joint european chambers’ business joint … release/business confidence... · labor corruption...

TRANSCRIPT

Copyright ©2017 The Nielsen Company. Confidential and proprietary.

JOINT EUROPEAN

CHAMBERS’

BUSINESS

CONFIDENCE INDEX

2016

1

Copyright ©

2

017 Th

e

Nielsen Co mpany. Co

n

fiden; al and

propr ietary.

JOINT EUROPEAN

CHAMBERS’

BUSINESS

CONFIDENCE INDEX

2016

CREATED & MANAGED BY: COMMISSIONED BY: SURVEY PARTNER: CO-FUNDED BY: IN PARTNERSHIP WITH:

1

Copyright ©2017 The Nielsen Company. Confidential and proprietary.

RESEARCH METHODOLOGY

SELF-COMPLETION VIA

ONLINE INTERVIEWS

QUESTIONNAIRE15 MINUTE

FIELDWORK CONDUCTED

2ND DEC’16 – 26TH JAN’17

SAMPLE SIZE

148COVERAGE

JAKARTA

2

Copyright ©2017 The Nielsen Company. Confidential and proprietary. 3

PROFILE OF SURVEY

RESPONDENTS

Copyright ©2017 The Nielsen Company. Confidential and proprietary.

PROFILE OF RESPONDENTS

Increasing number of respondents affiliated with the British Chamber of Commerce, with private services as the main business sector

Reff: Q7 & Q11| Base: 148

MAIN CHAMBER AFFILIATION KEY BUSINESS SECTORS OF COMPANIES

46%BRITISH CHAMBER

(+8%)

25%EURO CHAMBER

(+3%)

11%GERMAN

CHAMBER

(-3%)

5%DUTCH

CHAMBER

(-2%)

5%FRENCH CHAMBER

(-2%)

8%OTHER CHAMBER

(-2%)

24% 16% 13% 11% 11% 7%

BANKING,

FINANCE, &

INSURANCE

INFRASTRUCTURE

& CONSTRUCTION

ENERGY &

NATURAL RESOURCES(+8%)(-3%) (-1%)

(XX%) : DIFFERENCES FROM ’15 DATA

CHEMICALS,

PHARMA,

COSMETICS

RETAIL /

CONSUMER

GOODS

(-1%)

(+2%) (0%)

SERVICES

(PRIVATE)

4

Copyright ©2017 The Nielsen Company. Confidential and proprietary. 5

OUTLOOK TOWARDS

BUSINESS ENVIRONMENT

Copyright ©2017 The Nielsen Company. Confidential and proprietary.

