investor presentation interim results to 30 september 2009 and february 2010 update axs february...

TRANSCRIPT

Investor PresentationInterim Results to 30 September 2009

and February 2010 update

AXS February 2010

2

Disclaimer The purpose of this document is to provide general information about Accsys Technologies PLC

(“Accsys”) and its operations solely to the addressee. By accepting this document the recipient agrees to keep confidential at all times information contained in it or made available in connection with this or any further investigation. This document is for the exclusive use of the persons to whom it is addressed and their advisers and shall not be copied or reproduced or distributed, communicated or disclosed in whole or in part by recipients to any other person nor should any other person act on it. The recipient has further agreed, on request, to return all documents and other material, including this document, received from Accsys.

The information in this document has not been independently verified by Accsys. Except in the case of fraudulent misrepresentation, no responsibility, liability or obligation is accepted by Accsys or by any of its officers, employees, advisers or agents as to or in relation to the accuracy or sufficiency of this document or any other written or oral information made available to any interested party or its advisers and any such liability is expressly disclaimed. In particular, but without limitation, no representation or warranty, express or implied, is given by Accsys or any of its officers, employees or agents as to the achievement or reasonableness of, and no reliance should be placed on, any projections, estimates, forecasts, targets, prospects or returns contained herein. Any projections, estimates, forecasts, targets, prospects or returns contained herein are not a reliable indicator of future performance. Nothing in these materials should be relied upon as a promise or representation as to the future.

Accsys gives no undertaking and is under no obligation to provide the recipient with access to any additional information or to update this document or any additional information or to correct any inaccuracies in it which may become apparent, and it reserves the right, without giving reasons, at any time and in any respect to amend anything described in this document.

This document does not constitute in any jurisdiction an invitation or inducement to engage in investment activities or an offer by Accsys or any of its officers, employees, advisers or agents for the sale or purchase of securities or of any of the assets, business or undertaking of Accsys. If you require any investment advice, please consult with a professional financial adviser.

Without prejudice to any liability for fraudulent misrepresentation, Accsys and each of its officers, employees, advisers and agents disclaims any liability which may arise from this document, or any other written or oral information provided in connection therewith, and any errors contained therein and/or omissions therefrom.

By accepting this document the recipient agrees to be bound by the foregoing limitations.

The Company

• We are an environmental science and technology company, focussed on the licensing and production of environmentally friendly and sustainable acetylated wood products

• AIM and Euronext Listings Accsys was admitted to trading on the London Stock

Exchange AIM market in October 2005 Accsys was admitted to trading on NYSE Euronext

Amsterdam in September 2007

• Executive Directors:

• Paul Clegg CEO (appointed 1 August 2009)Formerly CEO of Cowen International

• Kevin Wood CFO & COO (appointed 18 June 2008)Formerly DOF, Arla Foods (Express Dairies)

3

4

wood without compromise

Financials

5

Six Months Ended 30 Sept 2009

Financial Highlights

• Revenue of €9.3 million (2008: €17.9 million) and a pre-tax loss of €8.0 million (2008: profit of €0.2 million) in the period

• Restructuring costs of €0.9 million, reducing headcount from 126 to 102

• Net cash position of €9.5 million (2008: €29.6m)

Operational Highlights

• Paul Clegg appointed as CEO

• Willy Paterson-Brown to assume the role of non-executive Chairman

• Additional distribution agreements including Universal Forest Products Inc, making a total of 12 distribution agreements and 2 agency agreements

• Further improvements to Arnhem facility including automation of wood handling systems

• First test runs of Tricoya ® MDF produced

6

Financial Overview

• Accoya Sales up 17% (up 51% in Q1 but down 12% in Q2 due to plant shutdown)

• Manufacturing sales down 6% due to by-product sales in prior period

• Licensing Income down 61% to €5.4m

• One off loss on disposal of fixed assets of €0.7m

• One off restructuring costs of €0.9m to implement headcount reductions (Ongoing Cost savings of €2.4m expected in H2)

• Loss from operations of €7.8m (€0.5m in 2008) due to timing of licensing income

• No further recognition of potential deferred tax asset (€2.4m for the period)

