investment research ikano...

TRANSCRIPT

Important disclosures and certifications are contained from page 17 of this report. www.danskeresearch.com

Investment Research

With its origins in IKEA, Ikano Bank was founded in 1995 and serves mainly as a

consumer bank with a strong foothold in the Nordics. The bank is part of the Ikano

Group, which is fully owned by the Kamprad family, the main founders of IKEA.

Much more than a branchless consumer bank

Ikano Bank divides its operation in three areas: Corporate, Sales Finance and Consumer.

The Corporate business area accounts for 25% of receivables and offers leasing, object

financing, invoice purchasing and factoring. Sales Finance offers financing and sales

support mainly to retailers. Finally, the Consumer business area offers savings and loans

to private individuals. Ikano Bank has no physical branches as it only operates through its

website or business partners.

Strong capitalisation, high coverage ratio but modest RoE

Capitalisation is high with a common equity tier-1 (CET1) ratio at 14.7% and total capital

ratio at 17.4% end-H1 14 measured by standard method. The leverage ratio is as high as

11.9%. RoE after tax has been lagging peers the past couple of years, mainly due to an

average NIM and somewhat higher loan losses. However, the coverage ratio stands out in

the peer group, which is the result of more conservative provisioning, in our view.

Overall we view capitalisation and credit management as credit positive and profitability

as neutral.

We view Ikano Bank as a stable ‘BBB’ bank issuer

We assign a ‘BBB’ rating to Ikano Bank with a stable outlook based on our view of its

business and financial risk profile. We do not include any support from the owner but do

believe the owner would be very constructive in case the bank is in a situation where

support is needed. We might consider a notch higher rating if the profitability improves

further or a formal support structure from the owner is introduced. Downside risk to our

rating includes among others deteriorating asset quality.

Key metrics

SEKm 2009 2010 2011 2012 2013 H1 14

Pre-Provision Income 608 706 801 762 728 392

Loan Losses and Provisions 416 172 241 242 295 146

Net Income 257 145 414 234 190 101

Receivables 13,801 15,329 15,289 15,839 19,830 20,953

Risk exposure amount (REA) 14,920 15,382 16,346 16,537 20,093 20,487

Equity 1,498 1,420 1,809 1,944 2,370 2,504

Impaired Receiv. % Gross Loans & Guar. 10.3% 4.6% 6.1% 6.4% 5.0% 5.1%

Common Equity Tier-1 Ratio (CET1) 9.6% 9.9% 11.7% 13.5% 14.0% 14.7%

Total Capital Ratio 12.2% 13.5% 15.1% 16.5% 16.7% 17.4% Note: We have used historical exchange rates in order to change 2009-2011 from EUR to SEK

Source: Company data, Danske Bank Markets

Facts

Sector: Bank, financing company

Corporate ticker: IKANO

Equity ticker: Private

Equity book value: SEK2.5bn

Ratings

Rating agencies:

Not rated

Danske Bank Markets:

Issuer rating: BBB

Senior unsecured: BBB

Analysts:

Lars Holm [email protected] +45 45 12 80 41 Thomas Hovard [email protected] +45 45 12 85 05

Key credit issues

Strengths

Diversified lender cooperating with

several corporate brands incl. IKEA.

High capitalisation and high

coverage ratio of impaired loans.

Large and stable deposit base.

Challenges Profitability under pressure due to

falling income and increasing costs.

Dependent on private consumption,

which could be hurt by slowing GDP

growth or falling house prices.

Mainly unsecured lending that is

likely to be hit first in an economic

downturn.

Source: Danske Bank Markets

30 October 2014

Ikano Bank

Issuer profile

2 | 30 October 2014 www.danskeresearch.com

Ikan

o B

an

k

Ikano Bank

Company profile

Ikano Bank is one of four business areas in the Ikano Group that is owned by the Swedish

Kamprad family through Ikano SA, Luxembourg. Originally the Ikano Group was part of

IKEA (founded by Ingvar Kamprad) but it was spun off as an independent group in 1988.

Ikano Bank was founded in 1995 and is predominantly known as a consumer bank but it

also offers various products to corporate clients. Geographically Ikano Bank is

represented in six countries but with the by far largest operation in Sweden (76% of total

business volume in 2013) followed by the UK, Denmark and Norway. The bank does not

have any physical branches but distributes its products through its website or its business

partners. The foreign units operate as branches of the Swedish parent company, which

means that they are under supervision of the Swedish Financial Authorities.

Ikano Group

Note: Ikano is part of the Finance division

Source: Company website, Danske Bank Markets

The bank can be divided in three business areas: Corporate, Sales Finance and Consumer.

The Corporate business area offers leasing, object financing, invoice purchasing (Ikano

Bank takes on the credit risk) and factoring (customer still bears the credit risk) and

accounts for around 25% of total receivables. Sales Finance offers financing and sales

support mainly to retailers. Finally, the Consumer business area offers savings and loans

to private individuals in the form of unsecured loans, mortgage loans and Visa credit

cards. Mortgage loans are offered in cooperation with SBAB Bank AB (SBAB) under the

bank’s ‘Ikano Bolån’ brand (loans are provided and underwritten by SBAB). Deposit

products are only offered in Sweden and Denmark (started up in Denmark in 2014) and

mortgage loan products are only offered in Sweden.

Given Ikano Bank’s origins IKEA is the largest business partner within the Sales Finance

business area. However, it is important to emphasise that Ikano Bank operates

independent of IKEA and competes against other suppliers whenever IKEA looks for a

financing partner. Examples of other business partners are Audi, Hemköp, Hemtex,

Lindex, Shell and Skoda. See also table to the right.

Total assets were SEK25.7bn end-H1 14 (SEK23.8bn end-2013) with gross receivables

accounting for SEK21.7bn (SEK20.6bn end-2013).

Examples of business partners for

Sales Finance

Source: Company website, Danske Bank Markets

3 | 30 October 2014 www.danskeresearch.com

Ikan

o B

an

k

Ikano Bank

Distribution of lending and business volume (2003) - geographic and by product

Source: Company data, Danske Bank Markets

Note that Ikano Bank has decided to wind up its operation in the Netherlands as it never

reached a sufficient return. Given the small size we see this as immaterial for the

company (less than 1% of total assets).

