june 2, 2014 2014 - jefferies · tennova healthcare •6 hospitals •1,000 physicians central...

TRANSCRIPT

2014

Jefferies Healthcare ConferenceJune 2, 2014

Forward-Looking Statements

This presentation contains forward looking statements within the meaning of Section 27A of the Securities Act,

Section 21E of the Exchange Act and the Private Securities Litigation Reform Act of 1995 that involve risk and

uncertainties. All statements in this presentation other than statements of historical fact, including statements

regarding projections, expected operating results, and other events that depend upon or refer to future events or

conditions or that include words such as “expects,” “anticipates,” “intends,” “plans,” “believes,” “estimates,” “thinks,”

and similar expressions, are forward ‐ looking statements. Although the Company believes that these forward ‐

looking statements are based on reasonable assumptions, these assumptions are inherently subject to significant

economic and competitive uncertainties and contingencies, which are difficult or impossible to predict accurately and

are beyond the control of the Company. Accordingly, the Company cannot give any assurance that its expectations

will in fact occur and cautions that actual results may differ materially from those in the forward‐looking statements.

A number of factors could affect the future results of the Company or the healthcare industry generally and could

cause the Company’s expected results to differ materially from those expressed in this presentation.

The consolidated operating results for the three months ended March 31, 2014, are not necessarily indicative of the

results that may be experienced for any such future period or for any future year. The Company cautions that the

projections for calendar year 2014 set forth in this presentation are given as of the date hereof based on currently

available information. The Company undertakes no obligation to revise or update any forward ‐ looking statements, or

to make any other forward ‐ looking statements, whether as a result of new information, future events or otherwise

2

CHS – An Experienced Operator

3

$1,306$1,531$2,039

$2,677$3,204

$3,738$4,180

$7,127

$10,840

$12,108

$11,092

$11,906

$13,029$12,998

0

2,500

5,000

7,500

10,000

12,500

15,000 ($MM) Revenues

$251 $291$349

$429$494

$573 $572

$827

$1,525

$1,671$1,761

$1,837$1,978

$1,841

0

250

500

750

1,000

1,250

1,500

1,750

2,000

EBITDA **($MM)

Proforma YE 2013

Revenue (1) $18,791 $12,998

EBITDA (1) ** $2,566 $1,841

** See the Unaudited Supplemental Information contained in this presentation for a definition of EBITDA and a reconciliation of Adjusted EBITDA, as defined, to our net cash provided by operating activities as derived directly from our consolidated financial statements for the three months ended March 31, 2014 and 2013 (Slides 34 and 35). For purposes of this presentation, EBITDA means Adjusted EBITDA.

(1) See note on slide 27.

* CAGR is calculated prior to the change in presentation of bad debt.

Revenue and EBITDA for 2009 and prior years have not been adjusted for discontinued operations.

2007 amounts include adjustments for change in estimate taken in Q407.

2006 EBITDA excludes increase in allowance for doubtful accounts of $65 million taken in Q306.

Community Health Systems

44

• Founded in 1985

• NYSE Listed Company since 2000 Symbol: CYH

• 208 Hospitals in 29 States

• 1 Million Annual Admissions

• 5 Million Annual ED Visits

• 135,000 Employees

• 22,000 Physicians on Medical Staffs

Why CHS has Long-Term Opportunities

• Improvement in the reduction of self-pay to insurance (Medicaid or Exchanges)

• Hospitals located in 9 of top 10 highest uninsured states and 26 of top 30 highest uninsured states

Affordable Care Act

• Potential synergies of $250 million over two years

• HMA’s adjusted EBITDA margin was 12-13% in 2013 vs. 15-16% in 2010, 2011 & 2012

• Key Markets of HMA transaction, including large presence in Florida, Tennessee, Oklahoma, and Mississippi. Building on network development.

