jpo global macro i

TRANSCRIPT

JP Omega Ltd.

Discussion Document

Berlin,

April 20, 2015

JP Omega Ltd.

JP Omega Ltd.

Global Macro I - JP Omega optimized

Performance Evaluation

Optimized w.r.t. Johnson OmegaPortfolio Type LongBiasLeverage 1574Risfree Rate USD Libor 1MUniverse Global Macro

RebalancingFrequency MonthlyDay LastBusinessDayOffset DaysLag Days Exposure Long (rhs)

Transaction Cost Turnover (p.a.) 1751%Long bps Exposure Short (rhs) 279Short bps

Exposure

MinMax

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec YTD BenchConstituent (Classes): 2015 1,2% -0,3% 2,7% 3,7% 1,3%

2014 -1,7% 0,4% 0,2% 1,2% 2,8% 1,4% 2,8% 1,8% -0,1% 0,8% 1,6% 0,9% 12,5% 1,7%1. Equity - Developed 2013 2,3% 1,3% 1,4% 2,2% -0,7% -0,9% -0,2% 0,2% -0,1% 1,5% 0,4% -2,7% 4,7% 2,4%2. Equity - Emerging 2012 0,8% 1,9% 2,2% -0,5% -0,1% -0,8% 0,5% 0,3% -3,1% -0,7% -0,7% 3,8% 3,4% 8,5%3. BondsBonds 2011 3,6% 1,2% -1,9% 3,9% -0,1% -1,7% 2,3% 0,8% -0,6% -1,3% -0,1% 0,1% 6,0% -7,3%4. CommoditiesCommodities 2010 -4,7% -1,2% 0,1% 2,0% -0,3% 1,9% -0,2% 3,4% 1,3% 6,2% -2,5% 8,5% 14,4% 10,7%5. CashCash 2009 -1,4% 0,2% 0,8% 12,9% 11,0% -1,1% 10,4% 1,3% 0,1% -2,6% 5,9% -1,0% 41,2% 35,2%

2008 -1,7% 5,2% -2,0% 0,1% 4,9% -4,2% -0,2% -0,1% 0,7% 3,2% 4,9% 4,7% 16,0% -27,9%Constituent (Assets): 2007 -3,8% 0,1% -0,2% 1,8% 1,4% 1,5% 10,3% 0,4% 3,0% 14,6% -3,1% 2,5% 30,5% 12,5%

2006 10,1% 0,1% 7,5% 9,0% 0,1% -1,8% 3,9% 3,6% 1,8% 2,7% 6,5% 9,5% 66,8% 24,1%Equity-Developed (0 to 75%): 2005 -0,1% 1,7% -4,2% -8,2% 0,5% 3,3% 0,6% 1,3% 11,3% -2,1% 10,2% 8,2% 22,9% 25,9%

a) S&P 500 COMPOSITE 2004 -2,5% 7,1% -0,7% -2,4% -0,1% 0,9% -0,5% -0,3% 1,7% 0,0% 5,1% 4,4% 12,9% 14,1%b) EURO STOXX 50 2003 0,9% 1,5% -1,8% 0,3% 2,1% 0,9% 6,7% 13,6% 1,1% 7,8% 1,0% 11,4% 54,7% 24,7%c) KOREAN KOSPI 200 2002 5,0% 2,2% 2,9% -0,4% 0,7% 0,0% 0,5% 1,4% 0,6% -1,1% 0,9% -0,7% 12,5% 1,6%d) NIKKEI 225 STOCK AVERAGE 2001 -0,4% 1,2% 0,9% 0,4% 3,2% 1,0% 0,2% 0,4% 0,4% 0,7% -0,2% 10,6% 19,5% -4,3%e) S&P/ASX 200 2000

Bonds (0 to 150%): a) US Gov 10 YEAR Commodities (-12.5% to 25%) a) S&P GSCI Crude OilEquity-Emerging (0 to 50%): a) HANG SENG CHINA ENTERPRISES b) BD Gov 10 YEAR b) S&P GSCI Gold

b) FTSE/JSE TOP 40 c) JP Gov 10 YEAR c) S&P GSCI IndustrialMetals (Copper, Aluminum and Zinc)c) CNX NIFTY (50) d) AU Gov 10 YEAR d) S&P GSCI Softs

-1 JP Omega Ltd.