Arm’s length principle to the owner

Given its historical roots one would assume a tight link between Ikano Bank and IKEA

and the other companies controlled by the Kamprad family. However, this is not the case

as the subsidiaries even within the Ikano Group generally are run with an arm’s length

principle and as such are expected to operate as independent companies. That said, Ikano

Bank has got support from its owner when it comes to capital and funding up until now

whenever needed and we generally believe this will continue also in a situation with

financial distress. As an example, Ikano Bank got SEK242m in new equity in 2013 and

has got all its SEK551m in subordinated loans from its owner.

Nevertheless, we have not included any support from the owner in our rating of the bank.

The reasons are not just the arm’s length principle but also the fact that the financial

results from Ikano Group or Ikano SA, Luxembourg are not publicly available. It is thus

impossible for us to conclude whether or not the owner has the financial strength to

support Ikano Bank in a situation of distress.

4 | 30 October 2014 www.danskeresearch.com

Ikan

o B

an

k

Ikano Bank

Key credit considerations

Nordic and European macro environment

With the by far largest exposure to customers in the Nordic region, the macroeconomic

development in this region is of particular importance to Ikano Bank. This includes GDP

growth but first and foremost the unemployment rate, as it has a large impact on private

consumption and not least the level of loan losses.

As can be seen from the chart below, the Nordic region generally benefits from a low

unemployment rate, which furthermore is expected to decline the coming years on the

back of slightly higher GDP growth. In addition, the Nordic region is well known for its

relatively generous welfare entitlements for the unemployed, which means that people are

able to pay their debt even after they lose their job (at least for 1-2 years). In the largest

market, Sweden, the unemployment rate has wavered around 6-8% since 2004.

When it comes to GDP growth, the picture is much the same with the Nordic countries

faring relatively well after they got hit by the financial crisis in 2009. Finland stands out

due to the country’s large reliance on Russia, which Danske Bank Macro Research

expects to mean negative GDP growth of 0.4% for 2014 and risk is to the downside for

2015 as well. Against this background we are pleased to note that Ikano Bank’s exposure

to Finland is only around 1% of total business volume. Sweden is expected to see the

largest growth with 2.2% in 2014E and 2.6% in 2015E.

Unemployment rate in Nordic countries (Eurostat

harmonised) GDP growth Nordic countries

Source: Macrobond, Danske Bank Markets Source: Danske Bank Markets

The generally positive economic environment in the Nordic region in combination with,

among others, low interest rates has boosted the housing market resulting in all-time-high

prices in both Norway and Sweden. The risk of inflated prices is real and a concern to us

as it could threaten the economic stability. Near term we do not believe in a material and

swift correction but it cannot be ruled out completely. If this occurs the risks to Ikano

Bank would be through two different channels: (i) lower house prices would reduce home

equity and increase the risk of second-priority lenders (e.g. unsecured consumer credit)

and (ii) lower house prices would reduce private consumption and increase

unemployment.

-10.0-8.0-6.0-4.0-2.00.02.04.06.08.0

Denmark Sweden NorwayFinland Euro area

5 | 30 October 2014 www.danskeresearch.com

Ikan

o B

an

k

Ikano Bank

Growth in Nordic house prices

Source: Macrobond, Danske Bank Markets

6 | 30 October 2014 www.danskeresearch.com

Ikan

o B

an

k

Ikano Bank

Financial profile

Profitability and efficiency

After some strong years with double-digit returns on equity after tax (RoE) Ikano Bank’s

RoE fell to a modest 8.8% for 2013 (8.3% annualised in H1 14, 12.5% in 2012). In the

past two years costs have outgrown income, resulting in an increasing cost/income-ratio.

This development is of course negative, as it gives Ikano Bank less economic leeway

against loan losses in case they increase from the current level. However, we see the

increasing costs as a result of the bank’s business expansion the past couple of years, both

when it comes to product offering and geographic exposure. The best example of this is

the acquisition of fellow subsidiary Ikano Financial Services UK from Ikano Group in

May 2013, which added 184 employees to a new total of 719 on average for 2013. We

also note that the change of reporting currency from EUR to SEK has had a negative

impact on the 2013 earnings.

Recurring earnings power, which is profit before loan losses in % of risk exposure

amount (REA, formerly known as RWA), has fallen from 5% to 4% from 2011 to 2013

(3.8% in H1 14).

Return on average equity after tax Profitability and efficiency

Source: Company data, Danske Bank Markets Source: Company data, Danske Bank Markets

