investments in customer centricity are seeing dividends for financial services firms

TRANSCRIPT

Investments in Customer Centricity Are Seeing Dividends for Financial Services Firms

A look at how Retail Banks and Insurance Companies are evolving their product-focused missions into customer-centric strategies for financial gains

Exerpted Articles From:

1to1 ®

mediaa division of Peppers & Rogers Group

©2014 www.1to1media.com 2

Retail banking is undergoing a massive disruption. While banks have traditionally been the provid-ers of retail services, they’re now facing real competitive threats as new mobile technologies and emerging financial and non-financial intermediaries combine to provide trusted alternatives and less-expensive solutions for both the unbanked and for profitable customers.

Consumer banks are rapidly losing market share as a result. In fact, according to the 2013 Accenture study, Banking 2020, banks could lose about 35 percent of their market share by 2020, and up to 25 percent of U.S. banks could disappear completely.

The same study estimated that 15 percent of traditional banks’ revenues could shift to online-only players—including branchless banks and new technology entrants—in the next seven years as more consumers flock to technology driven services. Another 20 percent could go to “retail-driven players with a mass-market focus.”

Some of these non-traditional providers include Wal-Mart, which has partnered with American Express to offer Bluebird, an alternative to debit and checking accounts designed to enable con-sumers to deposit checks and pay bills via mobile devices, maintain a zero minimum balance, and avoid any overdraft fees; and 7-Eleven, which offers prepaid banking cards that enable customers with the ease of doing business by allowing ATM transactions, the purchase of money orders, fund transfers, check cashing, and bill pay.

In addition, online-only providers have made a splash on the scene. Top players include: Moven, an online debit account provider that promises to support its customers’ financial wellness through transparency, the ability to connect customers with their money 24/7, and the knowledge to make sound financial decisions; GoBank, which offers custom Visa and debit cards and mobile deposits; and Simple, which promises “no surprise fees,” offers budgeting tools, and boasts a branchless banking experience. [Note: Multinational bank BBVA acquired Simple in February 2014 for approximately $117 million, validating the importance of these new competitors.]

Traditional and non-traditional financial services institutions alike are seeing some of the big-gest advances happening in mobile banking. Accenture reported a 50 percent increase in mobile banking activity since 2012, with consumers saying online banking is the single most important investment banks can make.

By leveraging the wide range of mobile functionality available, including mobile POS such as Square and Paypal; near-field communication payments like Google Wallet; mobile banking, and in-app billing, traditional and non-traditional financial providers are offering a low-cost channel to acquire new customers and scale-up efficiently. In doing so, they’re hedging their bets for a share of the massive market currently dominated by the large consumer banking providers.

These mobile developments, as well as the introduction of mass market players, are posing a threat to financial institutions as profitable customers become less satisfied with their banks. According to the World Retail Banking Report 2013, from Capgemini and Efma, customers are mostly unsatisfied with their banks in five core areas: knowledge of customer’s needs and prefer-ences (37 percent satisfied); product-channel fit (43 percent satisfied); trust and confidence (51 percent satisfied); intimacy and relationship-building (43 percent satisfied); and providing a con-sistent multichannel experience (44 percent satisfied).

This research shows that today’s banks must understand their customers, repair their relation-ships, and focus on providing personalized cross-channel engagements to defend against new competitors, avoid commoditization, and ultimately lead to higher revenue growth.

These repairs will only work if they’re established upon a foundation of trust, which requires banks to deliver on the moments of truth for their customers, forming a trusted bond that trans-

forms the customer experience.

—Weston McDonald, Senior Vice President, Financial Services, TeleTech

Restoring Trust in Banking

Executive Overview:

Table of Contents

Executive Overview ............. 2

Banking ................................ 3

Insurance ........................... 33

©2014 www.1to1media.com 3

Every business—and every bank—has a corporate culture. And cultures are made up of attitudes, behav-

iors, and company values. The question of culture is a key one for banks that are looking to become more

customer-centric.

Customer centricity is a hot topic of discussion among banks in the Middle East in particular. It is a

strategy that both global and local banks are taking very seriously in their quest to stay ahead of growing

competition in the region.

At a time when most banks are struggling to grow, many banks in the region are well-capitalized and have the

funds at their disposal to exploit new growth. They are engaged in pursuing new revenue opportunities and diver-

sifying their income streams. In this environment, customer centricity fits as a natural strategy for many reasons.

Many banks are seeing impressive growth in the number of new, young customers. These customers are

increasingly sophisticated and value customer centricity. They see how customer focus is being applied in

other industries and with new technologies. They expect the financial services industry to keep up.

There is rising intolerance for bank service that simply goes through the motions. Customers

are demanding more. Relationships are very important culturally when doing business in the

region, and customers are looking to build a trusting relationship with their bank. Most want

respect in the relationship to be reciprocal. They want to be treated as people rather than

as just account numbers. Competition is fierce as banks look to capitalize on the region’s

wealth, its growing young population, and pace of economic development.

Most importantly, however, becoming a customer-centric bank can have tangible ben-

efits for the bottom line. Turkey’s Isbank, for example, implemented an enterprisewide

customer-centric transformation within the past few years, with its stated mission to be the

“bank closest to customers.” Working with Peppers & Rogers Group, it implemented measures

such as installing customer relationship managers in every branch, overseeing specific “cus-

tomer portfolios” (i.e., groups of customers with similar needs) and centralizing reporting functions

previously performed by branch personnel in order to allow more time to interact with customers.

This approach achieved some impressive results:

• Total assets rose by 130 percent

• Loans rose by 160 percent

• Deposits rose by 137 percent

• Net interest income rose by 140 percent

Creating a Customer-Centric Culture for Middle East BanksThe banking environment is primed for leaders to step up and transform their business around the customer to create long-term strength and stability in an ever-changing region.

Adapted from Customer Strategist Journal

Banks: ArticlesCreating a Customer-Centric Culture for Middle East Banks ...................................................... 3

SunTrust Learn Why Customers Behave the Way They Do ... 6

Customer Focus Sits at the Forefront in Financial Services ......................................................... 8

NedBank Embarks on a Client-Centric Journey ............ 10

What’s Keeping Banks From Reaching Their Innovation Potential in Social Media? ................... 12

Social Media Energizes Traditional Banking Strategy ...... 15Study Shows Potential for Social Media in Emerging Markets ...................................................... 18

Five Steps to Big Data Dominance in Banking ............... 19

Associated Banc-Corp’s Customer Listening Makeover..22

Financial Firms Cash in on VoC ...................................... 23

Akbank’s Analytics Initiative Improves the Customer Experience ............................................... 25

AMP Financial Services Invests in Knowledgebase Optimization ......................................... 27

la Caxia Banks on Innovation ......................................... 29

Standard Bank’s 4 Steps Toward Becoming a Customer-Focused Organization .................................... 31

Retail Banks

©2014 www.1to1media.com 4

Retail Banks

The end goal is for the new culture to be internalized rather than imposed from the outside. New ways of thinking and behavior should become automatic and the organization will use the new cultural principles to drive development and progress.

In addition, Isbank branches operating within the new business model increased their assets under

management by 25 percent compared to branches in which transformation initiatives were not carried out.

Egypt’s CIB is also very focused on customer service and customer-friendly banking channels. In a

2008 interview, CEO Hisham Ezz Al-Arab said that he believes the bank’s reputation for well-established

customer relationships is a distinct competitive advantage. He believes that each customer deserves to

enjoy a unique banking experience. The bank has invested heavily in training, for example, empowering a

knowledgeable workforce to provide an outstanding service.

