investors’ call presentation full year 2016 … · investors’ call presentation full year 2016...

TRANSCRIPT

INVESTORS’ CALL PRESENTATION

FULL YEAR 2016 AND

Q1 2017 RESULTS

POSITIONED FOR RECOVERY

AND GROWTH

2

This presentation contains or incorporates by reference

‘forward-looking statements’ regarding the belief or current

expectations of Diamond Bank, the Directors and other

members of its senior management about the Group’s

businesses and the transactions described in this presentation.

Generally, words such as ‘‘could’’, ‘‘will’’, ‘‘expect’’, ‘‘intend’’,

‘‘anticipate’’, ‘‘believe’’, ‘‘plan’’, ‘‘seek’’ or similar expressions

identify forward-looking statements.

These forward-looking statements are not guarantees of future

performance. Rather, they are based on current views and

assumptions and involve known and unknown risks,

uncertainties and other factors, many of which are outside the

control of the Company and/or its Group and are difficult to

predict, that may cause actual results to differ materially from

any future results or developments expressed or implied from

the forward-looking statements. Such risks and uncertainties

include, but are not limited to, regulatory developments,

competitive conditions, technological developments and

general economic conditions. The Bank assumes no

responsibility to update any of the forward looking statements

contained in this presentation.

Any forward-looking statement contained in this presentation

based on past or current trends and/or activities of Diamond

Bank should not be taken as a representation that such trends

or activities will continue in the future. No statement in this

presentation is intended to be a profit forecast or to imply that

the earnings of the Company for the current year or future

years will necessarily match or exceed the historical or

published earnings of the Company. Each forward-looking

statement speaks only as of the date of the particular

statement. Diamond Bank expressly disclaims any obligation

or undertaking to release publicly any updates or revisions to

any forward-looking statements contained herein to reflect any

change in Diamond Bank’s expectations with regard thereto or

any change in events, conditions or circumstances on which

any such statement is based.

3

OVERVIEW

UZOMA DOZIE

CEO

STRATEGY &

BUSINESS

UPDATE

UZOMA DOZIE

CEO

FY 2016 & Q1

2017 RESULTS

& ANALYSIS

CHIUGO NDUBISI

CFO

2017

OUTLOOK &

CONCLUSION

UZOMA DOZIE

CEO

Q&A

5

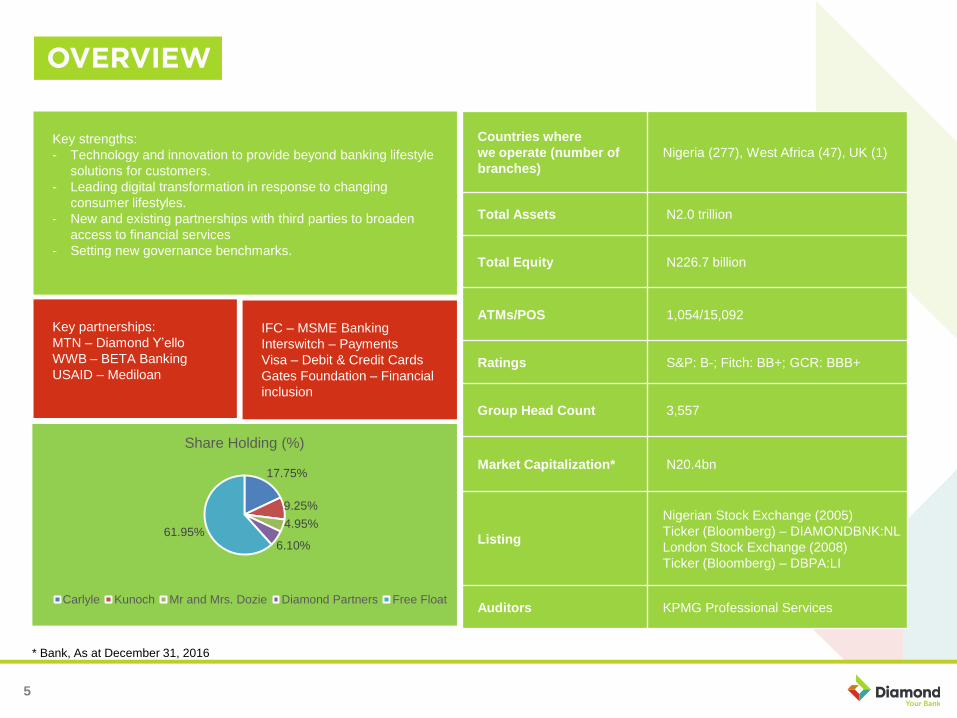

Key strengths:

- Technology and innovation to provide beyond banking lifestyle

solutions for customers.

- Leading digital transformation in response to changing

consumer lifestyles.

- New and existing partnerships with third parties to broaden

access to financial services

- Setting new governance benchmarks.

Key partnerships:

MTN – Diamond Y’ello

WWB – BETA Banking

USAID – Mediloan

Countries where

we operate (number of

branches)

Nigeria (277), West Africa (47), UK (1)

Total Assets N2.0 trillion

Total Equity N226.7 billion

ATMs/POS 1,054/15,092

Ratings S&P: B-; Fitch: BB+; GCR: BBB+

Group Head Count 3,557

Market Capitalization* N20.4bn

Listing

Nigerian Stock Exchange (2005)

Ticker (Bloomberg) – DIAMONDBNK:NL

London Stock Exchange (2008)

Ticker (Bloomberg) – DBPA:LI

Auditors KPMG Professional Services

IFC – MSME Banking

Interswitch – Payments

Visa – Debit & Credit Cards

Gates Foundation – Financial

inclusion

17.75%

9.25%

4.95%

6.10%61.95%

Share Holding (%)