0% 150%-50% 100%-50% 150%

Min Max0% 150%0% 150%

0% -50%

0

200% 150%

0

Monthly Returns

Basic Information, Performance Chart & Table Global Macro I - JP Omega optimizedDescription

100%

Gross Net

Performance & Exposure Chart Start: End:29-Dec-00 31-Mar-15

00

Exposure (Net)

-50%

-25%

0%

25%

50%

75%

100%

125%

150%

0

200

400

600

800

1000

1200

1400

1600

1800

Dec-00 Dec-02 Dec-04 Dec-06 Dec-08 Dec-10 Dec-12 Dec-14

Johnson Omega

Benchmark

Optimized Benchmark Magnitude t-stat Optimized Benchmark

Return comp. ann. 21,3% 7,5% Mean Exc. Return ann. 12,4% 3,74 worst 3,22% -16,60%

Volatility ann. 12,7% 11,1% Tracking Error ann. 12,6% na 2nd worst -0,58% -7,53%

Skewness 0,53 -0,64 Jensen Alpha ann. 15,4% 5,05 3rd worst 0,75% -7,51%

p-value 11% 5% Market Beta 0,51 6,50 4th worst -0,05% -6,21%

Kurtosis 3,16 2,79 5th worst 0,39% -5,81%

p-value 0,8% 0,6% Comments & Portfolio Highlights 5th best -1,34% 6,62%

Downside Deviation ann. 5,2% 11,1% 1. Clearly higher annualized compounded return 4th best 10,06% 6,64%

Magnitude 12,0% 35,9% 2. Slightly higher volatility 3rd best 10,45% 6,74%

Peak 28-Feb-05 31-Oct-07 3. Outperformance at 99,9907% Confidence Level 2nd best 10,97% 6,88%

Trough 29-Apr-05 27-Feb-09 4. Positive Skewness of Strategy best 0,85% 7,25%

Recovery 5 22 5. Fat tail to upside

6. Lower downside deviation

7. Substantially lower Maximum Drawdown

Optimized Benchmark 8. Much faster recovery from Max Drawdown Optimized Benchmark

Sharpe 1,45 0,54 9. Higher Sharpe, Sortino , Calmar Ratio 0,1% -0,40% -7,47%

Sortino 3,53 0,54 10. Positive Treynor Ratio 1,0% -0,27% -4,34%

Calmar 1,77 0,21 11. Excellent Information Ratio 2,5% -0,18% -3,26%

Treynor 24,4% 12. Substantial Skill: Jensen Alpha, significant at 99,9999777% CL 5,0% -0,08% -2,50%

Information 0,99 13. No Luck: Returns not generated through excessive exposure. 10,0% 0,06% -1,77%

Maximum Exp. Gain 4,7% 3,0% 14. Better outliers to the upside versus downside ratio 50,0% 0,91% 0,02%

Maximum Exp. Loss -0,1% -5,7% 15. Better overall upside potential versus downside risk 90,0% 1,22% 1,34%

Gain vs. Loss Ratio 48,37 0,52 16. Performed 5 times better within 5 CL brackets on downside 95,0% 2,56% 1,38%

Call (Upside) 0,7% 0,2% 17. Performed 4 times better within 5 CL brackets on upside 97,5% 3,19% 1,80%

Put (Downside) 0,2% 1,0% 18. Performed 5 times better in 5 worst months 99,0% 3,78% 2,22%

Omega 4,16 0,20 19. Performed 3 times better in 5 best months 99,9% 4,49% 2,77%

JP Omega Ltd.

