iron harbor roundtable_debt & deleveraging

TRANSCRIPT

Iron Harbor Capital Management

IPI Roundtable Discussion

The End of an Era: The Consequences of Debt and Deleveraging

Spring, 2015

Global debt-to-GDP has sharply expanded…

1

Source: ICMB Geneva Reports

Figure A.1: Total debt of private non-financial sector +39 ppt since 2007Global debt ex-financials (% of GDP)

1.60

1.70

1.80

1.90

2.00

2.10

2.20

2001 2003 2005 2007 2009 2011 2013

• Since 2007, global debt-to-GDP +39ppt

• The equivalent of $49 trillion

• Global GDP grew by $18 trillion

…and financial leverage is at all-time highs

2

Source: World Bank, ICMB Geneva Reports, Iron Harbor Calculations

Figure A.2: Marginal utility of debt is diminishingGlobal total debt (ex-financials), global nominal GDP

20

50

80

110

140

170

200

230

260

2001 2003 2005 2007 2009 2011 2013

Global debt

Global nominal GDP• 2002 – 2007:

• Annualized debt +12.0%• Annualized GDP +10.8%

• 2008 – 2013:• Annualized debt +7.0%• Annualized GDP +3.8%

• Deleveraging would have required GDP x 2

Inflexibility of debt creates vulnerabilities

3

Figure A.3: Gap between debt and GDP growth worseningGlobal total debt ex-financials/GDP normalized (2001)

0.90

1.40

1.90

2.40

2.90

3.40

2001 2003 2005 2007 2009 2011 2013

Global GDP

Global debt

Source: World Bank, ICMB Geneva Reports, Iron Harbor Calculations

• Nominal GDP is comprised of:• Real GDP• Inflation

• Debt is debt…inflexible

• Service costs will increase when Fed hikes

Worsening labor force dynamics are a global trend

4

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

1950 1970 1990 2010 2030 2050

US

Japan

Figure A.4: Lower inverse dependency ratio means lower demand for…Inverse dependency ratio

Figure A.5: …financial services and real assets.Inverse dependency ratio

Source: UN Dept of Economic and Social Affairs Source: UN Dept of Economic and Social Affairs

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

2.60

2.80

3.00

1950 1970 1990 2010 2030 2050

China

BRICS

EU-15

The twin peaks of demographics…

5

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

US

Japan

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

Spain

Ireland

Figure A.4: Housing is an important component of global GDPInverse dependency ratio

Figure A.6: For 50 years, demographic trend supported demandInverse dependency ratio

Source: UN Dept of Economic and Social Affairs Source: UN Dept of Economic and Social Affairs

…and demand for housing…

6

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

1950 1970 1990 2010 2030 2050

US

Japan

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

1950 1970 1990 2010 2030 2050

Spain

Ireland

Figure A.4: Now that the demographic trend has reversed…Inverse dependency ratio

Figure A.6: …a secular decline in housing is likely.Inverse dependency ratio

Source: UN Dept of Economic and Social Affairs Source: UN Dept of Economic and Social Affairs

Peak of Japanese property bubble

ca 1990

Peak of US sub-prime bubble

ca 2007+

Peak of Irish property bubble

ca 2006+

Peak of Spanish property bubble

ca 2008

…darken the BRICS outlook

7

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

2.60

2.80

3.00

1950 1970 1990 2010 2030 2050

China

BRICS

EU-15

Figure A.5: After 30 years, will continuing changes in 1-child policy…Inverse dependency ratio

Source: UN Dept of Economic and Social Affairs

China working age population peaked in 2012

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

1973 1983 1993 2003 2013

Employed persons 5yma % YoY

Figure A.7: …be sufficient to reverse the trend?Year-on-year change in employed persons

Source: Conference Board, Iron Harbor’s calculation

Global trend is lower for productivity

8

-2.00

0.00

2.00

4.00

6.00

8.00

1973 1983 1993 2003 2013

Japan

Germany

US

-10.00

-5.00

0.00

5.00

10.00

15.00

1973 1983 1993 2003 2013

China

India

Brazil

Figure A.8: Labor productivity in secular decline in G-7…Labor productivity per person employed

Figure A.9: …and could be taking hold in the BRICSLabor productivity per person employed

Source: Conference Board, Iron Harbor’s calculation Source: Conference Board, Iron Harbor’s calculation

13

The relentless increase of debt dependency

Causes of the debt supercycle?Among the advanced economies alone, the ratio of debt-to-GDP has risen from 167%in 1980 to 314% in 2011, or by an average of more than five percentage points of GDPper year over the past three decades. Should we be worried?

Policymaker inattention1. Prior to 2008, credit and debt dynamics were not a meaningful part of

policymaking frameworks.2. Focus on the real economy has not been sufficient to avoid serious

macroeconomic problems.

Monetary policy asymmetry1. Monetary policy does not “lean” against the booms, but eases aggressively and

persistently during busts.2. This induces a downward bias in interest rates and an upward bias in debt levels.

