iphone and its supply chain

TRANSCRIPT

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

23 May 2017 Global

Equity Research Technology

iPhone and its supply chain The Credit Suisse Connections Series leverages our

exceptional breadth of macro and micro research to deliver

incisive cross-sector and cross-border thematic insights for

our clients.

Credit Suisse Global Technology Research Team

Credit Suisse equity research team

Manish Nigam

852 2101 7067

Kulbinder Garcha

212 325 4795

Randy Abrams, CFA

886 2 2715 6366

Pauline Chen

886 2 2715 6323

Keon Han

82 2 3707 3740

Akinori Kanemoto

81 3 4550 7363

Sang Uk Kim

82 2 3707 3795

Sam Li

852 2101 6775

Hideyuki Maekawa

81 3 4550 9723

Mika Nishimura

81 3 4550 7369

John W. Pitzer

212 538 4610

Achal Sultania

44 20 7883 6884

Jerry Su

886 2 2715 6361

Kyna Wong

852 2101 6950

Thompson Wu

886 2 2715 6386

CONNECTIONS SERIES

Identifying winners through the chain

Figure 1: Our top OUTPERFORM-rated ideas for the theme

BBG Price TP PE (x) CS EPS growth (%)

Company Ticker Curr. Rat Local Cur. Local Cur. 2017 2018 2017 2018

ams AMS SW CHF O 63.20 72.00 45.1 14.9 (11.4) 212.4

Apple AAPL US USD O 153.99 170.00 16.8 14.3 10.7 17.6

Hon Hai 2317 TT TWD O 102.50 120.00 10.8 9.4 10.2 15.3

Largan 3008 TT TWD O 4,900.00 5,200.00 21.0 17.2 46.0 24.1

LGI 011070 KS KRW O 128,000 165,000 13.2 12.4 4,656.2 7.9

Lens Tech 300433 CH CNY O 34.24 42.40 32.7 21.8 81.8 47.6

Micron MU US USD O 28.06 40.00 7.1 5.5 6,115.9 28.1

Murata 6981 JP JPY O 15,810.00 18,200.00 17.2 15.3 20.0 14.9

SEC 005930 KS KRW O 2,255,000 2,900,000 8.7 8.0 65.1 10.2

SONY 6758 JP JPY O 3,943.00 4,300.00 17.8 16.5 523.5 10.7

Source: Bloomberg, Company data, Credit Suisse estimates, at closing price on 22 May 2017

■ A major new product update. We believe the upcoming iPhone 8 model will

revive medium-term unit growth (we forecast an 8% CAGR over 2016-19)

even in our base-case scenario, given pent-up demand (as per our installed

base model) and meaningful new specs/features in the new offering. In this

global Connections Series report, based on inputs from our 15 analysts from

around the world, we look at the implications of the iPhone 8 cycle on Apple

and its global supply chain. On Pages 5-8, we list the major parts suppliers,

their exposure to this product and their valuations.

■ A big deal for the supply chain; but not everyone gains equally. In

Asia, about 60% of our coverage universe of hardware/semis’ stocks fall

within the Apple supply chain, signifying the importance of the product for

the Asian tech space. In addition to the resumption of unit growth, the

current cycle will also lead to some meaningful bill of material increases,

particularly for the OLED model (incremental ~US$55 per unit versus the

7 Plus). Providers of OLED display, casing, imaging/3D sensing parts,

memory, select sensors and select assemblers stand to gain through both

unit growth as well as dollar content growth.

■ Stock calls. Our top pick takes into account the impact of this product cycle

on earnings, performance of the businesses not related to the iPhone 8 and

valuations (i.e. what is already priced in). That leads us globally to the

following 10 stocks: Apple, Samsung Electronics, LG Innotek, Largan, Hon

Hai, Lens Tech, Sony, Murata, Micron and ams.

23 May 2017

iPhone and its supply chain 2

Focus tables

Figure 2: Comparison of key specs—iPhone 7+ versus likely specs for iPhone 8 Pro (OLED model)

Specs iPhone 7 Plus iPhone 8 Pro (OLED model)

Keu components

Acoustics Dual-speaker solution Enhanced dual-speaker solution

Cameras "12MP + 7 MP/ 12MP + 12 MP for Dual camera" Dual camera adds Dual OIS

Casing Unibody Al7000 Stainless steel frame + Two sides 2.5D Glass

Display & touchscreen 5.5" Retina Display with in-cell touch: 1920x1080 5.8” OLED Flat screen & DITO touch sensor

Force touch Capacitive sensing structure Enhanced force touch with resistive/strain gauge structure

Semis

Application processor 64-bit A10 on 16nm with embedded M10 Co processor A11 processor on 10nm

Audio Codec Cirrus Logic 338S00105/338S00220 Similar

Fingerprint sensor USI module + Authentec IC Under glass sensor (remove sapphire)

Memory (DRAM) 3 GB LPDDR4 PoP Similar

Memory (NAND) 32 / 128/ 256GB (TLC -20-25%) Possibly only 64/256GB Skus

Modem - Baseband, RF QCOM MDM9635M + WTR 3925 / Intel XMM 7480 QCOM X16 10nm / INTC 7480 28nm / 3PAMiD & 2 Diversity module

Power amplifier + Switch Multi-band PA module for global regions Similar RF content

User Interface & Sensors Accelerometer, e-compass , Gyro , Temperature, Touch IC Similar + 3D sensing + Gesture recognition

WLAN / BT / FM / GPS BRCM: BT 4.0+FM+Wifi 11ac in a USI Module Maybe Bluetooth 5.0, 802.11ac MIMO in Murata and USI module

Others

Battery 1960 mAh Dual cell L shape battery

Charger n.a. Wireless Charging chipset (full module not in box)

PCB 10-layer Any Layer Stacked Via HDI PCB + flex PCB HDI + Flex PCB + Substrate Like PCB

Source: Company data, Credit Suisse estimates

Figure 3: Apple—iPhone unit and ASP forecasts by models (2017-19)

iPhone Segmentation Sep-17 Dec-17 Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 Jun-19 Sep-19 Dec-19 CY17E CY18E CY19E

USD 4Q FY17 1Q FY18 2Q FY18 3Q FY18 4Q FY18 1Q FY19 2Q FY19 3Q FY19 4Q FY19 1Q FY20 Dec-17 Dec-18 Dec-19

iPhone units ('000) 48,838 85,222 57,099 48,534 53,406 90,790 61,737 51,859 56,483 99,974 228,986 249,828 270,054

%yoy 7% 9% 12% 10% 9% 7% 8% 7% 6% 10%

%qoq 11% 75% -33% -15% 10% 70% -32% -16% 9% 77% 6% 9% 8%

iPhone 7 13,186 4,261 3,711 2,184 2,136 2,724 1,235 1,037 847 1,500 63,200 10,755 4,619

iPhone 7 Plus 5,861 1,960 2,056 1,941 1,335 2,724 1,235 1,037 1,412 2,499 31,552 8,056 6,183

iPhone 8 12,014 23,436 17,701 16,259 6,943 6,355 3,704 2,593 2,824 2,999 35,450 47,257 12,121

iPhone 8 Plus 7,814 6,221 7,994 8,057 5,074 2,724 1,605 1,556 1,412 2,499 14,035 23,848 7,072

iPhone 8 Pro - 40,906 17,415 13,104 9,880 2,724 1,235 1,037 988 1,750 40,906 43,123 5,010

iPhone 9 - - - - 9,934 26,783 22,843 19,240 12,003 6,998 36,717 61,083

iPhone 9 Plus - - - - 3,204 7,808 6,791 5,705 2,259 2,499 11,012 17,254

iPhone 9 Pro - - - - 7,210 29,507 15,434 12,965 5,366 2,999 36,717 36,764

iPhone 10 - - - - - - - - 10,506 28,743 39,248

iPhone 10 Plus - - - - - - - - 3,954 6,598 10,552

iPhone 10 Pro - - - - - - - - 7,908 28,493 36,400

ASP ($ all in ) 646 750 702 705 711 702 669 670 683 680 676 704 676

ASP ($ H/W) 629 740 687 687 695 693 659 659 668 673 661 691 666

iPhone 7 551 536 527 517 523 524 526 526 512 512 589 523 519

iPhone 7 Plus 622 630 603 595 597 556 551 551 548 528 685 584 541

iPhone 8 742 659 667 667 619 581 575 554 543 544 687 648 555

iPhone 8 Plus 850 741 755 771 729 631 602 597 605 568 802 741 590

iPhone 8 Pro - 884 858 865 852 717 705 685 654 639 884 850 668

iPhone 9 - - - - 723 663 628 633 599 588 679 619

iPhone 9 Plus - - - - 802 769 732 732 701 637 779 714

iPhone 9 Pro - - - - 861 858 856 856 847 733 859 844

iPhone 10 - - - - - - - - 723 658 675

iPhone 10 Plus - - - - - - - - 812 772 787

iPhone 10 Pro - - - - - - - - 857 861 860

Source: Credit Suisse estimates

23 May 2017

iPhone and its supply chain 3

iPhone and its supply chain

iPhone 8: Rising demand; rising price We maintain our long-standing view of significant pent-up demand in terms of iPhone

volumes and based on our installed base model analysis (cross-checked with high-end

market share and share by region), we conclude that iPhone volumes will grow robustly

from 214 mn in 2016, to 230 mn/250 mn/270 mn in 2017/2018/2019. Our pricing trend

analysis also suggests that Apple's ability to further raise pricing is intact. We assume a

45%/40% mix of the Pro model in 2017/2018, which positively impacts ASPs. Our analysis

shows that the bill of materials (BOM) for the OLED version will be ~US$55 higher than

the 7 Plus at launch). However, we conclude the improved mix and pricing could offset the

anticipated BOM rise. Apple remains a key OUTPERFORM with a target price of US$170.

Display, casing, 3D-sensing: Likely major changes While changes from the iPhone 7 to iPhone 8 do not a add a lot of content dollars for most

suppliers, the bill of materials for the OLED model is likely to be driven higher by the usage

of a new display (OLED panels would add ~US$27 per unit—supplied by Samsung), a

complete change in casing design (steel frame and front and back 2.5D glass adding

~US$10) and the introduction of 3D sensing (front facing, mainly for facial recognition and

gesture control; adding ~US$12). Suppliers of these parts stand to gain from both unit and

content growth. Other downstream part suppliers are likely to gain via overall unit growth,

and in some cases, through market share gains. Our top ideas are: Samsung Electronics,

Largan, LG Innotek, Lens Tech, Sony and Murata.

Asian semis: The Big 2 to make more money Moving from the iPhone 7 to iPhone8, there isn’t a major content gain story for Asian

semis. So, the bulk of the changes is being driven by unit growth, share gains or mix.

TSMC's 100% share of the applications processor and Apple’s fingerprint IC and NAND

controller should lift direct sales to Apple from 17% in 2016 to an estimated 22%/24% in

2017/2018. Apple’s ramp should be a good driver in 2H for TSMC, but we believe will be

partially offset by on-going inventory adjustments from other fabless customers and

continued high-end migration by its #2 customer, Qualcomm, into Samsung’s fabs well

into 2018. Samsung's operating profit from selling memory to Apple also increases as a

result of substantially higher year-on-year ASP for DRAM, a product mix shift in favour of

3GB iPhones and overall iPhone unit growth driving total DRAM bits and unit growth (and

the potential discontinuation of the 32GB sku) driving NAND bits.

