jpm research: samsung's supply chain (4 mar)

TRANSCRIPT

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 1/55www.jpmorganmarkets.c

Asia Pacific Equity Research04 March 2013

Tech Supply Chain 101 (SEC)Samsung supply chains: Finding winning sub-sectorsand companies

Technology - Semiconductors

JJ Park AC

(822) 758-5717

J.P. Morgan Securities (Far East) Ltd, SeoBranch

Jay Kwon AC

(82-2) 758-5725

J.P. Morgan Securities (Far East) Ltd, SeoBranch

Masashi Itaya AC

(81-3) 6736 8633

JPMorgan Securities Japan Co., Ltd.

Helaine Kang AC

(82-2) 758- 5712

J.P. Morgan Securities (Far East) Ltd, SeoBranch

Yumi Tanaka AC

(81-3) 6736-8603

JPMorgan Securities Japan Co., Ltd.

See page 52 for analyst certification and important disclosures, including non-US analyst disclosures.J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that tfirm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factormaking their investment decision.

Given Samsung Electronics’ Galaxy S4 launch on March 14th and a series of upcoming tablet PCs, we analyze SEC’s handset/tablet supply chains to

illustrate: (1) supplier relationships between Samsung and major component

makers across smartphones and tablets; (2) supply chains’ financial and stock performance over the years to find winning sectors and companies; (3) finding

the biggest beneficiaries from the upcoming flagship models; and (4) summary of meeting notes with key supply chain names.

Qualitative findings from Samsung supply chain: Given the fast moving product cycle and diversified product mix, SEC prefers local suppliers with prompt response while it is still heavily dependent on Japan componentmakers for high-end components. Hence, SEC tries to maintain long-term

relationships with qualified component suppliers for the timely launch of new products in the market. These qualified names enjoy higher margins,more volumes and receive priority information.

Winners and losers in supply chain heat map: Touch panel, PCB,Electronic components have outperformed Electronic materials and SPE onstrong revenue growth and margin expansion. Like the trend seen in big capnames, we find the trend of “bigger getting stronger” for even SMid namessince downstream companies are also investing in R&D and capacityexpansion to hold their ground in the marketplace. Hence, we recommendinvestors stay with tier 1 names in the respective components.

Component value change in Galaxy S4: We expect ASP for screens toincrease and upgrades in camera modules along with increasing adoption of LTE to benefit related supply chains such as SEC, SEMCO, and Patron.We also recommend SDI and rechargeable battery related component

names on increasing battery capacity.

Tablet opportunity for key vendors: Given the significant growthopportunity in SEC’s tablet PC, we expect touch panel, casing makers, andPCB makers to benefit from meaningful growth in tablets, assuming thesame volume provides larger screen, bigger form-factor and substrate in the

products. Casing players like Intops and KH Vatec and touch panel makersclaim to enjoy higher ASP and margin upon size migration.

Implications for Japan component makers: Since Japanese componentmanufacturers have a high share in markets for high-frequency components,

board connectors, and optical films, major Japanese component supplierscould benefit considerably from SEC's growing share in worldwidesmartphone and tablet markets. Those names include Wacom (which has anexclusive deal to supply styli), Murata, Hirose Electric, and Nitto Denko.

Asia Pacific

Technology

Research

SEC supply chain YTD performanceYTD performance (%)

Source: Bloomberg

60

30%

29%

26%

24%

20%

10%

-2%

-7%

-9%

-30% -10% 10% 30% 50% 70%

Wacom

Nitto

Partron

KH Vatec

Murata

Intops

Hirose

SEC

SEMCO

SSDI

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 2/55

2

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Table of Contents

Executive Summary .................................................................3Section I: Who does what?......................................................4

Mobile device (handset) ............ ............. .............. ............. ............. ............. ............4

Mobile device (Tablet) ............ ............. ............. .............. ............. ............. ............. .6

Qualitative findings from Samsung supply chain......................................................8

Korea Tech – Small Cap DB constituents ................................................................9

Section II: Supply Chain Heat Map........................................10

Sub-sector performance comparison ............ ............. ............. ............. .............. .....10

Section III: Finding winners within the sub-sectors ............15

Electronic components sector ................................................................................15

PCB sector............................................................................................................17Electronic Materials sector ....................................................................................18

SPE sector.............................................................................................................20

Touch Panel..........................................................................................................21

Section IV: Where is the market heading? ...........................24

Samsung vs. Sub-sectors ............. .............. ............. ............. ............. ............. ........25

Section V: Implication from potential component valuechanges in next Galaxy S-series...........................................28

Galaxy series shipment momentum vs. Market Cap analysis ............. ............. ........29

Section VI: Implications to Japan component makers........31

Section VII: Meeting Note Summary .....................................33Duksan Hi-Metal (NC, 077360.KQ) ............ ............. ............. ............. .............. .....34

Duksan Hi-Metal: Summary of Financials.........................................35

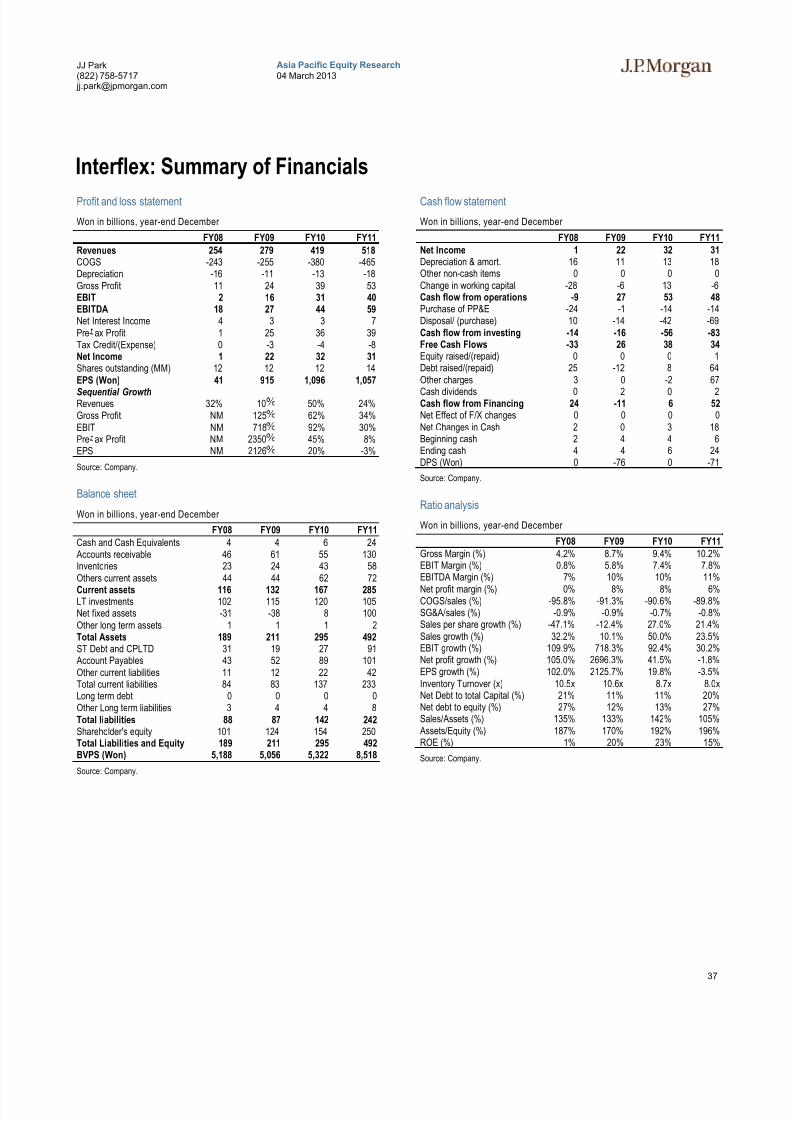

Interflex (NC, 051370.KQ)................... ............. .............. ............. ............. ............ 36

Interflex: Summary of Financials ....................................................37

Partron (NC, 091700.KQ)....................... .............. ............. ............. ............. ..........38

Partron: Summary of Financials .....................................................39

KH Vatec (NC, 060720.KQ) .................................................................................40

KH Vatec: Summary of Financials...................................................41

SFA Engineering (NC, 056190.KS)........ .............. ............. ............. ............. ..........42

SFA Engineering: Summary of Financials ........................................43

AP Systems (NC, 054620.KQ)..............................................................................44

Asia Pacific Systems: Summary of Financials ..................................45

Iljin Display (NC, 020760.KS) ............. ............. .............. ............. ............. ............ 46

Iljin Display: Summary of Financials ...............................................47