The best examples of customer-centric transformation from anywhere in the world all share a common

thread—leadership that drives change in favor of customer focus.

What is the role of leadership in changing culture?

Strong leadership is integral for any bank that wants to develop a customer-centric corporate culture.

Leaders must be the driving force for cultural transformation and they must relentlessly promote values

such as openness, innovativeness, friendliness, and personalization that are key to a customer-centric

banking experience. A strong, consistent message from the top is a signal that customer service is no mere

window dressing and that employees need to take it seriously as a key priority.

The leader must articulate a vision for the future of the bank as an organization that focuses on custom-

ers’ needs through every process and on every level of doing business. For the truly customer-centric

bank, the customer IS king. The leader must help ever one in the bank understand this and lead them in

working together to make that vision a reality. The bank will first have to identify its strengths and weak-

nesses regarding customer centricity. Honest feedback from everyone in the company is desirable here

to get a true picture of the company culture as it really is, rather than what employees think management

would like it to be.

There are several tools banks can use for such assessments, ranging from in-house surveys to internal

working groups, that will best be determined according to the needs of the organization. In some cases,

bringing in outside consultants who specialize in change management can allow a bank to benefit from

others’ experiences and create a change plan based on proven methods.

The bank will also need to identify what customer centricity means for its organization and the expected

benefits of the change. These should be clearly outlined so that employees can see the reason for the

changes. Employees will be much more enthusiastic and much less resistant to positive change when they

can see that the desired changes will be good for the organization, as well as for them personally.

The end goal is for the new culture to be internalized rather than imposed from the outside. New ways

of thinking and behavior should become automatic and the organization will use the new cultural principles

to drive development and progress.

Going from the old culture to the new will not be accomplished instantly. Culture is deeply ingrained

and encompasses not only processes, but attitudes, assumptions, communication styles, goals and roles,

among other elements. True change will require carefully planned, step-by-step progress that is closely

monitored and guided by management.

A dedicated change management team, composed of representatives from all areas of the organization,

can oversee the change effort and help it stay on track. Leaders must clearly emphasize the importance of

the change management effort and give the team the status and authority needed to implement effective

initiatives.

Before the plan is rolled out, those spearheading the change initiatives must dig deep into the details

of how the organization can go from point A to point B. Part of this process must be anticipating how the

changes will affect people on a day-to-day basis, as well as thinking ahead to the questions and objections

that could be raised as every level of the organization.

©2014 www.1to1media.com 5

Retail Banks

Reaping the rewards

Transforming a bank’s corporate culture to be truly customer-centric is not an easy task, but it is a must

in the atmosphere of growing competition and high customer expectations that banks in the Middle East

are experiencing today.

Once leaders decide on a customer-centric cultural change, communication and consistency are criti-

cal, starting with the highest levels of the organization and working down to every single employee.

Ideally, each person in the organization will become an agent for change who can influence those

around him or her. Think of it as a cascade of change that starts at the top and gathers strength as it pours

down through the organization.

Middle East banks that succeed in creating a customer-centric corporate culture will reap the competi-

tive advantages of an improved reputation for customer service, stronger relationships with customers, a

mindset that contributes to more successful products designed with the customer in mind and more selling

opportunities, among others. Focusing on the customer is another way to focus on success for the future.

Once leaders decide on a customer-centric cultural change, communication and consistency are critical, starting with the highest levels of the organization and working down to every single employee.

©2014 www.1to1media.com 6

Retail Banks

“Grow consumer market and wallet share.” This is one of SunTrust Bank’s strategic priorities, formalized in

its 2011 annual report by Chairman and CEO William H. Rogers, Jr. Such a statement is easy to say, but can

be difficult to implement. There are many avenues a company can take to achieve such a goal. SunTrust

chose to shift its business from a product-focused orientation into one that is more customer-focused

and service-oriented. It’s a way to build relationships and stand out from competitors in the crowded and

volatile banking industry. “We believe that delivering industry-leading service quality will lead to improved

client loyalty and increased consumer wallet and market share,” Rogers wrote in a letter to shareholders

earlier this year.

Instead of giving in to the temptation of just customer acquisition, SunTrust is working to improve client

loyalty and share of wallet. In 2011, the company improved product penetration per relationship in eight of

its 10 largest markets, Rogers noted. What’s behind the company’s approach to customer relationships?

New actionable insight about customer behavior and the reasons behind their banking decisions.

“Customer centricity is the act of understanding, from the customer perspective, their needs and their

perception of the value proposition, then delivering it in the best possible way,” says Greg Holzwarth, man-

aging director of client information at SunTrust. To that end, his team is tasked with creating actionable

insight from both internal and external customer data. In the past, SunTrust studied customer behavior

and made strategic decisions based on how customers acted. But, that wasn’t enough. “We do just fine

in understanding client behavior,” he says. “We didn’t know the ‘why’ behind the behavior. We needed to

better understand customers’ attitudes and emotions around their behavior. Knowing why someone does

something is very useful.”

Deeper customer insight yields new opportunities

SunTrust, along with Peppers & Rogers Group’s iKnowtion analytics group and other partners, conducted a

survey of U.S. consumers to learn about how and why they make their banking decisions. With this insight,

the team created new multi-dimensional market segments that mixed behavioral and demographic infor-

mation with common attitudes and needs shared by members of each segment. SunTrust then mapped

the new segments to existing customers and prospects within its database to gain a clearer picture of

its customers. The new segments combine customer needs, value, behavior, and attitudes in a holistic

way. “We couldn’t influence positive behavior until we understood their attitudes, goals, and emotions,”

Holzwarth says.

SunTrust observed changing attitudes around borrowing money, for example. Since the financial crisis,

people still borrow money, but often it’s for something pragmatic like education, a new car, or healthcare.

They are less likely to borrow for extravagant or impractical reasons. And, they are looking for the bank to

help them manage not only the actual loan, but also the best way to pay it back.

“We’re now starting to marry our practices—how do we use that understanding to derive effective

interactions,” Holzwarth says. Internally, the new segments inform further market research, product devel-

opment, and value proposition development. Externally, the insight guides advertising, direct marketing,

and channel management decisions. This allows the company to optimize channels and interact appropri-

ately with the right types of customers. In the loan example, bank employees are also encouraged to have

SunTrust Learns Why Customers Behave the Way They DoThe bank uses customer data and predictive analytics to be more relevant to customers and prospects, leading to improved satisfaction, revenue, and loyalty.

Adapted from Customer Strategist Journal

“ We believe that delivering industry-leading service quality will lead to im-proved client loyalty and increased consumer wallet and market share.”

—William H. Rogers, Jr., Chairman and CEO, SunTrust Bank

©2014 www.1to1media.com 7

Retail Banks

‘‘ ’’a- ‘‘ ’’ha

conversations about customer cash flow and offer advice on the best ways to pay back the loan.

An understanding of customer needs and attitudes also helped ease dissatisfaction when the company

recently transitioned away from its free checking program. The company looked at which customers would

be impacted and determined unique ways to communicate with different customer groups. SunTrust was

required to notify all customers, but those above the minimum deposit threshold received a different

message than those who would be charged the fee. The team overlaid attitudinal and other information

about those segments to create a strategy around how to help them make that journey. “We helped them

understand what’s happening, explained how it will affect them, and offered potential ways to avoid the

fee or cope with the issue,” Holzwarth says. In addition, employees were trained to acknowledge customer

anger and be patient with customers as they processed this information.

