investor presentation · pdf fileiso 9001:2015 certified cops and cpc iso 9001:2015 customer...

TRANSCRIPT

Investor PresentationJanuary 2018

This presentation and the accompanying slides (the “Presentation”), which have been prepared by PNB Housing

Finance Ltd (the “Company”), have been prepared solely for information purposes and do not constitute any offer,

recommendation or invitation to purchase or subscribe for any securities, and shall not form the basis or be relied on in

connection with any contract or binding commitment what so ever. No offering of securities of the Company will be

made except by means of a statutory offering document containing detailed information about the Company.

This Presentation has been prepared by the Company based on information and data which the Company considers

reliable, but the Company makes no representation or warranty, express or implied, whatsoever, and no reliance shall

be placed on, the truth, accuracy, completeness, fairness and reasonableness of the contents of this Presentation. This

Presentation may not be all inclusive and may not contain all of the information that you may consider material. Any

liability in respect of the contents of, or any omission from, this Presentation is expressly excluded.

Certain matters discussed in this Presentation may contain statements regarding the Company’s market opportunity

and business prospects that are individually and collectively forward-looking statements. Such forward-looking

statements are not guarantees of future performance and are subject to known and unknown risks, uncertainties and

assumptions that are difficult to predict. These risks and uncertainties include, but are not limited to, the performance of

the Indian economy and of the economies of various international markets, the performance of the industry in India and

world-wide, competition, the company’s ability to successfully implement its strategy, the Company’s future levels of

growth and expansion, technological implementation, changes and advancements, changes in revenue, income or cash

flows, the Company’s market preferences and its exposure to market risks, as well as other risks. The Company’s

actual results, levels of activity, performance or achievements could differ materially and adversely from results

expressed in or implied by this Presentation. The Company assumes no obligation to update any forward-looking

information contained in this Presentation. Any forward-looking statements and projections made by third parties

included in this Presentation are not adopted by the Company and the Company is not responsible for such third party

statements and projections.

Safe Harbor

2

About PNB Housing Finance

3

4

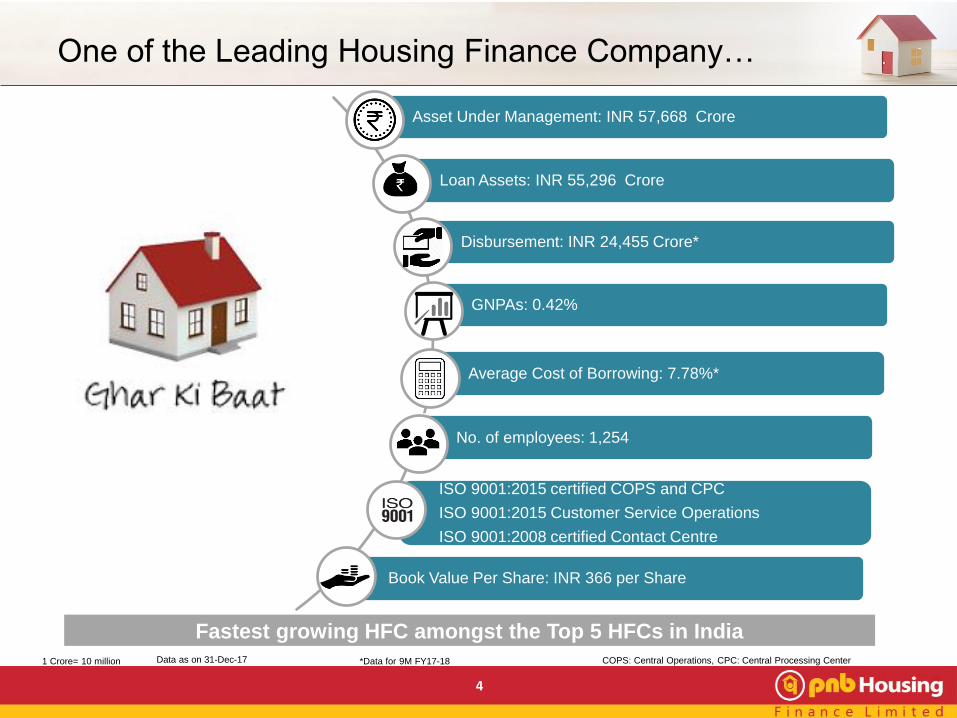

Disbursement: INR 24,455 Crore*

GNPAs: 0.42%

Fastest growing HFC amongst the Top 5 HFCs in India

*Data for 9M FY17-18

No. of employees: 1,254

One of the Leading Housing Finance Company…

ISO 9001:2015 certified COPS and CPC

ISO 9001:2015 Customer Service Operations

ISO 9001:2008 certified Contact Centre

Book Value Per Share: INR 366 per Share

Average Cost of Borrowing: 7.78%*

Loan Assets: INR 55,296 Crore

COPS: Central Operations, CPC: Central Processing Center1 Crore= 10 million Data as on 31-Dec-17

Asset Under Management: INR 57,668 Crore

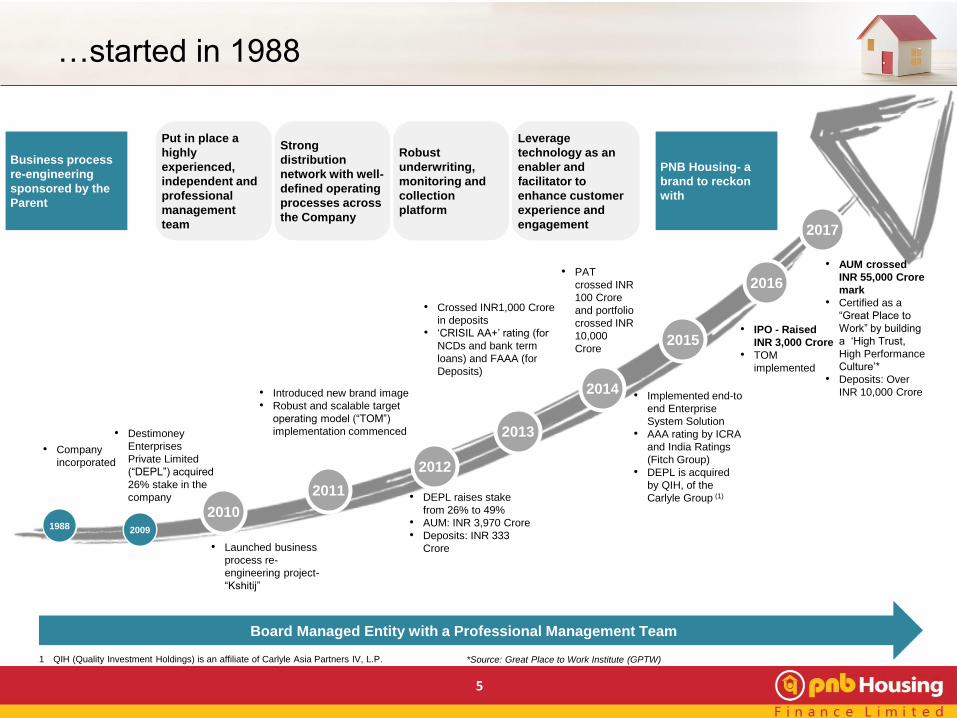

• Company

incorporated

• Destimoney

Enterprises

Private Limited

(“DEPL”) acquired

26% stake in the

company

• Crossed INR1,000 Crore

in deposits

• ‘CRISIL AA+’ rating (for

NCDs and bank term

loans) and FAAA (for

Deposits)

• Introduced new brand image

• Robust and scalable target

operating model (“TOM”)

implementation commenced

1988 2009

2010

2011

2012

2013

2014

2015

2016

• Launched business

process re-

engineering project-

“Kshitij”

• DEPL raises stake

from 26% to 49%

• AUM: INR 3,970 Crore

• Deposits: INR 333

Crore

• PAT

crossed INR

100 Crore

and portfolio

crossed INR

10,000

Crore

• Implemented end-to

end Enterprise

System Solution

• AAA rating by ICRA

and India Ratings

(Fitch Group)

• DEPL is acquired

by QIH, of the

Carlyle Group (1)

Business process

re-engineering

sponsored by the

Parent

Put in place a

highly

experienced,

independent and

professional

management

team

Robust

underwriting,

monitoring and

collection

platform

Leverage

technology as an

enabler and

facilitator to

enhance customer

experience and

engagement

Board Managed Entity with a Professional Management Team

1 QIH (Quality Investment Holdings) is an affiliate of Carlyle Asia Partners IV, L.P.

Strong

distribution

network with well-

defined operating

processes across

the Company

PNB Housing- a

brand to reckon

with

• IPO - Raised

INR 3,000 Crore

• TOM

implemented

5

2017

• AUM crossed

INR 55,000 Crore

mark

• Certified as a

“Great Place to

Work” by building

a ‘High Trust,

High Performance

Culture’*

• Deposits: Over

INR 10,000 Crore

*Source: Great Place to Work Institute (GPTW)

…started in 1988

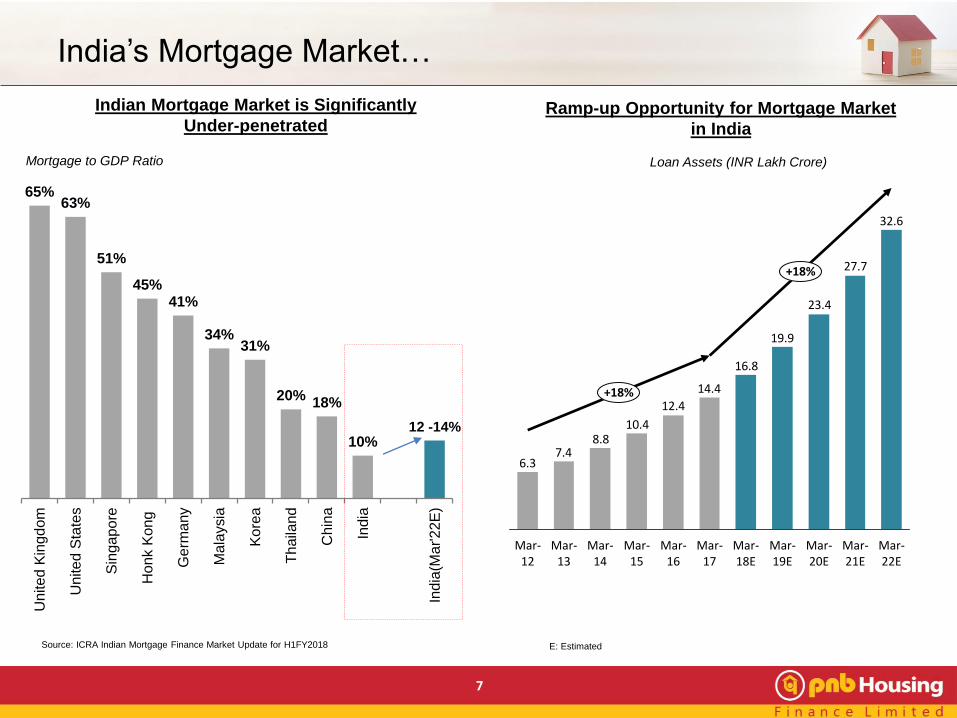

HFC Sector well placed…

6

65%63%

51%

45%41%

34%31%

20%18%

10%12 -14%

Un

ite

d K

ingd

om

Un

ite

d S

tate

s

Sin

ga

po

re

Ho

nk K

ong

Germ

any

Ma

laysia

Ko

rea

Thaila

nd

Ch

ina

India

India

(Ma

r'2

2E

)

