investor sentiment and the cross-section of stock...

TRANSCRIPT

THE JOURNAL OF FINANCE • VOL. LXI, NO. 4 • AUGUST 2006

Investor Sentiment and the Cross-Sectionof Stock Returns

MALCOLM BAKER and JEFFREY WURGLER∗

ABSTRACT

We study how investor sentiment affects the cross-section of stock returns. We pre-

dict that a wave of investor sentiment has larger effects on securities whose valua-

tions are highly subjective and difficult to arbitrage. Consistent with this prediction,

we find that when beginning-of-period proxies for sentiment are low, subsequent re-

turns are relatively high for small stocks, young stocks, high volatility stocks, un-

profitable stocks, non-dividend-paying stocks, extreme growth stocks, and distressed

stocks. When sentiment is high, on the other hand, these categories of stock earn

relatively low subsequent returns.

CLASSICAL FINANCE THEORY LEAVES NO ROLE FOR INVESTOR SENTIMENT. Rather, thistheory argues that competition among rational investors, who diversify to opti-mize the statistical properties of their portfolios, will lead to an equilibrium inwhich prices equal the rationally discounted value of expected cash flows, andin which the cross-section of expected returns depends only on the cross-sectionof systematic risks.1 Even if some investors are irrational, classical theory ar-gues, their demands are offset by arbitrageurs and thus have no significantimpact on prices.

In this paper, we present evidence that investor sentiment may have signifi-cant effects on the cross-section of stock prices. We start with simple theoreticalpredictions. Because a mispricing is the result of an uninformed demand shockin the presence of a binding arbitrage constraint, we predict that a broad-based wave of sentiment has cross-sectional effects (that is, does not simplyraise or lower all prices equally) when sentiment-based demands or arbitrage

∗Baker is at the Harvard Business School and National Bureau of Economic Research; Wurgler

is at the NYU Stern School of Business and the National Bureau of Economic Research. We thank

an anonymous referee, Rob Stambaugh (the editor), Ned Elton, Wayne Ferson, Xavier Gabaix,

Marty Gruber, Lisa Kramer, Owen Lamont, Martin Lettau, Anthony Lynch, Jay Shanken, Meir

Statman, Sheridan Titman, and Jeremy Stein for helpful comments, as well as participants of

conferences or seminars at Baruch College, Boston College, the Chicago Quantitative Alliance,

Emory University, the Federal Reserve Bank of New York, Harvard University, Indiana University,

Michigan State University, NBER, the Norwegian School of Economics and Business, Norwegian

School of Management, New York University, Stockholm School of Economics, Tulane University,

the University of Amsterdam, the University of British Columbia, the University of Illinois, the

University of Kentucky, the University of Michigan, the University of Notre Dame, the University

of Texas, and the University of Wisconsin. We gratefully acknowledge financial support from the

Q Group and the Division of Research of the Harvard Business School.1 See Gomes, Kogan, and Zhang (2003) for a recent model in this tradition.

1645

1646 The Journal of Finance

constraints vary across stocks. In practice, these two distinct channels lead toquite similar predictions because stocks that are likely to be most sensitive tospeculative demand, those with highly subjective valuations, also tend to bethe riskiest and costliest to arbitrage. Concretely, then, theory suggests twodistinct channels through which the shares of certain firms—newer, smaller,more volatile, unprofitable, non-dividend paying, distressed or with extremegrowth potential, and firms with analogous characteristics—are likely to bemore affected by shifts in investor sentiment.

To investigate this prediction empirically, and to get a more tangible sense ofthe intrinsically elusive concept of investor sentiment, we start with a summaryof the rises and falls in U.S. market sentiment from 1961 through the Internetbubble. This summary is based on anecdotal accounts and thus by its naturecan only be a suggestive, ex post characterization of fluctuations in sentiment.Nonetheless, its basic message appears broadly consistent with our theoreticalpredictions and suggests that more rigorous tests are warranted.

Our main empirical approach is as follows. Because cross-sectional patternsof sentiment-driven mispricing would be difficult to identify directly, we ex-amine whether cross-sectional predictability patterns in stock returns dependupon proxies for beginning-of-period sentiment. For example, low future returnson young firms relative to old firms, conditional on high values for proxies forbeginning-of-period sentiment, would be consistent with the ex ante relativeovervaluation of young firms. As usual, we are mindful of the joint hypothesisproblem that any predictability patterns we find actually reflect compensationfor systematic risks.

The first step is to gather proxies for investor sentiment that we can use astime-series conditioning variables. Since there are no perfect and/or uncontro-versial proxies for investor sentiment, our approach is necessarily practical.Specifically, we consider a number of proxies suggested in recent work andform a composite sentiment index based on their first principal component. Toreduce the likelihood that these proxies are connected to systematic risk, wealso form an index based on sentiment proxies that have been orthogonalized toseveral macroeconomic conditions. The sentiment indexes visibly line up withhistorical accounts of bubbles and crashes.

We then test how the cross-section of subsequent stock returns varies withbeginning-of-period sentiment. Using monthly stock returns between 1963 and2001, we start by forming equal-weighted decile portfolios based on several firmcharacteristics. (Our theory predicts, and the empirical results confirm, thatlarge firms will be less affected by sentiment, and hence value weighting willtend to obscure the relevant patterns.) We then look for patterns in the averagereturns across deciles conditional upon the beginning-of-period level of senti-ment. We find that when sentiment is low (below sample average), small stocksearn particularly high subsequent returns, but when sentiment is high (aboveaverage), there is no size effect at all. Conditional patterns are even sharperwhen we sort on other firm characteristics. When sentiment is low, subsequentreturns are higher on very young (newly listed) stocks than older stocks, high-return volatility than low-return volatility stocks, unprofitable stocks thanprofitable ones, and nonpayers than dividend payers. When sentiment is high,

Investor Sentiment and the Cross-Section of Stock Returns 1647

these patterns completely reverse. In other words, several characteristics thatdo not have any unconditional predictive power actually display sign-flippingpredictive ability, in the hypothesized directions, once one conditions on senti-ment. These are our most striking findings. Although earlier data are not asrich, some of these patterns are also apparent in a sample that covers 1935through 1961.

The sorts also suggest that sentiment affects extreme growth and distressedfirms in similar ways. Note that when stocks are sorted into deciles by salesgrowth, book-to-market, or external financing activity, growth and distressfirms tend to lie at opposing extremes, with more “stable” firms in the middledeciles. We find that when sentiment is low, the subsequent returns on stocks atboth extremes are especially high relative to their unconditional average, whilestocks in the middle deciles are less affected by sentiment. (The result is notstatistically significant for book-to-market, however.) This U-shaped patternin the conditional difference is also broadly consistent with theoretical pre-dictions: both extreme growth and distressed firms have relatively subjectivevaluations and are relatively hard to arbitrage, and so they should be expectedto be most affected by sentiment. Again, note that this intriguing conditionalpattern would be averaged away in an unconditional study.

We then consider a regression approach, which allows us to control for co-movement in size and book-to-market-sorted stocks using the Fama-French(1993) factors. We use the sentiment indexes to forecast the returns of varioushigh-minus-low portfolios (in terms of sensitivity to sentiment). Not surpris-ingly, given that our decile portfolios are equal-weighted and several of thecharacteristics we examine are correlated with size, the inclusion of SMB asa control tends to reduce the magnitude of the predictability, although somepredictive power generally remains.

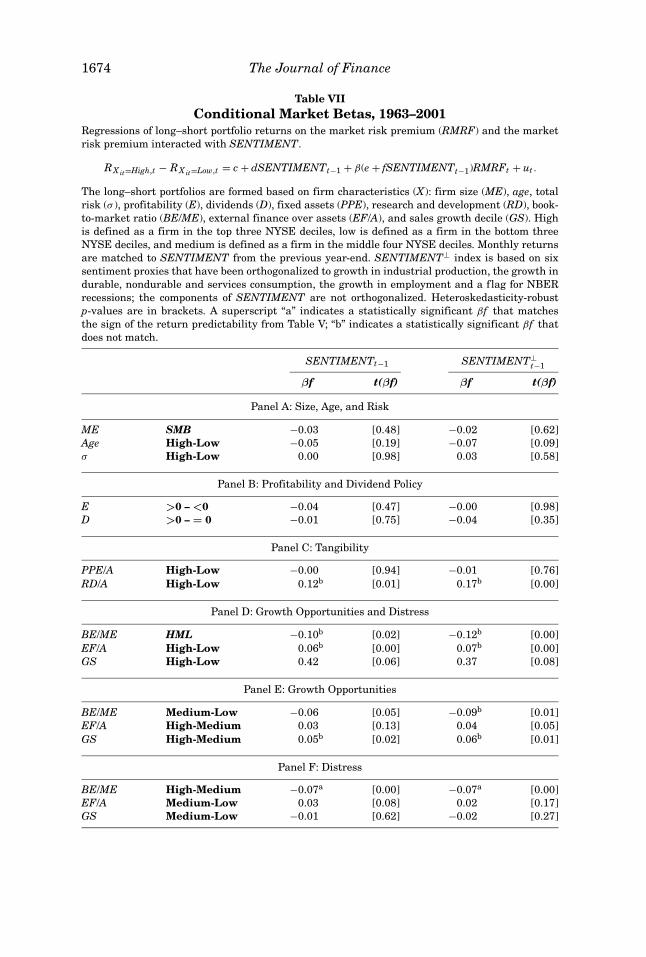

We then turn to the classical alternative explanation, namely, that they sim-ply reflect a complex pattern of compensation for systematic risk. This expla-nation would account for the predictability evidence by either time variationin rational, market-wide risk premia or time variation in the cross-sectionalpattern of risk, that is, beta loadings. Further tests cast doubt on these hy-potheses. We test the second possibility directly and find no link between thepatterns in predictability and patterns in betas with market returns or con-sumption growth. If risk is not changing over time, then the first possibilityrequires not just time variation in risk premia, but also changes in sign. Putsimply, it would require that in half of our sample period (when sentiment isrelatively low), older, less volatile, profitable, and/or dividend-paying firms ac-tually require a risk premium over very young, highly volatile, unprofitable,and/or nonpayers. This is counterintuitive. Other aspects of the results alsosuggest that systematic risk is not a complete explanation.

