investmentworth investment worth. given a minimum attractive rate-of-return, be able to evaluate the...

TRANSCRIPT

Investment Worth

ENGM 661 Engineering

Economics for Managers

Given a minimum attractive rate-of-return, be able to evaluate the investment worth of a project using Net Present Worth Equivalent Annual Worth Internal Rate of Return External Rate of Return Capitalized Cost Method

Tonight’s Learning Objectives

MARRSuppose a company can earn 12% / annum in U. S. Treasury bills

No way would they ever invest in a project earning < 12%

Def: The Investment Worth of all projects are measured at the Minimum AttractiveRate of Return (MARR) of a company.

Investment Worth

MARR is company specific utilities - MARR = 10 - 15% mutuals - MARR = 12 - 18% new venture - MARR = 20 - 30%

MARR based on firms cost of capital Price Index Treasury bills

MARR

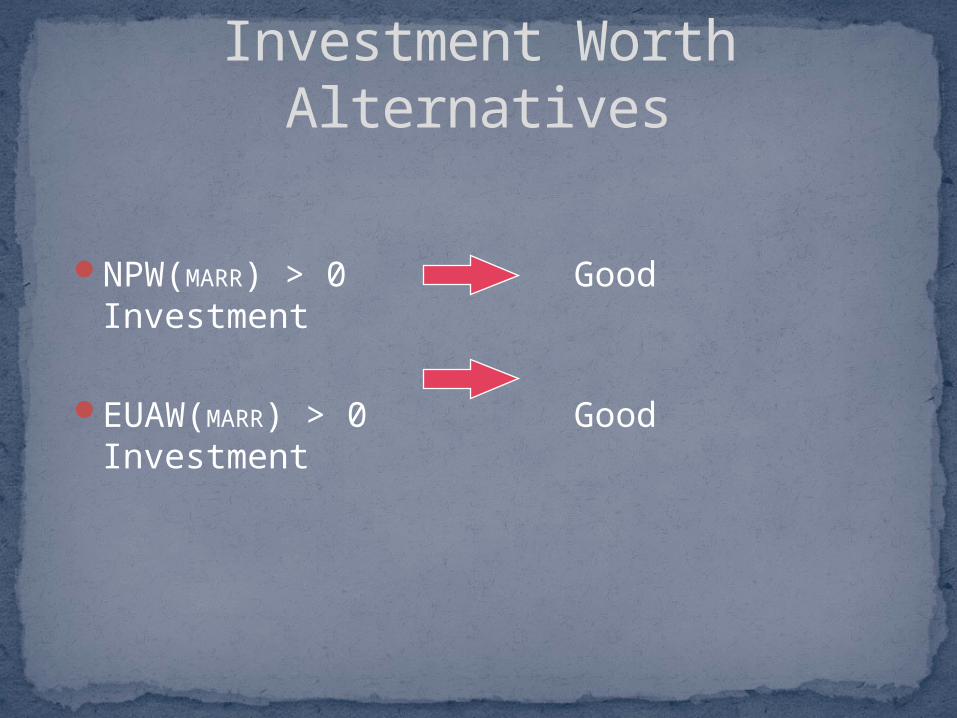

NPW(MARR) > 0 Good Investment

Investment Worth Alternatives

NPW(MARR) > 0 Good Investment

EUAW(MARR) > 0 Good Investment

Investment Worth Alternatives

NPW(MARR) > 0 Good Investment

EUAW(MARR) > 0 Good Investment

IRR > MARR Good Investment

Investment Worth Alternatives

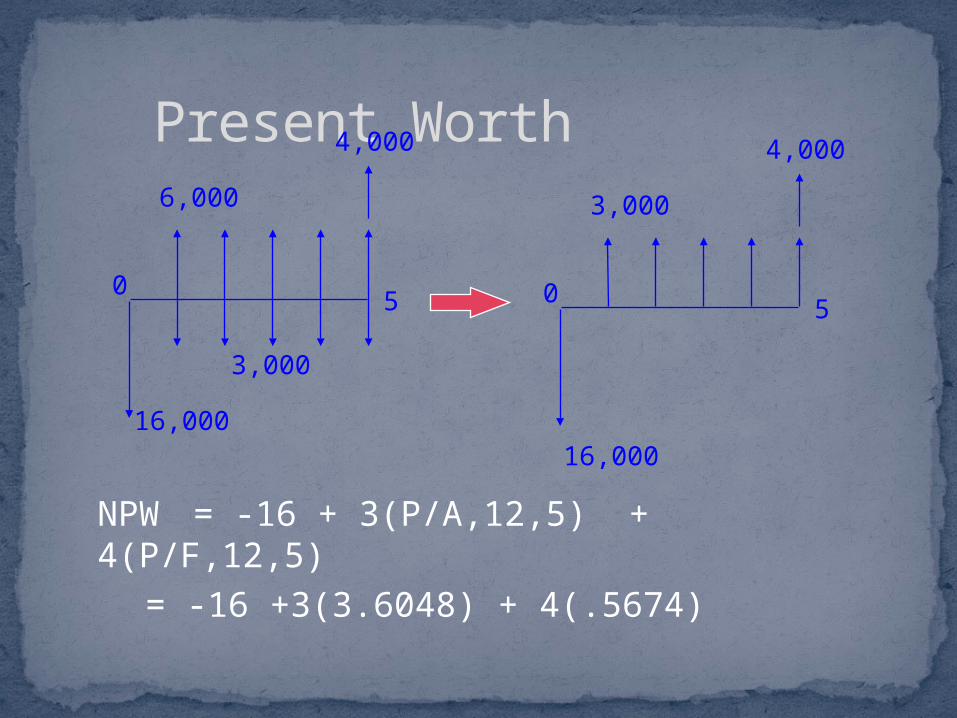

Example: Suppose you buy and sell a piece of equipment.

Purchase Price $16,000 Sell Price (5 years)

$ 4,000 Annual Maintenance $ 3,000 Net Profit Contribution $ 6,000

MARR 12%Is it worth it to the company to buy the machine?

Present Worth

Present Worth

NPW = -16 + 3(P/A,12,5) + 4(P/F,12,5)

16,000

6,000

3,000

50

4,000

16,000

3,000

50

4,000

Present Worth

NPW = -16 + 3(P/A,12,5) + 4(P/F,12,5)= -16 +3(3.6048) + 4(.5674)

16,000

6,000

3,000

50

4,000

16,000

3,000

50

4,000

Present Worth

NPW = -16 + 3(P/A,12,5) + 4(P/F,12,5)= -16 +3(3.6048) + 4(.5674)= -2.916= -$2,916

16,000

6,000

3,000

50

4,000

16,000

3,000

50

4,000

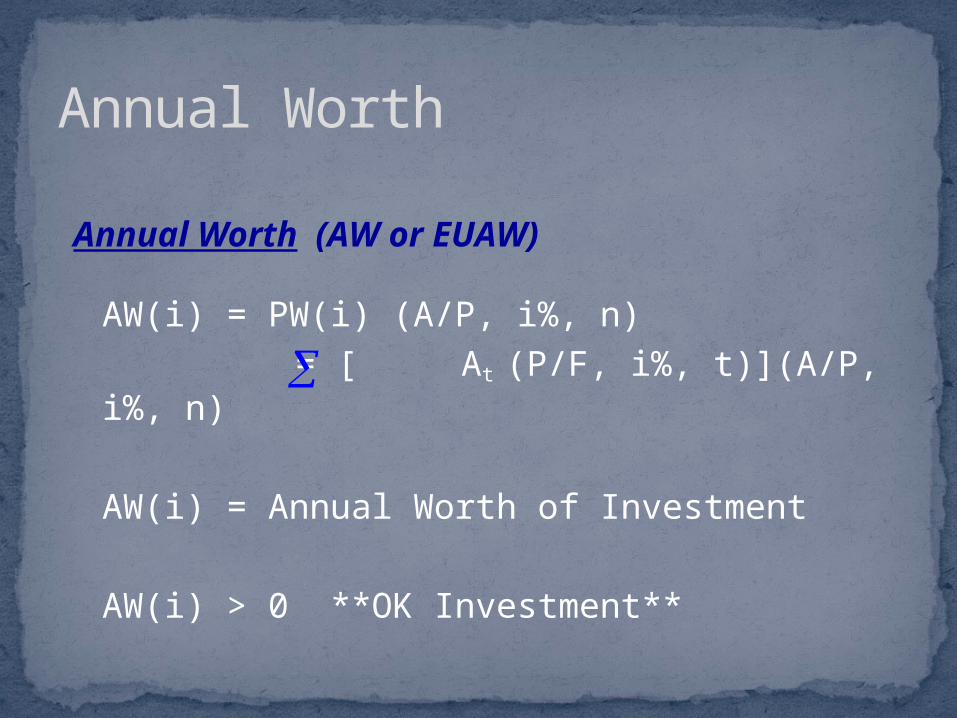

Annual Worth (AW or EUAW)

