investor presentation 1q 2011.ppt - metsä board results/2011... · investor presentation 1q 2011 1...

TRANSCRIPT

4.5.2011Investor presentation 1Q 20111

Contents

Investment highlights and update2 Investment Highlights3 Strategy15 Financial Targets17 1Q 2011 Results & Outlook29 Price Development31 Dividend34 InvestmentsFunding and debt information37 Divestments38 Funding and Debt45 Credit Facilities46 Rating History

General presentation47 General Info54 Business Portfolio63 Operations69 Deliveries71 Sourcing79 Owners81 Market Position

4.5.2011Investor presentation 1Q 20112

Investment Highlights

• Strong growing core in high-quality cartonboards– M-real the European market leader in folding boxboard– Good growth potential

• Material profitability turn-around in 2010

• Significant net debt reduction in recent years

• Strategic review ongoing– M-real the forerunner in paper merchanting and coated papers industry

restructuring in Europe– Asset divestments– Extensive cost savings and cash flow improvement programmes

Strategy

Investor presentation 1Q 20114

Consistent Strategic Direction Since 2006

• Cartonboards for consumer packaging the strategic core business

• Divestment of underperforming paper businesses

• Major cost savings through complexity reduction and efficiency improvement

• High pulp and energy self-sufficiency

• Customer orientation and proactive approach to increase prices Extensive restructuring programme 2006

Extension of the restructuring programme 2007

Divestment of Map Merchant Group 2007

New efficiency improvement programme 2007

Self-sufficiency in pulp 2008

Divestment of Graphic Papers 2008

Divestment of Metsä-Botnia’s Uruguayan operations 2009

Profit improvement programme 2010

New profit improvement programme 2011

Investor presentation 1Q 201155

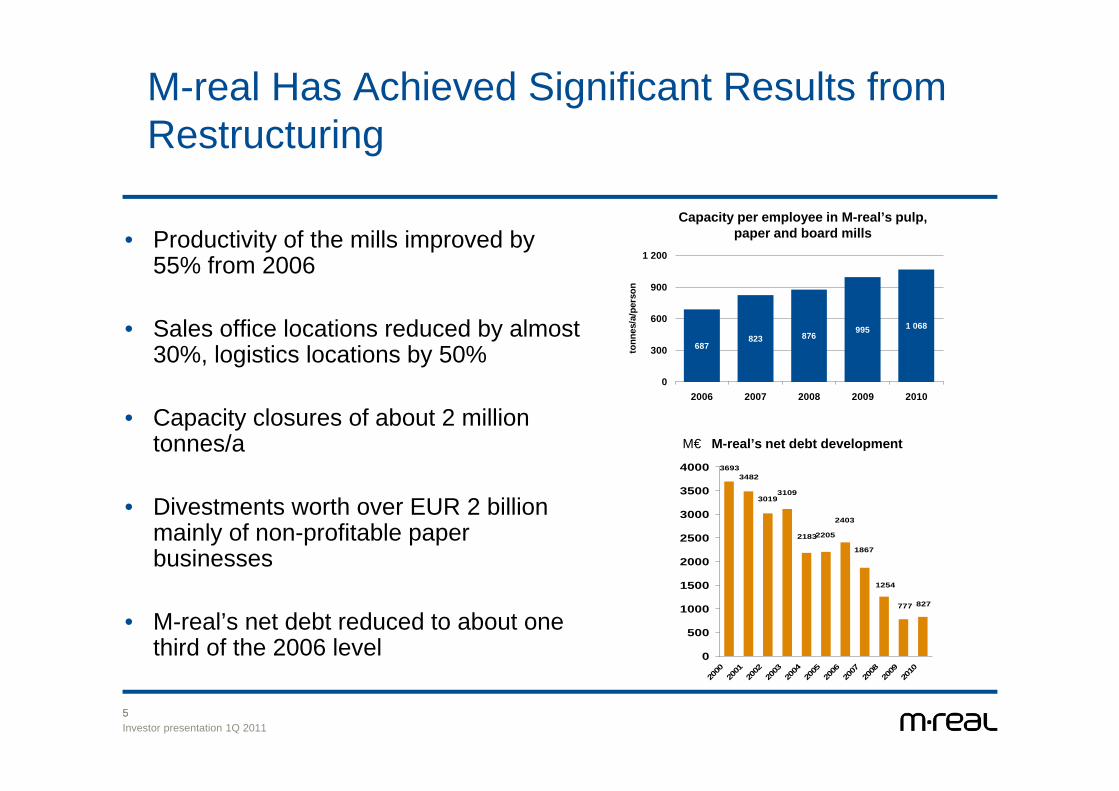

M-real Has Achieved Significant Results from Restructuring

• Productivity of the mills improved by 55% from 2006

• Sales office locations reduced by almost 30%, logistics locations by 50%

• Capacity closures of about 2 million tonnes/a

• Divestments worth over EUR 2 billion mainly of non-profitable paper businesses

• M-real’s net debt reduced to about one third of the 2006 level

687823

1 068995876

0

300

600

900

1 200

2006 2007 2008 2009 2010

tonn

es/a

/per

son

Capacity per employee in M-real’s pulp, paper and board mills

827777

1254

2183

31093019

34823693

2205

2403

1867

0

500

1000

1500

2000

2500

3000

3500

4000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

M-real’s net debt developmentM€

6

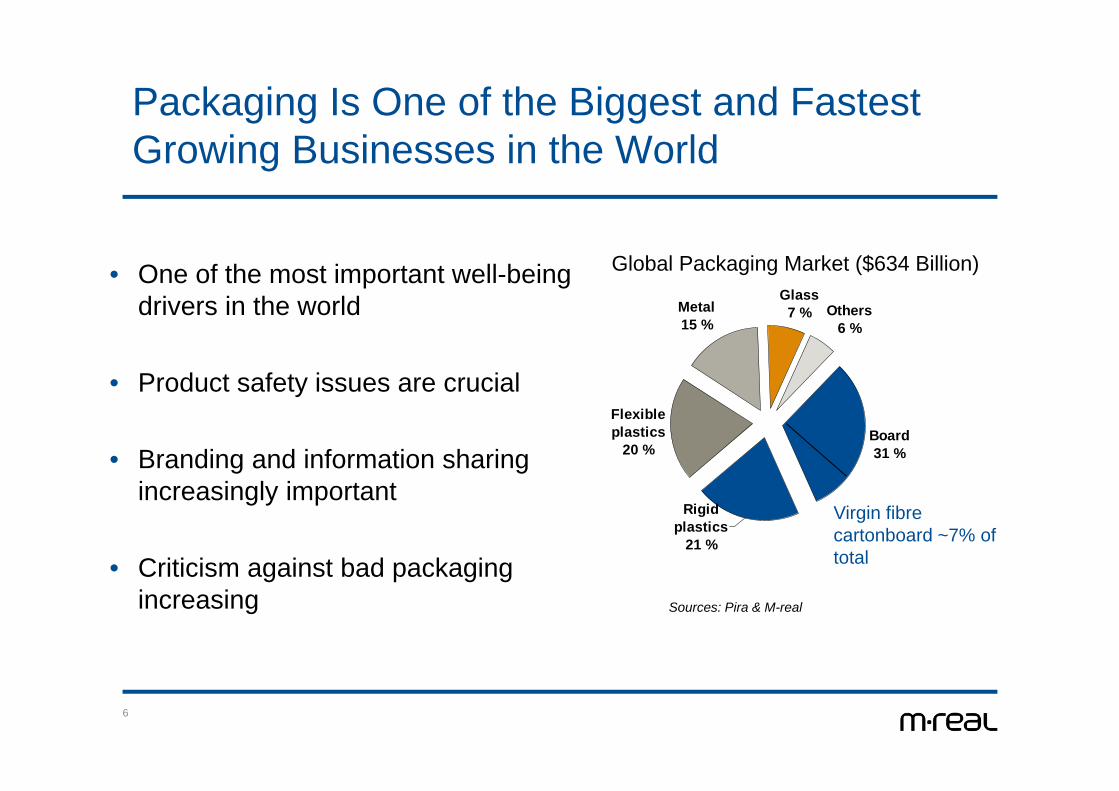

Packaging Is One of the Biggest and Fastest Growing Businesses in the World

• One of the most important well-being drivers in the world

• Product safety issues are crucial

• Branding and information sharing increasingly important

• Criticism against bad packaging increasing

Flexible plastics

20 %

Metal15 %

Glass7 % Others

6 %

Board31 %

Rigid plastics

21 %

Sources: Pira & M-real

Global Packaging Market ($634 Billion)

Virgin fibre cartonboard ~7% of total

Investor presentation 1Q 20117

Several Megatrends Supporting Good Packaging

• Demand for good packaging heavily increasing

• Good packaging is environmentally sustainable– Made out of renewable raw material and recyclable– High energy self-sufficiency in production– Low carbon footprint– Lightweight

• Good packaging is safe– Durable– No migration– Good printing surface

• Good packaging is economical

2.3.2011Investor presentation 1Q 20118

Virgin Fibre Board Is the Best Example of Good Packaging – Lowest Carbon Footprint

• Virgin fibre based lightweight cartonboards the most environmentally sound packaging material

• Wood fibre based products replace non-renewable materials like plastic and aluminium

• Virgin fibre board replaces also recycled fibre based packaging materials

0

2000

4000

6000

8000

10000

12000

14000

M-real's CartaSolida

HDPE PET PLA (Biobasedpolymer)

Aluminium

kg/to

nne

Source: M-real and Sustainable Packaging Coalition - SPC

Cartonboard has the lowest carbon footprint

2.3.2011Investor presentation 1Q 20119

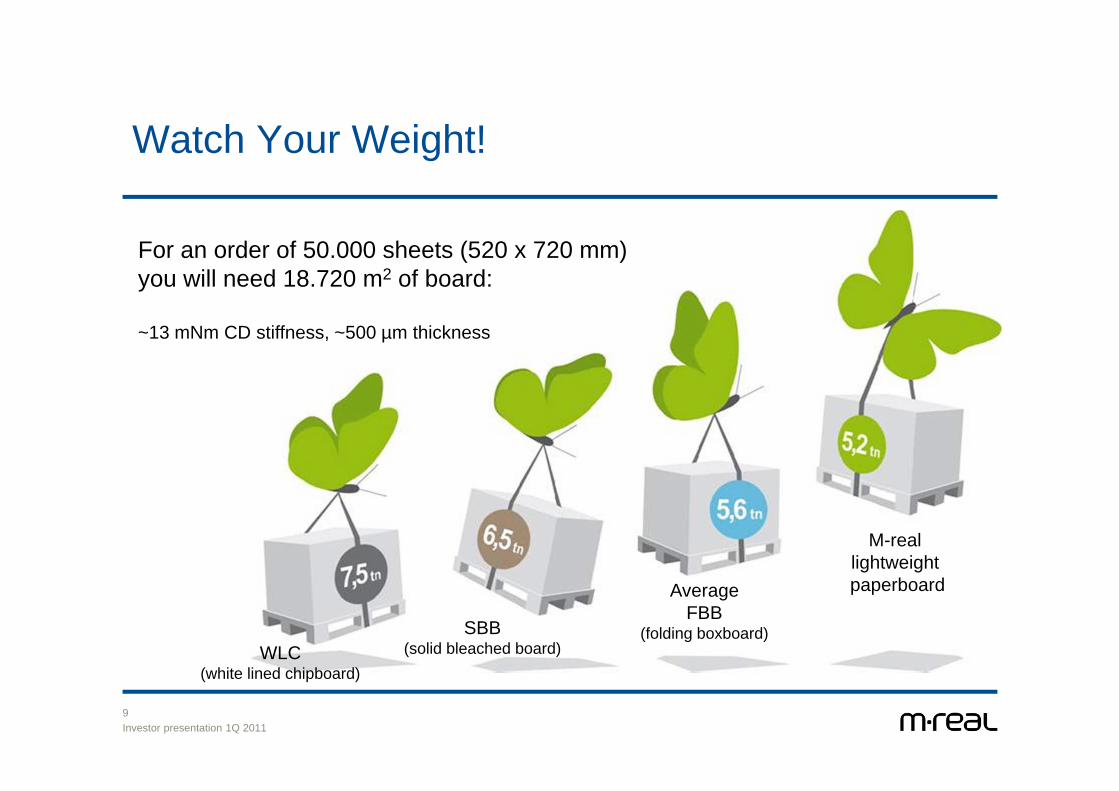

Watch Your Weight!

