jimmy marin q2 magazine

DESCRIPTION

Jimmy Marin's Official Q2 MagazineTRANSCRIPT

A Member Of Real Living

PacUnion.com

Jimmy Marin Real Estate Report

Q2. 2011

Pacific Union International Luxury Real Estate Report

A Member Of Real Living

Pacific Union International Luxury Real Estate Report Q2. 2011

MARIN COUNTY

Pacific Union International Luxury Real Estate Report Q2. 2011

MARIN COUNTY

Pacific Union International Luxury Real Estate Report

MARIN COUNTYA Member Of Real Living

New Escrows Increase by 15% - 20% in Marin CountyReal Estate News vs. “Noise”

We recognize the “noise” you are exposed to via national and regional real estate news and quarterly reports. Most of these reports track closings (sales) and are reported anywhere from 30 – 60 days after the completion of the research cycle (either monthly or quarterly). The information is, by design, general in nature and somewhat dated by the time it is published. The S&P/Case-Shiller Report Index™ and the First Republic Prestige Home Index™ both report sales on a month-to-date, quarter-to-date or year-to-date basis. These reports provide retrospective and relative indicators of value and activity; however, they do not provide insight into future trends on a local basis.

Please understand that we believe real estate is local and furthermore, market activities and trends can be unique within a market (county) by neighborhood and/or by price point. We also believe that properties “under contract” or “new escrows” are the industry’s most meaningful indicator of near term trends.

Our review of Marin County real estate “under-contract” or “in-escrow” reveals encouraging movement even though it isn’t peak season. The chart below illustrates current trends (by percentage) for properties currently “under contract” vs. the same time period twelve (12) and twenty-four (24) months ago. So, while your specific neighborhood may be performing differently and pricing may be less than meets our sellers’ expectations, our markets are continuing to accelerate, at least in terms of properties “under contract”.

Listing inventory continues to exceed demand and increase at a faster pace than new escrows or properties under contract. Months of Inventory (above) illustrates that it would take between 3.7 and 11.5 months of current demand to exhaust the on-market inventory. This suggests that seller’s pricing is critical to be in the deal flow vs. in the active listing inventory. Do not underestimate the power of demand-based pricing. Price your property within local market demand tolerances and you will likely ratify a new escrow. Flirt with the high-end of your pricing range and prepare to simply be part of our inventory statistics.

In this market place, we encourage families to make housing decisions first, on the quality of the environment they are striving to accomplish at home and second, on the opportunity associated with their investment. It is our feeling that a “buy and hold” strategy for at least five (5) years will likely be a lucrative investment.

We do not see the “buyers’ window” closing. In a broader sense, we see more realistic sellers everyday which translates into more demand based, realistic pricing for pre-qualified, motivated buyers!

Please remember to seek out local news, trend analysis and advice for your real estate decisions. If you are a seller, be realistic on your presentation (by staging when recommended)and meet market demands with pricing. If you are a buyer, seizeopportunities when they arise, as the truly best priced propertiesgenerally receive multiple offers.

All Price Ranges

15.2%

46.3%

-7.7%

-28.8%

3.7

$1 million and Up

20.7%

65.5%

-30.1%

-24.6%

6.0

$3 Million and Up

17.8%

55.8%

-11.37%

19.4%

11.5

Single Family Homes and Condos

Under Contract (v 24 months ago)

Under Contract (v 12 months ago)

Listing Inventory (v 24 months ago)

Listing Inventory (v 12 months ago)

Months of Inventory

1800

1600

1400

1200

1000

800

600

400

200

0

For Sale Under Contract Sold

Jun 10 Jul 10 Aug 10 Sep 10 Oct 10 Nov 10 Dec 10 Jan 11 Feb 11 Mar 11 Apr 11 May 11 Jun 11

# o

f H

om

es

Market DynamicsSupply & Demand - # Homes (FS, UC, Sold)

Jun-10 through Jun-11

Jimmy Wanninger!iimmmmyy WWaannnniinnggeerr

!iimmmmyy WWaannnniinnggeerr990011 SSiirr FFrraanncciiss DDrraakkee BBllvvddKKeennttffiieelldd,, CCAA 9944990044441155..999900..88999900jjiimmmmyy@@jjiimmmmyymmaarriinn..ccoommwwwwww..!iimmmmyyMMaarriinn..ccoommDDRREE## 0011335522228877

441155..999900..88999900jjiimmmmyy@@jjiimmmmyymmaarriinn..ccoommwwwwww..!iimmmmyyMMaarriinn..ccoomm

