investor presentation may 29, 2018 dpm an innovative ... · investor presentation may 29, 2018...

TRANSCRIPT

Investor Presentation

May 29, 2018

Krumovgrad Gold Project

April 2018

DPM – AN INNOVATIVE, GROWING GOLD PRODUCER

TSX:DPM

2

Forward Looking Statements

Certain statements and other information included in this presentation and our other disclosure documents constitute “forward looking information” or “forward

looking statements” within the meaning of applicable securities legislation, which we refer to collectively hereinafter as “Forward Looking Statements”.

Statements that constitute Forward Looking Statements include, but are not limited to, certain statements with respect to the estimated capital costs, operating

costs, key project operating costs and financial metrics and other project economics with respect to Krumovgrad; the timing of development, permitting,

construction, commissioning activities and commencement of production in respect of Krumovgrad; timing of further optimization work at Tsumeb and potential

benefits of rotary furnace installation; price of gold, copper, silver and acid; toll rates; metals exposure and stockpile interest deductions; the estimation of Mineral

Reserves and Mineral Resources and the realization of such mineral estimates; the timing and amount of estimated future production and output, life of mine,

costs of production, cash costs and other cost measures, capital expenditures, rates of return at Krumovgrad and other deposits and timing of the development

of new deposits; results of economic studies; success of exploration activities; success of permitting activities; permitting time lines; currency fluctuations;

requirements for additional capital; government regulation of mining and smelting operations; success of permitting activities; environmental risks; reclamation

expenses; potential or anticipated outcome of title disputes or claims; and timing and possible outcome of pending litigation. Forward Looking Statements are

statements that are not historical facts and are generally, but not always, identified by the use of forward looking terminology such as “plans”, “expects”, or “does

not expect”, “is expected”, “budget”, scheduled”, “estimates”, “forecasts”, “outlook”, “intends”, “anticipates”, or “does not anticipate”, or “believes”, or variations of

such words and phrases or that state that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved.

Forward looking statements are based on certain key assumptions and on the opinions and estimates of management and Qualified Persons (in the case of

technical and scientific information) as of the date such statements are made and they involve known and unknown risks, uncertainties and other factors which

may cause the actual results, performance or achievements of the Company to be materially different from any other future results, performance or

achievements expressed or implied by the Forward Looking Statements. In addition to factors already discussed in this presentation, such factors include,

among others: the uncertainties with respect to actual results of current exploration activities, actual results of current reclamation activities, conclusions of

economic evaluations and economic studies; changes in project parameters as plans continue to be refined; possible variations in ore grade or recovery rates;

failure of plant, equipment or processes to operate as anticipated; accidents, labour disputes and other risks of the mining industry; delays in obtaining

governmental approvals or financing or in the completion of development or construction activities; uncertainties and risks inherent to developing and

commissioning new mines into production, such as the Krumovgrad project, which may be subject to unforeseen delays, costs or other issues; uncertainties

inherent with conducting business in foreign jurisdictions where corruption, civil unrest, political instability and uncertainties with the rule of law may impact the

Company’s activities; social and non-governmental organizations (“NGO”) opposition to mining projects and smelting operations; fluctuations in metal and acid

prices, toll rates and foreign exchange rates; unanticipated title disputes; claims or litigation; limitation on insurance coverage; cyber attacks; failure to realize

projected financial results from MineRP; risks related to operating a technology business reliant on the ownership, protection and ongoing development of key

intellectual properties; as well as those risk factors discussed or referred to in any other documents (including without limitation the Company’s most recent AIF)

filed from time to time with the securities regulatory authorities in all provinces and territories of Canada and available on SEDAR at www.sedar.com. Although

the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in Forward

Looking Statements, there may be other factors that cause actions, events or results not to be anticipated, estimated or intended. There can be no assurance

that Forward Looking Statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements.

Unless required by securities laws, the Company undertakes no obligation to update forward looking statements if circumstances or management’s estimates or

opinion should change. Accordingly, readers are cautioned not to place undue reliance on forward looking statements.

TSX:DPM

3

Investment Highlights

Operating in mining friendly jurisdictions

Strong resource and reserve base

High quality, low cost, flagship asset

Near term, low cost growth in gold production

Growing exploration pipeline

Strong balance sheet

Strong management team

Attractive valuation

Strong Asset Base, Near Term Growth & Attractive Valuation

TSX:DPM

4

Metal Prices and DPM Share Price

Gold and Copper Price Trend

2010 to Present

$1.80

$2.10

$2.40

$2.70

$3.00

$3.30

$3.60

$3.90

$4.20

$4.50

$4.80

$1,000

$1,100

$1,200

$1,300

$1,400

$1,500

$1,600

$1,700

$1,800

$1,900

$2,000

Apr-10 Apr-11 Apr-12 Apr-13 Apr-14 Apr-15 Apr-16 Apr-17 Apr-18

Gold Price Trend(US$/oz)Copper Price Trend(US$/lb)

Historical Relative Trading

January 2017 – April 2018

(20%)

0%

20%

40%

60%

Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18

C$DPM US$GDX US$GDXJ

26%

4%

(1%)

DPM has outperformed benchmarks but still trades at discounted valuation multiples

TSX:DPM

5

Company Overview

Share Price / 52 week low-high (C$ per share) $3.37 / $2.13 - $3.60

Shares Outstanding – Current 178,492,566

Market Capitalization – Current $464 M

P/NAV (23) 0.51x (consensus)

Metals contained in concentrate produced

Gold

Copper

197,684 oz

35.8 Mlbs

AISC/oz Au (1,2) $729

Adjusted EBITDA $92 M

+ Krumovgrad starting in Q4 2018 + 85,700 oz/yr

Cash $15 M

Investment portfolio (21) $36.8 M

Undrawn RCF $242 M

Debt $33 M

2017 Quick Glance Production & Financial Metrics

Dundee Corporation 20.38%

GMT Capital Corporation 12.47%

EBRD 9.9%

USAA Asset Mgmt. 3.18%

Kopernik Global Advisors 2.91%

Low cost

production

with 50%

growth starting

in Q4 2018

Strong

liquidity

position

Long term

shareholders

Attractive

Valuation

1, 2, 21 See footnotes contained in Appendix on slide 48

Share Capital (@ May 25, 2018)

Liquidity Position (@ March 31, 2018)

Top Five Shareholders (@ May 25, 2018)

TSX:DPM

6

Timok Gold Project

Serbia

Tsumeb Smelter

Namibia

Chelopech Mine

Bulgaria

Sabina Gold & Silver Corp.

