jai balaji industries ltd. · this presentation is confidential and may not be copied or...

TRANSCRIPT

JAI BALAJI INDUSTRIES LTD.Corporate Presentation

2

Disclaimer

No representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or opinions contained in this presentation. Such information and opinions are in all events not current after the date of this presentation. Certain statements made in this presentation may not be based on historical information or facts and may be "forward looking statements" based on the currently held beliefs and assumptions of the management of Jai Balaji Industries Limited (“Company”

or “Jai Balaji”), which are expressed in good faith and in their opinion reasonable, including those relating to the Company’s general business plans and strategy, its future financial condition and growth prospects and future developments in its industry and its competitive and regulatory environment.

Forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual results, financial condition, performance or achievements of the Company or industry results to differ materially from the results, financial condition, performance or achievements expressed or implied by such forward-looking statements, including future changes or developments in the Company’s business, its competitive environment and political, economic,

legal and social conditions. Further, past performance is not necessarily indicative of future results. Given these risks, uncertainties and other factors, viewers of this presentation are cautioned not to place undue reliance on these forward-looking statements. The Company disclaims any obligation to update these

forward-looking statements to reflect future events or developments.

This presentation is for general information purposes only, without regard to any specific objectives, financial situations or informational needs of any particular person. This presentation does not constitute an offer or invitation to purchase or subscribe for any securities in any jurisdiction, including the United

States. No part of it should form the basis of or be relied upon in connection with any investment decision or any contract or commitment to purchase or subscribe for any securities. None of our securities may be offered or sold in the United States, without registration under the U.S. Securities Act of 1933, as amended, or pursuant to an exemption from registration therefrom.

This presentation is confidential and may not be copied or disseminated, in whole or in part, and in any manner.

3

Background

Jai Balaji Industries Ltd. (“JBIL” or “Company”) was incorporated in 1999 by the current promoters, Mr. Aditya Jajodia, Mr. Sanjiv Jajodia and Mr. Rajeev Jajodia

Integrated steel manufacturing company

―

Established its 1st

Sponge Iron Plant in 2000 with an initial capacity of 50 tons per day

―

Currently amongst the largest integrated steel producers in

West Bengal*

―

Metallics’

capacity of c. 1 million tons per annum (“MnTPA”)

―

Products range from metallics (Sponge Iron and Pig Iron) to steel products (TMT bars and Alloy Steels).

―

Also currently developing Ductile Iron Pipes and expanding

rolling mill facilities to manufacture alloy steel bars

Listed on the National Stock Exchange and Calcutta Stock Exchange in 2003 and on the Bombay Stock Exchange in 2008 with market capitalization of c. Rs. 12,250 million as at 26 August 2009

High growth in last 5 years

―

Gross block (as at 31 March 2009) of Rs. 14,119 million, grown at a CAGR of 99% y-o-y**

―

Annual revenue of Rs. 17,495 million for FY09 , grown at a CAGR growth of 70%**

Strategic institutional investors

–

Citigroup Venture Capital invested Rs. 2,000 million in February

2008 and currently has a c. 11% stake including Board representation

–

India Equity Partners invested Rs. 733 million in February 2008 for a c. 4% stake including Board representation

* Source: West Bengal Sponge Iron Manufacturers Association (Aug 2009)** Annual reports of Jai Balaji Industries Limited (formerly known as Jai Balaji Sponge Limited (JBSL)): Growth with respect to JBSL. JBSL and another Jai Balaji Group Company, Shri Ramrupai Balaji Steels Ltd. (“SRBSL”) merged in FY07

4

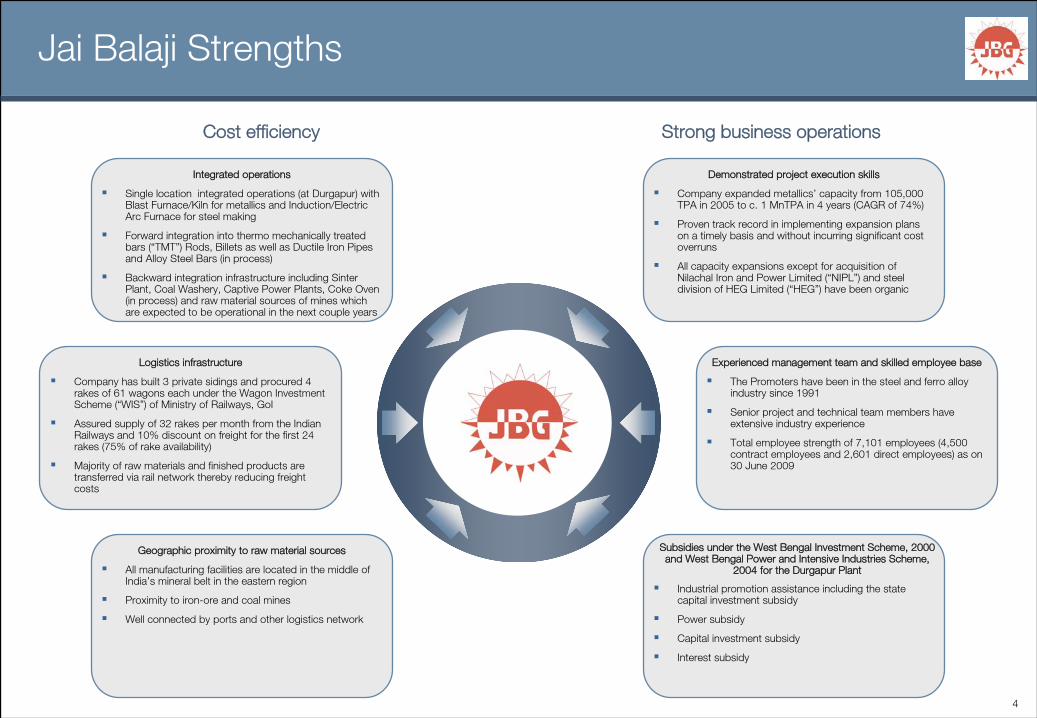

Jai Balaji Strengths

Logistics infrastructure

Company has built 3 private sidings and procured 4 rakes of 61 wagons each under the Wagon Investment Scheme (“WIS”) of Ministry of Railways, GoI

Assured supply of 32 rakes per month from the Indian Railways and 10% discount on freight for the first 24 rakes (75% of rake availability)

Majority of raw materials and finished products are transferred via rail network thereby reducing freight costs

Demonstrated project execution skills

Company expanded metallics’ capacity from 105,000 TPA in 2005 to c. 1 MnTPA in 4 years (CAGR of 74%)

