is the cheese still there? julie l. hulsey, clu, lutcf insurance professionals zynia business...

TRANSCRIPT

IS THE CHEESE STILL THERE? Julie L. Hulsey, CLU, LUTCF

Insurance ProfessionalsZynia Business Solutions

6601 I-40 West Suite 1Amarillo, TX 79106

(806) [email protected]

Healthcare Reform Certified

The information provided in this presentation is only intended to be a brief summary of the laws that have been enacted and is not intended to be an exhaustive description of the laws or a legal opinion of such laws. This information does not constitute legal or tax advice and it may be subject to change.

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

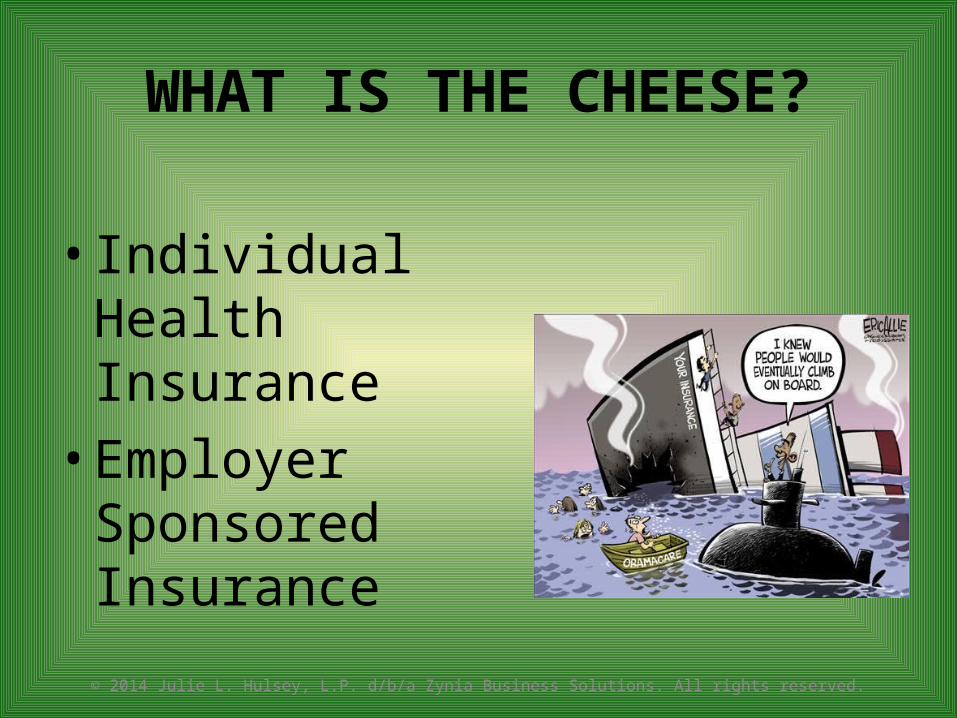

WHAT IS THE CHEESE?

• Individual Health Insurance • Employer

Sponsored Insurance

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

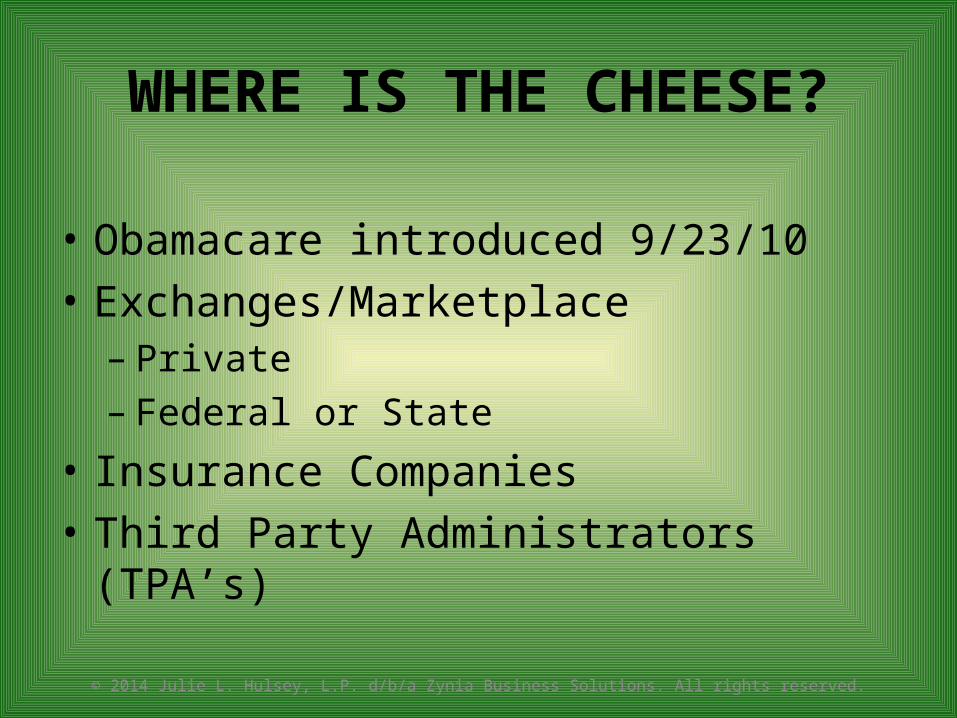

WHERE IS THE CHEESE?

• Obamacare introduced 9/23/10• Exchanges/Marketplace– Private– Federal or State

• Insurance Companies • Third Party Administrators (TPA’s)

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

WHO IS AFFECTED BY THE CHEESE?

• Insurance Companies • Brokers/Agents• Customers– Individual – Employers

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

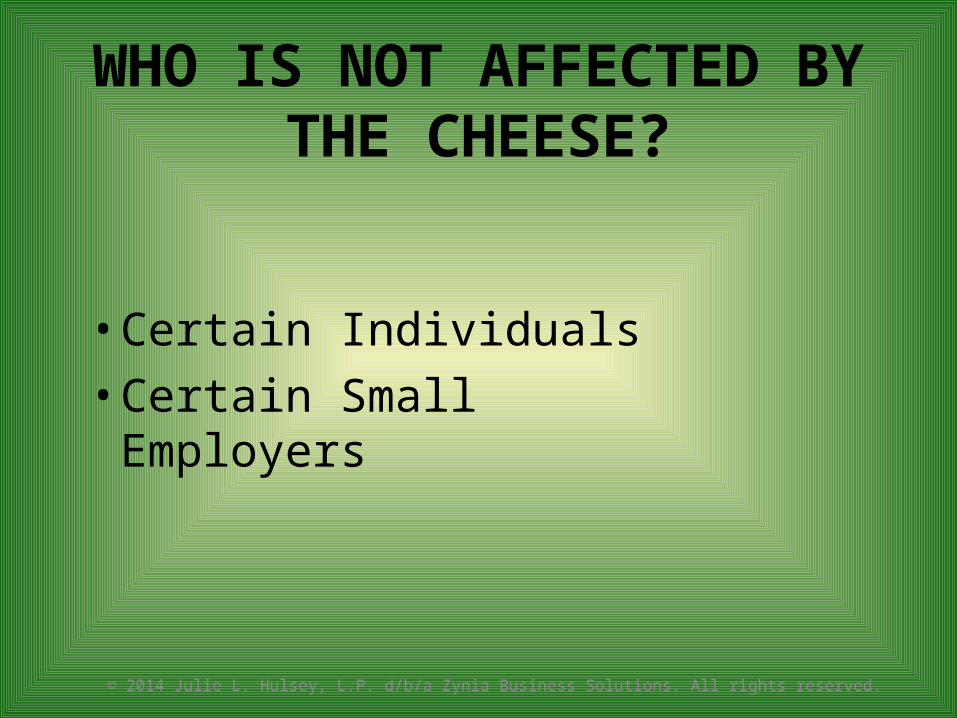

WHO IS NOT AFFECTED BY THE CHEESE?