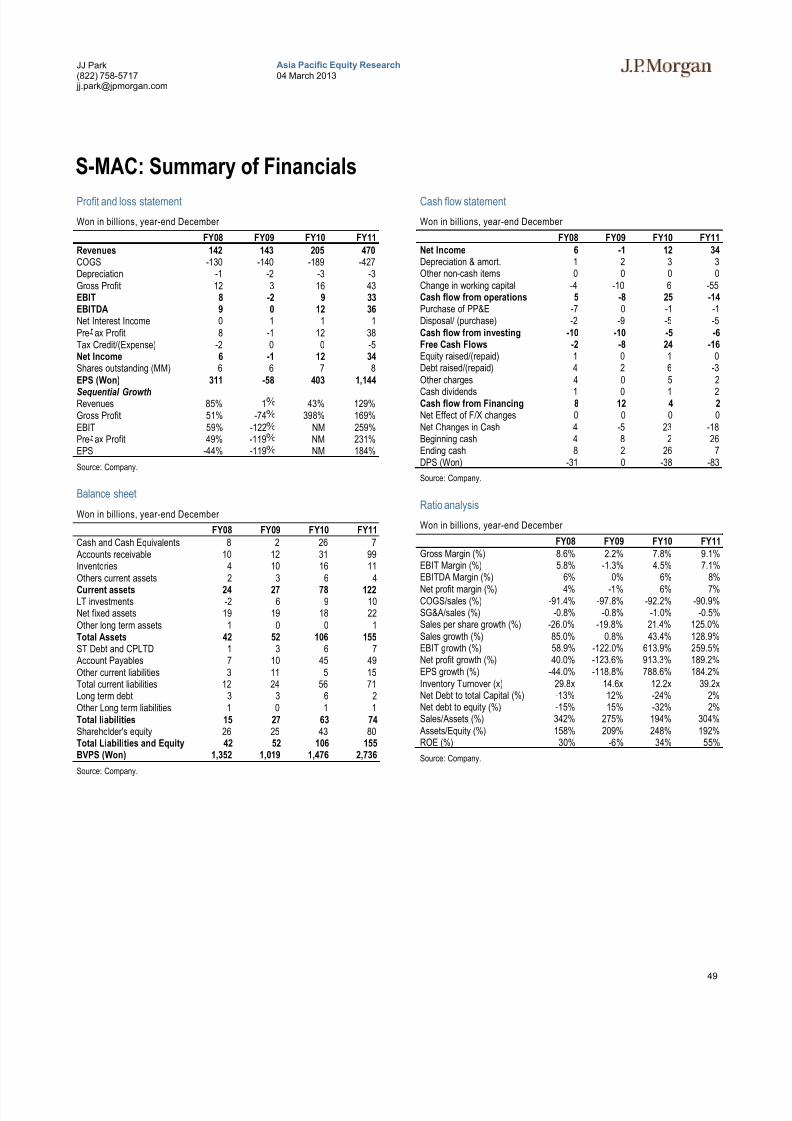

S-MAC (NC, 097780.KQ).....................................................................................48

S-MAC: Summary of Financials ......................................................49

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 3/55

3

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Executive Summary

This is our first intensive report on “Tech supply chain 101 – Samsung supply

chain” and herein we illustrate: (1) Supplier relationships between Samsung and

supply chains across smartphones and tablets; (2) Supply chains’ financial and

share performance over the years to analyze key winning sectors; (3) JPM’s view

and implication on sub-sectors for upcoming new flagship series as well as a

comparison between Samsung and supply chain sub-sectors; and (4) Meeting notes

summary with supply chain companies. We expect this detailed handbook report to

help investors capture key changes and upcoming key trends in Samsung’s supply

chain. As some companies have not disclosed their 4Q12 performance yet, actual financial numbers may change from the one in the report.

Supply chain at a glance

We categorize SEC’s key supply chains in five sub-sectors: (1) Electronic materials,(2) PCB, (3) Electronic components, (4) Touch panels, and (5) SPE. We conduct ananalysis of financial performance, share price performance, and their relative positionin various matrix. Finally, we identify key growth drivers for each sub-sector to findrelative performance to other sub-sectors. Accordingly, we try to provideimplications from component value changes in the next Galaxy S-series (Galaxy S4and Note3) to find winning sub-sectors.

Tablet PC opportunity

As most suppliers in tablet PC overlap and we expect SEC's tablet shipmentmomentum to accelerate, we believe touch panel, casing makers, and PCB makerswill benefit more from strong growth in tablets, assuming the same volume provideslarger screen, bigger form-factor and substrate in the products in terms of top-line

and earnings. In terms of SEC’s Galaxy-series shipment momentum vs. market captrend, touch panel has stronger correlation with tablet PC shipment momentum.

Beneficiaries: Sectors and companies

Increasing value of display continues to benefit Samsung Display (SDC) and OLEDrelated material players– Duksan Hi-Metal and potentially Cheil Industries.Casing players (KH Vatec and Intops) could benefit as larger device form-factor usually incurs higher ASP and better margin (especially for tablet PCs). PCB players(Interflex and Flexcom) will likely benefit as set makers require slimmer substrateand even flexible substrate.

With upgrades in camera modules, SEMCO could be the main supplier along withfront camera suppliers such as Partron, Jawha and Power Logics. Also, emergence

of diverse functional antenna would benefit Partron and Amotech. Finally,Samsung SDI remains the largest battery supplier for SEC's mobile devices.

In Japan, Wacom which has an exclusive deal to supply styli, and Murata, Hirose

Electric and Nitto Denko for high frequency components, board connectors, andoptical films. Also, Ibiden could benefit given SEC is using layer printed circuit

boards for its Galaxy S4.

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 4/55

4

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Section I: Who does what?

Mobile device (handset)

Smartphone supply chain: Qualified suppliers with technology edge benefit

As Korea handset makers increase their presence in the smartphone market, keycomponent suppliers from Samsung group (e.g. SEC, Samsung SDI, SEMCO), andnon-Samsung suppliers— Patron (091700 KQ, NC; camera module), Iljin Display

(035720 KQ, NC; Touch panel makers), Intops & KH Vatec (casing players), andother related supply chain would benefit. In this section, we lay out the supplier relationship for each component. Below is a teardown picture of SEC's key flagshipsmartphone–Galaxy Note II.

Figure 1: Smartphone Teardown Figure by components (Samsung Galaxy Note II)

Source: Company data, J.P. Morgan

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 5/55

5

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Major components are internally supplied across Samsung supply chain

As is well known in the market, key smartphone components (i.e. AP, OLED panel,

mDRAM, MLCC, Camera, and Battery) are supplied by SEC or Samsung groupaffiliates. A large number of chipset components (i.e. baseband, model and network chipset, and sensor components) were supplied externally, however, Samsung hasrecently begun to adopt internally developed components (baseband and modelchipset for new flagship smartphones). According to our BOM cost analysis, totalBOM + manufacturing cost is slightly above $250, which accounts for ~45% of Galaxy S III's retailer price ($550 w/o lock-up discount).

Table 1: Smartphone supplier relationship table (Samsung smartphone)

Components Galaxy S III Detailed Components Supplier Rev. Exposure (FY12)

Memory 30.0NAND Flash 17.4 NAND (Internal Memory) SEC SEC (6%)DRAM 12.6 mobile DRAM SEC SEC (4%)Display & Touch Screen 51.5 OLED panel SDC SDC small mobile (+60%)Display 37.5 OLED material SDC, Duksan hi-metal, Doosan, UDC Duksan (~85%), Doosan (<1%)

LCD panel SDC SDC small mobile (~40%)Mobile BLU SDC, E-litecom SDC small mobile (~40%), E-litecom (~50%)

Touch Screen 14.0 Touch Panel module Iljin Display, S-MAC, Melfas, ELK Iljin (95%), S-MAC (95%), Melfas (85 )Touch Panel sensor Melfas Melfas (85%)Driver IC SDC, Siliconworks Siliconworks (<5%)

Processor 25.3 Application Processor SEC, Qualcomm SEC (2%), Qualcomm (18%)MLCC SEMCO SEMCO (~20%)

Camera(s) 19.6 Camera module SEMCO, Partron SEMCO (~25%), Partron (~80%)Image sensor/components SEC / Sony / Jahwa Elec Jahwa Elec (100%)Camera lens SonyProximity Sensor SEC

Wireless section - 38.0 Baseband chip Qualcomm, Intel, SEC Intel (<1%), Qualcomm (18%)BB/RF/PA Radio Frequency chip Partron Partron (~80%)

Power Amplifier chip SkyworksLTE, HSPA, Modem Chip Qualcomm, SEC Qualcomm (18%)

User Interface & Sensors 6.9 Accelerometer ST Micro ST Micro (~10%)

Gyroscope ST Micro ST Micro (~10%)Pressure sensor Partron Partron (~80%) Audio Interface Wolfson Micro Wolfson Micro (+30%)

WLAN/BT/FM/GPS 6.5 WLAN Broadcom Broadcom (17%)FM transceiver Infineon Infineon (low single %)Bluetooth Broadcom, Murata, Partron, Amotech Partron (~80%), Amotech (~45%)Wi-Fi Broadcom, Murata, Partron Partron (~80%)NFC chipset NXP, Partron, Amotech Partron (~80%), Amotech (~45%)

Power Management 10.0 Power management IC Maxim, TI, Silicon Mitus, Magna ChipBattery 4.5 Battery Pack Samsung SDI Samsung SDI (60%)

Battery Cell Samsung SDI Samsung SDI (60%)Battery Components mater ia l Power Logics, I ljin Mater ials Power Logics (65%), I lj in Mater ia ls (50%)

Mechanical 38.0 PCB / FPCB / FC-CSPDaeduck Electronics, Interflex,Flexcom, Simm Tech, BH

Daeduck (50%), Interflex (+40%), Flexcom(+90%)

/ Electro-mechanical Microphone BSE CM, Partron BSE CM (~70%), Partron (~80%)Speaker receiver BSE CM BSE CM (~70%)

Casing Intops, KH Vatec, Shinyang Intops (~95%), KH Vatec (60%)LCD bracket KH Vatec, Innox KH Vatec (60%)SAW filter Wisol

Box Contents 7.0 Charger RF Tech RF Tech (+40%)BOM Cost 237.1Manufacturing Cost 16.0BOM Cost + Manufact. 253.1Smartphone ASP (US$) 550.0

Source: Gartner, Company data, J.P. Morgan estimates. *Supplier revenue exposure data based on company data. BOM cost based on Galaxy SIII, component supply status based on overall

Samsung smartphone line-ups. Supplier list includes companies above US$ 100mn market cap only. Revenue exposure (%) stands for total Samsung Electronics.