Carlyle Kunoch Mr and Mrs. Dozie Diamond Partners Free Float

* Bank, As at December 31, 2016

6

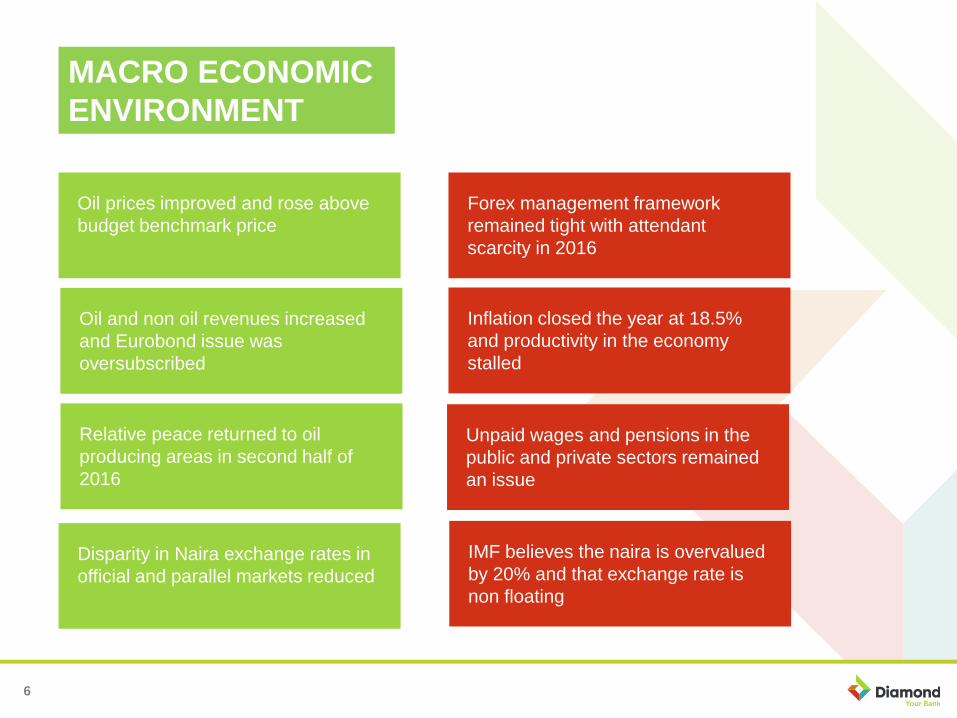

Oil prices improved and rose above

budget benchmark price

Oil and non oil revenues increased

and Eurobond issue was

oversubscribed

Relative peace returned to oil

producing areas in second half of

2016

Forex management framework

remained tight with attendant

scarcity in 2016

Inflation closed the year at 18.5%

and productivity in the economy

stalled

Unpaid wages and pensions in the

public and private sectors remained

an issue

IMF believes the naira is overvalued

by 20% and that exchange rate is

non floating

Disparity in Naira exchange rates in

official and parallel markets reduced

MACRO ECONOMIC

ENVIRONMENT

7

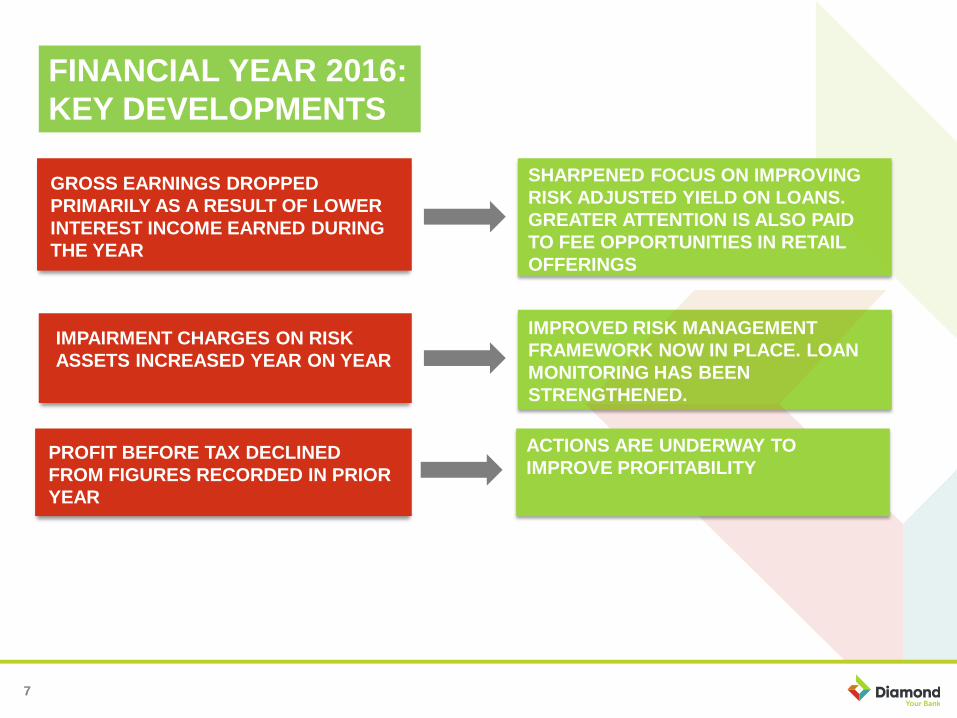

GROSS EARNINGS DROPPED

PRIMARILY AS A RESULT OF LOWER

INTEREST INCOME EARNED DURING

THE YEAR

SHARPENED FOCUS ON IMPROVING

RISK ADJUSTED YIELD ON LOANS.

GREATER ATTENTION IS ALSO PAID

TO FEE OPPORTUNITIES IN RETAIL

OFFERINGS

IMPAIRMENT CHARGES ON RISK

ASSETS INCREASED YEAR ON YEAR

IMPROVED RISK MANAGEMENT

FRAMEWORK NOW IN PLACE. LOAN

MONITORING HAS BEEN

STRENGTHENED.

FINANCIAL YEAR 2016:

KEY DEVELOPMENTS

PROFIT BEFORE TAX DECLINED

FROM FIGURES RECORDED IN PRIOR

YEAR

ACTIONS ARE UNDERWAY TO

IMPROVE PROFITABILITY

8

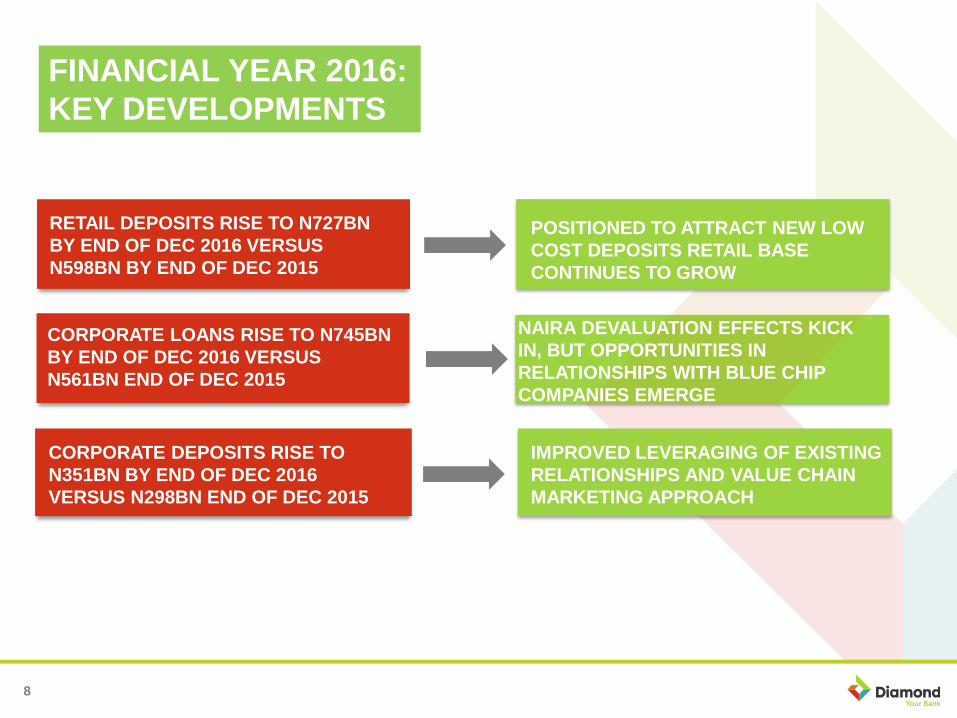

CORPORATE LOANS RISE TO N745BN

BY END OF DEC 2016 VERSUS

N561BN END OF DEC 2015

NAIRA DEVALUATION EFFECTS KICK

IN, BUT OPPORTUNITIES IN

RELATIONSHIPS WITH BLUE CHIP

COMPANIES EMERGE

FINANCIAL YEAR 2016:

KEY DEVELOPMENTS

CORPORATE DEPOSITS RISE TO

N351BN BY END OF DEC 2016

VERSUS N298BN END OF DEC 2015

IMPROVED LEVERAGING OF EXISTING

RELATIONSHIPS AND VALUE CHAIN

MARKETING APPROACH

RETAIL DEPOSITS RISE TO N727BN

BY END OF DEC 2016 VERSUS

N598BN BY END OF DEC 2015

POSITIONED TO ATTRACT NEW LOW

COST DEPOSITS RETAIL BASE

CONTINUES TO GROW

9

RETAIL

BANKING

• Technology led customer acquisition and service delivery

• Innovation and expansion of service options on ADCs

• Spread our footprint without increasing the traditional banking channels

• Migrate more customers to the electronic banking channels and cards

• Develop additional merchant relationships

• Increase volume of asset finance loans and advances

• Retain status as a leading agent of financial inclusion

VALUE CHAIN Promoting business synergy between corporate, Retail/MSME and business

banking

Connect people and markets

Promote collaboration with ecosystem partners to create value for customers

COST CONTAINMENT Improve ADC uptake to reduce cost of branch services

Balance sheet management – guided growth to contain AMCON fees, NDIC

premium etc.

Zero by 2017 – Non value adding processes and resources

Reduce cost of funds by leveraging financial inclusion

IMPROVED

UNDERWRITING & RISK

MANAGEMENT

• Strengthen enterprise risk management framework.

• Improve post disbursement loan monitoring.

• Focus on recoveries from delinquent or previously written off loans.

STRATEGY AND

BUSINESS UPDATEUZOMA DOZIE, CEO

11

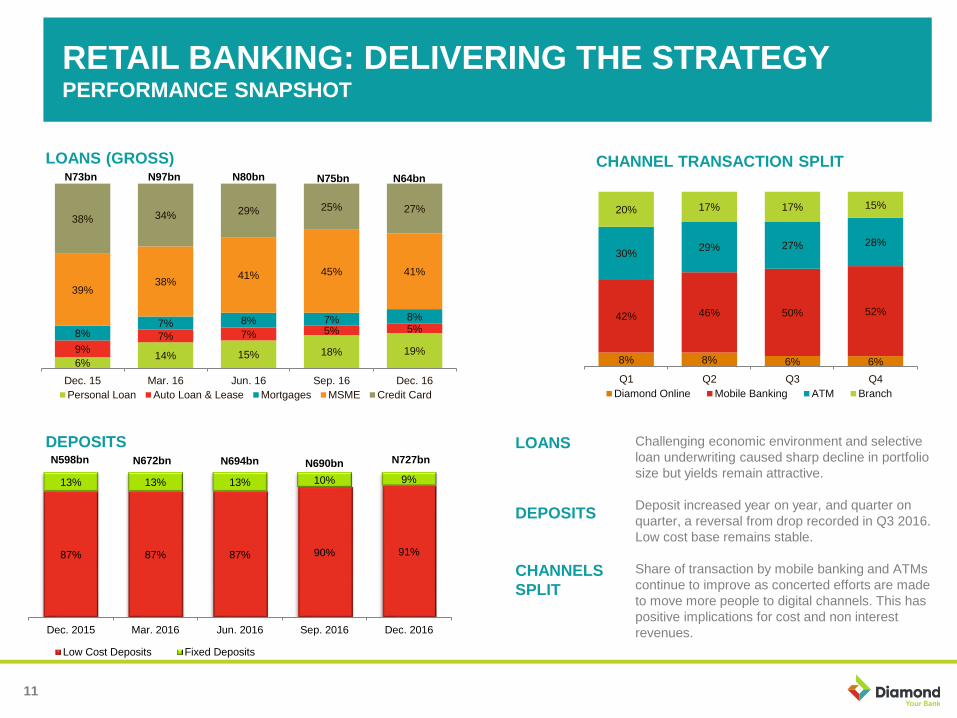

LOANS

DEPOSITS

CHANNELS

SPLIT

Challenging economic environment and selective

loan underwriting caused sharp decline in portfolio

size but yields remain attractive.

