islamic (non-interest) banking and finance -oyindamola …

TRANSCRIPT

ISLAMIC (NON-INTEREST) BANKING AND

FINANCE

- Oyindamola Dada

ESSENTIAL ELEMENTS OF ISLAMIC FINANCE

VALID (SAHIH)

IRREGULAR (FASID)

VOID (BATIL)CO

NT

RA

CT

3

ESSENTIAL ELEMENTS OF ISLAMIC FINANCE

Classification of Contracts According to their

Legal Validity:

1. Valid Contract: A contract which its nature/essence and attributes are in line with

Islamic Law. A valid contract enjoys the following features:I. Its elements are complete II. Conditions relating to elements are met, andIII. It is free from external prohibited elements

2. Irregular Contract: In this contract, elements are present, and all the essential

conditions are complete, however, an external attribute included in this contract is forbidden by the lawgiver.

The contract is legal in respect to its origin, but it is irregular due to the prohibition of the attribute.

ESSENTIAL ELEMENTS OF ISLAMIC FINANCE

ESSENTIAL ELEMENTS OF ISLAMIC FINANCE

3. Void Contract:

A void contract is against Islamic Law in respect to both its essence and external attributes. It does not give any effect.

No ownership is transferred nor is any type of obligation created.

There is no room for ratification.

•Contracting Parties: Buyer and Seller

• Discernment – excludes the insane, the intoxicated, and the minor without intellect;

• Legal capacity – excludes the imbecile and a person placed under guardianship;

• Ownership or representation of owner or authority over an owner or his deputy;

• Assent (negated by compulsion, ignorance, error, deception, concealment of defect, jest): “O you who believe! Do not devour the wealth of one another unjustly, except if it is from a trading based on consent from yourselves” [Qur’an 4 : 29].

•Subject Matter: Al Thaman (Consideration) and Al Muthman (Object of sale)

• Existence – Give exception to Salam and Istisna’

• Permissibility – of possession and having a utility permissible for exchange (excluded are impure items, like alcohol and pork, items with no utility like insects or those with impermissible utility like musical instruments or with utility that is impermissible for exchange like dogs)

• Known to the contracting parties

• Ability and certainty of delivery

•Offer and Acceptance:

• Clear statements denoting mutual consent by custom;

• Continuity (negated by revocation, rejection, lapse of time or separation)

• Communication

ESSENTIAL ELEMENTS OF ISLAMIC FINANCE

Element of a Sale Contract:

1) Transfer of the Subject Matters of the Contract• It is binding on the buyer to effect the transfer of the price, and

in the event of dispute, he is the party to be compelled to effect the transfer first.

• The seller is entitled to keep hold of the sold item till he receives the price.

• Expenses of delivery of price is on the buyer and of the sold item is on the seller, except if there is a custom or stipulation to the contrary.

• It is not permissible to sell an identified item on a delayed delivery basis.

ESSENTIAL ELEMENTS OF ISLAMIC FINANCE

Effects of the Sale Contract:

2) Taking of Possession: It is the appropriation of an item and having the right of administration and disposal over it and the removal of all restrictions over it, real or customary;

• The basis for determining mode of taking of possession is al ‘urf (custom)

• There is actual possession by relinquishing of immovables, and physical and corporeal delivery in movables; and constructive possession depending on the item and the contract. Valid registration and possession of documents like bills of lading and warehouse receipts

• Constructive possession includes:

I. Crediting money to an account directly or through bank transfer;

II. Depositing money to an account upon the demand of the one taking possession or with his consent;

III. Receipt of a bank cheque or bank draft;

IV. Payments of a credit card and receipt of a voucher by a merchant signed by the credit card holder.

• Prior possession of a tangible item stands in place of subsequent possession irrespective of the earlier possession being of liability or of trust.

ESSENTIAL ELEMENTS OF ISLAMIC FINANCE

Effects of the Sale Contract:

3) Transfer of Responsibility and Liability over the sold item• Bearing the responsibility over loss, deficiency or damage in a contract that is

subject of sale or lease.

• After taking of possession, responsibility is on the buyer except in the case of sale of crops that become affected by crop damage or crop failure;

• Responsibility is transferred to the buyer with the conclusion of the sale contract, even before taking of possession, except in five cases:

1. Sale of an item that is not there based on description;

2. Sale of an item in a sale contract that has an option condition;

3. Sale of fruits before complete ripeness;

4. Sale of an item that is sold based on volume, weight or number

5. Sale of an item in an invalid sale contract

In all the 5 cases, responsibility is on the seller until the buyer takes possession.

ESSENTIAL ELEMENTS OF ISLAMIC FINANCE

Effects of the Sale Contract:

4) Disposal of the Sold Item by Sale Before Taking of Possession

• It is not permissible if the sold item is foodstuff that is sold by measure only.

5) Disposal of the Sold Item by Other than Sale Before Taking of Possession

• It is permissible to dispose a sold item before taking possession even if it is foodstuff that is sold by measure, if the disposal in not through an exchange contract, which includes: gift, charity, loan, partnership or sale at cost price.

ESSENTIAL ELEMENTS OF ISLAMIC FINANCE

Effects of the Sale Contract:

Questions ?

TRADE BASED CONTRACTS

• MURABAHA

• BAI’-MUAJJAL

• SALAM

• ISTISNA’

LEASE BASED CONTRACTS

IJARAH

IJARAH OF SERVICES

EQUITY (PARTNERSHIP) BASEDCONTRACTS

MUSHARAKAH

MUDARABAH

FEE BASED CONTRACTS

WAKALAH

KAFALAH

OTHER CONTRACTS

QARD HASSAN (BENEVOLENT LOAN)

13

ISLAMIC FINANCE CONTRACTS

MURABAHA (COST PLUS FINANCING)

THE ORIGIN OF MURABAHA IS THE WORD

‘RABAHA’ (I.E. TO MAKE A PROFIT (FROM A DEAL).

IT IS ONE OF THE TRUST SALES CONTRACTS,

WHICH REQUIRES A SELLER TO FULLY DISCLOSE

THE COST PRICE OF A GOOD OR ASSET AND HIS

PROFIT MARGIN, WHICH COULD BE A LUMP SUM

OR A PERCENTAGE OF THE COST PRICE.

A MURABAHA IS A SALE IN WHICH THE SELLER’S

COST OF ACQUIRING THE ASSET AND THE PROfiT

EARNED FROM IT ARE DISCLOSED TO THE

CLIENT OR BUYER.