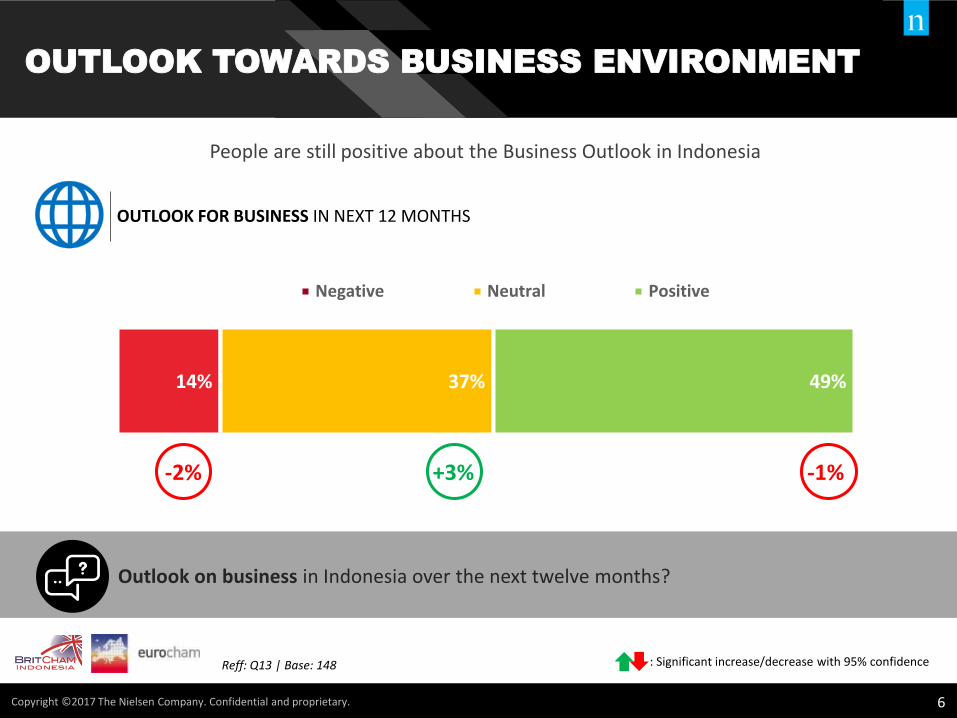

OUTLOOK TOWARDS BUSINESS ENVIRONMENT

People are still positive about the Business Outlook in Indonesia

Reff: Q13 | Base: 148

Outlook on business in Indonesia over the next twelve months?

OUTLOOK FOR BUSINESS IN NEXT 12 MONTHS

14% 37% 49%

Negative Neutral Positive

-2% +3% -1%

: Significant increase/decrease with 95% confidence

6

Copyright ©2017 The Nielsen Company. Confidential and proprietary.

TOP 5 BUSINESS SECTORS WITH POSITIVE

OUTLOOK

Increasingly positive outlook towards Infrastructure/Construction and Travel & Tourism

IN NEXT 12 MONTHS

Reff: Q14| Base: 148

Which are the key business sectors with positive outlooks?

OUTLOOK FOR BUSINESS IN NEXT 12 MONTHS

76%64% 59%

52% 48%

TOP 2 BOX : INDICATES “POSITIVE” + “VERY POSITIVE”

INFRASTRUCTURE & CONSTRUCTION

HOSPITALITY, TRAVEL & TOURISM

FOOD & BEVERAGE

RETAIL / CONSUMER GOODS

SERVICE (PRIVATE)

7

Copyright ©2017 The Nielsen Company. Confidential and proprietary.

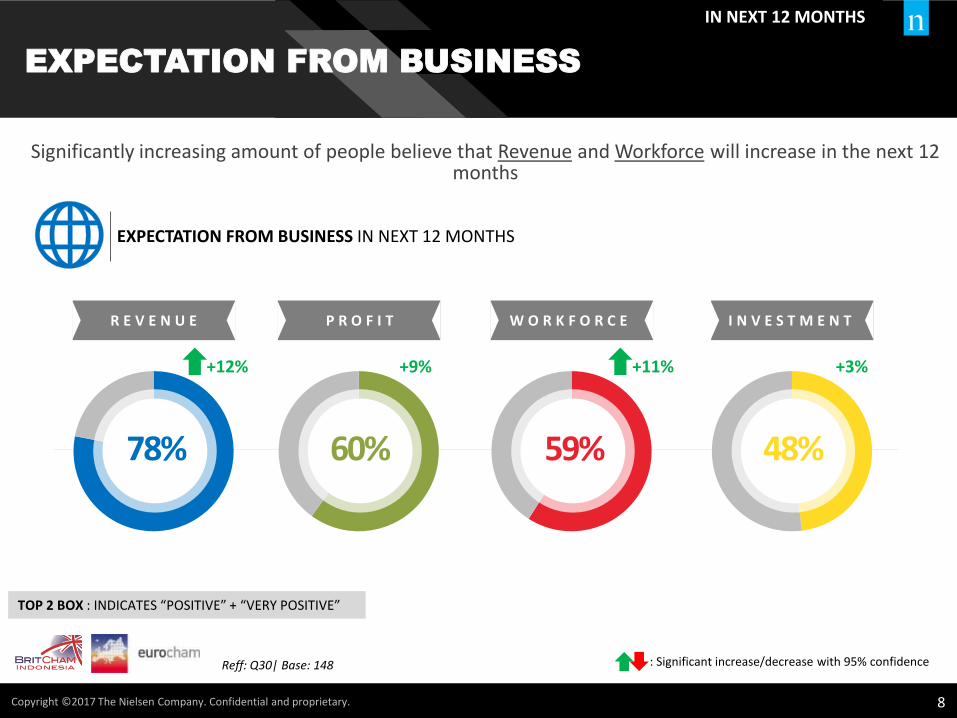

EXPECTATION FROM BUSINESS

Significantly increasing amount of people believe that Revenue and Workforce will increase in the next 12 months

