investment research general market conditions weekly focus · stronger-than-expected developments...

TRANSCRIPT

Important disclosures and certifications are contained from page 14 of this report. www.danskeresearch.com

Investment Research — General Market Conditions

Market movers ahead

In the US, next week’s main event is the FOMC meeting on Wednesday. Stronger

growth in H2 supports our view that the Fed will raise the target range by 25 points. All

eyes will be on indicators for next year’s hiking path.

OPEC is set to meet non-OPEC producers in Vienna tomorrow to discuss oil output

cuts.

The Bank of England (BoE) meets on Thursday. We do not expect any action, so focus

will be on the tone of the minutes. We think we need to see significantly slower growth

and/or higher unemployment before easing becomes likely again.

Next week, we will get inflation data out of Sweden and Denmark. We expect it to

show that annual inflation has picked up in both countries. This is the final piece of

meaningful information the Riksbank will receive before its monetary policy meeting

on 20 December.

At the Norges Bank meeting, we expect a 10-15bp downward revision of the interest

rate path for next year. However, we do not expect Norges Bank to cut rates, due to

stronger-than-expected developments in the housing market.

Global macro and market themes

There is a strong case for further extension of ECB QE purchases beyond December

2017.

Solid US data lend support for the reflation case.

Fed doves will only partly offset the expected fiscal boost from Donald Trump.

Focus

The ECB extends QE purchases by nine months (see ECB Review: Less 'punch in the

bowl' from Draghi, 8 December).

ECB extends QE – and we expect it to

do it again

Fed set to hike – markets to focus on

next year

Source: ECB, Danske Bank Markets Source: Macrobond Financial

0

10

20

30

40

50

60

70

80

90

jan-16 jul-16 jan-17 jul-17 jan-18 jul-18Current QE programme ECB announce QE extension (December)Potential additional QE extensions

EUR bn Monthly QE purchases

?

Contents

Market movers ....................................................... 2

Global Macro and Market Themes ........... 6

Scandi Update ......................................................... 8

Latest research from Danske Bank

Markets ........................................................................ 9

Macroeconomic forecast ............................ 10

Financial forecast .............................................. 11

Calendar .................................................................. 12

9 December 2016

Editor Louise Aggerstrøm Hansen Senior Analyst +45 12 85 31 [email protected]

Weekly Focus

Fed will give us a rate hike for Christmas

Financial views

Source: Danske Bank

Follow us on Twitter for the latest on

macroeconomic and financial market developments:

@Danske_Research

Major indices

09-Dec 3M 12M

10yr EUR swap 0.76 0.75 1.35

EUR/USD 106 104 112

ICE Brent oil 54 49 55

09-Dec 6M 12-24M

S&P500 2246 5 -10% 10-15%

2 | 9 December 2016 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Market movers

Global

The Organisation of Petroleum Exporting Countries (OPEC) is set to meet a group of

non-OPEC oil producers, including Mexico and Russia, on Saturday 10 December in

Vienna to discuss contributions from non-OPEC producers to the OPEC agreement to

cut output from last week. OPEC has pledged to cut output by 1.2m bpd and is looking

for non-OPEC producers to contribute with 600,000bpd in output cuts.

In the US next week, focus will be on the FOMC meeting, with the policy

announcement on Wednesday at 20:00 CET. It is one of the big meetings with updated

‘dots’ and a press conference. At its last meeting, the FOMC noted that the case for a

hike ‘has continued to strengthen’, although it would like to see ‘some further evidence

of continued progress towards its objectives’. As growth has rebounded in H2 16,

following a weak H1 16, the labour market continues to tighten, wage growth is

increasing and financial markets are calm, we think (in line with consensus and market

pricing) that the Fed will raise the target range by 25 points to 0.50-0.75%. Most focus

will be on what to expect from the Fed next year. We expect the ‘median dots’ to stay

unchanged at two hikes in 2017 and three hikes in 2018. Our own expectation is that

the Fed will hike twice each year. Triggers for the next Fed hike will be higher wage

growth and higher actual core inflation. For more details see FOMC Preview: Fed to

hike - focus on outlook for 2017, 9 December.

In terms of data releases, retail sales data for November are due on Wednesday. We

estimate the retail sales control group (which feeds into GDP) rose 0.4% m/m in

November, so Q4 seems like another strong quarter for private consumption. With

consumer confidence at a high level, we expect private consumption to continue to be

the main growth engine in the US.

On Thursday, we get the preliminary Markit PMI manufacturing index for December.

The index rose to 54.1 in November, the highest level since October 2015 but,

unfortunately, we have not seen higher actual production yet (November data are due

on Wednesday). It seems as though the global manufacturing business cycle has turned,

as global PMIs are increasing across regions and we expect this trend to continue, so

we expect a slight increase in the Markit PMI manufacturing index to 54.5.

Also on Thursday, we are due to get the CPI figures for November. CPI core inflation

has been more or less flat in 2016, suggesting that the economy still has room to run.

We estimate the core CPI index (s.a.) rose 0.2% m/m in November implying an

unchanged core inflation rate of 2.2% y/y. We estimate the headline CPI index

increased 0.2% m/m in November, implying the headline inflation rate increased to

1.7% y/y from 1.6% y/y in October, due mainly to the base effects of energy prices.

In the euro area, the first release of interest is the German ZEW expectations on

Tuesday. Since July, ZEW expectations have followed a rising tendency to 13.8 in

November but the December figure may bring this tendency to a halt. The Sentix

released this week saw an unexpected fall, which maybe reflected the uncertainty

related to the Italian referendum. However, although the ‘no’ vote in Italy on Sunday

caused an initial fall in equities on Monday morning, they quickly recovered within the

first few hours of the day. Therefore, we expect a somewhat unchanged ZEW with a

risk of a small decrease.

Fed hike fully priced in the markets,

focus on what to expect next year

Source: Bloomberg, Federal Reserve

Markit PMI manufacturing index is

increasing

Source: Markit Economics, Federal Reserve

ZEW set to lose momentum

Source: Sentix, ZEW, Danske Bank Markets

3 | 9 December 2016 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

The euro area employment growth figure for Q3 is also scheduled to be released on

Tuesday. The Q1 and Q2 figures were solid, with 0.4% quarterly employment growth,

and we expect a similar figure for Q3. Related to employment, the labour costs figure

for Q3 is due to be released on Friday. Despite the solid employment growth in recent

quarters, wage growth is still not picking up and we believe the ECB is still too

optimistic in its projections on wage growth in the new forecast released this week.

Labour costs growth has been very low in recent quarters and the Q2 figure was as low

as 1% yearly growth. We expect the Q3 figure to remain low.

On Wednesday, we get the euro area industrial production figures for October. Like the

modest increase in the German figure released this week, we expect the euro area

production figure to show positive growth in October.

On Thursday, the euro area PMI figures are due for release. Over the past three months,

we have seen improving PMIs but the leading indicators suggest a loss of momentum.

