july 2013 final draft - city of greater bendigo · ref: m13038 final draft p a g e 1 | 74 hill pda...

TRANSCRIPT

Ref: M13038 FINAL DRAFT P a g e 1 | 74 Hill PDA

Hill PDA

Bendigo Hospital Precinct Structure Plan

Technical Assessment:

Economics and Land Use

PREPARED FOR

City of Greater Bendigo

July 2013

FINAL DRAFT

Hill PDA

ABN 52 003 963 755

Sydney

3rd

Floor 234 George Street Sydney

GPO Box 2748 Sydney NSW 2001

t. +61 2 9252 8777

f. +61 2 9252 6077

Melbourne

Level 9, 365 Little Collins St Melbourne

GPO Box 3424 Melbourne VIC 3001

t. +61 3 9642 2449

f. +61 3 9642 2459

www.hillpda.com

Liability limited by a scheme approved under the Professional Standards Legislation

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 3 | 74 Hill PDA

QUALITY ASSURANCE REPORT CONTACTS:

FERGUS STEWART

B. Urban Planning & Development (MELB)

Senior Consultant, Planning & Property Economics

BEN PEACH

B. Applied Science & Valuation (Hons) (RMIT) PMA PI

Consultant, Property Economics

[email protected] QUALITY CONTROL: This document is for discussion purposes only unless signed and dated by a Principal of Hill PDA. DRAFT Dated

VICTORIA TOMPSETT

B. Land Econ./B. Arts International Studies

Principal, Property Economics

REPORT DETAILS: Job Ref No: M13038 Version: FINAL DRAFT Date Printed: 3/07/2013 File Name: M13038 - Bendigo PSP - Hill PDA Technical Assessment FINAL DRAFT 260613

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 4 | 74 Hill PDA

CONTENTS

1. INTRODUCTION ............................................................................................................................................ 7

1.1 Project Brief ................................................................................................................................... 7

1.1 Background Documentation and Consultation .............................................................................. 7

2. PROJECT STUDY AREA ............................................................................................................................... 9

2.1 Bendigo Hospital Precinct ............................................................................................................. 9

2.2 Surrounding Land Uses ............................................................................................................... 14

3. CITY OF BENDIGO ECONOMIC CONTEXT ..................................................................................................... 20

3.1 Key Industry Sectors in Bendigo ................................................................................................. 20

3.2 Key Institutions and Businesses in Bendigo ................................................................................ 21

3.3 Tourism in Bendigo...................................................................................................................... 22

3.4 Significant Projects ...................................................................................................................... 22

4. SOCIO-ECONOMIC AND INDUSTRY PROFILING ............................................................................................. 23

4.2 Age Distribution and Population Growth ...................................................................................... 24

4.3 Household and Dwelling Characteristics ..................................................................................... 26

4.4 Employment and Workforce Profile ............................................................................................. 28

5. RESIDENTIAL AND ACCOMMODATION MARKET ........................................................................................... 31

5.1 Residential Dwelling Development Trends .................................................................................. 31

5.2 Student Housing Development Trends ........................................................................................ 39

5.3 Short-Term Accommodation Development Trends ..................................................................... 41

5.4 Implications ................................................................................................................................. 43

6. RETAIL AND COMMERCIAL MARKET ............................................................................................................ 46

6.1 Retail and Commercial Development Trends .............................................................................. 46

6.2 Retail Market ............................................................................................................................... 50

6.3 Commercial Market ..................................................................................................................... 63

6.4 Implications ................................................................................................................................. 66

7. IMPLICATIONS FOR THE STUDY AREA ......................................................................................................... 67

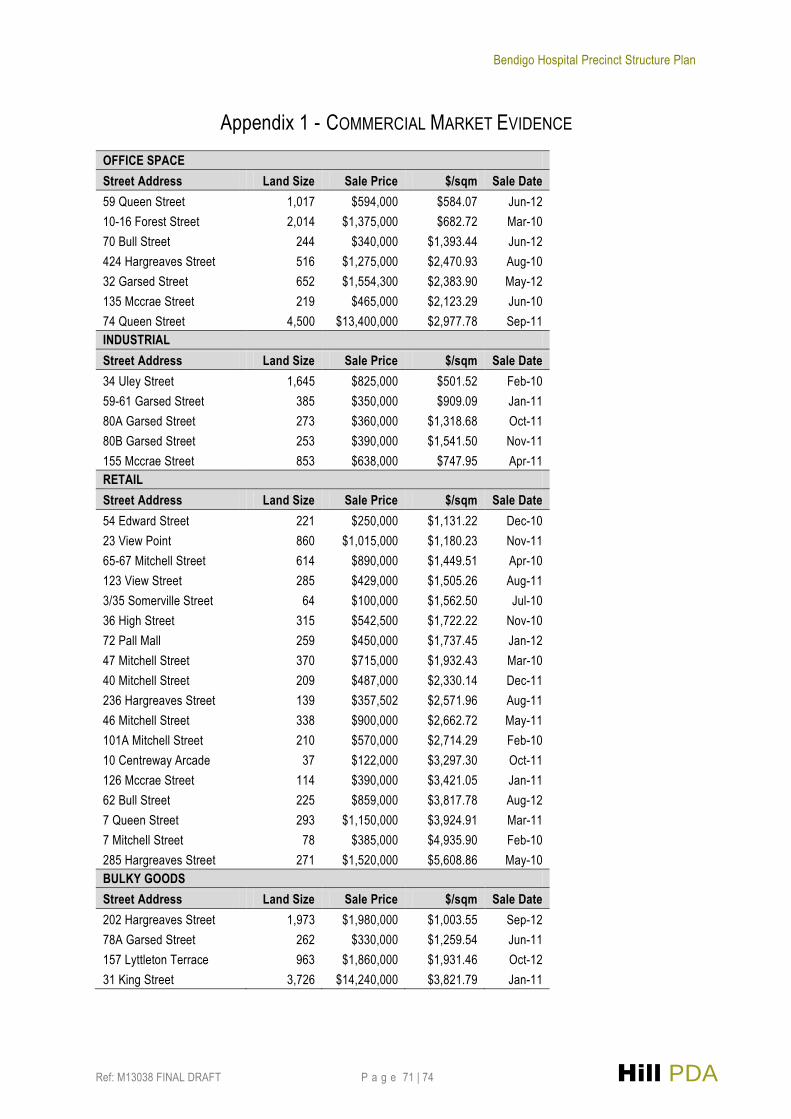

Appendix 1 - Commercial Market Evidence

Appendix 2 - Residential Market Evidence

LIST OF FIGURES

Figure 1 - Bendigo Hospital Precinct Map ......................................................................................................... 11

Figure 2 - Major Tenants in the Study Area ....................................................................................................... 15

Figure 3 - Bendigo Hospital Precinct Structure Plan Study Area Map ................................................................ 17

Figure 4 - Bendigo Hospital Precinct Structure Plan Land Use Map .................................................................. 18

Figure 5 - Bendigo Precinct Structure Plan Existing Zoning Map ....................................................................... 19

Figure 6 - Central SLA Context ......................................................................................................................... 23

Figure 7 - Median Age (2001-2011) .................................................................................................................. 24

Figure 8 - Distribution of Population by Age Cohort in the Central SLA (2001 to 2031) ..................................... 26

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 5 | 74 Hill PDA

Figure 9 - Median Weekly Household Income (2001 to 2011) ........................................................................... 28

Figure 10 - Residential Building Approvals by Dwelling Type (1996-2012) ........................................................ 31

Figure 11 - Average Residential Lots Constructed by Small Area Per Annum (2006-2012) ............................... 32

Figure 12 - Bendigo Core Development Areas .................................................................................................. 33

Figure 13 - Recent Townhouse Development in the Study Area ....................................................................... 34

Figure 14 - Vacant and Subdivided Lots in the Study Area ................................................................................ 35

Figure 15 - Sample of Newly Developed Townhouses and Villas in Bendigo (April 2013) ................................. 37

Figure 16 - Average Forecast Dwelling Growth and Change by Period (2011-2031) ......................................... 39

Figure 17 - Location of Accommodation Providers in Bendigo (2013) ............................................................... 41

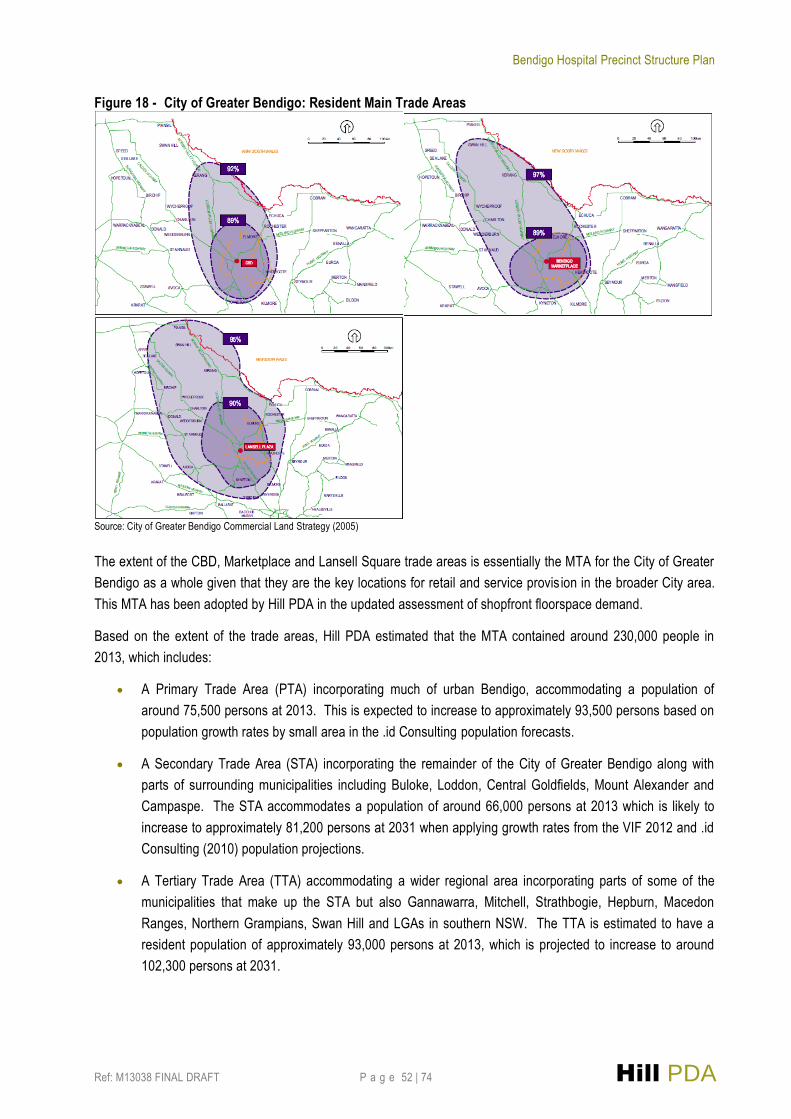

Figure 18 - City of Greater Bendigo: Resident Main Trade Areas ...................................................................... 52

Figure 19 - Examples of Bendigo Retail and Bulky Goods Sales Transactions .................................................. 63

Figure 20 - 74 Queen Street, Bendigo ............................................................................................................... 64

Figure 21 - Examples of Bendigo Office Space Sales Transactions .................................................................. 64

LIST OF TABLES

Table 1 - Study Area Population and Age Distribution ......................................................................................... 9

Table 2 - Key Economic Drivers and Significant Local Industries in the City of Greater Bendigo (2012) ............ 20

Table 3 - Estimated Resident Population Change by Area (2001-2011) ............................................................ 24

Table 4 - Estimated Resident Population in the Central SLA (2001 to 2031) ..................................................... 25

Table 5 - Dwelling Change by Area (2001-2011) ............................................................................................... 26

Table 6 - Family and Dwelling Type and Household Structure (2001-2011) ...................................................... 27

Table 7 - Central SLA Industry of Employment (2001-2011) ............................................................................. 29

Table 8 - City of Greater Bendigo: Health Care & Social Assistance Workers (2011) ........................................ 30