7

Indian Mortgage Market is Significantly

Under-penetratedRamp-up Opportunity for Mortgage Market

in India

Loan Assets (INR Lakh Crore)Mortgage to GDP Ratio

Source: ICRA Indian Mortgage Finance Market Update for H1FY2018 E: Estimated

India’s Mortgage Market…

32.6

27.7

23.4

19.9

16.8

14.4

12.4

10.48.8

7.46.3

Mar-20E

Mar-19E

Mar-21E

Mar-22E

+18%

Mar-12

Mar-17

Mar-13

Mar-16

Mar-14

Mar-18E

Mar-15

+18%

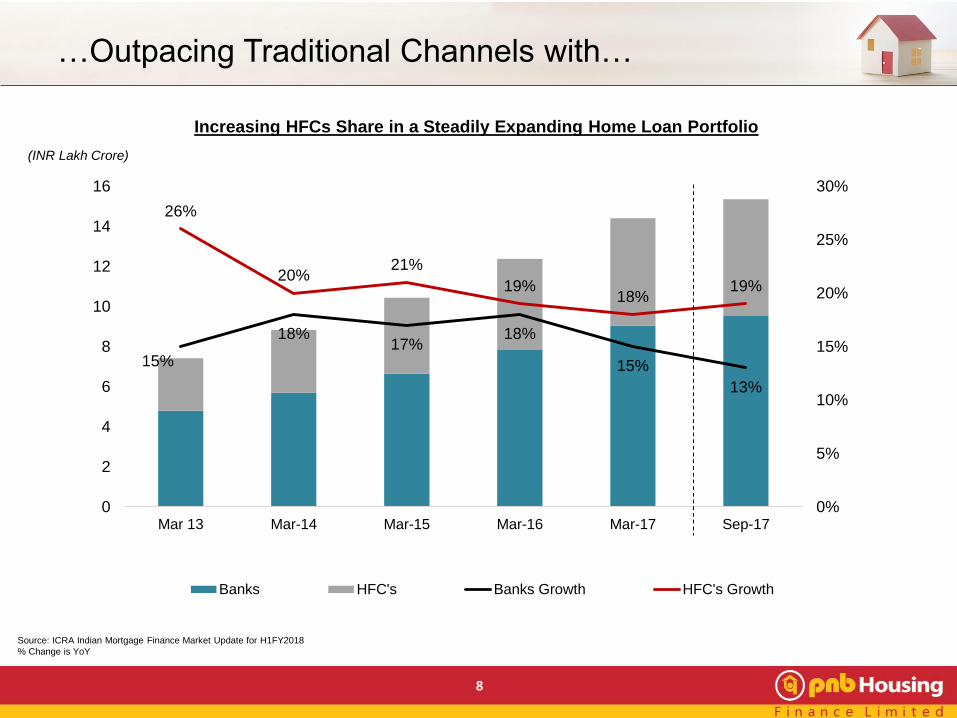

8

Increasing HFCs Share in a Steadily Expanding Home Loan Portfolio

(INR Lakh Crore)

Source: ICRA Indian Mortgage Finance Market Update for H1FY2018

% Change is YoY

15%

18%17%

18%

15%

13%

26%

20%21%

19%18%

19%

0%

5%

10%

15%

20%

25%

30%

0

2

4

6

8

10

12

14

16

Mar 13 Mar-14 Mar-15 Mar-16 Mar-17 Sep-17

Banks HFC's Banks Growth HFC's Growth

…Outpacing Traditional Channels with…

9

38%

18%

11%

10%

6%

2% 2% 1% 4%

HDFC Ltd LIC HF

IBHF DHFL

PNBHFL Gruh

Can Fin Repco HF

Others

Total Loan of all HFCs: INR 8.5 Lakh Crore

as on 30-Sep-17

Source: ICRA Indian Mortgage Finance Market Update for H1FY2018

% Change is YoY

Key HFC Metrics

Total No. of HFCs (Dec-17) : 91

Total Loan (Sep-17): INR 8.5 Lakh Crore

3 Years CAGR (Mar-17): 21.3%

Portfolio Composition of All HFCs

as on 31-Mar-17

67%

15%

10%

5% 3%

Home Loan LAP Construction Finance LRD Others

Deposit taking HFCs (Dec-17): 18

Portfolio Growth of HFCs

Top 5 HFCs: 82%

19%21%

19% 18% 19%

21%

26% 26% 27%30%

20%

22% 21% 20%23%

Mar-14 Mar-15 Mar-16 Mar-17 Sep-17

Home Loans Other Loans Overall Portfolio

….Sustainable Growth of HFCs

Government Initiatives

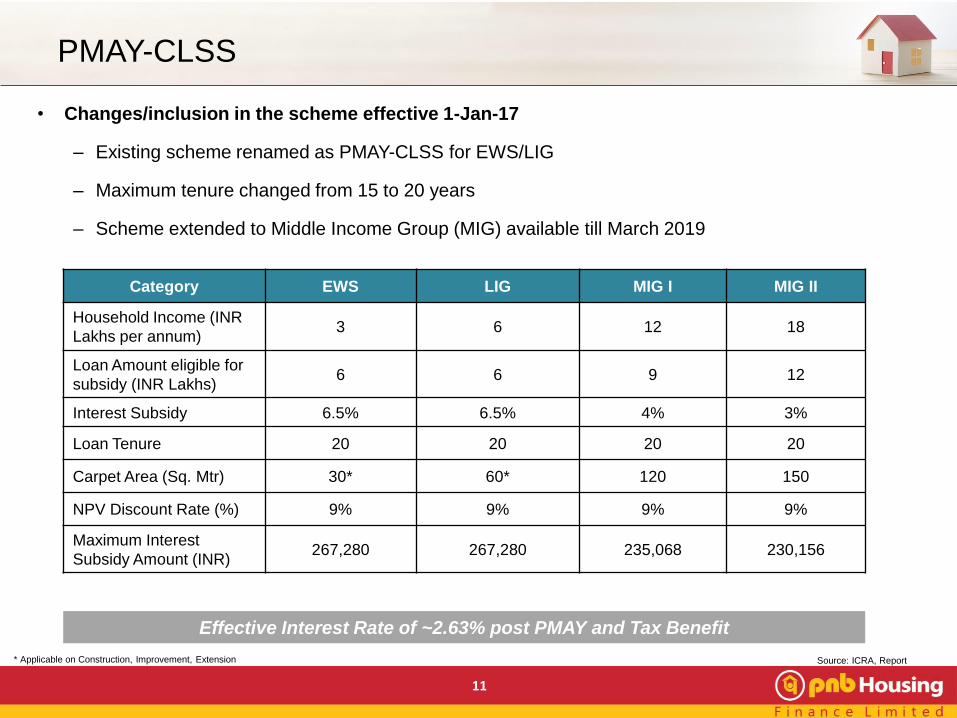

10

• Changes/inclusion in the scheme effective 1-Jan-17

– Existing scheme renamed as PMAY-CLSS for EWS/LIG

– Maximum tenure changed from 15 to 20 years

– Scheme extended to Middle Income Group (MIG) available till March 2019

11

Category EWS LIG MIG I MIG II

Household Income (INR

Lakhs per annum)3 6 12 18

Loan Amount eligible for

subsidy (INR Lakhs)6 6 9 12

Interest Subsidy 6.5% 6.5% 4% 3%

Loan Tenure 20 20 20 20

Carpet Area (Sq. Mtr) 30* 60* 120 150

NPV Discount Rate (%) 9% 9% 9% 9%

Maximum Interest

Subsidy Amount (INR)267,280 267,280 235,068 230,156

Effective Interest Rate of ~2.63% post PMAY and Tax Benefit

Source: ICRA, Report* Applicable on Construction, Improvement, Extension

PMAY-CLSS

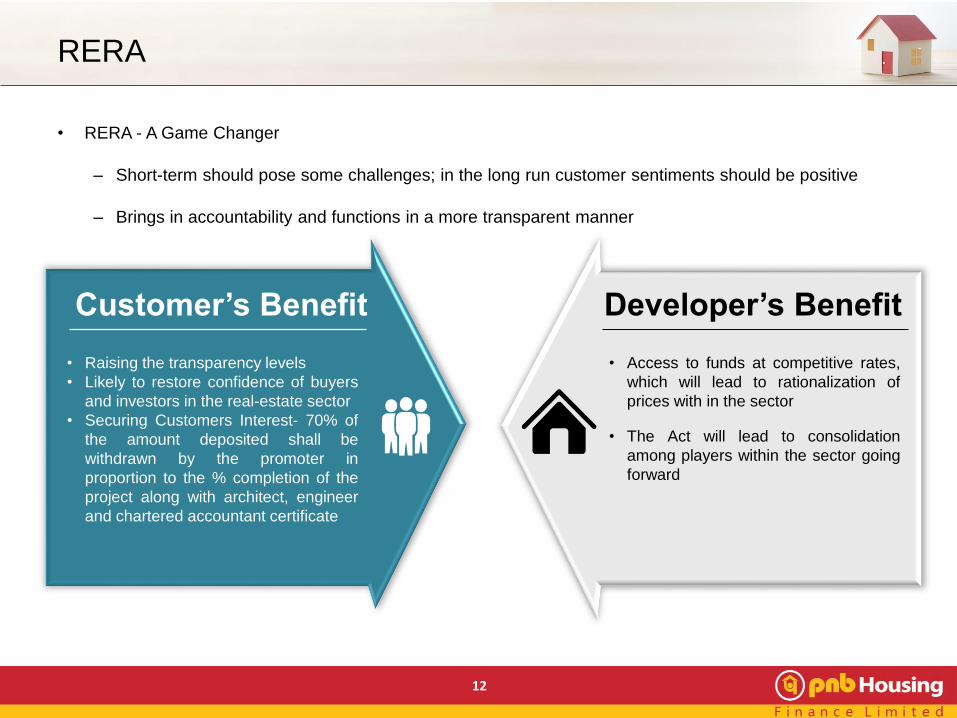

• RERA - A Game Changer

– Short-term should pose some challenges; in the long run customer sentiments should be positive

