islamic banking mudaraba islamic bank of britain

DESCRIPTION

An overview is conducted on a banking product named Mudaraba which is currently being offered by Islamic Bank of BritainTRANSCRIPT

Table of Contents1.0 Introduction...........................................................................................................................................2

1.1 Overview............................................................................................................................................2

2.0 Banks in Great Britain............................................................................................................................3

2.1 Banking Landscape of Britain.............................................................................................................3

2.2 Mudaraba..........................................................................................................................................4

2.3 Bank Management of IBB..................................................................................................................5

3.0 Previous Research Model......................................................................................................................6

3.1 Introduction of the Research Model (CARTER)..................................................................................6

3.2.1 Reliability........................................................................................................................................7

3.2.2 Assurance.......................................................................................................................................7

3.2.3 Responsiveness...............................................................................................................................7

3.2.4 Tangibles.........................................................................................................................................8

3.2.5 Empathy..........................................................................................................................................8

4.0 Previous Research and Findings............................................................................................................9

5.0 Conclusion...........................................................................................................................................10

References:................................................................................................................................................11

1.0 Introduction

1.1 Overview

This article will conduct an analysis on a banking product named Mudaraba which is a service

offered by the Islamic Bank of Britain. “Mudaraba refers to an investment on your behalf by a

more skilled person. It takes the form of contracts between two parties, one who provides the

funds and the other who provides the expertise and who agrees to the division of any profits

made in advance” (Webmaster [a], 2010). When a customer partakes in Mudaraba with IBB the

bank would make investments on behalf of the customer that does not violate the Shari‘a

compliance and share any profits obtained from this venture with the customer. This is done

because the bank charges the customer for the time and effort they put in (Webmaster [b],

2010). In this process they effectively get rid of the interest factor also known as Riba.

Islamic Banking has been enjoying a period of exponential growth due to its transparency and

principal of Banking with a sense of Social Responsibility. It is due to this particular factor that

this product and bank we chosen.

2.0 Banks in Great Britain

2.1 Banking Landscape of Britain

The banking landscape in Britain paints a very grim picture with many conventional banking

system loosing public confidence due to improper management and because many analysts are

unable to understand why the rate of Inflation in UK remains so high despite many

interventions by the government. When observing the history of Britain it is very clear that they

have always bounced back from recessions since it significantly undercut the rate of inflation in

the region. Despite the severity of the recession that the region experienced the rate of

inflation doesn’t show any sign of budging which leads to public loosing confidence in the banks

and a sense of “what is going on?” (Peter Saunders, 2010).

A lot of the largest conventional banking institutions in the country are struggling, Northern

Rock PLLC one the largest banks in England had to be preserved by the government intervening

in the year 2007 by assuring public discontent by publicly guaranteeing all the banks deposit

(Sean Farrell, 2007). The industry hasn’t seemed to move forward since that period of time and

the rising inflation in the country is a stark reminder of a system that is failing to keep up with

the changing tides. Northern Rock PLLC wasn’t the only victim in the 2007 crises many other

banks were affected too and seem to be unable to recover four years down the track. The other

most notable banks were Alliance & Leicester, who were unable to assure a growing public

unrest which lead to the events of mass withdrawals in the early 2008.

In the year 2011 public confidence hasn’t got any better with many individuals still

remembering the events that took place and lead to Northern Rocks shares hitting rock bottom

by falling 35.4 percent which lead to an unprecedented amount of withdrawal of £2billion in

only a week. In the midst of this scenario the bank which is going to be observed is Islamic Bank

of Britain due to its stability and increase in popularity despite operating in a predominantly

Catholic country. The report will conduct a customer satisfaction study on a product of theirs

called Mudaraba.

2.2 Mudaraba

The driving force behind the idea of Mudaraba practiced by IBB is that there is a meeting of two

willing parties to venture together to mutually benefit each other financially. The two parties

consist of the Financer (the party that provides the capital and plays no role in the business

venture) and the entrepreneur which in this case is the specialist investment department of

IBB.