IN NEXT 12 MONTHS

Reff: Q30| Base: 148

EXPECTATION FROM BUSINESS IN NEXT 12 MONTHS

TOP 2 BOX : INDICATES “POSITIVE” + “VERY POSITIVE”

R E V E N U E P R O F I T W O R K F O R C E I N V E S T M E N T

78%

+12% +9% +11% +3%

60% 59% 48%

: Significant increase/decrease with 95% confidence

8

Copyright ©2017 The Nielsen Company. Confidential and proprietary. 9

FACTORS AFFECTING

BUSINESS

Copyright ©2017 The Nielsen Company. Confidential and proprietary.

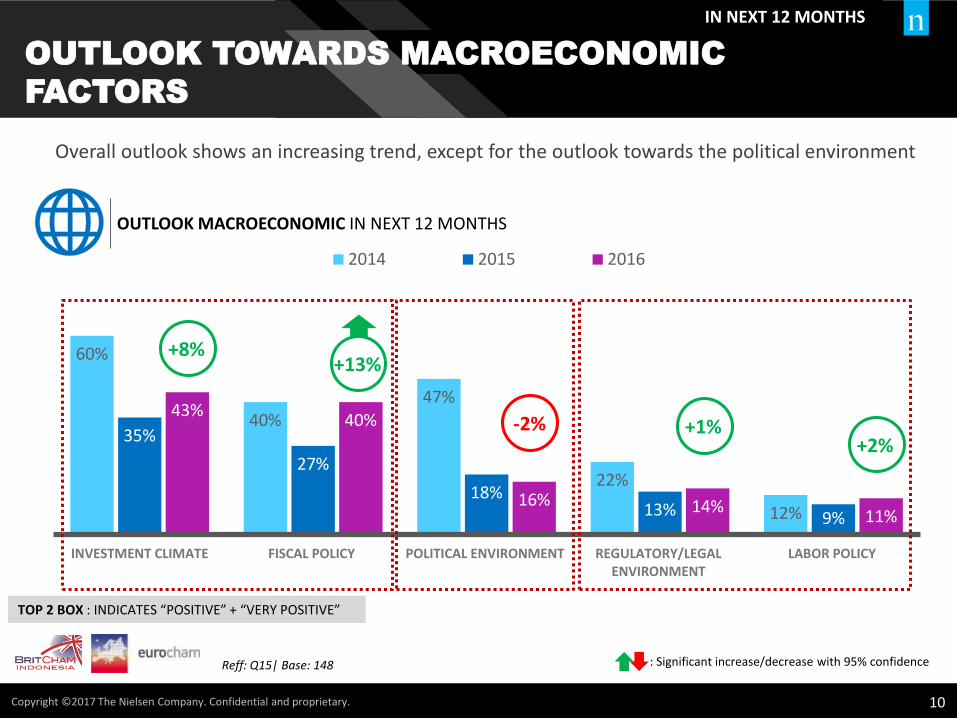

OUTLOOK TOWARDS MACROECONOMIC

FACTORS

Overall outlook shows an increasing trend, except for the outlook towards the political environment

IN NEXT 12 MONTHS

Reff: Q15| Base: 148

OUTLOOK MACROECONOMIC IN NEXT 12 MONTHS

60%

40%47%

22%

12%

35%

27%

18%13% 9%

43%40%

16% 14%11%

INVESTMENT CLIMATE FISCAL POLICY POLITICAL ENVIRONMENT REGULATORY/LEGALENVIRONMENT

LABOR POLICY

2014 2015 2016

+8%+13%

-2% +1%+2%

TOP 2 BOX : INDICATES “POSITIVE” + “VERY POSITIVE”

: Significant increase/decrease with 95% confidence

10

Copyright ©2017 The Nielsen Company. Confidential and proprietary.