AW(i) = PW(i) (A/P, i%, n) = [ At (P/F, i%, t)](A/P, i%, n)

AW(i) = Annual Worth of Investment

AW(i) > 0 **OK Investment**

Annual Worth

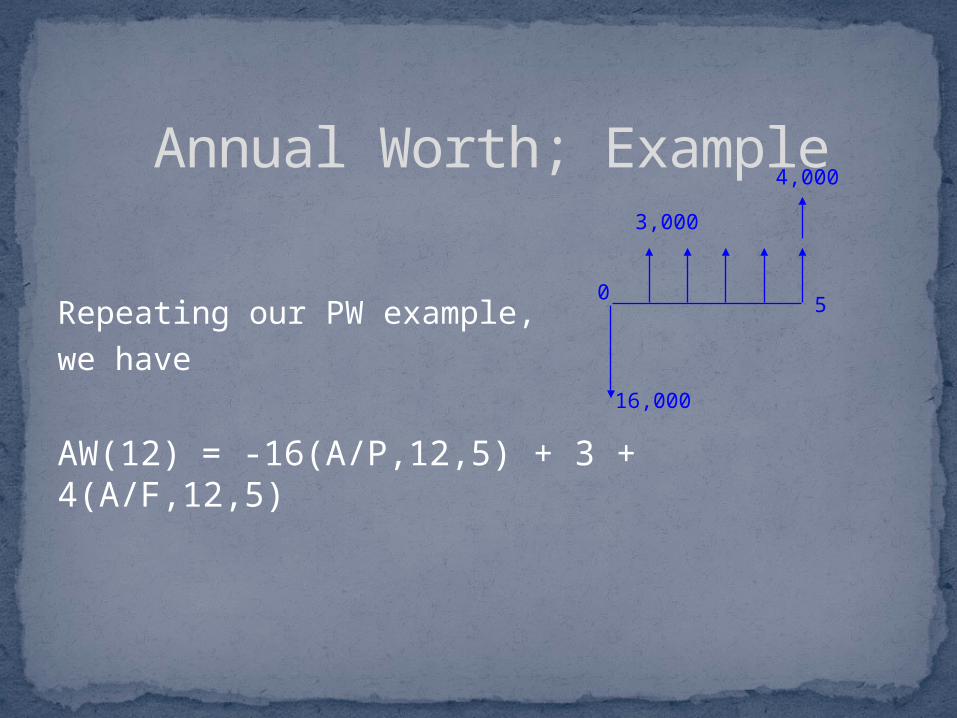

Annual Worth; Example

Repeating our PW example, we have

AW(12) = -16(A/P,12,5) + 3 + 4(A/F,12,5)

3,000

50

4,000

16,000

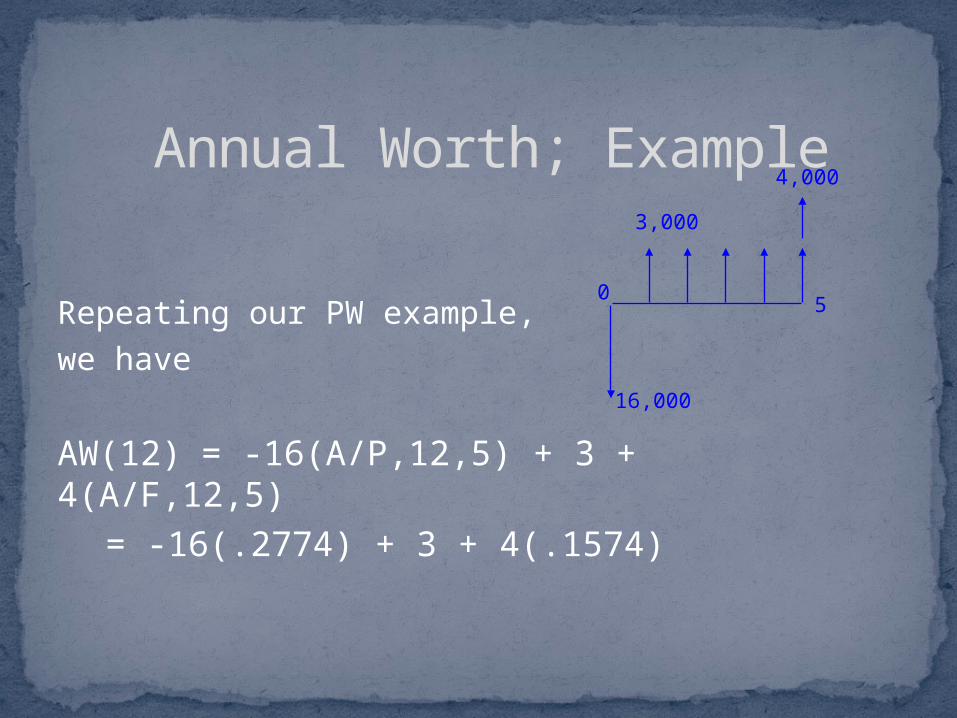

Annual Worth; Example

Repeating our PW example, we have

AW(12) = -16(A/P,12,5) + 3 + 4(A/F,12,5)

= -16(.2774) + 3 + 4(.1574)