Deposit increased year on year, and quarter on

quarter, a reversal from drop recorded in Q3 2016.

Low cost base remains stable.

Share of transaction by mobile banking and ATMs

continue to improve as concerted efforts are made

to move more people to digital channels. This has

positive implications for cost and non interest

revenues.

LOANS (GROSS)

DEPOSITS

8% 8% 6% 6%

42% 46% 50% 52%

30%29% 27% 28%

20% 17% 17% 15%

Q1 Q2 Q3 Q4

Diamond Online Mobile Banking ATM Branch

CHANNEL TRANSACTION SPLIT

RETAIL BANKING: DELIVERING THE STRATEGYPERFORMANCE SNAPSHOT

6%14% 15% 18% 19%9%

7% 7% 5% 5%8%7% 8% 7% 8%

39%38%

41% 45% 41%

38% 34% 29% 25% 27%

Dec. 15 Mar. 16 Jun. 16 Sep. 16 Dec. 16

Personal Loan Auto Loan & Lease Mortgages MSME Credit Card

N73bn N80bnN97bn N75bn N64bn

87% 87% 87% 90% 91%

13% 13% 13% 10% 9%

Dec. 2015 Mar. 2016 Jun. 2016 Sep. 2016 Dec. 2016

Low Cost Deposits Fixed Deposits

N598bn N672bn N694bn N690bn N727bn

12

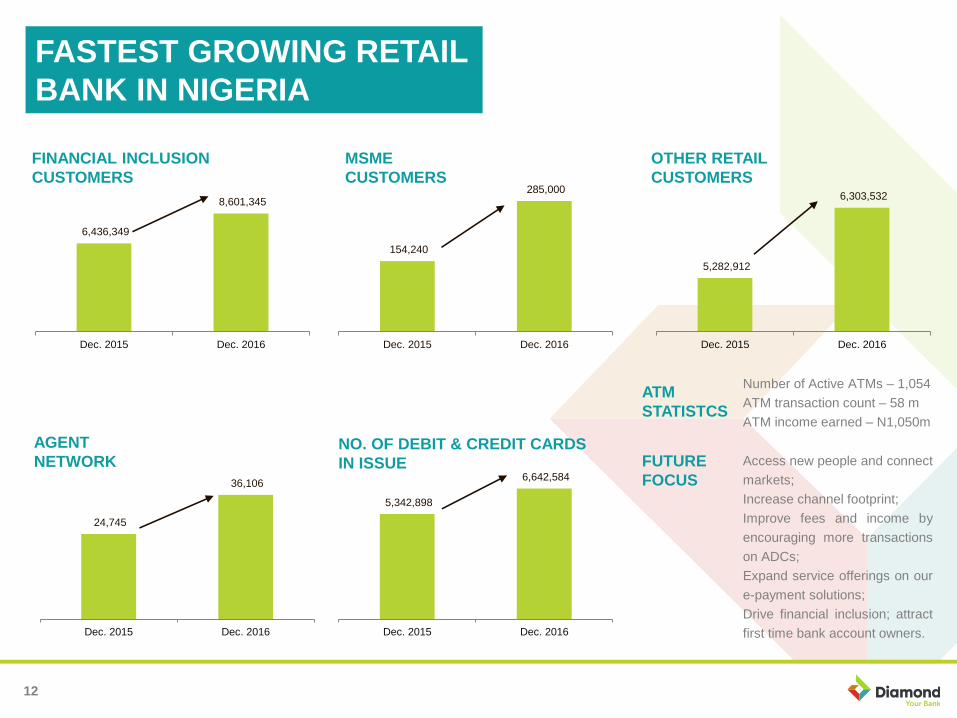

5,282,912

6,303,532

Dec. 2015 Dec. 2016

6,436,349

8,601,345

Dec. 2015 Dec. 2016

154,240

285,000

Dec. 2015 Dec. 2016

24,745

36,106

Dec. 2015 Dec. 2016

5,342,898

6,642,584

Dec. 2015 Dec. 2016

FINANCIAL INCLUSION

CUSTOMERS

MSME

CUSTOMERS

OTHER RETAIL

CUSTOMERS

AGENT

NETWORKNO. OF DEBIT & CREDIT CARDS

IN ISSUE

ATM

STATISTCS

Number of Active ATMs – 1,054

ATM transaction count – 58 m

ATM income earned – N1,050m

FUTURE

FOCUS

Access new people and connect

markets;

Increase channel footprint;

Improve fees and income by

encouraging more transactions

on ADCs;

Expand service offerings on our

e-payment solutions;

Drive financial inclusion; attract

first time bank account owners.

FASTEST GROWING RETAIL

BANK IN NIGERIA

13

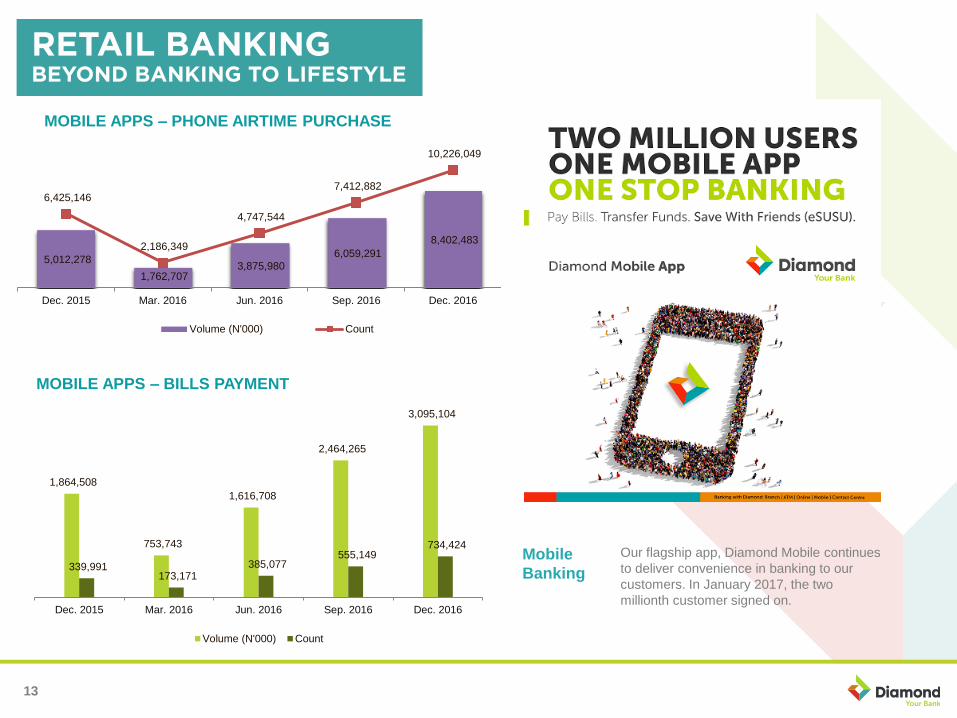

MOBILE APPS – PHONE AIRTIME PURCHASE

MOBILE APPS – BILLS PAYMENT

Our flagship app, Diamond Mobile continues

to deliver convenience in banking to our

customers. In January 2017, the two

millionth customer signed on.