THE MURABAHA OPERATED BY NIFIS IS

REFERRED TO AS MURABAHA TO PURCHASE

ISLAMIC FINANCE CONTRACTS

MURABAHA …..CONT’D

August 23, 2021 ©2019 Your Company. All Rights Reserved

15

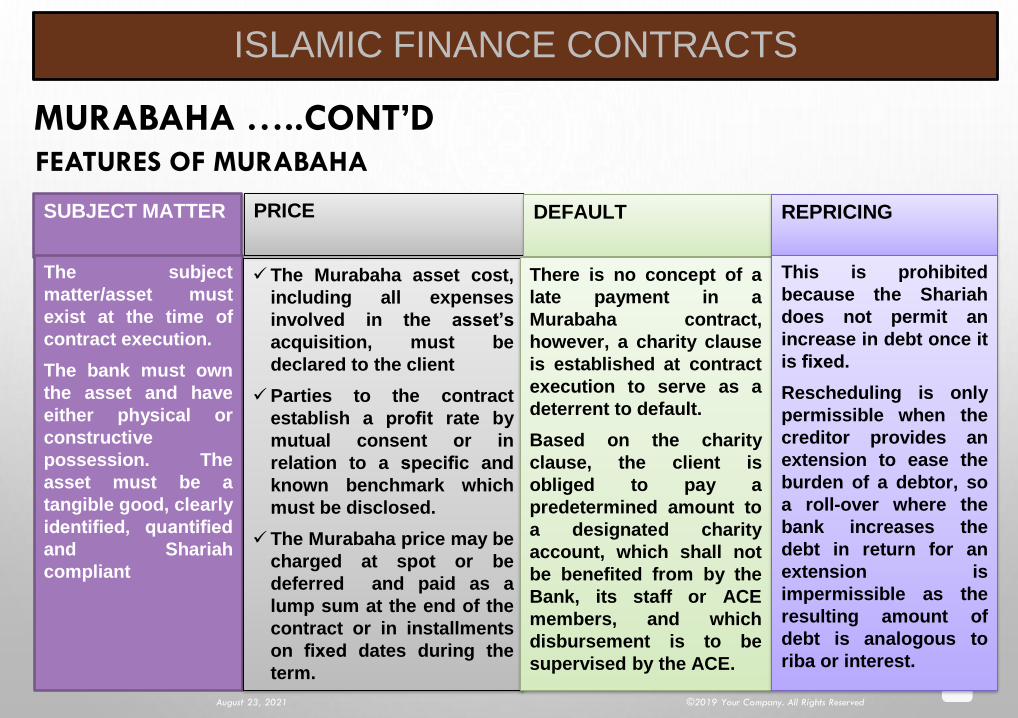

FEATURES OF MURABAHA

ISLAMIC FINANCE CONTRACTS

SUBJECT MATTER

The subject

matter/asset must

exist at the time of

contract execution.

The bank must own

the asset and have

either physical or

constructive

possession. The

asset must be a

tangible good, clearly

identified, quantified

and Shariah

compliant

The Murabaha asset cost,

including all expenses

involved in the asset’s

acquisition, must be

declared to the client

Parties to the contract

establish a profit rate by

mutual consent or in

relation to a specific and

known benchmark which

must be disclosed.

The Murabaha price may be

charged at spot or be

deferred and paid as a

lump sum at the end of the

contract or in installments

on fixed dates during the

term.

PRICE DEFAULT REPRICING

There is no concept of a

late payment in a

Murabaha contract,

however, a charity clause

is established at contract

execution to serve as a

deterrent to default.

Based on the charity

clause, the client is

obliged to pay a

predetermined amount to

a designated charity

account, which shall not

be benefited from by the

Bank, its staff or ACE

members, and which

disbursement is to be

supervised by the ACE.

This is prohibited

because the Shariah

does not permit an

increase in debt once it

is fixed.

Rescheduling is only

permissible when the

creditor provides an

extension to ease the

burden of a debtor, so

a roll-over where the

bank increases the

debt in return for an

extension is

impermissible as the

resulting amount of

debt is analogous to

riba or interest.

MURABAHA……CONT’D

STEPS OF MURABAHA EXECUTION

August 23, 2021 ©2019 Your Company. All Rights Reserved

16

ISLAMIC FINANCE CONTRACTS

PRU (Purchase Requisition Undertaking)

The client’s

submission of

a purchase

requisition for

Murabaha

goods.

EARNEST MONEY

The client’s unilateral

promise to purchase the

Murabaha goods and the

financial institution’s

acceptance of collateral.

The Bank requests the

client to furnish a security

or earnest money called

Haamish Jiddiyyah. In

case the client backs out

from entering into a

Murabaha, the bank

makes up for the actual

loss from it and returns the

remainder to the client.

AGENCY

The agency agreement

between the financial institution

and the client or a third party.

During the Agency stage the

bank’s exposure to asset risk.

The Bank must also ensure

that the asset to be purchased

is not already in the client’s

possession by paying to the

supplier before the

agent/customer purchases the

goods. The Bank can equally

procure Murabaha goods

directly or establish a third

party agency.

POSSESSION

The

possession of

the Murabaha

goods by the

agent on

behalf of the

financial

institution

ACTUAL SALE

The exchange

of an offer and

acceptance

between the

client and the

financial

institution to

implement the

Murabaha sale.

BAI’ MUAJJAL (DEFERRED/CREDIT SALE)

ISLAMIC FINANCE CONTRACTS

Bai’ Muajjal is a contract between a

Buyer and a Seller for the sale of a

specific asset to the Buyer at an

agreed fixed price payable at a fixed

future date in lump sum or by fixed

instalments.

As a Sale contract, the buyer must

have ownership of the asset before

the sale of same. The ownership may

be actual or constructive

DIFFERENCES BETWEEN MURABAHA AND BAI’-MUAJJAL

ISLAMIC FINANCE CONTRACTS

MURABAHAH BAI’ MUAJJAL

1. Sale on an agreed mark-up which

may be at the spot or deferred

Sale on credit or deferred payment basis

2. Key objective of a Murabahah is to

make profit, the profit mark-up is thus

an essential part of the contract

The key objective of a Bai’ Muajjal is

deferred payment of a sale which may be

at discount, par, or premium of the cost

price of the asset.

3. As one of the Trust Sale contracts,

the actual purchase price of the asset

and the mark-up must be

transparently disclosed in the contract

document

The Vendor/Seller is not bound to disclose

the actual purchase price to the customer

orally or in the contract documents.

4. Murabahah purchase may be effected

either in cash or on credit

Bai’ Muajjal sale must always be on credit.

Payment is deferred.

ISLAMIC FINANCE CONTRACTS

i. Ribawi items (are six items associated to interest) against same

except while fulfilling the required rules of same quantity and on

the spot and if different any quantity but also on the spot as

guided by the Prophet (peace be upon him).

ii. Non-existent items except in Salam and Istisna.

iii. Items not owned by the seller.

iv. Items already owned by the buyer (buy back).

v. Items that could not be delivered by the seller.

vi. Injurious assets that are harmful to either individual or society.

vii. Items prohibited by Shari’ah such as alcohol, pork meat and pork

accessories, dead animals, blood, phonographic films, etc.

viii. Stolen items if the seller is aware.

ITEMS THAT CANNOT BE FINANCED IN SALE CONTRACTS

ISLAMIC FINANCE CONTRACTS

Ribawi items or similar against one another.

Gold-Silver

Gold –Naira ALL MUST BE ON THE SPOT

Naira – USD

USD – Gold

Transactions where both subject and payment are

deferred.