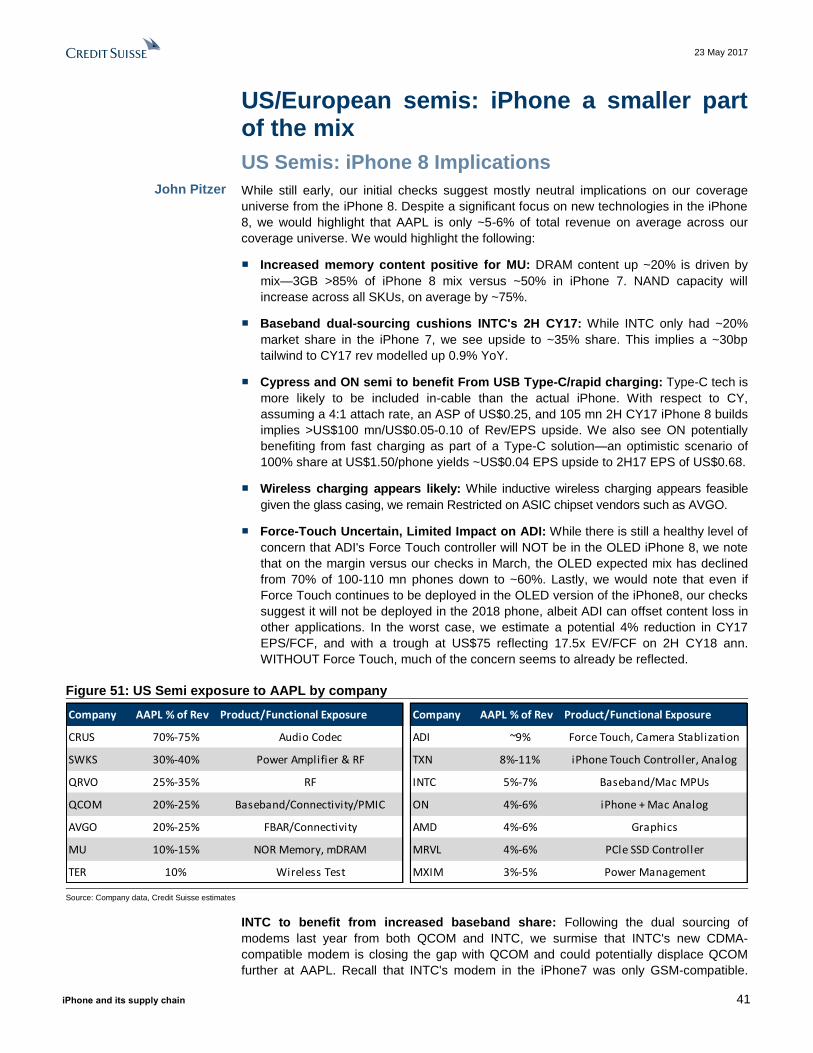

US/European semis: iPhone a smaller part of the mix We see mostly neutral implications for our US semi universe from the iPhone 8. Despite a

significant focus on new technologies in the iPhone 8, AAPL is only ~5-6% of total

revenues on average across our US semi coverage universe. Specifically, we highlight

that increased memory dollar content should be positive for Micron, Intel's share of

baseband should increase from ~20% in iPhone 7 to ~35% in the iPhone 8 and RF names

will continue to benefit from content growth. Across our EU coverage, we continue to see

ams (various sensors) as the biggest beneficiary from rising content within upcoming

iPhone generations over the next few years and it remains our top pick. ST Micro also

stands to gain from 3D-sensing, but valuations leave it as a NEUTRAL-rated stock.

Assembly: Rising tide might lift all boats We believe that the iPhone8 cycle accelerates volume growth for all three iPhone

assemblers: Hon Hai, Pegatron and Wistron. Timing of this growth varies. Hon Hai leads

the pack in 2017 with a 100% allocation of the iPhone 8 OLED model (the other two gain

share in 2018 as OLED displays are adopted in all models), but gives up share of LTPS

models (Pegatron gains share in the 4.7"; Wistron in the 5.5" model). Hon Hai remains our

top buy in the Asia Hardware sector despite a 21% YTD share price appreciation.

23 May 2017

iPhone and its supply chain 4

Table of contents

Focus tables 2

iPhone and its supply chain 3

iPhone 8: Rising demand; rising price ...................................................................... 3

Display, casing, 3D-sensing: Likely major changes ................................................. 3

Asian semis: The Big 2 to make more money .......................................................... 3

US/European semis: iPhone a smaller part of the mix ............................................. 3

Assembly: Rising tide might lift all boats .................................................................. 3

iPhone 8—supply chain and valuations 5

iPhone 8: Rising demand, rising price 9

iPhone 8: A major update in a super cycle ............................................................... 9

Unit Outlook heading to 270 mn units at least........................................................ 13

Raising price could offset BOM pressure ............................................................... 16

Scenarios analysis—US$14 EPS power in bull case ............................................ 20

Display, casing, 3D-sensing: Likely major changes 22

OLED—the new path for iPhone displays .............................................................. 22

Casing/ cover glass: A major change in all iPhone 8s ........................................... 25

Camera upgrade and 3D sensing .......................................................................... 26

Acoustic .................................................................................................................. 28

Haptics .................................................................................................................... 29

PCB ........................................................................................................................ 29

Passive Components .............................................................................................. 30

RF Front End/Wifi Module ...................................................................................... 30

Asian semis: The Big 2 to make more money 31

Foundry and backend ............................................................................................. 31

Memory: Largely an ASP-led dollar content gain ................................................... 33

How AAPL's DRAM demand impacts Samsung .................................................... 34

Fingerprint and touch sensor .................................................................................. 39

US/European semis: iPhone a smaller part of the mix 41

US Semis: iPhone 8 Implications ........................................................................... 41

EU Semis: iPhone 8 implications ........................................................................... 44

Assembly: Rising tide might lift all boats 47

Increase estimates for Hon Hai, Pegatron and Wistron ....................................... 47

Potential risks with QCOM complaint filing on 17 May ........................................... 48

Hon Hai: Top pick among iPhone assemblers (OUTPERFORM, raising TP to

NT$120 from NT$105) ............................................................................................ 48

23 May 2017

iPhone and its supply chain 5

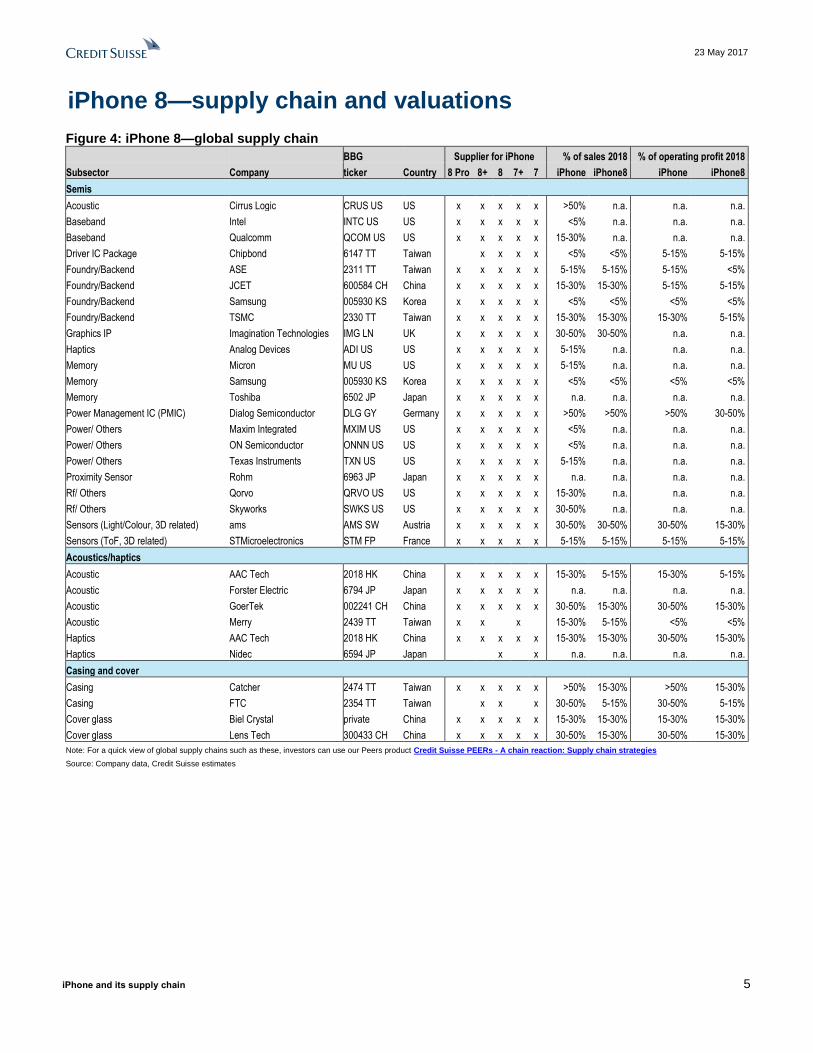

iPhone 8—supply chain and valuations

Figure 4: iPhone 8—global supply chain

BBG Supplier for iPhone % of sales 2018 % of operating profit 2018

Subsector Company ticker Country 8 Pro 8+ 8 7+ 7 iPhone iPhone8 iPhone iPhone8

Semis

Acoustic Cirrus Logic CRUS US US x x x x x >50% n.a. n.a. n.a.

Baseband Intel INTC US US x x x x x <5% n.a. n.a. n.a.

Baseband Qualcomm QCOM US US x x x x x 15-30% n.a. n.a. n.a.

Driver IC Package Chipbond 6147 TT Taiwan x x x x <5% <5% 5-15% 5-15%

Foundry/Backend ASE 2311 TT Taiwan x x x x x 5-15% 5-15% 5-15% <5%

Foundry/Backend JCET 600584 CH China x x x x x 15-30% 15-30% 5-15% 5-15%

Foundry/Backend Samsung 005930 KS Korea x x x x x <5% <5% <5% <5%

Foundry/Backend TSMC 2330 TT Taiwan x x x x x 15-30% 15-30% 15-30% 5-15%

Graphics IP Imagination Technologies IMG LN UK x x x x x 30-50% 30-50% n.a. n.a.

Haptics Analog Devices ADI US US x x x x x 5-15% n.a. n.a. n.a.

Memory Micron MU US US x x x x x 5-15% n.a. n.a. n.a.

Memory Samsung 005930 KS Korea x x x x x <5% <5% <5% <5%

Memory Toshiba 6502 JP Japan x x x x x n.a. n.a. n.a. n.a.

Power Management IC (PMIC) Dialog Semiconductor DLG GY Germany x x x x x >50% >50% >50% 30-50%

Power/ Others Maxim Integrated MXIM US US x x x x x <5% n.a. n.a. n.a.

Power/ Others ON Semiconductor ONNN US US x x x x x <5% n.a. n.a. n.a.

Power/ Others Texas Instruments TXN US US x x x x x 5-15% n.a. n.a. n.a.

