investor presentation - vakıfbank · the other shareholders consist of individual or legal...

TRANSCRIPT

1

Investor PresentationBRSA figures as of September 30, 2005

January 2006

2

Following successful IPO in November 2005, c. 25% of Vakifbank of is now listed

Main Shareholders General Directorate of Foundations The GDF manages foundations owning 58.45% of the shares in the Bank (43.0% in the form of Class A shares and 15.45% in the form of Class B shares). The GDF was established in 1924 to administer and regulate existing and future Turkish charitable foundations as a state entity directly reporting to the Prime Minister. Non-Affiliated Foundations The non-affiliated foundations are independent foundations with separate boards of trustees. They currently hold Class B shares, constituting 0.19% of the Bank’s equity. Vakifbank Pension Fund The Vakifbank Pension Fund has a 16.10% stake in the Bank’s capital as a Class C shareholder. The Bank’s employees contribute to the Vakifbank Pension Fund as opposed to the mandatory social security coverage provided by the state Social Insurance Institution. Other Shareholders The other shareholders consist of individual or legal entities that together own 0.08% of the Bank’s equity as Class C Shareholders. Free Float Public domestic and international shareholders.

Ownership structure

General Directorate

of Foundations58,45%

VakifBankEmployee

Pension fund16,10%

Other0,27%

Free float25,18%

3

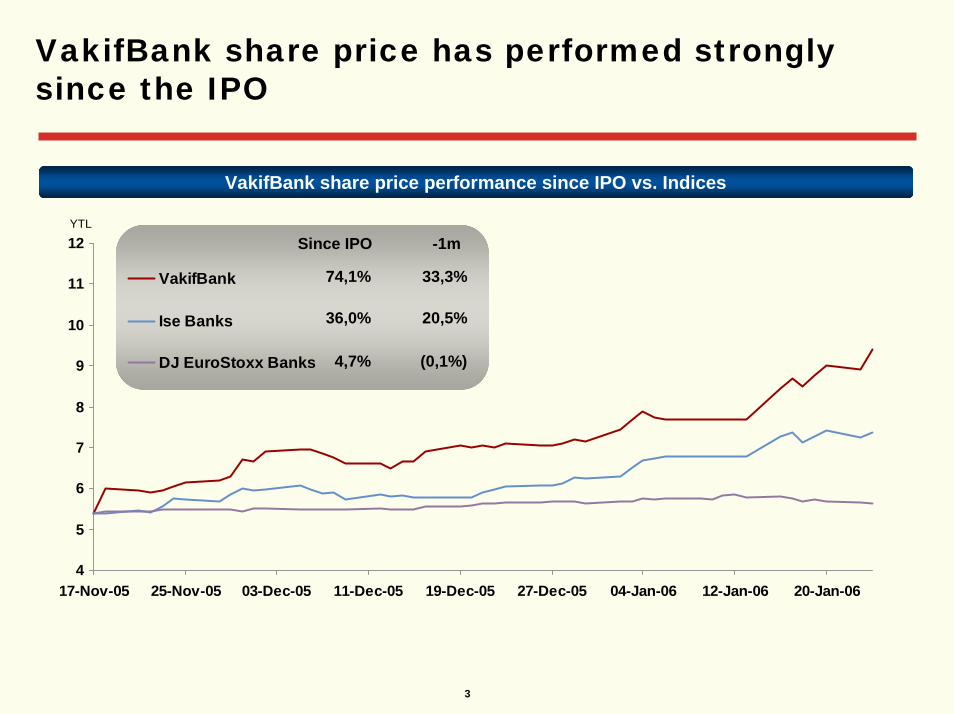

VakifBank share price has performed strongly since the IPO

VakifBank share price performance since IPO vs. Indices

4

5

6

7

8

9

10

11

12

17-Nov-05 25-Nov-05 03-Dec-05 11-Dec-05 19-Dec-05 27-Dec-05 04-Jan-06 12-Jan-06 20-Jan-06

VakifBank

Ise Banks

DJ EuroStoxx Banks

YTL

74,1%

Since IPO -1m

33,3%

36,0% 20,5%

4,7% (0,1%)