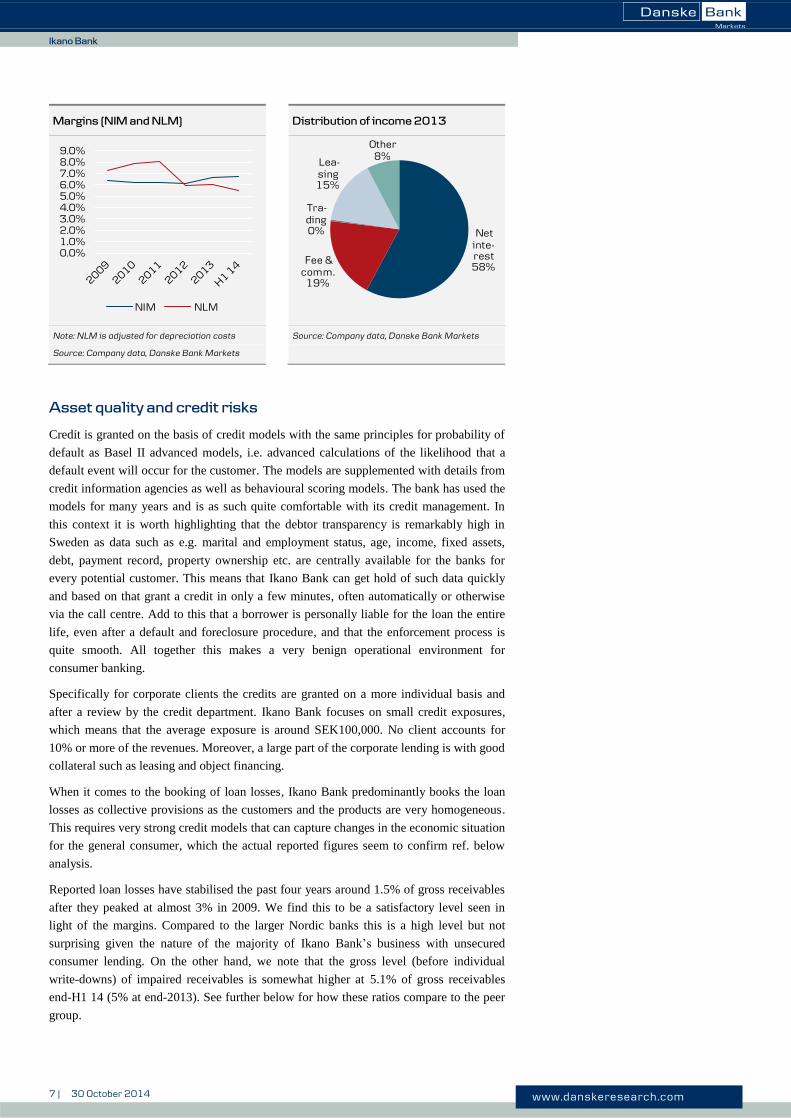

Another reason for costs outgrowing income are the stagnating margins, especially the

leasing margin (NLM). After peaking at 8.1% in 2011 the NLM dropped to 6.1% end-

2013 and was testing a new low at 5.5% end of H1 14. The net interest margin (NIM) has

been more stable and has in fact increased slightly since 2012 reaching a historical high

of 6.8% end-H1 14 (6.7% end-2013). As net interest income accounted for 58% of the

total income in 2013 (including depreciation that mainly relates to leasing), the NIM is

essential to higher income and as such we favour the bank’s ability to raise the level.

A NIM of 6.8% is high compared to more traditional banks. This is clearly a result of the

segments in which Ikano Bank operates. Although the segments have several suppliers,

and hence some competition, it often comes down to the individual cooperation between

the bank and the business partner (retail chains like for example IKEA). Price is normally

not the most important parameter for clients. Instead flexibility and speedy access to

credit (for ‘impulse’ buying) are very important parameters. Therefore marketing and

point-of-sale competition are clear focus areas.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

48%50%52%54%56%58%60%62%64%

20

09

20

10

20

11

20

12

20

13

H1

14

Recurring earnings power, RHSAdjusted cost/income

7 | 30 October 2014 www.danskeresearch.com

Ikan

o B

an

k

Ikano Bank

Margins (NIM and NLM) Distribution of income 2013

Note: NLM is adjusted for depreciation costs

Source: Company data, Danske Bank Markets

Source: Company data, Danske Bank Markets

Asset quality and credit risks

Credit is granted on the basis of credit models with the same principles for probability of

default as Basel II advanced models, i.e. advanced calculations of the likelihood that a

default event will occur for the customer. The models are supplemented with details from

credit information agencies as well as behavioural scoring models. The bank has used the

models for many years and is as such quite comfortable with its credit management. In

this context it is worth highlighting that the debtor transparency is remarkably high in

Sweden as data such as e.g. marital and employment status, age, income, fixed assets,

debt, payment record, property ownership etc. are centrally available for the banks for

every potential customer. This means that Ikano Bank can get hold of such data quickly

and based on that grant a credit in only a few minutes, often automatically or otherwise

via the call centre. Add to this that a borrower is personally liable for the loan the entire

life, even after a default and foreclosure procedure, and that the enforcement process is

quite smooth. All together this makes a very benign operational environment for

consumer banking.

Specifically for corporate clients the credits are granted on a more individual basis and

after a review by the credit department. Ikano Bank focuses on small credit exposures,

which means that the average exposure is around SEK100,000. No client accounts for

10% or more of the revenues. Moreover, a large part of the corporate lending is with good

collateral such as leasing and object financing.

When it comes to the booking of loan losses, Ikano Bank predominantly books the loan

losses as collective provisions as the customers and the products are very homogeneous.

This requires very strong credit models that can capture changes in the economic situation

for the general consumer, which the actual reported figures seem to confirm ref. below

analysis.

Reported loan losses have stabilised the past four years around 1.5% of gross receivables

after they peaked at almost 3% in 2009. We find this to be a satisfactory level seen in

light of the margins. Compared to the larger Nordic banks this is a high level but not

surprising given the nature of the majority of Ikano Bank’s business with unsecured

consumer lending. On the other hand, we note that the gross level (before individual

write-downs) of impaired receivables is somewhat higher at 5.1% of gross receivables

end-H1 14 (5% at end-2013). See further below for how these ratios compare to the peer

group.

0.0%1.0%2.0%3.0%4.0%5.0%6.0%7.0%8.0%9.0%

NIM NLM

Net inte-rest58%

Fee & comm.

19%

Tra-ding0%

Lea-sing15%

Other8%

8 | 30 October 2014 www.danskeresearch.com

Ikan

o B

an

k

Ikano Bank

Ikano Bank keeps impaired loans on the balance sheet for a year before it sells them off to

a debt collector but normally it is able to collect money before then given the legal

possibilities for doing this in Sweden.

Loan loss ratio (% of gross receivables) Impaired receivables in % of gross

receivables

Source: Company data, Danske Bank Markets Source: Company data, Danske Bank Markets

The provisioning ratio stood at 71% of impaired receivables end-H1 14 (78% by the end

of 2013). We consider this a high level and credit positive.

Coverage ratio (provisions to gross

impaired receivables) Gross receivables development

Source: Company data, Danske Bank Markets Source: Company data, Danske Bank Markets

As stated above we see unemployment as the biggest risk factor for asset quality for

unsecured consumer financing. In general the average retail customer in the Nordic

countries has experienced a long period of a reasonable benign economic environment

even during the financial crisis. We view the stable unemployment rate in the Nordics as

the main reason for this.