Mobile

Banking

5,012,278

1,762,707 3,875,980

6,059,291

8,402,483

6,425,146

2,186,349

4,747,544

7,412,882

10,226,049

Dec. 2015 Mar. 2016 Jun. 2016 Sep. 2016 Dec. 2016

Volume (N'000) Count

1,864,508

753,743

1,616,708

2,464,265

3,095,104

339,991 173,171

385,077 555,149

734,424

Dec. 2015 Mar. 2016 Jun. 2016 Sep. 2016 Dec. 2016

Volume (N'000) Count

14

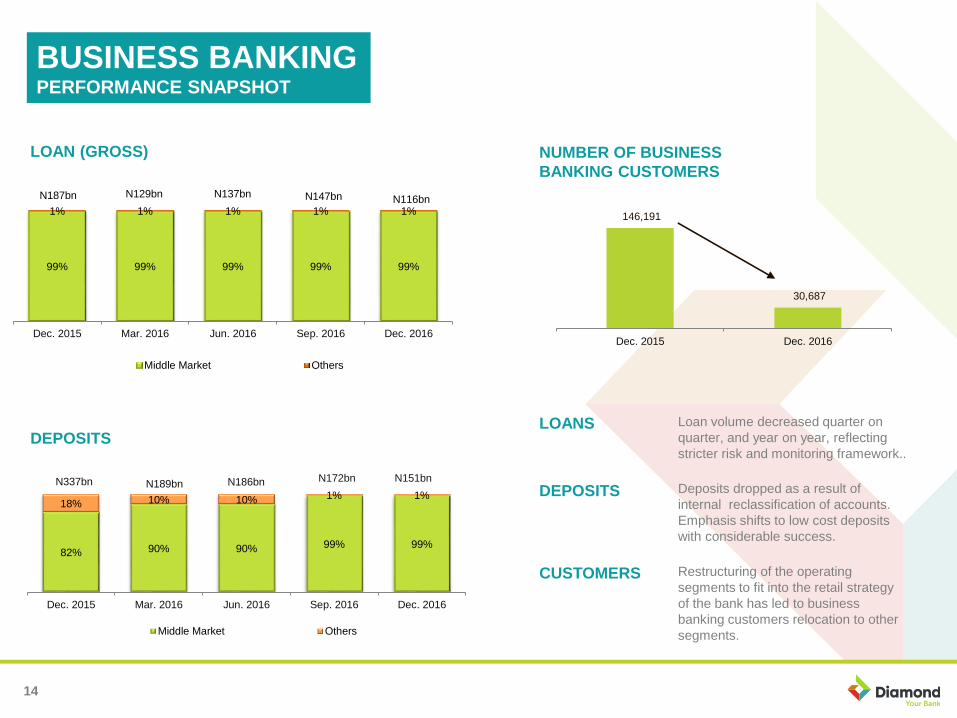

146,191

30,687

Dec. 2015 Dec. 2016

LOAN (GROSS)

DEPOSITS

NUMBER OF BUSINESS

BANKING CUSTOMERS

LOANS Loan volume decreased quarter on

quarter, and year on year, reflecting

stricter risk and monitoring framework..

DEPOSITS Deposits dropped as a result of

internal reclassification of accounts.

Emphasis shifts to low cost deposits

with considerable success.

CUSTOMERS Restructuring of the operating

segments to fit into the retail strategy

of the bank has led to business

banking customers relocation to other

segments.

BUSINESS BANKINGPERFORMANCE SNAPSHOT

99% 99% 99% 99% 99%

1% 1% 1% 1% 1%

Dec. 2015 Mar. 2016 Jun. 2016 Sep. 2016 Dec. 2016

Middle Market Others

N147bnN187bn N137bnN129bnN116bn

82% 90% 90% 99% 99%

18% 10% 10% 1% 1%

Dec. 2015 Mar. 2016 Jun. 2016 Sep. 2016 Dec. 2016

Middle Market Others

N172bnN337bn N186bnN189bnN151bn

15

LOANS (GROSS)

DEPOSITS

CUSTOMER COLLECTIONS

(N’m)

LOANSCorporate banking loans increased

by 33% Y-o-Y on the strength of

emerging opportunities in

relationships with blue chip

companies and devaluation of the

naira.

DEPOSITS Deposits increased through the year

as we leveraged relationships,

payment gateways and VCM.

COLLECTIONS Improved collections reflect successes

in VCM as we increased share with

existing clients and signed on more

corporates.

CORPORATE BANKINGPERFORMANCE SNAPSHOT

584,720

618,571

Dec. 2015 Dec. 2016

23%37% 37% 34%

23%

20%4% 3% 4%

15%

57% 59% 60% 62% 62%

Dec. 2015 Mar. 2016 Jun. 2016 Sep. 2016 Dec. 2016

Institutional banking Infrastructure & Transport Energy Business

N561bn N823bnN495bn N898bn N745bn

45% 69% 86% 80% 30%

35%

20%

6%7%

24%

20%11% 8%

13%

46%

Dec. 2015 Mar. 2016 Jun. 2016 Sep. 2016 Dec. 2016

Institutional banking Infrastructure & Transport Energy Business

N298bn N453bnN418bn N539bn N351bn

FY 2016 RESULTS

& ANALYSISCHIUGO NDUBISI, CFO

17

GROSS EARNINGS DROPPED – DRIVEN BY SHORTFALL IN

INTEREST INCOME, BUT FEES & COMM. INCOME INCREASED

PROFIT IS DOWN DUE TO IMPAIRMENT CHARGES – BUT

ACTION IS UNDERWAY TO DELIVER FUTURE IMPROVEMENT

OPERATING EXPENSES STABILIZE – GREATER COST

DISCIPLNE UNDERWAY

2016 FULL YEAR

FINANCIAL SUMMARY

NPL RATIO IS UP – BUT STRENGHTENED RISK MANAGEMENT

IS DELIVERING VALUE

TOTAL ASSETS, GROSS LOANS AND CUSTOMER DEPOSITS

ALL IMPROVE YEAR ON YEAR

18

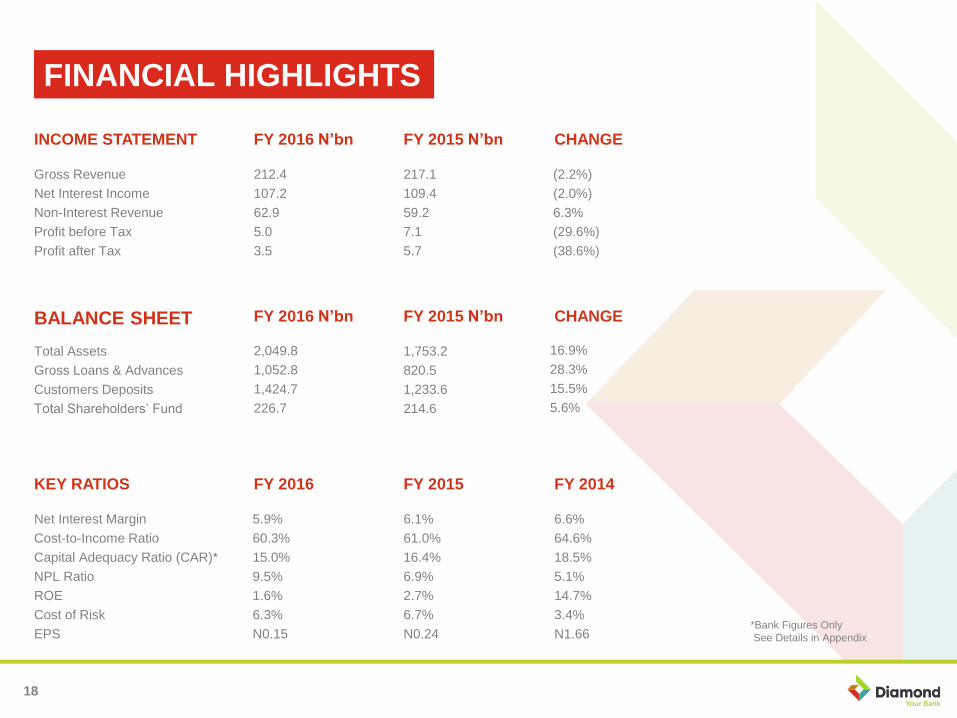

INCOME STATEMENT

Gross Revenue

Net Interest Income

Non-Interest Revenue

Profit before Tax

Profit after Tax

FY 2016 N’bn FY 2015 N’bn

217.1

109.4

59.2

7.1

5.7

CHANGE

BALANCE SHEET

Total Assets

Gross Loans & Advances

Customers Deposits

Total Shareholders’ Fund

FY 2016 N’bn FY 2015 N’bn

1,753.2

820.5

1,233.6

214.6

CHANGE

KEY RATIOS

Net Interest Margin

Cost-to-Income Ratio

Capital Adequacy Ratio (CAR)*

NPL Ratio

ROE

Cost of Risk

EPS

FY 2016 FY 2015

6.1%

61.0%

16.4%

6.9%

2.7%

6.7%

N0.24

FY 2014

6.6%

64.6%

18.5%

5.1%

14.7%

3.4%

N1.66*Bank Figures Only

See Details in Appendix

FINANCIAL HIGHLIGHTS

212.4

107.2

62.9

5.0

3.5

2,049.8

1,052.8

1,424.7

226.7

5.9%

60.3%

15.0%

9.5%

1.6%

6.3%

N0.15

(2.2%)

(2.0%)

6.3%

(29.6%)

(38.6%)

