josé maria piñero campos oecd fiscal federalism

DESCRIPTION

Tax autonomy and decentralisation in OECD countries. Network on Fiscal relations across levels of Government. José Maria Piñero Campos OECD Fiscal Federalism. INDEX. Tax autonomy and decentralisation Tax decentralisation Tax autonomy Tax Decentralisation vs. Tax Autonomy - PowerPoint PPT PresentationTRANSCRIPT

Tax autonomy and decentralisation in OECD countries.Network on Fiscal relations across levels of Government

José Maria Piñero CamposOECD Fiscal Federalism

INDEX

• Tax autonomy and decentralisation

– Tax decentralisation

– Tax autonomy

– Tax Decentralisation vs. Tax Autonomy

– Tax autonomy structure

– Pros and cons of tax Autonomy

– Tax Autonomy and disparities

– Tax autonomy and tax rate evolution

• Network on Fiscal relations across levels of government

– Documents

– Workshops

– Statistical databases

– Current Tasks

Tax Decentralisation

0

10

20

30

40

50

60

70

80

Belgi

um

Germ

any

Cana

da

Spain

Unite

d St

ates

Switz

erlan

d

Austr

ia

Swed

en

Austr

ia

Switz

erlan

d

Denm

ark

Czec

h Re

publi

c

Finla

nd

Fran

ce

Italy

Japa

n

Norw

ay

Germ

any

Portu

gal

Kore

a

Luxe

mbo

urg

Belgi

um

Spain

Hung

ary

Unite

d Ki

ngdo

m

Gree

ce

Irelan

d

Neth

erlan

ds

States/regions Municipalities

% of total revenues

Tax Autonomy

0

10

20

30

40

50

60

70

Can

ada

Uni

ted

Stat

es

Switz

erla

nd

Spai

n

Belg

ium

Ger

man

y

Aust

ria

Swed

en

Switz

erla

nd

Den

mar

k

Finl

and

Nor

way

Japa

n

Fran

ce

Luxe

mbo

urg

Spai

n

Belg

ium

Italy

Kore

a

Ger

man

y

Portu

gal

Hun

gary

Uni

ted

King

dom

Net

herla

nds

Gre

ece

Cze

ch R

epub

lic

Aust

ria

Irela

nd

States/regions Municipalities

% of total revenues

Tax Decentralisation vs. Tax Autonomy

Canada STA

United States STA

Switzerland STA

Spain STA

Germany STAAustria STA

Sweden LOC

Switzerland LOC

Denmark LOCFinland LOCNorway LOC

Japan LOC

Spain LOC France LOCLuxembourg LOCBelgium LOC Italy LOCKorea LOC

Germany LOC

Portugal LOCHungary LOC

United Kingdom LOCNetherlands LOC

Greece LOCCzech Republic LOC

Austria LOCIreland LOC0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

0 10 20 30 40 50 60 70

Autonomous tax revenues (% of Total revenues)

Tax revenues (% of Total revenues)

