javier lozano 1 advanced applied macroeconomics economics of the exchange rate javier lozano...

TRANSCRIPT

1Javier LozanoJavier Lozano

Advanced Applied MacroeconomicsAdvanced Applied Macroeconomics

Economics of the Exchange RateEconomics of the Exchange Rate

Javier Lozano

Universitat de les Illes Balears

Master and PhD programs in Tourism and Environmental Economics

University of the Balearic Islands

2Javier LozanoJavier Lozano

Learning objectives

• We shall study several topics on international macroeconomics.– How is the exchange rate determined?– Classification of exchange rate regimes– Main criteria for adoption of exchange rate regimes– Relationship between fiscal policy, monetary policy and ER– Sustainability of current account imbalances– Real world topics:

• EMS crisis (1992-1995)• Mexican crisis (1994)• Asian crisis (1997)• Argentina’s crisis (2001)• Current international imbalances

• Combination of macro theory, data analysis and readings.

3Javier LozanoJavier Lozano

Today’s session

• Basic definitions and motivation

• The Uncovered Interest Parity (UIP)

• Relationship between monetary policy and exchange rate

4Javier LozanoJavier Lozano

Basic definitions and motivation

5Javier LozanoJavier Lozano

Definitions

• Exchange rate: relative price of two currencies. Relative value of assets denominated in different currencies

• $/€ €/$

• Flexible/fixed exchange rates

• Depreciation/appreciation

• Devaluation/revaluation

6Javier LozanoJavier Lozano

Motivation

• ERs play a key role in international transactions:– Goods & services: relative prices

(competitiveness)– Assets: rates of return

• ER is one of the main policy variables for open economies– Important for unemployment– Important for inflation

• International tourism

7Javier LozanoJavier Lozano

• Short-run: UIP

• Long-run: Purchasing Power Parity (PPP)

• Long-run: beyond PPP

Models of ER determination

8Javier LozanoJavier Lozano

Uncovered Interest Parity (UIP)

9Javier LozanoJavier Lozano

Uncovered Interest Parity

Main determinants of ER in the short-run

International transactions

Goods and services (current account)

Assets (capital account)

Asset approach to ER determination

10Javier LozanoJavier Lozano

Uncovered Interest Parity

• With no restrictions to capital flows, two assets of the same liquidity and risk should yield the same return even if they are denominated in different currencies

t

te

t

E

EERR

€,/$

€,/$1€,/$€$

11Javier LozanoJavier Lozano

Uncovered Interest Parity

t

et

E

ERR

€,/$

1€,/$€$ 11

Every investor is willing to hold € deposits instead of $ deposits

$ depreciates against € (€ appreciates relative to $)

Equality is restored

12Javier LozanoJavier Lozano

Uncovered Interest Parity

t

te

t

E

EERR

€,/$

€,/$1€,/$€$

approximation

t

et

E

ERR

€,/$

1€,/$€$ 11 exact condition

13Javier LozanoJavier Lozano

Interest Rates in US and Mexico

0

10

20

30

40

50

60

70

80

90

100

USMexico

Source: IFS

14Javier LozanoJavier Lozano

Interest Rates in US and Argentina

0

10

20

30

40

50

60

70

80

Q41994

Q41995

Q41996

Q41997

Q41998

Q41999

Q42000

Q42001

Q42002

Q42003

USArgentina

Source: IFS

15Javier LozanoJavier Lozano

UIP: Graphical Representation

Rates of return in $ terms

E$/€

E2$/€

E1$/€

E3$/€

R$

Return on $ deposits (in $ terms)

Expected return on € deposits (in $ terms)

t

te

t

E

EER

€,/$

€,/$1€,/$€

16Javier LozanoJavier Lozano

UIP: Changes in own interest rate

Rates of return in $ terms

E$/€

E1$/€

R1$ R2

$

E2$/€

Increases in own interest rate tend to appreciate our

currency

17Javier LozanoJavier Lozano

UIP: Changes in foreign interest rate

Rates of return in $ terms

E$/€

R$

E1$/€

Increases in foreign interest

rate tend to depreciate our

currency

E2$/€

18Javier LozanoJavier Lozano

UIP: Changes in future ER expectations

Rates of return in $ terms

E$/€

R$

E1$/€

Increases in expected future

ER tend to depreciate our

currency

E2$/€

19Javier LozanoJavier Lozano

What determines previous changes? (looking ahead)

• What does determine interest rates?– We will mainly focus on monetary policy

• What does determine expected future ER? – Long-run model of ER determination (PPP)– Sustainability of current account deficits– Same UIP