The results challenge the classical view of the cross-section of stock pricesand, in doing so, build on several recent themes. First, the results complementearlier work that shows sentiment helps to explain the time series of returns(Kothari and Shanken (1997), Neal and Wheatley (1998), Shiller (1981, 2000),Baker and Wurgler (2000)). Campbell and Cochrane (2000), Wachter (2000),Lettau and Ludvigson (2001), and Menzly, Santos, and Veronesi (2004) examine

1648 The Journal of Finance

the effects of conditional systematic risks; here we condition on investor sen-timent. Daniel and Titman (1997) test a characteristics-based model for thecross-section of expected returns; we extend their specification into a condi-tional characteristics-based model. Shleifer (2000) surveys early work on sen-timent and limited arbitrage, two key ingredients here. Barberis and Shleifer(2003), Barberis, Shleifer, and Wurgler (2005), and Peng and Xiong (2004) dis-cuss category-level trading, and Fama and French (1993) document comove-ment of stocks of similar sizes and book-to-market ratios; uninformed demandshocks for categories of stocks with similar characteristics are central to ourresults. Finally, we extend and unify known relationships among sentiment,IPOs, and small stock returns (Lee, Shleifer, and Thaler (1991), Swaminathan(1996), Neal and Wheatley (1998)).

Section I discusses theoretical predictions. Section II provides a qualitativehistory of recent speculative episodes. Section III describes our empirical hy-potheses and data, and Section IV presents the main empirical tests. Section Vconcludes.

I. Theoretical Effects of Sentiment on the Cross-Section

A mispricing is the result of both an uninformed demand shock and a limiton arbitrage. One can therefore think of two distinct channels through whichinvestor sentiment, as defined more precisely below, might affect the cross-section of stock prices. In the first channel, sentimental demand shocks varyin the cross-section, while arbitrage limits are constant. In the second, thedifficulty of arbitrage varies across stocks but sentiment is generic. We discussthese in turn.

A. Cross-Sectional Variation in Sentiment

One possible definition of investor sentiment is the propensity to speculate.2

Under this definition, sentiment drives the relative demand for speculativeinvestments, and therefore causes cross-sectional effects even if arbitrage forcesare the same across stocks.

What makes some stocks more vulnerable to broad shifts in the propensityto speculate? We suggest that the main factor is the subjectivity of their valu-ations. For instance, consider a canonical young, unprofitable, extreme growthstock. The lack of an earnings history combined with the presence of appar-ently unlimited growth opportunities allows unsophisticated investors to de-fend, with equal plausibility, a wide spectrum of valuations, from much too lowto much too high, as suits their sentiment. During a bubble period, when thepropensity to speculate is high, this profile of characteristics also allows invest-ment bankers (or swindlers) to further argue for the high end of valuations. Bycontrast, the value of a firm with a long earnings history, tangible assets, and

2 Aghion and Stein (2004) develop a model with both rational expectations and bounded ratio-

nality in which investors periodically emphasize growth over profitability. While the emphasis is

on the corporate and macroeconomic effects, the bounded-rationality version of the model offers

some similar predictions for the cross-section of returns.

Investor Sentiment and the Cross-Section of Stock Returns 1649

stable dividends is much less subjective, and thus its stock is likely to be lessaffected by fluctuations in the propensity to speculate.3

While the above channel suggests how variation in the propensity to spec-ulate may generally affect the cross-section, it does not take a stand on howsentimental investors actually choose stocks. We suggest that they simply de-mand stocks that have the bundle of salient characteristics that is compatiblewith their sentiment.4 That is, investors with a low propensity to speculate maydemand profitable, dividend-paying stocks not because profitability and divi-dends are correlated with some unobservable firm property that defines safetyto the investor, but precisely because the salient characteristics “profitability”and “dividends” are essentially taken to define safety.5 Likewise, the salientcharacteristics “no earnings,” “young age,” and “no dividends” mark the stockas speculative. Casual observation suggests that such an investment processmay be a more accurate description of how typical investors pick stocks thanthe process outlined by Markowitz (1959), in which investors view individualsecurities purely in terms of their statistical properties.

B. Cross-Sectional Variation in Arbitrage

One might also define investor sentiment as optimism or pessimism aboutstocks in general. Indiscriminate waves of sentiment still affect the cross-section, however, if arbitrage forces are relatively weaker in a subset of stocks.

This channel is better understood than the cross-sectional variation in senti-ment channel. A body of theoretical and empirical research shows that arbitragetends to be particularly risky and costly for young, small, unprofitable, extremegrowth, or distressed stocks. First, their high idiosyncratic risk makes relative-value arbitrage especially risky (Wurgler and Zhuravskaya (2002)). Moreover,such stocks tend to be more costly to trade (Amihud and Mendelsohn (1986))and particularly expensive, sometimes impossible, to sell short (D’Avolio (2002),Geczy, Musto, and Reed (2002), Jones and Lamont (2002), Duffie, Garleanu, and

3 The favorite-longshot bias in racetrack betting is a static illustration of the notion that investors

with a high propensity to speculate (racetrack bettors) have a relatively high demand for the most

speculative bets (longshots have the most negative expected returns; see Hausch and Ziemba

(1995)).4 The idea that investors view securities as a vector of salient characteristics borrows from

Lancaster (1966, 1971), who views consumer demand theory from the perspective that the utility

of a consumer good (e.g, oranges) derives from more primitive characteristics (fiber and vitamin C).5 The implications of categorization for finance are explored by Baker and Wurgler (2003),

Barberis and Shleifer (2003), Barberis, Shleifer, and Wurgler (2005), Greenwood and Sosner (2003),

and Peng and Xiong (2004). Note that if investors infer category membership from salient char-

acteristics (some psychologists propose that category membership is determined by the presence

of defining or characteristic features, see, for example, Smith, Shoben, and Rips (1974)), then

sentiment-driven demand will be directly connected to characteristics even if sentimental investors

undertake an intervening process of categorization and trade entirely at the category level. It is

also empirically convenient to boil key investment categories down into vectors of stable and mea-

surable characteristics: One can use the same empirical framework to study episodes such as the

late 1960s growth stocks bubble and the Internet bubble. In other words, the term “Internet bub-

ble” is interesting, but it does not make for a useful or testable theory. The key is to examine the

recurring underlying characteristics.

1650 The Journal of Finance

Pedersen (2002), Lamont and Thaler (2003), Mitchell, Pulvino, and Stafford(2002)). Further, their lower liquidity also exposes would-be arbitrageurs topredatory attacks (Brunnermeier and Pedersen (2005)).

The key point of this discussion is that, in practice, the same stocks that arethe hardest to arbitrage also tend to be the most difficult to value. While forexpositional purposes we have outlined the two channels separately, they arelikely to have overlapping effects. This may make them difficult to distinguishempirically; however, it only strengthens our predictions about what region ofthe cross-section is most affected by sentiment. Indeed, the two channels can re-inforce each other. For example, the fact that investors can convince themselvesof a wide range of valuations in some regions of the cross-section generates anoise-trader risk that further deters short-horizon arbitrageurs (De Long et al.(1990), Shleifer and Vishny (1997)).6

II. An Anecdotal History of Investor Sentiment, 1961–2002

Here we briefly summarize the most prominent U.S. stock market bubblesbetween 1961 and 2002 (matching the period of our main data). The reader ea-ger to see results may skip this section, but it is useful for three reasons. First,despite great interest in the effects of investor sentiment, the academic litera-ture does not contain even the most basic ex post characterization of most of therecent speculative episodes. Second, a knowledge of the rough timing of theseepisodes allows us to make a preliminary judgment about the accuracy of thequantitative proxies for sentiment that we develop later. Third, the discussionsheds some initial, albeit anecdotal, light on the plausibility of our theoreticalpredictions.

We distill our brief history of sentiment from several sources. Kindleberger(2001) draws general lessons from bubbles and crashes over the past few hun-dred years, while Brown (1991), Dreman (1979), Graham (1973), Malkiel (1990,1999), Shiller (2000), and Siegel (1998) focus more specifically on recent U.S.stock market episodes. We take each of these accounts with a grain of salt, andemphasize only those themes that appear repeatedly.