Nunavut, Canada

Krumovgrad Gold Project

Bulgaria

DPM’s Global Portfolio of Assets

Operating assets

Development asset

Late stage exploration assets

Early stage exploration assets

Malartic JV

Quebec, Canada

Chelopech

• Location: Chelopech, Bulgaria

• Ownership: 100%

• 2017 Production: 197,684 oz Au;

35.8 Mlbs Cu

• Mine Life: 8.5 years

• Operation: Underground

Krumovgrad

• Location: Southern Bulgaria

• Ownership: 100%

• Stage: Construction

• Production: 103,000 oz (yrs 1-5 avg)

• Mine life: 8 years

• Operation: Open pit

• Commissioning: Q4 2018

Tsumeb

• Location: Tsumeb, Namibia

• Ownership: 100%

• 2017 Concentrate Smelted: 219,000 tonnes

• Operation: Specialty smelter

• Location: Serbia

• Ownership: 100%

• Stage: Advanced exploration

• Resource: 1.72 Moz

Timok Sabina Gold & Silver

• Location: Nunavut, Canada

• Ownership: 10%

• Stage: Pre-construction

• Production: 240,000 Au (yrs 1-8) (18)

• Operation: Open pit/underground

• DPM’s equity stake: $36.8 M

Corporate Head Office

Toronto, Canada

18 See footnotes contained in Appendix on slide 48

TSX:DPM

7

Bulgaria… • Overview:

• Uninterrupted operations since 2003

• Member of the EU since 2007

• 4th largest gold producer in Europe

• Stable regulatory environment & government

• Corporate Tax Rate: 10%

• Chelopech Royalty Rate: 1.5% of gross Cu, Au and Ag

• Krumovgrad Royalty Rate: 1% - 4% of gross value

• GDP Forecast: +2.8% in 2017 (IMF)

• Mining industry forms 5% of the GDP (2016)

Namibia…• Overview:

• Political party stability

• 5th largest producer of uranium and 9th largest producer of

diamonds

• Ranked in top 10 as Africa’s most attractive countries over last

5 years according to the Fraser Institute

• Glencore, Rio Tinto, Anglo American, Paladin Energy, etc.

• Corporate Tax Rate: 0% (Export Processing Zone status)

• GDP Forecast: +5.3% in 2017 (IMF)

• Mining industry forms 11.5% of the GDP (Jan. 2017)

Serbia…• Overview:

• EU candidate since 2012

• 3rd largest copper producer in Europe

• Industry benefits from high level government support

• Corporate Tax Rate: 15%

• GDP Forecast: +3.0% in 2017 (IMF)

• Mining industry forms 2% of the GDP (2013)

Operating in Mining Friendly Jurisdictions

TSX:DPM

8

Strong Mineral Resource and Reserve Base

1.9 Moz

0.8 Moz

Proven and probable

Total Gold Ounces

Proven and Probable

Total Copper

1.4 Moz 0.01 Moz

1.7 Moz

3.8 Moz

Measured & Indicated Inferred

Total Gold Ounces

2.7 Moz

376 Mlbs

Measured & Indicated Inferred

Total Copper

2.8 Bnlbs

311 Mlbs

Krumovgrad

ChelopechChelopech

TimokKrumovgrad

Chelopech

Chelopech

3.1 Moz

0.12 Moz

Chelopech

Tulare

Tulare

2.8 Bnlbs

29 Mlbs

3.9 Moz

3, 4, 5, A, B. See footnotes contained in Appendix on slides 48 & 49

TOTAL MINERAL RESERVES (3,5,A)

TOTAL MINERAL RESOURCES (4,5,A)

Exclusive of Reserves

As of December 31, 2017 As of December 31, 2017

TSX:DPM8

HIGH QUALITY, LOW COST, FLAGSHIP ASSET

Chelopech

Location: Chelopech, Bulgaria

Ownership: 100%

2017 Production: 197,684 oz Au; 35.8 Mlbs Cu

Mine Life: 8.5 years

Operation: Underground

TSX:DPM

10

57

133

196

153

118

9987

108

0

300

600

900

1200

1500

1800

0

50

100

150

200

250

2010 2011 2012 2013 2014 2015 2016 2017

Cash Cost / tonne of ore processed (US$/t) (6) Ore Mined (Mt)

1.09

1.31

1.812.03 2.05 2.04

2.21 2.22

2010 2011 2012 2013 2014 2015 2016 2017 Q12018

2018E

56 55

4640 40

3733 34

37

2010 2011 2012 2013 2014 2015 2016 2017 Q12018

2018E

Adjusted EBITDA (US$M) (7)

2006 2015 2016 2017

21.5 21.5

14.1 Total ore

mined

since 2006 (Mt)

Ore Reserve (Mt)

16.3

19.8

Gold price trend

Growing throughput in recent years with

opportunity to optimize further

Continuing to optimize through innovation

2018E slightly higher due to FX

Stronger EBITDA due to grades & metal prices Exploration successful in replacing reserves

6, 7, 9 See footnotes contained in Appendix on slide 48

Copper price trend (AuEq)

Chelopech – Continually Improving

2.1-2.2

37-40

9 9

18.818.5

0.558

TSX:DPM

11

139

172 140-170

2016 2017 Q1 2018 2018E

Chelopech Highlights

Payable gold in concentrate sold (000s oz) (8)Metals contained in concentrate produced (8)

166

198 165-195

38.5 35.8

33.7-40.4

2016 2017 Q1 2018 2018E

Gold (000s oz) Copper (Mlbs)

Record gold production in 2017

Guidance for another strong year in 2018

Focused on mine and process plant optimization

8, 9 See footnotes contained in Appendix on slide 48

All in sustaining cost (US$/oz gold sold)

9

9 9

57.3

9.3

35.2

747 729

2016 2017 Q1 2018 2018E

640-855

696

TSX:DPM

12

Chelopech – Next Phase of Optimization Underway

Change in mining method

0.5 mtpy 1.0 mtpy

Underground crushing and conveying;

“Taking the lid off the mine”