In the graphs below it is illustrated for Norway and the US how close the correlation is

between unemployment and losses on consumer loans. As the outlook for unemployment

in the Nordic countries is positive, this implies that asset quality transparency is relatively

high, in our view.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2009 2010 2011 2012 2013 H1 14

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

20092010201120122013 H1 14

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2009 2010 2011 2012 2013 H1 14

0

5,000

10,000

15,000

20,000

25,000

Gross loans Gross leasing assets

9 | 30 October 2014 www.danskeresearch.com

Ikan

o B

an

k

Ikano Bank

Unemployment and losses on

consumer lending (US)

Unemployment and losses on

consumer lending (Norway)

Source: Macrobond, Danske Bank Markets Source: Norwegian FSA, Macrobond

Capitalisation

Ikano Bank is highly capitalised with a common equity tier-1 (CET1) ratio according to

fully loaded Basel III rules of 14.7% end-H1 14 (14% end-2013) and a total capital ratio

of 17.4% (16.7% end-2013). The internal target is a total capital ratio of 17%.

Furthermore, the company uses the standard method when calculating its risk exposure

amount, which applies much higher risk-weights than internal rating based (IRB) models.

The minimum requirements in Sweden are 7% CET1 and 10.5% in total capital ratio.

This is excluding the Swedish counter-cyclical buffer of 1% and any company-specific

pillar 2 requirements. The capital requirements are expected to be fully effective from

September 2015. We expect that Ikano Bank is able to meet the requirements with a large

margin based on its current capitalisation, although we emphasise that we do not know

Ikano Bank’s pillar 2 requirement. That the capitalisation is robust can also be measured

by the more simple leverage ratio (tier-1 capital/total assets) that was as high as 11.9%

end-H1 14. This could be compared to around 4% for the largest Nordic banks.

Overall, we find the capitalisation credit positive.

Capitalisation Leverage ratio (tier-1 capital/total assets)

Source: Company data, Danske Bank Markets Source: Company data, Danske Bank Markets

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

02 04 06 08 10 12

Loan loss ratio

Unemployment

0%

5%

10%

15%

20%

2009 2010 2011 2012 2013 H1 14

Common equity tier-1 (CET1) Total capital ratio

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

2009 2010 2011 2012 2013 H1 14

10 | 30 October 2014 www.danskeresearch.com

Ikan

o B

an

k

Ikano Bank

Funding and liquidity

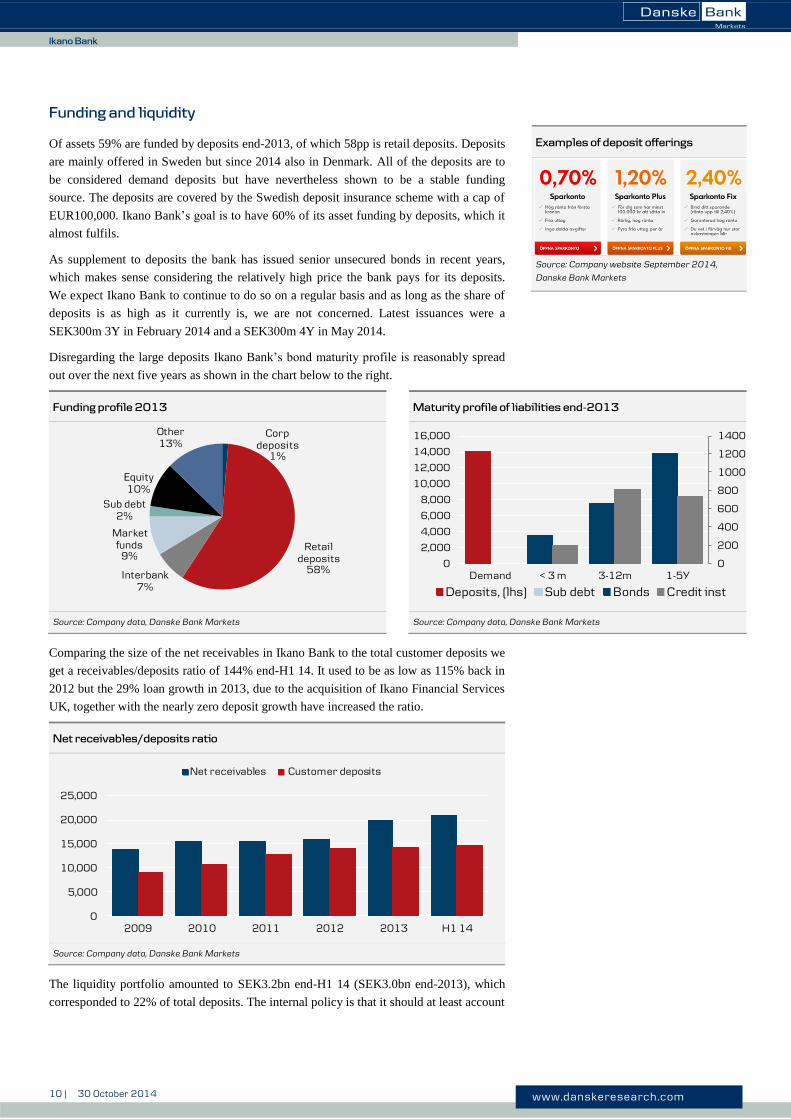

Of assets 59% are funded by deposits end-2013, of which 58pp is retail deposits. Deposits

are mainly offered in Sweden but since 2014 also in Denmark. All of the deposits are to

be considered demand deposits but have nevertheless shown to be a stable funding

source. The deposits are covered by the Swedish deposit insurance scheme with a cap of

EUR100,000. Ikano Bank’s goal is to have 60% of its asset funding by deposits, which it

almost fulfils.

As supplement to deposits the bank has issued senior unsecured bonds in recent years,

which makes sense considering the relatively high price the bank pays for its deposits.

We expect Ikano Bank to continue to do so on a regular basis and as long as the share of

deposits is as high as it currently is, we are not concerned. Latest issuances were a

SEK300m 3Y in February 2014 and a SEK300m 4Y in May 2014.

Disregarding the large deposits Ikano Bank’s bond maturity profile is reasonably spread

out over the next five years as shown in the chart below to the right.