CHALLENGES FOR BUSINESS IN INDONESIA

In line with that finding, political & social stability is considered to be an increasing concern

IN NEXT 12 MONTHS

Reff: Q17| Base: 148

BUSINESS IN INDONESIA IN NEXT 12 MONTHS

72% 72%

46%

60%

71% 68%62%

69% 71%

32%

57%50% 51%

45%

72% 70%

47% 49% 48% 47%43%

REGULATORYENVIRONMENT

BUREAUCRATICINEFFICIENCY/RED

TAPE

POLITICAL & SOCIALSTABILITY

LABOR POLICY LACK OFINFRASTRUCTURE

LACK OF SKILLEDLABOR

CORRUPTION

2014 2015 2016

TOP CHALLENGES CHALLENGES 2016 vs. 2015INCREASING

CONCERN

+3% -1%

+15%

-8% -2% -4%

-2%

TOP 2 BOX : INDICATES “LIKELY” + “VERY LIKELY” TO AFFECT INDONESIA

: Significant increase/decrease with 95% confidence

11

Copyright ©2017 The Nielsen Company. Confidential and proprietary.

MAJOR INVESTMENTS IN INDONESIA

Thus, it is no wonder that investors are still on the fence when considering FURTHER INVESTMENTS in Indonesia compared to last year

Reff: Q12| Base: 148

Major investments in Indonesia over the next 12 months?

MAJOR INVESTMENTS IN INDONESIA IN NEXT 2 YEARS

24% 41% 35%

No Maybe Yes

-11%

+22%

-11%

IN NEXT 12 MONTHS

: Significant increase/decrease with 95% confidence

12

Copyright ©2017 The Nielsen Company. Confidential and proprietary.

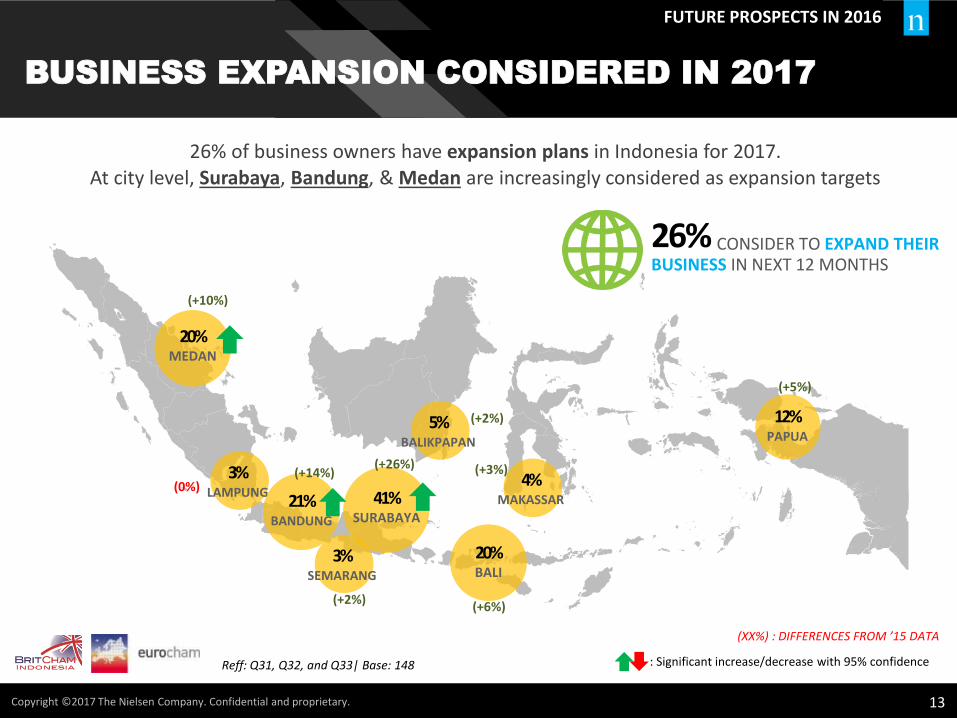

BUSINESS EXPANSION CONSIDERED IN 2017

26% of business owners have expansion plans in Indonesia for 2017.At city level, Surabaya, Bandung, & Medan are increasingly considered as expansion targets

