it sector update - mailers.sparkcapital.inmailers.sparkcapital.in/uploads/daily/sector...

TRANSCRIPT

IT Sector Update Sector Outlook

Neutral

Stock performance (%)

1m 3m 12m

CNXIT (0.3) (10.3) 23.6

Sensex (2.3) (8.2) 3.5

Date June 10, 2015

Market Data

SENSEX 26482

Nifty 8022

CNX IT 11143

Relative performance

Impact of Redefining Demand environment

In this report, we discuss three themes: Digital, Rebirth of Captives and attrition. We believe these three themes

are intertwined and drive each other. Digital has been a buzzword in the sector over the last couple of years and

this shift is being driven by rapid changes in technology. The key differentiator for vendors in Digital would be

their ability to demonstrate deep domain knowledge and build use case, thus favouring firms which has higher

consultative approach to selling. Companies under our coverage are investing significantly to beef up their

capabilities resulting in increased cost in people and capability development. Number of global corporations are

increasingly leveraging technology to drive their competitive advantage and this decision is driving higher

usage of captives especially in newer areas of spend “Change the business”. Coupled with increased

compliance requirements especially in BFS, we believe captives are back in vogue. A combination of increased

competitive pressure, growth of captives and weakness in select verticals such as Oil & Gas and Retail would

result in constant currency revenue growth of 10-11% for FY16E. We retain our preference for large-caps in the

sector with TCS and Wipro being our top picks.

Digital a double edged sword for vendors: Companies especially with high consumer interaction are adopting digital

technologies in a hurry, with some of the companies relying on vendors while others such as Tesco, Target and Wal-

Mart are using in-house capabilities. Even companies, which have existing vendors, are leaning in favour of vendors

with not only strong technological capability but also deep domain knowledge and ability to deliver outcomes such as

better customer satisfaction, higher revenues or lower costs. Vendors are investing significant resources to partner with

clients in their chosen verticals.

Rise of Captives: Our channel checks indicate increased activity from captive centres in India especially in BFS

vertical. The common thread across these captives are in two areas: 1) Incremental discretionary spend in digitizing

their business process or to drive better insights into customers 2) Activities focused on regulatory reporting and

compliance in BFS.

Spike in attrition: Industry level attrition is at four year high led by strong growth in captives rapid growth in

ecommerce and increased start up activity in India. Traditionally increased attrition has been correlated with better

revenue growth, however we do not subscribe to this view for FY16E/FY17E. Higher attrition and fight for talent would

impact offshore costs for vendors.

TCS and Wipro top picks: Large-caps are our preferred ownership in the sector especially TCS and Wipro led by

diversified business and attractive risk reward. We would continue to stay away from mid caps as the risk reward

continues to be unattractive with low growth differential. Also, we believe companies (like Persistent) which have

technical capabilities and weak domain expertise would face strong revenue headwinds in the coming years

SRIVATHSAN RAMACHANDRAN, CFA [email protected] +91 44 4344 0039

AISHWARIYA KPL [email protected] +91 44 4344 0040 Find Spark Research on Bloomberg (SPAK <go>),

Thomson First Call, Reuters Knowledge and Factset

Page 1

Sector Update

-10%

0%

10%

20%

30%

40%

50%

Jun-1

4

Aug-1

4

Oct-

14

Dec-1

4

Feb-1

5

Apr-

15

Jun-1

5

Sensex Index

CNXIT Index

IT Sector Update Sector Outlook

Neutral

Page 2

IT coverage universe

* * Dec end FY16E refers to CY15E; *** June end, * adjusted for treasury shares

Financial summary

P/E EV/EBITDA EV/sales

Company CMP Rs. TP Rs. Rating FY15P FY16E FY17E FY15P FY16E FY17E FY15P FY16E FY17E

Cyient 530 550 Add 16.8 15.1 13.5 12.9 9.7 9.0 1.9 1.5 1.4

eClerx 1,562 1,140 Sell 21.0 18.3 17.8 16.2 13.2 13.2 5.4 4.9 4.6

Firstsource 29 45 Buy 8.8 7.0 6.1 5.5 4.5 3.4 0.7 0.6 0.5

HCL Tech*** 911 850 Reduce 17.0 17.4 16.5 12.7 12.3 11.4 3.2 2.9 2.6

Hexaware** 277 240 Reduce 25.6 19.8 17.9 16.2 13.8 13.0 3.0 2.6 2.3

Infosys 1,992 2,060 Add 18.5 18.3 17.4 13.6 12.6 11.7 3.8 3.5 3.1

KPIT 104 120 Reduce 8.7 8.6 7.5 6.3 5.1 4.6 0.7 0.7 0.6

Mindtree 1,356 940 Sell 21.4 21.2 20.2 15.3 13.8 12.9 3.0 2.6 2.3

Mphasis 372 330 Reduce 11.6 11.7 11.3 6.8 6.6 5.8 1.1 1.0 0.9

NIIT Tech 387 370 Reduce 20.7 12.8 10.5 8.8 5.6 5.7 0.9 0.8 0.8

Persistent 748 560 Sell 20.6 20.3 18.8 13.7 11.9 11.0 2.8 2.5 2.2

TCS 2,562 2,590 Add 25.5 22.4 20.8 17.7 16.1 15.0 5.1 4.6 4.2

Tech Mahindra* 541 560 Add 18.1 16.3 14.6 12.1 11.4 10.3 2.2 1.9 1.7

Wipro 544 620 Add 15.5 14.6 14.2 11.4 10.1 9.4 2.6 2.4 2.1

Intellect 101 140 Buy NM NM 87.8 NM NM 73.4 0.9 0.8 0.8

IT Sector Update Sector Outlook

Neutral

Page 3

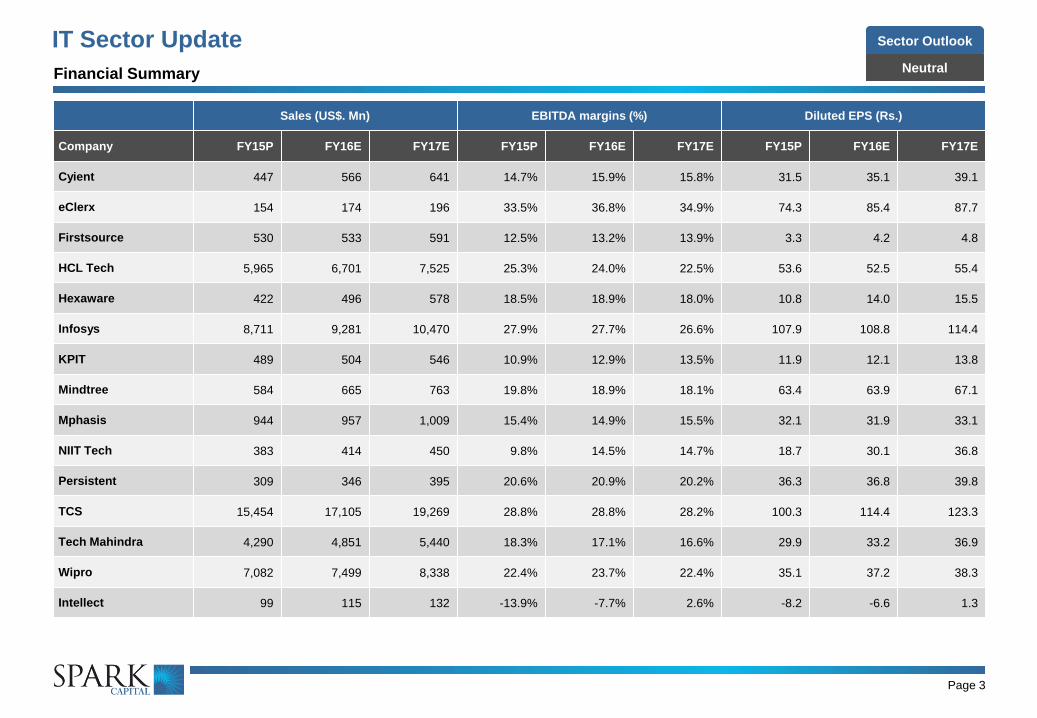

Sales (US$. Mn) EBITDA margins (%) Diluted EPS (Rs.)