We start in 1961, a year that Graham (1973), Malkiel (1990) and Brown(1991) note as characterized by a high demand for small, young, growth stocks;Dreman (1979, p. 70) confirms their accounts. For instance, Malkiel writes ofa “new-issue mania” that was concentrated on new “tronics” firms. “ . . . Thetronics boom came back to earth in 1962. The tailspin started early in the yearand exploded in a horrendous selling wave . . . Growth stocks took the brunt ofthe decline, falling much further than the general market” (p. 54–57).

The next major bubble developed in 1967 and 1968. Brown writes that“scores of franchisers, computer firms, and mobile home manufactures seemed

6 We do not incorporate the equilibrium prediction of DeLong et al. (1990), namely that securities

with more exposure to sentiment have higher unconditional expected returns. Elton, Gruber, and

Busse (1998) argue that expected returns are not higher on stocks that have higher sensitivities

to the closed-end fund discount. However, Brown et al. (2003) argue that exposure to a sentiment

factor constructed from daily mutual fund flows is a priced factor in the United States and Japan.

Investor Sentiment and the Cross-Section of Stock Returns 1651

to promise overnight wealth . . . . [while] quality was pretty much forgotten”(p. 90). Malkiel and Dreman also note this pattern of a focus on firms withstrong earnings growth or potential and an avoidance of “the major industrialgiants, ‘buggywhip companies,’ as they were sometimes contemptuously called”(Dreman 1979, p. 74–75). Another characteristic apparently out of favor wasdividends. According to the New York Times, “during the speculative marketof the late 1960s many brokers told customers that it didn’t matter whether acompany paid a dividend—just so long as its stock kept going up” (9/13/1976).But “after 1968, as it became clear that capital losses were possible, investorscame to value dividends” (10/7/1999). In summarizing the performance of stocksfrom the end of 1968 through August 1971, Graham (1973) writes: “[our] com-parative results undoubtedly reflect the tendency of smaller issues of inferiorquality to be relatively overvalued in bull markets, and not only to suffer moreserious declines than the stronger issues in the ensuing price collapse, but alsoto delay their full recovery—in many cases indefinitely” (p. 212).

Anecdotal accounts invariably describe the early 1970s as a bear market,with sentiment at a low level. However, a set of established, large, stable, con-sistently profitable stocks known as the “nifty fifty” enjoyed notably high val-uations. Brown (1991), Malkiel (1990), and Siegel (1998) each highlight thisepisode. Siegel writes, “All of these stocks had proven growth records, contin-ual increases in dividends . . . and high market capitalization” (p. 106). Note thatthis speculative episode is a mirror image of those described above (and below).That is, the bubbles associated with high sentiment periods centered on small,young, unprofitable growth stocks, whereas the nifty fifty episode appears tobe a bubble in a set of firms with an opposite set of characteristics (old, large,and continuous earnings and dividend growth) that happened in a period of lowsentiment.

The late 1970s through mid 1980s are described as a period of generallyhigh sentiment, perhaps associated with Reagan-era optimism. This periodwitnessed a series of speculative episodes. Dreman describes a bubble in gam-bling issues in 1977 and 1978. Ritter (1984) studies the hot-issue market of1980, and finds greater initial returns on IPOs of natural resource start-upsthan on large, mature, profitable offerings. Of 1983, Malkiel (p. 74–75) writesthat “the high-technology new-issue boom of the first half of 1983 was an al-most perfect replica of the 1960’s episodes . . . The bubble appears to have burstearly in the second half of 1983 . . . the carnage in the small company and new-issue markets was truly catastrophic.” Brown confirms this account. Of themid 1980s, Malkiel writes that “What electronics was to the 1960s, biotech-nology became to the 1980s . . . . new issues of biotech companies were eagerlygobbled up . . . . having positive sales and earnings was actually considered adrawback” (p. 77–79). But by 1987 and 1988, “market sentiment had changedfrom an acceptance of an exciting story . . . to a desire to stay closer to earth withlow-multiple stocks that actually pay dividends” (p. 79).

The late 1990s bubble in technology stocks is familiar. By all accounts, in-vestor sentiment was broadly high before the bubble started to burst in 2000.Cochrane (2003) and Ofek and Richardson (2002) offer ex post perspectives on

1652 The Journal of Finance

the bubble, while Asness et al. (2000) and Chan, Karceski, and Lakonishok(2000) were arguing even before the crash that late 1990s growth stockvaluations were difficult to ascribe to rationally expected earnings growth.Malkiel draws parallels to episodes in the 1960s, 1970s, and 1980s, and Shiller(2000) draws parallels to the late 1920s. As in earlier speculative episodes thatoccurred in high sentiment periods, demand for dividend payers seems to havebeen low (New York Times, 1/6/1998). Ljungqvist and Wilhelm (2003) find that80% of the 1999 and 2000 IPO cohorts had negative earnings per share andthat the median age of 1999 IPOs was 4 years. This contrasts with an averageage of over 9 years just prior to the emergence of the bubble, and of over 12years by 2001 and 2002 (Ritter (2003)).

These anecdotes suggest some regular patterns in the effect of investor senti-ment on the cross-section. For instance, canonical extreme growth stocks seemto be especially prone to bubbles (and subsequent crashes), consistent with theobservation that they are more appealing to speculators and optimists and atthe same time hard to arbitrage. The “nifty fifty” bubble is a notable excep-tion, but anecdotal accounts suggest that this bubble occurred during a periodof broadly low sentiment, so it may still be consistent with the cross-sectionalprediction that an increase in sentiment increases the relative price of thosestocks that are the most subjective to value and the hardest to arbitrage. Wenow turn to formal tests of this prediction.

III. Empirical Approach and Data

A. Empirical Approach

Theory and historical anecdote both suggest that sentiment may cause sys-tematic patterns of mispricing. Because mispricing is hard to identify directly,however, our approach is to look for systematic patterns of mispricing correc-tion. For example, a pattern in which returns on young and unprofitable growthfirms are (on average) especially low when beginning-of-period sentiment is es-timated to be high may represent the correction of a bubble in growth stocks.

Specifically, to identify sentiment-driven changes in cross-sectional pre-dictability patterns, we need to control for two more basic effects, namely, thegeneric impact of investor sentiment on all stocks and the generic impact ofcharacteristics across all time periods. Thus, we organize our analysis looselyaround the following predictive specification:

Et−1[Rit] = a + a1Tt−1 + b′1xit−1 + b′

2Tt−1xit−1, (1)

where i indexes firms, t denotes time, x is a vector of characteristics, and T is aproxy for sentiment. The coefficient a1 picks up the generic effect of sentiment,and the vector b1 the generic effect of characteristics. Our interest centers onb2. The null is that b2 equals zero or, more precisely, that any nonzero effect isrational compensation for systematic risk. The alternative is that b2 is nonzeroand reveals cross-sectional patterns in sentiment-driven mispricing. We callEquation (1) a “conditional characteristics model” because it adds conditionalterms to the characteristics model of Daniel and Titman (1997).

Investor Sentiment and the Cross-Section of Stock Returns 1653

B. Characteristics and Returns

The firm-level data are from the merged CRSP-Compustat database. Thesample includes all common stock (share codes 10 and 11) between 1962 through2001. Following Fama and French (1992), we match accounting data for fiscalyear-ends in calendar year t − 1 to (monthly) returns from July t through Junet + 1, and we use their variable definitions when possible.

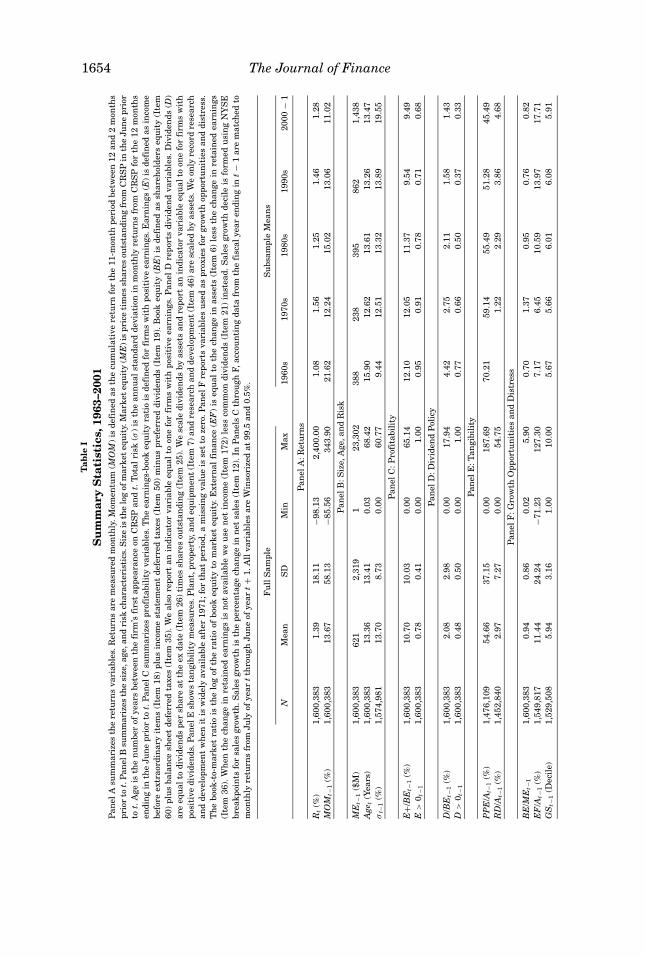

Table I shows summary statistics. Panel A summarizes returns variables.Following common practice, we define momentum, MOM, as the cumulativeraw return for the 11-month period from 12 through 2 months prior to theobservation return. Because momentum is not mentioned as a salient charac-teristic in historical anecdote, and theory does not suggest a direct connectionbetween momentum and the difficulty of valuation or arbitrage, we use mo-mentum merely as a control variable to understand the independence of ourresults from known mispricing patterns.