Detailed Performance Measurement - Entire Period

Confidence Level

Advanced

Traditional

Performance Ratios

Global Macro - JP Omega optimized

Best/Worst Benchmark vs Strategy

Probabilities for Minimum Realized Returns

Best Months

Maximum Drawdown

Worst MonthsReturn and

Moments

Excess Returns

Market Model

Absolute Performance Measures Relative Performance Measures

10 Y since 31-Mar-05 5 Y since 31-Mar-10 3 Y since 30-Mar-12 1 Y since 31-Mar-14

Portfolio Optimized Benchmark Optimized Benchmark Optimized Benchmark Optimized Benchmark

Return comp. ann. 21,3% 6,8% 10,2% 3,3% 6,4% 2,5% 18,0% 2,2%

Volatility ann. 13,1% 11,7% 7,0% 9,3% 5,2% 6,8% 3,6% 4,8%

Skewness 1,14 -1,13 1,05 -0,19 -0,18 -1,16 -0,01 -0,76

p-value 0% 4% 1% 29% 29% 0% 49% 4%

Kurtosis 1,77 4,86 2,93 1,28 0,33 2,12 -0,68 -0,06

p-value 1,5% 2,9% 1,1% 2,2% 24,0% 3,8% 10,9% 47,7%

Downside Deviation ann. 5,8% 12,2% 3,8% 9,0% 3,8% 7,8% 0,4% 5,7%

Magnitude 8,2% 35,9% 5,1% 12,5% 5,1% 6,3% 0,3% 4,5%

Peak 31-Mar-05 31-Oct-07 30-Mar-12 29-Apr-11 30-Mar-12 30-Mar-12 30-Jan-15 29-Aug-14

Trough 29-Apr-05 27-Feb-09 30-Nov-12 30-Sep-11 30-Nov-12 31-May-12 27-Feb-15 31-Dec-14

Recovery (Months) 5 22 2 25 2 4 1 no recovery

Mean Exc. Return ann. 12,9% 6,3% 3,6% 14,5%

t-stat 3,16 1,37 0,75 2,88

Tracking Error ann. 13,0% 10,3% 8,3% 5,0%

Jensen Alpha ann. 15,7% 9,2% 6,0% 16,1%

t-stat 4,25 2,99 1,94 4,44

Market Beta 0,50 0,17 0,06 0,23

t-stat 5,49 1,73 0,44 0,99

Sharpe 1,43 0,48 1,40 0,37 1,17 0,38 4,61 0,44

Sortino 3,19 0,46 2,58 0,38 1,62 0,33 41,50 0,37

Calmar 2,60 0,19 2,01 0,26 1,26 0,41 70,28 0,48

Treynor 25,9% 38,2% 61,1% 64,0%

Information 1,00 0,61 0,43 2,88

Max Gain vs. Loss 22,05 0,47 7,79 0,82 2,36 0,35 3,83 0,45

Omega 4,58 0,21 11,68 0,44 9,13 0,50 10,56 0,56

JP Omega Ltd.

Relative Performance

Measures

Advanced

Excess Returns

Market Model

Performance Ratios

Traditional

Maximum Drawdown

Return and Moments

Absolute Performance

Measures

Global Macro - JP Omega optimizedPerformance Measurement - Subperiods

1. Return (ann., comp.): Return per anno including compounding (profits reinvested)

2. Volatility (ann.):

3. Skewness (p-value): Asymmetry of distribution: Negative/positive indicates a tendency for extreme returns to downside/upside. P-value indicates the significance.

4. Kurtosis (p-value):

5. Downside Deviation:

6. Maximum Drawdown:

7. Excess Returns:

8. Market Model:

JP Omega Ltd.