Company FY15P FY16E FY17E FY15P FY16E FY17E FY15P FY16E FY17E

Cyient 447 566 641 14.7% 15.9% 15.8% 31.5 35.1 39.1

eClerx 154 174 196 33.5% 36.8% 34.9% 74.3 85.4 87.7

Firstsource 530 533 591 12.5% 13.2% 13.9% 3.3 4.2 4.8

HCL Tech 5,965 6,701 7,525 25.3% 24.0% 22.5% 53.6 52.5 55.4

Hexaware 422 496 578 18.5% 18.9% 18.0% 10.8 14.0 15.5

Infosys 8,711 9,281 10,470 27.9% 27.7% 26.6% 107.9 108.8 114.4

KPIT 489 504 546 10.9% 12.9% 13.5% 11.9 12.1 13.8

Mindtree 584 665 763 19.8% 18.9% 18.1% 63.4 63.9 67.1

Mphasis 944 957 1,009 15.4% 14.9% 15.5% 32.1 31.9 33.1

NIIT Tech 383 414 450 9.8% 14.5% 14.7% 18.7 30.1 36.8

Persistent 309 346 395 20.6% 20.9% 20.2% 36.3 36.8 39.8

TCS 15,454 17,105 19,269 28.8% 28.8% 28.2% 100.3 114.4 123.3

Tech Mahindra 4,290 4,851 5,440 18.3% 17.1% 16.6% 29.9 33.2 36.9

Wipro 7,082 7,499 8,338 22.4% 23.7% 22.4% 35.1 37.2 38.3

Intellect 99 115 132 -13.9% -7.7% 2.6% -8.2 -6.6 1.3

Financial Summary

IT Sector Update Sector Outlook

Neutral

Page 4

Our current estimates assumes Rs./$ rate of Rs.60.8/$ for FY16E & Rs.58/$ for FY17E. Given below is the EPS sensitivity analysis at various rates

Source: Spark Capital Research

Company Name

FY16E EPS FY17E EPS

Rs.60/$ Rs.62/$ Rs.64/$ Rs.58/$ Rs.60/$ Rs.62/$

Cyient 35.1 37.2 39.0 39.1 41.5 43.6

eClerx 85.4 91.8 97.1 87.7 94.5 100.2

HCL Tech 52.5 55.7 58.4 55.4 58.8 61.7

Hexaware 14.0 14.7 15.4 15.5 16.3 17.0

Infosys 108.8 115.4 121.0 114.4 121.5 127.6

KPIT 12.1 12.8 13.4 13.8 14.7 15.4

Mindtree 63.9 68.2 71.5 67.1 71.7 75.3

Mphasis 31.9 33.5 34.8 33.1 34.8 36.2

NIIT Tech 30.1 31.8 33.1 36.8 38.9 40.6

Persistent 36.8 39.4 41.4 39.8 42.7 44.9

TCS 114.4 121.2 127.1 123.3 130.9 137.5

Tech Mahindra 33.2 35.2 36.9 36.9 39.2 41.2

Wipro 37.2 39.4 41.4 38.3 40.6 42.7

IT Sector Update Sector Outlook

Neutral

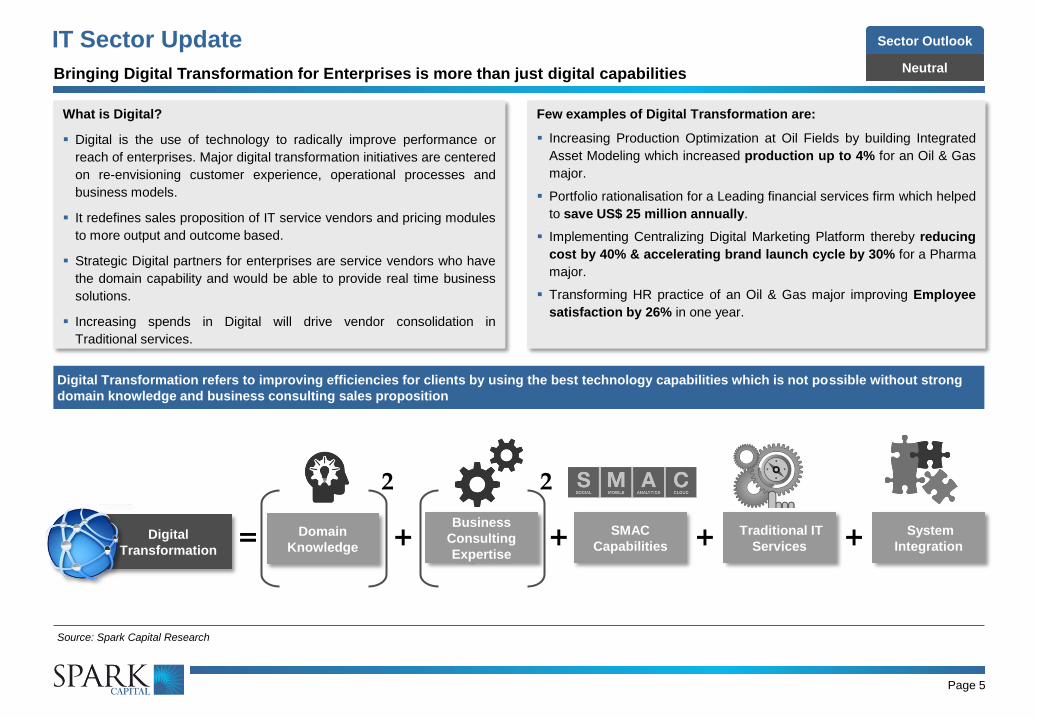

Digital Transformation refers to improving efficiencies for clients by using the best technology capabilities which is not possible without strong

domain knowledge and business consulting sales proposition

Source: Spark Capital Research

Page 5

Digital

Transformation

SMAC

Capabilities

Traditional IT

Services

System

Integration = + + + + Domain

Knowledge

2

Business

Consulting

Expertise

2

What is Digital?

Digital is the use of technology to radically improve performance or

reach of enterprises. Major digital transformation initiatives are centered

on re-envisioning customer experience, operational processes and

business models.

It redefines sales proposition of IT service vendors and pricing modules

to more output and outcome based.

Strategic Digital partners for enterprises are service vendors who have

the domain capability and would be able to provide real time business

solutions.

Increasing spends in Digital will drive vendor consolidation in

Traditional services.

Few examples of Digital Transformation are:

Increasing Production Optimization at Oil Fields by building Integrated

Asset Modeling which increased production up to 4% for an Oil & Gas

major.

Portfolio rationalisation for a Leading financial services firm which helped

to save US$ 25 million annually.

Implementing Centralizing Digital Marketing Platform thereby reducing

cost by 40% & accelerating brand launch cycle by 30% for a Pharma

major.

Transforming HR practice of an Oil & Gas major improving Employee

satisfaction by 26% in one year.

Bringing Digital Transformation for Enterprises is more than just digital capabilities

IT Sector Update Sector Outlook

Neutral Case study explaining how Digital solution is a bundled offering

Page 6

Digital (Big Data Analytics) Case Study: How Infosys helped a US

based Pharmacy Retailer to reduce shrink by 5%

Background:

A US based pharmaceutical retailer which operates more than 5,000 stores

globally. The client had challenges with the existing loss prevention

management system. Large scale of operations and disparate data

sources slowed their ability to take informed, timely decisions which further

affected their ability to reduce losses across all its stores.

Business Need:

A solution which enables management of unwarranted losses arising from

theft, wastage and poor inventory management (commonly known as

shrink) and improve profitability with the existing hardware infrastructure.

Notably, these losses are close to 1% of the overall revenue in the retail

industry and the average net profitability is also 1%, which means

profitability will be a washout if losses are not arrested.

IT Solution:

1. A centralised data repository which stores data in structured data model

2. Alert based reporting capabilities which uses consolidated data from all

sources including POS data, stock ledger data, store data, master data

etc.

3. Advanced analytics to track and manage losses at store and SKU level

and project data for future analysis.

Outcome achieved:

1. Client was able to identify additional losses prevention cases which

reduced the losses by 5%

2. Time taken to identify a “case” reduced from 6-8 weeks to less than a

week while time taken for data mining reduced from 4-6 weeks to less

than a week.