Six Months Ended 30 Sept 2009

7

Statement of Comprehensive Income

Unaudited Unaudited Audited6 months 6 months Year

ended ended ended30 Sept 30 Sept 31 March

2009 2008 2009€’000 €’000 €’000

Revenue 9,330 17,867 31,191 Cost of sales (7,292) (10,902) (20,209)

Gross profit 2,038 6,965 10,982

Administrative expenses before restructuring costs (8,956) (7,420) (18,292)Restructuring costs (878) - -

Total Administrative expenses (9,834) (7,420) (18,292)Other income - - 8,290

(Loss)/ Profit from operations (7,796) (456) 980

Finance income 14 690 923 Finance expense (246) - (82)

(Loss)/ Profit before taxation (8,028) 234 1,821

Tax (expense)/credit (294) (106) 3,608

(8,322) 128 5,429

Basic earnings per ordinary share €(0.05) € 0.00 €0.03

Diluted earnings per ordinary share €(0.05) € 0.00 €0.03

(Loss)/ Profit for the period andtotal comprehensive income

8

Segmental AnalysisLicensing Manufacturing Total

Unaudited Unaudited Audited Unaudited Unaudited Audited Unaudited Unaudited Audited6 months 6 months Year 6 months 6 months Year 6 months 6 months Year

ended ended ended ended ended ended ended ended ended30 Sept 30 Sept 31 March 30 Sept 30 Sept 31 March 30 Sept 30 Sept 31 March

2009 2008 2009 2009 2008 2009 2009 2008 2009€’000 €’000 €’000 €'000 €'000 €'000 €'000 €'000 €'000

Revenue 5,367 13,673 22,705 3,963 4,195 8,486 9,330 17,867 31,191

Cost of sales (1,434) (3,885) (6,092) (5,858) (7,017) (14,117) (7,292) (10,902) (20,209)

Gross profit/ (loss) 3,933 9,788 16,613 (1,894) (2,822) (5,632) 2,038 6,965 10,982

Administrative expenses before restructuring costs

(4,789) (5,061) (11,515) (4,167) (2,359) (6,776) (8,956) (7,420) (18,292)

Restructuring costs (792) - - (86) - - (878) - -

Total Administrative expenses (5,581) (5,061) (11,515) (4,253) (2,359) (6,776) (9,834) (7,420) (18,292)Other income - - 8,290 - - - - - 8,290

(Loss)/ profit from operations (1,649) 4,726 13,388 (6,147) (5,181) (12,408) (7,796) (455) 980

Finance income 14 690 923 Finance expense (246) - (82)

(Loss)/ profit before taxation (8,028) 235 1,821

Analysis of Revenue by geographical area Unaudited Unaudited Audited6 months 6 months Year

ended ended ended30 Sept 30 Sept 31 March

2009 2008 2009€'000 €'000 €'000

Europe 2,714 4,035 6,624 Asia 6,334 13,832 24,476 North America 282 - 91

9,330 17,867 31,191

9

Balance SheetUnaudited Unaudited Audited6 months 6 months Year

ended ended ended30 Sept 30 Sept 31 March

2009 2008 2009€’000 €’000 €’000

Non-current assetsIntangible assets 7,720 7,984 7,852 Property, plant and equipment 27,998 27,227 28,013 Available for sale investments 10,000 6,000 6,000 Deferred tax 2,371 - 2,630 Trade receivables 3,200 - 6,400

51,289 41,211 50,895 Current assetsInventories 3,767 6,838 4,888 Trade and other receivables 41,217 46,938 42,185 Cash and cash equivalents 9,512 29,580 17,503

54,496 83,356 64,576

Current liabilitiesTrade and other payables 20,878 36,564 23,004 Corporation tax 107 1,471 128

20,985 38,035 23,132

Net Current assets 33,512 45,321 41,444

Total net assets 84,800 86,532 92,339

Equity and reserves Share capital - Ordinary shares 1,564 1,556 1,556 Share premium account 78,726 78,191 78,191 Capital redemption reserve 148 148 148 Warrants reserve 82 - 82 Merger relief reserve 106,707 106,707 106,707 Retained earnings (102,427) (100,070) (94,345)

