islamic finance and derivatives lse islamic finance seminar series habib motani, partner 6 november...

TRANSCRIPT

Islamic Finance and Derivatives LSE Islamic Finance Seminar SeriesHabib Motani, Partner

6 November 2013

1. Islamic Finance - An Introduction

2. Islamic Hedging and Risk Management (Ta'hawwut)

3. Structure charts

4. ISDA / IIFM Ta'hawwut Master Agreement

5. Current Trends

6. Conclusion

Order of the Presentation

2Islamic Derivatives and the ISDA/IIFM Master Agreement

Islamic Finance –An Introduction

Islamic Derivatives and the ISDA/IIFM Master Agreement

■ Body of institutions and commercial and financial arrangements which adhere to the core tenets of Islamic law (Shari'a)

■ The idea of Shari'a-compliant financing has been prevalent for over 1,400 years (at the advent of Islam), slowly evolving over the centuries

■ Phase of more dramatic growth can be traced back to the founding of the Islamic Development Bank (in 1974) and more recently the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) and the International Islamic Financial Market (IIFM).

Background

4Islamic Derivatives and the ISDA/IIFM Master Agreement

■ The industry has been growing at around 10% per annum (FSA) for the last decade with Clifford Chance helping to lead the way

■ Since 2000, Islamic banking assets have been growing at a rate of just under 20% p.a. (Financial Times)

■ Steady rise in sukuk issuance from $500m in 2002 to $140bln in 2012 (with global outstanding at $240bln) (Zawya)

■ Sovereign sukuks on the rise and outside the Middle East – Turkey (2012) and announcement of UK sovereign sukuk to be issued in 2014

■ Estimated 350 Islamic Financial Institutions holding $1.46trln of assets under management and the industry could control $2trln of assets by 2013 (Reuters).

Growth so far…..

5Islamic Derivatives and the ISDA/IIFM Master Agreement

■ Many banks have established Islamic banking operations, joint ventures and subsidiaries in the Middle East (e.g. Deutsche Bank, HSBC, Standard Chartered Saadiq etc.)

■ Ever increasing range of Shari'a-compliant indices produced by Dow Jones, FTSE, Standard & Poor's and MSCI (e.g. S&P/TSX 60 Shari'a recently launched in Canada)

■ The industry has increasingly international appeal (significant recent developments in traditionally non-core markets including the UK, Russia, Nigeria, Turkey, Egypt, Sri Lanka, Australia and Tunisia)

■ UK government support - (i) HM Treasury's Islamic Finance Experts Group was established in April 2007, (ii) tax amendments made in 2009 to allow for Islamic finance products and (iii) announcement of £200 million sovereign sukuk issuance in 2014.

A Global Rapidly Expanding Industry

6Islamic Derivatives and the ISDA/IIFM Master Agreement

■ Shari'a carries ethical, social, political and religious dimensions that inform its structure

■ It is derived from a number of primary (Quran, Sunnah and Hadith) and secondary (Ijtihad, Ijma and Qiyas) sources

■ Not a codified body of law

■ There are a number of schools of jurisprudence (Madhabs)

■ There are a number of core tenets of Shari'a which must be considered in the context of financial transactions.

Shari'a Fundamentals

7Islamic Derivatives and the ISDA/IIFM Master Agreement

1. Riba - Prohibiting the receipt and payment of interest - the return of an investment should be linked to profits actually generated

2. Gharar - Avoiding uncertainty - e.g. traditional insurance, indemnities, options, need to be adapted

3. Maisir - Discouraging speculative behavior - e.g. speculation, gambling, games of chance

4. Sharik - Advocating risk sharing - investors should earn returns by sharing profits and assuming the risk of any loss

5. Haraam/Halal - Prohibiting haraam activities - e.g. activities that are strictly forbidden under Shari'a, such as financial investments in alcohol, pork related activities, tobacco, gambling and pornography

6. 'Aqd - Maintaining the sanctity of contracts.

Tenets of Islamic Economic Thought

8Islamic Derivatives and the ISDA/IIFM Master Agreement

■ For example, a conventional cross-currency swap would infringe the tenets of:

■ Riba

■ Gharar

■ Maisir

In the context of a Derivative Transaction

9Islamic Derivatives and the ISDA/IIFM Master Agreement

■ The Scholars■ Small number of scholars specialising in the application of Shari'a who have played a significant

role on the offshore structures to date

■ There is a wide range of views and scope for uncertainty

■ Notable scholars include:

■ "The credibility of institutions comes from the stature of the Shari'a boards they have" – Afaq Khan (CEO, Standard Chartered Saadiq)

■ Role of Scholars■ Islamic institutions place reliance on their opinions (fatwas) in determining whether transactions

are in compliance with Shari'a

■ Weight is given to the identity of the scholars

■ Prior to launching a transaction, the scholar/board will issue a fatwa confirming that the transaction adheres to the tenets of Shari'a (this fatwa may be disclosed)

Shari'a Scholars and Boards

10Islamic Derivatives and the ISDA/IIFM Master Agreement

– Sheikh Taqi Usmani (Pakistan)

– Sheikh Nizam Yaquby (Bahrain)

– Sheikh Hussain Hassan (Dubai)

– Dr. Mohammed Ali Elgari (Saudi Arabia)

– Dr. Abdul Sattar Abu Ghuddah (Syrian based in Saudi Arabia)

– Dr. Muhammad Imran Ashraf Usmani (Pakistan)

– Dr. Mohd Daud Bakar (Malaysia)

– Sheikh Yusuf Talal De Lorenzo (USA)

■ Appointing and Dealing with Scholars and Shari'a Boards■ Scholars may be employed on a transaction by transaction basis or through the establishment of

a Shari'a board

■ Establishment of a Shari'a board can provide greater comfort to Islamic investors or counterparties

■ Based predominantly in the Middle East and Pakistan

■ Typically three scholars on retainer

■ Typically commercially astute and have exposure to issues through acting on several Shari'a boards for various banks (often with educational background in Western economics or finance)

■ Involved whilst settling the term sheet and in reviewing the penultimate draft of documents

■ Typically contact is through telephone, fax and email but meetings also usually required

■ Typically a renowned scholar can earn up to $250,000 on a capital markets deal

■ Fatwa■ One, some or all parties to a transaction may or may not be bound by the fatwa

■ Not all aspects of the transaction necessarily have to be covered by the fatwa

■ No precedent system for fatwas (save for public deals).

