june 22nd - 23rd - pwc · 2015-06-03 · agenda • global transfer pricing landscape • ifrs and...

TRANSCRIPT

Challenging timesImpact of IFRS, CFC & GAAR on TPAugust 2010

Agenda

• Global Transfer Pricing Landscape

• IFRS and Transfer Pricing

• CFC Rules and Transfer Pricing

• GAAR and Transfer Pricing

Global Transfer Pricing Landscape

Significant Developments – Transfer PricingOECD Guidelines on comparability

and business restructuring

ATO’s Strategic

Compliance Initiative

German Government’s

Business Restructuring

Rules

Canada’s “ACAP

Program”

IRS Final Service Regulations; Obama proposals on IP

Slide 5August 2010Thriving Through Challenging Times – An Interactive Session on Transfer Pricing

PricewaterhouseCoopers

• Dispute Resolution Panel

• Safe Harbour Rules • Advance Pricing

Arrangement (proposed)

• General Anti-Avoidance Rules

• DTC

IFRS and Transfer Pricing

PricewaterhouseCoopers

IFRS and TP

Slide 7August 2010Thriving Through Challenging Times – An Interactive Session on Transfer Pricing

Phase I – April 2011

Phase II – April 2013

Phase III – April 2014

Net worth > Rs 1000 crShares listed abroad

Nifty 50BSE 30

All listed companies

Net worth > Rs 500 cr

Transition to IFRS in India is Expected in Three Phases • Compare ‘like with like’

• Tested party & comparables may be adopting different accounting standards

• Use of PLIs, economic adjustments are highly sensitive to accounting standards used

• Limited information available to adjust for differences in accounting standards

Result Economic conditions remaining same, a company may not meet arm’s length

criterion under IFRS

PricewaterhouseCoopers

Fundamental changes in accounting and TP implications

Slide 8August 2010Thriving Through Challenging Times – An Interactive Session on Transfer Pricing