• Certain Individuals • Certain Small Employers

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

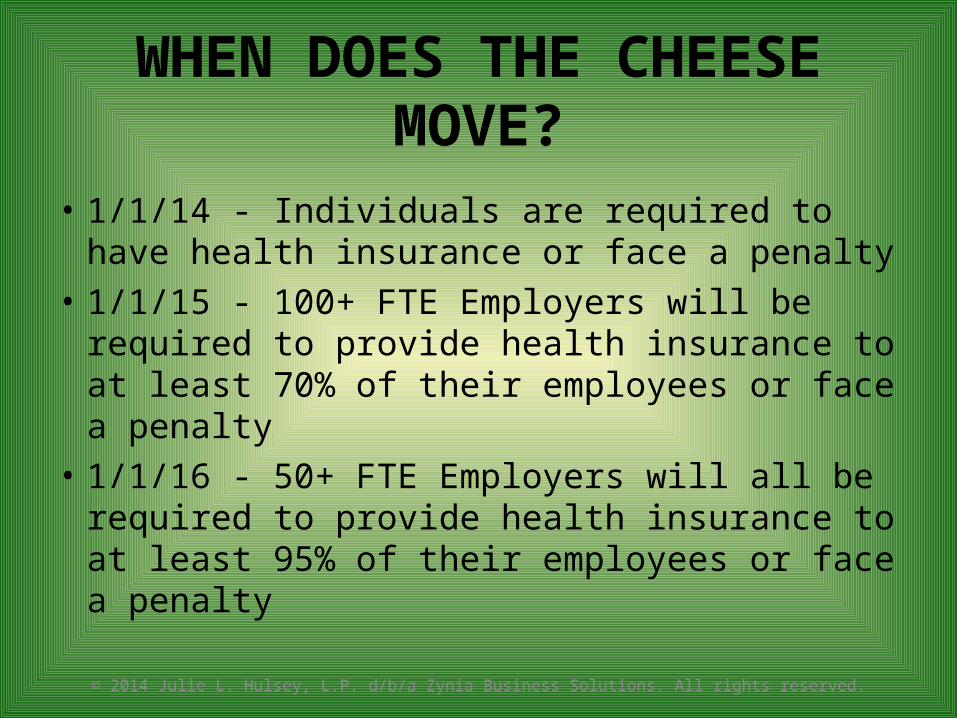

WHEN DOES THE CHEESE MOVE?

• 1/1/14 - Individuals are required to have health insurance or face a penalty

• 1/1/15 - 100+ FTE Employers will be required to provide health insurance to at least 70% of their employees or face a penalty

• 1/1/16 - 50+ FTE Employers will all be required to provide health insurance to at least 95% of their employees or face a penalty

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

THE INDIVIDUAL MANDATE• Coverage under an eligible employer-sponsored plan• Individual health policy• Medicare• Medicaid• CHIP• Tricare• Self-funded student health coverage and

state high-risk pools• Refugee medical assistance supported by

the Administration for Children and Families• Medicare Advantage plans• Any additional coverage that HHS

designates or recognizes as minimum essential coverage

Minimum Essential Coverage includes:

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

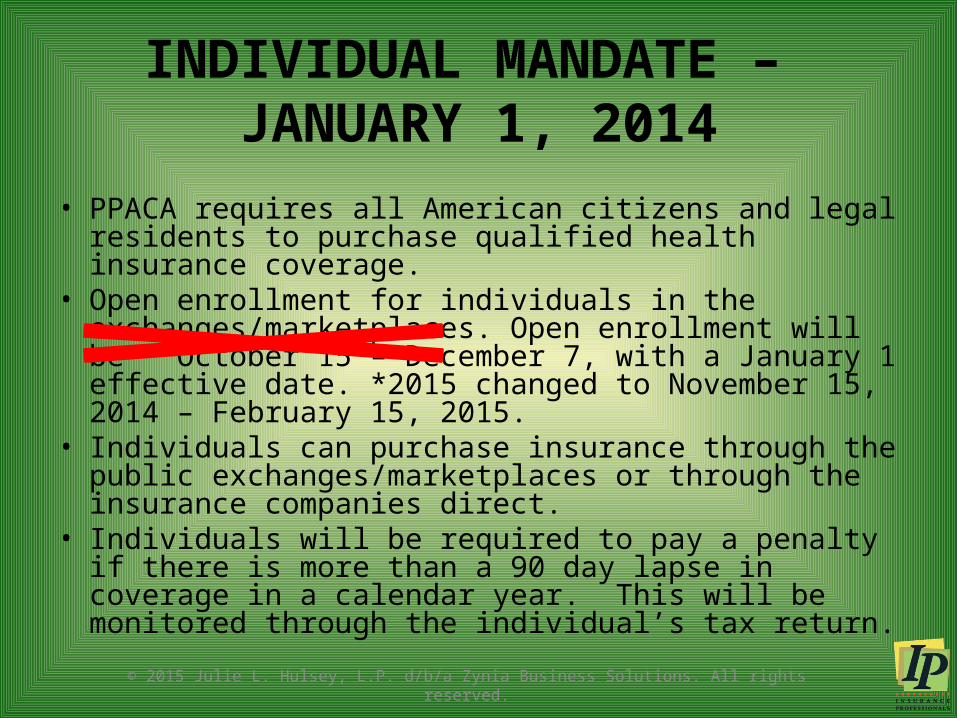

INDIVIDUAL MANDATE – JANUARY 1, 2014

• PPACA requires all American citizens and legal residents to purchase qualified health insurance coverage.

• Open enrollment for individuals in the exchanges/marketplaces. Open enrollment will be October 15 – December 7, with a January 1 effective date. *2015 changed to November 15, 2014 – February 15, 2015.

• Individuals can purchase insurance through the public exchanges/marketplaces or through the insurance companies direct.

• Individuals will be required to pay a penalty if there is more than a 90 day lapse in coverage in a calendar year. This will be monitored through the individual’s tax return.

© 2015 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

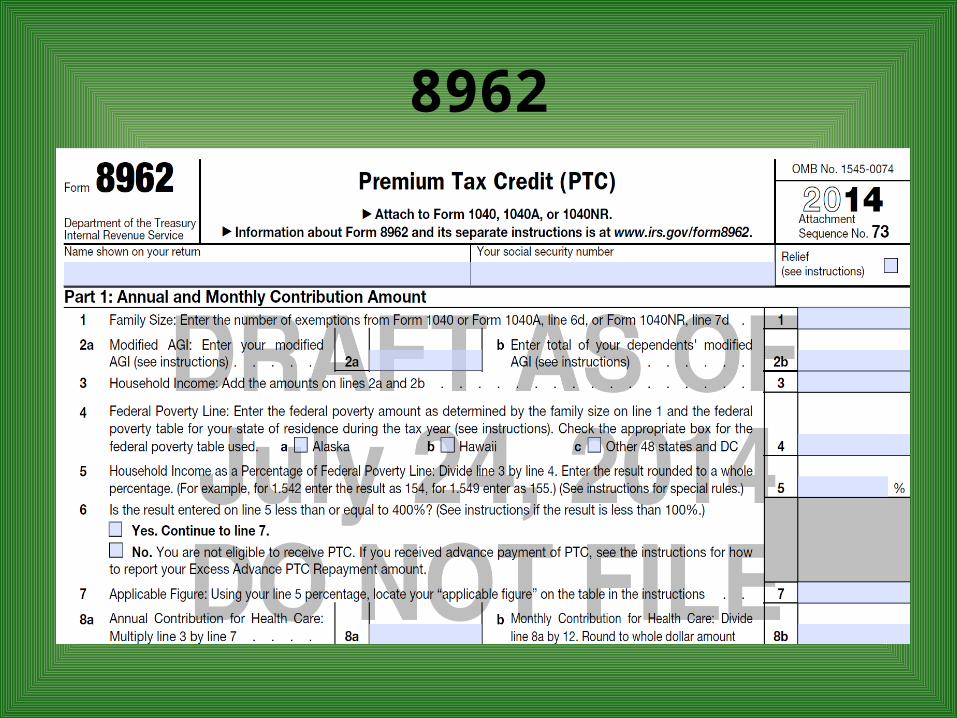

8962

HEALTH COVERAGE EXEMPTION FORM 8965 (12 PAGES)

