italian trade commission webinar canada – december 9, 2014 gs global solutions

TRANSCRIPT

Canadian Automotive Industry Overview

Italian Trade CommissionWebinar Canada – December 9, 2014GS Global Solutions

GS Global Solutions

Global LV Production(2009 – 2021)

20092010

20112012

20132014

20152016

20172018

20192020

20210

10,000,00020,000,00030,000,00040,000,00050,000,00060,000,00070,000,000

Middle-East/AfricaAsia-PacificEastern EuropeWestern EuropeSouth AmericaNorth America

Region 2013 (Mil) 2021 (Mil) 2021 VS. 2013 Growth 2021 vs. 2009 CAGR 2021 vs. 2013 CAGR

NA 16.18 18.69 15.5% 6.7% 1.8%

SA 4.57 6.08 33.2% 4.3% 3.6%

WE 12.54 15.40 22.9% 2.1% 2.6%

EE 6.76 8.00 18.5% 4.2% 2.1%

AP 43.48 58.43 34.4% 6.0% 3.8%

ME/A 0.75 1.03 38.1% 6.9% 4.1%

TOTAL 84.26 107.62 27.7% 5.2% 3.1%

Source: AutoForecast Solutions – October 2014

2021 = 107.6 Million

GS Global Solutions

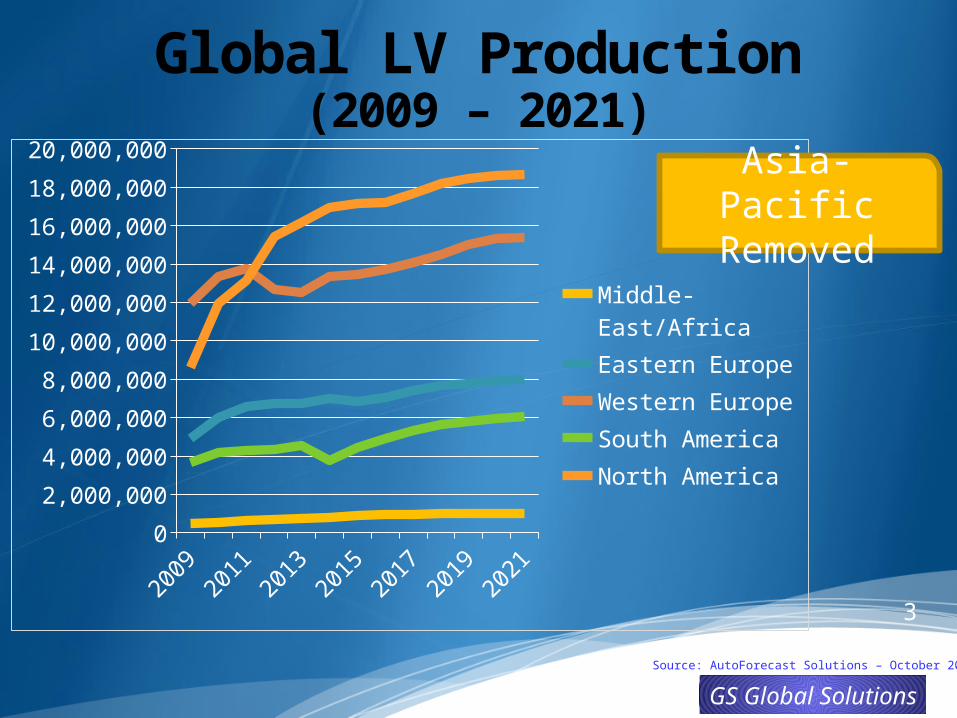

Global LV Production(2009 – 2021)

20092011

20132015

20172019

20210

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

20,000,000

Middle-East/AfricaEastern EuropeWestern EuropeSouth AmericaNorth America

3

Source: AutoForecast Solutions – October 2014

Asia-Pacific Removed

GS Global Solutions

New NAFTA Environmental RegulationsSmaller, lighter vehicles, with upgraded fuel-efficient powertrains.

Will people want to drive much smaller vehicles? Will vehicle profit be high enough to justify investment?2017-2025 standards require a 65% improvement in fuel economy over current levels.