ITEMS THAT CANNOT BE SOLD ON DEFERRED PAYMENT

ISLAMIC FINANCE CONTRACTS

Vehicles

Household appliances

Undeveloped plot of land

Automobiles

Computers and accessories

Electronics

Furniture

Agricultural equipment

Imports Finance

Any other goods that can be easily delivered

AREAS OF FINANCING USING MURABAHA/BAI’ MUAJJAL

ISLAMIC FINANCE CONTRACTS

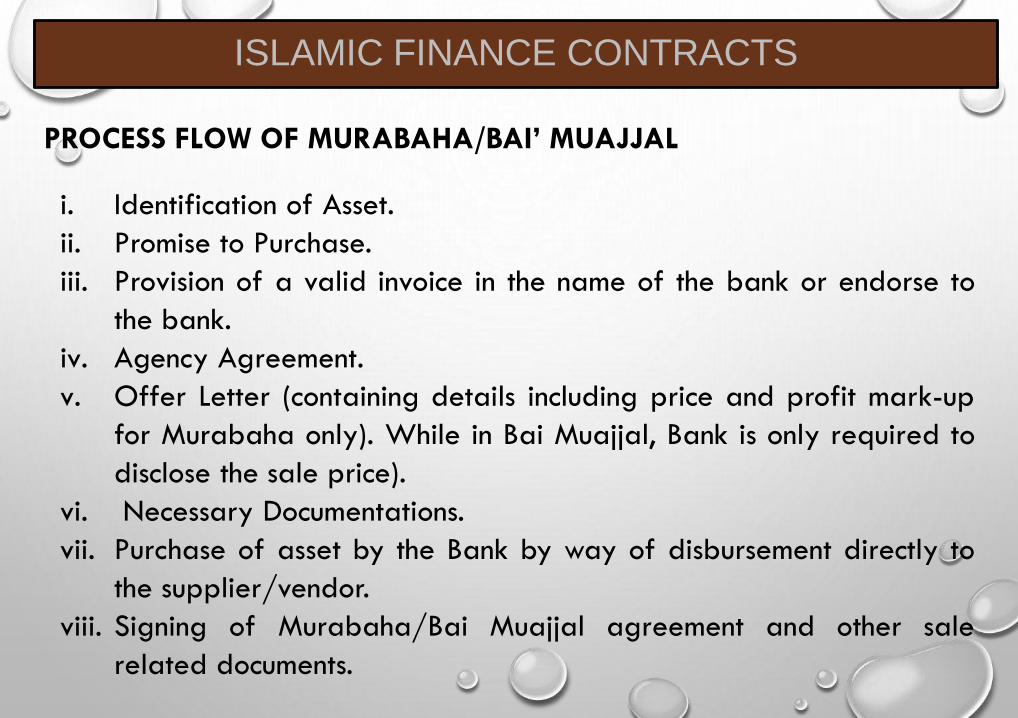

i. Identification of Asset.

ii. Promise to Purchase.

iii. Provision of a valid invoice in the name of the bank or endorse to

the bank.

iv. Agency Agreement.

v. Offer Letter (containing details including price and profit mark-up

for Murabaha only). While in Bai Muajjal, Bank is only required to

disclose the sale price).

vi. Necessary Documentations.

vii. Purchase of asset by the Bank by way of disbursement directly to

the supplier/vendor.

viii. Signing of Murabaha/Bai Muajjal agreement and other sale

related documents.

PROCESS FLOW OF MURABAHA/BAI’ MUAJJAL

SALAM (FORWARD SALE)

ISLAMIC FINANCE CONTRACTS

Salam is one of the exceptions to

the general rule of sale, i.e.

tangibility, availability and

ownership of the asset to be sold.

Salam is a sale where the price

of the subject matter is paid in full

at the time of the contract’s

execution while the delivery of

the subject matter is deferred to a

future date.

SALAM (FORWARD SALE)…..CONT’D

ISLAMIC FINANCE CONTRACTS

It is not necessary that the subject

matter exist, and be owned and

possessed by the seller at the time of

the Salam’s execution as is the

customary requirement of a standard

sale, provided it meets the other criteria

specific to it.

Salam allows the buyer to purchase

commodities for a price lower than the

spot market price, while providing

capital for the vendor at the point when

he needs it most, thus creating a win-

win situation. The vendor wins and the

purchaser wins.

FEATURES OF SALAM (FORWARD SALE)

ISLAMIC FINANCE CONTRACTS

HOMOGENEITY

Salam may be

executed for

homogeneous

commodities but

not for specific

commodities and

mediums of

exchange

The quantity and quality

of Salam goods must be

specified in order to

avoid any ambiguity that

may lead to dispute

between contracting

parties

NO AMBIGUITY PRICE DELIVERY

Salam price must be

paid at spot. The price

is fixed and cannot be

increased due to an

increase in the price of

Salam goods in the

market during the

contract’s term

The place of

delivery of Salam

goods must be

specified and they

must be delivered in

their entirety on a

fixed future date or

in instalments on

predetermined

dates

FEATURES OF SALAM (FORWARD SALE)….CONT’D

ISLAMIC FINANCE CONTRACTS

PARALLEL SALAM

Salam goods cannot be sold to a

third party before receiving

possession however a parallel Salam

may be executed for them. A Parallel

Salam is a transaction executed

simultaneously with the original

Salam. The buyer of goods in the

first Salam is the seller of goods in

the second or Parallel Salam. It is

permitted with a third party only.

The Khiyar al ‘Aib

(option of defect) may

be exercised for

Salam subject matter,

however, not the

Khiyar al Rooyat

(option of refusal).

OPTIONS SALAM TERMINATION

Once executed, a Salam may

not be revoked unilaterally by

either party. It is a sale

contract binding on both

parties and may be

terminated completely or

partially by mutual consent

by returning the actual or

proportionate amount of the

price paid

ISLAMIC FINANCE CONTRACTS

AREAS OF FINANCING USING SALAM

Agricultural Financing such as fertilizer, seeds,

equipment, etc.

Working Capital Financing (for raw materials

requirement of companies).

PROCESS FLOW OF SALAM (FORWARD SALE)

ISLAMIC FINANCE CONTRACTS

Discussion/Request to the Bank

Application

Promise to sell

Items identified and description made

Bank enters into parallel Salam with a buyer

Offer Letter (with full details)

Necessary documentation

Sale/Buy agreement signed

Disbursement is made to customer

Described goods supplied to the Bank at harvest or on maturity

Facility terminated.

Bank deliver goods to the second buyer in parallel Salam.

ISLAMIC FINANCE CONTRACTS

PROCESS FLOW OF SALAM……CONT’D

ISTISNA’ (MANUFACTURING/CONSTRUCTION) FINANCING

ISLAMIC FINANCE CONTRACTS

Istisna, like Salam, is the second exception

to the general rule of sale.

An Istisna is a transaction used to acquire an

asset manufactured on order. It may be

executed directly with the supplier or any

other party that undertakes to have the asset

manufactured.

There are usually three parties involved in an

Istisna contract; the Istisna requestor, or

orderer, the manufacturer and the Bank.

An Istisna takes place when one party

agrees to manufacture a product for another

party at a specific price. This agreement

involves an exchange of an offer and an

acceptance which completes the contract.

FEATURES OF ISTISNA’

ISLAMIC FINANCE CONTRACTS

SUBJECT MATTER

The subject matter

of an Istisna need

not exist, be

owned or

possessed by the

manufacturer at

the time of

contract execution

It must be an item that

is manufactured as

customary market

practice and undergoes

processing to convert

from one form to

another

SUBJECT MATTER SUBJECT MATTER PRICE

The quantity or

quality of Istisna

subject matter can

be changed by

mutual consent of

the contracting

parties

The Istisna price, agreed

at the time of contracting

between the istisna

requestor and the

manufacturer, may be

paid at the time of

contract execution, in

fixed instalments over the

contract’s term or as a

lump sum at the end of

the contract’s term

FEATURES OF ISTISNA’

ISLAMIC FINANCE CONTRACTS

PARALLEL ISTISNA

A parallel Istisna is a

second Istisna

contract executed

alongside the first

Istisna. The

manufacturer in the

original contract

serves as the Istisna

requestor in the

parallel contract and

profits from a

difference in price.

The parallel Istisna is

completely separate

and independent of

the original Istisna

contract

The Islamic bank

may demand security

in its capacity as

requestor or

manufacturer. Such a

security is called

Urbun. Urbun is a

non-refundable down

payment that the

seller/manufacturer

receives from the

buyer/requestor, in

order to secure the

purchase of goods

URBUN NO BUY-BACK ISTISNA TERMINATION

The Istisna must

not involve a buy-

back at any stage.

Before the Istisna

is executed it is

important to

ensure that the

contracting parties

are separate and

independent legal

entities

Either of the two

contracting parties may

terminate the Istisna

unilaterally provided the

manufacturing process

has not commenced. If

manufacturing has

begun, then the contract

is binding on both parties

and can only be

terminated by mutual

consent

ISLAMIC FINANCE CONTRACTS

House Financing

Project Financing such as power, roads, water

treatment plants etc.