Holzwarth notes that the initiative exceeded its goals. Overall satisfaction and loyalty initially dipped when the

news was announced, as expected, but it’s now higher than it was before the free checking program ended.

This new information also helps to enable CEO Rogers’ vision of a service-based culture. “We’re moving

away from a traditional bank/client relationship,” Holzwarth says. “In the past we’ve put it on clients to figure

out what they need, then come to us. Now we build awareness and help them figure out what they need in

a way that’s best for them.”

The sales function is evolving into more of an advisory role, for example. The goal now is to better under-

stand client needs, then package a solution to meet those needs. “We’re striving to change the experience

so it doesn’t feel as much like a traditional sales process,” he says. Instead, “we’re solution processing.”

Salespeople create a dialogue with customers about their needs and circumstances before the sale is

introduced. “It becomes a completely different conversation when it’s not led by the product,” Holzwarth

says. The company hasn’t removed the notion of “sales,” but it’s now at the tail end of the process.

SunTrust’s analytics activities also revealed opportunity for improved customer communications. By

observing customer behavior together with their attitudes and needs, Holzwarth’s team quickly discovered

that customers did not think in product terms. “The big a-ha moment was that none [of what customers

talked about] was in the vocabulary of traditional banking products,” he says. No one ever mentioned the

word “account,” for example. SunTrust changed how it spoke to customers to consider the client point of

view. The word “client” is now a noun that is spoken in internal business discussions, something Holzwarth

says was missing before. “Conversations need to change so they are in the customers’ language,” he says.

For example, SunTrust is in the midst of creating a detailed customer experience process based on sav-

ings from a customer point of view. It is enhancing its automatic bill pay tools so clients can create savings

buckets with customizable nicknames. It will provide tools to help customers determine how much they

should save per pay period, and set up automatic transfers into this new bucketed account. Customers can

use the technology to pay themselves first and save for an upcoming event or purchase. It requires no new

deployments on the bank’s part. All that’s needed is the customer perspective.

“It’s not earth-shattering stuff, but it’s important and relevant to customers,” Holzwarth says. “We’re chang-

ing the way we talk about and represent our products,” which involves simply changing the conversation.

It’s not the initiative that’s important, he adds. It’s the strategy and philosophy behind it. “Think about

attitudes, not just behavior, and think about your strategy to influence positive attitudes and behavior for

clients and the business,” Holzwarth says.

A culture evolves

Like many executives, Holzwarth doesn’t like to use the word ‘culture’ when discussing SunTrust’s inter-

nal approach to doing business. For him, the term represents something that may not be perceived as

actionable. Instead, he’s proud of the fact that customer centricity is woven into the fabric of the company.

“It’s ingrained into what we do, rather than having to go through a checklist,” he says, adding that it’s not

just marketing’s job to think about the customer experience. “Everyone’s a part of it, rather than being

reminded that they have to think about the customer. We’re all redesigning the client journey

“ The big a-ha moment was that none [of what customers talked about] was in the vocabulary of traditional banking products.”

—William H. Rogers, Jr., Chairman and CEO, SunTrust Bank

©2014 www.1to1media.com 8

Retail Banks

Success in the financial industry pivots around building strong and lasting relationships. When a client

charges an organization with taking care of his financial security, he is putting a high level of trust in assum-

ing that the business will act in his best interests and do its best to safeguard his finances.

The financial crisis has shone a spotlight on the need for organizations to be trustworthy and act in the

best interest of their customers. This event brought to the fore the vulnerability of the financial industry, the

need for regulations, and emphasized the importance of transparency.

This focus on relationships, trust, and doing what’s right for clients makes it imperative that financial

organizations adopt a customer-centric strategy. Yet, the industry has a transaction-based legacy. In

many cases, customers are thought of in terms of their account balances only. Financial institutions often

struggle to execute the philosophy of customer centricity and embed it in their day-to-day operations. It’s

too easy to fall back on the traditional ways of handling customers and accounts where products trump

individual customer value.

Three pillars of customer centricity

Transforming an organization into a truly customer-centric entity isn’t an easy task that happens over-

night. However, organizations that invest in the right people and processes are able to become more

client-focused, using this strategy as a differentiator in a cutthroat environment.

Customer data is of fundamental importance in this transformative endeavor. Often financial organiza-

tions believe they don’t have sufficient customer information. Although this may be true, often we observe

that many companies don’t use existing available customer information to the full extent and instead seek

to collect more. Similarly, we observe that customer data is rarely stored and shared, and what is shared

remains in product silos.

Such processes fail to bring together the different data points that allow the organization to have a

360-degree view of its clients on which to base future decisions. Forward-thinking businesses are bridging

their different data silos to get a holistic picture of customers. They use this information as the basis of their

decisions, leading to a companywide strategy that drives business results while doing what’s right for the

customer.

When it comes to an organization’s nature, customer focus needs to be ingrained in the makeup of an

organization. After organizing their data, financial institutions need to determine who owns customer rela-

tions, and then work toward setting up departments to manage this holistic view of customers. Although

organizations need to move from being product-focused to being customer-centric, it’s possible for an

organization to have a customer-centric strategy while retaining product expertise and working to make

them the best for its clients.

Finally, customer focus needs to be visible throughout the organization, from the C-suite right down to

frontline employees. Customer-centric organizations make decisions for the benefit of customers rather

than just for financial gains. The attitudes of all employees must reflect that. At Peppers & Rogers Group,

we help businesses implement this philosophy and ensure it’s practiced and not merely praised.

“ After organizing their data, financial institu-tions need to determine who owns customer relations, and then work toward setting up departments to manage this holistic view of customers.”

Customer Focus Sits at the Forefront in Financial ServicesFinancial organizations are challenged more than ever with becoming truly

customer centric and gaining the trust of their clients.

Adapted from Customer Strategist Journal

©2014 www.1to1media.com 9

Retail Banks

Transforming into a client-focused company

In order to become customer centric, organizations need to steer away from the one-size-fits-all

approach and instead treat different customers differently. While there are a variety of ways to achieve

this with differing levels of complexity, we at Peppers & Rogers Group believe the strategy ultimately

comes down to four main steps:

1. Identify who customers are, use the information to get to know them and understand them, and start treating them as unique individuals.

2. Differentiate customers by segmenting them according to current and future value, allowing the organization to design and execute strategies that address the diverse needs of different customer groups.

3. Interact with customers to ensure comprehension of their goals and expectations, leading to more effective future interactions.

4. Customize both communications and offers according to customers’ expectations, needs, and

value to the organization.

Savvy financial services organizations have already begun ingraining customer centricity into their

DNA. Germany’s Fidor Bank uses Facebook to connect customers’ online, offline, and virtual worlds. And

Barclaycard recently launched its Ring MasterCard in the U.S., where interest rates, payment schedules,

and other features are crowdsourced by the community. These organizations, and others like them, are

guided by forward-thinking business leaders who are cognizant that a great customer experience is a

necessary differentiator without which the company’s success is jeopardized.

Progressive organizations are working on their data strategy and governance to enhance their capabili-

ties to identify and create a 360-degree view of their client-base. More advanced businesses are creating

segmentation models that don’t only focus on customer value, but also incorporate behavior and needs.

They are working on customized client value propositions and contact strategies to better interact with

their customers and get to know them.

Customer focus isn’t the future. The necessity for organizations to become customer centric is here

now. Those firms that haven’t embarked on a process to become truly customer centric should not waste

any more time. Otherwise, customers will pivot towards competitors that exude customer centricity and

trustability.