990011 SSiirr FFrraanncciiss DDrraakkee BBllvvdd,, KKeennttffiieelldd,, CCAA 9944990044

Q2. 2011

A Member Of Real Living

Pacific Union International Luxury Real Estate Report Q2. 2011

HOME COMPARISONA Member Of Real Living

Pacific Union International Luxury Real Estate Report

HOME COMPARISON

Marin County $1 Million & Under - SFH

Source: BAREIS, as of June 30, 2011

Apr - Jun '09

$198,920,570

305

105

$680,000

$652,199

$1,000,000

Apr - Jun '10

$252,479,042

375

77

$670,000

$673,277

$1,000,000

Apr - Jun '11

$232,983,609

363

99

$631,400

$641,828

$993,350

'09 - '10% Change

27%

23%

-27%

-1%

3%

0%

'10 - '11% Change

-8%

-3%

29%

-6%

-5%

-1%

TIME PERIOD

VOLUME

HOMES SOLD

AVG. DAYS ON MKT

MEDIAN PRICE

AVERAGE PRICE

MAX PRICE SOLD

Marin County $1 Million & Higher - SFH

Source: BAREIS, as of June 30, 2011

Apr - Jun '09

$235,284,700

136

81

$1,487,500

$1,730,035

$5,200,000

Apr - Jun '10

$371,657,419

201

83

$1,550,000

$1,849,042

$7,800,000

Apr - Jun '11

$343,235,998

184

84

$1,520,500

$1,865,413

$8,750,000

'09 - '10% Change

58%

48%

2%

4%

7%

50%

'10 - '11% Change

-8%

-8%

1%

-2%

1%

12%

TIME PERIOD

VOLUME

HOMES SOLD

AVG. DAYS ON MKT

MEDIAN PRICE

AVERAGE PRICE

MAX PRICE SOLD

Marin County $1-$3 Million - SFH

Source: BAREIS, as of June 30, 2011

Apr - Jun '09

$202,171,700

127

79

$1,470,000

$1,591,903

$3,000,000

Apr - Jun '10

$277,911,169

177

81

$1,395,000

$1,570,120

$3,000,000

Apr - Jun '11

$273,737,338

168

82

$1,465,000

$1,629,389

$3,000,000

'09 - '10% Change

37%

39%

3%

-5%

-1%

0%

'10 - '11% Change

-2%

-5%

1%

5%

4%

0%

TIME PERIOD

VOLUME

HOMES SOLD

AVG. DAYS ON MKT

MEDIAN PRICE

AVERAGE PRICE

MAX PRICE SOLD

Marin County Market StatisticsQ2 2010 vs Q2 2011

Source: BAREIS, as of June 30, 2011

$1M and under

-8%

-3%

29%

-6%

-5%

$1M and higher

-8%

-8%

1%

-2%

1%

APR - JUN

VOLUME

HOMES SOLD

DOM

MEDIAN PRICE

AVERAGE PRICE

Marin County $3 Million & Higher - SFH

Source: BAREIS, as of June 30, 2011

Apr - Jun '09

$36,113,000

10

118

$3,240,250

$3,611,300

$5,200,000

Apr - Jun '10

$96,746,250

25

97

$3,350,000

$3,869,850

$7,800,000

Apr - Jun '11

$72,498,660

17

98

$3,800,000

$4,264,627

$8,750,000

'09 - '10% Change

168%

150%

-18%

3%

7%

50%

'10 - '11% Change

-25%

-32%

1%

13%

10%

12%

TIME PERIOD

VOLUME

HOMES SOLD

AVG. DAYS ON MKT

MEDIAN PRICE

AVERAGE PRICE

MAX PRICE SOLD

Marin County Median & Average Home PriceQ1 2009 - Q2 2011

Q109

$948,355

$720,910

Q209

$984,557

$775,000

Q309

$1,015,120

$800,000

Q409

$996,236

$753,000

Q110

$984,178

$751,000

Q210

$1,083,861

$816,500

Q310

$1,022,077

$790,000

Q410

$1,022,299

$763,500

Q1111

$937,817

$705,000

AVG. PRICE

MEDIAN PRICE

Source: BAREIS, June 30, 2011

Q211

$1,053,418

$779,000

WWee llooookk ffoorrwwaarrdd ttoo sseerrvviinngg yyoouu iinn 22001111..

A Member Of Real Living

Pacific Union International Luxury Real Estate Report Q2. 2011

SONOMA

Pacific Union International Luxury Real Estate Report Q2. 2011

SONOMA

Pacific Union International Luxury Real Estate Report

SONOMAA Member Of Real Living

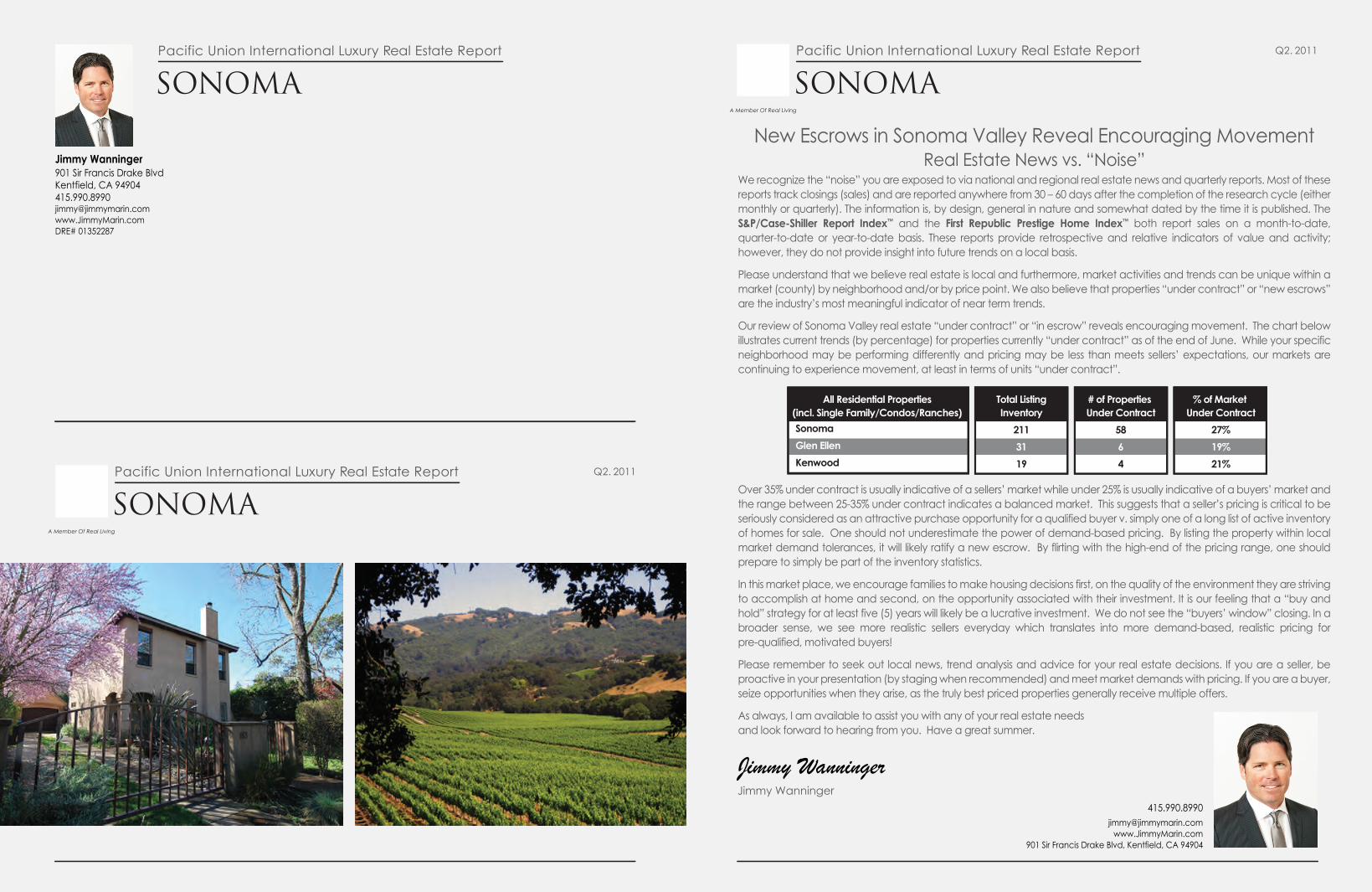

New Escrows in Sonoma Valley Reveal Encouraging Movement Real Estate News vs. “Noise”

We recognize the “noise” you are exposed to via national and regional real estate news and quarterly reports. Most of these reports track closings (sales) and are reported anywhere from 30 – 60 days after the completion of the research cycle (either monthly or quarterly). The information is, by design, general in nature and somewhat dated by the time it is published. The S&P/Case-Shiller Report Index™ and the First Republic Prestige Home Index™ both report sales on a month-to-date, quarter-to-date or year-to-date basis. These reports provide retrospective and relative indicators of value and activity; however, they do not provide insight into future trends on a local basis.