The manufacturing PMI order-inventory balance showed a slowdown in November,

which indicates the December manufacturing PMI will not see a further increase but

has a risk of a small decrease instead. The signals for services PMI for December are

more mixed. The future business expectations index decreased marginally, while the

incoming new business index increased. Overall, we expect the services PMI to remain

broadly unchanged.

In the UK, we have a very busy week next week. The most important event is the Bank

of England (BoE) meeting on Thursday. We expect the BoE to maintain its monetary

policy unchanged in line with consensus and market pricing. Focus is on the minutes,

as it is one of the small meetings without an updated Inflation Report and a press

conference, but we do not expect them to contain any big news, as economic data

continue to be resilient to Brexit uncertainties. At the November meeting, the BoE

shifted from easing to a neutral bias (see Bank of England Review: BoE shifts from

easing to neutral bias – we no longer expect a further rate cut, 3 November) and while

we think it is unlikely that the BoE will tighten monetary policy in a time of elevated

political uncertainty, we think we would need to see significantly slower growth and/or

higher unemployment before easing becomes likely again.

In terms of data releases, we get CPI data for November on Tuesday. We estimate the

headline index rose 0.2% m/m in November, implying that the CPI inflation rate rose

to 1.1% y/y, from 0.9% in October. The increase is driven mainly by higher energy

prices and a smaller negative contribution from non-energy industrial goods. We

estimate the core index rose 0.2% m/m, implying an increase in the CPI core inflation

rate to 1.4% y/y, from 1.2%.

On Wednesday, we get the labour market report for October. The labour market has

been quite resilient to Brexit uncertainties so far, although the increase in claimant

counts in recent months may be a bit worrying. This said, we estimate the

unemployment rate (3M average) rose back to 4.9%, from 4.8%, as the very low single-

month print in July falls out of the three-month average. We estimate average weekly

earnings excluding bonuses (3M average) rose 2.5% y/y in October, up from 2.4% y/y

in September.

We also intend to look out for retail sales data for November on Thursday.

PMI manufacturing set to decline

Source: Markit PMI, Danske Bank Markets

BoE on hold next week, as the UK

economy continues to be resilient

Source: ONS, Markit Economics

UK unemployment rate likely rose to

4.9%, as very low July print falls out of

the three-month average

Source: ONS

4 | 9 December 2016 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

China is set to release a batch of data on Wednesday, as industrial production, retail

sales and fixed asset investments are due. Chinese PMI manufacturing has been strong

recently, suggesting that industrial production should see a further pickup. However,

industrial production data have generally been weaker than the picture painted by PMI,

giving some uncertainty to the forecast. We look for an unchanged growth rate of 6.1%

y/y in November. Electricity production which is a better indicator for activity is likely

to continue to show a robust growth rate. Retail sales have hovered just above 10% y/y

over the past two years and we do not see any change to this picture in November. Fixed

asset investments have generally shown a pickup in public infrastructure investment,

while private investments have stayed weak. We expect this to be the case in November

as well. We could see a small decline in infrastructure investment though, as investment

plans have pointed to a fading boost from the infrastructure programme launched early

in the year.

China is also set to release credit data (Total Social Finance). Over the past three to four

months, our measure of the credit impulse has weakened quite strongly. We see it as a

sign that credit-fuelled infrastructure investment is slowing somewhat, which is part of

the reason we look for slower growth in 2017. We estimate the credit impulse remained

soft in November.

Scandi

In Denmark, the statistical office is due to release inflation figures for November on

Monday. We expect base effects from the fall in food prices to push up the rate of

inflation, which has been hit hard by falling prices for mobile telephony and clothing.

We expect prices to climb 0.0% m/m and 0.5% y/y. Elsewhere, the Association of

Danish Mortgage Banks releases its housing market data for Q3 on Friday. We already

have Statistics Denmark’s figures for how prices have moved on a nationwide basis but

it will be interesting to see what has been happening at a local level.

In Sweden, the week ahead provides some long-awaited data on inflation (due Tuesday

at 09:30 CET). Given the recent weakening of the SEK and a rise in oil prices, we

expect a pronounced uptick in the overall CPI inflation numbers but more subdued

developments in ‘core’ measures such as CPIF excluding energy (see chart). This is the

final piece of (meaningful) information the Riksbank will receive before its upcoming

monetary policy meeting on Tuesday 20 December (decision published 21 December

at 09:30 CET), so its importance should not be underestimated.

Also, Statistics Sweden (SCB) is set to reveal how the labour market is faring when it

publishes the labour force survey on Thursday (at 09:30 CET). By and large, we expect

the current trends of continued (but moderating) employment growth and a relatively

stable unemployment rate to continue. This said, we note that the unemployment rate,

in particular, is a fairly volatile time series, so it might be wiser to look at trend estimates

(published simultaneously by the SCB).

Chinese credit impulse points to

weakening ahead

Source: Macrobond Financial

Inflation still hovering close to zero

Source: Statistics Denmark

Inflation outlook still troubling

Source: Statistics Sweden, Riksbank. Danske

calculations

5 | 9 December 2016 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

In Norway, Norges Bank is due to hold a rate-setting meeting and publish a new

monetary policy report on Thursday. Although the September report indicated a

roughly 40% chance of a further rate cut by June next year, the executive board was

much clearer in its communication, taking pains to signal that interest rates have hit

bottom – a message that was repeated at the meeting in October. Since September,

global forward rates have picked up and there is also reason to expect Norges Bank to

revise up its global growth projections slightly. In isolation, this would push up the

interest rate path somewhat. On the other hand, inflation seems to be weaker than

expected and the wage growth data from the regional network survey suggest that the

wage projections for 2017 in the September report were too high. Nibor rates are higher

than Norges Bank assumed. Together with higher bank lending rates, this points to a

slightly lower interest rate path. The NOK has also been slightly stronger than expected,

although this is probably due to oil prices being USD6-7/bl higher than assumed. It also

appears that the domestic growth outlook may have deteriorated slightly but both

unemployment data and the capacity constraints in the regional network survey suggest

that capacity utilisation has been more or less as expected. Nevertheless, our analysis

indicates, on balance, that we are looking at a 10-15bp downward revision of the

interest rate path for next year. In isolation, this would mean the new path showing an

almost 100% chance of a further rate cut. However, the reason we do not expect Norges

Bank to go that far but to continue signalling that interest rates have probably hit bottom

is that the housing market seems to have been even stronger than expected. The long-

term costs of lowering interest rates further have risen and there is also less need for a

cut now that growth is picking up and interest rates seem to have bottomed elsewhere

in the world.