Proximity Sensor Rohm 6963 JP Japan x x x x x n.a. n.a. n.a. n.a.

Rf/ Others Qorvo QRVO US US x x x x x 15-30% n.a. n.a. n.a.

Rf/ Others Skyworks SWKS US US x x x x x 30-50% n.a. n.a. n.a.

Sensors (Light/Colour, 3D related) ams AMS SW Austria x x x x x 30-50% 30-50% 30-50% 15-30%

Sensors (ToF, 3D related) STMicroelectronics STM FP France x x x x x 5-15% 5-15% 5-15% 5-15%

Acoustics/haptics

Acoustic AAC Tech 2018 HK China x x x x x 15-30% 5-15% 15-30% 5-15%

Acoustic Forster Electric 6794 JP Japan x x x x x n.a. n.a. n.a. n.a.

Acoustic GoerTek 002241 CH China x x x x x 30-50% 15-30% 30-50% 15-30%

Acoustic Merry 2439 TT Taiwan x x x 15-30% 5-15% <5% <5%

Haptics AAC Tech 2018 HK China x x x x x 15-30% 15-30% 30-50% 15-30%

Haptics Nidec 6594 JP Japan x x n.a. n.a. n.a. n.a.

Casing and cover

Casing Catcher 2474 TT Taiwan x x x x x >50% 15-30% >50% 15-30%

Casing FTC 2354 TT Taiwan x x x 30-50% 5-15% 30-50% 5-15%

Cover glass Biel Crystal private China x x x x x 15-30% 15-30% 15-30% 15-30%

Cover glass Lens Tech 300433 CH China x x x x x 30-50% 15-30% 30-50% 15-30%

Note: For a quick view of global supply chains such as these, investors can use our Peers product Credit Suisse PEERs - A chain reaction: Supply chain strategies

Source: Company data, Credit Suisse estimates

23 May 2017

iPhone and its supply chain 6

Figure 5: iPhone 8—global supply chain (cont’d)

BBG Supplier for iPhone % of sales 2018 % of operating profit 2018

Subsector Company ticker Country 8 Pro 8+ 8 7+ 7 iPhone iPhone8 iPhone iPhone8

Imaging

3D sensing Himax HIMX US Taiwan x <5% <5% 15-30% 15-30%

3D sensing Win Semi 3105 TT Taiwan x <5% <5% 5-15% 5-15%

Camera Lens Genius 3406 TT Taiwan x x x x x n.a. n.a. n.a. n.a.

Camera Lens Largan 3008 TT Taiwan x x x x x >50% 15-30% n.a. n.a.

Camera module Cowell 1415 HK China x x x x x >50% >50% >50% >50%

Camera module LGI 011070 KS Korea x x x x x 30-50% 15-30% 30-50% 30-50%

Camera module Shenzhen O-film 002456 CH CNY x x x x x 15-30% 15-30% 15-30% 15-30%

Display related

Display JDI 6740 JP Japan x x x x n.a. n.a. n.a. n.a.

Display LGD 034220 KS Korea x x x x 5-15% <5% 5-15% <5%

Display Radiant 6176 TT Taiwan x x x x 5-15% 5-15% 5-15% 5-15%

Display Samsung 005930 KS Korea x <5% <5% <5% <5%

Display Sharp 6753 JP Japan x x n.a. n.a. n.a. n.a.

Touch GIS 6456 TT Taiwan x x x x x 30-50% 15-30% >50% 30-50%

Touch Nissha Printing 7915 JP Japan x n.a. n.a. n.a. n.a.

Touch TPK 3673 TT Taiwan x x x x x 30-50% 15-30% 30-50% 30-50%

Misc./ multiple components

Battery TDK 6762 JP Japan x x x x x n.a. n.a. n.a. n.a.

Battery, RF devices Samsung SDI 006400 KS Korea x x x x x <5% <5% <5% <5%

Battery/CIS SONY 6758 JP Japan x x x x x n.a. n.a. n.a. n.a.

Quartz Crystal Daisinku 6962 JP Japan x x x x x n.a. n.a. n.a. n.a.

Quartz Crystal Nihon Dempa 6779 JP Japan x x x x x n.a. n.a. n.a. n.a.

Quartz Crystal Seiko Epson 6724 JP Japan x x x x x n.a. n.a. n.a. n.a.

Quartz Crystal TXC 3042 TT Taiwan x x x x x 5-15% <5% n.a. n.a.

Rubber ring Tongda 698 HK China x x x x x 5-15% 5-15% 5-15% 5-15%

VCM/OIS/Haptic/Mech/Backlight Alps 6770 JP Japan x x x x x n.a. n.a. n.a. n.a.

VCM/OIS/Haptic/Mech/Backlight MinebeaMitsumi 6479 JP Japan x x x x x n.a. n.a. n.a. n.a.

PCB/ connectors/ passive

Ceramic Package/MLCC/Connector Kyocera 6971 JP Japan x x x x x n.a. n.a. n.a. n.a.

Ceramic Package/MLCC/Connector NGK Spark Plug 5334 JP Japan x x x x x n.a. n.a. n.a. n.a.

Connector Hirose 6806 JP Japan x x x x x n.a. n.a. n.a. n.a.

Connector JAE 6807 JP Japan x x x x x n.a. n.a. n.a. n.a.

Connector/ cable Luxshare 002475 CH China x x x x x 30-50% 15-30% 30-50% 15-30%

HDI/FC-CSP Ibiden 4062 JP Japan x n.a. n.a. n.a. n.a.

Passive components Taiyo Yuden 6976 JP Japan x x x x x n.a. n.a. n.a. n.a.

Passive, Connector, RF devices Murata 6981 JP Japan x x x x x n.a. n.a. n.a. n.a.

PCB Kinsus 3189 TT Taiwan x x x x x 15-30% 5-15% 15-30% 5-15%

PCB NYPCB 8046 TT Taiwan x x x x x <5% <5% n.a. n.a.

PCB Unimicron 3037 TT Taiwan x x x x x 5-15% <5% n.a. n.a.

Power Inductor/MLCC Delta 2308 TT Taiwan x x x x x 5-15% <5% n.a. n.a.

EMS

Assembly Hon Hai 2317 TT Taiwan x x x 30-50% 30-50% 30-50% 30-50%

Assembly Pegatron 4938 TT Taiwan x x >50% 30-50% >50% 30-50%

Assembly Wistron 3231 TT Taiwan x x 30-50% 30-50% 30-50% 15-30%

Note: For a quick view of global supply chains such as these, investors can use our Peers product Credit Suisse PEERs - A chain reaction: Supply chain strategies

Source: Company data, Credit Suisse estimates

23 May 2017

iPhone and its supply chain 7

Figure 6: iPhone 8 global supply chain—valuation comparison

BBG Price TP P/E (x) CS EPS growth

(%)

P/B (x) Div. yield

Subsector Company Ticker Curr. Rat loc curr. loc curr. 2017 2018 2017 2018 2017 2017

Semis

Acoustic Cirrus Logic CRUS US USD NC 65.07 n.a. 14.2 13.5 n.a. n.a. 1.5 -

Baseband Intel INTC US USD N 35.77 35.00 12.6 11.9 4.8 5.5 2.3 2.8

Baseband Qualcomm QCOM US USD R 59.28 n.a. 13.2 13.9 n.a. n.a. (1.9) 3.7

Driver IC Package Chipbond 6147 TT TWD O 43.95 54.00 13.1 11.2 16.4 19.1 1.2 5.0

Foundry/Backend ASE 2311 TT TWD R 37.60 n.a. 15.1 13.4 (6.0) 14.8 1.7 3.8

Foundry/Backend JCET 600584 CH CNY U 16.43 11.80 140.8 99.9 9.1 38.9 2.4 0.1

Foundry/Backend Samsung 005930 KS KRW O 2,255,000 2,900,000 8.7 8.0 65.1 10.2 1.3 1.6

Foundry/Backend TSMC 2330 TT TWD N 205.00 202.00 15.9 14.6 6.4 10.6 3.5 3.4

Graphics IP Imagination Technologies IMG LN GBP N 101.25 100.00 14.8 (41.1) 24.8 n.a. 1.8 -

Haptics Analog Devices ADI US USD O 82.09 100.00 20.5 17.5 29.5 17.5 3.2 1.2

Memory Samsung 005930 KS KRW O 2,255,000 2,900,000 8.7 8.0 65.1 10.2 1.3 1.6

Memory Toshiba 6502 JP JPY N 230.00 223.00 5.3 5.9 n.a. (7.7) (2.3) -

Power Management IC (PMIC) Dialog Semiconductor DLG GY EUR O 42.82 54.00 17.8 14.0 33.6 18.6 2.8 -

Power/ Others ON Semiconductor ONNN US USD U 15.57 13.50 12.3 10.4 39.8 18.2 2.9 -

Power/ Others Texas Instruments TXN US USD O 80.37 95.00 20.0 18.9 13.1 5.9 7.2 2.4

Proximity Sensor Rohm 6963 JP JPY O 8,560.00 8,400.00 28.7 21.9 9.8 34.0 1.3 1.2

Rf/ Others Qorvo QRVO US USD NC 78.07 n.a. 13.4 11.6 n.a. n.a. 23.1 -

Sensors (Light/Colour, 3D related) ams AMS SW CHF O 63.20 72.00 45.1 14.9 (11.4) 212.4 4.5 0.2

Sensors (ToF, 3D related) STMicroelectronics STM FP EUR N 14.37 15.50 21.0 16.1 171.8 31.0 2.9 1.5

Acoustic Cirrus Logic CRUS US USD NC 65.07 n.a. 14.2 13.5 n.a. n.a. 1.5 -

Baseband Intel INTC US USD N 35.77 35.00 12.6 11.9 4.8 5.5 2.3 2.8

Baseband Qualcomm QCOM US USD R 59.28 n.a. 13.2 13.9 n.a. n.a. (1.9) 3.7

Acoustics/haptics

Acoustic AAC Tech 2018 HK HKD N 82.60 98.40 16.7 13.7 27.7 19.9 5.1 2.3

Acoustic Forster Electric 6794 JP JPY NC 1,737.00 n.a. 9.8 8.1 n.a. n.a. 331.9 n.a.

Acoustic GoerTek 002241 CH CNY O 17.54 21.60 24.2 20.8 28.7 14.8 4.2 0.6

Acoustic Merry 2439 TT TWD O 188.00 176.00 16.6 16.0 11.1 5.4 4.9 4.1

Haptics AAC Tech 2018 HK HKD N 82.60 98.40 16.7 13.7 27.7 19.9 5.1 2.3

Haptics Nidec 6594 JP JPY O 10,410.00 14,200.00 23.3 20.3 20.7 17.5 3.3 1.3

Casing and cover

Casing Catcher 2474 TT TWD O 317.50 350.00 11.7 10.3 1.5 16.0 1.8 3.1

Casing FTC 2354 TT TWD N 87.00 98.00 11.8 11.0 3.3 9.3 1.1 4.2

Cover glass Biel Crystal n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

Cover glass Lens Tech 300433 CH CNY O 34.24 42.40 32.7 21.8 81.8 47.6 4.7 0.6

Note: Closing price as at 22 May 2017 Source: Bloomberg, IBES, Thomson Reuters, Company data, Credit Suisse estimates

23 May 2017

iPhone and its supply chain 8

Figure 7: iPhone 8 global supply chain—valuation comparison table (cont’d)

BBG Price TP P/E (x) CS EPS growth (%) P/B

(x)

Div. yield

Subsector Company Ticker Curr. Rat loc. curr. loc. curr. 2017 2018 2017 2018 2017 2017

Imaging

3D sensing Himax HIMX US USD N 6.93 6.70 92.8 23.0 (74.7) 303.3 2.7 0.9

3D sensing Win Semi 3105 TT TWD N 127.50 125.00 16.1 13.0 12.0 25.7 2.7 3.5

Camera Lens Genius 3406 TT TWD NC 310.00 n.a. n.a. n.a. n.a. n.a. 83.8 n.a.

