irs, tax policy and legislative update - ey · pdf fileirs, tax policy and legislative update...

TRANSCRIPT

IRS, Tax policy and legislative update Heather Maloy Nick Giordano Eric Solomon

2

Agenda

► IRS update ► Legislative and tax policy outlook ► Political outlook ► 385 regs

3

IRS update

4

Changing IRS Controversy Landscape Impact on taxpayers

► IRS Budget Challenges ► LB&I Reorganization ► Change in LB&I’s Examination Approach ► Updated LB&I Examination Process

5

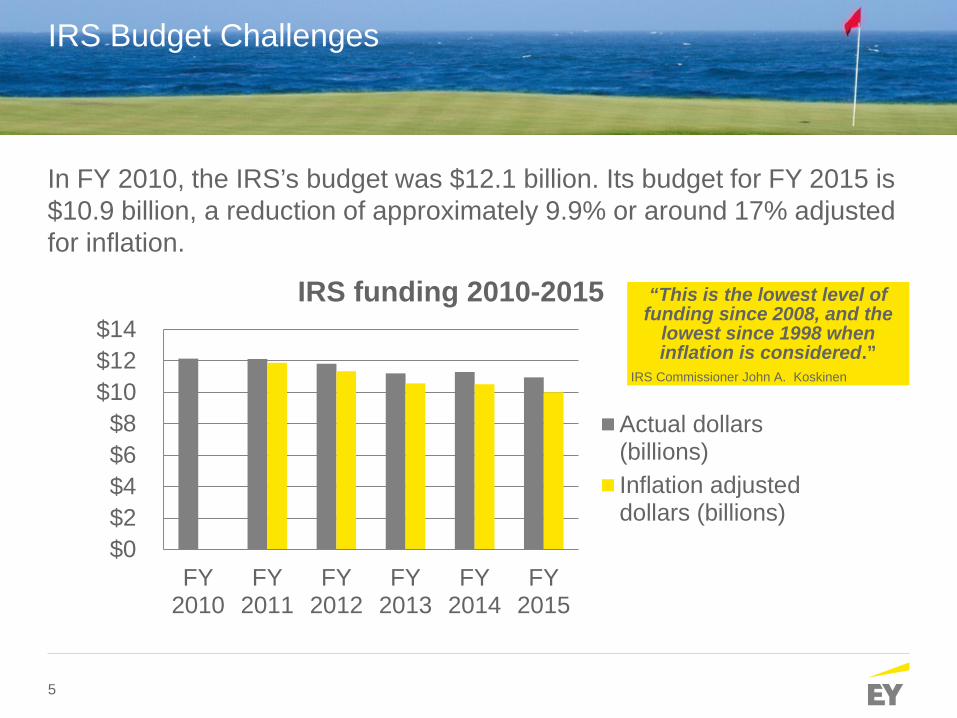

IRS Budget Challenges

In FY 2010, the IRS’s budget was $12.1 billion. Its budget for FY 2015 is $10.9 billion, a reduction of approximately 9.9% or around 17% adjusted for inflation.

$0$2$4$6$8

$10$12$14

FY2010

FY2011

FY2012

FY2013

FY2014

FY2015

IRS funding 2010-2015

Actual dollars(billions)Inflation adjusteddollars (billions)

“This is the lowest level of funding since 2008, and the

lowest since 1998 when inflation is considered.”

IRS Commissioner John A. Koskinen

6

Number of employees down

94,346

91,380

89,551

83,613

78,121

76,540

0 20,000 40,000 60,000 80,000 100,000

Number of full-time equivalents (FTEs) at fiscal year-end

2015

2014

2013

2012

2011

2010

Source; IRS Data Book(s) 2010 -2015, Table 30.

7

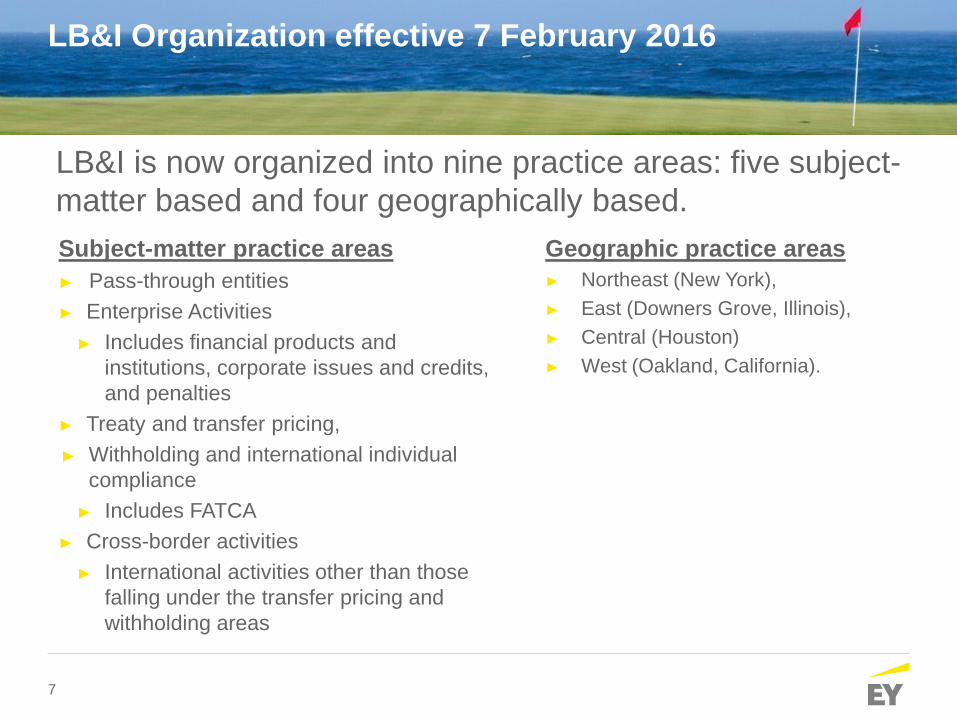

LB&I Organization effective 7 February 2016

LB&I is now organized into nine practice areas: five subject-matter based and four geographically based.

Geographic practice areas ► Northeast (New York), ► East (Downers Grove, Illinois), ► Central (Houston) ► West (Oakland, California).

Subject-matter practice areas ► Pass-through entities ► Enterprise Activities

► Includes financial products and institutions, corporate issues and credits, and penalties

► Treaty and transfer pricing, ► Withholding and international individual

compliance ► Includes FATCA

► Cross-border activities ► International activities other than those

falling under the transfer pricing and withholding areas

8

LB&I Organization Chart

Director of Field Operations

Foreign Payments Practice

Johanna McGeady-Muirphy

LB&I Commissioner

Douglas O’Donnell

Deputy Commissioner Rosemary Sereti

Assistant Deputy Commissioner International

Theodore Setzer

Director Program and Business

Solutions Susan Latham

Director Technology and

Program Solutions Kathryn Greene (A)

Director Resource Solutions

Keith Walker

Assistant Deputy Commissioner Compliance

Integration David Horton

Director Data Mgt.

William Holmes

Director Compliance Planning

and Analytics Christopher Larsen

Director Western Compliance

PA Kimberly Edwards

Director Pass Through Entities

PA Cheryl Claybough

Director Enterprise Activities

PA Kathy Robbins

Director Central Compliance

PA Tina Meaux

Director Cross Border Activities

PA John Hinding

Director Eastern Compliance

PA Lavena Williams

Director Withholding and Int’l Individual Compliance PA

Pamela Drenthe

Director Treaty and Transfer

Pricing Operations PA Sharon Porter

Director Northeastern Compliance

PA Barbara Harris

Director of Field Operations West Don Sniezek (A)

Deputy Director Pass Through

Entities Cliff Scherwinski

Director Financial Institutions and

Products Gloria Sullivan

Director of field Operations North

Central Katheryn Houston

Director of Field Operations East

Orrin Byrd

Director of Field Operations Great Lakes

Steve Whiteaker

Director of Field Operations

Transfer Pricing Practice

Cheryl Teifer

Director of Field Operations

North Atlantic Catherine Jones

Director of Field Operations Southwest Paul Curtis

Promoter Program Financial Products

Director of Field Operations West Jolanta Sander

Director of Field Operations

International Individual

Compliance Elise Gardner

Economists

Director of Field Operations Mid-Atlantic Dennis Figg

Computer Audit Specialists

Global High Wealth

Banks/Insurance/ RICs-REITs-

REMICs

Affordable Care Act

Director Corporate/Credit Holly Paz

Corporate Issues and Credits

Penalties

Engineers

Director of Field Operations

South Central Margie Maxwell (A)

Tax Computation Specialists

Director of Field Operations Southeast

John Hinman (A)

Director Advance Pricing and Mutual

Agreement Hareesh Dhawale

Director Treaty Administration

Deborah Palacheck

Treaty Assistance and Interpretation Team

Exchange of Information

Joint International Tax Shelter

Information Center

Senior Advisor Elizabeth Wagner

9

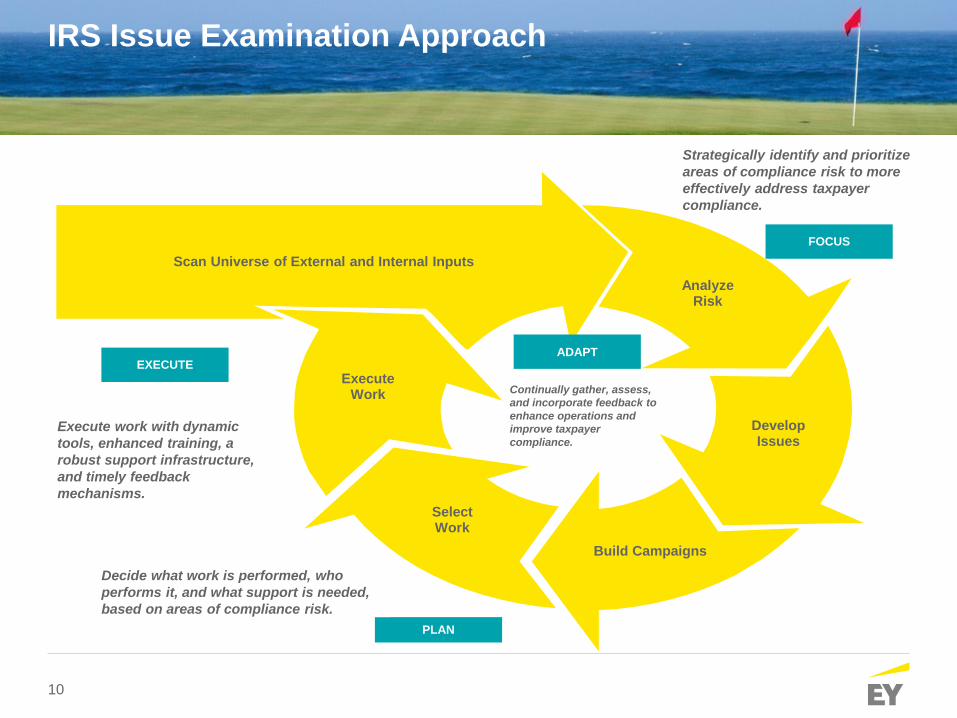

LB&I Shift in Examination Focus

► LB&I is moving to a centralized issue selection and return selection approach over the next few years. ► LB&I seeking to create a more flexible and knowledgeable

workforce, using data analytics to better identify areas of noncompliance, and creating tailored treatments to respond to issues.