Case Process chart shows how Digital offering is a bundled product of

traditional IT services with Analytics services

Source: Company, Spark Capital Research

Page 6

Data Collection

Streamlining of Data

Creating Repository of Consolidated Data

Data Validation & Testing

Analytics on Collected Data

Creation of Virtual Store Setup

Creation of Similar User Interface Across all

System

Communication among all servers to fetch real-

time data

Modeling existing data for future analysis on

real-time basis (e.g. Inventory loss, Mismatch)

Generating reports on consistent basis

Data

Warehousing

Testing

Data

Analytics

Digital

User Interface

Digital

User Interface

System

Integration

Data

Analysis

BPO

In memory for processing real-time data Storage &

Services

Source: http://www.infosys.com/industries/retail/casestudies/Documents/loss-prevention-

pharmacy-retailer.pdf

IT Sector Update Sector Outlook

Neutral

Digital or SMAC is a new layer complemented by Traditional IT services. We subscribe to TCS, CTSH and INFY’s view that

Digital revenues can’t be quantified separately as deals won are bundled with Traditional IT services.

Going ahead, growth in Digital services will drive growth in Traditional IT services as well.

Page 7

Digital is not a Standalone

Service

Digital offerings begin as pilot projects or as proof of concept to an existing client. As these deals materialize and gain scale,

service providers get upgraded as strategic Digital partners and scale up market share with the client. With increasing budget

allocations to Digital, companies would reduce the budgets for Traditional IT services. This would drive vendor

consolidation across major accounts in the medium term.

Digital Transformation

Projects Would Drive Vendor

Consolidation in Traditional IT

services

When Digital moves from peripheral to core processes of companies the differentiation for the IT service vendor is not only in

Digital capabilities but also domain expertise and consulting acumen.

Vertical strength differs across companies and large caps (including CTSH, ACN, CapGemini) are more strongly positioned

given their traditional consulting practice.

Vishal Sikka’s recent initiative of increasing collaborative efforts of consultants & sales managers of Traditional IT services

would aid Infosys in winning more deals & other companies would follow suit.

We believe companies (like Persistent) which have technical capabilities and weak domain expertise would face

strong revenue headwinds in the coming years

Digital transforms sales

proposal from an IT service

proposition to business

consulting proposition

Pricing from Traditional services would continue to decline for all companies.

It would not be surprisingly to see sharp pricing decline for ISPs (like Infosys 4QFY15) in the near term.

Lower realisations will bring in cost rationalisation across ISPs and we would see decline in travel expenses, pyramid

rationalisation and sharp increased in utilisation in the near term.

Channel checks indicate there are price cuts of 5%-15% across some verticals.

Pricing would become

increasingly become more

outcome and output based

from fixed and T&M

We will see business consulting firms (like McKinsey, Deloitte Bain, BCG, Booz etc.) developing IT capabilities either

by organically or inorganically (acquisitions or by strategic partnerships).

Strategic partnerships with consulting firms would be a win win situation for mid cap service providers who have limited domain

expertise or Digital capabilities

Deloitte is the strong growing contender in both spaces. Deloitte IT services had a CAGR of 9.5% in the last six years and is a

US$ 17.5 bn entity (FY14)

Differentiation between IT

service providers and

consulting firms would

become minimal

Digital Transformation: Key pointers

CTSH – Cognizant; ACN - Accenture

IT Sector Update Sector Outlook

Neutral

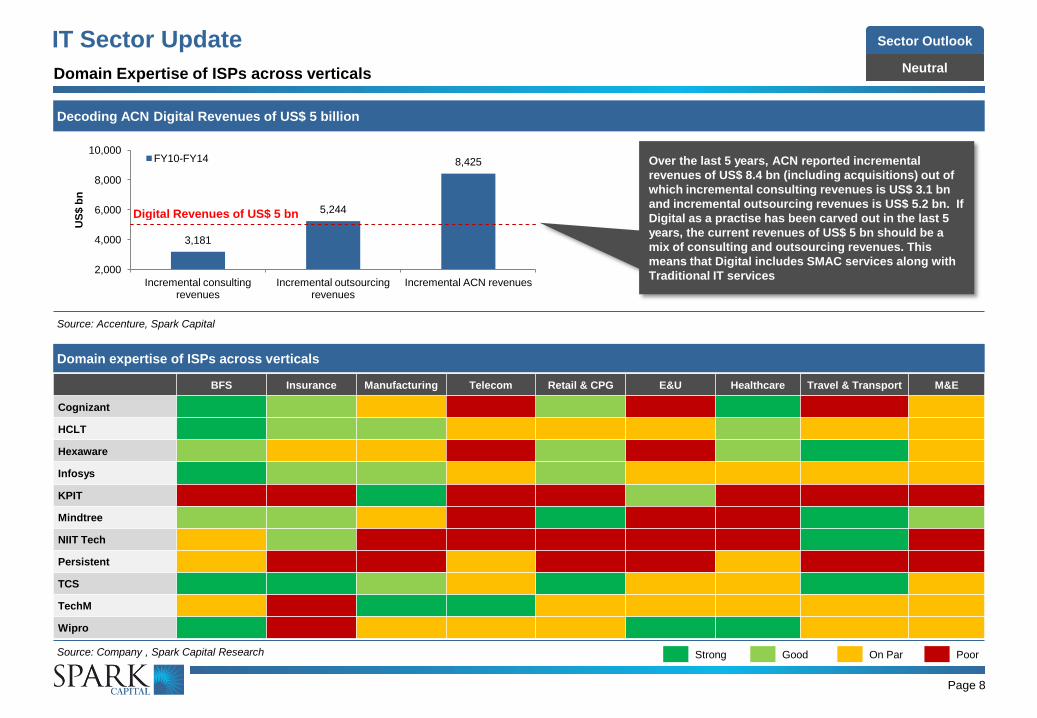

Domain expertise of ISPs across verticals

Source: Company , Spark Capital Research

Page 8

Decoding ACN Digital Revenues of US$ 5 billion

Source: Accenture, Spark Capital

Over the last 5 years, ACN reported incremental

revenues of US$ 8.4 bn (including acquisitions) out of

which incremental consulting revenues is US$ 3.1 bn

and incremental outsourcing revenues is US$ 5.2 bn. If

Digital as a practise has been carved out in the last 5

years, the current revenues of US$ 5 bn should be a

mix of consulting and outsourcing revenues. This

means that Digital includes SMAC services along with

Traditional IT services

3,181

5,244

8,425

2,000

4,000

6,000

8,000

10,000

Incremental consulting revenues

Incremental outsourcing revenues

Incremental ACN revenues

US

$ b

n

FY10-FY14

Digital Revenues of US$ 5 bn

Strong Good On Par Poor

Domain Expertise of ISPs across verticals

BFS Insurance Manufacturing Telecom Retail & CPG E&U Healthcare Travel & Transport M&E

Cognizant

HCLT

Hexaware

Infosys

KPIT

Mindtree

NIIT Tech

Persistent

TCS

TechM

Wipro

IT Sector Update Sector Outlook

Neutral

Deloitte: The silent competitor whose inherent strength could pose

huge risks to ISPs

Deloitte is one the most reputed consultancy firms which provides audit,

consulting, financial advisory, tax related services and enterprise risk

services to various clients worldwide.

As of FY14, Deloitte had revenues of US$ 34.2 bn out of which US$

17.5 bn revenues are from IT services. This segment grew at a CAGR

of 9.5% over the last six years.

Given strong Digital capabilities and domain expertise, Deloitte has

been winning significant deals in the tech space. Strengthening foothold

of Deloitte could pose huge risks to traditional IT services firms.