Manufacturing Companies

Financing of Raw Materials

Government Awarded Contracts

Any other Shariah compliant project.

AREAS OF FINANCING USING ISTISNA’

PROCESS FLOW OF ISTISNA’

ISLAMIC FINANCE CONTRACTS

ISLAMIC FINANCE CONTRACTS

Idea discussion/request

Promise to buy

Identification and description of asset to be manufactured.

Identification and engagement of contractor for second Istisna

Offer letter (including details of price, payment date and delivery)

Necessary documentation

Istisna Sale Agreement

Agreement with contractor (separate and independent from the Sale

agreement above)

Completion of the project

Delivery to the Bank and the Bank to the customer.

PROCESS FLOW OF ISTISNA’…….CONT’D

DIFFERENCES BETWEEN SALAM AND ISTISNA’

ISLAMIC FINANCE CONTRACTS

Salam Istisna

Subject Commodity Agricultural produce or existing

and off the shelf goods or assets

Items not in existence or not fully

developed or assembled to be fit

for purpose

Price Paid in full in advance Flexible; may be in advance, at

milestones or upon project delivery

Time of Delivery Must be fixed at the contracting

stage

May be reviewed, especially in the

case of project delivery

Cancellation of Contract Can not be unilaterally cancelled

once concluded

Can be cancelled unilaterally even

after concluding the contract, but

must be before manufacturer or

developer commence the project

IJARAH (LEASING)

IJARAH IS THE LEASE OF A

SPECIfiC ASSET OR SERVICE TO A

CLIENT FOR AN AGREED PERIOD

OF TIME IN EXCHANGE FOR RENT

WHICH AT THE END OF THE LEASE

PERIOD MAY RESULT IN

TRANSFERRING THE SUBJECT

MATTER’S OWNERSHIP TO THE

LESSEE. IN PRINCIPLE, AN IJARAH

CONTRACT IS EXECUTED FOR AN

ASSET OWNED BY THE LESSOR OR

AN USUFRUCT OWNED BY THE

SUB-LESSOR.

THE SUBJECT OF LEASE MUST

HAVE A VALUABLE USE, SO THINGS

HAVING NO USUFRUCT AT ALL

CANNOT BE LEASED.

ISLAMIC FINANCE CONTRACTS

IJARAH (LEASING)…..CONT’D

August 23, 2021

©2019 Your Company. All Rights Reserved

38

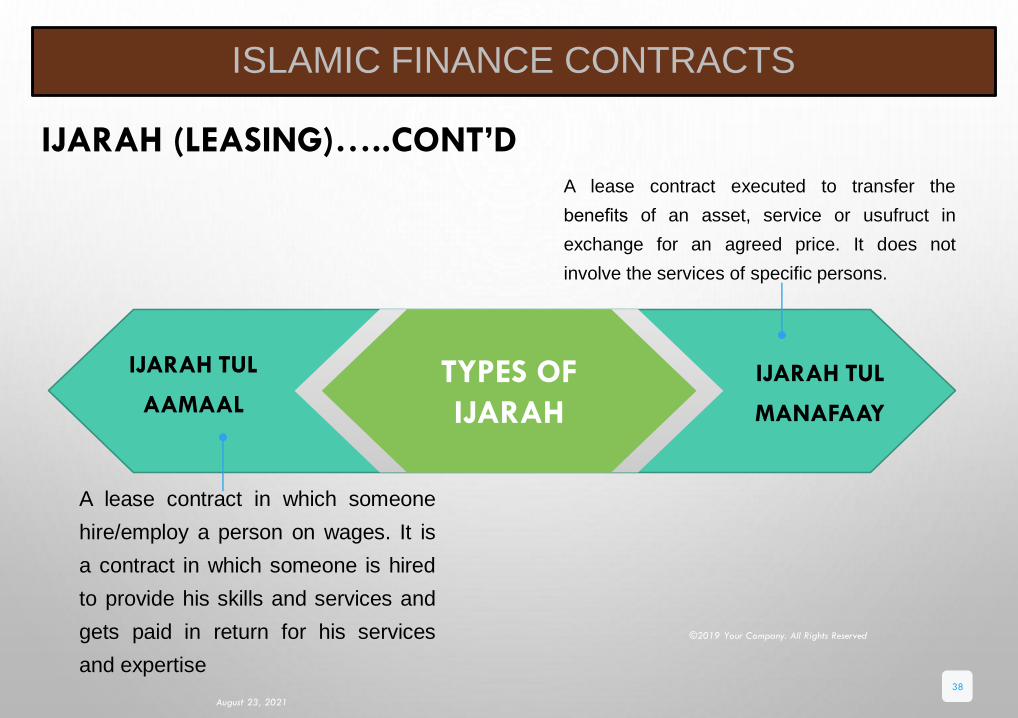

TYPES OF

IJARAH

A lease contract in which someone

hire/employ a person on wages. It is

a contract in which someone is hired

to provide his skills and services and

gets paid in return for his services

and expertise

IJARAH TUL

AAMAAL

IJARAH TUL

MANAFAAY

A lease contract executed to transfer the

benefits of an asset, service or usufruct in

exchange for an agreed price. It does not

involve the services of specific persons.

ISLAMIC FINANCE CONTRACTS

IJARAH (LEASING)……CONT’D

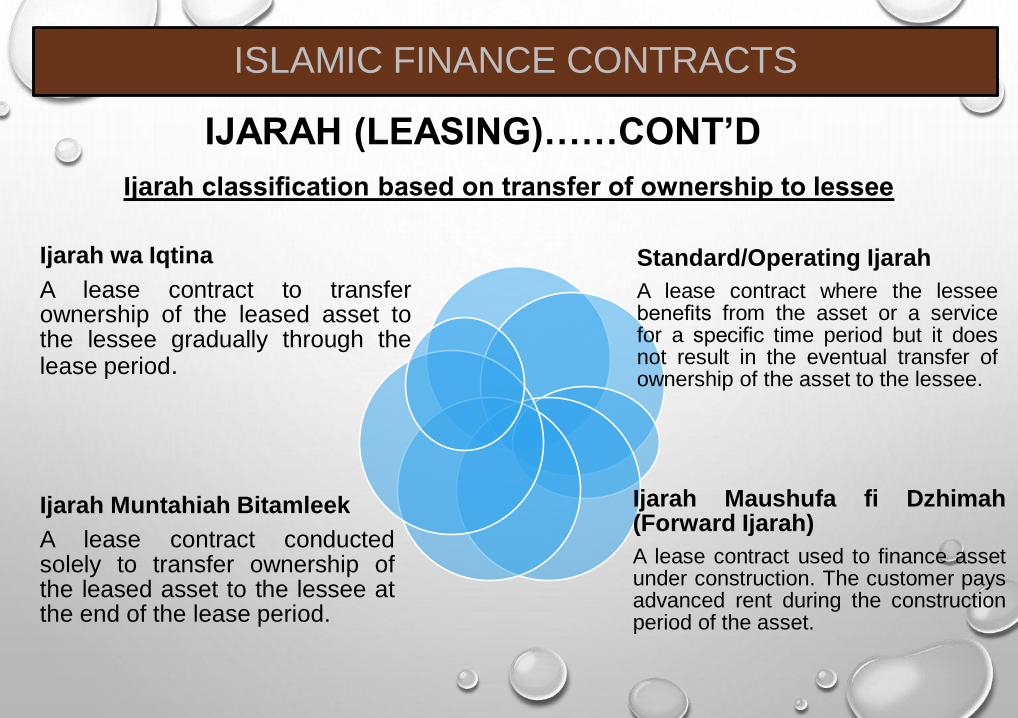

Ijarah classification based on transfer of ownership to lessee

Standard/Operating Ijarah

A lease contract where the lesseebenefits from the asset or a servicefor a specific time period but it doesnot result in the eventual transfer ofownership of the asset to the lessee.