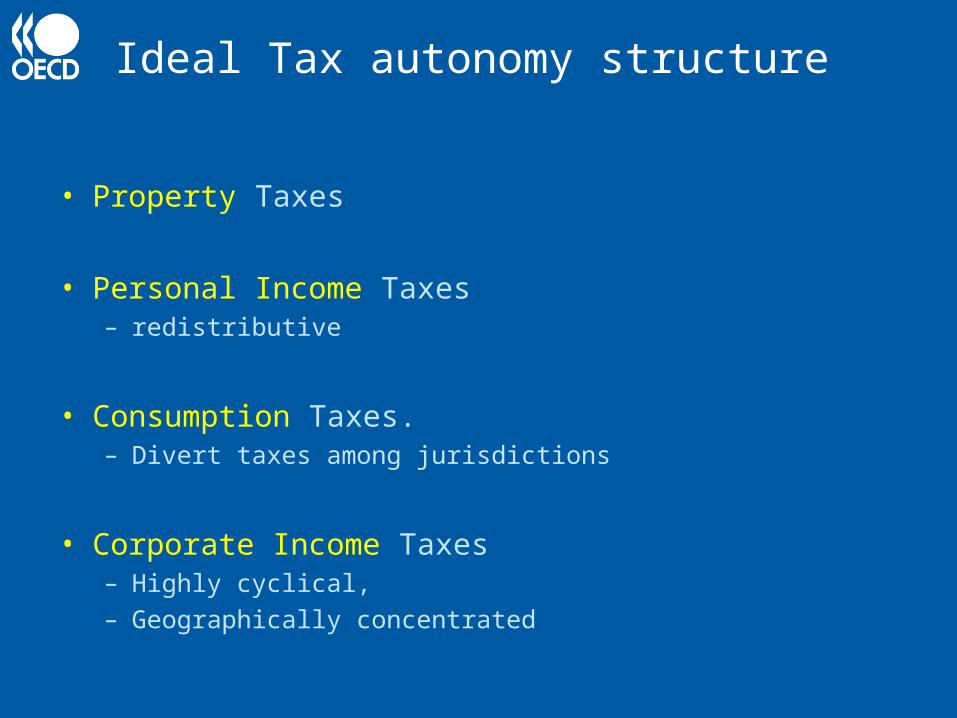

Ideal Tax autonomy structure

• Taxes which are growth-enhancing at sub-central level are the same as the ones which are growth-enhancing at central level

• But, there are some additional requirements :– Link between taxes paid and public services received– SCG Taxes should be non-mobile– Non redistributive– Non cyclical– Tax base should be evenly distributed across jurisdictions

Ideal Tax autonomy structure

• Property Taxes

• Personal Income Taxes– redistributive

• Consumption Taxes.– Divert taxes among jurisdictions

• Corporate Income Taxes– Highly cyclical, – Geographically concentrated

Real Tax autonomy structure

0

10

20

30

40

50

60

70

Can

ada

Uni

ted

Stat

es

Switz

erla

nd

Spai

n

Belg

ium

Ger

man

y

Aust

ria

Swed

en

Switz

erla

nd

Den

mar

k

Finl

and

Nor

way

Japa

n

Fran

ce

Luxe

mbo

urg

Spai

n

Belg

ium

Italy

Kore

a

Ger

man

y

Portu

gal

Hun

gary

Uni

ted

King

dom

Net

herla

nds

Gre

ece

Cze

ch R

epub

lic

Aust

ria

Irela

nd

CIT Consumption PIT Property Others

States/regions Municipalities

% of total revenues

Pros and cons or Tax autonomy• Pros

– Make governments more responsive to citizens’ tastes and preferences

– Improve budget management efficiency. A more reduced size of sub-central governments have been reported (Rodden (2003), Fiva (2006), Sorens (2008))

– Promote democratic accountability– Provide incentives for growth-oriented economic and fiscal policies– Could reduce disparities when small jurisdictions could benefit from

bigger neighbour jurisdictions

• Cons– Could increase disparities. If equalisation is not enough poorer

jurisdictions could be obliged to do a bigger effort– Could deteriorate SCG revenues (race to the bottom). – Could deteriorate SCG fiscal stability, if it is based on more volatile

taxes as Corporate or consumption taxes

Tax Autonomy and disparirites. What happen when equalisation is small?:

0

20

40

60

80

100

120

140

160

180

200

0 30 60 90 120 150 180 210 240 270 300

Implicit tax rate (in % of average)

Tax raising capacity per capita (in % of average)

1997

2006

0

20

40

60

80

100

120

140

160

180

200

0 30 60 90 120 150 180 210 240 270 300

Implicit tax rate (in % of average)

Tax raising capacity per capita (in % of average)

1998

2006

0

20

40

60

80

100

120

140

160

180

200

0 30 60 90 120 150 180 210 240 270 300

Implicit tax rate (in % of average)

Tax raising capacity per capita (in % of average)

2002

2007

0

20

40

60

80

100

120

140

160

180

200

0 30 60 90 120 150 180 210 240 270 300

Tax rate (in % of Regional average)

Tax raising capacity per capita (in % of average)

CASTILLA LA MANCHA (Municipios de más de 10.000 hab.)