Camera Lens Largan 3008 TT TWD O 4,900.00 5,200.00 21.0 17.2 46.0 24.1 6.6 1.7

Camera module Cowell 1415 HK HKD NC 2.26 n.a. 5.0 4.1 n.a. n.a. 70.6 -

Camera module LGI 011070 KS KRW O 128,000 165,000 13.2 12.4 4,656.2 7.9 1.5 0.3

Display related

Display JDI 6740 JP JPY N 206.00 250.00 8.4 12.5 n.a. (31.4) 0.3 2.4

Display LGD 034220 KS KRW N 29,250 30,600 6.5 10.7 91.5 (38.2) 0.7 1.7

Display Radiant 6176 TT TWD U 64.20 45.00 10.0 10.7 0.6 (4.7) 1.3 6.6

Display Samsung 005930 KS KRW O 2,255,000 2,900,000 8.7 8.0 65.1 10.2 1.3 1.6

Display Sharp 6753 JP JPY U 420.00 180.00 40.8 33.4 n.a. 24.8 6.0 -

Touch GIS 6456 TT TWD NC 219.00 n.a. 16.2 13.9 n.a. n.a. 44.1 n.a.

Touch Nissha Printing 7915 JP JPY O 2,971.00 3,700.00 18.2 8.6 n.a. 118.3 1.9 1.5

Touch TPK 3673 TT TWD N 102.50 95.00 11.3 12.7 n.a. (9.2) 1.1 4.4

Misc./ multiple components

Battery TDK 6762 JP JPY N 6,870.00 8,500.00 11.7 11.0 6.7 9.3 1.1 1.7

Battery, RF devices Samsung SDI 006400 KS KRW N 156,500 115,000 24.1 19.9 108.2 23.0 1.0 0.6

Battery/CIS SONY 6758 JP JPY O 3,943.00 4,300.00 17.8 16.5 523.5 10.7 1.7 2.0

Quartz Crystal Daisinku 6962 JP JPY NC 1,547.00 n.a. 16.1 13.2 n.a. n.a. 11.4 n.a.

Quartz Crystal Nihon Dempa 6779 JP JPY NC 889.00 n.a. 20.1 17.5 n.a. n.a. 42.3 n.a.

Quartz Crystal Seiko Epson 6724 JP JPY NC 2,320.00 n.a. 14.1 12.5 n.a. n.a. 20.5 n.a.

Quartz Crystal TXC 3042 TT TWD N 43.05 45.00 11.9 10.9 14.0 9.4 1.2 6.7

Rubber ring Tongda 698 HK HKD N 2.63 2.50 12.9 10.6 28.4 21.0 3.0 2.3

VCM/OIS/Haptic/Mech/Backlight Alps 6770 JP JPY O 3,220.00 3,400.00 13.3 11.5 36.8 19.2 2.1 1.1

VCM/OIS/Haptic/Mech/Backlight MinebeaMitsumi 6479 JP JPY NC 1,743.00 n.a. 17.0 16.0 n.a. n.a. (4.2) n.a.

PCB/ connectors/ passive

Ceramic Package/MLCC/Connector Kyocera 6971 JP JPY N 6,493.00 6,400.00 22.5 21.1 13.7 9.4 1.0 1.5

Ceramic Package/MLCC/Connector NGK Spark Plug 5334 JP JPY O 2,308.00 3,000.00 11.9 9.5 17.1 27.7 1.2 2.5

Connector Hirose 6806 JP JPY N 14,660.00 13,900.00 24.2 22.5 3.2 10.4 1.7 1.6

Connector JAE 6807 JP JPY N 1,483.00 1,600.00 10.7 9.2 28.6 20.0 1.1 2.0

Connector/ cable Luxshare 002475 CH CNY O 29.14 32.60 33.0 25.5 n.a. 27.7 4.8 0.4

HDI/FC-CSP Ibiden 4062 JP JPY U 1,964.00 1,340.00 36.3 31.3 n.a. 18.9 1.0 1.8

Passive components Taiyo Yuden 6976 JP JPY N 1,544.00 1,000.00 23.6 20.0 45.1 20.3 1.2 1.3

Passive, Connector, RF devices Murata 6981 JP JPY O 15,810.00 18,200.00 17.2 15.3 20.0 14.9 2.2 1.5

PCB Kinsus 3189 TT TWD N 79.30 76.00 17.0 14.4 (0.8) 20.0 1.2 4.4

PCB NYPCB 8046 TT TWD N 25.15 26.00 (80.8) 21.0 69.2 n.a. 0.5 -

PCB Unimicron 3037 TT TWD N 17.45 14.00 62.0 23.7 n.a. 160.4 0.6 1.5

Power Inductor/MLCC Delta 2308 TT TWD O 167.00 190.00 20.7 18.7 18.7 12.6 3.3 3.4

EMS

Assembly Hon Hai 2317 TT TWD O 102.50 120.00 10.8 9.4 10.2 15.3 1.5 4.4

Assembly Pegatron 4938 TT TWD N 92.80 85.00 10.8 9.3 14.1 16.8 1.6 5.4

Assembly Wistron 3231 TT TWD O 27.30 34.00 11.3 8.6 100.9 32.5 1.0 4.4

Note: Closing price as at 22 May 2017 Source: Bloomberg, IBES, Thomson Reuters, Company data, Credit Suisse estimates

23 May 2017

iPhone and its supply chain 9

iPhone 8: Rising demand, rising price In this section, we present our outlook for the iPhone business heading into the iPhone 8

Super-cycle, based on all the available evidence (please see full report for more details).

We maintain our long-standing view that there is significant pent-up demand in terms of

volume and raise our unit estimates slightly to 229 mn/250 mn/270 mn in CY17/18/19.

Additionally, our analysis of pricing trends suggests that Apple's ability to further raise

pricing remains intact. Given this and a better view on the mix, we raise our ASPs to

US$676/US$704/US$676 in CY17/18/19. Our analysis does conclude that the improved

mix as well as pricing could offset the anticipated BOM increase and we arrive at three

main conclusions:

Units heading to 270 mn. Our bias has been to look at the impact of the Apple

product cycle over two years and not just one, as we anticipate the OLED

penetration of Apple's complete portfolio will take place over two years. We rely

on our installed base model to forecast unit shipments, which we then cross-

check with high-end market share and share by region. We conclude that iPhone

volumes will see robust growth from 214 mn in 2016, to 230 mn/250 mn/270 mn

in 2017/2018/2019 or a CAGR of 8%.

ASPs to rise, multiple reasons why a price increase may be implemented.

Given a significant feature upgrade, relative lack of elasticity observed so far, an

affluent user base as well as the price increases on Samsung's Galaxy 8 devices,

we assume the starting prices for the three new models at

US$670/US$770/US$900, which are referred to here as iPhone 8/8 Plus and

8 Pro for the sake of naming convention. Given that we assume a 45%/40% mix

of the Pro model in 2017/2018, this positively impacts ASPs, which we now see at

US$676/US$704 for CY17/18.

BOM higher, but mix and pricing key. We acknowledge that the BOM for the

OLED version will be US$55 higher than the comparable iPhone 7 Plus at launch,

per our teardown analysis performed in conjunction with our Asian Team. We also

assume that the iPhone 8 and iPhone 8 Plus see higher BOM by around US$10-

15. However given the price increase discussed above as well our mix

assumptions, we see the iPhone GM rising to 39% in 2018 versus 38% in 2016.

Figure 8: iPhone mini P&L—LT revenue of US$183 bn and GP of US$69 bn

CY14 CY15 CY16 CY17 CY18 CY19

iPhone revenue (US$ mn) 120,675 155,494 139,443 154,849 175,928 182,625

as % total revenue 60.4% 66.2% 63.9% 64.7% 65.8% 65.3%

iPhone unit ('000) 192,662 231,529 215,395 228,986 249,828 270,054

ASP (US$) 626 672 647 676 704 676

Gross profit (US$ mn) 50,109 64,281 53,484 57,123 68,319 69,039

as % total GP 63.9% 68.2% 63.7% 62.8% 63.9% 61.5%

Gross margin % 41.5% 41.3% 38.4% 36.9% 38.8% 37.8%

Source: Company data, Credit Suisse estimates

iPhone 8: A major update in a super cycle

Before discussing the unit, ASP or margin outlook, we need to arrive at the importance of

the actual feature set, as this impacts all of these assumptions. Please see the following

figure for details of the expected features. Our base case is as follows:

■ Launch of three Models. Unlike previous years, we believe that Apple will launch

three devices: the iPhone (4.7 inch), iPhone 8 (5.5 inch) Plus and the iPhone Pro (5.8

inch) device.

■ The OLED model featuring Iris recognition or in-display fingerprint. We now think

the OLED model is likely to adopt Iris recognition or in-display finger footprint

Kulbinder Garcha

23 May 2017

iPhone and its supply chain 10

recognition. The home button will be removed as a result. As development of in-display

finger footprint recognition for the Galaxy S8 has missed the deadline, it remains to be

seen whether the development will be completed over the next couple of months for

the iPhone 8 launch. We expect the 4.7- and 5.5-inch LCD models to feature a

fingerprint scanner in the home button, as they do today.

■ Better cameras featuring dual OIS; possibly more advanced laser auto focus. We

think the 5.8-inch OLED model will have dual main cameras and OIS/OIS. We also

think the laser auto-focus may be adopted. We expect the 4.7-inch LCD model to have

a single camera with OIS and the 5.5-inch model to feature dual main cameras and a

combination OIS/VCM, on par with the iPhone 7.

■ Faster application processor based on 10nm FinFET. We forecast adoption of A11

10nm FinFET/InFO WLP, which will improve processing performance.

■ More storage and memory. For NAND, we think all three models will feature two

memory specs: 64Gb and 256Gb, with some regions likely to adopt 512Gb. We also

expect all models to feature 3Gb of DRAM.

■ L-shaped battery to improve capacity. In the OLED model, in addition to reduction in

substrate area due to SLP, we think the li-ion polymer battery will be larger due to an L-

shaped design, which will help the battery capacity.

We note that the above is a major relative upgrade to the iPhone portfolio, which impacts

our assumptions for future rates of replacement and upgrades.

BOM pressures are evident

A glance at Figure shows that across all of the improved hardware-related features, there

will be an associated rise in the BOM. The increase should be most pronounced in the

iPhone 8 Pro (OLED version), where it could be some US$55 higher than the 7 Plus

device. We also assume that the BOM will be about US$10-15 higher for the iPhone 8 and

Plus device compared with last year's models.