The remaining panels summarize the firm and security characteristics thatwe consider. The previous sections’ discussions point us directly to several vari-ables. To that list, we add a few more characteristics that, by introspection,seem likely to be salient to investors. Overall, we roughly group characteristicsas pertaining to firm size and age, profitability, dividends, asset tangibility, andgrowth opportunities and/or distress.

Size and age characteristics include market equity, ME, from June of yeart, measured as price times shares outstanding from CRSP. We match ME tomonthly returns from July of year t through June of year t + 1. Firm age, Age,is the number of years since the firm’s first appearance on CRSP, measured tothe nearest month,7 and Sigma is the standard deviation of monthly returnsover the 12 months ending in June of year t. If there are at least nine returnsavailable to estimate it, Sigma is then matched to monthly returns from Julyof year t through June of year t + 1. While historical anecdote does not identifystock volatility itself as a salient characteristic, prior work argues that it islikely to be a good proxy for the difficulty of both valuation and arbitrage.

Profitability characteristics include the return on equity, E+/BE, which ispositive for profitable firms and zero for unprofitable firms. Earnings (E) isincome before extraordinary items (Item 18) plus income statement deferredtaxes (Item 50) minus preferred dividends (Item 19), if earnings are positive;book equity (BE) is shareholders equity (Item 60) plus balance sheet deferredtaxes (Item 35). The profitability dummy variable E > 0 takes the value onefor profitable firms and zero for unprofitable firms.

Dividend characteristics include dividends to equity, D/BE, which is divi-dends per share at the ex date (Item 26) times Compustat shares outstanding(Item 25) divided by book equity. The dividend payer dummy D > 0 takes thevalue one for firms with positive dividends per share by the ex date. The declinenoted by Fama and French (2001) in the percentage of firms that pay dividendsis apparent.

7 Barry and Brown (1984) use the more accurate term “period of listing.” A large number of firms

appear on CRSP for the first time in December 1972, when Nasdaq coverage begins. Excluding these

firms from our analyses of age does not change any of our inferences.

1654 The Journal of FinanceT

able

I

Su

mm

ary

Sta

tist

ics,

1963

–200

1P

an

el

Asu

mm

ari

zes

the

retu

rns

va

ria

ble

s.R

etu

rns

are

mea

sure

dm

on

thly

.M

om

en

tum

(MO

M)

isd

efi

ned

as

the

cum

ula

tive

retu

rnfo

rth

e1

1-m

on

thp

eri

od

betw

een

12

an

d2

mon

ths

pri

or

tot.

Pa

nel

Bsu

mm

ari

zes

the

size

,a

ge,a

nd

risk

cha

ract

eri

stic

s.S

ize

isth

elo

gof

ma

rket

eq

uit

y.M

ark

et

eq

uit

y(M

E)

isp

rice

tim

es

sha

res

ou

tsta

nd

ing

from

CR

SP

inth

eJu

ne

pri

or

tot.

Age

isth

en

um

ber

of

yea

rsb

etw

een

the

firm

’sfi

rst

ap

pea

ran

ceon

CR

SP

an

dt.

Tota

lri

sk(σ

)is

the

an

nu

al

sta

nd

ard

devia

tion

inm

on

thly

retu

rns

from

CR

SP

for

the

12

mon

ths

en

din

gin

the

Ju

ne

pri

or

tot.

Pa

nel

Csu

mm

ari

zes

pro

fita

bil

ity

va

ria

ble

s.T

he

ea

rnin

gs-

book

eq

uit

yra

tio

isd

efi

ned

for

firm

sw

ith

posi

tive

ea

rnin

gs.

Ea

rnin

gs

(E)

isd

efi

ned

as

inco

me

befo

reextr

aord

ina

ryit

em

s(I

tem

18

)p

lus

inco

me

sta

tem

en

td

efe

rred

taxes

(Ite

m5

0)

min

us

pre

ferr

ed

div

iden

ds

(Ite

m1

9).

Book

eq

uit

y(B

E)

isd

efi

ned

as

sha

reh

old

ers

eq

uit

y(I

tem

60

)p

lus

ba

lan

cesh

eet

defe

rred

taxes

(Ite

m3

5).

We

als

ore

port

an

ind

ica

tor

va

ria

ble

eq

ua

lto

on

efo

rfi

rms

wit

hp

osi

tive

ea

rnin

gs.

Pa

nel

Dre

port

sd

ivid

en

dva

ria

ble

s.D

ivid

en

ds

(D)

are

eq

ua

lto

div

iden

ds

per

sha

rea

tth

eex

da

te(I

tem

26

)ti

mes

sha

res

ou

tsta

nd

ing

(Ite

m2

5).

We

sca

led

ivid

en

ds

by

ass

ets

an

dre

port

an

ind

ica

tor

va

ria

ble

eq

ua

lto

on

efo

rfi

rms

wit

h

posi

tive

div

iden

ds.

Pa

nel

Esh

ow

sta

ngib

ilit

ym

ea

sure

s.P

lan

t,p

rop

ert

y,a

nd

eq

uip

men

t(I

tem

7)

an

dre

sea

rch

an

dd

evelo

pm

en

t(I

tem

46

)a

resc

ale

db

ya

ssets

.W

eon

lyre

cord

rese

arc

h

an

dd

evelo

pm

en

tw

hen

itis

wid

ely

ava

ila

ble

aft

er

19

71

;fo

rth

at

peri

od

,a

mis

sin

gva

lue

isse

tto

zero

.P

an

el

Fre

port

sva

ria

ble

su

sed

as

pro

xie

sfo

rgro

wth

op

port

un

itie

sa

nd

dis

tress

.

Th

eb

ook

-to-m

ark

et

rati

ois

the

log

of

the

rati

oof

book

eq

uit

yto

ma

rket

eq

uit

y.E

xte

rna

lfi

na

nce

(EF

)is

eq

ua

lto

the

cha

nge

ina

ssets

(Ite

m6

)le

ssth

ech

an

ge

inre

tain

ed

ea

rnin

gs

(Ite

m3

6).

Wh

en

the

cha

nge

inre

tain

ed

ea

rnin

gs

isn

ot

ava

ila

ble

we

use

net

inco

me

(Ite

m1

72

)le

ssco

mm

on

div

iden

ds

(Ite

m2

1)

inst

ea

d.

Sa

les

gro

wth

deci

leis

form

ed

usi

ng

NY

SE

bre

ak

poin

tsfo

rsa

les

gro

wth

.S

ale

sgro

wth

isth

ep

erc

en

tage

cha

nge

inn

et

sale

s(I

tem

12

).In

Pa

nels

Cth

rou

gh

F,

acc

ou

nti

ng

da

tafr

om

the

fisc

al

yea

ren

din

gin

t−

1a

rem

atc

hed

to

mon

thly

retu

rns

from

Ju

lyof

yea

rt

thro

ugh

Ju

ne

of

yea

rt+

1.

All

va

ria

ble

sa

reW

inso

rize

da

t9

9.5

an

d0

.5%

.

Fu

llS

am

ple

Su

bsa

mp

leM

ea

ns

NM

ea

nS

DM

inM

ax

19

60

s1

97

0s

19

80

s1

99

0s

20

00

−1

Pa

nel

A:

Retu

rns

Rt

(%)

1,6

00

,38

31

.39

18

.11

−98

.13

2,4

00

.00

1.0

81

.56

1.2

51

.46

1.2

8

MO

Mt−

1(%

)1

,60

0,3

83

13

.67

58

.13

−85

.56

34

3.9

02

1.6

21

2.2

41

5.0

21

3.0

61

1.0

2

Pa

nel

B:

Siz

e,

Age,

an

dR

isk

ME

t−1

($M

)1

,60

0,3

83

62

12

,31

91

23

,30

23

88

23

83

95

86

21

,43

8

Age

t(Y

ea

rs)

1,6

00

,38

31

3.3

61

3.4

10

.03

68

.42

15

.90

12

.62

13

.61

13

.26

13

.47

σt−

1(%

)1

,57

4,9

81

13

.70

8.7

30

.00

60

.77

9.4

41

2.5

11

3.3

21

3.8

91

9.5

5

Pa

nel

C:

Pro

fita

bil

ity

E+/

BE

t−1

(%)

1,6

00

,38

31

0.7

01

0.0

30

.00

65

.14

12

.10

12

.05

11

.37

9.5

49

.49

E>

0t−

11

,60

0,3

83

0.7

80

.41

0.0

01

.00

0.9

50

.91

0.7

80

.71

0.6

8

Pa

nel

D:

Div

iden

dP

oli

cy

D/B

Et−

1(%

)1

,60

0,3

83

2.0

82

.98

0.0

01

7.9

44

.42

2.7

52

.11

1.5

81

.43

D>

0t−

11

,60

0,3

83

0.4

80

.50

0.0

01

.00

0.7

70

.66

0.5

00

.37

0.3

3

Pa

nel

E:

Ta

ngib

ilit

y

PP

E/A

t−1

(%)

1,4

76

,10

95

4.6

63

7.1

50

.00

18

7.6

97

0.2

15

9.1

45

5.4

95

1.2

84

5.4

9

RD

/At−

1(%

)1

,45

2,8

40

2.9

77

.27

0.0

05

4.7

51

.22

2.2

93

.86

4.6

8

Pa

nel

F:

Gro

wth

Op

port

un

itie

sa

nd

Dis

tress

BE

/ME

t−1

1,6

00

,38

30

.94

0.8

60

.02

5.9

00

.70

1.3

70

.95

0.7

60

.82

EF

/At−

1(%

)1

,54

9,8

17

11

.44

24

.24

−71

.23

12

7.3

07

.17

6.4

51

0.5

91

3.9

71

7.7

1

GS

t−1

(Deci

le)

1,5

29

,50

85

.94

3.1

61

.00

10

.00

5.6

75

.66

6.0

16

.08

5.9

1

Investor Sentiment and the Cross-Section of Stock Returns 1655

The referee suggests that asset tangibility may proxy for the difficulty ofvaluation. Asset tangibility characteristics are measured by property, plantand equipment (Item 7) over assets, PPE/A, and research and developmentexpense over assets (Item 46), RD/A. One concern is the coverage of the R&Dvariable. We do not consider this variable prior to 1972, because the FinancialAccounting Standards Board did not require R&D to be expensed until 1974and Compustat coverage prior to 1972 is very poor. Also, even in recent yearsless than half of the sample reports positive R&D.

Characteristics indicating growth opportunities, distress, or both includebook-to-market equity, BE/ME, whose elements are defined above. Externalfinance, EF/A, is the change in assets (Item 6) minus the change in retainedearnings (Item 36) divided by assets. Sales growth (GS) is the change in net sales(Item 12) divided by prior-year net sales. Sales growth GS/10 is the decile of thefirm’s sales growth in the prior year relative to NYSE firms’ decile breakpoints.

As will become clear below, one must grasp the multidimensional nature ofthe growth and distress variables in order to understand how they interact withsentiment. In particular, book-to-market wears at least three hats: High valuesmay indicate distress; low values may indicate high growth opportunities; and,as a scaled-price variable, book-to-market is also a generic valuation indicatorthat varies with any source of mispricing or rational expected returns. Sim-ilarly, sales growth and external finance wear at least two hats: Low values(which are negative) may indicate distress, and high values may reflect growthopportunities. Further, to the extent that market timing motives drive externalfinance, EF/A also wears a third hat as a generic misvaluation indicator.

All explanatory variables are Winsorized each year at their 0.5 and 99.5 per-centiles. Finally, in Panels C through F, the accounting data for fiscal yearsending in calendar year t − 1 are matched to monthly returns from July of yeart through June of year t + 1.

C. Investor Sentiment

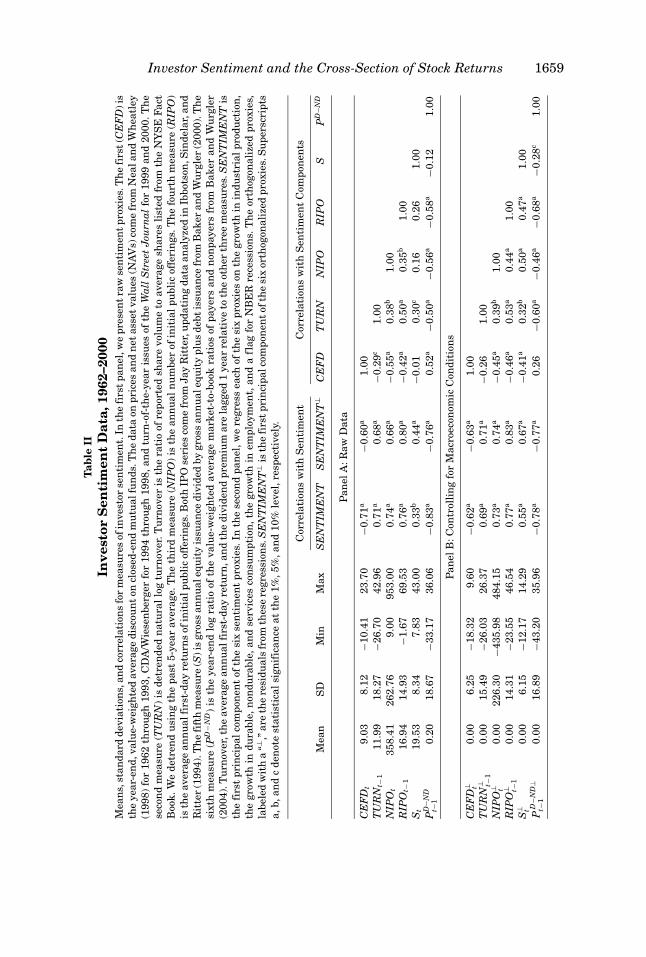

Prior work suggests a number of proxies for sentiment to use as time-seriesconditioning variables. There are no definitive or uncontroversial measures,however. We therefore form a composite index of sentiment that is based on thecommon variation in six underlying proxies for sentiment: the closed-end funddiscount, NYSE share turnover, the number and average first-day returns onIPOs, the equity share in new issues, and the dividend premium. The sentimentproxies are measured annually from 1962 to 2001. We first introduce eachproxy separately, and then discuss how they are formed into overall sentimentindexes.

The closed-end fund discount, CEFD, is the average difference between thenet asset values (NAV) of closed-end stock fund shares and their market prices.Prior work suggests that CEFD is inversely related to sentiment. Zweig (1973)uses it to forecast reversion in Dow Jones stocks, and Lee et al. (1991) arguethat sentiment is behind various features of closed-end fund discounts. Wetake the value-weighted average discount on closed-end stock funds for 1962

1656 The Journal of Finance

through 1993 from Neal and Wheatley (1998), for 1994 through 1998 fromCDA/Wiesenberger, and for 1999 through 2001 from turn-of-the-year issues ofthe Wall Street Journal.

NYSE share turnover is based on the ratio of reported share volume to av-erage shares listed from the NYSE Fact Book. Baker and Stein (2004) suggestthat turnover, or more generally liquidity, can serve as a sentiment index: In amarket with short-sales constraints, irrational investors participate, and thusadd liquidity, only when they are optimistic; hence, high liquidity is a symp-tom of overvaluation. Supporting this, Jones (2001) finds that high turnoverforecasts low market returns. Turnover displays an exponential, positive trendover our period and the May 1975 elimination of fixed commissions also has avisible effect. As a partial solution, we define TURN as the natural log of theraw turnover ratio, detrended by the 5-year moving average.

The IPO market is often viewed as sensitive to sentiment, with high first-day returns on IPOs cited as a measure of investor enthusiasm, and the lowidiosyncratic returns on IPOs often interpreted as a symptom of market timing(Stigler (1964), Ritter (1991)). We take the number of IPOs, NIPO, and theaverage first-day returns, RIPO, from Jay Ritter’s website, which updates thesample in Ibbotson, Sindelar, and Ritter (1994).

The share of equity issues in total equity and debt issues is another measure offinancing activity that may capture sentiment. Baker and Wurgler (2000) findthat high values of the equity share predict low market returns. The equityshare is defined as gross equity issuance divided by gross equity plus grosslong-term debt issuance using data from the Federal Reserve Bulletin.8

Our sixth and last sentiment proxy is the dividend premium, PD−ND, the logdifference of the average market-to-book ratios of payers and nonpayers. Bakerand Wurgler (2004) use this variable to proxy for relative investor demand fordividend-paying stocks. Given that payers are generally larger, more profitablefirms with weaker growth opportunities (Fama and French (2001)), the divi-dend premium may proxy for the relative demand for this correlated bundle ofcharacteristics.

Each sentiment proxy is likely to include a sentiment component as well asidiosyncratic, non-sentiment-related components. We use principal componentsanalysis to isolate the common component. Another issue in forming an indexis determining the relative timing of the variables—that is, if they exhibit lead-lag relationships, some variables may reflect a given shift in sentiment earlierthan others. For instance, Ibbotson and Jaffe (1975), Lowry and Schwert (2002),and Benveniste et al. (2003) find that IPO volume lags the first-day returns onIPOs. Perhaps sentiment is partly behind the high first-day returns, and thisattracts additional IPO volume with a lag. More generally, proxies that involvefirm supply responses (S and NIPO) can be expected to lag behind proxies

8 While they both reflect equity issues, the number of IPOs and the equity share have important

differences. The equity share includes seasoned offerings, predicts market returns, and scales by

total external finance to isolate the composition of finance from the level. On the other hand, the

IPO variables may better reflect demand for certain IPO-like regions of the cross-section that

theory and historical anecdote suggest are most sensitive to sentiment.

Investor Sentiment and the Cross-Section of Stock Returns 1657

that are based directly on investor demand or investor behavior (RIPO, PD−ND,TURN, and CEFD).