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 6/55

6

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Mobile device (Tablet)

Tablet supply chain: Similar to smartphone, but less profitable due to higher

BOM

We expect 2013 would be the turning point for the tablet space as Android andWindow-OS based set makers aggressively penetrate into Apple dominated marketwith various pricing points and product features. Although Tablets do not providehealthy margins to set makers compared to smartphones due to higher BOM cost

burden, Samsung is generating a profit from supplying same components and benefits from cost spread effect upon economies of scale.

Samsung SDI (OW, 006400.KS) is our top preferable supply chain name under our coverage thanks to larger battery capacity. For non-Samsung supply chain names,touch panel makers (Iljin Display, NC; 035720.KS, S-MAC, NC; 097780.KQ, and

ELK, NC; 094190.KQ) could benefit thanks to increasing ASP on larger screen size.Also, cost-driven suppliers like PCB/FPCB players (Interflex, NC; 051370.KQ and

Flexcom, NC; 065270.KQ) could benefit from larger substrate components. Casing

players (Intops, NC; 049070.KQ, KH Vatec, NC; 060720.KQ) also claim to enjoyhigher ASP and margin from increasing tablet PC penetration given sophisticatedmanufacturing processes.

Figure 2: Smartphone Teardown Figure by components (Samsung Galaxy Note 10.1”)

Source: ifixit, Company data, J.P. Morgan

No major change from smartphone suppliers, qualified names continue to stay

A comparison of tablet PC supply chain names with smartphone suppliers indicatesthat they have lots of names in common. Although revenue and earnings contributionfrom tablets may be different from smartphones, we believe proliferation of Samsungtablets in the market should be beneficial for the relevant supply chain. Major components are internally supplied (i.e. AP, mDRAM, MLCC, and Battery). Unlikesmartphones, camera exposure from SEMCO is much smaller given tablets usually

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 7/55

7

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

adopt lower-spec camera module. Moreover, due to higher pricing points and tightsupply, OLED panel adoption into tablet PC is at a premature stage. As battery

consumption becomes a critical point, PMIC component becomes more important(but no domestic players have yet made a notable presence). S-Pen (pen-type inputdevice for tablet PC) has been added to tablet PC recently in addition to Galaxy Notesmartphone series (developed by Wacom and manufactured by SEC). According toour BOM cost analysis, total BOM + manufacturing cost is slightly below $280,which accounts for 56% of Galaxy Note 10.1's retailer price (~$499).

Table 2: Tablet PC supplier relationship table (Samsung Tablet PC)

ComponentsGalaxy

Note 10.1”Detailed Components Supplier Rev. Exposure (FY12)

Memory 30.0NAND Flash 17.4 NAND (Internal Memory) SEC SEC (6%)

DRAM 12.6 mobile DRAM SEC SEC (4%)Display & Touch Screen 100.0 LCD panel SDC SDC small mobile (+60%)Display 60.0 Mobile BLU SDC, E-litecom SDC small mobile (~40%), E-litecom (~50%)Touch Screen 40.0 Touch Panel module Iljin Display, S-MAC, Melfas, ELK Iljin (95%), S-MAC (95%), Melfas (85%)

Touch Panel sensor Melfas Melfas (85%)Driver IC / Controller IC SDC, Siliconworks, Melfas Siliconworks (<5%), Melfas (85%)

Processor 18.8 Application Processor SEC, Qualcomm SEC (2%), Qualcomm (18%)MLCC SEMCO SEMCO (~20%)

Camera(s) 15.0 Camera module Partron, SEMCO SEMCO (~25%), Partron (~80%)Image sensor/components SEC, Sony, Jahwa Elec Jahwa Elec (100%)Camera lens SonyProximity Sensor SEC

User Interface & Sensors 18.0 Accelerometer ST Micro ST Micro (~10%)Gyroscope ST Micro ST Micro (~10%)S-Pen input Wacom, SECPressure sensor Partron Partron (~80%) Audio Interface Wolfson Micro Wolfson Micro (+30%)

WLAN/BT/FM/GPS 15.0 WLAN Broadcom Broadcom (17%)FM transceiver Infineon Infineon (low single %)Bluetooth Broadcom, Murata, Partron, Amotech Partron (~80%), Amotech (~45%)Wi-Fi Broadcom, Murata, Partron Partron (~80%)

Power Management 12.0 Power management IC Maxim, TI, Silicon Mitus, Magna ChipBattery 18.0 Battery Pack Samsung SDI Samsung SDI (60%)

Battery Cell Samsung SDI Samsung SDI (60%)Battery Components mater ia l Power Logics, I ljin Mater ials Power Logics (65%), I lj in Mater ia ls (50%)

Mechanical 35.0 PCB / FPCB / FC-CSPDaeduck Electronics, Interflex,Flexcom, Simm Tech, BH

Daeduck (50%), Interflex (+40%), Flexcom(+90%)

/ Electro-mechanical Microphone BSE CM BSE CM (~70%)Speaker receiver BSE CM BSE CM (~70%)Casing Intops, KH Vatec, Shinyang Intops (~95%), KH Vatec (60%)LCD bracket KH Vatec, Innox KH Vatec (60%)SAW filter Wisol

Box Contents 6.0 Earphone, Charger RF Tech RF Tech (+40%)

BOM cost 267.8Manufacturing Cost 10.0BOM + Manufacturing 277.8

Tablet PC ASP (US$) 499.0

Source: Gartner, Company data, J.P. Morgan estimates. *Supplier revenue exposure data based on company data. BOM cost based on Galaxy Note 10.1”, component supply status based on

overall Samsung tablet PC line-ups. Supplier list includes companies above US$ 100mn market cap only. Revenue exposure (%) stands for total Samsung Electronics.

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 8/55

8

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Qualitative findings from Samsung supply chain

1. Which company continues as the top vendor is a major supply chain concern

Samsung did not disclose its supplier list officially to the public before Galaxy SIII.Although names were not provided, the company provided a hint to the market aboutits supplier guideline. Given the fast moving product life-cycle, it is extremelyimportant for set makers to launch new products in the market in a timely fashion.For example, Galaxy SIII experienced casing yield issues at the beginning of itsglobal launch and the company said it solved the issue within three days. This leadsto a continuous relationship between SEC and qualified suppliers. Hence, qualifiednames (Top Vendors) enjoy higher margins, more volumes and receive priorityinformation, which in turn generates positive feedback from SEC.

2. Localization trend continues. SEC prefers local suppliers with prompt

response

There are many suppliers outside Korean (especially from Japan; material, chipset,

and SPE makers). We believe SEC increased its Korean supplier portion from low-10% in early 2000 to high 20% or more in 2011 and this trend is likely to continue.Recently, as Samsung set up a production site outside Korea (i.e. handset productionat Vietnam and China), many supply chain names have kicked in overseas

production to actively deal with SEC. For instance, casing players (KH Vatec and

Intops) have built majority of capacity overseas and this strategy has workedsuccessfully.

3. Level of product differentiation does matter. Is the supplier dominant enough?

Although highly differentiated products are internally supplied, there are few products in which non-Samsung players maintain a dominant position. For OLEDmaterial (HIL/HTL materials), Duksan Hi-Metal (DSHM) has been the major supplier from the beginning. SEC has put OLED upfront to differentiate it from

competitors, and this strategy has worked successfully. Samsung tried to internalizematerial supply from Cheil Industries, but progress is still at the premature stage. Asa result, DSHM has been enjoying good OPM (~30%) for the last 2 years.

4. Are non-Samsung players ready to embrace in-Samsung supplier position?

Given the shortened product life-cycle, SEC and in-Samsung suppliers are efficientlyrestructuring the supply chain system. Key challenges to non-Samsung suppliers arewhether they are ready to take the empty positions and step up to be a part of theinner-circle. SEC merged with Samsung Hainan Fiberoptics-Korea (SEHF) in Sept-2012 and the merger process was completed by end of Dec-2012. Partron took over SEHF's camera module business in the SEC supply chain and Power Logics / Jahwa

Electronics stepped up to directly supply camera image sensor to SEC's handsetdivision. This is a good example of opportunity pursuit from non-Samsung supplychains and we are likely to see more such cases going forward as SEC continues totry outsourcing less profitable components to external parties and focus on corecomponents.

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 9/55

9

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Korea Tech – Small Cap DB constituents

Table 3: Korea SMid-cap Tech list

Company List with sub-sector Ticker Company List with sub-sector Ticker

Small caps - Electronics Components Small caps - SPEPartron 091700 KQ SFA Engineering 056190 KSJahwa Electronics 033240 KS Nepes 033640 KQSekonix 053450 KQ ICD 040910 KQFoosung 093370 KS AP System 054620 KQIljin Materials 020150 KS Jusung Engineering 036930 KSIntops 049070 KQ SNU Precision 080000 KSKH Vatec 060720 KQ Soulbrain 036830 KQShinyang Engineering 086830 KQ Wonik IPS 030530 KQInnochip Technology 080420 KQ Small caps - Touch PanelWisol 122990 KQ Iljin Display 020760 KS

RFSemi Technologies 096610 KQ S-MAC 097780 KQE-litecom 041520 KQ Melfas 096640.KQBSE CM 045970 KQ ELK 094190 KQ

Crucial Tech 114120 KQ Small caps - Others

Small caps - PCB Silicon Works 108320 KSDaeduck Electronics 008060 KS Anapass 123860 KQInterflex 051370 KQ Power Logics 047310 KQFlexcom 065270 KQ DnF solution 092070 KQSimmTech 036710 KQ Infraware 041020 KQKorea Circuit 007810 KS Barun Electronics 064520 KQBH 090460 KQ ABCO Electronics 036010 KQSmall caps - Electronics Material Sangsin EDP 091580 KQDuksan Himetal 077360 KQ Lumens 038060 KSI-Component 059100 KQ Sapphire Technology 123260 KSSangbo 027580 KQ Od-Tech 080520 KQInnox 088390 KQ Kumho Electric 001210 KS