For an order of 50.000 sheets (520 x 720 mm) you will need 18.720 m2 of board:

~13 mNm CD stiffness, ~500 µm thickness

M-real lightweight paperboardAverage

FBB(folding boxboard)SBB

(solid bleached board)WLC(white lined chipboard)

2.3.2011Investor presentation 1Q 201110

M-real Targets Growth in Its Core Business Packaging

• Huge growth potential in wood fibre based packaging applications when replacing non-sustainable packaging materials

• M-real a strong producer of virgin fibre based cartonboard and white top linerboard as well as packaging related speciality papers

• Access to wood raw material, superior fibre knowhow and pulp self-sufficiency M-real’s important competitive advantages

2.3.2011Investor presentation 1Q 201111

M-real is Investing in Its Cartonboard Business

• 26 m€ investment in 80 kton/a capacity expansion at Simpele

• 16 m€ investment in Kemiart Liners to increase the share of coated products

• M-real invests 30 m€ to expand capacity annually by approximately

70.000 tonnes at Äänekoski and Kyröskoski

– Potential to further increase capacity of existing mills by some 70.000 t/a

• Evaluations regarding further development steps in cartonboard

business continue

2.3.2011Investor presentation 1Q 201112

M-real Strategic Review- M-real’s Response to the Changes in Business Environment

• In March 2006, M-real's Board of Directors initiated a strategic review

• M-real was the first major paper company to emphasize the need for industry consolidation and extensive restructuring

• M-real took the leading role in European paper merchanting restructuring in 2007

• M-real also took the leading role in European coated paper industry restructuring in 2008

• Extensive internal profit improvement programmes

2.3.2011Investor presentation 1Q 201113

Strategic Review of the Paper Business Proceeds

• M-real in strong position in participating restructuring of the European uncoated fine paper business

• M-real Zanders is a leading European speciality paper producer

• Potentially, also separate divestments of the non-profitable units

2.3.2011Investor presentation 1Q 201114

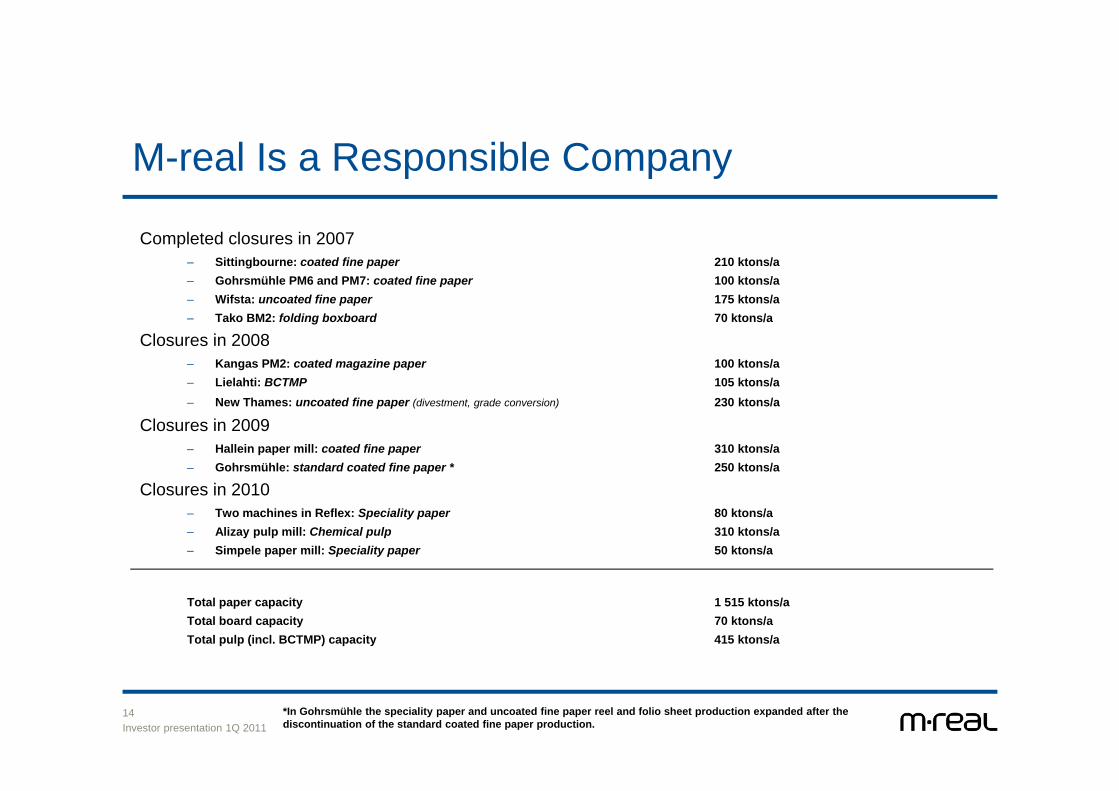

M-real Is a Responsible Company

Completed closures in 2007– Sittingbourne: coated fine paper 210 ktons/a– Gohrsmühle PM6 and PM7: coated fine paper 100 ktons/a– Wifsta: uncoated fine paper 175 ktons/a– Tako BM2: folding boxboard 70 ktons/a

Closures in 2008– Kangas PM2: coated magazine paper 100 ktons/a – Lielahti: BCTMP 105 ktons/a – New Thames: uncoated fine paper (divestment, grade conversion) 230 ktons/a

Closures in 2009– Hallein paper mill: coated fine paper 310 ktons/a – Gohrsmühle: standard coated fine paper * 250 ktons/a

Closures in 2010– Two machines in Reflex: Speciality paper 80 ktons/a– Alizay pulp mill: Chemical pulp 310 ktons/a– Simpele paper mill: Speciality paper 50 ktons/a

Total paper capacity 1 515 ktons/a Total board capacity 70 ktons/a Total pulp (incl. BCTMP) capacity 415 ktons/a

*In Gohrsmühle the speciality paper and uncoated fine paper reel and folio sheet production expanded after the discontinuation of the standard coated fine paper production.

Financial Targets

2.3.2011Investor presentation 1Q 201116

Financial Targets

• ROCE target set at a minimum of 10% on average over the business cycle• Net gearing not to exceed 100%

Minimum ROCE 10%* Maximum net gearing 100%

* Excluding non-recurring items

184%

119%137%

82%95%

126%99%90%84%83%78%83%

145%

99 00 01 02 03 04 05 06 07 08 09 10 1Q11

Maximum level of 100%

13,5%

6,2%

2,1%1,6%0,5%0,9%2,8%

-0,5%

-5,6%

7,6%7,8%10,2%

7,6%

99 00 01 02 03 04 05 06 07 08 09 10 1Q11

Minimum target of 10%

1Q 2011 results and Outlook

1818

Key Events in 1Q 2011

• Profitability improved from previous quarter

• Consumer Packaging ’s result improved to EBIT 17 % of sales

• Impact of accelerated cost inflation bigger than earlier expected in 1Q

• Decisions to increase Äänekoski and Kyröskoski folding boxboard capacity in total by 70 000 tonnes per annum

• New 70 m€ internal profit improvement programme was launched

• Price increases announced in linerboard, uncoated fine and speciality papers

• New plans to eliminate losses of paper business announced in May

19

623 585 618 606 602 676 685665662

250

500

750

1000

I II III IV I II III IV I

Sales Operating result excl. non-rec. itemsm€ m€

m€Result before taxes excl. non-rec. items

Key Figures – Quarterly

20102009

-65 -70

-227

39 54 37 4343

-75

-50

-25

0

25

50

75

I II III IV I II III IV I

-62

24 28

-83

-15

-70

15 2033

-100-75-50-25

02550

I II III IV I II III IV I

2011

2020

• Result improved vs. 4Q 2010 due to higher prices

• Increased energy costs had a negative result impact

• Demand seems to continue strong

• Liner price increase of about 6% implemented successfully

• New FBB price increase needed due to accelerated cost inflation

• Simpele investment shutdown and maintenance shutdowns at other mills impact negatively 2Q 2011 result

EBIT, excl non-recurring itemsm€

4Q 2010 1Q 2011

Salesm€

4Q 2010 1Q 2011

Consumer Packaging Result Improved

2121

• Result was weakened vs. 4Q 2010 by higher raw material and energy costs as well as unfavourable exchange rates

• Higher average prices improved results from 4Q 2010

• Demand expected to continue stable

• M-real has pushed for price increase but with very limited success

• New Husum turbine started in April

• Alizay mill is planned to be divested or, if divestment does not materialize, closed

Office Papers Result to Improve Clearly If Losses From Alizay Eliminated as Planned

EBIT, excl non-recurring itemsm€

181 184

0

50

100

150

200Salesm€

4Q 2010 1Q 2011

4Q 2010 1Q 2011

0

2222

Speciality Papers Operations Planned to Be Mostly Divested or Clearly Downsized

• Result was weakened vs. 4Q 2010 by higher raw material costs and lower average prices due to mix issues

• Result was improved by higher delivery volumes

• Demand expected to remain stable. No material near-term price changes in sight

• Planned divestment of Gohrsmühle mill or potential closure of WFU and unprofitable speciality paper production