16.9%

28.3%

15.5%

5.6%

19

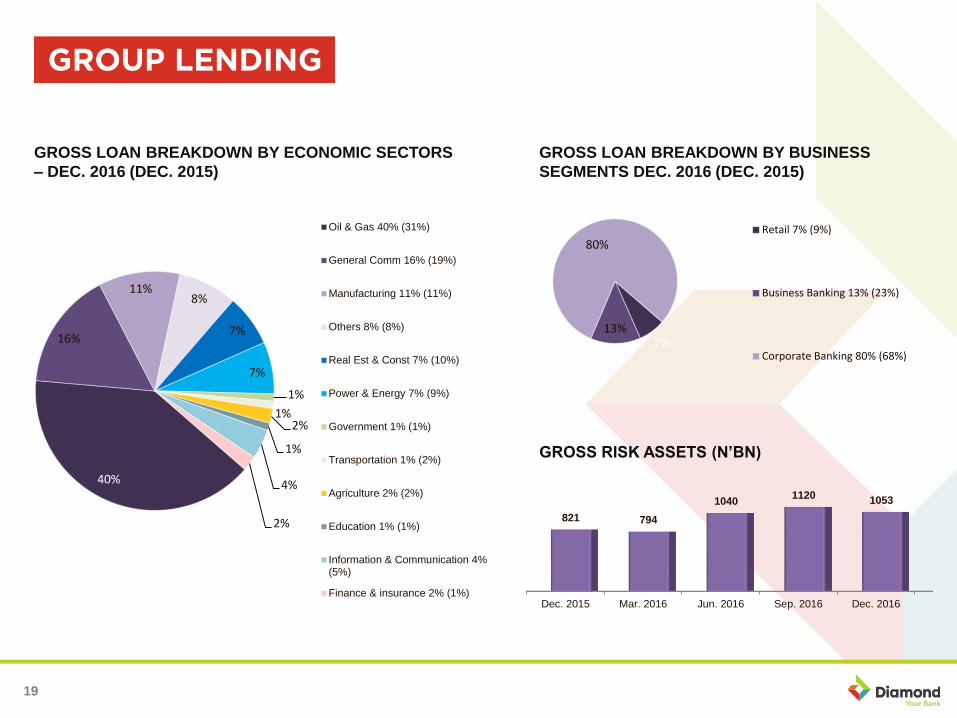

40%

16%

11%8%

7%

7%

1%

1%2%

1%

4%

2%

Oil & Gas 40% (31%)

General Comm 16% (19%)

Manufacturing 11% (11%)

Others 8% (8%)

Real Est & Const 7% (10%)

Power & Energy 7% (9%)

Government 1% (1%)

Transportation 1% (2%)

Agriculture 2% (2%)

Education 1% (1%)

Information & Communication 4%(5%)

Finance & insurance 2% (1%)

7%13%

80%Retail 7% (9%)

Business Banking 13% (23%)

Corporate Banking 80% (68%)

GROSS LOAN BREAKDOWN BY ECONOMIC SECTORS

– DEC. 2016 (DEC. 2015)

GROSS LOAN BREAKDOWN BY BUSINESS

SEGMENTS DEC. 2016 (DEC. 2015)

GROSS RISK ASSETS (N’BN)

Dec. 2015 Mar. 2016 Jun. 2016 Sep. 2016 Dec. 2016

821 794

10401120

1053

20

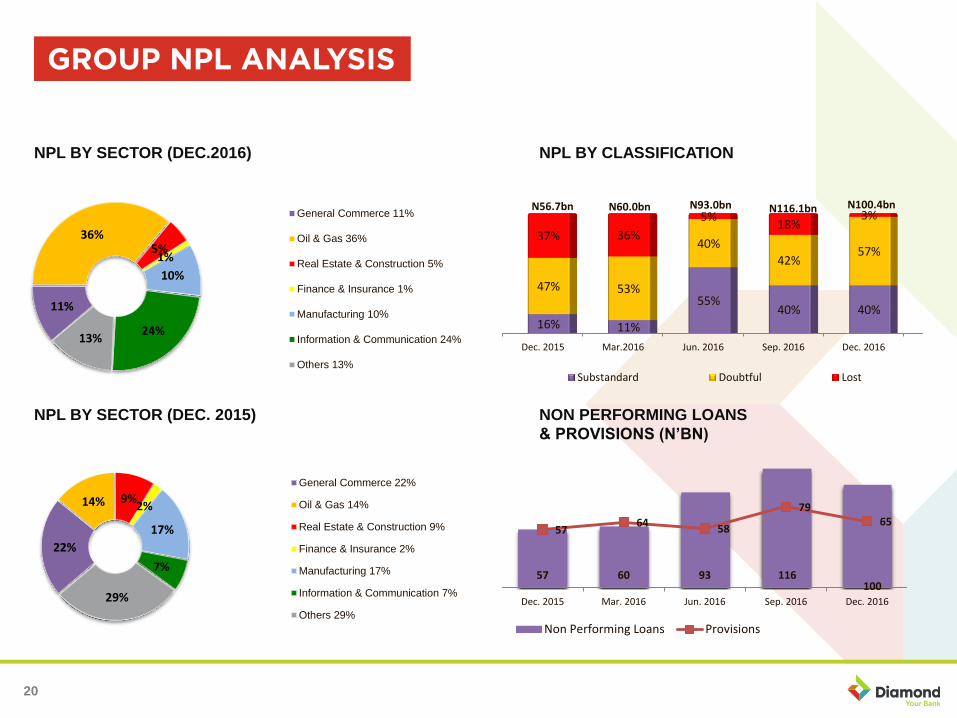

11%

36%5%

1%

10%

24%13%

General Commerce 11%

Oil & Gas 36%

Real Estate & Construction 5%

Finance & Insurance 1%

Manufacturing 10%

Information & Communication 24%

Others 13%

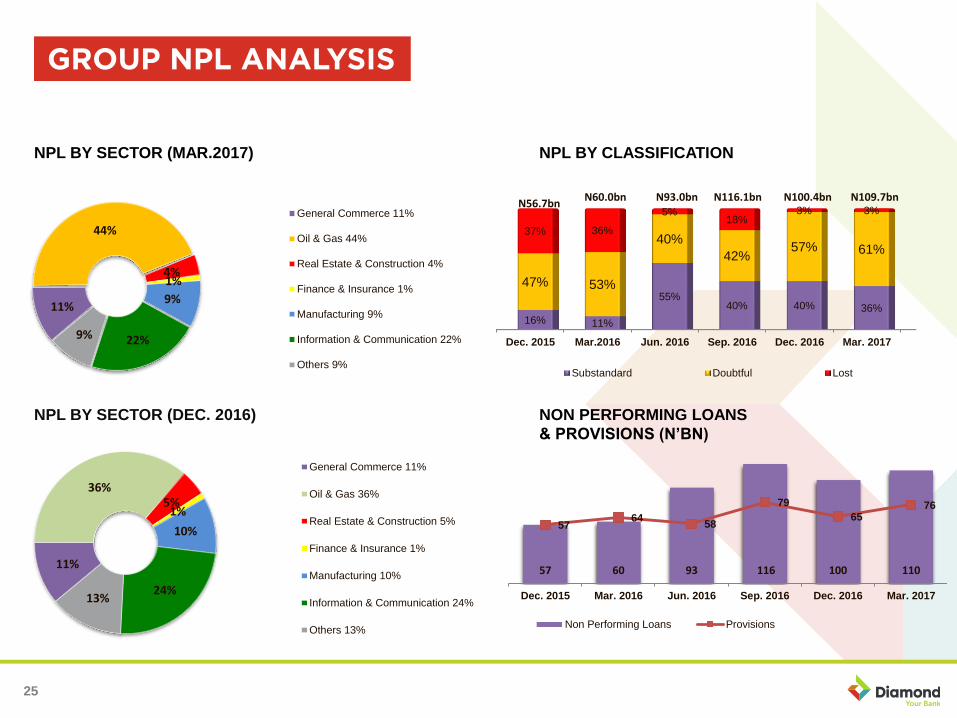

NPL BY SECTOR (DEC.2016) NPL BY CLASSIFICATION

NPL BY SECTOR (DEC. 2015) NON PERFORMING LOANS

& PROVISIONS (N’BN)