“ Progressive organizations are working on their data strategy and governance to enhance their capabili-ties to identify and create a 360-degree view of their client-base.”

©2014 www.1to1media.com 10

Retail Banks

The banking industry has traditionally not been known to be client-centric. However, cutthroat competition

and more discerning customers have impelled a number of banks to start focusing on becoming just that.

Nedbank, one of South Africa’s largest banks, is one financial organization that’s aspiring to be totally

client-centric. In the words of Doug Hardie, executive general manager at Nedbank, “we want to get to the

stage where client centricity becomes part of our DNA.”

Cognizant that this is not an overnight endeavor, Nedbank embarked on a journey towards client cen-

tricity five years ago. Hardie says the team spearheading the change recognized that the only way to

succeed was if the transformation was embraced whole-heartedly by the company’s leadership. While this

took some time, Mike Brown, the bank’s chief executive, is passionate about being client sensitive and

has surrounded himself with like-minded people. “That passion is shining through very clearly in everything

the leadership team does,” Hardie says. “This has to be the single, most-important success factor.” The

commitment towards client centricity is deeply embedded in the bank’s strategy and three-year-plan’s

aspiration to “build many deep and enduring client relationships.”

The very first step was identifying areas within the organization that were not working as well as they

should. “We had to start working consistently on a strategic journey to get the basics right,” says Hardie.

After addressing the fundamentals, the bank started working upwards, methodically and consistently

bringing change to all tiers of the organization.

In order to deliver world-class service, Nedbank’s leadership was committed to creating brand ambas-

sadors, starting with its own employees. The organization embarked on a seven-pillar strategy to make

sure it had the right people in place:

• Getting its employees to be more client-focused

• Making the recruitment and selection process more client-centric

• Enhancing the induction process to expose new hires to the organization’s service-driven culture

• Developing the right skills through a robust learning and development curriculum

• Empowering staff members to deliver a magical client experience

• Measuring the day-to-day processes

• Rewarding and recognizing the right behavior, making it the focus of the organization

Underpinning all the pillars is a robust change management and communication strategy. To instill an

effective client engagement culture, Nedbank reviewed its client communications and created its Believe

to Achieve charter for customers:

• Know me and understand my aspirations

• Listen and care about my financial fitness

• Treat me with respect, value, and appreciate me and my business

• Give me great advice to make smart financial decisions

• Deliver with diligence—I only Ask Once

• Give me great value banking

An essential ingredient in this journey was to undertake an outside-in view from the clients’ eyes. Hardie

says this practice went from being an aspiration to increasingly manifesting itself in forums, decision-

making, and informed strategies.

“ We had to start working consistently on a strategic journey to get the basics right.”

— Doug Hardie Executive General manager, Nedbank

Nedbank Embarks on a Client-Centric Journey One of South Africa’s largest banks aspires to become more client-focused.

Adapted from Customer Strategist Journal

©2014 www.1to1media.com 11

Retail Banks

Measurement drives momentum

“Any strategic change journey requires constantly measuring and tracking improvements. In order to

succeed Nedbank established a robust voice of the customer strategy,” Hardie explains. Although the

organization had been tracking its client focus and Net Promoter Score (NPS) through an annual industry

study, to maintain momentum the bank wanted to establish an in-house client management capability.

“We developed a 35-agent outbound contact center to reach out to clients within 48 hours of an interac-

tion with the bank while the experience was still top of mind. After analyzing the 150,000 surveys that are

completed annually, a team of statistical experts score the results and mine client insights allowing the

team/bank to make incremental improvements in service-delivery,” Hardie says.

Through this process, Nedbank found that up to 8 percent of clients still had an unresolved issue at the

time of contact, and established new processes to make sure the issue was resolved within that same tele-

phone call, either by the person conducting the survey or by special resolution experts, ensuring clients’

satisfaction when they get off the phone.

“You need to have a very robust measurement engine in place as a foundational step to start building

more aspirational initiatives,” Hardie says. The process allows for an extreme level of granularity to the

point where Nedbank is able to produce an NPS for its individual bankers, creating clear targets in staff

members’ scorecards that are directly linked to the client experience being delivered.

However, measuring on its own is not enough. Hardie underlines the need to bring an organization-

wide cultural revolution that encourages employees to change their behavior as they interact with clients,

while also promoting a more client-centric experience with internal clients. One of the ways Nedbank

began manifesting its commitment to clients was through its “Ask Once” promise, through which the bank

pledges to resolve client requests the first time around. In case the bank fails to keep this promise, it will

make a donation in the client’s name to the client’s choice from a list of charities.

“This was a very clear commitment to clients and non-clients alike that we were determined to start fix-

ing the basics and embark on a client-centered journey,” Hardie adds.

Results

This strategy demonstrates that Nedbank not only knows about its clients, but also knows them individu-

ally. Hardie says the company’s strategy has driven impressive results. In the first half of the year, NPS has

increased “drastically” across the board, reaching in excess of 80 percent in some channels. This lift after a

five-year journey is believed to be due to the different initiatives meshing together and starting to drive real

change. “We got to the critical stage where the cohesiveness of the initiatives started to drive real results.”

Customer acquisition rates also improved, which were below the bank’s expectations three years ago.

These have since increased and compare with those of international retail banks. With the help of Peppers

& Rogers Group, Nedbank now better understands the causes of attrition and has identified 16 initiatives

to address this problem.

Despite its achievements, Nedbank’s leadership recognizes that the bank still has more to do to achieve

its goals. “It has been a long journey with a lot of hard work and dedication—we are delighted that we are

half way there,” Hardie says.

Through these various but complementary initiatives, Nedbank continues in its efforts toward building

deeper relationships with clients. The bank’s most current initiative includes a coordinated review of its

client loyalty strategy with the goal of deepening relationships with clients in real time.

“ You need to have a very robust measurement engine in place as a foundational step to start building more aspirational initiatives.”

— Doug Hardie Executive General Manager, Nedbank

Retail Banks

On paper, financial institutions seem primed to excel with social customer interactions. They have large

amounts of customer data at their disposal to engage and advise them via social channels. At the same

time, money and finance are extremely important issues to most consumers. They use social media to

share insights and learn about new products, services, and make financial decisions.

Every day, consumers sign up for tools such as electronic transfers, mobile check deposits, online branch

and ATM locators, and other digital applications they find convenient and valuable. Younger, digital-native

consumers are approaching banking age, searching for banks that will meet their interaction preferences.

In addition, the banking industry has been working to break away from its less-than-stellar reputation

with consumers. Social media offers ways to make genuine connections with consumers in an effective

and cost-efficient way, all while strengthening individual relationships.

Advanced social media strategy therefore seems like a natural extension of a bank’s customer experi-

ence strategy.

But the fact is that banks aren’t doing much beyond just being present on social media sites. Sure, many

banks have Facebook or Twitter pages to broadcast PR or marketing messages and monitor customer

complaints. But you’d be hard pressed to find much more than that.

What’s holding banks back from advanced social media activities? The simple answer is that it’s chal-

lenging, and without a proven go-to strategy for social media in banking, the ROI is not always obvious.

Many banks choose to maintain the status quo rather than try to innovate with an unproven strategy. We

think that’s a lost opportunity to build revenue, trust, and long-term relationship strength with banking

consumers. It’s time for banks to dip more than a toe in the water if they want to reap the potential rewards

of social media strategy.