HMA

• Proforma currently at 6x’s and expect to delever to mid 4x’s in 24 months

• Maintain disciplined approach to deploying capital

• ACA expected to contribute meaningfully to 2014 through 2017

Deleveraging

Low Valuation

5

• EV/EBITDA – Peers .7x differential or $54.07 stock price

• PE – Peers 9x differential or $62.48 stock price

Note: Calculations as of mid-May 2014

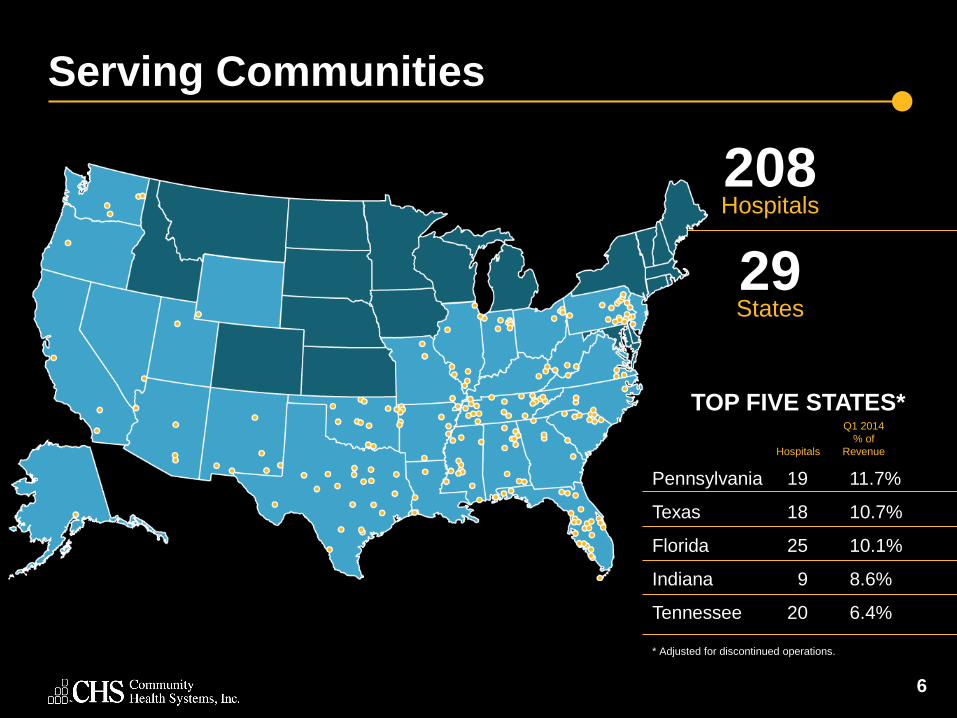

Serving Communities

6

208Hospitals

29States

Pennsylvania 19 11.7%

Texas 18 10.7%

Florida 25 10.1%

Indiana 9 8.6%

Tennessee 20 6.4%

Q1 2014

% of

Hospitals Revenue

TOP FIVE STATES*

* Adjusted for discontinued operations.