► A shift to a centralized issue development process or “campaign” that focuses on how to identify and address compliance risks. ► Campaign-related actions would include development of training

materials, technical positions, and audit aids, among other tools. ► LB&I will generally be moving away from the Coordinated Industry

Case (CIC) approach ► Any potentials changes to the compliance assurance process (CAP)

have yet to be determined

10

Scan Universe of External and Internal Inputs Analyze

Risk

Develop Issues

Build Campaigns

Execute Work

Select Work

FOCUS

PLAN

EXECUTE ADAPT

Strategically identify and prioritize areas of compliance risk to more effectively address taxpayer compliance.

Decide what work is performed, who performs it, and what support is needed, based on areas of compliance risk.

Execute work with dynamic tools, enhanced training, a robust support infrastructure, and timely feedback mechanisms.

Continually gather, assess, and incorporate feedback to enhance operations and improve taxpayer compliance.

IRS Issue Examination Approach

11

New LB&I Examination Process Publication 5125 (February 2016)

► Replaces current “Quality Exam Process” incorporating ► Information Document Request Directive ► Appeals Judicial Approach and Culture

► Updates to IRM 4.46 sections 1-6 issued March 2016. ► Effective for examinations starting as of 1 May 2016. ► For cases in process as of May 1st, transition to the new

process by adopting changes in the Execution and Resolution phases.

https://www.irs.gov/Businesses/Corporations/Large-Business- and-International-Examination-Process

12

LB&I Examination Process

► Expectations for LB&I Examiners ► Expectations for Taxpayers and Representatives ► Informal Claims for Refund ► Issue Driven Examination Process ► Issue Development Model

► Fact Development/Acknowledgement

13

LB&I Examination Process – Resolution

► Issue Resolution Tools ► Consistently encourages available issue resolution tools ► Requires consideration of Fast Track Settlement with Appeals

► Exit Strategy ► Discussions must include efforts to resolve tax controversy for

certainty ► Joint critique of the exam process to recommend improvements ► Address future tax treatment of issues to eliminate

carryover/recurring issues

14

Legislative and tax policy outlook

15

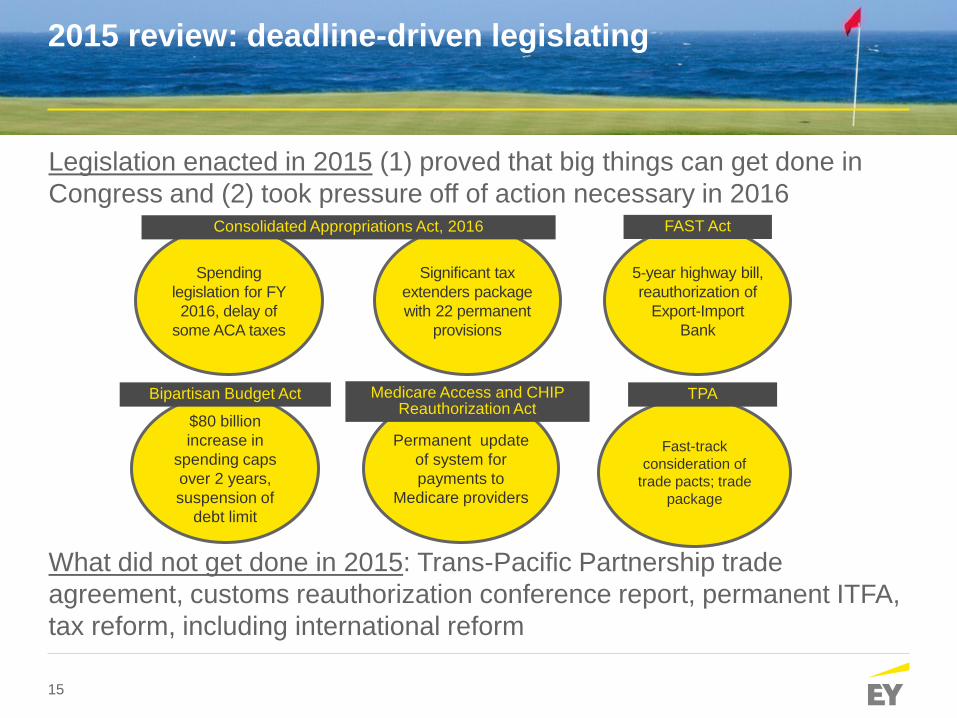

Legislation enacted in 2015 (1) proved that big things can get done in Congress and (2) took pressure off of action necessary in 2016

What did not get done in 2015: Trans-Pacific Partnership trade agreement, customs reauthorization conference report, permanent ITFA, tax reform, including international reform

2015 review: deadline-driven legislating

Spending legislation for FY 2016, delay of

some ACA taxes

Significant tax extenders package with 22 permanent

provisions

5-year highway bill, reauthorization of

Export-Import Bank

Consolidated Appropriations Act, 2016 FAST Act

Fast-track consideration of

trade pacts; trade package

$80 billion increase in

spending caps over 2 years, suspension of

debt limit

Permanent update of system for payments to

Medicare providers

TPA Bipartisan Budget Act Medicare Access and CHIP Reauthorization Act

16

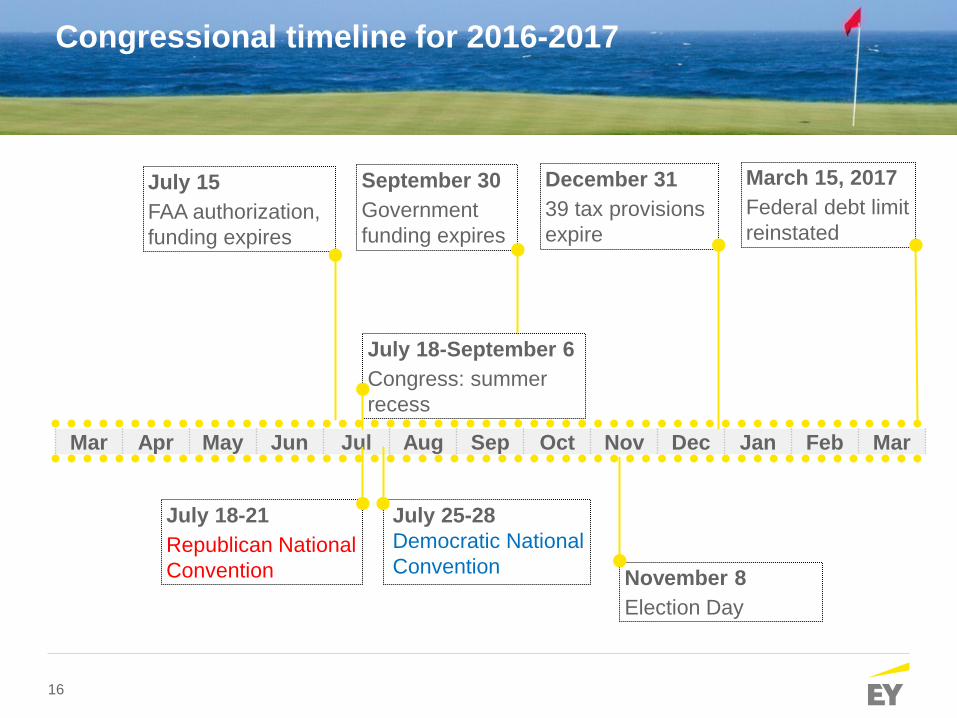

Congressional timeline for 2016-2017

Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

September 30 Government funding expires

July 15 FAA authorization, funding expires

December 31 39 tax provisions expire

March 15, 2017 Federal debt limit reinstated

July 18-21 Republican National Convention November 8

Election Day

July 18-September 6 Congress: summer recess

July 25-28 Democratic National Convention

17

Outlook for 2016: different agendas in House and Senate

House: Develop ideas Republicans can run on in elections ► Speaker Ryan: “For me, 2016 is about going on offense on

ideas…This means putting together a bold, pro-growth agenda.” ► Six committee-led task forces to develop agenda:

Senate: Appropriations a focus, but rest of agenda limited ► Senator McConnell:

► “What we take up in the Senate will be different, with a special eye toward our incumbents.”

► “The House is just better suited to be kind of an idea factory and to pursue things that the Speaker hopes will be picked up by the presidential nominee.”

Tax Reform National Security Health Care

Reform Poverty &

Opportunity Constitutional

Authority Reducing

Regulatory Burdens

18

Miscellaneous 2016 tax policy agenda items

► ID theft/taxpayer protection ► FAA reauthorization ► Puerto Rico relief measure (non-tax and possibly tax) ► 2016 expiring tax provisions ► Technical corrections package ► Tax Treaties (7 plus multilateral convention) ► BEPS/country-by-country reporting regulations/EU public

disclosure ► EU State aid/section 891 ► Panama papers ► Regulatory activity (section 385/anti-inversion items, section

367, etc.)