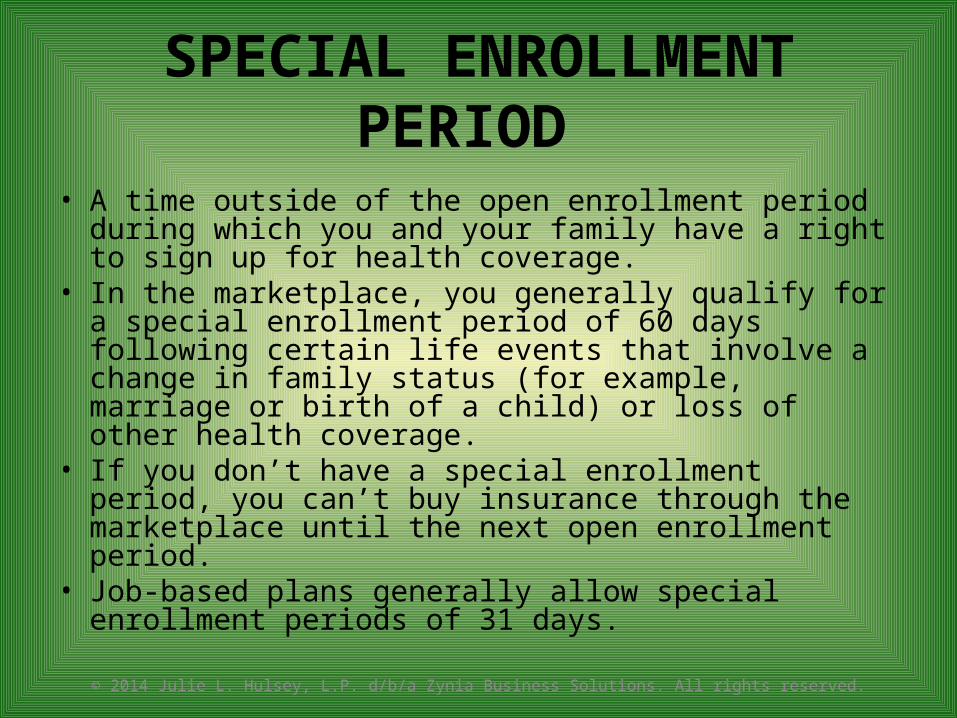

SPECIAL ENROLLMENT PERIOD

• A time outside of the open enrollment period during which you and your family have a right to sign up for health coverage.

• In the marketplace, you generally qualify for a special enrollment period of 60 days following certain life events that involve a change in family status (for example, marriage or birth of a child) or loss of other health coverage.

• If you don’t have a special enrollment period, you can’t buy insurance through the marketplace until the next open enrollment period.

• Job-based plans generally allow special enrollment periods of 31 days.

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

• SUBSIDY DISCLAIMER

•HIPAA CLIENT CONSENT FORM

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

WHO IS ELIGIBLE FOR TAX CREDITS?

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

Federal Poverty Guidelines 2014 – for Continental U.S.

Persons in Household

2014 Federal Poverty Level (100% FPL)

Medicaid Eligibility* (138% of FPL)

Cost Sharing Reduction and Premium cap guideline (150% FPL)

Cost Sharing Reduction subsidy threshold (250% FPL)

Premium subsidy threshold (400% of FPL)

1 $11,670 $16,105 $17,505 $29,175 $46,680

2 $15,730 $21,707 $23,595 $39,325 $62,920

3 $19,790 $27,310 $29,685 $49,475 $79,160

4 $23,850 $32,913 $35,775 $59,625 $95,400

5 $27,910 $38,516 $41,865 $69,775 $111,640

6 $31,970 $44,119 $47,955 $79,925 $127,880

7 $36,030 $49,721 $54,045 $90,075 $144,120

8 $40,090 $55,324 $60,135 $100,225 $160,360

EXEMPTIONS FROM THE INDIVIDUAL MANDATE

• Members of federally recognized Indian tribes;• Individuals who experience a hardship;

Those for whom the lowest cost plan option exceeds 8% of an individual’s income

Those with incomes below the tax filing threshold• Individuals who experience a gap in coverage for less than a continuous

three-month period (may only be used for one period without coverage per year);

• Members of certain religious sects;• Members of a health care sharing ministry;• Incarcerated individuals (more than 3 days)• Individuals who are not citizens, nationals or lawfully present in the U.S.

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

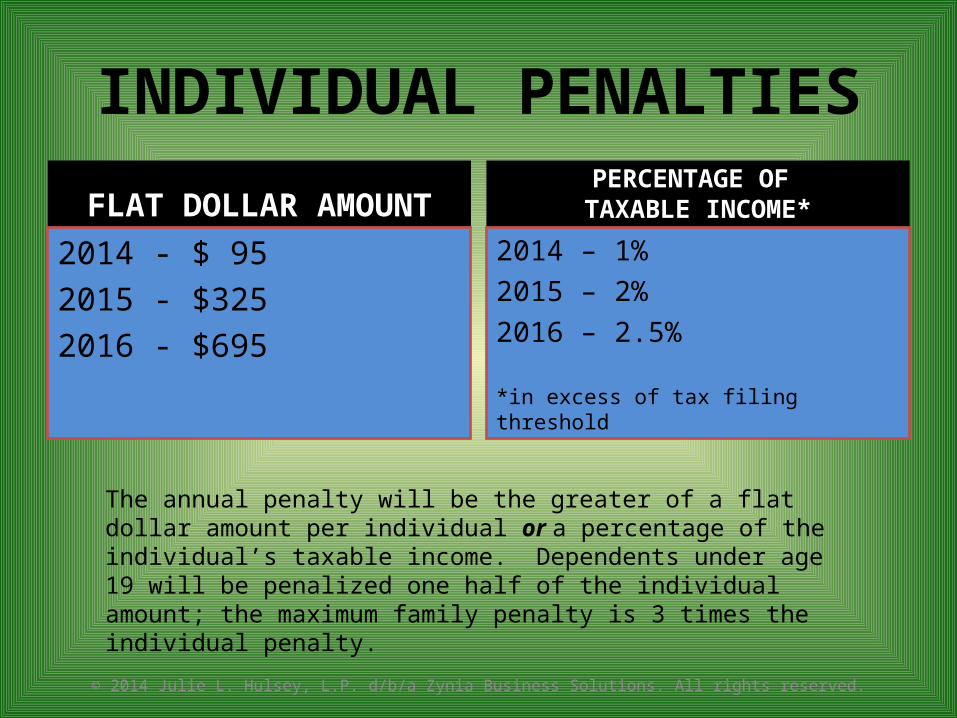

INDIVIDUAL PENALTIES

FLAT DOLLAR AMOUNT2014 - $ 952015 - $3252016 - $695

PERCENTAGE OF TAXABLE INCOME*

2014 – 1%2015 – 2%2016 – 2.5%

*in excess of tax filing threshold

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

The annual penalty will be the greater of a flat dollar amount per individual or a percentage of the individual’s taxable income. Dependents under age 19 will be penalized one half of the individual amount; the maximum family penalty is 3 times the individual penalty.