4

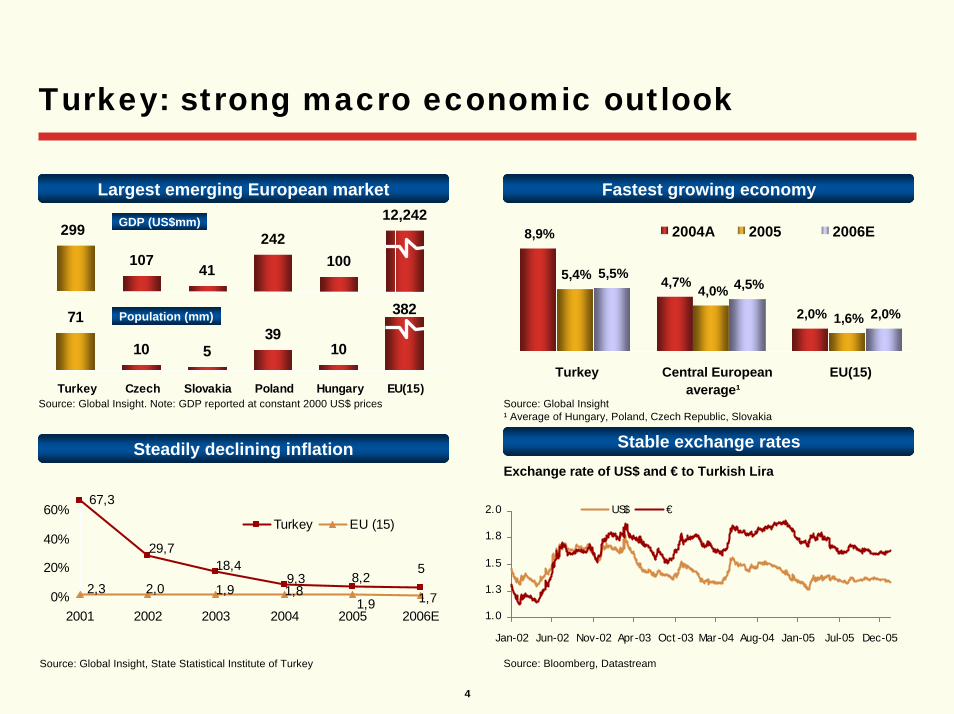

Turkey: strong macro economic outlook

Largest emerging European market Fastest growing economy

71

10 539

10

382

Turkey Czech Slovakia Poland Hungary EU(15)

10741

242100

29912,242

8,9%

4,7%

2,0%4,0%

5,5%4,5%

2,0%

5,4%

1,6%

Turkey Central Europeanaverage¹

EU(15)

2004A 2005 2006E

Steadily declining inflation

Source: Global Insight. Note: GDP reported at constant 2000 US$ prices

Source: Global Insight, State Statistical Institute of Turkey

GDP (US$mm)

Population (mm)

67,3

8,25

9,318,4

29,7

2,3 2,0 1,9 1,81,9 1,70%

20%

40%

60%

2001 2002 2003 2004 2005 2006E

Turkey EU (15)

Source: Global Insight¹ Average of Hungary, Poland, Czech Republic, Slovakia

Stable exchange rates

Source: Bloomberg, Datastream

Exchange rate of US$ and € to Turkish Lira

1.0

1.3

1.5

1.8

2.0

Jan-02 Jun-02 Nov-02 Apr-03 Oct-03 Mar-04 Aug-04 Jan-05 Jul-05 Dec-05

US$ €

5

Banking sector: rapid and profitable growth

Strong recovery following 2001 Low penetration ratios (2004)

• Strong lending and deposit growth• Good regulatory environment and reporting

standards• Good asset quality• Still high interest margins, though declining trend• Strong capitalization• High foreign strategic investor interest