Deloitte IT services revenue grew at a CAGR of 9.5% over the last 6

years

Source: Bloomberg, Spark capital

Deloitte IT services is the Fifth largest company (by revenues) in the

Tech space

Source: NASSCOM, Company

Deloitte: The silent competitor whose inherent strength could pose huge risks to ISPs

Page 9

Deloitte capabilities in the emerging service lines as rated by third

party consultants:

Global Leader in Analytics IT consulting – Kennedy consulting research

and advisory

Worldwide Leader in business consulting Service – IDC Marketscape

Leader in Business Intelligence in Asia Pacific - Forrester Research

Global leader in HR process consulting – Kennedy consulting research

and advisory

Leader in Life science sector consulting - Kennedy consulting research

and advisory

Leader in mobility IT and strategy Consulting - Kennedy consulting

research and advisory

10.7%

14.9%

10.9% 5.1%

6.2%

0.0%

4.0%

8.0%

12.0%

16.0%

0

4,000

8,000

12,000

16,000

20,000

2010 2011 2012 2013 2014

US

$ m

n

Revenues YoY Growth

56.4

32.5 29.0

18.9 17.5

0

10

20

30

40

50

60

IBM Global Services

HP Services Accenture PLC

Fujitsu Ltd Deloitte Consulting

LLP

US

$ b

n

ISP – Indian service provider

IT Sector Update Sector Outlook

Neutral

Page 10

Disruptions is happening at all layers of IT stack whether it is Servers, Storage, Software, Network or Applications

Source: Company , Spark Capital Research

Professional

Services

Professional

Services

Professional

Services

Professional

Services

Professional

Services

Applications

Data

Runtime

Middleware

O/S

Virtualization

Servers

Storage

Networking

Applications

Data

Runtime

Middleware

O/S

Virtualization

Servers

Storage

Networking

Applications

Data

Runtime

Middleware

O/S

Virtualization

Servers

Storage

Networking

Applications

Data

Runtime

Middleware

O/S

Virtualization

Servers

Storage

Networking

Applications

Data

Runtime

Middleware

O/S

Virtualization

Servers

Storage

Networking

Four disruptions to traditional IT services – SaaS, IaaS, PaaS, BPaaS

On-Premises Infrastructure as a

Service

Platform as a

Service

Software as a

Service

Business Process

as a service

Managed by the Enterprise either in-house or outsourced Managed by cloud vendors

IT Sector Update Sector Outlook

Neutral

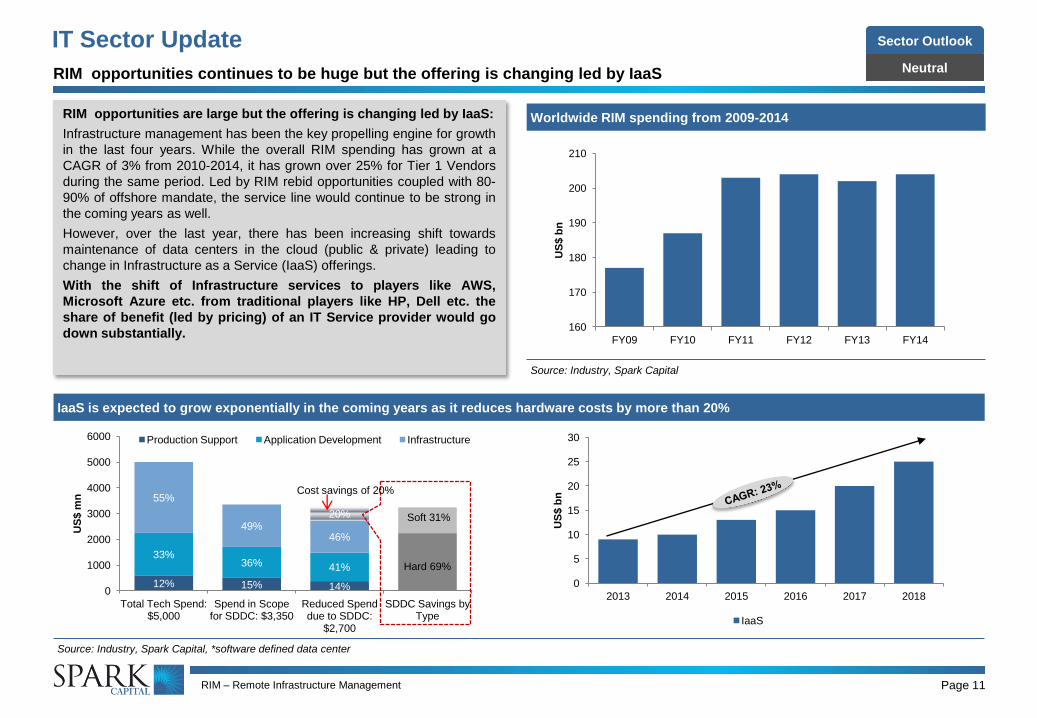

RIM opportunities are large but the offering is changing led by IaaS:

Infrastructure management has been the key propelling engine for growth

in the last four years. While the overall RIM spending has grown at a

CAGR of 3% from 2010-2014, it has grown over 25% for Tier 1 Vendors

during the same period. Led by RIM rebid opportunities coupled with 80-

90% of offshore mandate, the service line would continue to be strong in

the coming years as well.

However, over the last year, there has been increasing shift towards

maintenance of data centers in the cloud (public & private) leading to

change in Infrastructure as a Service (IaaS) offerings.

With the shift of Infrastructure services to players like AWS,

Microsoft Azure etc. from traditional players like HP, Dell etc. the

share of benefit (led by pricing) of an IT Service provider would go

down substantially.

Worldwide RIM spending from 2009-2014

Source: Industry, Spark Capital

IaaS is expected to grow exponentially in the coming years as it reduces hardware costs by more than 20%

Source: Industry, Spark Capital, *software defined data center

Page 11

RIM opportunities continues to be huge but the offering is changing led by IaaS

12% 15% 14%

33% 36% 41%

55%

49% 46%

20%

0

1000

2000

3000

4000

5000

6000

Total Tech Spend: $5,000

Spend in Scope for SDDC: $3,350

Reduced Spend due to SDDC:

$2,700

SDDC Savings by Type

US

$ m

n

Production Support Application Development Infrastructure

Hard 69%

Soft 31%

Cost savings of 20%

160

170

180

190

200

210

FY09 FY10 FY11 FY12 FY13 FY14

US

$ b

n

0

5

10

15

20

25

30

2013 2014 2015 2016 2017 2018

US

$ b

n

IaaS

RIM – Remote Infrastructure Management

IT Sector Update Sector Outlook

Neutral

Universe of Cloud Services

)

Source: Cap Gemini, Spark Capital

Revenue/Employee & margins of Standalone Platform BPO companies

Source: Spark Capital

CLOUD

UNIVERSE

SaaS

PaaS

En

ab

lem

en

t an

d

Pro

fessio

na

l S

erv

ices

IaaS

ERP

CRM

Security

Billing Document

Management Communication

and Collaboration Business

Intelligence Digital

Content

Creation

Content

Management

Desktop

Productivity

Consulting

Maintenance

and Support

Wholesale

Capacity

White Label

Services

Cloud

Broker

System

Integration

Disaster

Recovery

Hosting on

Demand

Service

Management

Storage

on Demand

Testing and

Development

Compute

on Demand

Backup

Services

Virtual

Servers

App Server

Database

Integration

Middleware

Network Assets Object Data Stores

Message Queues

Application Development

Environment

SCM

BPaaS would become increasingly popular in the BPO space:

With the increase adoption of SMAC, As-a-Service business proposition

has become very popular and better defined. Subscription based models in

SaaS is extending to Pay as you use and Pay per transaction (in PaaS and

IaaS) respectively. However, this business proposition is not entirely a new

concept as Standalone BPO platforms entities especially in payments

processing, payrolls, procurement etc. has been working on these modules

for the last 10 years. These business operate at an healthy EBITDA

margins of ~30% and have better Rev/employee metrics than both IT and

BPO players. With domain based BPO to continue on a strong growth

trajectory, BPaaS would grow better than legacy outsourcing in the coming

years.

Among ISPs, large caps (TCS, Infosys & Wipro, CTSH) have strong

BPO platforms, with TCS Diligenta earning the largest revenue

amongst all. However, IT mid caps doesn't have scalable BPO

platforms and we believe this would reduce BPO growth in mid caps

in 2-3 year timeframe.

As a service business proposition would replace legacy outsourcing

Page 12

EBITDA margins (%) Rev/employee ('000)

Paychex Inc. 43% 198

ADP 22% 200

FIS 30% 160

Fiserv Corp. 32% 241

Global payment Inc. 21% 618

Jack Henry & Associates 35% 235

IT Sector Update Sector Outlook

Neutral

Industry wise attrition remains at an all time high despite tepid

revenue growth

Source: Company, Spark Capital, *includes cognizant and excludes Mphasis, TechM & KPIT

With SMAC gaining momentum, the number of start-ups incorporated

in India is on the rise and expected to quadruple by 2020

Source: NASSCOM, Company

29.0

%

23.8

%

11.4

%

14.1

%

11.9

%

19.9

%

14.6

%

15.6

%

17.4

%

18.0

%

0%

5%

10%

15%

20%

25%

30%

35%

FY11 FY12 FY13 FY14 FY15

US$ revenue growth Attrition (%)

Industry wise attrition – led by change in market dynamics while

overall demand environment continues to be stable:

Historically, sharp increase in attrition among ISPs used to be a leading

indicator for better revenue growth. However, in the last six quarters,

though attrition has increased more than 200 bps across companies,

demand commentary continues to remain tepid. We believe FY16E

industry revenue growth would come in at the lower end of the

NASSCOM guided range of 11-13%.