20Javier LozanoJavier Lozano

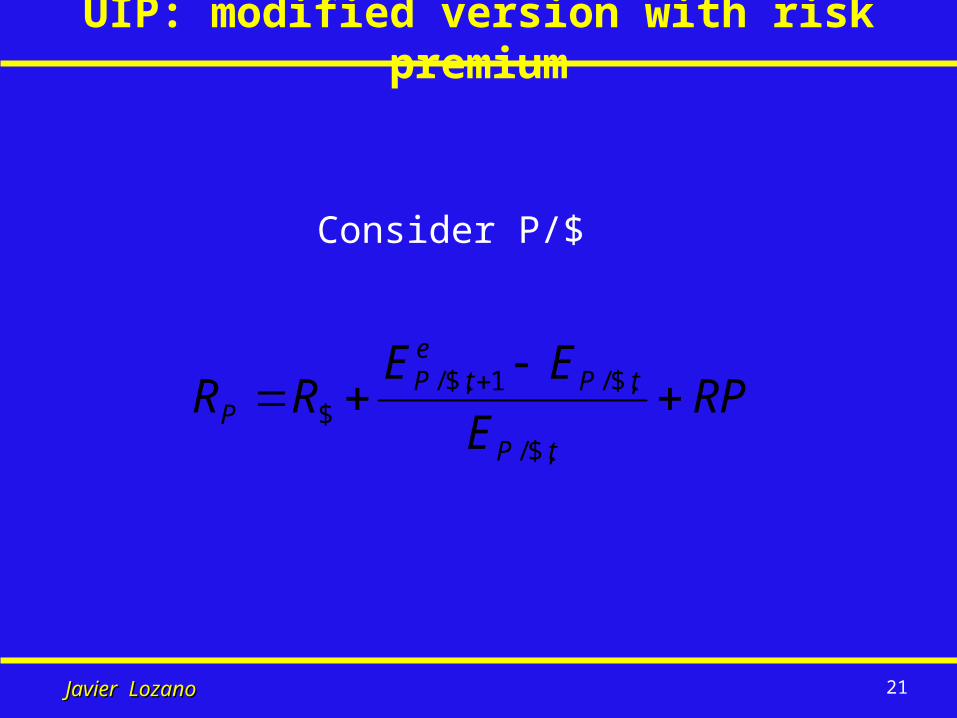

UIP: modified version with risk premium

• Previous discussion have neglected differences in risk (perfect substitutability)

• Differences in risk comparing two individual assets

• Differences in risk comparing two countries:

-Polítical risk

-Sovereign risk The risk that a host government may unilaterally repudiate its foreign obligations or may prevent local firms from honoring their foreign obligations. Sovereign risk is often regarded as a subset of political risk.

The risk that political and/or governmental actions may unfavorably influence the value of an investment

21Javier LozanoJavier Lozano

UIP: modified version with risk premium

RPE

EERR

tP

tPe

tPP

$,/

$,/1$,/$

Consider P/$

22Javier LozanoJavier Lozano

Interest rates in US and Argentina

0

10

20

30

40

50

60

70

80Q

4 19

94

Q3

1995

Q2

1996

Q1

1997

Q4

1997

Q3

1998

Q2

1999

Q1

2000

Q4

2000

Q3

2001

Q2

2002

Q1

2003

Q4

2003

USArgentina (P)Argentina ($)

Source: IFS

RPE

EERR

tP

tPe

tPP

$,/

$,/1$,/$

RPRRP $

23Javier LozanoJavier Lozano

UIP: Changes in Risk Premium

EP/$

RP

E1P/$

Increase in risk premium tend to depreciate our

currencyE2

P/$

RPE

EER

t

te

t

€,/$

€,/$1€,/$€

24Javier LozanoJavier Lozano

Monetary Policy and the ER

25Javier LozanoJavier Lozano

Monetary Policy and the ER

• Monetary Policy

• Short run relationship between MP and ER

• Expected ER and expected interest rates

• Long run relationship between MP and ER– Money supply and prices– Prices and ER (PPP)

• Fiscal policy, monetary policy and the ER

26Javier LozanoJavier Lozano

Monetary Policy and the ERMonetary Policy

27Javier LozanoJavier Lozano

What is money?

• Characteristics of money– Medium of exchange (liquidity)– Unit of account– Store of value

• Monetary assets– Currency (coins and notes)– Bank deposits on which checks may be written

M1

28Javier LozanoJavier Lozano

Money Market

• Money supply: determined by central bank

• Money demand: Md=P.L(R,Y)

• Money market equilibrium: – Ms=P.L(R,Y) (nominal terms)– Ms/P=L(R,Y) (real terms)

29Javier LozanoJavier Lozano

Money market equilibrium

Nominal interest rate

Real money supply and demand

Ms/P

L(R,Y)