1.0 mtpy 2.0 mtpy

Digital transformation

Phase 1

2003-2008

Phase 2

2009-2014

Phase 3

2015+

- Dynamic mine planning

- Intelligent use of data

- Digital collaboration

- Smart centre

- Automating mining process

2018

2020

2019

Key benefits:

Recovery improvement in 2017

Deep understanding of Reserve base

Optimization of material & asset flow

Improved anticipation of failures

Increase automation

Real time monitoring of performance vs. plan

TSX:DPM

13

Chelopech – Near Mine Exploration

Drilling demonstrates excellent potential for hosting additional resources:

New zone of breccia pipes

Found over 1500 m & is open to the east

Large areas remain between drilled sections

Similar geology to Central and Western orebodies

Opens up whole new area

10,000 m infill drill program proposed for at SEBP zone initiated in January. Results from the first drill

hole in Q1 include: • 25 m averaging 4.53 g/t AuEq from start of the hole followed by 132 m averaging 0.49 g/t AuEq

5,000 m of drilling planned for Krasta target

TSX:DPM13

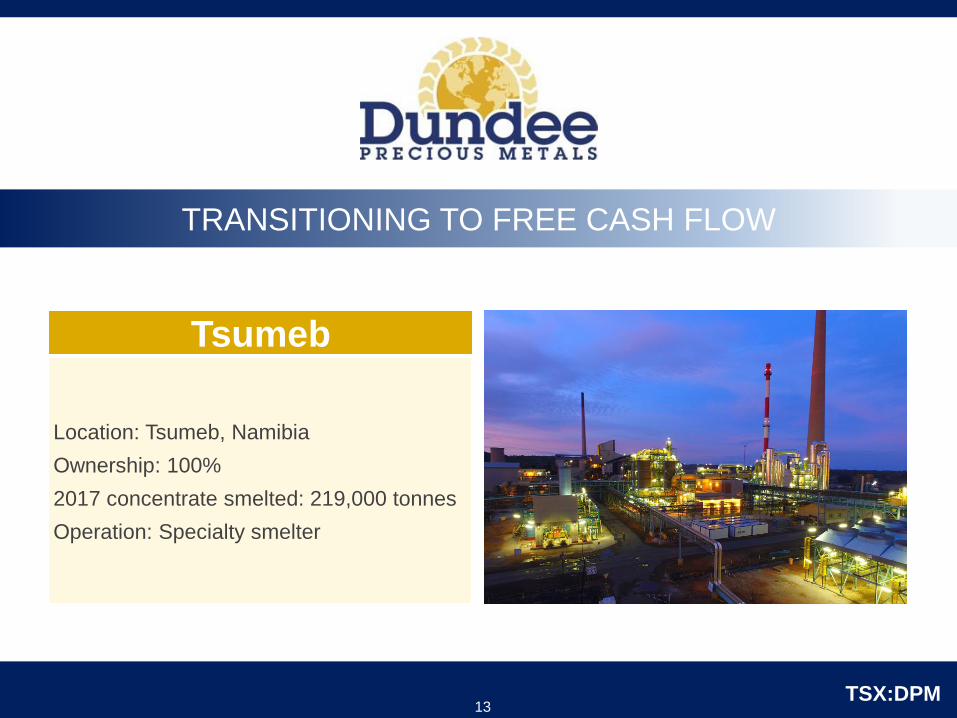

TRANSITIONING TO FREE CASH FLOW

Tsumeb

Location: Tsumeb, Namibia

Ownership: 100%

2017 concentrate smelted: 219,000 tonnes

Operation: Specialty smelter

TSX:DPM

15

2012 2013 2014 2015 2016 2017 2018E 2019F 2020F 2021F 2022F

(2)

Tsumeb – Increased Stability with Growth Potential

Total Capital Expenditures (US$M)

63

140

130

44

19

8.6

2012 2013 2014 2015 2016 2017 2018E

219

240-

265

196198

152159

265-

300

200

300-

370

Production (‘000s tonnes)Cash cost/t of

con smelted

(net of by

product credits)

Third Party

con supplied

to smelter

(000s)

Chelopech

concentrate

supplied to

smelter (000s)

Potential future

capacity

$440-$500

240-

265

Growth Capital

Sustaining Capital

Secured processing outlet for Chelopech

Growing cash flow generating custom toll business

Focused on stable operations at current throughput

Option to expand to 370k tpa in the future

Will evaluate strategic partnership alternatives

6, 9 See footnotes contained in Appendix on slide 48

99 99

(6)

Major investment phase complete Major investment phase complete

220-

250

12-18

99

TSX:DPM

16

200219

2016 2017 Q1 2018 2018E

Tsumeb Smelter Highlights

Complex Concentrate Smelted

(‘000s t)

Adjusted EBITDA (US$M) (7) Sustaining Capital (US$M) (6)

Stable performance in 2017

Continued optimization of facility

Focused on improving availability of oxygen plant and unit cost reductions

Generated free cash flow of US$7 million in 2017

6, 7, 9 See footnotes contained in Appendix on slide 48

9

9

54

220 – 250

10

14

2

2016 2017 Q1 2018

11

7

12-18

2016 2017 Q1 2018 2018E

4

NEAR TERM, LOW COST GROWTH

TSX:DPM16

Krumovgrad

Location: Southern Bulgaria

Ownership: 100%

Stage: Construction

Production: 103,000 oz (yrs 1-5 avg)

Mine life: 8 years

Operation: Open pit

Commissioning: Q4 2018April 2018

TSX:DPM

18

Krumovgrad – Robust Economics

Project

Economics

Robust with a

28% After-Tax

IRR *

Production and Operating Costs (10, B)

Annual tons processed 775,000 t

Gold grade 4.04 g/t

Strip ratio 2.6:1 waste:ore (t:t)

Annual gold production 85,700 oz

Year 1 to 5 average 103,020 oz

Annual silver production 38,700 oz

Total cash cost per oz AuEq $403

Average Annual EBITDA (7) $66 million

Year 1 to 5 average $85 million

Construction capital $164 - $168 million

NPV (5%) (@ April 30, 2018) $318 million (adjusted for capital spent)