Social media obstacles

Many in the financial world offer excuses for why they don’t innovate through the

social media channel. All can be overcome. A few common challenges:

1. Compliance and regulations

The banking industry is a regulatory minefield. Banks must deal with laws pertaining

to the use of customer data, privacy requirements, records retention, and even inter-

actions that may be construed as investment advice. As such, they are very cautious

about doing much more than the basics regarding social media.

We think that challenge can be overcome with a strategic approach to social

media participation. It starts by establishing policies designed to manage internal

and external social media “rules of engagement.” Set expectations right from the

start about the types of conversations you will have in your different social media

accounts. Move to more appropriate channels if escalation is needed. Create

employee guidelines for participation and train the staff on social media compli-

ance, so they will feel comfortable knowing their boundaries. And recognize and

share great social media interactions to encourage others to participate.

©2014 www.1to1media.com 12

What’s Keeping Banks From Reaching Their Innovation Potential in Social Media?Three recommendations for attainable opportunities using social media strategy.

Adapted from Customer Strategist Journal

Social Media Reaches Across the Business

Social media is not just for one department. Many areas of the business can see enhancements, such as:

“ Many banks choose to maintain the status quo rather than try to innovate with an unproven strategy.”

©2014 www.1to1media.com 13

Retail Banks

2. Lack of proven ROI

As with all new and disruptive technologies, banks struggle to determine the value of their social media

activities and ultimately, their ROI. They are unsure how much likes, fans, and followers actually contribute

to the business fundamentals.

ROI is possible in social media, if measurable goals and objectives are defined. We recommend the fol-

lowing framework:

• Define SMART (specific, measurable, attainable, relevant, timely) social media objectives and KPIs that

are aligned to corporate goals and target segments. For example, one bank’s corporate goal may be to

generate leads in its youth segment. The specific social media objective would be to generate 10 percent

of overall leads in the youth segment from social media over a six-month period by driving traffic to bank-

owned channels such as its website, call center, or branch. When new customers sign up, the bank can ask

customers if they used social media in their search and consideration process. Then it can measure leads

generated through social media as a core KPI.

• Collect accurate data using social analytics tools, such as Google Analytics, to get a complete picture of

social media activity. It is important to collect data before and after the social media initiative to measure the

incremental impact. For those interested in brand awareness, measurements may include number of visits,

time on the site, number of followers or likes, and conversion rates for users taking specific action. If engage-

ment is more important, banks can focus on metrics such as number of community registrations, comments,

reviews, etc., or how influential customers are in terms of their own number of followers and interactions.

• Calculate the benefits associated with the social media initiative using collected data. The value of a

Facebook like can be determined by tracking the revenue generated via leads and traffic originating from

Facebook to a dedicated landing page on the company’s website (accessible only via Facebook). So the

benefit of a ‘Facebook engagement’ campaign is the total revenue generated from Facebook fans who

were encouraged to visit the website and enticed to purchase the promoted product or service. By sub-

sequently quantifying the cost of the social media initiative in terms of people, process, and technology

expenditures, the ROI calculation now becomes a trivial task.

Social media doesn’t have to be expensive. Tools and technology are readily available. The real invest-

ment comes from thinking and acting strategically about the best ways to engage with your customers via

social media.

Product-focused legacy

Banks are traditionally product-centric. They focus most of their energy on pushing products and services

to masses or specific segments. In the social media space, banks need to take on a different dimension

that encourages customers to create an emotional bond with the brand.

With so much happening in the social space, banks are unlikely to capture customers’ attention by just

pushing out messages about their products or services at random times across randomly selected chan-

nels. Instead, explore where the bank’s customers and prospects gather and offer something that the

audience wants, whether it be relevant content or quick responses to complaints. The discussions naturally

lead to sales opportunities, which banks can seize by creating compelling offers and delivering on the value

as promised.

Social media isn’t about products and services. It should reflect the experience and emotions of custom-

ers as they use products and services.

Social media opportunities

Banks that look at social media as a strategic channel will see many ways to engage with customers across

the lifecycle. In past issues of Customer Strategist we have wrriten that banks can mix offline and online

customer data to get, keep, and grow customers. We also see innovation potential through activities where

banks build customer trust, generate revenue, and achieve operational excellence.

“ In the social media space, banks need to take on a differ-ent dimension that encourages customers to create an emotional bond with the brand.”

©2014 www.1to1media.com 14

Retail Banks

1. Build customer trust

Banks are a necessity, but many consumers feel like they have an adversarial relationship with them. The

industry’s reputation leaves a lot to be desired. Yet there is great opportunity to advance social media to

build relationships with individuals to counteract that reputation.

In their book, Extreme Trust: Honesty as a Competitive Advantage, Don Peppers and Martha Rogers,

Ph.D. write that trustable companies do the right things and do things right, proactively. They act in cus-

tomers’ best interests with proactive competence and intent. What better channel to demonstrate proactive

competence and intention than social media? Banks can preemptively contact someone before a fee is

incurred, or connect with target segments about financial issues that are important to them.

More than just Facebook and Twitter accounts, we see great potential in bank-sponsored social com-

munities, provided consumers are willing to participate. Banks that position themselves as helpful advisors

with useful content can overcome poor reputations to be considered trustable. Community success

requires honest, genuine discussion about issues, led by consumers and merely facilitated by the bank.

And research shows that consumers who see a firm as a trustable source are more likely to spend more

and make recommendations to friends.

2. Generate revenue

Social media is about building and nurturing genuine relationships. The way to extract financial value from

those relationships is, first and foremost, to listen to what customers and prospects are saying and then

offer something compelling based on identified needs. Banks can respond with tailored messages and rel-

evant communications on how to benefit from using a specific product or service to meet customers’ needs.

Active listening can also uncover opportunities to identify customer life events, such as buying a home,

getting married, etc., which banks can turn into sales. Monitoring customer complaints presents an addi-

tional means to retain revenues—by addressing the concerns of existing customers and preventing them

from ceasing their relationship with the bank.

3. Achieve operational excellence

Leading banks use social media to develop more innovative products, services, and processes that reflect

customer demand. As a channel, social media is positioned as a cost-effective and easy way to seek and

incorporate multiple levels of customer feedback. Some examples:

• Product innovation: Crowdsourcing through relevant social channels yields new banking products.

• Service innovation: The ability to address inquiries and complaints on customers’ choice of media

helps nurture communities of advocates.

• Process innovation: Internal collaboration improves productivity.

The benefits of the social media channel come from its constant evolution. It’s not enough for banks to

have a social presence. They need to innovate and evolve along with their customers and the channel itself.

Will you do what it takes to reach your customer innovation potential?

Note: Claus Friis, Peppers & Rogers Group financial services subject matter expert, contributed to this article.

“ Banks that position themselves as help-ful advisors with useful content can overcome poor reputations to be considered trustable.”

©2014 www.1to1media.com 15

Retail Banks

Created in 2005, Boubyan Bank is one of the fastest growing banks in Kuwait, with a wide range of products

and services in consumer banking, corporate banking, and investments, including Islamic banking offerings.

As a Deputy CEO in charge of consumer banking and banking operations groups, Abdullah Al Najran for-

mulates business strategies and policies and is closely involved in the planning and execution of operational

activities. He is also a key advocate of learning and innovation culture, which continues to be the major

focus of the bank’s strategy. Here he shares his thoughts on the intersection of traditional and innovative

forms of customer strategy, specifically social media.

Customer Strategist: Why are customer strategy and innovation important to the company?