■ iPhone 8 Pro BOM higher by US$55. Across all of the improved hardware-related

features, there will be a rise in the BOM as well, specifically in the OLED version, which

we estimate as much as US$55 (compared to iPhone 7 Plus).

■ OLED and 3D Sensing major drivers of the BOM increase. We note that for the Pro

version, the larger screen adds US$27 to BOM (compared to iPhone 7 Plus) while 3D

Sensing and Gesture recognition adds a further US$12. Phone casing adds another

US$10. These three hardware components are responsible for the bulk of the BOM

increase.

■ Base models to increase as well. We assume that base models see an increase in

BOM of US$10-15 based on all the other major features such as new materials for the

body.

23 M

ay 2

017

iPh

on

e a

nd

its s

up

ply

ch

ain

1

1

Figure 4: iPhone 9 sees a major update in features to drive unit growth and better mix

Source: Company data, Credit Suisse estimates

iPhone6 iPhone6Plus iPhone6s iPhone6s Plus iPhone SE iPhone7 iPhone7 Plus iPhone8 4.7" iPhone8 5.5" iPhone 2017 5.85"

Announce 9/10/2014 9/10/2014 9/9/2015 9/9/2015 3/22/2016 9/7/2016 9/7/2016 2017 2017 2017

Release 9/19/2014 9/19/2014 9/25/2015 9/25/2015 3/31/2016 9/16/2016 9/16/2016 15-20% 10-15% 70%

Height (mm) 138.1 158.1 138.3 158.2 123.8 138.3 158.2 - -

Width (mm) 67 77.8 67.1 77.9 58.6 67.1 77.9 - -

Thickness (mm) 6.9 7.1 7.1 7.3 7.6 7.1 7.3 - -

Weight (g) 129 172 143 192 113 138 188 - -

Display size (inch) 4.7" in-cell 5.5" in-cell 4.7" in-cell 5.5" in-cell 4" 4.7" in-cell 5.5" in-cell 4.7" in-cell 5.5" in-cell5.85" OLED with

G/F2

Display resolution (px) 1334x750px 1920x1080px 1334x750px 1920x1080px 1,136 x 640px 1334x750px 1920x1080px 1334x750px 1920x1080pxWQHD

(2560x 1440px)

Display (ppi) 326ppi 401ppi 326ppi 401ppi 326ppi 326ppi 401ppi 326ppi 401ppi --

8M 8M&OIS 12MP 12MP & OIS 12MP 12MP OIS

12MP OIS (Wide

Angel)

12MP VCM

(Telephoto)

12MP OIS

12MP OIS (Wide

Angel)

12MP VCM

(Telephoto)

12MP OIS (Wide

Angel)

12MP OIS

(Telephoto)

Laser AF

F2.2, 1/3", 1.5μm F2.2, 1/3", 1.5μm F2.2, NA, 1.22μm F2.2, NA, 1.22μmF2.2, 1/3", 1.22 µ

mF1.8

Wide-Angle F1.8

Telephoto F2.8F1.8

Wide-Angle F1.8

Telephoto F2.8NA

Camera (front) 1.2M 1.2M 5MP 5MP 1.2M 7MP 7MP 7MP 7MP7MP

Iris recognition

Wifi

Dual band

802.11a/b/g/n/ac

Wi‑Fi

Dual band

802.11a/b/g/n/ac

Wi‑Fi

Dual band

802.11a/b/g/n/ac

Wi‑Fi

(MIMO)

Dual band

802.11a/b/g/n/ac

Wi‑Fi

(MIMO)

Wi-Fi 802.11

a/b/g/n/ac,

hotspot

Dual band

802.11a/b/g/n/ac

Wi‑Fi

(MIMO)

Dual band

802.11a/b/g/n/ac

Wi‑Fi

(MIMO)

Dual band

802.11a/b/g/n/ac

Wi‑Fi

(MIMO)

Dual band

802.11a/b/g/n/ac

Wi‑Fi

(MIMO)

Dual band

802.11a/b/g/n/ac

Wi‑Fi

(MIMO)

Bluetooth Bluetooth 4.0 Bluetooth 4.0 Bluetooth 4.2 Bluetooth 4.2 Bluetooth 4.2 Bluetooth 4.2 Bluetooth 4.2 Bluetooth 4.2 Bluetooth 4.2 Bluetooth 4.2

CPU clock A8 /20nm & M8 A8 /20nm & M8 A9 A9 A9

CPU Core 64 bit 64 bit 64bit 64bit 64bit 64bit 64bit 64bit 64bit 64bit

CPU Die size 89 sqmm 89 sqmm 96 sqmm 96 sqmm 96 sqmm NA NA NA NA NA

GPU Core

Power VR

GX6450

(Quadl Core)

Power VR

GX6450

(Quad Core)

PowerVR 7XT

GT7600

(Hexa Core)

PowerVR 7XT

GT7600

(Hexa Core)

PowerVR

GT7600

(six-core

graphics)

NA NA NA NA NA

NAND16GB/64GB/128

GB

16GB/64GB/128

GB

16GB/64GB/128

GB

16GB/64GB/128

GB16GB/64GBGB

DRAM 1GB 1GB 2GB 2GB 2GB 2GB 3GB 3GB 3GB 3GB

Battery capacity 1810mAh 2915mAh 1715mAh 2915mAh 1642 mAh - - - - -

Casing

Aluminum

(space

grey/gold/silver)

Aluminum

(space

grey/gold/silver)

Aluminum

(rose gold/space

grey/gold/silver)

Aluminum

(rose gold/space

grey/gold/silver)

Aluminum

(rose gold/space

grey/gold/silver)

Aluminum

(jet

black/black/rose

gold/gold/silver)

Aluminum

(jet

black/black/rose

gold/gold/silver)

Glass + Metal Glass + Metal Glass + Metal

Connector Lightning/8 pins Lightning/8 pins Lightning/8 pins Lightning/8 pins Lightning/8 pins

Camera (main)

Lightning and Jack Adaptor

32GB/128GB/256GB 64GB/256GB

USB Type-C

A11 w/FO-WLP

Quad Core A10

(Added 2 lower power consumption

cores)

iPhone 8/ 8 Plus

• LCD display

• Dual-camera on 8 Plus

• Storage/Memory (64/256GB,

3G DRAM)

• Touch ID/Home button

• A11 10nm FinFET

iPhone 8 Pro– Expecting a

complete form factor

overhaul.

• 5.85” OLED display (other two

are 4.7” and 5.5” w/ LCD)

• WQHD display resolution

• Display to take up edge to

edge

• 2.5D cover glass

• In display finger print, no home

button

• Glass body and metal case

• Dual camera with OIS/OIS and

auto laser focus

• A11 10nm FinFET AP

• 3G DRAM for all 3 models

• NAND 64G/256G only

• L-shaped battery

• USB Type-C

• Wireless charging

23 M

ay 2

017

iPh

on

e a

nd

its s

up

ply

ch

ain

1

2

Figure 10: BOM pressures are evident, but offsets remain …

Source: Company data, Credit Suisse estimates

iPhone 8 Pro

Component Specs Supplier Added cost 256GB New

Display & Touchscreen 5.8" OLED Display Flat Screen Samsung $27.00 $80.00 iPhone 8 Pro BOM higher by

$55

Force touch Enhanced Force Touch Broadcom IC $4.00 $14.00

Application Processor A11 processor on TSMC 10nm (potentially smaller die) Apple fabbed at TSMC $0.00 $26.90

Co-processor Cost down ($0.20) $1.80

Modem - Baseband, RF QCOM X16 10nm / INTC 7480 28nm Qualcomm and Intel $2.00 $18.00

WLAN / BT / FM / GPS Similar chip - Cost down Broadcom ($0.70) $6.30

NFC IC Similar chip - Cost down AMS ($0.25) $2.25

Memory (DRAM) Similar chip - DRAM price up Samsung $0.00 $24.00

Memory (NAND) Possible only 64/256GB Skus Toshiba, Hynix, Micron $44.80

Power amplifier + Switch Similar RF content Skyworks, Broadcom, Qorvo $8.00 Touchcreen 3D Sensing

major drivers

User Interface & Sensors 3D sensing + Gesture recognition

Bosch, Invensense, AKM, STM, Broadcom, TI +

3D sense: AMS, Himax, Lumentum/Finisar,

Viavi, Win Semi, LG Innotek

$12.00 $27.00

Fingerprint sensor Under glass sensor (remove sapphire) Apple fabbed at TSMC ($2.00) $6.00

Analog Similar contentDialog PMIC, Qualcomm PMD9635 PMIC,

Passives, TI, MXIM, ISIL$9.50

Audio Codec Cost down Cirrus Logic ($0.30) $2.70

Cameras Dual camera adds Dual OIS, but also cost down Sony, Largan ($2.00) $33.00

Battery $2.50 ASP for Pro version to rise to

offset BOM

PCB HDI + Flex PCB + Substrate Like PCB $0.00 $4.75

Charger Wireless Charging chipset $2.00 $5.00

Acoustics Dual speaker acoustics upgrade AAC, Goertek, Merry $3.80 $10.00

Haptics Similar content AAC $9.00

CasingStainless Steel frame $40-45 + 2.5D Front Glass $5 + 2.5D

back glass $10Foxconn Tech, Catcher, Jabil $10.00 $45.00

Box Contents $8.80

Total BOM cost $55.35 $389.30

Manufacturing Margin (8%) $31.14

IP Licensing (4% of BOM and Manufacturing) $16.82

ASP $1,000.00

Apple GM% 41%

Across all of the improved

hardware related features there

will be a rise in the BOM as well,

specifically in the OLED version ,

which we estimate as much as

$55 (compare to iPhone 7 Plus)

We note that for the Pro

version, the larger screen adds

$27 to BOM (compare to

iPhone 7 Plus) while 3D sensing

+ Gesture recognition adds

another $12. Phone casing adds

another $10. These three

hardware components are

responsible fo the bulk of the

BOM increase

We expect Apple to raise prices

on iPhone 8 versions of the

model, with price on the highest

skew to cross $1000. We

estimate the ASP on the highest

end skew of iPhone 8 Pro at

$1000, with GM of >40%.

23 May 2017

iPhone and its supply chain 13

Unit Outlook heading to 270 mn units at least

To assess the unit outlook for Apple iPhone business, we looked at it in three ways: (1) the

installed base model (which is our preference); (2) market share by price points; (3) and

market share by region. Based on all of these, we believe that Apple could see robust unit

growth towards 270 mn in the long term.