Funding profile 2013 Maturity profile of liabilities end-2013

Source: Company data, Danske Bank Markets Source: Company data, Danske Bank Markets

Comparing the size of the net receivables in Ikano Bank to the total customer deposits we

get a receivables/deposits ratio of 144% end-H1 14. It used to be as low as 115% back in

2012 but the 29% loan growth in 2013, due to the acquisition of Ikano Financial Services

UK, together with the nearly zero deposit growth have increased the ratio.

Net receivables/deposits ratio

Source: Company data, Danske Bank Markets

The liquidity portfolio amounted to SEK3.2bn end-H1 14 (SEK3.0bn end-2013), which

corresponded to 22% of total deposits. The internal policy is that it should at least account

Corp deposits

1%

Retail deposits

58%Interbank7%

Market funds

9%

Sub debt2%

Equity10%

Other13%

0

200

400

600

800

1000

1200

1400

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Demand < 3 m 3-12m 1-5Y

Deposits, (lhs) Sub debt Bonds Credit inst

0

5,000

10,000

15,000

20,000

25,000

2009 2010 2011 2012 2013 H1 14

Net receivables Customer deposits

Examples of deposit offerings

Source: Company website September 2014,

Danske Bank Markets

11 | 30 October 2014 www.danskeresearch.com

Ikan

o B

an

k

Ikano Bank

for 14% of deposits. The portfolio consisted of deposits with banks, short-term lending to

credit institutions and investments in liquid interest-bearing securities, which can be sold

and converted into cash on short notice.

We regard the funding and liquidity profile of Ikano Bank as satisfactory and credit

neutral.

Indicative pricing of senior bonds, ASW

Source: Danske Bank Markets

Peer group analysis

In this section we make a short comparison of Ikano Bank’s key ratios versus its closest

competitors. As always, such an analysis should be viewed with caution as the different

banks differ on several parameters, for instance on geographic exposure and/or business

mix, not to forget accounting methods. It nevertheless gives a reasonably fair view on

asset quality and credit management, in our view.

We start out at the very top with the NIM, which gives some indication of the intrinsic

risk in the different banks’ business profiles. However, it is important to note that product

mix and interest rate level play an important role as well. As stated above, Ikano Bank’s

NIM has been stable to slightly increasing the past couple of years, which places it in the

middle of its peer group. Highest level in the peer group is Bank Norwegian at almost

9%.

IKANO '18 (NR/NR)

IKANO '17 (NR/NR)IKANO '16 (NR/NR)

IKANO '17 (NR/NR)IKANO '17 (NR/NR)

IKANO '16 (NR/NR)

IKANO '16 (NR/NR)

IKANO '15 (NR/NR)

NORDAX '16 (NR/NR)

SBAB '21 (A/A2)

SBAB '18 (A/A2)SBAB '17 (A/A2)

SBAB '16 (NR/A2)

SBAB '15 (NR/A2)

SBAB '14 (A/A2)0

25

50

75

100

125

150

175

200

225

250

2014 2015 2016 2017 2018 2019 2020 2021

Indicative ASW offer (bps)

12 | 30 October 2014 www.danskeresearch.com

Ikan

o B

an

k

Ikano Bank

NIM

Source: Company data, Danske Bank Markets

Moving on to the loan loss ratio (LLR), Ikano Bank is at the very top with the reported

1.6% for 2013. At first glance this is negative, but it could be a result of a more

conservative provisioning policy and not just worse asset quality.

Loan losses in % of avg. receivables (lending and leasing)

Source: Company data, Danske Bank Markets

One factor that speaks in favour of the high loan loss ratio being a result of conservatism

is the size of impaired loans in % of total receivables (mainly lending but in the case of

e.g. Ikano Bank also leasing). Only 5% of receivables are impaired, which is only second

to one other bank in the peer group. GE Money Bank is one of a kind with 32% of its

receivables being impaired. Note that Santander bought GE Money Bank AB in June

2014.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2009 2010 2011 2012 2013Ikano Bank Eika KredittbankBank Norwegian GE Money BankNordax Santander Consumer Bank Nordics

0.00%

1.00%

2.00%

3.00%

4.00%

2009 2010 2011 2012 2013Ikano Bank Eika KredittbankBank Norwegian GE Money BankNordax Santander Consumer Bank Nordics

13 | 30 October 2014 www.danskeresearch.com

Ikan

o B

an

k

Ikano Bank

Impaired receivables in % of receivables (lending and leasing)