Market movers ahead

Source: Bloomberg, Danske Bank Markets

Global movers Event Period Danske Consensus Previous

Tue 13-Dec 3:00 CNY Industrial production y/y Nov 6.1% 6.1% 6.1%

3:00 CNY Retail sales y/y Nov 10.2% 10.2% 10.0%

10:30 GBP CPI m/m|y/y Nov 0.2%|1.1% 0.2%|1.1% 0.1%|0.9%

11:00 DEM ZEW expectations Index Dec 13.5 14.0 13.8

Wed 14-Dec 10:30 GBP Average weekly earnings ex bonuses (3M) y/y Oct 2.5% 2.6% 2.4%

14:30 USD Retail sales control group m/m Nov 0.4% 0.5% 0.8%

20:00 USD FOMC meeting % 0.75% 0.75% 0.50%

20:00 USD Updated projections

20:30 USD Yellen press conference

Thurs 15-Dec 9:30 CHF SNB 3-month Libor target rate % -0.75% -0.75% -0.75%

10:00 EUR PMI composite, preliminary Index Dec 53.8 53.9

13:00 GBP BoE Bank rate % 0.25% 0.25% 0.25%

14:30 USD CPI core m/m|y/y Nov 0.2%|2.2% 0.2%|2.2% 0.1%|2.2%

15:45 USD Markit PMI manufacturing, preliminary Index Dec 54.5 54.1

Fri 16-Dec 11:30 RUB Central Bank of Russia rate decision % 10.0% 10.0% 10.0%

Scandi movers

Mon 12-Dec 9:00 DKK CPI m/m|y/y Nov 0.0%|0.5% -0.1%|0.4% 0.2%|0.3%

Tue 13-Dec 9:30 SEK Underlying inflation CPIF m/m|y/y Nov 0.0%|1.6% 0.1%|1.6% 0.4%|1.4%

Wed 14-Dec 8:00 SEK Prospera inflation expectations

Thurs 15-Dec 10:00 NOK Norges Banks monetary policy meeting % 0.50% 0.50% 0.50%

Higher oil price behind krone rally

Source: Macrobond Financial, Danske Bank

Markets

6 | 9 December 2016 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Global Macro and Market Themes

The danger of the consensus view

Since the Donald Trump US presidential election victory, a strong consensus has

formed that the USD will strengthen substantially and that US rates will head a lot

higher. The story goes that Trump-led fiscal stimulus will drive a higher US neutral rate

and a stronger USD – much like during the first Ronald Reagan administration in 1981-84.

Near term, we agree – rising US growth expectations will drive a stronger USD and

higher global rates. As we have pointed out recently (see Strategy: The case for reflation

– what it means and what to watch, 18 November), the US economy was already gaining

speed before the Trump victory. Over the past few weeks, euro area October retail sales,

Germany factory orders and China PMI Manufacturing have all surprised substantially on

the upside, suggesting that the US-led recovery is spreading to Europe. However, for us,

the view of a stronger USD is a short-term one and there is a high risk that the push higher

in global yields will lose steam.

For a start, there is a lot of uncertainty about the type of US fiscal stimulus and how

quickly it will filter through to the economy. For example, the infrastructure spending

that Trump has been advocating will not be financed by the federal government but rather

by a ‘deficit-neutral system of infrastructure credits’. There is no guarantee that Congress

will agree to the tax credits or that business will respond as intended. In addition, Trump’s

tax cuts will tend to benefit the ‘better off’, who have a lower propensity to consume and

hence a lower fiscal multiplier (see Table 1). Finally, the output gap in the US is largely

closed, which suggests that fiscal stimulus will be more inflationary than growth boosting

and there may be a negative growth impact beyond a year (see Table 2 overleaf).

Chart 1: The USD tends to weaken

when the US budget deficit widens…

Chart 2: …and Trump is not Reagan, as

real interest rates will NOT rise

Source: Macrobond Financial; Danske Bank Source: Macrobond Financial, Danske Bank

Key points

The market is convinced that

significant US fiscal stimulus will

drive a stronger USD and higher

rates – particularly US rates.

However, there is high uncertainty

regarding the type of US fiscal

stimulus and how it will filter

through to the economy.

For now, we are USD bulls and

bearish US FI.

However, an inflationary US fiscal

boost should over time lead to a

weaker USD – not a stronger one.

Table 1: US fiscal multipliers are low

for tax cuts for higher income earners

Source: Congressional Budget Office

7 | 9 December 2016 www.danskeresearch.com

Weekly Focus

As such, there is a substantial risk that at some point during 2017 the market will be

disappointed with US growth prospects. From a USD perspective, Trump/Janet Yellen are

very different from how Reagan/Paul Volker were during the early 1980s, when significant

fiscal stimulus was combined with a much more hawkish outlook, driving a rapid increase

in real interest rates (see Chart 1 and Chart 2). Indeed, we see the risks skewed towards the

Fed lowering its long-term neutral rate at next week’s meeting. In our view, the FOMC will

shift in a more dovish direction in 2017 due to the change in voting rights, even taking into

account that Trump may appoint hawkish governors for the two vacant seats. We note that

the Fed’s trade-weighted dollar has reached the strongest level since 2002. If the USD

becomes too strong, the Fed will turn dovish exactly as it did early this year. Hence,

Trump’s policies should lead to higher inflation and higher inflation expectations and lower

US real interest rates. This is exactly the opposite of the Reagan/Volcker period and is not

USD bullish – quite the opposite. Lower real interest rates should lead over time to a

weaker USD – not a stronger one.

Meanwhile, it is becoming increasingly costly to be bearish on US FI if you do not get the

timing right. For example, the 10Y UST yield is around 2.44%. Taking into account the

carry and roll-down, the 10Y UST yield will need to be above 2.70% in 12 months for

investors to make money being short 10Y UST now. We need only remind ourselves about

what happened in 2014 when the USD rallied strongly. At end-2013, most observers were

expecting a sharp increase in US rates but instead the 10Y UST yield fell to 2.17% at end-

2014, from 3.03% at end-2013. For 2017, it is difficult to imagine both that the USD will

rally sharply and that US rates will head a lot higher. Something has to give. In our view,

the USD will be first to give, when we expect dollar strength in late 2016 to early 2017

to give way to a broadly weaker greenback later in the year.

Table 3: Global market views

Source: Danske Bank Markets

Asset class Main factorsEquitiesOverweight stocks short and medium term Cyclical recovery.

Overweight US, underweight Europe and Nordics, underweight emerging markets (EM) Fiscal boost to US will raise earnings relative to Europe. High risk of protectionism and tighter monetary policy hurting EM assets.

Bond marketHigher yields, further steepening 2Y10Y curve

US-euro spread: slightly wider in 2017

Peripheral spreads: tightening Economic recovery and QE mean further tightening but politics and tapering remain clear risk factors.

Credit spreads: neutral The ECB is keeping spreads contained.

FXEUR/USD � lower going into FOMC meeting in December and early 2017 USD set to remain supported by Trump and Fed in the near term. EUR/USD to head higher beyond 3M.