Proven track record in implementing expansion plans on a timely basis and without incurring significant cost overruns

All capacity expansions except for acquisition of Nilachal Iron and Power Limited (“NIPL”) and steel division of HEG Limited (“HEG”) have been organic

Integrated operations

Single location integrated operations (at Durgapur) with Blast Furnace/Kiln for metallics and Induction/Electric Arc Furnace for steel making

Forward integration into thermo mechanically treated bars (“TMT”) Rods, Billets as well as Ductile Iron Pipes and Alloy Steel Bars (in process)

Backward integration infrastructure including Sinter Plant, Coal Washery, Captive Power Plants, Coke Oven (in process) and raw material sources of mines which are expected to be operational in the next couple years

Geographic proximity to raw material sources

All manufacturing facilities are located in the middle of India’s mineral belt in the eastern region

Proximity to iron-ore and coal mines

Well connected by ports and other logistics network

Experienced management team and skilled employee base

The Promoters have been in the steel and ferro alloy industry since 1991

Senior project and technical team members have extensive industry experience

Total employee strength of 7,101 employees (4,500 contract employees and 2,601 direct employees) as on 30 June 2009

Cost efficiency Strong business operations

Industrial promotion assistance including the state capital investment subsidy

Power subsidy

Capital investment subsidy

Interest subsidy

Subsidies under the West Bengal Investment Scheme, 2000 and West Bengal Power and Intensive Industries Scheme,

2004 for the Durgapur Plant

5

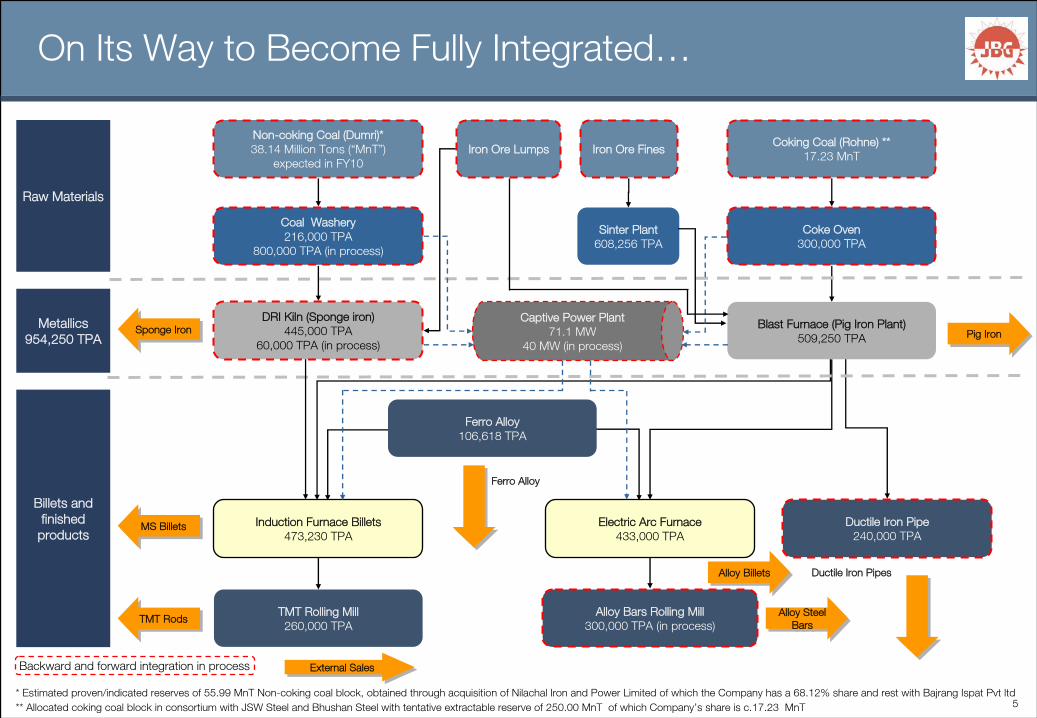

On Its Way to Become Fully Integrated…

Non-coking Coal (Dumri)*38.14 Million Tons (“MnT”)

expected in FY10

Coal Washery216,000 TPA

800,000 TPA (in process)

Induction Furnace Billets473,230 TPA

MS BilletsMS Billets

TMT Rolling Mill260,000 TPA

Iron Ore FinesCoking Coal (Rohne) **

17.23 MnT

Coke Oven300,000 TPA

Electric Arc Furnace433,000 TPA

Ductile Iron Pipe240,000 TPA

Ferro Alloy

Ferro Alloy106,618 TPA

Raw Materials

Metallics954,250 TPA

Billets and finished

products

Sponge IronSponge Iron

TMT RodsTMT Rods

Pig IronPig Iron

Sinter Plant608,256 TPA

Blast Furnace (Pig Iron Plant)509,250 TPA

DRI Kiln (Sponge iron)445,000 TPA

60,000 TPA (in process)

Captive Power Plant71.1 MW

40 MW (in process)

* Estimated proven/indicated reserves of 55.99 MnT Non-coking coal block, obtained through acquisition of Nilachal Iron

and Power Limited of which the Company has a 68.12% share and rest with Bajrang Ispat Pvt ltd** Allocated coking coal block in consortium with JSW Steel and Bhushan Steel with tentative extractable reserve of 250.00 MnT of which Company’s share is c.17.23 MnT

Iron Ore Lumps

Ductile Iron Pipes

Backward and forward integration in process External SalesExternal Sales

Alloy Bars Rolling Mill300,000 TPA (in process)