Table 9 - City of Greater Bendigo Residential Development Pipeline in Inner Bendigo (2013) .......................... 36

Table 10 - City of Greater Bendigo Comparison of Median House and Unit Values (2009-2013)....................... 36

Table 11 - City of Greater Bendigo Residential Rental Comparison (September Qtr 2013) ............................... 38

Table 12 - Forecast Residential Dwelling Change to 2031 ................................................................................ 38

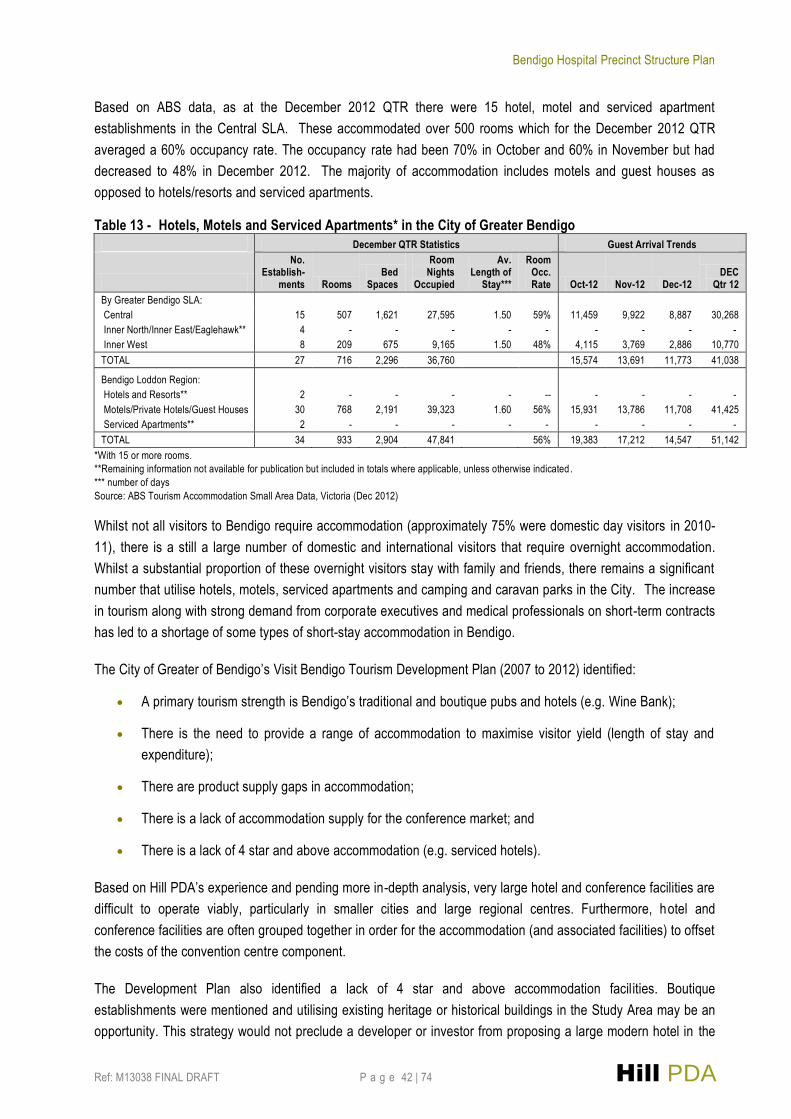

Table 13 - Hotels, Motels and Serviced Apartments* in the City of Greater Bendigo ......................................... 42

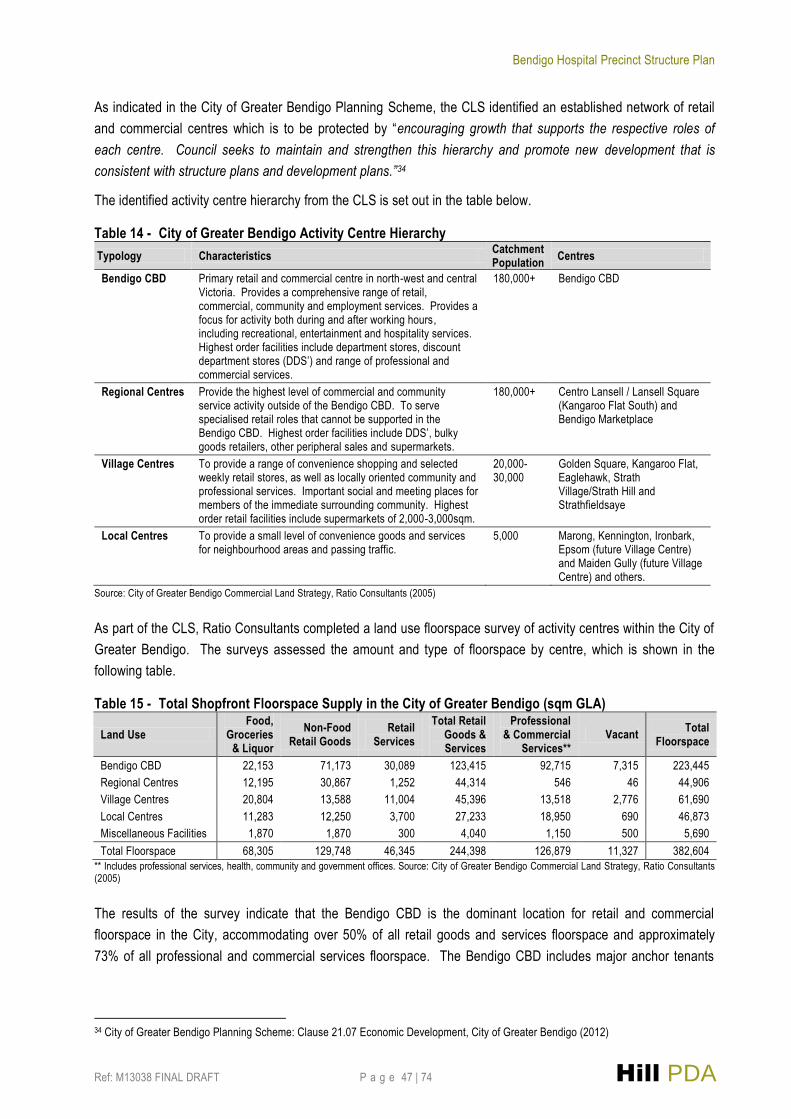

Table 14 - City of Greater Bendigo Activity Centre Hierarchy ............................................................................ 47

Table 15 - Total Shopfront Floorspace Supply in the City of Greater Bendigo (sqm GLA) ................................. 47

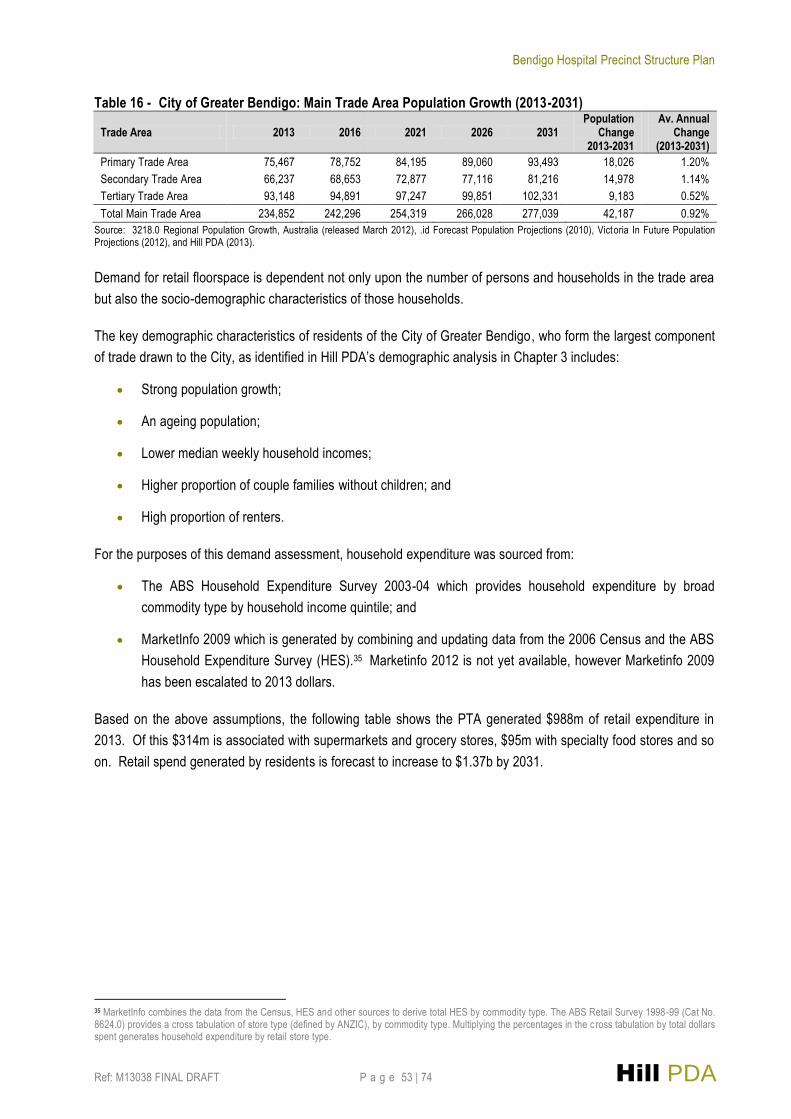

Table 16 - City of Greater Bendigo: Main Trade Area Population Growth (2013-2031) ...................................... 53

Table 17 - City of Greater Bendigo Primary Trade Area Resident Expenditure to 2031 ($m) ............................. 54

Table 18 - City of Greater Bendigo Secondary Trade Area Resident Expenditure to 2031 ($m) ........................ 54

Table 19 - Retail Spend Per Capita Comparison (2013) .................................................................................... 54

Table 20 - City of Greater Bendigo Tertiary Trade Area Resident Expenditure to 2031 ($m) ............................. 55

Table 21 - City of Greater Bendigo Assumed Capture Rates (2013-2031) ........................................................ 56

Table 22 - Capture of MTA Resident Retail Spend by the City of Greater Bendigo to 2031 ($m) ....................... 56

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 6 | 74 Hill PDA

Table 23 - Bendigo Loddon Region Tourism and Visitor Data* (2011) ............................................................... 57

Table 24 - Bendigo Loddon Region Tourism Expenditure by Type (2010/11) .................................................... 57

Table 25 - Bendigo Loddon Tourism Expenditure in 2013 ($m) ......................................................................... 58

Table 26 - Capture of Tourism Retail Spend by the City of Greater Bendigo to 2031 ($m) ................................ 58

Table 27 - Total Forecast Retail Expenditure in the City of Greater Bendigo to 2031 ($m) ................................ 59

Table 28 - Demand for Retail Floorspace in the City of Greater Bendigo to 2031 (sqm GLA) ............................ 59

Table 29 - Distribution of Floorspace Demand in the City of Greater Bendigo to 2004-2021 (sqm GLA)............ 61

Table 30 - Distribution of Floorspace Demand in the City of Greater Bendigo to 2031 (sqm GLA) .................... 61

Table 31 - Issues and Opportunities for the Study Area .................................................................................... 67

LIST OF ABBREVIATIONS Australian Bureau of Statistics ABS

Australian and New Zealand Standard Industrial Classification ANZSIC

Business 4 Zone B4Z

Commercial Land Strategy CLS

Community Focussed Development CFD

Department of Planning & Community Development DPCD

Discount Department Store DDS

Estimated Resident Population ERP

General Residential Zone GRZ

Global Financial Crisis GFC

Gross Domestic Product GDP

Gross Regional Product GRP

Gross Floor Area GFA

Gross Lettable Area GLA

Local Government Area LGA

Local Planning Policy Framework LPPF

Main Trade Area MTA

Municipal Strategic Statement MSS

Neighbourhood Residential Zone NRZ

Primary Trade Area PTA

Secondary Trade Area STA

Research and Development R&D

Residential 1 Zone R1Z

Residential Growth Zone RGZ

Residential Development Strategy RDS

State Planning Policy Framework SPPF

Statistical Local Area SLA

Tourism Research Australia TRA

Victoria in Future VIF

Visitor Profile & Satisfaction Project VPS

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 7 | 74 Hill PDA

1. INTRODUCTION

1.1 PROJECT BRIEF

Bendigo Hospital is currently undergoing an estimated $650m redevelopment which will see it become the largest

Hospital in regional Victoria. The redevelopment represents the greatest investment in regional health

infrastructure in Victoria’s history and will be a catalyst for a range of economic and business development

opportunities in the areas surrounding the Hospital. The scale of development is also expected to stimulate non -

health related sectors including education, business and residential development within the City of Greater

Bendigo and broader region.