EUR/GBP � risk skewed on the upside in the run-up to when the UK government is likely to trigger Article 50 Expect EUR/GBP to settle in the 0.83-0.88 range near term. Risk skewed on the upside over the medium term due to Brexit.

USD/JPY � neutral with short-term risks skewed on the upside USD/JPY set to remain supported near term by relative monetary policy and risk appetite.

EUR/SEK � set to stay elevated in coming months before turning in 2017 Gradually lower on relative fundamentals and valuation in 2017. Near term, the SEK will remain weak due mainly to the Riksbank.

EUR/NOK � short-term risks skewed on the upside At YE, liquidity set to prove a headwind for NOK. Cross set to move lower next year on valuation and real rate differentials normalising.

CommoditiesOil price � OPEC rally over; awaiting response from non-OPEC Support from positive growth and inflation sentiment; near-term focus implementation of OPEC deal.

Metal prices � rallying on outlook for US infrastructure spending Underlying support from consolidation in mining industry and recovery in global manufacturing.

Gold price � change in risk sentiment negative for gold price Rising yields and USD pushing gold price down.

Agriculturals � strong output has sent prices down again Attention has turned to La Niña weather risks over the winter, large stocks limit upside risk to prices.

More expansive fiscal policy in the US adds to steepening trend. Tapering, higher inflation prints and a global recovery also point to a steeper curve. ECB QE should mitigate some of the effects.

The Fed hike is moving closer, adding upside potential to the long end of the US curve but ECB tapering and higher inflation prints are risks for the European bond markets, which could potentially tighten the US-Euro spread given that European yields are record low.

Table 2: Fiscal multipliers are low when output is close to potential and Fed will react (as of now)

Source: Congressional Budget Office

The effect of a one dollar increase in aggregate demand over eight quarters

Quarter Low High Low High

1 0.5 1.5 0.5 1.42 0.0 0.6 0.0 0.53 0.0 0.3 0.0 0.14 0.0 0.2 -0.1 -0.15 0.0 0.0 -0.1 -0.36 0.0 0.0 -0.1 -0.37 0.0 0.0 -0.1 -0.38 0.0 0.0 -0.1 -0.3TOTAL 0.5 2.5 0.2 0.8

Output well below potential,

no Fed response

Output close to potential,

typical Fed response

8 | 9 December 2016 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Scandi Update

Denmark – Nationalbank warns of overheating in Copenhagen

apartment market

The Nationalbank published its latest forecast for the Danish economy during the week.

Overall, the forecast is very similar to our own, with moderate growth both this year and

next. The central bank also notes that apartment prices in Copenhagen are somewhat higher

than can be explained by incomes and interest rates. This is worrying, because it may be a

sign of overheating in the property market.

Statistics Denmark, meanwhile, released data for exports and the current account in

October. Exports of goods climbed 0.9% but this comes after a sluggish Q3. The current

account showed a surplus of DKK14.1bn, which is up slightly on September. Although the

surpluses on the current account are smaller than in 2015, they are still among the largest

in the world. The reasons for the decline include exports of services coming under pressure

this year from falling freight rates, which have pulled down earnings in the shipping

industry. However, the recent appreciation of the USD means that help may be on hand for

the shipping companies: they generally bill in USD, so a stronger USD means higher

revenue in DKK terms.

Although there was a sharp increase in repossessions in November in percentage terms, we

need to bear in mind that these figures can be volatile from month to month and that this

was from a low level. Finally, the industrial production figures for October showed an

increase but technicalities are currently causing such problems with the data that they are

very difficult to interpret.

Sweden – currency induced upswing?

Over the past few weeks, Swedish data has clearly stabilised and there are even hints of

reacceleration. However, so far, the improvement seems to be confined to industrial sectors,

which leads us to believe that it is the result of a recent weakening of the SEK. We saw

further signs of an industrial upswing over the past week, as both production and orders

developed strongly. To be specific, it is the low value added commodity-related industries

that seem to be enjoying the strongest boom currently. We have yet to see an amelioration

in consumption or inflation but next week should provide some input on possible currency

effects on inflation from the weak SEK.

Norway – lower trend growth

The aggregated output growth index in the regional network survey has edged down from

0.75 in August to 0.73, which points to growth in mainland GDP of just under 0.4% q/q

over the next two quarters, which is slightly less than Norges Bank assumed in its

September monetary policy report. The underlying data also reveal relatively minor

changes in different sectors. Greater optimism in business services offset slightly reduced

optimism in exports and construction. As business services (around 35% of GDP) are very

important for assessing the possible second-round effects of the downturn in the oil sector,

the improvement here reduces this risk. The oil supply sector was more or less unchanged

from August, with slightly weaker data on the domestic side offset by a slight improvement

on the export side. Taken together, this still points to a decline but with substantially weaker

headwinds than before the summer. Other data were also relatively encouraging: capacity

utilisation was slightly higher than in August and employment is expected to continue to

climb, albeit slightly less than in August. Lower growth but higher capacity utilisation than

expected suggest that trend growth has come down, which means we do not expect these

changes to have any great impact on future rate setting.

Another big current-account surplus

Source: Statistics Denmark

Sweden, another upswing ahead?

Note: One-sided HP filters are employed to take

away statistical noise

Source: Statistics Sweden

Capacity utilisation higher than

expected

Source: Macrobond Financial, Danske Bank

Markets

9 | 9 December 2016 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Latest research from Danske Bank Markets

FOMC Preview: Fed to hike - focus on outlook for 2017

We expect the Fed to raise the Fed funds target range 25bp to 0.50%-0.75% from the current

0.25%-0.50% at the FOMC meeting next week, in line with both consensus and market

pricing.

8/12 ECB review: less 'punch in the bowl' from Draghi

The ECB extended its QE purchases by nine months to December 2017, but reduced the

monthly purchases to EUR60bn from EUR80bn.

7/12 China: Decline in FX reserves shows rising vulnerability

Chinese FX reserves for November fell more than expected to USD3051.6bn – a decline

of around USD69.1 bn. Reserves have not been lower since February 2011.