Alloy BilletsAlloy Billets

Alloy Steel Bars

Alloy Steel Bars

6

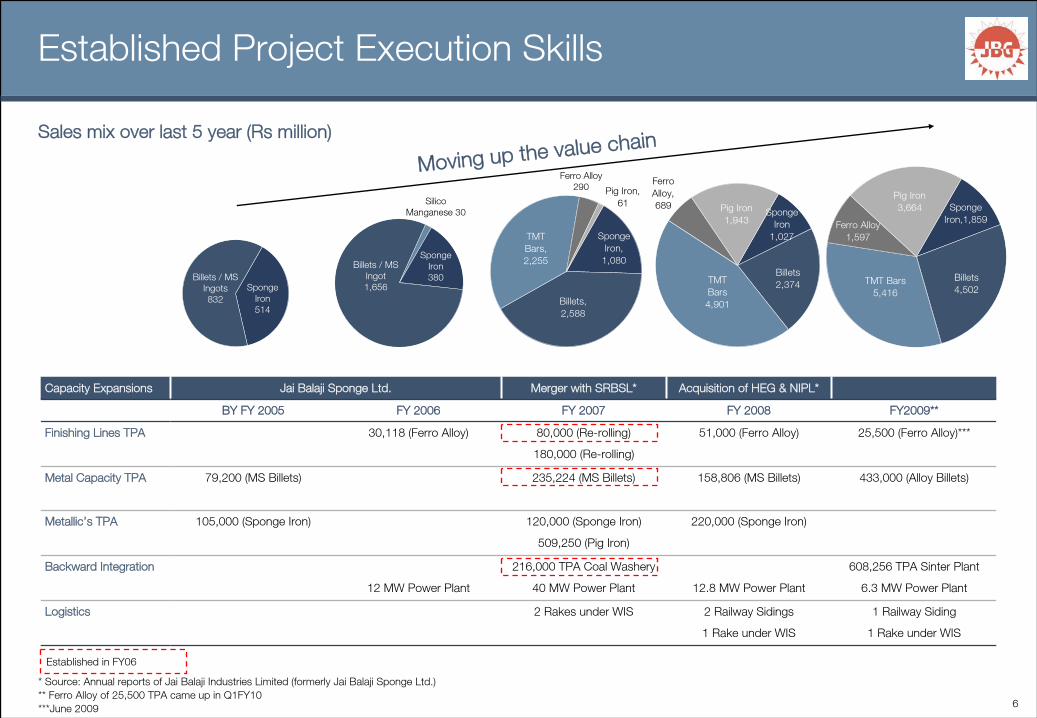

TMT Bars 4,901

Billets 2,374

Sponge Iron

1,027

Pig Iron 1,943

Ferro Alloy, 689

Established Project Execution Skills

Billets2,588m

Capacity Expansions Jai Balaji Sponge Ltd. Merger with SRBSL* Acquisition of HEG & NIPL*

BY FY 2005 FY 2006 FY 2007 FY 2008 FY2009**

Finishing Lines TPA 30,118 (Ferro Alloy) 80,000 (Re-rolling)

180,000 (Re-rolling)

51,000 (Ferro Alloy) 25,500 (Ferro Alloy)***

Metal Capacity TPA 79,200 (MS Billets) 235,224 (MS Billets) 158,806 (MS Billets) 433,000 (Alloy Billets)

Metallic’s TPA 105,000 (Sponge Iron) 120,000 (Sponge Iron)

509,250 (Pig Iron)

220,000 (Sponge Iron)

Backward Integration

12 MW Power Plant

216,000 TPA Coal Washery

40 MW Power Plant 12.8 MW Power Plant

608,256 TPA Sinter Plant

6.3 MW Power Plant

Logistics 2 Rakes under WIS 2 Railway Sidings

1 Rake under WIS

1 Railway Siding

1 Rake under WIS

Moving up the value chain

Billets / MS Ingots832

Sponge Iron 514

Sales mix over last 5 year (Rs million)

Sponge

1,080

* Source: Annual reports of Jai Balaji Industries Limited (formerly Jai Balaji Sponge Ltd.)** Ferro Alloy of 25,500 TPA came up in Q1FY10 ***June 2009

Established in FY06

Sponge Iron 380

Billets / MS Ingot 1,656

Silico Manganese 30

Ferro Alloy 290 Pig Iron,

61

TMT Bars, 2,255

Sponge Iron,

1,080

Billets, 2,588

Billets 4,502

Sponge Iron,1,859

Pig Iron 3,664

Ferro Alloy 1,597

TMT Bars 5,416

7

Cost Effective Logistics Infrastructure

Company estimates rail transport to be over 50% cheaper than road transport; however transport is limited by siding congestion and non-availability of rakes and locomotives

Approximately 3 tons of raw material required for every 1 ton of steel

Company has already invested in 3 railway sidings at the plant facility and at raw material sourcing locations in Orissa and Chhattisgarh at a cost of Rs. 412m

Procured and delivered 4 railway rakes of 61 Box Wagons each to Indian Railways under the Wagon Investment Scheme at a total cost of Rs. 546m

Most raw materials transported via rail network

Assured allotment of 32 rakes per month from Indian Railways

10% discount on the freight charges for first 24 rakes under the scheme (75% of rake availability)

Increased flexibility in delivering finished goods

Reduced freight costs

Reduced pilferage, theft and ground loss in transporting raw materials

Reduced turnaround time

BenefitsBenefits

Private railway sidings

Railway rakes

8

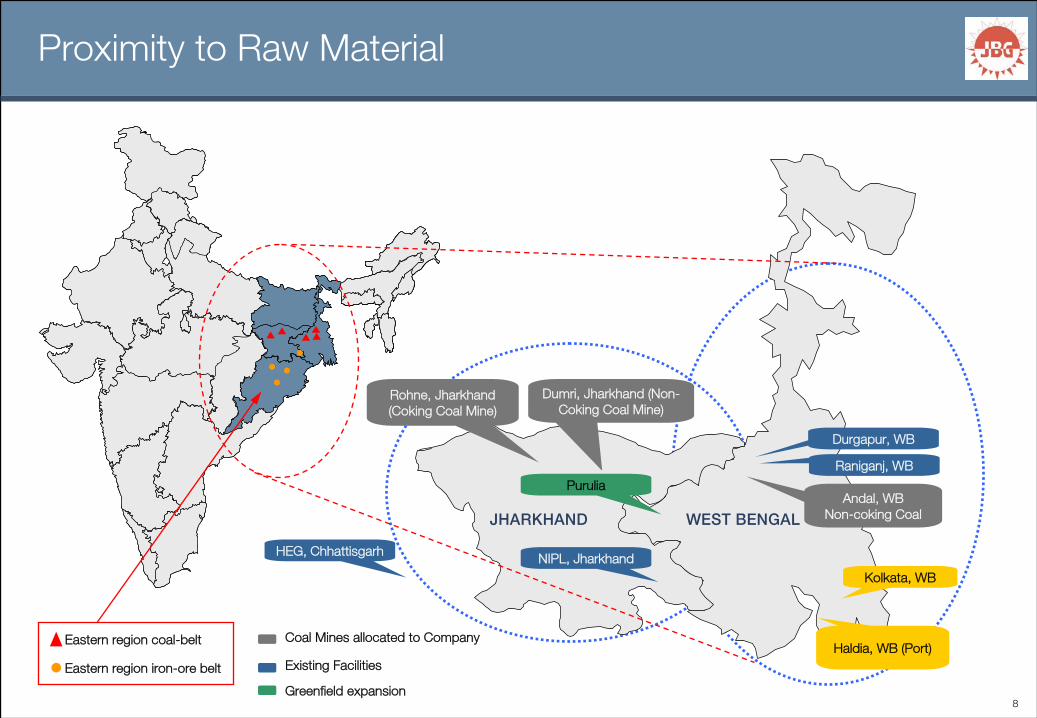

Coal Mines allocated to Company

Existing FacilitiesHaldia, WB (Port)