Such growth requires careful management and in order to fully understand these impacts, a Bendigo Hospital

Precinct Structure Plan is being prepared. As part of the Structure Plan process, Hill PDA provides this Technical

Assessment of economic and land use conditions in the Study Area and other areas around the Hospital including

the CBD, central Bendigo and the broader City. Locations beyond the Study Area are analysed to provide a

better understanding of broader economic and land use issues and opportunities that have an influence on the

Study Area itself.

The Technical Assessment informs the future uses and opportunities for residential development, short -term

accommodation, retail, commercial, and other uses in the Study Area.

1.1 BACKGROUND DOCUMENTATION AND CONSULTATION

The following documents were reviewed as background to the Technical Assessment:

Bendigo Health Annual Report (2012)

Bendigo Health Report of Operations (2011)

Report on the Geographical Distribution of Patients who attend Bendigo Health (2011/12)

City of Greater Bendigo Commercial Land Strategy, Ratio Consultants (2005)

Bendigo Residential Development Strategy, Parsons Brinckerhoff (2004)

Bendigo Residential Development Strategy Review: Audit Report, City of Greater Bendigo (2011)

Bendigo Residential Development Strategy Review: Issues and Opportunities Paper (2013)

Bendigo Residential Development Strategy Review: Land Supply and Assessment (2013)

Visit Bendigo Tourism Development Plan (2007 to 2012)

Loddon Mallee South Regional Growth Plan, DPCD (2013)

Bendigo CBD Plan, Planisphere and the City of Greater Bendigo (2005)

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 8 | 74 Hill PDA

Greater Bendigo Economic Development Strategy: Volume 3 Background Material, SGS Economics &

Planning (2008)

Greater Bendigo Economic Development Strategy, SGS Economics & Planning (2008)

Regional Tourism Profile for Bendigo Loddon 2010/2011, Tourism Research Australia (2011)

Bendigo Visitor Profile and Tourism Survey, Tourism Research Australia (2011)

The following individuals were consulted as part of the research process which informed this Assessment.

Bendigo Health, Robyn Lindsay, consultation sessions (April 2013)

Bendigo Health, David Walker, consultation sessions (April 2013)

Doug Lougoon Real Estate, Doug Lougoon, phone interview (April 2013)

Professionals Real Estate Bendigo, Danny Clarke, phone interview (April 2013)

Luke Goggin Real Estate Bendigo, Paul Dalton, phone interview (April 2013)

Tweed Sutherland First National Bendigo, Tom Harrop, phone interview (April 2013)

Colliers International Ballarat, Travis Hurst, phone interview (April 2013)

Apelbaum Healthcare Real Estate, Phillip Apelbaum, phone interview (May 2013)

In order to inform the preparation of the Structure Plan, five workshops were undertaken with the community and

key stakeholders, with each focusing on broad topics such as transport, infrastructure, economics, planning,

urban design and health. The following groups attended the health and economics workshops which were

attended by Hill PDA:

Various Bendigo local residents, business operators and land owners;

Bendigo Health;

Bendigo Business Council;

Bendigo Holiday Accommodation;

Bendigo Chinese Association;

Centrum Town Planning;

City of Greater Bendigo Council staff;

Regional Development Victoria (Loddon Mallee); and

Bendigo Senior Secondary College.

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 9 | 74 Hill PDA

2. PROJECT STUDY AREA The Study Area for the Bendigo Hospital Precinct Structure Plan includes not only the Bendigo Hospital Precinct,

but also land on the periphery, of up to and sometimes more than a radius of 800m. The focus of the Structure

Plan is to understand the influence of the Hospital on redevelopment in the Study Area and therefore it is relevant

to understand the residential areas, institutional uses and retail and commercial land within this peripheral area.

At 2011, the Study Area accommodated an Estimated Resident Population (ERP) of 1,510 persons. The

distribution of population by age group is identified in the table below.

Table 1 - Study Area Population and Age Distribution

Age Cohort 2011

Population %

0-14 211 14.0

15-29 349 23.1

30-44 280 18.5

45-59 318 21.0

60-74 205 13.6

75+ 147 9.8

Total 1,509 100.0

Source: ABS Community Profiles

In 2011, the resident population was accommodated in approximately 600 occupied private dwellings, equivalent

to an average of 2.5 persons per dwelling. The vast majority of dwellings (approximately 79%) were separate

detached dwellings. The remainder of dwellings in the Study Area were either flat-unit-apartments or other

dwellings.

Just under half of all residents in the Study Area were employed at 2011 (approximately 710 residents). Of these

resident workers, around 155 (close to 22%) were employed in health care and social assistance, with the vast

majority of these likely to be employed within the Hospital Precinct. Other significant employing industries for

working residents in the Study Area included retail trade (84 resident workers or 11.8%) and education and

training (84 resident workers or 11.8%), which are both unsurprising given the proximity of the Bendigo CBD and

educational facilities present in the Study Area.

2.1 BENDIGO HOSPITAL PRECINCT

Bendigo Health is a 6781 bed service that includes a 60-bed rehabilitation unit, eight bed critical care unit and five

operating theatres where around 10,000 surgical procedures are performed annually2. Bendigo Health also

manages 5 residential care homes elsewhere off campus offer permanent and respite nursing home and hostel

care including Carshalton House, Golden Oaks Nursing Home, Joan Pinder Nursing Home, Simpkin House and

Stella Anderson Nursing Home.

1 Note: The 653 beds include the 60 bed rehabilitation unit and intensive care unit beds.

2 www.bendigohealth.com.au (2013)

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 10 | 74 Hill PDA

Bendigo Health is a significant provider of health services across the Loddon-Mallee Region. The main campus is

the Bendigo Hospital Precinct, with many services extended to regional areas including Mildura, Echuca, Swan

Hill, Kyneton and Castlemaine. In 2011/12 there were 35,497 discharges of patients of which 74% (26,276) were

patients who resided in the City of Greater Bendigo. Of the remaining 26% (9,221), 92.5% (8,535) were from other

parts of Victoria, 6.1% (562) were from NSW with the balance of patients from other states3.

Based on the 2012 Bendigo Health Annual Report:

In 2011 Bendigo Health employed 2,205 full-time equivalent staff, which increased to 2,254 staff in 2012.

In 2012 the majority of staff were in nursing services (45%), followed by administration and clerical

services (16.7%), ancillary support (9.8%) and medical support services (8.7%).

Bendigo Health currently employs almost 300 volunteers, in 32 areas. Volunteers give their time to

patients, residents and visitors in a range of settings including Child and Adolescent Unit, Day Procedure

Unit, Palliative Care, Emergency Department and our five residential aged care facilities.

In 2011 Bendigo Health hosted 26,199 student placement days and supported 11 educational partners.

Subsidised accommodation is provided for medical staff and some students, which includes meals and

entertainment benefits.

In 2011/2012 Bendigo Health secured Health Workforce Australia cl inical training funding which will allow

Bendigo Health to support additional staff, refurbishment of student learning areas and office spaces

together with purchasing additional equipment to support students undertaking clinical placement at

Bendigo Health.

In terms of staff characteristics, Bendigo Health has indicated4:

Where staff reside – the majority of staff live in the City of Greater Bendigo including the suburbs of

Bendigo (18% or 650 staff, also the largest representation), Golden Square (6.3% or 218), Eaglehawk

(6% or 208), Kangaroo Flat (5.7% or 198), Strathfieldsaye (5.1% or 176). Smaller proportions of staff do

travel from further afield including Castlemaine/Harcourt/Campbells Court (2.7% or 95), Echuca (0.7% or

24), and Mildura (0.4% or 14). A very small proportion reside in Melbourne metropolitan suburbs such as

Parkville, Richmond, Fitzroy, Hoppers Crossing, Melbourne, Brunswick East, Box Hill and Balwyn.

Mode of transport of staff - no formal study has been completed however anecdotally it is understood

existing staff travel to work by car, bike, walk and a minor proportion arrive by bus. Some catch the train

to Bendigo station and then either walk or take a taxi to the Hospital Precinct

Most common shift hours - most common shift hours are 7am to 3.30pm and 1.30pm to 10pm. Monday

to Friday is busier as there are large numbers of support staff on site.

Residential accommodation for visiting medical staff – subsidised accommodation is provided for visiting

medical staff dependent on salary packages and often includes meal and entertainment allowances. If

accommodation is not available on site, Bendigo Health has provided rooms in rented private dwellings

surrounding the Hospital Precinct.

3 Report on the Geographical Distribution of Patients who attend Bendigo Health (2011/12)

4 Robyn Lindsay, Bendigo Health (May 2013)

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 11 | 74 Hill PDA

Residential accommodation for medical students - subsidised accommodation for students is provided

dependent on the individual agreement Bendigo Health has with education providers.

The following information from the 2011 Bendigo Health Quality of Care Report indicates the extent of the

catchment of Bendigo Health services. In 20115:

58,797 occasions of service were provided by the outpatients clinic (acute and allied health);

45,368 people went through the Emergency Department for treatment;

37,709 people were admitted to the hospital;

9,975 operations were performed;

9,639 ambulance arrivals were handled by the Emergency Department;

1,938 admissions of children under age 19 to the Child and Adolescent Unit; and

1,169 babies were delivered.

The Hospital Precinct itself is located approximately 1km north of Bendigo CBD and comprises the Bendigo

Hospital and the Anne Caudle Centre. The St John of God Private Hospital is located at the corner of Lily and

Chum Street 2.5km west of the Bendigo Hospital Precinct. Bendigo Hospital and associated facilities provide a

range of medical and health related services including (but not limited to) emergency, women’s health, medical

imaging, pathology, rehabilitation, cardiology and renal dialysis.

Figure 1 - Bendigo Hospital Precinct Map

Source: Bendigo Health (2013)

5 Bendigo Health Quality of Care Report (2011)

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 12 | 74 Hill PDA

Outside of health services the Hospital Precinct accommodates a coffee shop, kiosk, gift shop (flowers, gifts and

personal items including toiletry packs), ATM, pastrol care and two chapels.

The health education precinct between Mercy and Arnold streets within the Hospital Precinct broadens the overall

health education role and function of the Hospital and accommodates the Monash University Bendigo Regional

Clinical School, the Bendigo Primary Care Centre and the new La Trobe University School of Rural Health . The

addition of these education facilities assists the Hospital in creating their own health workforce for the future. It is

anticipated that in doing so, the Hospital will not have to rely on the metropolitan clinical schools as has been the

case in the past6. In particular recent health education projects have included7:

The new Monash University facilities which opened in 2010 and were designed to draw students,

practitioners, clinical teaching staff and other institutions into much closer collaboration.

A Dental Training Clinic on the Anne Caudle Centre campus was opened in April 2010. The expansion

significantly increases the access of La Trobe dental and oral health students to the latest technology in

dental education.

La Trobe’s new Physiotherapy Clinical School, located on the Anne Caudle Centre campus, opened in

July 2010. Having this facility based at Bendigo Health enables students to have access to

physiotherapists and work in a variety of practice areas in rehabilitation and acute care.

The new La Trobe Rural Health School was opened in March 2013 and will offer an extra 750 student

places, and train an additional 200 graduates each year to tackle critical health care worker shortages.

The vision for the new school is to provide theoretical and clinical learning to students in the disciplines of

nursing and midwifery, dentistry, oral health, human biosciences, physiotherapy, occupational therapy,

podiatry, speech pathology, paramedic practice, health sciences and social work.