48%

111%

60%42%

56%42%34%

88%

36%

16%

37%50%

TurkeyCzech RepSloveniaHungaryPolandEurozone

Deposits/GDP Loans/GDP

Source: Central Bank of Turkey; Central Banks of respective countries

Untapped mortgage market Improved loan quality

35%

17%6% 5% 2% 2,5%

EU

Hun

gary

Cro

atia

Pol

and

Cze

chR

epub

lic

Turk

ey

Mortgage loans/GDP

5.480 4.997

9.599

4.756 6.193 6.361

5,1%5,8%11,1% 5,3%

27,2%16,5%

2001 2002 2003 2004 1H05 3Q05

NPLs (US$mm) NPLs/loans

5,1%

Source: Central Banks Source: Turkish Banks Association reports under BRSA standards

6

VakıfBank at a glance

7.8% market share in assets with over 5.8mm customers and 10mm debit cards302 branches and 114 satellite branches nationwideStrong alternative distribution channels (1,812 ATMs)Strong balance sheet growth and profitability

Strong balance sheet growth (YTLbn) Impressive profitability (YTLmm)

1.444,4

975,6

Operating income(before provisioning)20,4

10,0

8,1

5,4

17,6

14,5

2003 2004 3Q05

Loans Deposits

1.188,1

3Q03 3Q04 3Q05

(YTLmm) 2003 2004 3Q05

Total assets 19.487 24.199 28.580Shareholders’ equity 1.335 2.012 2.528CAR 14,9% 17,3% 18,5%

1

1

Source: Annual and Interim reports, BRSA- Bank-only financials

2003 3Q04 3Q05Cost/income 52,4% 45,7% 36,5%RoAE 19,8% 27,6% 21,7%

Source: Annual and Interim reports, BRSA bank only financials1 2003 numbers restated to 2004 according to inflation accounting

7

Superior growth and profitability prospects

5th largest bank in the fast growing Turkish market

Strengths in fastest growing segments and well developed distribution network• Leading consumer and SME products• Extensive nationwide branch network and well developed alternative channels

Excellent client relationships and cross-selling potential to large customer base• 5.6mm retail customers, of which 1.9mm payroll customers • Leading long-lasting SME franchise with over 105,000 customers • Unique access and understanding of State related companies • Significant recent investment is unlocking important cross-selling potential

Superior financial performance• Solid balance sheet with diversified sources of funding

• Cost conscious culture with focus on profitability instead of market share

8

Balance sheet is supported by a strong TL deposit base

Deposits/liabilities and equity

Total TL deposits¹(YTLmm) (3Q05)

Total FX deposits¹(YTLmm) (3Q05)

Excellent deposit franchise to fund a significant portion of its liabilitiesStrong TL deposit franchise – Third largest among Turkish private banks in terms of TL deposits• Particular strength has been establishment of relationships with companies and public sector

entities in order to obtain employees’ salary accounts, contributing toward maintenance of a stable source of deposit funding

Relatively lower FX deposit base

6,366

14,769 14,145

7,635

9,701

Vakif IS AK YKB GAR

71.5

%

58.9

%

63.2

%

67.4

%

62.1

%

63.1

%

72.7

%

67.0

%

57.1

%

58.0

%

Vakif IS AK YKB GAR20043Q05

14,060

17,98416,615

7,903

10,382

Vakif IS AK YKB GAR

Source: BRSA Bank Only financials¹ Time and demand split based on BRSA financials, Deposit figures exclude Interbank deposits

9

VakıfBank is a market leader, particularly in retail and SME finance…

Total market share (%) (3Q05)

8.8%

29.0% *

13.8%

4.8%

12.4%

4.9%

22%

TotalDeposits

TL deposits ATMs Debit Card #Public Salary

accounts

Mutual funds Branches

7.4%6.8%

16.4%

HousingLoans4

CommercialInstalment

Loans

Creditcards

7.3%10.4%

Retailloans³

Total loans

Deposits / Funding Credits Distribution

Source: Turkish Banks Association reports under bank-only BRSA standards as of September 30, 2005, Capital Markets Board* VakıfBank estimates, MIS

² Total banking system loans = Short term + Medium and Long Term + Loans under Follow up - Specific Provisions³ Includes home, auto and other. Credit card loans, overdrafts, and State Mass Housing Authority (TOKI) loans not included4 Including TOKI housing loans