– Brings in accountability and functions in a more transparent manner

12

Customer’s Benefit

• Raising the transparency levels

• Likely to restore confidence of buyers

and investors in the real-estate sector

• Securing Customers Interest- 70% of

the amount deposited shall be

withdrawn by the promoter in

proportion to the % completion of the

project along with architect, engineer

and chartered accountant certificate

Developer’s Benefit

• Access to funds at competitive rates,

which will lead to rationalization of

prices with in the sector

• The Act will lead to consolidation

among players within the sector going

forward

RERA

Financial Performance of the Company

13

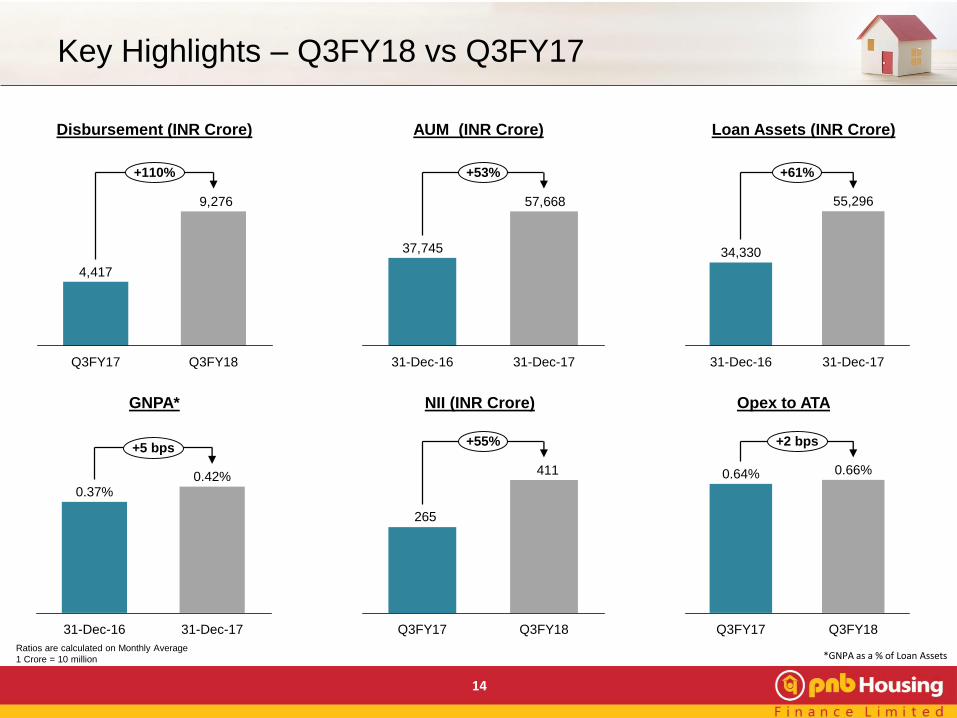

14

Ratios are calculated on Monthly Average

1 Crore = 10 million *GNPA as a % of Loan Assets

9,276

4,417

Q3FY17 Q3FY18

+110%

Disbursement (INR Crore)

57,668

37,745

+53%

31-Dec-1731-Dec-16

AUM (INR Crore)

31-Dec-16

55,296

31-Dec-17

+61%

34,330

Loan Assets (INR Crore)

GNPA*

31-Dec-17

+5 bps

0.42%0.37%

31-Dec-16

NII (INR Crore) Opex to ATA

0.66%

Q3FY18Q3FY17

0.64%

+2 bps

Key Highlights – Q3FY18 vs Q3FY17

411

265

Q3FY17 Q3FY18

+55%

15

PAT (INR Crore)NIM

Average Cost of BorrowingsAverage Yield Spread

217

138

Q3FY18Q3FY17

+58%

-75 bps

Q3FY18

10.74%9.99%

Q3FY17

-115 bps

Q3FY18

7.49%

8.64%

Q3FY17

3.01%

+2 bps

Q3FY18

2.99%

Q3FY17

2.50%

Q3FY17 Q3FY18

+40 bps

2.10%

+1 bps

Q3FY18

1.54%1.53%

Q3FY17

ROA

Key Highlights – Q3FY18 vs Q3FY17

Ratios are calculated on Monthly Average

1 Crore = 10 million

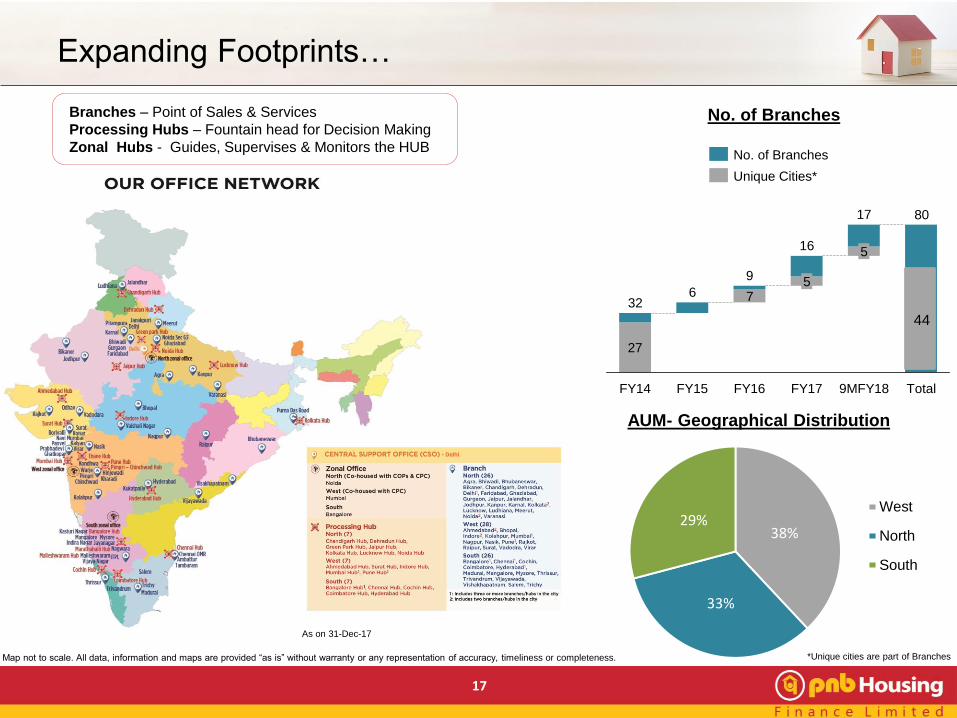

Expansion Led Growth and Robust TOM

16

17

No. of Branches

Map not to scale. All data, information and maps are provided “as is” without warranty or any representation of accuracy, timeliness or completeness.

Branches – Point of Sales & Services

Processing Hubs – Fountain head for Decision Making

Zonal Hubs - Guides, Supervises & Monitors the HUB

38%

33%

29%West

North

South

AUM- Geographical Distribution

*Unique cities are part of Branches

27

7

80

6

FY17

5

FY15FY14

32

9MFY18

16

FY16

17

5

Total

9

Unique Cities*

No. of Branches

44

Expanding Footprints…

As on 31-Dec-17

18

Customer

Acquisition/ Service

DSA DST

File received at

HUB

Fountain Head for

Decision Making

Fraud Control Unit

Legal Team

Collection Team

Technical Service

Group

Underwriter reviews

the reports and does

financial assessment

UnderwriterNo

Yes

Digital

Platform

Field Investigation

Lead

Aggregators

…with Robust Hub and Spoke Target Operating Model…

19

(INR Crore)

24,455

20,639

14,456

9,440

FY17FY15 9MFY18FY16

CAGR+48%

16,81927,177

38,531

55,296

57,668

31-Mar-17 31-Dec-1731-Mar-16

41,492

CAGR+55%

27,555

31-Mar-15

17,297

AUM Loan Assets

Asset

Disbursement

1 Crore = 10 million

…leading to Strong Disbursement and Asset growth…

20

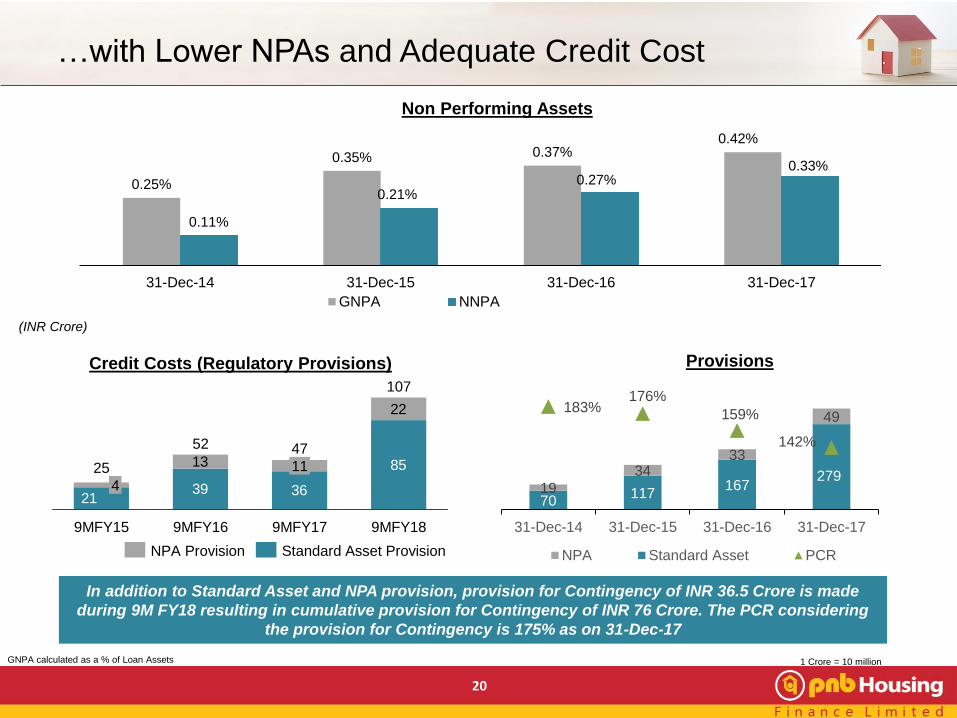

GNPA calculated as a % of Loan Assets

0.25%

0.35% 0.37%0.42%

0.11%

0.21%0.27%

0.33%

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

31-Dec-14 31-Dec-15 31-Dec-16 31-Dec-17

GNPA NNPA

39 36

8513

22

21

47

9MFY17 9MFY18

11

52

9MFY15 9MFY16

107

4

25

Credit Costs (Regulatory Provisions)