• Planned closure of the remaining operations in Reflex

EBIT, excl non-recurring itemsm€

Salesm€

4Q 2010 1Q 2011

4Q 2010 1Q 2011

2323

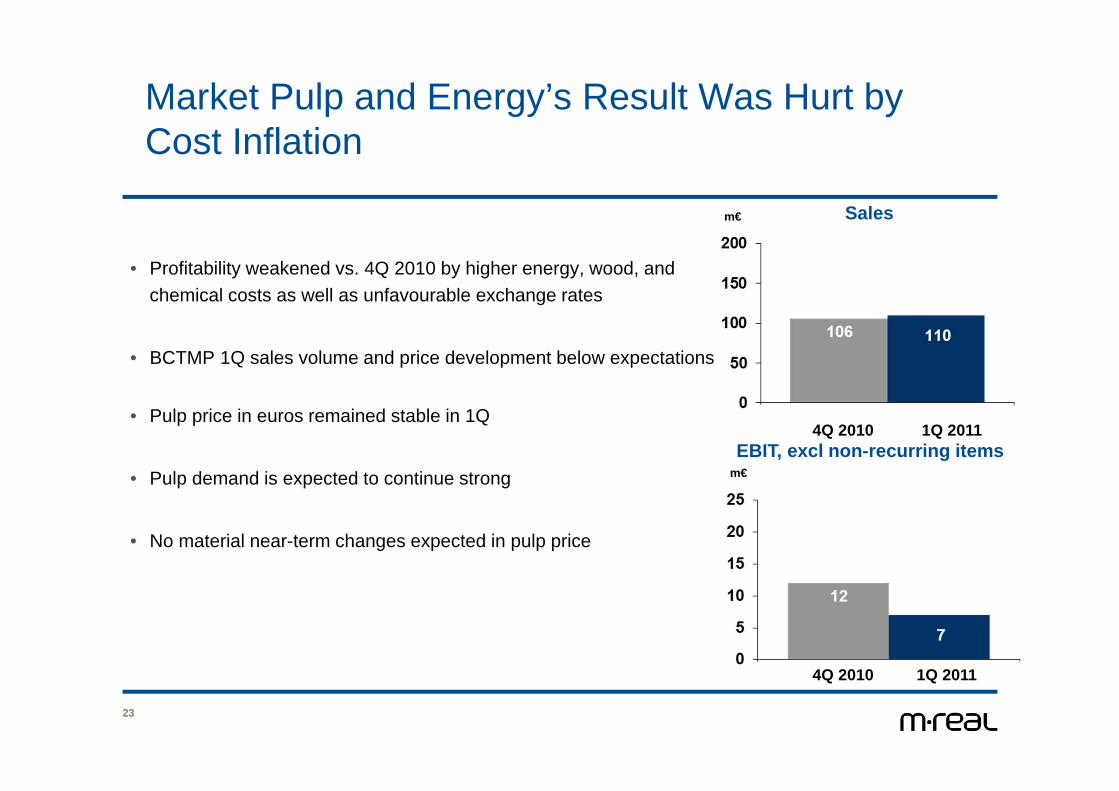

Market Pulp and Energy’s Result Was Hurt by Cost Inflation

• Profitability weakened vs. 4Q 2010 by higher energy, wood, and chemical costs as well as unfavourable exchange rates

• BCTMP 1Q sales volume and price development below expectations

• Pulp price in euros remained stable in 1Q

• Pulp demand is expected to continue strong

• No material near-term changes expected in pulp price

EBIT, excl non-recurring itemsm€

Salesm€

4Q 2010 1Q 2011

4Q 2010 1Q 2011

24

2011 Result Expected to Be Boosted by 90 m€ vs. 2010 Due to Internal Actions

Cumulative

Profit impact vs. 2010, m€total

target 2011 20121 Profit improvement programme 2011 70 30 70

2 Rollover impact of 2010 profit improvement programme 40 40 40

3 Rollover impact of older programmes 20 20 20

Total 130 90 130

M-real expects to mostly cover the accelerated cost inflation in 2011 by the profit impact of own actions

Cost inflation expected to be 4-5 % in 2011

25

Folding Boxbord Capacity Increase Investments to the Implementation Phase

• Demand growth for M-real’s ecological and safe virgin fibre board in food packaging faster than expected

• Simpele 80 000 t/a capacity increase investment to be finalized in early June 2011

• Kyröskoski 40 000t/a investment is scheduled for November 2011 and Äänekoski 30 000 t/a investment for April 2012

• M-real has still potential to further increase the cartonboard capacity at the existing mills

M-real Plans to Eliminate the Losses Generated by Its Paper Business

26

• M-real plans to divest the entire Gohrsmühle mill or alternatively parts of the mill separately based on a Paper Park concept

• If the divestment does not materialize M-real plans to close the unprofitable uncoated fine and speciality paper production at Gohrsmühle

- M-real plans to continue the production of Chromolux- label and packaging products (~50 000 t/a)

• M-real commences a public process to divest Alizay paper mill - If the divestment does not materialize by end September 2011, M-real considers closing the mill

• Reflex Premium Papers business planned to be sold and the remaining operation, carbonless paper converting, is planned to be closed

• Implementations of possible closures are subject to finalization of the consultation processes based on the local legislations

Financial Impact of the Planned Measures

27

• M-real’s annual sales would reduce by about 390 m€ and the operating result increase by about 60 m€ based on 2010 actual performances

- Most of the impact seen in 2012, full annual financial impact from 2013

• M-real’s annual paper production capacity would reduce by about 500 000 t/a

- WFU 430 000 t/a, specialities 70 000 t/a

- Amount of personnel would decrease by about 800

• Preliminarily expected negative non-recurring financial impacts about 170 m€

- Negative net cash impact about 50 m€

- Numbers will be further determined when the final decisions are taken

• Speciality Papers 2Q 2011 result to include about -20 m€ non-recurring items

28

Profitability Outlook

M-real’s 2Q 2011 operating result excluding non-recurring items is expected to

weaken slightly from 1Q 2011 due to the investment shutdown at

Simpele mill and the unfavorable exchange rate development

2.3.2011Investor presentation 1Q 201129

EUR / tn

Folding Boxboard Market Price in Europe2004 – 1Q 2011

800

900

1000

1100

2004 2005 2006 2007 2008 2009 2010 2011

Source: Pöyry Forest Industry Consulting

2.3.2011Investor presentation 1Q 201130

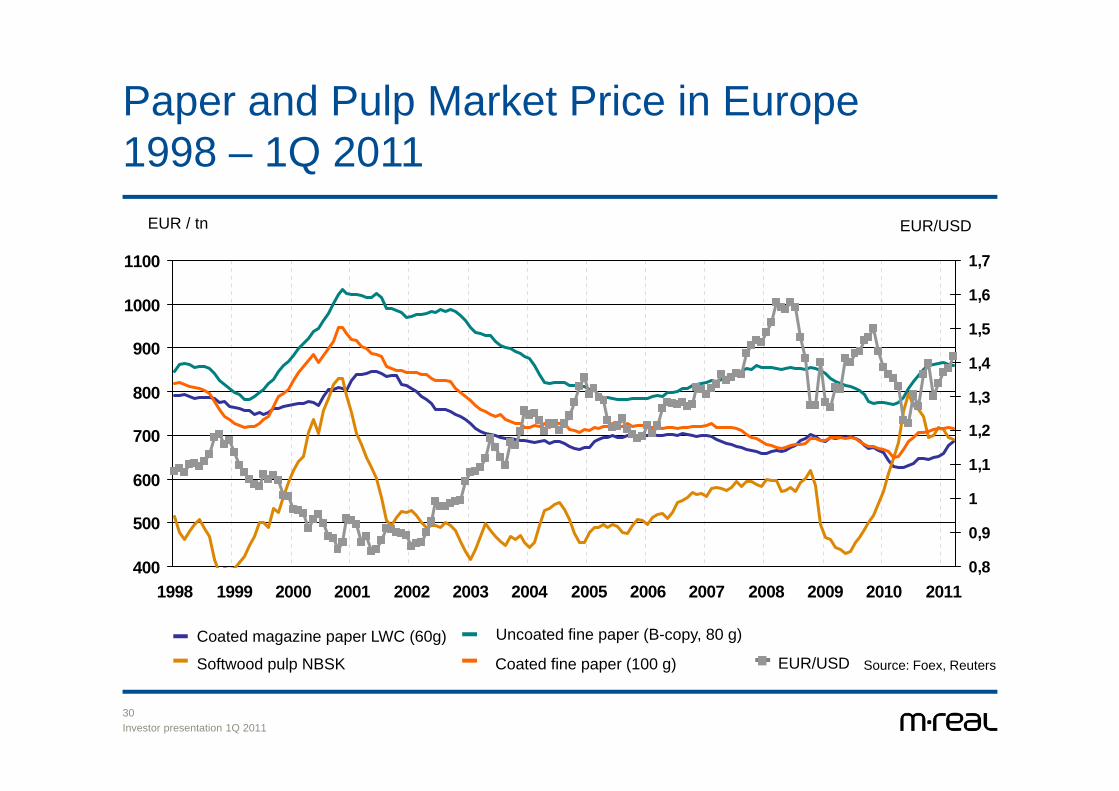

EUR / tn

Paper and Pulp Market Price in Europe1998 – 1Q 2011

Coated fine paper (100 g)

Uncoated fine paper (B-copy, 80 g)

Softwood pulp NBSK

Coated magazine paper LWC (60g)

Source: Foex, ReutersEUR/USD

EUR/USD

400

500

600

700

800

900

1000

1100

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 20110,8

0,9

1

1,1

1,2

1,3

1,4

1,5

1,6

1,7

Dividend

2.3.2011Investor presentation 1Q 201132

Dividend Policy

• Future dividends will take into account the need to achieve and maintain sufficient financial flexibility

• The Company remains committed to an attractive and competitive dividend

M-real's dividend policy is stable and rewarding to shareholders, and aims at paying a dividend of at least 1/3 of the Company's EPS on average over the business cycle, nonetheless taking into account the Company's gearing target

2.3.2011Investor presentation 1Q 201133

0,50

1,09 1,13

1,85

0,460,30

-0,79

-1,58

-1,09

0,26 0,37 0,380,51 0,51 0,51

0,25 0,00 0,00 0,000,09

-0,59

-1,21

-0,25-0,430,23 0,060,06

0,14 0,12 0,12

0,0%0,0%

4,3%

0,0%1,3%1,4%

2,1%2,8%3,3%

4,1%

5,6% 5,5%6,9%

8,6%

7,2%

-2

-1,5

-1

-0,5

0

0,5

1

1,5

2

2,5

3

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

€ pe

r sha

re

-8 %

-6 %

-4 %

-2 %

0 %

2 %

4 %

6 %

8 %

10 %

12 %

Div

iden

d yi

eld,

%

Earnings per share Dividend per share Dividend yieldDividend yield calculated from annual average B-share volume weighted price

Dividend Yield

Investments

2.3.2011Investor presentation 1Q 201135

Capital Investments

-1 500

-1 000

-500

0

500

1 000

1 500

2 000

2 500

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

E

Mill

ion

€

Disposals

Acquisitions

Capitalexpenditure onfixed assets

Capital Investments about 100 m€ in 2011

*Indicative level for 2011

Funding and debt information

2.3.2011Investor presentation 1Q 201137

Significant Divestments- EUR 3.4 billion in assets divested since 2001

2004 Metsä Tissue 570

2002 Papierfabrik Albbruck 235

2001 MD Papier 300

2001 Noviant (19%) 41

3,387

Year Divestiture Enterprise Value

EUR millions

2005 Savon Sellu 20

2005 Forestia (95%) 163

2005 Botnia (8%) 164

2007 Botnia (9%) 2402007 Folding carton plants 602007 Map Merchant Group 3822008 New Thames mill 82**2008 100 000 B2 shares in PVO 802008 Graphic Papers 750