Other recent developments completed within the Hospital Precinct have included8:

The coffee shop on the hospital campus has been refurbished.

The re-development of the Emergency Department which officially opened in October 2010. It features

an increase in treatment spaces, a new short stay unit and a dedicated fast-track area, so patients with

less serious illnesses and injuries can receive quicker assessments and treatment.

Relocation of Ambulance Victoria services from Arnold Street to strategic locations in the Bendigo area

as part of the enabling works for the new Hospital. Stations were constructed at Epsom, Eaglehawk and

North Bendigo, the Bendigo CBD and Strathdale facilities nearing completion.

A temporary energy centre was built on the Barnard Street site near the front gate as part of the enabling

works for the new Hospital. For the first time in 60 years, all buildings are being fed from the front of the

site. This project delivers the site’s main electrical switchboard, generator enclosure, generator fuel tank

and boiler house.

6 Bendigo Health Quality of Care Report (2011)

7 Bendigo Health Quality of Care Report (2011)

8 Bendigo Health Annual Report (2012) and Bendigo Health Report of Operations (2011 )

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 13 | 74 Hill PDA

Demolition of existing buildings on the Barnard Street site as enabling works for the new Hospital.

In April 2013 the Exemplar consortium (Lend Lease, Capella, Spotless Services, Bates Smart and Silver Thomas

Hanley) was announced as the preferred bidder for the new Bendigo Hospital project. The new Bendigo Hospital

redevelopment will significantly expand the existing services offered at the Hospital Precinct. The redevelopment

will not only expand the existing facility but will also lead to a greater number of people working in, travelling

through and staying in the Study Area.

The redeveloped Hospital will provide9:

A new hospital built on one site at Barnard Street;

372 new beds and 10 new operating theatres;

An integrated cancer centre and mental health unit; and

A helipad to be built on top of a new multi-story car park on the Lucan Street site. A bridge link will

connect the car park to the main hospital site, making it easy for patients and visitors to get to the

hospital and other amenities.

Over and above health services, the redeveloped Hospital Precinct is also anticipated to include10:

A childcare and wellness centre;

128 serviced apartments and 15 apartments for short stay accommodation;

New kitchen, supply and linen handling facility within the new hospital;

180 seat conference facility;

A large atrium as the entrance with retail, cafes and multiple internal courtyards;

Enhanced landscaping across the entire hospital precinct;

Refurbishment and re-use of some heritage buildings; and

The latest integrated technology nurse call system.

The redeveloped Hospital will also accommodate approximately 1,800sqm of retail which will include cafes, a

florist, chemist, newsagents and a convenience store (less than 500sqm).

The redeveloped Hospital will also expand the capacity for daily and overnight treatment. It is expected that with

expanded capacity the number of annual patients will increase gradually over the coming years.

Construction of the new Hospital is anticipated to be complete in 2016 and will generate more than 770

construction industry and supply chain jobs, with at least 300 jobs maintained for a minimum of three years during

the peak construction period for the Hospital11.

9 www.newbendigohospital.org.au. (23.05.2013)

10 Health Precinct Benchmarking / Best Practice Review: Bendigo Hospital Precinct Structure Plan Draft 1, Billard Leece (May 2013)

11 www.newbendigohospital.org.au (31.05.2013)

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 14 | 74 Hill PDA

Once the Hospital redevelopment is complete and operational, there will be an increase of around 1,000 staff

working in the Hospital Precinct. Bendigo Health has indicated that the exact forecast of campus staff including a

breakdown of new recruits, visiting doctors/specialists and medical students is not yet available as it will depend

on a range of factors which are yet to be resolved12.

With an increase in capacity, beds and permanent staff will also be an increase in visiting medical specialists as

well as an increase in family and friends visiting patients in care. Many visitors from rural and regional

communities beyond the City of Greater Bendigo will choose to stay overnight and some may stay for weeks at a

time to offer support.

2.2 SURROUNDING LAND USES

Outside of the Hospital Precinct, the Study Area is defined by:

Hustlers Reef Reserve to the north-west;

The Catholic College located on the corner of Barkly and View Streets;

Rosalind Park including the primary school and secondary college and soon to developed theatre;

The north of Pall Mall, in particularly the area Park Road and the Chinese Precinct;

The Bendigo Creek to the south east; and

Residential areas to the north on rising topography leading towards the recently closed Bendigo North

Primary School.

The Study Area accommodates a range of regionally significant cultural, sporting and recreation precincts

including:

The Bendigo Chinese Association Precinct and Museum;

Tom Flood Sports Centre;

Bendigo Aquatic Centre;

Bendigo Bowling Club;

Bendigo Art Gallery;

The Queen Elizabeth Oval; and

Bendigo Tennis Complex.

Retail and commercial uses are predominately located in the south-west of the Study Area in Bridge Street and

the southern part of Arnold Street. Bridge Street, which is quite arterial in nature, provides a direct vehicle

connection with Bendigo CBD via Charles Street and the Midland Highway. This area, as shown on the following

12 Robyn Lindsay, Bendigo Health (May 2013)

Bendigo Hospital Precinct Structure Plan

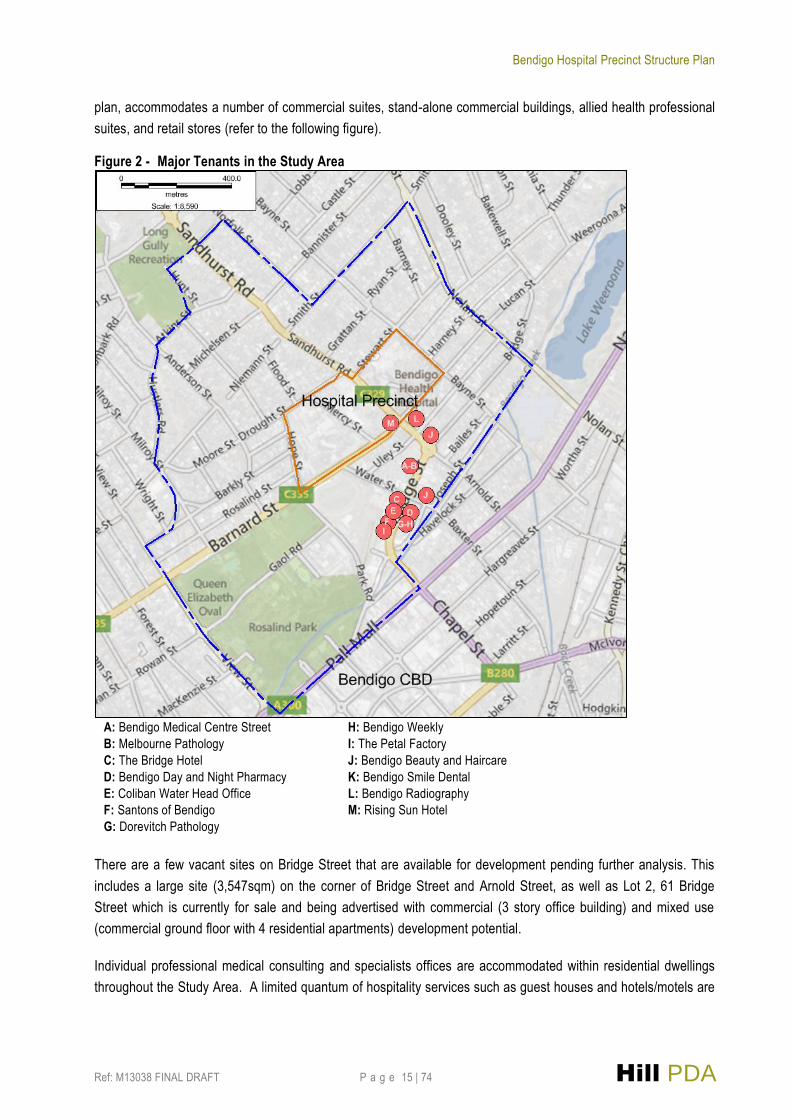

Ref: M13038 FINAL DRAFT P a g e 15 | 74 Hill PDA

plan, accommodates a number of commercial suites, stand-alone commercial buildings, allied health professional

suites, and retail stores (refer to the following figure).

Figure 2 - Major Tenants in the Study Area

A: Bendigo Medical Centre Street

B: Melbourne Pathology

C: The Bridge Hotel

D: Bendigo Day and Night Pharmacy

E: Coliban Water Head Office

F: Santons of Bendigo

G: Dorevitch Pathology

H: Bendigo Weekly

I: The Petal Factory

J: Bendigo Beauty and Haircare

K: Bendigo Smile Dental

L: Bendigo Radiography

M: Rising Sun Hotel

There are a few vacant sites on Bridge Street that are available for development pending further analysis. This

includes a large site (3,547sqm) on the corner of Bridge Street and Arnold Street, as well as Lot 2, 61 Bridge

Street which is currently for sale and being advertised with commercial (3 story office building) and mixed use

(commercial ground floor with 4 residential apartments) development potential.

Individual professional medical consulting and specialists offices are accommodated within residential dwellings

throughout the Study Area. A limited quantum of hospitality services such as guest houses and hotels/motels are

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 16 | 74 Hill PDA

scattered throughout the Study Area, although the majority of this type of accommodation is located outside of the

Study Area along Midland Highway and on the fringe of the CBD.

Whilst cultural, retail, commercial and civic uses lie predominately to the south of the Study Area, residential uses

are predominant to the north, east and west, both within and bounding the Study Area. The majority of housing is

detached with substantial pockets to the west and north-west covered by Heritage Overlays. There are some

instances of medium density residential, however this largely comprises small-lot subdivisions for townhouses and

villas.

Elsewhere within the Study Area there are scattered retail stores such as the small cluster located north of the

Hospital Precinct at the intersection of Arnold Street and Drought Street which include the likes of Arnold Street

Pharmacy, Central Victorian Sports Physiotherapy, Bendigo Eye Clinic, and other professional medical consulting

suites.

At the very north of the Study Area, 700m north of the Hospital Precinct, is the $25m Bendigo Health

Accommodation Project which is currently under construction and is due for completion in mid-2013. The project

comprises 120 one and two bedroom units to accommodate health professionals.

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 17 | 74 Hill PDA

Figure 3 - Bendigo Hospital Precinct Structure Plan Study Area Map

Source: Hansen Partnership (May 2013)

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 18 | 74 Hill PDA

Figure 4 - Bendigo Hospital Precinct Structure Plan Land Use Map

Source: Hansen Partnership (May 2013)

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 19 | 74 Hill PDA

Figure 5 - Bendigo Precinct Structure Plan Existing Zoning Map

Source: Hansen Partnership (May 2013)

Bendigo Hospital Precinct Structure Plan

Ref: M13038 DRAFT P a g e 20 | 74 Hill PDA

3. CITY OF BENDIGO ECONOMIC CONTEXT The City of Greater Bendigo is located approximately 150km to the north-west of Melbourne. Bendigo acts as a

major regional service centre providing a range of retail, commercial, entertainment, community and

administrative services for the municipality and wider region. The City is located at the confluence of a number of

major roads including the Calder Highway, Midland Highway and McIvor Highway. The centres of influence

outside the City include Horsham, Ballarat and Shepparton.

3.1 KEY INDUSTRY SECTORS IN BENDIGO

The City of Greater Bendigo’s Gross Regional Product (GRP) was $5.08b at 2012, with a per capita GRP of

approximately $50,500, which is higher than those found in the Loddon Mallee South Region ($44,110) but is

lower than the broader state of Victoria ($61,370)13.

Those industries which are considered to be key economic propulsive sectors in the City of Greater Bendigo given

their contributions to the local economy through employment, exports, value-added and local expenditure on

goods and services include: manufacturing; health care and social assistance; and financial and insurance

services.

The Bendigo Hospital is an especially important economic driver of the City. This is reflected in more detailed

REMPLAN data which shows that a number of industries sell a large amount of goods and services to the health

care and social assistance sector in the City.

Table 2 - Key Economic Drivers and Significant Local Industries in the City of Greater Bendigo (2012)

Economic Driver

Definition Total Value

Top 5 Highest Contributing Industries

Output Total revenue generated by businesses/organisations in the City of Greater Bendigo. Can also be referred to as total sales or total income.