70117

167279

19

3433

49183%

176%

159%

142%

80%80%80%81%81%81%81%82%82%82%82%82%83%83%83%83%83%84%84%84%84%85%85%85%85%85%86%86%86%86%86%87%87%87%87%88%88%88%88%88%89%89%89%89%89%90%90%90%90%91%91%91%91%91%92%92%92%92%93%93%93%93%93%94%94%94%94%94%95%95%95%95%96%96%96%96%96%97%97%97%97%97%98%98%98%98%99%99%99%99%99%100%100%100%100%101%101%101%101%101%102%102%102%102%102%103%103%103%103%104%104%104%104%104%105%105%105%105%105%106%106%106%106%107%107%107%107%107%108%108%108%108%108%109%109%109%109%110%110%110%110%110%111%111%111%111%112%112%112%112%112%113%113%113%113%113%114%114%114%114%115%115%115%115%115%116%116%116%116%116%117%117%117%117%118%118%118%118%118%119%119%119%119%120%120%120%120%120%121%121%121%121%121%122%122%122%122%123%123%123%123%123%124%124%124%124%124%125%125%125%125%126%126%126%126%126%127%127%127%127%127%128%128%128%128%129%129%129%129%129%130%130%130%130%131%131%131%131%131%132%132%132%132%132%133%133%133%133%134%134%134%134%134%135%135%135%135%135%136%136%136%136%137%137%137%137%137%138%138%138%138%139%139%139%139%139%140%140%140%140%140%141%141%141%141%142%142%142%142%142%143%143%143%143%143%144%144%144%144%145%145%145%145%145%146%146%146%146%146%147%147%147%147%148%148%148%148%148%149%149%149%149%150%150%150%150%150%151%151%151%151%151%152%152%152%152%153%153%153%153%153%154%154%154%154%154%155%155%155%155%156%156%156%156%156%157%157%157%157%158%158%158%158%158%159%159%159%159%159%160%160%160%160%161%161%161%161%161%162%162%162%162%162%163%163%163%163%164%164%164%164%164%165%165%165%165%165%166%166%166%166%167%167%167%167%167%168%168%168%168%169%169%169%169%169%170%170%170%170%170%171%171%171%171%172%172%172%172%172%173%173%173%173%173%174%174%174%174%175%175%175%175%175%176%176%176%176%176%177%177%177%177%178%178%178%178%178%179%179%179%179%180%180%180%180%180%181%181%181%181%181%182%182%182%182%183%183%183%183%183%184%184%184%184%184%185%185%185%185%186%186%186%186%186%187%187%187%187%188%188%188%

1060

110160210260310

31-Dec-14 31-Dec-15 31-Dec-16 31-Dec-17

NPA Standard Asset PCR

…with Lower NPAs and Adequate Credit Cost

1 Crore = 10 million

Provisions

(INR Crore)

In addition to Standard Asset and NPA provision, provision for Contingency of INR 36.5 Crore is made

during 9M FY18 resulting in cumulative provision for Contingency of INR 76 Crore. The PCR considering

the provision for Contingency is 175% as on 31-Dec-17

Non Performing Assets

Standard Asset ProvisionNPA Provision

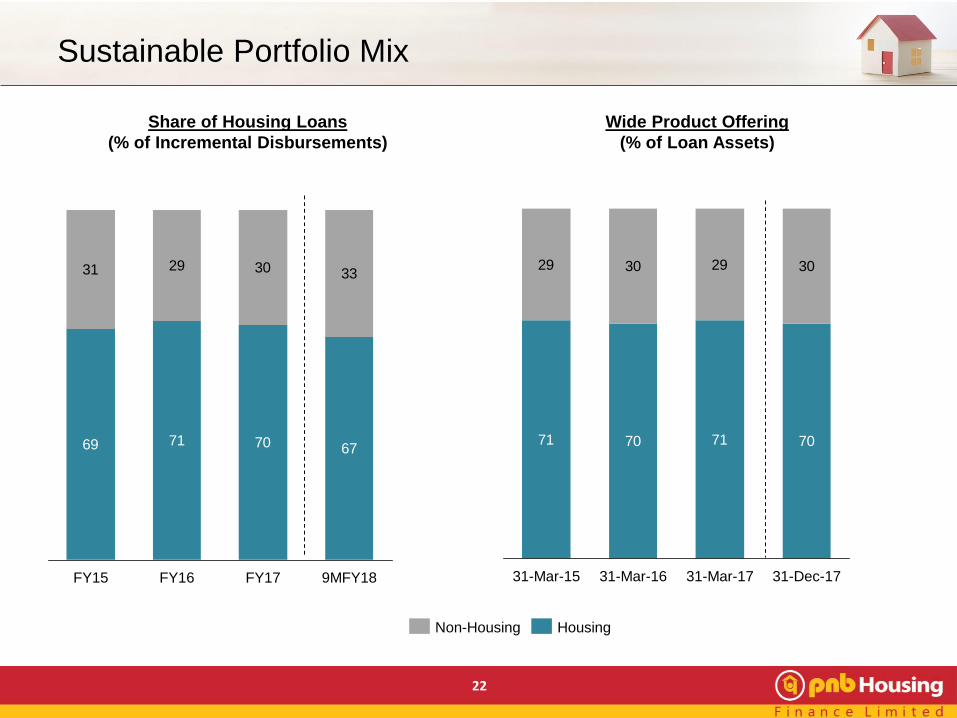

Sustainable Portfolio Mix

21

Share of Housing Loans

(% of Incremental Disbursements)

Wide Product Offering

(% of Loan Assets)

69 71 70

31 29 30

67

33

9MFY18FY17FY16FY15

HousingNon-Housing

22

71 70 71

29 30 29

70

30

31-Dec-1731-Mar-15 31-Mar-1731-Mar-16

Sustainable Portfolio Mix

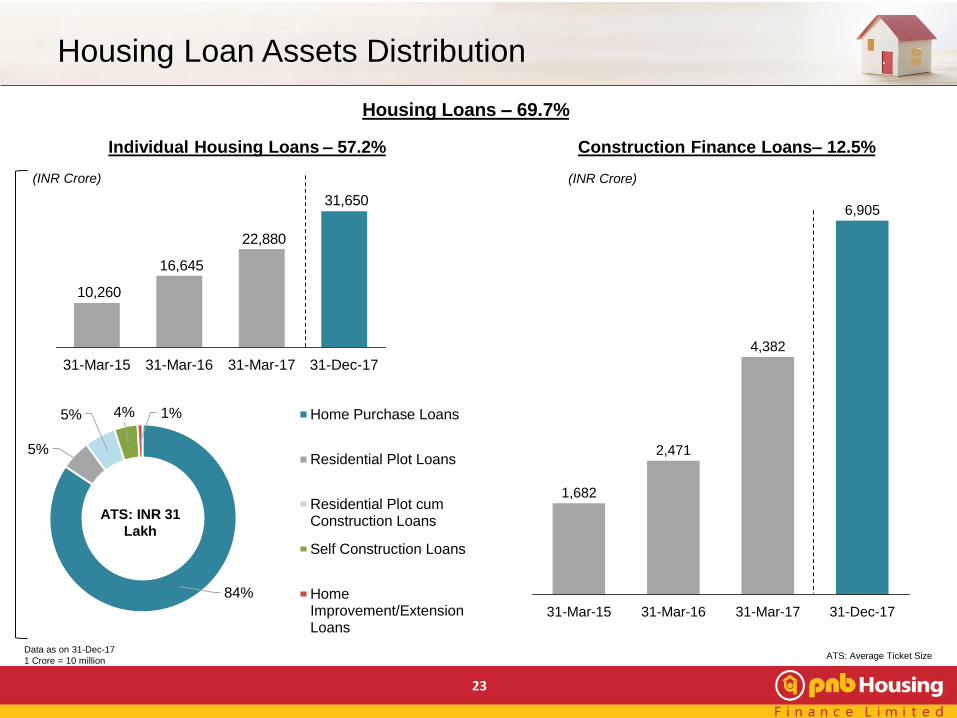

Construction Finance Loans– 12.5%Individual Housing Loans – 57.2%

84%

5%

5% 4% 1% Home Purchase Loans

Residential Plot Loans

Residential Plot cumConstruction Loans

Self Construction Loans

HomeImprovement/ExtensionLoans

ATS: INR 31

Lakh

Data as on 31-Dec-17

1 Crore = 10 million

Housing Loans – 69.7%

31,650

22,880

16,645

10,260

31-Mar-17 31-Dec-1731-Mar-1631-Mar-15

4,382

31-Mar-15 31-Mar-17

2,471

1,682

31-Mar-16 31-Dec-17

6,905

23

(INR Crore) (INR Crore)

ATS: Average Ticket Size

Housing Loan Assets Distribution

53%

21%

15%

11%

LAP LRD CTL NRPL

ATS:

INR 80 Lakh

ATS: Average Ticket Size

16,741

11,269

8,025

4,878

31-Mar-1731-Mar-1631-Mar-15 31-Dec-17

24

Non-Housing Loans - 30.3%

(INR Crore)