First concentrate production Q4 2018

LOM 8 years

High grade low strip ratio open pit gold mine

Operating synergies with Chelopech

Fully funded with near term production in Q4 2018

• @ US$1,250/oz Au

• Based on midpoint of updated construction capital

7, 10, B See footnotes contained in Appendix on slides 48 & 49

TSX:DPM

19

Krumovgrad – Project Progress

Milestone Actual/Expected Completion

Construction permit RECEIVED AUGUST 9, 2016

Mobilize earthworks contractor to site and commence earthworks Q4 2016

Commenced main civil/mechanical/electrical construction Q3 2017

Commissioning and start up Q3 2018

First concentrate production Q4 2018

Construction capital spent (@ Apr. 30, 2018) / remainder to be spent in 2018 $101 million / $63-$67 million

Percent complete (@ April 30, 2018) 65%

Vertimills for fine grinding – April 2018Krumovgrad site – April 2018

Project Progress

Krumovgrad Project Facility

TSX:DPM

20

Krumovgrad – Construction Progress

TSX:DPM

21

Krumovgrad – Exploration (22)

Surnak Exploration Target

22 See footnotes contained in Appendix on slides 38 & 39

Previous exploration work at the Surnak Prospect, which includes over

10,800 metres of trenching and drilling, has been used to outline an

exploration target of 80,000 to 160,000 oz Au contained within 1.8 to 2.4 Mt

grading 1.5 to 2 g/t Au. The exploration target potential was derived upon

review of historic Mineral Resource estimates at Surnak, in combination with

ongoing development of the 3D geologic model at Surnak. The potential

ranges of tonnes and grade are conceptual in nature are based on previous

drill results that defined the approximate length, thickness, depth and grade

of the portion of the historic Mineral Resource estimate. There has been

insufficient exploration to define a current Mineral Resource and the company

cautions that there is a risk further exploration will not result in the delineation

of a current Mineral Resource.

KUPEL NORTHDiscovery Hole

KPDD0098m at 12.81 ppm Au &

4.95 ppm Ag

SKALAK

SYNAP

KUKLITSA

KUPEL

SURNAK

SURNAK EXPLORATION TARGET

Exploration target potential of 80,000 to

160,000 oz Au contained within 1.8 to 2.4 Mt

grading 1.5 to 2 g/t Au

ADA TEPEProven and Probable

Reserves Au: 806 Koz at 4.05 g/tAg: 443 Koz at 2.2g/t

Surnak is one of six registered Commercial Discoveries within the mine concession

Located 3 km west of Ada Tepe

Sediment-hosted low sulphidation epithermal gold veins like Ada Tepe

Last explored by DPM in 2004-5

6,000 m diamond drill program planned for 2018. Results from first holes include:• SUDD028: 13m at 1.29 g/t gold from 106m

• SUDD029: 15m at 1.22 g/t gold from 130m

Additional 1,600 m drilling on regional licences

Chelopech Mine, Bulgaria

FUTURE GROWTH PIPELINE

TSX:DPM

ADVANCED EXPLORATION

20

Location: Serbia

Ownership: 100%

Stage: Advanced exploration

Resource: 1.72 million ounces (19)

Timok

19. See footnotes contained in Appendix on slide 48

TSX:DPM

23

Serbia Advanced ExplorationTimok Gold Project

Total Indicated Mineral Resources

1.72 Moz Au @ 1.54 g/t

contained within 34.7 MT

Inferred Mineral Resources

0.02 Moz Au @ 1.4 g/t

contained within 0.4 MT

Indicated Mineral Resource for Bigar Hill (19)

1.16 Moz Au @ 1.57 g/t

contained within 22.97 MT

Indicated Mineral Resource for Korkan (19)

0.33 Moz Au @ 1.55 g/t

Contained within 6.71 MT

Indicated Mineral Resource for Pester (19)

0.23 Moz Au @ 1.40 g/t

contained within 5.06 MT

19. See footnotes contained in Appendix on slide 48

Previously assumed sulphide resource

Potential for oxides within previous resource

Initial bottle roll tests indicate recoveries of:

90-95% for Korkan and Bigar Hill oxides

75% for Korkan West oxides

50-55% for Korkan transitional zone

Potential to improve economics

TSX:DPM

24

Serbia Exploration (22)

Timok Gold Project: Korkan West Discovery

Near resource target drilled Nov. 2016

KW016: 105m at 1.21 g/t gold from

surface

Two phases of drilling at KW during

2017

41 holes for 6,770 m

Gold mineralization found over a

strike length of 220 m

Almost all reported intervals are oxide

11,500 m drilling program at Korkan

West and other targets started in April

If successful proceed to updated

resource and scoping study

KORKAN

BIGAR HILL

KW Zone

KO Zone

46

37

33

47

41

45

42

35

39

166

168

173

Timok Gold ProjectIndicated Mineral

Resources1.72 Moz Au at 1.54 g/t

Inferred Mineral Resources

0.02 Moz Au at 1.4 g/t

KORKAN WESTDISCOVERY

167

169171

38170

172

40

36

43

44

22. See footnotes contained in Appendix on slide 48

KWDD016

TSX:DPM

25

Additional Upside Potential Through Equity Interests

35km2 of prospective Abitibi geology located 25 km west of

Val-d’Or

$2.5 M within first 3 yrs to earn 51% with option to increase

to 71% following an additional $3.5 M expenditure in the

following 3 yrs

Winter scout drilling program completed. Results of first three

holes included 2m of 5.53 g/t gold within a 10m wide vein

zone

Value of DPM stake May 14, 2018 = ~$36.8M (incl. warrants)

M&I resource – 5.3M oz Au

Inferred resource – 1.85M oz Au

Targeting Au production Q1 2021

Production of ~240k oz Au/year (yrs 1 through 8)

Success at Umwelt Vault Zone and Llama extension provides

upside potential to mine life

Proceeding with pre-construction activities for 2018

Sabina Gold and Silver Corp.