Durgapur, WB

Andal, WBNon-coking Coal

Kolkata, WB

Dumri, Jharkhand (Non-

Coking Coal Mine)

NIPL, JharkhandHEG, Chhattisgarh

Raniganj, WBPurulia

Rohne, Jharkhand (Coking Coal Mine)

ge^ohe^ka tbpq=_bkd^i

Proximity to Raw Material

Eastern region coal-belt

Eastern region iron-ore belt

Greenfield expansion

9

Experienced Promoters

Mr. A. Jajodia

Chairman and Managing Director

Age: 38 years

Bachelor of Commerce (Honors) from St. Xavier’s College, Kolkata

Over 15 years of experience in the steel and power industry

Responsible for all major financial and strategic decisions

Under his guidance, both the Jai Balaji Group Companies - Jai Balaji Sponge Limited and Shri Ramrupai Balaji Steels Limited – went public on the Indian stock exchanges

Mr. S. Jajodia

Whole-time Director

Age: 45 years

Bachelor of Commerce (Honors) from St. Xavier’s College, Kolkata

Over 2 decades experience in the steel industry

Supervises and controls overall administration, legal aspects, human resource as well as financial planning of the Jai Balaji Group

Joined the Group in 1991 with Chandi Steel Industries Ltd.

Mr. R. Jajodia

Non-executive Director

Age 44 years

Bachelor of Commerce (Honors) from St. Xavier’s College, Kolkata

Over 2 decades experience in the steel industry

Manages the operations of the Company and supervises the iron ore and coal linkages, and procurement of other raw materials

Also supervises the sales and marketing function of the Jai Balaji Group

Instrumental in getting coal allocation and implementing railway sidings and purchasing rakes from Indian Railways

Joined the Group in 1991 with Chandi Steel Industries Ltd.

Gourav Jajodia

Non-executive Director

Age 29 years

Bachelor of Commerce (Honors) from St. Xavier’s College, Kolkata

Over 5 years of experience in the steel industry

Supervises the operations and the production process of the Company

Joined the Company in 2008

10

Qualified Management Team

Mr.Chandramukh Patnaik

Executive Director (Projects)

Age: 57 years

B.Tech. and M.Tech. in Chemical Engineering from IIT Kharagpur

Spearheading the 5 MnTPA greenfield integrated steel project at Raghunathpur, Purulia Dist of West Bengal

Over 30 years of experience in operation and projects in major steel companies like Tata Steel, Essar Steel, Ispat, Saudi Iron and Steel, Jindal Stainless and Uttam Galva

Prior to joining JBIL worked as ED (Technology) with Jindal Steel & Power Limited

Mr. Raj Kumar Sharma

Chief Financial Officer

Age: 42 years

B.Com. and ICWA

Over 18 years of experience in finance and accounts with various companies

Responsible for Company’s finance and accounts operations and other financial strategies

Prior to joining JBIL worked with Adhunik Group

Mr.S.K. Sachan

Vice President (Projects)

Age: 39 years

B.Tech. in Mechanical Engineering from Regional Engineering College, University of Raipur

Leading the company’s expansion and brown field projects at Durgapur, West Bengal

Over 17 years of experience in project implementation in major steel companies like Malvika Steel and Jindal Steel & Power

Prior to joining JBIL worked with Visa Steel Limited in project implementation

Mr. Partho Kumar Roy

Vice President (Marketing)

Age: 54 years

B.Tech. in Metallurgical Engineering from Banaras Hindu University

Responsible for the development of markets and sale of alloy steel

Over 30 years of experience in marketing of alloy steel products in companies like Gonterman Pipes and Bihar Alloys & Steel Limited

Prior to joining JBIL worked with Usha Martin Industries Limited as Vice President (Marketing)

Mr. John Joseph

Vice President (HR)

Age: 48 years

M.A.(SW) from the University of Madras

Responsible for formulation and implementation of human resource strategies for the Company

Over 24 years of experience in all aspects of HR with leading companies like Bharat Heavy Electricals Limited, Shalimar Paints and the OP Jindal Group

Prior to joining JBIL, headed corporate HR for Jindal Steel & Power limited

Mr. Bivas Chakraborty

Deputy General Manager

Age: 43 years

B.Sc. from Calcutta University

Responsible for the development of markets and sale of ductile iron pipes (DI Pipes)

Over 20 years of experience in marketing and sale of DI Pipes and other pipe solutions in companies like Bengal Tools Limited and Electro Steel Casting Limited.

Prior to joining JBIL worked with Doshion-Veolia Water Solution Company as Manager (M&S) for its EPC division

11

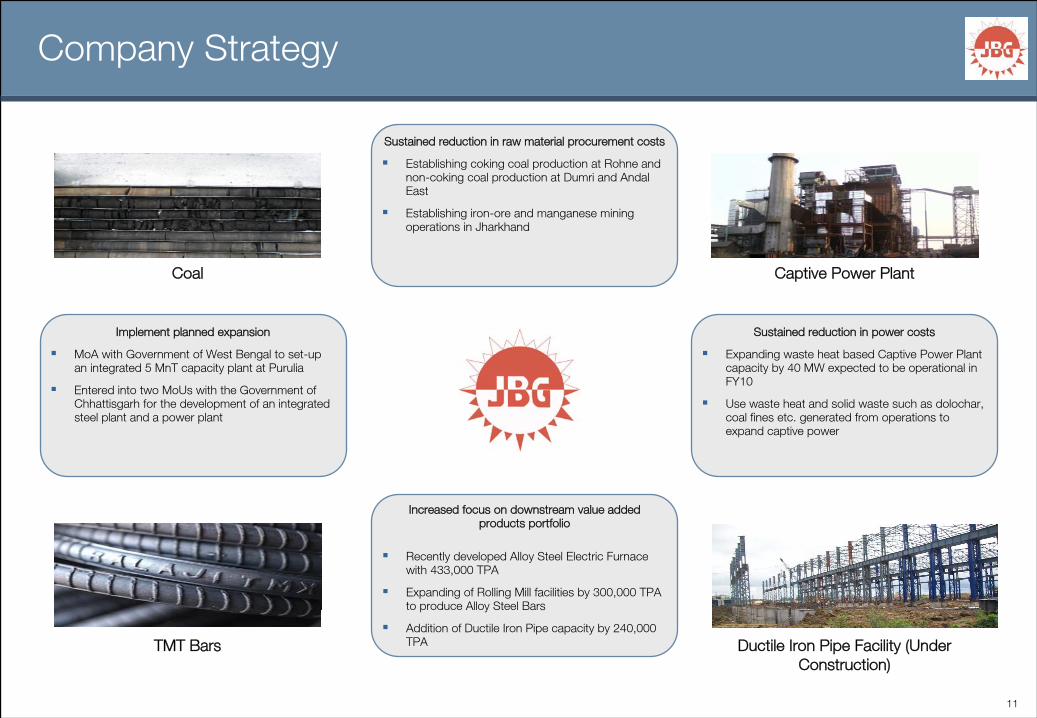

Company Strategy

Sustained reduction in raw material procurement costs

Establishing coking coal production at Rohne and non-coking coal production at Dumri and Andal East