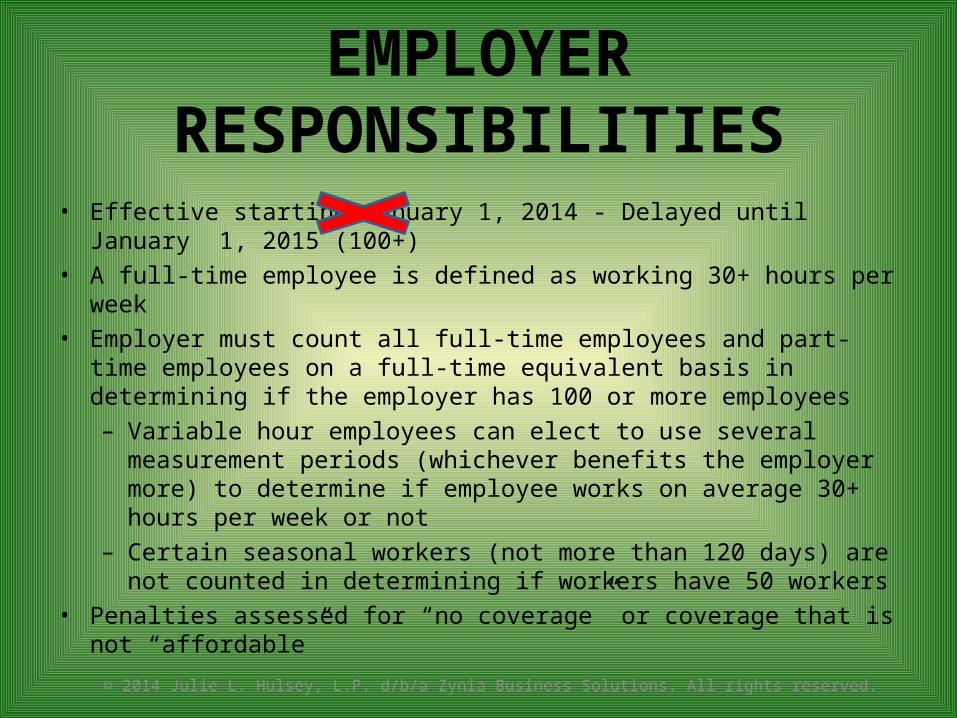

EMPLOYER RESPONSIBILITIES

• Effective starting January 1, 2014 - Delayed until January 1, 2015 (100+)• A full-time employee is defined as working 30+ hours per week• Employer must count all full-time employees and part-time employees on

a full-time equivalent basis in determining if the employer has 100 or more employees– Variable hour employees can elect to use several measurement

periods (whichever benefits the employer more) to determine if employee works on average 30+ hours per week or not

– Certain seasonal workers (not more than 120 days) are not counted in determining if workers have 50 workers

• Penalties assessed for “no coverage” or coverage that is not “affordable”

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

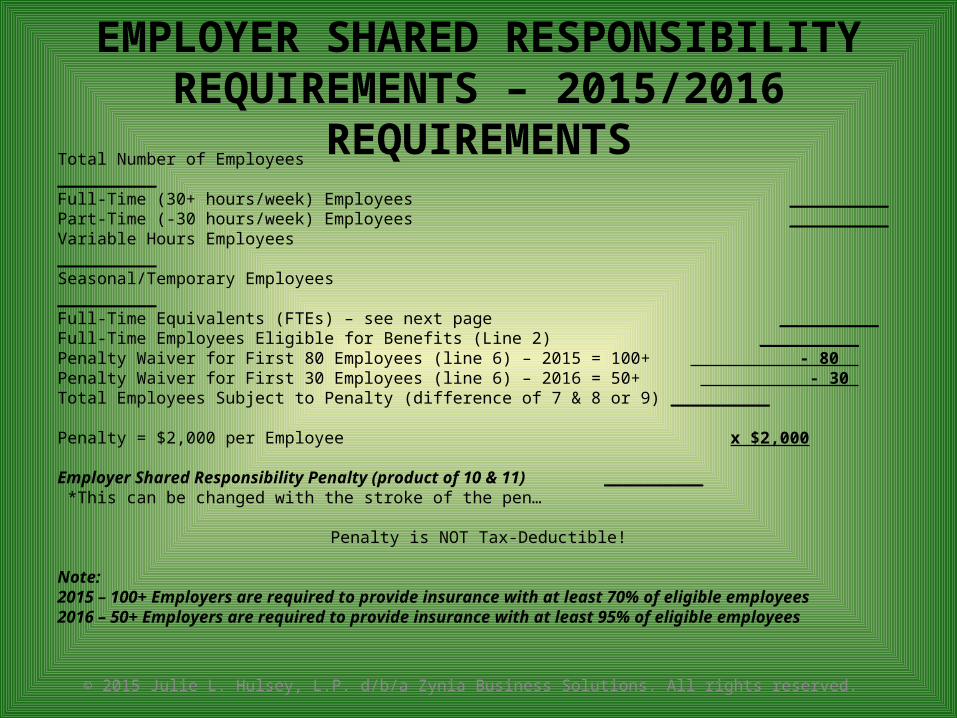

EMPLOYER SHARED RESPONSIBILITY REQUIREMENTS – 2015/2016 REQUIREMENTS

Total Number of Employees __________Full-Time (30+ hours/week) Employees __________Part-Time (-30 hours/week) Employees __________Variable Hours Employees __________Seasonal/Temporary Employees __________Full-Time Equivalents (FTEs) – see next page __________Full-Time Employees Eligible for Benefits (Line 2) __________ Penalty Waiver for First 80 Employees (line 6) – 2015 = 100+ - 80 Penalty Waiver for First 30 Employees (line 6) – 2016 = 50+ - 30 Total Employees Subject to Penalty (difference of 7 & 8 or 9) __________

Penalty = $2,000 per Employee x $2,000 Employer Shared Responsibility Penalty (product of 10 & 11) __________ *This can be changed with the stroke of the pen…

Penalty is NOT Tax-Deductible! Note: 2015 – 100+ Employers are required to provide insurance with at least 70% of eligible employees2016 – 50+ Employers are required to provide insurance with at least 95% of eligible employees

© 2015 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

Full- Time Equivalents (FTE) Calculation

1. Number of Full-Time Employees

2. Total Number of Hours Worked for Part-Time Employees (Not Exceeding 120 Hours for Any Employee)

3. Divide Hours listed in #2 by 120 =

4.Add Number of Employees together in #1 & #3 = FTEs

Variable Hour & Seasonal/Temporary Employees This requires a more in-depth discussion and will be conducted in person if you employ these type employees.

© 2015 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

“SHARED RESPONSIBILITY” (PENALTIES)

• No Penalty– Effective 1/1/16, employers with 50 FTEs who offer “minimum essential coverage” to at least 95%

of all full-time employees will face no penalty. (Effective 1/1/15, 100+ employers - 70% of full-time employees)

– Only full-time (30+ hours per week) employees can create a penalty for employers by qualifying for a subsidy through the exchange/marketplace; part-time employees are not eligible for employer benefits.

– Employees that sign a waiver to not accept the employer’s “minimum essential coverage” that meets the “affordable” and “minimum value” testing will not cause the employer to pay a penalty.