CANADA S/R SWITZERLAND S/R

FRANCE (Departments)

Tax Autonomy and disparirites. What happen when equalisation is high?:

0

20

40

60

80

100

120

140

160

180

200

0 30 60 90 120 150 180 210 240 270 300

Implicit tax rate (in % of average)

Tax raising capacity per capita (in % of average)

1997

2007

0

20

40

60

80

100

120

140

160

180

200

0 30 60 90 120 150 180 210 240 270 300

Implicit tax rate (in % of average)

Tax raising capacity per capita (in % of average)

1997

2007

0

20

40

60

80

100

120

140

160

180

200

0 30 60 90 120 150 180 210 240 270 300

CIT and Property tax (CA or IMI) Implicit tax rate (in % of average)

Aggregate tax base per capita (in % of average)

2002

2007

0

20

40

60

80

100

120

140

160

180

200

0 30 60 90 120 150 180 210 240 270 300

Implicit tax rate (in % of average)

Tax raising capacity per capita (in % of average)

1997

2007

SWEDEN LOCPORTUGAL LOC

DENMARK LOC FINLAND LOC

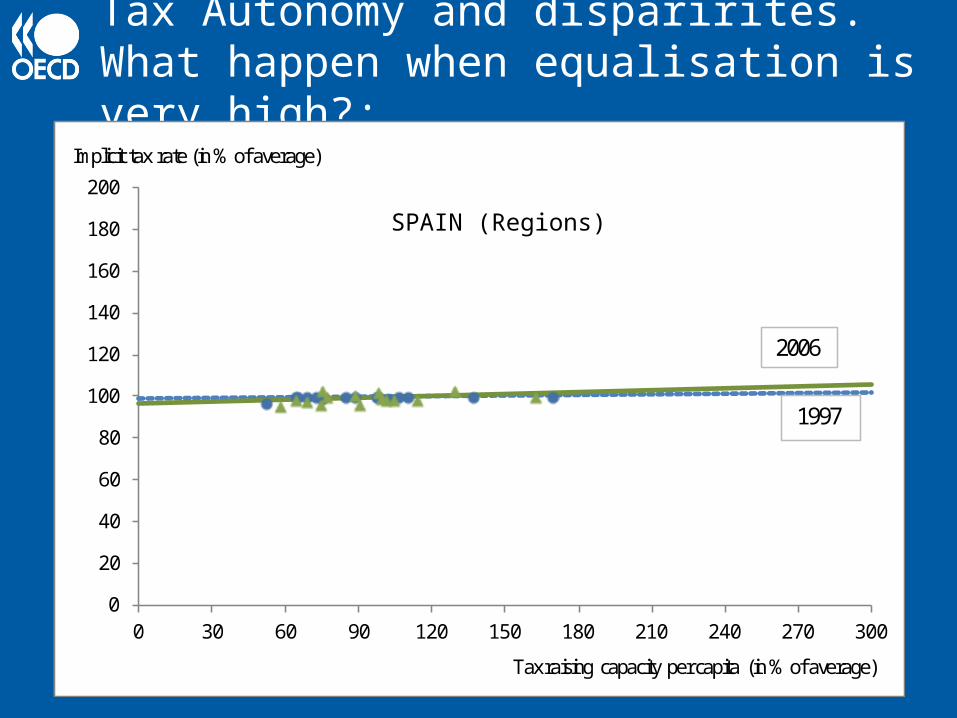

Tax Autonomy and disparirites. What happen when equalisation is very high?:

0

20

40

60

80

100

120

140

160

180

200

0 30 60 90 120 150 180 210 240 270 300

Implicit tax rate (in % of average)

Tax raising capacity per capita (in % of average)

1997

2006

SPAIN (Regions)