Installed base model, robust growth in the base help

As shown in Figure , Apple's installed base has seen robust growth over the past few

years from 440 mn at the end of 2014 to 600 mn/690 mn in 2015/2016 (+36%/+15% YoY)

despite relatively muted 6S and 7 cycles. We see the 8 Super-cycle could unleash the

pent-up demand for the 10th anniversary iPhones, driving unit shipments to

229mn/250mn/270mn in 2017/2018/2019 with the iPhone installed base expanding to

775mn/890mn/970mn. There two key assumptions here:

Figure 5: iPhone installed base growth and normalisation of replacement, we see units toward 270 mn LT

iPhone global installed base analysis (mn) 2014 2015 2016E 2017E 2018E 2019E 2020E

iPhone subs 440.0 600.0 690.0 775.0 890.0 970.0 1,025.0

Gross add 140.0 180.0 120.0 125.0 155.0 130.0 110.0

Churn 33.9 20.0 30.0 40.0 40.0 50.0 55.0

as % of subs 10.2% 4.5% 5.0% 5.8% 5.2% 5.6% 5.7%

Sub net adds 106.1 160.0 90.0 85.0 115.0 80.0 55.0

Replacement units demanded 125.2 185.3 232.3 263.3 300.0 345.1 376.1

Adjusted replacement rate 37.5% 42.1% 38.7% 38.2% 38.7% 38.8% 38.8%

Adjusted replacement cycle (in months) 32.0 28.5 31.0 31.5 31.0 31.0 31.0

Total iPhone units demanded 265.2 365.3 352.3 388.3 455.0 475.1 486.1

Second hand phones recycled into the base 75.0 135.0 135.0 159.0 205.0 205.0 216.0

iPhone unit sell-through 190.2 230.3 217.3 229.3 250.0 270.1 270.1

iPhone units Sell-in 191.0 233.0 214.3 229.3 250.0 270.1 270.1

yoy % 26.0% 22.0% -8.0% 7.0% 9.0% 8.0% 0.0%

Source: Company data, Credit Suisse estimates

Replacement or upgrade rate. We note that the rate of Apple replacement or upgrades

has tended to fluctuate with the significance of the new features. This has been anywhere

between 28.5 months and 32 months (see Figure ). Additionally, any long-term

assumption needs to take into account changes in the regional mix as well. The iPhone

replacement cycle was 31.5 months in 2016, by our estimate. As Apple has one of the

fastest upgrade rates versus other brands, we assume a slight acceleration going forward

to 31 months.

Android switchers or gross adds. We note that a more competitive offering could also

mean that gross additions from other Android users should grow. We note that in 2015 this

reached 180 mn. However, going forward, we assume 155 mn in 2018, before declining to

130 mn/110 mn in 2019/2020.

Market share price point—growing the high end again

While 1.4 bn smartphones were sold in 2016 and we expect 1.6 bn in 2017, we note that

Apple has continued its premium segmentation and is really only operating in the above-

US$350 ASP segment. We point out that in the premium segment with an ASP above

US$700, iPhone commands a 74% market share and so by itself can be a driver of the

market. In the market with an ASP between US$500 and US$700, Apple takes ~50%

market share.

23 May 2017

iPhone and its supply chain 14

Figure 6: iPhones dominate the higher end market with ASP above US$500

iPhone share by price band 2013 2014 2015 2016 2017E 2018E 2019E

Global market 1,018,738 1,301,690 1,437,250 1,433,893 1,552,061 1,694,088 1,799,905

Apple units 153,448 192,650 231,530 215,403 228,986 249,828 270,054

% of market 15% 15% 16% 15% 15% 15% 15%

<US$200 442,369 668,226 770,022 737,663 819,816 874,914 926,647

Apple units 24 0 48 763 170 314 68

% of <US$200 market 0% 0% 0% 0% 0% 0% 0%

US$200-300 137,722 159,540 172,857 211,224 207,648 238,102 246,890

Apple units 55 1,898 1,250 5,849 4,776 2,381 5,678

% of US$200-300 market 0% 1% 1% 3% 2% 1% 2%

US$300-400 78,876 97,698 100,879 139,008 144,342 157,550 167,391

Apple Units 7,290 9,898 3,687 11,919 8,661 9,453 10,043

% of US$300-400 market 9% 10% 4% 9% 6% 6% 6%

US$400-500 67,218 63,710 59,961 59,111 62,082 67,764 71,996

Apple units 11,775 12,094 7,218 16,293 11,796 10,842 9,432

% of US$400-500 market 18% 19% 12% 28% 19% 16% 13%

US$500-700 187,641 189,282 153,988 141,733 155,206 169,409 215,989

Apple units 73,617 79,631 85,923 72,670 80,707 83,349 112,314

% of US$500-700 market 39% 42% 56% 51% 52% 49% 52%

US$700+ 104,913 123,235 179,542 145,154 162,966 186,350 170,991

% of Global market 10% 9% 12% 10% 11% 11% 10%

Apple units 60,686 89,130 133,405 107,910 122,877 143,489 132,518

% of US$700+ market 58% 72% 74% 74% 75% 77% 78%

Source: Company data, Credit Suisse estimates

US$500+ ASP segment has grown to unprecedented levels … Based on our

expectations for the iPhone8 as well as Samsung Galaxy 8's sales so far, we now believe

that the premium segment will grow and rise to 204 mn/227 mn/245 mn for Apple in

2017/2018/2019. Specifically, we note that the premium tier at the very high end with ASP

above US$700 is set to expand to 163mn/186mn/171mn in 2017/2018/2019. We believe

that such growth comes at the expense of alternative computer devices, mainly the tablet

market.

Apple gaining … Samsung losing. In the above-US$500 smartphone market, Apple has

enjoyed a market share above 60% over the past 2-3 years. We expect it to maintain the

same dominant position in the premier tier, but grow share in the US$700+ market with the

success of the iPhone 8. We expect this share gain for Apple to come at the expense of

Samsung, and that Samsung's market share will decline to 25% in the US$500+ market in

two years from 37% in 2013.

23 May 2017

iPhone and its supply chain 15

Figure 7: High-end market to grow driven by iPhone … Figure 8: … iPhone dominates with a 64% market share

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Market share by region—NA drives growth and an inflection in China

As shown in Figure , Apple's market share has kept constant at 15-16% globally, but has

seen fluctuations regionally, based on its product cycles. We note that in the past year

there have been very different geographic trends—with North America (NA) stronger and

China weaker. We believe that based on the quality of its offering of the iPhone 8 cycle,

Apple could further increase its strength in NA as well as in China.

Figure 9: Apple maintain 15% global market share—stronger in North America and weaker in China

iPhone market share by region 2013 2014 2015 2016 2017 2018 2019

APAC (ex. Japan) 8.6% 9.2% 12.5% 9.5% 9.5% 9.7% 10.3%

Western Europe 19.6% 21.2% 23.6% 26.3% 25.0% 25.0% 25.0%

Japan 41.0% 50.0% 47.3% 51.4% 51.0% 50.0% 50.0%

North America 39.3% 38.4% 39.3% 38.1% 39.2% 39.3% 39.3%

CEMA 7.7% 7.7% 7.4% 7.6% 7.6% 7.6% 7.6%

Latin America 5.5% 5.2% 4.7% 5.1% 5.0% 5.0% 5.0%

Total as % of global market share 15.1% 14.8% 16.1% 15.0% 14.8% 14.7% 15.0%

Source: Company data, Credit Suisse estimates

Market share woes in China a concern, but we believe more a function of product

cycles. As shown in Figure , Apple's market share in China has come under severe

pressure, declining from 12.5% at its peak to 9.5% now. We note, however, that this has

been much more a function of its product cycle and believe that its replacement rates tend

to vary year to year.

0

50

100

150

200

250

300

350

400

2013 2014 2015 2016 2017E 2018E 2019E

ASP

$5

00

+ u

nit

s (m

n)

Apple Samsung Huawei Other

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013 2014 2015 2016 2017E 2018E 2019E

Apple Samsung Huawei Other

23 May 2017

iPhone and its supply chain 16

Figure 10: Apple's share in China fluctuates more with the product cycle

Source: Company data, Credit Suisse estimates

Our conviction at this point comes from the fact that iOS users are quite similar globally.

Indeed, as we note in Figure iOS users tend to have high levels of services attached.

Even in Emerging Markets, this is ~90%, as well as high levels of income (according to our

survey). They are also as invested in terms of app downloads as shown in Figure . In other

words, the market share volatility shown in Figure is a function of varying replacement

rates, rather than losing users in China to rivals. We believe that the iPhone upgrade rates

could accelerate with the upcoming product cycle, driving unit growth and market share

gains in China.

Figure 11: Apple's EM invested in the ecosystem... Figure 18: ...and download and use more apps

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Raising price could offset BOM pressure

With the introduction of OLED, wireless charging and an all-glass display, Apple could see

a rise in its BOM. However, we believe that Apple can raise prices to offset some BOM

pressures. We have slightly adjusted our view on pricing and we now assume

US$670/US$770/US$900 for the three devices at launch.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Brazil China India Indonesia Russia South

Africa

Turkey Mexico

iOS Services Attach

0

5

10

15

20

25

30

35

40

45

China India South

Korea

Brazil US Japan UK

Nu

mb

er

of

Ap

ps

23 May 2017

iPhone and its supply chain 17

Figure 19: Highest-end ASP has been rising … Figure 12: … while high-end mix has been solid

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Successfully increasing price for some time now. Apple has increased prices historically. It

has raised prices on the highest end offerings twice in the past three years, first with the 6

Plus, where the highest offering ASP increased from US$849 to US$949 and then again

with the 7 Plus, which was increased to US$969. We note that despite increasing the price

of its phones (e.g. the 6 Plus was US$100 more than any phone it had ever introduced),

Apple has seen strong demand. In fact, we see that demand for the 7 Plus is significantly

outweighing supply, even with the extra US$20 price tag. As such, we believe that even if

Apple raises the price on its OLED iPhone, it will still continue to see a positive mix shift to

the high end.

Figure 13: Apple has room to raise prices given Samsung Galaxy's pricing points

Source: Company data, Credit Suisse estimates

Samsung's S8 pricing bodes well for an iPhone price increase. Historically, the iPhone has

always commanded higher prices than Samsung's competing models, even when

Samsung's model featured better specs. For example, the basic version of the iPhone 6S

featured 16GB storage with a US$650 price tag, US$50 higher than the competing

$700

$750

$800

$850

$900

$950

$1,000

iPhone 432GB

iPhone 4s64GB

iPhone 564GB

iPhone 5s64GB

iPhone 6Plus 128GB

iPhone 6sPlus 128GB

iPhone 7Plus 128GB

$600

$650$640

$650

$600

$650

$750

$600

$650

$700

$750

$600

$650

$700

$770

$720

$670

$825

$770

$900

$500

$550

$600

$650

$700

$750

$800

$850

$900

Gala

xy

S3

-16

G

iPh

on

e 5

-16

G

Gala

xy

S4

-16

G

iPh

on

e 5

S-1

6G

Gala

xy

S5

-16

G

iPh

on

e 6

-16

G

iPh

on

e 6

Plu

s-1

6G

Gala

xy

S6

-32

G

iPh

on

e 6

S-1

6G

Gala

xy

S6

Ed

ge

-32G

iPh

on

e 6

S P

lus-1

6G

Gala

xy

S7

-32

G

iPh

on

e 7

-32

G

Gala

xy

S7

Ed

ge

-32G

iPh

on

e 7

Plu

s-3

2G

Gala

xy

S8

-64

G

iPh

on

e 8

-3

2G

Gala

xy

S8

Plu

s-6

4G

iPh

on

e 8

Plu

s -

32G

iPh

on

e -

Pro

-6

4G

2012 2013 2014 2015 2016 2017

23 May 2017

iPhone and its supply chain 18

Samsung Galaxy S7 model that had 32Gb storage. In March 2017, Samsung released the

Galaxy S8 at US$720 for the 64GB model and the Galaxy S8 Plus at US$825 for the

64GB model. Given Apple's ability to historically secure at least a 10% premium (which

does not appear to have impacted demand), we believe that our assumption of the starting

prices of the 8/8Plus/8 Pro could prove conservative at US$670/US$770/US$900.

