july-2017 employer - employee transactions etc. • company arranges catering services for serving...

TRANSCRIPT

July-2017

Employer - Employee Transactions

The tax position and interpretations contained in this presentation arebased on current law, its understanding and interpretation

ANAR & Co., Its Partners, Affiliates and Team, etc., do not accept anyresponsibility and/or liability arising out of actions / decisions based on thispresentation

The said presentation is mean for circulation to Clients of ANAR & Co. only

Clients are requested to consult giving all necessary information anddocumentation, the aspects covered in the presentation, being generic innature

Supply from Employer to Employee:

Where ‘gift’ up to value of INR 50,000 is provided by employer to employee in a financial year, same would not qualify as ‘supply’. The term ‘gift’ has not been defined in the GST law.

In case there are other supplies made by employer to employee (with or without consideration), the same may qualify as ‘supply’.

Supply from Employee to Employer:

Same would not be treated as supply provided the same is in course of or in relation to the employment.

Since employer and employee have been deemed as ‘related person’ under CGST Act(Section 15) , valuation for supplies which are taxable under GST are to be governed in terms of the Valuation Rules issued for related party transactions (discussed in subsequent slide).

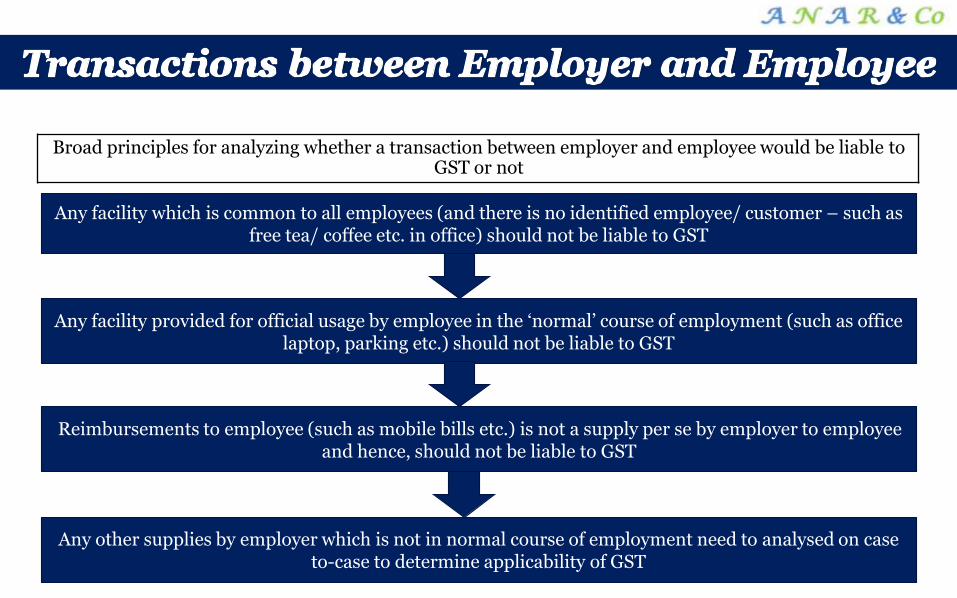

Broad principles for analyzing whether a transaction between employer and employee would be liable to GST or not

Any facility which is common to all employees (and there is no identified employee/ customer – such asfree tea/ coffee etc. in office) should not be liable to GST

Any facility provided for official usage by employee in the ‘normal’ course of employment (such as officelaptop, parking etc.) should not be liable to GST

Reimbursements to employee (such as mobile bills etc.) is not a supply per se by employer to employeeand hence, should not be liable to GST

Any other supplies by employer which is not in normal course of employment need to analysed on case to-case to determine applicability of GST

Specific order to be followed

• Full value in money for supply of goods at the same time of transaction between two unrelated parties where price is sole consideration

Open market value

• Supply of goods under similar circumstances in respect of characteristics ,quality, quantity, functional components, materials and reputation of goods

Value of supply of

goods of like kind

and quality

• 110% of cost of production or manufacture or cost of acquisition of such goods or cost of provision of such services.Cost plus basis

• Reasonable means consistent with the principles and general provisions of Section 15 of CGST Act and the Valuation rulesResidual method

