investor update - lic housing finance · home loans continue to dominate loan book of hfcs...

TRANSCRIPT

Investor UpdateMarch 2018

Population(cr)

2

Section

80C IT Act

Deduction on account of principal

repayment of up to Rs.1.5 lakh on home

loans from the borrowers gross total

income

Section 24,

IT Act

Deduction on account of annual interest

payment of up to Rs. 2 lakh on home

loans, where the house is self-occupied.

Section 54,

IT Act

Capital gains from transfer of residential

property, if invested is acquiring a

residential house, exempt from income tax

Urb

an p

opula

tion (

cr)

Urb

aniz

ation R

ate

%

Pro

pert

y c

ost (r

s lac)

&

Aff

ord

abili

ty

Indian housing industry: Strong growth drivers

Rising population Growing urbanization

Improvement in affordability Favorable tax legislations

1 Crore (cr)=10 million

Several initiatives to promote housing

3

• Real Estate Regulatory Authority ‘RERA” Bill in 2016: 24 out of 35 States &

Union Territories have notified RERA

• Incentives for Builders in Affordable Housing-Union Budget 2016

• Budget 2017: “Infrastructure Status” for Affordable Housing

• Budget 2018: Affordable Housing Fund to be created

Several initiatives to promote housing

4

• “Housing For All” by 2022

• Launch of Pradhan Mantri Awas Yojana in 2015

• 100 “Smart Cities” notified

• Announcement of Interest Subsidy for Loans upto Rs 9 lacs & Rs12 lacs by

Hon’ble Prime Minister on 31.12.2016 (MIG-I & MIG-II)

5

No

. of

citi

es

61.20% 63% 64.70% 65%

34.70% 30.10% 27.20% 26.40%

4.10% 6.80% 8.20% 8.50%

0%

20%

40%

60%

80%

100%

2001 2006 2011E 2016E

Working Age(15-59 years) <15 Years >59 years

20-59 years <20 years

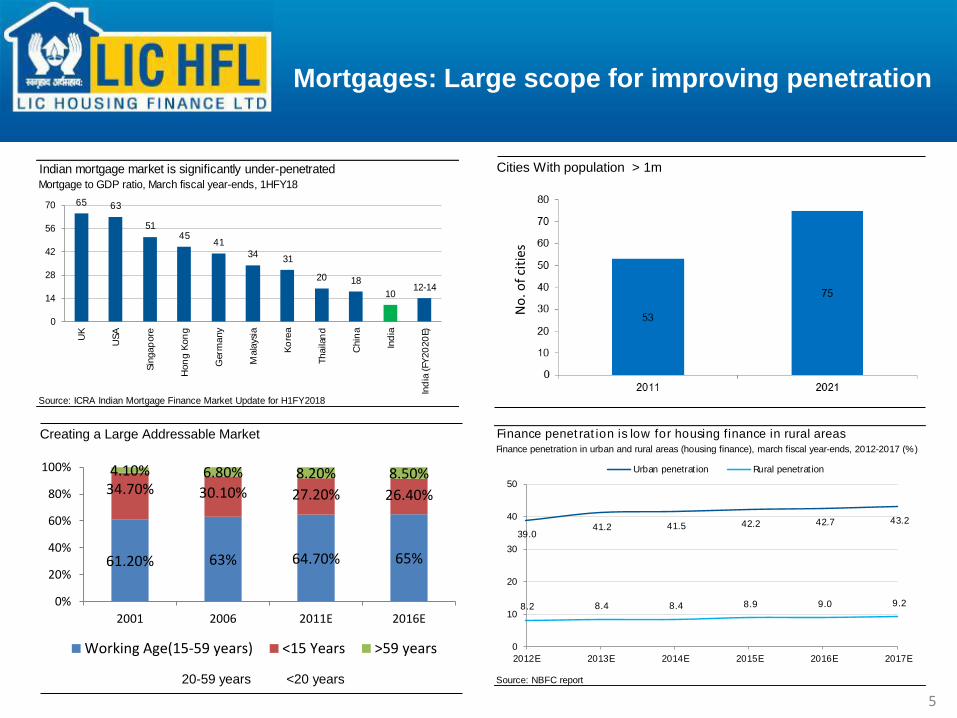

Mortgages: Large scope for improving penetration

Finance penet rat ion is low for housing finance in rural areas

Finance penetration in urban and rural areas (housing finance), march fiscal year-ends, 2012-2017 (%)