R

30Javier LozanoJavier Lozano

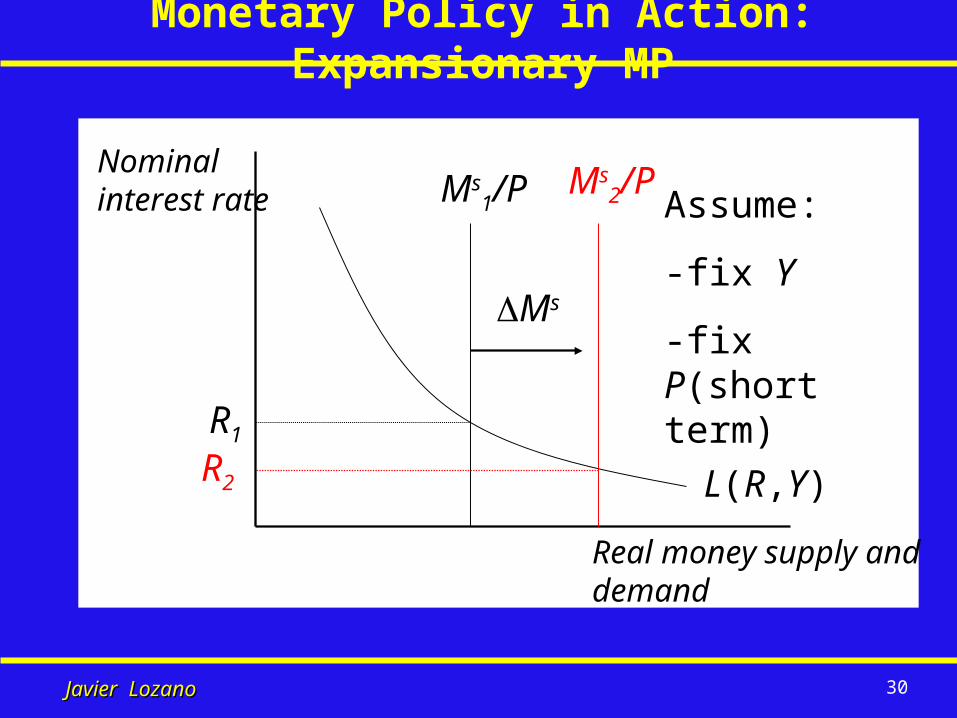

Monetary Policy in Action: Expansionary MP

Nominal interest rate

Real money supply and demand

Ms1/P

L(R,Y)

R1

Ms2/P

Ms

R2

Assume:

-fix Y

-fix P(short term)

31Javier LozanoJavier Lozano

Monertary Policy in Action: Contractionary MP

Nominal interest rate

Real money supply and demand

Ms1/P

L(R,Y)

R1

Ms2/P

M

s

R2

Assume:

-fix Y

-fix P(short term)

32Javier LozanoJavier Lozano

Monetary Policy: Summary

• Expansionary (easy, loose) MP:– Increase of Ms (increase of Ms growth rate)– Decrease of R (of short term nominal interest

rate)

• Contractionary (tight) MP:– Reduction of Ms (reduction of Ms growth rate)– Increase of R (of short term nominal interest

rate)

33Javier LozanoJavier Lozano

Monetary Policy: Short and Long Run Effects

• We define:– Short run: fixed (sticky) prices– Long run: flexible prices

• Effects of monetary policy:– Short run: mostly on real output and

employment. Less in prices– Long run: no effect on output and employment.

Proportional variation in price level (money neutrality)

34Javier LozanoJavier Lozano

Monetary Policy: Short and Long Run Effects

P

Y

AD

AS (short run)

AS (long run)

easytight

Y

35Javier LozanoJavier Lozano

Monetary Policy and the ERShort Run Relationship

36Javier LozanoJavier Lozano

MP & ER in the short run: assumptions

• Fixed price (definition of short run)

• Fixed output (not necessary)

37Javier LozanoJavier Lozano

MP & ER in the short run: graphical rep.

0

incr

easi

ng

Ms2/P

E2$/€

Ms/P, L

Ms1/P

L

E$/€

E1$/€

Rates of return in $ terms

Expansionary MP causes ER

depreciation

38Javier LozanoJavier Lozano

MP & ER in the short run: graphical rep.

0

incr

easi

ng

Ms3/P

E3$/€

Ms/P, L

Ms1/P

L

E$/€

E1$/€

Rates of return in $ terms

Contractionary MP causes ER appreciation

39Javier LozanoJavier Lozano

MP & ER in the short run: impossible trinity

• It is not possible to meet the following three policy targets simultaneously:– Free capital mobility– Fixed exchange rate– Independent monetary policy

40Javier LozanoJavier Lozano

MP & ER in the short run: impossible trinity

• With free capital mobility (UIP holds) it is not possible to set RP (Ms) and EP/€ independently.