Equity attributable to equity holders of the parent 84,800 86,532 92,339

10

Statement of Cash flowUnaudited Unaudited Audited6 months 6 months Year

ended ended ended30 Sept 30 Sept 31 March

2009 2008 2009€’000 €’000 €’000

Profit before taxation (8,028) 129 1,821 Adjustments for:Amortisation of intangible assets 132 132 264 Depreciation of property, plant and equipment 740 728 1,572 Loss on disposal of property, plant and equipment 658 - - Finance expense/(income) 232 (690) (923)

Equity-settled share-based payment expenses 240 380 804

Equity-settled warrant expenses - - 82

(6,026) 679 3,620

Decrease/(Increase) in trade and other receivables 4,168 (41,838) (43,485)

Decrease/(Increase) in inventories 1,122 (1,906) 44

(Decrease)/Increase in trade and other payables (7,759) 27,940 19,533

Cash absorbed by operating activities (8,495) (15,125) (20,288)

Tax paid (56) - (258)

Net cashflows from operating activities (8,551) (15,125) (20,546)

Cash flows from investing activitiesInterest received 14 690 923 Purchase of available for sale investments (2,000) - - Disposal of property, plant and equipment 2 - - Purchase of property, plant and equipment (1,753) (786) (7,676)

Net cash from investing activities (3,737) (96) (6,753)

Cashflows from financing activitiesProceeds from loans 4,000 - - Finance expenses (246) - - Dividends paid - (1,553) (1,553)Proceeds from issue of share capital 556 115 118 Share issue costs (13) - -

Buyback cost for deferred shares - - (2)

Net cash from financing activities 4,297 (1,438) (1,437)

Net decrease in cash and cash equivalents (7,991) (16,659) (28,736)Opening cash and cash equivalents 17,503 46,239 46,239

Closing cash and cash equivalents 9,512 29,580 17,503

Cash flows from operating activities before changes in working capital

11

Cash Position

Unqualified Accountant’s Review but with ‘Emphasis of Matter’ on going concern in the same format as the Auditor’s Report as at 31 March 2009.

Cash of €9.5m at 30 September 2009

• Convertible debt of €4m (now converted under the same terms as €16.9m of new funds raised.

• Additional cash expected to be raised from sale and leaseback of land in Arnhem in 2010/11.

• The net cash burn continues to improve following restructuring in H1 2009/10:

H1 2008/9 H2 2008/9 H1 2009/10

€16m €12m €8m

February 2010 update

12

• Sales volumes of Accoya® wood increased by 36% in four months to January 2010 compared to the same period in the previous year.

• Arnhem facility continues to benefit from process improvements in 2009. Further process improvements are being planned with target of Arnhem facility generating positive cash-flows.

• Eleven new agency and distribution agreements signed since 1 October 2009.

• Increased interest from companies around the globe looking to explore the possibilities of licensing our technologies.

• New funds of €16.9m raised by subscription of new shares on 10 February 2010.

• Diamond Wood fund raising process ongoing.

13

wood without compromise

Strategy

Management

CEOPaul Clegg

Sales & Business

DevelopmentHal

Stebbins

MarketingStuart

Greenfield

Global Projects & BD (Panel)

Michel Maes

Technology Centre

TBA

Global Projects(Solid Wood)

Rombout van

Herwijnen

Finance /Operations

Kevin Wood

Legal / HRAdrian

Wyn-Griffiths

PA / Office ManagerCatherine Dewsbery

R&D Engineering

14

The cumulative knowledge and Intellectual Property (IP) that we own lie at the very heart of our continuing success. The protection and ongoing development of our technology and the ability to deliver the highest possible levels of support to our customers, partners and licensees is critical.

The Accoya® Technology Centre will bring together R&D, Global Projects (licensing), Engineering, Technical Support and our core IP, enabling better communication and synergies between these functions in order that we can maintain our world leadership in the development of high technology wood solutions.