19

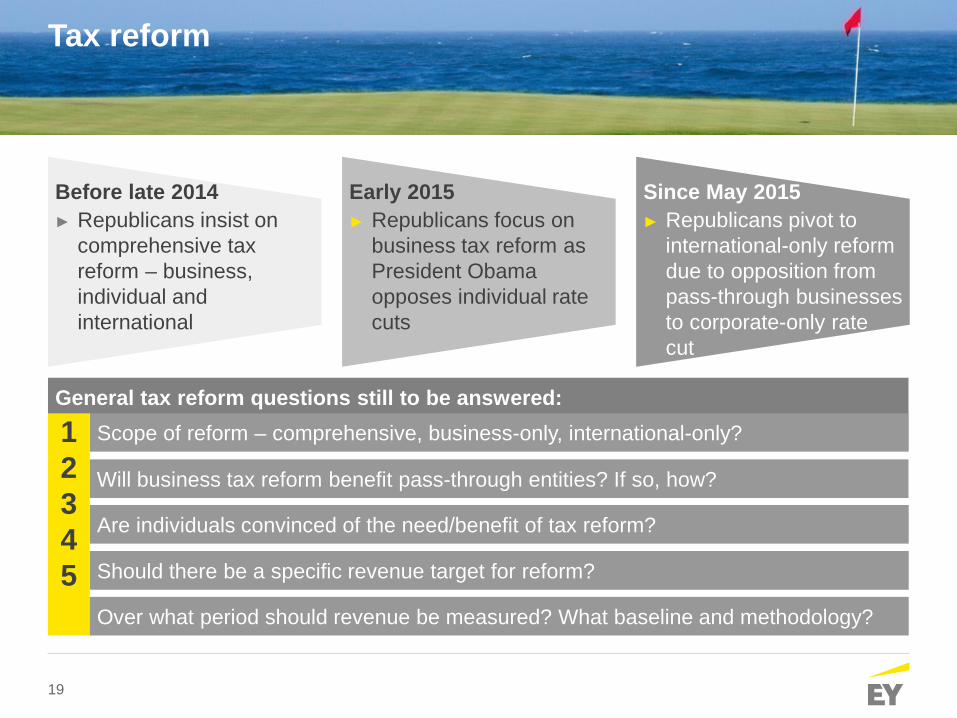

Tax reform

Scope of reform – comprehensive, business-only, international-only?

Will business tax reform benefit pass-through entities? If so, how?

Are individuals convinced of the need/benefit of tax reform? Should there be a specific revenue target for reform?

1 2 3 4 5

General tax reform questions still to be answered:

Before late 2014 ► Republicans insist on

comprehensive tax reform – business, individual and international

Early 2015 ► Republicans focus on

business tax reform as President Obama opposes individual rate cuts

Since May 2015 ► Republicans pivot to

international-only reform due to opposition from pass-through businesses to corporate-only rate cut

Over what period should revenue be measured? What baseline and methodology?

20

Tax reform: latest developments

► Elections and partisan differences make tax reform impossible in 2016

► Speaker Ryan/Chairman Brady will issue “tax reform blueprint” as part of pro-growth agenda, but it is not likely to get a House vote ► Released prior to Republican convention ► Blueprint is more detailed than an outline and less detailed than a bill ► Chairman Brady wants to “leap-frog” on rates, reduce corporate rate to 20% or

less ► Continued interest in international tax reform

► Updated Ways and Means international tax proposal not likely until September or later

► Numerous unresolved technical details including specific anti-base erosion measures and specifics of dividend exemption, innovation box, mandatory tax on foreign earnings, etc.

► Finance Chairman Hatch working on corporate integration proposal

21

Possible elements of international reform legislation

International tax reform has been under discussion by bipartisan members of both the House and Senate. The likely elements include:

Move to a dividend exemption (territorial) system 100% or something less?

Mandatory “deemed” repatriation transition tax on accumulated foreign earnings rate structure? how will revenue be used?

Patent or “innovation” box discounted rate on certain income tied to IP

Minimum tax/anti-base erosion measures for future foreign earnings of multinationals

Some form of interest expense limitation across-the-board or limited to foreign-based companies?

22

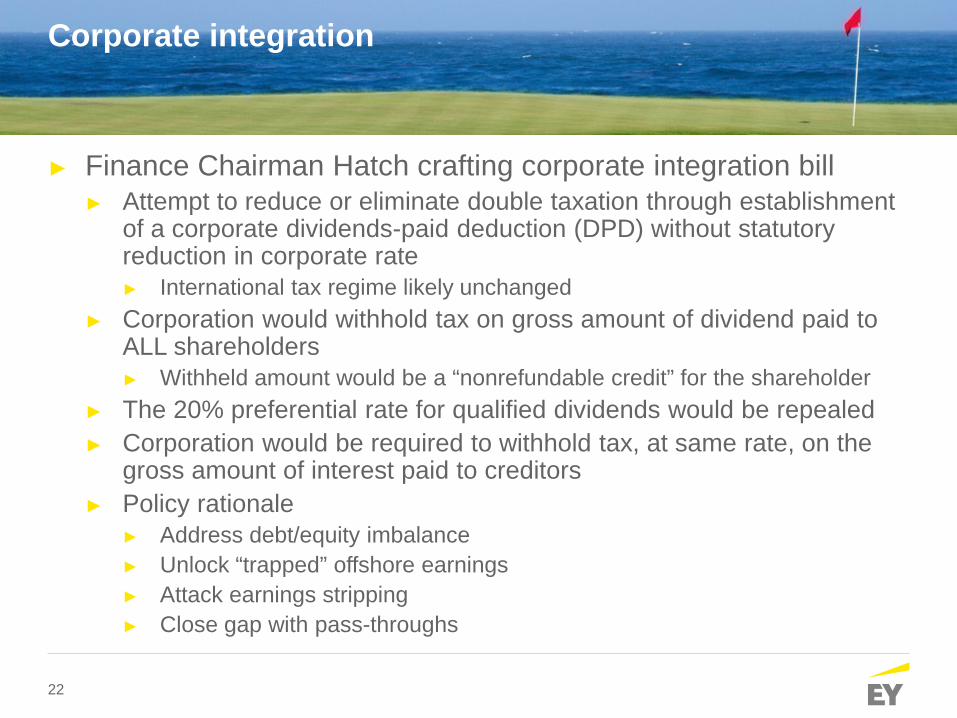

Corporate integration

► Finance Chairman Hatch crafting corporate integration bill ► Attempt to reduce or eliminate double taxation through establishment

of a corporate dividends-paid deduction (DPD) without statutory reduction in corporate rate ► International tax regime likely unchanged

► Corporation would withhold tax on gross amount of dividend paid to ALL shareholders ► Withheld amount would be a “nonrefundable credit” for the shareholder

► The 20% preferential rate for qualified dividends would be repealed ► Corporation would be required to withhold tax, at same rate, on the

gross amount of interest paid to creditors ► Policy rationale

► Address debt/equity imbalance ► Unlock “trapped” offshore earnings ► Attack earnings stripping ► Close gap with pass-throughs

23

Political outlook

24

2016 U.S. elections overview

Currently 54 Republicans, 46 Democratic votes (includes 2 independents) 24 Republican, 10 Democratic seats up for re-election

Presidential Election Day: 8 November 2016

House ► At 246 seats, largest Republican

majority in House since 1930 ► All 435 seats up for re-election ► Likely to stay under Republican

control

Senate ► 54 Republicans, 46 Democrats

(includes 2 independents) ► 24 Republican, 10 Democratic seats

up for re-election ► Control up for grabs

25

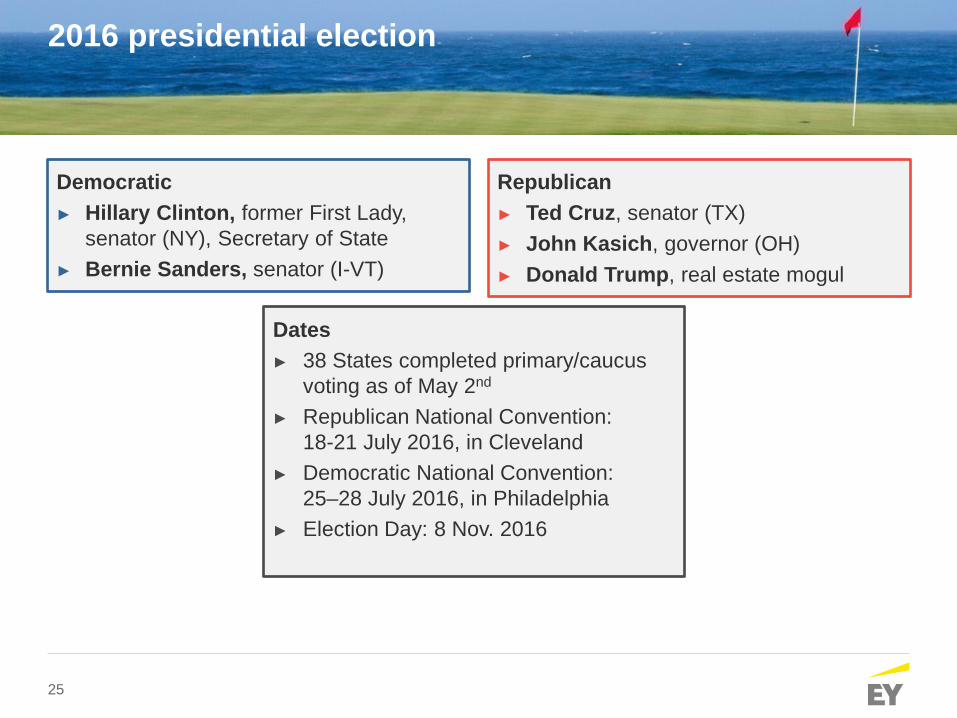

2016 presidential election

Democratic ► Hillary Clinton, former First Lady,

senator (NY), Secretary of State ► Bernie Sanders, senator (I-VT)

Republican ► Ted Cruz, senator (TX) ► John Kasich, governor (OH) ► Donald Trump, real estate mogul

Dates ► 38 States completed primary/caucus

voting as of May 2nd ► Republican National Convention:

18-21 July 2016, in Cleveland ► Democratic National Convention:

25–28 July 2016, in Philadelphia ► Election Day: 8 Nov. 2016

26

0

200

400

600

800

1000

1200

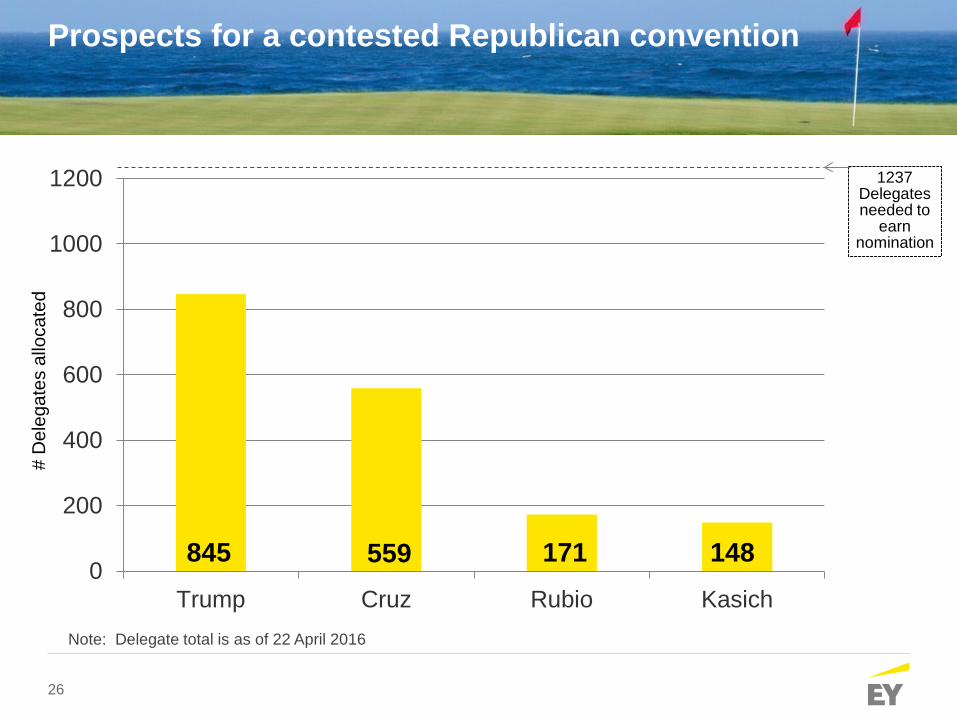

Trump Cruz Rubio Kasich

148 171

Prospects for a contested Republican convention

1237 Delegates needed to

earn nomination

# D

eleg

ates

allo

cate

d

845 559

Note: Delegate total is as of 22 April 2016

27

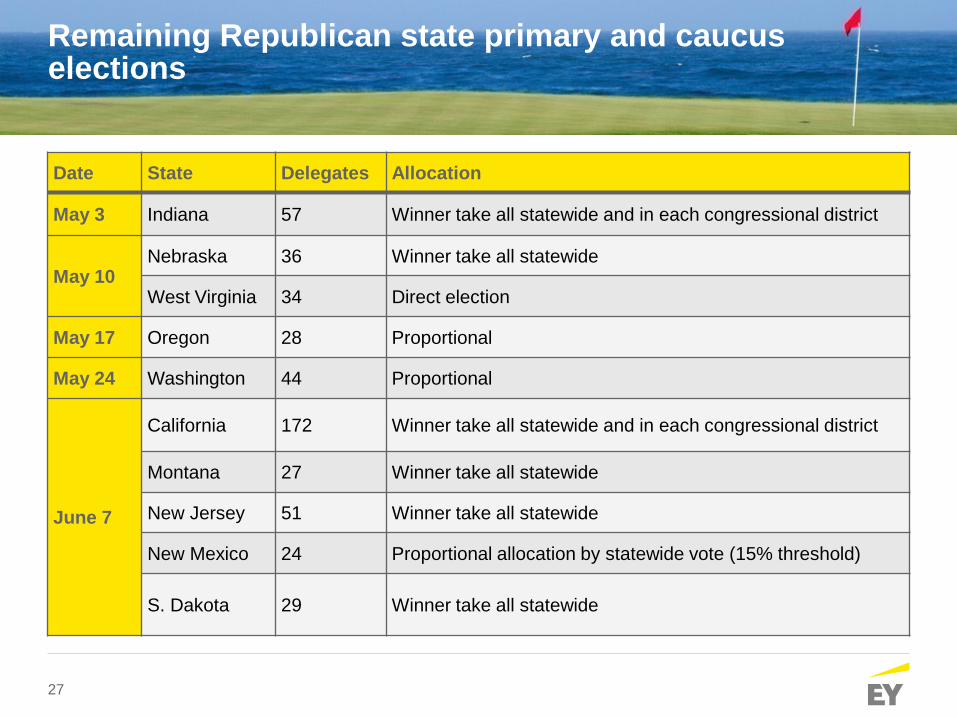

Remaining Republican state primary and caucus elections

Date State Delegates Allocation

May 3 Indiana 57 Winner take all statewide and in each congressional district

May 10 Nebraska 36 Winner take all statewide

West Virginia 34 Direct election

May 17 Oregon 28 Proportional

May 24 Washington 44 Proportional

June 7

California 172 Winner take all statewide and in each congressional district

Montana 27 Winner take all statewide

New Jersey 51 Winner take all statewide

New Mexico 24 Proportional allocation by statewide vote (15% threshold)

S. Dakota 29 Winner take all statewide

28

Congressional profile, 114th congress

Senate, 114th congress House, 114th congress

54 / 46*

* Includes 2 independents

246* / 188

*1 vacancy: Boehner (R-OH), election June 7

24 Republican, 10 Democratic seats up for re-election in 2016

► Majority Leader: Mitch McConnell (R-KY) ► Majority Whip: John Cornyn (R-TX) ► Republican Conference Chair: John Thune

(R-SD) ► Democratic leader: Harry Reid (D-NV) ► Democratic Whip: Dick Durbin (D-IL) ► Democratic Conference Vice Chair: Chuck

Schumer (D-NY) ► Strategic policy adviser to the DPCC:

Elizabeth Warren (D-MA)

At 246 seats, currently largest Republican majority in House since 1930

► Speaker Paul Ryan (R-WI) ► Majority Leader: Kevin McCarthy (R-CA) ► Majority Whip: Steve Scalise (R-LA) ► Democratic leader: Nancy Pelosi (D-CA) ► Democratic Whip: Steny Hoyer (D-MD) ► Asst. Democratic Leader: James Clyburn

(D-SC)

Republicans Democrats Republicans Democrats

29

2016 Senate elections

Seats up for re-election: 24 Republican, 10 Democratic Democrats Republicans ► Michael Bennet (D-CO) ► R. Blumenthal (D-CT) ► Barbara Boxer (D-CA)

retiring ► Pat Leahy (D-VT) ► Barbara Mikulski (D-MD)

retiring ► Patty Murray (D-WA) ► Harry Reid (D-NV) retiring ► Brian Schatz (D-HI) ► Chuck Schumer (D-NY) ► Ron Wyden (D-OR)

► Kelly Ayotte (R-NH) ► Roy Blunt (R-MO) ► John Boozman (R-AR) ► Richard Burr (R-NC) ► Daniel Coats (R-IN) retiring ► Mike Crapo (R-ID) ► Chuck Grassley (R-IA) ► John Hoeven (R-ND) ► Johnny Isakson (R-GA) ► Ron Johnson (R-WI) ► Mark Kirk (R-IL) ► James Lankford (R-OK) ► Mike Lee (R-UT)

► John McCain (R-AZ) ► Jerry Moran (R-KS) ► Lisa Murkowski (R-AK) ► Rand Paul (R-KY) ► Rob Portman (R-OH) ► Marco Rubio (R-FL) retiring

due to presidential run ► Tim Scott (R-SC) ► Richard Shelby (R-AL) ► John Thune (R-SD) ► Pat Toomey (R-PA) ► David Vitter (R-LA)

= state won by President Obama in 2012 presidential election

30

First major piece of legislation recent presidents enacted after taking office

Barack Obama Took office January 20, 2009

American Recovery and Reinvestment Act of 2009 Enacted February 17, 2009 - Stimulus legislation, included bonus depreciation

George W. Bush Took office January 20, 2001

Economic Growth and Tax Relief Reconciliation Act of 2001 Enacted June 7, 2001 - The “Bush tax cuts” reduced individual rates, estate tax

Bill Clinton Took office January 20, 1993

Omnibus Budget Reconciliation Act of 1993 Enacted August 10,1993 - Increased individual, corporate taxes

George H. W. Bush Took office January 20, 1989

Omnibus Budget Reconciliation Act of 1990 Enacted November 5,1990 - Increased individual taxes despite ‘no new tax’ pledge

Ronald Reagan Took office January 20, 1981

Economic Recovery Tax Act of 1981 Enacted August 13, 1981 - Sharply reduced individual, corporate taxes

31

Appendix

32

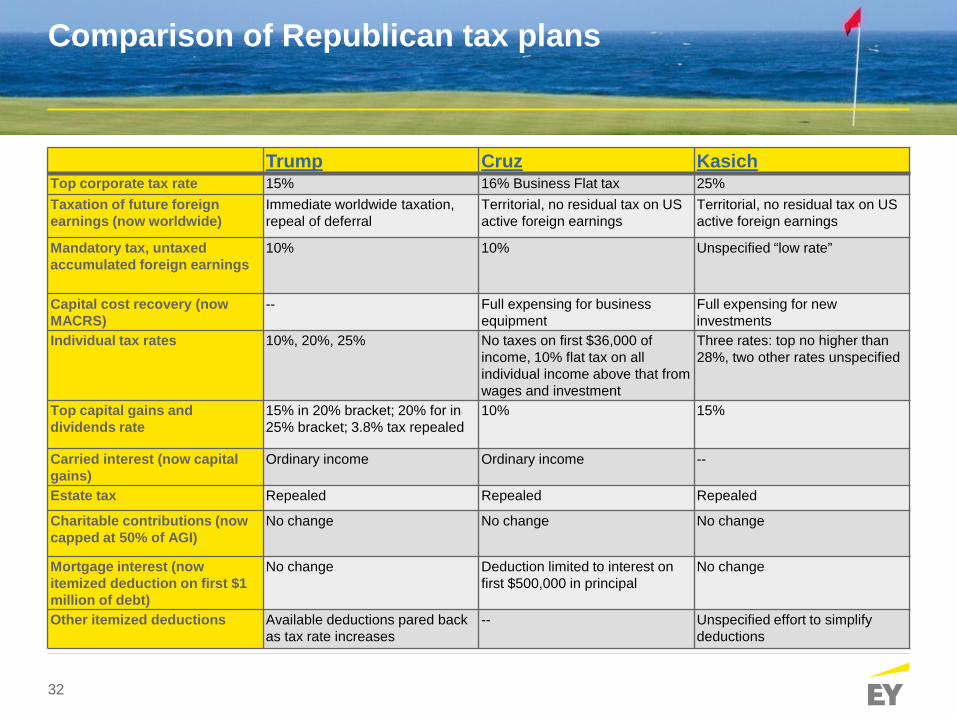

Comparison of Republican tax plans

Trump Cruz Kasich Top corporate tax rate 15% 16% Business Flat tax 25% Taxation of future foreign earnings (now worldwide)