Back River Project, Nunavut

DPM Ownership – 10.2% (18)

Malartic Property, Quebec

Joint Venture

18. See footnotes contained in Appendix on slide 48

SUMMARY

TSX:DPM

GROWTH OPTIMIZATION INNOVATION

24

TSX:DPM

27

Chelopech Record gold

production

Digital transformation

15,000 m regional drilling

30,000 m resource

drilling

Digital

transformation

Digital

transformation

Tsumeb Stable production

Transition to free

cash flow

Further optimize

EIA approval

Commercial

agreements for

expansion

Decision on

expansion

Commence

expansion

construction

Krumovgrad Construction 50%

complete

Construction completion

and commissioning (Q3)

First concentrate

production (Q4)

6,000 m drilling on

satellite deposits

Ramp-up (Q1)

Commercial

production

Timok Drilling of Korkan

West targets

11,500 m Korkan West

drilling

Resource update (Q3)

Metallurgical testwork

Scoping study

PEA or

Prefeasibility

study

2017 2018 2019 2020

Key Value Generating Catalysts

TSX:DPM

28

US$95MUS$95M

DPM Outlook – A Growing Low Cost Producer

AuEq Production

Growing to

>350,000 oz

at $600/oz

2016 2017 2018 Guidance 2018F + Krumovgrad

747

640-855

607

All-in Sustaining Cost (US$/oz) (1, 17)

Krumovgrad gold production

commences Q4 2018

2016 2017 2018 Guidance midpoint 2018F + Krumovgrad

Au Cu Ag

Gold Equivalent Production (000s oz) (15)

(based on metals contained in concentrate produced)

254

369

264280

1, 9, 15, 17, 20, See footnotes contained in Appendix on slide 48

(9) (9, 20)

(9, 20)(9)

(15)

(15)

Annual EBITDA Less: Sustaining Capex

From Operating AssetsTotal ~$183M

~ US$81M

Chelopech(FYE Dec 31, 2017)

Krumovgrad (20)

(years 1 to 5)

Tsumeb(FYE Dec 31, 2017)

~ US$7M

Total ~$102M

Tsumeb(FYE Dec 31, 2017)

Chelopech(FYE Dec 31, 2017)

US$7M

2017 With Krumovgrad

(years 1 to 5)

(years 1 to 5)

729

TSX:DPM

29

845

560

844 845 848900

959 964 980 991 998 1,011

1,121

1,292

DPM +Krum

DPM Saracen Premier Guyana Roxgold Ramelius Argonaut Alacer TMAC Resolute Teranga Alio Asanko

640

$3,2

12

$2,0

69

$5,6

67

$4,0

93

$3,8

60

$3,2

46

$2,9

45

$2,8

61

$2,8

33

$2,0

00

$1,9

59

$1,8

26

$1,4

61

$1,4

26

Alacer TMAC Premier Guyana DPM Saracen Roxgold Resolute DPM +Krum

Teranga Argonaut Asanko Ramelius Alio

Attractive Valuation

2018E All In Sustaining Costs (US$/oz) 6,12

EV/Reserves ($/oz) 12

(11)(13)

EV/2018E Gold Production ($/oz)

Undervalued on Mineral Reserves…

… and Cash Flow

… and Production

… with AISC in lowest quartile

6, 11,12, 13 See footnotes contained in Appendix on slide 48

(11)

(13)

EV/2018E AdjCF 12

(12)(13)

$161

$440 $429

$339

$180 $171 $165 $153$128 $119

$89$74

$51

Roxgold Saracen Ramelius Alacer TMAC Resolute DPM Guyana Premier Teranga Alio Argonaut Asanko

10.0x

4.3x

45.7x

31.9x

20.0x

15.0x 14.1x 14.0x

7.5x 7.1x 7.0x 6.3x 6.0x3.9x

Premier Alacer Resolute TMAC Asanko Teranga DPM Saracen Alio Guyana Argonaut Roxgold DPM +Krum

Ramelius

TSX:DPM

30

Attractive Valuation

Leverage Ratio 12

Debt to Capital

2018E P/NAV 12

Stability in operating jurisdictions

Tsumeb capital program complete & transitioning to FCF

Balance sheet deleveraged

Krumovgrad permitting & near term growth

DPM valuation

With a strong balance sheet… … and undervalued on P/NAV

Historical concerns have been addressed:

12 See footnotes contained in Appendix on slide 48

Klondex Roxgold Asanko Guyana Teranga Argonaut Premier Resolute Alacer DPM

1.22x

1.09x

0.80x

0.91x

0.67x

0.80x0.74x

0.51x

0.63x

25% 25%

13%

11%

6% 6%5%

2%1%

Asanko Roxgold Alacer Guyana Klondex Premier DPM Resolute Teranga Argonaut

27%

0.63x

consensus

23

TSX:DPM

31

Investment Highlights

Operating in mining friendly jurisdictions

Strong resource and reserve base

High quality, low cost, flagship asset

Near term, low cost growth in gold production

Growing exploration pipeline

Strong balance sheet

Strong management team

Attractive valuation

Strong Asset Base, Near Term Growth & Attractive Valuation

THANK YOU

TSX:DPM

Corporate Head Office:

One Adelaide Street East, Suite 500

Toronto, Ontario, M5C 2V9

T: 416 365-5191

Investor Relations

T: 416 365-2549

TSX:DPM

www.dundeeprecious.com

30

APPENDICES

TSX:DPM31

Business Strategy …………………………………………………………… 34

Mineral Resource and Reserve Base…………………………………….... 35

2018 Guidance……………………………………………………………….. 36

Krumovgrad

Open pit design and phases………………………………….37

Mine plan summary……………………………………………38

Process plant flowsheet……………………………………….39

Plant area……………………………………………………….40

Integrated mine waste facility…………………………………41

CSR……………………………………………………………...45

Hedge Position…………………………………………………………...........47

Mine RP…………………………………………………………………………48

Summary………………………………………………………………………..49Footnotes and Disclaimers……………………………………………….......50

TSX:DPM

34

Business Strategy

TSX:DPM

35

Mineral Resources (4,14,A,B) Million Tonnes Au (Moz) Cu (Mlbs) Au (g/t) Cu (%)

Chelopech

M&I

Inferred

12.9

1.4

1.400

0.121

311

29

3.39

2.7

1.10

0.93

Krumovgrad

Inferred (Upper Zone) 0.3 0.013 1.3

Timok

Indicated

Inferred

34.7

0.4

1.720

0.000

1.54

1.4

Tulare

Inferred (Kiseljak)

Inferred (Yellow Creek)

459.0

88.0

3.000

0.800

2,200

600

0.2

0.3

0.22

0.3

Total Mineral Resources

Measured & Indicated

Inferred

47.6

549.1

3.120

3.934

311

2,829

Mineral Reserves (4,14,A,B) Million Tonnes Au (Moz) Cu (Mlbs) Au (g/t) Cu (%)