10 | 9 December 2016 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

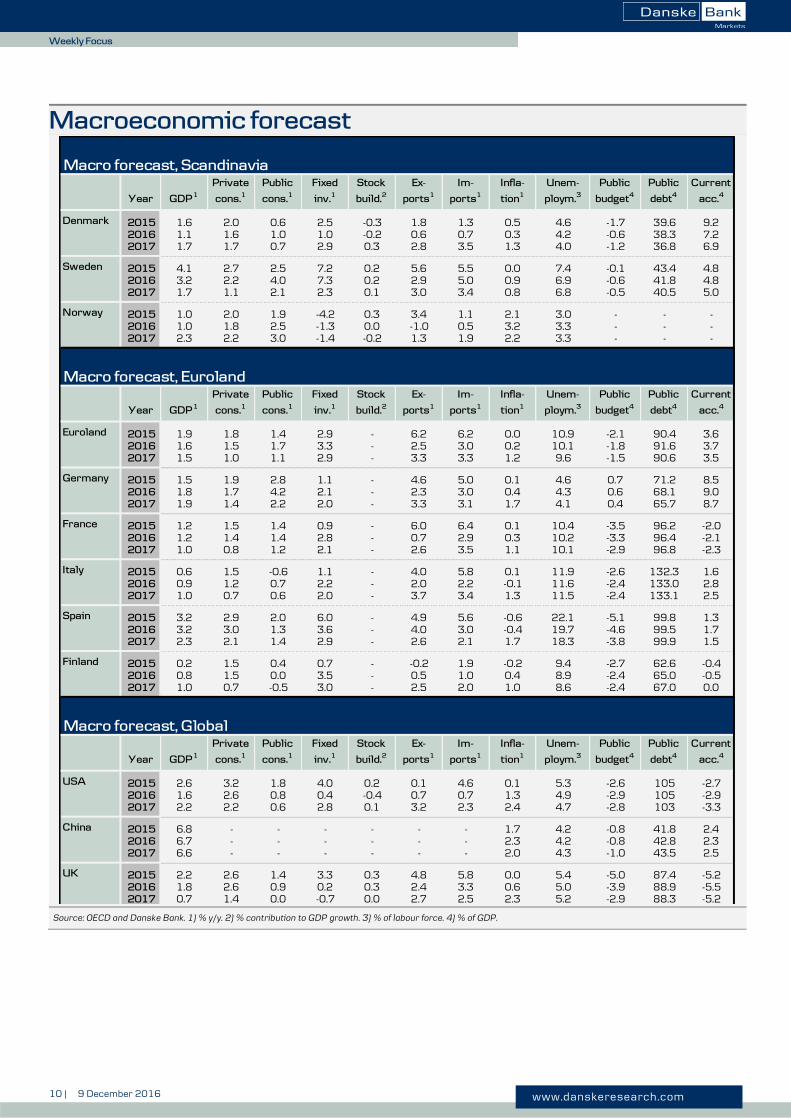

Macroeconomic forecast

Source: OECD and Danske Bank. 1) % y/y. 2) % contribution to GDP growth. 3) % of labour force. 4) % of GDP.

Macro forecast, Scandinavia

Denmark 2015 1.6 2.0 0.6 2.5 -0.3 1.8 1.3 0.5 4.6 -1.7 39.6 9.22016 1.1 1.6 1.0 1.0 -0.2 0.6 0.7 0.3 4.2 -0.6 38.3 7.22017 1.7 1.7 0.7 2.9 0.3 2.8 3.5 1.3 4.0 -1.2 36.8 6.9

Sweden 2015 4.1 2.7 2.5 7.2 0.2 5.6 5.5 0.0 7.4 -0.1 43.4 4.82016 3.2 2.2 4.0 7.3 0.2 2.9 5.0 0.9 6.9 -0.6 41.8 4.82017 1.7 1.1 2.1 2.3 0.1 3.0 3.4 0.8 6.8 -0.5 40.5 5.0

Norway 2015 1.0 2.0 1.9 -4.2 0.3 3.4 1.1 2.1 3.0 - - -2016 1.0 1.8 2.5 -1.3 0.0 -1.0 0.5 3.2 3.3 - - -2017 2.3 2.2 3.0 -1.4 -0.2 1.3 1.9 2.2 3.3 - - -

Macro forecast, Euroland

Euroland 2015 1.9 1.8 1.4 2.9 - 6.2 6.2 0.0 10.9 -2.1 90.4 3.62016 1.6 1.5 1.7 3.3 - 2.5 3.0 0.2 10.1 -1.8 91.6 3.72017 1.5 1.0 1.1 2.9 - 3.3 3.3 1.2 9.6 -1.5 90.6 3.5

Germany 2015 1.5 1.9 2.8 1.1 - 4.6 5.0 0.1 4.6 0.7 71.2 8.52016 1.8 1.7 4.2 2.1 - 2.3 3.0 0.4 4.3 0.6 68.1 9.02017 1.9 1.4 2.2 2.0 - 3.3 3.1 1.7 4.1 0.4 65.7 8.7

France 2015 1.2 1.5 1.4 0.9 - 6.0 6.4 0.1 10.4 -3.5 96.2 -2.02016 1.2 1.4 1.4 2.8 - 0.7 2.9 0.3 10.2 -3.3 96.4 -2.12017 1.0 0.8 1.2 2.1 - 2.6 3.5 1.1 10.1 -2.9 96.8 -2.3

Italy 2015 0.6 1.5 -0.6 1.1 - 4.0 5.8 0.1 11.9 -2.6 132.3 1.62016 0.9 1.2 0.7 2.2 - 2.0 2.2 -0.1 11.6 -2.4 133.0 2.82017 1.0 0.7 0.6 2.0 - 3.7 3.4 1.3 11.5 -2.4 133.1 2.5

Spain 2015 3.2 2.9 2.0 6.0 - 4.9 5.6 -0.6 22.1 -5.1 99.8 1.32016 3.2 3.0 1.3 3.6 - 4.0 3.0 -0.4 19.7 -4.6 99.5 1.72017 2.3 2.1 1.4 2.9 - 2.6 2.1 1.7 18.3 -3.8 99.9 1.5

Finland 2015 0.2 1.5 0.4 0.7 - -0.2 1.9 -0.2 9.4 -2.7 62.6 -0.42016 0.8 1.5 0.0 3.5 - 0.5 1.0 0.4 8.9 -2.4 65.0 -0.52017 1.0 0.7 -0.5 3.0 - 2.5 2.0 1.0 8.6 -2.4 67.0 0.0

Macro forecast, Global

USA 2015 2.6 3.2 1.8 4.0 0.2 0.1 4.6 0.1 5.3 -2.6 105 -2.72016 1.6 2.6 0.8 0.4 -0.4 0.7 0.7 1.3 4.9 -2.9 105 -2.92017 2.2 2.2 0.6 2.8 0.1 3.2 2.3 2.4 4.7 -2.8 103 -3.3

China 2015 6.8 - - - - - - 1.7 4.2 -0.8 41.8 2.42016 6.7 - - - - - - 2.3 4.2 -0.8 42.8 2.32017 6.6 - - - - - - 2.0 4.3 -1.0 43.5 2.5

UK 2015 2.2 2.6 1.4 3.3 0.3 4.8 5.8 0.0 5.4 -5.0 87.4 -5.22016 1.8 2.6 0.9 0.2 0.3 2.4 3.3 0.6 5.0 -3.9 88.9 -5.52017 0.7 1.4 0.0 -0.7 0.0 2.7 2.5 2.3 5.2 -2.9 88.3 -5.2