Immediate worldwide taxation, repeal of deferral

Territorial, no residual tax on US active foreign earnings

Territorial, no residual tax on US active foreign earnings

Mandatory tax, untaxed accumulated foreign earnings

10% 10% Unspecified “low rate”

Capital cost recovery (now MACRS)

-- Full expensing for business equipment

Full expensing for new investments

Individual tax rates 10%, 20%, 25% No taxes on first $36,000 of income, 10% flat tax on all individual income above that from wages and investment

Three rates: top no higher than 28%, two other rates unspecified

Top capital gains and dividends rate

15% in 20% bracket; 20% for in 25% bracket; 3.8% tax repealed

10% 15%

Carried interest (now capital gains)

Ordinary income Ordinary income --

Estate tax Repealed Repealed Repealed

Charitable contributions (now capped at 50% of AGI)

No change No change No change

Mortgage interest (now itemized deduction on first $1 million of debt)

No change Deduction limited to interest on first $500,000 in principal

No change

Other itemized deductions Available deductions pared back as tax rate increases

--

Unspecified effort to simplify deductions

33

Clinton vs. Sanders: two approaches to increasing taxes on individuals

Clinton

► Buffett Rule = minimum 30% effective tax rate for millionaires

► 4% Fair Share Surcharge on annual income over $5 million

► Increase capital gains rates: ► Assets held less than 2 years taxed as

ordinary income ► 23.8% capital gains rate on assets held 6

or more years

► Carried interest = ordinary income Tax on high-frequency trading

► Limit the tax value of specified deductions and exclusions to 28%

► Return to 2009 estate tax regime

Sanders ► Surtaxes above current 28% bracket

► 9%-24%, so top rate = 52%

► New 2.2% surtax on taxable income ► Lift payroll tax cap and increase payroll

tax by 0.2% ► Tax capital gains as ordinary income for

those above current 28% bracket ► Carried interest = ordinary income ► Financial Transaction Tax on each

security trade ► Limit tax value of deductions, exclusions

to 30.2% ► Repeal PEP and Pease ► Reduce estate tax exemption threshold

and increase rates

34

Comparison of candidates’ tax plan estimates

-$15

-$12

-$9

-$6

-$3

$0

$3

$6

$9

$12

$15

Sources: Citizens for Tax Justice (CTJ), Tax Policy Center (TPC), and Tax Foundation (TF) estimates. The three organizations estimate slightly different policies, so are not strictly comparable.

Trillions of dollars, 10-year

Rev

enue

gai

n or

loss

Tax Foundation (Static)

Tax Foundation (Dynamic)

Tax Policy Center

Citizens for Tax Justice

Cruz Trump

Clinton Sanders

-$10.1

-$12

-$9.5

-$12

-$0.8

-$3.6

-$8.6

-$13.9

$0.5 $1.1

$0.5 $0.2

$9.8

$13.6

$15.3

$13

35

Proposed Section 385 Regulations

36

Section 385 and its History

► Section 385(a) authorizes the Secretary to prescribe such regulations as may be necessary or appropriate to determine whether an interest in a corporation is treated as stock or indebtedness (in whole or in part) for purposes of the Code.

► Section 385(b) provides that the regulations prescribed under section 385 shall set forth factors to be taken into account in determining whether an interest in a corporation is stock or indebtedness. Section 385(b) identifies certain factors that may be taken into account for this purpose, which generally track the case law.

► Section 385 was amended in 1989 and 1992.

► Section 385(a) was amended in 1989 to expressly authorize the Secretary to issue regulations to treat an interest in a corporation as part stock and part indebtedness.

► Section 385(c) was added in 1992 to provide that the issuer’s characterization (as of the time of issuance) of an interest in a corporation as stock or indebtedness is binding on the issuer and on all holders of the interest (but not on the Secretary).

37

Purpose of Proposed Regulations

► The proposed section 385 regulations address whether an interest in a related corporation is treated as stock or indebtedness, or as in part stock or in part indebtedness, for all purposes of the Code.

► Although the proposed regulations were partially motivated by the enhanced incentives for related parties to create “excessive” indebtedness in the cross-border context, the proposed regulations go far beyond earnings stripping and apply to a wide range of common internal transactions.

► The proposed regulations do not apply to issuances of interests and related transactions among members of a consolidated group.

38

High-level Summary

► §1.385-1: General definitions; IRS has ability to split an instrument into part-debt and part-equity

► §1.385-2: Documentation requirements

► §1.385-3: Debt issued in, or to fund, the following transactions:

Distributions Certain acquisitions of “EG” stock Boot in a reorg

► §1.385-4: Consolidated group issues ► Members of a consolidated group generally treated as one corporation ► Prop. Reg. §1.385-4 provides rules addressing when an interest

• Ceases to be a consolidated group debt instrument; or • Becomes a consolidated group debt instrument

39

Prop. Reg. §1.385-2(b): Documentation and Information Requirements

► Subject to certain exceptions, an expanded group instrument (“EGI”) is treated as stock if certain threshold documentation and information is not prepared and/or maintained. ► Exceptions apply to an expanded group with assets and revenues below certain

thresholds or with no members with stock traded on an established market. ► An EGI is a debt instrument issued by a member of an expanded group that is held

by another member of that expanded group. ► What is considered a “debt instrument”?

► The term “expanded group” means an affiliated group as defined in section 1504(a), but with the following modifications: ► includes foreign and tax-exempt corporations ► includes corporations held directly OR indirectly (through application of section

304(c)(3)) ► modifies the ownership test to 80 percent of the vote OR value (instead of 80

percent of vote AND value).

► Documentation rules effective when regulations are finalized

40

Prop. Reg. §1.385-2(b): Documentation and Information Requirements (cont’d)

► The documentation and information must satisfy the following four requirements: 1. Binding obligation to repay funds advanced under Prop. Reg. §1.385-

2(b)(2)(i): ► Written documentation which establishes that the issuer has entered into an

unconditional and legally binding obligation to pay a sum certain on demand at one or more fixed dates.

2. Creditor’s rights to enforce terms of the debt under Prop. Reg. §1.385-2(b)(2)(ii): ► The written documentation must establish that the holder has the rights of a

creditor to enforce the obligation.

► These creditor’s rights typically include the right to trigger default or acceleration of the instrument for non-payment of interest or principal, and these rights must include a superior right to shareholders to share in the assets of the issuer in case of dissolution

41

Prop. Reg. §1.385-2(b): Documentation and Information Requirements (cont’d)

3. Reasonable expectation that funds can be repaid under Prop. Reg. §1.385-2(b)(2)(iii); and ► Written documentation that establishes the issuer’s financial position supported a

reasonable expectation that the issuer intended to, and would be able to, meet its obligations pursuant to the terms of the applicable instrument.

► E.g., cash flow projections, financial statements, business forecasts, determinations of debt-to-equity and other relevant financial ratios of the issuer in relation to industry averages, and other information regarding the sources of funds enabling the issuer to meet its obligations pursuant to the terms of the applicable instrument.

4. Actions evidencing a genuine creditor-debtor relationship under Prop. Reg. §1.385-2(b)(2)(iv). ► Evidence of payments of principal and interest which could include a wire transfer or bank

statement proving payment;

► In the event of a default or similar type event, written documentation evidencing the holder’s reasonable exercise of the diligence and judgment of a creditor; e.g., evidence of the holder’s efforts to assert its rights, the parties’ efforts to renegotiate the debt, mitigate the breach, or change any material terms, and any documentation detailing the holder’s decision to refrain from pursuing any actions to enforce payment.

42

Prop. Reg. §1.385-2(b): Documentation and Information Requirements (cont’d)

► Observations and considerations regarding documentation requirements ► The 4 documentation requirements must also be met for “revolving credit

agreements” and “cash pooling arrangements” ► The documentation requirements must be met at the time the “facility” is first

established (i.e., the relevant date) ► The documentation related to the first 3 requirements must be prepared no later than 30

days after the relevant date ► The documentation related to the 4th requirement must be prepared no later than 120 days

after the relevant date ► Appears that the “facility” must have a maximum “draw down” amount or each

“draw down” will be treated as a separate loan subject to separate documentation requirements

► How will taxpayers meet the 4 requirements for routine cash pooling arrangements? – e.g,. What processes need to be in place to satisfy requirement #3 for every draw down? ► Material documentation governing ongoing operations of cash pooling arrangements must

be maintained for EGI’s issued pursuant to the arrangement ► What are we advising clients to do now?

43

Prop. Reg. §1.385-2(b): Documentation and Information Requirements (cont’d)

► Even once the 4 documentation requirements are satisfied, general tax principles will apply to determine whether, and to what extent, an interest is debt

► The documentation and information on prior slides must be maintained for all taxable years that the expanded group instrument is outstanding, and until the period of limitations expires for any return with respect to which the treatment of the instrument is relevant.

► Debt instruments that are re-characterized as equity under §1.385 will be characterized based on the terms of the instrument.

► What are the effects of the re-characterization?

44

Prop. Reg. §1.385-3(b)(2): General Rule

► Assuming a debt instrument is not already recharacterized pursuant to the documentation requirement under §1.385-2 or based on a determination under general tax principles pursuant to §1.385-1(d) or §1.385-2(a)(1), then, subject to certain exceptions, it is treated as stock for all federal tax purposes to the extent it is issued by a corporation to a member of its expanded group, ► In a distribution with respect to its stock; ► In exchange for stock of a member of the same expanded group (“expanded group

stock”) (including “hook stock” issued by a related corporate shareholder), other than in an exempt exchange; or

► In exchange for property in an asset reorganization to the extent that, pursuant to the plan of reorganization, the debt instrument is received as “boot” by a corporation that is a shareholder of the target corporation and a member of the issuer’s expanded group immediately before the reorganization.