Chelopech

Proven

Probable

10.5

8.3

0.965

0.921

216

160

2.86

3.46

0.93

0.88

Krumovgrad

Proven (Upper Zone)

Proven (Wall)

Probable (Upper Zone)

Probable (Wall)

1.1

1.5

3.5

0.1

0.124

0.325

0.337

0.020

3.46

6.83

3.00

5.54

Total P&P Mineral Reserves 25.00 2.692 376 3.36

Strong Mineral Resource and Reserve Base

4, 14, A, B See footnotes contained in Appendix on slides 48 & 49

TSX:DPM

36

2018 Guidance

US millions, unless otherwise indicated Chelopech Tsumeb Consolidated (5)

Ore mined/milled (‘000s tonnes) 2,100-2,200 - 2,100-2,200

Complex concentrate smelted (‘000s tonnes) - 220-250 220-250

Metals contained in concentrates produced (1)(2)

Gold (‘000s ounces) 165-195 - 165-195

Copper (million pounds) 33.7-40.4 - 33.7-40.4

Payable metals in concentrate sold (1)

Gold (‘000s) 140-170 - 140-170

Copper (million pounds) 31.0-37.0 - 31.0-37.0

Cash cost per tonne of ore processed ($) (3)(4) 37-40 - 37-40

All-in sustaining cost per ounce of gold ($) (3)(4)(5) - - 640-855

Cash cost per tonne of complex concentrate smelted, net of by-product credits ($) (3)(4) - 440-500 440-500

General & administrative expenses (3)(6) - - 20-24

Exploration expenses (3) - - 10-15

Sustaining capital expenditures (3)(4) 17-21 12-18 29-39

1) Gold produced includes gold in pyrite concentrate produced of 47,000 to 55,000 ounces and payable gold sold includes payable gold in pyrite concentrate sold of 30,000 to 35,000 ounces.

2) Metals contained in concentrate produced are prior to deductions associated with smelter terms.

3) Based on foreign exchange rates and, where applicable, metal prices that approximate current rates and prices after reflecting existing 2018 copper and ZAR hedges. In particular, 56% of 2018 payable copper

production has been hedged at a fixed price of $2.62 per pound and 28% of ZAR denominated operating expenses have been hedged at a fixed rate of 13.59.

4) Cash cost per tonne of ore processed, all-in sustaining cost per ounce of gold and cash cost per tonne of complex concentrate smelted, net of by-product credits, and sustaining capital expenditures have no

standardized meaning under GAAP. Refer to the “Non-GAAP Financial Measures” section of the MD&A for reconciliations to IFRS.

5) Includes the treatment charges, transportation and other selling costs related to the sale of pyrite concentrate, and payable gold in pyrite concentrate sold. Cash cost per ounce of gold sold, net of by-product

credits, excluding payable gold in pyrite concentrate sold and related costs, is expected to be between $550 and $600 in 2017. All-in sustaining cost per ounce of gold, excluding payable gold in pyrite

concentrate sold and related costs, is expected to be between $630 and $855 in 2018.

6) Excludes mark-to-market adjustments on share-based compensation and MineRPs’ general and administrative expenses.

TSX:DPM

37

Krumovgrad – Open Pit Design and Phases

Open Pit Design

Y1

Y2 Long Section Showing the Four Mining Phases

Y1 Y2

PhaseMaximum Elevation

(mRL)

Minimum Elevation

(mRL)

1 480 405

2 470 370

3 460 360

4 455 340

Minimum and Maximum Elevations of Each Mining Phase

TSX:DPM

38

Krumovgrad – Mine Plan Summary

TSX:DPM

39

Krumovgrad – Process Plant Flowsheet

KRUMOVGRAD PROCESS FLOWSHEET

OreRun of

mine pad

Primary

crushingSAG mill

Primary

regrind

Pebble

crusher

Roughers ScavengersThickened

tailings plantIMWF

Tailings

deposition

Ultra-fine

grinding

Process water

tank

RPWR /

SWOR

Water

Treatment

Environ-

ment

Cleaner 1Concentrate

thickener

Filter

press

Final

concentrate

Cleaner

scavengerCleaner 2

Crusher Thickener

Mill Filter

Flotation Water

Legend:

TSX:DPM

40

Krumovgrad – Plant Area

Crushing (0100)

Coarse ore

Storage (0100)

and Pebble

Crushing (0200)

Flotation (0300)

Conc Thickening

and Filtration

(0400)

Grinding (0200)

Tailings Thickening

Plant (1400) and HV

Area (0900/1050)

TSX:DPM

41

Krumovgrad – Integrated Mine Waste Facility (IMWF)Integrated Mine Waste

Facility (IMWF)