Transactions

Nature of transaction GST Applica

ble

Likely GST implications

Credit availability to Company

Medicalinsurance foremployeesand familymembers

• Company offers medical insurance to its employees and their family members• No charges are recovered on account of medical insurance from employees• This is covered in theemployment manual for the employees which form part of the employment contract

No • No GST liability since there is no underlying supply per se by the company to its employees• In the agreements/contracts with the medical insurer it should be clearlyprovided that company ismerely making payment on behalf of its employees

• Supply is made by insuranceCompany directly to the employee and not to company and hence, no credit availability• Further, taxes paid on expenses incurred in relation to employee health insurance (unless notified as obligatory under any law) are not eligible as credit

Personalaccidentinsurance

• Company offers personal accident insurance to its employees• No charges are recovered onaccount of such insurance from employees

No • No GST liability sincethere is no underlyingsupply per se by Companyto its employees (and thereis no identified employee to whom supply is made)

• Supply is made by insurance Company directly to the employee and not to company and hence, no credit availability• Further, taxes paid on expenses incurred in relation to employee life insurance (unless notified as obligatory under any law) are not eligible as credit

Transactions Nature of transaction

GSTApplicable

Likely GST implications

Credit availability to

Company

Health checkup facility

• Company offers annual health check facility to its employees within office premise

No • No GST liability since there is no underlying supply per se by the Company to its employees (and there is no identified employee towhom supply is made)

• Taxes paid in relation to health services should not be eligible as Credit

Provision ofsubsidized orfree food• All employeeevent• Lunch foremployees –women’s day,Diwali etc.

• Company arrangescatering services forserving food at free of cost to its employees on fruits, women’s day lunch etc.• In certain cases, partial amount may be recovered fromcustomer s and balance payment made by Company

Yes • Company can explore the possibility of structuring the contract with caterer to the effect that the caterer is supplying food directly to the employee (and may also recover subsidized value from the employee) and raises invoice on the Company for recovery of the amount. In such a case, GST liability should ideally not arise on the Company

• Taxes paid on outdoorcatering would beavailable as creditwhere Companydischarges GST onoutward supply to theemployee at openmarket value, otherwisethe same would be acost

Transactions Nature of transaction

GSTApplicable

Likely GST implications

Credit availability to

Company

Health checkup facility

• Company offers annualhealth check facility to its employees within office premise

No • No GST liability since there is no underlying supply per se by the Company1 to its employees (and there is no identified employee towhom supply is made)

• Taxes paid in relation to health services should not be eligible asCredit

Provision ofsubsidized orfree food• All employeeevent• Lunch foremployees –women’s day,Diwali etc.

• Company arrangescatering services forserving food at free of cost to its employeeson fruits, women’s daylunch etc.• In certain cases, partialamount may be recovered from customer s and balancepayment made by Company

Yes • Company can explore the possibility of structuring the contract with caterer to the effect that the caterer is supplying food directly to the employee (and may also recover subsidized value from the employee) and raises invoice on the Company for recovery of the amount. In such a case, GST liability should ideally not arise onthe Company

• Taxes paid on outdoorcatering would be available as creditWhere Companydischarges GST on outward supply to theemployee at open market value, otherwisethe same would be aCost

Transactions Nature oftransaction

GST Applicable

Likely GST implications Credit availability toCompany

Free cabor subsidizedfacility• Car facility-Pick up and Drop from home to Office

• CompanyProvides cab facility at free of cost to itsEmployees

In case not covered in employment contract• GST liability to arise since the transaction would be treated as supply by employer to employee. Being a related party transaction (and employee not eligible to claim input tax credit), GST would need to be paid as per the open market value (which may be considered as the amount paid by Company to transporter)

• Taxes paid on cab expenses would be available as credit where company discharges GST on outward supply tothe employee at open market value, otherwise the same would be a cost