► An exempt exchange means an acquisition of expanded group stock in which the transferor and transferee of the stock are parties to an asset reorganization, and either ► Section 361(a) or (b) applies to the transferor of the expanded group stock and the

stock is not transferred by issuance; or ► Section 1032 or §1.1032-2 applies to the transferor of the expanded group stock

and the stock is distributed by the transferee pursuant to the plan of reorganization.

45

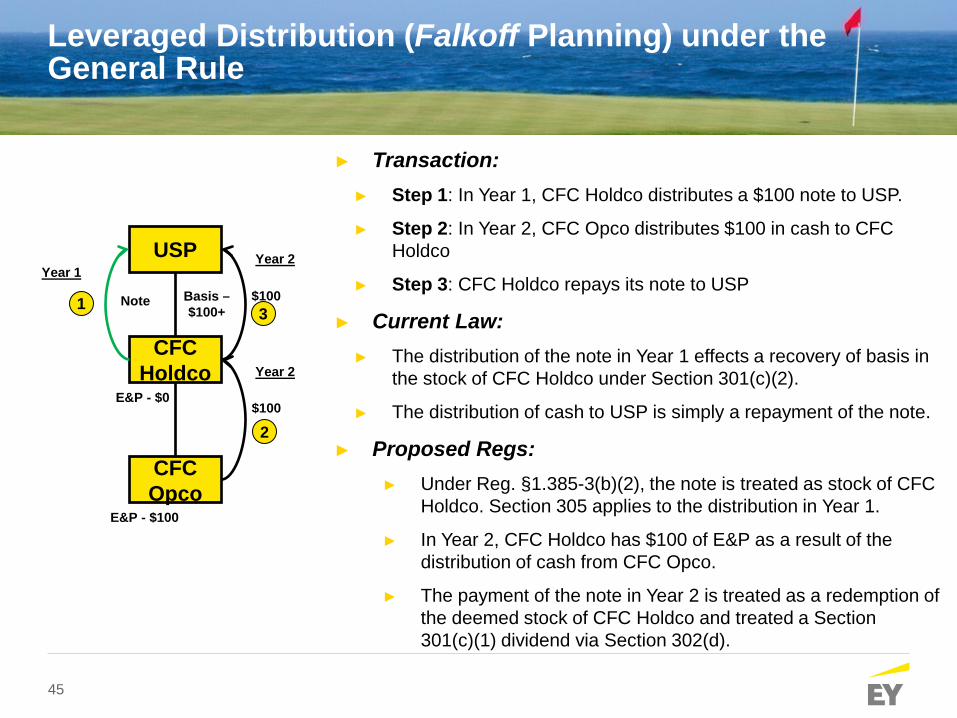

Leveraged Distribution (Falkoff Planning) under the General Rule

USP

CFC Holdco

CFC Opco

Basis – $100+

Note

E&P - $0

E&P - $100

$100

$100

Year 1 Year 2

► Transaction: ► Step 1: In Year 1, CFC Holdco distributes a $100 note to USP.

► Step 2: In Year 2, CFC Opco distributes $100 in cash to CFC Holdco

► Step 3: CFC Holdco repays its note to USP

► Current Law: ► The distribution of the note in Year 1 effects a recovery of basis in

the stock of CFC Holdco under Section 301(c)(2).

► The distribution of cash to USP is simply a repayment of the note.

► Proposed Regs: ► Under Reg. §1.385-3(b)(2), the note is treated as stock of CFC

Holdco. Section 305 applies to the distribution in Year 1.

► In Year 2, CFC Holdco has $100 of E&P as a result of the distribution of cash from CFC Opco.

► The payment of the note in Year 2 is treated as a redemption of the deemed stock of CFC Holdco and treated a Section 301(c)(1) dividend via Section 302(d).

Year 2

1

2

3

46

CFC CFC

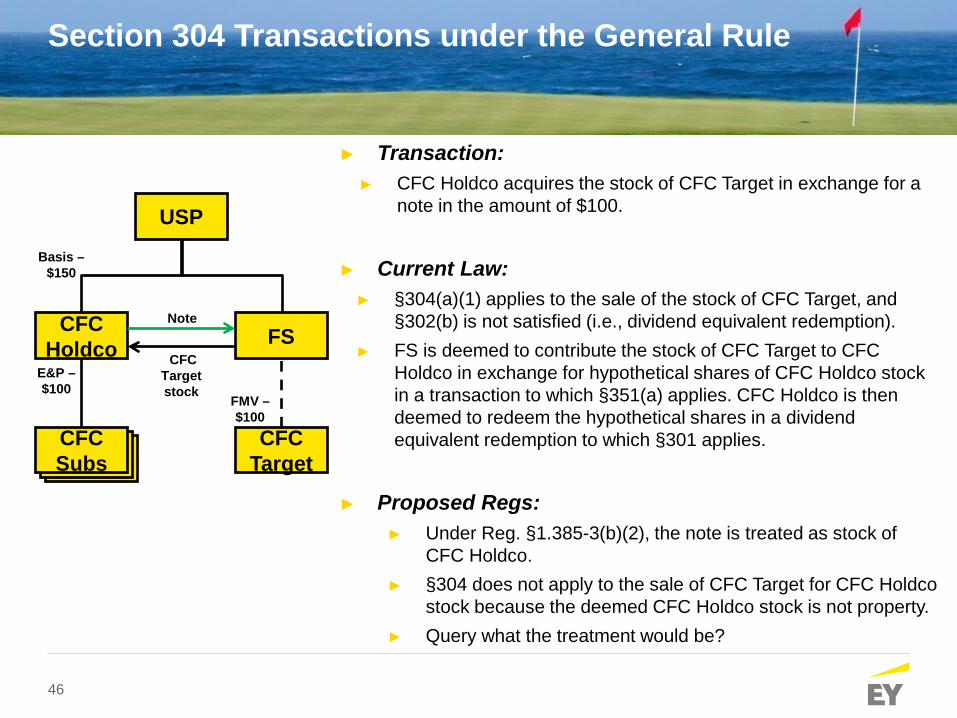

Section 304 Transactions under the General Rule

USP

CFC Holdco FS

CFC Subs

CFC Target

CFC Target stock

Note

E&P – $100

Basis – $150

FMV – $100

► Transaction: ► CFC Holdco acquires the stock of CFC Target in exchange for a

note in the amount of $100.

► Current Law:

► §304(a)(1) applies to the sale of the stock of CFC Target, and §302(b) is not satisfied (i.e., dividend equivalent redemption).

► FS is deemed to contribute the stock of CFC Target to CFC Holdco in exchange for hypothetical shares of CFC Holdco stock in a transaction to which §351(a) applies. CFC Holdco is then deemed to redeem the hypothetical shares in a dividend equivalent redemption to which §301 applies.

► Proposed Regs:

► Under Reg. §1.385-3(b)(2), the note is treated as stock of CFC Holdco.

► §304 does not apply to the sale of CFC Target for CFC Holdco stock because the deemed CFC Holdco stock is not property.

► Query what the treatment would be?

47

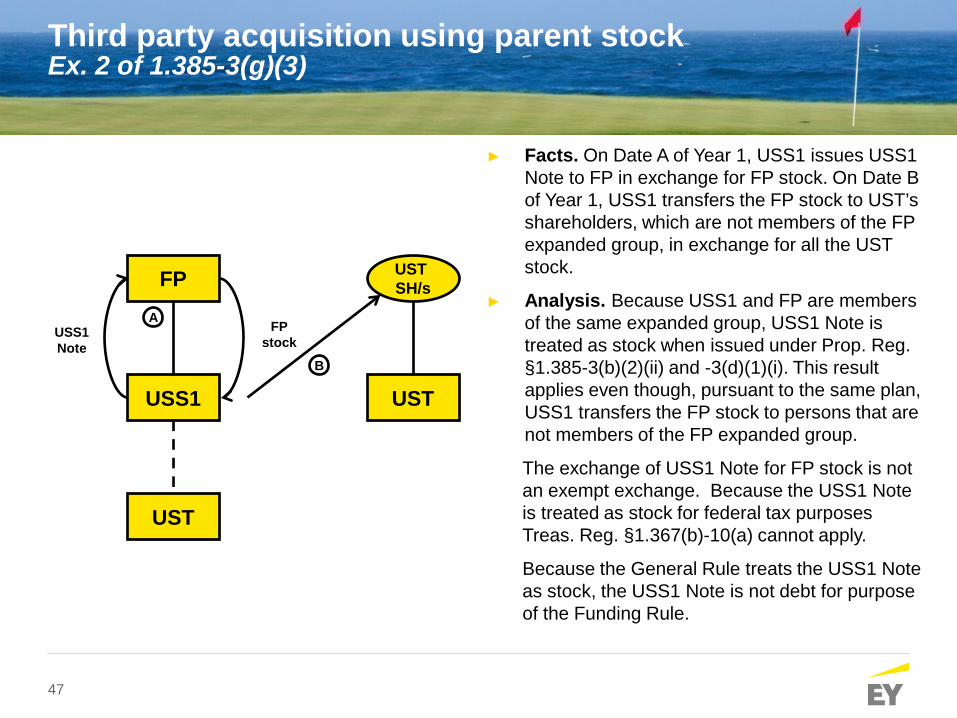

Third party acquisition using parent stock Ex. 2 of 1.385-3(g)(3)

► Facts. On Date A of Year 1, USS1 issues USS1 Note to FP in exchange for FP stock. On Date B of Year 1, USS1 transfers the FP stock to UST’s shareholders, which are not members of the FP expanded group, in exchange for all the UST stock.

► Analysis. Because USS1 and FP are members of the same expanded group, USS1 Note is treated as stock when issued under Prop. Reg. §1.385-3(b)(2)(ii) and -3(d)(1)(i). This result applies even though, pursuant to the same plan, USS1 transfers the FP stock to persons that are not members of the FP expanded group.

The exchange of USS1 Note for FP stock is not an exempt exchange. Because the USS1 Note is treated as stock for federal tax purposes Treas. Reg. §1.367(b)-10(a) cannot apply.

Because the General Rule treats the USS1 Note as stock, the USS1 Note is not debt for purpose of the Funding Rule.