Shari'a Scholars and Boards(cont/…)

11Islamic Derivatives and the ISDA/IIFM Master Agreement

■ Legal documents are usually drafted to be governed by either English or New York law

■ Questions of enforceability of obligations are dealt with according to the applicable national law

■ With exceptions (Sudan, Iran and Saudi Arabia), Shari'a is not the national law

■ As Shari'a is not the governing law of the documentation, being bound by Shari'a is essentially elective and seen as an extra layer of compliance

■ The Shamil case affirms that English courts will only ever seek to interpret English law and will not interpret Shari'a

■ It is for each party to satisfy itself that a transaction is compliant with Shari'a

■ Subsequent ruling by scholars that a transaction does not comply with Shari'a will not affect its enforceability under the applicable national law.

Documentation and Enforceability

12Islamic Derivatives and the ISDA/IIFM Master Agreement

Islamic Hedging and Risk Management (Ta'hawwut)

Islamic Derivatives and the ISDA/IIFM Master Agreement

■ New OTC Islamic derivatives market

■ In November 2006 Bank Islam Berhad and Bank Mumalat Malaysia Berhad agreed to execute a pro-forma derivative Master Agreement for documentation of Islamic derivative transactions

■ Each house has over the past few years been developing its own template documentation

■ ISDA/IIFM Shari'a-compliant Ta'hawwut Master Agreement ("TMA") published on 1st March 2010

■ Profit Rate Swaps (Mubdalatul Arbaah) template documentation to be used with published on 27th March 2012

■ Most common forms of derivative transactions used by Islamic banks and corporations are cross-currency swaps, profit rate swaps, total return swaps and fund index-linked derivatives

■ In recent years, some Shari'a scholars have gradually accepted the use of hedging as a tool of prudence and risk management

■ Given current market volatility, producers, consumers, counterparties and scholars are more aware of the need for hedging market risk (to minimise systemic risk) and demand for such products is growing accordingly.

Islamic Hedging and Risk Management

14Islamic Derivatives and the ISDA/IIFM Master Agreement

Building Blocks

Islamic Derivatives and the ISDA/IIFM Master Agreement

■ Literally means "promise"

■ Can be regarded as a unilateral undertaking by one party to do or not to do certain actions in the future

■ Does not bind anyone but the promisor (i.e. the party giving the undertaking)

■ Contrast this with a bilateral contract (aqd') which binds both parties to the contract

■ English law, draft under deed poll: lack of consideration

■ Qualified analogy with Promissory Estoppel.

Wa'ad Structure

16Islamic Derivatives and the ISDA/IIFM Master Agreement

■ Binding nature and enforceability is a subject of debate amongst scholars

■ Sample of views:

Wa'ad Structure(cont/…)

17Islamic Derivatives and the ISDA/IIFM Master Agreement

Group A Imam Abu Hanifah, Imam Al-Shafai', Imam Ahmad and some of the Maliki JuristsFulfilling a promise is noble but it is neither mandatory nor enforceable through a court of law

Group B Samurah b. Jundub, Umar b. Abdul Aziz, Hasan Al-Basri, Said b. al-Ashwa', Ishaq b. Rahwaih, Imam Al-Bukhari and some Maliki JuristsFulfilling a promise is mandatory and the promisor is under a moral as well as a legal obligation to honour his promise

Group C Some Maliki Jurists, Islamic Fiqh Academy (IFA)A promise is not binding under normal circumstances but becomes binding where the promisor has caused the promisee (i.e. the party having the benefit of the undertaking) to incur certain expenses or undertake work or any form of liability

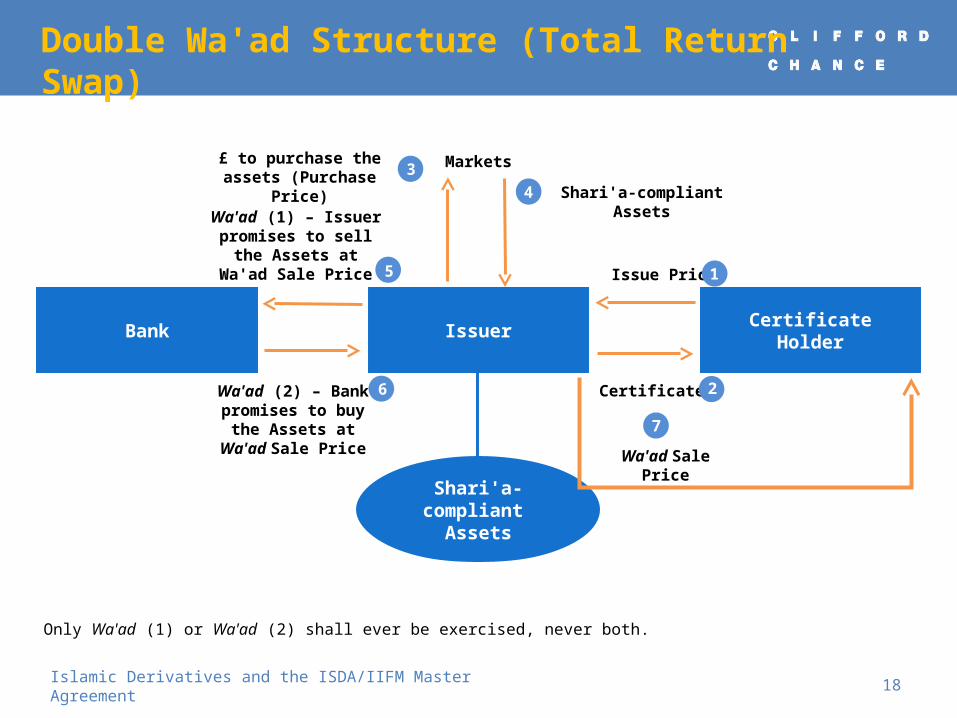

Double Wa'ad Structure (Total Return Swap)

18Islamic Derivatives and the ISDA/IIFM Master Agreement

IssuerBank Certificate Holder

Shari'a-compliant

Assets

Markets

Shari'a-compliant Assets

£ to purchase the assets (Purchase Price)

Wa'ad (1) – Issuer promises to sell the

Assets at Wa'ad Sale Price

Wa'ad (2) – Bank promises to buy the

Assets at Wa'ad Sale Price

Issue Price

Certificates

Wa'ad Sale Price

4

1

7

26

5

3

Only Wa'ad (1) or Wa'ad (2) shall ever be exercised, never both.