Open Pit

IMWF Haul Roads

and sump access

road

Raw and Process Water

Reservoir / Storm water

Overflow Reservoir

Grout Curtain

Pump

station

General Overview

TSX:DPM

42

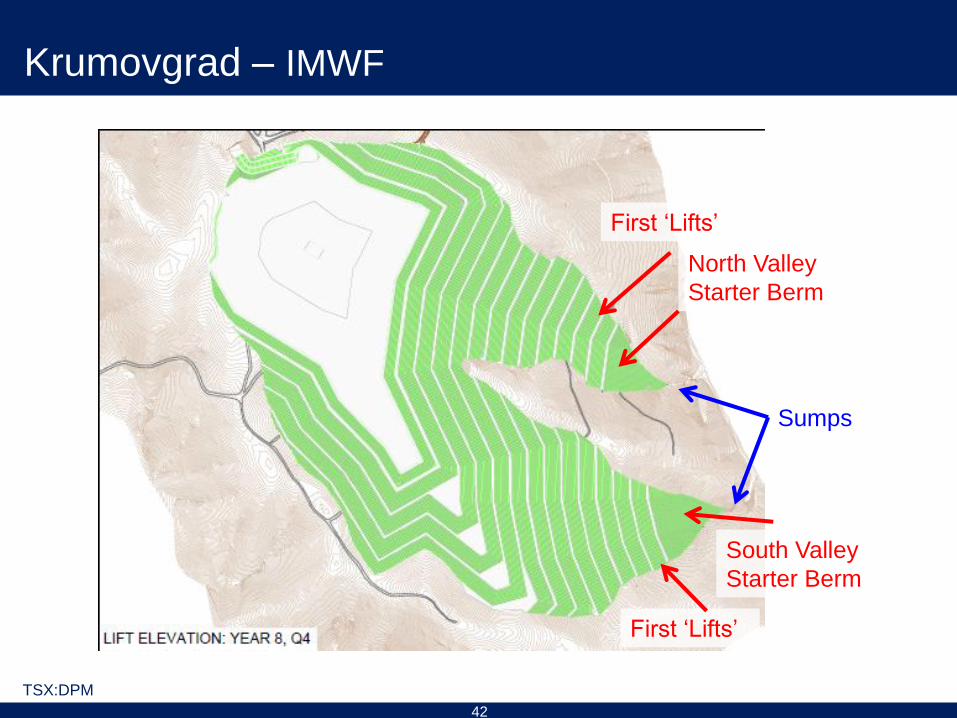

Krumovgrad – IMWF

South Valley

Starter Berm

North Valley

Starter Berm

First ‘Lifts’

First ‘Lifts’

Sumps

TSX:DPM

43

Krumovgrad – IMWF

Design is compliant with BGN, EU, and international standards

High level of confidence in structural stability

Contingency measures and safety features built into design

Meets all EIA commitments

Key Outcomes:

TSX:DPM

44

Krumovgrad – CSR – Community Relations

Memorandum of Understanding with Municipality of Krumovgrad signed

Stakeholders Engagement Plan

Social Management Plan

Proactive Company Actions

Company information center

Local Consultative Forums - operating at 8 settlements

Grievance Mechanisms

Training of local business is part of project development

TSX:DPM

45

Hedge Position at March 31, 2018

Production Hedges - Swaps YearVolume Hedged

(lbs) % Hedged Average fixed price ($/lb)

Payable copper Balance of 2018 14,375,225 53% $2.62

QP Hedges Year Volume Hedged % Hedged Average fixed price

Payable gold Balance of 2018 5,995 oz 100% $1,343.07/oz

Operating Cost FX Hedges YearForeign Currency

Amount Hedged% Hedged Average exchange rate

ZAR Balance of 2018 359,075,750 33% 13.6791

Production Hedges - Options Year Volume Hedged % HedgedAvg Ceiling

PriceFloor Price

Payable copper Balance of 2018 9,523,958 lbs 35% $3.32/lb $2.80/lb

Capital Expenditure FX Hedges YearForeign Currency

Amount Hedged% Hedged

Average exchange rate

(Foreign currency/US$)

Euro Balance of 2018 36,151,000 100% 1.1467

Production Hedges - Prepaid Forward Gold Sale Year Volume Hedged (oz) % Hedged Avg Forward Price

Payable Gold

Payable Gold

2019

2020

18,013

27,969

9%

11%

$1,390

$1,425

TSX:DPM

46

Creating a Leading Technology Provider

MineRP

Faster deployment of Terrative

Complementary technologies

Establishes DPM at the forefront of digital

innovation

Unique opportunity for DPM shareholders

Positions DPM to remain focussed on its core

mining operations

DPM acquired a 78% interest (70% fully

diluted) for an investment of ~US$20 million

in cash and Terrative assets

22% held by MineRP management

US$5 million of additional financing to

support working capital and growth

initiatives

MineRP Holdings Inc.+ =

Strategic HighlightsTransaction Overview

Independent software vendor ("ISV") for

the mining industry

Industry leading platform

Improves productivity in planning and

operations by integrating applications

Headquartered in South Africa

Wireless underground

communications technology

developed at Chelopech

TSX:DPM

47

DPM Summary

Chelopech

Krumovgrad

Subtotal

~$95 MM EBITDA Less: Sustaining (1) / yr

$81 MM first 5 yrs EBITDA Less: Sustaining (2) / yr(~$61 MM LOM)

~US$176 MM EBITDA Less: Sustaining (1)(2) / yr

• Exploration / mine life extension• Consistent track record of reserve

replacement

Sabina Equity(Incl. warrants)

$36.8 M equity value (stock price at May 14, 2018, warrants at Mar. 31, 2018)

Tsumeb

Timok

Other Assets

Debt

Market Cap: $464 MShare Price: C$3.37

• Transitioning to FCF positive• $7 MM in EBITDA Less: Sustaining (1)

• 370 Ktpa potential capacity with significant operating leverage and modest capital

1.7 MM oz resource in Serbia• Exploration• Oxide potential

Marlartic JV, Tulare and other Serbian licenses, Armenian JV, Kapan NSR, MineRP (78%)

$33M (as at March 31, 2018)

• Exploration on original license

1 Based on FYE Dec. 31, 2017 audited annual financial statements.

2 Based on NI 43-101 technical report entitled “Revised NI 43-101 Technical Report, Ada Tepe Deposit, Krumovgrad Project, Bulgaria” dated November 7, 2017

Cash $15M (as at March 31, 2018)

TSX:DPM

48

Footnotes and Disclaimers

1. AISC per ounce of gold represents cost of sales at Chelopech less depreciation, amortization and other non-cash items plus treatment charges, penalties, transportation and other selling costs, sustaining capital expenditures,

rehabilitation related to accretion expenses and an allocated portion of the Company’s G&A expenses less by-product revenues in respect of copper and silver including realized gains on copper derivative contracts divided by the

payable gold in copper and pyrite concentrates sold. Based on metals prices that approximate current rates.