FP

USS1 UST

USS1 Note

FP stock

UST SH/s

A

B

UST

48

Prop. Reg. §1.385-3(b)(3): Funding Rule

► Subject to certain exceptions, a debt instrument is treated as stock to the extent it is issued by a corporation (funded member) to a member of its expanded group in exchange for property with a principal purpose of funding (a “principal purpose debt instrument”),

► A distribution of property by the funded member to a member of its expanded group, other than a distribution of stock pursuant to an asset reorganization that is permitted to be received without the recognition of gain or income under section 354(a)(1) or 355(a)(1), or that is not treated as “boot” under section 356;

► An acquisition of expanded group stock, other than in an exempt exchange, by the funded member from a member of its expanded group in exchange for property other than expanded group stock; or

► An acquisition of property by the funded member in an asset reorganization to the extent that, pursuant to the plan of reorganization, a corporation that is a shareholder of the target corporation and a member of the funded member’s expanded group immediately before the reorganization receives “boot” with respect to its stock in the target in the reorganization.

49

Prop. Reg. §1.385-3(b)(3): Funding Rule

► Whether a debt instrument is a principal purpose debt instrument is determined based on all facts and circumstances, whether the instrument is issued prior to or after a distribution or acquisition.

► Per se treatment: Subject to an “ordinary course exception,” a debt instrument is treated as a principal debt instrument if it is issued during the period beginning 36 months before the date of a relevant distribution or acquisition, and ending 36 months after the date of the relevant distribution or acquisition (72-month period).

► Ordinary Course Exception: The “Per-Se Treatment” does not apply to a debt instrument that arises in the ordinary course of the issuer’s trade or business in connection with the purchase of property or the receipt of services to the extent that it reflects an obligation to pay an amount that is currently deductible by the issuer under section 162 or currently included in the issuer’s cost of goods sold or inventory, provided that the amount of the obligation outstanding at no time exceeds the amount that would be ordinary and necessary to carry on the trade or business of the issuer if it was unrelated to the lender.

► Rules are provided to coordinate the application of the Funding Rule when multiple debt instruments may be treated as principal purpose debt instruments, or when a debt instrument may be treated as funding more than one distribution or acquisition.

50

Leveraged Distribution under the Funding Rule

USP

CFC Holdco

CFC Opco

Basis – $150

E&P - $0

E&P - $100

$100

$100

Year 1

Year 2

► Transaction: ► Step 1: In Year 1, CFC Holdco borrows $100 from CFC

Finco in exchange for a note. ► Step 2: In Year 1, CFC Holdco distributes the proceeds to

USP. ► Step 3: In Year 2, CFC Opco distributes $100 in cash to

CFC Holdco. ► Step 4: CFC Holdco uses the cash to repay the note to

CFC Finco.

► Current Law: ► The distribution in Year 1 effects a recovery of basis in the

stock of CFC Holdco under Section 301(c)(2).

► Proposed Regs: ► Under Reg. §1.385-3(b)(3), the note is treated as stock

of CFC Holdco. ► The distribution of the loan proceeds in Year 1 effects

a recovery of basis in the stock of CFC Holdco under Section 301(c)(2).

► Consider the consequences to CFC Finco on repayment of the note – e.g., Section 302 redemption? FTC consequences? E&P consequences?

CFC Finco

Note Year 1

Year 2

$100

$100

2 1

4 4

51

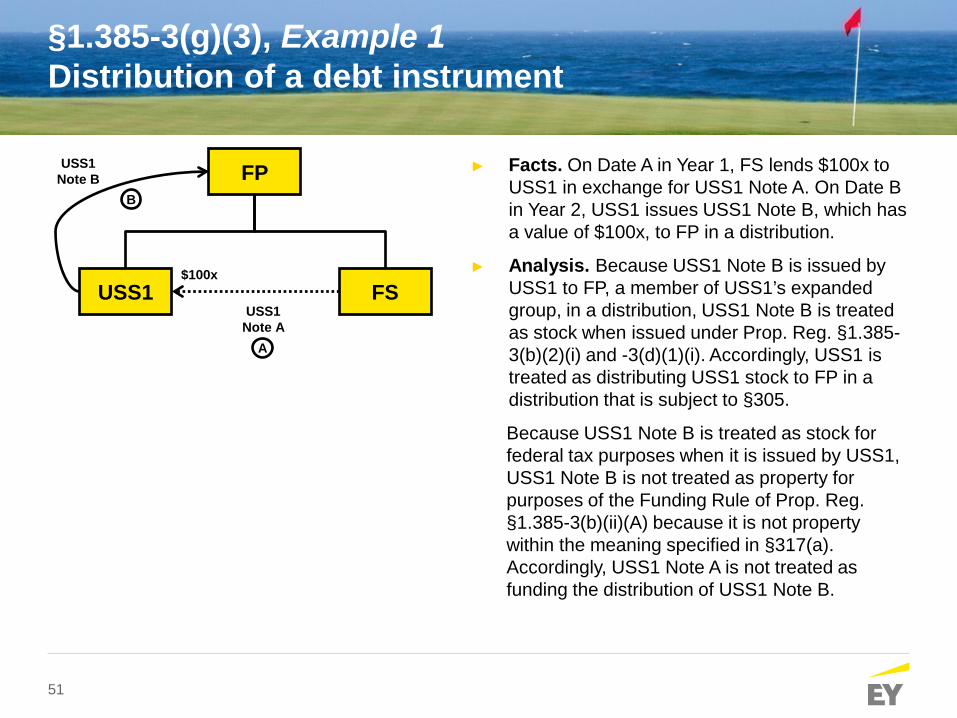

§1.385-3(g)(3), Example 1 Distribution of a debt instrument

► Facts. On Date A in Year 1, FS lends $100x to USS1 in exchange for USS1 Note A. On Date B in Year 2, USS1 issues USS1 Note B, which has a value of $100x, to FP in a distribution.

► Analysis. Because USS1 Note B is issued by USS1 to FP, a member of USS1’s expanded group, in a distribution, USS1 Note B is treated as stock when issued under Prop. Reg. §1.385-3(b)(2)(i) and -3(d)(1)(i). Accordingly, USS1 is treated as distributing USS1 stock to FP in a distribution that is subject to §305.

Because USS1 Note B is treated as stock for federal tax purposes when it is issued by USS1, USS1 Note B is not treated as property for purposes of the Funding Rule of Prop. Reg. §1.385-3(b)(ii)(A) because it is not property within the meaning specified in §317(a). Accordingly, USS1 Note A is not treated as funding the distribution of USS1 Note B.

FP

USS1 FS $100x

USS1 Note B

B

A

USS1 Note A

52

Prop. Reg. §1.385-3: Exceptions to the General Rule and the Funding Rule

► Current E&P Reduction: For purposes of applying the General Rule and the Funding Rule with respect to a taxable year to a member of an expanded group, the aggregate amount of any distributions or acquisitions described in the General Rule and the Funding Rule are reduced by an amount equal to the member’s current E&P. Multiple distributions or acquisitions are reduced based on the order in which they occur.

► Threshold Exception: A debt instrument is not treated as stock if, immediately after the debt instrument is issued, the aggregate adjusted issue price of debt instruments held by members of the expanded group that would otherwise be treated as stock does not exceed $50 million. If this limitation is exceeded, the limitation will not apply to any additional debt instruments issued by the expanded group so long as any debt instrument that is treated as debt by reason of this exception remains outstanding.

► Funded Acquisitions of Subsidiary Stock by Issuance: An acquisition of expanded group stock will not be taken into account for purposes of the Funding Rule if the acquisition results from a transfer of property by a funded member (the transferor) to an expanded group member (the issuer) in exchange for stock of the issuer, provided that, for the 36-month period immediately following the issuance, the transferor holds, directly or indirectly, more than 50 percent of the total combined voting power of all classes of stock of the issuer entitled to vote and more than 50 percent of the total value of the stock of the issuer.

53

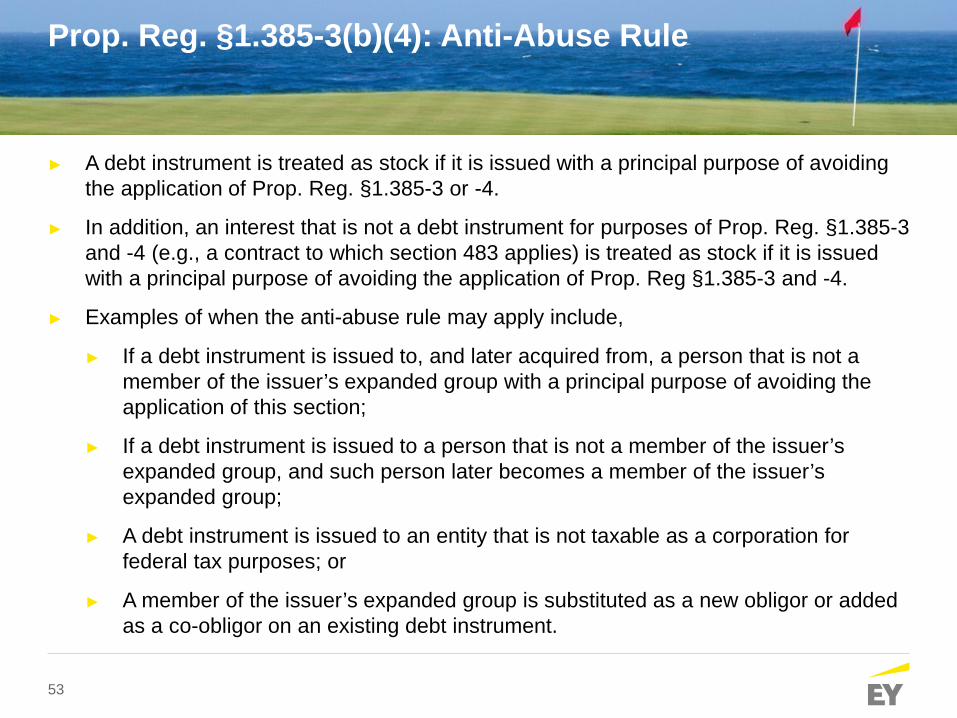

Prop. Reg. §1.385-3(b)(4): Anti-Abuse Rule

► A debt instrument is treated as stock if it is issued with a principal purpose of avoiding the application of Prop. Reg. §1.385-3 or -4.