Year GDP 1

Private

cons.1

Public

cons.1

Fixed

inv.1

Stock

build.2

Current

acc.4

Im-

ports1

Public

debt4

Public

budget4

Ex-

ports1

Infla-

tion1

Unem-

ploym.3

Ex-

ports1

Im-

ports1

Infla-

tion1

Unem-

ploym.3

Public

budget4

Current

acc.4

Public

debt4

Unem-

ploym.3

Public

budget4

Public

debt4

Year

Year GDP 1

Private

cons.1

Public

cons.1

Fixed

inv.1

Stock

build.2

Current

acc.4

GDP 1

Private

cons.1

Public

cons.1

Fixed

inv.1

Stock

build.2

Ex-

ports1

Im-

ports1

Infla-

tion1

11 | 9 December 2016 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Financial forecast

Source: Danske Bank Markets

Bond and money markets

Currencyvs USD

Currencyvs DKK

USD 09-Dec - 700.6

+3m - 715.6

+6m - 689.1+12m - 664.5

EUR 09-Dec 106.2 743.8

+3m 104.0 744.3

+6m 108.0 744.3+12m 112.0 744.3

JPY 09-Dec 114.4 6.12

+3m 115.0 6.22

+6m 115.0 5.99+12m 115.0 5.78

GBP 09-Dec 126.0 882.7

+3m 118.2 845.7

+6m 120.0 826.9+12m 124.4 826.9

CHF 09-Dec 101.6 689.3

+3m 102.9 695.6

+6m 101.9 676.6+12m 100.9 658.6

DKK 09-Dec 700.6 -

+3m 715.6 -

+6m 689.1 -+12m 664.5 -

SEK 09-Dec 914.2 76.6

+3m 932.7 76.7

+6m 870.4 79.2+12m 830.4 80.0

NOK 09-Dec 845.8 82.8

+3m 884.6 80.9

+6m 833.3 82.7+12m 785.7 84.6

Equity Markets

Regional

Price trend12 mth

Regional recommen-dations

USA (USD) Growth boost: fisc. expansion, tax cuts, infl./growth-impulse 10-15% Overweight

Emerging markets (local ccy) Hurt by stronger USD and increased protectionism -5-+5% Underweight

Japan (JPY) Valuation and currency support 10-15% Overweight

Euro area (EUR) Weaker growth and EPS momentum than USA 0-5% Underweight

UK (GBP) Currency support, stronger infl. exp. o ff-set Brexit negativity 5-10% NeutralNordics (local ccy) Currency support on earnings, continued domestis demand 5-10% Neutral

Commodities

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2017 2018

NYMEX WTI 53 55 57 59 60 60 61 61 56 61

ICE Brent 53 55 57 59 60 60 61 61 56 61

Copper 5,850 5,900 5,950 6,000 6,025 6,050 6,075 6,100 5,925 6,063

Zinc 2,400 2,300 2,200 2,200 2,225 2,250 2,275 2,300 2,275 2,263

Nickel 11,200 11,300 11,400 11,500 11,600 11,700 11,800 11,900 11,350 11,750

Aluminium 1,750 1,760 1,770 1,780 1,790 1,800 1,810 1,820 1,765 1,805

Gold 1,100 1,120 1,140 1,160 1,170 1,180 1,190 1,200 1,130 1,185

Matif Mill Wheat (€/t) 164 166 168 168 169 169 170 170 167 170

Rapeseed (€/t) 420 410 410 410 415 420 425 430 413 423

CBOT Wheat (USd/bushel) 450 475 500 510 520 530 540 550 484 535CBOT Soybeans (USd/bushel) 1,150 1,100 1,100 1,100 1,125 1,125 1,150 1,150 1,113 1,138