• Either:

– Set capital controls

– Let the ER change

– Subordinate MP to ER policy

Ms/P

EP/$

0

incr

easi

ng

Ms/P, L

L

EP/$

Ra. of ret. in Pesos

41Javier LozanoJavier Lozano

MP & ER in the short run: impossible trinity

Ms/P

EP/$

0

incr

easi

ng

Ms/P, L

L

EP/$

Ra. of ret. in Pesos

•Suppose we face an increase in risk premium or in foreign interest rate or depreciation

expectations emerge (fixed ER regime loses credibility)

•Fixed ER policy may be in conflict with other targets:

–Help economic recovery–Avoid high fiscal deficit

•Why want to keep ER fixed? (see later)

–Fight inflation (in case fall in foreign interest rates)

42Javier LozanoJavier Lozano

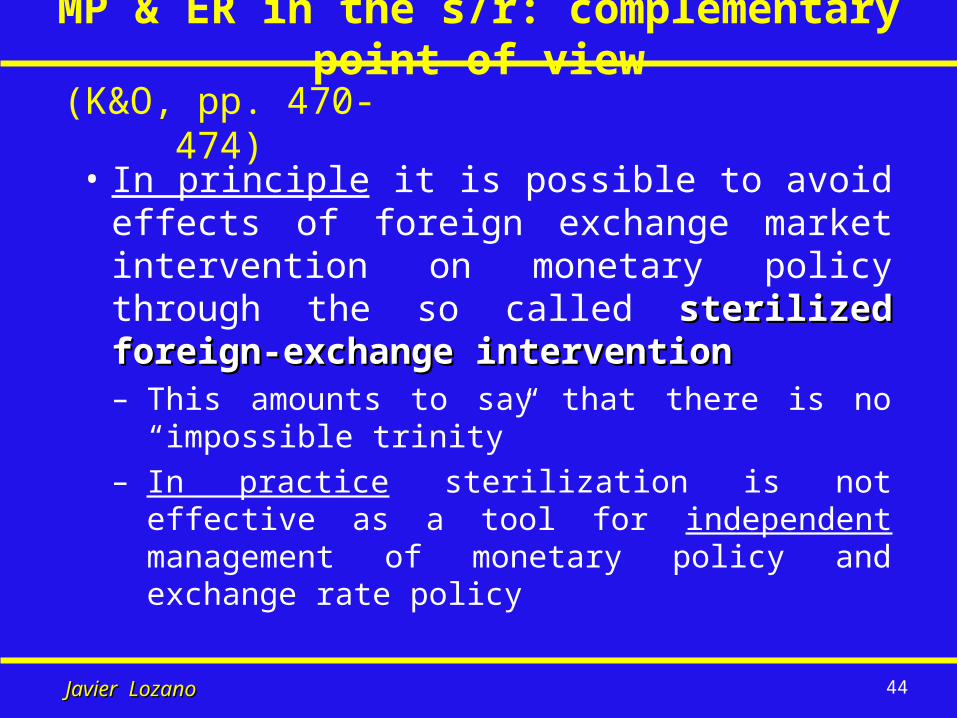

MP & ER in the s/r: complementary point of view

• Apart from Ms and R, the central bank has an apparently different instrument to control ER level: direct intervention in ER markets

If Mexican CB wants peso appreciation (wants to avoid

peso depreciation)

If Mexican CB wants peso depreciation (wants to avoid

peso appreciation)

buys pesos =sells $ assets

sells pesos=buys $ assets

Limited by $ reserves

Technically unlimited

(K&O, pp. 470-474)

43Javier LozanoJavier Lozano

MP & ER in the s/r: complementary point of view

• Are we really speaking about a different instrument?

buy pesos Ms RP Ep/$

UIP

sell pesos Ms RP Ep/$

(K&O, pp. 470-474)

44Javier LozanoJavier Lozano

MP & ER in the s/r: complementary point of view

• In principle it is possible to avoid effects of foreign exchange market intervention on monetary policy through the so called sterilized foreign-exchange interventionsterilized foreign-exchange intervention– This amounts to say that there is no “impossible

trinity”– In practice sterilization is not effective as a tool

for independent management of monetary policy and exchange rate policy

(K&O, pp. 470-474)

45Javier LozanoJavier Lozano

Interest Rates in US & Argentina and Foreign Exchange Reserves

0

10

20

30

40

50

60

70

80

0

5000

10000

15000

20000

25000

R$

Rp

Argentina'sforeignexchangereserves

Source: IFS

46Javier LozanoJavier Lozano

Interest Rates in US & Mexico and Foreign Exchange Reserves

0

10

20

30

40

50

60

70

80

90

100Q

1 19

90

Q2

1990

Q3

1990

Q4

1990

Q1

1991

Q2

1991

Q3

1991

Q4

1991

Q1

1992

Q2

1992

Q3

1992

Q4

1992

Q1

1993

Q2

1993

Q3

1993

Q4

1993

Q1

1994

Q2

1994

Q3

1994

Q4

1994

Q1

1995

Q2

1995

Q3

1995

Q4

1995

0

2

4

6

8

10

12

14

16

18

20

R$

Rp

mexican foreignexchange reserves

Source: IFS

47Javier LozanoJavier Lozano

Monetary Policy and the ERExpected ER and Expected Interest Rate

48Javier LozanoJavier Lozano

Expected ER and Expected Interest Rate

• Relationship between MP and ER is more complex than explained before.