The disconnect is primarily led by increase in the number of start-ups

especially in the SMAC space, strong hiring by captives with renewed

focus on insourcing and increase in involuntary attrition. Notably, sharp

increase in attrition not only point at supply side changes but also shift in

demand environment as well.

Industry level attrition at the highest level in the last 4 years

Page 13

Tech Start-ups employs around 65,000 to 75,000 people as of 2014:

India currently has more than 3,100 start-ups with 800+ start-ups added

in 2014. Led by the Digital & E-Commerce wave coupled with strong

funding by PE players & Tech giants, the start-up count is expected to

increase to 11,500+ by 2020, while the number of employees is expected

to move up to 2,50,0000 to 3,50,000 from the current 65,000-75,000.

Notably, more than 60% of these start-ups boosts of a decent presence in

either Big Data, App Development, Cloud or IoT space. The Top tier

among the start ups boosts of fortune 500 companies like Citi, AIG, P&G,

Microsoft, Pfizer, Novartis, Airbus, Boeing etc.

With increase in demand for niche services and strong access to capital,

start-ups could provide stiff competition in hiring limited talent (especially

in Digital).

480 525 590 680

805

2000

0

500

1000

1500

2000

2500

2010 2011 2012 2013 2014 2020

IT Sector Update Sector Outlook

Neutral

As of FY15, GIC contributes around US$ 27 bn of the total IT-BPM revenues (US$ 7.5 bn – IT, US$ 5.5 bn - BPM, US$ 14 bn – ER&D) and employs

around 10-15%, 20-25% and 55-60% of total employees in IT, BPM and ER&D segments respectively

Source: NASSCOM, Spark Capital

ISP 70-72%

GIC 10-15%

MNC 10-15%

ISP 60-65% GIC 20-25%

MNC 15-16%

ISP 28-35%

GIC 55-60%

MNC 10-12%

Page 14

Insourcing is gaining more steam across all verticals and this time it is different:

Our channel checks and media reports suggest insourcing is gaining more steam over the last two years with more than 70 companies setting up GICS in

India increasing the total number to 1,440+. Existing captives are aggressively increasing the headcount as well. The pickup in captive activity is seen

across verticals, largely skewed towards BFS and most of the captives are putting in capabilities to gain end-to-end ownership of products/processes.

Channel checks indicates gross hiring in captives could be around 2,00,000-2,50,000 for FY16E. We believe the change in trend from outsourcing to

insourcing is led by key structural changes in enterprises due to which we believe captives, this time, is here to stay forever. The changes include:

1. Technology is getting redefined as core competency with increased focus in Digital & Analytics investments. Companies prefer to establish their our

R&D centers rather than outsourcing to a third party vendor. E.g. Wal-Mart Labs established a tech centre in Bangalore to take on its E-commerce rival

Amazon.

2. During 2006-2010 period, most Indian captives were managed by employees of the parent company with less stringent processes on utilisation rates,

employee pyramid and cost structures which made outsourcing to a third party vendor more profitable. Today, most of the GICs are managed by ex-

veterans of ISP who have prior in hand experience in rationalizing pyramid, driving utilisation rates, offshore effort etc., which has made GICs more

profitable than outsourcing to ISPs.

3. With the recent data breach in some banks and a retail firm, companies have become increasingly reluctant to offshore work related to data

compliance, security and competitive differentiated offerings.

IT

Number of people employed by MNC, GIC & ISP as % of total employees in IT, BPM & ER&D segments

Insourcing is gaining more steam and this time it is different

BPM ER&D

GIC – Global In house center

IT Sector Update Sector Outlook

Neutral

Page 15

Interesting quotes on reasons for insourcing:

“Silicon Valley is coming. There are hundreds of start-ups with a lot of

brains and money working on various alternatives to traditional banking,

There is much for us to learn in terms of real-time systems, better

encryption techniques, and reduction of costs and ‘pain points’ for

customers” – Jamie Dimon, Chairman and CEO JP Morgan on

disruption technology.

“We are changing our technology DNA, because historically most of our

technology has been outsourced to third-party vendors. But now we’re like,

“hey we’ve got to build world-class capability”, because we are not

competing with an average technology company. We are competing with a

top technology company like, say, Amazon. It’s a technology company first

and a retailer second” – Naveen Kapoor, MD, Target India.

Snapshot of few insourcing activities across Global majors

Company Vertical/ Country of Origin Hiring Target Other Details

RBS BFSI/UK 5,600 (12 mths) Current strength: 14,000 Major hiring in Analytics (SaaS & SQL).

Citibank BFSI/US 3,500 Developing centers in Chennai & Pune, establishing management team

Astra Zeneca Pharma/UK 400 Center in Chennai, current strength 600 and plans to increase headcount to 2,500

Visa BFSI/US 2,000 Center in Bangalore, for development of key API and SDKs.

Danse Bank BFSI/Denmark 800 Establishing captive in Bangalore. Buying out employees of ITC Infotech, used to handle IT activities of

Danse Bank from 2006.

Daimler Auto/Germany 1,000 Center in Bangalore housing more than 2,300 people out of which 1,100 are part of IT team and

remaining are R&D engineers

Red Mart Retail/Singapore Development center in Bangalore for Analytics.

Cargill Food & Agri/US 650 Center in Bangalore, hired 120 people. Planning to increase the total strength to 1,000 overtime

MasterCard BFSI/US Center Baroda & Pune. To build mobility solutions such as Master-Pass

Source: Channel checks, News Articles, Spark Capital

Revenue and cost implications for ISPs led by captives

Implications for ISPs:

Ramp up in captive strength is revenue detrimental for ISPs especially for

companies which have large revenue contribution from a single client (E.g.

Polaris Consulting earns > 40% of revenues from Citi Bank) and for IT

service vendors who have a huge exposure to services like Risk &

Compliance, Security etc. E.g. Mphasis has a huge exposure to Risk &

Compliance activities of U.S banks.

Captives in India are scouting for the top talent especially in Digital areas

and are willing to pay top dollars for them. With these resources being

limited, strong demand can drive up salaries for Digital segments, posing

strong headwinds to margins.