We form a composite index that captures the common component in the sixproxies and incorporates the fact that some variables take longer to reveal thesame sentiment.9 We start by estimating the first principal component of thesix proxies and their lags. This gives us a first-stage index with 12 loadings,one for each of the current and lagged proxies. We then compute the correla-tion between the first-stage index and the current and lagged values of eachof the proxies. Finally, we define SENTIMENT as the first principal compo-nent of the correlation matrix of six variables—each respective proxy’s lead orlag, whichever has higher correlation with the first-stage index—rescaling thecoefficients so that the index has unit variance.

This procedure leads to a parsimonious index

SENTIMENTt = −0.241CEFDt + 0.242TURNt−1 + 0.253NIPOt

+ 0.257RIPOt−1 + 0.112St − 0.283P D−NDt−1 , (2)

where each of the index components has first been standardized. The firstprincipal component explains 49% of the sample variance, so we conclude thatone factor captures much of the common variation. The correlation between the12-term first-stage index and the SENTIMENT index is 0.95, suggesting thatlittle information is lost in dropping the six terms with other time subscripts.

The SENTIMENT index has several appealing properties. First, each indi-vidual proxy enters with the expected sign. Second, all but one enters withthe expected timing; with the exception of CEFD, price and investor behaviorvariables lead firm supply variables. Third, the index irons out some extremeobservations. (The dividend premium and the first-day IPO returns reachedunprecedented levels in 1999, so for these proxies to work as individual predic-tors in the full sample, these levels must be matched exactly to extreme futurereturns.)

One might object to equation (2) as a measure of sentiment on the groundsthat the principal components analysis cannot distinguish between a commonsentiment component and a common business cycle component. For instance,the number of IPOs varies with the business cycle in part for entirely rationalreasons. We want to identify when the number of IPOs is high for no good reason.We therefore construct a second index that explicitly removes business cyclevariation from each of the proxies prior to the principal components analysis.

Specifically, we regress each of the six raw proxies on growth in the indus-trial production index (Federal Reserve Statistical Release G.17), growth inconsumer durables, nondurables, and services (all from BEA National IncomeAccounts Table 2.10), and a dummy variable for NBER recessions. The residu-als from these regressions, labeled with a superscript ⊥, may be cleaner proxiesfor investor sentiment. We form an index of the orthogonalized proxies followingthe same procedure as before. The resulting index is

9 See Brown and Cliff (2004) for a similar approach to extracting a sentiment factor from a set

of noisy proxies.

1658 The Journal of Finance

SENTIMENT ⊥t = −0.198CEFD⊥

t + 0.225TURN ⊥t−1 + 0.234 NIPO⊥

t

+ 0.263RIPO⊥t−1 + 0.211S ⊥

t − 0.243P D−ND,⊥t−1 . (3)

Here, the first principal component explains 53% of the sample variance of theorthogonalized variables. Moreover, only the first eigenvalue is above 1.00. Interms of the signs and the timing of the components, SENTIMENT⊥ retainsall of the appealing properties of SENTIMENT.

Table II summarizes and correlates the sentiment measures, and Figure 1plots them. The figure shows immediately that orthogonalizing to macro vari-ables is a second-order issue. It does not qualitatively affect any componentof the index or the overall index (see Panel E). Indeed, Table II suggests thaton balance the orthogonalized proxies are slightly more correlated with eachother than are the raw proxies. If the raw variables were driven by commonmacroeconomic conditions (that we failed to remove through orthogonalization)instead of common investor sentiment, one would expect the opposite. In anycase, to demonstrate robustness we present results for both indexes in our mainanalysis.

More importantly, Figure 1 shows that the sentiment measures roughly lineup with anecdotal accounts of fluctuations in sentiment. Most proxies pointto low sentiment in the first few years of the sample, after the 1961 crash ingrowth stocks. Specifically, the closed-end fund discount and dividend premiumare high, while turnover and equity issuance-related variables are low. Eachvariable identifies a spike in sentiment in 1968 and 1969, again matching anec-dotal accounts. Sentiment then tails off until, by the mid 1970s, it is low by mostmeasures (recall that for turnover this is confounded by deregulation). The late1970s through mid 1980s sees generally rising sentiment, and, according tothe composite index, sentiment has not dropped far below a medium level since1980. At the end of 1999, near the peak of the Internet bubble, sentiment is highby most proxies. Overall, SENTIMENT⊥ is positive for the years 1968–1970,1972, 1979–1987, 1994, 1996–1997, and 1999–2001. This correspondence withanecdotal accounts seems to confirm that the measures capture the intendedvariation.

There are other variables that one might reasonably wish to include in asentiment index. The main constraint is availability and consistent measure-ment over the 1962–2001 period. We have considered insider trading as a sen-timent measure. Unfortunately, a consistent series does not appear to be avail-able for the whole sample period. However, Nejat Seyhun shared with us hismonthly series, which spans 1975 to 1994, on the fraction of public firms withnet insider buying (as plotted in Seyhun (1998, p. 117)). Lakonishok and Lee(2001) study a similar series. We average Seyhun’s series across months toobtain an annual series. Over the overlapping 20-year period, insider buyinghas a significant negative correlation with both the raw and orthogonalizedsentiment indexes, and also correlates with the six underlying components asexpected.

Investor Sentiment and the Cross-Section of Stock Returns 1659

Tab

leII

Inve

stor

Sen

tim

ent

Dat

a,19

62–2

000

Mean

s,st

an

dard

devia

tion

s,an

dco

rrela

tion

sfo

rm

easu

res

ofin

vest

or

sen

tim

en

t.In

the

firs

tp

an

el,

we

pre

sen

tra

wse

nti

men

tp

roxie

s.T

he

firs

t(C

EF

D)is

the

year-

en

d,valu

e-w

eig

hte

davera

ge

dis

cou

nt

on

close

d-e

nd

mu

tualfu

nd

s.T

he

data

on

pri

ces

an

dn

et

ass

et

valu

es

(NA

Vs)

com

efr

om

Nealan

dW

heatl

ey

(1998)

for

1962

thro

ugh

1993,

CD

A/W

iese

nberg

er

for

1994

thro

ugh

1998,

an

dtu

rn-o

f-th

e-y

ear

issu

es

of

the

Wal

lS

tree

tJo

urn

alfo

r1999

an

d2000.

Th

e

seco

nd

measu

re(T

UR

N)

isd

etr

en

ded

natu

ral

log

turn

over.

Tu

rnover

isth

era

tio

of

rep

ort

ed

share

volu

me

toavera

ge

share

sli

sted

from

the

NY

SE

Fact

Book

.W

ed

etr

en

du

sin

gth

ep

ast

5-y

ear

avera

ge.T

he

thir

dm

easu

re(N

IPO

)is

the

an

nu

al

nu

mber

of

init

ial

pu

bli

coff

eri

ngs.

Th

efo

urt

hm

easu

re(R

IPO

)

isth

eavera

ge

an

nu

alfi

rst-

day

retu

rns

of

init

ialp

ubli

coff

eri

ngs.

Both

IPO

seri

es

com

efr

om

Jay

Rit

ter,

up

dati

ng

data

an

aly

zed

inIb

bots

on

,S

ind

ela

r,an

d

Rit

ter

(1994).

Th

efi

fth

measu

re(S

)is

gro

ssan

nu

alequ

ity

issu

an

ced

ivid

ed

by

gro

ssan

nu

alequ

ity

plu

sd

ebt

issu

an

cefr

om

Bak

er

an

dW

urg

ler

(2000).

Th

e

sixth

measu

re(P

D−N

D)

isth

eyear-

en

dlo

gra

tio

of

the

valu

e-w

eig

hte

davera

ge

mark

et-

to-b

ook

rati

os

of

payers

an

dn

on

payers

from

Bak

er

an

dW

urg

ler

(2004).

Tu

rnover,

the

avera

ge

an

nu

al

firs

t-d

ay

retu

rn,an

dth

ed

ivid

en

dp

rem

ium

are

lagged

1year

rela

tive

toth

eoth

er

thre

em

easu

res.

SE

NT

IME

NT

is

the

firs

tp

rin

cip

al

com

pon

en

tof

the

six

sen

tim

en

tp

roxie

s.In

the

seco

nd

pan

el,

we

regre

sseach

of

the

six

pro

xie

son

the

gro

wth

inin

du

stri

al

pro

du

ctio

n,

the

gro

wth

ind

ura

ble

,n

on

du

rable

,an

dse

rvic

es

con

sum

pti

on

,th

egro

wth

inem

plo

ym

en

t,an

da

flag

for

NB

ER

rece

ssio

ns.

Th

eort

hogon

ali

zed

pro

xie

s,

labele

dw

ith

a“⊥ ,

”are

the

resi

du

als

from

these

regre

ssio

ns.

SE

NT

IME

NT

⊥is

the

firs

tp

rin

cip

alco

mp

on

en

tofth

esi

xort

hogon

ali

zed

pro

xie

s.S

up

ers

crip

ts

a,b,an

dc

den

ote

stati

stic

al

sign

ific

an

ceat

the

1%

,5%

,an

d10%

level,

resp

ect

ively

.