• $2,000 Penalty – Failure to Offer Coverage– Employers with 50 FTEs who do not offer any coverage to at least 95% of full-time employees and at

least one full-time employee receives a subsidy in the individual exchange/marketplace.– $2,000 penalty per full-time employee, not FTE.– Excludes first 30 employees

• $3,000 Penalty – “Unaffordable” or “Not Minimum Value” Coverage– Effective 1/1/16, employers with 50 or more FTEs that offer any coverage to 95% of their full-time

employees, (effective 1/1/15, 100+ employers - 70% of full-time employees) penalty is the lesser of: $3,000 for each employee that receives subsidized coverage through an exchange/marketplace

because the employer’s coverage does not meet “minimum essential coverage”, or $2,000 per full-time employee (excluding the first 30 employees)

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

RECAPPING THE TRANSITION RELIEFFOR MID-SIZE ALES (50-99 FT + FTES)

• Limited Workforce Size. The employer must employ on average at least 50 full-time employees (including full-time equivalents) but fewer than 100 full-time employees (including full-time equivalents) on business days during 2014.

• Maintenance of Workforce and Aggregate Hours of Service. During the periodbeginning on Feb. 9, 2014 and ending on Dec. 31, 2014, the employer may not reducethe size of its workforce or the overall hours of service of its employees in order toqualify for the transition relief. However, an employer that reduces workforce size oroverall hours of service for bona fide business reasons is still eligible for the relief.

• Maintenance of Previously Offered Health Coverage. During the period beginning on Feb. 9, 2014 and ending on Dec. 31, 2015 (or, for employers with non-calendar-year plans, ending on the last day of the 2015 plan year) the employer does not eliminate or materially reduce the health coverage, if any, it offered as of Feb. 9, 2014.

© 2015 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

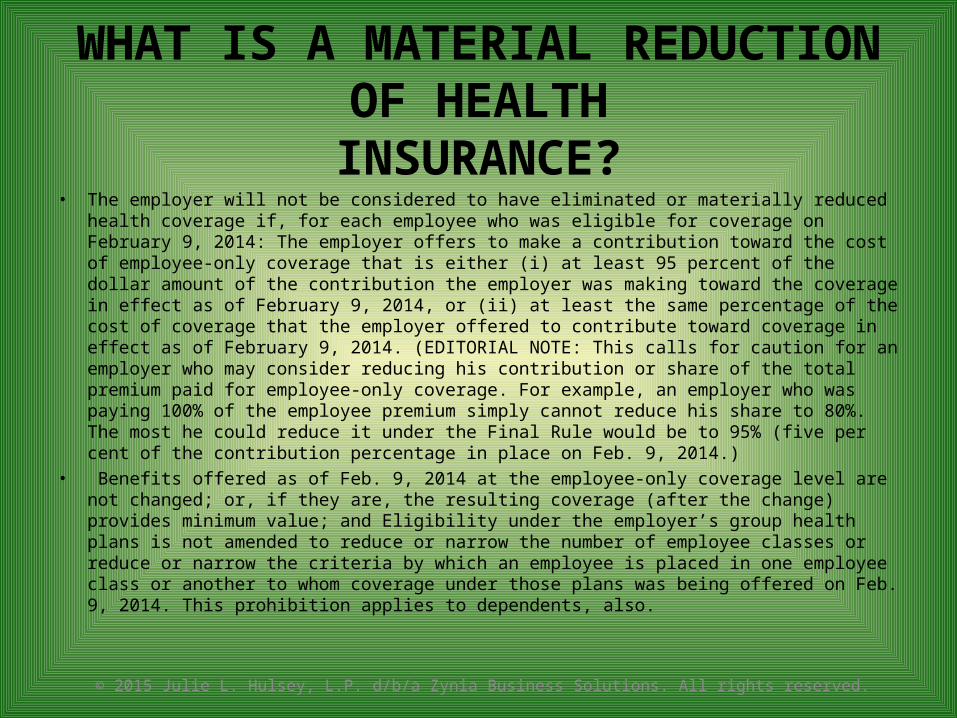

WHAT IS A MATERIAL REDUCTION OF HEALTH

INSURANCE?• The employer will not be considered to have eliminated or materially reduced health

coverage if, for each employee who was eligible for coverage on February 9, 2014: The employer offers to make a contribution toward the cost of employee-only coverage that is either (i) at least 95 percent of the dollar amount of the contribution the employer was making toward the coverage in effect as of February 9, 2014, or (ii) at least the same percentage of the cost of coverage that the employer offered to contribute toward coverage in effect as of February 9, 2014. (EDITORIAL NOTE: This calls for caution for an employer who may consider reducing his contribution or share of the total premium paid for employee-only coverage. For example, an employer who was paying 100% of the employee premium simply cannot reduce his share to 80%. The most he could reduce it under the Final Rule would be to 95% (five per cent of the contribution percentage in place on Feb. 9, 2014.)

• Benefits offered as of Feb. 9, 2014 at the employee-only coverage level are not changed; or, if they are, the resulting coverage (after the change) provides minimum value; and Eligibility under the employer’s group health plans is not amended to reduce or narrow the number of employee classes or reduce or narrow the criteria by which an employee is placed in one employee class or another to whom coverage under those plans was being offered on Feb. 9, 2014. This prohibition applies to dependents, also.

© 2015 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

OTHER PENALTY CLARIFICATIONS!• If an employer offers a “minimum essential coverage” plan that meets the

“affordable” and “minimum value” tests to an employee who declines it, no employer penalty will be owed for that employee. Keep a copy of the signed waiver of coverage form.

• No employer penalty is owed for part-time employees even if they receive a subsidy.

• No penalty is owed if the employee obtains coverage from other means; i.e., spouse’s employer plan.

• To avoid a penalty, employers that offer coverage to full-time employees must also offer coverage to the dependents of those full-time employees who are children under age 26. “Offering coverage” to dependents does not mean the employer has to pay for or subsidize the dependent coverage and coverage need not be offered to spouses.

• Penalties will be calculated on a monthly basis so if you are out of compliance for just one month, you will only be penalized for that month. Therefore, become compliant as soon as possible to avoid accumulating more monthly penalties.