At the end of the business transaction if the business venture is successful the bank and the

customer share the profit on a previously agreed arrangement. Whereas if this is not the case

the loss is borne directly by the customer since the bank does not gain any benefit from their

efforts which was their responsibility at the start of the venture. Mudaraba when translated to

its simplest form means profit and loss sharing. While it may in principal seem very simple it

could also be viewed as a scenario where profit is shared and loss is absorbed by the financer

(customer). (Gafoor, 2001)

It is very important to understand that even though on paper the product may look straight

forward IBB actually practices participatory financing. Firstly since they are a bank they have

many potential investors in the form of customers (who could also be viewed as sleeping

partners) then IBB acts as an intermediary who finances projects put forward by entrepreneurs.

This builds a very cohesive triangle in which every party member depends on each other to

benefit. IBB does not take part in any entrepreneurs venture, the entrepreneur has to present a

promising project proposal and convince the bank that their idea is actually a working model

which is viable and profitable. (Gafoor, 2001)

In this product that IBB offers they take the role of both entrepreneur and financer. When IBB

accepts money from their customers they are entrepreneurs and when the bank invests in a

project they become a financer. This product also offers features of time deposits and unit

trusts.

2.3 Bank Management of IBB

The management principles of IBB revolve closely around three forms of banking which is

specially designed for the different types of customers they serve. The three different banking

approaches come in the forms of Personal, Business and Premier Banking.

The management principle behind the practice of personal banking relies on Principles,

transparency and choice. The bank emphasizes heavily on the fact that their products and

services should appeal to Muslims and non-Muslims alike and the management tries to make

people realize that when holding an account with them they are duty bound to perform and

behave in an ethical manner while investing your money (Webmaster C,2010). Unlike many

High Street banks, IBB refuses to invest their customer’s capital to finance armaments, alcohol,

tobacco or drugs companies. Their personal products are all approved by our Shari’a

Supervisory Committee, which means that as well as being in accordance with Shari’a

Principles, they offer transparency: (Webmaster C, 2010)

In terms of business banking the bank operates in a way that it gives customers who are both

Muslims and non-Muslims alike to have a choice of doing their business in a Halal manner. The

bank believes that their branch Managers should be dedicated to being seen as the most

accessible Managers in Retail Banking ready to speak to the customer personally and discuss

the features of their business product range. (Webmaster d, 2010)

With premier the bank understands that financial issues can become pretty complicated and

the responsibilities and opportunities that come with wealth can sometimes become

overwhelming. Therefore the bank makes their management adapt Shari’a compliant retail

bank in the UK so that they are in a unique position that would enable them to offer the

customer their Premier Banking service. Islamic Bank of Britain believes that premier Banking is

all about making life as simple as possible for the customer in a Shari’a compliant manner.

(Webmaster E, 2010)