Abdullah Al Najran: The customer is at the center of everything we do and our customer strategy focuses on

providing differentiating products and the best quality service to our main target segment of affluent Kuwaitis.

We have also identified the potential of other strategic segments, such as youth and ladies, for which we devel-

oped compelling value propositions that would appeal to new customers, as well as retain the existing ones.

Innovation takes the bank’s signature customer experience to the next level as we strive to continu-

ously exceed our customers’ expectations. We have embarked on a transformation journey and are in

the process of implementing various customer-centric initiatives, such as upgrading the call center with

biometric features such as automatic customer voice recognition, revamping our website for superior digi-

tal experience with “chat” and enhanced Internet banking features, focusing on social media as a market

differentiator to engage with our customers on a more personalized level, amongst others.

Essentially, the customer strategy defines the “wow” experiences for our target customers, whereas

innovation ensures that we keep delivering on the Boubyan promise in line with our customers’ ever-

changing needs and preferences.

CS: What potential is there for banks to advance their customer strategy through social media activity?

AAN: Social media has become the primary channel of communication for young, digital, socially savvy

customers. Banks need to adapt to this trend in order to build credibility and trust with this segment. Social

networking sites are where youths of today gather to socialize, be entertained, share stories, seek advice,

and prefer to have their complaints and questions answered. Consumers view social media as the platform

for meaningful engagement through on-demand content customization, sharing and collaboration, all of

which banks can leverage to build trust and create opportunities to grow their customer portfolio.

If positioned correctly, social media can be a very effective customer acquisition and retention tool. First

and foremost, social media marketing is a far less expensive option relative to traditional media, such as

TV, radio, billboards, etc. Social media is also a well-positioned platform to build superior relationships

with customers, as banks have a direct path to interacting with the audience to gather immediate feedback

on the products and services. People can immediately “like” the product /service, comment on it, share it

with their friends. This “know-like-trust” cycle with customers and prospects will ultimately lead to revenue

growth through new acquisitions and repeat business.

CS: What type of social media activity do you think holds the most promise from a business perspective?

AAN: The key to social media success starts with “listening” across all social media platforms to what is

Social Media Energizes Traditional Banking StrategyKuwait’s Boubyan Bank undergoes a customer-focused transformation, using social media as the strategic lynchpin.

Adapted from Customer Strategist Journal

“ Essentially, the customer strategy defines the “wow” experiences for our target customers, whereas innovation ensures that we keep delivering on the Boubyan promise in line with our customers’ ever-changing needs and preferences.”

— Abdullah Al Najram, Deputy CEO, Boubyan Bank

Banks

being said about the brand and products, competitors, and following industry trends. This gives insight on

customers’ and prospects’ needs and preferences, which guides communication and engagement efforts

in order to create high brand awareness and keep the brand top of mind for consumers.

With a social media monitoring tool in place searching for brand and product mentions, banks can

identify customer service issues as they come up, even on fast moving social networking sites like Twitter.

Furthermore, a good listening program can proactively manage the brand’s reputation and in the case of a

crisis, mitigate the potentially negative effects on the brand by responding quickly and properly according

to the corporate crisis response plan.

CS: What social lessons from other industries can help banks with their social initiatives?

AAN: Focus on business outcomes—most banks are using social media channels merely to push mes-

sages out. Social platforms offer a golden opportunity to engage with customers in a two-way dialogue

and to create an emotional bond with the brand. Customers can also become the most significant source

of innovation—banks need to embed social capabilities in the business processes to continuously collect

customer feedback.

Change starts from within—social media adoption requires transformational change, so dedicate a

social business team (comprising representatives from relevant business groups) to act as change agents

to build awareness and drive the adoption across the organization. [Boubyan is in the process of defining

an employee transformation program to start down this journey]. Furthermore, banks should empower

their employees to become brand ambassadors and leverage them to grow the network of followers and

external brand evangelists.

CS: What do you think are some of the biggest roadblocks to banks’ use of social media as a relation-

ship channel?

AAN: I believe the biggest challenge lies in maintaining customer data privacy in terms of the extent and

scope of customers’ information being shared over social media platforms. These platforms are typically

provided by external third parties, which means that data is stored on the provider’s servers. Naturally,

banks are very uncomfortable with such a set-up, since regulations dictate that customer information of a

sensitive or confidential nature cannot be stored outside of the bank’s systems.

So when a customer makes a complaint about a bank on Twitter, for example, the bank needs to shift

that conversation offline and typically asks the customer to contact the call center or a direct number to

the bank staff member. The challenge becomes when a customer does not necessarily want to call the

bank on the phone. Banks need to look for alternative online solutions to address this issue. One way is to

direct a customer to a click-to-chat tool with a live agent that resides on the bank’s servers and provides

a secure environment over which to share personal banking details. Live chat is something that Boubyan

will implement in the near future, not only to resolve customer complaints but also to engage in informative

discussions.

CS: How should a bank balance social media activity with the rules and guidelines of Islamic banking?

AAN: Social media and Islamic banking are not conflicting; indeed social media is a channel like any other

and the same rules and guidelines of Islamic banking apply across all customer touchpoints. Since custom-

ers and users interested in Islamic banking are generally more conservative, there are additional guidelines

that apply in the social media space with respect to moderation and stricter filtering of the language used

(tone / content) and photos shared. The flexibility in interaction should be there, but with clear redlines not

to cross.

CS: What is the biggest challenge you see to social media expansion?

AAN: Customer perception and experience of the bank’s brand can be relatively easily swayed by the

©2014 www.1to1media.com 16

“ Banks should empower their employees to become brand ambas-sadors and leverage them to grow the network of followers and external brand evangelists.”

— Abdullah Al Najram, Deputy CEO, Boubyan Bank

Banks

conversations taking place across social media channels, which we have very little control over. That’s

why we felt it was important to invest in establishing clear governance and social media policies to enable

us to respond quickly and communicate in a manner that is aligned with our brand values and consistent

across the channels.

Another area that we needed to address was how to manage employee communication through their

personal accounts. Since we encourage our employees to get involved in social media adoption and

innovation, we also invested in developing clear social media guidelines for staff to avoid any public embar-

rassment and liability with any potential miscommunication.

CS: What would you say to other banking executives looking to expand their customer initiatives into social channels?

AAN: Start with the solid governance to guide your decision making and oversee social media activities in

an efficient and effective way. Build internal policies for your employees to follow to ensure consistency in

branding, communication, and customer experience across all social media platforms. Furthermore, build-

ing engagement on your social media channels requires active listening so invest in a good social media

monitoring tool. Understand where your target customers are gathering, listen to what they are saying, and

finally provide them with content and propositions based on their needs.

©2014 www.1to1media.com 17

“ Start with the solid governance to guide your decision making and oversee social media activities in an efficient and effective way.”

— Abdullah Al Najram, Deputy CEO, Boubyan Bank

Retail Banks

With so many types of social media platforms out there, it can be hard to determine which one to focus on.

Peppers & Rogers Group conducted a study of nearly 3,000 social media users in Kuwait to determine how

they use social media and their potential for stronger banking relationships.

According to the study, Facebook, Twitter, and YouTube are the most popular social media channels,

attracting more than 60 percent of users.

While Facebook has the highest usage, Twitter

is accessed the most per day. And users are

diverse – a small but growing population also

uses emerging platforms such as Whatsapp,

Pinterest, Skype, and Orkut.

Consumers use social media for a variety

of reasons—to stay in touch with friends and

family, share common interests with others,

find information about products and ser-

vices, and share photos, videos, and music.