Source: NBFC report

39.0 41.2 41.5 42.2 42.7 43.2

8.2 8.4 8.4 8.9 9.0 9.2

0

10

20

30

40

50

2012E 2013E 2014E 2015E 2016E 2017E

Urban penetrat ion Rural penetrat ion

Indian mortgage market is significantly under-penetrated

Mortgage to GDP ratio, March fiscal year-ends, 1HFY18

Source: ICRA Indian Mortgage Finance Market Update for H1FY2018

65 63

5145

41

3431

20 18

1012-14

0

14

28

42

56

70

UK

USA

Sin

gap

ore

Hon

g K

on

g

Germ

any

Mala

ysi

a

Ko

rea

Thailan

d

Chin

a

Ind

ia

Ind

ia (

FY

20

20

E)

Cities With population > 1m

Creating a Large Addressable Market

Mortgage book to witness strong growth going ahead

March fiscal year-ends, 2011-2019P

Note:

1) Includes the overall portfolio of HFCs and only developer and housing loans of banks.

Source: NBFC report

7.4 8.6 10.4

12.4 14.7

17.3 19.9

22.8 26.6

17.0

20.9

19.2 18.5

17.7

15.0 14.6

16.7

0

5

10

15

20

25

0

6

12

18

24

30

2011 2012 2013 2014 2015 2016 2017E 2018P 2019P

(%)(Rs tn) Mortgage loan book LHS) YoY (RHS)

Housing loans to witness strong traction as impact of GST and RERA fade away

March fiscal year-ends, 2012-2019P

Source: NBFC report

6.2 7.5 8.9 10.5

12.4 14.4

16.6 19.6

20.6 19.0 18.6 18.1

16.1 15.0

18.0

0

5

10

15

20

25

0

5

10

15

20

25

2012 2013 2014 2015E 2016E 2017E 2018P 2019P

(%)(Rs tn)Housing f inance (LHS) YoY (RHS)

Mortgages: High growth trajectory

LAP market to pick pace post lowering in last two years

March fiscal year-ends, 2013-2019P

Source: NBFC report

1.3 1.7 2.3 2.9 3.2 3.7 4.3

34.4

30.1 28.8

12.0 13.5

15.5

0

7

14

21

28

35

0

1

2

3

4

5

2013E 2014E 2015E 2016E 2017E 2018P 2019P

(%)(Rs tn) LAP loan book (LHS) YoY (RHS)

6

HFCs cont inue to dominate mortgage market

March fiscal year-ends. 2012-2019P (%)

Source: NBFC report

66 63 63 62 62 60 60 59

34 37 37 38 38 40 40 41

0

20

40

60

80

100

2012 2013 2014 2015 2016 2017E 2018P 2019P

Banks HFC

Mortgages: HFCs play a key role

HFC cont inue to dominate home loan market

YoY increase in home loan portfolio of banks and HFCs

Source: ICRA Indian Mortgage Finance Market Update for H1FY2018

15

1817

18

1513

26

2021

1918

19

0

6

12

18

24

30

2013 2014 2015 2016 2017 1HFY18

Banks HFC

7

HFCs: Home loans dominate mortgage book

Home loans continue to dominate loan book of HFCs

Portfolio composition of HFCs, March fiscal year-ends, 2017 (%)

Source: CRA Indian Mortgage Finance Market Update for H1FY2018

Home loan,

67

LAP, 15

Construction

finance, 10

LRD, 5Others, 3

HFCs are growing their non-housing loan portfolio at a fast pace

YoY increase in loans, March fiscal year-ends, 2014-1HFY18 (%)