10

... moving today to a strong position among top Turkish banks

14,3%

13,7%

10,8%

9,1%

7,3%

7,3%

5,0%

4,1%

3,5%

2,6%

Akbank

Isbank

Garanti

Ziraat

Yapi Kredi

VakifBank

Finansbank

Kocbank

Halkbank

Fortis Bank

Ranking by total loans Ranking by total deposits Ranking by branches

20,3%

13,3%

14,2%

8,8%

8,5%

8,7%

6,7%

3,4%

2,5%

1,6%

Ziraat

Akbank

Isbank

VakifBank

Halkbank

Garanti

Yapi Kredi

Kocbank

Finansbank

Fortis Bank

18,6%

14,1%

10,6%

9,6%

6,6%

6,8%

4,9%

3,1%

2,8%

2,8%

Ziraat

Isbank

Akbank

Halkbank

Yapi Kredi

Garanti

VakifBank

Finansbank

Fortis Bank

Kocbank

Total banking system: USD 271 bn

Total banking system: USD 172 bn

Total banking system: 6,053 branches

State owned banksSource: Turkish Banks AssociationAs at 3Q05

11

VakıfBank’s vision: on the path to becoming a top three private bank

Targetprofitable

growth

Focus onretail and

SMEs

Becomeprimary

bank for itscustomers

Becomeone of

Turkey’s top 3 private banks

Where is the potential? Evidence of future potential

Leverage key strengths

Very large existing SME & retail customer base that is still untapped

Improving cross-selling, which is significantly below that of peer banks• limited sales effort in the past• low historic advertising spend

Grow network in under-penetrated regions

Consistent market share growth since 1999 demonstrates embedded strengths

Tapping key segments with targeted marketing programs

Management focus on sales effort

Ongoing company wide restructuring is well advanced and pilot projects show impressive results

Strong positioning and competitive advantage in Ankara and Anatolian Turkey

12

A leading retail franchise

Key retail strengths c.50% CAGR in retail lending

A leading YTL franchise in the market

Over 5.6mm customers, of which 1.9mm highly valuable payroll customers

Leader in consumer lending, excl. credit cards

Well positioned to benefit from the expected significant growth in housing loans

Good retail loan portfolio quality

Major opportunity to increase cross-selling ratio (incl. insurance and leasing products of subsidiaries)

Y T Lm n 2003 2004 3Q 05

C A G R 2003–3Q 05

H ous ing ¹ 287 439 803 80 .0%

C red it cards 391 598 706 40 .2%

A u to 166 388 257 28 .4%

O ther 921 1 .243 1 .571 N /M

T ota l re ta il 1 .765 2 .668 3 .337 43 .9%

Source: BRSA bank only financials, VakıfBank, inflation adjusted¹ House loans include TOKI-funded loans

High lending yields (%) Continued strength in YTL deposit market share

Credit cards OverdraftIns talm ent (Retail+Corporate) Interbank avg bid rate

Source: BRSA bank only financials, VakıfBank

58,8

36,1

38,6 36,8

48,6

61,4

41,7 45,6

72,6

27,629,441,7

49,7

21,815,6

49,6

2002 2003 2004 1H05

11.7%12.3%

9.8%8.8%

9.9%

9.7%

2003 2004 3Q05

Demand (YTL) Term (YTL)

Source: BRSA bank only financials

13

Strong corporate and SME lending culture

Attractive client and product mix Number of SME clientsSuperb focus on SMEs• # of SME clients increased from 40,000 (2002) to

105,000 (3Q05)• Successful introduction of relationship managers • Diversified portfolio of products• Unique relationships with financing organisations

(World Bank, EIB, CEDB, KOSGEB and others)Traditionally strong with large corporatesAccelerate development of project finance activities Source: VakıfBank

99,000105,000

52,000

2003 2004 3Q05

Corporate lending growthCorporate loans average yields

44.2

24.720.7 20.3

7.88.49.39.6

6.96.77.59.6

2002 2003 2004 H1 2005

TL FX-indexed FX

(YTLmm) 2003 2004 3Q05

CAGR 2003 – 3Q05

Short term (<1 year) 1.868 2.265 2.504 18.2%

Long term (>1 year) 865 1.238 1.675 45.9%

Instalment 712 1.730 2.204 90.7%

Other 157 161 281 39.5%

Total 3602 5.394 6.664 42.1%

Source: BRSA bank only, VakıfBank, Note: Instalment loans best proxy for SME lending