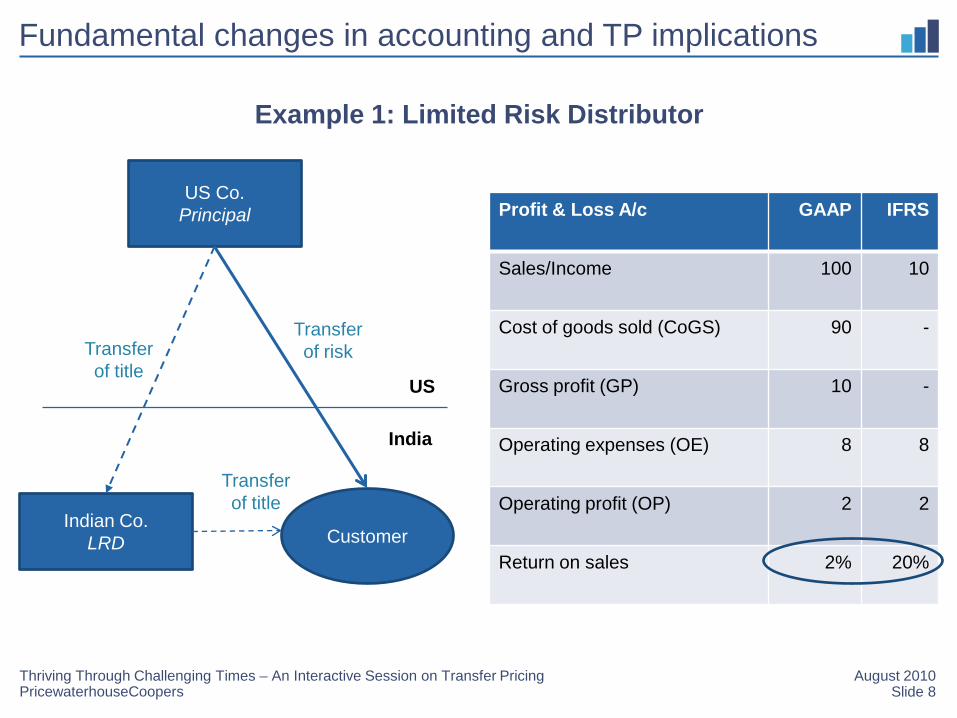

India

US

US Co.Principal

Indian Co.LRD Customer

Transfer of riskTransfer

of title

Transfer of title

Example 1: Limited Risk Distributor

Profit & Loss A/c GAAP IFRS

Sales/Income 100 10

Cost of goods sold (CoGS) 90 -

Gross profit (GP) 10 -

Operating expenses (OE) 8 8

Operating profit (OP) 2 2

Return on sales 2% 20%

PricewaterhouseCoopers

Fundamental changes in accounting and TP implications

Slide 9August 2010Thriving Through Challenging Times – An Interactive Session on Transfer Pricing

Profit & Loss A/c GAAP IFRS

Sales to AE 100 95

Interest income from AE 5

Cost of goods sold (CoGS) 70 70

Operating expenses (OE) 15 15

Operating profit (OP) 15 10

Return on Cost 17.64% 11.76%

US Co.Principal

Indian Co.Contract

Manufacturer

IndiaUS

Sale under long credit period Non operating

Example 2: Contract Manufacturer

PricewaterhouseCoopers

Fundamental changes in accounting and TP implications

Slide 10August 2010

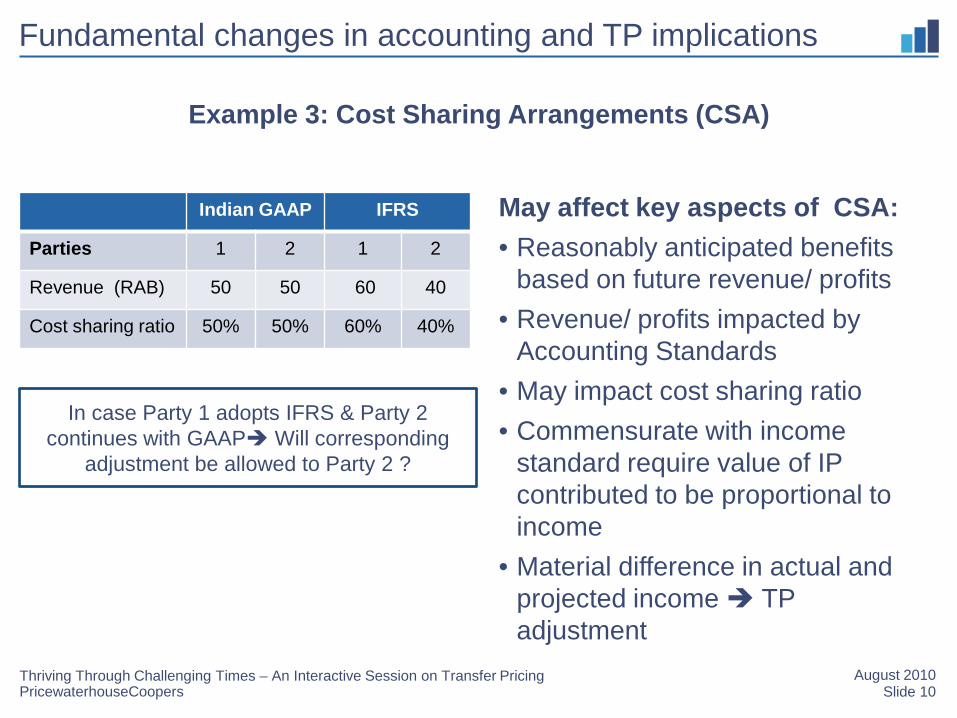

May affect key aspects of CSA:• Reasonably anticipated benefits

based on future revenue/ profits• Revenue/ profits impacted by

Accounting Standards• May impact cost sharing ratio• Commensurate with income

standard require value of IP contributed to be proportional to income

• Material difference in actual and projected income TP adjustment

Indian GAAP IFRS

Parties 1 2 1 2

Revenue (RAB) 50 50 60 40

Cost sharing ratio 50% 50% 60% 40%

In case Party 1 adopts IFRS & Party 2 continues with GAAP Will corresponding

adjustment be allowed to Party 2 ?