FUTURE PROSPECTS IN 2016

Reff: Q31, Q32, and Q33| Base: 148

26% CONSIDER TO EXPAND THEIR BUSINESS IN NEXT 12 MONTHS

5%BALIKPAPAN

12%PAPUA

41%SURABAYA

3%LAMPUNG

20%MEDAN

21%BANDUNG

4%MAKASSAR

20%BALI

3%SEMARANG

(+10%)

(0%)(+14%)

(+2%)

(+26%)

(+2%)

(+6%)

(+3%)

(+5%)

(XX%) : DIFFERENCES FROM ’15 DATA

: Significant increase/decrease with 95% confidence

13

Copyright ©2017 The Nielsen Company. Confidential and proprietary.

BUSINESS CONFIDENCE INDEX

With a positive business outlook but negative political environment, Business Confidence Index is more or less balanced and remain stable compared to 2015

Reff: Q13| Base: 148

60%71%

50% 49%

2013 2014 2015 2016

BUSINESS CONFIDENCE INDEX

14

Copyright ©2017 The Nielsen Company. Confidential and proprietary. 15

GOVERNMENT’S POLICY

Copyright ©2017 The Nielsen Company. Confidential and proprietary.

GOVERNMENT'S ATTITUDE

The government attitude remains strong.

IN NEXT 12 MONTHS

Reff: Q19| Base: 148

TOP 2 BOX : INDICATES “WILL IMPROVE” + “WILL IMPROVE A LOT”

GOVERNMENT'S ATTITUDE

26%26%

36%43%

55%

Clear And Concise

Explanations Provided

Effective ImplementationPro-Business DecisionCoordination With Other

Ministries

Consultation With

Business

-4%

0%-3%

+4% +5%

: Significant increase/decrease with 95% confidence

16

Copyright ©2017 The Nielsen Company. Confidential and proprietary.

GOVERNMENT'S ACTION

Even more so, companies believe that increasing action will be taken by the government compared to the previous year

IN NEXT 12 MONTHS

Reff: 20| Base: 148

TOP 2 BOX : INDICATES “WILL IMPROVE” + “WILL IMPROVE A LOT”

GOVERNMENT'S ACTION

53%54%57%51%51%

Clear And Concise

Explanations Provided

Effective ImplementationPro-Business DecisionCoordination With Other

Ministries

Consultation With

Business

+9% +15%+16% +30% +31%

: Significant increase/decrease with 95% confidence

17

Copyright ©2017 The Nielsen Company. Confidential and proprietary.

IMPACT OF ECONOMIC STIMULUS PACKAGES

One third of corporate respondents are positively impacted by the government economic stimulus packages. However, more do not yet feel impacted.

Reff: Q37| Base: 148

TOP 2 BOX : INDICATES “SOMEWHAT AFFECTING” + “AFFECTING A LOT”

IMPACT OF ECONOMIC STIMULUS PACKAGES TO BUSINESS DEVELOPMENT PLAN

30% 37% 33%

Not Affecting Neutral Affecting

18

Copyright ©2017 The Nielsen Company. Confidential and proprietary. 19

SUMMARY

Copyright ©2017 The Nielsen Company. Confidential and proprietary.