Establishing iron-ore and manganese mining operations in Jharkhand

Implement planned expansion

MoA with Government of West Bengal to set-up an integrated 5 MnT capacity plant at Purulia

Entered into two MoUs with the Government of Chhattisgarh for the development of an integrated steel plant and a power plant

Sustained reduction in power costs

Expanding waste heat based Captive Power Plant capacity by 40 MW expected to be operational in FY10

Use waste heat and solid waste such as dolochar, coal fines etc. generated from operations to expand captive power

Recently developed Alloy Steel Electric Furnace with 433,000 TPA

Expanding of Rolling Mill facilities by 300,000 TPA to produce Alloy Steel Bars

Addition of Ductile Iron Pipe capacity by 240,000 TPA

Increased focus on downstream value added products portfolio

TMT Bars

Coal

Ductile Iron Pipe Facility (Under Construction)

Captive Power Plant

12

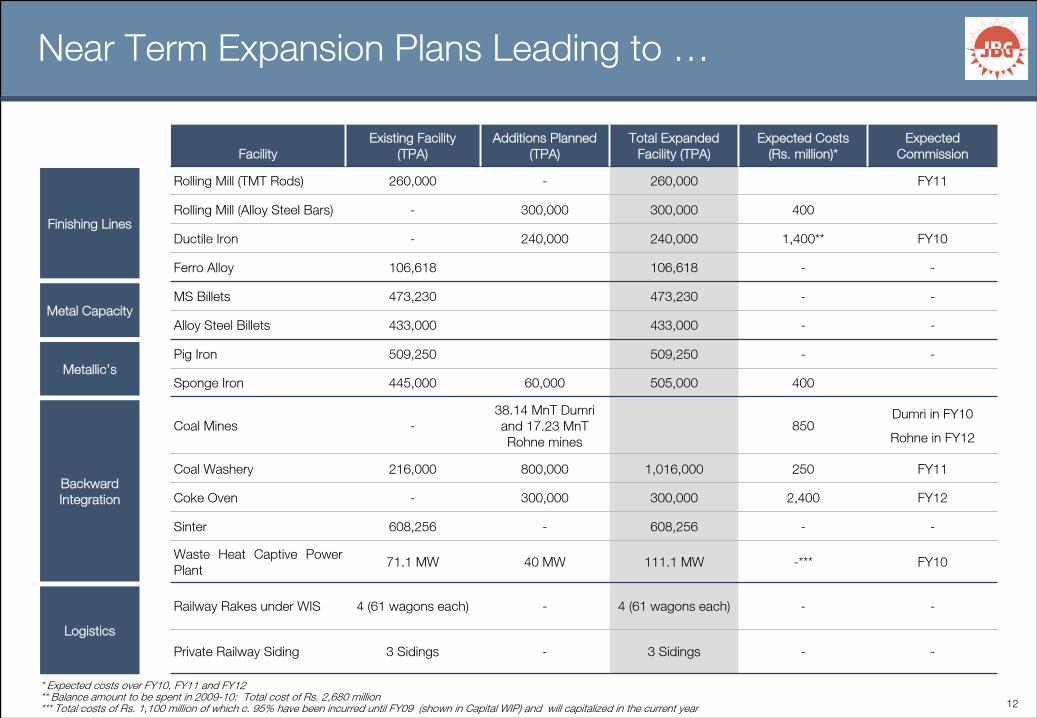

Near Term Expansion Plans Leading to …

FacilityExisting Facility

(TPA)Additions Planned

(TPA)Total Expanded

Facility (TPA)Expected Costs

(Rs. million)*Expected

Commission

Rolling Mill (TMT Rods) 260,000 - 260,000 FY11

Rolling Mill (Alloy Steel Bars) - 300,000 300,000 400

Ductile Iron - 240,000 240,000 1,400** FY10

Ferro Alloy 106,618 106,618 - -

MS Billets 473,230 473,230 - -

Alloy Steel Billets 433,000 433,000 - -

Pig Iron 509,250 509,250 - -

Sponge Iron 445,000 60,000 505,000 400

Coal Mines -38.14 MnT Dumri and 17.23 MnT Rohne mines

850Dumri in FY10

Rohne in FY12

Coal Washery 216,000 800,000 1,016,000 250 FY11

Coke Oven - 300,000 300,000 2,400 FY12

Sinter 608,256 - 608,256 - -

Waste Heat Captive Power Plant

71.1 MW 40 MW 111.1 MW -*** FY10

Railway Rakes under WIS 4 (61 wagons each) - 4 (61 wagons each) - -

Private Railway Siding 3 Sidings - 3 Sidings - -

Finishing Lines

Metal Capacity

Metallic’s

Backward Integration

Logistics

* Expected costs over FY10, FY11 and FY12** Balance amount to be spent in 2009-10: Total cost of Rs. 2,680 million*** Total costs of Rs. 1,100 million of which c. 95% have been incurred until FY09 (shown in Capital WIP) and will capitalized in the current year

13

… Reduced Raw Material and Power Costs

Product Highest cost Medium cost Low cost

Iron-ore Spot market

Acquire Iron Ore Lumps from spot market

Sinter plant

Purchases lower cost Iron Ore Fines from local vendors and converts to lumps in a sinter plant

Commissioned a 608,256 TPA plant in September 2008

Owned mines

NIPL has been granted mining lease over 450 hectares for Iron Ore and Manganese ore mining in Jharkhand

Geological survey for these mines is expected to start in 3rd quarter of FY10

Coking coal Spot market

Initially Company purchased low ash Met coke at spot rates

Given rising prices, Company has commenced buying in bulk through merchant importers on high sea basis