19

The Wa’ad and Murabaha

Islamic risk managements products are now often structured using the combination of a promise (the wa’ad), in the form of a purchase undertakings, together with the traditional murabaha sale agreement

The purchase undertakings act as a promise to buy on certain conditions: certain assets (i.e. commodities) on a certain date for a certain price and to enter into a murabaha sale agreement

At the onset, each party gives the other a purchase undertaking setting out the conditions of a trade, for example a profit rate swap:

BANK (PROMISSOR)

BORROWER (PROMISSOR)

BORROWER (PROMISSEE)

BANK (PROMISSEE)

FIXED RATE Less Than FLOATING RATE

PURCHASE UNDERTAKING

FLOATING RATE Less Than FIXED RATE

PURCHASE UNDERTAKING

Islamic Derivatives and the ISDA/IIFM Master Agreement

Price $x

FINANCIER (BANK)

SELLER

BUYER (COUNTERPARTY)

Price $(x+y)

Assets

Step 2Financier sells Assets to Buyer for $

(x+y) (where y is the pre-agreed profit element)

Step 1Financier buys

Assets from Seller for $x

Step 3Buyer settles price at end of an agreed

period in one lump-sum or in instalments

Assets

Murabaha – Cost Plus Financing

20Islamic Derivatives and the ISDA/IIFM Master Agreement

* Islamic finance is based on real assets

21

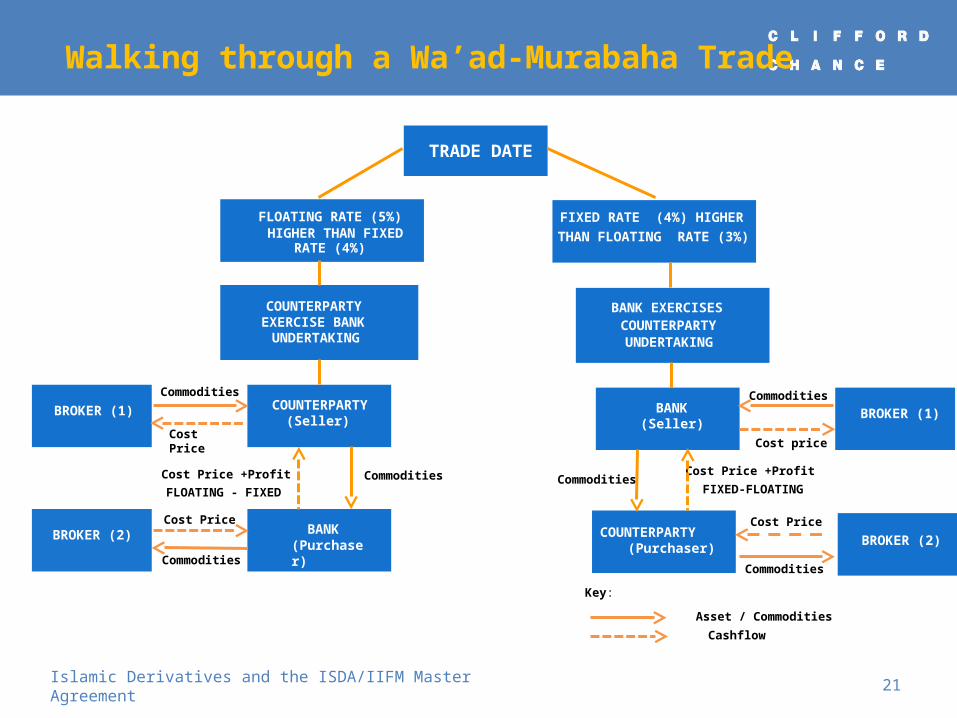

Walking through a Wa’ad-Murabaha Trade

Key:

Asset / Commodities

Cashflow

TRADE DATE

FLOATING RATE (5%) HIGHER THAN FIXED

RATE (4%)

FIXED RATE (4%) HIGHER

THAN FLOATING RATE (3%)

BROKER (1)

BROKER (2)

COUNTERPARTY (Seller)

BANK (Purchaser)

Commodities

Commodities

Cost Price

Cost Price

Cost Price +Profit

FLOATING - FIXED Commodities

COUNTERPARTY EXERCISE BANK UNDERTAKING

Islamic Derivatives and the ISDA/IIFM Master Agreement

BANK EXERCISES COUNTERPARTY UNDERTAKING

BROKER (2)

BROKER (1) BANK (Seller)

COUNTERPARTY (Purchaser)

Commodities

Commodities

Cost Price

Cost Price +Profit FIXED-FLOATING

Commodities

Cost price

22

Features of the Wa’ad-Murabaha

Two purchase agreements are entered into on day 1. Thereafter, only one commodity trade has to be effected on each subsequent trade date depending on the conditions of the purchase undertaking.

Reduced costs

Reduced ownership risk

No execution risk – as the obligation to purchase assets and pay sale price arises under the purchase undertaking once exercised. A murabaha sale agreement is signed to evidence the trade rather than effect it.

As the sale price is effectively the netted price, this can also avoid issues of netting in certain jurisdictions.

Islamic Derivatives and the ISDA/IIFM Master Agreement

23

Wa’ad-Murabaha Flexibility – Cross Currency

Key:

Asset / Commodities

Cashflow

TRADE DATE

US$ @ LIBOR FOR

EURO @ EURIBOR

EURO @ EURIBOR FORUS$ @ LIBOR

BROKER (1)

BROKER (2)

COUNTERPARTY (Seller)

BANK (Purchaser)

Commodities

Commodities

Cost Price (EUR)

Cost Price (US$)

COST PRICE (US$)

Commodities

COUNTERPARTY EXERCISE BANK UNDERTAKING

BANK EXERCISES COUNTERPARTY UNDERTAKING

BROKER (2)

BROKER (1) BANK (Seller)

COUNTERPARTY (Purchaser)

Commodities

Commodities

Cost price (US$)

Cost Price (EUR)

COST PRICE (EUR)