Cost of debt financing1. Implicit incentives can make debt more appealing2. Low policy rates -> low debt service payments -> debt more affordable

Unconventional Policy1. QE & forward guidance…triggering search for yield2. Global asset managers are leading the charge

The rate bias of policy implementation has been lower

12

Figure B.1: Policy asymmetry produces a bias for lower ratesOfficial monetary policy rate, total central government debt

Source: Bloomberg

0

5

10

15

20

25

30

0

2

4

6

8

10

12

14

16

18

20

1980 1984 1988 1992 1996 2000 2004 2008

Total central gov't debt

FED

BOE

BOC• Monetary policy has drifted steadily lower

• Globalization a contributor

• Greenspan ‘put’ reveals inherent rate bias

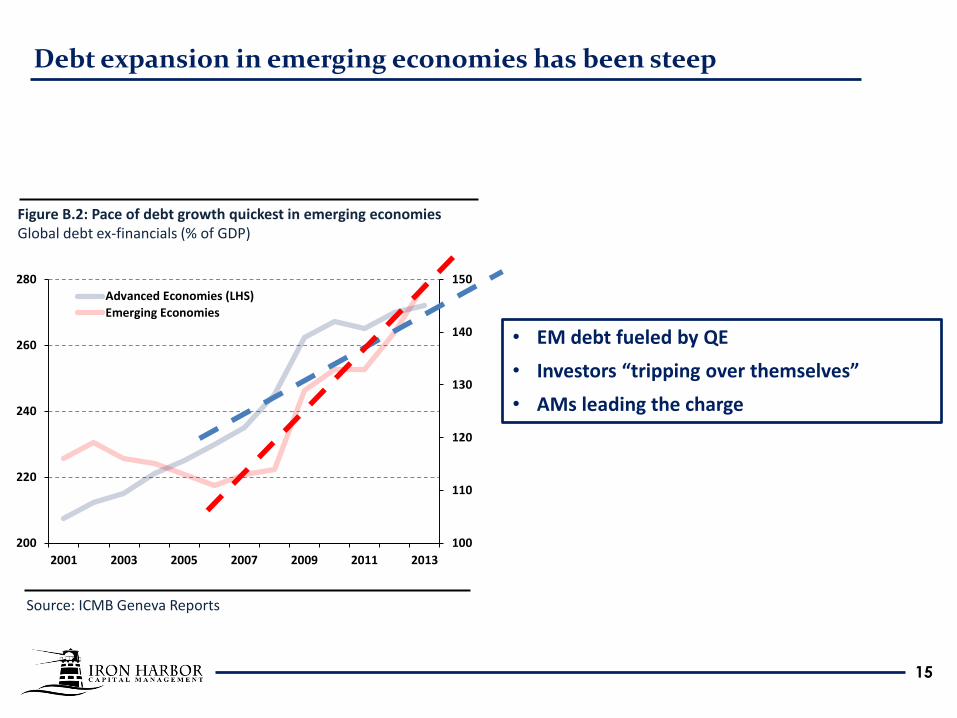

Debt expansion in emerging economies has been steep

14

Figure B.2: Pace of debt growth quickest in emerging economiesGlobal debt ex-financials (% of GDP)

100

110

120

130

140

150

200

220

240

260

280

2001 2003 2005 2007 2009 2011 2013

Advanced Economies (LHS)

Emerging Economies

• EM debt fueled by QE

• Investors “tripping over themselves”

Source: ICMB Geneva Reports

15

Figure B.2: Pace of debt growth quickest in emerging economiesGlobal debt ex-financials (% of GDP)

100

110

120

130

140

150

200

220

240

260

280

2001 2003 2005 2007 2009 2011 2013

Advanced Economies (LHS)

Emerging Economies

• EM debt fueled by QE

• Investors “tripping over themselves”

• AMs leading the charge

Debt expansion in emerging economies has been steep

Source: ICMB Geneva Reports

19

2nd Phase• FX appreciation• Local commodities boom• Asset prices rally

1st Phase• Slow growth/low yields search for yield• Hot money• Steady flows into Asia and LatAm

3rd Phase• Domestic credit expansion• Households• Public sector

4th Phase• Flows either stop or reverse

• Monetary policy• Geopolitical• End in a bang or whimper

Carmen and Vincent Reinhart, “Capital Flow Bonanzas”, 2008.

Capital Flow Bonanzas: Tracking investor flows

Stay on target with the correct policies and infrastructure

20

Investment goals and objectives1. Values clarity reassessment2. Investor Policy Statement3. Appropriate time horizon4. Acceptable levels of volatility5. Planning for liquidity needs6. Investor education

Asset diversification1. Avoid tactical deviations2. Forward looking strategic allocation3. Region/asset category concentration4. Active vs. passive

Current investment themes perform well in debt adjustment

21

Low and stable global inflation

Higher market volatility

Stronger US$

Downside growth surprise in China

Eurozone/Asia equities outperform US

Ongoing commodities opportunities