3,000

50

4,000

16,000

Annual Worth; Example

Repeating our PW example, we have

AW(12) = -16(A/P,12,5) + 3 + 4(A/F,12,5)= -16(.2774) + 3 + 4(.1574)= -.808= -$808

3,000

50

4,000

16,000

Alternately

AW(12) = PW(12) (A/P, 12%, 5) = -2.92 (.2774) = - $810 < 0 NO

GOOD

3,000

50

4,000

16,000

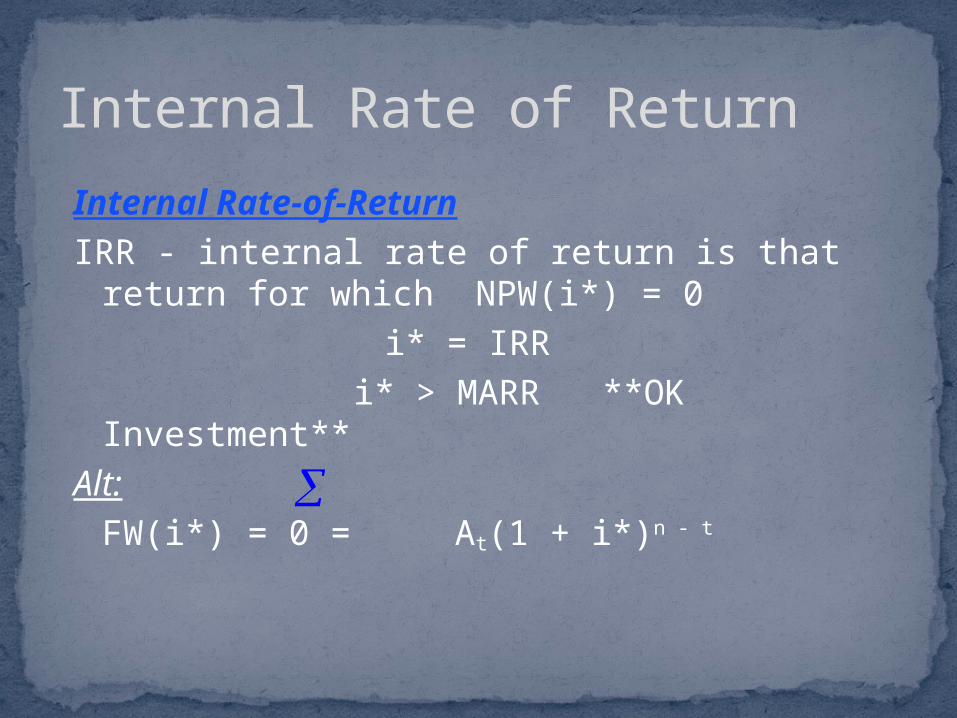

Internal Rate-of-ReturnIRR - internal rate of return is that

return for which NPW(i*) = 0 i* = IRR

i* > MARR **OK Investment**

Internal Rate of Return

Internal Rate-of-ReturnIRR - internal rate of return is that

return for which NPW(i*) = 0 i* = IRR

i* > MARR **OK Investment**

Alt:FW(i*) = 0 = At(1 + i*)n - t

Internal Rate of Return

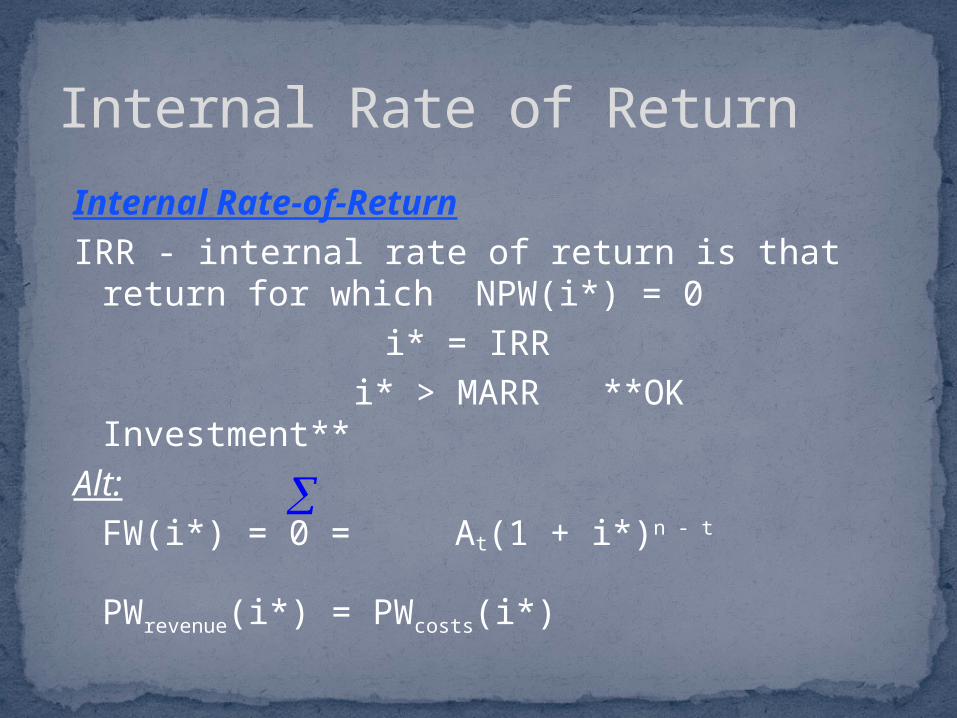

Internal Rate-of-ReturnIRR - internal rate of return is that

return for which NPW(i*) = 0 i* = IRR

i* > MARR **OK Investment**

Alt:FW(i*) = 0 = At(1 + i*)n - t

PWrevenue(i*) = PWcosts(i*)

Internal Rate of Return

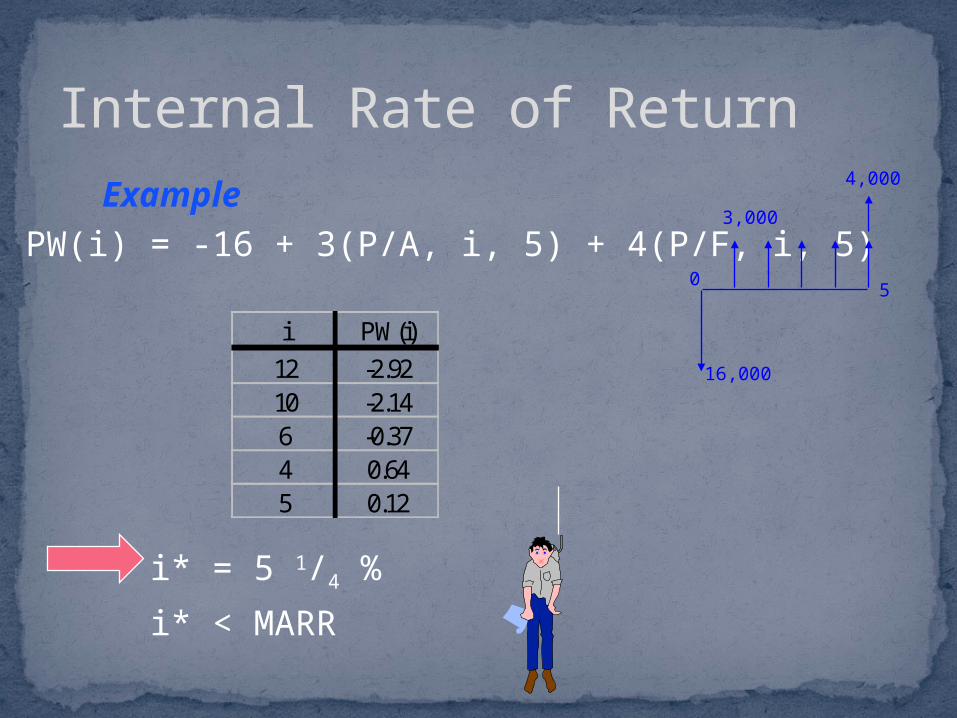

ExamplePW(i) = -16 + 3(P/A, i, 5) + 4(P/F, i, 5)

Internal Rate of Return

3,000

50

4,000

16,000

ExamplePW(i) = -16 + 3(P/A, i, 5) + 4(P/F, i, 5)

Internal Rate of Return

i PW(i)

12 -2.9210 -2.146 -0.374 0.645 0.12

3,000

50

4,000

16,000

ExamplePW(i) = -16 + 3(P/A, i, 5) + 4(P/F, i, 5)

i* = 5 1/4 %

i* < MARR

Internal Rate of Return

i PW(i)

12 -2.9210 -2.146 -0.374 0.645 0.12

3,000

50

4,000

16,000

Spreadsheet Example

1

2

3

456789

10111213

A B C D E F

ExamplePeriod Cash Flow

0 (16,000)1 3,0002 3,0003 3,0004 3,0005 7,000 MARR = 12.0%

NPV = (2,916) = NPV(E9,C5:C9)+ C4PMT = (809) = -PMT(E9,5,C10)IRR = 5.2% = IRR(C4:C9,E9)