Samsung Galaxy S8 series sales strong despite higher pricing and brand damage. After

Samsung's launch of the Galaxy S8/S8 Plus, sales have been strong, with 5mn reportedly

sold so far, despite higher price tags and some brand damage caused by the Note 7 last

year. We believe this indicates that consumers are ready to pay up for premier tier

smartphones as long as there are sufficient new innovations. This, in turn, bodes well for

the upcoming iPhone 8 Cycle.

What about elasticity? Clearly, in any discussion around price, it is hard to argue against

an impact in terms of elasticity of demand. While this is also the case for the iPhone

business, we believe that the combination of improvements in functionality, a high

retention rate of the eco-system and an affluent user base means that the impact on

demand could actually be negligible.

Income levels of Apple users higher than non-Apple users

We also note that Apple users have higher levels of income, versus non-Apple users,

indicating greater ability on Apple's part to raise prices. We see that iPhone users in the

US and Emerging Markets earn 55%/25% more than non-Apple users. In fact, the average

annual income of iPhone users is higher than the average annual income of Android users

in every country we surveyed earlier this year.

Figure 14: Apple US users earn 55% more … Figure 15: In EM, Apple users earn 25% more …

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Better mix could have material benefit

An improving mix towards the higher-end offering will also help offset GM pressure from a

potential BOM increase. We note here that with the introduction of an OLED screen,

wireless charging, and an all-glass enclosure, Apple could very likely experience a shift in

its mix towards the highest end phones. Indeed, the initial build data suggest that

somewhere around 50% of the overall volumes could be for the iPhone 8 Pro. We believe

this can have a material impact on the EPS power for several reasons.

ASP accretive, materially GP/Unit accretive. Even allowing for the higher BOM, discussed

before, we note that the OLED version will likely have an ASP that is 26% accretive to the

iPhone business, the GM at 42% about 400bp accretive, and GP per unit that would be

~40% higher. Given this, a mix shift towards such a product line would likely have a

material impact on the outcome to estimates.

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

China India Indonesia Russia South

Africa

Turkey Mexico

iOS User Android User

23 May 2017

iPhone and its supply chain 19

Figure 16: Pro model is accretive to iPhone (Hardware only) GM

Source: Company data, Credit Suisse estimates

A long-term shift to highest end tier. While Apple already operates in the high end of the

smartphone market, what has been surprising is that there has been a continued shift

towards Apple's highest end tier of the portfolio. Indeed, we see the Plus/Pro range rising

to above 40% of volume recently, as shown in Figure .

Figure 17: Mix has been shifting to higher end models ...

Source: Company data, Credit Suisse estimates

OLED mix shift is important. We assume 45% of the new portfolio mix will be OLED in

2H17. While there are many moving parts to this analysis, the initial build plans for 2H17

for the iPhone 8 are expected to be 100–110 mn units (25–30 mn units in the September

quarter and 75–80 mn units in the December quarter), which is up around 0-10% versus

the iPhone 7 builds of roughly 100 mn units. We would note that given the accretion

discussed before that the model is very sensitive to such an assumption, both GM and

EPS, as we show in Figure .

$452

$659

$752

$871

$135

$219

$297

$364

29.9%33.2%

39.5% 41.7%

Average: $693

Average: $259

Average: 37.5%

Old iPhone 8 Plus Pro Old iPhone 8 iPhone 8

Plus

Pro Old iPhone 8 iPhone 8

Plus

Pro

ASP GP($) per unit GM (%)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

CY13 CY14 CY15 CY16 CY17E

Base Plus/Pro

23 May 2017

iPhone and its supply chain 20

Figure 18: iPhone output by form factor

Source: Company data, Credit Suisse estimates—based upon build estimates

ASP rising to US$676/US$704, revenues heading up to US$155 bn/US$176 bn in

CY17/18. As shown, we assume that the ASP for the iPhone business moderately grows

from US$647 in 2016 to US$676/US$704 in CY17/18. This is based on the mix of the

iPhone 8 Pro becoming 40-45% of volume going forward. Combined with our projected

unit growth, we now see iPhone revenues growing to US$155 bn/US$176 bn from

US$139 bn in 2016 or growth of 11%/14%.

Services is GM accretive and an increasing GP mix. We see material growth in Apple's

Services segment, which should help offset the GM impact long term. Management

expects services to double over the next four years, in line with our forecasts in our note

AAPL: Services Update – The Annuity Continues. As such, we see a material potential for

Apple's Services, with growth being driven by the App Store, an inflection in Apple Music

revenues and iCloud. We believe Services can grow from 20% of GP in FY16 to one third

of GP long term, and with Services being ~70% GM business, should help Apple’s GM

long term.

We note that services growth can absorb 250-300bp of iPhone GM pressure, as it

contributes incremental GP to overall corporate.

Figure 27: Apple Services could offset 250-300bp GP pressure from iPhones

(US$ mn, unless otherwise stated)

2016 2017 2018 2019

Services revenue 25,464 31,083 37,652 45,183

Services GP 17,500 21,741 26,394 31,673

Services GM 68.7% 69.9% 70.1% 70.1%

as % of corp. GM 21% 24% 25% 28%

Incremental GP 3,022 4,241 4,653 5,279

Average incremental GP 4,299 4,299 4,299 4,299

iPhone revenues 139,443 154,849 175,928 182,625

Margin pressure offset 308bp 278bp 244bp 235bp

Source: Company data, Credit Suisse estimates

Scenarios analysis—US$14 EPS power in bull case

The issue for Apple investors is that while the feature upgrade is arguably well understood

and therefore the potential impact on units, what is less clear is how consumers will

respond to a price increase and the resulting mix. This can have, per our analysis, a major

impact on the fundamental EPS power that Apple sees as result of the upcoming product

cycle. We believe that the key sensitivity concerns the price of the iPhone 8 Pro, the mix

mn untis, as a % of total CY2014 CY2015 CY2016CY2017

as of 2017/5

4" incl. SE 51.6% 10.5% 18.2% 8.9%4.7"/5.5" old models 0.0% 55.2% 37.8% 44.4% 4.7" 0.0% 69.5% 70.4% 54.9% 5.5" 0.0% 30.5% 29.6% 45.1%4.7"/5.5"/5.8" new models 48.4% 34.3% 44.0% 46.7% 4.7" 72.8% 70.0% 58.0% 26.2% 5.5" 27.2% 30.0% 42.0% 15.7% 5.8" OLED 0.0% 0.0% 0.0% 58.1%Total 100.0% 100.0% 100.0% 100.0% 4" 51.6% 10.5% 18.2% 8.9% 4.7" 35.3% 62.4% 52.1% 36.6% 5.5" 13.2% 27.1% 29.7% 27.4% 5.8" OLED 0.0% 0.0% 0.0% 27.1%

23 May 2017

iPhone and its supply chain 21

and the replacement rate. Below are three scenarios we analyse in Error! Reference

source not found.:

Base case: In our base case, we assume 45%/40%/35% of the Pro mix in

2017/2018/2019 with blended ASPs at US$676/US$704/US$676, which results in EPS of

US$9.50/US$11.95/US$13.16 in 2017/2018/2019.

Bull case: In the bull case, we assume the same mix and ASP, but raise units to

271 mn/293 mn, driven by 29 months of replacement cycle seen in the iPhone 6 Cycle.

This results in EPS of US$9.50/US$12.76/US$14.05 in 2017/2018/2019.

Bear case: In the bear case, we assume a 25% Pro mix over the new phones for future

years and assume that the BOM is US$10-15 higher than the base case for the new

phones, resulting in a lower GM of about 36%. In this case, we see EPS of

US$9.11/US$10.90/US$12.33.

Figure 19: Apple iPhone Scenario analysis—a range of outcomes but EPS power of US$14 in the bull case

Source: Company data, Credit Suisse estimates

23 May 2017

iPhone and its supply chain 22

Display, casing, 3D-sensing: Likely major changes

OLED—the new path for iPhone displays

One major change in the upcoming iPhone 8 release will be the usage of OLED display for

the first time. AAPL has begun using OLED screens on its watches, which is now

spreading to iPhones. We do not rule out OLED display adoption in the iPad in the near

future. Among the three iPhone 8 models, in our base case, we believe only the Pro

version will be launched using flexible OLED displays, which should enable a thinner and

more energy efficient device—the merits for which OLED is known. Adopting flexible

OLED also indicates some intention to bend the display around the edges to enable

design changes. Other two models will continue to use LTPS TFT-LCD displays. The

OLED display size should be 5.8 inches with about 5.15 inches of usable area and with

minimum amount of bezel area should enable a very compact form factor. Current intent is

to remove the physical "Home Button" and replace it with a "Virtual Button" on the OLED

screen. The uncertainty revolves around embedding the Touch ID and ambient light

sensor into the OLED screen. If the technology is not successful given the tight product

launch timeline, the Touch ID could be placed on the back of the device.

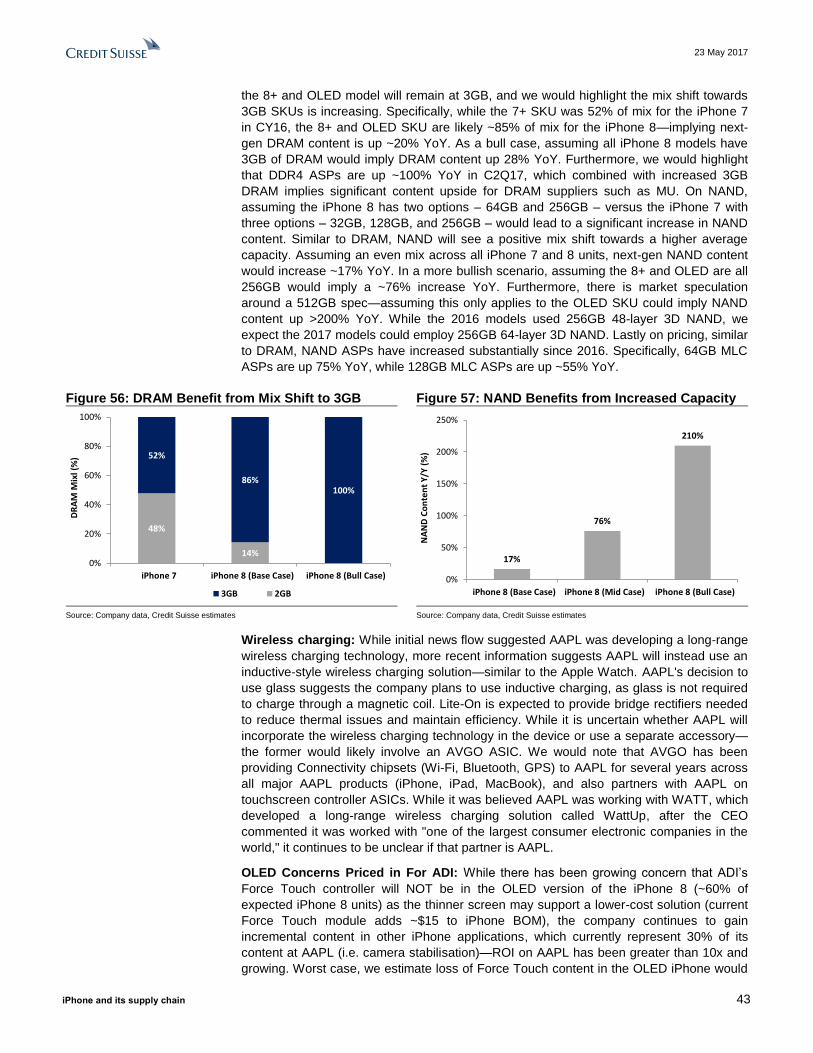

Figure 29: Samsung's OLED capacity growth trend into 2020E (mobile only,

based on glass output area)