3.0 Previous Research Model

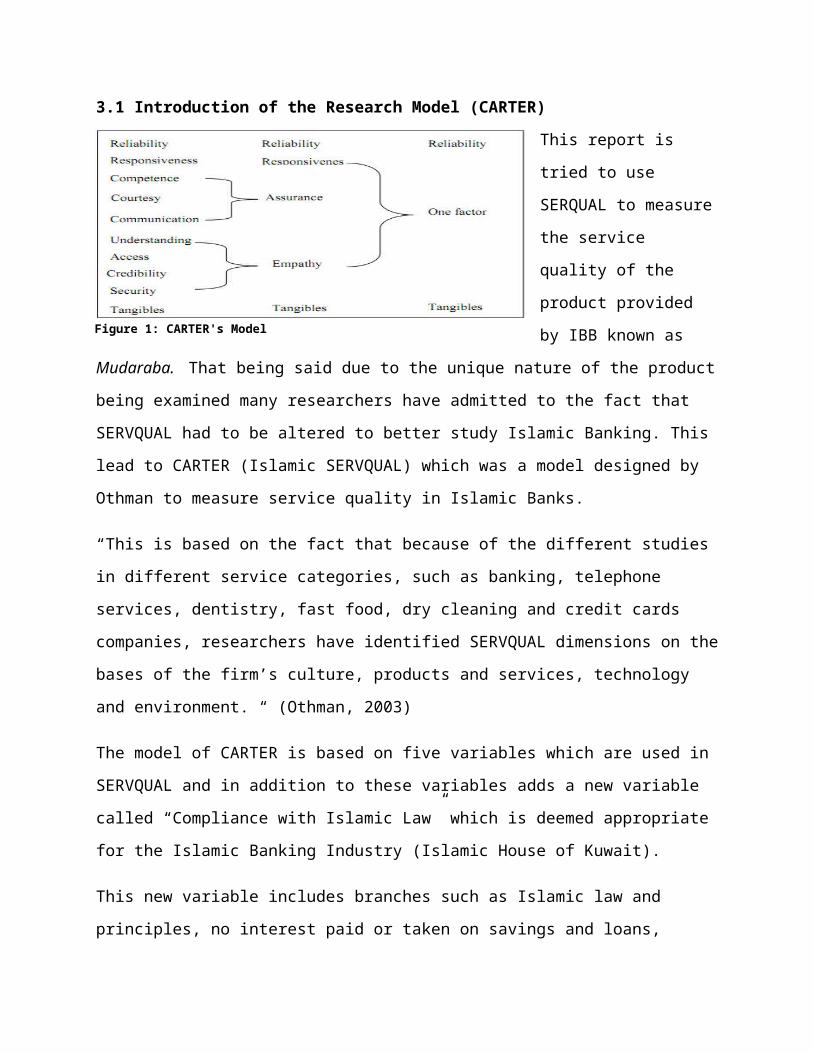

3.1 Introduction of the Research Model (CARTER)

This report is tried to use

SERQUAL to measure the

service quality of the

product provided by IBB

known as Mudaraba. That

being said due to the

unique nature of the

product being examined

many researchers have admitted to the fact that SERVQUAL had to be altered to better study

Islamic Banking. This lead to CARTER (Islamic SERVQUAL) which was a model designed by

Othman to measure service quality in Islamic Banks.

“This is based on the fact that because of the different studies in different service categories,

such as banking, telephone services, dentistry, fast food, dry cleaning and credit cards

companies, researchers have identified SERVQUAL dimensions on the bases of the firm’s

culture, products and services, technology and environment. “ (Othman, 2003)

The model of CARTER is based on five variables which are used in SERVQUAL and in addition to

these variables adds a new variable called “Compliance with Islamic Law” which is deemed

appropriate for the Islamic Banking Industry (Islamic House of Kuwait).

This new variable includes branches such as Islamic law and principles, no interest paid or taken

on savings and loans, provision of Islamic products and services, provision of free interest loans

and provision of profit sharing investment products. The only drawback of this model was that

it was designed to be conducted in regions such as the Middle East where the demography is

predominantly Muslims. (Shafie, Azmi and Haron, 2004)

An Illustration of CARTERS model can be seen in Fig.1 and the critical factors in the model will

be explained in following section of the report.

Figure 1: CARTER's Model

3.2.1 Reliability

The reliability element in the model can be explained in terms of a firm performing a particular

service right the first time around. It refers to the outcome of a particular service and promises

kept. It involves consistent performance over a period of time and dependability.(Parasurman,

1985)

According to scholarly literature, the factors that are taken into consideration for reliability are:

account accuracy (keeping records correctly, accuracy in billing), keeping promises, meeting

deadlines, providing a timely service (performing the service at the designated time), accurate

information to customers, improved cash machines, availability and dependability. Convenience

(short time for service anywhere), wide range of products and services provided, security of

transactions and more tills open at peak time have been added in the Islamic banking sector by

Othman (2003)

3.2.2 Assurance

The second element known as Assurance takes into consideration the employees attitudes to

provide competent, confidential service, courteous service, and staffs ability to provide friendly

service. (Newton, 2001) According to Assurance is defined as employees’ knowledge, courtesy

and ability of the organization and its employees to inspire trust and confidence.