Source: BRSA bank only financials, VakıfBank

14

Well-developed distribution network with unique reach

No. of branches (top 10 banks by assets) Branch network strategy

Well distributed nationwide branch networkRegional strengths in Ankara, Anatolia and Eastern Turkey—up to 40% market share in some regionsPlans for further expansion in Istanbul and Marmara on a selective basisCurrent restructuring to increase sales focus

302

1.146

869

654

418

592

405

416

172194

219

Ziraat

IsBan

k

HalkBan

k

AkBan

k

YKB

Garanti

VakifB

ank

Denizb

ank

Finansb

ank

KocBan

k

114

Alternative channels

Second largest ATM networkInternet banking since 2000— # of customers increased from 500,000 in 2003 to over 731.000 in September 2005Mobile Phone bankingCall centre with 100 staffMobile banking

Branches Satellite branches

Source: Turkish Banks Association, BRSA bank only , 3Q05

15

11,7%14,2% 11,8%

40,3%35,5%

35,7%

35,0%33,3%27,5%

8,2%5,5%

3,5%

5,7% 4,6% 5,8%

2003 2004 3Q05Loans Interbank¹ Securities Fixed Assets Other²

19,5 24,2 28,6

Loans/deposits increased from 37,1% in 2003 to 49,0% in 3Q05

Relatively low and declining share of non-interesting earning assets with increasing share of lending

Below peers ratio of fixed assets to total assets

Continued effort to rationalise fixed assets and equity participations portfolio

Continued enhancement of asset mix

Increasing share of earning assets Breakdown of assets (YTLbn)

Source: BRSA bank only¹ Interbank includes also balance with Central Bank and reverse repos² Other assets include: Liquid assets, Trade receivable and Sundry