Please understand that we believe real estate is local and furthermore, market activities and trends can be unique within a market (county) by neighborhood and/or by price point. We also believe that properties “under contract” or “new escrows” are the industry’s most meaningful indicator of near term trends.

Our review of Sonoma Valley real estate “under contract” or “in escrow” reveals encouraging movement. The chart below illustrates current trends (by percentage) for properties currently “under contract” as of the end of June. While your specific neighborhood may be performing differently and pricing may be less than meets sellers’ expectations, our markets are continuing to experience movement, at least in terms of units “under contract”.

Over 35% under contract is usually indicative of a sellers’ market while under 25% is usually indicative of a buyers’ market and the range between 25-35% under contract indicates a balanced market. This suggests that a seller’s pricing is critical to be seriously considered as an attractive purchase opportunity for a qualified buyer v. simply one of a long list of active inventory of homes for sale. One should not underestimate the power of demand-based pricing. By listing the property within local market demand tolerances, it will likely ratify a new escrow. By flirting with the high-end of the pricing range, one should prepare to simply be part of the inventory statistics.

In this market place, we encourage families to make housing decisions first, on the quality of the environment they are striving to accomplish at home and second, on the opportunity associated with their investment. It is our feeling that a “buy and hold” strategy for at least five (5) years will likely be a lucrative investment. We do not see the “buyers’ window” closing. In a broader sense, we see more realistic sellers everyday which translates into more demand-based, realistic pricing for pre-qualified, motivated buyers!

Please remember to seek out local news, trend analysis and advice for your real estate decisions. If you are a seller, be proactive in your presentation (by staging when recommended) and meet market demands with pricing. If you are a buyer, seize opportunities when they arise, as the truly best priced properties generally receive multiple offers.

As always, I am available to assist you with any of your real estate needsand look forward to hearing from you. Have a great summer.

Total ListingInventory

211

31

19

# of Properties Under Contract

58

6

4

% of Market Under Contract

27%

19%

21%

Sonoma

Glen Ellen

Kenwood

All Residential Properties(incl. Single Family/Condos/Ranches)

Jimmy Wanninger!iimmmmyy WWaannnniinnggeerr

!iimmmmyy WWaannnniinnggeerr990011 SSiirr FFrraanncciiss DDrraakkee BBllvvddKKeennttffiieelldd,, CCAA 9944990044441155..999900..88999900jjiimmmmyy@@jjiimmmmyymmaarriinn..ccoommwwwwww..!iimmmmyyMMaarriinn..ccoommDDRREE## 0011335522228877

441155..999900..88999900jjiimmmmyy@@jjiimmmmyymmaarriinn..ccoommwwwwww..!iimmmmyyMMaarriinn..ccoomm