Source: J.P. Morgan

Table 4: Korea SMid-cap tech supply chain - Asia peer list

Ticker Company Taiwan peers Japan peers

056190 KS SFA Engineering Corp Acter/United Integrated Services Tokki (Canon), ULVAC091700 KQ Partron Co Ltd Foxconn/Chicony/Lite-on Sony/Sharp077360 KQ Duksan Hi-Metal Co Ltd Hodogaya, Idemitsu Kosan036830 KQ Soulbrain Co Ltd Sino-American Silicon SUMCO/Shin Etsu/Hitachi Chemical/JSR051370 KQ Interflex Co Ltd Unimicron/Compeq/Tripod Sumitomo batelite/Ibiden/Meiko020760 KS Iljin Display Co Ltd TPK/WintekYoungfast/Jtouch/Jtouch/CMI Alps Electric/Nissha Printing008060 KS Daeduck Electronics Co Unimicron/Compeq/Tripod Sumitomo batelite/Ibiden/Meiko007810 KS Korea Circuit Co Ltd Unimicron/Compeq/Tripod Sumitomo batelite/Ibiden/Meiko033640 KQ NEPES Corp Acter/United Integrated Services Tokki (Canon), ULVAC030530 KQ Wonik IPS Co Ltd Acter/United Integrated Services Tokki (Canon), ULVAC096640.KQ Melfas Inc TPK/WintekYoungfast/Jtouch/Jtouch/CMI Alps Electric/Nissha Printing033240 KS Jahwa Electronics Co Ltd Foxconn/Chicony/Lite-on Sony/Sharp108320 KS Silicon Works Co Ltd Novatek/Realtek/Himax/Orise/Sitronix/Itlitek Renesas

Source: J.P. Morgan

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 10/55

10

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Section II: Supply Chain Heat Map

Sub-sector performance comparison

Share price trend – snapshot of performanceWe note that the electronics material/PCB/electronic components sub-sectors haveoutperformed other sub-sectors in terms of share price performance (Jan 2012 -YTD).The PCB sub-sector's impressive performance can be attributed to increasingcompetitiveness of domestic FPCB makers such as Flexcom, Interflex and Korea

Circuit. In addition, proactive capex investments have increased investor hopes for a better topline and bottomline growth in this sub-sector.

The touch panel sector has been riding the smartphone/tablet growth wave asdemand for touch functionality percolates to feature phones. Moreover, with thelaunch of Windows 8 in October 2012, the touch functionality is now being

increasingly adopted in notebooks. These factors have fueled the growth of domestictouch panel module makers and touch sensor chip providers (Melfas).

The electronics components sector thrived under high demand for ever-increasingimage resolution specs and high pixel modules. SPE's poor run is mainly an indicator of negative investor sentiment on the AMOLED sector owing to delays in investment

by SEC and technological glitches which affected yield. Further, high demand for Innox’s FCCL and EMI films and Duksan’s dominant position in OLED materialsupply has fueled growth in the electronics materials sector.

Figure 3: Sub-sector wise share price performance (Market-capweighted); Jan 2012 – YTDJan 2012 = 100

Source: Bloomberg, J.P. Morgan

Figure 4: Sub-sector wise share price (Market-cap weighted)appreciation; Jan 2012 – YTD% change since Jan,2012

Source: Bloomberg, J.P. Morgan

Financial performance – Supply chain heat-map

In terms of top-line growth, touch panel sectors presented the strongest growth over years especially during 2009-2012 followed by Electronic materials and Electroniccomponents sectors. Margin-wise, the touch panel sector witnessed the highestmargin expansion. PCB sectors' general performance (both in terms of top-linegrowth and margin expansion) was rather muted compared to top two sectors. Wefind that this is mainly due to Interflex whose share performance heavily appreciatedupon serving Apple in addition to Samsung. While the SPE sector was the biggestrevenue generating sub-sector at the beginning of 2007, now an electroniccomponent has taken over its place.

60

80

100

120

140

160

180

Jan-12 Apr-12 Jul-12 Oct-12 Jan-13

Electronics Components PCB Electronics Material

SPE Touch Panel Others

57% 53%

38%

26% 25%

-10%-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Touch Panel PC B Elec components Elec Materials Ot hers (inclLED/Solar)

SPE

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 11/55

11

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Table 5: Korea Tech – Revenue and OP growth, margin trend with top two performing sub-sectors

Revenue/OP in US$ mn, Growth/Margin in %

2007 2008 2009 2010 2011 2012

RevenueElectronic Components 1,236 1,348 1,559 1,972 2,620 3,174PCB 1,206 1,209 1,282 1,762 2,226 2,799

Electronic Materials 156 143 189 323 428 512 SPE 1,049 1,095 956 1,629 2,192 1,783Touch Panel 168 206 353 700 1,161 1,406 Others (incl. LED/Solar) 793 862 1,096 1,568 1,821 1,623

Total 4,608 4,862 5,435 7,955 10,447 11,296

Revenue growth Y/Y Electronic Components 25.1% 9.0% 15.7% 26.5 32.8 21.2

PCB 8.0% 0.3% 6.0% 37.4 26.3 25.8 Electronic Materials 27.1% -8.7% 32.9% 70.6 32.4 19.7 SPE -0.1% 4.4% -12.7% 70.4 34.5 -18.7%Touch Panel 40.5% 22.3% 71.6% 98.6 65.7 21.1

Others (incl. LED/Solar) 9.0% 8.7% 27.1% 43.1 16.1 -10.9%

Total 11.7% 5.5% 11.8% 46.4% 31.3% 8.1%OPElectronic Components 70 40 160 176 197 215 PCB 1 38 85 143 154 198 Electronic Materials 23 16 18 32 61 72 SPE 134 100 76 165 217 140

Touch Panel 18 8 26 73 94 114Others (incl. LED/Solar) 67 74 91 168 93 108

Total 319 305 483 813 799 781

OP Margin

Electronic Components 5.7% 2.9% 10.2% 8.9 7.5 6.8 PCB 0.1% 3.1% 6.6% 8.1 6.9 7.1Electronic Materials 14.4% 11.5% 9.7% 9.9 14.4 14.0 SPE 12.8% 9.2% 7.9% 10.1 9.9 7.8

Touch Panel 10.7% 4.0% 7.4% 10.4 8.1 8.1Others (incl. LED/Solar) 8.5% 8.6% 8.3% 10.7 5.1 6.7

Total 6.8% 5.7% 8.4% 9.5% 7.8% 7.5%OP growth Y/Y Electronic Components -17.9% -43.7% 302.4% 10.3 11.8 9.5 PCB -96.0% 4908.6% 126.6% 68.1 7.7 28.9Electronic Materials 43.0% -27.5% 13.0% 73.1 92.3 16.5

SPE -8.4% -25.4% -24.7% 118.8% 31.1 -35.6%Touch Panel 180.1% -54.8% 222.7% 178.7% 28.9 20.6 Others (incl. LED/Solar) -16.7% 9.7% 23.8% 83.2 -44.2% 15.7

Total -11.5% -12.0% 65.4% 65.9% 7.9% 3.7%

Source: Bloomberg, J.P. Morgan

Revenue growth

The touch panel sector outperformed other sub-sectors with a CAGR of 59% from2009 - 2012. The success of Korean touch module makers hinges on stable

production yields and increasing technological competitiveness. Also, increasing

penetration of tablet-PCs has fueled the growth of this sector.

Electronic components, PCB and electronic materials have registered revenueCAGR of 27%/30%/39% respectively. PCB sub-sector revenue growth has beenresilient from 2009 - 2012, reflecting the ever changing landscape of the smartphoneand tablet-PC market.

SPE sector's revenue dipped in 2012 owing to yield issues while adopting theAMOLED technology for mid-large sized panels. Of note, Samsung's On cellAMOLED panels for its flagship smartphones is developed internally.

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 12/55

12

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Figure 5: Sub-sector wise revenue growthY/Y growth (%)

Source: Bloomberg, J.P. Morgan.

Figure 6: Sub-sector wise revenue growth (CAGR): 2009 – 2012CAGR (%)

Source: Bloomberg, J.P. Morgan

Operating Profit/Operating profit marginIn terms of OP CAGR, we find that touch panel, electronic materials, and PCB arethe top three performing sub-sectors within the Korean Tech supply chain. We findcommonalities across three sub-sectors; highly operating leverage as volume driveneconomies of scale provide margin improvement in longer-term. On the other hand,electronic components, SPE, and other sectors reported poor margin growth.

Figure 7: Sub-sector wise 3 yr OP CAGR (2009-2012)CAGR (%)

Source: Bloomberg, J.P. Morgan.

-40%

-20%

0%

20%

40%

60%

80%

100%

2007 2008 2009 2010 2011 2012

Electronic Components P CB E lectronic M aterials

SPE Touch Panel Others (incl. LED/Solar)

27% 30%39%

23%

59%

14%

0%

20%

40%

60%

80%

100%

ElectronicComponents

PCB ElectronicMaterials

S PE Touc h Panel O th ers (inc l.LED/Solar)

3yr Revenue CAGR (2009-2012)

11%

33%

57%

23%

63%

6%

0%

20%

40%

60%

80%

100%

ElectronicComponents

PCB ElectronicMaterials

SPE Touch Panel Others (incl.LED/Solar)

3yr OP CAGR (2009-2012)

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 13/55

13

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

On an annual OPM basis, FY12 margin remained flattish Y/Y while the electronicmaterial sub-sector outperformed its peer sub-sectors. We find this is largely due to

level of product differentiation as most electronic materials companies appear tohave secured a dominant position in the niche-segment.