The ACCOYA ® Technology Centre is our knowledge hub and asset

resource

15

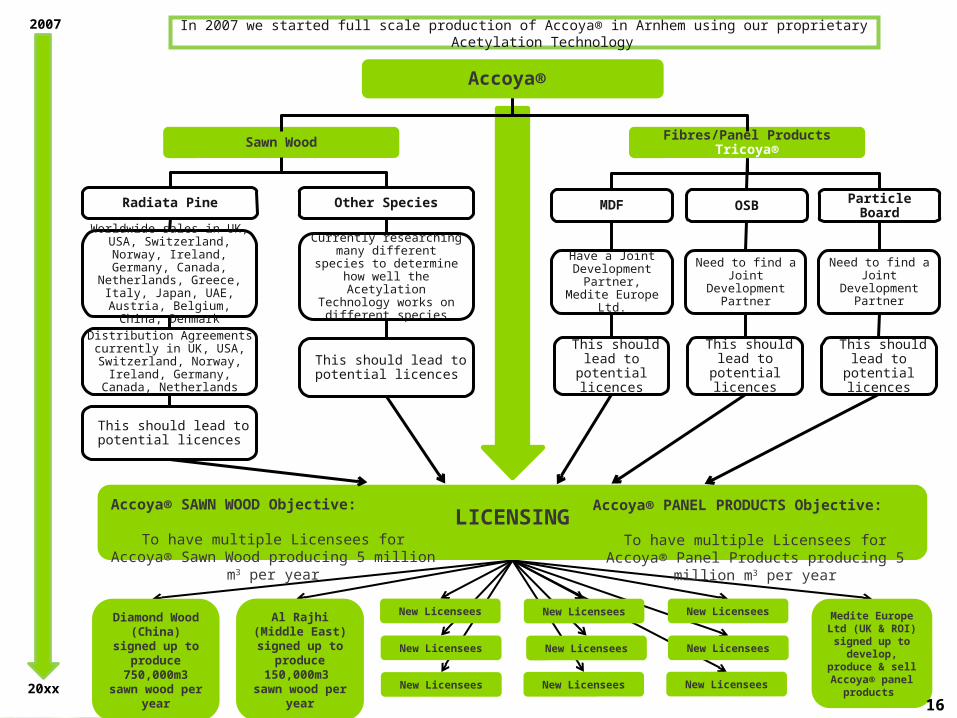

In 2007 we started full scale production of Accoya® in Arnhem using our proprietary Acetylation Technology

2007

20xx

Accoya®

LICENSING

MDF

Have a Joint Development

Partner, Medite Europe Ltd.

OSB

Need to find a Joint

Development Partner

This should lead to

potential licences

Particle Board

Need to find a Joint

Development Partner

Fibres/Panel Products Tricoya®

This should lead to

potential licences

This should lead to

potential licences

Worldwide sales in UK, USA, Switzerland, Norway, Ireland, Germany, Canada, Netherlands, Greece, Italy,

Japan, UAE, Austria, Belgium, China, Denmark

Distribution Agreements currently in UK, USA, Switzerland, Norway,

Ireland, Germany, Canada, Netherlands

Sawn Wood

Radiata Pine Other Species

Currently researching many different species to determine how well the Acetylation Technology

works on different species

This should lead to potential licences

This should lead to potential licences

Diamond Wood (China) signed up to

produce 750,000m3 sawn wood

per year

Al Rajhi (Middle East) signed up to

produce 150,000m3 sawn wood

per year

New Licensees New LicenseesNew Licensees Medite Europe Ltd (UK & ROI) signed up to

develop, produce & sell Accoya® panel

products New Licensees New Licensees

New Licensees

New Licensees

New Licensees New Licensees

Accoya® SAWN WOOD Objective:

To have multiple Licensees for Accoya® Sawn Wood producing 5 million m3 per year

Accoya® PANEL PRODUCTS Objective:

To have multiple Licensees for Accoya® Panel Products producing 5 million m3 per

year

16

Species Development

17

PHASE I: Screening Criteria

• Durability <Class 2 • Density <=750 kg/m³• Treatability <=2,1• Sapwood width > 1• Availability = „+“• IUCN rating

PHASE II: Properties:- MOE - Drying- MOR - Quality- Janka - Extractives- Density- Workability factor