990011 SSiirr FFrraanncciiss DDrraakkee BBllvvdd,, KKeennttffiieelldd,, CCAA 9944990044

Pacific Union International Luxury Real Estate Report Q2. 2011

HOME COMPARISON & CITY STATSA Member Of Real Living

Pacific Union International Luxury Real Estate Report Q2. 2011

HOME COMPARISONA Member Of Real Living

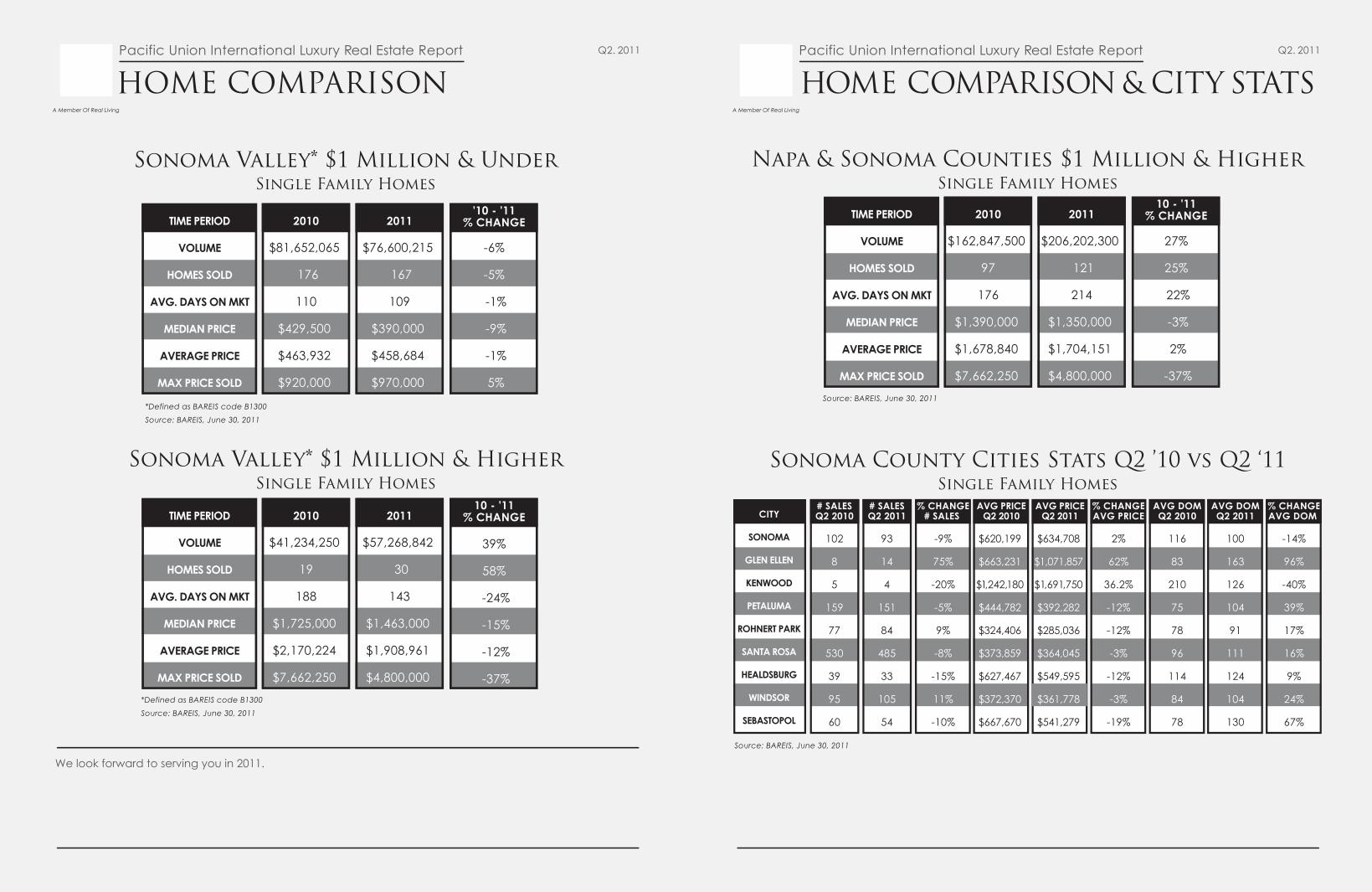

Napa & Sonoma Counties $1 Million & HigherSingle Family Homes

Source: BAREIS, June 30, 2011

Sonoma County Cities Stats Q2 ’10 vs Q2 ‘11Single Family Homes

Sonoma Valley* $1 Million & HigherSingle Family Homes

*Defined as BAREIS code B1300

Source: BAREIS, June 30, 2011

2010

$41,234,250

19

188

$1,725,000

$2,170,224

$7,662,250

2011

$57,268,842

30

143

$1,463,000

$1,908,961

$4,800,000

10 - '11% CHANGE

39%

58%

-24%

-15%

-12%

-37%

TIME PERIOD

VOLUME

HOMES SOLD

AVG. DAYS ON MKT

MEDIAN PRICE

AVERAGE PRICE

MAX PRICE SOLD

2010

$81,652,065

176

110

$429,500

$463,932

$920,000

2011

$76,600,215

167

109

$390,000

$458,684

$970,000

'10 - '11% CHANGE

-6%

-5%

-1%

-9%

-1%

5%

TIME PERIOD

VOLUME

HOMES SOLD

AVG. DAYS ON MKT

MEDIAN PRICE

AVERAGE PRICE

MAX PRICE SOLD

Sonoma Valley* $1 Million & UnderSingle Family Homes

*Defined as BAREIS code B1300

Source: BAREIS, June 30, 2011

# SALESQ2 2010

102

8

5

159

77

530

39

95

60

# SALESQ2 2011

93

14

4

151

84

485

33

105

54

% CHANGE# SALES

-9%

75%

-20%

-5%

9%

-8%

-15%

11%

-10%

AVG PRICEQ2 2010

$620,199

$663,231

$1,242,180

$444,782

$324,406

$373,859

$627,467

$372,370

$667,670

AVG PRICEQ2 2011

$634,708

$1,071,857

$1,691,750

$392,282

$285,036

$364,045

$549,595

$361,778

$541,279

% CHANGEAVG PRICE

2%

62%

36.2%

-12%

-12%

-3%

-12%

-3%

-19%

AVG DOMQ2 2010

116

83

210

75

78

96

114

84

78

AVG DOMQ2 2011

100

163

126

104

91

111

124

104

130

% CHANGEAVG DOM

-14%

96%

-40%

39%

17%

16%

9%

24%

67%

CITY

SONOMA

GLEN ELLEN

KENWOOD

PETALUMA

ROHNERT PARK

SANTA ROSA

HEALDSBURG

WINDSOR

SEBASTOPOL

Source: BAREIS, June 30, 2011

2010

$162,847,500

97

176

$1,390,000

$1,678,840

$7,662,250

2011

$206,202,300

121

214

$1,350,000

$1,704,151

$4,800,000

10 - '11% CHANGE

27%

25%

22%

-3%

2%

-37%

TIME PERIOD

VOLUME

HOMES SOLD

AVG. DAYS ON MKT

MEDIAN PRICE

AVERAGE PRICE

MAX PRICE SOLD

WWee llooookk ffoorrwwaarrdd ttoo sseerrvviinngg yyoouu iinn 22001111..