Assurance in this model is particularly vital for services that the customer judge as involving

high risk or about which they feel uncertain about their ability to evaluate outcomes-for

example, in banking, insurance, legal and medical services. Customers use tangible evidence to

assess the assurance dimension – visible evidence of degree, honesty, and awards and special

certifications may give a new customer confidence in a professional service provider.

3.2.3 Responsiveness

Responsiveness factors the readiness of the staff members to provide customers with precise

details as to when exactly things will be done, prompt service, giving the customers undivided

attention, being demonstrably responsiveness to the customers’ requests. Even though this

element is very hard to put dimensions to and study, Othman’s study (2003) described

responsiveness in the Islamic banking sector as knowledge of customer’s business or willingness

to help, the way staff treat customers, availability of credit on favorable terms, and branching,

also fast counter service.

3.2.4 TangiblesTangibles refers to physical facilities, tools or equipment used to provide the service, physical

representations of the service, such as a bank statement or plastic credit cards, and speed with

efficiency of transactions.

According to Al-Tamimi and Al-Amiri (2003) defined it in terms of the appearance of branches in

terms of appeal and found it to be one of the most important dimensions. Whereas Othman

(2003) mentions that tangibles should also take into consideration: external appearance, speed

and efficiency of transactions, opening hours of operations, counter partitions in the bank, and

overdraft privileges on current accounts.

3.2.5 EmpathyOne of the biggest issues customers face in today’s banking industry is that they want to feel

understood and feel appreciated. According to Parasurman (1995) empathy is caring,

individualized attention the organization provides its customers. The essence of empathy is

conveying, through personalized or customized service, that customers are unique and special.

This dimension refers to the level of caring and individualized attention the bank provides for its

customers.

4.0 Previous Research and Findings

Many of the subjects in the test were from different ethnic and religious background. Most of

the customers were happy with the Mudaraba services due to its simplicity and efficiency but

mentioned a lot of factors that could improve in order to make the product more attractiveness

to non-Muslims.

One of the major issues with IBB was their high service charges. This made many subjects

mention that even though they provided efficient services a lot of people do not switch banks

due to expensive service charges in comparison to non Islamic banks.

Another issue that was raised in the previous research was that IBB had to open up more

branches, cash points and have longer working hours. These statements reflect that even

though the customers were happy with the product the bank should do more to improve its

convenience.

The main factors that were raised from the non-Muslim subject were that they wanted to be

more aware of how Islamic Banking works and how their money is utilized. They mention that

IBB should work harder in making sure that they share the same amount of confidence that the

Muslim community bestows on them.

They also wanted to know what terms like Halal meant and IBB defines Halal profit,

explanations of the services and how these services fit with Islamic law. From the results found

so far it can be seen that no mention has been made about the product and even though the

majority of the customers were happy with it there are some underlying issues that IBB has to

address first before its services are appreciated.

It all boils down to the fact that IBB has to improve their communications with non Muslim

customers and make both their non Muslim and Muslim clientele feel secure and confident in

the bank's management and make both parties more aware of what Shari’a means .

5.0 Conclusion

Even though Islamic Banking is one of the most rapidly growing tributary in the financial river it

has to be understood that the peoples’ confidence in their Shari’a scholars is one of the most

fundamental pillar of Islamic banking. If the Shari’a scholars lose the confidence of its people,

Islamic banking will have a sad end before it even realized its full potential. Shari’a scholars play

an important role in the development and growth of the Islamic Banking system IBB is

practicing. As a result, they have to understand that their Muslim customers should never loose

confidence in their scholars. There is a question in every Muslims mind, whether it operates in a

Muslim country or a non-Muslim country, how is Islamic Bank of Britain’s operations in

accordance with the spirit of Islam or that are they merely following the conventional system

with a few changes here and there? Getting an ‘all clear’ from Shari’a scholars must be open for

discussion and customers have a right to know the facts about the operations. Are the Shari’a

scholars capable of handling the complex financial system and keeping the operation Islam

compliant? That is something that cannot be answered but only observed with time.