Source: Company data, Danske Bank Markets

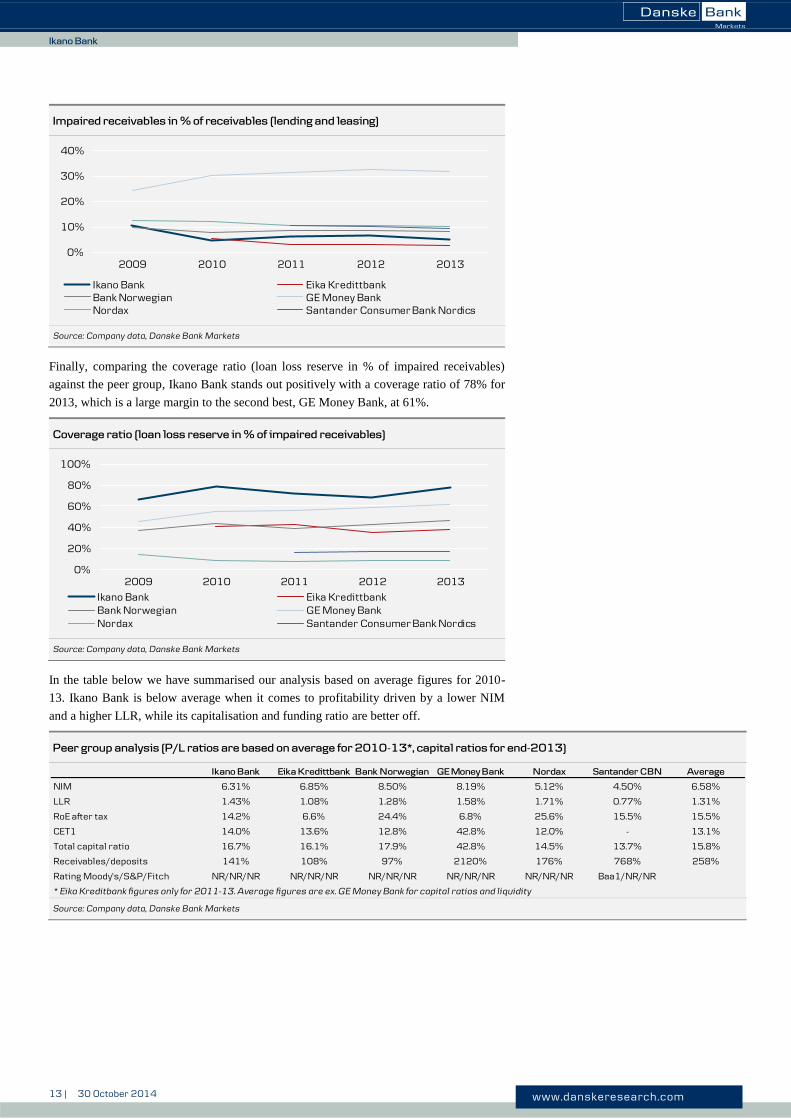

Finally, comparing the coverage ratio (loan loss reserve in % of impaired receivables)

against the peer group, Ikano Bank stands out positively with a coverage ratio of 78% for

2013, which is a large margin to the second best, GE Money Bank, at 61%.

Coverage ratio (loan loss reserve in % of impaired receivables)

Source: Company data, Danske Bank Markets

In the table below we have summarised our analysis based on average figures for 2010-

13. Ikano Bank is below average when it comes to profitability driven by a lower NIM

and a higher LLR, while its capitalisation and funding ratio are better off.

Peer group analysis (P/L ratios are based on average for 2010-13*, capital ratios for end-2013)

Ikano Bank Eika Kredittbank Bank Norwegian GE Money Bank Nordax Santander CBN Average

NIM 6.31% 6.85% 8.50% 8.19% 5.12% 4.50% 6.58%

LLR 1.43% 1.08% 1.28% 1.58% 1.71% 0.77% 1.31%

RoE after tax 14.2% 6.6% 24.4% 6.8% 25.6% 15.5% 15.5%

CET1 14.0% 13.6% 12.8% 42.8% 12.0% - 13.1%

Total capital ratio 16.7% 16.1% 17.9% 42.8% 14.5% 13.7% 15.8%

Receivables/deposits 141% 108% 97% 2120% 176% 768% 258%

Rating Moody's/S&P/Fitch NR/NR/NR NR/NR/NR NR/NR/NR NR/NR/NR NR/NR/NR Baa1/NR/NR

* Eika Kreditbank figures only for 2011-13. Average figures are ex. GE Money Bank for capital ratios and liquidity Source: Company data, Danske Bank Markets

0%

10%

20%

30%

40%

2009 2010 2011 2012 2013

Ikano Bank Eika KredittbankBank Norwegian GE Money BankNordax Santander Consumer Bank Nordics

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 2013

Ikano Bank Eika KredittbankBank Norwegian GE Money BankNordax Santander Consumer Bank Nordics

14 | 30 October 2014 www.danskeresearch.com

Ikan

o B

an

k

Ikano Bank

Our view of Ikano Bank

We assign an issuer credit rating of ‘BBB’ to Ikano Bank. The rating is based on a review

of the rating methodologies from the rating agencies and our assessment of Ikano Bank’s

business and financial risk profile.

We see the development away from being a sole consumer bank, predominantly granting

unsecured lending, to a more diversified bank with several different product offerings,

some with good collateral such as leasing and object financing, as credit positive.

Profitability with a RoE after tax of 8.8% for 2013 is a bit too low, in our view, whilst we

find asset quality and in particular the provisioning level to be high. In our peer group

analysis Ikano Bank stands out positively when it comes to coverage ratio, which speaks

of a conservative provisioning policy.

Capital-wise Ikano Bank is well off with a CET1 ratio of 14.7% and total capital ratio of

17.4% end-H1 14 (14% and 16.7% end-2013, respectively). This is higher than most

peers and positive from a credit perspective. Deposits are used as the main funding

source, which we find positive, but after having almost complete balance between

deposits and net receivables in 2012, the ratio has increased to 144% end-H1 14

following the acquisition in the UK in 2013.

We view Ikano Bank’s link to IKEA and not least the fact that the Kamprad family is the

sole owner of Ikano Bank as credit positive. However, we have not included any support

from the owner in our rating, as the financial results from the owner are not publicly

available. Moreover, Ikano Bank is generally run as an independent company. We might

consider a notch higher rating if the profitability improves further or a formal support

structure from the owner is introduced. Downside risk to our rating includes among others

deteriorating asset quality.