- processability - glueability - paintability

PHASE III: 20 species selected for further testing based on market size/application potential and appearance, as well as the criteria above

• Accoya® wood is currently only produced from Radiata Pine (New Zealand & Chile)

• Acetylation of indigenous species is important for progressing licensing opportunities

18

Accoya® Panel Products

Sustainably forested, low value wood chips, fibres or particles

Patented manufacturing process

High performance Tricoya® wood elements forMDF, OSB and other wood composites

• Joint Development Agreement with Medite Europe Ltd

• Medite to provide all capital investment in process plant

• Income generation expected circa 2011

Technology that will target the substantial wood-based composites market

19

Investment Highlights

• Validated technologies with proven tangible benefits

• High quality product with positive environmental attributes

• High margin/low capital employed business model

• Full scale production plant in operation

• Large volume scalability on a worldwide basis

• Building global sales

• First licence agreements signed

• New products under development

20

wood without compromise

Background

21

The Company

• An environmental science and technology company.

• Develops and commercialises transformational technologies based on the acetylation of solid wood and wood elements.

• Principal functions:• Accoya® wood production and sales• Technology licensing• Development of Tricoya® wood elements technology • New product development and testing

• The Company’s technologies and brands are internationally protected by patents and trademarks.

• Our technologies not only enable us to manufacture wood products that offer ‘best in class’ durability, dimensional stability and a wide range of environmental advantages over alternative products, but also provide attractive opportunities for licensees and our other stakeholders.

22

The Wood Industry is Changing

• Restrictions on chemical treatments

• Sustainable forest management and certification increasingly important (FSC, PEFC, etc.)

• Alternative materials gaining market share

• Quality sacrificed for environment, cost or easy option

• No longer a large supply of quality tropical timbers/hardwoods

• Reliability of supply, sustainability, legislation and cost issues

• Environmental issues for hardwoods and chemically treated softwoods

23

Recent Regulatory Trends

EU Tightens Myanmar Timber Ban

The EU’s new regulation (194/2008) tightens sanctions on imported Myanmar timber imported directly or via other countries. The regulation, which took effect on 10 March 2008, supercedes a previous regulation on Myanmar sanctions from 2006. While teak logs and lumber are the main products mentioned in the new regulation, ‘sawlogs and veneer logs, lumber, planed products, wood-based panels, veneer and wooden furniture’ are also restricted.

Tropical Timber Market Report 15 April 2008

Penalties to be Raised Under US-Peru FTA

Early this year, an American delegation composed of environment and intellectual property specialists visited Peru twice to monitor progress on its forest policy development. American officials were interested in implementation arrangements under the US-Peru Free Trade Agreement (FTA), which was signed in 2007. During the visit, the Peruvian Foreign Commerce Ministry and Coordinator, Silvia Hooker, noted that policy reform measures were being undertaken to increase penalties for those who participate in illegal logging.

Tropical Timber Market Report 31 March 2008

Commission Recommends Congo Cancel Majority of Logging Contracts

A government sponsored World Bank review of timber contracts in the Democratic Republic of Congo reported on Wednesday that the nation should withdraw more than 75 per cent of its logging deals for not meeting standards. The review was an attempt to recover millions of dollars in lost tax revenue and set the corruption-prone business straight.

RedOrbit 7 August 2008

Updated Lacey Act Becomes World’s

First Ban on Illegal Logging

New amendments added to the Lacey Act aim to cut down on illegal logging. Penalties range from $250 to in excess of $500,000 with a possibility of jail sentence for knowingly sourcing, or failing to exercise due care when sourcing, products that contain illegal timber or plants.

Furniture Today 24 June 2008

Recent Retail Trends

IKEA

IKEA is the world’s third largest wood buyer. It has recently tightened up the procurement procedures that it demands of subcontractors. IKEA´s long term goal is to source all of its wood from sustainably managed forests verified by an independent third party. Currently, FSC is the only certification system recognised by IKEA.