$10.19b Manufacturing (21.6% of total)

Financial and Insurance Services (9.3%)

Construction (8.9%)

Rental, Hiring & Real Estate Services (8.1%)

Health Care & Social Assistance (7.1%)

Employment Number of people employed by businesses/organisations in each industry sector in the City of Greater Bendigo.

37,659 jobs

Health Care & Social Assistance (17.3%)

Retail Trade (13.7%)

Education & Training (9.8%)

Manufacturing (9.4%)

Accommodation & Food Services (6.8%)

Regional Exports

Goods and services produced by industry sectors and then sold to consumers, businesses and government based beyond the City of Greater Bendigo.

$2.63b Manufacturing (33.6%)

Mining (20.1%)

Financial and Insurance Services (12.4%)

Health Care & Social Assistance (7.2%)

Electricity, Gas, Water & Waste Services (4.5%)

Regional Imports

Intermediate goods & services which are imported into the City of Greater Bendigo by local industry sectors.

$2.37b Manufacturing (48.8%)

Mining (10.8%)

Construction (6.2%)

13 REMPLAN Greater Bendigo Economic Snapshot, Compelling Economics and Regional Development Victoria (2012)

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 21 | 74 Hill PDA

Economic Driver

Definition Total Value

Top 5 Highest Contributing Industries

Accommodation & Food Services (3.4%)

Professional, Scientific & Technical Services (3.1%)

Value Added The marginal economic value that is added by each industry sector in a defined region. Calculated by subtracting local expenditure and expenditure on regional imports from the output generated by industries.

$4.68b Financial & Insurance Services (14.8%)

Rental, Hiring & Real Estate Services (12%)

Health Care & Social Assistance (10.3%)

Manufacturing (9.3%)

Education & Training (6.4%)

Source: REMPLAN City of Greater Bendigo Economic Profile (2012)

3.2 KEY INSTITUTIONS AND BUSINESSES IN BENDIGO

The City is the home of the Bendigo and Adelaide Bank, a major financial institution that employs over 3,000

people nationally and continues to have its headquarters in central Bendigo14. Other prominent national

companies have their foundations in Bendigo, including Jimmy Possum furniture, Fernwood Fitness, Thales,

Bendigo Mining and Myer.

The City of Greater Bendigo has two large institutional anchors being the Bendigo Hospital and the La Trobe

University Campus. Both of these facilities draw people into the City, act as regional attractors, and are major

employers.

La Trobe University’s Bendigo campus accommodates almost 5,000 local and international students and 400 full

time employees. The campus occupies 33ha of land 3km from Bendigo CBD at Flora Hill. Each of La Trobe's

faculties is represented at La Trobe Bendigo as well as programs unique to the campus such as Visual Arts,

Outdoor and Environmental Education, Civil Engineering, Dentistry, Oral Health, Paramedicine, Pharmacy and

Planning. The University provides a range of residential accommodation options both on and off-campus. These

are further discussed in Section 5 of this Technical Assessment.

Other significant education and health facilities in the City of Greater Bendigo include:

Bendigo TAFE which provides courses in professional industries (IT, hospitality, beauty services,

management and human resources), creative and design industries (digital media, creative arts, graphic

design, writing and music), primary industries and trade (agriculture, horticulture, land management,

building and construction, electronics, plumbing), community services/health/wellbeing (aged care and

disability, children and community services, nursing and allied health), and English and indigenous and

general education (Aboriginal and Torres Strait Islander, english studies, general education and training).

Secondary colleges including Bendigo Senior Secondary College, Eaglehawk Secondary College and

Weeroona College.

Hospitals, medical centres and specialist care facilities include the St John of God Private Hospital,

Bendigo Day Surgery, Bendigo Medical, Bendigo Primary Care Centre and the new Youth Prevention &

Recovery Care centre (youth mental health).

14 City of Greater Bendigo REMPLAN Modelling, Compelling Economics and City of Greater Bendigo (2013)

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 22 | 74 Hill PDA

3.3 TOURISM IN BENDIGO

Bendigo is also a popular tourist destination with over 2.5 million visitors travelling to the Bendigo Loddon Region

annually.15 Over the past few years tourism has further expanded, in part due to the popularity of a number of

high profile exhibitions at the Bendigo Art Gallery and improvements to regional rail infrastructure between

Bendigo and Melbourne (Regional Rail Link Authority figures show a 150% increase in V/Line services in

Bendigo, Geelong and Ballarat from 2005 to 201116).

Key cultural attractors and facilities in Bendigo include the Bendigo Art Gallery, Golden Dragon Museum, Bendigo

Pottery, Soldiers Memorial Museum, La Trobe University Visual Arts Centre, and the Discovery Science &

Technology Centre.

3.4 SIGNIFICANT PROJECTS

There are a number of significant projects which are either in the pipeline or have commenced development and

which are likely to encourage economic growth in the City. These include17:

Bendigo Airport Upgrade;

Bendigo Library Redevelopment;

Bendigo Art Gallery Extension;

Bendigo Health Accommodation Precinct;

Proposed Marong Business Park;

Edward Street Car Park Complex Development;

Kangaroo Flat Aquatic and Leisure Centre Development; and

Sandhurst Community Theatre Complex.

15 Bendigo Loddon Regional Tourism Profile, Tourism Research Australia (2011)

16 http://www.bendigoadvertiser.com.au/story/1232544/rail-upgrade-for-growth/ (25 June 2013)

17 Greater Bendigo Economic Snapshot, Compelling Economics and Regional Development Victoria (2012)

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 23 | 74 Hill PDA

4. SOCIO-ECONOMIC AND INDUSTRY PROFILING This Chapter reviews the social and economic profile of residents within the area directly influenced by the

Bendigo Hospital redevelopment. Bendigo Hospital is located within the suburb of Bendigo, however it also

affects (by way of land use, traffic, economic activity and planning) areas such as North Bendigo, Long Gully and

Golden Square. The Greater Bendigo – Central Statistical Local Area (Central SLA) broadly encompasses these

areas (refer to the following figure) and has been used as the area for social and economic profiling as part of this

Chapter.

Figure 6 - Central SLA Context

Source: ABS 2011 and Hill PDA

This demographic profile identifies the social and economic characteristics that have influenced demand for jobs,

retail space and commercial and community services. The Central SLA has also been benchmarked against the

wider City of Greater Bendigo, Victoria and in some cases the City of Ballarat in order to better develop an

understanding of the area compared to other regional locations.

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 24 | 74 Hill PDA

4.2 AGE DISTRIBUTION AND POPULATION GROWTH

The Estimated Resident Population (ERP) of the City of Greater Bendigo at 2011 was approximately 101,900

persons. This represents growth of over 11,000 persons between 2001 and 2011 at an average growth rate of

1.20% per annum. This rate of growth is comparable to that of the City of Ballarat (1.29% per annum) and slightly

less than Victoria as a whole (1.42% per annum). However, the Central SLA population declined over this period

by around 1,200 persons (refer to the following table) which is unusual given the rate of growth across the wider

City area. This is likely to be as a result of an empty nester trend which sees an older demographic remaining in

larger dwelling stock whilst children move beyond the area once they reach adulthood. It could also be partly

attributable to some residential housing being used and/or converted for business functions.

Table 3 - Estimated Resident Population Change by Area (2001-2011)

Area 2001 2006 2011 Change

2001-2011

Average Annual

Growth 2001-2011

Central SLA 19,204 18,449 17,997 -1,207 -0.65%

City of Greater Bendigo 90,449 96,543 101,868 11,419 1.20%

City of Ballarat 83,599 88,451 95,007 11,408 1.29%

Victoria 4,804,726 5,126,540 5,534,526 729,800 1.42%

Source: ABS ERP Data (Publication 3218.0)

The median age of Central SLA residents increased from 34 years to 37 years between 2001 and 2011. This

trend was common across the wider City (35 to 38 years over the period) and throughout Victoria (35 to 37 years

over the period).

Figure 7 - Median Age (2001-2011)

Source: ABS Census Time Series Data (2011)

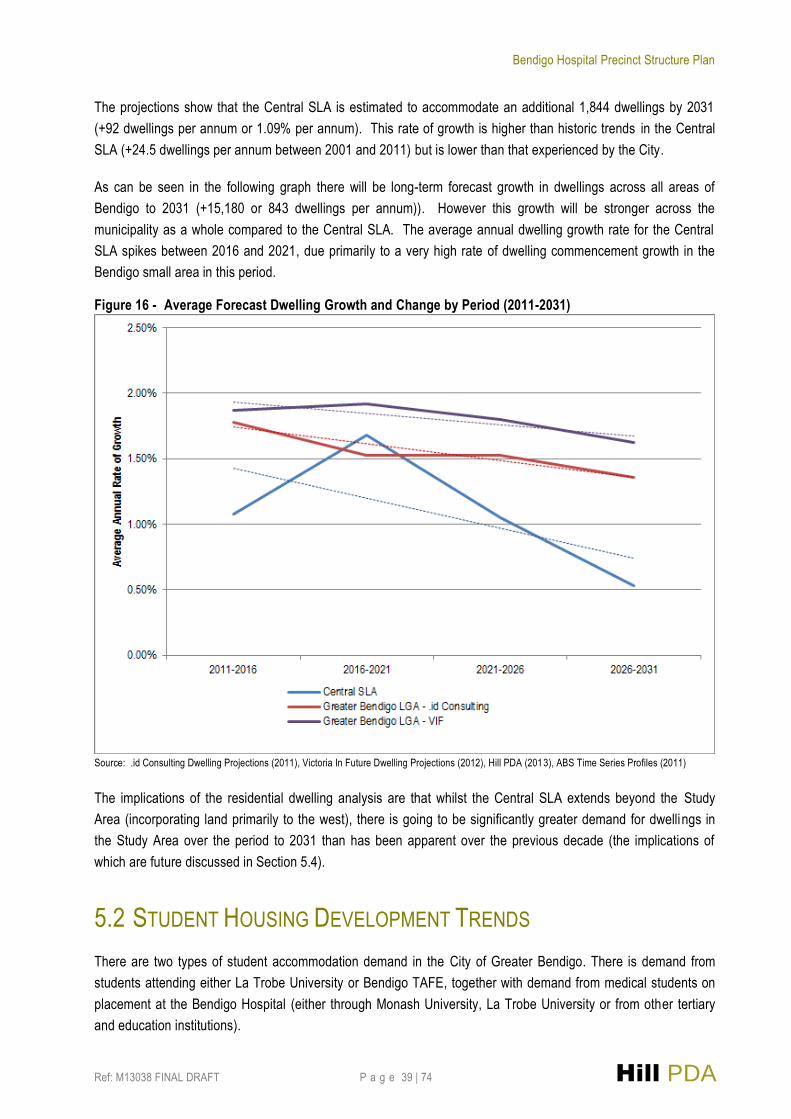

Projections of population growth have been forecast by Hill PDA for the Central SLA which largely corresponds to

the area of influence of the Bendigo Hospital. The projections have been determined through the following

methodology:

Calibrating .id Consulting forecasts (with a 2006 ABS Census base year) for the .id small areas that

roughly are equivalent to the Central SLA, to the ABS ERP at 2011; and

Forecasting growth from 2011 onwards by applying age cohort growth rates for the equivalent .id small

areas from the .id Consulting forecasts to 2031.

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 25 | 74 Hill PDA

As can be seen in the following table, the Central SLA has been forecast to grow from approximately 18,000

persons at 2011 to around 21,870 persons at 2031, at an average annual growth rate of approximately 1%. This

rate of growth may be conservative given the Bendigo Hospital redevelopment will significantly expand

employment in the local area and may stimulate demand for dwellings in and around the Hospital Precinct.

However, Hill PDA considers it appropriate given the historic decline in the resident population in the Central SLA

over the period 2001 to 2011.

Currently the 15-29 years age cohort is the most highly concentrated within the Central SLA and this will continue

to be the case at 2031. Growth in the older age cohorts (60-74 and 75+ years) is likely to be considerably

stronger than growth in all other age cohorts and indicates the further ageing of the population in this area.