Higher consumer ownership and operating cost. Will consumers accept paying more … possibly much more … for transportation?How de we as suppliers support global platforms and still look after local business opportunities?

4

NAFTA Megatrends

GS Global Solutions

Key drivers, enablers and constraints2013 2014-16

Employment/Income Growth

Driving Age Population Growth

Age of Fleet

Ownership and Operating Cost

Affluence/Financial Stability

Technology

Fuel Economy Regs

Supply Chain Constraints

5Source: AutomotiveCompass

NAFTA Auto Outlook

GS Global Solutions

NAFTA LV Production(2009 – 2021)

20092010

20112012

20132014

20152016

20172018

20192020

20210

5,000,000

10,000,000

15,000,000

20,000,000

United StatesMexicoCanada

Region 2013 (Mil) 2021 (Mil) 2021 VS. 2013 Growth 2021 vs. 2009 CAGR 2021 vs. 2013 CAGR

Canada 2.37 1.80 -24.0% 1.7% -3.4%Mexico 2.93 4.33 48.2% 9.1% 5.0%

United States 10.88 12.55 15.3% 6.9% 1.8%TOTAL NA 16.18 18.68 15.5% 6.7% 1.8%

6

Source: AutoForecast Solutions – October 2014

GS Global Solutions

NAFTA LV Production(2009 – 2021)

20092010

20112012

20132014

20152016

20172018

20192020

20210%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

United StatesMexicoCanada

7

18.7M (2021)

Canada NAFTA Market Share Declining

17.1%9.6%

Source: AutoForecast Solutions – October 2014

GS Global Solutions

NAFTA LV Production(2009 – 2021)

20092010

20112012

20132014

20152016

20172018

20192020

20210

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

CanadaMexicoUnited States

8

Continued gap

increase

Source: AutoForecast Solutions – October 2014

GS Global Solutions

NAFTA LV Production(2009 – 2021)

20092011

20132015

20172019

20210

2,000,0004,000,0006,000,0008,000,000

10,000,00012,000,00014,000,00016,000,00018,000,00020,000,000

Canada MichiganSouthern US MexicoRest of NA

9

Mexico growing at the expense of Canada

Region 2013 2021

Canada 14.7% 9.6%

Michigan &Southern US

40.0% 40.7%

Mexico 18.1% 23.2%

Rest of United States

27.3% 26.5%

Source: AutoForecast Solutions – October 2014

GS Global Solutions

Canadian Production Facilities5 Major OEMS – GM, Ford, Chrysler, Honda and ToyotaGM – 2 plants in Oshawa (Camaro, Regal, Impala, XTS), CAMI Facility in Ingersoll (Equinox/Terrain)Ford – Oakville (Edge, MKX, Flex, MKT), St. Thomas (Crown Vic, Grand Marquis, Town Car – closed Sep 11)Chrysler – Brampton (300C, Charger, Challenger, Lancia Thema), Windsor (Caravan, T&C, Lancia GV, Routan)Toyota – Cambridge (RX, Corolla, Matrix), Woodstock (RAV4)Honda – Alliston 1 & 2 (Civic, CR-V)

GS Global Solutions

Canadian LV Production(2009 – 2021)

20092010

20112012

20132014

20152016

20172018

20192020

20210

500,000

1,000,000

1,500,000

2,000,000

2,500,000

ToyotaHondaGMFordFiat-Chrysler

11

VM 2013 2021 Volume Diff (2021 vs. 2013)

Fiat-Chrysler 572K 557K -15KFord 258K 246K -12KGM 627K 133K -494K

Honda 408K 394K -14KToyota 505K 470K -35KTOTAL 2,371K 1,773K -570K

Source: AutoForecast Solutions – October 2014

GS Global Solutions

Top20 Country Ranking – 2013-20212013 Rank 2013 Volume 2021 Rank 2021 Volume

China 20,905,245 China 32,157,310United States 10,884,072 United States 12,327,504

Japan 9,194,394 Japan 9,719,592Germany 5,650,674 Germany 6,176,447

South Korea 4,463,220 India 5,472,900India 3,674,104 Brazil 4,839,542Brazil 3,489,242 South Korea 4,677,959