Example 3: Cost Sharing Arrangements (CSA)

Thriving Through Challenging Times – An Interactive Session on Transfer Pricing

PricewaterhouseCoopers

Fundamental changes in accounting and TP implications

Slide 11August 2010

Impact on Restructuring/ Combinations:• IFRS 3 all excess value over

acquired book value cannot be recognized as goodwill without analysis

• Purchase Price Allocation all acquired assets & liabilities including intangibles & contingent assets recorded at fair value

• Value of all assets & liabilities including goodwill to be allocated to each subsidiary

• Allocation of goodwill expected profits post merger transfer pricing policy

Others

Plant / Property / Equipment

Goodwill

Others

Trademark

Customer list

Goodwill

PPE

Purc

hase

Pric

eGAAP IFRS

Example 4: Business Combinations

Thriving Through Challenging Times – An Interactive Session on Transfer Pricing

PricewaterhouseCoopers

Transition to IFRS – Positive outcome in Transfer Pricing

Slide 12August 2010Thriving Through Challenging Times – An Interactive Session on Transfer Pricing

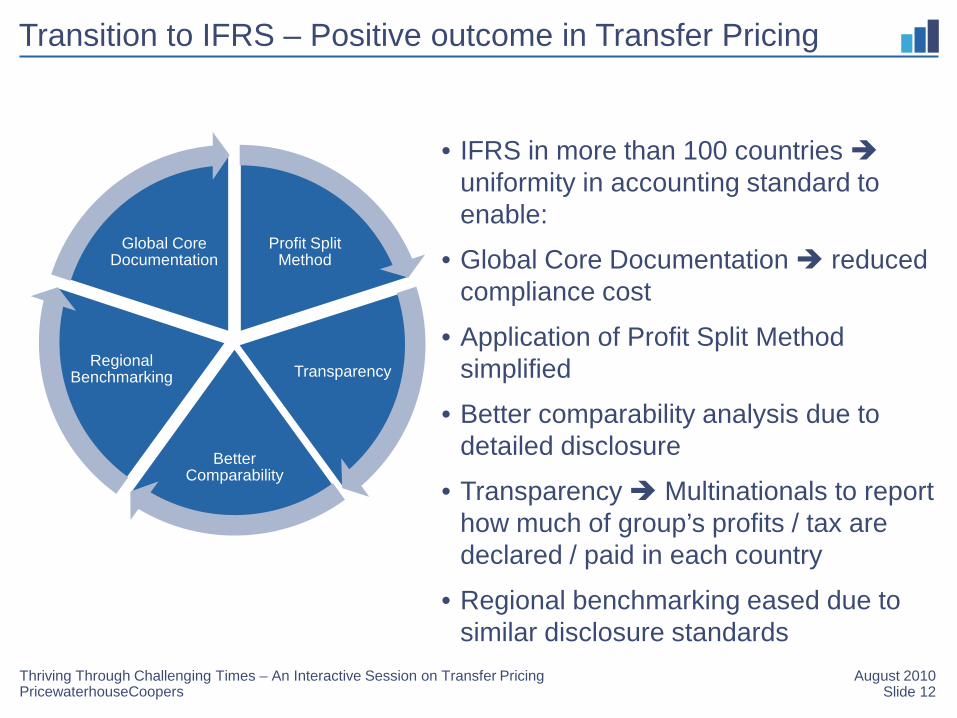

• IFRS in more than 100 countries uniformity in accounting standard to enable:

• Global Core Documentation reduced compliance cost

• Application of Profit Split Method simplified

• Better comparability analysis due to detailed disclosure

• Transparency Multinationals to report how much of group’s profits / tax are declared / paid in each country

• Regional benchmarking eased due to similar disclosure standards

Profit Split Method

Transparency

Better Comparability

Regional Benchmarking

Global Core Documentation

CFC Rules and Transfer Pricing

PricewaterhouseCoopers

CFC Regime and Transfer Pricing

Slide 14August 2010Thriving Through Challenging Times – An Interactive Session on Transfer Pricing

Scope of Controlled Foreign Companies (CFC) Rules

Passive income parked outside India at level of intermediate Hold Co, taxed in India

I Co

Hold Co[CFC]