Average

0.95

-0.32

-0.06

0.38

409

-0.65

-0.74

-

--

-0.17

-0.17

-0.17

1.08

1.241.50

-0.30

-0.30

-

-

Key int.rate

0.50

0.75

0.751.00

0.50

-0.75

0.00

0.00

-0.10-0.10

0.25

0.50

-0.60

0.25

-0.60-0.60

0.00

0.25

-

-0.65

10-yr swap yield

-0.62

0.05

0.050.05

3m interest rate

0.90

0.00

-0.10

0.25

-0.75

0.05

-0.30

0.40

0.400.40

0.50

0.50

1.00

-0.75-0.75

-0.50

-0.10

-0.19

1.551.85

0.55

0.550.60

-

-

1.30

-0.40

-

1.20

0.00

0.100.20

-

--

-0.42

-0.45

1.40

-0.45

1.311.14

0.90

-0.65

106.2

-

-

--

121.5

744.3

744.3744.3

970.6

898.0

880.0

970.0

900.0

940.0930.0

920.0

107.9

743.8

88.0

90.0

107.0

110.0113.0

104.0

108.0112.0

119.6

124.2128.8

Currencyvs EUR

2-yr swap yield

Risk profile3 mth

Price trend3 mth

2.40

2.28

2.60

1.35

-0.16

0.03

0.64

-0.62

0.05

-0.20

-0.100.00

1.35

84.3

2.90

90.0

1,171

162

54

1,724

2017

09-Dec

51

11,105

5,782

2,689

0.75

0.951.35

-

--

1.36

1.40

0.24

1,028391

0.76

1.201.40

2.03

1.80

2.00

1.501.75

0.20

-

--

2.30

1.201.60

1.05

1.16

1.20

1.04

2018

Medium

Medium

Medium 5 -10%

Medium 5 -10%

-5 -0%

0 -5%

Medium 3-8%Medium 3 -8%

12 | 9 December 2016 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

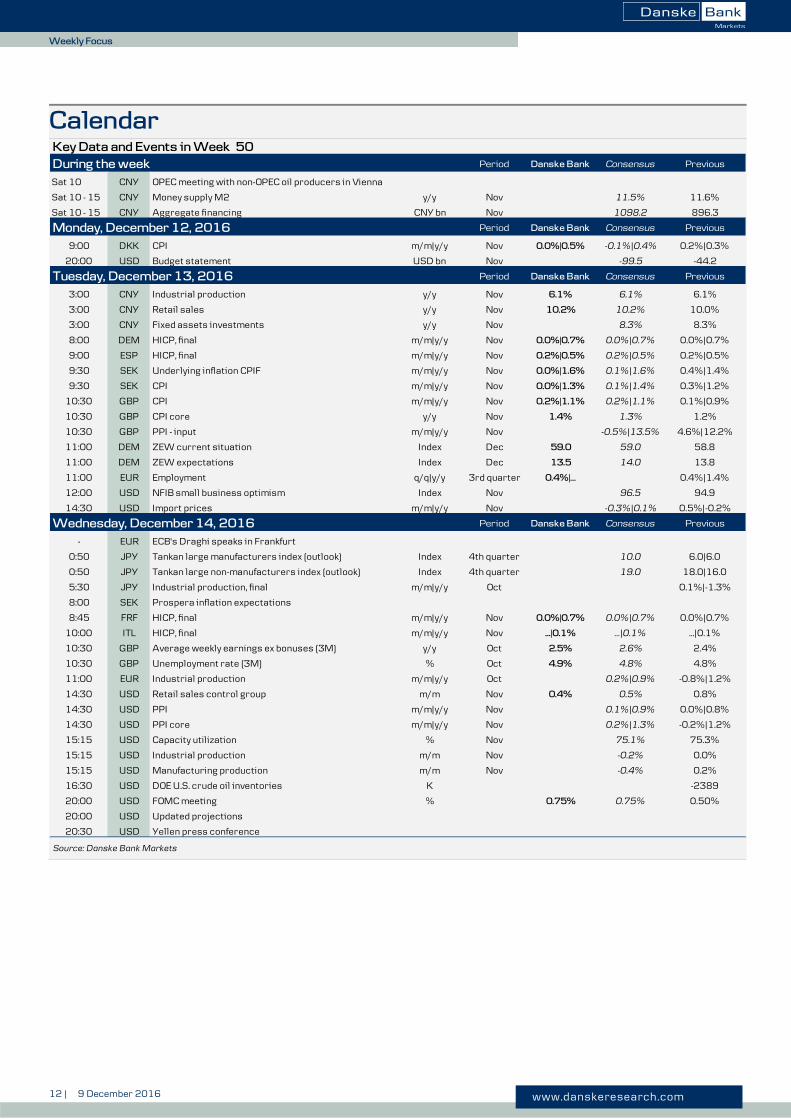

Calendar

Source: Danske Bank Markets

Key Data and Events in Week 50

During the week Period Danske Bank Consensus Previous

Sat 10 CNY OPEC meeting with non-OPEC oil producers in Vienna

Sat 10 - 15 CNY Money supply M2 y/y Nov 11.5% 11.6%

Sat 10 - 15 CNY Aggregate financing CNY bn Nov 1098.2 896.3

Monday, December 12, 2016 Period Danske Bank Consensus Previous

9:00 DKK CPI m/m|y/y Nov 0.0%|0.5% -0.1%|0.4% 0.2%|0.3%

20:00 USD Budget statement USD bn Nov -99.5 -44.2

Tuesday, December 13, 2016 Period Danske Bank Consensus Previous

3:00 CNY Industrial production y/y Nov 6.1% 6.1% 6.1%

3:00 CNY Retail sales y/y Nov 10.2% 10.2% 10.0%

3:00 CNY Fixed assets investments y/y Nov 8.3% 8.3%

8:00 DEM HICP, final m/m|y/y Nov 0.0%|0.7% 0.0%|0.7% 0.0%|0.7%

9:00 ESP HICP, final m/m|y/y Nov 0.2%|0.5% 0.2%|0.5% 0.2%|0.5%

9:30 SEK Underlying inflation CPIF m/m|y/y Nov 0.0%|1.6% 0.1%|1.6% 0.4%|1.4%

9:30 SEK CPI m/m|y/y Nov 0.0%|1.3% 0.1%|1.4% 0.3%|1.2%

10:30 GBP CPI m/m|y/y Nov 0.2%|1.1% 0.2%|1.1% 0.1%|0.9%

10:30 GBP CPI core y/y Nov 1.4% 1.3% 1.2%

10:30 GBP PPI - input m/m|y/y Nov -0.5%|13.5% 4.6%|12.2%

11:00 DEM ZEW current situation Index Dec 59.0 59.0 58.8

11:00 DEM ZEW expectations Index Dec 13.5 14.0 13.8

11:00 EUR Employment q/q|y/y 3rd quarter 0.4%|… 0.4%|1.4%

12:00 USD NFIB small business optimism Index Nov 96.5 94.9

14:30 USD Import prices m/m|y/y Nov -0.3%|0.1% 0.5%|-0.2%

Wednesday, December 14, 2016 Period Danske Bank Consensus Previous

- EUR ECB's Draghi speaks in Frankfurt

0:50 JPY Tankan large manufacturers index (outlook) Index 4th quarter 10.0 6.0|6.0

0:50 JPY Tankan large non-manufacturers index (outlook) Index 4th quarter 19.0 18.0|16.0

5:30 JPY Industrial production, final m/m|y/y Oct 0.1%|-1.3%

8:00 SEK Prospera inflation expectations

8:45 FRF HICP, final m/m|y/y Nov 0.0%|0.7% 0.0%|0.7% 0.0%|0.7%

10:00 ITL HICP, final m/m|y/y Nov ...|0.1% …|0.1% ...|0.1%

10:30 GBP Average weekly earnings ex bonuses (3M) y/y Oct 2.5% 2.6% 2.4%

10:30 GBP Unemployment rate (3M) % Oct 4.9% 4.8% 4.8%

11:00 EUR Industrial production m/m|y/y Oct 0.2%|0.9% -0.8%|1.2%

14:30 USD Retail sales control group m/m Nov 0.4% 0.5% 0.8%

14:30 USD PPI m/m|y/y Nov 0.1%|0.9% 0.0%|0.8%

14:30 USD PPI core m/m|y/y Nov 0.2%|1.3% -0.2%|1.2%

15:15 USD Capacity utilization % Nov 75.1% 75.3%

15:15 USD Industrial production m/m Nov -0.2% 0.0%

15:15 USD Manufacturing production m/m Nov -0.4% 0.2%

16:30 USD DOE U.S. crude oil inventories K -2389

20:00 USD FOMC meeting % 0.75% 0.75% 0.50%

20:00 USD Updated projections

20:30 USD Yellen press conference

13 | 9 December 2016 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Calendar — continued

Source: Danske Bank Markets

Thursday, December 15, 2016 Period Danske Bank Consensus Previous

- EUR EU summit in Brussels

1:30 AUD Employment change 1000 Nov 17.5 10.9

1:30 JPY Nikkei Manufacturing PMI, preliminary Index Dec 51.3

8:00 NOK Trade balance NOK bn Nov 10.4

9:00 FRF PMI manufacturing, preliminary Index Dec 51.5 51.9 51.7

9:00 FRF PMI services, preliminary Index Dec 51.7 51.6

9:30 CHF SNB 3-month Libor target rate % -0.75% -0.75% -0.75%

9:30 SEK Unemployment (n.s.a.|s.a.|trend) % Nov 6.1%|6.7%|6.8% 6.4%|6.9%|… 6.4%|6.9%|6.8%