References:

1. Abdul Gafoor. (2001). Mudaraba. Available: http://www.islamicbanking.nl/article2.html.

Last accessed o6th March 2010.

2. Andreasen, A., 2002. Marketing research that won’t break the bank: a practical guide to

getting the information you need. USA, Jossey-Bass; 2nd edition.

3. Angur, M. G., Nataraajan, R. and Jahera, J. S., 1999. Service quality in the banking

industry: an assessment in a developing economy. The International Journal of Bank

Marketing, 17(3), pp 116-125.

4. Antony, J., Antony, F. and Ghosh, S., 2004. Evaluating service quality in a UK hotel chain:

a case study. International Journal of Contemporary Hospitality Management, 16(6), pp

380-384.

5. Al-Tamimi, H. A. and Al-Amiri, A., Dec. 2003. Analysing service quality in the UAE Islamic

banks, Journal of Financial Services Marketing, 8(2), pp 119-133.

6. Carrillat, F., Jaramillo, F. and Mulki, J., 2007. The validity of the SERVQUAL and SERVPERF

scale: a meta- analytic view of 17 years of research across five continents. International

Journal of Service Industry Management, 18(5), pp 472-490

7. Casalo, L., Flavian, C. and Guinaliu, M., 2008. The role of satisfaction and website

usability in developing customer loyalty and positive word-of-mouth in the e-banking

services. International Journal of Bank Marketing, 26(6), pp 399-417.

8. Chapra, M. U., 2000. The future of economics: An Islamic perspective. The Islamic

Foundation, Markfiled conference center. Ciptono, W. and Soviyanti, E., 2007. Adopting

Islamic Banks’ CARTER model; an empirical study in RAU’s SYARIAH banks, Indonesia,

Proceeding PESAT (Psikologi, Ekonomi, Sastra, Arsitek and Sipil

9. Othman A. Q., 2003. Adopting and measuring customer service quality in Islamic banks:

A case study in Kuwait Finance House. PhD Thesis

10. Parasuraman, A., Berry L. and Zeithmal V., 1985. A conceptual model of SQ and its

implications for future research. Journal of Marketing, 49(3), pp 41-50.

11. Peter Spencer. (2010). The message for the bank Britain might just have got it

right. Available: http://www.parliamentarybrief.com/2010/10/the-message-for-the-

bank-britain-might-just-have-got. Last accessed 26th March 2010.

12. Sean Farrell. (2010). Banking crisis: The fear spreads. Available:

http://www.independent.co.uk/news/business/news/banking-crisis-the-fear-spreads-

402674.html. Last accessed 15th March 2010.

13. Shafie, S., Azmi, W. and Haron, S., 2004. Adopting and measuring customer service

quality (SQ) in Islamic banks: A case study in Bank Islam Malaysia Berhad. Journal of

Muamalat and Islamic Finance Research, 1(1), pp 91-102.

14. Webmaster(a). (2010). What is Islamic Finance?. Available: http://www.islamic-

bank.com/sharia-finance/. Last accessed 01th April 2010.

15. Webmaster(b). (2010). Glossary. Available: http://www.islamic-bank.com/glossary/. Last

accessed 26th March 2010.

16. Webmaster(c). (2010). Personal Banking: http://www.islamic-bank.com/personal-

banking/. Last accessed 29th March 2010.

17. Webmaster (d).(2010). Premier Banking: http://www.islamic-bank.com/business-

banking/ . Last Accessed 18th March 2010.

18. Webmaster (e).(2010).Business Banking: http://www.islamic-bank.com/premier-

banking/. Last Accessed 13th March 2010.