Commodities

Islamic Derivatives and the ISDA/IIFM Master Agreement

24

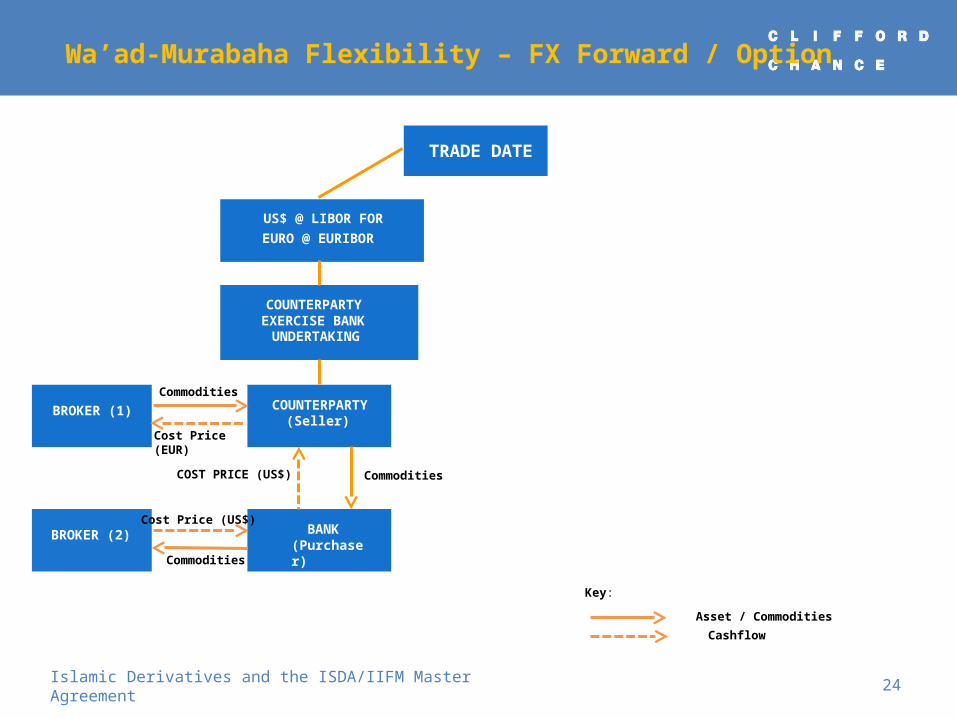

Wa’ad-Murabaha Flexibility – FX Forward / Option

Key:

Asset / Commodities

Cashflow

TRADE DATE

US$ @ LIBOR FOR

EURO @ EURIBOR

BROKER (1)

BROKER (2)

COUNTERPARTY (Seller)

BANK (Purchaser)

Commodities

Commodities

Cost Price (EUR)

Cost Price (US$)

COST PRICE (US$)

Commodities

COUNTERPARTY EXERCISE BANK UNDERTAKING

Islamic Derivatives and the ISDA/IIFM Master Agreement

ISDA / IIFM TA'HAWWUT MASTER AGREEMENT

Islamic Derivatives and the ISDA/IIFM Master Agreement

Lack of standardisation means a proliferation of bespoke documentation

Cost of evaluating and negotiating documentation

Documentation not likely to be balanced

Basis risk

Constrains the growth of the market

Standardisation contributes to efficiency, liquidity and certainty

Provides a benchmark in the market (as did the development of the original ISDA Master Agreement in the 1980s)

Help reduce price divergence between Islamic derivatives and their conventional counterparts

The Need for Standardisation

26Islamic Derivatives and the ISDA/IIFM Master Agreement

■ Joint initiative between ISDA/IIFM to produce a Master Agreement under which Shari'a-compliant hedging transactions can be documented

■ Published on 1 March 2010

■ Based on ISDA's 2002 Master Agreement with necessary amendments made for Shari'a compliance

■ Multiproducted – PRS launched, Cross Currency Swap is in development

■ To be used by all participants, in all geographical regions

■ CC is the law firm responsible for drafting the ISDA/IIFM Ta'hawwut Master Agreement and product documentation

ISDA/IIFM Ta'hawwut Master Agreement

27Islamic Derivatives and the ISDA/IIFM Master Agreement

Conventional ISDA Agreement Structure

28Islamic Derivatives and the ISDA/IIFM Master Agreement

Credit Support Documents to reduce credit risk

•2001 Margin Supplement (incorporating 2001 Margin Provisions)

•1995 Credit Support Annex (Transfer English law)

•1994 Credit Support Annex (New York law)

• 1995 Credit Support Deed (Security Interest - English law)

• 1995 Credit Support Deed (Japanese law)

• 2002 Master Agreement Protocol

Annexes

•North American Power Annex

•North American Gas Annex

•GTMA Annex (UK Power)