Source: CRA Indian Mortgage Finance Market Update for H1FY2018

20 22 21 20 23

1921

1918

19

21

26 2627

30

15

17

19

21

23

25

0

7

14

21

28

35

2014 2015 2016 2017 1HFY18

Overall port folio Home loans Other loans

8

1989

1994

2002

2004

2009

2011

2012

2013

Incorporated

IPO

AAA Rating

GDR Issue

Crossed Rs. 500 crs profit

Crossed Rs. 50,000 Cr loan portfolio

• Best HFC by CNBC TV 18

• Construction Industry Award

•Crossed Rs. 1000 cr profit &

Rs 75,000 Cr assets

20152014

• Best HFC by

ABP News

•Crosses Rs 1

lakh cr in portfolio

•Best Housing

Finance Co. by

BFSI Awards

• Best data quality

in HFC

by CIBIL

LICHFL: A Journey of 29 Years…

•Business Today-

Best CEO Award

• Business World -

Most Respected Co

Award

•Outlook Money-Best

HFC

•Best HFC by ABP

News

•Best Data Quality by

CIBIL

•Asia Pacific

Entrepreneurship

Award

•Power Brands

Awards by Franchise

India

2016

2017

•Crosses 150,000 cr in assets

•Outlook Money-Best HFC

•Business Today BFSI Best

CEO

•NSE for highest Debt

Issuance

9

• Highest ratings (AAA) since 2002

• More than 22 lakh customers serviced till date

• Total assets more than Rs 150,000 cr

• 96% of loan assets in retail category

• Cumulative Disbursements > Rs 2,60,000 cr since

inception

• Gross NPAs in retail loans amongst lowest in Industry

LICHFL: Key highlights

Shareholding Pattern

10

LICHFL: Key highlights

24359 2527130327

3615141541

0

10000

20000

30000

40000

50000

2013 2014 2015 2016 2017

Disbursement (Rs. Cr) CAGR 14% Loan Portfolio (Rs.cr) CAGR 17%

Income (Rs. cr) CAGR 16% Profit After Tax (Rs. cr) CAGR 17%

11

* Provisions Including Provisions on Std. Assets & Teaser Loans

LICHFL: Key highlights

Gross & Net NPAs Total Provisions* (Rs cr)

Operating Expense to Total Income Profit per employee (Rs. lacs)

12

LICHFL: Key highlights

EPS (Rs) (Rs 2/- pd up) Book Value (Rs)(Rs 2/- pd up)

Return on Avg Equity Return on Avg Loan Assets

13

Trends in retail disbursements

14

23,230 24,289 29,255 34,529 38,334 29,976

21.51

4.56

20.45

18.03

11.02

22.98

0

5

10

15

20

25

-

9,000

18,000

27,000

36,000

45,000

2013 2014 2015 2016 2017 9MFY18

(%)(Rs cr) Disbursements (LHS) YoY (RHS)

16.08 17.21 18.08 19.95 21.41 21.32

7.03

5.06

10.34

7.32

0.0

2.5

5.0

7.5

10.0

12.5

-

5

10

15

20

25

2013 2014 2015 2016 2017 9MFY18

(%)(Rs lacs) Average ticket size (LHS) YoY (RHS)

96 96 92 79 77 82 -

20

40

60

80

100

2013 2014 2015 2016 2017 9MFY18

(%) Share of home loans

Low NPLs in retail segment over the years

15

239 240 253 246 284 710

0.32

0.270.24

0.2 0.2

0.47

0.0

0.2

0.4

0.6

0.8

1.0

-

200

400

600

800

1,000

2013 2014 2015 2016 2017 9MFY18

(%)(Rs cr) Retail GNPA (LHS) Retail GNPA ratio (RHS)

Amongst the lowest GNPAs in the sector with Net Credit losses since inception less than 7 bps