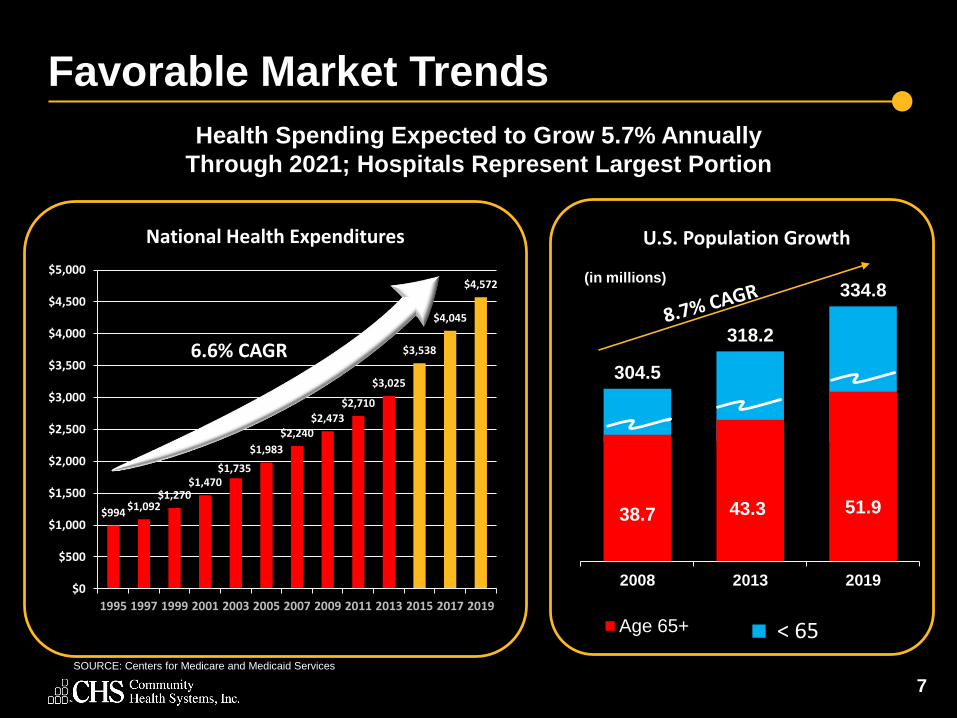

304.5

318.2

334.8

< 65

38.7 43.3 51.9

2008 2013 2019

Age 65+

Favorable Market Trends

7

$994$1,092

$1,270$1,470

$1,735

$1,983

$2,240$2,473

$2,710

$3,025

$3,538

$4,045

$4,572

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Health Spending Expected to Grow 5.7% Annually

Through 2021; Hospitals Represent Largest Portion

National Health Expenditures U.S. Population Growth

SOURCE: Centers for Medicare and Medicaid Services

6.6% CAGR

(in millions)

Changing Healthcare Environment

Requires New Approaches

8

Movement to value-based payment

Challenging reimbursement

Narrow networks forming

More insured consumers through exchanges and Medicaid expansion

Well-Positioned for Healthcare Reform

Demonstrate Quality

Build Services and Infrastructure

Deliver Care More

Efficiently

Clinical Integration & Collaboration

26 million Newly Insured Patients by 2017*

* Congressional Budget Office: April 2014

9

Well-Positioned for Healthcare Reform

CHS and HMA are well positioned to participate as a network provider on

various health insurance exchanges

Hospitals located in 9 of top 10 highest uninsured states and 26 of top 30

highest uninsured states

195 of 197 hospitals participating

− Participating in the lowest cost HIX plan in our markets

− 90% in bronze plans

− 93% in silver plans

Most CHS exchange reimbursement arrangements reflect slight discount vs. commercial rates

2014 Healthcare Reform benefit to EBTIDA: 0.5% to 0.8% of net operating revenues; approx. $95 - $160 million

Our self-pay adjusted admissions are expected to decrease from approximately 8% into 4% in 2016.

10

Affordable Care Act

11

Admissions Q1 2013 Q1 2014 Change % Change

Self Pay

% of Admissions

3,783

6.6%

2,728

5.2%

-1,055 -28%

-140 BPS

Medicaid

% of Admissions

10,951

19.2%

11,415

21.7%

464 4%

+250 BPS

Adjusted Admissions Q1 2013 Q1 2014 Change % Change

Self Pay

% of Adjusted Admissions

8,102

7.1%

5,687

5.3%

-2,415 -30%

-180 BPS

Medicaid

% of Adjusted Admissions

23,413

20.6%

25,226

23.3%

1,813 8%

+270 BPS

Data from Same Store Expansion States

We have estimated an approximate 15% reduction in self-pay adjusted admissions in 2014.

Admissions and adjusted admissions from expansion states represent approximately 25% of the total.