2. Chelopech figures as per 2017 public filings; AISC includes gold production in pyrites

3. Effective dates for Reserves – contained in the 2017 Annual Information form dated March 28, 2018 for the year ended December 31, 2017, filed on SEDAR at www.SEDAR.com and available on our website at

www.dundeeprecious.com

4. Measured and Indicated Mineral Resources are in addition to Mineral Reserves

5. See slide 35 in Appendix for detailed Mineral Reserve and Mineral Resource Estimates

6. A non-GAAP measure. Refer to the “non-GAAP Financial Measures” section of the Q4 2017 MD&A for reconciliations to IFRS

7. Adjusted EBITDA represents earnings before interest, taxes, depreciation and amortization, adjusted for impairment charges, unrealized losses/gains on derivative contracts and investments at fair value, minus interest income

8. Includes gold in pyrite concentrate produced

9. Forecast/guidance information is subject to a number of risks. 2018E is based on guidance issued February 15, 2018. See “Forward Looking Statements” on slide 2

10. Krumovgrad figures as per June 6, 2016 press release.

11. Source DPM Guidance issued February 15, 2018

12. Source RBC Capital Markets, May 8, 2018 - Au US$1,307/oz, Ag US$17.32/oz, Cu US$3.24/lb; DPM balance sheet as at March 31, 2018; Adjusted cash flow defined as cash flow from operations before sustaining capital

expenditures. Analysts consensus for DPM NAV (RBC for peers) with P/NAV range of 0.4x-0.73x

13. Includes DPM 2018E plus Krumovgrad LOM average as per June 6, 2016 press release using RBC Capital Markets’ metal prices

14. Contained in the 2017 Annual Information Form dated March 28, 2018, filed on sedar at www.SEDAR.com and available on our website at www.dundeeprecious.com

15. Based on Au of $1,250/oz, Cu of $2.75/lb, Euro/US$ = 1.15

16. Calculated using Au production

17. AISC based on 2018 guidance for concentrate smelted

18. Source: Technical report for the Initial project Feasibility Study on the Back River Gold Property, Nunavut, Canada, Dated October 28, 2015, filed on sedar at www.SEDAR.com

19. Source: Timok Gold Project, Serbia – Updated Mineral Resource contained in the 2016 Annual Information Form, Dated March 28, 2017, filed on sedar at www.SEDAR.com

20. Based on NI 43-101 technical report entitled “Revised NI 43-101 Technical Report, Ada Tepe Deposit, Krumovgrad Project, Bulgaria” dated November 7, 2017, filed on sedar at www.SEDAR.com; Using gold price $1,250/oz

21. Includes 5 million warrants valued at US$3.4M as at March 31, 2018

22. For more information regarding the company’s current Mineral Resource and Mineral Reserve estimates, please refer to Dundee Precious Metals Annual Mineral Reserve and Mineral Resource Statement as at December 31,

2017 contained in our Annual Information Form, dated March 28, 2018, which is available on our website at http://www.dundeeprecious.com and on sedar at www.SEDAR.com

23. P/NAV consensus based on most recent analyst reports (April and/or May 2018): CIBC 0.4x (5%), RBC 0.75x (8%), Paradigm 0.45x (5%), GMP 0.35 (5%), Scotiabank 0.6x (5%)

TSX:DPM

49

Footnotes and Disclaimers Cont’d

A. The Mineral Resource and Mineral Reserve estimates for Chelopech and other scientific and technical information which supports this presentation was prepared by Petya Kuzmanova, MIMMM, CSci, Senior Resource

Geologist, of the Company, under the guidance of CSA Global (UK) Ltd. (“CSA”), in accordance with Canadian regulatory requirements set out in National Instrument 43-101 Standards of Disclosure for Mineral Projects, and

were reviewed and approved by, as relates to Mineral Resources, Maria O’Connor, BSc, MAusIMM, MAIG, Principal Resource Geologist of CSA, Ross Overall, Senior Corporate Resource Geologist, of the Company, and as

relates to Mineral Reserves, Karl van Olden, BSc (Eng), GDE, MBA, FAusIMM, Mining Manager of CSA. Maria O’Connor, Ross Overall and Karl van Olden are Qualified Persons (“QP”), as defined under NI 43-101 and are

independent of the company, with the exception of Mr. Overall who is not independent of the company. Ross Overall, Senior Corporate Resource Geologist, of the company, who is a QP, as defined under NI 43-101, has

reviewed and approved the contents of this presentation.

B. The Mineral Resource and Mineral Reserve estimates for the Krumovgrad project and other scientific and technical information which supports this presentation was prepared by CSA Global (UK) Ltd. (“CSA”), in accordance

with Canadian regulatory requirements set out in National Instrument 43-101 Standards of Disclosure for Mineral Projects, and were reviewed and approved by, as relates to Mineral Resources, Galen White, BSc (Hons)

FAusIMM FGS, Director and Principal Consultant of CSA, and Julian Bennett, BSc ARSM FIMMM CEng, as relates to Mineral Reserves. Both Galen White and Julian Bennett are independent Qualified Persons (“QP”), as

defined under NI 43-101. The NI 43-101 technical report (the “Krumovgrad Technical Report”) entitled “Revised NI 43-101 Technical Report, Ada Tepe Deposit, Krumovgrad Project, Bulgaria” dated November 7, 2017, in

respect of the study for the construction and operation of its Krumovgrad gold project disclosed herein, was filed November 7, 2017 on SEDAR at www.sedar.com. Simon Meik, former Corporate Director Processing of the

Company, and Edgar Urbaez, formerly Corporate Director, Technical Services, both of DPM, who are QPs and not independent of the Company, have reviewed and approved the contents of this presentation. The Mineral

Resource and Mineral Reserve estimates contained herein may be subject to legal, political, environmental or other risks that could materially affect the potential development of such Mineral Resources. See the Krumovgrad

Technical Report for more information with respect to the key assumptions, parameters, methods and risks of determination associated with the foregoing Mineral Resource estimates.

Qualified Person Disclosure

Cautionary note to U.S. Investors concerning estimates of Mineral Resources. These estimates have been prepared in accordance with the requirements of Canadian securities laws, which differ from the requirements of U.S.

securities laws. The terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are defined in NI 43-101 and recognized by Canadian securities laws but are not defined

terms under the U.S. Securities and Exchange Commission (“SEC”) Guide 7 (“SEC Guide 7”) or recognized under U.S. securities laws. U.S. investors are cautioned not to assume that any part or all of mineral deposits in these

categories will ever be upgraded to mineral reserves. “Inferred mineral resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all

or any part of an “inferred mineral resource” will ever by upgraded to a higher category. Under Canadian securities laws, estimates of “inferred mineral resources” may not form the basis of feasibility or pre-feasibility studies. U.S.

investors are cautioned not to assume that all or any part of an inferred mineral resource exists or is economically or legally mineable. Accordingly, these mineral resource estimates and related information may not be comparable to

similar information made public by U.S. companies subject to the reporting and disclosure requirements under the U.S. federal securities laws and the rules and regulations thereunder, including SEC Guide 7.