* Cash portion

**Incl. pension liabilities

2009 Metsä-Botnia’s Uruguayn operations 300*

38

Strong Financing Situation Continues

• Current net debt 799 m€ and net gearing 78 %

• Metsä-Botnia dividend to M-real 45 m€

• Early repayment of 49 m€ vendor note by Metsäliitto

• ONWC increased by about 40 m€ in 1Q due to higher volumes and average prices as well as preparations for Simpele shutdown

• Liquid funds 418 m€ at end 1Q 2011

• Average interest rate 5.1% at end 1Q

Net Debt, m€

799827

777

1254

2183

31093019

34823693

2205

2403

1867

0

500

1000

1500

2000

2500

3000

3500

4000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

1Q 11

2.3.2011Investor presentation 1Q 201139

Loans and Interest Rate

At the end of 1Q 2011• Average maturity of long term loans 2,4 years• Average interest rate of loans (including derivatives) 5,1 %• Interest rate maturity of loans (including derivatives) 7,7 months

• Of the loans about 83 per cent was subject to variable interest rates and 17 per cent to fixed interest rates

2.3.2011Investor presentation 1Q 201140

Total 1 120 m€ 31.3.2011

Long-term Interest Bearing Liabilities

5 %5 %3 %7 %

20 %

60 %

MTN ProgrammeBondsPension premium loansLoans from financial institutionsFinance leasesOther interest bearing liabilities

2.3.2011Investor presentation 1Q 201141

Short term interest bearing liabilities

Total 162 m€ 31.3.2011

Short-term Interest Bearing Liabilities4 %

96 %

Metsäliitto GroupShort-term bank loans and other

2.3.2011Investor presentation 1Q 201142

Interest bearing net liabilities 31.12.2003Interest Bearing Net Liabilities 31.3.2011 (m€)

• Long-term 1 120• Short-term 162Total interest bearing liabilities 1 282

• Liquidity and other interest bearing receivables 483

• Interest bearing net liabilities 799

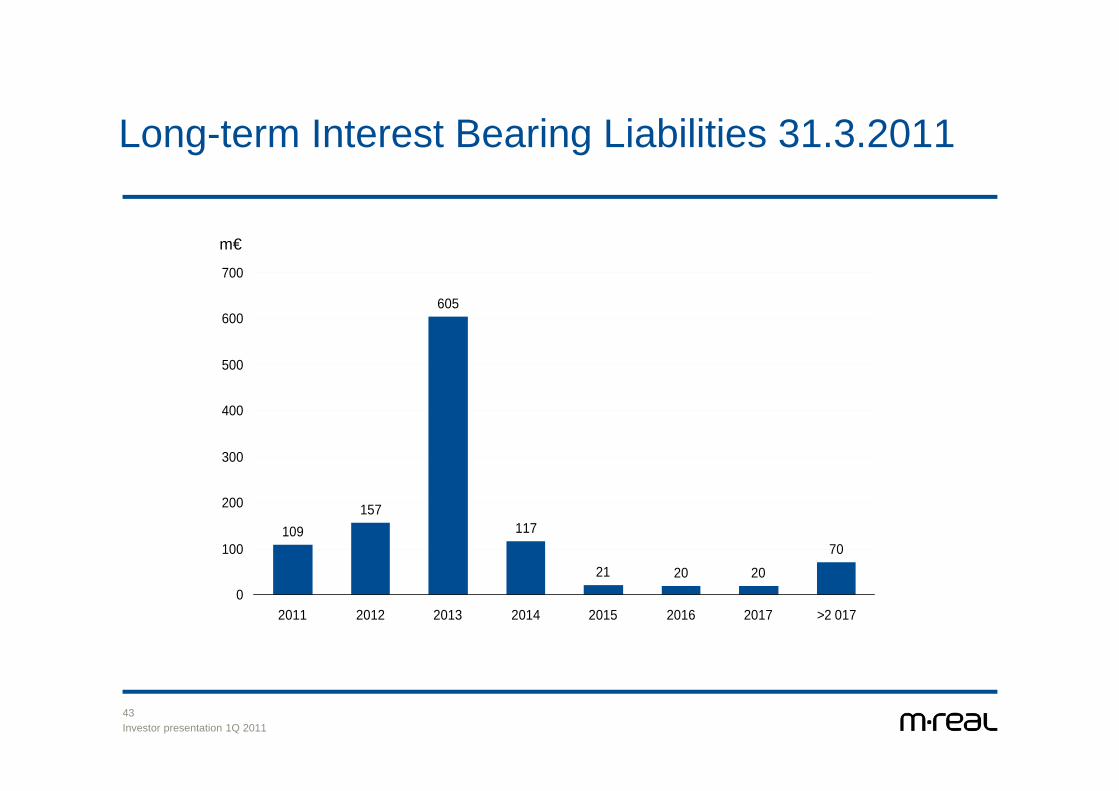

2.3.2011Investor presentation 1Q 201143

Long-term Interest Bearing Liabilities 31.3.2011

109157

605

117

21 20 20

70

0

100

200

300

400

500

600

700

2011 2012 2013 2014 2015 2016 2017 >2 017

m€

2.3.2011Investor presentation 1Q 201144

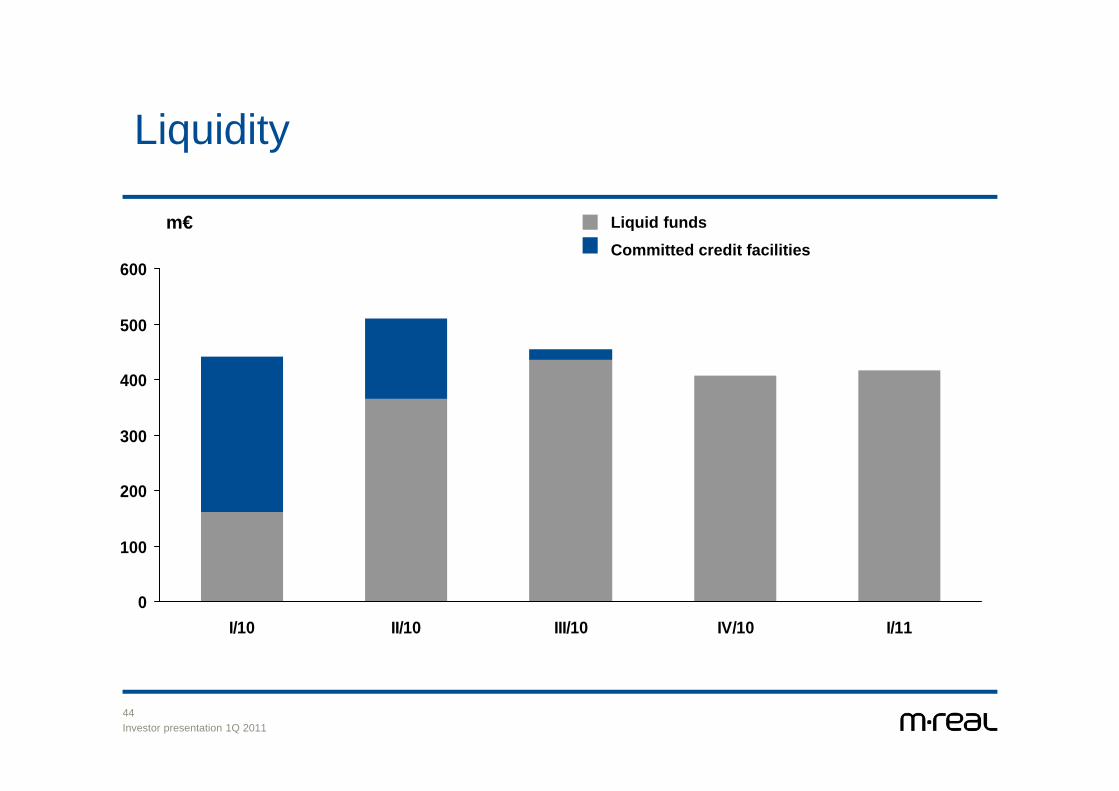

Liquidity

Committed credit facilitiesLiquid fundsm€

0

100

200

300

400

500

600

I/10 II/10 III/10 IV/10 I/11

2.3.2011Investor presentation 1Q 201145

Debt Programs

The following table sets forth the significant debt securities issued and outstanding of M-real as at March 31, 2011:

Average

Long-term borrowings Total amount Outstanding Interest Rate Maturity

USD 350 million Private Note Issue USD 350 USD 224 5.6% (1) 2012–2014EUR 500 million Bond Issue EUR 500 EUR 500 6.7% (1) 2013Global Medium-Term Note Program EUR 1 500 EUR 52 million private placements EUR 52 3,5 % 2011EUR 126 million bilateral loans EUR 126 EUR 126 1,7 % 2011–2013EUR 28 million finance leases EUR 28 EUR 28 2,2 % 2011–2017EUR 239 million pension loans EUR 239 EUR 232 5.4% (1) 2011–2020

Short-term funding programmes

EUR 350 million domestic CP-program EUR 350 EUR 0 – –EUR 150 milj. Belgian CP-program EUR 150 EUR 0 – –

Average interest rate of all M-real Group interest bearing liabilities including interest rate derivatives per 31.3.2011 is 5,1 %.

(currency in millions)

2.3.2011Investor presentation 1Q 201146

Ratings’ History2000

S&P: Short term ratings lowered to A3, Long term ratings placed to credit watch negativeMoody’s: Long and short term ratings outlook changed from stable to negative

2001S&P: Long term ratings lowered to BBB-,stable outlookMoody’s: Long and short term ratings lowered to Baa3/P3, negative outlook

2003S&P: Downgrade to BB+, stable outlookMoody’s: Downgrade to Ba1, negative outlook

2004S&P: Outlook changed from stable to negative, ratings affirmedMoody’s: Downgrade to Ba2, stable outlook

2005S&P: Downgrade to BB, stable outlookMoody’s: Outlook changed from stable to negative, ratings affirmed

2006S&P: Downgrade to BB-, negative outlookMoody’s: Downgrade to Ba3, negative outlookMoody’s: Downgrade to B2, negative outlookS&P: Downgrade to B+, negative outlook

2007Moody’s: Downgrade to B3, negative outlookS&P: Downgrade to B, negative outlookS&P: Downgrade to B-, stable outlook

2008S&P: Outlook to negative

2009S&P: Downgrade to CCC+, negative outlook Moody’s: Downgrade to Caa1, outlook negative

2010S&P: Outlook to stableMoody’s: Outlook to stableS&P: Upgrade to B-, stable outlookMoody’s: Upgrade to B3, outlook to positive

2011S&P: Outlook to positive

General presentation

2.3.2011Investor presentation 1Q 201148

M-real in Brief

• Annual sales about EUR 2.6 billion.• Approximately 4,500 employees.• Present in over 70 countries.• 13 production units in 5 European

countries.• Part of Metsäliitto Group and listed on

the NASDAQ OMX Helsinki Ltd.• Metsäliitto Group is one of the largest

forest industry groups in the world, owned by a cooperative of 130.000 private Finnish forest owners.

Consumer Packaging 45%Paper 38%Market pulp and energy 17%

Sales breakdown 2010

2.3.2011Investor presentation 1Q 201149

Offering for Consumer Packaging, Communications and Advertising

• Cartonboards and white-top kraftliners for packaging beautycare, healthcare, cigarettes, food, consumer durables etc.