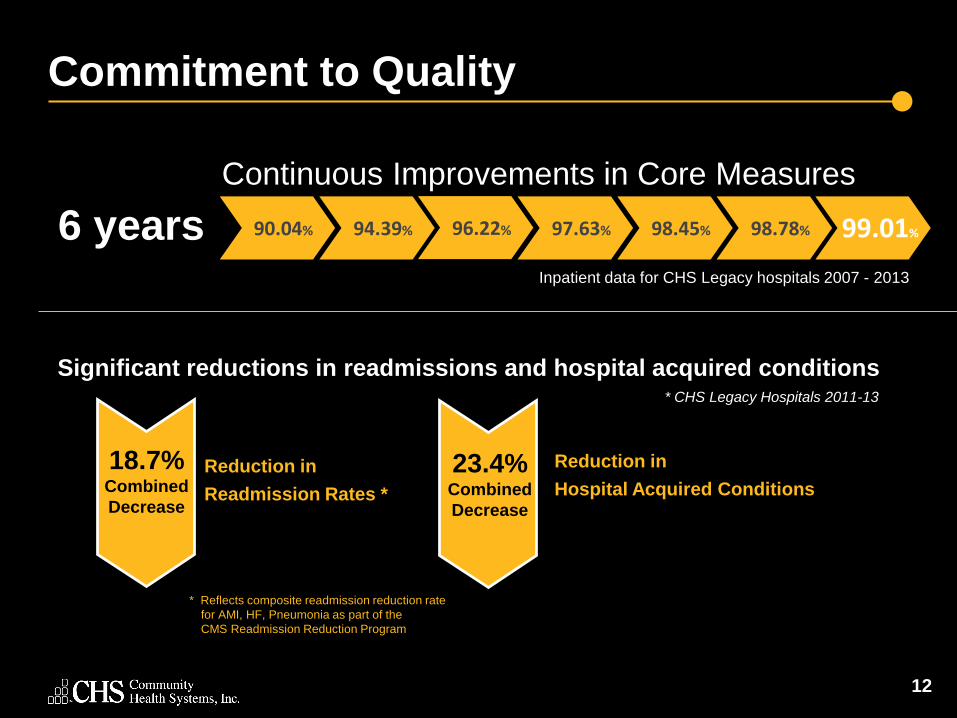

Commitment to Quality

Continuous Improvements in Core Measures

90.04%

Inpatient data for CHS Legacy hospitals 2007 - 2013

6 years 94.39% 96.22% 97.63% 98.45% 98.78% 99.01%

Reduction in

Readmission Rates *

18.7%Combined

Decrease

Reduction in

Hospital Acquired Conditions

23.4%Combined

Decrease

Significant reductions in readmissions and hospital acquired conditions* CHS Legacy Hospitals 2011-13

12

* Reflects composite readmission reduction rate

for AMI, HF, Pneumonia as part of the

CMS Readmission Reduction Program

High Reliability

Using techniques from high-risk

industries like nuclear power and

aviation to create inherently safe

hospital environments

13

15.5% Reduction

in Serious Safety

Event Rate in 2013

Accreditations

14

Joint Commission Top Performers

on Key Quality Measures in 2013

93 hospitals

80 hospitalsCertified Chest Pain Centers

20+ hospitalsCertified Stroke Centers

CHS Network Development

15

Rockwood Health System• 2 hospitals

• 570 physicians

Commonwealth Health• 8 hospitals

• 890 physicians

Northwest Health Arkansas• 4 hospitals

• 500 physicians

Northwest Healthcare• 2 hospitals

• 540 physicians

Lutheran Health Network• 8 hospitals

• 1,420 physicians

Valley Care Health of Ohio• 3 hospitals

• 500 physicians

Central Mississippi• 6 hospitals

• 1,000 physicians* Active Medical Staff Physicians

Bayfront Health• 7 hospitals

• 1,100 physicians

Northern Alabama Network• 5 hospitals

• 880 physicians

Tennova Healthcare• 6 Hospitals

• 1,000 physicians

Central Oklahoma Healthcare• 7 hospitals

• 600 physicians

Lutheran Health Network

16

Physician

Offices/Clinics

8 Hospitals

Urgent Care/

Occupational Health

Outpatient

Clinics11

Ambulatory

Surgery Centers4

9

87

Regional Networks

• Building eleven major networks in key states:

- Incorporates over 30 percent of affiliated hospitals

- Supported by strong physician base and outpatient services

- Developing clinical destinations and centers of excellence

Growth Strategies

17

Service Line Approach

• Enhancing services with the

greatest growth potential:

– Orthopedics

– Neuroscience

– Cardiovascular Care

– Women’s Health

– Cancer Care

Access Points

• Maximizing existing physician practices

• Developing urgent care and retail

clinic partnerships

• Growing outpatient diagnostic and surgery

capacity

• Advancing tele-health strategies

Emergency Medicine

• Focusing on throughput and the

patient experience

• Expanding services and accreditations

• Building coordinated call and

transfer centers

• Developing EMS and other partnerships

1,679

1,852 1,864

2,125 2,141

418

613

0

500

1000

1500

2000

2500

2009 2010 2011 2012 2013 Q1 2013 Q1 2014

• Almost 10,000 physicians recruited over the past 5 years

• Over 1,100 mid-level licensed professionals employed at March 31, 2014

Physician Recruitment

18

Physician Satisfaction

19

I am satisfied with this hospital as a place to practice medicine.