Transactions

Nature oftransactio

n

GST Applicabl

e

Likely GST implications Credit availability toCompany

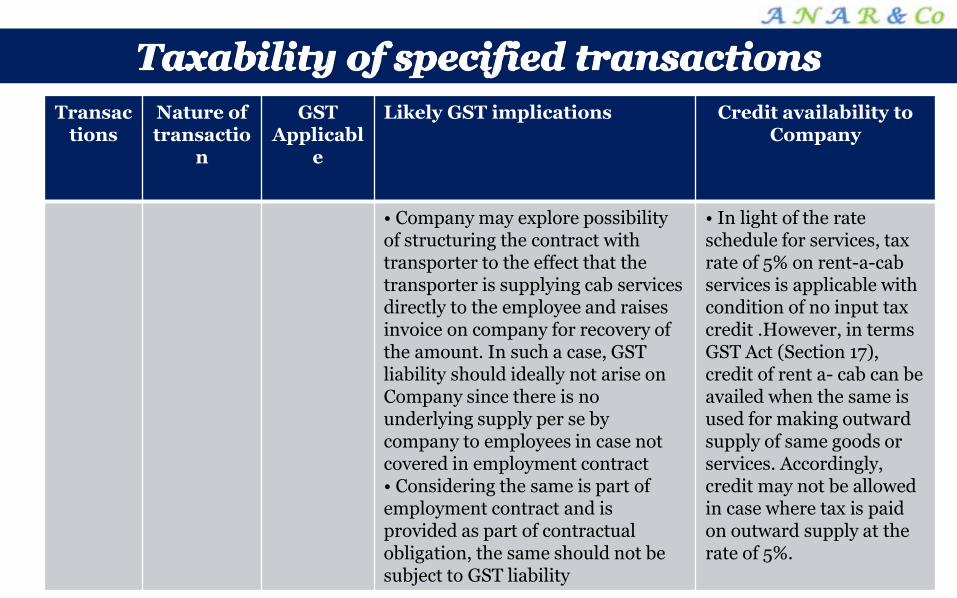

• Company may explore possibility of structuring the contract with transporter to the effect that the transporter is supplying cab services directly to the employee and raises invoice on company for recovery of the amount. In such a case, GST liability should ideally not arise on Company since there is no underlying supply per se by company to employees in case not covered in employment contract• Considering the same is part of employment contract and is provided as part of contractual obligation, the same should not be subject to GST liability

• In light of the rate schedule for services, tax rate of 5% on rent-a-cab services is applicable with condition of no input tax credit .However, in terms GST Act (Section 17), credit of rent a- cab can be availed when the same is used for making outward supply of same goods or services. Accordingly, credit may not be allowed in case where tax is paid on outward supply at the rate of 5%.

Transactions Nature of transaction

GSTApplicable

Likely GST implications

Credit availability to Company

Mobilehandsetsgiven toemployees

• Company provides mobile handsets to itsemployees for official Purposes

No • No GST liability since such benefits are extended by Company to employee for official use/ purposes

• Taxes paid on procurement of mobile handsets would be available as credit since such goods are used in course or furtherance of business

Mobilephoneentitlements

• Specified employees are eligible to claimreimbursement ofmobile phone bills(basis eligibility criteria)

No • No GST liability on reimbursements made to employee since there is nounderlying supply per se by Company to its employees

• Not applicable since invoice would not be in name of Company –Process may be defined by the company for claiming credit in case of Reimbursements

Transactions

Nature of transaction

GST Applicab

le

Likely GST implications

Credit availability to Company

Relocationbenefits

• In case of any employee relocation, company reimburses travel related expenses and also incur certain expenses in relation to transportation ofhousehold goods of

employee, etc.

No • No GST liability since such benefits are extended by Company to employee for official use/ purposes

• Taxes paid on travel/transportation expenses (other than those which are specifically not allowed) likely to be available as credit since such services are used in course or furtherance of business - Process may be defined by the Company for claiming credit in case of Reimbursements

TemporaryAccommodation for first few weeks ofJoining

• Company providestemporary accommodation to itsemployees in the firstfew weeks of joining

No • No GST liability since such benefitsare extended by company to employee for official use/ purposes

• No input tax credit will be available as used by the employee for personal consumption

Transactions Nature of transaction

GST Applicabl

e

Likely GST implications Credit availability

toCompany

Recovery onaccount ofloss of IDcards/ otherAssets

• Company recoverscharges from employees through payroll deduction in case of loss of any asset (such as ID cards, laptops etc.) by the employee