Data as on 31-Dec-17

1 Crore = 10 million

Non- Housing Loan Assets Distribution

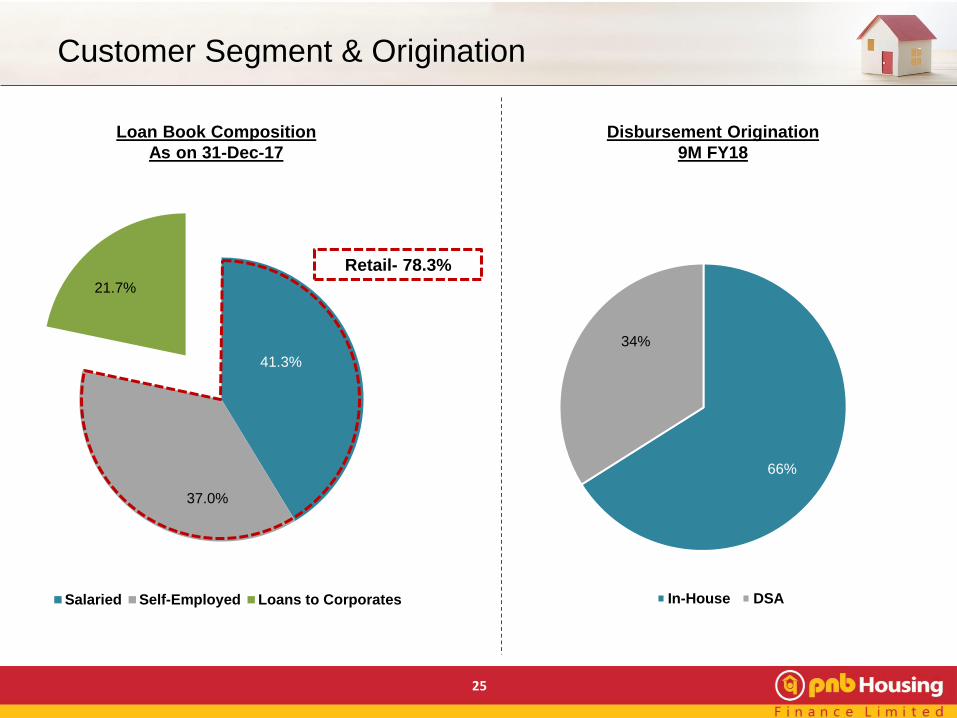

Disbursement Origination

9M FY18

Loan Book Composition

As on 31-Dec-17

25

41.3%

37.0%

21.7%

Salaried Self-Employed Loans to Corporates

66%

34%

In-House DSA

Retail- 78.3%

Customer Segment & Origination

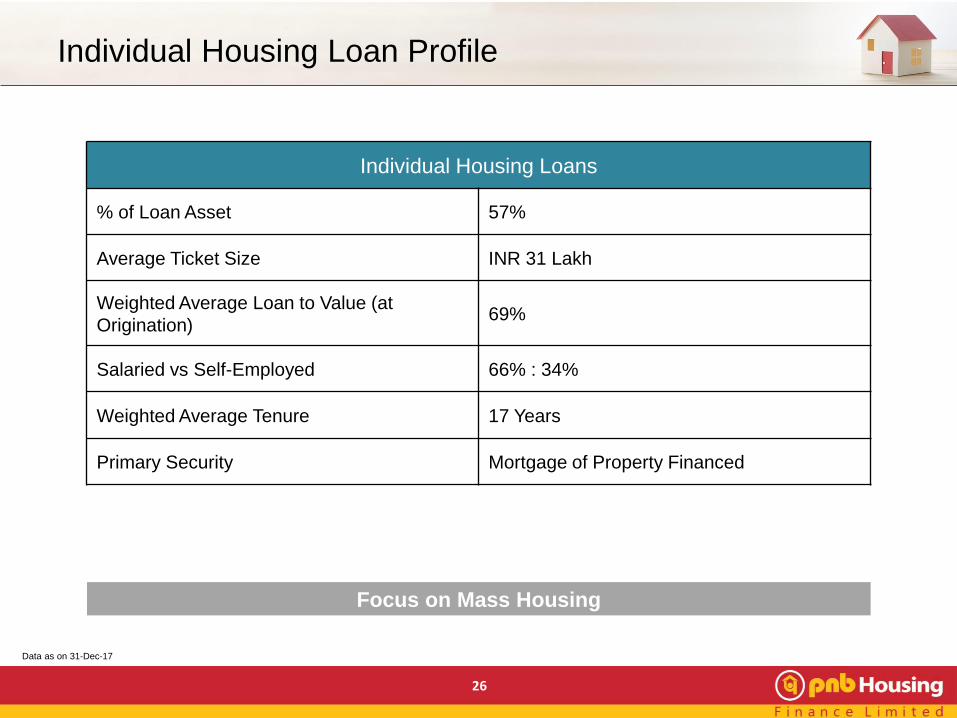

Individual Housing Loans

% of Loan Asset 57%

Average Ticket Size INR 31 Lakh

Weighted Average Loan to Value (at

Origination)69%

Salaried vs Self-Employed 66% : 34%

Weighted Average Tenure 17 Years

Primary Security Mortgage of Property Financed

26

Individual Housing Loan Profile

Data as on 31-Dec-17

Focus on Mass Housing

Loan Against Property

% of Loan Asset 16%

Average Ticket Size INR 49 Lakh

Weighted Average Loan to Value (at

Origination)48%

Salaried vs Self-Employed proportion 18% : 82%

Weighted Average Tenure 12 Years

Primary Security Mortgage of Property Financed

27

Loan Against Property Profile

Data is for LAP in retail segment

Data as on 31-Dec-17

Conservative and Robust Credit Underwriting Process

Operational and Financial Performance

28

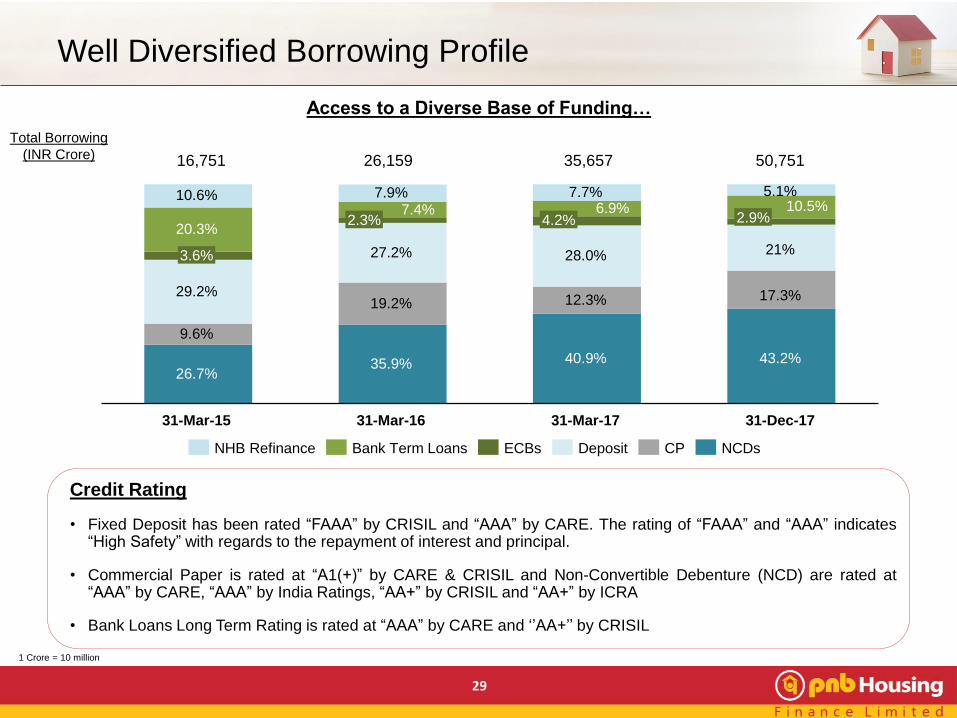

Credit Rating

• Fixed Deposit has been rated “FAAA” by CRISIL and “AAA” by CARE. The rating of “FAAA” and “AAA” indicates“High Safety” with regards to the repayment of interest and principal.

• Commercial Paper is rated at “A1(+)” by CARE & CRISIL and Non-Convertible Debenture (NCD) are rated at“AAA” by CARE, “AAA” by India Ratings, “AA+” by CRISIL and “AA+” by ICRA

• Bank Loans Long Term Rating is rated at “AAA” by CARE and ‘’AA+’’ by CRISIL

29

NHB Refinance CPECBsBank Term Loans NCDsDeposit

3.6%

7.7%

29.2%

6.9%

27.2%

7.4%

19.2%

35.9%

31-Mar-15

28.0%

4.2%

9.6%

2.3%

26.7%

31-Mar-16

20.3%

10.6% 7.9%

40.9%

31-Dec-1731-Mar-17

12.3%

2.9%

43.2%

10.5%

21%

17.3%

5.1%

16,751 35,65726,159

Total Borrowing

(INR Crore)