• Important assumption made before: expected ER independent from monetary policy.

• In fact, the expected ER depends on MP. For instance, expected ER depends on expected interest rates differentials (expected monetary policies)

49Javier LozanoJavier Lozano

Expected ER and Expected Interest Rate

et

t

tt E

R

RE 1€,/$

$,

€,€,/$ 1

1

ete

t

ete

t ER

RE 2€,/$

1$,

1€,1€,/$ 1

1

ete

tt

ett

t ERR

RRE 2€,/$

1$,$,

1€,€,€,/$ 11

11

50Javier LozanoJavier Lozano

Expected ER and Expected Interest Rate

• Effects of interest rates changes on ER depend on whether they are interpreted as permanent or temporary

• Statements by monetary authorities are signals of future interest rates and therefore affect ER.

• An increase in interest rate could trigger an ER depreciation if the increase is lower than expected (if monetary policy is less tight than expected)

51Javier LozanoJavier Lozano

Monetary Policy and the ERLong Run Relationship

52Javier LozanoJavier Lozano

Monetary Policy and ER in the long run

monetary policy prices exchange

rate

53Javier LozanoJavier Lozano

Monetary Policy and ER in the long run

• First it is important to remember that domestic and foreign prices, as well as nominal ER interplay in the determination of a country’s price-competitiveness

• The real exchange rate is a synthetic indicator of price-competitiveness:

q$/€=(E$/€xPEU)/PUS

• In principle real appreciation is “bad” for growth and employment (real depreciation “good” for growth and employment) (we will qualify this statement later)

54Javier LozanoJavier Lozano

Monetary Policy and the ERLong Run Relationship Money Supply and Prices

55Javier LozanoJavier Lozano

MP and ER in l/r: Money Supply & Prices

• We can reasonably assume that in the long run increases in money supply have no positive effect on real variables, only on prices Ms P

• This implies that money growth (in excess of real economic growth) will eventually end up in inflation

56Javier LozanoJavier Lozano

MP and ER in l/r: Money Supply & Prices

Relationship between money growth rate and inflation for some selected Latinamerican countries (1980-1990)

0%

200%

400%

600%

800%

1000%

1200%

1400%

1600%

0% 200% 400% 600% 800% 1000% 1200%

average annual money growth rate

ann

ual

infl

atio

n r

ate

Bolivia

Peru

Argentina

Brazil

MexVen

ParChile

Source: IFS

57Javier LozanoJavier Lozano

Monetary Policy and the ERLong Run Relationship

Prices and ER (PPP)

58Javier LozanoJavier Lozano

MP and ER in l/r: Prices & ER

• Law of one price (LOOP): prices of the same good sold in two different countries should be equal when they are expressed in the same currency Pi

US= PiEUxE$/€

• Purchasing Power Parity (PPP): given a basket of goods (let us say the basket used to calculate the CPI) sold in two different countries, the price of this basket, expressed in the same currency, should be equal PUS= PEUxE$/€

59Javier LozanoJavier Lozano

MP and ER in l/r: Prices & ER

•Absolute PPP:EU

US

P

PE €/$

•Relative PPP: EUUSt

tt

E

EE

1€,/$

1€,/$€,/$

(can be derived mathematically) Imply q does

not change!

60Javier LozanoJavier Lozano

MP and ER in l/r: Prices & ER

Countries: Austria, Australia, Belgium, Germany, Italy, Spain, United Kingdom, Greece, Kenya, Mexico, Zimbabwe, Bolivia, Brazil, Argentina, Chile, Colombia, Tanzania, Cameroon, South Africa

-20

-10

0

10

20

30

40

50

60

70

80

-20 -10 0 10 20 30 40 50 60 70 80

inflation minus US inflation in 1999

annual exchange r

ate

deprecia

tion/a

pprecia

tion a

gain

st

$

in 1

999

45º line

Source: WDI

PPP does not hold in the short run...