•European Gas Annex

2002 MASTER AGREEMENT

Confirmations

•Long form confirmations

Confirmations

•Short form confirmations

•Master confirmation agreements

Bridges

•2002 Energy Agreement Bridge

•2001 Cross-Agreement Bridge

•1996 FRABBA Bridge

•1996 BBAIRS Bridge

Definitions for use in documenting Transactions

•2007 Property Index Derivatives Definitions

•2006 Definitions

•2006 Inflation Derivatives Definitions

•2005 Commodity Definitions

•2003 Credit Derivatives Definitions

•2002 Equity Derivatives Definitions

•1998 Euro Definitions

•1998 FX and Currency Option Definitions

•1997 Government Bond Option Definitions

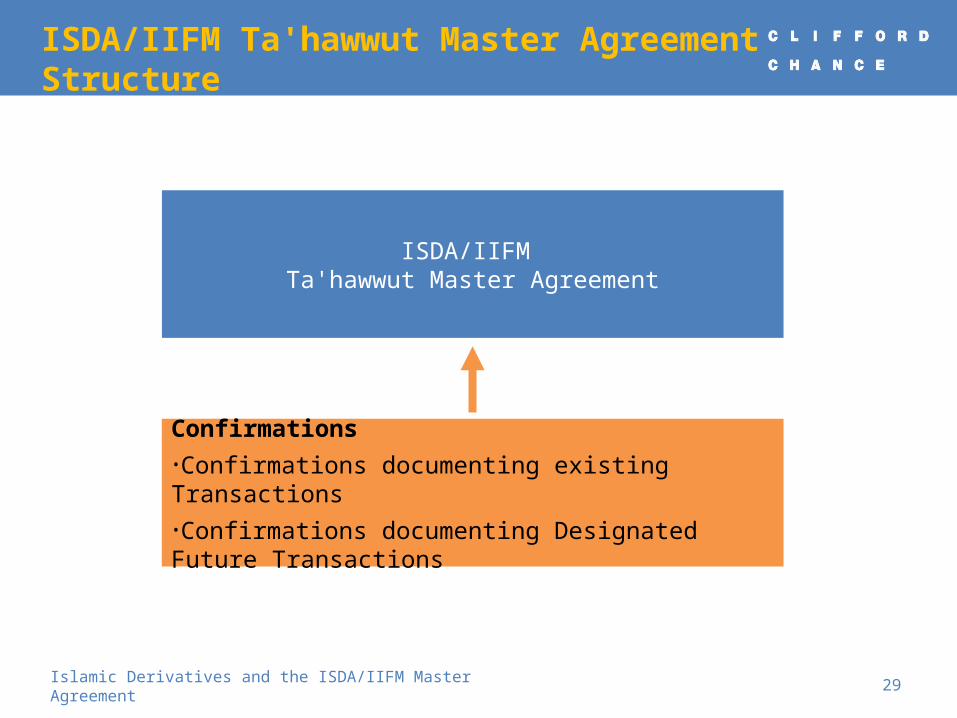

ISDA/IIFM Ta'hawwut Master Agreement Structure

29Islamic Derivatives and the ISDA/IIFM Master Agreement

ISDA/IIFM Ta'hawwut Master Agreement

Confirmations•Confirmations documenting existing Transactions•Confirmations documenting Designated Future Transactions

Architecture

Multiproduct Agreement (all murabaha , musawama and wa’ad based products but also potentially salam and arbun)

Available for use by all market participants, in all geographical regions (madhabs)

Not part of ISDA modular library

New concept hard-wired throughout the Agreement

Transactions: live transactions (concluded transactions) – “Confirmation”

transactions: Designated Future transactions (non- concluded transactions) – “DFT Terms

Agreement”, “DFT Terms confirmation”

ISDA/IIFM Tahawwut Master Agreement Architecture

30Islamic Derivatives and the ISDA/IIFM Master Agreement

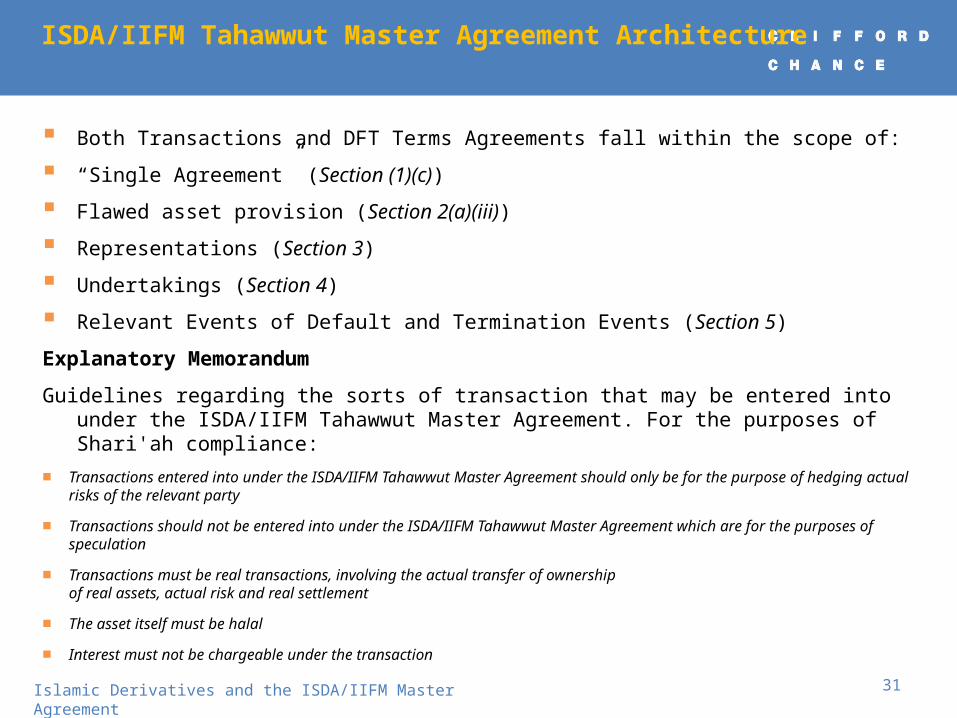

Both Transactions and DFT Terms Agreements fall within the scope of:

“Single Agreement” (Section (1)(c))

Flawed asset provision (Section 2(a)(iii))

Representations (Section 3)

Undertakings (Section 4)

Relevant Events of Default and Termination Events (Section 5)

Explanatory Memorandum

Guidelines regarding the sorts of transaction that may be entered into under the ISDA/IIFM Tahawwut Master Agreement. For the purposes of Shari'ah compliance:

■ Transactions entered into under the ISDA/IIFM Tahawwut Master Agreement should only be for the purpose of hedging actual risks of the relevant party

■ Transactions should not be entered into under the ISDA/IIFM Tahawwut Master Agreement which are for the purposes of speculation

■ Transactions must be real transactions, involving the actual transfer of ownership of real assets, actual risk and real settlement

■ The asset itself must be halal

■ Interest must not be chargeable under the transaction

ISDA/IIFM Tahawwut Master Agreement Architecture

31Islamic Derivatives and the ISDA/IIFM Master Agreement

The IIFM Shari’ah Advisory Panel has given Shari’ah Approval on the Agreement only

Disclaimer on front of Agreement re Transactions, DFT Terms Agreements and amendments or additions

Footnotes do not form part of Agreement

Although it is intended that Shari’ah-compliant derivatives be documented under the Agreement, the onus is on each of the parties to the Agreement to confirm with its own Shari’ah advisers or panel the Shari’ah compliance of the Agreement itself and each transaction traded under it

Preliminaries

32Islamic Derivatives and the ISDA/IIFM Master Agreement

The Master Agreement is a new market document and in preparing it, we have sought, where practical, to be consistent with other market standard documentation.

1.ISDA architecture (confirmations, single agreement, flawed assets concept)

2.No compensation or interest on defaulted or deferred payments and deliveries

3.No interest payable

4.Additional Representations as to Shari'a compliance

5.Governing law and dispute resolution

6.Early Termination

7.Dual Close-out mechanism

8.Set-off and netting mechanics

Analysis between 2002 Master Agreement &ISDA-IIFM Ta’hawwut Agreement

33Islamic Derivatives and the ISDA/IIFM Master Agreement

34

3 Pillars of the ISDA Master Agreement

SINGLE AGREEMENT FLAWED ASSET/CONDITIONALITY

CLOSE-OUT NETTING

Section 9(h) - No Compensation or Interest on Defaulted or Deferred Payments and Deliveries

There is no equivalent of Section 9(h) of the 2002 ISDA Master Agreement contained in the ISDA/IIFM Tahawwut Master Agreement.