Ijarah wa Iqtina

A lease contract to transferownership of the leased asset tothe lessee gradually through thelease period.

Ijarah Muntahiah Bitamleek

A lease contract conductedsolely to transfer ownership ofthe leased asset to the lessee atthe end of the lease period.

Ijarah Maushufa fi Dzhimah(Forward Ijarah)

A lease contract used to finance assetunder construction. The customer paysadvanced rent during the constructionperiod of the asset.

ISLAMIC FINANCE CONTRACTS

IJARAH (LEASING)….CONT’D

The client and lessor enter intoa promise to execute an Ijarahfor the usufruct of a particularasset or service

The bank undertakes to providethe asset or service and theclient undertakes to enter into alease contract for it

The asset or service must be ownedby the lessor and made availableto the lessee before the Ijarahcommences

The lease period commencesonce the subject matter of thelease is made available to thelessee.

Prerequisites of an Ijarah

ISLAMIC FINANCE CONTRACTS

PROCESS FLOW OF IJARAH

ISLAMIC FINANCE CONTRACTS

ISLAMIC FINANCE CONTRACTS

Idea discussion/Declaration of interest

Promise to rent and buy

Identification of asset

Offer Letter and Acceptance

Ijarah Wa Iqtina Agreement

Necessary documentations

Provision of equity contribution by customer

Purchase of asset by the bank

Signing of agreement (Lease and Sale).

PROCESS FLOW OF IJARAH……..CONT’D

IJARAH SERVICES

IJARAH SERVICES IS BASED

ON THE CONTRACT OF IJARAH

I.E. THE HIRE/ACQUISITION OF

SERVICES OF PERSONS IN

EXCHANGE FOR A FEE,

FINANCIAL OR MATERIAL

CONSIDERATION.

THE BANK ASSIGNS TO THE

CUSTOMER THE ENJOYMENT

OF THE ACQUIRED SERVICE AT

A MARKED-UP RATE, WHICH

THE CUSTOMER PAYS UP IN A

DEFERRED LUMP SUM OR ON

AGREED INSTALMENTS.

ISLAMIC FINANCE CONTRACTS

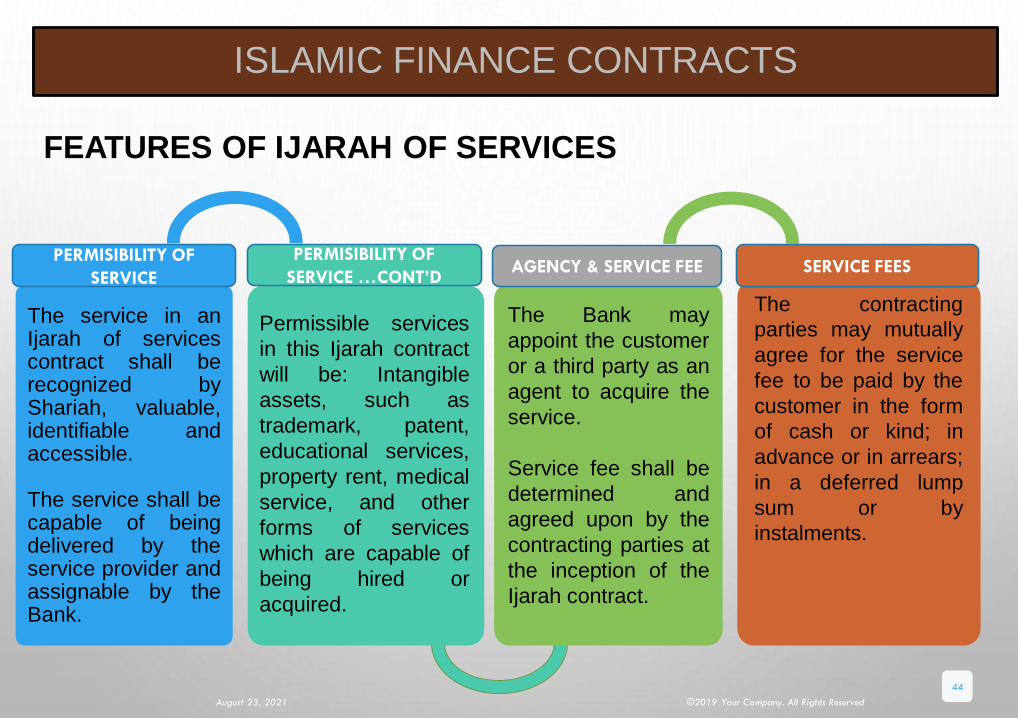

The service in anIjarah of servicescontract shall berecognized byShariah, valuable,identifiable andaccessible.

The service shall becapable of beingdelivered by theservice provider andassignable by theBank.

Permissible services

in this Ijarah contract

will be: Intangible

assets, such as

trademark, patent,

educational services,

property rent, medical

service, and other

forms of services

which are capable of

being hired or

acquired.

The Bank may

appoint the customer

or a third party as an

agent to acquire the

service.

Service fee shall be

determined and

agreed upon by the

contracting parties at

the inception of the

Ijarah contract.

The contracting

parties may mutually

agree for the service

fee to be paid by the

customer in the form

of cash or kind; in

advance or in arrears;

in a deferred lump

sum or by

instalments.

FEATURES OF IJARAH OF SERVICES

August 23, 2021 ©2019 Your Company. All Rights Reserved

44

PERMISIBILITY OF

SERVICE

PERMISIBILITY OF

SERVICE …CONT’DAGENCY & SERVICE FEE SERVICE FEES

ISLAMIC FINANCE CONTRACTS

The contractingparties may agreefor the service feeto paid in fixedamount; to bedetermined via areference to aspecifiedbenchmark orformula; or to bepaid using acombination ofboth.

The Bank cannotincrease the service feeonce it is fixed andagreed upon.No increase in theservice fee due may bestipulated by the bank incase of delay in paymentby the customer. Theunpaid fee becomes adebt and any penaltypaid by the customerdue to delay in paymentof the service fee shallbe donated to charity

It is permissible for the

Institution to require

the customer to pay

an initial service

amount to ensure the

customer’s

seriousness in hiring

the acquired service.

This amount of

Customer’s payment

shall be adjusted

against the total hire

amount of the

Services instalments.