Captive coke oven

Establishing a 300,000 TPA coke-oven for its Durgapur plant

Total costs expected to be Rs. 2,400m

Captive coke oven and owned mines

NIPL allocated Coking Coal block at Rohne in consortium with JSW Steel Limited and Bhushan Steel Limited,

Tentative extractable reserve of 250.00 MnT in which Company’s share of coal is approximately 17.23 MnT

Expected to be commissioned in FY12 and will contribute to most of the requirement

Non-coking coal

Spot market Linkage from Coal India Limited

A 216,000 TPA Coal Washery set up to wash coal from the mines in order to lower the ash content

Another 800,000 TPA Coal Washery being set up in Jharkhand for the Dumri coal mines

Owned mines

Allocated Non-coking Coal block at Dumri which has estimated proved reserves of 55.99 MnT of coal, and the Company has a 68.12% share (38.14 MnT)

Mining plans at Dumri have been prepared and commercial production is expected by FY10, resulting in significant savings

Also allocated another mine with estimated geological reserve of 700 MnT with Company share being 229.50 MnT

Power Market access Grid supply from the State Government

Estimated around 40% of power requirements is met via waste heat based captive generation while the balance 60% accessed via state grid

Captive Power Plant

Generate power from waste heat and solid waste such as dolochar, coal midlings etc., generated from operations

Another 40 MW to be commissioned by 3rd

quarter of FY10

Current Status Future Plans

14

Organic Growth in Purulia

Signed a development agreement with the Government of West Bengal (“GWB”), the West Bengal Industrial Development Corporation Ltd. and the West Bengal Mineral Development and Trading Corporation Limited (“WBMDTC”), for setting up

―

5 MnTPA Integrated steel plant

―

3 MnTPA Cement plant

―

1,215 MW Captive power plant

c. Rs. 562 million has been incurred including purchase of land

Current Status

―

c. 1,130 acres of land have been acquired from the GWB

―

GWB has identified and applied for the allocation of three coal blocks in the vicinity of the project site in the name of WBMDTC, which will enter into a coal mining agreement with the Company

―

Intend to develop in a modular fashion in phases through 2017

―

Teams have started relocating to begin initial process

―

Water clearance , railways traffic clearance , in principle approval from state electricity board for

construction power have been received and application for environmental clearance have been submitted