Access to a Diverse Base of Funding…

50,751

1 Crore = 10 million

Well Diversified Borrowing Profile

30

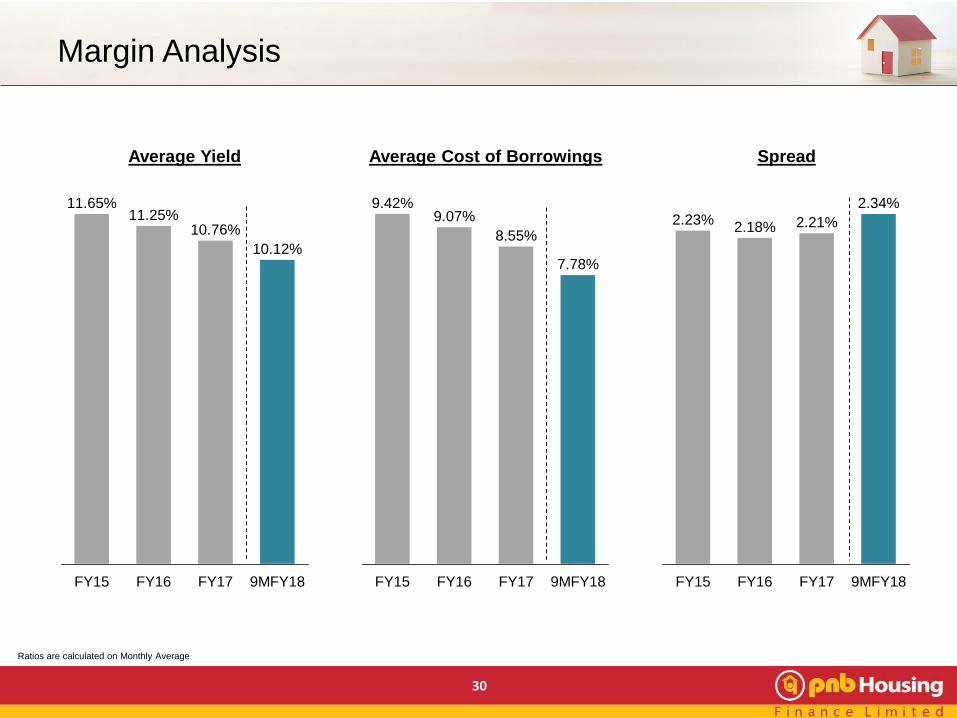

10.12%

10.76%

FY17FY16 9MFY18

11.65%11.25%

FY15 9MFY18FY17FY16

9.07%

FY15

8.55%

7.78%

9.42%

FY17FY16 9MFY18

2.18% 2.21%

FY15

2.23%2.34%

Average Yield Average Cost of Borrowings Spread

Ratios are calculated on Monthly Average

Margin Analysis

31

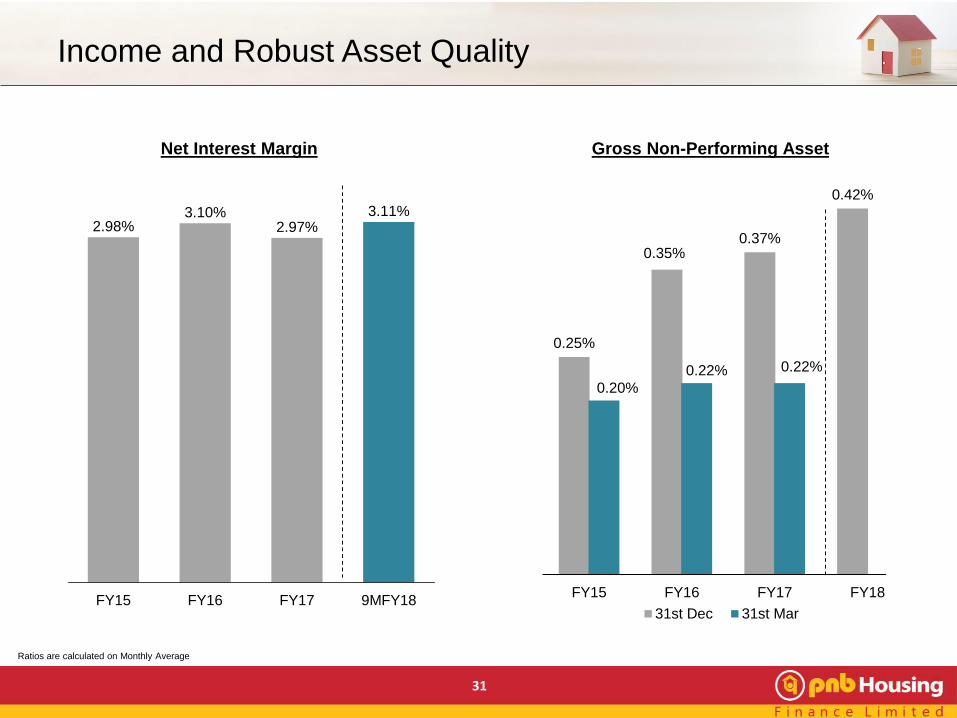

Net Interest Margin

3.11%

FY15 FY17

2.97%3.10%

2.98%

FY16 9MFY18

0.25%

0.35%0.37%

0.42%

0.20%

0.22% 0.22%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

FY15 FY16 FY17 FY18

31st Dec 31st Mar

Gross Non-Performing Asset

Income and Robust Asset Quality

Ratios are calculated on Monthly Average

32

Cost to Income RatioOpex to ATA Ratio

Return on Asset Return on Equity

Operating Leverage playing out with Better Return Profile

14.92%

9MFY18**FY17*FY16

17.12%

FY15

16.08%

13.92%

FY17

0.65%0.73%

FY16 9MFY18

0.98%

0.83%

FY15

25.15%

FY15 9MFY18FY16

30.87%

FY17

22.43%

18.32%

9MFY18**FY15

1.28%

FY17

1.37%1.46%

FY16

1.62%

Ratios are calculated on Monthly AverageOpex to ATA is calculated as Operating Expenditure(Employee Cost + Other Expenses + Depreciation - Acquisition Cost - CSR cost)/Average Total Assets as per Balance sheetCost to Income Ratio is calculated as Operating Expenditure(Employee Cost + Other Expenses + Depreciation - Acquisition Cost - CSR cost) / (Net Revenue-Acquisition Cost)Return on Asset is on Average Total Assets as per Balance sheet* Capital of INR 3,000 Crore raised through IPO of 3,87,19,309 fresh equity shares** Annualized

Maintaining Prudence…

33

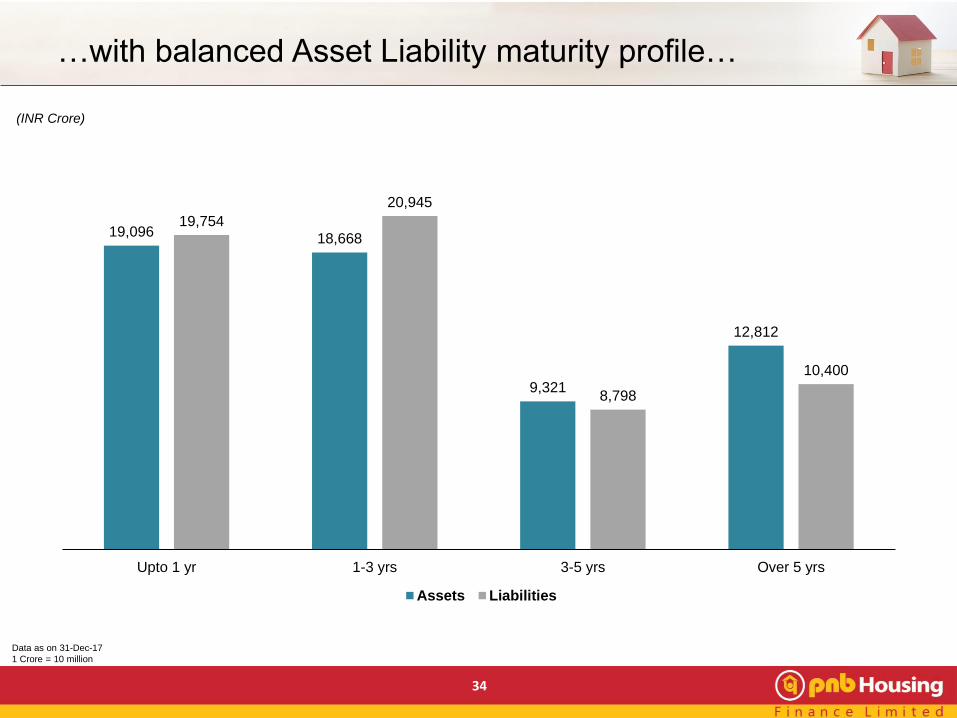

(INR Crore)

34

Data as on 31-Dec-17

1 Crore = 10 million

19,096 18,668

9,321

12,812

19,754

20,945

8,798

10,400

Upto 1 yr 1-3 yrs 3-5 yrs Over 5 yrs

Assets Liabilities

…with balanced Asset Liability maturity profile…

35

Capital to Risk Asset Ratio

Average Gearing (x)

Ratio is calculated on Monthly Average

7.24

8.72

10.7710.73

31-Mar-1731-Mar-1631-Mar-15 31-Dec-17

…and adequate Capital & Comfortable Gearing

17.39%

31-Dec-17

3.35%

5.14%

4.06%12.70%

13.33%

31-Mar-1731-Mar-16

3.66%

31-Mar-15

21.62%

13.76%

10.41% 9.04%

16.48%

Tier 2 Tier 1

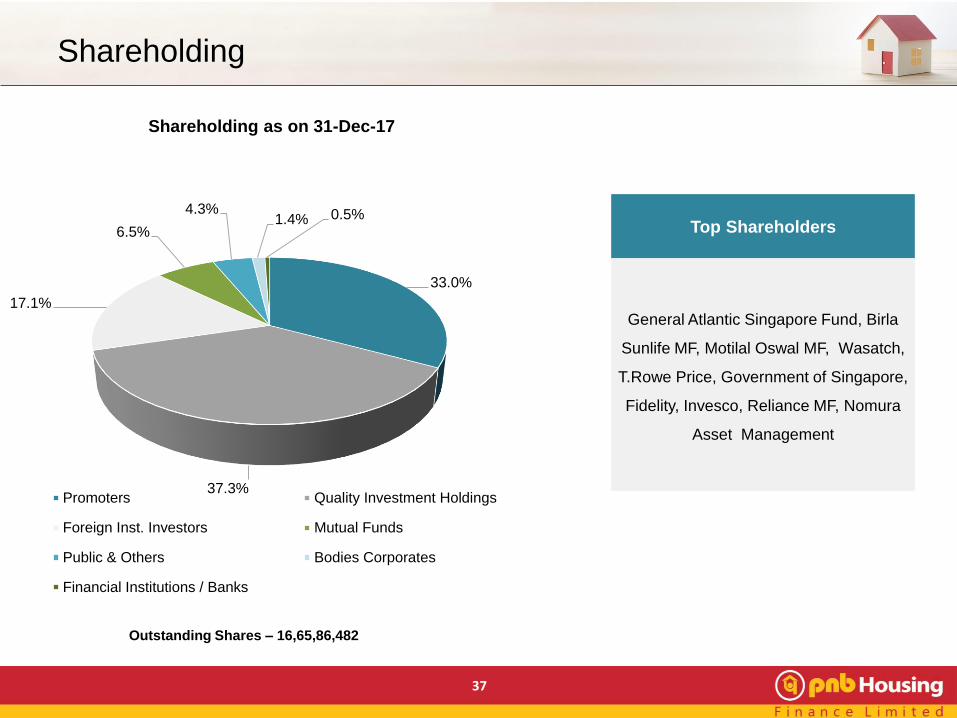

Shareholding

36

37

Shareholding

Top Shareholders

General Atlantic Singapore Fund, Birla

Sunlife MF, Motilal Oswal MF, Wasatch,

T.Rowe Price, Government of Singapore,

Fidelity, Invesco, Reliance MF, Nomura

Asset Management

33.0%

37.3%

17.1%

6.5%

4.3%1.4% 0.5%

Shareholding as on 31-Dec-17

Promoters Quality Investment Holdings

Foreign Inst. Investors Mutual Funds

Public & Others Bodies Corporates

Financial Institutions / Banks

Outstanding Shares – 16,65,86,482

Detailed Financials

38

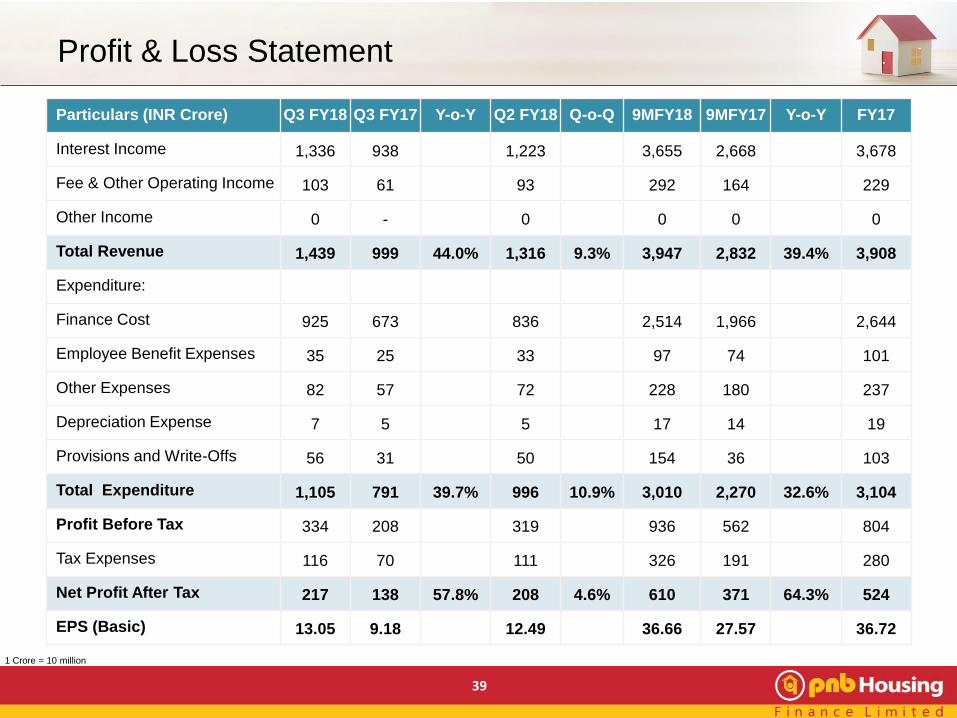

Profit & Loss Statement

39

Particulars (INR Crore) Q3 FY18 Q3 FY17 Y-o-Y Q2 FY18 Q-o-Q 9MFY18 9MFY17 Y-o-Y FY17