• Graphic boards e.g. for book covers, postcards, greeting cards, CD or DVD covers

• Office papers from high-volume copying and printing to high-quality color presentations

• Speciality papers for advertising and corporate materials,flexible packaging, creative designs, labeling, self-adhesive laminates and for wallcovering industry

2.3.2011Investor presentation 1Q 201150

M-real’s Customers

Office product resellers

Publishers

Brand owners

Printers and converters

Advertising and design agencies

Office paper users

Paper merchants

2.3.2011Investor presentation 1Q 201151

17 %

32 %

12 %

9 %

12 %

6 %

9 %3 %

Paper PulpPaperboard PackagingTissue Mechanical Forest ProductsMerchanting Chemicals

45 %38 %

17 %

Focus on Core Businesses1995 Sales€2.3 billion

2010 Sales€2.6 billion

8 Businesses 3 Businesses

2.3.2011Investor presentation 1Q 201152

1997 20001998 1999

Acquisitions

Divestments

Biberist Paper Mill

Simpele Mill UK Paper

Modo Paper

Zanders

ChemicalsBusiness

Botnia Wood

CorrugatedPackaging

MD Papier Metsä Tissue

2001 2002

Albbruck

2003 2004

M-real Restructuring Story

2005

SavonSellu

Forestia

Kemiart Liners (53 %)

8% in Botnia

2006

PSM

2007

9% in Botnia

Cartonplants

Map

100 000 B2 shares

in PVO

20092008

New Thames

MB Uruguay

Graphic Papers

2010 2011

Part of Reflex mill

2.3.2011Investor presentation 1Q 201153

Annual Sales Development

26052432

3236

4440

56245241

54606044

65646923

5898

33193014

2313

4044

0

1000

2000

3000

4000

5000

6000

7000

8000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

EUR, million

Business Portfolio

2.3.2011Investor presentation 1Q 201155

Business Portfolio

Consumer Packaging Speciality Papers

Office Papers Market Pulp and Energy

2.3.2011Investor presentation 1Q 201156

Consumer PackagingMainly Folding Boxboard and Linerboard

• Fibre-based high value-added packaging solutions for global brand owners in beautycare, healthcare, cigarette, food and consumer electronics industries as well as for graphical end-uses

• Relatively high earnings stability• High segment consolidation• Competitive folding boxboard mills with end use specified production

Capacity Share (%)

8 %

9 %

10 %

25 %

32 %

0 % 5 % 10 % 15 % 20 % 25 % 30 % 35 %

IP

Careo

Mayr-Melnhoff

Stora Enso

M-real

No. 1 Folding Boxboard Producer in Europe

Source: Pöyry Management Consulting Oy

2.3.2011Investor presentation 1Q 201157

Office PapersMainly Uncoated Fine Paper

Capacity Share (%)

9 %

10 %

11 %

14 %

14 %

0 % 5 % 10 % 15 %

M-real

UPM-Kymmene

Mondi

Stora Enso

Portucel

No. 5 Uncoated Fine Paper Producer in Europe

• High quality uncoated fine papers for printing and photocopying as well as for forms, envelopes, manuals and communication purposes

• Diversified customer base, e.g. merchants, retail chains, office equipment manufacturers and corporations

• Leading European office paper brands like DataCopy and Evolve as well as revolutionary lightweight SAVE!

Source: Pöyry Management Consulting Oy

2.3.2011Investor presentation 1Q 201158

Speciality Papers

• Leading European speciality paper producer with strong focus on packaging applications

• Packaging specialities• Flexible packaging• Luxury packaging• Labels

• Graphical specialities• Premium fine papers • Carbonless papers• Digital imaging papers

• Uncoated fine papers Packaging specialities 50%Graphical specialities 30%WFU 20%