No • Such recovery may be treated as recovery of ‘liquidated damages’ and hence, should not qualify as supply liable to GST

• Not applicable

Sale of usedlaptops(capitalized inthe books)

• Used laptops are given by Company to employees on FoCbasis or at subsidized value

Yes • Such transaction to be treated as supply and accordingly, liable to GST• Open market value (being a capital goods/ asset) would be treated as the higher of amount of credit availed (as reduced by 5% per quarter from the date of underlying input invoice) or the tax on transaction (sale) value

• Not applicable

Transactions Nature oftransaction

GSTApplicab

le

Likely GST implications Credit availability to

Company

Gifts toemployees- Diwali orother occasion(such asfarewell)- T-shirts,stationery,miniatures,etc

• Gifts such as T-shirts, stationery, momento, car models,trophies,etcare distributed toEmployees on Diwali, farewell or other Occasions

Yes • GST payable in case value of gifts provided to an employee during a FY exceeds INR 50,000 – Open market value to apply. Tax to be paid where total value exceeds INR 50,000• For instance: 1) In case individual gifts given during a FY exceeds INR 50,000 (sayINR55,000), GST to be paidon INR 5,000. 2) In case single gift exceeding INR 50,000 (say INR 55,000) given to employee, GST should be applicable on full INR 55,000• Company to track gifts given to individuals during FY to calculate applicable GST Liability

• Requirement of reversal of input credit, if availedbecause of specific exclusion

Transactions

Nature of transaction GSTApplic

able

Likely GST implications Credit availability to

Company

Company car given toemployees

• Company provides car to its employees for both personal and official purpose (remains as asset in books)

No • No GST liability on car provided to employee, as it is made in the course of employment (part of employment contract). Hence, there is no underlying supply per se by Company

• No credit should be available of the GST paid

Car leasescheme

• Car obtained on financial lease by the Company fromdealer and given to employees for official use. Car is recorded as an asset in Company's books• Amount equivalent to car entitlement is reduced from the basic salary of the employee. Notional amount is added as perquisite in employees' CTC

No • No GST liability since such benefits are extended by company to employee for official use/ purposes (the underlyingemployment contract should also substantiate the same)

• Since the Company has purchased the car, in light of specific restriction on credit eligibility for motor vehicles, tax paid on procurement of motor vehicle should not be eligible as credit to company

Transactions Nature of transaction

GSTApplicab

-le

Likely GST implications Credit availabilityto Company

Employeereferral policy

• Cash allowance to be given for successful reference.TDS is deducted

No • No GST liability sinceconsideration (viz. referral bonus) paid by Company is towards services provided by employee in the normal course of employment (on which applicable Income tax is also deducted at the time of payout)

• Not applicable

Notice payrecovery

• Company recovers notice pay charges through payrolldeduction in case of early relieving of the employees

Debatable

Matter

• Notice pay recovery is an issue under current Service tax regime and may continue to remain an issue under GST regime• However, considering that the same appears from contractual obligation, a position may be taken that no GST should be charged on the same• Company needs to appropriately word the same in employment manual

• Not applicable

Transactions Nature of transaction

GSTApplicable

Likely GST implications Creditavailability to

Company

Long ServiceAwards

• On Completion ofspecified years-gifts ormoney in payroll isgiven to employees byCompany. TDS borneby employer

No • No GST liability since such benefits are extended by Company to employee forofficial use/ purposes• Further, income tax is also borne by the employee on such expenses

• Not applicable

House lease • Company offers houselease facility to specified employees. Company pays rent, security deposit,brokerage, etc. to thelandlord and recoversrent paid from employees through payroll deduction

No • Not applicable since rental of residential property is exempt from GST.