I would recommend this hospital to my own family or friends.

I am satisfied with the quality of nursing care at this hospital.

I am satisfied with this hospital’s efforts to provide safe care to patients.

89%

94%

91%

92%

* CHS Legacy Hospitals 2013 Survey

I am proud to be a part of the organization.

I am satisfied with the courtesy and respect I receive from others in my department.

I believe the leadership in my hospital iscommitted to the Community Cares culture.

I believe patients are treated as valued customers.

Employee Satisfaction

20

90%

92%

93%

National Employee Satisfaction Survey:

85% Overall Satisfaction in 2013

88%

* CHS Legacy Hospitals 2013 Survey

Standardized and Centralized

21

• Acquisitions

• Ancillary Services(Pharmacy, Laboratory, Imaging)

• Billing and Collections

• Compliance

• ER Management

• Executive Recruitment

• Facilities Management

• Financial Reporting

• Group Purchasing

• Health Information Management

• Home Care

• Human Resources/Recruiting

• Information Systems

• Legal Services

• Managed Care

• Physician Practice Management

• Physician Recruitment

• Quality and Clinical Support

• Revenue Strategies

• Strategy and Marketing

Shared Resources for Performance Improvement

Improve Efficiency to Lower Costs

• Consolidating some business office and other support functions to Shared Services Centers

• Standardized procurement processes

• Cost controls to manage operating expenses

Operational Efficiency

• Reducing clinical variation to improve quality and reduce costs

• Case management focus to reduce length of stay and improve clinical documentation

• Appropriate utilization of services and supplies

Clinical Efficiency

22

History of Successful Acquisitions

23

Focused on Network

Development, Clinical

Excellence and Value

to succeed in the Era of Healthcare

Reform

2014 - Future

71 Hospitals added in Health

Management AssociatesAcquisition

2014

Select Divestitures

Strategic Acquisitions

2008-2013

50+ Hospitals Added in Triad

Hospitals Acquisition

Larger, More Competitive

Markets

2007

Significant Growth through

Acquisitions

IPO on the NYSE in 2000

1985-2006

2007 Number of

Hospitals:1282013 Number

of Hospitals: 135Current Number

of Hospitals: 208

2006 Number of

Hospitals: 77

2013 Acquisition Performance –CHS Legacy

24

Trailing Actual 2013

2012 - 4 hospitals

2010 - 4 hospitals

2009 - 3 hospitals

2008 - 2 hospital

2007 - 2 hospitals & Triad

2006 - 7 hospitals

2005 - 4 hospitals

2004 - 2 hospitals

2003 - 10 hospitals

2002 - 6 hospitals

1997 - 2001 - 21 hospitals

Trailing Actual 2013

EBITDA **Net Revenue*

$1,718 (a)

$898

$10,308

$11,927

65 hospitals acquired since 1997, excluding Triad (approximately

50 hospitals)

15.7%

91.3%

* Revenues have not been restated to reflect the change in bad debt. ** See the Unaudited Supplemental Information contained in this presentation for a definition of EBITDA and a reconciliation of Adjusted EBITDA, as

defined, to our net cash provided by operating activities as derived directly from our consolidated financial statements for the three months ended March 31, 2014 and 2013 (Slides 34 and 35). For purposes of this presentation, EBITDA means Adjusted EBITDA.

(a) EBITDA includes corporate overhead.

2014 Acquisitions to Date

25

Health Management Associates

• 71 hospital facilities, 11,000 beds

Munroe Regional Medical Center

• 421 beds

Sharon Regional Medical Center

• 251 beds

January 27, 2014

April 1, 2014

April 1, 2014

HMA: A Strategic Acquisition

• Adds 71 hospital facilities to create the largest U.S. footprint

• Complementary geographic fit with hospitals in CHS states

• Expands and strengthens hospital and physician networks

• Leverages economies of scale and operating efficiencies

Unique Opportunity

• HMA’s adjusted EBITDA margin was 12-13% in 2013 vs. 15-16% in 2010, 2011 & 2012