Indeed the proportion of elderly residents (60+ years) in the Central SLA is forecast to increase from around 23%

at 2011 to 27% at 2031 which may precipitate greater demand for smaller, higher density dwelling types in this

area. Despite this trend, there will still be net additional growth in all other age groups in the area, with significant

growth in the 15-29 (+622 persons between 2011 and 2031) and 30-44 year age groups (+786 persons).

The wider City of Greater Bendigo is estimated to grow to approximately 140,500 persons at 2031. This would

represent an average annual growth rate of around 1.6%, which is significantly higher than that forecast for the

Central SLA. As can be seen in the following table, the SLA would make up just over 10% of the City’s population

growth to 2031.

Table 4 - Estimated Resident Population in the Central SLA (2001 to 2031)

Age Cohort Historic Forecast Change

(2011-2031)

Av. Annual

Change 2001 2006 2011 2016 2021 2026 2031

0-14 3,655 3,346 3,122 3,195 3,405 3,552 3,601 565 0.7%

15-29 4,608 4,171 4,146 4,239 4,498 4,666 4,728 622 0.7%

30-44 3,851 3,595 3,347 3,436 3,739 3,980 4,058 786 1.0%

45-59 3,151 3,333 3,273 3,348 3,482 3,525 3,567 236 0.4%

60-74 2,220 2,274 2,428 2,754 3,105 3,295 3,388 870 1.7%

75+ 1,720 1,729 1,680 1,842 2,067 2,344 2,525 917 2.1%

Total 19,204 18,449 17,997 18,815 20,297 21,362 21,868 3,871 1.0%

City of Greater Bendigo

90,449 96,543 101,868 111,199 121,374 131,128 140,509 38,641 1.6%

Source: ABS Time Series Data (2011), .id Consulting Population Forecasts and ABS Estimated Resident Population, publication 3218.0

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 26 | 74 Hill PDA

Figure 8 - Distribution of Population by Age Cohort in the Central SLA (2001 to 2031)

Source: ABS Time Series Data (2011), .id Forecast Population Projections and ABS Estimated Resident Population, publication 3218.0

4.3 HOUSEHOLD AND DWELLING CHARACTERISTICS

At 2011, the Central SLA accommodated 7,640 dwellings compared to around 7,400 dwellings at 2001. This

represents growth of approximately 240 dwellings at an average annual growth rate of just 0.3% (+24 dwellings

per annum). In comparison, over the same period the City of Greater Bendigo experienced an increase of around

6,610 dwellings at an average annual growth rate of 1.8% (around +660 dwellings per annum). This was higher

than that of Victoria (1.6% average annual growth) and was only slightly less than the City of Ballarat (2% average

annual growth).

Lower growth in dwellings in the Central SLA compared to the wider City may be partly due to the fact that the

Central SLA has fewer residential infill development opportunities, with a number of precincts also subject to

heritage preservation controls.

Table 5 - Dwelling Change by Area (2001-2011)

Area 2001 2006 2011 Change

(2001-2011) Av. Annual

Change

Greater Bendigo - Central SLA 7,398 7,494 7,643 245 0.3%

Household Size (persons per household) 2.6 2.5 2.4 - -

City of Greater Bendigo 33,029 36,114 39,638 6,609 1.8%

City of Ballarat 30,496 33,165 37,059 6,563 2.0%

Victoria 1,731,343 1,869,387 2,031,227 299,884 1.6% Source: ABS Census Time Series Data (2011)

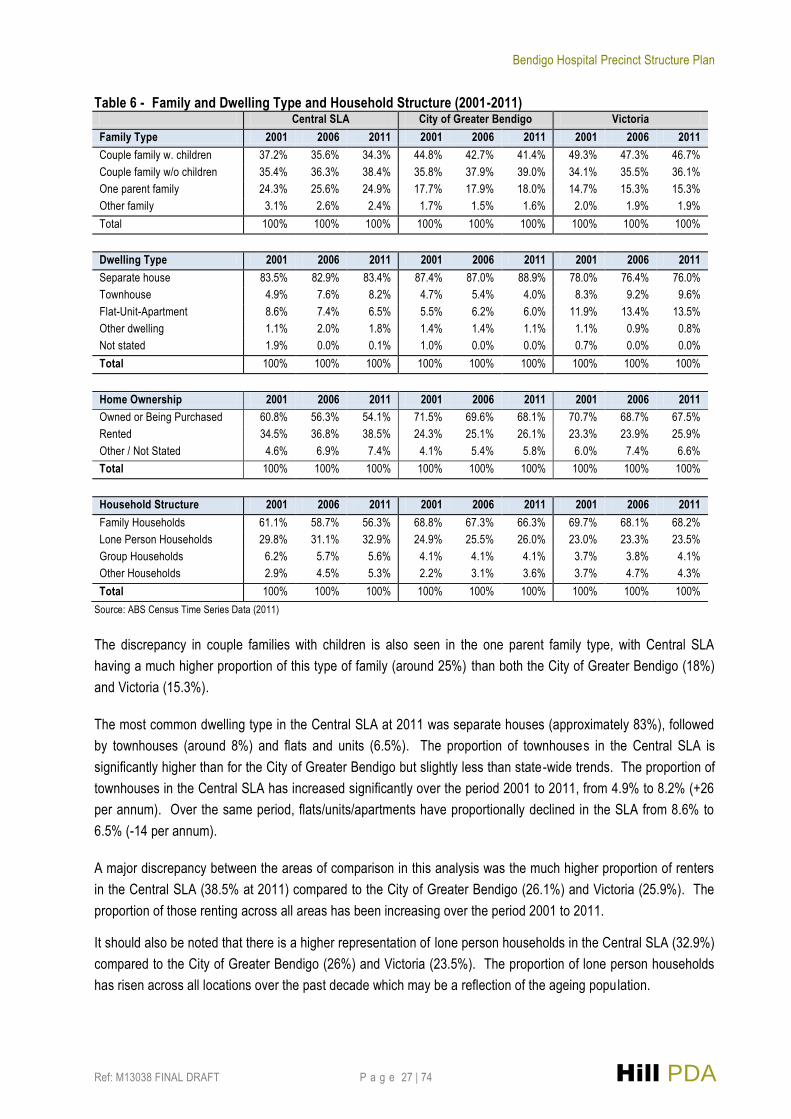

Historic trends in family and dwelling type composition and household structure was also analysed as part of this

Technical Assessment. The following table indicates that the Central SLA has a lower proportion of couple

families with children (34.3%) than both the City of Greater Bendigo (41.4%) and Victoria (46.7%). Across all of

these locations, there has been a decline in this family type since 2001.

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 27 | 74 Hill PDA

Table 6 - Family and Dwelling Type and Household Structure (2001-2011) Central SLA City of Greater Bendigo Victoria

Family Type 2001 2006 2011 2001 2006 2011 2001 2006 2011

Couple family w. children 37.2% 35.6% 34.3% 44.8% 42.7% 41.4% 49.3% 47.3% 46.7%

Couple family w/o children 35.4% 36.3% 38.4% 35.8% 37.9% 39.0% 34.1% 35.5% 36.1%

One parent family 24.3% 25.6% 24.9% 17.7% 17.9% 18.0% 14.7% 15.3% 15.3%

Other family 3.1% 2.6% 2.4% 1.7% 1.5% 1.6% 2.0% 1.9% 1.9%

Total 100% 100% 100% 100% 100% 100% 100% 100% 100%

Dwelling Type 2001 2006 2011 2001 2006 2011 2001 2006 2011

Separate house 83.5% 82.9% 83.4% 87.4% 87.0% 88.9% 78.0% 76.4% 76.0%

Townhouse 4.9% 7.6% 8.2% 4.7% 5.4% 4.0% 8.3% 9.2% 9.6%

Flat-Unit-Apartment 8.6% 7.4% 6.5% 5.5% 6.2% 6.0% 11.9% 13.4% 13.5%

Other dwelling 1.1% 2.0% 1.8% 1.4% 1.4% 1.1% 1.1% 0.9% 0.8%

Not stated 1.9% 0.0% 0.1% 1.0% 0.0% 0.0% 0.7% 0.0% 0.0%

Total 100% 100% 100% 100% 100% 100% 100% 100% 100%

Home Ownership 2001 2006 2011 2001 2006 2011 2001 2006 2011

Owned or Being Purchased 60.8% 56.3% 54.1% 71.5% 69.6% 68.1% 70.7% 68.7% 67.5%

Rented 34.5% 36.8% 38.5% 24.3% 25.1% 26.1% 23.3% 23.9% 25.9%

Other / Not Stated 4.6% 6.9% 7.4% 4.1% 5.4% 5.8% 6.0% 7.4% 6.6%

Total 100% 100% 100% 100% 100% 100% 100% 100% 100%

Household Structure 2001 2006 2011 2001 2006 2011 2001 2006 2011

Family Households 61.1% 58.7% 56.3% 68.8% 67.3% 66.3% 69.7% 68.1% 68.2%

Lone Person Households 29.8% 31.1% 32.9% 24.9% 25.5% 26.0% 23.0% 23.3% 23.5%

Group Households 6.2% 5.7% 5.6% 4.1% 4.1% 4.1% 3.7% 3.8% 4.1%

Other Households 2.9% 4.5% 5.3% 2.2% 3.1% 3.6% 3.7% 4.7% 4.3%

Total 100% 100% 100% 100% 100% 100% 100% 100% 100%

Source: ABS Census Time Series Data (2011)

The discrepancy in couple families with children is also seen in the one parent family type, with Central SLA

having a much higher proportion of this type of family (around 25%) than both the City of Greater Bendigo (18%)

and Victoria (15.3%).

The most common dwelling type in the Central SLA at 2011 was separate houses (approximately 83%), followed

by townhouses (around 8%) and flats and units (6.5%). The proportion of townhouses in the Central SLA is

significantly higher than for the City of Greater Bendigo but slightly less than state-wide trends. The proportion of

townhouses in the Central SLA has increased significantly over the period 2001 to 2011, from 4.9% to 8.2% (+26

per annum). Over the same period, flats/units/apartments have proportionally declined in the SLA from 8.6% to

6.5% (-14 per annum).

A major discrepancy between the areas of comparison in this analysis was the much higher proportion of renters

in the Central SLA (38.5% at 2011) compared to the City of Greater Bendigo (26.1%) and Victoria (25.9%). The

proportion of those renting across all areas has been increasing over the period 2001 to 2011.

It should also be noted that there is a higher representation of lone person households in the Central SLA (32.9%)

compared to the City of Greater Bendigo (26%) and Victoria (23.5%). The proportion of lone person households

has risen across all locations over the past decade which may be a reflection of the ageing population.

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 28 | 74 Hill PDA

Comparatively, Central SLA also has a significantly lower proportion of family households compared to the two

other areas.

The Central SLA had a lower median weekly household income compared to both the City of Greater Bendigo and

Victoria at 2011. The rate of growth in median weekly household incomes between 2001 and 2011 was

consistent across all locations.

Figure 9 - Median Weekly Household Income (2001 to 2011)

Source: ABS Census Time Series Data (2011)

4.4 EMPLOYMENT AND WORKFORCE PROFILE

4.4.1 RESIDENT WORKFORCE BY OCCUPATION

The characteristics of a resident workforce are an important factor in defining a region’s employment strengths

and weaknesses. It is important to note that the resident workforce (or labour force) in many cases will travel

outside of the local government boundary to work.

At 2011 there were approximately 7,740 working residents in the Central SLA. The most common occupations of

residents were professionals (21%), technicians and trade workers (15%) and labourers (13%). There was a

similar occupational breakdown for the City of Greater Bendigo and Victoria, however both had a higher

concentration of clerical and administrative workers. The proportion of professional workers has been steadily

increasing over the period 2001 to 2011 across all locations.

4.4.2 RESIDENT WORKFORCE BY INDUSTRY

At 2011, health care and social assistance was easily the largest employing industry for residents within the

Central SLA (17.5% of all working residents). Other significant employing industries for residents in the SLA

included retail trade (12.5%) and manufacturing (10%).