Debtors, Equity Participation and Other

Fixed assets/Total assets, 3Q05

3,9%

1,3%

3,5%4,4%

5,8%

Vakifbank Akbank IS Garanti YKB

Source: Turkish Banks Association, BRSA bank only , 3Q05

Average: 3,8%

16

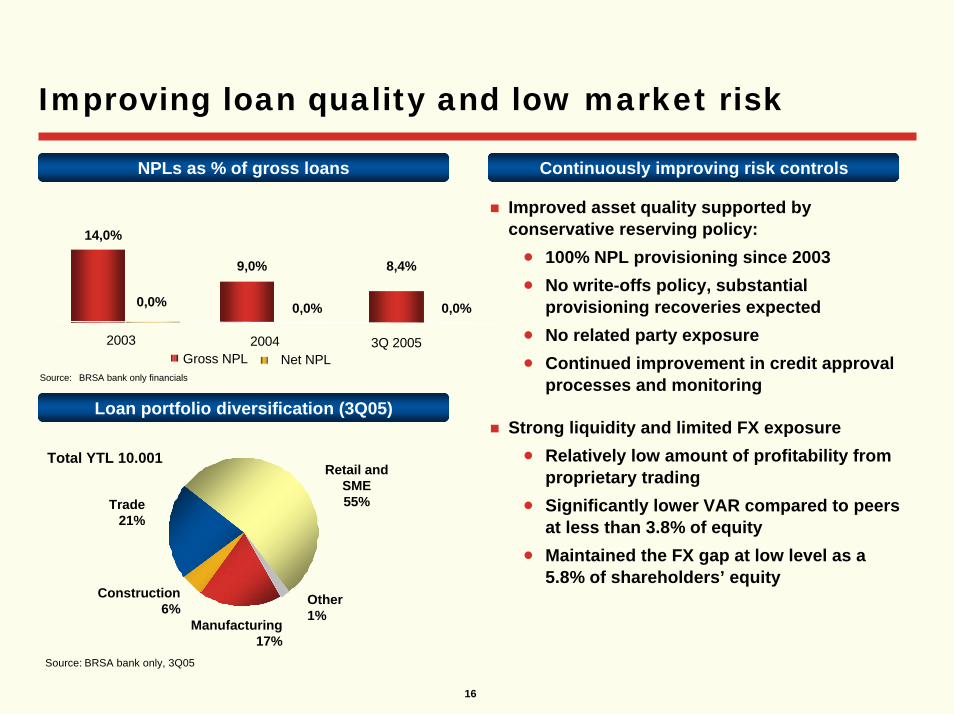

Improving loan quality and low market risk

NPLs as % of gross loans Continuously improving risk controls

14,0%

9,0% 8,4%

0,0% 0,0% 0,0%

2003 2004 3Q 2005Gross NPL Net NPL

Improved asset quality supported by conservative reserving policy:• 100% NPL provisioning since 2003• No write-offs policy, substantial

provisioning recoveries expected• No related party exposure• Continued improvement in credit approval

processes and monitoring

Strong liquidity and limited FX exposure• Relatively low amount of profitability from

proprietary trading• Significantly lower VAR compared to peers

at less than 3.8% of equity• Maintained the FX gap at low level as a

5.8% of shareholders’ equity

Source: BRSA bank only financials

Manufacturing17%

Construction6%

Trade21%

Retail and SME55%

Other1%

Total YTL 10.001

Loan portfolio diversification (3Q05)

Source: BRSA bank only, 3Q05

17

Diversifying & strengthening core revenue generation

Improving profitability (YTLmm)

Future margin pressure to be partially offset by increased share of loans in total assets

Potential to further expand fee & commission income as part of cross-selling initiatives

Aim to maintain strong cost control culture

Strong revenue generation and cost control

319.9

527.8

1444.4

1002.3

539.8543.3

1188.1

864.8

3Q04 3Q05

+15.9

+21.6%

(2.8)%

+68.7

Net Interest Income

Total Banking Income

Operating expense

Net operating income²

Source: BRSA bank only financials

18

40.653.0 36.5

4.0

2.53.0

2003 2004 3Q05

Cost/income

Cost/assets

Stringent cost control and conservative provisioning

Cost control measures (%) Loan loss provisions/NPLs (%)

Comments

Vakifbank maintained strict cost controls keeping C/I ratio at below 40%

• Future cost increases planned mainly in marketing

Provisioning expense were affected by conservative provisioning ahead of IPO -YTL192mm of general reserves in Q105

Source: BRSA bank only financials¹ Annualised

Source: BRSA bank only financials

100.0%100.0% 100.0%

2003 2004 3Q05

Loan loss provisions/NPLs (%)

5.1%9.0%

5.6%¹

2003 2004 3Q05

19

Consistently delivering impressive results

Strong profitability driven by enhanced balance sheet structure Continued improvement in asset quality and more prudent (100%) reserving policyImproved cost efficiencies following rationalization of branch network

Operating income and Net income evolution—YTLmm RoAE (%)

3 year average: 26.3%

264

624

307370

706

1,279

522

813

2003 2004 3Q05 3Q05

Net Income

OperatingIncome¹

21.7%

37.3%

19.8%

2003 2004 3Q05

+55.8% Y-o-Y

Source: BRSA bank only financials¹ Excluding provisions and other operating income (recoveries are significant portion of other operating income)

20

Strong foundations for profitable growth

EXISTING STRENGTHS FUTURE GROWTH DRIVERS

Retail and SME products and platform Healthy macro environment

5.6mm retail customers Sector growth potential, especially retail and SMEs

Extensive nationwide network High cross selling potential

Very high cost efficiency Further non-interest income improvement

Highest profitability in sector Lower loan loss provisioning

STRONG LONG TERM GROWTH AND PROFITABILITY

21

Appendices

22

Balance sheet details: assets

Key financials

CAGR2003-3Q0520042003(YTLmm) 3Q05

Liquid Assets 163 180 256 29%Balances With The Central Bank 301 555 929 90%Balances With Banks 1.965 2.233 2.235 8%Interbank Funds Sold 313 1.100 1.150 -96%Trading Securities Portfolio 5.517 2.678 1.090 -60%Available for Sale Portfolio 1.339 5.365 8.526 188%Reserve Deposits at the Central Bank 814 935 1.140 -98%Loans 5.367 8.062 10.001 43%Sundry Debtors 80 63 132 33%Equity Participations 548 184 549 0%Held to Maturity Securities 581 1.002 552 -3%Premises & Equipment 1.119 1.127 1.029 -5%Other Assets 51 204 183 108%Total Assets 19.487 24.199 28.580 24%