• HMA lags CHS facilities in core measures and HCAHPs (patient satisfaction)

• Potential synergies of $250 million over two years

Improvement Potential

• CHS successfully integrated Triad - $5 billion revenue

• Improved Triad operating margin from 12% to 16%

• 94% of current CHS senior executives helped integrate Triad

Proven Ability to Integrate

26

Number of hospitals acquired since 1997: 115

Combined Company

CHS(1) HMA(1) Combined

Revenues $12,998 $5,793 $18,791

Adjusted EBITDA $1,841 $725 $2,566

Hospitals 135 71 206

Licensed Beds 20,175 11,065 31,245

Surgery Centers 35 17 52

Home Health Agencies 80 14 94

Employed Physicians 2,500 1,000 3,500

Employees 95,000 40,000 135,000

27

(1) Certain unaudited financial information has been previously disclosed in other public presentations.

Significant Synergies

28

• Overhead and Corporate

Service Reduction

• Supply Management

• Case Management

• Revenue Cycle Management

40 percent of synergy potential projected in the first year

$250 Million

of synergies

within 2 years

Revenue and EBITDA

11,906

13,029 12,998

3,274

4,195

5,053

5,836 5,793

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2011 2012 2013 Q1 2013 Q1 2014

29

** See the Unaudited Supplemental Information contained in this presentation for a definition of EBITDA and a reconciliation of Adjusted EBITDA, as defined, to our net cash provided by operating activities as derived directly

from our consolidated financial statements for the three months ended March 31, 2014 and 2013 (Slides 34 and 35). For purposes of this presentation, EBITDA means Adjusted EBITDA.

* CAGR is calculated prior to the change in presentation of bad debt. Revenue and EBITDA for 2009 and prior years have not been adjusted for discontinued operations.

2007 amounts include adjustments for change in estimate taken in Q407. 2006 EBITDA excludes increase in allowance for doubtful accounts of $65 million taken in Q306.

1,837 1,880 1,841

495541

817

934

725

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2011 2012 2013 Q1 2013 Q1 2014