22%

14% 9%2%

17%

7%

29%

General Commerce 22%

Oil & Gas 14%

Real Estate & Construction 9%

Finance & Insurance 2%

Manufacturing 17%

Information & Communication 7%

Others 29%

Dec. 2015 Mar.2016 Jun. 2016 Sep. 2016 Dec. 2016

16% 11%

55%40% 40%

47% 53%

40%

42%57%

37% 36%

5%18%

3%

Substandard Doubtful Lost

N56.7bn N60.0bn N93.0bn N116.1bn N100.4bn

57 60 93 116 100

5764

58

7965

Dec. 2015 Mar. 2016 Jun. 2016 Sep. 2016 Dec. 2016

Non Performing Loans Provisions

Q1 2017 RESULTS

& ANALYSISCHIUGO NDUBISI, CFO

22

PROFIT DOWN YEAR ON YEAR DUE TO ADDITIONAL

IMPAIRMENT CHARGES – THIS WILL ABATE SOON

NET INTEREST INCOME UP 25% YEAR ON YEAR –

HIGHLIGHTING INCREASING MARGINS FROM LENDING

COMMISSION AND FEES INCOME INCREASE YEAR ON YEAR

LEVERAGING OUR LIFESTYLE APPROACH TO BANKING

Q1 2017 FINANCIAL

SNAPSHOT

TOTAL ASSETS CONTINUE TO GROW AS WE CONTINUE TO

EXPLORE NEW FRONTIERS

23

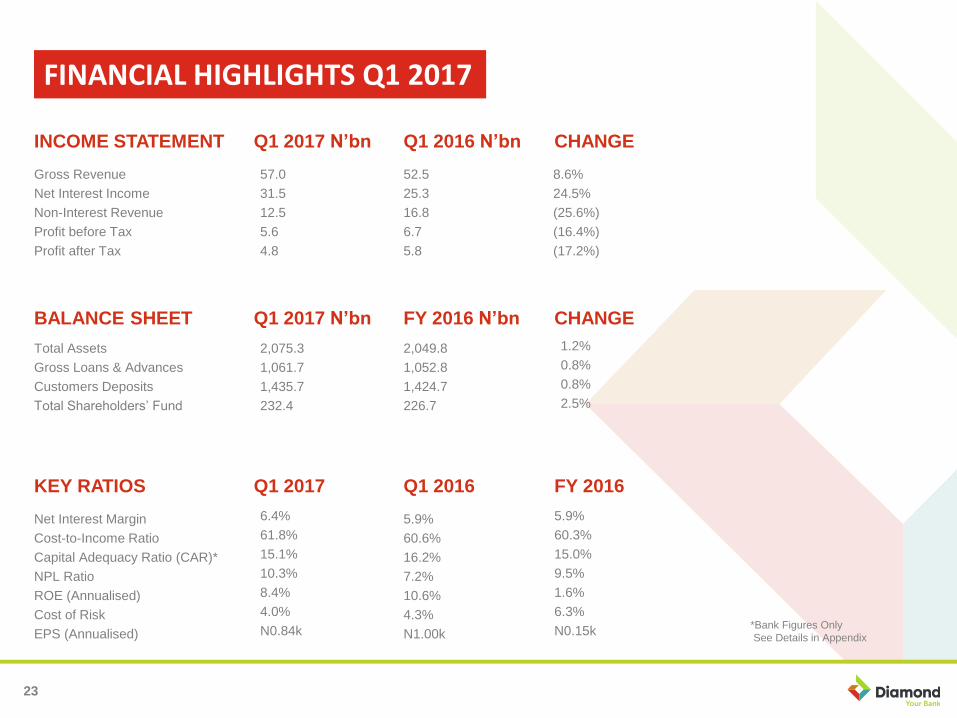

INCOME STATEMENT

Gross Revenue

Net Interest Income

Non-Interest Revenue

Profit before Tax

Profit after Tax

Q1 2017 N’bn Q1 2016 N’bn

52.5

25.3

16.8

6.7

5.8

CHANGE

BALANCE SHEET

Total Assets

Gross Loans & Advances

Customers Deposits

Total Shareholders’ Fund

Q1 2017 N’bn FY 2016 N’bn CHANGE

KEY RATIOS

Net Interest Margin

Cost-to-Income Ratio

Capital Adequacy Ratio (CAR)*

NPL Ratio

ROE (Annualised)

Cost of Risk

EPS (Annualised)

Q1 2017 Q1 2016

5.9%

60.6%

16.2%

7.2%

10.6%

4.3%

N1.00k

FY 2016

*Bank Figures Only

See Details in Appendix

FINANCIAL HIGHLIGHTS Q1 2017

5.9%

60.3%

15.0%

9.5%

1.6%

6.3%

N0.15k

6.4%

61.8%

15.1%

10.3%

8.4%

4.0%

N0.84k

57.0

31.5

12.5

5.6

4.8

2,049.8

1,052.8

1,424.7

226.7

2,075.3

1,061.7

1,435.7

232.4

8.6%

24.5%

(25.6%)

(16.4%)

(17.2%)

1.2%

0.8%

0.8%

2.5%

24

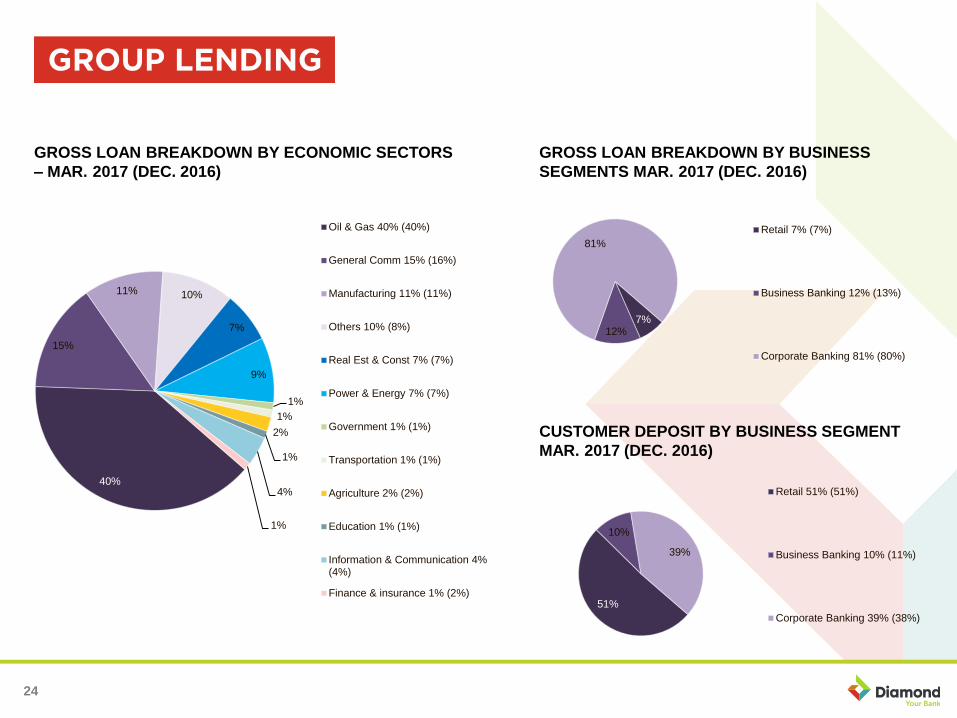

40%

15%

11% 10%

7%

9%

1%

1%

2%

1%

4%

1%

Oil & Gas 40% (40%)

General Comm 15% (16%)

Manufacturing 11% (11%)

Others 10% (8%)

Real Est & Const 7% (7%)

Power & Energy 7% (7%)

Government 1% (1%)

Transportation 1% (1%)

Agriculture 2% (2%)

Education 1% (1%)

Information & Communication 4%(4%)

Finance & insurance 1% (2%)

7%12%

81%

Retail 7% (7%)

Business Banking 12% (13%)

Corporate Banking 81% (80%)

GROSS LOAN BREAKDOWN BY ECONOMIC SECTORS

– MAR. 2017 (DEC. 2016)

GROSS LOAN BREAKDOWN BY BUSINESS

SEGMENTS MAR. 2017 (DEC. 2016)

CUSTOMER DEPOSIT BY BUSINESS SEGMENT

MAR. 2017 (DEC. 2016)

51%

10%

39%

Retail 51% (51%)

Business Banking 10% (11%)

Corporate Banking 39% (38%)

25

Dec. 2015 Mar.2016 Jun. 2016 Sep. 2016 Dec. 2016 Mar. 2017

16% 11%

55%40% 40% 36%

47% 53%

40%

42%57% 61%

37% 36%

5%18%

3% 3%

Substandard Doubtful Lost

N93.0bnN60.0bn N116.1bnN56.7bn

N100.4bn N109.7bn

11%

44%

4%1%

9%

22%9%

General Commerce 11%

Oil & Gas 44%

Real Estate & Construction 4%

Finance & Insurance 1%

Manufacturing 9%

Information & Communication 22%

Others 9%

11%

36%5%

1%

10%

24%13%

General Commerce 11%

Oil & Gas 36%

Real Estate & Construction 5%

Finance & Insurance 1%

Manufacturing 10%

Information & Communication 24%

Others 13%

57 60 93 116 100 110

5764

58

79

6576

Dec. 2015 Mar. 2016 Jun. 2016 Sep. 2016 Dec. 2016 Mar. 2017

Non Performing Loans Provisions

NPL BY SECTOR (MAR.2017) NPL BY CLASSIFICATION

NPL BY SECTOR (DEC. 2016) NON PERFORMING LOANS

& PROVISIONS (N’BN)