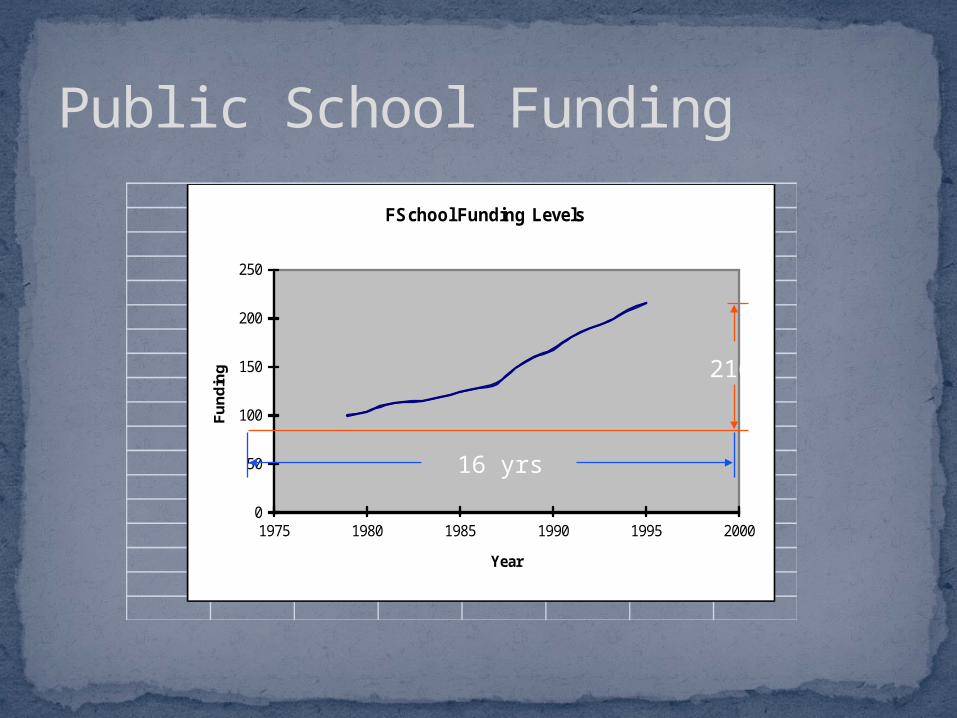

Public School Funding

0

50

100

150

200

250

1975 1980 1985 1990 1995 2000

Fu

nd

ing

Year

FSchool Funding Levels

Public School Funding

0

50

100

150

200

250

1975 1980 1985 1990 1995 2000

Fu

nd

ing

Year

FSchool Funding Levels

216%

16 yrs

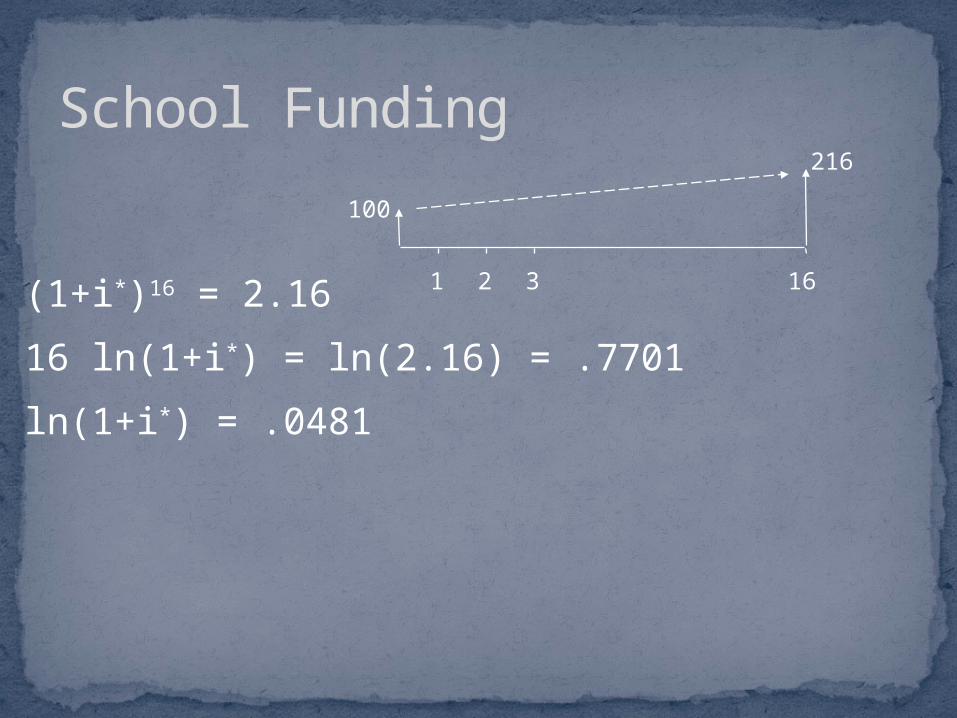

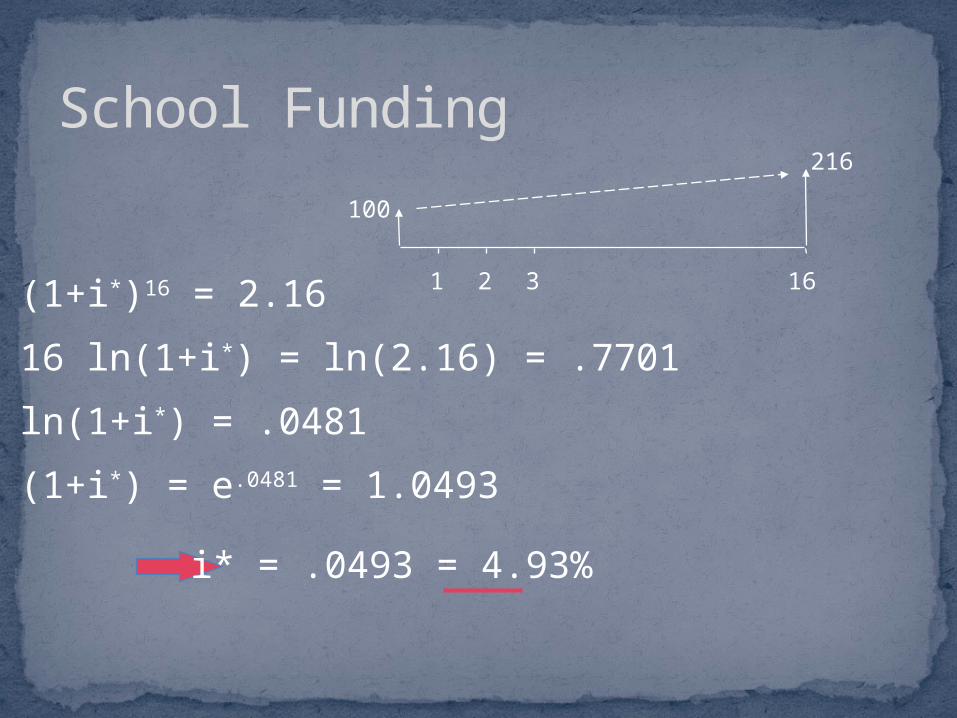

School Funding

1 2 3 16

100

216

F = P(F/P,i*,16)

(F/P,i*,16) = F/P = 2.16

(1+i*)16 = 2.16

School Funding

1 2 3 16

100

216

(1+i*)16 = 2.16

16 ln(1+i*) = ln(2.16) = .7701

School Funding

1 2 3 16

100

216

(1+i*)16 = 2.16

16 ln(1+i*) = ln(2.16) = .7701

ln(1+i*) = .0481

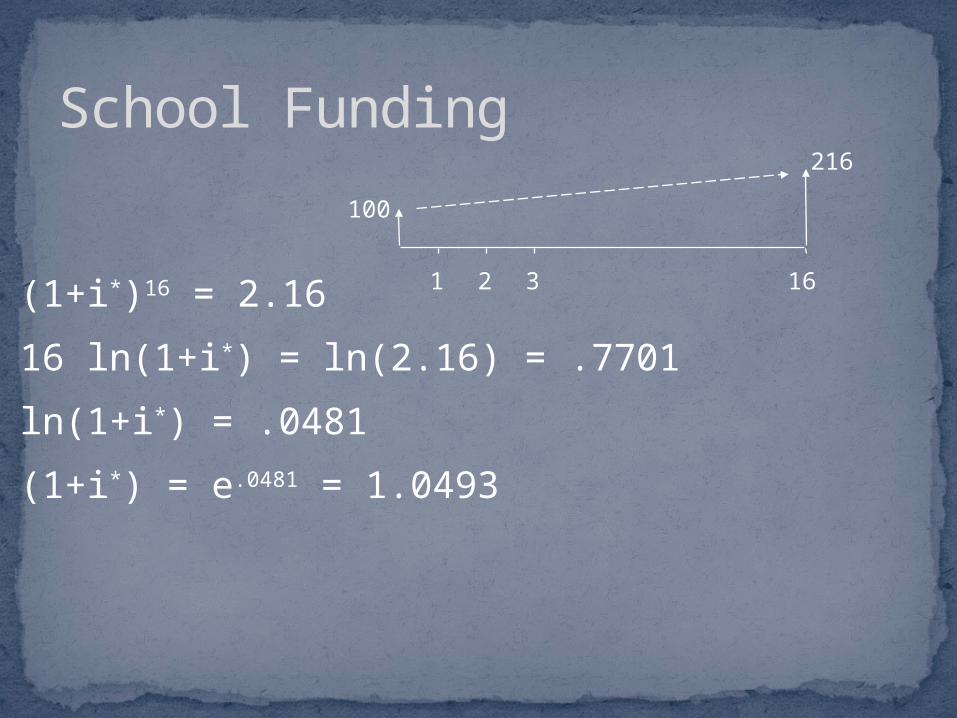

School Funding

1 2 3 16

100

216

(1+i*)16 = 2.16

16 ln(1+i*) = ln(2.16) = .7701

ln(1+i*) = .0481

(1+i*) = e.0481 = 1.0493

School Funding

1 2 3 16

100

216

(1+i*)16 = 2.16

16 ln(1+i*) = ln(2.16) = .7701

ln(1+i*) = .0481

(1+i*) = e.0481 = 1.0493

i* = .0493 = 4.93%

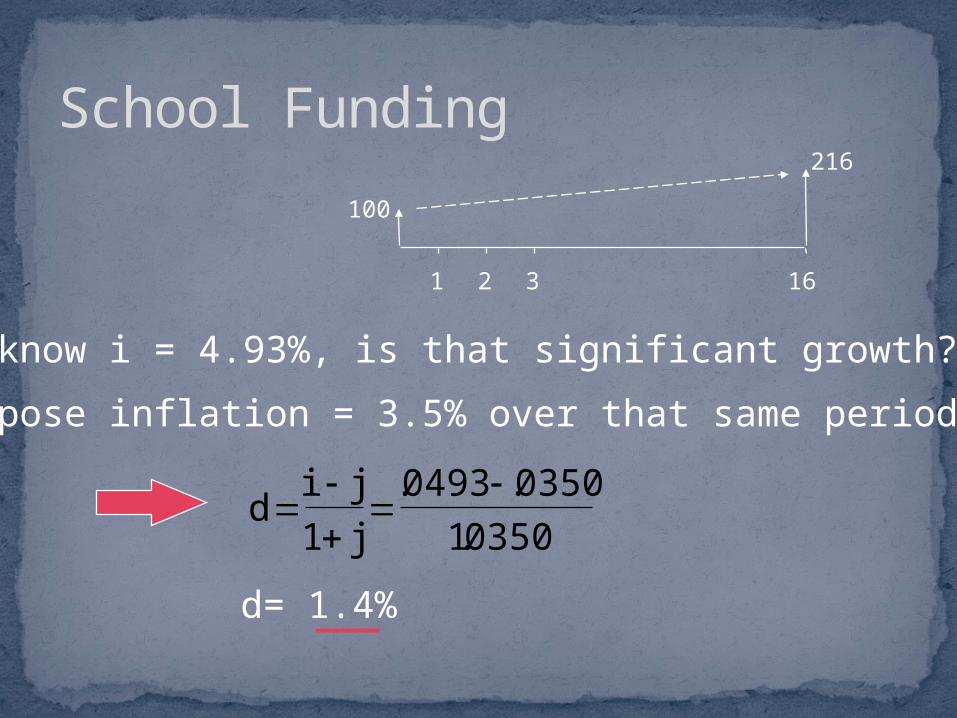

School Funding

1 2 3 16

100

216

We know i = 4.93%, is that significant growth?

School Funding

1 2 3 16

100

216

We know i = 4.93%, is that significant growth?

Suppose inflation = 3.5% over that same period.

School Funding

1 2 3 16

100

216

We know i = 4.93%, is that significant growth?

Suppose inflation = 3.5% over that same period.

di j

j

1

0493 0350

10350

. .

.

d= 1.4%

NPW > 0 Good Investment

Summary

NPW > 0 Good Investment

EUAW > 0 Good Investment

Summary

NPW > 0 Good Investment

EUAW > 0 Good Investment

IRR > MARR Good Investment

Summary

NPW > 0 Good Investment

EUAW > 0 Good Investment

IRR > MARR Good Investment

Note: If NPW > 0 EUAW > 0IRR > MARR

Summary

IRR Problems

1,000

4,100

5,580

2,520

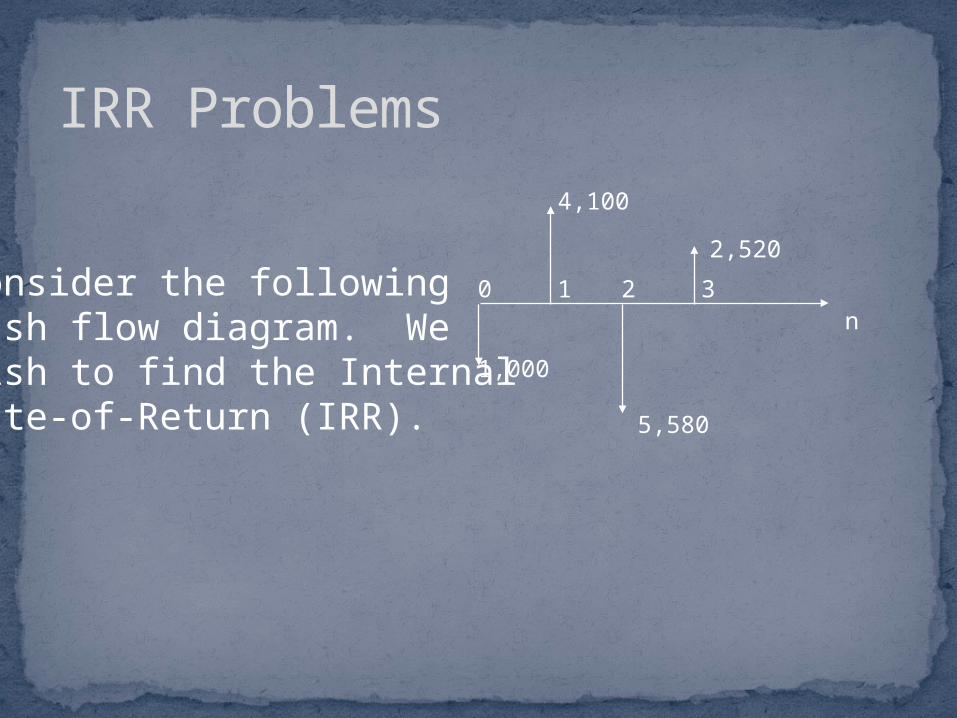

n0 1 2 3Consider the following

cash flow diagram. We wish to find the InternalRate-of-Return (IRR).

IRR Problems

1,000

4,100

5,580

2,520

n0 1 2 3Consider the following

cash flow diagram. We wish to find the InternalRate-of-Return (IRR).

PWR(i*) = PWC(i*)

4,100(1+i*)-1 + 2,520(1+i*)-3 = 1,000 + 5,580(1+i*)-2

IRR Problems

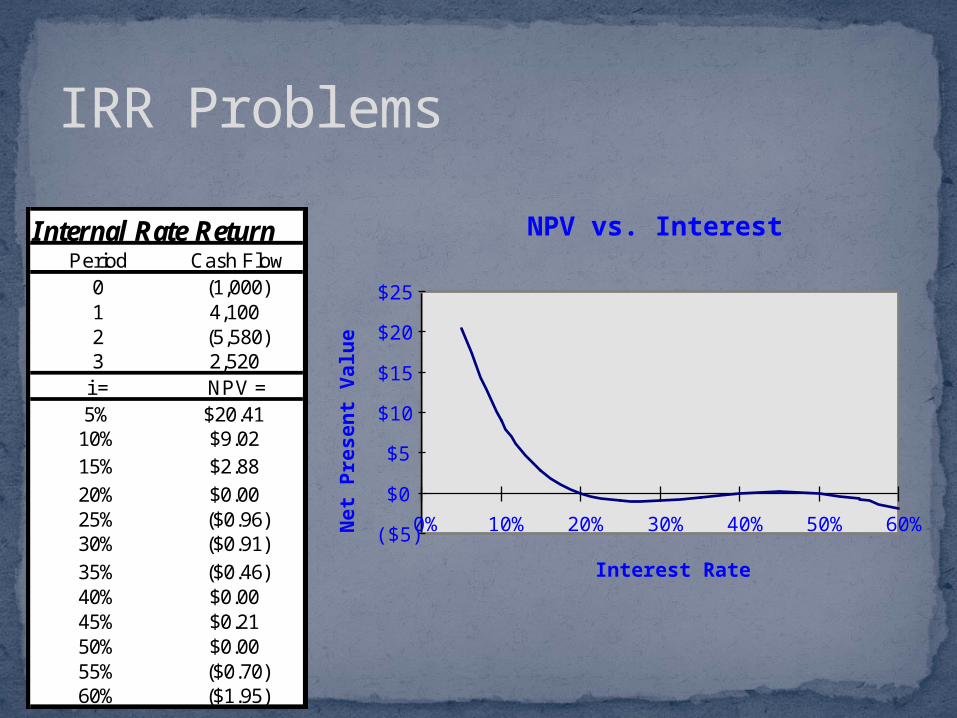

Internal Rate ReturnPeriod Cash Flow

0 (1,000)1 4,1002 (5,580)3 2,520

i = NPV =5% $20.41

10% $9.0215% $2.88

20% $0.0025% ($0.96)30% ($0.91)

35% ($0.46)40% $0.0045% $0.2150% $0.0055% ($0.70)60% ($1.95)

NPV vs. Interest

($5)

$0

$5

$10

$15

$20

$25

0% 10% 20% 30% 40% 50% 60%

Interest Rate

Ne

t P

res

en

t V

alu

e

Purpose: to get around a problem of multiple roots in IRR methodNotation:

At = net cash flow of investment in period t

At , At > 0

0 , else -At , At < 0

0 , else rt = reinvestment rate (+) cash flows

(MARR) i’ = rate return (-) cash flows

External Rate of Return

Rt =

Ct =

Method

find i = ERR such that

Rt (1 + rt) n - t = Ct (1 + i’) n - t

Evaluation

If i’ = ERR > MARR Investment is Good

External Rate of Return

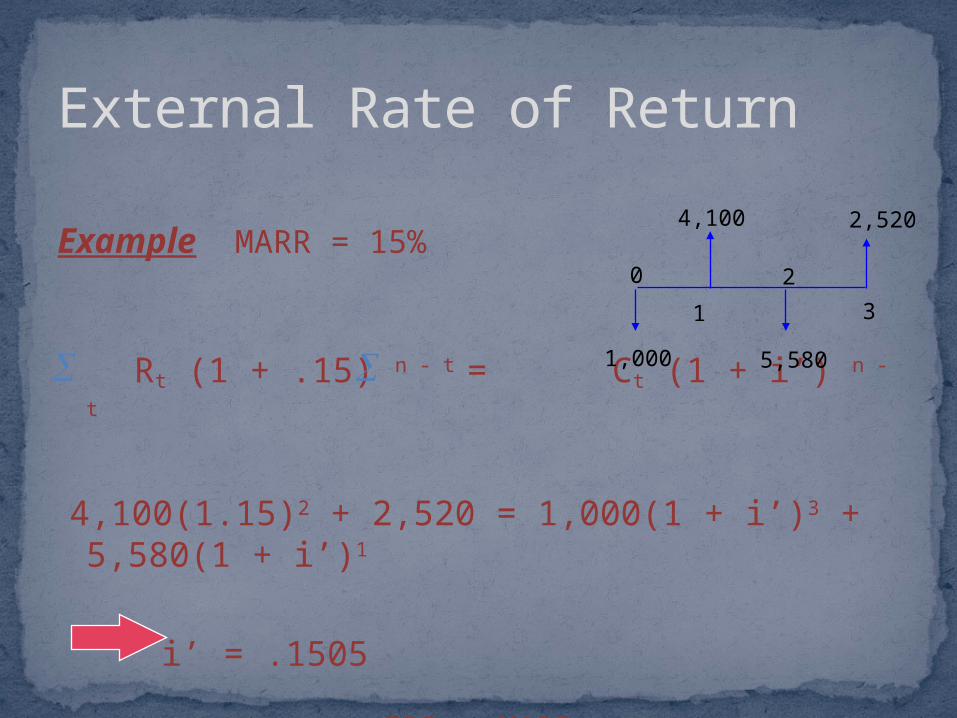

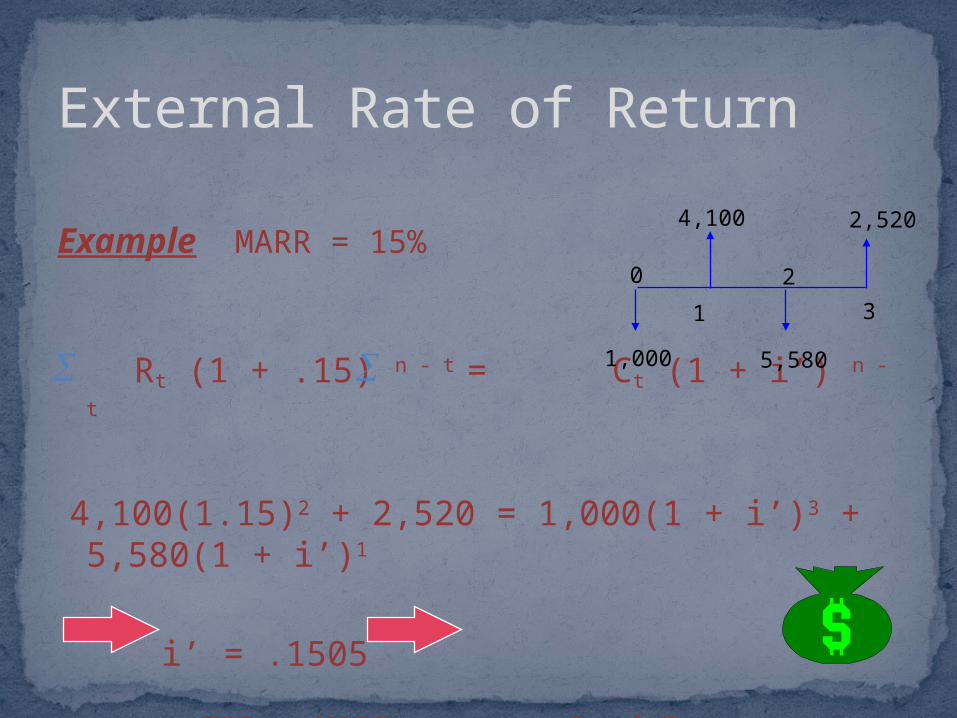

Example MARR = 15%

Rt (1 + .15) n - t = Ct (1 + i’) n - t

4,100(1.15)2 + 2,520 = 1,000(1 + i’)3 + 5,580(1 + i’)1

i’ = .1505

External Rate of Return

0

1

2

3

1,000

4,100

5,580

2,520

Example MARR = 15%

Rt (1 + .15) n - t = Ct (1 + i’) n - t

4,100(1.15)2 + 2,520 = 1,000(1 + i’)3 + 5,580(1 + i’)1

i’ = .1505

ERR > MARR

External Rate of Return

0

1

2

3

1,000

4,100

5,580

2,520

Example MARR = 15%

Rt (1 + .15) n - t = Ct (1 + i’) n - t

4,100(1.15)2 + 2,520 = 1,000(1 + i’)3 + 5,580(1 + i’)1

i’ = .1505

ERR > MARR Good Investment

External Rate of Return

0

1

2

3

1,000

4,100

5,580

2,520

Method 1 Let i = MARR

SIR(i) = Rt (1 + i)-t

Ct (1 + i)-t

= PW (positive flows) -

PW (negative flows)

Savings Investment Ratio

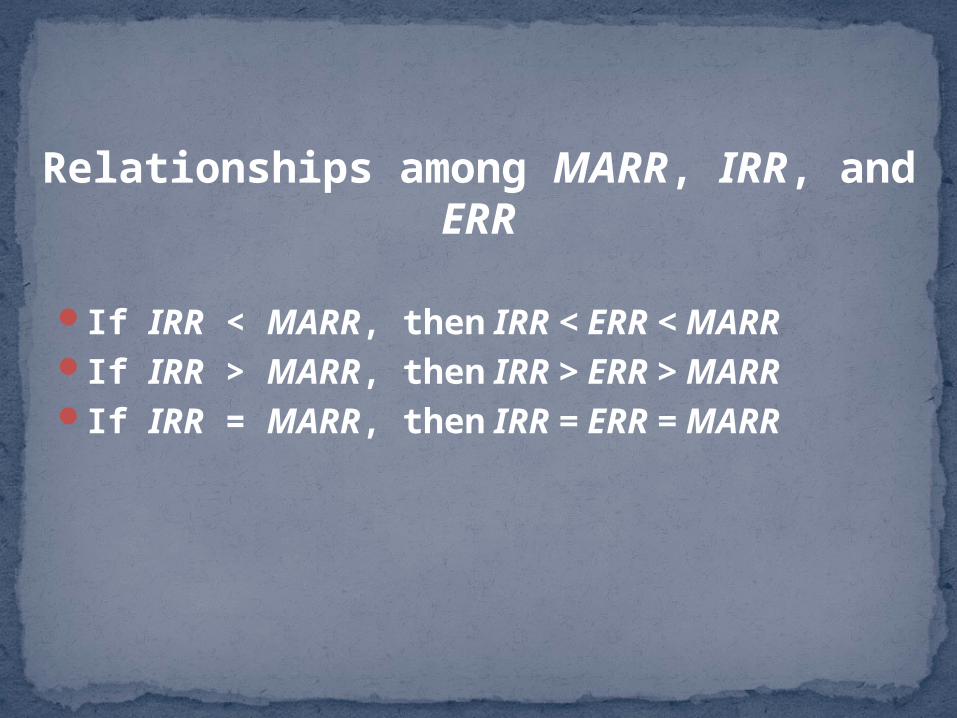

Relationships among MARR, IRR, and ERR

If IRR < MARR, then IRR < ERR < MARRIf IRR > MARR, then IRR > ERR > MARRIf IRR = MARR, then IRR = ERR = MARR

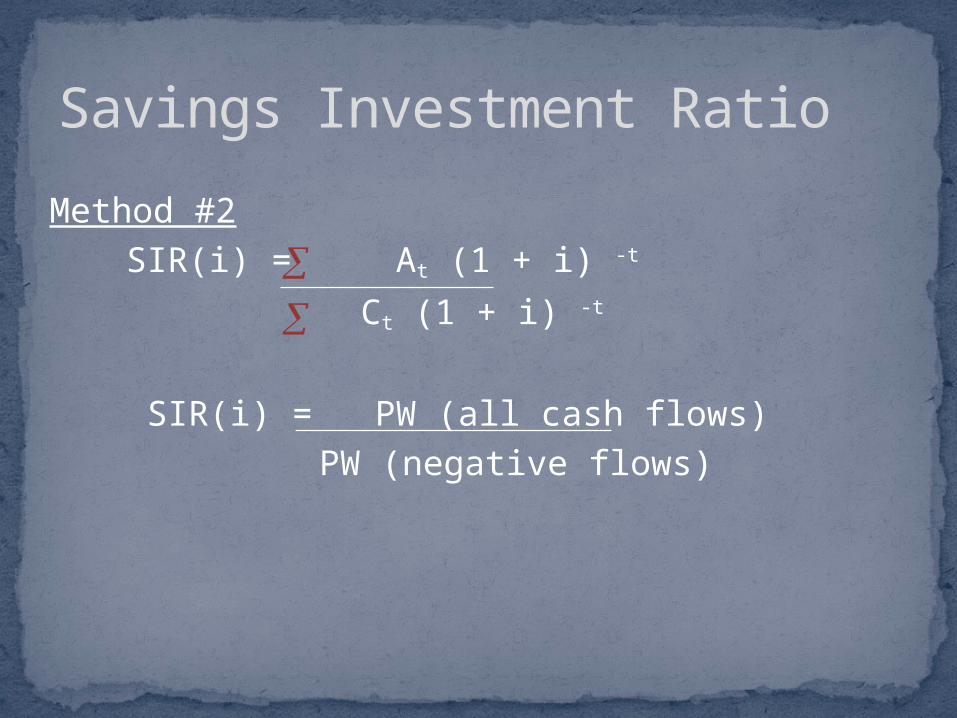

Method #2SIR(i) = At (1 + i) -t

Ct (1 + i) -t

SIR(i) = PW (all cash flows) PW (negative flows)

Savings Investment Ratio

Method #2SIR(i) = At (1 + i) -t

Ct (1 + i) -t

SIR(i) = PW (all cash flows) PW (negative flows)

Evaluation:Method 1: If SIR(t) > 1 Good Investment

Method 2: If SIR(t) > 0 Good Investment

Savings Investment Ratio

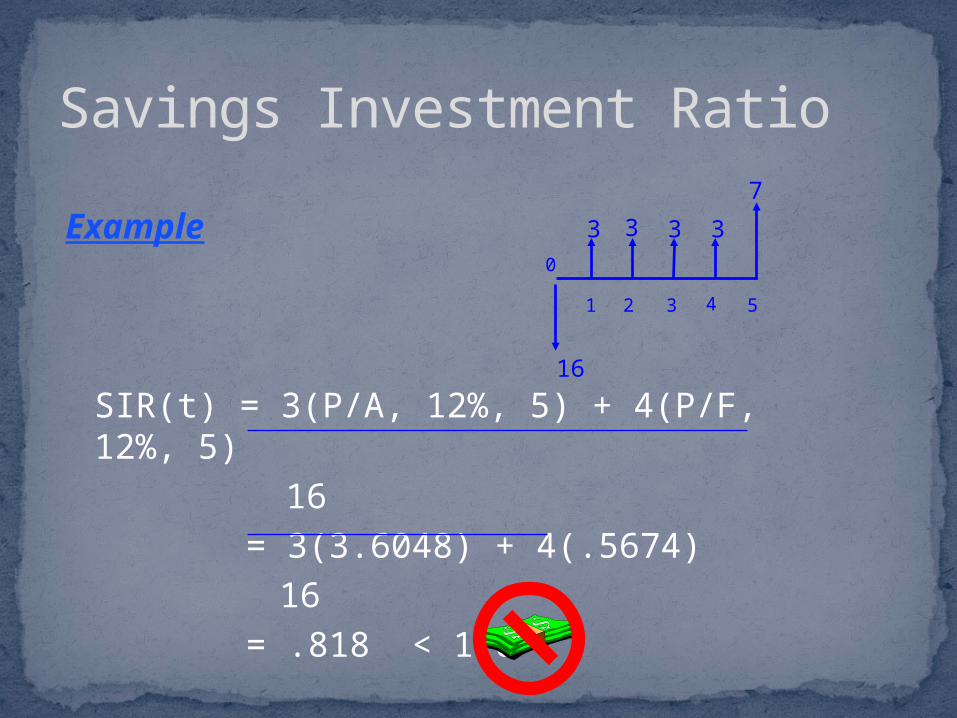

Example

SIR(t) = 3(P/A, 12%, 5) + 4(P/F, 12%, 5)16

= 3(3.6048) + 4(.5674) 16

= .818 < 1.0

Savings Investment Ratio

16

0

1 2 3 4 5

3 3 3 3

7

Example

SIR(t) = 3(P/A, 12%, 5) + 4(P/F, 12%, 5)16

= 3(3.6048) + 4(.5674) 16

= .818 < 1.0

Savings Investment Ratio

16

0

1 2 3 4 5

3 3 3 3

7

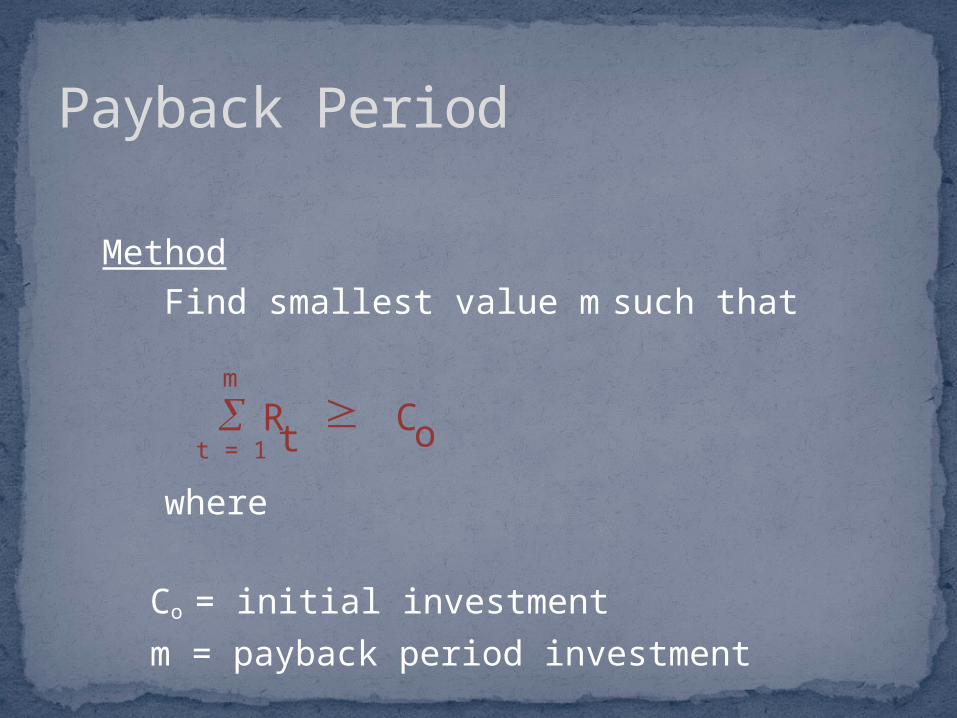

Method Find smallest value m such that

where

Co = initial investment

m = payback period investment

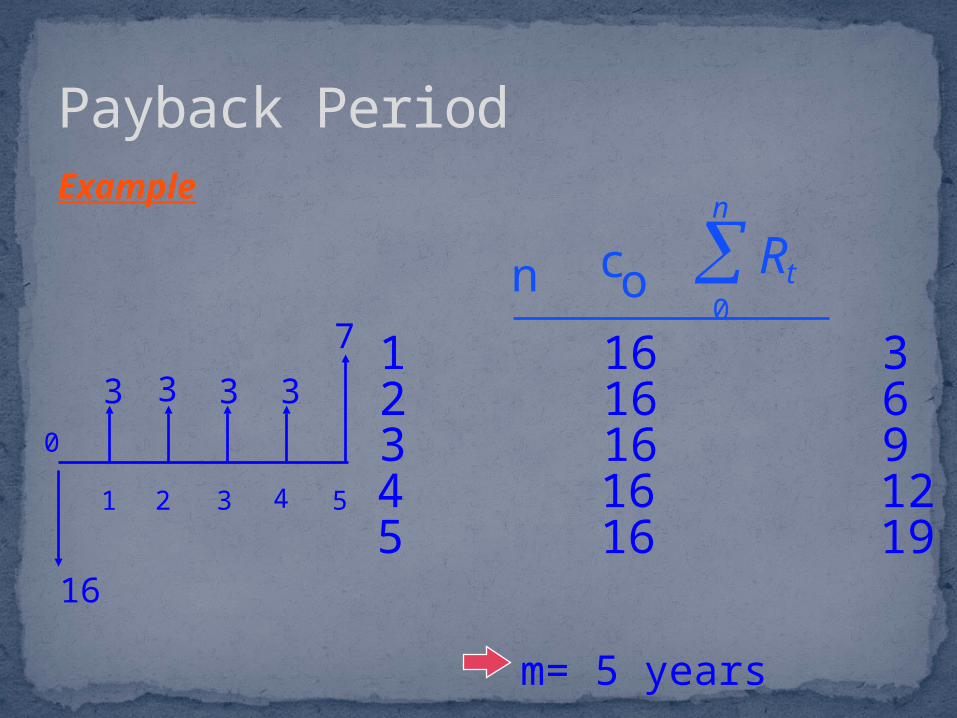

Payback Period

m

t = 1Rt Co

Example

Payback Period

m= 5 years

n co

1 16 3

3 16 94 16 125 16 19

2 16 6

16

0

1 2 3 4 5

3 3 3 3

7

Rtn

0

å

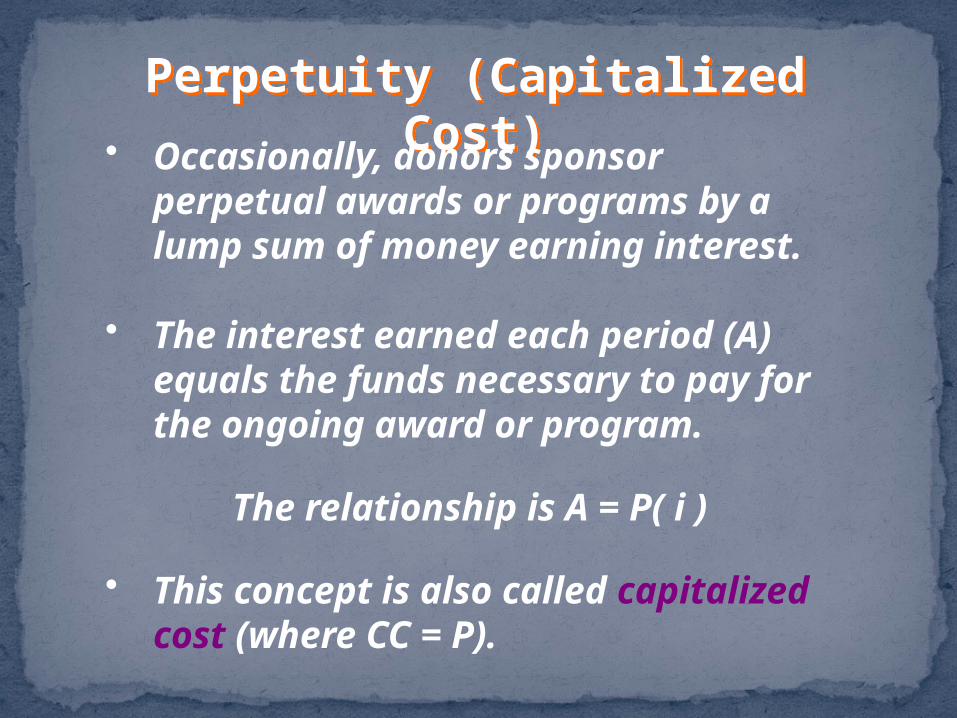

Perpetuity (Capitalized Cost)

Perpetuity (Capitalized Cost)• Occasionally, donors sponsor

perpetual awards or programs by a lump sum of money earning interest.

• The interest earned each period (A) equals the funds necessary to pay for the ongoing award or program.

The relationship is A = P( i )

• This concept is also called capitalized cost (where CC = P).

Perpetuity ExamplePerpetuity ExampleA donor has decided to establish a $10,000 per year scholarship. The first scholarship will be paid 5 years from today and will continue at the same time every year forever. The fund for the scholarship will be established in 8 equal payments every 6 months starting 6 months from now.

Determine the amount of each of the equal initiating payments, if funds can earn interest at the rate of 6% per year with semi-annual compounding.

Perpetuity ProblemPerpetuity ProblemGiven:

A = 10 000 per year, every year after Year 5

n = 8 payments @ 6 mo. intervals, starting @ 6 mo.

i = 6%, cpd semi-annually Find Amount of Initiating payments (Ai ):

Perpetuity ProblemPerpetuity ProblemGiven:

A = 10 000 per year, every year after Year 5

n = 8 payments @ 6 mo. intervals, starting @ 6 mo.

i = 6%, cpd semi-annually Find Amount of Initiating payments (Ai ):

A flood control project has a construction cost of $10 million, an annual maintenance cost of $100,000. If the MARR is 8%, determine the capitalized cost necessary to provide for construction and perpetual upkeep.

Class Problem

A flood control project has a construction cost of $10 million, an annual maintenance cost of $100,000. If the MARR is 8%, determine the capitalized cost necessary to provide for construction and perpetual upkeep.

Class Problem

1 2 3 4. . .

100 100 100 100

10,000

Pc = 10,000 + A/i = 10,000 + 100/.08 = 11,250

Capitalized Cost = $11.25 million

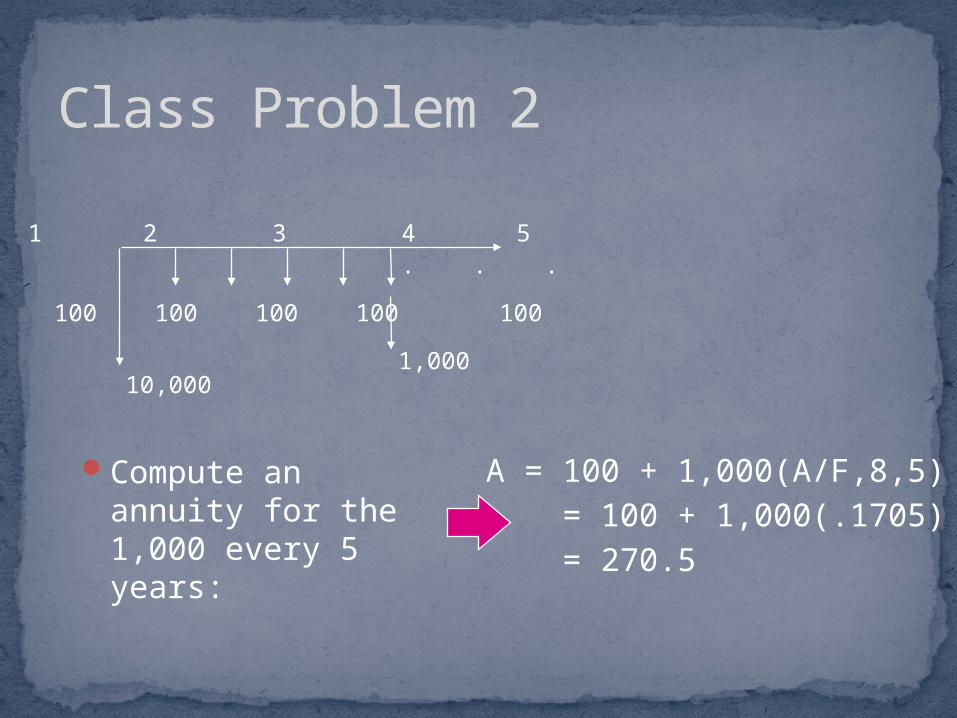

Suppose that the flood control project has major repairs of $1 million scheduled every 5 years. We now wish to re-compute the capitalized cost.

Class Problem 2

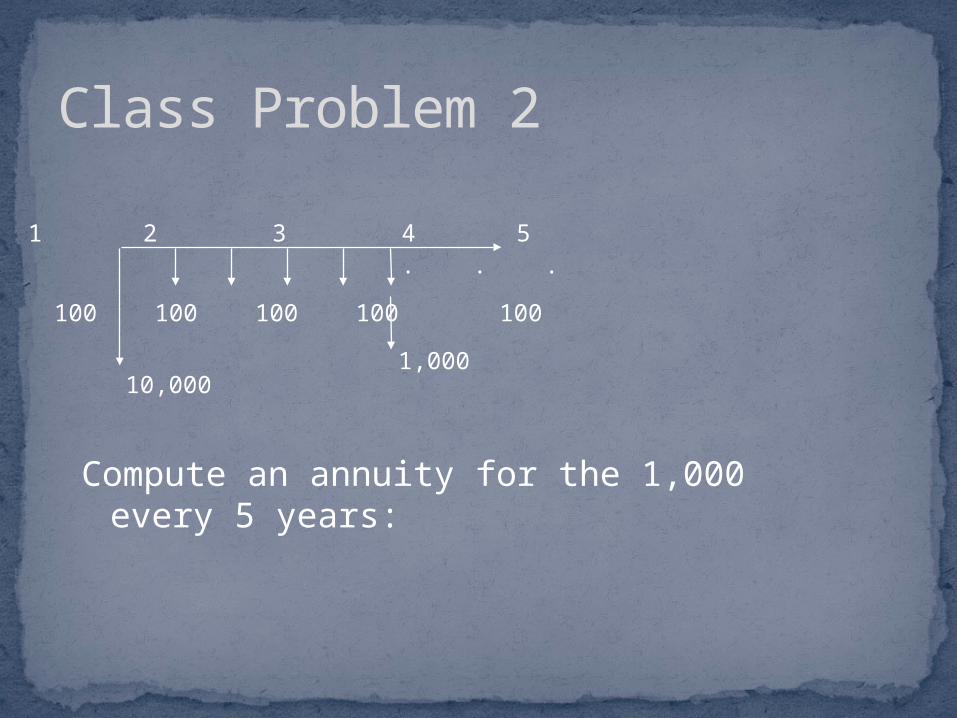

Compute an annuity for the 1,000 every 5 years:

Class Problem 2

1 2 3 4 5. . .

100 100 100 100 100

10,0001,000

Compute an annuity for the 1,000 every 5 years:

Class Problem 2

1 2 3 4 5. . .

100 100 100 100 100

10,0001,000

A = 100 + 1,000(A/F,8,5) = 100 + 1,000(.1705) = 270.5

Class Problem 2

1 2 3 4 5. . .

170.5 170.5 170.5 170.5

10,000

Pc = 10,000 + 270.5/.08

= 13,381

1 2 3 4 5. . .

100 100 100 100 100

10,0001,000

How Many to Change a Bulb?

How does Bill Gates changea light bulb?

How Many to Change a Bulb?

How does Bill Gates changea light bulb?

He doesn’t, he declares darknessa new industry standard!!!

How Many to Change a Bulb?

How many Industrial Engineers does it take to change a light bulb?

How Many to Change a Bulb?

How many Industrial Engineers does it take to change a light bulb?

None, IE’s only change dark bulbs!!!!!