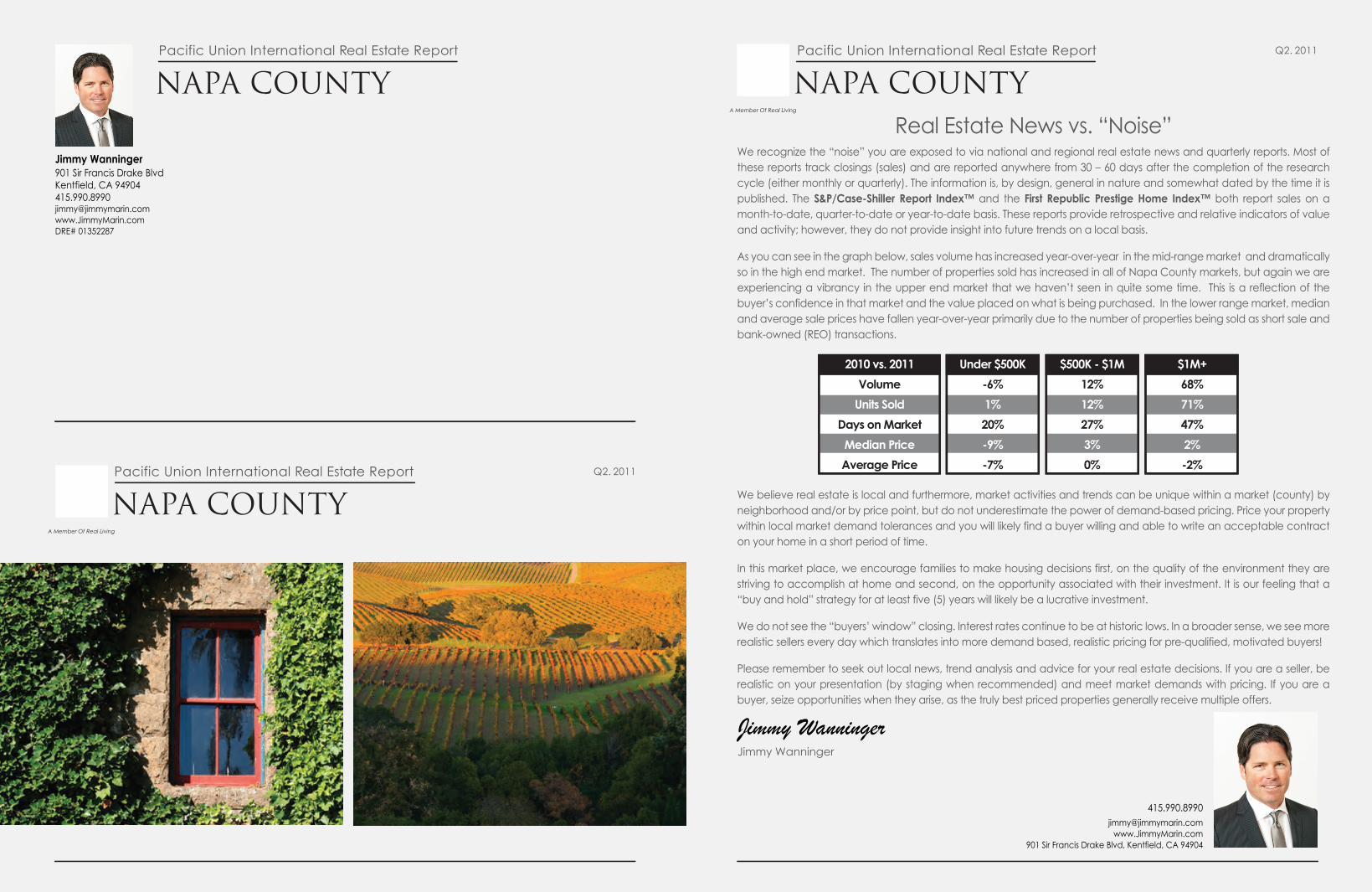

Real Estate News vs. “Noise”We recognize the “noise” you are exposed to via national and regional real estate news and quarterly reports. Most of these reports track closings (sales) and are reported anywhere from 30 – 60 days after the completion of the research cycle (either monthly or quarterly). The information is, by design, general in nature and somewhat dated by the time it is published. The S&P/Case-Shiller Report Index™ and the First Republic Prestige Home Index™ both report sales on a month-to-date, quarter-to-date or year-to-date basis. These reports provide retrospective and relative indicators of value and activity; however, they do not provide insight into future trends on a local basis.

As you can see in the graph below, sales volume has increased year-over-year in the mid-range market and dramatically so in the high end market. The number of properties sold has increased in all of Napa County markets, but again we are experiencing a vibrancy in the upper end market that we haven’t seen in quite some time. This is a reflection of the buyer’s confidence in that market and the value placed on what is being purchased. In the lower range market, median and average sale prices have fallen year-over-year primarily due to the number of properties being sold as short sale and bank-owned (REO) transactions.

We believe real estate is local and furthermore, market activities and trends can be unique within a market (county) by neighborhood and/or by price point, but do not underestimate the power of demand-based pricing. Price your property within local market demand tolerances and you will likely find a buyer willing and able to write an acceptable contract on your home in a short period of time.

In this market place, we encourage families to make housing decisions first, on the quality of the environment they are striving to accomplish at home and second, on the opportunity associated with their investment. It is our feeling that a “buy and hold” strategy for at least five (5) years will likely be a lucrative investment.

We do not see the “buyers’ window” closing. Interest rates continue to be at historic lows. In a broader sense, we see more realistic sellers every day which translates into more demand based, realistic pricing for pre-qualified, motivated buyers!

Please remember to seek out local news, trend analysis and advice for your real estate decisions. If you are a seller, be realistic on your presentation (by staging when recommended) and meet market demands with pricing. If you are a buyer, seize opportunities when they arise, as the truly best priced properties generally receive multiple offers.

A Member Of Real Living

Pacific Union International Real Estate ReportPacific Union International Real Estate Report Q2. 2011

NAPA COUNTY

Pacific Union International Real Estate Report Q2. 2011

NAPA COUNTY

NAPA COUNTYA Member Of Real Living

Under $500K

-6%

1%

20%

-9%

-7%

$500K - $1M

12%

12%

27%

3%

0%

$1M+

68%

71%

47%

2%

-2%

2010 vs. 2011

Volume

Units Sold

Days on Market

Median Price

Average Price

Jimmy Wanninger!iimmmmyy WWaannnniinnggeerr

!iimmmmyy WWaannnniinnggeerr990011 SSiirr FFrraanncciiss DDrraakkee BBllvvddKKeennttffiieelldd,, CCAA 9944990044441155..999900..88999900jjiimmmmyy@@jjiimmmmyymmaarriinn..ccoommwwwwww..!iimmmmyyMMaarriinn..ccoommDDRREE## 0011335522228877

441155..999900..88999900jjiimmmmyy@@jjiimmmmyymmaarriinn..ccoommwwwwww..!iimmmmyyMMaarriinn..ccoomm