Revenue EBITDA

CHSHMA

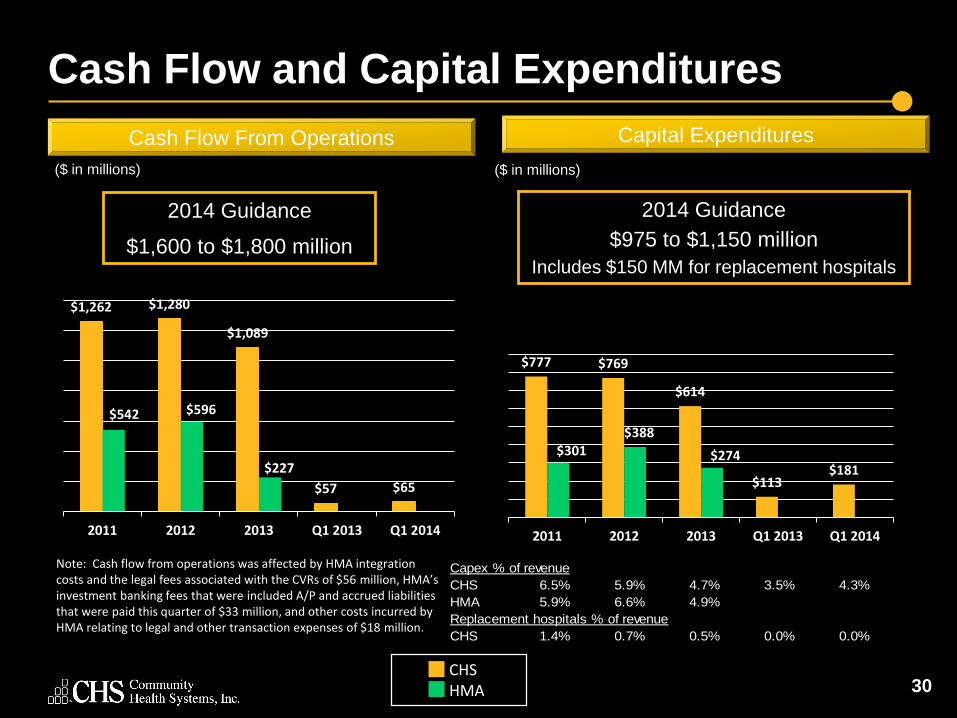

Cash Flow and Capital Expenditures

30

$1,262 $1,280

$1,089

$57 $65

$542 $596

$227

2011 2012 2013 Q1 2013 Q1 2014

$777 $769

$614

$113$181

$301$388

$274

2011 2012 2013 Q1 2013 Q1 2014

Capex % of revenue

CHS 6.5% 5.9% 4.7% 3.5% 4.3%

HMA 5.9% 6.6% 4.9%

Replacement hospitals % of revenue

CHS 1.4% 0.7% 0.5% 0.0% 0.0%

($ in millions)($ in millions)

2014 Guidance

$1,600 to $1,800 million

2014 Guidance

$975 to $1,150 million

Includes $150 MM for replacement hospitals

Capital ExpendituresCash Flow From Operations

Note: Cash flow from operations was affected by HMA integration costs and the legal fees associated with the CVRs of $56 million, HMA’s investment banking fees that were included A/P and accrued liabilities that were paid this quarter of $33 million, and other costs incurred by HMA relating to legal and other transaction expenses of $18 million.

CHSHMA

Quarterly Income Summary

31

(Amounts in millions, except margin and EPS)

Quarter Ended3-31-2014* 3-31-2013*

Net Revenue $ 4,195 $ 3,274

Adjusted EBITDA (2) ** $ 541 $ 495

EBITDA Margin ** 12.9% 15.1%

EPS from Continuing Operations Excluding Adjustments (1) $ 0.27 $ 0.89

Shares Outstanding (Weighted and Fully Diluted) 107 92

(1) The results for the three months ended March 31, 2014, include $0.30 per share of expenses related to acquisition and integration expenses from our acquisition of HMA; $0.02 per diluted

share of legal expenses related to HMA legal proceedings in existence prior to the HMA acquisition, which underlie the Contingent Value Rights (“CVR”) Agreement; $0.42 per diluted share of

expenses related to the loss from early extinguishment of debt; $0.24 per diluted share of expenses related to the accelerating amortization on software to be abandoned; $0.14 per diluted

share of expenses related to the impairment of software costs taken out of service; and a total after-tax loss of $0.19 per diluted share for discontinued operations. See slide 37 for

reconciliation.

(2) See slide 37 for reconciliation.

*2014 first quarter consolidated results include the HMA results from the acquisition date of January 27, 2014. The 2013 consolidated first quarter results represent last year’s performance for CHS

only. Same store results reflect the HMA performance from February 1st for both 2014 and 2013. Same store results include those hospitals that we have operated for a full year. CHS believes the

same store metrics are more meaningful since these metrics represent an equivalent comparison.

** See the Unaudited Supplemental Information contained in this presentation for a definition of EBITDA and a reconciliation of Adjusted EBITDA, as defined, to our net cash provided by operating

activities as derived directly from our consolidated financial statements for the three months ended March 31, 2014 and 2013 (Slides 34 and 35). For purposes of this presentation, EBITDA means

Adjusted EBITDA.

Financial Performance

32

$1,306$1,531

$2,039

$2,677$3,204

$3,738$4,180

$7,127

$10,840

$12,108

$11,092

$11,906

$13,029 $12,998

0

2,500

5,000

7,500

10,000

12,500

15,000

$251$291

$349$429

$494$573 $572

$827

$1,525

$1,671

$1,761$1,837

$1,978

$1,841

0

250

500

750

1,000

1,250

1,500

1,750

2,000

** See the Unaudited Supplemental Information contained in this presentation for a definition of EBITDA and a reconciliation of Adjusted EBITDA, as defined, to our net cash provided by operating activities as derived directly

from our consolidated financial statements for the three months ended March 31, 2014 and 2013 (Slides 34 and 35). For purposes of this presentation, EBITDA means Adjusted EBITDA.

* CAGR is calculated prior to the change in presentation of bad debt. Revenue and EBITDA for 2009 and prior years have not been adjusted for discontinued operations.

2007 amounts include adjustments for change in estimate taken in Q407. 2006 EBITDA excludes increase in allowance for doubtful accounts of $65 million taken in Q306.