Corr

ela

tion

sw

ith

Sen

tim

en

tC

orr

ela

tion

sw

ith

Sen

tim

en

tC

om

pon

en

ts

Mean

SD

Min

Max

SE

NT

IME

NT

SE

NT

IME

NT

⊥C

EF

DT

UR

NN

IPO

RIP

OS

PD

−ND

Pan

el

A:R

aw

Data

CE

FD

t9.0

38.1

2−1

0.4

123.7

0−0

.71

a−0

.60

a1.0

0

TU

RN

t−1

11.9

918.2

7−2

6.7

042.9

60.7

1a

0.6

8a

−0.2

9c

1.0

0

NIP

Ot

358.4

1262.7

69.0

0953.0

00.7

4a

0.6

6a

−0.5

5a

0.3

8b

1.0

0

RIP

Ot−

116.9

414.9

3−1

.67

69.5

30.7

6a

0.8

0a

−0.4

2a

0.5

0a

0.3

5b

1.0

0

St

19.5

38.3

47.8

343.0

00.3

3b

0.4

4a

−0.0

10.3

0c

0.1

60.2

61.0

0

PD

−ND

t−1

0.2

018.6

7−3

3.1

736.0

6−0

.83

a−0

.76

a0.5

2a

−0.5

0a

−0.5

6a

−0.5

8a

−0.1

21.0

0

Pan

el

B:C

on

troll

ing

for

Macr

oeco

nom

icC

on

dit

ion

s

CE

FD

⊥ t0.0

06.2

5−1

8.3

29.6

0−0

.62

a−0

.63

a1.0

0

TU

RN

⊥ t−1

0.0

015.4

9−2

6.0

326.3

70.6

9a

0.7

1a

−0.2

61.0

0

NIP

O⊥ t

0.0

0226.3

0−4

35.9

8484.1

50.7

3a

0.7

4a

−0.4

5a

0.3

9b

1.0

0

RIP

O⊥ t−

10.0

014.3

1−2

3.5

546.5

40.7

7a

0.8

3a

−0.4

6a

0.5

3a

0.4

4a

1.0

0

S⊥ t

0.0

06.1

5−1

2.1

714.2

90.5

5a

0.6

7a

−0.4

1a

0.3

2b

0.5

0a

0.4

7a

1.0

0

PD

−ND

⊥t−

10.0

016.8

9−4

3.2

035.9

6−0

.78

a−0

.77

a0.2

6−0

.60

a−0

.46

a−0

.68

a−0

.28

c1.0

0

1660 The Journal of Finance

Panel A. Closed-end fund discount %

-15

-10

-5

0

5

10

15

20

25

30

1962 1967 1972 1977 1982 1987 1992 1997

-20

-15

-10

-5

0

5

10

15

Panel B. Turnover %

-40

-30

-20

-10

0

10

20

30

40

50

1962 1967 1972 1977 1982 1987 1992 1997

-30

-20

-10

0

10

20

30

Panel C. Number of IPOs

0

200

400

600

800

1000

1200

1962 1967 1972 1977 1982 1987 1992 1997

-600

-400

-200

0

200

400

600

Panel D. Average first-day return

-10

0

10

20

30

40

50

60

70

80

1962 1967 1972 1977 1982 1987 1992 1997

-30

-20

-10

0

10

20

30

40

50

60

Panel E. Equity share in new issues

0

5

10

15

20

25

30

35

40

45

50

1962 1967 1972 1977 1982 1987 1992 1997

-15

-10

-5

0

5

10

15

20

Panel F. Dividend premium

-40

-30

-20

-10

0

10

20

30

40

1962 1967 1972 1977 1982 1987 1992 1997

-50

-40

-30

-20

-10

0

10

20

30

40

50

Panel E. Sentiment index (SENTIMENT)

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

1962 1967 1972 1977 1982 1987 1992 1997

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

Figure 1. Investor sentiment, 1962–2001. The first panel shows the year-end, value-weighted

average discount on closed-end mutual funds. The data on prices and net asset values (NAVs) come

from Neal and Wheatley (1998) for 1962 through 1993, CDA/Wiesenberger for 1994 through 1998,

and turn-of-the-year issues of the Wall Street Journal for 1999 through 2001. The second panel

shows detrended log turnover. Turnover is the ratio of reported share volume to average shares

listed from the NYSE Fact Book. We detrend using the past 5-year average. The third panel shows

the annual number of initial public offerings. The fourth panel shows the average annual first-day

returns of initial public offerings. Both series come from Jay Ritter, updating data analyzed in

Ibbotson, Sindelar, and Ritter (1994). The fifth panel shows gross annual equity issuance divided

by gross annual equity plus debt issuance from Baker and Wurgler (2000). The sixth panel shows

the year-end log ratio of the value-weighted average market-to-book ratios of payers and nonpayers

from Baker and Wurgler (2004). The solid line (left axis) is raw data. We regress each measure on the

growth in industrial production, the growth in durable, nondurable, and services consumption, the

growth in employment, and a flag for NBER recessions. The dashed line (right axis) is the residuals

from this regression. The solid (dashed) line in the final panel is a first principal component index of

the six raw (orthogonalized) measures. Both are standardized to have zero mean and unit variance.

In the index, turnover, the average annual first-day return, and the dividend premium are lagged

1 year relative to the other three measures, as discussed in the text.

Investor Sentiment and the Cross-Section of Stock Returns 1661

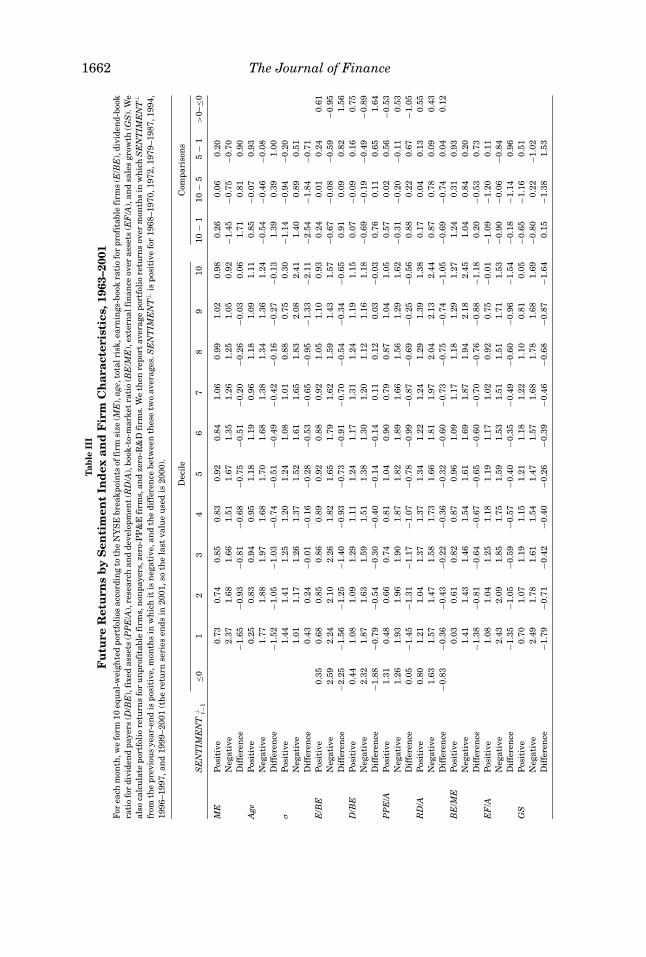

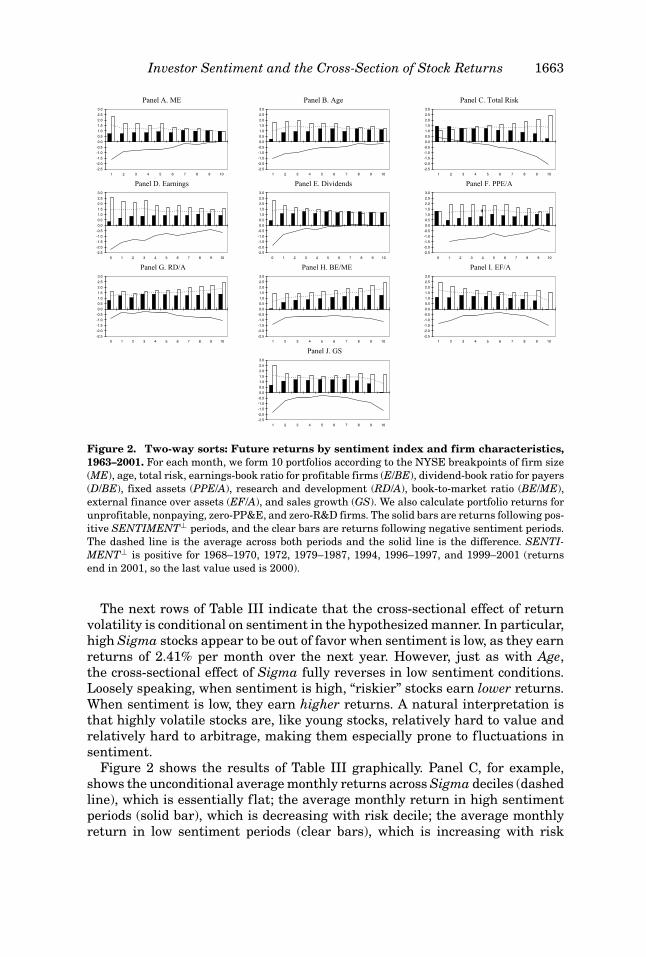

IV. Empirical Tests

A. Sorts

Table III looks for conditional characteristics effects in a simple, nonpara-metric way. We place each monthly return observation into a bin according tothe decile rank that a characteristic takes at the beginning of that month, andthen according to the level of SENTIMENT⊥ at the end of the previous calen-dar year. To keep the meaning of the deciles similar over time, we define thembased on NYSE firms. The trade-off is that there is not a uniform distribution offirms across bins in any given month. We compute the equal-weighted averagemonthly return for each bin and look for patterns. In particular, we identifytime-series changes in cross-sectional effects from the conditional difference ofaverage returns across deciles.