990011 SSiirr FFrraanncciiss DDrraakkee BBllvvdd,, KKeennttffiieelldd,, CCAA 9944990044

Pacific Union International Real Estate Report Q2. 2011

HOME COMPARISON & CITY STATSA Member Of Real Living

Pacific Union International Real Estate Report Q2. 2011

HOME COMPARISONA Member Of Real Living

Napa City Stats Q2 2010 vs Q2 2011# SALESQ2 2010

206

81

15

19

6

0

2

# SALESQ2 2011

232

68

11

23

5

0

0

% CHANGE# SALES

13%

-16%

-27%

21%

-17%

0%

-100%

AVG PRICEQ2 2010

$420,881

$341,267

$687,065

$1,144,284

$651,000

$0

$762,500

AVG PRICEQ2 2011

$461,523

$277,468

$732,182

$1,278,792

$576,732

$0

$0

% CHANGEAVG PRICE

9.7%

-18.7%

7%

12%

-11%

N/A

-100%

AVG DOMQ2 2010

104

81

224

103

154

0

46

AVG DOMQ2 2011

135

80

151

228

143

0

0

% CHANGEAVG DOM

30%

-1%

-33%

121%

-7%

N/A

-100%

CITY

NAPA

CALISTOGA

ST. HELENA

YOUNTVILLE

RUTHERFORD

ANGWIN

AMERICANCANYON

Source: BAREIS, June 30, 2011

Napa County $500K & Under - Single Family Homes

Source: BAREIS, June 30, 2011

Apr - Jun '09

$70,121,609

230

88

$315,000

$304,877

$500,000

Apr - Jun '10

$83,717,831

262

87

$325,000

$319,534

$500,000

Apr - Jun '11

$73,962,630

256

101

$285,000

$288,917

$500,000

'09 - '10% Change

19%

14%

-1%

3%

4.8%

0%

'10 - '11% Change

-12%

-2%

16%

-12%

-10%

0%

TIME PERIOD

VOLUME

HOMES SOLD

AVG. DAYS ON MKT

MEDIAN PRICE

AVERAGE PRICE

MAX PRICE SOLD

Napa County $1 Million & Higher - Single Family Homes

Source: BAREIS, June 30, 2011

Apr - Jun '09

$31,394,168

18

121

$1,593,334

$1,744,120

$3,450,000

Apr - Jun '10

$29,266,250

15

196

$1,420,000

$1,951,083

$3,900,000

Apr - Jun '11

$56,655,900

30

300

$1,515,000

$1,888,530

$4,775,000

'09 - '10% Change

-7%

-17%

62%

-11%

12%

13%

'10 - '11% Change

94%

100%

53%

7%

-3%

22%

TIME PERIOD

VOLUME

HOMES SOLD

AVG. DAYS ON MKT

MEDIAN PRICE

AVERAGE PRICE

MAX PRICE SOLD

Napa County $500K - $1 Million - Single Family Homes

Source: BAREIS, June 30, 2011

Apr - Jun '09

$42,401,750

62

112

$635,000

$683,899

$1,000,000

Apr - Jun '10

$40,123,471

60

130

$637,000

$668,725

$995,000

Apr - Jun '11

$42,575,354

62

174

$666,500

$686,699

$965,000

'09 - '10% Change

-5%

-3%

16%

0.3%

-2.2%

-1%

'10 - '11% Change

6%

3%

34%

5%

3%

-3%

TIME PERIOD

VOLUME

HOMES SOLD

AVG. DAYS ON MKT

MEDIAN PRICE

AVERAGE PRICE

MAX PRICE SOLD

WWee llooookk ffoorrwwaarrdd ttoo sseerrvviinngg yyoouu iinn 22001111..

Pacific Union International Real Estate Report

A Member Of Real Living

Q2. 2011

SAN FRANCISCO

Pacific Union International Real Estate Report Q2. 2011

SAN FRANCISCO

Pacific Union International Real Estate Report

SAN FRANCISCOA Member Of Real Living

TENANCIES IN COMMON

CONDOMINIUMS

SINGLE FAMILY HOMESAs of June 30, 2011

Tenancies-inCommon

7%

Single FamilyHomes

48%Condos &

Co-ops45%

“All politics is local,” the memorable one-liner coined by iconic House Speaker Tip O’Neill, is a concept appropriately convertible to the often-elusive practice of divining general real estate pricing and direction. Pundits’ pronouncements regarding national, state-wide and even “Bay Area-wide” real estate valuation and trends too often ignore the myriad and substantial differences between properties situated in, say, Presidio Heights vs. Pittsburg (CA or PA), Noe Valley vs. Newark (CA or NJ), etc.

Accordingly, when faced with occasionally ominous proclamations – even from such well-regarded analysts as S&P/Case-Shiller – that “San Francisco” property values are going this way or that, careful and discriminating readers will take into account that S&P/Case-Shiller’s “San Francisco” is, in actuality, a combination of San Francisco, Contra Costa, San Mateo, Marin and Alam-eda counties. The disparities in terms of business base, cultural offerings, public services/infrastructure, economic vitality and general life-style, amenities, land scarcity and other factors between and among these five counties that influence real estate values are so striking as to call into question the usefulness of these predictions for the typical home-buyer and home-seller.

So where did the city and county of San Francisco stand at the end of Q2 2011? Carrying forward the overall performance of condos in Q1, Year-to-Date Q1/Q2 figures reported to the MLS showed robust increases in number of units sold (in all price ranges) versus Q1/Q2 2010, even as median sales price trended modestly downward. An appreciably higher number of under-$1M single family homes sold YTD 2011 than in Q1/Q2 2010, the median price (as with condos) slightly lower; volume and median sales price of higher-end SFHs were off to a somewhat great extent vs. 2010.

Condos – and, remarkably enough, higher-end condos – moved particularly well during the first half of 2011 as insightful and well-advised condo owners priced their units to sell.

As was the case when we closed out Q1, opportunities (for home buyers and sellers alike) abound as we enter Q3. And again contributing to an atmosphere of success are the still unusually attractive home mortgage rates, though speculation continues as to how long they will remain in the basement.

In any event, the prudent and perceptive buyer and seller will look behind and beyond real estate headlines – whether doom and gloom or breathlessly positive – and recognize that they may have limited (and perhaps even no) application to his or her particular situation. Because, like politics, “all real estate is local.”

Sincerely,

Q1/Q2 2011 YTD vs. Q1/Q2 2010, City-wide

remained even

Jimmy Wanninger!iimmmmyy WWaannnniinnggeerr

!iimmmmyy WWaannnniinnggeerr990011 SSiirr FFrraanncciiss DDrraakkee BBllvvddKKeennttffiieelldd,, CCAA 9944990044441155..999900..88999900jjiimmmmyy@@jjiimmmmyymmaarriinn..ccoommwwwwww..!iimmmmyyMMaarriinn..ccoommDDRREE## 0011335522228877

441155..999900..88999900jjiimmmmyy@@jjiimmmmyymmaarriinn..ccoommwwwwww..!iimmmmyyMMaarriinn..ccoomm