The Scholars requested removal of this provision in its entirety and thus the related concepts of “fair market value”, “Applicable Deferral Rate” and “Default Rate” have also been removed

Subsequently parties cannot recover amounts for any cost of funding they incur as a result of any late payment or delivery; however the possibility of this leading to an EOD under the Agreement is in itself a deterrent

No Compensation or Interest

35Islamic Derivatives and the ISDA/IIFM Master Agreement

Section 9(h) - No Interest Payable

All references to "interest" have been deleted due to interest / riba being haraam and thus forbidden under Shari'ah principles

Section 9(h) of the ISDA/IIFM Tahawwut Master Agreement is essentially a waiver of the right to interest arising as a result of any arbitral or judicial award or by operation of law

In the event that interest is "payable or receivable under or in connection with the Agreement" ................. then such interest will be donated by the recipient to an officially recognised or registered charity

Similarly there is no interest element on the calculation of Unpaid Amounts (the Applicable Close-out Rate which is usually different for the Defaulting and Non-defaulting Party)

No Interest Payable

36Islamic Derivatives and the ISDA/IIFM Master Agreement

New Representations

Satisfaction as to compliance with Shari’ah – Section 3(h)

Each party represents it has satisfied itself as to the Shari’ah-compliance of the Agreement, each Transaction, each DFT Terms Agreement (and each Designated Future Transaction under it)

Note: “Insofar as it wishes or is required for any reason to enter ....”

Non-reliance – Section 3(i)

Each Party represents that it has not relied on the other party or on any documents (including a pronouncement/fatwa) prepared by or on behalf of the other party for the purposes of determining whether the Agreement, each Transaction, each DFT Terms Agreement (and each Designated Future transactions under it) is Shari’ah-compliant

Representations

37Islamic Derivatives and the ISDA/IIFM Master Agreement

Amended Representations Capacity as Principal (Section 3(g)):

An extra limb has been introduced to the standard “No Agency” representation to clarify that where a party enters into the Agreement, a Transaction or a DFT Terms Agreement through an agent (common in Islamic Financing), such party represents that the obligations that arise are obligations of the party itself and not the agent

Consents (Section 3(a)(iv)):

Additional wording has been added to ensure that any “declaration, pronouncement, opinion or other attestation” required to satisfy Section 3(h) has been obtained and is in full force and effect

Representations

38Islamic Derivatives and the ISDA/IIFM Master Agreement

No reference to Shari'ah in the governing law clause

Parties may elect either English law or the laws of the State of New York as the governing law of the Agreement and each Transaction and Designated Future transaction made thereunder

The term "law", does not include principles of Shari'ah

In line with the 2002 ISDA Master Agreement no wording incorporated into the Agreement to accommodate Regulation (EC) No 864/2007 on the "Law Applicable to Non-Contractual Obligations (the Rome II Regulation)" which came into effect on the 11 January 2009

Both parties at the outset have the flexibility to elect whether dispute resolution should take place through the courts or through arbitration

Common practice for parties who currently enter into transactions with Middle Eastern counterparties to amend forum provision under a 1992/2002 ISDA Master Agreement by providing for arbitration

Governing Law and Dispute Resolution

39Islamic Derivatives and the ISDA/IIFM Master Agreement

Arbitration tends to be more enforceable as most countries are signatories to the 1958 Convention on the "Recognition and Enforcement of Foreign Arbitral Awards, the NY convention" and, thus, arbitral awards are perceived to be more easily enforceable than a judgement from English or New York courts

Common Questions

What are the repercussions if Shari’ah thinking evolves?

Is Agreement enforceable if it ceases to be Shari’ah-compliant?

Governing Law and Dispute Resolution

40Islamic Derivatives and the ISDA/IIFM Master Agreement

Early Termination (General)

■ Defined Terms:■ Transactions – documented in a Confirmation■ DFT Terms Agreements – documented in a DFT Terms confirmation■ Designated Future transaction – becomes a Transaction when entered into and

to be documented in a Confirmation at that time

■ the parties may “from time to time agree (the document and other confirming evidence exchanged between the parties or otherwise effective for the purpose of confirming or evidencing any such agreement being a “DFT Terms confirmation” and each such agreement being a “DFT Terms Agreement”) the terms of further transactions in each case being either (i) a transaction which, by such DFT Terms Agreement, the parties agree to enter into between them in the future under this Master Agreement or (ii) a transaction which, by such DFT Terms Agreement, one party (the first party) undertakes to the other (the second party) to enter into under this Master Agreement at the election of the second party at a future date (all of such further transactions being “Designated Future transactions). ”

41Islamic Derivatives and the ISDA/IIFM Master Agreement

■ Event of Default:

■ All Transactions

■ All DFT Terms Agreements

■ Termination Event

■ All Affected Transactions

■ All Affected DFT Terms Agreements

■ Except where Illegality or Force Majeure, in which case less than all can be terminated

Early Termination (General)

42Islamic Derivatives and the ISDA/IIFM Master Agreement

■ Party A grants wa’ad (DFT Terms Agreement) exercisable annually for 3 years by Party B. On exercise Party A must purchase under a murabaha (Designated Future transaction) commodity for immediate delivery at a deferred purchase price

■ Wa’ad exercised after one year; murabaha entered into (becomes a Transaction), commodity delivered, purchase price deferred and payable at end of year 2

■ Early Termination after 15 months leaves outstanding:

■ deferred purchase price payable at end of year 2 under murabaha (Transaction)

■ Wa’ad potentially exercisable at end of year 2 and end of year 3 (DFT Terms Agreement)

Early Termination Example

43Islamic Derivatives and the ISDA/IIFM Master Agreement

■ Fully Delivered Terminated Transaction means, with respect to any Early Termination Date, any Terminated Transaction under which all goods or assets falling to be delivered have been delivered, irrespective of whether any payments fall to be made (Section 14)

■ (section 6(d)): accelerate all payments due after the Early Termination Date (Close-out Amount)