Wal-Mart

Wal-Mart has joined the GFTN. Wal-Mart announced that through this initiative they will be phasing out illegal and unwanted wood sources from its supply chain and increasing its proportion of wood products originating from credibly certified sources. Within one year, Wal-Mart will complete an assessment of where its wood furniture is coming from and whether the wood is legal and well-managed. Once the assessment is completed, Wal-Mart has committed to eliminating wood from illegal and unknown sources within five years. The company will also eliminate wood from forests that are of critical importance due to their environmental, socio-economic, biodiversity or landscape values and that are not well-managed.

The Home Depot

The Home Depot is the world's leading wood buyer and the first major home improvement retailer in the USA to adopt the FSC principles. The Home Depot is a member of the Certified Forest Products Council (CFPC) - a US based certification organization that works in partnership with FSC - and a member of the Global Forest and Trade Network (GFTN). Lowe’s

Following in the footsteps of The Home Depot, Lowe's, the world’s second largest wood buyer, adopted the FSC principles. Lowe's is a member of the CFPC and a member of the GFTN.

24

25

Greenhouse Gas Emissions per m3/(424 Board Feet)

The calculated associated GHG emissions per m3 of Accoya® wood have been compared to materials that Accoya® wood can replace.

Source: Camco Greenhouse Gas Emissions Assessment for Accoya® Wood, March 2009

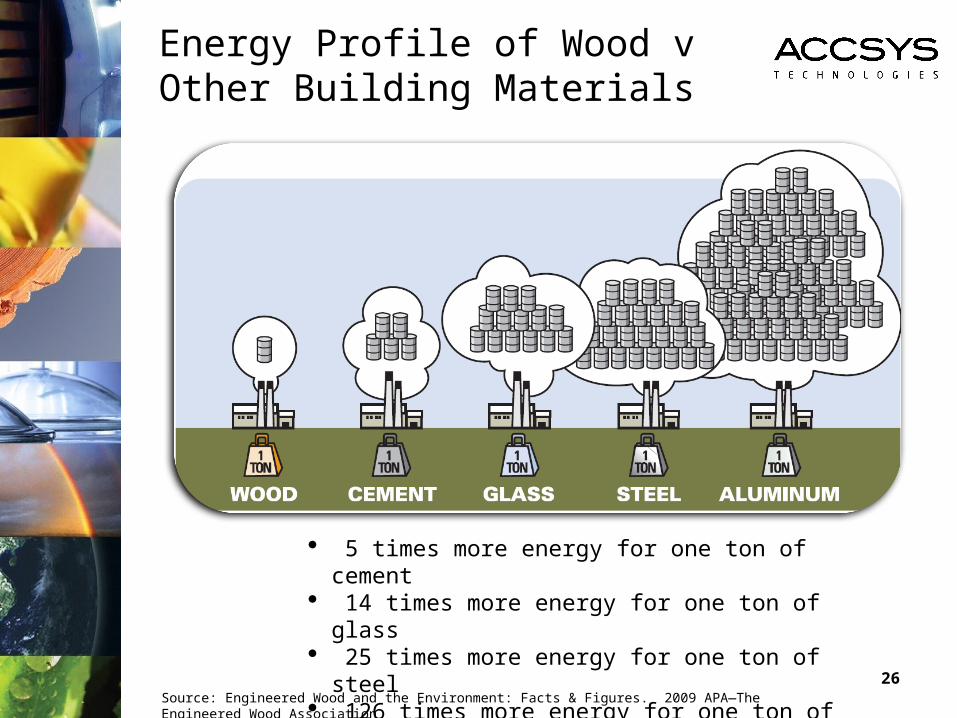

Energy Profile of Wood vOther Building Materials

5 times more energy for one ton of cement 14 times more energy for one ton of glass 25 times more energy for one ton of steel 126 times more energy for one ton of

aluminum

Source: Engineered Wood and the Environment: Facts & Figures. 2009 APA—The Engineered Wood Association

26

27

The Acetylation Process

• The improved properties are created by altering the chemistry of the wood, not by impregnation of biocides / water repellents

• No disposal or production hazards and costs• No challenges for coatings – in fact, coating is easier