IT Sector Update Sector Outlook

Neutral Disclaimer

Page 16

0

500

1000

1500

2000

1-May-12 1-Nov-12 1-May-13 1-Nov-13 1-May-14 1-Nov-14 1-May-15

Historical Target

eClerx

0

10

20

30

40

50

60

1-May-12 1-Nov-12 1-May-13 1-Nov-13 1-May-14 1-Nov-14 1-May-15

Historical Target

Firstsource Solutions

0

200

400

600

800

1000

1200

1-May-12 1-Nov-12 1-May-13 1-Nov-13 1-May-14 1-Nov-14 1-May-15

Historical Target

HCL Tech

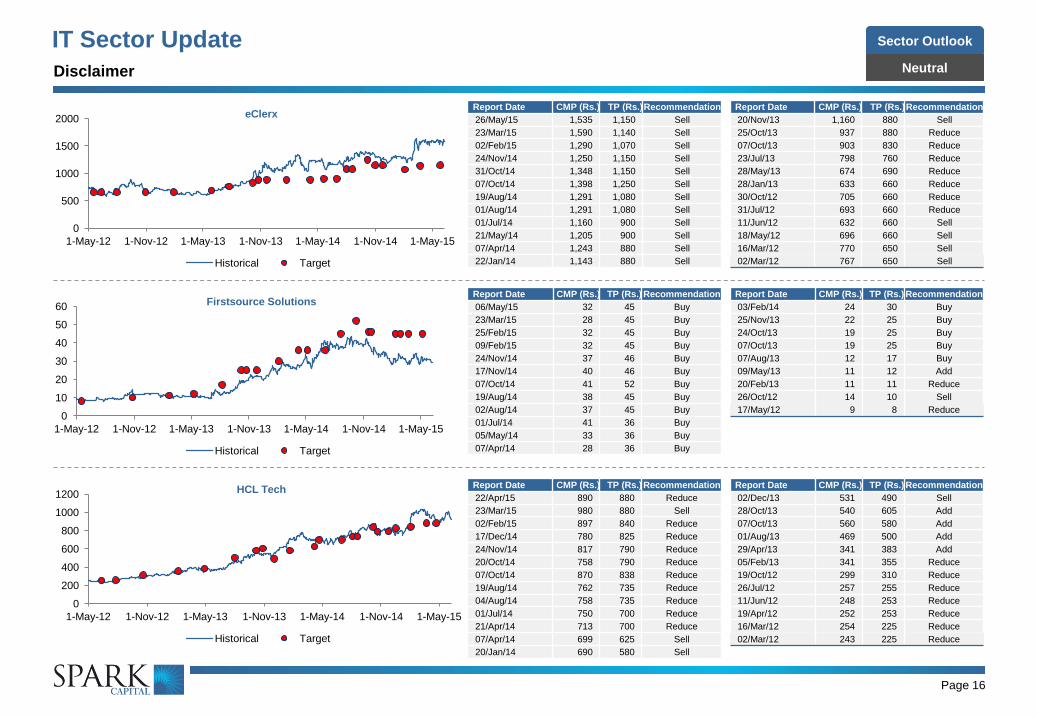

Report Date CMP (Rs.) TP (Rs.) Recommendation

26/May/15 1,535 1,150 Sell

23/Mar/15 1,590 1,140 Sell

02/Feb/15 1,290 1,070 Sell

24/Nov/14 1,250 1,150 Sell

31/Oct/14 1,348 1,150 Sell

07/Oct/14 1,398 1,250 Sell

19/Aug/14 1,291 1,080 Sell

01/Aug/14 1,291 1,080 Sell

01/Jul/14 1,160 900 Sell

21/May/14 1,205 900 Sell

07/Apr/14 1,243 880 Sell

22/Jan/14 1,143 880 Sell

Report Date CMP (Rs.) TP (Rs.) Recommendation

20/Nov/13 1,160 880 Sell

25/Oct/13 937 880 Reduce

07/Oct/13 903 830 Reduce

23/Jul/13 798 760 Reduce

28/May/13 674 690 Reduce

28/Jan/13 633 660 Reduce

30/Oct/12 705 660 Reduce

31/Jul/12 693 660 Reduce

11/Jun/12 632 660 Sell

18/May/12 696 660 Sell

16/Mar/12 770 650 Sell

02/Mar/12 767 650 Sell

Report Date CMP (Rs.) TP (Rs.) Recommendation

06/May/15 32 45 Buy

23/Mar/15 28 45 Buy

25/Feb/15 32 45 Buy

09/Feb/15 32 45 Buy

24/Nov/14 37 46 Buy

17/Nov/14 40 46 Buy

07/Oct/14 41 52 Buy

19/Aug/14 38 45 Buy

02/Aug/14 37 45 Buy

01/Jul/14 41 36 Buy

05/May/14 33 36 Buy

07/Apr/14 28 36 Buy

Report Date CMP (Rs.) TP (Rs.) Recommendation

03/Feb/14 24 30 Buy

25/Nov/13 22 25 Buy

24/Oct/13 19 25 Buy

07/Oct/13 19 25 Buy

07/Aug/13 12 17 Buy

09/May/13 11 12 Add

20/Feb/13 11 11 Reduce

26/Oct/12 14 10 Sell

17/May/12 9 8 Reduce

Report Date CMP (Rs.) TP (Rs.) Recommendation

22/Apr/15 890 880 Reduce

23/Mar/15 980 880 Sell

02/Feb/15 897 840 Reduce

17/Dec/14 780 825 Reduce

24/Nov/14 817 790 Reduce

20/Oct/14 758 790 Reduce

07/Oct/14 870 838 Reduce

19/Aug/14 762 735 Reduce

04/Aug/14 758 735 Reduce

01/Jul/14 750 700 Reduce

21/Apr/14 713 700 Reduce

07/Apr/14 699 625 Sell

20/Jan/14 690 580 Sell

Report Date CMP (Rs.) TP (Rs.) Recommendation

02/Dec/13 531 490 Sell

28/Oct/13 540 605 Add

07/Oct/13 560 580 Add

01/Aug/13 469 500 Add

29/Apr/13 341 383 Add

05/Feb/13 341 355 Reduce

19/Oct/12 299 310 Reduce

26/Jul/12 257 255 Reduce

11/Jun/12 248 253 Reduce

19/Apr/12 252 253 Reduce

16/Mar/12 254 225 Reduce

02/Mar/12 243 225 Reduce

IT Sector Update Sector Outlook

Neutral Disclaimer

Page 17

0

50

100

150

200

250

300

350

1-May-12 1-Nov-12 1-May-13 1-Nov-13 1-May-14 1-Nov-14 1-May-15

Historical Target

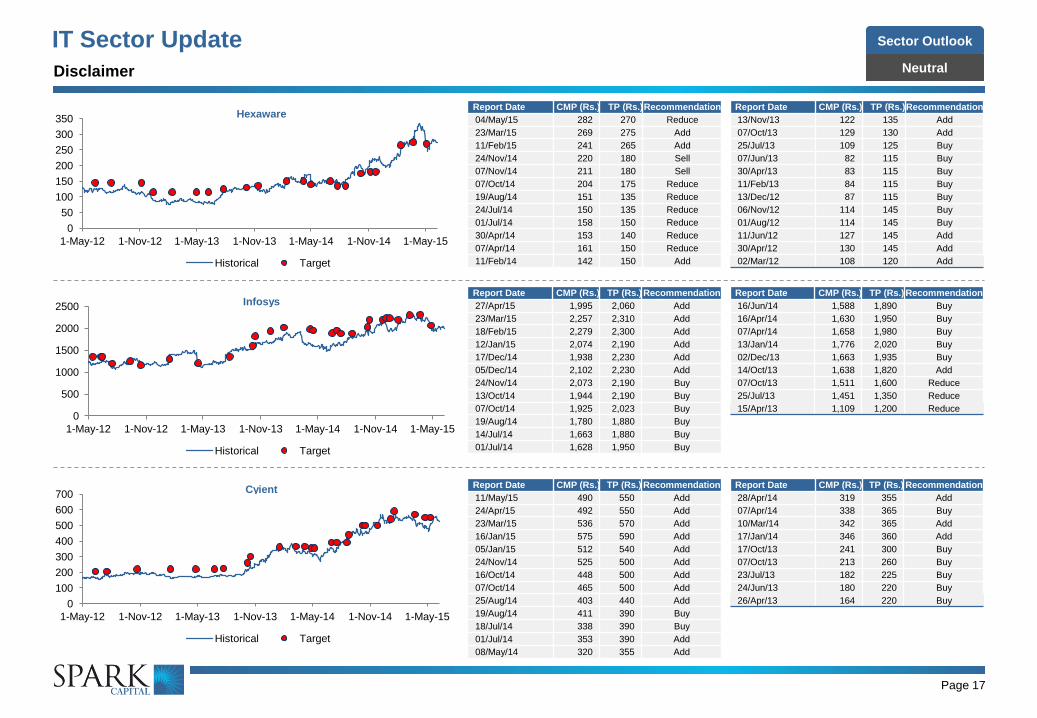

Hexaware Report Date CMP (Rs.) TP (Rs.) Recommendation

04/May/15 282 270 Reduce

23/Mar/15 269 275 Add

11/Feb/15 241 265 Add

24/Nov/14 220 180 Sell

07/Nov/14 211 180 Sell

07/Oct/14 204 175 Reduce

19/Aug/14 151 135 Reduce

24/Jul/14 150 135 Reduce

01/Jul/14 158 150 Reduce

30/Apr/14 153 140 Reduce

07/Apr/14 161 150 Reduce

11/Feb/14 142 150 Add

Report Date CMP (Rs.) TP (Rs.) Recommendation

13/Nov/13 122 135 Add

07/Oct/13 129 130 Add

25/Jul/13 109 125 Buy

07/Jun/13 82 115 Buy

30/Apr/13 83 115 Buy

11/Feb/13 84 115 Buy

13/Dec/12 87 115 Buy

06/Nov/12 114 145 Buy

01/Aug/12 114 145 Buy

11/Jun/12 127 145 Add

30/Apr/12 130 145 Add

02/Mar/12 108 120 Add

0

500

1000

1500

2000

2500

1-May-12 1-Nov-12 1-May-13 1-Nov-13 1-May-14 1-Nov-14 1-May-15

Historical Target

Infosys

0

100

200

300

400

500

600

700

1-May-12 1-Nov-12 1-May-13 1-Nov-13 1-May-14 1-Nov-14 1-May-15

Historical Target

Cyient

Report Date CMP (Rs.) TP (Rs.) Recommendation

27/Apr/15 1,995 2,060 Add

23/Mar/15 2,257 2,310 Add

18/Feb/15 2,279 2,300 Add

12/Jan/15 2,074 2,190 Add

17/Dec/14 1,938 2,230 Add

05/Dec/14 2,102 2,230 Add

24/Nov/14 2,073 2,190 Buy

13/Oct/14 1,944 2,190 Buy

07/Oct/14 1,925 2,023 Buy

19/Aug/14 1,780 1,880 Buy

14/Jul/14 1,663 1,880 Buy

01/Jul/14 1,628 1,950 Buy

Report Date CMP (Rs.) TP (Rs.) Recommendation

16/Jun/14 1,588 1,890 Buy

16/Apr/14 1,630 1,950 Buy

07/Apr/14 1,658 1,980 Buy

13/Jan/14 1,776 2,020 Buy

02/Dec/13 1,663 1,935 Buy

14/Oct/13 1,638 1,820 Add

07/Oct/13 1,511 1,600 Reduce

25/Jul/13 1,451 1,350 Reduce

15/Apr/13 1,109 1,200 Reduce

Report Date CMP (Rs.) TP (Rs.) Recommendation

11/May/15 490 550 Add

24/Apr/15 492 550 Add

23/Mar/15 536 570 Add

16/Jan/15 575 590 Add

05/Jan/15 512 540 Add

24/Nov/14 525 500 Add

16/Oct/14 448 500 Add

07/Oct/14 465 500 Add

25/Aug/14 403 440 Add

19/Aug/14 411 390 Buy

18/Jul/14 338 390 Buy

01/Jul/14 353 390 Add

08/May/14 320 355 Add

Report Date CMP (Rs.) TP (Rs.) Recommendation

28/Apr/14 319 355 Add

07/Apr/14 338 365 Buy

10/Mar/14 342 365 Add

17/Jan/14 346 360 Add

17/Oct/13 241 300 Buy

07/Oct/13 213 260 Buy

23/Jul/13 182 225 Buy

24/Jun/13 180 220 Buy

26/Apr/13 164 220 Buy

IT Sector Update Sector Outlook

Neutral Disclaimer

Page 18

0

50

100

150

200

1-May-12 1-Nov-12 1-May-13 1-Nov-13 1-May-14 1-Nov-14 1-May-15

Historical Target

Intellect Design Arena

0

500

1000

1500

2000

1-May-12 1-Nov-12 1-May-13 1-Nov-13 1-May-14 1-Nov-14 1-May-15

Historical Target

Mindtree

Report Date CMP (Rs.) TP (Rs.) Recommendation

28/Apr/15 110 140 Buy

23/Mar/15 116 145 Buy

02/Feb/15 105 140 Buy

20/Nov/14 76 100 Buy

Report Date CMP (Rs.) TP (Rs.) Recommendation

17/Apr/15 1,380 910 Sell

23/Mar/15 1,402 1,000 Sell

09/Mar/15 1,475 1,040 Sell

20/Jan/15 1,418 1,090 Sell

24/Nov/14 1,212 910 Sell

16/Oct/14 1,035 910 Sell

07/Oct/14 1,141 890 Sell

19/Aug/14 1,029 720 Sell

18/Jul/14 875 720 Sell

01/Jul/14 881 680 Sell

10/Jun/14 791 620 Sell

21/Apr/14 703 620 Sell

Report Date CMP (Rs.) TP (Rs.) Recommendation

07/Apr/14 710 640 Sell

17/Jan/14 740 650 Reduce

17/Oct/13 690 635 Reduce

07/Oct/13 615 625 Reduce