© 2015 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

NEW FORMS TO BE FILED BY 1/31/16

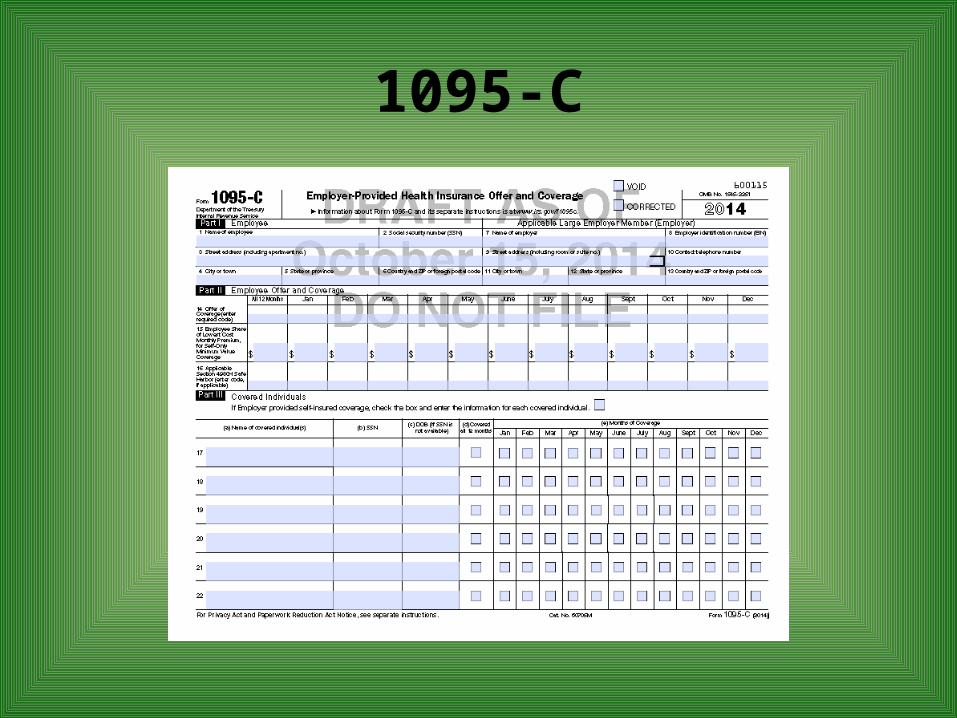

1095-A•Form 1095-A will be used by Health Care Exchanges – web-based health insurance marketplaces. This form will include information such as the level of coverage, identifying information for the primary insured, premiums amounts and advance credit payments for coverage. Other information necessary to determine if a taxpayer has received the appropriate advance credit payments will also be reported on the form. Every month, marketplaces will be required to report to the Department of Health and Human Services, who will in turn report to the IRS.1095-B•Form 1095-B will be provided by the health insurance provider to the individual member in order to report on the type of coverage provided, period of coverage, and for whom coverage was provided– including each dependent.•The health insurance provider will also be required to send a transmittal (1094-B) of coverage information to the IRS. 1095-C•Form 1095-C will be provided by large employers to their employees in order to report on the type of coverage provided as well as identification information for each employee and their dependents.•Large employers will also be required to send a transmittal (1094-C) of coverage information to the IRS.

© 2015 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

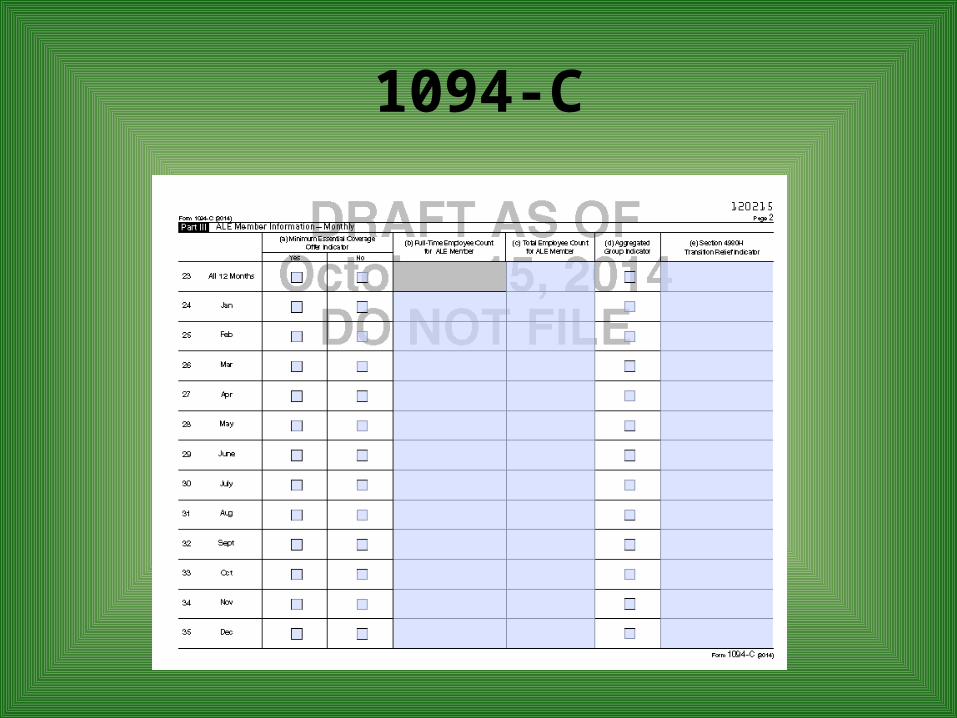

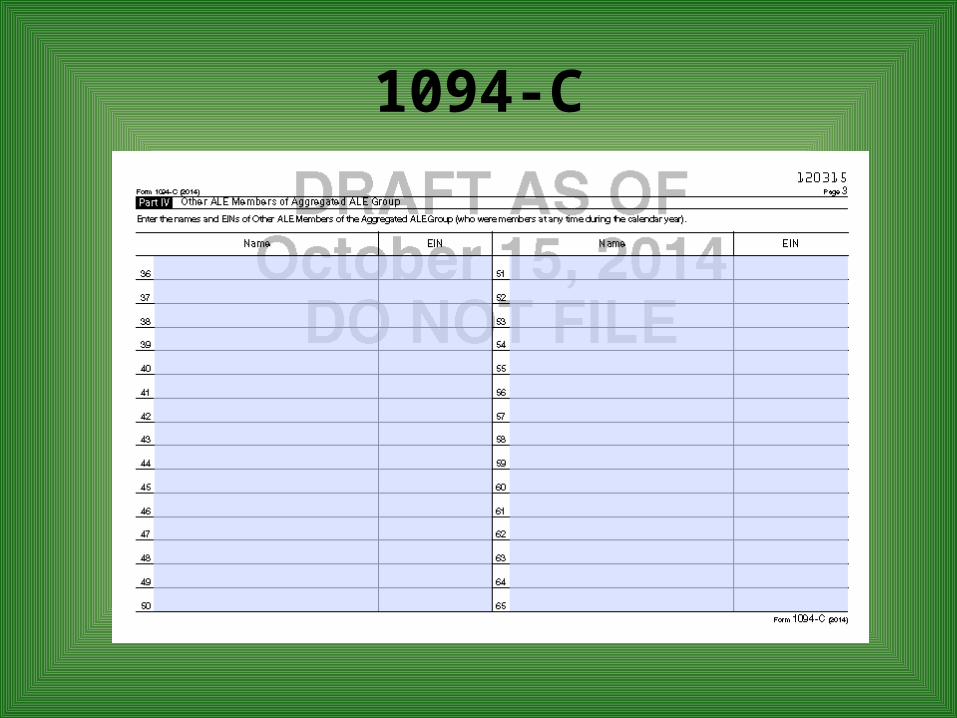

1094-C

1094-C

1094-C

1095-C

WHY IS OUR CHEESE MOVING?

• Commissions are reducing –Minimum loss ratios • 80% in the individual and small

group market (1-99)• 85% in the large group market

(100+)– Many small employers are

canceling their policies

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

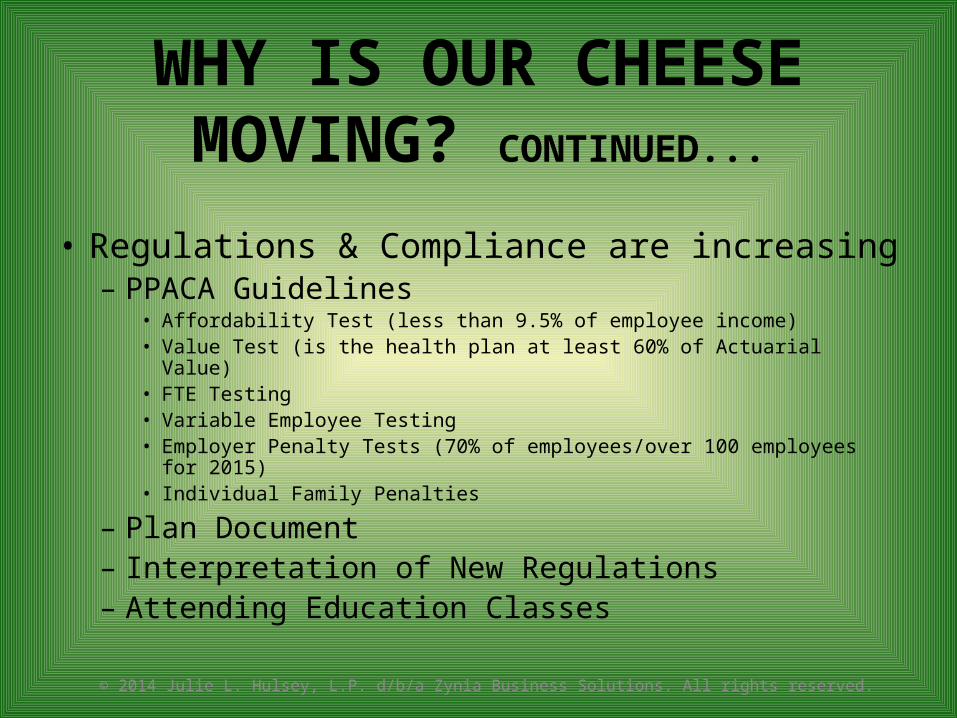

WHY IS OUR CHEESE MOVING? CONTINUED...