2017 OUTLOOK &

CONCLUSIONUZOMA DOZIE, CEO

27

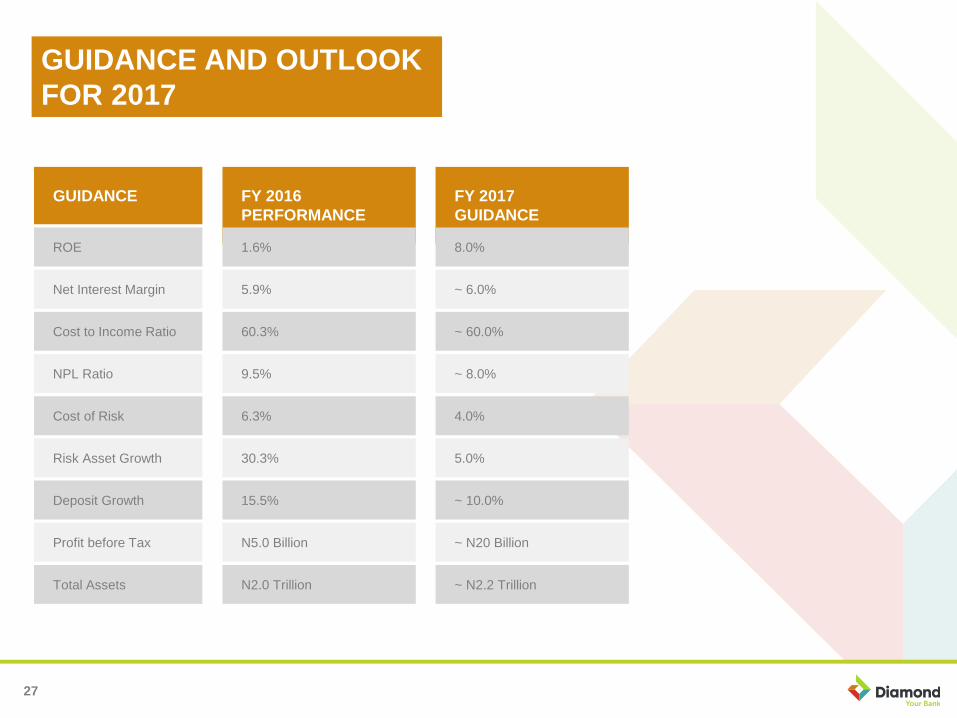

GUIDANCE FY 2016

PERFORMANCE

FY 2017

GUIDANCE

ROE

Net Interest Margin

Cost to Income Ratio

NPL Ratio

Cost of Risk

Risk Asset Growth

Deposit Growth

Profit before Tax

Total Assets

1.6%

5.9%

60.3%

9.5%

6.3%

30.3%

15.5%

N5.0 Billion

N2.0 Trillion

8.0%

~ 6.0%

~ 60.0%

~ 8.0%

4.0%

5.0%

~ 10.0%

~ N20 Billion

~ N2.2 Trillion

GUIDANCE AND OUTLOOK

FOR 2017

28

REITERATION OF TECHNOLOGY-LED RETAIL

STRATEGY

IMPROVED BALANCE SHEET STRUCTURE LEADING

TO EFFICIENCY

MACRO CONDITIONS REMAINS TOUGH BUT

OUTLOOK IS PROMISING

ACTIONS TAKEN TO POSITION THE BANK FOR

RECOVERY AND GROWTH

Q&A

31

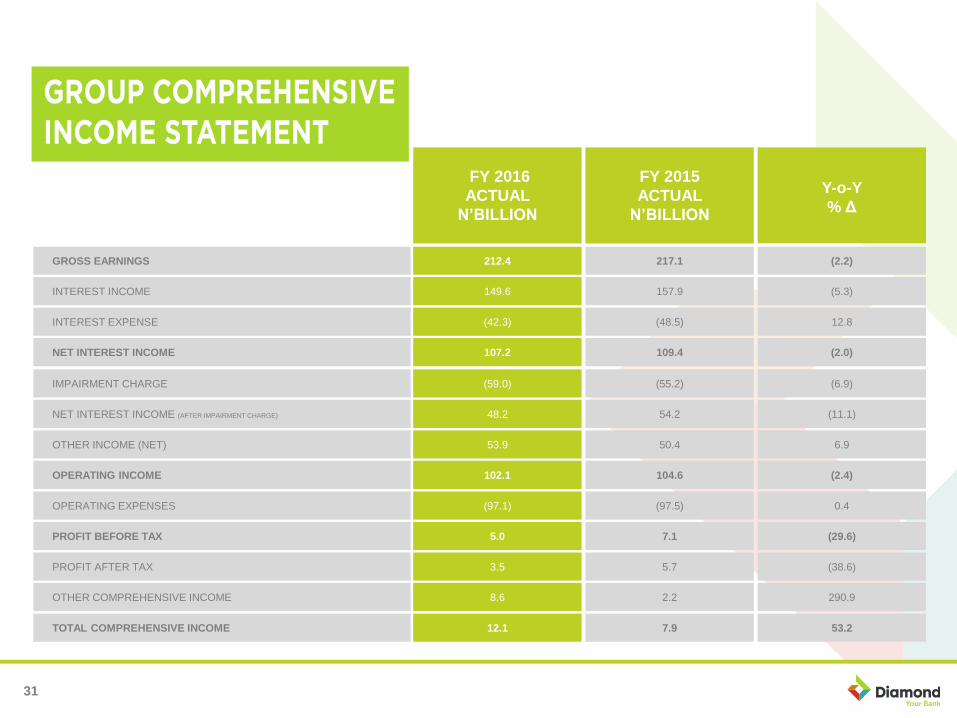

FY 2016

ACTUAL

N’BILLION

212.4GROSS EARNINGS

FY 2015

ACTUAL

N’BILLION

217.1

Y-o-Y

% Δ

(2.2)

149.6INTEREST INCOME 157.9 (5.3)

(42.3)INTEREST EXPENSE (48.5) 12.8

107.2NET INTEREST INCOME 109.4 (2.0)

(59.0)IMPAIRMENT CHARGE (55.2) (6.9)

48.2NET INTEREST INCOME (AFTER IMPAIRMENT CHARGE) 54.2 (11.1)

53.9OTHER INCOME (NET) 50.4 6.9

102.1OPERATING INCOME 104.6 (2.4)

(97.1)OPERATING EXPENSES (97.5) 0.4

5.0PROFIT BEFORE TAX 7.1 (29.6)

3.5PROFIT AFTER TAX 5.7 (38.6)

8.6OTHER COMPREHENSIVE INCOME 2.2 290.9

12.1TOTAL COMPREHENSIVE INCOME 7.9 53.2

32

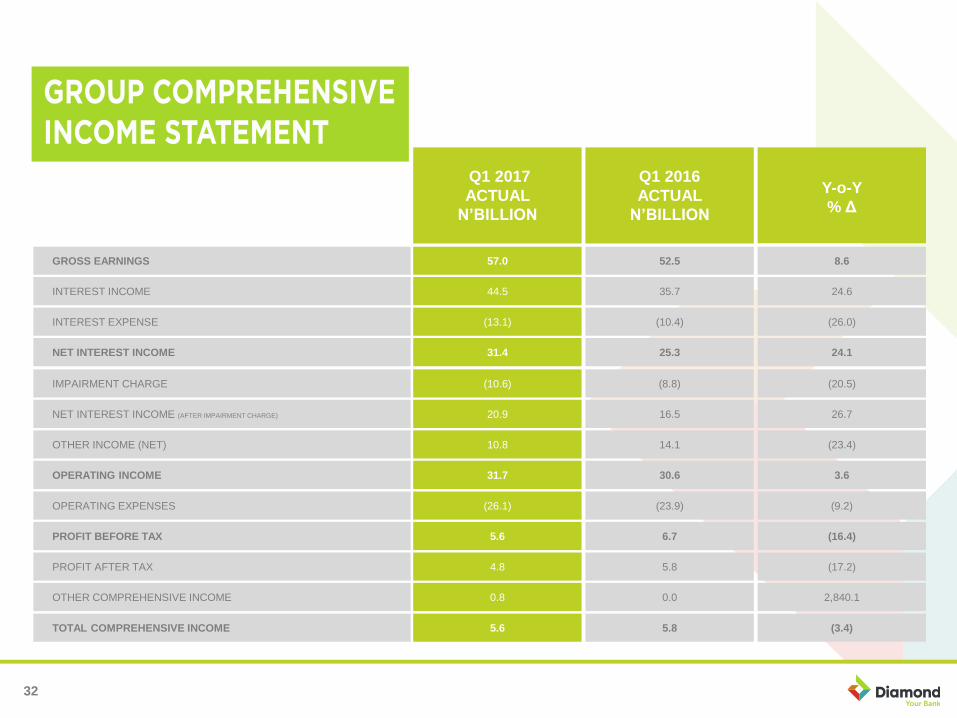

Q1 2017

ACTUAL

N’BILLION

57.0GROSS EARNINGS

Q1 2016

ACTUAL

N’BILLION

52.5

Y-o-Y

% Δ

8.6

44.5INTEREST INCOME 35.7 24.6

(13.1)INTEREST EXPENSE (10.4) (26.0)

31.4NET INTEREST INCOME 25.3 24.1

(10.6)IMPAIRMENT CHARGE (8.8) (20.5)