27/Sep/13 600 625 Reduce

23/Jul/13 473 510 Add

23/Apr/13 425 465 Add

0

100

200

300

400

500

600

1-May-12 1-Nov-12 1-May-13 1-Nov-13 1-May-14 1-Nov-14 1-May-15

Historical Target

MphasiS Report Date CMP (Rs.) TP (Rs.) Recommendation

26/May/15 379 350 Reduce

23/Mar/15 387 340 Sell

16/Feb/15 358 350 Reduce

24/Nov/14 408 350 Sell

31/Oct/14 408 350 Sell

07/Oct/14 422 395 Sell

19/Aug/14 435 350 Sell

04/Aug/14 443 350 Sell

01/Jul/14 426 360 Reduce

19/May/14 385 365 Reduce

07/Apr/14 411 360 Sell

19/Mar/14 404 380 Reduce

Report Date CMP (Rs.) TP (Rs.) Recommendation

07/Oct/13 439 430 Sell

10/Sep/13 423 400 Reduce

30/May/13 489 410 Sell

IT Sector Update Sector Outlook

Neutral Disclaimer

Page 19

0

200

400

600

800

1000

1-May-12 1-Nov-12 1-May-13 1-Nov-13 1-May-14 1-Nov-14 1-May-15

Historical Target

Persistent

0

100

200

300

400

500

600

1-May-12 1-Nov-12 1-May-13 1-Nov-13 1-May-14 1-Nov-14 1-May-15

Historical Target

NIIT Technologis

0

50

100

150

200

250

1-May-12 1-Nov-12 1-May-13 1-Nov-13 1-May-14 1-Nov-14 1-May-15

Historical Target

KPIT

Report Date CMP (Rs.) TP (Rs.) Recommendation

23/Apr/15 710 560 Sell

23/Mar/15 737 640 Sell

28/Jan/15 900 650 Sell

24/Nov/14 643 545 Sell

21/Oct/14 634 545 Sell

07/Oct/14 745 600 Sell

19/Aug/14 610 455 Sell

31/Jul/14 625 455 Sell

01/Jul/14 541 485 Sell

22/Apr/14 526 440 Sell

07/Apr/14 543 430 Sell

28/Jan/14 495 430 Sell

Report Date CMP (Rs.) TP (Rs.) Recommendation

02/Dec/13 435 430 Reduce

22/Oct/13 371 400 Add

07/Oct/13 345 315 Add

17/Sep/13 288 315 Add

01/Aug/13 262 288 Add

Report Date CMP (Rs.) TP (Rs.) Recommendation

06/May/15 395 370 Reduce

23/Mar/15 375 390 Reduce

15/Jan/15 384 400 Reduce

24/Nov/14 379 410 Reduce

16/Oct/14 394 410 Reduce

07/Oct/14 412 460 Reduce

19/Aug/14 370 390 Reduce

15/Jul/14 408 390 Reduce

01/Jul/14 443 520 Buy

Report Date CMP (Rs.) TP (Rs.) Recommendation

30/Apr/15 124 125 Reduce

23/Mar/15 191 190 Reduce

23/Jan/15 212 200 Reduce

24/Nov/14 171 160 Reduce

27/Oct/14 168 160 Reduce

07/Oct/14 162 180 Reduce

19/Aug/14 153 155 Reduce

24/Jul/14 155 155 Reduce

01/Jul/14 172 170 Reduce

IT Sector Update Sector Outlook

Neutral Disclaimer

Page 20

0

500

1000

1500

2000

2500

3000

1-May-12 1-Nov-12 1-May-13 1-Nov-13 1-May-14 1-Nov-14 1-May-15

Historical Target

TCS

0

200

400

600

800

1-May-12 1-Nov-12 1-May-13 1-Nov-13 1-May-14 1-Nov-14 1-May-15

Historical Target

Tech mahindra

0

200

400

600

800

1-May-12 1-Nov-12 1-May-13 1-Nov-13 1-May-14 1-Nov-14 1-May-15

Historical Target

Wipro

Report Date CMP (Rs.) TP (Rs.) Recommendation

17/Apr/15 2,574 2,620 Add

23/Mar/15 2,611 2,670 Add

09/Mar/15 2,696 2,780 Add

16/Jan/15 2,539 2,790 Add

17/Dec/14 2,499 2,760 Add

15/Dec/14 2,450 2,760 Add

24/Nov/14 2,615 2,680 Add

17-0ct-14 2,678 2,680 Buy

07/Oct/14 2,775 2,750 Add

09/Sep/14 2,643 2,740 Add

19/Aug/14 2,488 2,580 Add

18/Jul/14 2,380 2,580 Add

Report Date CMP (Rs.) TP (Rs.) Recommendation

01/Jul/14 2,425 2,430 Add

16/Jun/14 2,213 2,400 Add

22/Apr/14 2,220 2,430 Add

17/Apr/14 2,196 2,420 Add

07/Apr/14 2,136 2,420 Add

17/Jan/14 2,350 2,460 Add

02/Dec/13 1,985 2,280 Buy

17/Oct/13 2,215 2,330 Add

07/Oct/13 2,090 2,160 Add

25/Jul/13 1,783 1,890 Add

18/Apr/13 1,455 1,610 Add

Report Date CMP (Rs.) TP (Rs.) Recommendation

27/May/15 636 670 Add

23/Mar/15 678 690 Add

03/Feb/15 724 753 Add

07/Jan/15 635 735 Buy

17/Dec/14 670 688 Add

24/Nov/14 654 710 Add

21/Nov/14 675 710 Add

30/Oct/14 599 650 Add

07/Oct/14 630 680 Add

19/Aug/14 551 575 Add

04/Aug/14 532 575 Add

01/Jul/14 538 568 Buy

Report Date CMP (Rs.) TP (Rs.) Recommendation

15/May/14 460 528 Buy

07/Apr/14 453 566 Buy

05/Feb/14 443 508 Buy

02/Dec/13 423 463 Buy

08/Nov/13 394 450 Buy

07/Oct/13 361 408 Buy

12/Sep/13 333 395 Buy

20/Aug/13 313 363 Buy

04/Jul/13 250 293 Buy

11/Jun/13 242 293 Buy

Report Date CMP (Rs.) TP (Rs.) Recommendation

22/Apr/15 588 620 Add

23/Mar/15 653 670 Add

12/Mar/15 655 700 Add

19/Jan/15 556 660 Buy

17/Dec/14 535 685 Buy

24/Nov/14 570 660 Buy

27/Oct/14 560 660 Buy

07/Oct/14 615 660 Buy

16/Sep/14 568 660 Buy

19/Aug/14 548 590 Add

28/Jul/14 550 590 Add

01/Jul/14 546 580 Add

16/Jun/14 530 580 Add

Report Date CMP (Rs.) TP (Rs.) Recommendation

21/Apr/14 554 580 Reduce

07/Apr/14 553 580 Reduce

20/Jan/14 553 520 Reduce

02/Dec/13 473 470 Reduce

23/Oct/13 515 460 Sell

07/Oct/13 482 460 Reduce

01/Aug/13 438 410 Reduce

IT Sector Update Sector Outlook

Neutral

Spark Disclaimer

Spark Capital Advisors (India) Private Limited (Spark Capital) and its affiliates are engaged in investment banking, investment advisory and institutional equities and

infrastructure advisory services. Spark Capital is registered with SEBI as a Stock Broker and Category 1 Merchant Banker.

We hereby declare that our activities were neither suspended nor we have defaulted with any stock exchange authority with whom we are registered in the last five years. We

have not been debarred from doing business by any Stock Exchange/SEBI or any other authorities, nor has our certificate of registration been cancelled by SEBI at any point of

time.

Spark Capital has a subsidiary Spark Investment Advisors (India) Private Limited which is engaged in the services of providing investment advisory services and is registered

with SEBI as Investment Advisor. Spark Capital has also an associate company Spark Infra Advisors (India) Private Limited which is engaged in providing infrastructure

advisory services.

This document does not constitute or form part of any offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Nothing in this document should

be construed as investment or financial advice, and nothing in this document should be construed as an advice to buy or sell or solicitation to buy or sell the securities of