• Regulations & Compliance are increasing – PPACA Guidelines

• Affordability Test (less than 9.5% of employee income)• Value Test (is the health plan at least 60% of Actuarial Value)• FTE Testing • Variable Employee Testing • Employer Penalty Tests (70% of employees/over 100 employees for 2015)• Individual Family Penalties

– Plan Document – Interpretation of New Regulations – Attending Education Classes

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

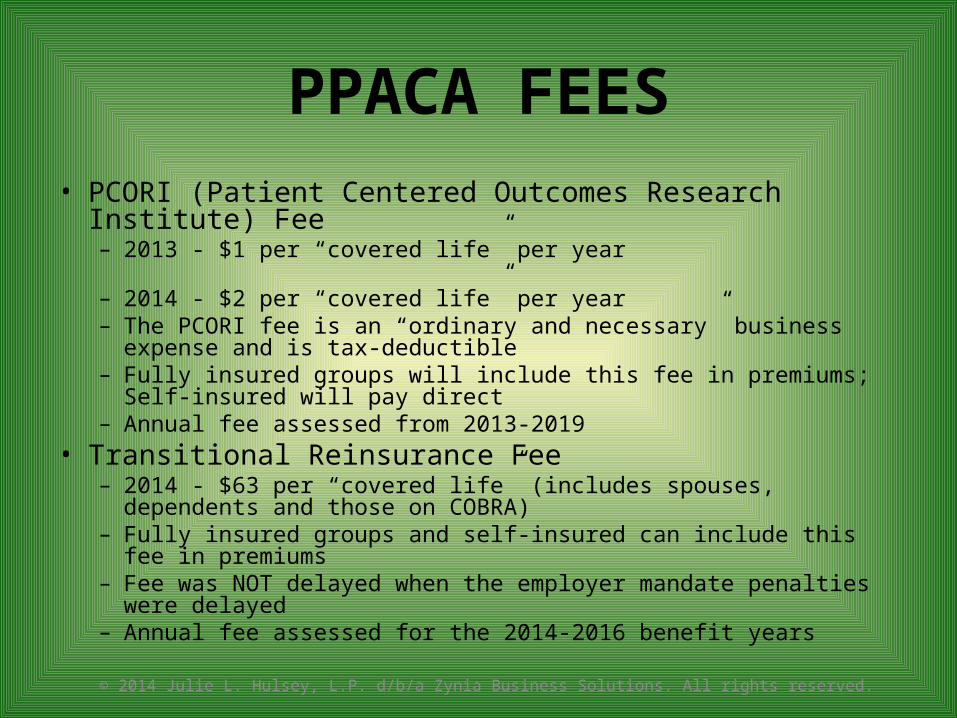

PPACA FEES• PCORI (Patient Centered Outcomes Research Institute) Fee

– 2013 - $1 per “covered life” per year – 2014 - $2 per “covered life” per year– The PCORI fee is an “ordinary and necessary” business expense and is

tax-deductible– Fully insured groups will include this fee in premiums; Self-insured will

pay direct – Annual fee assessed from 2013-2019

• Transitional Reinsurance Fee– 2014 - $63 per “covered life” (includes spouses, dependents and those

on COBRA)– Fully insured groups and self-insured can include this fee in premiums– Fee was NOT delayed when the employer mandate penalties were

delayed– Annual fee assessed for the 2014-2016 benefit years

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

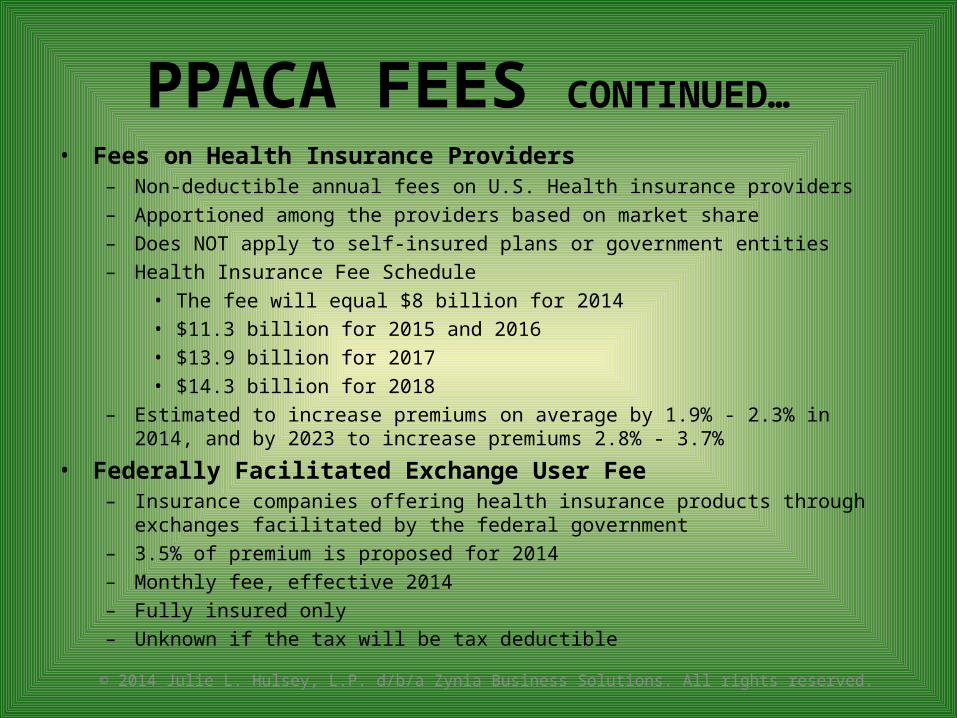

PPACA FEES CONTINUED… • Fees on Health Insurance Providers

– Non-deductible annual fees on U.S. Health insurance providers – Apportioned among the providers based on market share – Does NOT apply to self-insured plans or government entities – Health Insurance Fee Schedule

• The fee will equal $8 billion for 2014 • $11.3 billion for 2015 and 2016• $13.9 billion for 2017 • $14.3 billion for 2018

– Estimated to increase premiums on average by 1.9% - 2.3% in 2014, and by 2023 to increase premiums 2.8% - 3.7%

• Federally Facilitated Exchange User Fee – Insurance companies offering health insurance products through exchanges facilitated by the

federal government – 3.5% of premium is proposed for 2014– Monthly fee, effective 2014 – Fully insured only – Unknown if the tax will be tax deductible