15 | 30 October 2014 www.danskeresearch.com

Ikan

o B

an

k

Ikano Bank

Financials and key figures

Income statement (SEKm) 2008 2009 2010 2011 2012 2013 H1 14

Net interest income 699 795 853 927 915 1,081 617

Fee & Commision Income 267 329 295 403 351 356 173

Trading & Fair Value Gains -2 -8 -22 -34 -34 7 1

Leasing Income 1,229 1,374 1,500 1,612 1,777 2,039 1,106

Other Income 79 73 124 177 280 142 117

Total Operating Income 2,272 2,562 2,749 3,085 3,290 3,625 2,014

Total Operating Expenses 1,728 1,955 2,043 2,284 2,528 2,897 1,622

Pre-Provision Income 543 608 706 801 762 728 392

Loan Losses and Provisions 245 416 172 241 242 295 146

Appropriations -31 153 -327 -33 -196 -178 -122

Pre-tax Income 267 345 207 527 324 255 124

Net Income 192 257 145 414 234 190 101

Balance sheet (SEKm) 2008 2009 2010 2011 2012 2013 H1 14

Loans 10,339 10,491 12,009 11,657 11,584 14,887 15,664

Loan Loss Reserve 419 894 499 643 673 744 794

Leasing 2,848 3,311 3,320 3,632 4,255 4,943 5,288

Loan Loss Reserve Leasing 15 114 77 64 57 57 0

Total Assets 14,609 15,977 17,779 19,206 20,107 23,783 25,226

Risk exposure amount (REA) 8,887 14,920 15,382 16,346 16,537 20,093 20,487

Customer Deposits 6,735 8,953 10,717 12,692 13,831 14,075 14,531

Market Funds 509 2,202 2,387 2,008 1,640 2,622 3,286

Subordinated debt 241 394 554 553 542 551 566

Equity 1,340 1,498 1,420 1,809 1,944 2,370 2,504

Growth % 2008 2009 2010 2011 2012 2013 H1 14

Receivables, Gross - 8.7% 7.4% 0.6% 3.6% 24.5% 5.4%

Total Assets - 9.4% 11.3% 8.0% 4.7% 18.3% 6.1%

Risk-weighted Assets - 67.9% 3.1% 6.3% 1.2% 21.5% 2.0%

Customer Deposits - 32.9% 19.7% 18.4% 9.0% 1.8% 3.2%

Pre-Provision Income - 12% 16% 13% -5% -4% 0%

Net Income - 34% -44% 186% -44% -19% 0%

Asset Quality & Market Risk 2008 2009 2010 2011 2012 2013 H1 14

Impaired Receivables % Gross Receivables and Guarantees - 10.3% 4.6% 6.1% 6.4% 5.0% 5.1%

Impaired Receivables % (Equity + Loss Reserves) - 61% 37% 39% 40% 32% 34%

Loss Reserves % Impaired Receivables - 66% 79% 72% 69% 78% 71%

Loss Reserves % Gross Receivables & Guarantees - 6.8% 3.6% 4.4% 4.4% 3.9% 3.7%

Equities & Non-Trading Assets % Adj. Equity - 0.1% 0.1% 0.1% 0.1% 0.1% 0.1%

Earnings 2008 2009 2010 2011 2012 2013 H1 14

Net Interest Margin (Including Dividends) - 6.38% 6.18% 6.25% 6.13% 6.67% 6.77%

PPI % Avg. RWA - 5.11% 4.66% 5.05% 4.63% 3.97% 3.83%

PPI excl Trading % Avg. RWA - 5.18% 4.81% 5.27% 4.84% 3.94% 3.82%

Net Income % Avg. RWA - 2.16% 0.96% 2.61% 1.42% 1.04% 0.98%

Efficiency 2008 2009 2010 2011 2012 2013 H1 14

Adjusted Cost % Operating Income 57% 57% 54% 54% 56% 61% 63%

Operating Expenses % Avg. Assets 23.7% 12.8% 12.1% 12.4% 12.9% 13.2% 12.9%

Liquidity 2008 2009 2010 2011 2012 2013 H1 14

Avg. Customer Deposits % Avg. Total Funding - 66% 71% 76% 82% 80% 72%

Avg. Gross Loans % Avg. Customer Deposits - 141% 121% 106% 93% 100% 112%

Market Funds Reliance (Total Assets) - 14.4% 12.0% 1.0% -3.9% 5.7% 8.0%

Capitalisation 2008 2009 2010 2011 2012 2013 H1 14

Common Equity Tier-1 Ratio (CET1) 11.9% 9.6% 9.9% 11.7% 13.5% 14.0% 14.7%

Total Capital Ratio 12.7% 12.2% 13.5% 15.1% 16.5% 16.7% 17.4% Note: We have used historical exchange rates in order to change 2008-2011 from EUR into SEK

Source: Company data, Danske Bank Markets

16 | 30 October 2014 www.danskeresearch.com

Ikan

o B

an

k

Ikano Bank

Knut-Ivar Bakken

Fish farming (+47) 85 40 70 74 [email protected]

Wiveca Swarting

Real Estate, Construction (+46) 8 568 80617 [email protected]

Ola Heldal

TMT (+47) 85408433 [email protected]

Henrik René Andresen

Credit Portfolios (+45) 45 13 33 27 [email protected]

Brian Børsting

Industrials (+45) 45 12 85 19 [email protected]

Mads Rosendal

Industrials, Pulp & Paper (+45) 45 14 88 79 [email protected]

Lars Holm

Financials (+45) 45 12 80 41 [email protected]

Jakob Magnussen

Utilities, Energy (+45) 45 12 85 03 [email protected]

Åse Haagensen

High Yield, Industrials (+47) 22 86 13 22 [email protected]

Fixed Income Credit Research

Louis Landeman

TMT, Industrials (+46) 8 568 80524 [email protected]

Thomas Hovard

Head of Credit Research (+45) 45 12 85 05

Find the latest Credit Research

Danske Bank Markets: Bloomberg: http://www.danskebank.com/danskemarketsresearch DNSK<GO>

Gabriel Bergin

Strategy, Industrials (+46) 8 568 80602 [email protected]

Niklas Ripa

High Yield, Industrials (+45) 45 12 80 47 [email protected]

Bjørn Kristian Røed

Shipping (+47) 85 40 70 72 [email protected]

Sondre Dale Stormyr

Offshore rigs (+47) 85 40 70 70 [email protected]

Øyvind Mossige

Oil services (+47) 85 40 54 91 [email protected]

17 | 30 October 2014 www.danskeresearch.com

Ikan

o B

an

k

Ikano Bank

Disclosures This research report has been prepared by Danske Bank Markets, a division of Danske Bank A/S (‘Danske

Bank’). The authors of the research report are Lars Holm, Senior Analyst and Thomas Hovard, Chief Analyst.

Analyst certification

Each research analyst responsible for the content of this research report certifies that the views expressed in the

research report accurately reflect the research analyst’s personal view about the financial instruments and issuers

covered by the research report. Each responsible research analyst further certifies that no part of the compensation

of the research analyst was, is or will be, directly or indirectly, related to the specific recommendations expressed

in the research report.

Regulation

Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject

to the rules and regulation of the relevant regulators in all other jurisdictions where it conducts business. Danske

Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority

(UK). Details on the extent of the regulation by the Financial Conduct Authority and the Prudential Regulation

Authority are available from Danske Bank on request.

The research reports of Danske Bank are prepared in accordance with the Danish Society of Financial Analysts’

rules of ethics and the recommendations of the Danish Securities Dealers Association.