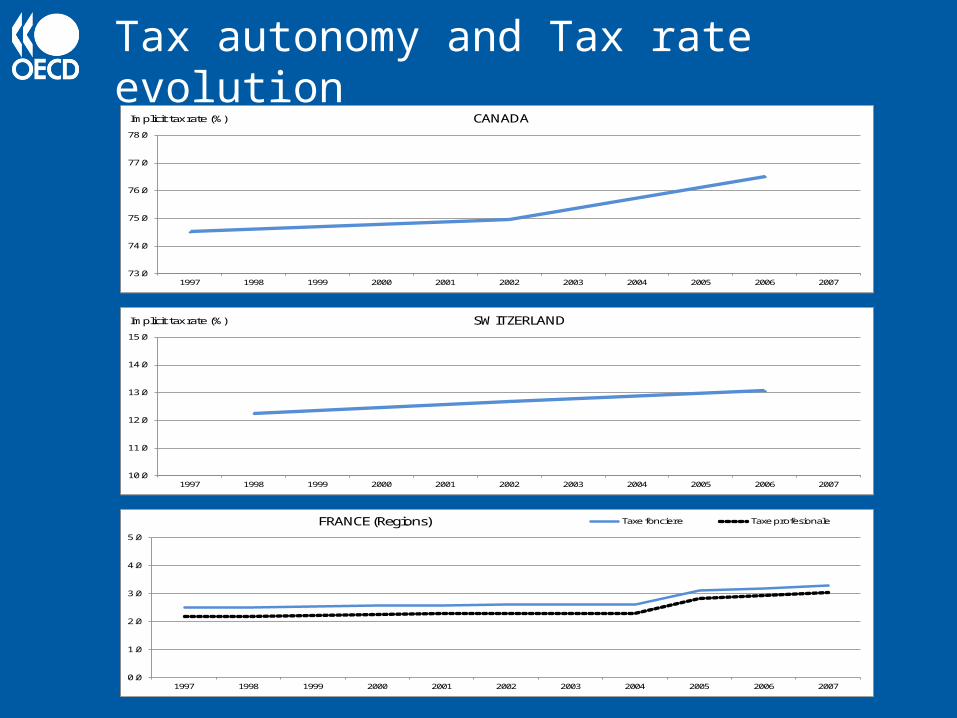

Tax autonomy and Tax rate evolution

73.0

74.0

75.0

76.0

77.0

78.0

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

CANADAImplicit tax rate (%)

10.0

11.0

12.0

13.0

14.0

15.0

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

SWITZERLANDImplicit tax rate (%)

0.0

1.0

2.0

3.0

4.0

5.0

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Taxe fonciere Taxe profesionaleFRANCE (Regions)