Not only is health care and social assistance the largest employer of residents in the SLA, it has also been one of

the fastest growing industries of employment (+31% between 2001 and 2011). This growth was only outstripped

by mining, electricity, gas, water and waste services and construction.

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 29 | 74 Hill PDA

By comparison, the number of working residents in the following industries has declined: information, media and

telecommunication services (-56% between 2001 and 2011), wholesale trade (-36%), agriculture, forestry and

fishing (-30%), and manufacturing (-21%). Manufacturing has also experienced the greatest decline in number of

working residents over the period (-205). The total number of working residents in the SLA grew by 515 (or around

7%) over the period 2001 and 2011.

Table 7 - Central SLA Industry of Employment (2001-2011)

Industry of Employment 2001 2006 2011 Change

2001-2011 Proportional

Change 2001-2011

Agriculture, forestry and fishing 135 105 95 -40.0 -30%

Mining 19 86 67 48.0 253%*

Manufacturing 977 891 772 -205.0 -21%

Electricity, gas, water and waste services 66 77 102 36.0 55%

Construction 482 579 696 214.0 44%

Wholesale trade 302 238 194 -108.0 -36%

Retail trade 977 971 967 -10.0 -1%

Accommodation and food services 540 579 569 29.0 5%

Transport, postal and warehousing 196 212 255 59.0 30%

Information media and telecommunications 245 232 108 -137.0 -56%

Financial and insurance services 196 259 266 70.0 36%

Rental, hiring and real estate services 66 61 78 12.0 18%

Professional, scientific and technical services 287 267 313 26.0 9%

Administrative and support services 239 210 252 13.0 5%

Public administration and safety 373 470 458 85.0 23%

Education and training 531 606 665 134.0 25%

Health care and social assistance 1,040 1,162 1,358 318.0 31%

Arts and recreation services 107 87 100 -7.0 -7%

Other services 317 262 282 - 35.0 -11%

Inadequately described/Not stated 128 165 141 13.0 10%

Total 7,223 7,519 7,738 515 7%

* It is noted that since the 2011 Census, Unity Mine at Henty has gone into sleeper arrangement and closure and this would have impacted on mining employment figures since that time.

Source: ABS Census Time Series Data (2011)

4.4.3 JOB CONTAINMENT AND HEALTH CARE WORKER TRENDS

Journey to work data as compiled by the ABS18 uses employment counts for specific locations to analyse industry

trends and methods of travel to work. The results indicate the City provides a total of 37,915 jobs, whilst

accommodating 45,749 resident workers at 2011. Hence the City is a net exporter of workers with 7,834

residents leaving the City for employment. Mount Alexander and Melbourne LGAs were the most common

destinations for employment for working Bendigo residents.

The journey to work data also indicates where those that work in the City of Greater Bendigo live. The analysis

shows that approximately 7.4% of workers (2,820 persons) reside beyond the City, most commonly in the

surrounding LGAs of Mount Alexander, Loddon and Macedon Ranges.19 Of those that work in Bendigo but live

beyond the City, 20% or 567 are employed in the health care and social assistance sector. This is around 9% of

all jobs in this sector in the City of Greater Bendigo.

19 City of Greater Bendigo Community Profile, .id Consulting (2013)

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 30 | 74 Hill PDA

The following table identifies where those that work in the health care and social assistance sector in the City of

Greater Bendigo reside.

Table 8 - City of Greater Bendigo: Health Care & Social Assistance Workers (2011)

Place of Usual Residence (LGA) No. Workers Proportion of Total

Greater Bendigo 5,914 90.8%

Mount Alexander 218 3.3%

Loddon 75 1.2%

Campaspe 44 0.7%

Macedon Ranges 34 0.5%

Boroondara 21 0.3%

Other 205 3.1%

Total Workers 6,511 100%

*Count of employed persons aged 15 years and over (excludes overseas visitors). Source: ABS, Journey to work, REMPLAN Copy, (2011)

The analysis indicates that residents of Mount Alexander LGA fill the greatest number of Health Care and Social

Assistance jobs in the City of Greater Bendigo (excluding residents of the City of Greater Bendigo).

Other surrounding LGAs including Loddon and Campaspe also had a significant number of residents working in

the health care and social assistance sector within the City of Greater Bendigo. Interestingly, the inner urban

Melbourne LGA of Boroondara had the 6 th highest number of residents working in health care and social

assistance in Bendigo. This indicates that health care facilities in Bendigo, including the Bendigo Hospital, attract

workers from a wide regional base that includes some parts of Melbourne.

4.4.4 UNEMPLOYMENT

Unemployment within the Greater Bendigo – Central SLA declined from 11.4% to 6.8% over the 2001 to 2011

period. The 2011 unemployment rate is higher than that found in the City of Greater Bendigo (5.3%) and Victoria

(5.4%).

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 31 | 74 Hill PDA

5. RESIDENTIAL AND ACCOMMODATION MARKET This Chapter examines supply and demand for residential dwellings in the City of Greater Bendigo based on an

examination of Council’s 2004 Residential Development Strategy (RDS)20, as well as through discussions with

local agents and developers. As part of the continuing monitoring and assessment process, the RDS is currently

undergoing a review which has incorporated a Land Audit (2011) and Land Supply and Demand Assessment

(2013) which have also informed this Chapter.

This Chapter also examines the different residential product types and markets prevalent in Bendigo including

reference to the short-term accommodation and student housing markets, which may also influence the potential

for residential development around the Bendigo Hospital.

5.1 RESIDENTIAL DWELLING DEVELOPMENT TRENDS

5.1.1 DWELLING APPROVALS IN THE CITY OF GREATER BENDIGO

Historically detached residential dwellings have predominated throughout the City of Greater Bendigo. The Land

Supply and Demand Assessment (2013) found that the vast majority of the 5,676 dwelling approvals that had

occurred between 2006 and 2012 and which had moved through to the construction phase (around 92%) had

been for detached dwellings. The remainder (around 8%) has been for medium density dwellings such as

townhouses and flats/units/apartments.21

Figure 10 - Residential Building Approvals by Dwelling Type (1996-2012)

Source: ABS Catalogue Number 8731.0 and Profile id (2013)

20 Bendigo Residential Development Strategy, Parsons Brinckerhoff (2004)

21 Bendigo Residential Development Strategy Review: Land Supply and Demand Assessment, City of Greater Bendigo (2013)

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 32 | 74 Hill PDA

To further note, minor lot construction (projects yielding less than 10 lots) accounted for 39% of all residential

development activity over the period, with major lot construction (projects yielding greater than 10 lots) accounting

for 49%. The following figure highlights lot construction by area in the City of Greater Bendigo.

Figure 11 - Average Residential Lots Constructed by Small Area Per Annum (2006-2012)

Source: Residential Development Strategy Review: Land Supply and Demand Assessment (2013)

Average residential lot construction in areas around the Hospital Precinct varied, with Golden Square having the

greatest quantum in the City (over 700 lots per annum), whilst Bendigo was toward the lower end of lot

construction during this period (around 150 lots per annum).

5.1.2 DEVELOPMENT TRENDS IN THE STUDY AREA AND SURROUNDS

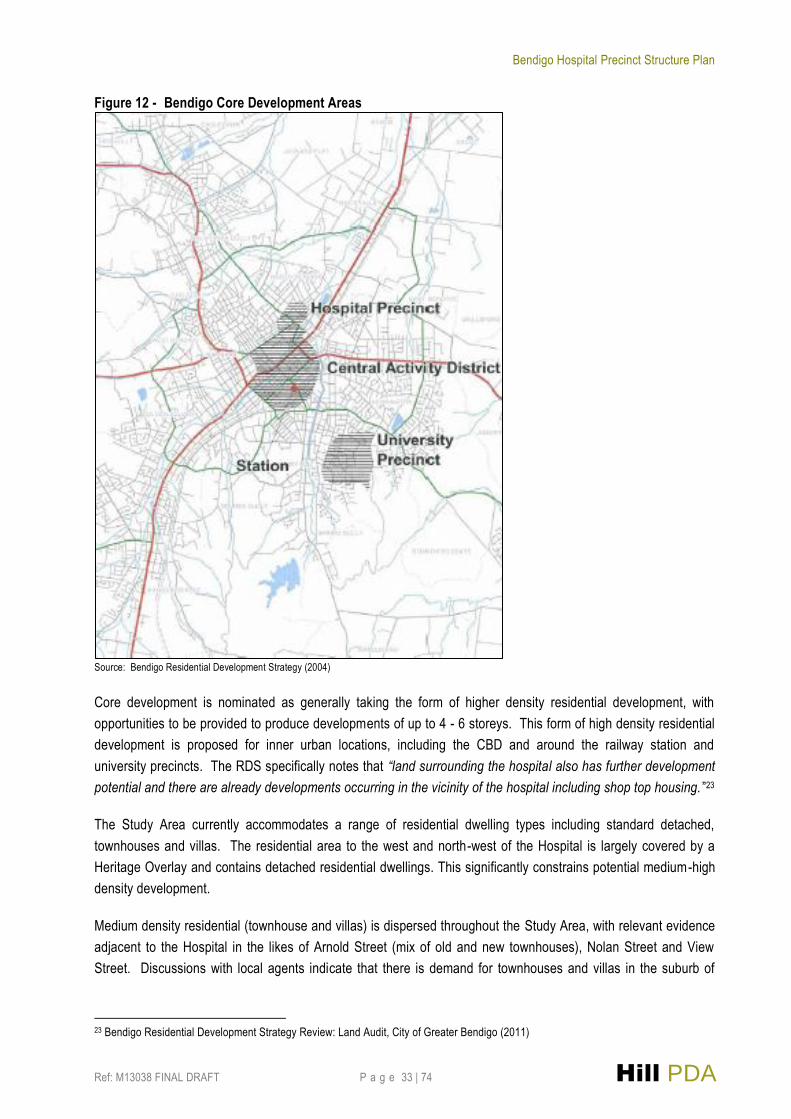

The Study Area of the Bendigo Hospital Structure Plan is within a nominated core development area of the RDS.

The RDS forecast 950 additional dwellings (to accommodate 1,500 persons) in the core development areas of

Bendigo from 2004 to 2031. The Land Audit (2011) identified that just 16% of growth nominated for the core

development area had been completed since 2004.22

22 Bendigo Residential Development Strategy Review: Land Audit, City of Greater Bendigo (2011)

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 33 | 74 Hill PDA

Figure 12 - Bendigo Core Development Areas

Source: Bendigo Residential Development Strategy (2004)

Core development is nominated as generally taking the form of higher density residential development, with

opportunities to be provided to produce developments of up to 4 - 6 storeys. This form of high density residential

development is proposed for inner urban locations, including the CBD and around the railway station and

university precincts. The RDS specifically notes that “land surrounding the hospital also has further development

potential and there are already developments occurring in the vicinity of the hospital including shop top housing. ”23

The Study Area currently accommodates a range of residential dwelling types including standard detached,

townhouses and villas. The residential area to the west and north-west of the Hospital is largely covered by a

Heritage Overlay and contains detached residential dwellings. This significantly constrains potential medium-high

density development.

Medium density residential (townhouse and villas) is dispersed throughout the Study Area, with relevant evidence

adjacent to the Hospital in the likes of Arnold Street (mix of old and new townhouses), Nolan Street and View

Street. Discussions with local agents indicate that there is demand for townhouses and villas in the suburb of

23 Bendigo Residential Development Strategy Review: Land Audit, City of Greater Bendigo (2011)

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 34 | 74 Hill PDA

Bendigo which has been reflected in many local developers purchasing older dilapidated houses on large blocks

for 2-3 lot subdivisions. The 2011 Audit Report and 2013 Land Supply and Demand Assessment indicated that

more than 30% of the annual net lots created in the City since 2004 have been ‘minor infill’ lots (less than 4 lot

subdivisions) which is reported to be creating improved efficiencies for services, infrastructure and land use. This

trend is likely to continue over the long-term as the population ages and elderly residents seek to move to smaller

dwellings which are close to services and community activity.