BUSINESS OUTLOOK FACTORS AFFECTING BUSINESS

BUSINESS CONFIDENCEINDEX

GOVERNMENT POLICY

• Business outlook remains

positive

• Infrastructure, Hospitality,

and F&B are the key

business sectors in 2017

• Business expansion targets

are Surabaya, Bandung, &

Medan

• While the Macroeconomic

outlook shows a positive

trend, political environment

is lower than 2016

• In line with that, political &

social stability is a

significantly increasing

concern, while main

challenges are still regulatory

environment & bureaucratic

inefficiency

• Investors are adopting a

“wait-and-see” attitude to

investing in Indonesia

• Business Confident Index

remains stable and balanced

between the positive outlook

and increasing political

concerns

• Better perception towards

Government Policy &

Regulations

• There is opportunity for

growth by utilizing more

targeted revamped

economic stimulus

packages

20

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

21

AN UNCOMMON SENSE OF THE CONSUMER

Copyright ©2017 The Nielsen Company. Confidential and proprietary.

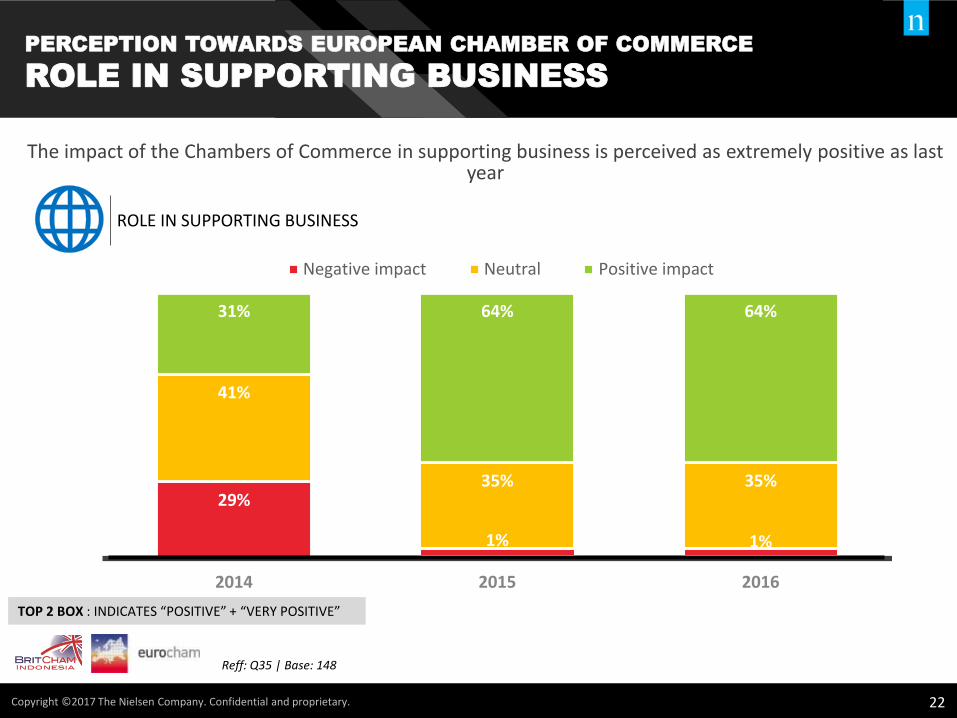

PERCEPTION TOWARDS EUROPEAN CHAMBER OF COMMERCE

ROLE IN SUPPORTING BUSINESS

The impact of the Chambers of Commerce in supporting business is perceived as extremely positive as last year

Reff: Q35 | Base: 148

TOP 2 BOX : INDICATES “POSITIVE” + “VERY POSITIVE”

29%

1% 1%

41%

35% 35%

31% 64% 64%

2014 2015 2016

Negative impact Neutral Positive impact

ROLE IN SUPPORTING BUSINESS

22

Copyright ©2017 The Nielsen Company. Confidential and proprietary.

THANK YOU

23

Copyright ©

2

017 Th

e

Nielsen Co mpany. Co

n

fiden; al and

propr ietary.

JOINT EUROPEAN

CHAMBERS’

BUSINESS

CONFIDENCE INDEX

2016

CREATED & MANAGED BY: COMMISSIONED BY: SURVEY PARTNER: CO-FUNDED BY: IN PARTNERSHIP WITH:

1