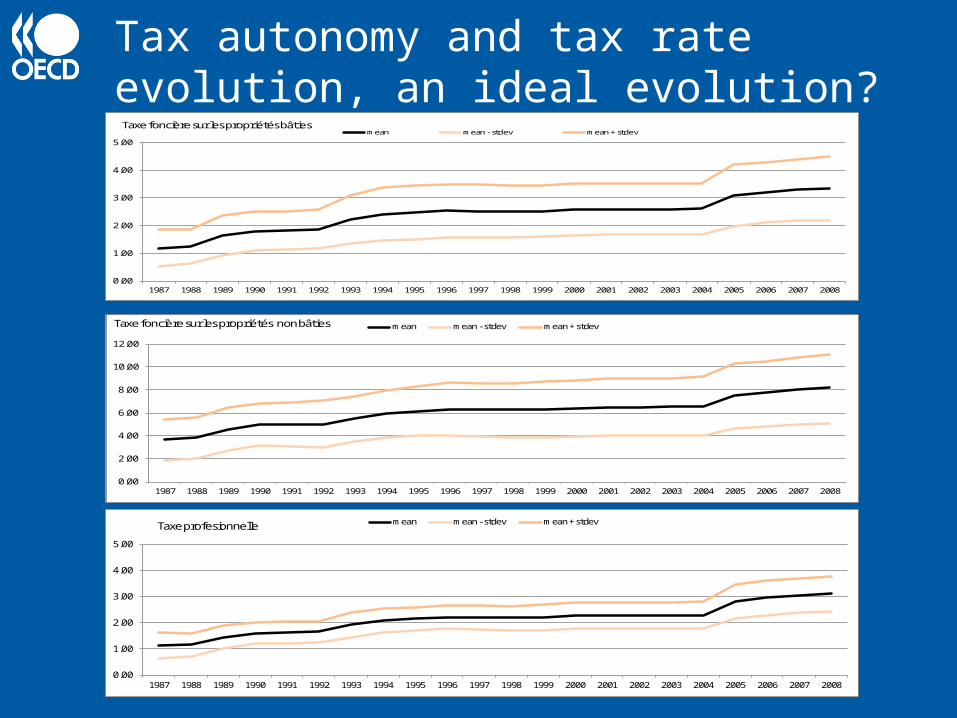

Tax autonomy and tax rate evolution, an ideal evolution?

0.00

1.00

2.00

3.00

4.00

5.00

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

mean mean - stdev mean + stdevTaxe foncière sur les propriétés bâties

0.00

2.00

4.00

6.00

8.00

10.00

12.00

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

mean mean - stdev mean + stdevTaxe foncière sur les propriétés non bâties

0.00

1.00

2.00

3.00

4.00

5.00

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

mean mean - stdev mean + stdevTaxe profesionnelle

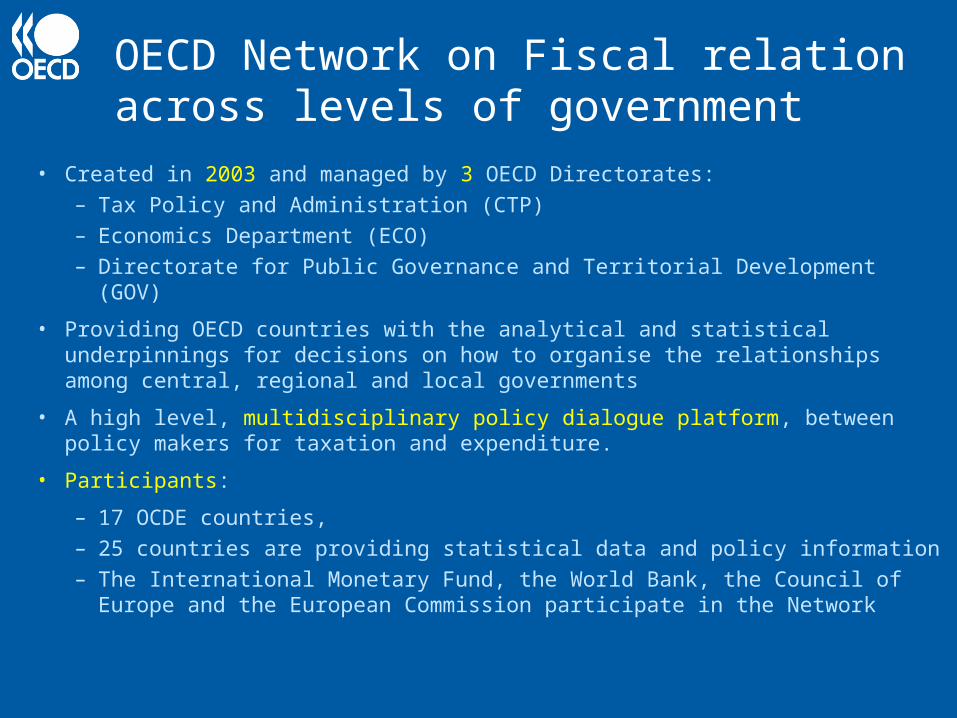

OECD Network on Fiscal relation across levels of government

• Created in 2003 and managed by 3 OECD Directorates:

– Tax Policy and Administration (CTP)

– Economics Department (ECO)

– Directorate for Public Governance and Territorial Development (GOV)

• Providing OECD countries with the analytical and statistical underpinnings for decisions on how to organise the relationships among central, regional and local governments

• A high level, multidisciplinary policy dialogue platform, between policy makers for taxation and expenditure.