Conflicts of interest

Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high-

quality research based on research objectivity and independence. These procedures are documented in Danske

Bank’s research policies. Employees within Danske Bank’s Research Departments have been instructed that any

request that might impair the objectivity and independence of research shall be referred to Research Management

and the Compliance Department. Danske Bank’s Research Departments are organised independently from and do

not report to other business areas within Danske Bank.

Research analysts are remunerated in part based on the overall profitability of Danske Bank, which includes

investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate

finance or debt capital transactions.

Danske Bank, its affiliates, subsidiaries and staff may perform services for or solicit business from Ikano Bank

and may hold long or short positions in, or otherwise be interested in, the financial instruments mentioned in this

research report. The Equity and Corporate Bonds analysts of Danske Bank and undertakings with which the

Equity and Corporate Bonds analysts have close links are, however, not permitted to invest in financial

instruments that are covered by the relevant Equity or Corporate Bonds analyst or the research sector to which the

analyst is linked.

Danske Bank, its affiliates and subsidiaries are engaged in commercial banking, securities underwriting, dealing,

trading, brokerage, investment management, investment banking, custody and other financial services activities,

may be a lender to Ikano Bank and have whatever rights are available to a creditor under applicable law and the

applicable loan and credit agreements. At any time, Danske Bank, its affiliates and subsidiaries may have credit

or other information regarding Ikano Bank that is not available to or may not be used by the personnel responsible

for the preparation of this report, which might affect the analysis and opinions expressed in this research report.

As an investment bank, Danske Bank, its affiliates and subsidiaries provide a variety of financial services,

including investment banking services. It is possible that Danske Bank and/or its affiliates and/or its subsidiaries

might seek to become engaged to provide such services to Ikano Bank in the next three months.

Danske Bank has made no agreement with Ikano Bank to write this research report. Parts of this research report

have been disclosed to Ikano Bank. No recommendations or opinions have been disclosed to Ikano Bank and no

amendments have accordingly been made to the same before dissemination of the research report.

Financial models and/or methodology used in this research report

Calculations and presentations in this research report are based on standard econometric tools and methodology

as well as publicly available statistics for each individual security, issuer and/or country. Documentation can be

obtained from the authors on request.

Risk warning

Major risks connected with recommendations or opinions in this research report, including a sensitivity analysis

of relevant assumptions, are stated throughout the text.

18 | 30 October 2014 www.danskeresearch.com

Ikan

o B

an

k

Ikano Bank

Expected updates

Credit Update: This research report will be updated on a quarterly basis following the quarterly results statements

from Ikano Bank.

Scandi Handbook: This research report will be updated bi-annually, usually in April and October.

See the front page of this research report for the date of first publication.

Recommendation structure

Investment recommendations are based on the expected development in the credit profile as well as relative value

compared with the sector and peers.

As at 30 September 2014 Danske Bank Markets had investment recommendations on 49 corporate bond issuers.

The distribution of recommendations is represented in the distribution of recommendations column below. The

proportion of issuers corresponding to each of the recommendation categories above to which Danske Bank

provided investment banking services in the previous 12 months ending 30 September 2014 is shown below.

Rating

Anticipated performance

Time horizon

Distribution of

recommendations

Investment banking

relationships

Buy Outperformance relative to peer group 3 months 33% 50%

Hold Performance in line with peer group 3 months 53% 42%

Sell Underperformance relative to peer group 3 months 14% 14%

Changes in recommendation within past 12 months:

Date New recommendation Old recommendation

30 October 2014 Not Rated N/A

General disclaimer This research has been prepared by Danske Bank Markets (a division of Danske Bank A/S). It is provided for

informational purposes only. It does not constitute or form part of, and shall under no circumstances be

considered as, an offer to sell or a solicitation of an offer to purchase or sell any relevant financial instruments

(i.e. financial instruments mentioned herein or other financial instruments of any issuer mentioned herein and/or

options, warrants, rights or other interests with respect to any such financial instruments) (‘Relevant Financial

Instruments’).

The research report has been prepared independently and solely on the basis of publicly available information that

Danske Bank considers to be reliable. While reasonable care has been taken to ensure that its contents are not

untrue or misleading, no representation is made as to its accuracy or completeness and Danske Bank, its affiliates

and subsidiaries accept no liability whatsoever for any direct or consequential loss, including without limitation

any loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts responsible for the research report and

reflect their judgement as of the date hereof. These opinions are subject to change, and Danske Bank does not

undertake to notify any recipient of this research report of any such change nor of any other changes related to the

information provided in this research report.

This research report is not intended for retail customers in the United Kingdom or the United States.

This research report is protected by copyright and is intended solely for the designated addressee. It may not be

reproduced or distributed, in whole or in part, by any recipient for any purpose without Danske Bank’s prior

written consent.

Disclaimer related to distribution in the United States This research report is distributed in the United States by Danske Markets Inc., a U.S. registered broker-dealer

and subsidiary of Danske Bank, pursuant to SEC Rule 15a-6 and related interpretations issued by the U.S.

Securities and Exchange Commission. The research report is intended for distribution in the United States solely

to ‘U.S. institutional investors’ as defined in SEC Rule 15a-6. Danske Markets Inc. accepts responsibility for this

research report in connection with distribution in the United States solely to ‘U.S. institutional investors’.

19 | 30 October 2014 www.danskeresearch.com

Ikan

o B

an

k

Ikano Bank

Danske Bank is not subject to U.S. rules with regard to the preparation of research reports and the independence

of research analysts. In addition, the research analysts of Danske Bank who have prepared this research report are

not registered or qualified as research analysts with the NYSE or FINRA but satisfy the applicable requirements

of a non-U.S. jurisdiction.

Any U.S. investor recipient of this research report who wishes to purchase or sell any Relevant Financial

Instrument may do so only by contacting Danske Markets Inc. directly and should be aware that investing in non-

U.S. financial instruments may entail certain risks. Financial instruments of non-U.S. issuers may not be

registered with the U.S. Securities and Exchange Commission and may not be subject to the reporting and

auditing standards of the U.S. Securities and Exchange Commission.