■ (Section 6(e)): add unpaid amounts

■ Non-Fully Delivered Terminated Transaction means, with respect to any Early Termination Date, any Terminated Transaction which is not a Fully Delivered Terminated Transaction (Section 14)

■ (section 6(e)): add unpaid amounts to Fully Delivered Transactions amount

■ (section 6(f)): treat not made deliveries and future payments like a DFT Terms Agreement

■ Early Termination Amount means (Section 6(e)) the sum of:

■ aggregated (and currency converted) accelerated future amounts under Fully Delivered Terminated Transactions

■ aggregated (and currency converted) unpaid amounts under all Terminated Transactions (both Fully Delivered and Non-Fully Delivered)

■ Payable on day on which notice of amount payable is effective if Event of Default or 2 Local Business days after notice if Termination Event

Early Termination – Terminated Transactions

44Islamic Derivatives and the ISDA/IIFM Master Agreement

■ For terminated DFT Terms Agreements, calculate Market Quotation (or Loss) (section 6(h))

■ Do the same for not made deliveries and future payments under Non-Fully Delivered Terminated Transactions

■ Result may be positive or negative

■ Becomes value of Relevant Index

■ Section 6(f)(v): if Relevant Index is positive (Determining Party is in the money), Determining Party can exercise the section 2(e) wa’ad of counterparty requiring counterparty to enter into musawama and purchase asset from Determining Party at the Positive Indexed Value

■ Section 6(f)(v): if Relevant Index is negative (Determining Party is out of the money) other party can exercise the section 2(e) wa’ad of the Determining Party requiring the Determining Party to purchase asset from the other party at the Negative Indexed Value

■ Need for real transaction with real assets

■ Supported by set off (section6(h))

■ The musawama price is expressed as a single number (actually calculated by adding cost of asset to Relevant Index Value plus applicable VAT or similar taxes)

■ The type and quantity of the asset to be the subject of the musawama will be fixed and specified in the Schedule at the outset (minimises gharar)

Early Termination – DFT Terms Agreements

45Islamic Derivatives and the ISDA/IIFM Master Agreement

In the Master Agreement, following the occurrence of an Early Termination Date, the Agreement provides for two separate payment amounts:

(a) Early Termination Amount

(b) Positive Indexed Value/Negative Indexed Value

Once determined and payable, these two amounts (Early Termination Amount and Positive/Negative Indexed Value) can be set-off against one another pursuant to Section 6(h) of the Agreement

To avoid Non-defaulting Party having to pay Early Termination Amount before any reciprocal claim to payment of the Positive/Negative Indexed value has become payable, Non-defaulting Party can defer payment of relevant proportion of Early Termination Amount until reciprocal claim becomes payable

Set-Off

46Islamic Derivatives and the ISDA/IIFM Master Agreement

Two sets of PRS templates (four documents in total) have been published, as follows:

■ one set of PRS templates that are Wa'ad-based (or undertaking-based) and involve a Two Sales structure ("Two Sales Structure")

■ another set of PRS templates that are Wa'ad-based (or undertaking-based) and involve a Single Sale structure ("Single Sale Structure")

■ Each set of templates comprises two DFT Terms confirmations, one relating to the Fixed Profit Rate leg of a PRS; the other relating to the Floating Profit Rate leg of a PRS. A form of Confirmation is provided in Annex 2 to document the Transaction that will be entered into pursuant to the terms of each DFT Terms Agreement.

Profit Rate Swap – Mubadalatul Arbaah

47Islamic Derivatives and the ISDA/IIFM Master Agreement

Features of the DFT Terms confirmations:

■ Each template DFT Terms confirmation contains line items for specific agreed terms to be completed on the Trade Date (e.g. Effective Date, Business Day, Purchase Dates, Payment Dates, Buyer, Seller, etc.), as agreed between the parties upon entry into the relevant DFT Terms Agreement.

■ For the purposes of enabling payment netting (i.e. the set off of sums due on the same day and in the same currency) between the two legs of the PRS, the DFT Terms confirmation for one leg of a PRS should identify the DFT Terms confirmation for the other leg as being related to it, as a "Related DFT Terms confirmation“.

■ A form of Exercise Notice is included in each DFT Terms confirmation at Annex 1. The form of Exercise Notice is intended to be extracted, completed and used by the Seller when it wishes to exercise the Buyer's Wa'ad (or undertaking) on an Exercise Date. This form may be used multiple times over the term of the PRS and is not to be completed upon entry into the DFT Terms Agreement.

■ A form of Murabaha Asset Sale Confirmation (i.e. a "Confirmation” for the purposes of the TMA) is included in Annex 2 of each DFT Terms confirmation. This form is intended to be extracted, completed and used to document entry into each Murabaha Sale (i.e. a "Transaction”) for the purposes of the TMA). This form may also be used multiple times over the term of the PRS and is not to be completed upon entry into the DFT Terms Agreement. Once completed and executed, the Murabaha Asset Sale Confirmation will constitute a Confirmation for the purposes of the TMA and the Murabaha Sale that it confirms will constitute a Transaction under the TMA.

Profit Rate Swap – Mubadalatul Arbaah

48Islamic Derivatives and the ISDA/IIFM Master Agreement

Current Trends and Future Developments

■ Central Bank of Bahrain and Saudi SAMA Committee approve TMA as standard

■ ISDA/IIFM – Product Development for TMA■ Cross Currency Swap product template to be launched in 2014■ Collateralised Murabaha (Islamic CSA) to be launched 2014/5

■ Legislative changes required for recognition of enforceability under the insolvency laws / tax laws of some key jurisdictions

■ Development of Islamic Repo using blend of Wa’ad, Murabahah and Title Transfer or a Mudarabah Profit Share Structure

■ Sovereign Sukuk issuances

Islamic Derivatives and the ISDA/IIFM Master Agreement 49

CONCLUSION

Islamic Derivatives and the ISDA/IIFM Master Agreement

OFFICES Worldwide Contact Information29* Offices in 20 countries

Abu DhabiClifford Chance9th FloorTel +971 (0)2 613 2300Fax +971 (0)2 613 2400

Al Sila TowerSowwah SquarePO Box 26492Abu DhabiUnited Arab Emirates

Bucharest Clifford Chance BadeaExcelsior CenterTel +40 21 66 66 100Fax +40 21 66 66 111