Op Co

100% equity

• Revised discussion draft on DTC proposes introduction of CFC Rules

• Dividend income parked at level of Hold Co (treated as CFC), would be taxed in India as “deemed dividends” prevents deferral of tax

• No proposal for granting “underlying tax credit” as yet

• Dividend income (under CFC rules) will attract double taxation once at level of Op Co and again at level of India Co [assuming zero tax at level of Hold Co on dividends]

100% equity

PricewaterhouseCoopers

CFC Regime and Transfer Pricing

Slide 15August 2010Thriving Through Challenging Times – An Interactive Session on Transfer Pricing

• Report of Working Group on Non Resident Taxation (2003) observed some features of CFC rules in context of other countries :– Threshold of “control”/ “ownership” varies between 10% to 50%– Two alternative approaches –

• Transactional approach CFC rules apply to passive incomes (irrespective of target jurisdiction)

• Jurisdictional approach CFC rules apply for target low tax jurisdictions

• Passive incomes dividend, interest, royalties (without substance), foreign base company sales (contract manufacturing structure), etc

• “Motive” exemption for CFCs not established to avoid tax• What is interplay between CFC & TP ?• Can TP be used as a planning tool

PricewaterhouseCoopers

CFC Regime and Transfer Pricing

Slide 16August 2010Thriving Through Challenging Times – An Interactive Session on Transfer Pricing

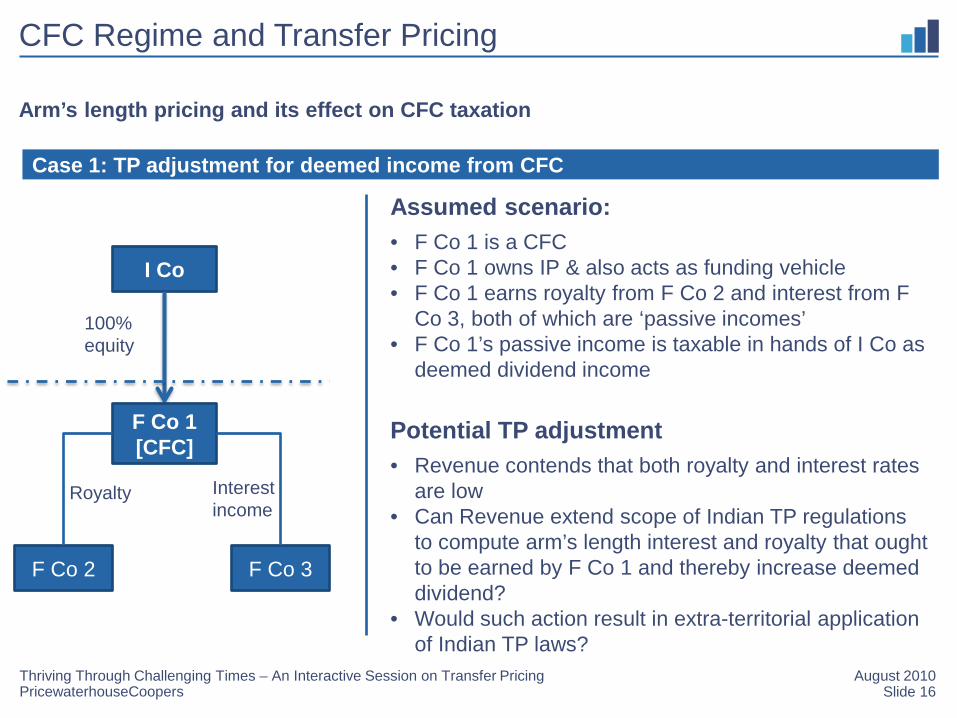

Arm’s length pricing and its effect on CFC taxation

Case 1: TP adjustment for deemed income from CFC

I Co

F Co 1[CFC]

F Co 2 F Co 3

100% equity

Assumed scenario:• F Co 1 is a CFC• F Co 1 owns IP & also acts as funding vehicle• F Co 1 earns royalty from F Co 2 and interest from F

Co 3, both of which are ‘passive incomes’• F Co 1’s passive income is taxable in hands of I Co as

deemed dividend income

Potential TP adjustment• Revenue contends that both royalty and interest rates

are low• Can Revenue extend scope of Indian TP regulations

to compute arm’s length interest and royalty that ought to be earned by F Co 1 and thereby increase deemed dividend?