Figure 8: Sub-sector wise Annual OPM trendOPM (%)

Source: Bloomberg, J.P. Morgan.

Big fishes becoming even bigger

We note that the market cap of the top 5 companies in the Korean supply chain as a %of the total market cap of all the companies has steadily grown from 2009 to 2012.This theory especially holds true in case of touch panel makers where the degree of vertical integration is crucial. Also, in an environment of changing technologicallandscape, it is important for downstream tech companies to invest in R&D andcapacity expansions in order to hold their ground in the marketplace. We note that

the total contribution of the top 5 companies has steadily increased both in terms of topline and bottomline from 2009 onwards. Like the trend in large cap Asian Technames, we find the trend of big fishes becoming even bigger even among Small Captech names ( Asia-Pacific Tech Database: Finding winning sector and country,

published in Sep. 2012).

Figure 9: Top 5 market cap trendPortion (%)

Source: Bloomberg, J.P. Morgan. *Note: Top 5 Market Cap companies refer toSFA, Partron, DSHM, Soulbrain and Interflex

Figure 10: Korean tech: Top-5 revenue and OP contributionPortion (%)

Source: Bloomberg, J.P. Morgan. *Note: Top 5 Market Cap companies refer toSFA, Partron, DSHM, Soulbrain and Interflex

3%

10%9%

8% 7%

3%

7%8%

7% 7%

11%10% 10%

14% 14%

9%8%

10% 10%8%

4%

7%

10%8% 8%9% 8%

11%

5%7%

0%

5%

10%

15%

20%

2008 2009 2010 2011 2012Electronic Components PCB Electronic MaterialsSPE Touch Panel Others (incl. LED/Solar)

Average

17%15%

21%

25%22%

19%

25% 26%28%

0%

5%

10%

15%

20%

25%

30%

2004 2005 2006 2007 2008 2009 2010 2011 2012

Major Top 5 Market Capitalization % over total Korea Tech small cap

10%

15%

20%

25%

30%

35%

40%

2007 2008 2009 2010 2011 2012

T op 5 r ev en ue c on tr ib ut io n ( %) T op 5 O P c on tr ib ut io n ( %)

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 14/55

14

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

The following table presents the market cap, revenue, OP and OPM for small capcompanies in the Korean tech supply chain, ranked in decreasing order of market cap.

Table 6: Korean tech supply chain (small cap)Market cap, Revenue and OP in USD millions, OPM (%)

Name Market Cap 2012 Rev 2012 OP 2012 OPM

SFA Engineering Corp 975 429 51 12%Partron Co Ltd 843 707 76 11%Duksan Hi-Metal Co Ltd 694 132 38 29%Soulbrain Co Ltd 627 525 88 17%Interflex Co Ltd 581 685 41 6%Iljin Display Co Ltd 555 527 58 11%Daeduck Electronics Co 506 657 49 7%Korea Circuit Co Ltd 373 393 31 8%Foosung Co Ltd 368 199 8 4%NEPES Corp 362 254 35 14%Melfas Inc 341 317 24 8%Wonik IPS Co Ltd 339 225 15 7%

Iljin Materials Co Ltd 333 310 (3) -1%Jahwa Electronics Co Ltd 329 268 28 10%Silicon Works Co Ltd 319 420 42 10%Lumens Co Ltd 312 400 24 6%CrucialTec Co Ltd 271 122 (8) -7%Simm Tech Co Ltd 265 559 40 7%ELK Corp/Korea 264 163 4 2%KH Vatec Co Ltd 264 215 16 7%S-MAC Co Ltd/Korea 260 399 27 7%Flexcom Inc 256 304 21 7%INTOPS Co Ltd 254 494 21 4%Innox Corp 219 126 19 15%Kumho Electric Co Ltd 214 54 5 10%Jusung Engineering Co Ltd 203 68 (52) -77%Infraware Inc 201 39 9 22%Sapphire Technology Co Ltd 198 28 (7) -27%ICD Co Ltd 195 47 2 4%

Sangbo Corp 189 225 15 7%e-LITECOM Co Ltd 183 448 30 7%BH Co Ltd 183 201 16 8%Innochips Technology Inc 174 68 12 18% Asia Pacific Systems Inc 174 197 9 4%Sekonix Co Ltd 157 131 14 11%Power Logics Co Ltd 148 227 5 2%WiSoL Co Ltd 141 76 13 17%ShinYang Engineering Co Ltd 136 97 2 2% Anapass Inc 124 99 11 11%Opto Device Technology Co Ltd 124 83 7 8%SNU Precision Co Ltd 119 39 (8) -20%RFsemi Technologies Inc 95 38 7 18%DNF Co Ltd 82 24 2 9%BSE Holdings Co Ltd 82 2 -0 3%i-Components Co Ltd 64 29 (0) -1%Barun Electronics Co Ltd 52 139 7 5% ABco Electronics Co Ltd 49 30 1 3%Sangsin Energy Display Precisi 40 82 4 4%Total 13,235 11,301 849 8%Source: Bloomberg; J.P. Morgan; Note: The aggregate OPM is calculated on a market-cap weighted basis

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 15/55

15

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Section III: Finding winners within the sub-

sectorsIn the below section, we categorize five sub-sectors, (1) Electronic components; (2)PCB; (3) Electronic materials; (4) SPE; and (5) Touch panel and analyze share pricetrend, financial performance, and key growth drivers of each sub sector.

Electronic components sector

Share performance

Recent share price trend (Jan 2012 – YTD) clearly shows the impressive share price performance of camera module maker Partron and camera component makers suchas Jahwa Electronics and Sekonix. Sekonix has been chosen as a supplier of 13MPcamera lenses for SEC’s flagship smartphone, Galaxy S IV. In addition, Sekonix has

been enjoying healthy production yield on its high-end lens business. Partron

maintains a dominant position in the 3-MP segment and this has translated to higher margins compared to its peers. Casing makers such as Shinyang and Intops alsodelivered a healthy share price appreciation thanks to SEC’s robust smartphonegrowth. Iljin Materials’ share price slump can be attributed to the delayed recoveryof profits in its PCB-elec foil business.

Figure 11: Electronic Components: Share price appreciation: Jan 2012 – YTD% change since Jan, 2012

Source: Bloomberg, J.P. Morgan

Figure 12: Electronic Components: Share price trend: Jan 2012 – YTDJan 2012 = 100

Source: Bloomberg, J.P. Morgan

256%

193%

112% 109% 103%78% 65%

41% 38%9%

-17% -18% -41% -47%-100%-50%

0%50%

100%150%200%250%300%

S h i n Y a n g

S e k o n i x

J a h w a E l e c

P a r t r o n

K H V a t e c

B S E H o l d i n g s

I N T O P S

R F s e m i T e c h

I n n o c h i p s

e - L I T E C O M

C r u c i a l T e c h

W i S o L C o

F o o s u n g

I l j i n M a t e r i a l s

Electronic components index

50

100

150

200

250

300

350

400

Jan-12 Apr-12 Jul-12 Oct-12 Jan-13

Partron Co L td Jahwa Electron ics C o L td ShinYang Engineering Co Ltd

Innochips Technology Inc Sekonix Co Ltd

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 16/55

16

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Financial performanceAs highlighted above, Partron’s dominant position in the 3MP segment has translated

to higher margins compared to its peers. Also, the migration to higher pixels has ledto increase in OP for camera module makers. Iljin materials recorded a slump in itsOP in 2012 on account of its PCB-electric foil business.

Figure 13: Electronic components: Revenue trend 2008 - 2012USD, millions

Source: Bloomberg, J.P. Morgan.

Figure 14: Electronic components: OP trend 2008 – 2012USD, millions

Source: Bloomberg, J.P. Morgan.

Figure 15: Electronic components: Financial snapshot 2007 - 2012Revenue and OP in USD millions; OPM (%)

Source: Bloomberg, J.P. Morgan.

Key growth driversAs smartphone makers are increasingly looking towards adopting hardwaredifferentiation strategies, demand for high pixel modules (8+MP) and enhancedresolution will gain momentum on the back of high-end smartphone launches slatedfor 2Q13. Camera module makers should also benefit from the technology shift fromstandalone cameras to handset cameras. In addition, video calling and other enhancedfeatures such as "motion recognition" should boost the specs for front cameras.

-

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

2008 2009 2010 2011 2012

Partron Jahwa Electronics Sekonix

Iljin Materials Intops E-litecom

-10.0

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2008 2009 2010 2011 2012

Partron Jahwa Electronics Sekonix

Intops Iljin Materials E-litecom

0%

2%

4%

6%

8%

10%

12%

0

500

1,0001,500

2,000

2,500

3,000

3,500

2007 2008 2009 2010 2011 2012

Revenue OP OPM (RHS)

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 17/55

17

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

PCB sector

Share performance

Flexcom, an established supplier of FPCB products to SEC, has been riding thesuccess of SEC's Galaxy Note 10.1 and Galaxy Note 2 after it began supplying itsdigitizer products, for use in these models, in 3Q12. Of note, Korea Circuit owns32% stake in Interflex, which is Korea's top FPCB maker. BH's share price ralliedduring Jan 2012-YTD owing to its capacity expansion in 2012 which is expected to

boost its bottomline.

Figure 16: PCB: Share price appreciation: Jan 2012 – YTDChange since Jan, 2012 (%)

Source: Bloomberg, J.P. Morgan.