Figure 13 - Recent Townhouse Development in the Study Area

83-87 Arnold Street

232 View Street Bendigo

Source: Hill PDA and Cordell Connect (2013)

There are no examples of higher density residential development (e.g. 4-6 level apartment buildings) in the Study

Area. There is a development application for the construction of a 5 storey apartment building comprising 18

apartments and a small office component at 71-75 Bridge Street approximately 500 meters south-east from the

Bendigo Hospital campus. However, it is understood that the development has been put on hold.

Other significant proposals include:

Approval has been granted for a 4 storey apartment building comprising 12 units at 23 Wills Street

approximately 2.5km south of the Bendigo Hospital Precinct and 1km from the Study Area border. The

building also comprises a retail and office component.

In addition to the above, applications for the subdivision of lots have become increasingly common in the Study

Area with approximately 25 having been assessed by Council from 2012 onwards. The following figure shows

where applications for all subdivision has occurred in the Study Area.

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 35 | 74 Hill PDA

Figure 14 - Vacant and Existing and Proposed Subdivided Lots in the Study Area

Source: City of Greater Bendigo and Hill PDA (2013)

Despite a lack of construction, there have been an increasing number of higher density development proposals in

the suburb of Bendigo, which suggests developer interest in less traditional dwelling forms including shop-top

apartments (particularly in the CBD and high amenity areas) and multi-unit developments. Consultation sessions

held during the Structure Plan process noted:

Demand and acceptance for higher density dwelling forms were slowly but steadily increasing in and

around central Bendigo with dwelling demand largely being driven by those seeking a more urban

lifestyle;

There was concern that high density residential would have a negative impact on traffic, amenity and the

streetscape of the local area around the Hospital, with multi-level development also potentially restricting

valuable view lines (particularly for those dwellings north of the Hospital); and

The need for planning to guide how further development of established residential sites around the

Hospital can occur. Small scale medium density is suitable in the short-term (perhaps as units at the

back of larger lots) with higher density over the longer-term. It was also noted however that this form of

development can lead to poor urban amenity and design outcomes.

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 36 | 74 Hill PDA

Potential areas for higher density residential development were identified during the Structure Plan consultation

sessions, including:

Barnard Street which has potential for high density mixed use development given its ability to overlook

Rosalind Park;

The triangular area between Barnard Street and Bridge Street;

Land between Bayne and Nolan Streets which are not subject to heritage constraints and there have

been a number of recent development applications in this area;

Larger blocks on Flood Street which could be suitable for residential infill.

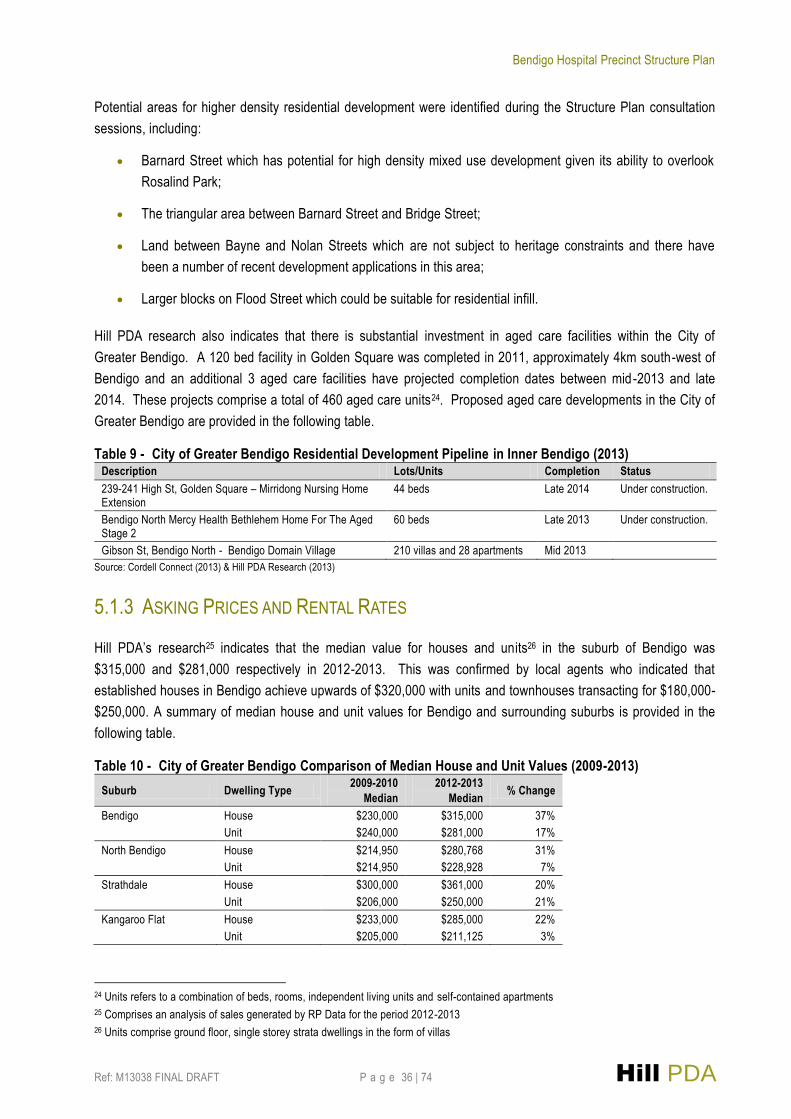

Hill PDA research also indicates that there is substantial investment in aged care facilities within the City of

Greater Bendigo. A 120 bed facility in Golden Square was completed in 2011, approximately 4km south-west of

Bendigo and an additional 3 aged care facilities have projected completion dates between mid-2013 and late

2014. These projects comprise a total of 460 aged care units24. Proposed aged care developments in the City of

Greater Bendigo are provided in the following table.

Table 9 - City of Greater Bendigo Residential Development Pipeline in Inner Bendigo (2013) Description Lots/Units Completion Status

239-241 High St, Golden Square – Mirridong Nursing Home Extension

44 beds Late 2014 Under construction.

Bendigo North Mercy Health Bethlehem Home For The Aged Stage 2

60 beds Late 2013 Under construction.

Gibson St, Bendigo North - Bendigo Domain Village 210 villas and 28 apartments Mid 2013

Source: Cordell Connect (2013) & Hill PDA Research (2013)

5.1.3 ASKING PRICES AND RENTAL RATES

Hill PDA’s research25 indicates that the median value for houses and units26 in the suburb of Bendigo was

$315,000 and $281,000 respectively in 2012-2013. This was confirmed by local agents who indicated that

established houses in Bendigo achieve upwards of $320,000 with units and townhouses transacting for $180,000-

$250,000. A summary of median house and unit values for Bendigo and surrounding suburbs is provided in the

following table.

Table 10 - City of Greater Bendigo Comparison of Median House and Unit Values (2009-2013)

Suburb Dwelling Type 2009-2010

Median

2012-2013

Median % Change

Bendigo House $230,000 $315,000 37%

Unit $240,000 $281,000 17%

North Bendigo House $214,950 $280,768 31%

Unit $214,950 $228,928 7%

Strathdale House $300,000 $361,000 20%

Unit $206,000 $250,000 21%

Kangaroo Flat House $233,000 $285,000 22%

Unit $205,000 $211,125 3%

24 Units refers to a combination of beds, rooms, independent living units and self-contained apartments

25 Comprises an analysis of sales generated by RP Data for the period 2012-2013

26 Units comprise ground floor, single storey strata dwellings in the form of villas

Bendigo Hospital Precinct Structure Plan

Ref: M13038 FINAL DRAFT P a g e 37 | 74 Hill PDA

Suburb Dwelling Type 2009-2010

Median

2012-2013

Median % Change

Jackass Flat House $247,125 $371,000 50%

Unit $208,625 $230,000 10%

Marong House $219,000 $312,500 43%

Strathfieldsaye House $315,000 $360,000 14%

Ballarat House $227,000 $316,000 39%

Unit $220,500 $256,000 16%

Source: RP Data (2013) & Hill PDA Research (2013)

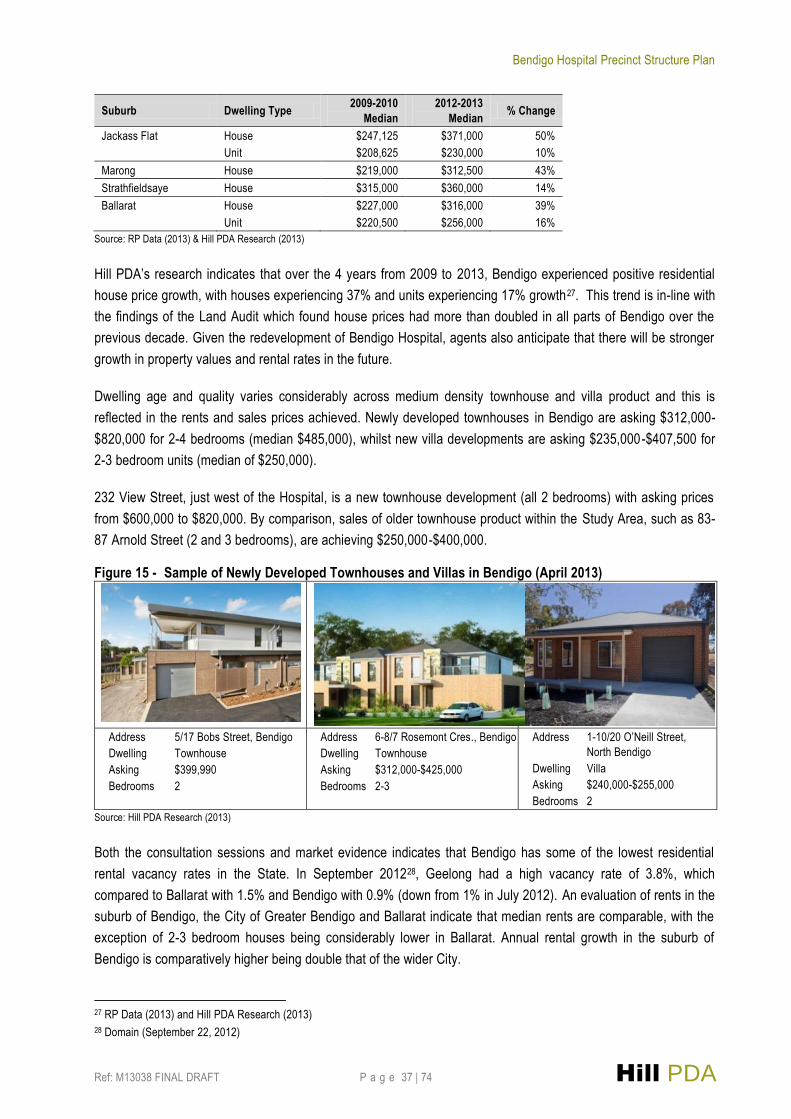

Hill PDA’s research indicates that over the 4 years from 2009 to 2013, Bendigo experienced positive residential

house price growth, with houses experiencing 37% and units experiencing 17% growth27. This trend is in-line with

the findings of the Land Audit which found house prices had more than doubled in all parts of Bendigo over the

previous decade. Given the redevelopment of Bendigo Hospital, agents also anticipate that there will be stronger

growth in property values and rental rates in the future.

Dwelling age and quality varies considerably across medium density townhouse and villa product and this is

reflected in the rents and sales prices achieved. Newly developed townhouses in Bendigo are asking $312,000-

$820,000 for 2-4 bedrooms (median $485,000), whilst new villa developments are asking $235,000-$407,500 for

2-3 bedroom units (median of $250,000).

232 View Street, just west of the Hospital, is a new townhouse development (all 2 bedrooms) with asking prices

from $600,000 to $820,000. By comparison, sales of older townhouse product within the Study Area, such as 83-

87 Arnold Street (2 and 3 bedrooms), are achieving $250,000-$400,000.

Figure 15 - Sample of Newly Developed Townhouses and Villas in Bendigo (April 2013)

Address 5/17 Bobs Street, Bendigo

Dwelling Townhouse

Asking $399,990

Bedrooms 2