990011 SSiirr FFrraanncciiss DDrraakkee BBllvvdd,, KKeennttffiieelldd,, CCAA 9944990044

Q2. 2011

A Member Of Real Living

Pacific Union International Real Estate Report Q2. 2011

MEDIAN PRICEA Member Of Real Living

Pacific Union International Real Estate Report

homes sold comparison

Second Quarter Median Price ByProperty Type And Neighborhood

TENANCIES IN COMMON

CONDOMINIUMS

SINGLE FAMILY HOMES

San Francisco Units Sold by Property Typeand Neighborhood Q2 2011

TENANCIES IN COMMON

CONDOMINIUMS

SINGLE FAMILY HOMES

Source: SFAR MLS, June 30, 2011

Under $1 Million

$296,839,038

477

66

$624,000

$622,304

$1-3 Million

$243,069,675

157

47

$1,350,000

$1,548,214

$3 Million+

$106,612,769

24

88

$3,502,500

$4,442,199

'10 - '11% CHANGE

-5%

0%

25%

-7%

-5%

'10 - '11% CHANGE

-9%

-8%

-18%

-4%

0%

'10 - '11% CHANGE

-14%

-14%

42%

-7%

0%

Apr - Jun 2011

VOLUME

UNITS SOLD

AVERAGE DOM

MEDIAN PRICE

AVERAGE PRICE

Under $1 Million

$289,169,929

483

76

$599,000

$598,696

$1-2 Million

$120,588,969

93

57

$1,207,500

$1,296,656

$2 Million+

$80,465,500

28

74

$2,599,000

$2,873,768

'10 - '11% CHANGE

-12%

-9%

4%

-4%

-4%

'10 - '11% CHANGE

5%

4%

12%

-3%

0%

'10 - '11% CHANGE

93%

100%

10%

-8%

-3%

Apr - Jun 2011

VOLUME

UNITS SOLD

AVERAGE DOM

MEDIAN PRICE

AVERAGE PRICE

Single Family Homes Q2 2011 Sold Comparison

Condominiums Q2 2011 Sold Comparison

Tenancies In Common Q2 2011 Sold Comparison

Source: SFAR MLS, June 30, 2011

Source: SFAR MLS, June 30, 2011

$500K and under

$13,389,276

32

105

$427,000

$418,415

$500K and higher

$59,274,809

68

72

$727,000

$871,688

'10 - '11% CHANGE

-1%

-6%

4%

2%

5%

'10 - '11% CHANGE

78%

48%

-18%

10%

20%

Apr - Jun 2011

VOLUME

UNITS SOLD

AVERAGE DOM

MEDIAN PRICE

AVERAGE PRICE

Source: SFAR MLS, June 30, 2011

‘10‘11

$2.95M

$1.02M

$1.33M

$3.1M

$2M $1.27M $1.4M

$723K

$570K

$1.18M $1.25M

$762K $827K

$995K

$734K

$469K

$1.06M

$639K

$567K$588K$675K

$1.3M

$634K

$700K

$654K

$685K$700K

$540K

$1.09M

$699K

‘10

‘11 ‘10 ‘11 ‘10 ‘11‘10 ‘11

NOB/RUSSIAN/TELEGRAPH HILL

LOWER PACHEIGHTS/

HAYES/NOPA

NOE/CASTRO/HAIGHT

RICHMOND/SEACLIFF

PAC HEIGHTS/MARINA

$790K $758K $731K $660K $900K $785K $595K $542K $480K $424K$345K$357K$330K$338K

$393K$430K$435K

$723K

$835K

$713K

$475K

$615K

$470K

$642K

$501K

ST. FRANCIS WOOD/MIRALOMA/FOREST HILL

SUNSET/PARKSIDE

SOMA/MISSION/POTRERO

LAKE MERCED/INGLESIDE

BAYVIEW/EXCELSIOR

‘10 ‘11 ‘10

‘11‘10 ‘11 ‘10 ‘11

‘10‘11

SOMA/MISSION/POTRERO

NOE/CASTRO/HAIGHT

NOB/RUSSIAN/TELEGRAPH HILL

ST. FRANCIS WOOD/MIRALOMA/FOREST HILL

LAKE MERCED/INGLESIDE

RICHMOND/SEACLIFF

SUNSET/PARKSIDE

PAC HEIGHTS/MARINA

LOWER PAC HEIGHTS/HAYES/NOPA

BAYVIEW/EXCELSIOR

6494

128114 106

19

10 1065 46

1226

8

48

19

27

68

11

96

160

0

10200

186

26

213

13

Real Estate News v. Real Estate “Noise”There are two types of real estate information out there in the media. One we would call “noise” and is typically reported on a quarterly basis and covers a region or more often the nation. Most of these reports track closed sales and are reported anywhere from thirty to sixty days after the completion of the research cycle, either monthly or quarterly. The information is, by design, general in nature and somewhat dated by the time it is published. The S&P/Case-Shiller Report Index™ and the First Republic Prestige Home Index™ are two examples of this type of reporting. These reports provide retrospective and relative indicators of value and activity; however, they do not provide insight into future trends on a local basis.

The other type of real estate information is provided by experts who work day to day in a local market. This information often looks similar to the information we provide in this quarterly newsletter. We believe that real estate is local, and further, that market activities and trends can be unique within a marketplace or county depending upon specific neighborhoods or even specific price points. We also believe that properties under contract (pending sales) or new escrows are the industry’s most meaningful indicator of near term trends.

Our review of new escrows in the East Bay* real estate market reveals encouraging movement even though early summer is not usually considered the peak sales season. The chart below illustrates current trends by percentage for properties currently “under contract” versus the same time period twelve and twenty-four months ago. While specific neighborhoods may be performing differently and prices may be lower than meet sellers’ expectations, our markets under the million dollar price point are continuing to accelerate, at least in terms of units “under contract”.

As the Months of Inventory figures above indicate, the listing inventory in most price ranges is meeting current demand. Almost half of the sales in the second quarter closed at or above the original list price with an average of sixteen days on the market, confirming that the market responds quickly to well-priced properties and that a realistic list price is critical to attracting today’s qualified buyer. Do not underestimate the power of demand-based pricing. Price your property within local market demand tolerances and you will likely ratify a new escrow in your first three weeks on the market. Flirt with the high end of your price range and prepare to be part of inventory statistics.

In this marketplace, we encourage buyers to make housing decisions based first on the quality of the home environment they are seeking and second on the opportunity associated with their investment. It is our feeling that a “buy and hold” strategy for at least five years will likely make today’s home purchase a lucrative investment. We do not see the “buyers’ window” closing. In a broader sense, we see more realistic sellers everyday, which translates into more demand-based, realistic pricing for pre-approved, motivated buyers.

Please remember to seek out local news, trend analysis and professional advice for your real estate decisions. If you are a seller, be realistic about your presentation; stage your home when it is recommended andmeet market demands with realistic pricing. If you are a buyer, seize opportunities when theyarise, as the best priced properties continue to move quickly and often receive multiple offers.