The common thread among them is that they

all connect people to others. And consum-

ers are receptive to the idea of connecting

to businesses as well, if the interaction is

valuable and relevant. Sixty-eight percent of

users are somewhat or most likely to click

on an ad within social media that is relevant

to them, and 66 percent are somewhat or

most likely to purchase a product or ser-

vice recommended on a social network.

When it comes to banking, there is opportunity to increase awareness and engagement. Only 40

percent of Facebook and Twitter users follow their banks on social media, and it’s even less on

other channels—17 percent for YouTube and less than 6 percent for all others. However, con-

sumers have a positive view of banks that do use social media: 78 percent agree that bank social

media presence “makes me feel that the bank is keeping its customers informed,” and 64 per-

cent agree that social media use by banks “makes me feel that it is open to people’s opinions.”

Social media has become a vital channel to the future of banking interactions. It must be considered a

strategic channel, not just a second thought or PR endeavor.

©2014 www.1to1media.com 18

Study Shows Potential for Social Media in Emerging MarketsPeppers & Rogers Group conducted a study of nearly 3,000 social media users in Kuwait to determine how they use social media and their potential for stronger banking relationships.

Adapted from Customer Strategist Journal

Consumer Perceptions Related to bank Social Media Presence

Consumers have a positive perception of banks that participate in social media.

Source: Peppers & Rogers Group

©2014 www.1to1media.com 19

Retail Banks

The use of digital channels is skyrocketing in financial services. New technologies serve customers in

unprecedented ways while driving internal efficiencies. And according to market research company Ovum,

U.S. banks will spend $41.5 billion on technology through 2013, with much of it on digital tools.

Customers now have access to accounts and can transact across mobile, social, and other self-serve

channels. The branch’s role is changing to focus on more complex issues while consumers use Facebook,

mobile apps, and virtual wallets to conduct financial business in a new ecosystem.

Today’s consumers share more information about their needs, risk tolerance, and personal profile

than ever before. Their expectations are higher, shaped by experiences outside banking. They are bet-

ter informed as they use internal and external channels to research products and services. They look

beyond banks to fulfill financial needs, engaging players such as Google Wallet, PayPal, Mint.com, and

even Costco and Wal-Mart. And consumers connect to brands and one another through social and mobile

channels, communicating their experiences broadly. They’re willing to take advantage of low cost channels

if they find them valuable and relevant to their daily lives. Many actually prefer them.

There is much potential to balance internal efficiencies with a superior customer experience in this new

reality. But achieving the balance requires banks to optimize the unprecedented amounts of customer data

now generated to make information actionable and relevant. New sources of customer Big Data consist of:

• Transactional data • Product usage data

• Web registration data • Customer value data

• Channel usage data • Web clickstream data

• Third-party data • Social media data

Banks are beginning to explore the opportunity to differentiate with insight. For example, the business

press reports that one of Capital One’s top priorities is to be a data-driven organization and use insight to

differentiate in customer service and product development, though specifics are hard to come by. And it

is not alone. Investment firm State Street Corp. is using semantic data models on the client side to opti-

mize investment strategies, while also improving regulatory reporting and risk calculation internally. Even

a smaller player like Midwest regional bank Great Western Bank is leveraging predictive analytics for its

marketing activities.

The industry is still in its nascent stage, however. According to a recent study by Celent, only 24 percent

of banks surveyed had implemented a Big Data solution, most commonly around risk and fraud monitoring

or product and service marketing. But of those who have had a Big Data initiative in place for more than a

year, 70 percent had met or exceeded business expectations. And to highlight data’s potential, 90 percent

of those surveyed said they think that successful Big Data initiatives will define the financial services win-

ners in the future.

So how can banks make the most of Big Data? By optimizing the collection and use of customer data,

banks and other financial institutions can simultaneously improve the customer experience while driving

efficiencies. Some examples include:

Provide consistent multichannel experiences. Consumers can now interact with a bank through multi-

ple channels for information and transactions. Banks must provide a seamless experience across whatever

Five Steps to Big Data Dominance in BankingSuperior customer experiences and improved internal efficiencies require smart use of newly available Big Data.

Adapted from Customer Strategist Journal

“ Achieving the balance requires banks to optimize the unprecedented amounts of customer data now generated to make information actionable and relevant.”

©2014 www.1to1media.com 20

Retail Banks

channels are used. Employees in the branch must know if a customer has called the contact center or

visited the website; transactions started in one channel can be completed in another. This will create satis-

fied, engaged customers.

Acquire new, mobile-savvy customers. Young, digital native consumers are beginning to open accounts

and create lifelong relationships with financial services firms. They’re mobile and they expect the compa-

nies they do business with to be mobile, too. Banks will succeed reaching this new customer group if they

deliver insight-driven experiences through mobile devices.

Sense and respond with effective targeting. Reaching the right customer with the right offer at the right

time is the holy grail of sales and experience. And banks can generate new revenues through proactive

engagement and outreach to certain customers groups at the proper time.

Rightsize the customer experience. Use Big Data to find the most appropriate channels based on cus-

tomer needs, value, and behavior, and then go deeper to understand the best way to migrate customers to

serve them in the most efficient and effective channels.

Identify new sources of revenue and acquisition. Mine unstructured social data to activate advocates

and identify new customers. Optimize pricing based on customer segments, products, channels and geog-

raphies, and remove any revenue leaks such as ineffective lead generation, poor follow-up, low conversion

ratio, or high attrition to achieve sustainable revenue sources that are less sensitive to risk, sticky, and

recurring.

Build loyal relationships. Surprise and delight by knowing customers more intimately than ever before

and meeting their needs, whether they are verbalized or not. Show that your bank has its customers’ best

interests at heart, and they will reward you with their loyalty.

Improve service to sales. By mining customer service data and defining trends, banks can respond to

customer needs and make systemic changes to processes that can even result in up-sell success. For

example, rather than responding to and resolving complaints around monthly service fees, offer direct

deposit or other products and services as part of the care response that would eliminate these charges.

Invest smartly in the retail branch. Understand branch-level data and optimize investments in the net-

work. Learn what types of customers visit the branch and why. Focus branch initiatives on what matters

most to those customers.

With so many opportunities for revenue enhancement and relationship strength, why don’t more banks

take advantage of the Big Data potential? Because acting on these opportunities is a non-trivial matter.

Making sense of so much data is a challenge, as is where to prioritize efforts. Companies also want to

make sure to invest in the most effective initiatives while staying agile enough to meet changing customer

expectations. It can be a daunting undertaking.

Five Ways to Attack Big Data

We at Peppers & Rogers Group have outlined five steps to guide financial leaders as they craft smart

data strategies:

1. Elevate the importance of business-savvy data scientists. While there’s always a high demand for quan-

titative professionals to be part of the team, progressive banks are looking to complement that talent with

creative business professionals who see business opportunities in trends that produce bottom-line results.

2. Organize for one version of the truth. Too many banks are still organized in product- or channel-centric

silos. The bank can’t knit together a comprehensive picture of the customer. Silos need to be redefined

along with analytics practices. Online and offline data must be integrated into platforms across channels

that facilitate a comprehensive understanding to enable predictive analytics and inform real-time interac-

tion strategies.

Silos need to be redefined along with analytics prac-tices. Online and offline data must be integrated into platforms across channels that facilitate a comprehensive under-standing to enable predictive analytics and inform real-time interaction strategies.