• Participants:

– 17 OCDE countries,

– 25 countries are providing statistical data and policy information

– The International Monetary Fund, the World Bank, the Council of Europe and the European Commission participate in the Network

Fiscal Network. Documents • Fiscal policy across levels of government in times of crisis

• Explaining the Sub-National Tax-Grants Balance in OECD Countries

• Finding the Dividing Line between Tax Sharing and Grants: A Statistical Investigation

• The Fiscal Autonomy of Sub-Central Governments: An Update

• The Spending Power of Sub-Central Governments: A Pilot Study

• Taxes and Grants: On the Revenue Mix of Sub-Central Governments

• Market Mechanisms in Sub-Central Public Service Provision

• Promoting Performance: Using Indicators to Enhance the Effectiveness of Sub Central Spending

• Fiscal Equalisation in OECD countries

• Intergovernmental transfers and decentralised public spending

• Fiscal autonomy of sub-central governments

• Fiscal rules for sub-central governments: design and impact

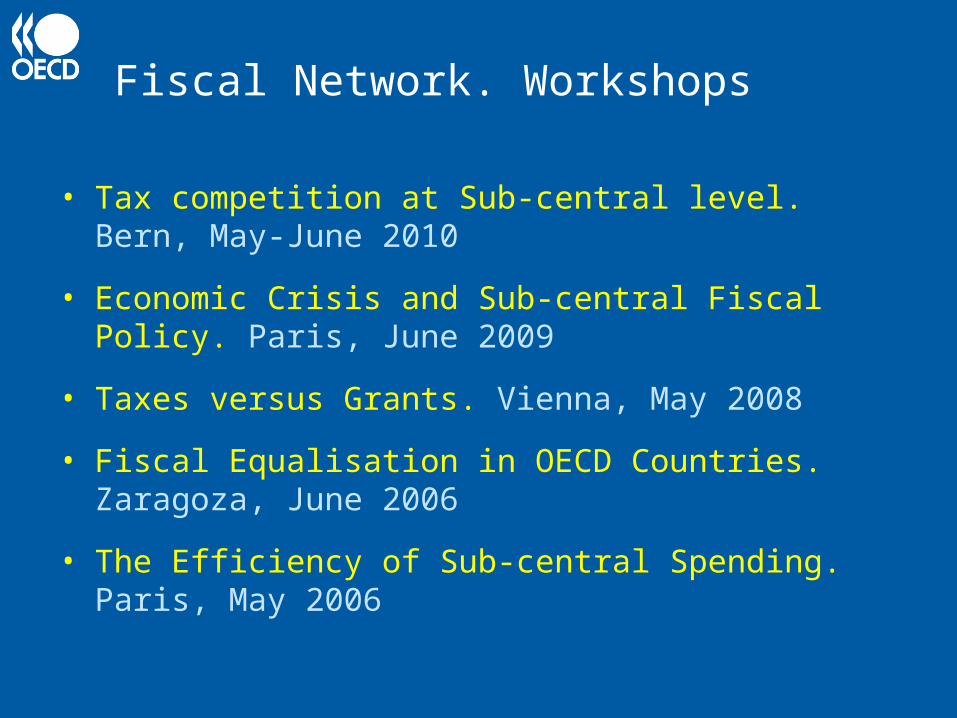

Fiscal Network. Workshops

• Tax competition at Sub-central level. Bern, May-June 2010

• Economic Crisis and Sub-central Fiscal Policy. Paris, June 2009

• Taxes versus Grants. Vienna, May 2008

• Fiscal Equalisation in OECD Countries. Zaragoza, June 2006

• The Efficiency of Sub-central Spending. Paris, May 2006

Fiscal Network. Statistical database

• Intergovernmental transfers: update of National Accounts data

• Taxing power of local and regional governments in OECD countries

• Revenue structure of sub central government

• Intergovernmental grants

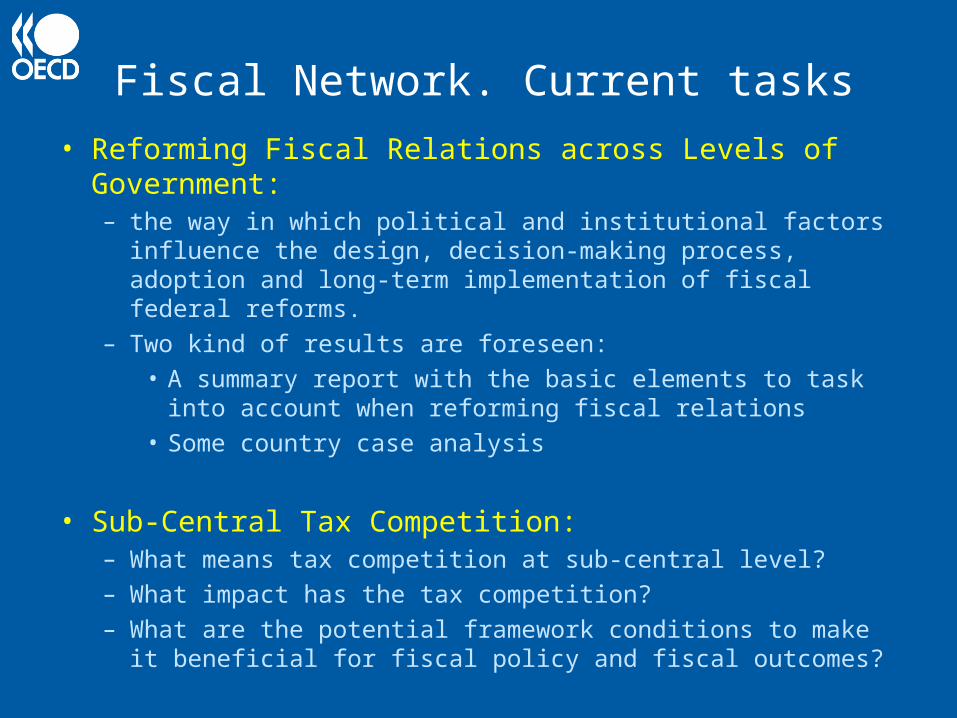

Fiscal Network. Current tasks

• Reforming Fiscal Relations across Levels of Government: – the way in which political and institutional factors influence the