Speciality paper sales

59

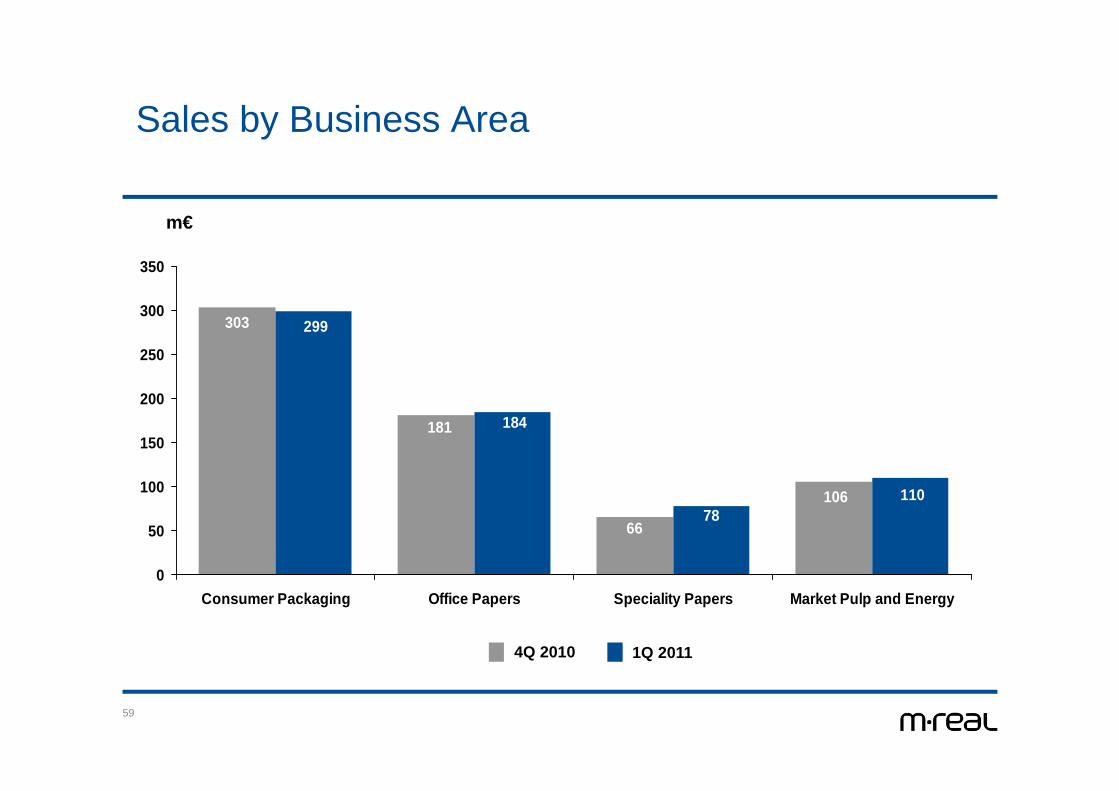

Sales by Business Area

m€

66

181

106

303

11078

184

299

0

50

100

150

200

250

300

350

Consumer Packaging Office Papers Speciality Papers Market Pulp and Energy

1Q 20114Q 2010

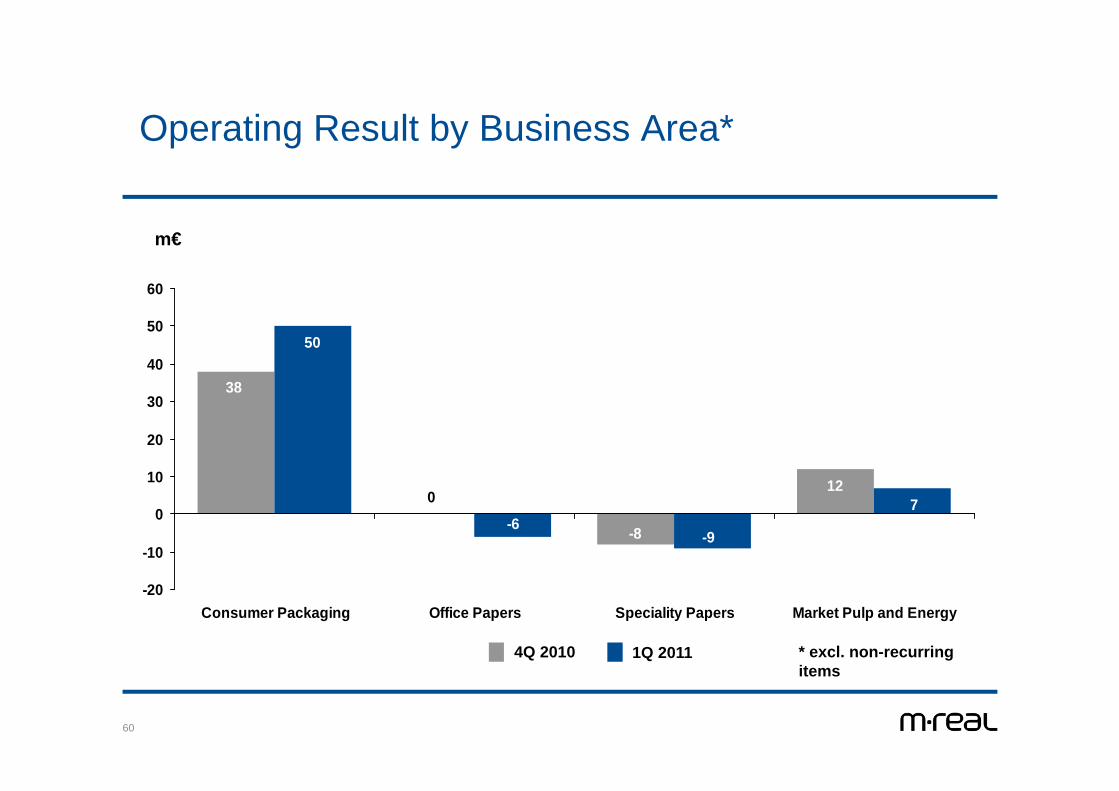

60

Operating Result by Business Area*

* excl. non-recurring items

-8

012

38

7

-9-6

50

-20

-10

0

10

20

30

40

50

60

Consumer Packaging Office Papers Speciality Papers Market Pulp and Energy

m€

1Q 20114Q 2010

61

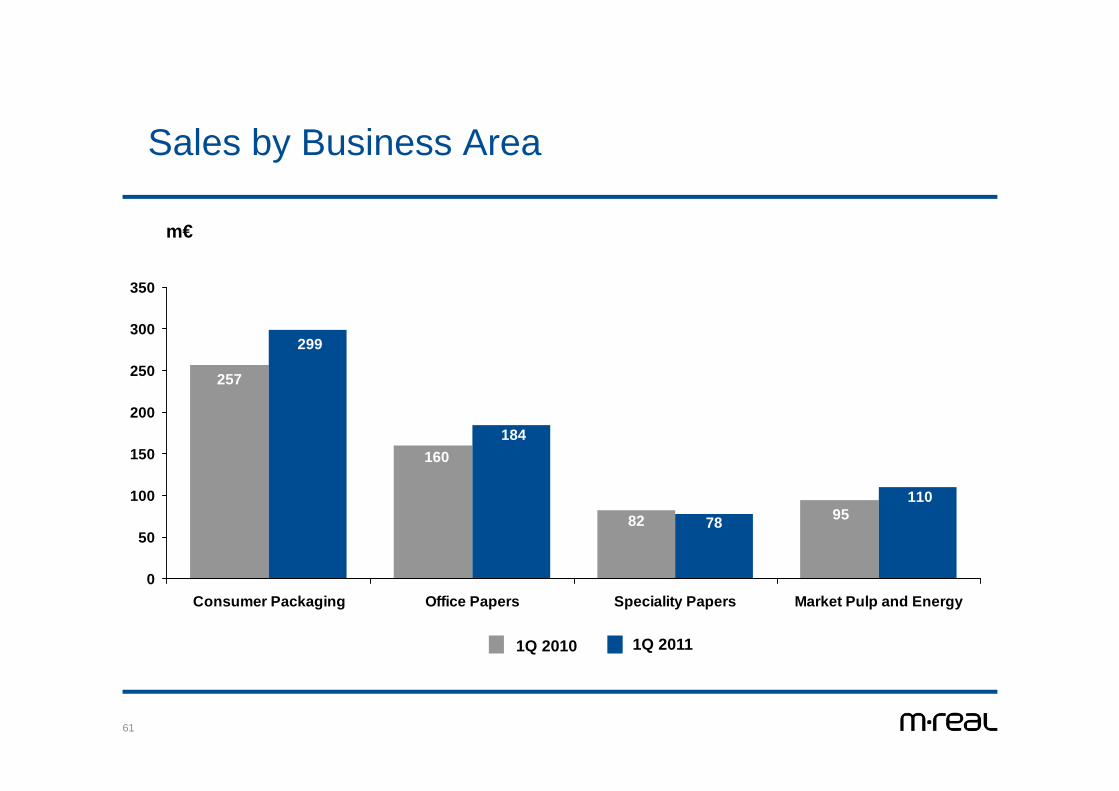

Sales by Business Area

m€

82

160

95

257

110

78

184

299

0

50

100

150

200

250

300

350

Consumer Packaging Office Papers Speciality Papers Market Pulp and Energy

1Q 20111Q 2010

62

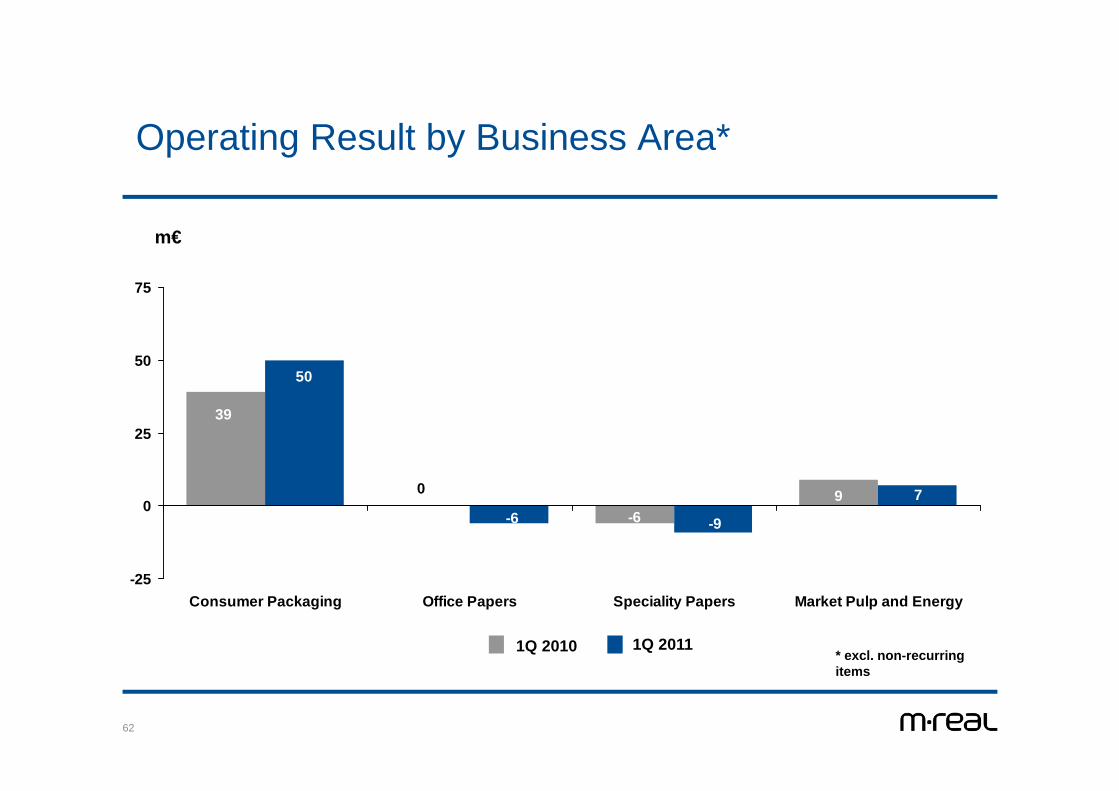

Operating Result by Business Area*

* excl. non-recurring items

m€

-6

0 9

39

7

-9-6

50

-25

0

25

50

75

Consumer Packaging Office Papers Speciality Papers Market Pulp and Energy

1Q 20111Q 2010

Operations

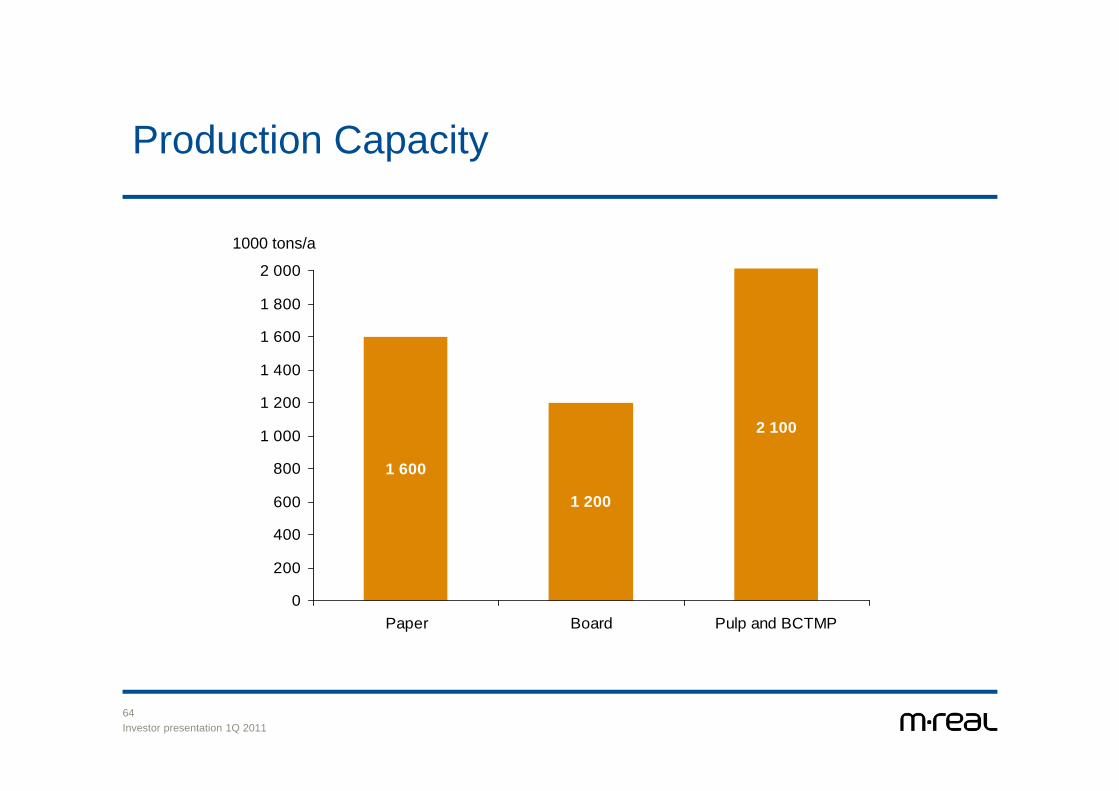

2.3.2011Investor presentation 1Q 201164

1 600

1 200

2 100

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

Paper Board Pulp and BCTMP

1000 tons/a

Production Capacity

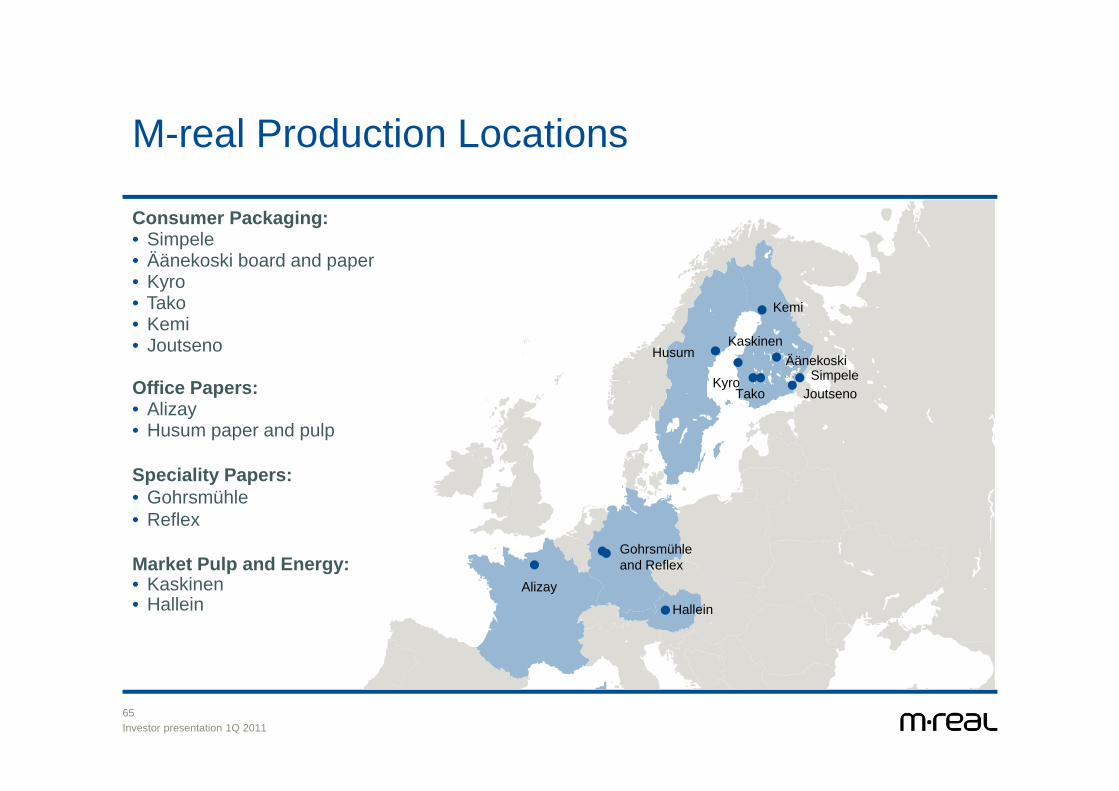

2.3.2011Investor presentation 1Q 201165

M-real Production Locations

Consumer Packaging:• Simpele• Äänekoski board and paper• Kyro• Tako • Kemi• Joutseno