©2014 www.1to1media.com 21

Retail Banks

3. Don’t underestimate the integration challenge. Today banks need to extract insights from structured

and unstructured data, statistical data, social media streams, click stream data, smartphone data, videos,

etc. Small-scale experiments using Big Data are recommended to start, with slow rollout from there.

4. Integrate intelligence into customer-facing business practices. The biggest opportunity for Big Data

is the potential to identify and integrate insights into customer-facing applications in real time. Analytics

have come a long way, but many banks neglect to push the intelligence to front-line applications.

5. Use Big Data to accelerate the customer-centric transition. Customer centricity is no longer a nice

to have strategy for banks, it’s the only differentiator. And data is the backbone. It’s critical to think beyond

technology and analytics to what organization, process, and people-related changes are necessary to

really put the data and insights to work.

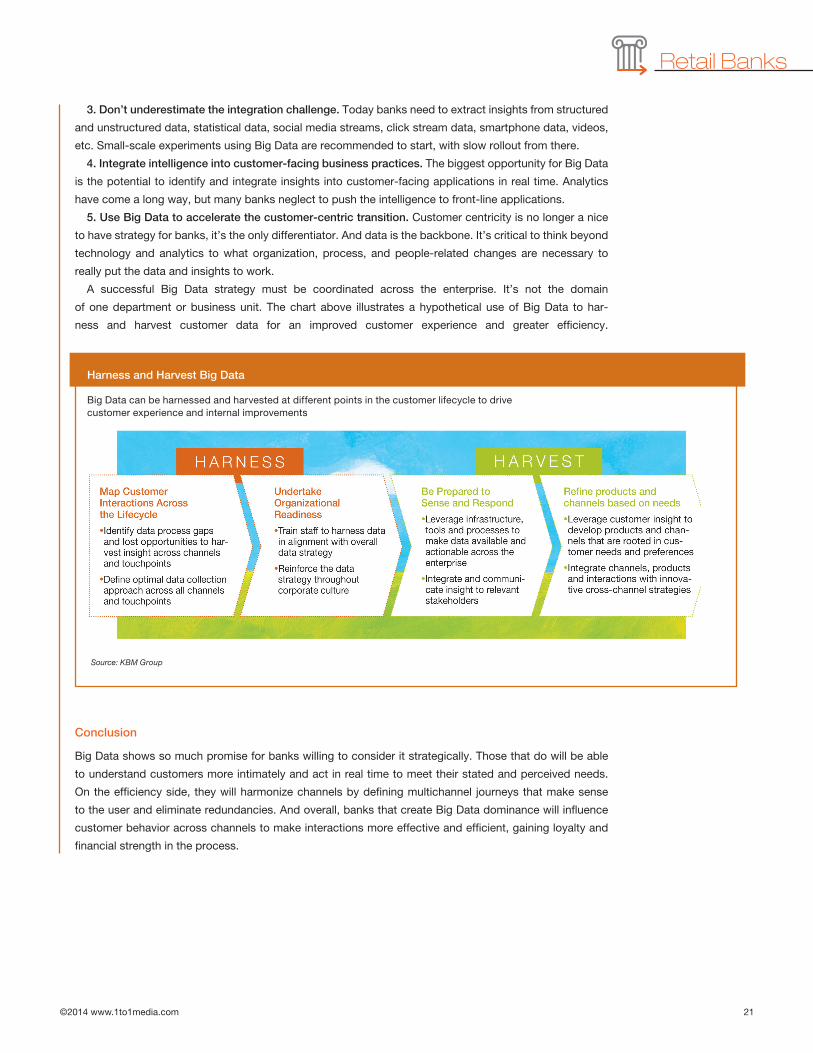

A successful Big Data strategy must be coordinated across the enterprise. It’s not the domain

of one department or business unit. The chart above illustrates a hypothetical use of Big Data to har-

ness and harvest customer data for an improved customer experience and greater efficiency.

Conclusion

Big Data shows so much promise for banks willing to consider it strategically. Those that do will be able

to understand customers more intimately and act in real time to meet their stated and perceived needs.

On the efficiency side, they will harmonize channels by defining multichannel journeys that make sense

to the user and eliminate redundancies. And overall, banks that create Big Data dominance will influence

customer behavior across channels to make interactions more effective and efficient, gaining loyalty and

financial strength in the process.

Harness and Harvest Big Data

Big Data can be harnessed and harvested at different points in the customer lifecycle to drive customer experience and internal improvements

Source: KBM Group

©2014 www.1to1media.com 22

Round-the-clock customer service is becoming essential for most organizations. This is especially true in

the financial services industry since customers want to get help whenever they need it, even after normal

office hours.

Having recognized the importance of being there for customers whenever they need, irrespective of the

time of the day, Associated Banc-Corp decided to start operating its contact center around the clock. “We

wanted to improve the customer experience and felt there was adequate need for [24/7 service,]” explains

Wendy Kumm, vice president of customer service.

To make the extended hours work, the bank started hiring college students to fill the openings created

by the additional shifts. This new reality highlighted the need for a better scheduling system for the bank,

which manages about $23 billion in assets, employs close to 5,000 people, and serves more than one mil-

lion customers. Kumm explains that previously the company was preparing schedules manually. While the

spreadsheet-based scheduling system had worked in the past, the bank needed a better way to assign

shifts. “We had been doing a good job, but we needed to simplify the process,” Kumm notes. In order to

address this issue, Associated Banc-Corp implemented a workforce management tool to help with sched-

uling the additional shifts.

The company’s leadership quickly realized that technology could also help with the company’s quality

control and training efforts, Kumm says. In the past Associated Banc-Corp had relied extensively on live

monitoring for quality control and compliance, but it wanted to go a step further and analyze speech. In

2009 the company decided to implement Verint’s workforce optimization suite. “The secret sauce was

speech analytics,” Kumm says. “It’s every call center manager’s dream come true.”

Results

The deep insight into what customers are saying is giving Associated Banc-Corp actionable insights that

it’s able to use to improve the customer experience. For example, the company identified that its online

banking system wasn’t always as user-friendly as customers desired. After analyzing customers’ com-

ments, the bank made changes that improved the experience for customers using online banking.

Further, it allows the organization to resolve individual problems that customers are facing. “We want to

identify customers who have had issues and reach out to them and offer a resolution,” Kumm says. She

explains that the bank has a specific team which listens to calls and then reaches out to customers. This

system also allows the organization to identify repeat callers and address their needs.

An additional benefit has been using customer insights for training purposes. Kumm explains that the

bank developed an e-learning module and uses recordings from actual calls to highlight best practices.

Kumm says the organization surveys customers after a contact center interaction and has seen an

increase in positive comments since it adopted the new system. She says comments that are made dur-

ing interactions with agents have also been very positive, many times praising agents for their help. “Our

company is focused on improving customer experience and making it easier for customers to do business

with us. This fits right into that aim,” Kumm says.

By listening to calls to its contact center, the bank is able to identify problems and address them, improving the customer experience.

Associated Banc-Corp’s Customer Listening Makeover

Adapted from 1to1 Media

Retail Banks

“ Our company is focused on improving customer experience and making it easier for customers to do business with us. This fits right into that aim.”

— Wendy Kumm, Vice President, Customer Service, Banc-Corp

©2014 www.1to1media.com 23

Trust is easy to lose and difficult to gain back. Cutthroat competition in several industries is making it

essential for organizations to retain customer trust or, if they’ve lost it, work hard to earn it back.

The financial services industry has been going through a PR crisis in the past years, as bailouts, subprime