Figure 17: PCB: Share price Trend: 2008 - 2012Jan 2012 = 100

Source: Bloomberg, J.P. Morgan.

Financial performance

The PCB sector enjoyed a healthy growth during 2009 - 2010, both in terms of OPMand revenue. However, the growth appears to have slowed down during 2010 – 2012.Korea Circuit has enjoyed higher operating margins, thanks to stable production

yields for PCB, and it is gaining increasing competitiveness in the PCB domain. Of note, Simm Tech’s revenue and OP both declined in 2012.

Figure 18: PCB: Financial snapshot: 2007 – 2012Revenue and OP in USD millions; OPM (%)

Source: Bloomberg, J.P. Morgan

179%

158%

104%

20%

-6%

-27%-50%

0%

50%

100%

150%

200%

Flexcom Korea Circuit BH Co Ltd Interflex Daeduck Simm Tech

PCB sector index

50

100

150

200

250

300

Jan-12 Apr-12 Jul-12 Oct-12 Jan-13

Daeduck Electronics Co Interflex Co Ltd Flexcom Inc

Simm Tech Co Ltd Korea Circuit Co Ltd BH Co Ltd

0%

1%2%3%4%5%6%7%8%9%

0

500

1,000

1,500

2,000

2,500

3,000

2007 2008 2009 2010 2011 2012

Revenue OP OPM (RHS)

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 18/55

18

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Figure 19: PCB: Revenue trend: 2008 – 2012USD millions

Source: Bloomberg, J.P. Morgan.

Figure 20: PCB: OP trend: 2008 – 2012USD millions

Source: Bloomberg, J.P. Morgan.

Key growth drivers

Migration towards slimmer and lighter mobile devices will continue to boost thePCB sector (high-density wiring). We expect demand for FPCB will grow in linewith the smartphone and tablet-market growth as FPCB links the smartphone/tabletcomponents to the main substrate. On an average, around five FPCBs are used per handset and around 10 FPCBs are used per tablet-PC. FPCB sector is largelyimpacted by economies of scale and yield. Higher economies of scale and high yieldtranslate to higher margins. Increase in capacity expansion spending is also a keydriver for this sector.

Electronic Materials sector

Share performanceThe tepid performance of Duksan Hi-Metal is primarily due to negative investor sentiment owing to delays in AMOLED TV launches, uncertainties in facilityinvestment and doubts regarding marketability of AMOLED panels. As panel makersfocus on producing large sized panels, the demand for multi-functional sheets(protection + prism) developed by Sangbo is gaining momentum, which hastranslated to positive share price movement. Further, high demand for Innox’s EMIfilms and flexible copper clad laminate (FCCL) films has fueled its growth.

-

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

2008 2009 2010 2011 2012

Daeduck Electronics Interflex Flexcom

SimmTech Korea Circuit BH

-20.0

-

20.0

40.0

60.0

80.0

2008 2009 2010 2011 2012

Daeduck Electronics Interflex

Flexcom SimmTech

Korea Circuit BH

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 19/55

19

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Figure 21: Electronic Materials: Share price appreciation: Jan 2012 – YTD% change since, Jan 2012

Source: Bloomberg, J.P. Morgan.

Figure 22: Electronic Materials: Share price rend: Jan 2012 – YTDJan 2012 = 100

Source: Bloomberg, J.P. Morgan.

Financial performance

We note that revenue growth of this sector has slowed in recent years. Primaryreason for Duksan’s muted response in 2011-12 was the delay in OLED investment

by SEC. However, both Innox and Sangbo have posted increasing revenue and OP inrecent years.

Figure 23: Electronic Materials: Revenue trend: 2008 – 2012USD millions

Source: Bloomberg, J.P. Morgan.

Figure 24: Electronic Materials: OP trend: 2008 – 2012USD millions

Source: Bloomberg, J.P. Morgan.

Figure 25: Electronic Materials: Financial performance: 2007-2012Revenue and OP in USD millions, OPM (%)

Source: Bloomberg, J.P. Morgan

49%

40%

-5%

-23%-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Innox Sangbo D uksan Hi Metal i-Component

Electronic materials index

40

60

80

100

120

140

160

Jan-12 Apr-12 Jul-12 Oct-12 Jan-13

Duksan Hi-Met al Co Ltd i-Com ponents Co Ltd

Sangbo Corp Innox Corp

-

50.0

100.0

150.0

200.0

250.0

2008 2009 2010 2011 2012

Duksan Himetal I-Component Sangbo Innox

-5.0

-

5.0

10.015.0

20.0

25.0

30.0

35.0

40.0

45.0

2008 2009 2010 2011 2012

Duksan Himetal I-Component Sangbo Innox

0%

2%

4%

6%

8%10%

12%

14%

16%

0

100

200

300400

500

600

2007 2008 2009 2010 2011 2012

Revenue OP OPM (RHS)

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 20/55

20

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Key growth driversStronger AMOLED panel demand fueled by strong sales of SEC's AMOLED

smartphones and technological development to enable economical shift to AMOLED panels in tablet-PCs, monitors and TVs should be key growth drivers for companiessuch as Duksan Hi-Metal and SFA Engineering. Continued focus on lighter,smaller and multi-functional mobile devices should be a key driver for Innox'ssmartflex division. Success of Sangbo's CNT (carbon nanotube) transparentelectrode film could be a key swing factor.

SPE sector

Share performanceNEPES share prices tumbled starting in 3Q12 on account of negative investor sentiment based on speculation that Apple will diversify its AP chips procurementfrom SEC to include TSMC. Overhang concerns dragged on Soulbrain’s share price

performance in 2012. Share price performances of SFA, AP Systems, SNU and ICD

were all impacted due to negative investor outlook on the AMOLED sector.

Figure 26: SPE: Share price appreciation: Jan 2012 – YTD% change since Jan 2012

Source: Bloomberg, J.P. Morgan.

Figure 27: SPE: Share price rend: Jan 2012 – YTDJan 2012 = 100

Source: Bloomberg; J.P. Morgan

Financial performance

We note a decline in the revenue and OP, primarily on account of delay in OLEDinvestment by SEC. Further, yield issues with adopting OLED technology to mid-large sized panels has led to a further squeeze in OPM. Of note, NEPES has postedan increase in revenue and OP on the back of growth in smartphone shipments fromcustomers using SEC foundries.

9%

0%

-6%

-36%-42%

-49% -50% -50%-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

NEPES Soulbrain SFA Engg AP Sys tem SNUPrecision

ICD Co Ltd JusungEngg

Wonik IPS

SPE sector index

20

40

60

80

100

120

140

Jan-12 Apr-12 Jul-12 Oct-12 Jan-13

SFA Engineering Corp NEPES CorpICD Co Ltd Asia Pacific Systems Inc

SNU Precision CoLtd Soulbrain Co Ltd

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 21/55

21

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Figure 28: SPE: Financial performance: 2007 – 2012Revenue and OP in USD millions, OPM (%)

Source: Bloomberg, J.P. Morgan

Figure 29: SPE: Revenue trend: 2008 – 2012

USD millions

Source: Bloomberg, J.P. Morgan

Figure 30: SPE: OP Trend: 2008 – 2012

USD millions

Source: Bloomberg, J.P. Morgan

Key growth drivers:SPE sector should benefit from technological development that will enable usage of AMOLED panels in tablet PCs, monitors and TVs in an economical way. Order momentum from panel makers should boost the topline for this sector. In addition,rapid growth of the tablet PC market should help packaging firms such as NEPES.

Touch Panel

Share performance

The leading names in the Korean touch panel sector, except Melfas, have all performed well as can be seen from the share price appreciation from Jan 2012 – YTD.

0%

2%

4%

6%

8%

10%

12%

14%

0

500

1,000

1,500

2,000

2,500

2007 2008 2009 2010 2011 2012

Revenue OP OPM (RHS)

-

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

2008 2009 2010 2011 2012

SFA Engineering Nepes ICD

AP System SNU Precision Soulbrain

-20.0

-

20.0

40.0

60.0

80.0

100.0

2008 2009 2010 2011 2012

SFA Engineering Nepes ICD

AP System SNU Precision Soulbrain

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 22/55

22

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Figure 31: Touch panel: Share price appreciation: Jan 2012 – YTDChange since Jan, 2012 (%)

Source: Bloomberg, J.P. Morgan.

Figure 32: Touch panel: Share price rend: Jan 2012 – YTDJan 2012 = 100

Source: Bloomberg, J.P. Morgan.

Financial performance

The touch panel sector has posted solid top line and bottom line growth on increasingsmartphone and tablet shipments. Key beneficiaries of SEC's growth in handset andtablet PC markets have been Iljin Display, S-MAC and Melfas. Note that, IljinDisplay, whose production yield is stable and high, has outperformed others in thissector.

Figure 33: Touch panel sector: Financial performance (2007-2012)Revenue and OP in millions, OPM (%)

Source: Bloomberg

Figure 34: Touch panel: Revenue trend: 2008 - 2012USD millions

Source: Bloomberg

Figure 35: Touch panel: OP trend: 2008 – 2012USD millions

Source: Bloomberg

80% 80%

49%

-22%-40%

-20%

0%

20%

40%

60%

80%

100%

S-MAC Iljin Display Elk Corp Melfas

ouch panel sector index

50

70

90

110

130

150

170

190

210

Jan-12 Apr-12 Jul-12 Oct-12 Jan-13

Iljin Display Co Ltd S-MAC Co Ltd/Korea

Melfas Inc ELK Corp/Korea

0%

2%

4%

6%

8%

10%

12%

0

200

400600

800

1,000

1,200

1,400

1,600

2007 2008 2009 2010 2011 2012

Revenue OP OPM (RHS)

-

100.0

200.0

300.0

400.0

500.0

600.0

2008 2009 2010 2011 2012

Iljin Display S-MAC Melfas ELK

-10.0

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

2008 2009 2010 2011 2012

Iljin Display S-MAC Melfas ELK

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 23/55

23

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Key growth driversRising smartphone/tablet shipments and increased touch screen adoption in feature

phones remains the top growth driver. In addition, with the launch of Windows 8,touch screen notebooks are likely to become an attractive option for consumers,though the market for touch screen notebooks is still in its infancy. The key growthfactors for companies in this sector are the ability to adapt to new technologies,stable (high) yield and the degree of vertical integration. Given the tight supply of ITO film, established players, with stable production yields, such Iljin Display,Melfas and S-Mac should continue to bag more orders from SEC as SEC seeks todiversify its touch panel suppliers to prepare for potential demand increases in 2013.