Source: Company data, Credit Suisse estimates

We also believe that 100% of AAPL's initial OLED requirement in 2017 will be supplied by

Samsung. Samsung remains the most critical component supplier for AAPL that includes

memory semiconductor solutions such as the LP DDR4 DRAM and NAND flash, and now

OLED. Samsung is the only supplier in the world with a proven track record in OLED

display. Also, Samsung's IP related to OLED and extensive control of its supply chain can

guarantee the high volume required by AAPL. We believe that the Samsung A3 6G OLED

fab will be the facility that will manufacture for AAPL. Terms of long-term supply contracts

have already been agreed, with AAPL active in qualifying not only Samsung, but many of

its raw material suppliers.

Sufficient OLED capacity safeguard in place

According to our AAPL analyst, Kulbinder Garcha, AAPL is likely to ship about 41 mn

iPhone 8 Pro devices during 4Q17. An additional 43 mn iPhone 8 Pro units are expected

to be shipped in 2018. If the following version iPhone 9 Series in 2018 all adopt OLED

displays, then AAPL will likely require 128 mn OLED displays in 2018 (iPhone 8 Pro and

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2010 2011 2012 2013 2014 2015 2016 2017E 2018E 2019E 2020E

(K m²)

Samsung Display LG Display AUO BOE

GoVisionox EverDisplay JDI

Keon Han Jerry Su

23 May 2017

iPhone and its supply chain 23

all iPhone 9 Series. As Samsung will likely remain the sole supplier, sufficient capacity

must be prepared to ensure a guaranteed supply incorporating potentially low product-

yield scenarios. According to our analysis, more than enough safe guards are in place by

Samsung to ensure ample supply of OLED panels to AAPL, to compensate for low

production yields or better-than-expected iPhone volume sales.

As a base case, if AAPL is scheduled to ship 41 mn OLED iPhones by 4Q17, this implies

Samsung would need ~60 mn OLED panels dedicated to AAPL, with inventory preparation

beginning at least several months ahead. We believe that three 6G OLED lines are

already production-ready in the AAPL-dedicated A3 fab and the capacity will grow to four

lines in 3Q17 and six by 4Q17. The A3 fab is expected to be full, running nine lines by

2Q18. According to our estimates, the capacity ramp-up schedule will enable a total

production of 64 mn 5.8-inch OLED panels in 2017 under a 43% average yield

assumption. By 2018, Samsung will be able to produce over 240 mn OLED panels for

AAPL with a 74% yield assumption under the current capacity expansion plan. This

suggests that even if all of AAPL's 230 mn iPhones were to adopt OLED, Samsung would

have sufficient capacity to cover the entire demand. Therefore, we believe there is

sufficient capacity prepared to hedge against various operating conditions.

Figure 30: Quarterly 5.8-inch OLED panel production for AAPL with yield rates

Source: Company data, Credit Suisse estimates

The only other potential supplier could be LG Display during the early phase. However,

LGD's first 15K of 6G flexible OLED capacity will not be ready until 2H17 and is dedicated to

its automobile and Chinese smartphone makers. Negotiation to supply AAPL is ongoing, so

from a timing perspective, LGD could supply AAPL by 2H18 with additional 15K of 6G

capacity announced. LGD is currently reviewing its 2017/2018 OLED strategy to potentially

increase capacity further provided large customers commit long-term to capacity.

Samsung's OLED sales to AAPL should prove to be lucrative

Attaining AAPL as a new OLED panel customer should prove to be a very lucrative move

for Samsung. First, all OLED panels destined for AAPL are flexible OLED which

commands a substantial price premium over Rigid OLED. For example, the 5.8-inch OLED

display module to AAPL should average about US$80 per device compared to about a

US$25 ASP for the current Rigid (glass-based) OLED. Currently, Samsung produces

flexible OLED primarily for its own use in its flagship smartphone devices. All incremental

panel volume ordered from AAPL will be higher priced flexible OLED that will improve the

overall mix and increase the blended ASP. Even with a lower yield rate assumption and

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

10

20

30

40

50

60

70

1Q17 2Q17E 3Q17E 4Q17E 1Q18E 2Q18E 3Q18E 4Q18E 1Q19E 2Q19E 3Q19E 4Q19E

Panel outputs(5.8",mn) Yield rates (RHS)

mn units

23 May 2017

iPhone and its supply chain 24

rising fixed cost associated with start-up of a new fab, the ASP is high enough not to dilute

Samsung's current profit margin structure of around ~20% OPM.

Second, capacity roll-out, ASP and volume agreements were likely set at low-yield rates of

~50%. The normalised yield rate at the current flexible OLED line is substantially higher at

75%. As a more mature technology, rigid OLED yields are higher at 80%. We surmise that

since additional lines in the A3 fab set up for AAPL are essentially the same line Samsung

is currently using on its own products, little risk exists on the production side, except for

some change in OLED materials used at the request of AAPL. Therefore, higher yields

can provide substantial upside to OPM assumptions on higher productivity in addition to

freeing up capacity to supply other external customers, where supply remains in shortage.

According to our analysis Samsung should be able to more than double its OLED revenue

from W15.4 tn in 2016 to W34.9 tn in 2018, mostly driven by the new, incremental OLED

business from AAPL. We expect that by 2018, the OLED revenue contribution derived

from AAPL will surpass Samsung’s own internal OLED sales to its smartphone division,

given the richer mix and higher ASP. Maintaining a stable OPM rate assumption of ~20%,

we calculate the OP contribution from AAPL business to be W1.1 tn in 2017 and could

potentially rise to about W3.5 tn in 2018. This would account for 25% of Samsung's OLED

OP in 2017, rising to 56% by 2018.

Figure 201: Total square metre OLED capacity consumed by AAPL (glass input

based)

Source: Company data, Credit Suisse estimates

0%

10%

20%

30%

40%

50%

60%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17E 3Q17E 4Q17E 1Q18E 2Q18E 3Q18E 4Q18E

AAPL Samsung/Others % of AAPL to total Samsung OLED capacity (RHS)

'000 m2

23 May 2017

iPhone and its supply chain 25

Figure 32: AAPL’s annualised OLED profit to Samsung

Source: Company data, Credit Suisse estimates

Possible negative impact on backlight and traditional TFT supply chain

The adoption of OLED panels for iPhone display will negatively impact the backlight

supply chain. Radiant currently is the main backlight supplier for the 5.5-inch iPhone with

~60% allocation. iPhone accounted for ~20% of its 2016 revenue and we believe this will

decline to ~9% by 2018 and could eventually drop to a minimum when all new iPhones

adopt OLED display.

Chipbond could also see negative impact in 2017 as it is the sole backend supplier for the

driver IC used on TFT iPhone (~12% of sales in 2016). Nevertheless, we think the iPhone

shifting to OLED could hurt its 2017 sales by 6%, but it should be offset by the TDDI ramp

and more RF bumping revenue. We think that Chipbond will be able to regain some share

in 2H18, after JDI, LGD, or Sharp start to supply OLED panels for iPhone.

Casing/ cover glass: A major change in all iPhone 8s

We expect the casing design for all three models will be changed from current aluminium

full unibody case, to "glass cover + metal frame" design. We expect the OLED model will

use stainless steel, to provide a thinner and stronger frame, while the LTPS models will

use an aluminium alloy frame. We believe that the casing design change is not only to

provide a fresh look for the iPhone, but also to facilitate the adoption of wireless charging.

We believe the stainless steel frame will be ASP comparable to the aluminium full unibody

casing, but the aluminium frame will be ASP dilutive (by 20%). We also believe the design

change (by combining the cover glass to metal frame) will require sub-assembly work to

be done by the metal casing makers, i.e. Catcher and Hon Hai.

1. Total # of 5.8" OLED panels (mn units) 2016 2017E 2018E 2019E 2020E

Panel inputs (5.8", mn) 41 133 347 367 367

Yield rates (annual avg) 0% 43% 74% 75% 75%

Utilization rates (% , annual avg) 0% 83% 95% 95% 95%

Market shares (%) 100% 100% 100% 100% 100%

Panel outputs(5.8",mn) 0 64 243 261 261

ASP(US$, avg) $0 $79 $69 $59 $50

ASP YoY (%) n/a n/a -12% -15% -15%

USD/KRW 1150 1150 1150 1150 1150

Revenue (Wbn) 0 5,755 19,346 17,728 15,057

OPM(%) 18% 20% 18% 18% 17%

OP(Wbn) 0 1,165 3,531 3,102 2,560

2. Earnings impact to Samsung

% of sales impact on the division/total (Wbn) 2016 2017E 2018E 2019E 2020E

SEC's OLED sales(Wbn) 15,360 23,246 34,902 42,927 49,016

SEC's total sales(Wbn) 201,867 238,508 272,705 289,887 303,801

Sales from OLED supply to AAPL(Wbn) 0 5,755 19,346 17,728 15,057

% to SEC's OLED sales 0% 25% 55% 41% 31%

% to SEC's total sales 0% 2% 7% 6% 5%

% of sales impact on the division/total (Wbn) 2016 2017E 2018E 2019E 2020E

SEC's OLED OP(Wbn) 2,784 4,721 6,333 7,493 8,333

SEC's total OP(Wbn) 29,241 50,653 57,046 60,921 61,792

OP from OLED supply to AAPL(Wbn) 0 1,165 3,531 3,102 2,560

% to SEC's OLED OP 0% 25% 56% 41% 31%

% to SEC's total OP 0% 2% 6% 5% 4%

Pauline Chen Sam Li

23 May 2017

iPhone and its supply chain 26

Figure 33: New iPhone casing spec expectations

4.7" iPhone 5.5" iPhone OLED iPhone

Back cover 2.5D glass 2.5D glass 2.5D glass

Metal frame Al alloy Al alloy Stainless steel

Source: Company data, Credit Suisse estimates

Rather than a one-time upgrade to two-side glass (both 2.5D) at Apple for cosmetic and

wireless charging considerations, we see more reasons for a sustainable cycle for the

industry, such as more adoption of wireless charging in mid-term and 5G in the long run

(for back casing), or to cover curved AMOLED screens (for cover lens). In addition to

simple volume growth, we also see a clear ASP improvement path for glass ASPs. From