Sincerely,

A Member Of Real Living

Pacific Union International Real Estate Report Q2. 2011

EAST BAY

Pacific Union International Real Estate Report Q2. 2011

EAST BAY

Pacific Union International Real Estate Report

EAST BAYA Member Of Real Living

All Price Ranges

38.5%

39.2%

30.9%

8.9%

2.1

$ 500K to $1 Million

12.0%

26.0%

19.8%

6.4%

1.9

$1 Million and Up

34.8%

-22.5%

-7.7%

-8.9%

3.1

Single Family Homes

Under Contract (v 24 months ago)

Under Contract (v 12 months ago)

Listing Inventory (v 24 months ago)

Listing Inventory (v 12 months ago)

Months of Inventory

Source: EBRD June 30, 2011 *Oakland zip codes 94602, 94609, 94610, 94611, 94618, 94619, 94705, Piedmont, Berkeley, Albany, Kensington and El Cerrito.

!ee llooookk ffoorrwwaarrdd ttoo sseerrvviinngg yyoouu iinn 22001111..

Jimmy WanningerJJiimmmmyy !aannnniinnggeerr

!iimmmmyy WWaannnniinnggeerr990011 SSiirr FFrraanncciiss DDrraakkee BBllvvddKKeennttffiieelldd,, CCAA 9944990044441155..999900..88999900jjiimmmmyy@@jjiimmmmyymmaarriinn..ccoommwwwwww..JJiimmmmyyMMaarriinn..ccoommDDRREE## 0011335522228877

441155..999900..88999900jjiimmmmyy@@jjiimmmmyymmaarriinn..ccoommwwwwww..JJiimmmmyyMMaarriinn..ccoomm

990011 SSiirr FFrraanncciiss DDrraakkee BBllvvdd,, KKeennttffiieelldd,, CCAA 9944990044

Pacific Union International Real Estate Report Q2. 2011

HOMES SOLD COMPARISONA Member Of Real Living

Pacific Union International Real Estate Report Q2. 2011

HOMES SOLD COMPARISONA Member Of Real Living

Kensington All Prices - Single Family Homes

Source: EBRD

Apr - Jun '09

$9,377,400

13

40

$775,000

$721,338

$975,000

Apr - Jun '10

$13,573,000

19

23

$750,000

$714,368

$935,000

Apr - Jun '11

$10,097,000

14

27

$702,500

$721,214

$1,275,000

'09 - '10% Change

45%

46%

-43%

-3%

-1%

-4%

'10 - '11% Change

-26%

-26%

17%

-6%

1%

36%

TIME PERIOD

VOLUME

HOMES SOLD

AVG. DAYS ON MKT

MEDIAN PRICE

AVERAGE PRICE

MAX PRICE SOLD

El Cerrito All Prices - Single Family Homes

Source: EBRD

Apr - Jun '09

$27,821,120

50

35

$542,500

$556,422

$910,000

Apr - Jun '10

$34,536,272

63

30

$560,000

$548,194

$834,136

Apr - Jun '11

$27,446,275

53

35

$487,000

$517,854

$875,000

'09 - '10% Change

24%

26%

-14%

3%

-1%

-8%

'10 - '11% Change

-21%

-16%

17%

-13%

-6%

5%

TIME PERIOD

VOLUME

HOMES SOLD

AVG. DAYS ON MKT

MEDIAN PRICE

AVERAGE PRICE

MAX PRICE SOLD

Piedmont All Prices - Single Family Homes

Source: EBRD

Apr - Jun '09

$35,920,600

26

37

$1,141,250

$1,381,561

$3,100,000

Apr - Jun '10

$35,328,000

25

19

$1,280,000

$1,413,120

$3,150,000

Apr - Jun '11

$64,658,048

42

20

$1,350,500

$1,539,477

$4,500,000

'09 - '10% Change

-1.6%

-4%

-49%

12%

2%

2%

'10 - '11% Change

83%

68%

5%

6%

9%

43%

TIME PERIOD

VOLUME

HOMES SOLD

AVG. DAYS ON MKT

MEDIAN PRICE

AVERAGE PRICE

MAX PRICE SOLD

Albany All Prices - Single Family Homes

Source: EBRD

Apr - Jun '09

$14,404,830

23

45

$620,000

$626,296

$867,000

Apr - Jun '10

$12,629,580

20

28

$585,700

$631,479

$975,000

Apr - Jun '11

$11,619,400

19

28

$585,000

$611,547

$1,089,000

'09 - '10% Change

-12%

-13%

-38%

-6%

1%

12%

'10 - '11% Change

-8%

-5%

0%

0%

-3%

12%

TIME PERIOD

VOLUME

HOMES SOLD

AVG. DAYS ON MKT

MEDIAN PRICE

AVERAGE PRICE

MAX PRICE SOLD

Berkeley All Prices - Single Family Homes

Source: EBRD

Apr - Jun '09

$98,352,844

138

34

$626,707

$712,701

$2,505,000

Apr - Jun '10

$124,789,616

152

24

$727,500

$820,984

$2,300,000

Apr - Jun '11

$107,539,950

148

29

$655,000

$726,621

$2,555,000

'09 - '10% Change

27%

10%

-29%

16%

15%

-8%

'10 - '11% Change

-14%

-3%

21%

-10%

-11%

11%

TIME PERIOD

VOLUME

HOMES SOLD

AVG. DAYS ON MKT

MEDIAN PRICE

AVERAGE PRICE

MAX PRICE SOLD

Oakland Area* All Prices - Single Family Homes

Source: EBRD

*Defined by Oakland zipcodes: 94602, 94609, 94610, 94611, 94618, 94619, 94705

Apr - Jun '09

$153,357,992

240

35

$632,500

$638,991

$2,000,000

Apr - Jun '10

$196,325,373

308

32

$610,000

$637,420

$2,250,000

Apr - Jun '11

$170,309,174

276

41

$572,500

$617,062

$2,405,000

'09 - '10% Change

28%

28%

-9%

-4%

0%

13%

'10 - '11% Change

-13%

-10%

28%

-6%

-3%

7%

TIME PERIOD

VOLUME

HOMES SOLD

AVG. DAYS ON MKT

MEDIAN PRICE

AVERAGE PRICE

MAX PRICE SOLD

www.JimmyMarin.com

Follow Jimmy Marin: