investor day london - natuzzisap implementation commercial and retail processes new organization...

TRANSCRIPT

Investor day

London

February 23, 2011

1

2

Pasquale Natuzzi

Welcome and Company Overview

Simon Hughes

Leverage on Natuzzi and Italsofa

Mimmo Cavallo

Recover core business with Editions

Vittorio Notarpietro

KPI

Walk-through:

Stefano Sette - Giuseppe Clemente

Product Innovation, New Manufacturing Process (moving line)

Agenda

3

Global business matrix

to build the future

Pasquale Natuzzi

1959: 52 Years of Challenges

4

KEY FACTS

DNA:

− Innovation

− Product development and

manufacturing Know how

− International presence

BASIC VALUES:

− Integrity

− Responsibility

− Transparency

1959: the long running starts

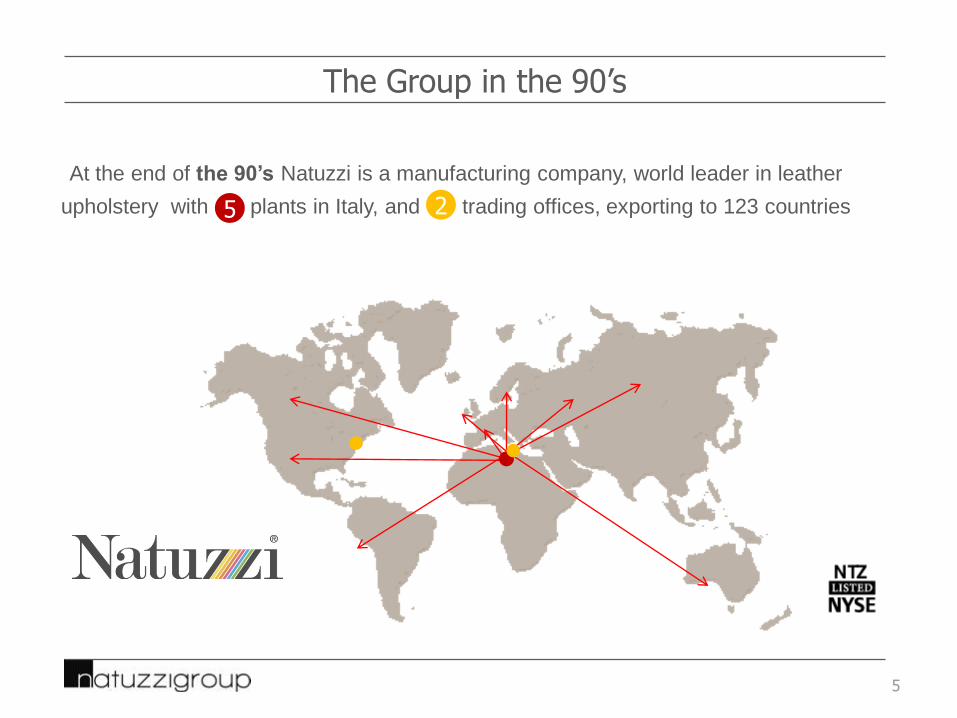

The Group in the 90‟s

5

At the end of the 90’s Natuzzi is a manufacturing company, world leader in leather

upholstery with plants in Italy, and trading offices, exporting to 123 countries5 2

New competitive scenario

6

1997

KEY FACTS

Chinese Competition,

and market globalization

Natuzzi concerns:

Protect the existing business

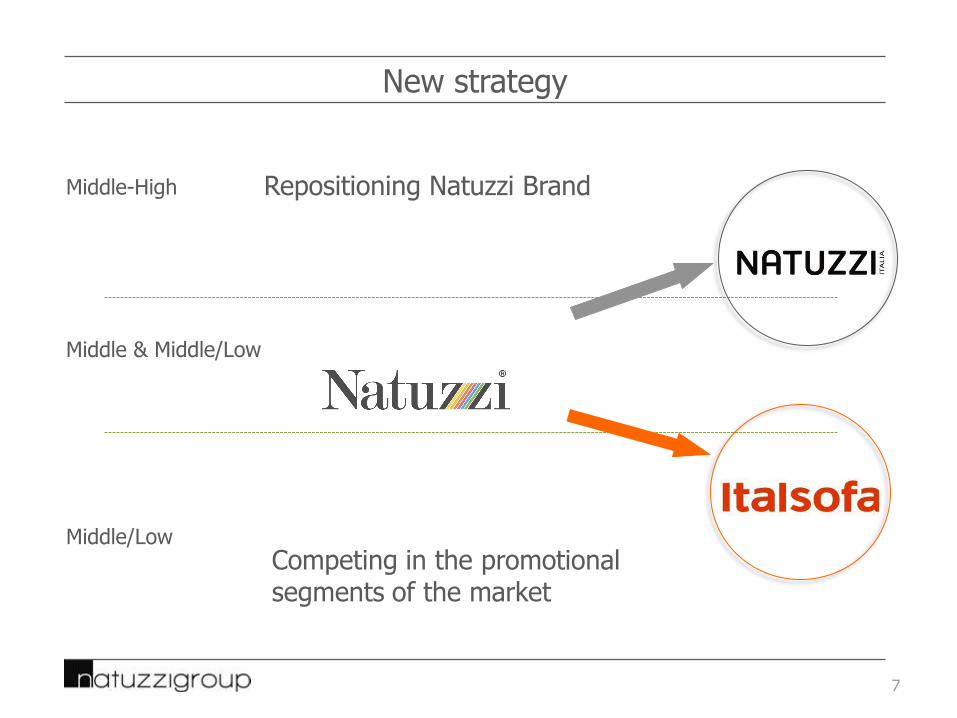

New strategy

7

Middle-High

Middle & Middle/Low

Middle/Low

Repositioning Natuzzi Brand

Competing in the promotional segments of the market

New strategy

8

Global production: New Factories abroad

BAIA MARE - ROMANIASALVADOR DE BAHIA -

BRASILE SHANGHAI - CINA

To compete in the middle-low part of the market

The brand building project

9

Visual identity

Old Product

10

New product: Total Living

11

Product extension

12

Old Store

13

New Store

14

International development

15

48 stores in the Asia Pacific Region of which 21 in China

SHANGHAI

International development

16

ADELAIDE – (AU)

15 Stores in Australia

International development

17

MILAN

100 Stores in Italy

International development

18

BARCELLONA

21 Stores in Spain

International development

19

PARIS

27 Stores in France

International development

20

WINTERTHUR – (CH)

5 Stores in Switzerland

International development

21

LONDON

UK: 22 Stores / Concessions

International development

22

UK: Galleries at Harrods, Selfridges and House of Fraser

Old advertising

23

New advertising

24

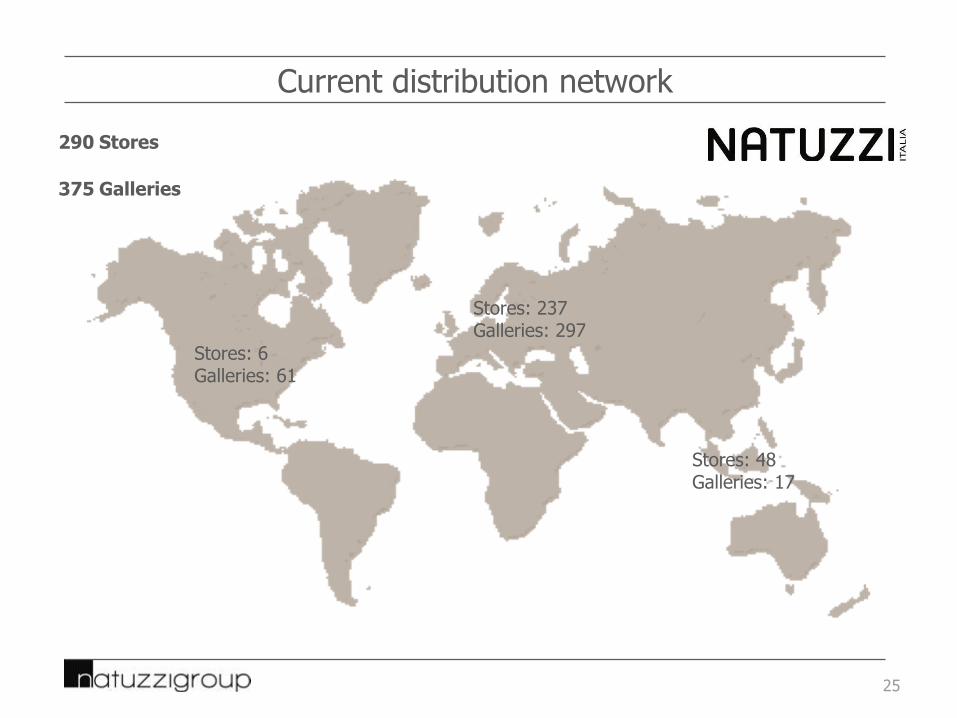

Current distribution network

25

Stores: 6Galleries: 61

Stores: 237 Galleries: 297

Stores: 48 Galleries: 17

290 Stores

375 Galleries

Investments

26

Total investment of € 420 mln

Equal to 9% on total revenues of € 4,5 bln

Natuzzi Brand Building Investment

2003 - 2010

• New Product Development

• Italian Plant requalification

• Store and Gallery development

• Marketing and Advertising

Group brands portfolio

27

Mission: Italian Total livingPositioning: Middle/highChannel: B2C, Retail

Mission: Affordable innovationPositioning: Middle/young generationChannel: B2C, Retail

Mission: Surrounding comfortPositioning: Middle/lowChannel: Wholesale

NTZ Group global presence

28

Despite market crisis, emergence of Chinese competition and high currency volatility, we invested and created:

•Global sales network•International production hubs linked to brands/ markets

Trading

Offices8

Stores/

Galleries763

Plants 11

Next step: Reduce complexity

Integration, simplification & innovation: Global business matrix

29

BRANDS - CONSUMER

SEGMENTATION

• Natuzzi

• Italsofa

• Editions

3

MACRO MARKETS

• Europe

• America

• Asia Pacific

3

DISTRIBUTION

CHANNELS

• Retail

• Wholesale

• Key customers

3

MANUFACTURING HUBS

• Europe (Italy and Romania)

• America (Brazil)

• Asia (China)

3

ORGANIZATION LEVELS

• Corporate

• Regions

• Country

3

GUIDELINES AT EVERY

ORGANIZATION LEVEL

• Sharing

• Accountability

• Discipline

3

Management

30

Chief Internal ControlSystems Officer

Giuseppe Cacciapaglia

Chief HR & Organization Officer

Fernando Rizzo

CFO

Vittorio Notarpietro

Chief Procurement Officer

Giambattista Massaro

Chief Natuzzi& Italsofa Division

Simon Hughes

Chief Editions& Softaly Division

Cosimo Cavallo

Audit Committee

Chief Legal Officer

Stelio Campanale

CIO

Angelo Colacicco

Chief Operations Officer

Giuseppe Clemente

Chief Research& Development

Officer

Stefano Sette

Chief Institutional Relations &

Corporate Comm. Officer

Giacomo Ventolone

Chairman & CEO

Pasquale Natuzzi

31

Global business matrix

Brands

Simon Hughes

Natuzzi Retail

32

1) Direct vs. Partner•Existing DOS focus on operations + profit•Partners primarily for development markets (local knowledge and retail expertise)

2) Growth•2010 DOS 2011 DOS

3) Performance•Traffic driver “affordability”•Total look “sales”•Increase average tickets price “service”

•A more affordable concept•Training critical •Rigorous analysis

4) Collection rationalization•Core collection (10 models 65% total sales)•Retail collection (only 60 models)•Replenishment program

5) Marketing•Consolidate spend•Promote total look•Drive traffic

a

b

Italsofa Brand

33

Mission: Affordable innovation

Positioning: Middle/young generation

Channel: B2C, Retail

Products

34

Store concept

35

Distribution Network

36

Stores: 2

Galleries: 2

Stores: 9

Galleries: 7

Stores: 15

Galleries: 8

26 Stores

16 Galleries

Advertising

37

Co-Advertising

38

Retail Key Actions

39

1) Reposition with more contemporary design aesthetic

2) More affordable brand for young (in spirit) consumers

3) Upgrade existing network from wholesale to retail model

4) 220 Gallery committed (2010)

40

Global business matrix

Markets

Mimmo Cavallo

Editions

41

Mission: recover our core

business with Wholesalers

& Mass Merchants

Editions

42

Editions

43

Editions

44

45

Mass Merchants program

• Identify/ open existing and new accounts in the Mass Merchants

cluster

• Capitalize on the success with IKEA and duplicate the same

business model

• Regain sales with the Key Accounts

Mass Merchants program

46

Key success factors:

• Excellent service (10 days from order entry to finished products, plus transit time)

• High quality standards

Rationale:

• Limited number of models, coverings and versions

• Accurate forecasting

• Targeted price points

• Strict monitoring of the KPI‟s

• Dedicated production lines

47

Mass Merchants: Business opportunities

NORTH AMERICA

Nearly € 100 mln worth of sales to be

recovered with the major accounts. E.g.:

• MACY'S

• THE BRICK

• R.C. WILLEY

• ART VAN

• SOFA MART

• ROOMS TO GO

• SLUMBERLAND

• DILLARD'S

• AMERICAN SIGNATURE

EUROPE

Over € 50 mln worth of sales to be

recovered with the major accounts. E.g.:

• REID

• LIVING

• BEGROS

• BOHUS

• UNION

• ATLAS

• MIO

IKEA

48

Leverage on our best practice with IKEA, the most demanding retailer in the world

18 years of strong partnership based on high level of service, quality and value

Baiamare

Plant

IKEA

Warehouse

13

49

2010 Achievements&

2011 targets

Vittorio Notarpietro

IT System AS WAS

50

Natuzzi Italia Impe e Natco USA Romania Brasile Cina Europa

Bus

ines

s

inte

llige

nce

DW reporting

Retail / Presa ordine

Gestione ordini (credito,

validazioni, …)

Aftersales

Pianificazione a breve

Spedizione

Fatturazione

Acquisti mat indiretti

MRP Mat. Diretti

Acquisti mat diretti

Gestione fisica stabilimenti

e magazzini

Avanzamento produzione

Amministrazione

Vefa Indiretti

VeFa Diretti

Tesoreria

Controllo

Product Costing

Consolidamento

Pia

nif

icaz

io

ne a

med

i

oPian. a medio produzione

Fina

nce

& C

ontr

ollin

gC

iclo

del

l'ord

ine

Acq

uist

i e p

rodu

zion

e

BI Microsoft

RPG Order Management

NCRM

WEBCLAIM,

JDE JDEJDE

RPG manufacturing

Ares

Ares

RPG acquisti JDE

NARES

DSS trasporti

Ares

Manuale

DPM

Cybertec

RPG manufacturing

NARESAresRPG Invoice

JDE

CDR

ACG

Piteco

ACGJDE

ACG

Local

application

JDE JDE

Natplan

Local

application

CDR

NCRM

NARES

Order

Management

RPG trasporti managementAres

RPG Invoice

PitecoPiteco

CDR

ACG

Outlooksoft

AresRPG Manufacturing

ACG

Local

application

RPG manufacturing

RPG Invoice

RPG order management

RPG manufacturing

RPG Manufacturing

ACG

RPG Order

Management

NCRM

NARES

RPG Order

management

ACG

RPG

OM

Business Portal Business Portal Business Portal

Board Sales Board Sales

BI Microsoft

Board Sales

BI Microsoft

Datasys

Local applicationLocal

application

JDE

Local

application

Easy Report

Easy report

Incas WMS

Sofapacker

Soluzione

forecast

Local

application

Local

application

Local

application

Local

application

Local

application

Local

application

Board, as400

WEBCLAIM,

Board, as400

DSS (…) AresUnix (…)

ACG

IT System AS IS

51

Production

Planning

PP

Financial

Accounting

FI

Controlling

CO

Material

Management

MM

Sales and

Distribution

SD

Demand

Planning

APO

Warehouse

Management

WM

Business Planning

and Consolidation

BPC

Business Intelligence – Corporate Performance Management

NARES

BUSINESS PORTAL

WEB CLAIM

Legacy MES (Unix + DSS)

• Ottimizzazione sequenze produttive, attribuzione

ad operatori,…

• Analisi produttività

• Gestione stampe di produzione (nota lavoro,

etichette imballo, …)

• Controllo qualità (*)

• Gestione manutenzione (*)

• Avanzamento di produzione

Price Lists tools

Tesoreria - Piteco

NATPLAN

NADOS

SOFAPACKER

Byte Payroll and time management

ARES - Conceria NATCO

Human

Resource

HCM

Quality

Management

QM

2010 Achievements: SAP roll-out

52

Italy

USA

Romania

China

Brazil

UK

Switz.

Spain

Finance &

Controlling

(FI-CO)

Prouction

Planning

(PP)

Purchasing (MM)

IndirettiDiretti

2008

2009

2009

2009

2009

2009

2009

2008

2009

2009

2009

2011

Live Non live

2008

2010 2010

2009 2010 2010

2011

Demand

Planning

(APO)

Warehouse

(WM)

Sales

Distribution

(SD)

Benelux 2011

2010

2011

2011

2010

2011

2011

2011

2011

2011

Human

Resource

(HCM)

2011

2011

2011

2011

2011

2011

2011

2011

2011

2010 Achievements (*)

53

• Recovery of Sales in North America 32.7% and Asia 27.2%

• Entered in India and Brazil markets

• Improved business with IKEA

• Good initial reaction of the Market for the new Italsofa Brand

• Improved operations efficiency COGS from 65.2% in „09 to 62.3% in „10

• Successful NAP process: reduction lead time from 16 to 10 weeks

• Important SG&A reduction plan from 38.3% in ‘09 to 37.7% in ‘10

(*) all numbers and % are as at 30 September 2010

EBIT 2010 = in the area of breakeven

2010 Achievements

54

Relocation of the primary China factory

• Construction of the new factory of 88.000 SQM in “Minhang Export Processing Zone” in Shanghai

• Production full Capacity completed by May 2011

• Entire Chinese NTZ production will be grouped within the next future in the new factory

• Total Indemnity: €47 million approximately 420 million RMB

• Account effects:•€47 million cash (420 M Rmb)•€19 million write off of the Book value of the old factory (166 M Rmb)•€28 million approximately as extraordinary revenues

•Payment in 3 trances:•50% within 5 day from signing (January 26th 2011)•45% within end of February 2011•5% within end of May 2011

2011 targets

55

NET SALES: single digit increase

COGS: to continue efficiency process

SG&A: to carry on reduction plan

EBIT : positive % on Sales

NFP : significant increase (almost doubling)

Natuzzi Group is working on a 5 year BP that will focus:

•Recover sales in the major markets •Development in fast growing markets (China, Brazil, India)

Innovation

56

Today the Company is ready to get focused on its strengths and get competitive advantage through innovation

PRODUCTStyle and Materials innovationSynergies in componentsInnovation according to “moving line” production system

MANUFACTURING PROCESS

Moving line to recover productivity

From manual cutting to virtual nesting and automatic cutting

HQ ACTIVITIES AND SERVICES

Focus on strategic markets and priorities. SAP implementation

COMMERCIAL AND RETAIL PROCESSESNew organization with high focus on brands differentiation and Channel management

57

Forward-looking Statements contained in this document, particularly the

ones regarding any Natuzzi Group possible or assumed future performance,

are or may be forward-looking statements and in this respect they involve

some risks and uncertainties.

Natuzzi Group actual results and developments may differ materially from

the ones expressed or implied by the above statements depending on a

variety of factors.

Any reference to past performance of Natuzzi Group shall not be taken as

an indication of future performance.

This announcement does not constitute an offer to sell or the solicitation

of an offer to buy the securities discussed herein.