Revenue EBITDA

Focused Strategy Delivers Results

33

Company

Growth

Quality

Improvements

Acquisition

Opportunities

ConsistentFinancial

Performance

Experienced

Management

Attractive

Markets

Geographic

Diversity

Proven

Formula

34

Unaudited Supplemental Information

EBITDA consists of net income attributable to Community Health Systems, Inc. before interest, income taxes,

and depreciation and amortization. Adjusted EBITDA is EBITDA adjusted to exclude discontinued

operations, gain/loss from early extinguishment of debt and net income attributable to noncontrolling

interests. The Company has from time to time sold noncontrolling interests in certain of its subsidiaries or

acquired subsidiaries with existing noncontrolling interest ownership positions. The Company believes that it

is useful to present adjusted EBITDA because it excludes the portion of EBITDA attributable to these third

party interests and clarifies for investors the Company’s portion of EBITDA generated by continuing

operations. The Company uses adjusted EBITDA as a measure of liquidity. The Company has included this

measure because it believes it provides investors with additional information about the Company’s ability to

incur and service debt and make capital expenditures. Adjusted EBITDA is the basis for a key component in

the determination of the Company’s compliance with some of the covenants under the Company’s senior

secured credit facility, as well as to determine the interest rate and commitment fee payable under the senior

secured credit facility.

Adjusted EBITDA is not a measurement of financial performance or liquidity under generally accepted

accounting principles. It should not be considered in isolation or as a substitute for net income, operating

income, cash flows from operating, investing or financing activities, or any other measure calculated in

accordance with generally accepted accounting principles. The items excluded from adjusted EBITDA are

significant components in understanding and evaluating financial performance and liquidity. This calculation

of adjusted EBITDA may not be comparable to similarly titled measures reported by other companies.

Unaudited Supplemental Information

35

The following table reconciles ADJUSTED EBITDA, as defined, to net cash provided by

operating activities as derived directly from the condensed consolidated financial statements

(in millions):

2014 2013

Adjusted EBITDA 485$ 495$

Interest expense, net (224) (156)

Provision for income taxes 57 (49)

Loss from operations of entities sold, net of taxes (2) (2)

Other non-cash expenses, net 17 11

Changes in operating assets and liabilities,

net of effects of acquisitions and divestitures (268) (242)

Net cash provided by operating activities 65$ 57$

Three Months Ended

March 31,

Other Financial Information

Q1 2014 Financial Results – Excluding Adjustments

37

Q1 2014 (1) Q1 2013

Net

Operating

Revenues

Adjusted

EBITDA **

EPS from

Cont.

Ops.

Net

Operating

Revenues

Adjusted

EBITDA **

EPS from

Cont.

Ops.

As Reported $ 4,195 $ 485 $ (1.04) $ 3,274 $ 495 $ 0.86

Discontinued Operations - - 0.19 - - 0.02

Loss on Early Extinguishment of Debt - - 0.42 - - 0.01

Amortization on Software to be Abandoned - - 0.24 - - -

Impairment of Long-Lived Assets - - 0.14 - - -

Subtotal Excluding Discontinued Operations,

Loss on Early Extinguishment of Debt,

Amortization on Software to be Abandoned,

and Impairment of Long-Lived Assets

$ 4,195 $ 485 $ (0.05) $ 3,274 $ 495 $ 0.89

Adjustments

HMA Acquisition and Integration Expenses - 53 0.30 - - -

CVR Legal Expense - 3 0.02 - - -

Subtotal of Above Adjustments - 56 0.32 - - -

Excluding All Adjustments, Discontinued

Operations, Loss on Early Extinguishment of Debt,

Amortization on Software to be Abandoned,

and Impairment of Long-Lived Assets

$ 4,195 $ 541 $ 0.27 $ 3,274 $ 495 $ 0.89

(1) The impact of the weather has not been factored into the calculation of net operating revenue, adjusted EBITDA, and EPS.

** See the Unaudited Supplemental Information contained in this presentation for a definition of EBITDA and a reconciliation of Adjusted EBITDA, as defined, to our net cash provided by

operating activities as derived directly from our consolidated financial statements for the three months ended March 31, 2014 and 2013 (Slides 34 and 35). For purposes of this

presentation, EBITDA means Adjusted EBITDA.