Source: BRSA –Bank Only Financials

23

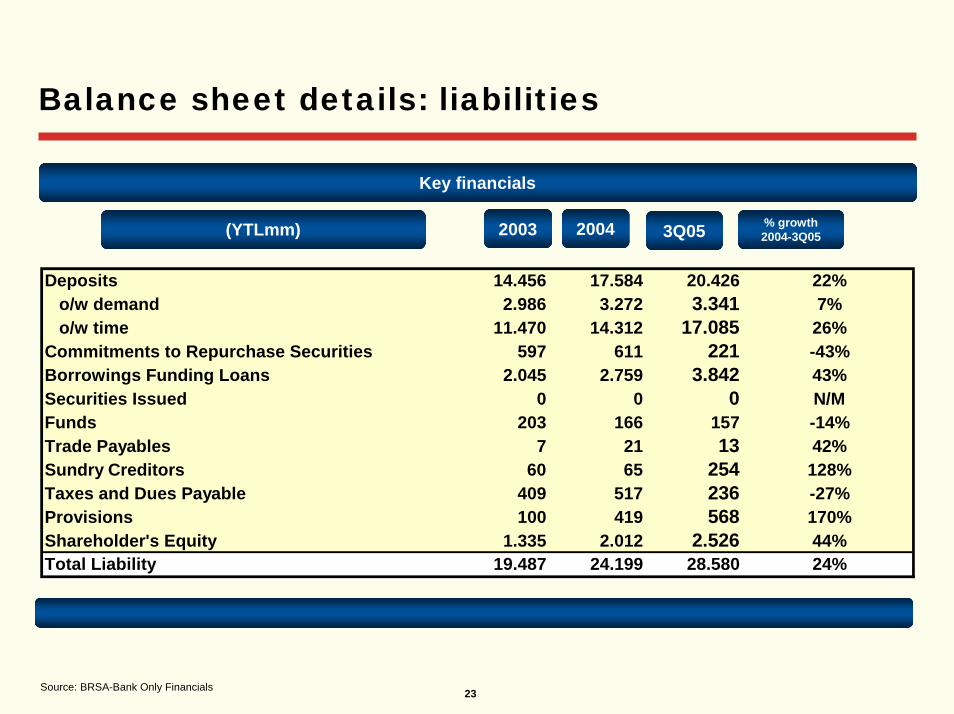

Balance sheet details: liabilities

Key financials

20042003(YTLmm) 3Q05 % growth 2004-3Q05

Deposits 14.456 17.584 20.426 22% o/w demand 2.986 3.272 3.341 7% o/w time 11.470 14.312 17.085 26%Commitments to Repurchase Securities 597 611 221 -43%Borrowings Funding Loans 2.045 2.759 3.842 43%Securities Issued 0 0 0 N/MFunds 203 166 157 -14%Trade Payables 7 21 13 42%Sundry Creditors 60 65 254 128%Taxes and Dues Payable 409 517 236 -27%Provisions 100 419 568 170%Shareholder's Equity 1.335 2.012 2.526 44%Total Liability 19.487 24.199 28.580 24%

Source: BRSA-Bank Only Financials

24

Income statement

(YTLmm) 3Q053Q03 3Q04 % growth 3Q03-3Q05

Interest Income 1.889 2.217 2.645 19%Interest Expense -1.674 -1.353 -1.643 21%Net Interest Income 830 865 1.002 19%Operating Income 1.141 1.188 1.444 -42%Net Banking Income 254 320 540 69%Income /(Loss) from Associates 16 14 4 -71%Monetary Gain/(Loss) 11 -8 0 NMIncome Before Taxes 280 326 544 67%Provisions for Taxes on Income 0 -19 -174 NMNet Income 280 307 370 21%

Source: BRSA Bank Only Financials

25

THANK YOU