companies referred to in this document.

Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies

referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. This

document is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published,

copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to or use by any person or entity who is a citizen or resident of or located in

any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Spark Capital

and/or its affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to

a certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such applicable restrictions. This

material should not be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

Spark Capital makes no representation or warranty, express or implied, as to the accuracy, completeness or fairness of the information and opinions contained in this

document. Spark Capital , its affiliates, and the employees of Spark Capital and its affiliates may, from time to time, effect or have effected an own account transaction in, or

deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit

investment banking or other business from, any company referred to in this report.

This report has been prepared on the basis of information, which is already available in publicly accessible media or developed through an independent analysis by Spark

Capital. While we would endeavour to update the information herein on a reasonable basis, Spark Capital and its affiliates are under no obligation to update the information.

Also, there may be regulatory, compliance or other reasons that prevent Spark Capital and its affiliates from doing so. Neither Spark Capital nor its affiliates or their respective

directors, employees, agents or representatives shall be responsible or liable in any manner, directly or indirectly, for views or opinions expressed in this report or the contents

or any errors or discrepancies herein or for any decisions or actions taken in reliance on the report or the inability to use or access our service in this report or for any loss or

damages whether direct or indirect, incidental, special or consequential including without limitation loss of revenue or profits that may arise from or in connection with the use of

or reliance on this report.

Absolute

Rating

Interpretation

BUY Stock expected to provide positive returns of >15% over a 1-year horizon REDUCE Stock expected to provide returns of <5% – -10% over a 1-year

horizon

ADD Stock expected to provide positive returns of >5% – <15% over a 1-year

horizon SELL Stock expected to fall >10% over a 1-year horizon

Disclaimer

Page 21

IT Sector Update Sector Outlook

Neutral Disclaimer (Cont’d)

Spark Capital and/or its affiliates and/or employees may have interests/positions, financial or otherwise in the securities mentioned in this report. To enhance transparency,

Spark Capital has incorporated a disclosure of interest statement in this document. This should however not be treated as endorsement of views expressed in this report:

Disclosure of interest statement ECLX, FSOL HCLT, HEXW, CYL, INDA, MTCL,

MPHL, PSYS, NITEC, KPIT, TECHM, WPRO TCS, INFO

Analyst financial interest in the company No No

Group/directors ownership of the subject company covered No No

Investment banking relationship with the company covered No No

Spark Capital’s ownership/any other financial interest in the company covered No Yes

Associates of Spark Capital’s ownership more than 1% in the company covered No No

Any other material conflict of interest at the time of publishing the research report No No

Receipt of compensation by Spark Capital or its Associate Companies from the subject company covered for in

the last twelve months:

Managing/co-managing public offering of securities

Investment banking/merchant banking/brokerage services

products or services other than those above

in connection with research report

No

No

Whether Research Analyst has served as an officer, director or employee of the subject company covered No No

Whether the Research Analyst or Research Entity has been engaged in market making activity of the Subject

Company; No No

Analyst Certification of Independence

The views expressed in this research report accurately reflect the analyst’s personal views about any and all of the subject securities or issuers; and no part of the research

analyst’s compensations was, is or will be, directly or indirectly, related to the specific recommendation or views expressed in the report.

Additional Disclaimer for US Institutional Investors

This research report prepared by Spark Capital Advisors (India) Private Limited is distributed in the United States to US Institutional Investors (as defined in Rule 15a-6 under

the Securities Exchange Act of 1934, as amended) only by Decker and Co, LLC, a broker-dealer registered in the US (registered under Section 15 of Securities Exchange Act

of 1934, as amended). Decker and Co accepts responsibility on the research reports and US Institutional Investors wishing to effect transaction in the securities discussed in

the research material may do so through Decker and Co. All responsibility for the distribution of this report by Decker and Co, LLC in the US shall be borne by Decker and Co,

LLC. All resulting transactions by a US person or entity should be effected through a registered broker-dealer in the US. This report is not directed at you if Spark Capital

Advisors (India) Private Limited or Decker and Co, LLC is prohibited or restricted by any legislation or regulation in any jurisdiction from making it available to you. You should

satisfy yourself before reading it that Decker and Co, LLC and Spark Capital Advisors (India) Private Limited are permitted to provide research material concerning investment

to you under relevant legislation and regulations;

Page 22