Relative Performance Measures

A) Jensen Alpha (SKILL) is the intercept from a regression line for strategy excess returns w.r.t. riskfree on benchmark excess returns w.r.t. riskfree. It is a measure for the skill inherent in a strategy. Significance indicates whether Jensen Alpha was not generated by chance.

Excess returns from strategy versus benchmark. It is required that those are significant. Necessary, but not sufficient to evaluate a strategy as significant excess returns generated in a bull market might be simply generated by plain leverage. Here Jensen Alpha required for complete picture.

B) Beta (LUCK) is the slope of the regression line and the explanatory variable for returns in this simple factor model. Returns explained by beta are considered to be generated by luck, supposed market timing is impossible.

Tail fatness of distribution: Large indicates fat tails (whether to upside/downside or neutral depends on skew). P-value indicates the significance of excess kurtosis with respect to kurtosis equals 3 of Normal distribution.

Standard Deviation of returns below mean of excess returns with respect to risk-free rate. To be compared with plain volatility can shown asymmetry in returns and is supplementary to skewness. Remark: Whereas volatility may also discriminate upside risk, downside volatility exclusively measures downside risk.

Worst possible loss from investing at highest level and selling at subsequent lowest level. Peak is start date for decline. Trough is date of highest loss. Recovery is the time until prior peak was reached again.

Monthly volatility (stdev) of absolute returns multiplied by sqrt(12). Basic risk measure for fluctuation of returns. Does not distinguish between upside and downside risk.

Glossary I

Absolute Performance Measures

Jensen Alpha(mthly, i.e. intercept)