design, decision-making process, adoption and long-term implementation of fiscal federal reforms.

– Two kind of results are foreseen:• A summary report with the basic elements to task into

account when reforming fiscal relations• Some country case analysis

• Sub-Central Tax Competition:– What means tax competition at sub-central level?– What impact has the tax competition?– What are the potential framework conditions to make it beneficial

for fiscal policy and fiscal outcomes?

Seminar about Fiscal decentralisation of Public AdministrationsCartagena, 2-6 November 2010

In collaboration with Instituto de Estudios Fiscales• To share Spain and OECD knowledge in fiscal federalism• To create a policy dialog platform about the most relevant trends and the

exchange of experienceies and information about regional and local financing, fiscal rules and budgetary discipline

The inscription is open till 24th September in the Centro de Formation de la AECID de Cartagena de Indias webpage:

http://www.aecidcf.org.co/aeci_cartagena/on_line/

Seminar about Fiscal decentralisation of Public AdministrationsCartagena, 2-6 November 2010

ISSUES• Sub-central governments financing: Basic principles. Tax financing and

transfer financing. International existing models.

• Taxes as financing source of sub-central governments. Taxes adequate for decentralisation. Tax decentralisation and tax autonomy. Consequences of tax decentralisation. Tax competition. Equalisation

• Fiscal decentralisation and budgetary stability. Budgetary consolidation. Sub central governments debt.

• Management of a fiscal decentralised system. Responsibilities distribution. Principles: institutional loyalty and co-ordination, transparency, etc. Decentralized public services provision. Indicators, market mechanisms in the provision of public services. The new technologies.