The customer shall

be bound to utilize

the Services solely

for the purpose for

which it was acquired

and is intended

FEATURES OF IJARAH OF SERVICES…..CONT’D

August 23, 2021 ©2019 Your Company. All Rights Reserved

45

DYNAMIC OF SERVICE

FEE

INCREASE IN SERVICE

FEE

INITIAL SERVICE

AMOUNTUTILIZATION OF SERVICE

ISLAMIC FINANCE CONTRACTS

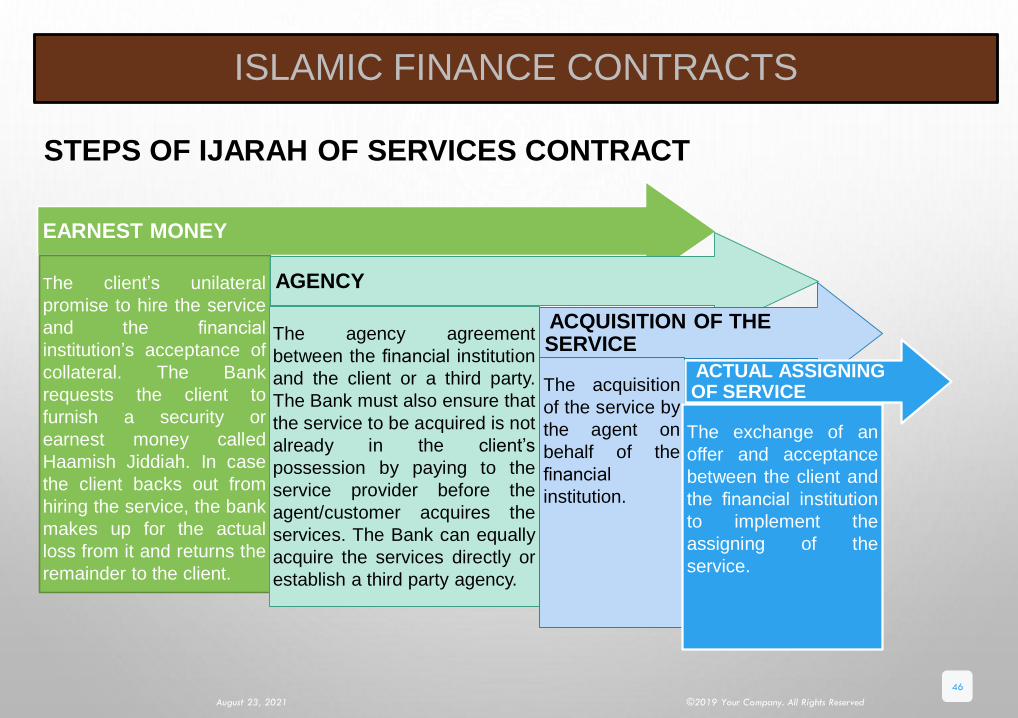

STEPS OF IJARAH OF SERVICES CONTRACT

August 23, 2021 ©2019 Your Company. All Rights Reserved

46

EARNEST MONEY

The client’s unilateral

promise to hire the service

and the financial

institution’s acceptance of

collateral. The Bank

requests the client to

furnish a security or

earnest money called

Haamish Jiddiah. In case

the client backs out from

hiring the service, the bank

makes up for the actual

loss from it and returns the

remainder to the client.

AGENCY

The agency agreement

between the financial institution

and the client or a third party.

The Bank must also ensure that

the service to be acquired is not

already in the client’s

possession by paying to the

service provider before the

agent/customer acquires the

services. The Bank can equally

acquire the services directly or

establish a third party agency.

ACQUISITION OF THE SERVICE

The acquisition

of the service by

the agent on

behalf of the

financial

institution.

ACTUAL ASSIGNING OF SERVICE

The exchange of an

offer and acceptance

between the client and

the financial institution

to implement the

assigning of the

service.

ISLAMIC FINANCE CONTRACTS

ISLAMIC FINANCE CONTRACTS

Education

Medical services

Property Rent

Airtime

Consultancy/Advisory

Travels including Hajj and Umrah

Any other permissible services

MAJOR AREAS OF FINANCING USING IJARAH SERVICE CONTRACT

ISLAMIC FINANCE CONTRACTS

Physical asset (buy)

Already owned or enjoyed services

Salaries of companies – Except where the Bank gets

direct contact/contract with the employees of such

companies.

Any services that is unlawful or aims towards

unethical.

NOT ALLOWED UNDER IJARAH SERVICES

Identification of the services by customer

Discussion with the bank

Promise to buy/hire the service

Provision of security deposit

Offer Letter

Ijarah Service Agreement

Necessary documentation

Purchase or hiring of the services by the bank

Sale/re-hire of the services to the customer by the bank at a

higher cost.

ISLAMIC FINANCE CONTRACTS

PROCESS FLOW OF IJARAH SERVICE

MUSHARAKAH (ACTIVE PARTNERSHIP)

A MUSHARAKAH IS A PARTNERSHIP THAT IS SET UP BETWEEN TWO OR MORE

PARTIES USUALLY TO CONDUCT BUSINESS OR TRADE. IT IS CREATED BY

INVESTING CAPITAL OR POOLING TOGETHER EXPERTISE OR GOODWILL.

PARTNERS SHARE PROfiT BASED ON OWNERSHIP RATIOS AND TO THE EXTENT

OF THEIR PARTICIPATION IN THE BUSINESS AND SHARE LOSS IN PROPORTION

TO THE CAPITAL THEY INVEST.

PROfiT CANNOT NOT BE FIXED IN ABSOLUTE TERMS SUCH AS A NUMBER OR

PERCENTAGE OF INVESTED CAPITAL OR REVENUE.

ISLAMIC FINANCE CONTRACTS

Musharakah capitalmay be in the formof cash or it may bein kind, for instancecontributing assetsto the business inwhich case it isnecessary to ensurethe assets arevalued at the time ofMusharakahexecution.

Profit may not be

guaranteed or fixed

in absolute terms for

any of the

Musharakah

partners

Profit may not be set

as a percentage of

capital

One partner cannot

guarantee any part

of the profit or

capital of another

partner.

Silent partner’s

profit ratio may not

exceed his

investment ratio.

During the

Musharakah, a

partner may

surrender all or part

of his profit share to

another provided

doing so is not

agreed at the time

of Musharakah

execution.

Profit sharing

mechanism and

profit ratios must be

clearly determined

at Musharakah

inception.

Musharakah may

only announce an

expected return for

the business; actual

returns are declared

only after they are

known.

FEATURES OF MUSHARAKAH

August 23, 2021 ©2019 Your Company. All Rights Reserved

51

MUSHARAKAH

CAPITALMUSHARAKA PROFIT

MUSHARAKAH

PROFITMUSHARAKAH PROFIT

ISLAMIC FINANCE CONTRACTS

PROCESS FLOW OF MUSHARAKAH

August 23, 2021 ©2019 Your Company. All Rights Reserved

52

ISLAMIC FINANCE CONTRACTS

ISLAMIC FINANCE CONTRACTS

Any business that is permissible can be considered.

However emphasis should be on only businesses that

could not be accommodated by either Murabaha,

Ijara etc.

Bring examples…………………..

AREAS OF MUSHARAKAH OPERATIONS

MUDARABAH (SILENT PARTNERSHIP)

A MUDARABAH IS A PARTNERSHIP BETWEEN TWO OR MORE PARTIES USUALLY TO

CONDUCT BUSINESS OR TRADE. TYPICALLY, ONE OF THE PARTIES SUPPLIES THE

CAPITAL FOR THE BUSINESS AND THE OTHER PROVIDES THE INVESTMENT

MANAGEMENT EXPERTISE.

WITH RESPECT TO THE SCOPE OF BUSINESS ACTIVITY, MUDARABAH MAY BE

UNRESTRICTED OR RESTRICTED.

UNRESTRICTED MUDARABAH: THE MUDARIB IS FREE TO INVEST CAPITAL IN ANY

SHARIAH-COMPLIANT PROJECT OF HIS CHOICE.

RESTRICTED MUDARABAH: THE MUDARIB’S INVESTMENT OF CAPITAL IS RESTRICTED

TO SPECIFIC SECTORS AND ACTIVITIES AND/OR GEOGRAPHICAL REGIONS ONLY. HERE

TOO, ALL INVESTMENTS MUST BE SHARIAH-COMPLIANT.

ISLAMIC FINANCE CONTRACTS

Partners capitalmay be in the formof cash or it may bein kind, for instancecontributing assetsto the business inwhich case it isnecessary to ensurethe assets arevalued at the time ofMudarabahexecution

The capital

contribution can be

made by more than

one Rabb al Maal.

The Mudarib can

also contribute

capital provided that

the Rabb al Maal/

Arbaab al Maal

approve

Only the Mudarib

possesses the right

to manage the

business.