20.9NET INTEREST INCOME (AFTER IMPAIRMENT CHARGE) 16.5 26.7

10.8OTHER INCOME (NET) 14.1 (23.4)

31.7OPERATING INCOME 30.6 3.6

(26.1)OPERATING EXPENSES (23.9) (9.2)

5.6PROFIT BEFORE TAX 6.7 (16.4)

4.8PROFIT AFTER TAX 5.8 (17.2)

0.8OTHER COMPREHENSIVE INCOME 0.0 2,840.1

5.6TOTAL COMPREHENSIVE INCOME 5.8 (3.4)

33

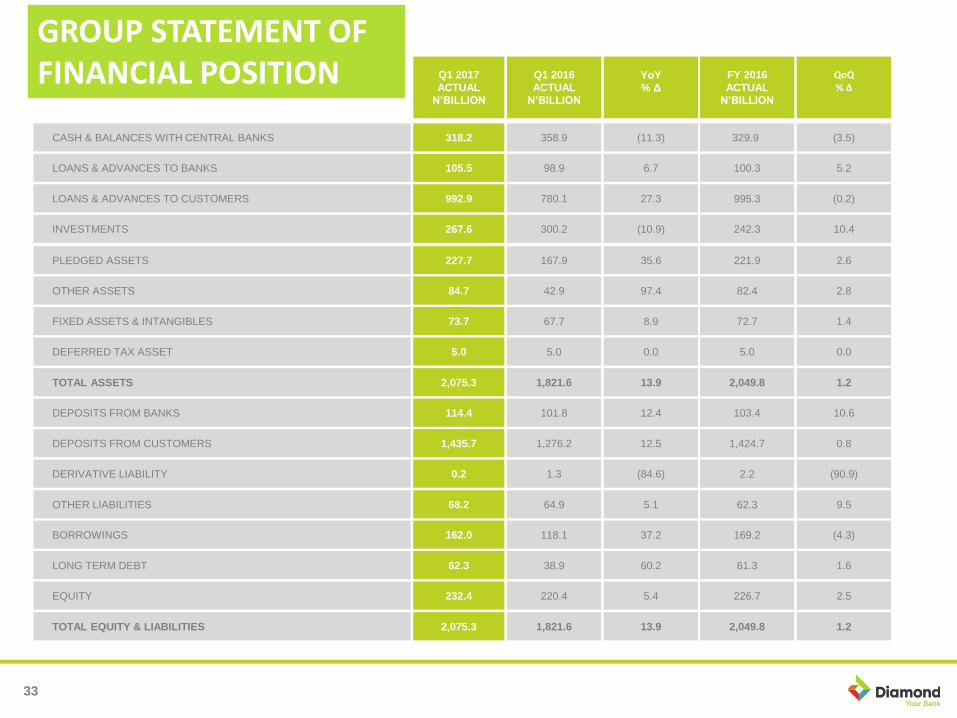

Q1 2017

ACTUAL

N’BILLION

318.2CASH & BALANCES WITH CENTRAL BANKS

Q1 2016

ACTUAL

N’BILLION

358.9

YoY

% Δ

(11.3)

105.5LOANS & ADVANCES TO BANKS 98.9 6.7

992.9LOANS & ADVANCES TO CUSTOMERS 780.1 27.3

267.6INVESTMENTS 300.2 (10.9)

227.7PLEDGED ASSETS 167.9 35.6

84.7OTHER ASSETS 42.9 97.4

73.7FIXED ASSETS & INTANGIBLES 67.7 8.9

5.0DEFERRED TAX ASSET 5.0 0.0

2,075.3TOTAL ASSETS 1,821.6 13.9

114.4DEPOSITS FROM BANKS 101.8 12.4

1,435.7DEPOSITS FROM CUSTOMERS 1,276.2 12.5

0.2DERIVATIVE LIABILITY 1.3 (84.6)

68.2OTHER LIABILITIES 64.9 5.1

FY 2016

ACTUAL

N’BILLION

329.9

QoQ% Δ

(3.5)

100.3 5.2

995.3 (0.2)

242.3 10.4

221.9 2.6

82.4 2.8

72.7 1.4

5.0 0.0

2,049.8 1.2

103.4 10.6

1,424.7 0.8

2.2 (90.9)

62.3 9.5

162.0BORROWINGS 118.1 37.2

62.3LONG TERM DEBT 38.9 60.2

232.4EQUITY 220.4 5.4

2,075.3TOTAL EQUITY & LIABILITIES 1,821.6 13.9

169.2 (4.3)

61.3 1.6

226.7 2.5

2,049.8 1.2

GROUP STATEMENT OF FINANCIAL POSITION

34

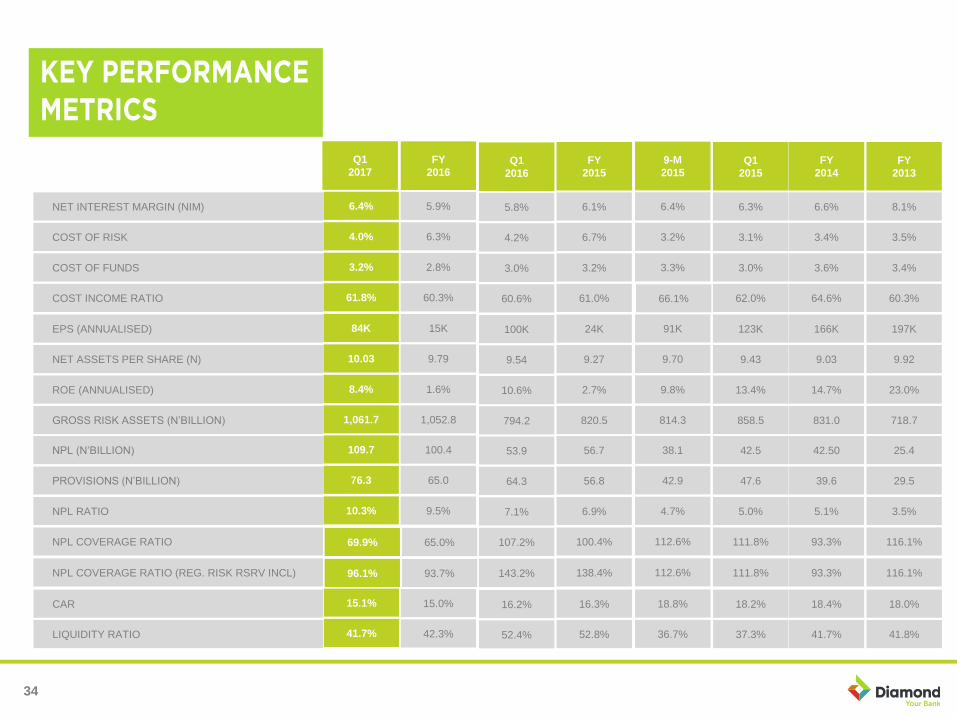

NET INTEREST MARGIN (NIM)

COST OF RISK

COST OF FUNDS

COST INCOME RATIO

EPS (ANNUALISED)

NET ASSETS PER SHARE (N)

ROE (ANNUALISED)

GROSS RISK ASSETS (N’BILLION)

NPL (N’BILLION)

PROVISIONS (N’BILLION)

NPL RATIO

FY

2015

6.1%

6.7%

3.2%

61.0%

24K

9.27

2.7%

820.5

56.7

56.8

6.9%

Q1

2015

6.3%

3.1%

3.0%

62.0%

123K

9.43

13.4%

858.5

42.5

47.6

5.0%

FY

2014

6.6%

3.4%

3.6%

64.6%

166K

9.03

14.7%

831.0

42.50

39.6

5.1%

FY

2013

8.1%

3.5%

3.4%

60.3%

197K

9.92

23.0%

718.7

25.4

29.5

3.5%

9-M

2015

6.4%

3.2%

3.3%

91K

9.70

9.8%

814.3

38.1

42.9

4.7%

66.1%

FY

2016

5.9%

6.3%

2.8%

60.3%

15K

9.79

1.6%

1,052.8

100.4

65.0

9.5%

Q1

2017

6.4%

4.0%

3.2%

61.8%

84K

10.03

8.4%

1,061.7

109.7

76.3

10.3%

Q1

2016

5.8%

4.2%

3.0%

60.6%

100K

9.54

10.6%

794.2

53.9

64.3

7.1%

NPL COVERAGE RATIO 100.4% 111.8% 93.3% 116.1%112.6%65.0%69.9% 107.2%

15.1%

41.7%

CAR

LIQUIDITY RATIO

16.3%

52.8%

18.2%

37.3%

18.4%

41.7%

18.0%

41.8%

18.8%

36.7%

15.0%

42.3%

16.2%

52.4%

NPL COVERAGE RATIO (REG. RISK RSRV INCL) 138.4% 111.8% 93.3% 116.1%112.6%93.7%96.1% 143.2%