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 24/55

24

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Section IV: Where is the market heading?

To identify opportunities and challenges in sub-sectors, we conducted a comparisonanalysis vs. SEC from the past and project which respective sectors will benefit

based on our current estimate. Also, we provide which data points to follow in near-

term to identify direction of share performance.

Smartphone continues to post strong growth into 2013

According to JPM Tech team’s estimates, global smartphone market is expected toreach 922M units in 2013 posting 37% Y/Y growth followed by another amplegrowth of 17% Y/Y to 1.8 billion units in 2014. We expect SEC’s penetration intosmartphone in terms of unit shipment would be faster than market penetration. SEC'ssmartphone business is projected to post 40% Y/Y growth in 2013 to 301M followed

by 27% Y/Y growth in 2014.

Figure 36: Global handset shipment breakdown and penetrationtrendUnit millions, %

Source: IDC, Company data, J.P. Morgan estimates

Figure 37: SEC – Handset shipment breakdown and penetrationtrendUnit millions, %

Source: Company data, J.P. Morgan estimates

Robust earnings driven by strong smartphone business upon flagship models

SEC’s handset business earnings have improved significantly in 2012 achieving 21%operating margin vs 15% in 2011. We maintain a positive stance on SEC’s handset

business thanks to its momentum in high-end flagship models and full line-upstrategy serving low-to-mid segment as well.

Figure 38: Samsung Electronics – Handset revenue and margin trendWon billions, OPM (%)

Source: Company data, J.P. Morgan estimates

763949 1,086 1,201 1,177 1,318 1,309

1,066834 720

5480

123155 172

299 473671

922 1,079

7% 8% 10% 11% 13%18%

27%

39%

52%

60%

0%

10%

20%

30%

40%

50%

60%

70%

0200400600800

1,0001,2001,4001,6001,8002,000

2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E

Global - Fe ature phone Global - S martp ho ne Sm artphon e penetration

103 118161 197 222 256 234

186130

42

- --

-6

24 98 214 301382

0% 0% 0% 0% 2%9%

30%

54%

70%

90%

0%10%

20%

30%

40%

50%

60%70%

80%

90%

100%

050

100

150

200

250

300350

400

450

500

2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E

SEC - Feature phone SEC - Smartphone Smartphone penetration

13%10%

11%9%

11% 11%

15%

21% 21% 20%

0%

5%

10%

15%

20%

25%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2005 2006 2007 2008 2009 2010 2011 2012 2013E 2 014E

Revenue OPM

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 25/55

25

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Tablet: The growth driver for SEC’s handset division onward

As highlighted in our SEC tablet report ( “New growth engine for SEC and key

supply chains on 01 November, 2013" ), we expect its shipment momentum toaccelerate this year to 43M (+143% Y/Y growth, Y% M/S of global tablet marketdemand) followed by another growth into 2014E (64M, 50+% Y/Y growth). During2012, tablet revenue only contributed 9% of total handset revenue, but we expect its

portion to increase up to 16% by 2014. In terms of margin, we estimate tablet togenerate high-single digit margin in 2013.

Figure 39: SEC tablet revenue and tablet shipment trendWon billions, Unit millions

Source: Company data, J.P. Morgan estimates

Figure 40: SEC tablet revenue and % of total handset sales trendWon billions, % of total revenue

Source: Company data, J.P. Morgan estimates

Samsung vs. Sub-sectors

We note an inverse correlation between SEC’s handset division’s OPM and Koreantech's top 5 companies' OPM. This is expected, since the top 5 companies have ahealthy revenue exposure to SEC. Another key point to note here is that the averageOPM (total OP/total sales) for the top 5 companies in the Korean SMid-cap techsupply chain outperforms the average OPM for the entire supply chain.

Figure 41: SEC handset OPM v/s Korean SMid-cap tech OPMOPM (%)

Source: Bloomberg

26

17

43

64

-

10

20

30

40

50

60

70

0

5,000

10,000

15,000

20,000

25,000

2010 2011 2012 2013E 2014E

S EC t ab le t r ev en ue S EC ta bl et s hi pm en t [ RHS]

3%

6%

9%

14%16%

0%

2%

4%

6%8%

10%

12%

14%

16%

18%

0

5,000

10,000

15,000

20,000

25,000

2010 2011 2012 2013E 2014E

S EC t ab le t r ev en ue T ab le t r ev en ue % of to ta l ha nd set [ RHS]

0%

5%

10%

15%

20%

25%

2005 2006 2007 2008 2009 2010 2011 2012

SEC Handset OPM Top 5 OPM Korean Tech OPM

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 26/55

26

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Margin trendTouch panel and PCB sub-sectors usually incur high fixed costs and hence their

operating margins are more sensitive to sales compared to other sub-sectors.Again, we note here that the operating margins of the SPE sub-sector dipped inthe last two years as the companies within the sector faced increasing cost

pressure to come up with a viable AM-OLED solution amid fluctuating yields.

Figure 42: SEC handset operating margin vs. margin by sub-sectorsOPM (%)

Source: Company data, Bloomberg actual data for sub-sectors. *Note: Actual FY12 sub-sector number may be different as some

companies have yet introduced their annual performance.

Figure 43: SEC handset OPM vs. Electronic materials OPMWon billions, Sales growth Y/Y (%)

Source: Company data, Bloomberg actual data for sub-sectors. *Note: Actual FY12 sub-sector

number may be different as some companies have yet introduced their annual performance

Figure 14: SEC handset OPM vs. PCB OPMWon billions, Sales growth Y/Y (%)

Source: Company data, Bloomberg actual data for sub-sectors. *Note: Actual FY12 sub-sector

number may be different as some companies have yet introduced their annual performance

Figure 45: SEC handset OPM vs. Touch panel OPMWon billions, Sales growth Y/Y (%)

Source: Company data, Bloomberg actual data for sub-sectors. *Note: Actual FY12 sub-sector

number may be different as some companies have yet introduced their annual performance

Figure 46: SEC handset OPM vs. Electronic components OPMWon billions, Sales growth Y/Y (%)

Source: Company data, Bloomberg actual data for sub-sectors. *Note: Actual FY12 sub-sector

number may be different as some companies have yet introduced their annual performance

0%

5%

10%

15%

20%

25%

-10%

-5%

0%

5%

10%

15%

20%

2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E

Electronic components OPM PCB OPM Electronic materials OPMTouch Panel OPM SPE OPM SEC handset OPM [RHS]

0%

5%

10%

15%

20%

25

2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E

S EC h an ds et O PM [RH S] E le ct ro ni c mater ia ls O PM

0%

5%

10%

15%

20%

25%

2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E

SEC handset OPM [RHS] PCB OPM

-10%

-5%

0%

5%

10%

15%

20%

25

2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E

SEC handset OPM [RHS Touch Panel OPM

0%

5%

10%

15%

20%

25%

2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E

SEC handset OPM [RHS] Electronic components OPM

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 27/55

27

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Quick Snapshot of sub-sector tone toward Samsung

According to our research and discussion with sub-sector companies, ~60% of

companies guided their revenue exposure to Samsung would go up Y/Y and ~30% pointed out that their exposure will remain flat. While margin guidance is notdisclosed at this stage, given strengthened supplier-set maker confidential policy, weexpect qualified non-Samsung suppliers will continue to achieve margin expansionon strong customers' order momentum.

Table 7: Revenue exposure guidance for FY12 and FY13 by sub-sector companies

Revenue Exposure to Samsung (%)

Detailed Components Rev. Exposure (FY12) Rev. Exposure (FY13)

NAND (Internal Memory) SEC (6%) YoY slight downmobile DRAM SEC (4%) YoY slight downOLED panel SDC small mobile (+60%) YoY upOLED material Duksan (~85%), Doosan (<1%) Duksan (YoY up)LCD panel SDC small mobile (~40%) YoY upMobile BLU SDC small mobile (~40%), E-litecom (~50%) YoY latTouch Panel module Iljin (95%), S-MAC (50%), Melfas (85%), ELK Iljin (YoY lat), S-MAC (YoY lat), Melfas (YoY flat)Touch Panel sensor Melfas (85%) YoY latDriver IC Siliconworks (<5%) YoY down Application Processor SEC (2%) YoY upMLCC SEMCO (~20%) YoY upCamera module SEMCO (~25%), Partron (~80%) SEMCO (YoY up), Partron (YoY up)Image sensor/components Jahwa Elec (100%) YoY latCamera lens SonyProximity Sensor SECBaseband chip Intel (<1%), Qualcomm (18%) Qualcomm (YoY up)Radio Frequency chip Partron (~80%) YoY upPower Amplifer chip SkyworksLTE, HSPA+ 21Mbps Modem Chip Qualcomm (18%) YoY up Accelerometer ST Micro (~10%) YoY downGyroscope ST Micro (~10%) YoY down