• The Accoya® wood production process is irreversible • No risk of chemical leaching / loss• Wood is uniformly modified throughout, it is not a

surface treatment• Permanent improvement in performance

• Acetylation changes wood at the molecular level

28

The Commercial Production of Accoya® Wood

Sustainably forested, low value wood

Patented manufacturing process

High performance Accoya® wood

29

• The world’s first commercial production plant, opened March 2007 in Arnhem, The Netherlands

• Initial nameplate capacity of 30,000 m3, increased to 40,000 m3 in 2009 following a series of process improvements

• Arnhem Facility has three main functions: • Accoya® wood production for market development• Demonstration and training• Product development and testing

• Wood certification agencies and research institutes actively supported and assisted in commercial development

Full Scale Production Plant

30

High Performance Wood for Exterior Applications

claddingwindows

decking

furniture

doors

shutters &

shading

civil engineering

soffits

flooring

31

Tangible Benefits of Accoya® Wood

Outstanding dimensional stability: improved hardnessClass 1 durability – the best available

≥50 yrs above & ≥25 yrs in-ground/fresh H20 contactEasy to machine and manually process

Superior resistance to UV degradation

Retained natural strength and beauty

Coatings last 3-4 times longer = cost benefit

Highly improved thermal insulation

Non-toxic

Consistent supply from sustainable, certified sources

Consistent measurable quality, surface to core

100% recyclableNaturally renewable

Improved mould & insect resistance

32

Tried & Tested

Coatings after 9.5 years

Extended coatings guarantees for windows and doors

Coatings after 5.5 years

Accoya® Licence – Sawn Wood

Licence Option Agreement

• Reserves territory

• 6/12 month exclusivity

• Option fee of €1 per m³ of licensed capacity, payable on signing

Licence Agreement

• Exclusive manufacturing rights in the territory

• 10% of Technology fee payable on signing

• Technology fee is €200 per m³ of licensed capacity

Plant Build out

• 1-2 year estimated build out period

• Remainder of Technology fee paid out evenly over this period

Start of Production

• Royalty fee payments begin after plant completion

• €22 per m³ produced subject to RPI indexation

Capital

• Approx €512 per m³ - based on 80,000m³ capacity plant

• Excludes cost of Land and Licence fee

IRR

• Range of between 20–39% return

• Cost assumptions used for IRR calculations vary significantly depending on region and location of plant

Potential Cost Reduction Options

• Onsite ANH production using recycled ACA from the acetylation process

• Synergies with existing facilities

• Availability of Economic Development Benefits

33

34

Accoya® Wood Strategy

• The strategy is focused on maximising the global use of Accoya®

• Follow an asset light model through development of large scale licensing of our technology – high margin, low capital employed business model

• Actively developing large scale potential demand for Accoya® by working with selected partners to generate demand and supplying through appointed distributors

• Testing and development of additional wood species for acetylation

• Final demand > distribution > licences

35

Large Volume Scalability on a Worldwide Basis

• Abundant availability of the raw material for acetylation, with Accoya® wood being best produced using species from well managed, sustainable sources

• Global annual production of wood products exceeds 3 billion m3

• The market for solid wood is 600 million m3 per year

• Accoya® wood is anticipated to capture market share in those applications that involve exterior use

• Total market volume in the applications most relevant to Accoya® wood is conservatively estimated to be 120 to 150 million m3. This represents c.€100 billion worldwide market

• Given Accoya® wood’s superior performance and the increasing demand for non-toxic, sustainable alternatives, the Company believes that total global Accoya® wood demand will be several million m3

Sales & Distribution

• Current Distribution Agreements: 12 Distribution Agreements 2 Agency Agreements 8 countries

• Sales in 17+ countries currently

• Target 30 Distribution Agreements by 2010

36

37

Licensing Agreements

• Commercial and trial materials are being supplied to customers and potential licensees worldwide from the production plant

• The 40,000m3 per annum Accoya® production plant began operations in March 2007

• Licence Agreements per cubic metre of nameplate capacity and production royalties per cubic metre for the life of the licence

• 500,000 cubic metres agreement plus 250,000 cubic metres option in China

• 150,000 cubic metres agreement in GCC (Middle East)

• Trading agreements and additional licensing options under negotiation

38

wood without compromise