• Would such action result in extra-territorial application of Indian TP laws?

Interest income

Royalty

PricewaterhouseCoopers

CFC Regime and Transfer Pricing

Slide 17August 2010Thriving Through Challenging Times – An Interactive Session on Transfer Pricing

Arm’s length pricing and its effect on CFC taxation

Case 2: TP adjustment to transactions between CFC and another group company

I Co 2I Co 1

F Co 1[CFC]

Interest free loan

F Co 2

Interest

100% equity

Assumed scenario:• F Co 1 is a CFC• I Co 2 (group company) lends interest free loan to F

Co 1• F Co 1 lends onwards to F Co 2 and earns interest

income which is ‘passive income’• CFC’s passive income is taxable in hands of I Co 1

as deemed dividend income (no exemptions available)

• Arm’s length interest income computed in the hands of I Co 2

• Double taxation of same income in hands of I Co 1 (CFC rules) & I Co 2 (TP rules)

• CFC rules to be robust to address above issue; else TP adjustment to get preference as per foreign legal precedent

PricewaterhouseCoopers

CFC Regime and Transfer Pricing

Slide 18August 2010Thriving Through Challenging Times – An Interactive Session on Transfer Pricing

Interplay between CFC and TP

Passive income parked outside India at level of intermediate Hold Co, taxed in India

I Co

Hold Co[CFC]

Op Co

100% equity

• Can Hold Co be converted into an IP headquartered company, by moving “substance” and “IP” to Hold Co?

• Transfer Pricing planning could mitigate hardship of double taxation, through portability of entrepreneurial profits at level of I Co (in case it serves Group’s objectives) single level of tax in India

100% equity

GAAR and Transfer Pricing

PricewaterhouseCoopers

General Anti Avoidance Rules (‘GAAR’) and Transfer Pricing

Slide 20August 2010Thriving Through Challenging Times – An Interactive Session on Transfer Pricing

• GAAR under draft DTC – impermissible avoidance arrangement, if

– entered into with the objective of obtaining tax benefit

and,

– creates rights or obligations, which would not normally be created if the transaction was implemented at arm’s length; or

– results in, directly or indirectly, misuse or abuse of the provisions of the Code; or

– lacks commercial substance in whole or in part; or

– is not for bonafide purpose.

PricewaterhouseCoopers

GAAR and Transfer Pricing

Slide 21August 2010Thriving Through Challenging Times – An Interactive Session on Transfer Pricing

• Tax consequences if GAAR is invoked :

– Disregard, combine, re-characterize part or whole of the arrangement

– Disregard any accommodating party

– Deem persons who are connected to be one and the same person

– Re-characterize or re-allocate income

– Re-characterize multi-party financing transaction

– Re-characterize debt financing as equity or vice versa

• Onus on taxpayer to demonstrate obtaining tax benefit was not main purpose of arrangement

• No compensatory adjustment provisions

PricewaterhouseCoopers

GAAR and Transfer Pricing

Slide 22August 2010Thriving Through Challenging Times – An Interactive Session on Transfer Pricing

• Thin capitalisation :

– Recharacterisation of loan to equity disallowance of relevant interest, even if rate at arm’s length

– How would non-deductible interest be treated ? Dividend, subject to DDT secondary adjustment ?

• Business restructuring :

– Commercial substance (transfer pricing) + commercial justification (GAAR) ?

– Exit cost upon conversion (transfer pricing) + acceptance of low risk model post conversion (GAAR) ?

PricewaterhouseCoopers

Key Takeaways

Slide 23August 2010Thriving Through Challenging Times – An Interactive Session on Transfer Pricing

• Economic Substance

• Robust Documentation

© 2010 PricewaterhouseCoopers. All rights reserved. “PricewaterhouseCoopers”, a registered trademark, refers to PricewaterhouseCoopers Private Limited (a limited company in India) or, as the context requires, other member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity.

Thank You