Purulia Plant

Plant Site

15

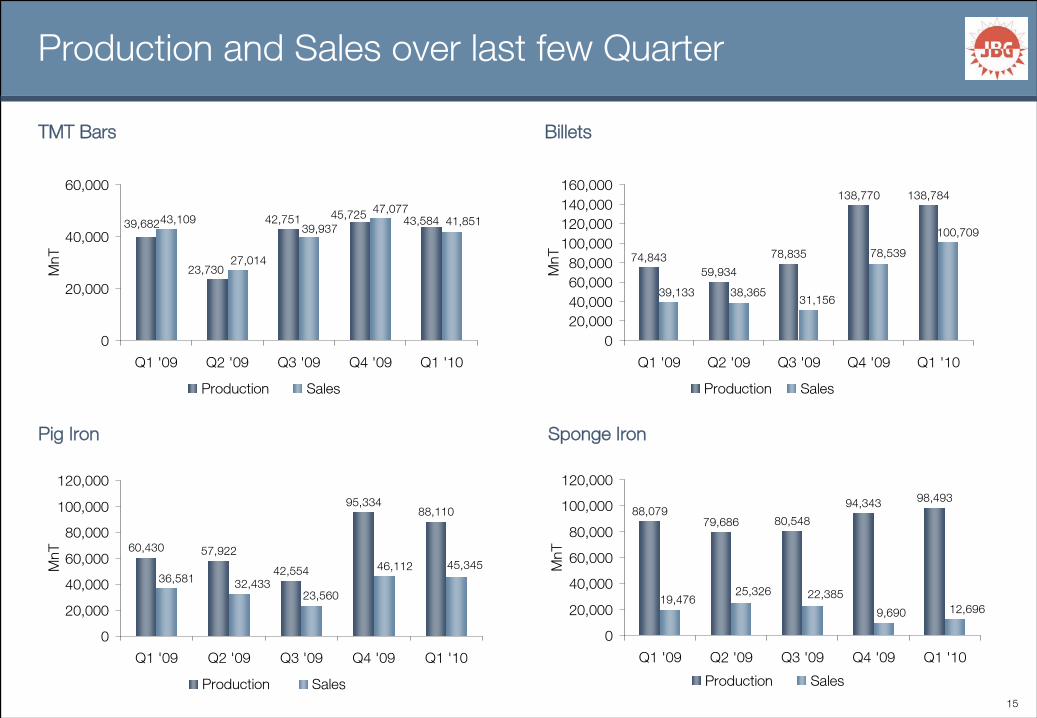

Production and Sales over last few Quarter

TMT Bars Billets

Pig Iron Sponge Iron

60,430 57,922

42,554

95,33488,110

36,581 32,43323,560

46,112 45,345

0

20,000

40,000

60,000

80,000

100,000

120,000

Q1 '09 Q2 '09 Q3 '09 Q4 '09 Q1 '10

MnT

Production Sales

74,84359,934

78,835

138,770 138,784

100,709

78,539

31,15638,36539,133

020,00040,00060,00080,000

100,000120,000140,000160,000

Q1 '09 Q2 '09 Q3 '09 Q4 '09 Q1 '10

MnT

Production Sales

39,682 43,58445,72542,751

23,730

41,85147,077

27,014

39,93743,109

0

20,000

40,000

60,000

Q1 '09 Q2 '09 Q3 '09 Q4 '09 Q1 '10

MnT

Production Sales

88,07979,686 80,548

94,343 98,493

19,47625,326 22,385

9,690 12,696

0

20,000

40,000

60,000

80,000

100,000

120,000

Q1 '09 Q2 '09 Q3 '09 Q4 '09 Q1 '10

MnT

Production Sales

16

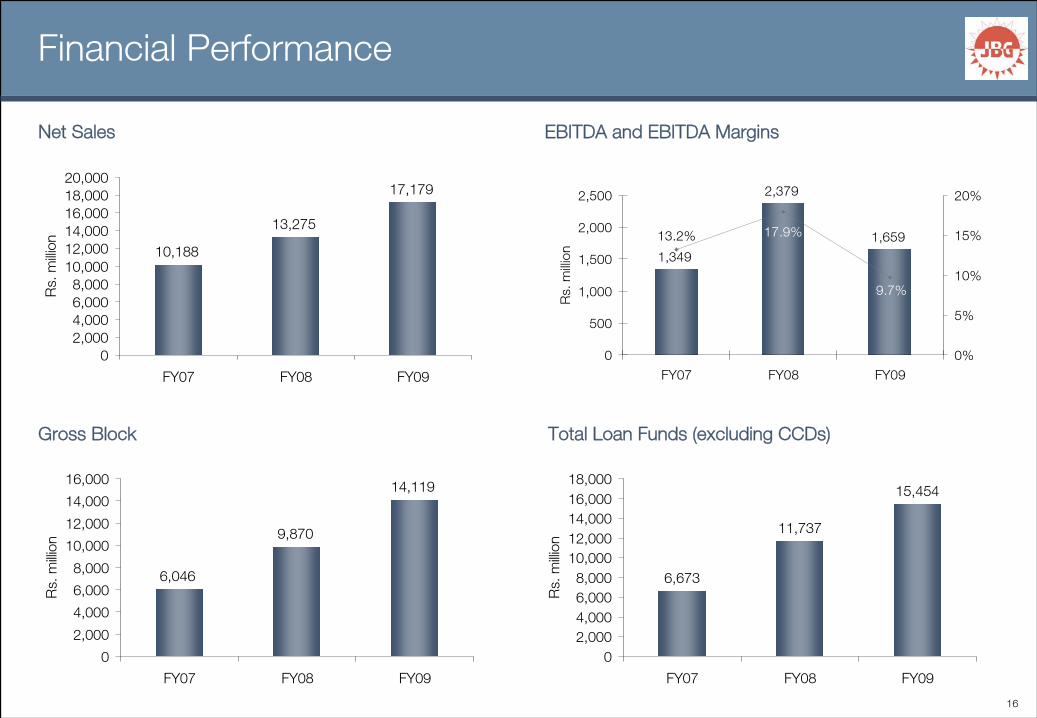

Financial Performance

Net Sales EBITDA and EBITDA Margins

Gross Block Total Loan Funds (excluding CCDs)

6,046

9,870

14,119

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

FY07 FY08 FY09

Rs.

milli

on

10,188

13,275

17,179

02,0004,0006,0008,000

10,00012,00014,00016,00018,00020,000

FY07 FY08 FY09

Rs.

milli

on

1,349

2,379

1,659

9.7%

17.9%13.2%

0

500

1,000

1,500

2,000

2,500

FY07 FY08 FY09

Rs.

milli

on

0%

5%

10%

15%

20%

6,673

11,737

15,454

02,0004,0006,0008,000

10,00012,00014,00016,00018,000

FY07 FY08 FY09

Rs.

milli

on

17

Consolidated Balance Sheet

Consolidated Balance Sheet (Rs. Million) March 07 March 08 March 09

Sources of Funds

Shareholder's Funds

Share Capital 251 471 471

Share Capital Suspense 220 - -

Application Money towards Equity warrants - 618 618

Preference Share Application Money - - 0

Reserves and Surplus 1,988 3,386 3,406

Total Shareholder's Funds 2,459 4,475 4,495

Loan Funds

Secured Loans 5,795 11,090 15,386

Unsecured Loans 878 3,379* 2,801*

Total Loan Funds 6,673 14,470 18,187

Deferred Tax Liability 630 697 772

Total Sources of Funds 9,762 19,641 23,454

Application of Funds

Gross Block 6,046 9,870 14,119

Less: Depreciation 430 967 1,512

Net Block 5,616 8,903 12,606

Capital Work in Progress 477 3,003 3,207

Net Fixed Assets 6,092 11,905 15,814

Investments 2 38 37

Cash 256 213 225

Other Current Assets 4,904 10,465 10,681

Less: Current Liabilities 1,513 2,980 3,303

Net Current Assets 3,648 7,697 7,603

Miscellaneous 20 - -

Total Application of Funds 9,762 19,641 23,454

* Includes Rs. 2733m of CCDs which have been converted in July 09

18

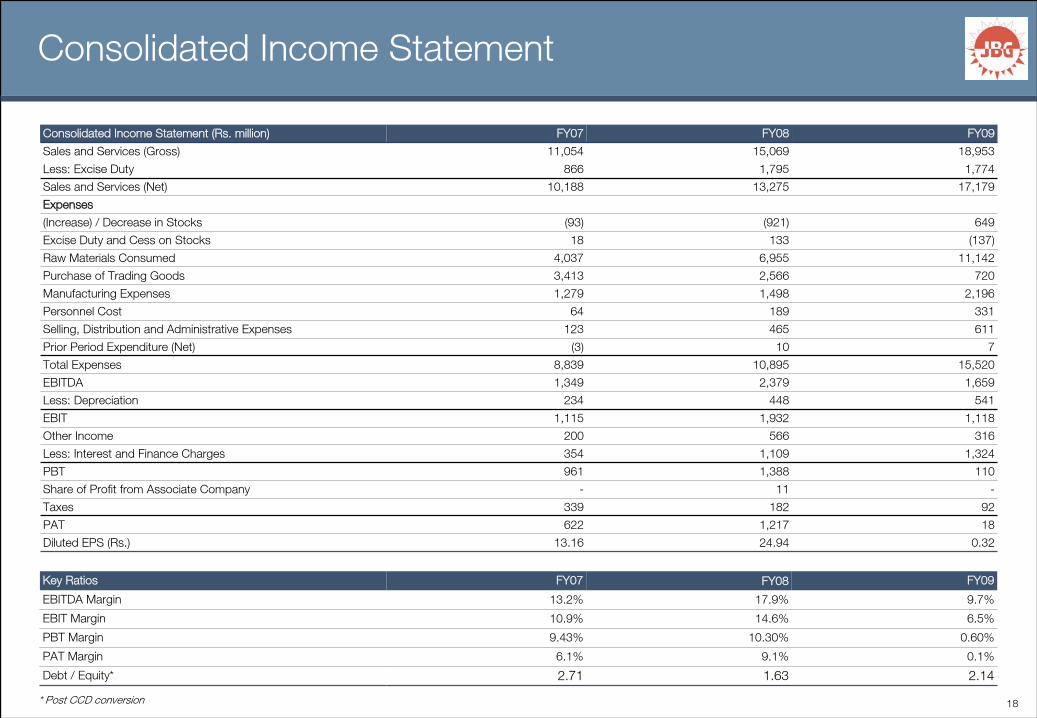

Consolidated Income Statement

Key Ratios FY07 FY08 FY09

EBITDA Margin 13.2% 17.9% 9.7%

EBIT Margin 10.9% 14.6% 6.5%

PBT Margin 9.43% 10.30% 0.60%

PAT Margin 6.1% 9.1% 0.1%

Debt / Equity* 2.71 1.63 2.14

* Post CCD conversion

Consolidated Income Statement (Rs. million) FY07 FY08 FY09

Sales and Services (Gross) 11,054 15,069 18,953

Less: Excise Duty 866 1,795 1,774

Sales and Services (Net) 10,188 13,275 17,179

Expenses

(Increase) / Decrease in Stocks (93) (921) 649

Excise Duty and Cess on Stocks 18 133 (137)