61Javier LozanoJavier Lozano

MP and ER in l/r: Prices & ER...but it may be a reasonable rule of thumb for long term movements of nominal ER... (see

comments on p. 93 in O&R paper)

-20

80

180

280

380

480

580

680

780

880

-20 80 180 280 380 480 580 680 780 880

average annual inflation during 82-99 minus US average annual inflation during same period

aver

age

annu

al E

R d

ep/a

p du

ring

82-

99

Countries: Austria, Australia, Belgium, Germany, Italy, Spain, United Kingdom, Greece, Kenya, Mexico, Zimbabwe, Bolivia, Brazil, Argentina, Chile, Colombia, Tanzania, Cameroon, South Africa

Source: WDI

45º line

62Javier LozanoJavier Lozano

MP and ER in l/r: Prices & ER...albeit not in all cases even in the long run.

yen/$ real exchange rate (1949=100)

0

20

40

60

80

100

120

140

1949

1952

1955

1958

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

Source: IFS

63Javier LozanoJavier Lozano

MP and ER in l/r: Prices & ER

• Reasons for deviations from the PPP are different in the short and in the long run.

• Short run: nominal factors (price stickiness or price inertia)

• Long run: real factors

64Javier LozanoJavier Lozano

MP and ER in l/r: Prices & ER

• An economy with high inflation adopts a fixed ER to support antiinflationary policy (reason seen later). Given price inertia, domestic inflation keeps at a higher level than foreign inflation. This results in real appreciation.

• Given a fixed ER, domestic agents expect devaluation. These expectations accelerate domestic inflation. If government do not devaluate, a real appreciation will take place (see Obstfeld and Rogoff’s paper, page 83)

• In these cases real appreciation is “bad” for the economy because of loss of price-competitiveness

Some Cases of Short Run Deviations from PPP (case of real appreciation)

65Javier LozanoJavier Lozano

MP and ER in l/r: Prices & ER

• Changes in world preferences that increase demand for products your country produces.

• Increases in the quality of your products.• Shift in sectoral specialization to sectors of higher

world demand.• These cases imply a “good” real appreciation:

the goods & services you produce are more expensive (relative to those of foreign competition) because they are more valued.

• (more of this in K&O pp. 396-412)

Some reasons for Long Run Deviations from PPP (case of real appreciation)

66Javier LozanoJavier Lozano

Monetary Policy and the ER Fiscal Policy, Monetary Policy and the ER

67Javier LozanoJavier Lozano

Fiscal Policy, Monetary Policy and the ER

• Historically in many cases (e.g. Latin America during the 80’s) monetary policy has been subordinated to the finance of public expenditure (fiscal deficit monetization). Monetization leads to high inflation (see slide 56) and high depreciation rates of the currency.

• A country that wants to maintain a fixed ER should avoid suspicions of future monetization (low deficits+CB independence) that could trigger devaluation expectations. This is specially true if the country has bad reputation because of past monetization.

68Javier LozanoJavier Lozano

Sustainability of current account deficitshttp://www.stern.nyu.edu/globalmacro/

Macro resources

Lectures in macroeconomics

Chapter 1 and 3

69Javier LozanoJavier Lozano

Sustainability of current account deficits

• Again, what determines future (expected) ER?– Future expected interest rates differentials– Inflation differentials– Current account imbalances

• How log can a country have a current account deficit (and of which magnitude)? What are the determinants of CA sustainability?

70Javier LozanoJavier Lozano

-10

-5

0

5

10

15

ArgentinaMexicoThailand

CA

def

icit

as

% o

f G

DP

Source: WDI

Sustainability of current account deficits

Mexican crisis

Argentinian crisisAsian

crisis

Relevant question since most ER crisis are preceded by large CA deficits and result in sharp CA corrections, suggesting that those

CA deficits were not sustainable.

71Javier LozanoJavier Lozano

Sustainability of current account deficits

Argentina

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

1997 1998 1999 2000 2001 2002 2003

-50

0

50

100

150

200

250

CA as % of GDP(left axis)

ER change in %(right axis)

Moreover, this sharp CA correction goes hand in hand with sharp currency depreciation

72Javier LozanoJavier Lozano

Sustainability of current account deficits

Mexico

-8

-7

-6

-5

-4

-3

-2

-1

0

1989 1990 1991 1992 1993 1994 1995

0

10

20

30

40

50

60

70

80

90

100

CA as % of GDP(left axis)

ER change in %(right axis)

73Javier LozanoJavier Lozano

Sustainability of current account deficits

Thailand

-10

-5

0

5

10

15

1992 1993 1994 1995 1996 1997 1998

-1

4

9

14

19

24

29

34

CA as % ofGDP (left axis)

ER change in% (right axis)

74Javier LozanoJavier Lozano

Sustainability of CA deficits: some national accounts identities

• GDP=C+I+G+NX

• GNP=C+I+G+NX+NFIA (1)

• CA=NX+NFIA– Brazil in 1986:

