutions and value-added products.

14

Current status of the Industry

A major change that took over the ceramic tiles industry, was the introduction of

vitrified and porcelain tiles. These new entrant product types are said to be the tiles

of the future. Internationally these tiles are already the major sellers. These

categories of products account for almost 50% of total tile sales by value in this

industry.

These new products and the conventional wall & floor tiles have together made the

organized industry grow to a formidable Rs. 7,200 crores industry. This coupled with

a spate of expansions by many players make the industry look very promising in the

future.

The Indian Industry has developed an export market although at the lower end. In

volume it constitutes less than half a percent of the global market. (Presently India

does not figure in the list of major exporting countries). But this reality could change

as Indian exports are rising at an accelerating growth annually. The top-end of the

global export market is presently dominated by China (36.8%) and Italy (15.1%).

_______________ ____ _________________________ Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation

for the purchase or sale of any financial instrument or as an official confirmation of any

transaction. The information contained herein is from publicly available data or other

sources believed to be reliable but do not represent that it is accurate or complete and it

should not be relied on as such. Firstcall India Equity Advisors Pvt. Ltd. or any of it’s

affiliates shall not be in any way responsible for any loss or damage that may arise to any

person from any inadvertent error in the information contained in this report. This document

15

is provide for assistance only and is not intended to be and must not alone be taken as the

basis for an investment decision.

Firstcall India Equity Research: Email – [email protected]

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods

B.Anil Kumar Diversified

Ashish.Kushwaha Diversified

A,Nagaraju Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s,Takeover

Offers, Offer for Sale and Buy Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,

Placement of Equity / Debt with multilateral organizations, Short Term Funds

Management Debt & Equity, Working Capital Limits, Equity & Debt

Syndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions(domestic and

cross-border), divestitures, spin-offs, valuation of business, corporate

restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial

Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising

of capital through FCCBs, GDRs, ADRs and listing of the same on International

Stock Exchanges namely AIMs, Luxembourg, Singapore Stock Exchanges and

other international stock exchanges.

For Further Details Contact:

3rd Floor,Sankalp,The Bureau,Dr.R.C.Marg,Chembur,Mumbai 400 071

Tel. : 022-2527 2510/2527 6077/25276089 Telefax : 022-25276089

E-mail: [email protected]

www.firstcallindiaequity.com