23 New Marketing Offices proposed to be opened in FY 2019

• 9 Regional Offices

• 23 Back Offices

• 249 Marketing Offices

• Rep offices in Dubai & Kuwait

• Coverage of more than 450 centres

• 2095 Employees

Back offices

Operating offices

Regional offices

Corporate office

Nagercoil

ThiruvananthapuramKottayam

Ernakulam

Kozhikode

Thrissur

Tirumangalam

Madurai

Thanjavur

Pondicherry

Tiruchirapalli

Coimbatore

Salem

Vellore

ChennaiHosurMysore

Mangalore

Bengaluru

Panjim

Vashi

Mumbai

NelloreHubliTirupati

Bellary

Anantapur

Kurnool

Guntur

Kakinada

Vijayawada

Hyderabad Rajahmundry

Visakapatnam

Warangal

Bhubaneshwar

Kolkata

Silchar

Guwahati

Siliguri

Gangtok

Patna

ShimlaJalandharAmritsar

LudhianaChandigarh

Dehradun

HaldwaniKarnal

Bareilly

Ghaziabad

New Delhi

AgraLucknow

Kanpur

JaipurAjmer

Gwalior

Bikaner

Jodhpur

Rajkot

Udaipur

Ahmedabad

Vadodara Indore

Bhopal

Allahabad

Jabalpur

Varanasi

Ranchi

Jamshedpur

RourkelaBilaspur

RaipurNagpurJalgaonSurat

Vapi

AurangabadNasik

Kalyan

ThaneJogeshwari

Pune

Kolhapur

Belgaum

Gulburga

Nallasopara

Kota

Hassan

Erode

Kannur

Kollam

Palghat

Gandhidham

Satara

Durg-Bhilai

Gorakhpur

Meerut

Behrampur

Cuttack

Dhanbad

Durgapur

Jorhat

Malda

GurgaonFaridabad

Noida

AmbalaBhatinda

HisarPatiala

Large geographic presence

Year No of

Marketing

Offices

No of Back

offices

No of

Regional

Offices

No of

Employees

Lon

Portfolio

Rs cr

2003 105 - 6 870 7772

2008 125 14 6 985 21936

2013 194 16 7 1446 77812

2018 249 23 9 2095 156176 * (Dec 2017)

Widening footprint…improved efficiencies

16

HOME LOAN AGENTS (HLAs)

(Agents of LIC)

DIRECT SALES AGENTS (DSAs)

(Small Firms/Companies etc)

CUSTOMER RELATIONS

ASSOCIATES (CRAs)

(Individual Agents of the Company)

249Marketing Offices

49 branches of

LICHFL Financial Services(100% subsidiary of LICHFL)

Distribution Network

Total No of Agents > 12300:

growth of over 20% y-o-y

17

Loan Book Composition

31.12.2017

O/s Portfolio Rs156176 cr

30.09.2017

O/s Portfolio Rs151417 cr

31.3.2017

O/s Portfolio Rs144534 cr

18

Installment to Net Income RatioOn Incremental Sanctions

For FY16 33.25%

For FY17 32.12%

For Q2FY18 30.28%

For Q3FY18 30.74%

Loan To Value RatioOn Incremental Sanctions

For FY16 47%

For FY17 45%

For Q2FY18 45%

For Q3FY18 44%

Pure Floating Rate LoansTo Outstanding Portfolio

As of FY16 47%

As of FY17 70%

As of Q2FY18 78%

As of Q3FY18 76%

PrepaymentLump Sum/ opening book

For FY16 11.9%

For FY17 10.9%

As of Q2FY18 10.9%

As of Q3FY18 10.9%

Individual Loans – Portfolio Stats

19

Origination Pattern & Average Ticket Size

Data for 9M FY 2018 20

9M FY2018 9M FY 2017

Return on Average Equity (%) 17% 19%

Return on Average Assets (%) 1.3% 1.5%

Earnings per share (on Rs 2 pd up) 28.74 27.78

Capital Adequacy Ratio

Tier I

Tier II

Total

Sept 2017

13.36

2.68

16.04

Sept 2016

13.99

2.65

16.63

Financial Highlights – Q3FY18

21

Q3 FY18 PAT at Rs 491.07 cr as against Rs 499.26 cr for Q3FY17

Q3 FY18 Revenue from operations up by 6 % to Rs 3738 cr

Outstanding Loan portfolio up by 15% to Rs.156176 cr

Individual Loan Portfolio up by 15% to Rs 149986 cr

Q3FY18 Disbursements Rs 12301 cr against Rs 9685 cr up by 27 %

Individual Loan Disbursements Rs 11323 cr against Rs 8555 cr, up by 32%

Net Interest Income Rs 898 cr against Rs 915 cr

Net Interest Margins 2.33% for Q3 FY18 as against 2.75% for Q3FY17

Gross NPAs at 0.87% as against 0.56% as on 31.12.2016

Net NPAs 0.49% as against 0.27% on corresponding dates

Individual Loans Gross NPAs at 0.47% as against 0.32% on 31.12.2016

Total Provisions at Rs 1227 cr as against total Gross NPAs of Rs 1360 cr

Executive Summary – Q3/FY18

22

Executive Summary – Q3/9MFY18

Var Q3

FY18

Q3

FY17

Var 9M

FY18

9M

FY17

Interest Income on Individual Loans 4% 3525.78 3384.81 6% 10461.38 9905.04

Interest Income on Project Loans 46% 186.63 127.72 43% 517.88 362.12

Total 6% 3712.41 3512.53 7% 10979.26 10267.16

Processing Fees & Other Fees 67% 25.68 15.41 3% 79.45 76.90

Other Income 42% 29.48 20.79 8% 80.08 74.43

Gross Income 6% 3767.57 3548.73 7% 11138.79 10418.49

Interest Expenses 8% 2814.81 2597.15 8% 8281.60 7661.57

Net Interest Income (2%) 897.60 915.38 4% 2697.66 2605.59

Salary & Other Establishment Exp. 5% 147.73 140.70 2% 423.32 415.22

Net Provisions & Diminutions 7% 48.45 45.27 10% 210.74 192.03

Profit before Tax (1%) 756.58 765.60 3% 2223.13 2149.67

Income Tax Provision including Deferred Tax (1%) 265.51 266.34 3% 772.87 747.81

Net Profit (2%) 491.07 499.26 3% 1450.26 1401.86

Rs cr

Executive Summary – Q3/9MFY18

Var Q3

FY18

Q3

FY17

Var 9M

FY18

9M

FY17

Disbursements

Individual 32% 11323 8555 23% 29976 24374

Project (13%) 978 1129 11% 2000 1975

Total 27% 12301 9684 21% 31976 26349

Outstanding Portfolio

Individual 15% 149986 130878

Project 38% 6189 4488

Total 15% 156175 135366

Net Interest Margins(%) 2.33% 2.75% 2.39% 2.67%

Borrowings during the Qtr 16430 13967

Incremental Cost/ytd 7.42% 8.19%

Incremental Yield(overall, annualised

YTD)

9.86% 10.69%

Incremental Spreads (YTD) 2.44% 2.50%

Rs cr

Yield & Cost of Funds on portfolio

25

Outstanding Borrowings – Rs. 137629 cr

Source Wtd

Avg

Cost

(%)

Banks & Institutions 8.18%

Non Convertible Debenture 8.41%

National Housing Bank 8.20%

Sub. Bonds & Upper Tier II 9.18%

Commercial Paper 6.44%

Deposits* 8.09%

Total 8.32%

as on 31.12.2017

Liability Profile

During Q3FY18, Borrowings were Rs 16430 cr @ 7.38%

* Includes Corporate Deposits of Rs 2749 cr26

Change in Liability Mix

Wtd. Avg. cost

of Funds

Bank funding has

reduced from

32% in FY12 to

25% in FY14.

Retail Deposits

increased to 2.2%

8.32% 8.37% 8.50% 8.59% 9.14% 9.48%

* Includes Corporate Deposits of Rs 2749 cr 27

Net Interest Margins

28

31.12.2017 31.12.2016

Gross NPA (Rs. cr) 1360 759

Gross NPA (%) 0.87% 0.56%

Provisions for NPA (Rs. cr)* 598 398

Net NPA(%) 0.49% 0.27%

Provisions including standard asset

provisions

1227 969

Gross & Net NPAs

*Excluding provisions on standard assets

Provisions cover including standard asset

provisions

90% 128%

29

Gross & Net NPAs

30

DISCLAIMER

This presentation is made purely for information. We have attempted to provide relevantinformation which we believe will help in knowing the Company. The users may use their ownjudgment and are advised to make their own calculations before deciding on any matter basedon the information given herein.

While every care is taken to verify the accuracy of the information given in this presentation,neither the Company nor its officials would in any way be liable for any action taken or nottaken by the viewers or the users of this presentation or for any claims, losses etc.

Thank you

31