The first rows of Table III show the effect of size, as measured by ME, con-ditional on sentiment. These rows reveal that the size effect of Banz (1981)appears in low sentiment periods only. Specifically, Table III shows that whenSENTIMENT⊥ is negative, returns average 2.37% per month for the bottomME decile and 0.92 for the top decile. A similar pattern is apparent when con-ditioning on CEFD (not reported). A link between the size effect and closed-endfund discounts is also noted by Swaminathan (1996). This pattern is consistentwith some long-known results. Namely, the size effect is essentially a Januaryeffect (Keim (1983), Blume and Stambaugh (1983)), and the January effect, inturn, is stronger after a period of low returns (Reinganum (1983)), which is alsowhen sentiment is likely to be low.

As an aside, note that the average returns across the first two rows of Table IIIillustrate that subsequent returns tend to be higher, across most of the cross-section, when sentiment is low. This is consistent with prior results that theequity share and turnover, for example, forecast market returns. More gen-erally, it supports our premise that sentiment has broad effects, and so theexistence of richer patterns within the cross-section is not surprising.

The conditional cross-sectional effect of Age is striking. In general, in-vestors appear to demand young stocks when SENTIMENT⊥ is positive andprefer older stocks when sentiment is negative. For example, when senti-ment is pessimistic, top-decile Age firms return 0.54% per month less thanbottom-decile Age firms. However, they return 0.85% more when sentimentis optimistic. When sentiment is positive, the effect is concentrated in thevery youngest stocks, which are recent IPOs; when it is negative, the con-trast is between the bottom and top several deciles of age. Overall, there isa nearly monotonic effect in the conditional difference of returns. This re-sult is intriguing because Age has no unconditional effect.10 The strong con-ditional effects, of opposite sign, average out across high and low sentimentperiods.

10 This conclusion is in seeming contrast to Barry and Brown’s (1984) evidence of an uncondi-

tional negative period-of-listing effect; however, their sample excludes stocks listed for fewer than

61 months.

1662 The Journal of FinanceT

able

III

Fu

ture

Ret

urn

sb

yS

enti

men

tIn

dex

and

Fir

mC

har

acte

rist

ics,

1963

–200

1F

or

ea

chm

on

th,w

efo

rm1

0eq

ua

l-w

eig

hte

dp

ort

foli

os

acc

ord

ing

toth

eN

YS

Eb

rea

kp

oin

tsoffi

rmsi

ze(M

E),

age,

tota

lri

sk,ea

rnin

gs-

book

rati

ofo

rp

rofi

tab

lefi

rms

(E/B

E),

div

iden

d-b

ook

rati

ofo

rd

ivid

en

dp

ayers

(D/B

E),

fixed

ass

ets

(PP

E/A

),re

sea

rch

an

dd

evelo

pm

en

t(R

D/A

),b

ook

-to-m

ark

et

rati

o(B

E/M

E),

exte

rna

lfi

na

nce

over

ass

ets

(EF

/A),

an

dsa

les

gro

wth

(GS

).W

e

als

oca

lcu

late

port

foli

ore

turn

sfo

ru

np

rofi

tab

lefi

rms,

non

payers

,ze

ro-P

P&

Efi

rms,

an

dze

ro-R

&D

firm

s.W

eth

en

rep

ort

avera

ge

port

foli

ore

turn

sover

mon

ths

inw

hic

hS

EN

TIM

EN

T⊥

from

the

pre

vio

us

yea

r-en

dis

posi

tive,m

on

ths

inw

hic

hit

isn

ega

tive,a

nd

the

dif

fere

nce

betw

een

these

two

avera

ges.

SE

NT

IME

NT

⊥is

posi

tive

for

19

68

–1

97

0,1

97

2,1

97

9–

19

87

,1

99

4,

19

96

–1

99

7,

an

d1

99

9–

20

01

(th

ere

turn

seri

es

en

ds

in2

00

1,

soth

ela

stva

lue

use

dis

20

00

).

Deci

leC

om

pa

riso

ns

SE

NT

IME

NT

⊥ t−1

≤01

23

45

67

89

10

10

−1

10

−5

5−

1>

0–≤0

ME

Posi

tive

0.7

30

.74

0.8

50

.83

0.9

20

.84

1.0

60

.99

1.0

20

.98

0.2

60

.06

0.2

0

Nega

tive

2.3

71

.68

1.6

61

.51

1.6

71

.35

1.2

61

.25

1.0

50

.92

−1.4

5−0

.75

−0.7

0

Dif

fere

nce

−1.6

5−0

.93

−0.8

1−0

.68

−0.7

5−0

.51

−0.2

0−0

.26

−0.0

30

.06

1.7

10

.81

0.9

0

Age

Posi

tive

0.2

50

.83

0.9

40

.95

1.1

81

.19

0.9

61

.18

1.0

91

.11

0.8

5−0

.07

0.9

3

Nega

tive

1.7

71

.88

1.9

71

.68

1.7

01

.68

1.3

81

.34

1.3

61

.24

−0.5

4−0

.46

−0.0

8

Dif

fere

nce

−1.5

2−1

.05

−1.0

3−0

.74

−0.5

1−0

.49

−0.4

2−0

.16

−0.2

7−0

.13

1.3

90

.39

1.0

0

σP

osi

tive

1.4

41

.41

1.2

51

.20

1.2

41

.08

1.0

10

.88

0.7

50

.30

−1.1

4−0

.94

−0.2

0

Nega

tive

1.0

11

.17

1.2

61

.37

1.5

21

.61

1.6

51

.83

2.0

82

.41

1.4

00

.89

0.5

1

Dif

fere

nce

0.4

30

.24

−0.0

1−0

.16

−0.2

8−0

.53

−0.6

5−0

.95

−1.3

3−2

.11

−2.5

4−1

.84

−0.7

1

E/B

EP

osi

tive

0.3

50

.68

0.8

50

.86

0.8

90

.92

0.8

80

.92

1.0

51

.10

0.9

30

.24

0.0

10

.24

0.6

1

Nega

tive

2.5

92

.24

2.1

02

.26

1.8

21

.65

1.7

91

.62

1.5

91

.43

1.5

7−0

.67

−0.0

8−0

.59

−0.9

5

Dif

fere

nce

−2.2

5−1

.56

−1.2

5−1

.40

−0.9

3−0

.73

−0.9

1−0

.70

−0.5

4−0

.34

−0.6

50

.91

0.0

90

.82

1.5

6

D/B

EP

osi

tive

0.4

41

.08

1.0

91

.29

1.1

11

.24

1.1

71

.31

1.2

41

.19

1.1

50

.07

−0.0

90

.16

0.7

5

Nega

tive

2.3

21

.87

1.6

31

.59

1.5

11

.38

1.3

01

.20

1.1

21

.16

1.1

8−0

.69

−0.1

9−0

.49

−0.8

9

Dif

fere

nce

−1.8

8−0

.79

−0.5

4−0

.30

−0.4

0−0

.14

−0.1

40

.11

0.1

20

.03

−0.0

30

.76

0.1

10

.65

1.6

4

PP

E/A

Posi

tive

1.3

10

.48

0.6

60

.74

0.8

11

.04

0.9

00

.79

0.8

71

.04

1.0

50

.57

0.0

20

.56

−0.5

3

Nega

tive

1.2

61

.93

1.9

61

.90

1.8

71

.82

1.8

91

.66

1.5

61

.29

1.6

2−0

.31

−0.2

0−0

.11

0.5

3

Dif

fere

nce

0.0

5−1

.45

−1.3

1−1

.17

−1.0

7−0

.78

−0.9

9−0

.87

−0.6

9−0

.25

−0.5

60

.88

0.2

20

.67

−1.0

5

RD

/AP

osi

tive

0.8

01

.21

1.0

41

.37

1.3

71

.34

1.2

21

.24

1.2

91

.39

1.3

80

.17

0.0

40

.13

0.5

5

Nega

tive

1.6

31

.57

1.4

71

.58

1.7

31

.66

1.8

11

.97

2.0

42

.13

2.4

40

.87

0.7

80

.09

0.4

3

Dif

fere

nce

−0.8

3−0

.36

−0.4

3−0

.22

−0.3

6−0

.32

−0.6

0−0

.73

−0.7

5−0

.74

−1.0

5−0

.69

−0.7

40

.04

0.1

2

BE

/ME

Posi

tive

0.0

30

.61

0.8

20

.87

0.9

61

.09

1.1

71

.18

1.2

91

.27

1.2

40

.31

0.9

3

Nega

tive

1.4

11

.43

1.4

61

.54

1.6

11

.69

1.8

71

.94

2.1

82

.45

1.0

40

.84

0.2

0

Dif

fere

nce