The profit sharing

mechanism must be

clearly defined for all

the partners at the

Mudarabah’s inception

or before profit or loss

is generated.

A partner may

voluntarily surrender

all or part of his profit

share to another

partner provided it is

not pre-agreed at

contract execution

The Rabb al

Maal/Arbaab al

Maal bear(s) the

entire loss

based on capital

contribution

ratios. The

Mudarib does

not bear any

loss except that

caused by his

proven

negligence.

FEATURES OF MUDARABAH

August 23, 2021 ©2019 Your Company. All Rights Reserved

55

MUDARABAH CAPITAL MUDARABAH BUSINESS MUDARABAH PROFIT MUDARABAH LOSS

ISLAMIC FINANCE CONTRACTS

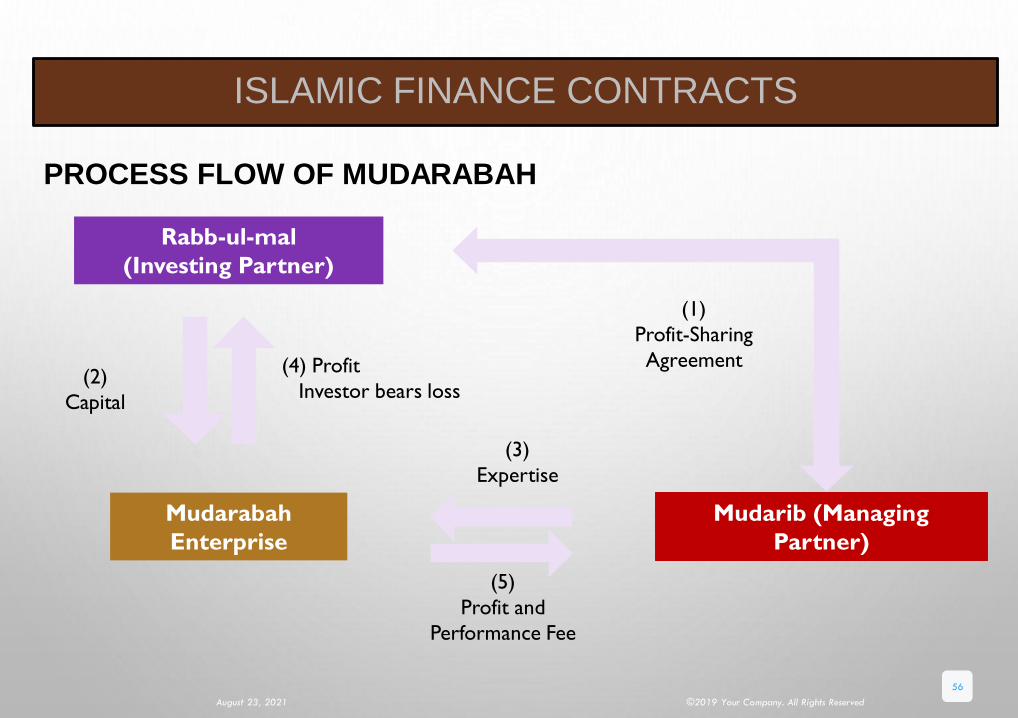

PROCESS FLOW OF MUDARABAH

August 23, 2021 ©2019 Your Company. All Rights Reserved

56

ISLAMIC FINANCE CONTRACTS

Rabb-ul-mal

(Investing Partner)

(4) Profit

Investor bears loss(2)

Capital

Mudarabah

Enterprise

Mudarib (Managing

Partner)

(3)

Expertise

(5)

Profit and

Performance Fee

(1)

Profit-Sharing

Agreement

ISLAMIC FINANCE CONTRACTS

Deposit Sourcing:

Savings Account

LOTUS Profit Sharing Account

Mudaraba Term Deposit

Financing:

Not yet operational due to issues of moral harzard.

AREAS OF MUDARABAH OPERATIONS

DIFFERENCES BETWEEN MUSHARAKAH AND MUDARABAH

MUSHARAKAH

All partners have the right to

participate in the business.

All partners must contribute capital.

All partners bear loss pro-rata to their

capital contributions

MUDARABAH

The Mudarib is solely responsible for managing the

business.

The Rabb al Maalprovides the business

capital.

Rabb al-Maal bears any loss to the

business provided it is not due to the

Mudarib’s negligence

ISLAMIC FINANCE CONTRACTS

WAKALAH (AGENCY)

WAKALAH IS A CONTRACT IN WHICH A PERSON (THE PRINCIPAL OR MUWAKKEL)

APPOINTS A REPRESENTATIVE (THE AGENT OR WAKIL) TO UNDERTAKE

TRANSACTIONS ON HIS/HER BEHALF, THAT THE PRINCIPAL DOES NOT HAVE THE

TIME, KNOWLEDGE OR EXPERTISE TO PERFORM THEMSELVES — SIMILAR TO A

POWER OF ATTORNEY AGREEMENT IN CONVENTIONAL LEGAL TERMS.

THE AGENT'S SERVICES MAY INCLUDE SELLING AND BUYING, LEASING, LENDING

AND BORROWING, DEBT ASSIGNMENT, GUARANTEE, GIFTING, LITIGATION AND

MAKING PAYMENTS, AND MAY BE UTILIZED IN NUMEROUS ISLAMIC PRODUCTS

LIKE MUSHARAKAH, MUDARABAH, MURABAHA, SALAM AND IJARAH.

WAKALAH ARE OF TWO TYPES VIZ:

WAKALAH WITHOUT FEE: WHERE THE BANK APPOINT ITS CUSTOMER AS AN

AGENT TO UNDERTAKE TRANSACTIONS ON HIS/HER BEHALF SUCH AS IN

MURABAHAH FINANCE, ISTISNA, ETC.

WAKALAH WITH FEE: WHERE CUSTOMERS APPOINT THE BANK TO INVEST THEIR

FUND ON AGENCY CONTRACT FOR A FIXED FEE, AND AT TIMES WITH A PROMISE

TO SHARE FROM THE PROFIT, IF THE RETURNS ON INVESTMENT EXCEEDS A

PARTICULAR BENCHMARK.

ISLAMIC FINANCE CONTRACTS

KAFALAH (GUARANTEE)

THIS IS A CONTRACT IN WHICH A THIRD PARTY ACCEPTS AN EXISTING

OBLIGATION AND BECOMES RESPONSIBLE FOR FULFILLING SOMEONE’S

LIABILITY. IT IS A PLEDGE GIVEN TO THE CREDITOR THAT A DEBTOR WILL REPAY

HIS DEBT.

IN CONVENTIONAL FINANCE, THIS SITUATION IS CALLED SURETY OR

GUARANTEE.

HOWEVER, IN ISLAMIC FINANCE, KAFALAH IS A GRATUITOUS CONTRACT. THIS

MEANS THAT THE SERVICE RENDERED BY THE GUARANTOR IS DONE FREELY

WITHOUT ANY REWARD OR PAYMENT. HOWEVER, IT IS POSSIBLE THAT A

GUARANTOR MAY RECOVER ACTUAL COST INCURRED FOR HIS SERVICE.

ISLAMIC FINANCE CONTRACTS

QARD HASSAN (BENEVOLENT LOAN)

QARD IS A LOAN EXTENDED ON A GOODWILL BASIS, WITH THE DEBTOR ONLY REQUIRED

TO REPAY THE AMOUNT BORROWED. IT IS THAT LOAN WHICH A PERSON GIVES TO

ANOTHER AS A HELP, CHARITY OR ADVANCE FOR A CERTAIN TIME (CHARITABLE OR NON-

COMMUTATIVE CONTRACTS).