• NX=$8.3b

• CA=-$5.3b

• NFIA=-$13.6b

• GNP=S+C+T (2)

• (1)+(2)CA=(S-I)+(T-G) (3)(net flows of

assets from/to abroad)

75Javier LozanoJavier Lozano

Sustainability of CA deficits: asset transactions with ROW

CA=(S-I)+(T-G)>0lend CA=(S-I)+(T-G)<0borrow

GNP>C+I+G

You earn more income than you expend (you lend excess

income abroad)

You earn less income than you expend (you borrow

from abroad)

From (1)

GNP<C+I+G

A CA deficit implies an increasing foreign debt whereas a CA surplus implies a fall in foreign debt

76Javier LozanoJavier Lozano

Sustainability of current account deficits

• Previous slides suggest the following interpretation: an excessive dependence on foreign borrowing (high and persistent CA deficit) may undermine foreign investor’s confidence (higher risk of default). This tends to reduce capital inflows and causes a combination of higher interest rates to curb the fall in capital inflows and pressures of ER depreciation/devaluation (because lower demand of domestic assets, among other reasons). This situation may become unbearable and end up in a sharp CA correction and strong ER depreciation/devaluation.

• Therefore CA deficit may not be sustainable. This sustainability depends on the causes of CA deficit as well as on other aspects related to the country’s characteristics.

77Javier LozanoJavier Lozano

Sustainability of CA deficits: causes of CA deficit

• Increase in national investment– Similar to a firm, it is normal and a good option for a country to

borrow from abroad in order to finance a boom in investment. Returns from investment in the form of economic growth should allow the country to repay the debt (to increase exports in the future and generate the CA surplus needed for repayment) In this case the CA deficit is sustainable (e.g. US situation during second half of 90s)

– However, there could be exceptions to this general rule:• When investments are made in sectors that do not generate

exports, for instance, real state sector (residential and commercial building).

• When most of investments are of low profitability• In the case of the Asian crisis you can find both situations

78Javier LozanoJavier Lozano

Sustainability of CA deficits: causes of CA deficit

• Increase in public budget deficit– To borrow abroad for financing public budget deficit is

not necessarily a bad idea, it depends on public expenditure allocation. If public expenditure generates economic growth (for instance, expenditure in infrastructures) then no problem.

– However, historically this has not been the case. Many experiences of CA deficits caused by public budget deficits where public expenditure has not been growth-enhancing. E.g., case of many developing countries during 70s that end up in Debt Crisis of the 80s; US current situation (military expenditure).

79Javier LozanoJavier Lozano

Sustainability of CA deficits: causes of CA deficit

• Decrease in private domestic saving– Again, a CA deficit whose main cause is a fall

in private savings does not need to be worrisome. It may reflect increase in consumption fueled by expectations of future higher income (usual in economic expansion).

– However expectations may be overoptimistic. In this case the country may have problems for debt repayment and if foreign investors suspect this, they will stop financing CA deficit.

80Javier LozanoJavier Lozano

Sustainability of CA deficits: other important factors

• A country’s economic openness, measured as Exports/GDP may be important for CA deficit sustainability since a country’s ability to service its external debt depends on its ability to obtain foreign currency receipts through exports. Low openness could be bad for sustainability of CA deficit.

81Javier LozanoJavier Lozano

Sustainability of CA deficits: other important factors

• Composition of capital inflows– Foreign Direct Investment (FDI) vs. short-term

speculative capital flows (hot money)

– Official public institutions vs. private investors

– Currency composition of foreign liabilities • If most domestic agent’s foreign liabilities are denominated

in foreign currency then ER crisis (ER devaluation) may be very harmful for the real economy since domestic agents get revenues in local currency

82Javier LozanoJavier Lozano

US CA deficit: situation

-6,00%

-5,00%

-4,00%

-3,00%

-2,00%

-1,00%

0,00%

1,00%

-30,00%

-25,00%

-20,00%

-15,00%

-10,00%

-5,00%

0,00%

currentaccount (leftaxis)

net foreignliabilities(right axis)

Source: IFS(All data as share of US GDP)

83Javier LozanoJavier Lozano

US CA deficit: situation

-6,00%

-3,00%

0,00%

3,00%

6,00%

9,00%

12,00%

15,00%

18,00%

21,00%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

currentaccount

publicbudget

privatesavingminusinvestmentinvestment

privatesaving

Source: IFS(All data as share of US GDP)

84Javier LozanoJavier Lozano

US CA deficit: situation• Huge capital inflows relative to US economy and to global

markets...• ...but very low US interest rates! Why do investors want to

invest so much in US economy?!– Very low risk of default (sound economy)– $ is the most widely used currency for international transactions

(high liquidity)– High productivity growth in US makes FDI and equity

investment in US very profitable (OK for late 90s, not for now; currently there are net FDI outflows; most of capital inflows buy Treasury bonds)

– According to many analysts, the main reason behind this situation is Asian (especially China’s) export-led growth strategy.