9:30 DEM PMI manufacturing, preliminary Index Dec 54.0 54.5 54.3

9:30 DEM PMI services, preliminary Index Dec 55.2 54.8 55.1

10:00 EUR PMI manufacturing, preliminary Index Dec 53.5 53.7 53.7

10:00 EUR PMI composite, preliminary Index Dec 53.8 53.9

10:00 EUR PMI services, preliminary Index Dec 54.0 53.7 53.8

10:00 NOK Norges Banks monetary policy meeting % 0.50% 0.50% 0.50%

10:30 GBP Retail sales ex fuels m/m|y/y Nov 0.0%|6.0% 2.0%|7.6%

13:00 GBP BoE minutes

13:00 GBP BoE government bond purchases (APF) GBP bn Dec 435 435 435

13:00 GBP BoE coporate bond purchases (CBPP) GBP bn Dec 10 10 10

13:00 GBP BoE Bank rate % 0.25% 0.25% 0.25%

14:30 USD CPI headline m/m|y/y Nov 0.2%|1.7% 0.2%|1.7% 0.4%|1.6%

14:30 USD CPI core m/m|y/y Nov 0.2%|2.2% 0.2%|2.2% 0.1%|2.2%

14:30 USD Current account USD bn 3rd quarter -111.0 -119.9

14:30 USD Initial jobless claims 1000 258

14:30 USD Philly Fed index Index Dec 9.0 7.6

14:30 USD Empire Manufacturing PMI Index Dec 2.6 1.5

15:45 USD Markit PMI manufacturing, preliminary Index Dec 54.5 54.1

16:00 USD NAHB Housing Market Index Index Dec 63.0 63.0

22:00 USD TICS international capital flow, Net inflow USD bn Oct -152.9

Friday, December 16, 2016 Period Danske Bank Consensus Previous

- EUR S&P may publish Germany's debt rating

8:45 FRF Business confidence Index Dec 102.0 102.0

9:00 DKK House prices (Association of Danish Mortgage Banks) q/q|y/y 3rd quarter

11:00 EUR HICP inflation m/m|y/y Nov ...|0.6% -0.1%|0.6% ...|0.5%

11:00 EUR HICP - core inflation, final y/y Nov 0.8% 0.8% 0.8%

11:00 EUR Trade balance EUR bn Oct 25.0 24.9

11:00 EUR Labour costs y/y 3rd quarter 1.0%

11:30 RUB Central Bank of Russia rate decision % 10.0% 10.0% 10.0%

14:30 USD Building permits 1000 (m/m) Nov 1243 1260.0 (2.9%)

14:30 USD Housing starts 1000 (m/m) Nov 1230 1323.0 (25.5%)

18:30 USD Fed's Lacker (non-voter, hawkish) speaks

The editors do not guarantee the accurateness of figures, hours or dates stated above

For furher information, call (+45 ) 45 12 85 22.

14 | 9 December 2016 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Disclosures This research report has been prepared by Danske Bank Markets, a division of Danske Bank A/S (‘Danske Bank’).

The author of the research report is Louise Aggerstrøm Hansen, Senior Analyst.

Analyst certification

Each research analyst responsible for the content of this research report certifies that the views expressed in the

research report accurately reflect the research analyst’s personal view about the financial instruments and issuers

covered by the research report. Each responsible research analyst further certifies that no part of the compensation

of the research analyst was, is or will be, directly or indirectly, related to the specific recommendations expressed

in the research report.

Regulation

Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject

to the rules and regulation of the relevant regulators in all other jurisdictions where it conducts business. Danske

Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority

(UK). Details on the extent of the regulation by the Financial Conduct Authority and the Prudential Regulation

Authority are available from Danske Bank on request.

The research reports of Danske Bank are prepared in accordance with the recommendations of the Danish Securities

Dealers Association.

Conflicts of interest

Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high-quality

research based on research objectivity and independence. These procedures are documented in Danske Bank’s

research policies. Employees within Danske Bank’s Research Departments have been instructed that any request

that might impair the objectivity and independence of research shall be referred to Research Management and the

Compliance Department. Danske Bank’s Research Departments are organised independently from and do not report

to other business areas within Danske Bank.

Research analysts are remunerated in part based on the overall profitability of Danske Bank, which includes

investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate finance

or debt capital transactions.

Financial models and/or methodology used in this research report

Calculations and presentations in this research report are based on standard econometric tools and methodology as

well as publicly available statistics for each individual security, issuer and/or country. Documentation can be

obtained from the authors on request.

Risk warning

Major risks connected with recommendations or opinions in this research report, including a sensitivity analysis of

relevant assumptions, are stated throughout the text.

Expected updates

None.

Date of first publication

See the front page of this research report for the date of first publication.

General disclaimer This research has been prepared by Danske Bank Markets (a division of Danske Bank A/S). It is provided for

informational purposes only. It does not constitute or form part of, and shall under no circumstances be considered

as, an offer to sell or a solicitation of an offer to purchase or sell any relevant financial instruments (i.e. financial

instruments mentioned herein or other financial instruments of any issuer mentioned herein and/or options,

warrants, rights or other interests with respect to any such financial instruments) (‘Relevant Financial Instruments’).

The research report has been prepared independently and solely on the basis of publicly available information that

Danske Bank considers to be reliable. While reasonable care has been taken to ensure that its contents are not untrue

or misleading, no representation is made as to its accuracy or completeness and Danske Bank, its affiliates and

subsidiaries accept no liability whatsoever for any direct or consequential loss, including without limitation any

loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts responsible for the research report and

reflect their judgement as of the date hereof. These opinions are subject to change, and Danske Bank does not

undertake to notify any recipient of this research report of any such change nor of any other changes related to the

information provided in this research report.

This research report is not intended for, and may not be redistributed to, retail customers in the United Kingdom or

the United States.

This research report is protected by copyright and is intended solely for the designated addressee. It may not be

reproduced or distributed, in whole or in part, by any recipient for any purpose without Danske Bank’s prior written

consent.

15 | 9 December 2016 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Disclaimer related to distribution in the United States This research report was created by Danske Bank A/S and is distributed in the United States by Danske Markets

Inc., a U.S. registered broker-dealer and subsidiary of Danske Bank A/S, pursuant to SEC Rule 15a-6 and related

interpretations issued by the U.S. Securities and Exchange Commission. The research report is intended for

distribution in the United States solely to ‘U.S. institutional investors’ as defined in SEC Rule 15a-6. Danske

Markets Inc. accepts responsibility for this research report in connection with distribution in the United States solely

to ‘U.S. institutional investors’.

Danske Bank is not subject to U.S. rules with regard to the preparation of research reports and the independence of

research analysts. In addition, the research analysts of Danske Bank who have prepared this research report are not

registered or qualified as research analysts with the NYSE or FINRA but satisfy the applicable requirements of a

non-U.S. jurisdiction.

Any U.S. investor recipient of this research report who wishes to purchase or sell any Relevant Financial Instrument

may do so only by contacting Danske Markets Inc. directly and should be aware that investing in non-U.S. financial

instruments may entail certain risks. Financial instruments of non-U.S. issuers may not be registered with the U.S.

Securities and Exchange Commission and may not be subject to the reporting and auditing standards of the U.S.

Securities and Exchange Commission.