Office Papers: • Alizay• Husum paper and pulp

Speciality Papers: • Gohrsmühle• Reflex

Market Pulp and Energy:• Kaskinen• Hallein

Alizay

Hallein

Husum

Gohrsmühle and Reflex

ÄänekoskiSimpele

Joutseno

Kemi

TakoKyro

Kaskinen

2.3.2011Investor presentation 1Q 201166

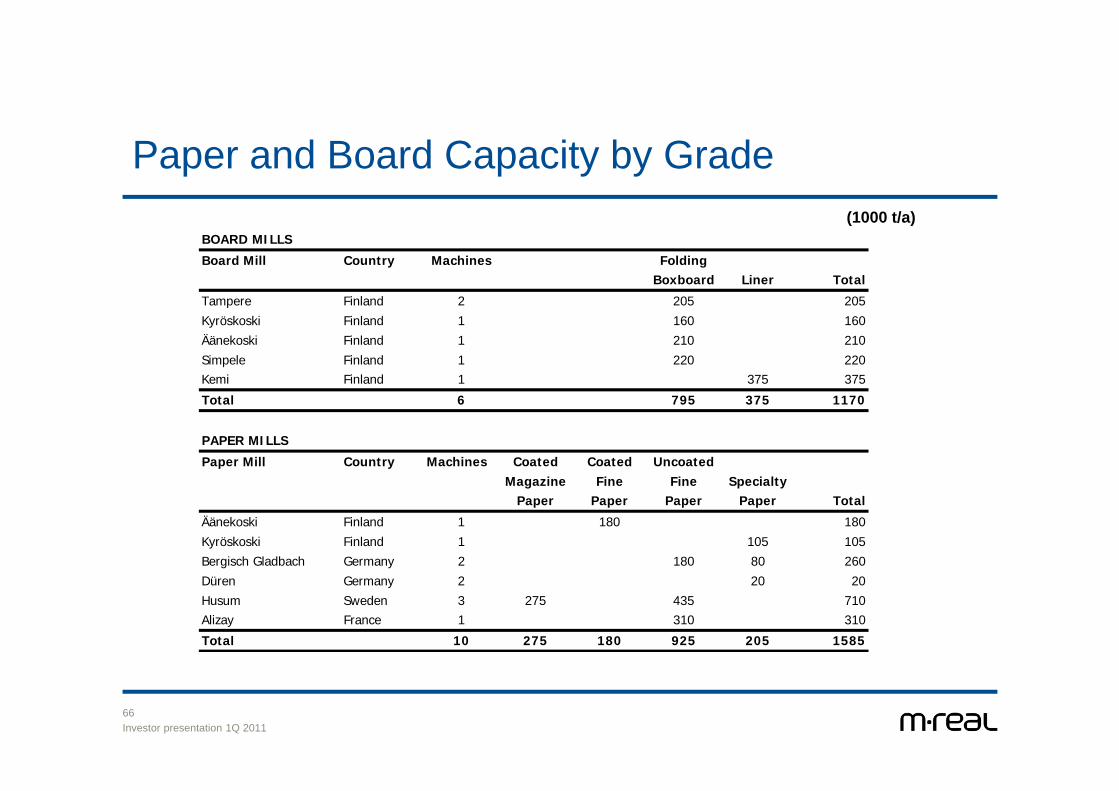

Paper and Board Capacity by Grade(1000 t/a)

BOARD MILLS

Board Mill Country Machines FoldingBoxboard Liner Total

Tampere Finland 2 205 205Kyröskoski Finland 1 160 160Äänekoski Finland 1 210 210Simpele Finland 1 220 220Kemi Finland 1 375 375

Total 6 795 375 1170

PAPER MILLS

Paper Mill Country Machines Coated Coated UncoatedMagazine Fine Fine Specialty

Paper Paper Paper Paper Total

Äänekoski Finland 1 180 180Kyröskoski Finland 1 105 105Bergisch Gladbach Germany 2 180 80 260Düren Germany 2 20 20Husum Sweden 3 275 435 710Alizay France 1 310 310

Total 10 275 180 925 205 1585

2.3.2011Investor presentation 1Q 201167

Pulp Capacity(1000 t/a)

PULP MILLS

Pulp Mill Country ChemicalPulp BCTMP Total

Husum Sweden 690 690Hallein Austria 160 160Joutseno Finland 280 280Kaskinen Finland 300 300

Total 850 580 1430

BOTNIA *

Mill Country ChemicalPulp Total

Äänekoski Finland 500 500Kemi Finland 590 590Rauma Finland 630 630Joutseno Finland 650 650

Total 2370 2370

* M-real share is 30% of the capacity

2.3.2011Investor presentation 1Q 201168

Personnel Development

4515453849036546

9508

1412515154

16490

203722107022237

17351

1388512637

11463

15572

0

5000

10000

15000

20000

25000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 1Q2011

Deliveries

2.3.2011Investor presentation 1Q 201170

Uncoated fine paperCartonboard

Annual Deliveries*

32 %

6 %

18 %

44 %

Western- Europe Eastern- Europe Americas Asia & Pacific

8 %

86 %

5 %1 %

* Indicative numbers

Sourcing

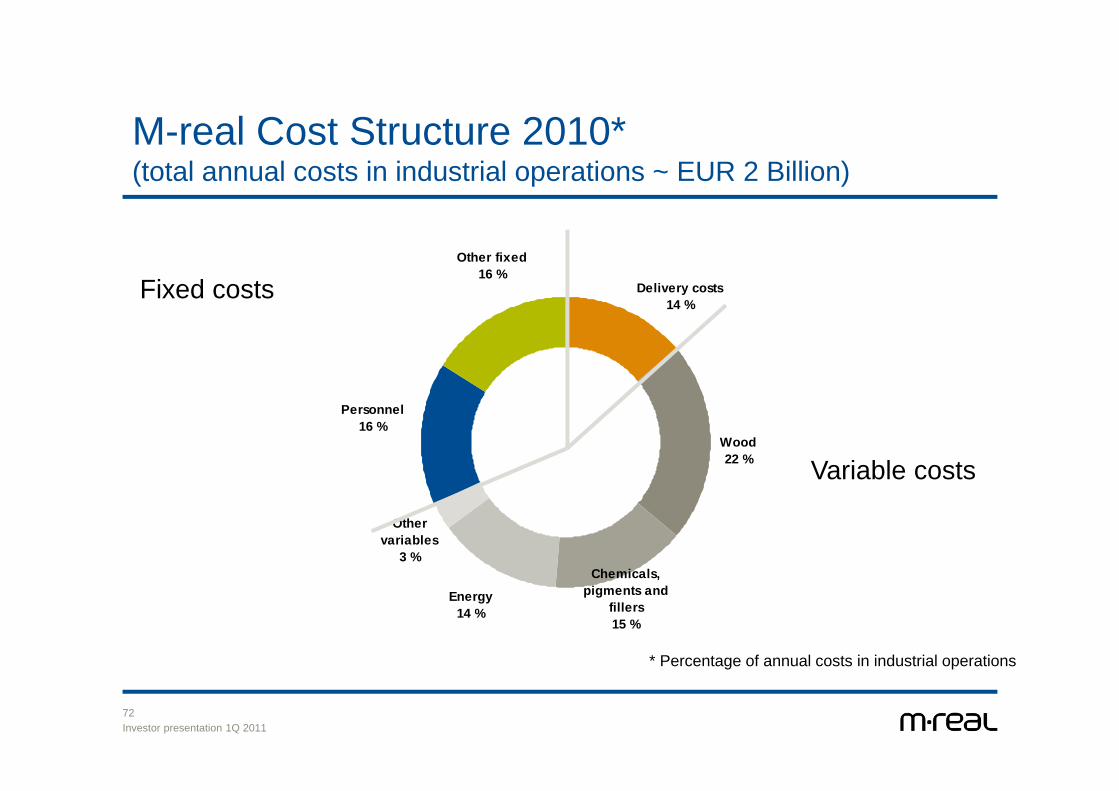

2.3.2011Investor presentation 1Q 201172

Personnel 16 %

Other fixed16 %

Delivery costs14 %

Wood22 %

Chemicals, pigments and

fillers15 %

Other variables

3 %

Energy14 %

M-real Cost Structure 2010* (total annual costs in industrial operations ~ EUR 2 Billion)

Fixed costs

Variable costs

* Percentage of annual costs in industrial operations

2.3.2011Investor presentation 1Q 201173

Electricity Sourcing 2010 (total 3 500 GWh)

Associated company

(PVO)29 %

Outsourced generation

2 %

Own generation

32 %Purchased energy37 %

2.3.2011Investor presentation 1Q 201174

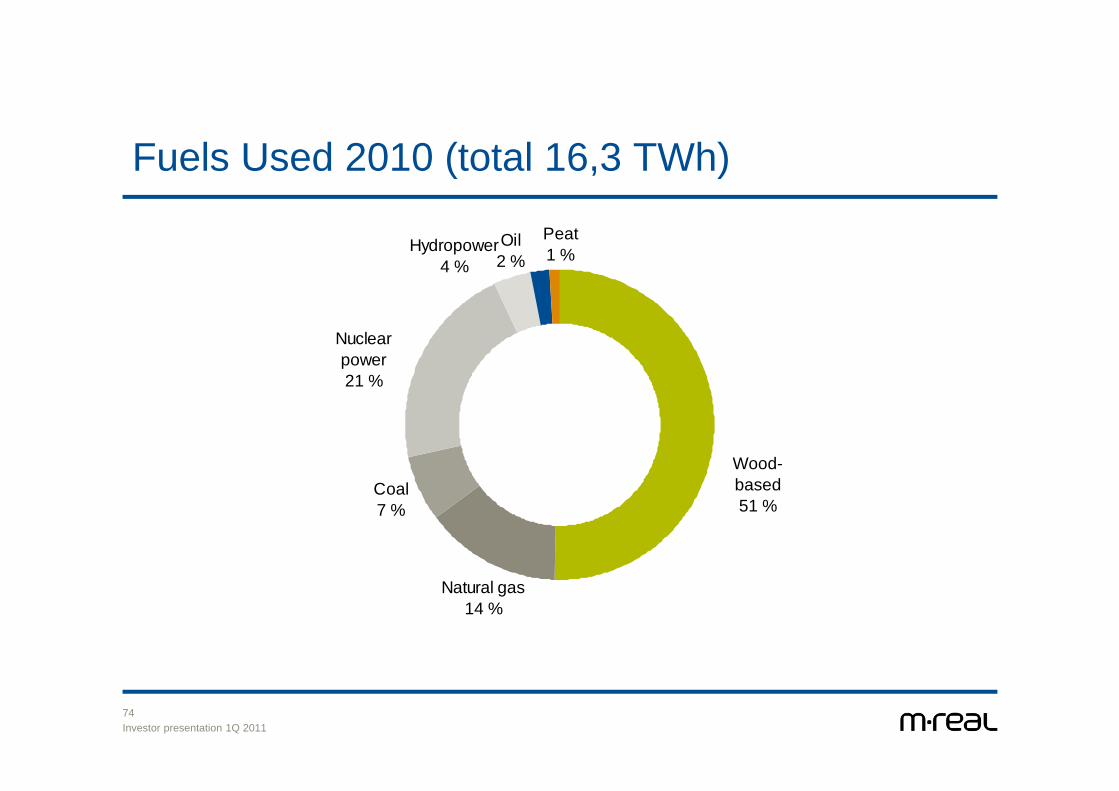

Fuels Used 2010 (total 16,3 TWh)