85Javier LozanoJavier Lozano

US CA deficit: situation. Asian export-led strategy• Policy consisting of keeping your currency at a low value (with

respect to $) to boost exports and to help growth, industrialization and employment

• This policy requires that the Asian CB buys $ to support a high value of $ relative to their local currencies (another reason for buying $ is to build foreign exchange reserves to avoid another Asian Crisis)

• For Asian countries this policy has two disadvantages and one risk :– It implies to imitate US monetary policy, that has been until now

quite expansionary. This is causing inflationary pressures in Asian countries.

– For most of Asian countries (except for Japan) domestic interest rates are higher than in US so for Asian central banks buying $ assets instead of assets denominated in local currency has an opportunity cost.

– Asian CB are taking the risk of capital losses if $ depreciates

86Javier LozanoJavier Lozano

US CA deficit: sustainability• Is this situation stable?• Dooley, Folkerts-Landau and Garber say yes because the

situation is in the interest of both Asian countries and the US:– China needs to follow this policy in order to industrialize the

country and reallocate underemployed from rural and public sector. Inconveniences stated before are minor.

– Other Asian countries (South Korea, India...) will not let their currencies appreciate against China’s currency.

– US obtains cheap (low interests) financing. Inconveniences (low price-competitiveness against Asian imports) are minor.

– For them this is the birth of BWII

87Javier LozanoJavier Lozano

US CA deficit: sustainability• Roubini, Setser and The Economist say no.• Main reason is based on the classical prisoners’ dilemma:

– If all Asian CB keep on buying $, the $ will not appreciate so Asian CB will not experience capital losses. Then each Asian CB has incentives to keep on buying $ as long as the others do the same.

– However, if you as a CB expect for this situation to be unsustainable (that is, you expect for the $ to depreciate a lot) then you have strong incentives to be the first to sell your $ before the $ depreciation takes place (if you sell too late, you will have to sell too cheap)

– Given that this “Asian cartel” is not a formal one, there are not institutions to solve this coordination problem, so these free-riding incentives will make the situation collapse sooner or later, specially because growth in external US debt increases risks of $ depreciation.

88Javier LozanoJavier Lozano

US CA deficit: sustainability• Finally, which are the threats for the global

economy that stem from this situation?– € appreciation against $ probably exacerbated by

Asian fixed ER against $ (bad for EU price-competitiveness; good for EU antiinflationary policy because oil not so expensive)

– A sharp fall in US capital inflows may increase US interest rates and consequently ROW interest rates.

– The increase in interest rates may slow US and ROW economic growth.

– Since ROW has many $ assets, sharp $ depreciation will reduce ROW wealth and then consumption and growth.

89Javier LozanoJavier Lozano

Choice of Exchange Rate Regime

90Javier LozanoJavier Lozano

Reasons for choosing a fixed ER1. To reduce ER volatility: ER volatility increase

uncertainty in international transactions. This discourages trade and long-term investment (e.g., European Monetary Union)

2. To help antiinflationary policy through two channels:2.1. Discipline: let us consider a country with high inflation

fueled by loose monetary policy (may be because of monetization). A fixed ER puts a constraint on undisciplined monetary policy (because of UIP arguments and/or because of PPP arguments)

2.2. Credibility: let us consider a country that truly wants to stop inflation through monetary policy tightening. In this case, the short-term effects on growth and employment of antiinflationary monetary policy will be more harmful the lower is the credibility of the announced policy.

91Javier LozanoJavier Lozano

c

c= short-run Phillips curve if

anttinflationary MP credible

Reasons for choosing a fixed ER (Credibility)

Unemployment

Inflationa= long-run Phillips

curve

U*

Current inflation

a

b= short-run Phillips curve if

anttinflationary MP not credible

b

recession

Targeted inflation

92Javier LozanoJavier Lozano

Reasons for choosing a fixed ER (Credibility)

• To peg the ER to a currency of a country of low inflation may help to reduce inflationary expectations and this way to reduce negative effects of antiinflationary monetary policy. (ER acts as a nominal anchor)

• ER pegging is not the only device for making antiinflationary policy credible. Another way is CB independence.

93Javier LozanoJavier Lozano

Inconveniences of fixed ER

• Finally, an important disadvantage of fixed ER is that you lose monetary policy for stabilization policy.

• This is important if you suffer from asymmetric shocks. For instance, suppose that you have pegged your currency to $. Then you experience a negative shock but the US not. You would like to loose your MP but since the US does not like and you have to mimic US MP, then you cannot.

94Javier LozanoJavier Lozano

Good luck with your exams!