► In addition, an interest that is not a debt instrument for purposes of Prop. Reg. §1.385-3 and -4 (e.g., a contract to which section 483 applies) is treated as stock if it is issued with a principal purpose of avoiding the application of Prop. Reg §1.385-3 and -4.

► Examples of when the anti-abuse rule may apply include,

► If a debt instrument is issued to, and later acquired from, a person that is not a member of the issuer’s expanded group with a principal purpose of avoiding the application of this section;

► If a debt instrument is issued to a person that is not a member of the issuer’s expanded group, and such person later becomes a member of the issuer’s expanded group;

► A debt instrument is issued to an entity that is not taxable as a corporation for federal tax purposes; or

► A member of the issuer’s expanded group is substituted as a new obligor or added as a co-obligor on an existing debt instrument.

54

Springing “receivables”

USP ► Transaction:

► Step 1: DRE checks-the-box to be treated as a corporation (Sub) ► At the time of the CTB election, DRE has a $100

loan owing from CFC

► Proposed Regs: ► CFC treated as issuing a $100 loan to Sub in exchange

for Sub stock ► Is this an acquisition of EG stock? ► If so, CFC loan becomes equity in CFC held by Sub ► What is Sub’s basis in CFC stock

► Compare to result if CFC contributed loan receivable under current law (see, e.g, RR 68-629, Perachi, Lessinger)

► Consequences when CFC “repays” loan? ► Consequences if USP later contributes property to CFC?

CFC

DRE Receivable

Payable

$100 1

USP

CFC

Sub

55

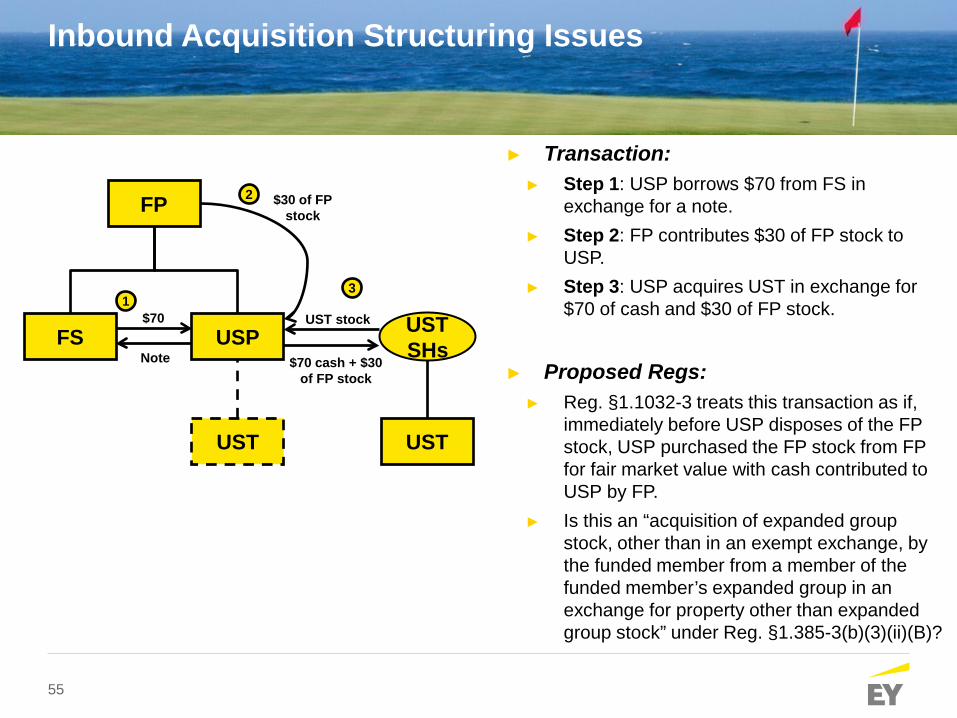

Inbound Acquisition Structuring Issues

FP

FS USP

UST

$30 of FP stock

► Transaction: ► Step 1: USP borrows $70 from FS in

exchange for a note. ► Step 2: FP contributes $30 of FP stock to

USP. ► Step 3: USP acquires UST in exchange for

$70 of cash and $30 of FP stock.

► Proposed Regs:

► Reg. §1.1032-3 treats this transaction as if, immediately before USP disposes of the FP stock, USP purchased the FP stock from FP for fair market value with cash contributed to USP by FP.

► Is this an “acquisition of expanded group stock, other than in an exempt exchange, by the funded member from a member of the funded member’s expanded group in an exchange for property other than expanded group stock” under Reg. §1.385-3(b)(3)(ii)(B)?

$70

Note

2

3 1

UST SHs

UST

$70 cash + $30 of FP stock

UST stock

56

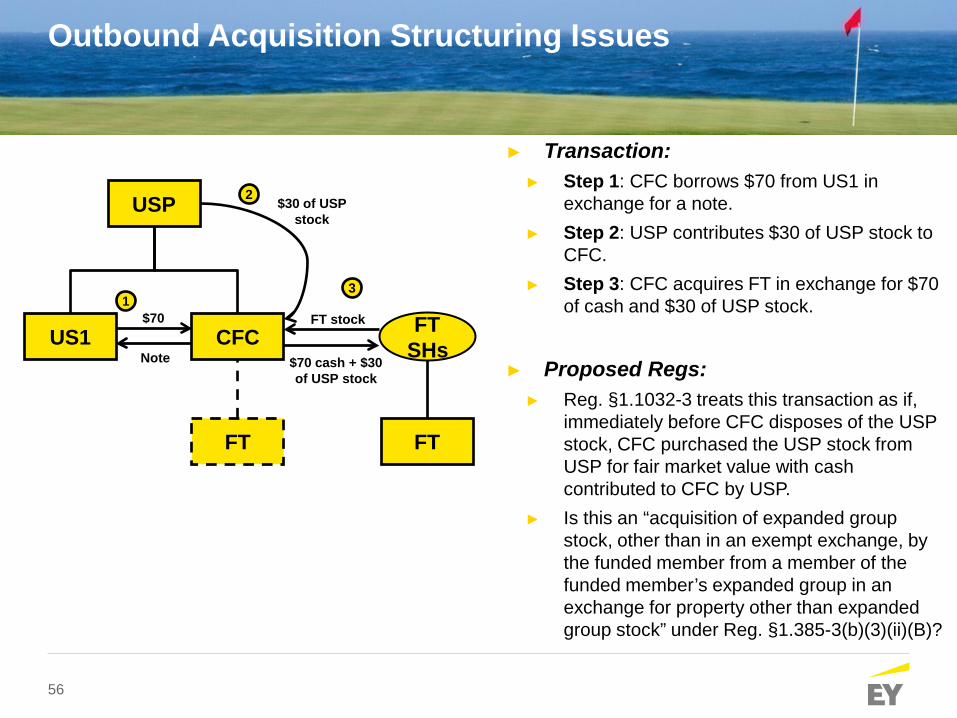

Outbound Acquisition Structuring Issues

USP

US1 CFC

FT

$30 of USP stock

► Transaction: ► Step 1: CFC borrows $70 from US1 in

exchange for a note. ► Step 2: USP contributes $30 of USP stock to

CFC. ► Step 3: CFC acquires FT in exchange for $70

of cash and $30 of USP stock.

► Proposed Regs:

► Reg. §1.1032-3 treats this transaction as if, immediately before CFC disposes of the USP stock, CFC purchased the USP stock from USP for fair market value with cash contributed to CFC by USP.

► Is this an “acquisition of expanded group stock, other than in an exempt exchange, by the funded member from a member of the funded member’s expanded group in an exchange for property other than expanded group stock” under Reg. §1.385-3(b)(3)(ii)(B)?

$70

Note

2

3 1

FT SHs

FT

$70 cash + $30 of USP stock

FT stock

57

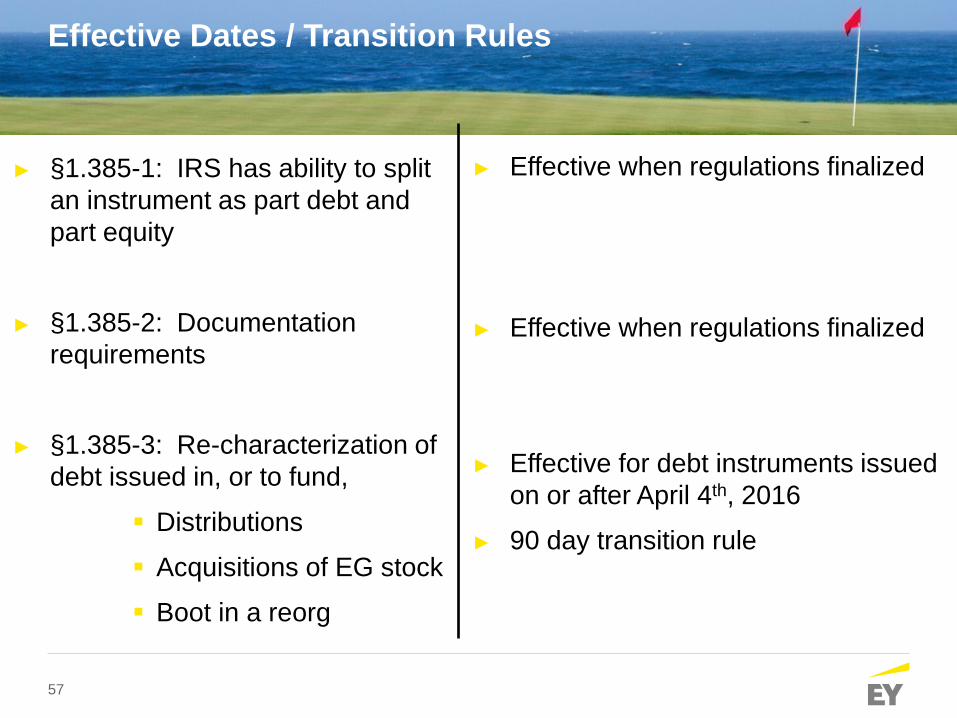

Effective Dates / Transition Rules

► §1.385-1: IRS has ability to split an instrument as part debt and part equity

► §1.385-2: Documentation requirements

► §1.385-3: Re-characterization of debt issued in, or to fund,

Distributions

Acquisitions of EG stock

Boot in a reorg

► Effective when regulations finalized

► Effective when regulations finalized

► Effective for debt instruments issued on or after April 4th, 2016

► 90 day transition rule