=0.7%

Market Beta(i.e. Slope)=0.75

-10%

-5%

0%

5%

10%

15%

-10% -8% -6% -4% -2% 0% 2% 4% 6% 8%

JP O

meg

a St

rate

gy E

xces

s Ret

urn

vers

us

Risk

free

Rat

e

Equally Weighted HFRI Indices Excess versus Riskfree Rate

Market Model

7. Sharpe:

8. Sortino:

9. Calmar:

10. Treynor:

11. Information:

12. JP Gain vs Loss:

13. JP Omega:

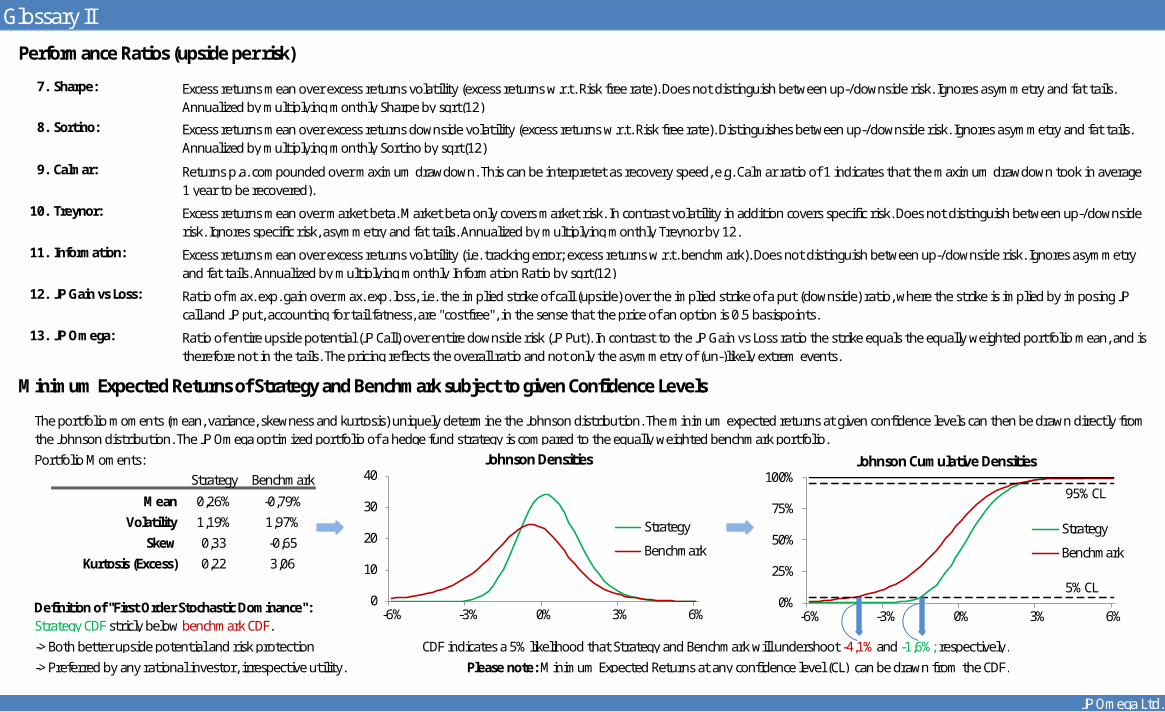

Portfolio Moments:Strategy Benchmark

Mean 0,26% -0,79%

Volatility 1,19% 1,97%

Skew 0,33 -0,65

Kurtosis (Excess) 0,22 3,06

-> Both better upside potential and risk protection.

-> Preferred by any rational investor, irrespective utility.

JP Omega Ltd.

Definition of "First Order Stochastic Dominance": Strategy CDF stricly below benchmark CDF.

Please note: Minimum Expected Returns at any confidence level (CL) can be drawn from the CDF.

Glossary II

Minimum Expected Returns of Strategy and Benchmark subject to given Confidence Levels

Performance Ratios (upside per risk)

Excess returns mean over excess returns volatility (excess returns w.r.t. Risk free rate). Does not distinguish between up-/downside risk. Ignores asymmetry and fat tails. Annualized by multiplying monthly Sharpe by sqrt(12)

Excess returns mean over excess returns downside volatility (excess returns w.r.t. Risk free rate). Distinguishes between up-/downside risk. Ignores asymmetry and fat tails. Annualized by multiplying monthly Sortino by sqrt(12)

The portfolio moments (mean, variance, skewness and kurtosis) uniquely determine the Johnson distribution. The minimum expected returns at given confidence levels can then be drawn directly from the Johnson distribution. The JP Omega optimized portfolio of a hedge fund strategy is compared to the equally weighted benchmark portfolio.

Returns p.a. compounded over maximum drawdown. This can be interpretet as recovery speed, e.g. Calmar ratio of 1 indicates that the maximum drawdown took in average 1 year to be recovered).

Excess returns mean over market beta. Market beta only covers market risk. In contrast volatility in addition covers specific risk. Does not distinguish between up-/downside risk. Ignores specific risk, asymmetry and fat tails. Annualized by multiplying monthly Treynor by 12.

Excess returns mean over excess returns volatility (i.e. tracking error; excess returns w.r.t. benchmark). Does not distinguish between up-/downside risk. Ignores asymmetry and fat tails. Annualized by multiplying monthly Information Ratio by sqrt(12)

Ratio of max. exp. gain over max. exp. loss, i.e. the implied strike of call (upside) over the implied strike of a put (downside) ratio, where the strike is implied by imposing JP call and JP put, accounting for tail fatness, are "costfree", in the sense that the price of an option is 0.5 basispoints.

Ratio of entire upside potential (JP Call) over entire downside risk (JP Put). In contrast to the JP Gain vs Loss ratio the strike equals the equally weighted portfolio mean, and is therefore not in the tails. The pricing reflects the overall ratio and not only the asymmetry of (un-)likely extrem events.

CDF indicates a 5% likelihood that Strategy and Benchmark will undershoot -4,1% and -1,6%; respectively.

5% CL

95% CL

0%

25%

50%

75%

100%

-6% -3% 0% 3% 6%

Johnson Cumulative Densities

Strategy

Benchmark

0

10

20

30

40

-6% -3% 0% 3% 6%

Johnson Densities

Strategy

Benchmark