THE REPAYMENT OF LOAN IS OBLIGATORY.

THE LENDER IS NOT ENTITLED TO DEMAND OR ENJOY ANY KIND OF BENEFITS FROM THE

BORROWER ON ACCOUNT OF THE LOAN. THIS IS BECAUSE THE LENDER HAS NOT

UNDERGONE ANY RISK, SINCE THE BORROWER MUST MAKE REPAYMENT TO THE LENDER

UPON REQUEST.

IMPOSING ANY SPECIFIC BENEFIT ON ACCOUNT OF THE LOAN BECOMES USURY, SAME

APPLIES WHERE THE BORROWER PROMISES THE CREDITOR A GIFT OR BENEFIT ON

ACCOUNT OF THE LOAN.

HOWEVER, THE SHARIAH PERMITS HUSNUL QADA (I.E. GRACIOUS REPAYMENT OF

LOANS/DEBTS) WHERE A DEBTOR REPAYS THE LENDER IN EXCESS OF THE PRINCIPAL OF

ISLAMIC FINANCE CONTRACTS

CASE STUDIES OF SHARIAH NON-COMPLIANCE

Non-Delivery of Asset in Murabaha

The Case:

•A murabaha was concluded with the customer and charges were taken by the Bank for 9 months without actually delivering the asset to the customer.

Shari’ah issue:

• Murabaha is a sale and no sale if the seller did not deliver the asset to the buyer.

Causes:

• Allowing customer to handle everything alone.

• Customer was not made to understand the importance of Shari’ahcompliance or even to know how murabaha works

MURABAHA TRANSACTION

CASE STUDIES OF SHARIAH NON-COMPLIANCE

• Depending on agency by allowing customer to do everything.

• Vendor does not own asset thereby invalidating the initial contract between him and the bank.

• Asset was not delivered to the customer which means no valid sale has taken place between the Bank and customer.

• Customer paid the bank principal and profit which is considered interest because no asset is involved.

Decision taken

• Transaction is invalid and all income earned for the 9 months should be reversed to charity.

MURABAHA …….Cont’d

CASE STUDIES OF SHARIAH NON-COMPLIANCE

MURABAHA …….Cont’d

Learning Points:

• Ensure you verify every invoice to ascertain its genuineness and availability of the asset with the vendor.

• Verify all vehicle finance to ensure that vehicles are actually purchased.

• Ensure that delivery is taken by the Bank and if done by agent, this should be clearly confirmed.

• Avoid disbursement when vendor does not have asset available.

• Ensure our customers understand how our products work and the dynamics involved especially in murabaha.

CASE STUDIES OF SHARIAH NON-COMPLIANCE

IJARAH TRANSACTION

Charging Rent Without Availability of Usufruct

The Case:

• A customer complained through the ACE that asset was not delivered to her while she was charged rent for several months. She complained that the contract she signed on Ijarah wa Iqtina stated that rent will be taken by the Bank on availability of the usufruct of the asset.

Shari’ah issue:

• Rent cannot be charged in all Ijarah contracts without the customer having access to the usufruct.

Causes:

• Financing asset under construction without taking care of the rent issue.

• Improper structuring of the facility and poor communication with customer.

• Lack of compliance with Shariah in the initial contract between the Bank and the supplier/owner as no date of delivery is specified.

CASE STUDIES OF SHARIAH NON-COMPLIANCE

• Not complying with conditions put in place in the agreement by the Bank itself.

• Lack of use of Istisna for transactions in which the asset are not ready and requires construction.Decision taken IAJA

• All income charged to the customer in the name of rent which was in excess of N2 million is not valid and should be refunded to the customer.

Learning Points

• Ijarah wa Iqtina is made for ready made asset and should be treated as such and where it must be combined with Istisna, rent should not be charged until asset is ready and delivered.

• The Bank must honor whatever conditions are contained in contracts signed by the Bank with their customers.

• Rent must only be charged when the asset and its usufruct is ready and handed over to the customer.

• Staff handling transactions must understand what is contained in contracts given to customers and their Shari’ah as well as legal implications.

• Offer letters presented by customers for financing must contain dates of delivery to enable the bank monitor the stages of construction.

CASE STUDIES OF SHARIAH NON-COMPLIANCE

IJARAH ……….Cont’d

The Case:

A customer of the Bank was availed a facility under Murabaha financing for the purchase of KOROPE BUS for which payment was made to the vendor directly (as required by Shari’ah). The vendor sent back the money to the customer’s account with a narration ‘Your Money’ referring to the money paid by the bank as customer’s money.

Shari’ah issue:

•There was fund diversion between customer and vendor.

•Where it came to the knowledge of the bank, it has become non-permissible transaction.

Issue of fund diversion in Murabaha sale contract

CASE STUDIES OF SHARIAH NON-COMPLIANCE

• Money meant for asset purchase collected back by customer and subsequently repaid to the bank in excess is regarded as interest which is prohibited in Shari’ah.

Causes

• Inability of the bank/representatives to confirm genuineness of transaction before contract execution.

• Poor monitoring after disbursement by the account officer.

• Absence of/or poor policy in place in relation to asset delivery.

• Lack of awareness of Islamic banking products and services and its modalities by some account officers/relationship managers.

• Disregard for Shari’ah issues in observing transaction sequence by processing officers.

• Ulterior motive of the customer

Cont’d………

CASE STUDIES OF SHARIAH NON-COMPLIANCE

• Lack of proper awareness on the side of customers on how Islamic finance contracts are packaged and executed.

Decisions taken:

• Invalidation of the transaction.

• Income reversed to charity account.

• Customer was made to apologise to the bank for connivance.

Learning Points:

• The branch did not ensure that asset is delivered.

• The Murabaha sequence as advised by ACE was not strictly followed.

• Delivery by the Bank was not taken seriously by the staff.

• Relying on customer to do everything.

Cont’d………

CASE STUDIES OF SHARIAH NON-COMPLIANCE

ISSUE OF FUND DIVERSION IN IJARA SERVICE CONTRACT

The Case:

• A travel agent that was to provide the service paid by the Bank in favour of a customer, transferred all the money (less 100,000.00) to the accounts of the customer in Bank A and Bank B. The customer utilized same money via POS, ATM withdrawals and fund transfer to third party. All these happened within the day of disbursement.

Shari’ah Issue:

• Fund meant for the purchase of the service and sale of same to the customer was routed back to the service beneficiary.

• Cash transferred back to the beneficiary, implies that the beneficiary indirectly collected cash upon which excess is charged for repayment with addition and this eventually becomes interest which is not permissible in shariah.

• There was connivance by the parties (customer and vendor) to go against the principles of shariah upon which the bank was established.

CASE STUDIES OF SHARIAH NON-COMPLIANCE

Cont’d…………

Causes:

• Lack of strict adherence to the ACE approved sequence of Ijarah service.

• Ignorance of customers on modalities of Islamic finance contract especially unique contract like Ijarah service.

• Reliance on the customer as agent to handle the transaction.

• Delivery of the service which is a requirement of Shariah was not emphasized by the branch.

CASE STUDIES OF SHARIAH NON-COMPLIANCE

Cont’d…………

Decision taken:

• The transaction was declared invalid.

• Income earned was transferred to charity.

• Customer was blacklisted and advised to repay the facility immediately.

• The service provider was also blacklisted for breach of trust and connivance.

Learning Points:

• Fund diversion is against the principles of Sharia.

• Like in Murabaha, it is a requirement in Ijarah service for the Bank to own and deliver service to the customer.

• The Bank should monitor closely every stage of transaction in Ijarah service as no physical asset is involved in most cases.

• Staff should take the advice of Shariah seriously.

CASE STUDIES OF SHARIAH NON-COMPLIANCE