• Not applicablesince rental ofresidential property is exempt fromGST

Transactions Nature of transaction

GSTApplicable

Likely GST implications

Credit availability toCompany

Employeewelfare schemes (such as off-site /town hall, etc)

• Company allocatescertain amount for each employee in relation to recreational activities (such as offsite, town hall, etc)

No • No GST liability since there is no underlying supply per se by company to its employees

• Taxes paid on procurement of goods/ services in relation to town hall/ offsite activities should be available as credit to Company provided goods/ service are not specifically restricted(e.g. food and beverages)

Free use ofcompany ownproductsincludinguniform,shoes, etcprovided forfree of costbasis

• We understand that this is covered in the employment manual for the employees as well

No • No GST liability since such benefits are extended bycompany to employees for official use/ purposes

• Taxes paid on procurement of uniforms should be available as credit since they are used in course or furtherance of business and not used by employees for personal consumption

Transactions

Nature of transaction GSTApplicable

Likely GST implications

Credit availability to

Company

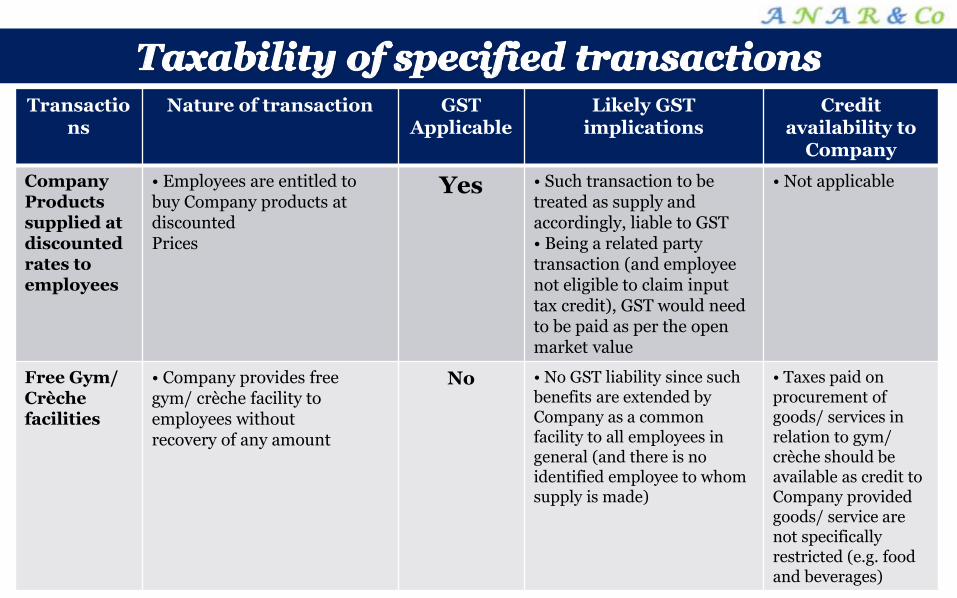

CompanyProducts supplied at discounted rates toemployees

• Employees are entitled to buy Company products at discountedPrices

Yes • Such transaction to be treated as supply and accordingly, liable to GST• Being a related party transaction (and employee not eligible to claim input tax credit), GST would need to be paid as per the open market value

• Not applicable

Free Gym/Crèchefacilities

• Company provides freegym/ crèche facility toemployees withoutrecovery of any amount

No • No GST liability since such benefits are extended by Company as a common facility to all employees in general (and there is no identified employee to whom supply is made)

• Taxes paid on procurement of goods/ services in relation to gym/ crèche should beavailable as credit toCompany provided goods/ service are not specifically restricted (e.g. food and beverages)

Transactions Nature of transaction

GSTApplicable

Likely GST implications

Credit availability to

Company

Leave Support • Employees are eligible for of earned leave, sick leave and casual leave

No • No GST liability since there is no underlying supply per se by company to its employees

• Not applicable

Supporttowardscorporateeducation

• Employees are eligible to claim reimbursementup to a certain amount for pursuing corporateeducation

No • No GST liability onreimbursements made to employee since there is nounderlying supply per se by company to its employees

• Not applicable

Various expenses are claimed by employees such as:• Travel expenses• Telephone expenses• Hotel expenses

• For Company to avail credit, invoices issued by vendor for travel, telephone or hotel expenses etc., should provide correct GSTIN of Company• Employees should be instructed to provide Company’s GSTIN to vendors• Vendor to issue invoice in the name of Company• Necessary modifications to be made in system to ensure employees : Enter necessary information (such as invoice number, invoice date, GSTIN of vendor, taxable value, tax amount etc.) at the time of claiming expense reimbursements Same should be verified at the time of processing of claims