28-30 Academiei Street12th Floor, Sector 1Bucharest, 010016Romania

Hong KongClifford Chance28th FloorTel +852 2825 8888Fax +852 2825 8800

Jardine HouseOne Connaught PlaceHong Kong

MilanClifford ChancePiazzetta M.Bossi, 3Tel +39 02 806 341Fax +39 02 806 34200

20121 MilanItaly

PragueClifford ChanceJungmannova PlazaTel +420 222 555 222Fax +420 222 555 000

Jungmannova 24110 00 Prague 1Czech Republic

SydneyClifford ChanceLevel 16Tel +612 8922 8000Fax +612 8922 8088

No. 1 O'Connell StreetSydney NSW 2000Australia

AmsterdamClifford ChanceDroogbak 1ATel +31 20 7119 000Fax +31 20 7119 999

1013 GE AmsterdamPO Box 2511000 AG AmsterdamThe Netherlands

CasablancaClifford Chance169, boulevard Hassan 1erTel +212 520 132 080Fax +212 520 132 079

Casablanca 20000Morocco

IstanbulClifford ChanceKanyon Ofis Binasi Kat 10Tel +90 212 339 0001Fax +90 212 339 0098

Büyükdere Cad. No. 18534394 LeventIstanbulTurkey

MoscowClifford ChanceUl. Gasheka 6Tel +7 495 258 5050Fax +7 495 258 5051

125047 MoscowRussian Federation

RomeClifford ChanceVia Di Villa Sacchetti, 11Tel +39 06 422 911Fax +39 06 422 91200

00197 RomeItaly

TokyoClifford ChanceAkasaka Tameike Tower, 7th FloorTel +81 3 5561 6600Fax +81 3 5561 6699

17-7 Akasaka 2-ChomeMinato-ku, Tokyo 107-0052Japan

BangkokClifford ChanceSindhorn Building Tower 3Tel +66 2 401 8800Fax +66 2 401 8801

21st Floor130-132 Wireless RoadPathumwanBangkok 10330Thailand

DohaClifford ChanceQFC BranchTel +974 4491 7040Fax +974 4491 7050

Suite B, 30th floorTornado TowerAl Funduq StreetWest Bay PO Box 32110DohaState of Qatar

KyivClifford Chance75 Zhylyanska StreetTel +380 44 390 5885Fax +380 44 390 5886

01032 KyivUkraine

MunichClifford ChanceTheresienstraße 4-6Tel +49 89 216 32-0Fax +49 89 216 32-8600

80333 MunichGermany

São PauloClifford ChanceRua Funchal 418 15th FloorTel +55 11 3019 6000Fax +55 11 3019 6001

04551-060 São Paulo SPBrazil

WarsawClifford ChanceNorway HouseTel +48 22 627 11 77Fax +48 22 627 14 66

ul. Lwowska 1900-660 WarszawaPoland

BarcelonaClifford ChanceAv. Diagonal 682Tel +34 93 344 22 00Fax +34 93 344 22 22

08034 BarcelonaSpain

DubaiClifford ChanceBuilding 6, Level 2Tel +971 4 362 0444Fax +971 4 362 0445

The Gate PrecinctDubai International Financial CentrePO Box 9380DubaiUnited Arab Emirates

LondonClifford Chance10 Upper Bank StreetTel +44 20 7006 1000Fax +44 20 7006 5555

London, E14 5JJUnited Kingdom

New YorkClifford Chance31 West 52nd StreetTel +1 212 878 8000Fax +1 212 878 8375

New York, NY 10019-6131USA

SeoulClifford Chance21st Floor, Ferrum TowerTel +82 2 6353 8100Fax +82 2 6353 8101

66 Sooha-dongJung-gu, Seoul 100-210Korea

Washington, D.C.Clifford Chance2001 K Street NWTel +1 202 912 5000Fax +1 202 912 6000

Washington, DC 20006 - 1001USA

BeijingClifford Chance33/F, China World Office 1Tel +86 10 6535 2288Fax +86 10 6505 9028

No. 1 Jianguomenwai DajieChaoyang DistrictBeijing 100004China

DüsseldorfClifford ChanceKönigsallee 59Tel +49 211 43 55-0Fax +49 211 43 55-5600

40215 DüsseldorfGermany

LuxembourgClifford Chance2-4 place de ParisTel +352 48 50 50 1Fax +352 48 13 85

B.P. 1147L-1011 LuxembourgGrand-Duché de Luxembourg

ParisClifford Chance9 Place VendômeTel +33 1 44 05 52 52Fax +33 1 44 05 52 00

CS 5001875038 Paris Cedex 01France

ShanghaiClifford Chance40th FloorTel +86 21 2320 7288Fax +86 21 2320 7256

Bund Centre222 Yan An East RoadShanghai 200002China

BrusselsClifford ChanceAvenue Louise 65 Box 2Tel +32 2 533 5911Fax +32 2 533 5959

1050 BrusselsBelgium

FrankfurtClifford ChanceMainzer Landstraße 46Tel +49 69 71 99-01Fax +49 69 71 99-4000

60325 Frankfurt am MainGermany

MadridClifford ChancePaseo de la Castellana 110Tel +34 91 590 75 00Fax +34 91 590 75 75

28046 MadridSpain

PerthClifford ChanceLevel 7, 190 St Georges TerraceTel +618 9262 5555Fax +618 9262 5522

Perth, WA 6000Australia

SingaporeClifford Chance12 Marina BoulevardTel +65 6410 2200Fax +65 6410 2288

25th Floor Tower 3Marina Bay Financial CentreSingapore 018982

Riyadh**(Co-operation agreement)Al-Jadaan & Partners Law FirmBuilding 15, The Business GateKing Khaled International Airport RoadCordoba District, Riyadh, KSA.PO Box 3515, Riyadh 11481, Kingdom of Saudi ArabiaTel +966 11 250 6500Fax +966 11 400 4201* Clifford Chance’s offices include a second office in London at 4 Coleman Street, London EC2R 5JJ.

**The Firm also has a co-operation agreement with Al-Jadaan & Partners Law Firm in Riyadh. 51

Clifford Chance, 10 Upper Bank Street, London, E14 5JJ

UK#2350806

© Clifford Chance 2013Clifford Chance LLP is a limited liability partnership registered in England and Wales under number OC323571Registered office: 10 Upper Bank Street, London, E14 5JJWe use the word 'partner' to refer to a member of Clifford Chance LLP, or an employee or consultant with equivalent standing and qualifications

Islamic Finance and Derivatives