Mexico 2,925,621 Mexico 4,395,016Thailand 2,651,035 Thailand 2,989,325Canada 2,370,493 Spain 2,844,354Spain 2,019,361 Russia 2,362,894Russia 1,909,115 France 2,144,283France 1,722,558 United Kingdom 1,929,163

United Kingdom 1,519,230 Indonesia 1,841,158

Indonesia 1,134,732 Canada 1,772,480Turkey 1,089,132 Czech Republic 1,398,801

Czech Republic 1,071,936 Turkey 1,261,532Slovakia 866,594 Italy 1,147,945

Argentina 781,940 Slovakia 1,005,616Italy 647,521 Argentina 880,392

12

<3 positions moved UP 3+ position moves UP

<3 positions moved DOWN 3+ position moves DOWN

No Change

10

15

Source: AutoForecast Solutions – July 2014

GS Global Solutions

Sales of Canadian-Assembled AP Vehicles

HondaThru October 2014

70% of domestic Honda car sales are Canadian-built.62% of domestic Honda Light Trucks are Canadian-built.

ToyotaThru October 2014

61% of domestic Toyota car sales are Canadian-built.40% of domestic Toyota Light Trucks are Canadian-built.

LexusThru October 2014

88% of domestic Lexus Light Trucks are Canadian-built.

Source: Global Automakers of Canada (GAC)– October 2014

GS Global Solutions

Canada: Production RiskFrom most stable to most risky

Honda/ToyotaProduction supports NAFTA consumptionOnly location for RAV4 production in NAFTAStrong domestic supply chain

FordOakville ONLY source of Edge, Flex, MKT, MKXNew investment in global Edge program

FCAWindsor only source for MinivansBramalea only source for Challenger, Charger, 300 (NAFTA)

GMAll Canadian-built vehicles can be built elsewhere!Equinox – 4 Locations in NAFTATerrain - 2 locations in NAFTA; exiting Canada in 2017Camaro – LEAVING Canada Prod in late 2015Regal – LEAVING Canada Prod 2017Impala – LEAVING Canada Prod late 2019XTS – Replaced by LTS in 2016/2017 (Hamtramck/China)

Source: AutoForecast Solutions – July 2014

GS Global Solutions

Top 20 Country Analysis(2013 vs. 2021)

ChinaUnited States

JapanGermany

South KoreaIndia

BrazilMexico

ThailandCanada

SpainRussiaFrance

United KingdomIndonesia

TurkeyCzech Republic

SlovakiaArgentina

Italy

0 20,000,000

2021 2013

South Korea (#7)

India (#5)

Brazil (#6)

Canada (#15)

Spain (#10)

Russia (#11)

France (#12)

United Kingdom (#13)

Indonesia (#14)

Turkey (#17)

Czech Republic (#16)

Slovakia (#19)

Argentina (#20)

Italy (#18)

-5 -4 -3 -2 -1 0 1 2

2021 Ranking Moves

15

Source: AutoForecast Solutions – October 2014

GS Global Solutions

Canadian Complete Vehicle vs. Parts Exports

GS Global Solutions

Why is Canada the best place in the G7 to do business?

Strongest Economic Growth in the G7

The Soundest Banking System in the World

The Lowest Business Costs in the G7

1 The International Monetary Fund. World Economic Outlook April 2010.2 The World Economic Forum. The Global Competitiveness Report 2010 - 2011.3 KPMG. Competitive Alternatives 2010.

GS Global Solutions

Connected Vehicle

CUTACanadian Urban

Transit Association

ITS CanadaIntelligent

Transportation Systems

APMAAutomotive Parts

Manufacturers

AcademiaUniversity

Researchers

Government

Federal & Provincial

CTA – OTACanadian & Ontario

Trucking Associations

EMCElectric Mobility

CanadaFirst

RespondersPolice/ Fire/Ambulance

Canadian Connected Vehicle Expertise

GS Global Solutions

6. Supply-Chain Transformation

1. Customer Facing Focus

Increasingthe Value

of theBusiness

10. Core Competencies

9. Systems & Modules

8. Globalization

7. Resource Pressure

2. Growth

3. Cost Reduction

4. Technology

5. Brand Management

Global Supplier Trends