Interest Income 1,336 938 1,223 3,655 2,668 3,678

Fee & Other Operating Income 103 61 93 292 164 229

Other Income 0 - 0 0 0 0

Total Revenue 1,439 999 44.0% 1,316 9.3% 3,947 2,832 39.4% 3,908

Expenditure:

Finance Cost 925 673 836 2,514 1,966 2,644

Employee Benefit Expenses 35 25 33 97 74 101

Other Expenses 82 57 72 228 180 237

Depreciation Expense 7 5 5 17 14 19

Provisions and Write-Offs 56 31 50 154 36 103

Total Expenditure 1,105 791 39.7% 996 10.9% 3,010 2,270 32.6% 3,104

Profit Before Tax 334 208 319 936 562 804

Tax Expenses 116 70 111 326 191 280

Net Profit After Tax 217 138 57.8% 208 4.6% 610 371 64.3% 524

EPS (Basic) 13.05 9.18 12.49 36.66 27.57 36.72

1 Crore = 10 million

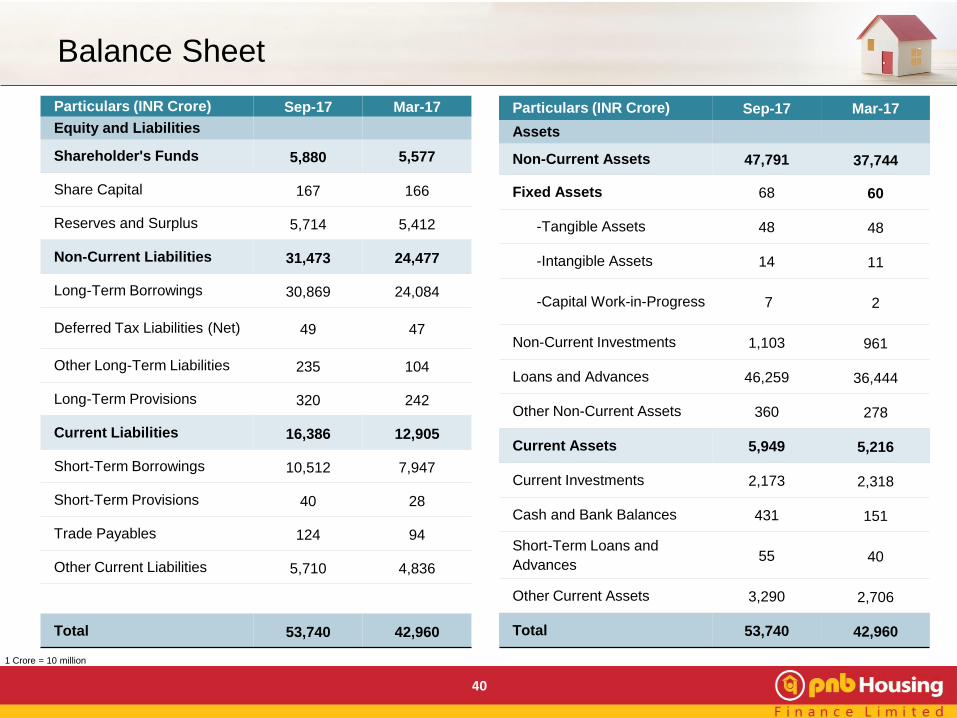

40

Particulars (INR Crore) Sep-17 Mar-17

Equity and Liabilities

Shareholder's Funds 5,880 5,577

Share Capital 167 166

Reserves and Surplus 5,714 5,412

Non-Current Liabilities 31,473 24,477

Long-Term Borrowings 30,869 24,084

Deferred Tax Liabilities (Net) 49 47

Other Long-Term Liabilities 235 104

Long-Term Provisions 320 242

Current Liabilities 16,386 12,905

Short-Term Borrowings 10,512 7,947

Short-Term Provisions 40 28

Trade Payables 124 94

Other Current Liabilities 5,710 4,836

Total 53,740 42,960

Particulars (INR Crore) Sep-17 Mar-17

Assets

Non-Current Assets 47,791 37,744

Fixed Assets 68 60

-Tangible Assets 48 48

-Intangible Assets 14 11

-Capital Work-in-Progress 7 2

Non-Current Investments 1,103 961

Loans and Advances 46,259 36,444

Other Non-Current Assets 360 278

Current Assets 5,949 5,216

Current Investments 2,173 2,318

Cash and Bank Balances 431 151

Short-Term Loans and

Advances55 40

Other Current Assets 3,290 2,706

Total 53,740 42,960

Balance Sheet

1 Crore = 10 million

Saksham – Contributing to the Society

41

42

Enhancing Human Potential

• Partnered with The Confederation of Real Estate

Developers Association of India (CREDAI) to conduct

Onsite & Offsite skills training programmes for

construction workers

Reaching Out, Reaching Far

• Collaborated with Mobile Creches and various real

estate developers to offer day care services to the

children of construction workers on various

construction sites and provide them with education,

hygiene and nutrition

Investing in Education

• Partnered with VIDYA, a NGO working for the

underprivileged children

• Adopted two school with Vidya- Rainbow Montessori

School (Bal Vihar) and Primary School of South Delhi

Municipal Corporation

Glimpses of Social Interventions

Improving Access to Health Care: Supporting Public hospitals with an aim to improve their Infrastructure

43

…winning Awards & Accolades

Awarded ‘Excellence in Customer Relation’ at GIHED CREDAI Property Show 2017. This award

testaments our belief in customer relations.

Our IPO has been awarded “IPO of the Year” by Finance Monthly Magazine (M&A Award)- A

leading international business publication. This award is a testimony of investor confidence in our

Organisation and recognition of ‘Kshitij – Our transformation journey over last 6 years’.

Honored in the field of “IT Security” at CSO 100 Awards organized by CSO 100 Award and IDG

Security. This accreditation is a testament of our dedication and commitment to serve our customers

and stakeholders by giving them an unparalleled security.

Mr. Nitant Desai (Chief Centralized Operation & Technology Officer) has been awarded amongst

Top 100 CIOs of India

PNB Housing Finance won bronze award at Outdoor Advertising Awards 2017, in the financial

services category for its innovative outdoor campaign executed during the IPO. The award was

presented by OAC (Outdoor Advertising Convention), one of the most credible outdoor advertising

award & knowledge sharing industry platform.

Awarded ‘Best Project Finance Company of the Year’ at Construction Times Builders Award. The

honour was bestowed by Shri Vijay Shivtare, Hon’ble Minister of State, Water Resources and Water

Conservation, Maharashtra and Shri Rahul Shiwale, Hon’ble Member of Parliament, in a grand

ceremony in Mumbai.

“Leading Housing Finance Company 2017” at National Awards for Best Housing Finance Companies

organized by CMO Asia on 24th November, 2017 in Mumbai.

Strong Management Team…

44

…with Extensive Industry Experience…

45

Age : 45 Years

No. of Years with

PNB HF : 5 Years

Prior Engagements :

IndusInd Bank

ABN AMRO Bank NV

ICICI Bank Limited

Age : 51 Years

No. of Years with

PNB HF : 5 Years

Prior Engagements :

Religare Finvest Ltd

GE Money Indiabulls

Financial Services

Shaji Varghese – ED - Business

Development

Ajay Gupta – ED - Risk Management

Age : 55 Years

No. of Years with

PNB HF : 6 Years

Prior Engagements :

HDFC Standard Life

Insurance, Union

National Bank, ICICI

Bank

Age : 53 Years

No. of Years with

PNB HF : 22 Years

Prior Engagements :

Ansal Group

Age : 50 Years

No. of Years with

PNB HF : 6 Years

Prior Engagements

: ARMS (Arcil)

Indian Army

Nitant Desai - Chief Centralised

Operation & Technology Officer

Sanjay Jain - Company Secretary &

Head ComplianceAnshul Bhargava - Chief People Officer

Sanjaya Gupta -

Managing Director

Age : 55 Years

No. of Years with PNB HF : 7 Years

Prior Engagements : AIG, ABN Amro Bank N.V. and HDFC Limited

Joining of new CFO is in process

…under the Aegis of a Highly Experienced Board

46

Mr. Sunil Mehta

Chairman – Non Executive

Dr. Ram S. Sangapure

Non Executive Director

Sunil Kaul

Non Executive Director

R Chandrasekaran

Independent Director

Nilesh S. Vikamsey

Independent Director

Shubhalakshmi Panse

Independent DirectorSanjaya Gupta

Managing Director

Age:

58 Years

Current Position:

MD & CEO of PNB

Age:

53 Years

Current Position:

Sr. Partner, Khimji

Kunverji and Co

President-ICAI

Age:

63 Years

Current Position:

Ex-Banker, CMD,

Allahabad Bank

Age:

55 Years

Current Position:

MD, PNB Housing

Finance

Age:

59 Years

Current Position:

Executive Director

of PNB

Age:

57 Years

Current Position:

MD, Carlyle

Head, SE Asia, FIG,

Carlyle

Shital Kumar Jain

Independent Director

Age:

78 Years

Current Position:

Ex Banker & Credit

Head India,

Citigroup

Ashwani Kumar Gupta

Independent Director

Age:

63 Years

Current Position:

Financial Consultant

Gourav Vallabh

Independent Director

Age:

40 Years

Current Position:

Professor of

Finance, XLRI

Age:

60 Years

Current Position:

Founder and

Executive Vice

Chairman, Cognizant

47

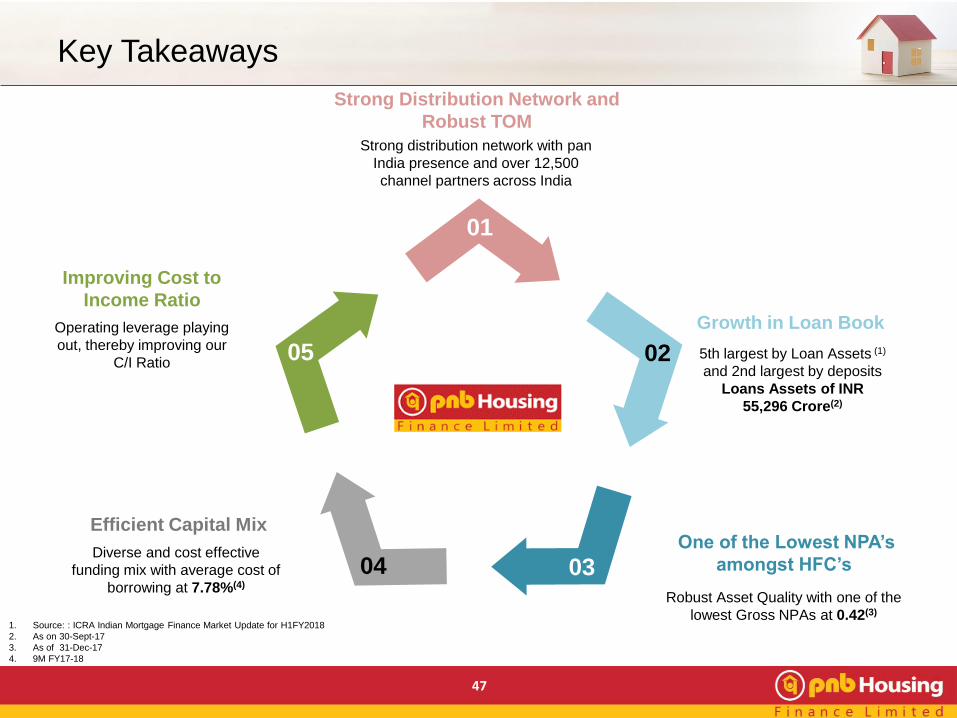

Key Takeaways

Strong distribution network with pan

India presence and over 12,500

channel partners across India

Strong Distribution Network and

Robust TOM

Diverse and cost effective

funding mix with average cost of

borrowing at 7.78%(4)

Efficient Capital Mix

Robust Asset Quality with one of the

lowest Gross NPAs at 0.42(3)

One of the Lowest NPA’s

amongst HFC’s

5th largest by Loan Assets (1)

and 2nd largest by deposits

Loans Assets of INR

55,296 Crore(2)

Growth in Loan BookOperating leverage playing

out, thereby improving our

C/I Ratio

Improving Cost to

Income Ratio

Bring your presentation to life.

Download this awesome diagram.

Text Here

01

04 03

0205

1. Source: : ICRA Indian Mortgage Finance Market Update for H1FY2018

2. As on 30-Sept-17

3. As of 31-Dec-17

4. 9M FY17-18

Annexure

48

49

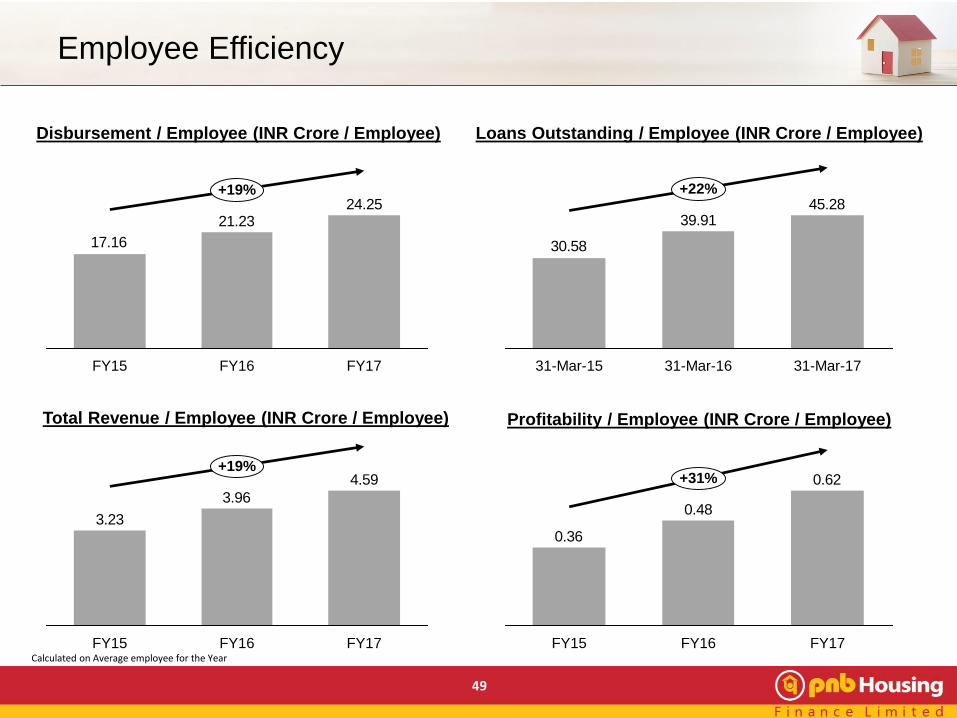

Employee Efficiency

Loans Outstanding / Employee (INR Crore / Employee)

Profitability / Employee (INR Crore / Employee)

Disbursement / Employee (INR Crore / Employee)

Total Revenue / Employee (INR Crore / Employee)

24.2521.23

17.16

FY16

+19%

FY15 FY17

45.2839.91

30.58

31-Mar-15 31-Mar-1731-Mar-16

+22%

4.59

3.96

3.23

FY15 FY16

+19%

FY17

0.62

0.48

0.36

+31%

FY17FY15 FY16Calculated on Average employee for the Year

50

Glossary

ATA Average Total Assets

ATS Average Ticket Size

AUM Asset Under Management

BVPS Book-value per Share

C/I Cost to Income

CRAR Capital to Risk Asset Ratio

CP Commercial Paper

CTL Corporate Term Loan

DPS Dividend per Share

DSA Direct Selling Agents

ECB External Commercial Borrowing

EPS Earning Per Share

GNPA Gross Non-Performing Asset

HFCs Housing Finance Companies

LAP Loan against Property

LRD Lease Rental Discounting

NCDs Non-Convertible Debentures

NII Net Interest Income

NIM Net Interest Margin

NNPA Net Non-Performing Asset

NPA Non-Performing Asset

NRPLs Non-Residential Premises Loans

PAT Profit After Tax

PCR Provision Coverage Ratio

ROA Return on Asset

ROE Return on Equity

51

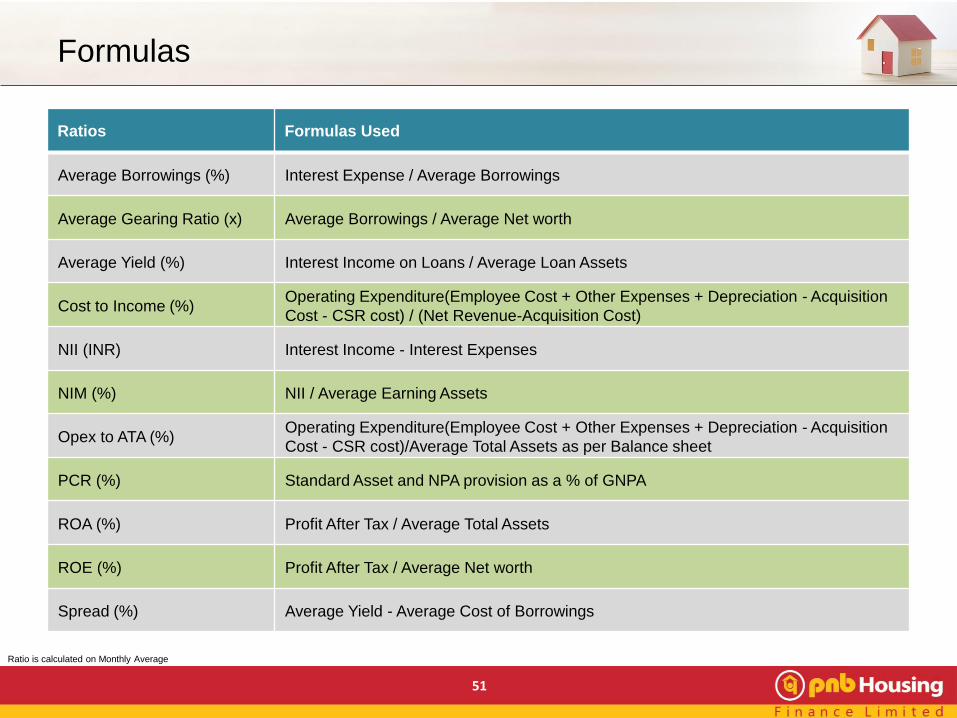

Formulas

Ratios Formulas Used

Average Borrowings (%) Interest Expense / Average Borrowings

Average Gearing Ratio (x) Average Borrowings / Average Net worth

Average Yield (%) Interest Income on Loans / Average Loan Assets

Cost to Income (%)Operating Expenditure(Employee Cost + Other Expenses + Depreciation - Acquisition

Cost - CSR cost) / (Net Revenue-Acquisition Cost)

NII (INR) Interest Income - Interest Expenses

NIM (%) NII / Average Earning Assets

Opex to ATA (%)Operating Expenditure(Employee Cost + Other Expenses + Depreciation - Acquisition

Cost - CSR cost)/Average Total Assets as per Balance sheet

PCR (%) Standard Asset and NPA provision as a % of GNPA

ROA (%) Profit After Tax / Average Total Assets

ROE (%) Profit After Tax / Average Net worth

Spread (%) Average Yield - Average Cost of Borrowings

Ratio is calculated on Monthly Average

Thank You

Company:

PNB Housing Finance Limited

CIN: L65922DL1988PLC033856

Ms. Deepika Gupta Padhi (Head-Investor Relations)

Phone: +91 11 23445214

www.pnbhousing.com