Wood-based51 %

Natural gas14 %

Coal7 %

Oil2 %

Peat1 %Hydropower

4 %

Nuclear power21 %

2.3.2011Investor presentation 1Q 201175

Wood Sourcing by Country

1 000 m3 2010Sweden 2210Finland 1243Austria 792Russia 573Latvia 443Estonia 236Lithuania 109Others 113Total 5719

2.3.2011Investor presentation 1Q 201176

Development of Softwood PulpwoodCost at Mill, Wood for Chemical Pulping

1980 – 2Q 2010

Source: Pöyry Management Consulting Oy

0

10

20

30

40

50

60EUR/m3sob, nominal

Finland, south, pineSweden, south, pineGermany, south, pineChile, radiata pineUSA South, SYPCanada East, SPF

2.3.2011Investor presentation 1Q 201177

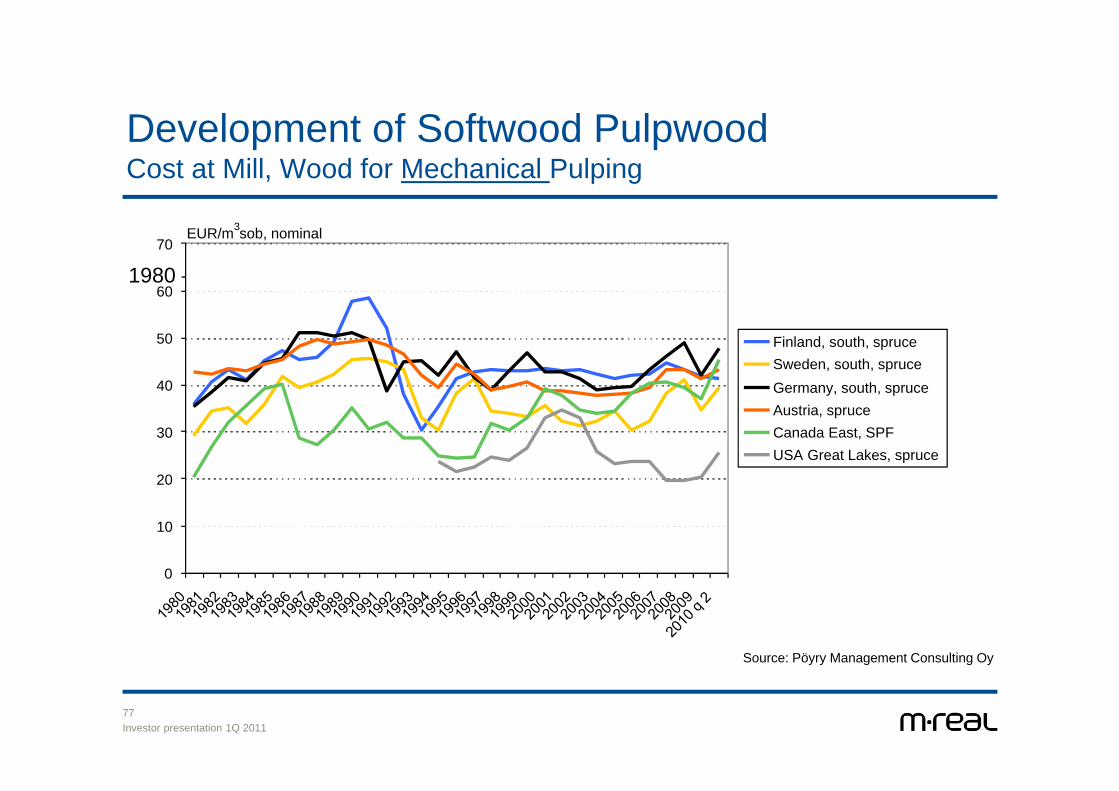

Development of Softwood PulpwoodCost at Mill, Wood for Mechanical Pulping

1980 – 2Q 2010

Source: Pöyry Management Consulting Oy

0

10

20

30

40

50

60

70EUR/m3sob, nominal

Finland, south, spruceSweden, south, spruceGermany, south, spruceAustria, spruceCanada East, SPFUSA Great Lakes, spruce

2.3.2011Investor presentation 1Q 201178

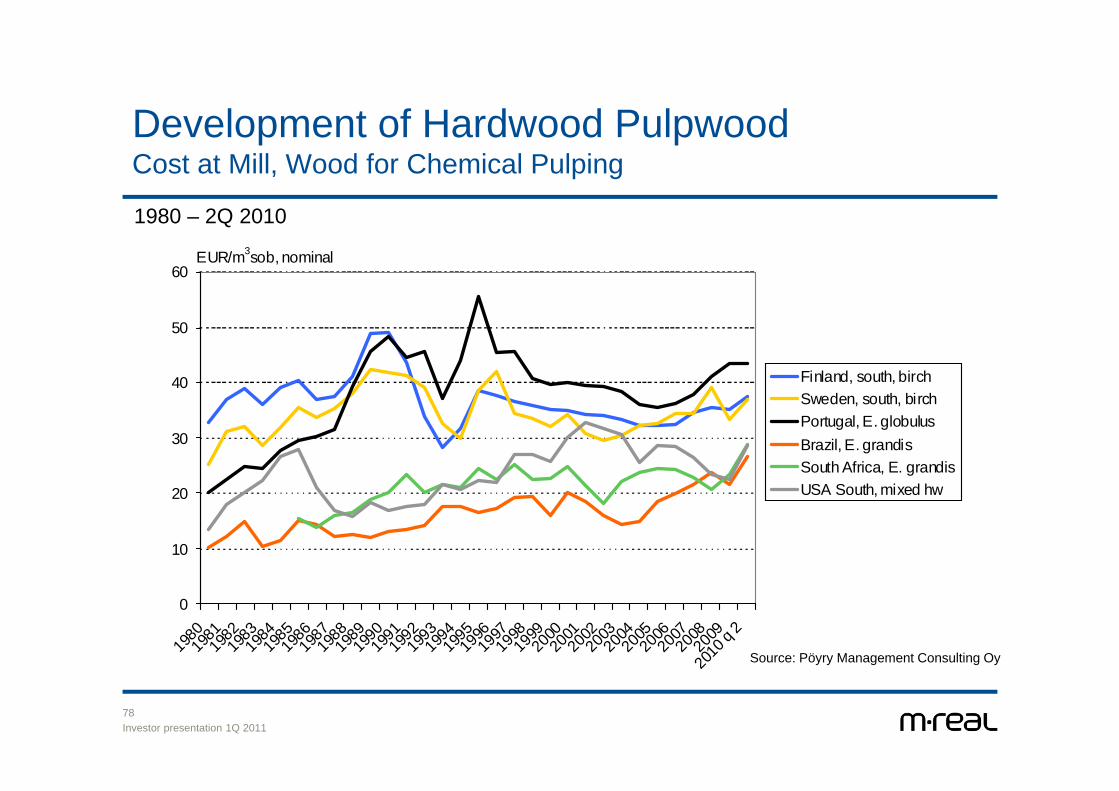

Development of Hardwood PulpwoodCost at Mill, Wood for Chemical Pulping

1980 – 2Q 2010

Source: Pöyry

0

10

20

30

40

50

60

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

q 2

EUR/m3sob, nominal

Finland, south, birchSweden, south, birchPortugal, E. globulusBrazil, E. grandisSouth Africa, E. grandisUSA South, mixed hw

Source: Pöyry Management Consulting Oy

Owners

2.3.2011Investor presentation 1Q 201180

Ownership Structure 31.3.2011

Shares Votes

Source: Euroland

Market Position

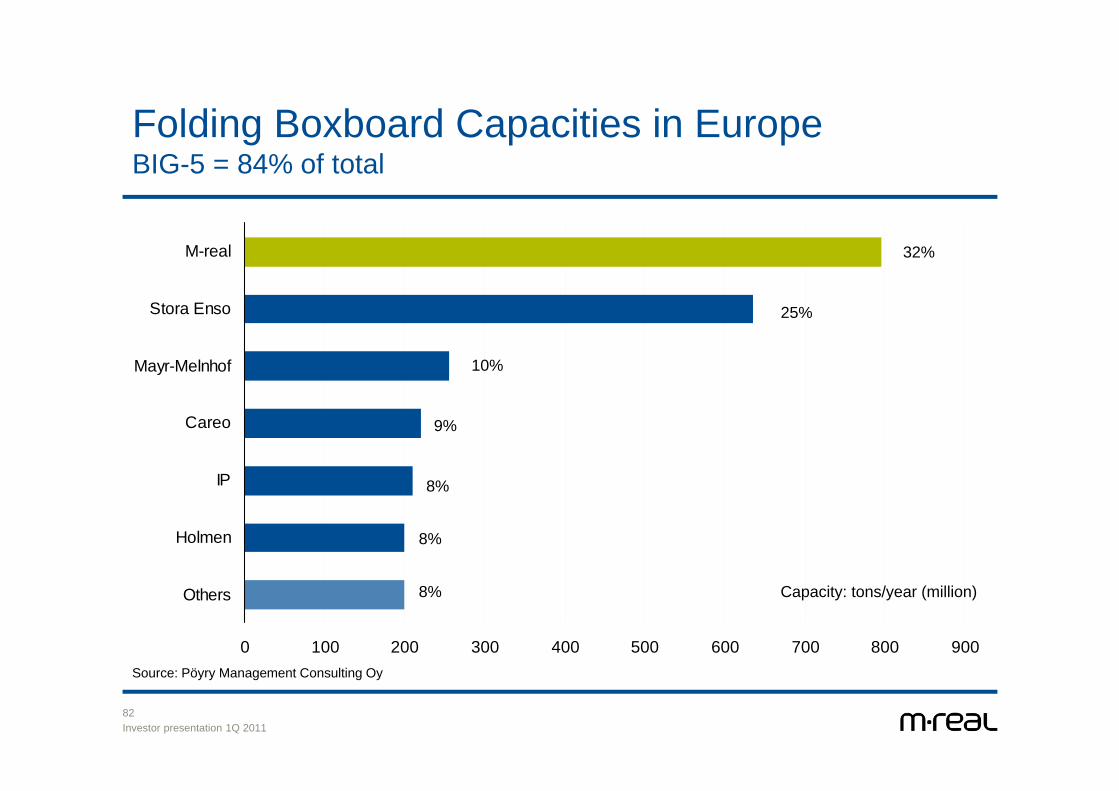

2.3.2011Investor presentation 1Q 201182

0 100 200 300 400 500 600 700 800 900

Others

Holmen

IP

Careo

Mayr-Melnhof

Stora Enso

M-real

Folding Boxboard Capacities in Europe BIG-5 = 84% of total

Source: Pöyry Forest Industry Consulting

Capacity: tons/year (million)

32%

25%

10%

9%

8%

8%

8%

Source: Pöyry Management Consulting Oy

2.3.2011Investor presentation 1Q 201183

0 500 1000 1500 2000 2500 3000 3500

Others

Sappi

Arctic Paper

International Paper

M-real

UPM

Mondi

Stora Enso

Portucel

Uncoated Fine Paper Capacities in EuropeBIG-5 = 57% of total

14%

14%

11%

10%

8%

8%

3%

3%

28%

Source: Pöyry Forest Industry Consulting, M-real

Capacity: tons/year (million)

Source: Pöyry Management Consulting Oy

Thank youwww.m-real.com