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

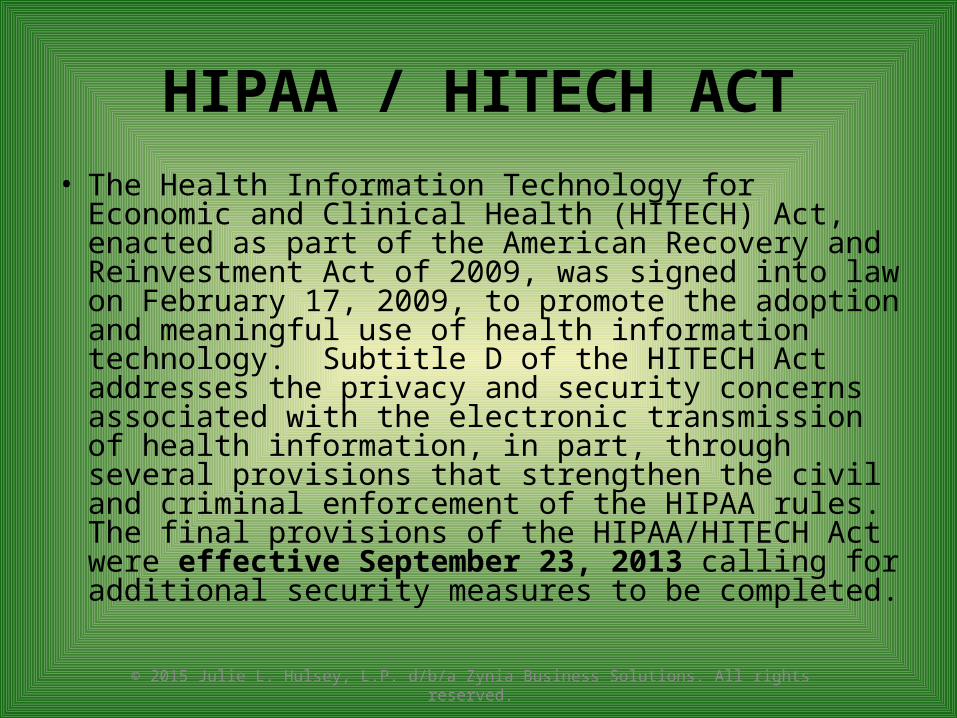

HIPAA / HITECH ACT• The Health Information Technology for Economic and

Clinical Health (HITECH) Act, enacted as part of the American Recovery and Reinvestment Act of 2009, was signed into law on February 17, 2009, to promote the adoption and meaningful use of health information technology. Subtitle D of the HITECH Act addresses the privacy and security concerns associated with the electronic transmission of health information, in part, through several provisions that strengthen the civil and criminal enforcement of the HIPAA rules. The final provisions of the HIPAA/HITECH Act were effective September 23, 2013 calling for additional security measures to be completed.

© 2015 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

BUSINESS ASSOCIATE AGREEMENT

• WHO: Subcontractors (creates, receives, maintains, has exposure to or transmits protected health information on behalf of a Business Associate)

– Cleaning Company, IT Support, Contract Labor• WHY: Compliance– you could be taking on direct liability for their

mistakes– you could jeopardize not only your business

relationships but also expose you to penalties• WHAT: Agreement– have them sign a Subcontractor Business Associate

Agreement

© 2015 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

HOW CAN WE CONTROL OUR CHEESE?

• Cut back our services/overhead and become an order taker

• Add services and expertise - charge a consulting fee

• Think outside the box

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

WHAT ARE YOU DOING TO REPLACE YOUR LOST

COMMISSIONS?

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

Socialized Medicine?

ARE YOUR SMALL EMPLOYEES HURTING FROM AUDITS AND

COMPLIANCE ISSUES?

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

DOL Audits?

WHO ARE YOUR CLIENTS?

• Individuals • Small Employers • Large Employers

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

WHAT NEEDS DO YOUR CLIENTS HAVE?

• Human Resources (HR)• Compliance • Procedures

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

HUMAN RESOURCES (HR)

• Hiring/Firing • Paperwork • Payroll • Scheduling• Training

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

COMPLIANCE

• Plan Document • Safety Manual (OSHA)• COBRA Manual • FMLA Manual • OSHA Log 300• Employee Handbook

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

AUDITS: DOL, IRS & HHS Plan Document Medical Dental Vision Life, Disability and Other Claims Report(s) Employer/Employee Cost Share Breakdown Employee Enrollment Packet

o Employee Choice Formo Summary of Benefits and Coverageo Preventive Fact Sheeto Benefit Applications (e.g. Medical, Dental, Vision, Life, etc.) o Carrier Contact Sheeto Claims & Certificate of Creditable Coverage Procedureso 213(d) Expenses (for HSA plans if applicable)o HIPAA Open Enrollment & Privacy Noticeso Exchange Noticeo COBRA/State Continuation Noticeso CHIPRA Noticeo Newborn & Women’s Cancer Rights Act Noticeso Mental Health Parity Act Notice (if applicable)

COBRA/State Continuation Form 5500

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

PROCEDURES

• HIPAA/HITECH Act• Sexual Harassment Training • Safety Training • Labor Law Posters• PPACA Requirements/Testing• Management Training Classes

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

HOW TO HELP OUR CLIENTS

• Hire HR Expert • Hire Payroll Expert • Expand your Business into HR Consulting • Employer Attorney on Retainer• Hire OSHA Safety Consultant • Hire a Talent Manager• Hire an Expert HRIM System

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

WHY WE DO WHAT WE DO

Think compliance isn’t important?

Think Again….

Typical Fines assessed for simple HR mistakes

Penalty fees for I-9 mistakes range from $110.00 - $1,100.00 per form!

Penalty fees for Wage and Hour mistakes range from $1,000.00 - $500,000.00 per violation!

The Department of Labor has hired 22,000 auditors!

Your business is NOT exempted from the possibility of an Audit!

© 2015 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

DOES THIS KEEP YOUR SMALL EMPLOYERS UP AT NIGHT?

– Recruiting – Job Descriptions – Resume Screening – Develop Interview Guidelines – Background and Reference Checks – Verbal/Written Offer Letter– On-Boarding – Manager/Employee Training – Assistance with Unemployment Hearings– Affirmative Action – Exit Interviews – I-9 Audits

© 2015 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

LETS GET SERIOUS! • HR consulting to include:

– HR Audit – PPACA Compliance Testing – HIPAA Business Associate Agreements – Section 125 POP Document – Plan Document and “DOL Notebook”– Payroll Deduction Audits – Discrimination Testing - Section 105(h)– Administer IRS Letters - Penalties and PPACA Questions – Information for Form 5500, Form 6056 and Form 6055– Assistance with Job Titles and Descriptions – HIPAA Training for Privacy Officers – Interview Process Guidelines – FMLA Information – 50+ Employers – Employee Handbook – New and/or Updated – Employee Exit Packets – OSHA Safety Manual And Meetings – HR Manager Help Line– Recruiting and Staffing Employees

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

HUMAN RESOURCE INFORMATION MANAGEMENT SYSTEM (HRIMS)

• Offer a customized system that will include:– Online Employment Applications– On-Boarding – Employee Benefit Enrollments– Employee Reviews and Warnings – Time Clock and Scheduling – Licensing & Evaluations– PPACA Tracking for Employees Hours and Affordability – COBRA Administration – Payroll

• Price based upon a per employee per month basis • Every employer will have their own website

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

HR STAFF LEASING PROGRAM • Services to Include (partial list)

– Job Descriptions – Resume Screening – Develop Interview Guidelines – Background and Reference Checks – Verbal/Written Offer Letter– On-Boarding – Manager/Employee Training – Assistance with Unemployment Hearings– Affirmative Action – Exit Interviews – I-9 Audits

• Pricing Services– Price based upon per employee per month – Price per Fee Schedule

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

• ERRORS & OMISSIONS POLICY

• LICENSING – LIFE & HEALTH INSURANCE COUNSELORS

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.

QUESTIONS AND ANSWERS Julie L. Hulsey, CLU, LUTCF

Insurance ProfessionalsZynia Business Solutions6601 I-40 West Suite 1

Amarillo, TX 79106(806) 354-8444

Healthcare Reform Certified

© 2014 Julie L. Hulsey, L.P. d/b/a Zynia Business Solutions. All rights reserved.