Raw Materials Consumed 4,037 6,955 11,142

Purchase of Trading Goods 3,413 2,566 720

Manufacturing Expenses 1,279 1,498 2,196

Personnel Cost 64 189 331

Selling, Distribution and Administrative Expenses 123 465 611

Prior Period Expenditure (Net) (3) 10 7

Total Expenses 8,839 10,895 15,520

EBITDA 1,349 2,379 1,659

Less: Depreciation 234 448 541

EBIT 1,115 1,932 1,118

Other Income 200 566 316

Less: Interest and Finance Charges 354 1,109 1,324

PBT 961 1,388 110

Share of Profit from Associate Company - 11 -

Taxes 339 182 92

PAT 622 1,217 18

Diluted EPS (Rs.) 13.16 24.94 0.32

19

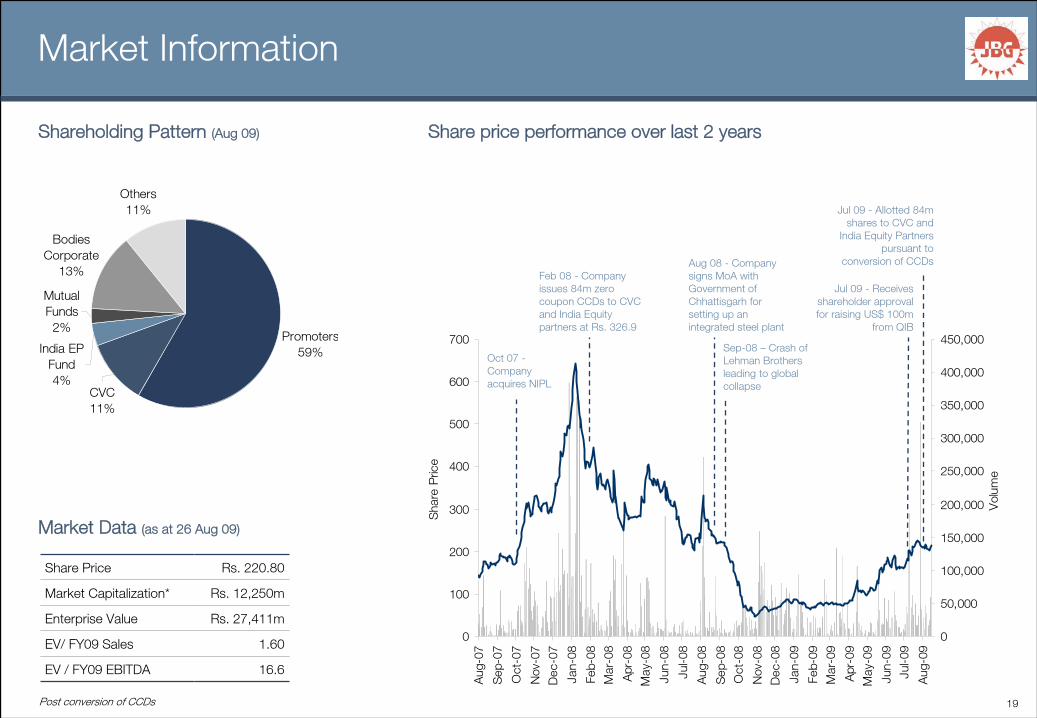

Promoters59%

Mutual Funds2%

Bodies Corporate

13%

India EP Fund4%

CVC11%

Others11%

Market Information

Shareholding Pattern (Aug 09)

Share Price Rs. 220.80

Market Capitalization* Rs. 12,250m

Enterprise Value Rs. 27,411m

EV/ FY09 Sales 1.60

EV / FY09 EBITDA 16.6

0

100

200

300

400

500

600

700

Aug

-07

Sep

-07

Oct

-07

Nov

-07

Dec

-07

Jan-

08

Feb-

08M

ar-0

8

Apr

-08

May

-08

Jun-

08

Jul-0

8

Aug

-08

Sep

-08

Oct

-08

Nov

-08

Dec

-08

Jan-

09

Feb-

09M

ar-0

9

Apr

-09

May

-09

Jun-

09Ju

l-09

Aug

-09

Sha

re P

rice

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Vol

ume

Jul 09 -

Allotted 84m shares to CVC and

India Equity Partners pursuant to

conversion of CCDs

Jul 09 -

Receives shareholder approval for raising US$ 100m

from QIB

Aug 08 -

Company signs MoA with Government of Chhattisgarh for setting up an integrated steel plant

Feb 08 -

Company issues 84m zero coupon CCDs to CVC and India Equity partners at Rs. 326.9

Oct 07 -

Company acquires NIPL

Sep-08 –

Crash of Lehman Brothers leading to global collapse

Market Data (as at 26 Aug 09)

Post conversion of CCDs

Share price performance over last 2 years

APPENDIX

21

Sales and Distribution

Distribution Strategy Target Customers

Sold under the “Balaji Shakti” Thermex TMT Bars

Sold through 3 consignment agents

Government Agencies

Power Projects and Industry Houses

Major civil contractors

Major real estate developers

Retail rural market

Sold through dealer network in local market and northern region (Punjab, Haryana and UP)

Secondary steel players at present

In future, it will be completely for captive use

Primarily Captive Usage

Sold directly to local customers within a 50 KM radius

Command a Rs. 200-300 premium for superior quality and reliability

Surplus to small non-integrated steel manufacturers

Primarily captive usage

Some exported through Trade Houses, when realizations are better

Surplus to Rolling Mills

Exported through big house traders and merchant exporters

Conversion agents for some of the large steel companies

Major steel companies

Some captive usage

Marketing team of 15 people

Products are primarily sold in the domestic market through short term contracts

Large volume purchasers buy directly from the Company whereas low volume purchasers buy through stockholders and 3 consignment agents

Markets for the metallic, semi-finished and ferro alloy products are usually located within a 50 kilometre radius of our manufacturing facilities, which enables significant savings in transportation cost

TMT Bars

Billets

Ferro Alloy

Pig Iron

Sponge Iron