Pressure sensor Partron (~80%) YoY up Audio Interface Wolfson Micro (+30%) YoY up (50%)WLAN Broadcom (17%) YoY upFM transceiver Infineon (low single %) YoY flatBluetooth Partron (~80%), Amotech (~45%) Partron (YoY up), Amotech (YoY up)Wi-Fi Partron (~80%) YoY upNFC chipset Partron (~80%), Amotech (~45%) Partron (YoY up), Amotech (YoY up)Power management IC Maxim, Texas Instruments, othersBattery Pack Samsung SDI (60%) YoY upBattery Cell Samsung SDI (60%) YoY upBattery Components material Power Logics (65%), Iljin Materials (50%) Power Logics (YoY up), Iljin Materials (YoY slightly up)PCB / FPCB / FC-CSP Daeduck (50%), Interflex (+40%), Flexcom (+90%) Daeduk (YoY slight up), Interflex (YoY up), Flexcom (YoY flat)Microphone BSE CM (~70%), Partron (~80%) BSE (YoY up), Partron (YoY up)Speaker receiver BSE CM (~70%) BSE (YoY up)Casing Intops (~95%), KH Vatec (60%) Intops (YoY flat), KH Vatec (YoY up)LCD bracket KH Vatec (60%), Innox KH Vatec (YoY up)SAW filter Wisol

Charger RF Tech (+40%) RF Tech (YoY slightly up)

Source: Company data, Gartner, Company data, J.P. Morgan estimates. *Supplier revenue exposure data based on company data. BOM cost based on Galaxy SIII, component supply status

based on overall Samsung smartphone line-ups. Supplier list includes companies above US$ 100mn market cap only. Revenue exposure (%) stands for total Samsung Electronics.

As most suppliers in tablet PC overlap, we have not included the list of names for tablet PC supply chain separately. However, we expect touch panel, casing makers,and PCB makers to benefit more from tablets assuming same volume provided larger screen, bigger form-factor and substrate in the products in terms of top-line andearnings.

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 28/55

28

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Section V: Implication from potential

component value changes in next GalaxyS-series

What are we hearing about Galaxy S IV?

As we move through mid-1Q13, we have begun to hear about potential productspecification and component changes in SEC's next flagship handset, Galaxy S IV(Source: Bloomberg). Herein, we lay out plausible product changes and identifywhich company and sub-sector could benefit from the change. Of note, we estimateGalaxy S IV to post ~100M unit shipment on cumulative basis since its launch.

Table 8: Potential BOM cost change comparison (Galaxy S III; previous version vs. Galaxy S IV)

US$

Components Galaxy S III Galaxy S IV

BOM + Manufacturing 253.1 Slight upManufacturing Cost 16.0 FlattishBOM Cost 237.1 Slight up

Memory 30.0 DownNAND Flash 17.4 DownDRAM 12.6 DownDisplay & Touch Screen 51.5 Slight up

Display 37.5 Slight upTouch Screen 14.0 Slight upProcessor 25.3 Flattish or slight upCamera(s) 19.6 Slight up

Wireless section - BB/RF/PA 38.0 Flattish or slight upUser Interface & Sensors 6.9 Flattish or slight upWLAN/BT/FM/GPS 6.5 Flattish or slight upPower Management 10.0 Up

Battery 4.5 UpMechanical / Electro-mechanical 38.0 FlattishBox Contents 7.0 Flattish

Source: Gartner, iSuppli, Company data, J.P. Morgan estimates

1. No major change in form-factor except for Display side

The market is expecting form-factor of next Galaxy S/Note-series to be similar to the previous versions. We agree with this view and expect a larger screen. However,given the tight supply at OLED capacity and yield issues, we will likely see the firstform of flexible (unbreakable) display adoption from the next Note-series (to belaunched during 3Q13 time-line). Accordingly, ASP for panel screen is expected toincrease and the relevant supply chain will likely benefit (mostly SDC and OLEDrelated material players; Duksan Hi-Metal and potentially Cheil industries). For casing players (KH Vatec, Intops, and others), companies claim size mix migration

could benefit them as larger device form-factor usually incurs higher ASP and better margin (especially for tablet PCs). PCB players (Interflex and Flexcom) will likely

benefit as set makers require slimmer substrate, even flexible substrate to come upwith fully-flexible handset in the future.

2. Higher camera pixel; 13MPx is high likely be online

We have already witnessed 13MPx camera module adoption into new smartphonesdisclosed at beginning of the year (over 9 models from different handset makers). We

believe 13MPx is likely to be adopted for SEC’s next flagship smartphone andSEMCO would be the main supplier, in our view. Accordingly, we will likely seeincreasing higher camera module adoption (8MPx) especially for back-end from low-

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 29/55

29

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

mid end cameras. Partron, Jawha Electronics, and Power Logics could be the keysuppliers.

3. Increasing adoption of LTE and emergence of diverse functional antenna

JPM analyst, Rod Hall, forecasts 2013 LTE smartphone to be 243M (up 180% Y/Y)and 2014 LTE smartphone to be 487M (up 100% Y/Y). This implies LTE

penetration within smartphone of 26%/45% in 2013/2014. SEC guided LTE handsetto drive its high-end line-up growth this year and we estimate SEC's LTE handsetshipment to top over 75M in 2013. Currently, a large portion of LTE components issupplied by Qualcomm, but we could likely see SEC coming up with its own LTEsolution this year given its product roadmap while absolute amount will have a bigimpact hit in 2014. Partron and Amotech are the major Korean suppliers for antenna components (i.e. DMB, NFC, Bluetooth, GPS, Wi-Fi, and others).

4. Battery, all about increasing capacity and power efficiency

Due to increasing complexity of handset functions and ongoing power consumptionfrom OLED panel, it is inevitable that battery capacity will be increased over modeldevelopment. Galaxy SIII's battery capacity has increased from 1,500 mAh (4”screen) to 2,100 mAh (4.8” screen). Samsung SDI is the sole vendor for SEC'sflagship smartphone line-ups and the largest battery supplier for SEC's mobiledevices (incl. tablet PC). Power Logics is currently supplying rechargeable batteryPCM (Power Circuit Module) for smartphones' BMS (Battery Management System).

5. Further potential changes; new functionality like S-Pen?

Based on various newsflow recently (Bloomberg), we have yet to discover anysurprising functionality in next Galaxy S IV. However, if anything comes up, weview it should come from different hardware features from user interface or sensors(e.g. S-Pen from first Galaxy Note version).

Galaxy series shipment momentum vs. Market Cap analysis

In this part, we compared SEC's Galaxy-series shipment momentum vs. Market Capof Korean Small Tech market cap and by individual sub-sectors. In conclusion,overall market cap trend was largely in-line with flagship models’ shipment volumechanges. By sub-sector comparison, Electronic components, Electronic materials andPCB sub-sector market cap performance were generally in-line with shipment whilemagnitude of momentum varied. Touch panel sub-sector had stronger correlationwith tablet PC shipment momentum. Overall touch panel market cap began toincrease since late 2Q12 as the market captured visibility on SEC’s tablet PCmomentum. However, SPE sector market performance was not highly correlated

since the key indicator to SPE sector was negative investment sentimental due todelay in OLED investment and limited LCD capacity supply growth.

7/29/2019 JPM Research: Samsung's Supply Chain (4 Mar)

http://slidepdf.com/reader/full/jpm-research-samsungs-supply-chain-4-mar 30/55

30

Asia Pacific Equity Research

04 March 2013JJ Park(822) 758-5717 [email protected]

Figure 47: Flagship smartphone shipment volume vs. Small Cap Tech Market Cap performanceUnit millions, US$ million [RHS]

Source: Bloomberg, Company data, J.P. Morgan estimates. Market Cap as of Feb 25 closes.

Figure 48: Flagship smartphone shipment volume vs. ElectronicComponents Market Cap performanceUnit millions, US$ million [RHS]

Source: Bloomberg, Company data, J.P. Morgan estimates. Market Cap as of Feb 25 closes.

Figure 49: Flagship smartphone shipment volume vs. PCB MarketCap performanceUnit millions, US$ million [RHS]

Source: Bloomberg, Company data, J.P. Morgan estimates. Market Cap as of Feb 25 closes.

Figure 50: Flagship smartphone shipment volume vs. Electronicmaterials Market Cap performanceUnit millions, US$ million [RHS]

Source: Bloomberg, Company data, J.P. Morgan estimates. Market Cap as of Feb 25 closes.

Figure 51: SEC’s tablet PC shipment volume vs. Touch Panel MarketCap performanceUnit millions, US$ million [RHS]

Source: Bloomberg, Company data, J.P. Morgan estimates. Market Cap as of Feb 25 closes.

3 7 10 812

2417 16 20

3526

1 54

310 11

8

8

16

0

2,000

4,000

6,000

8,000

10,000

12,000

14,00016,000

05

101520253035404550

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13A 2Q13E 3Q13E 4Q13E

Galaxy S-series Galaxy Note-series KR Total Market Cap [RHS]

3 7 10 8 12

2417 16 20

3526

1 54

310 11

8

8

16

0

500

1,000

1,5002,000

2,500

3,000

3,500

4,000

4,500

05

101520253035404550

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13A 2Q13E 3Q13E 4Q13E

Ga la xy S -s er ie s G al ax y N ot e- se ries E le ctr on ic C omp on en ts Market Cap [RH S]

- 3 7 10 8 12

2417 16 20

3526

--

-1 5

4

310 11

8

8

16

0

500

1,000

1,500

2,000

2,500

05

101520253035404550

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13A 2Q13E 3Q13E 4Q13E

Galaxy S-s eries Galax y Note-series PCB Market Cap [RHS]

- 3 7 10 812