investment recommendation report closing date: august 2, 2011 ic memo... · investment...

TRANSCRIPT

1

THE STERLING GROUP, L.P.

Powertrain

Investment Recommendation Report

Closing date: August 2, 2011

2

TABLE OF CONTENTS

I. Transaction Summary ................................................................................... 3

II. Company ......................................................................................................... 4

III. Industry Overview .......................................................................................18

IV. Historical Financials ....................................................................................21

V. Standalone Cost Analysis ............................................................................23

VI. Management .................................................................................................24

VII. Attractiveness and Opportunities of Investment ......................................26

VIII. Issues and Risks of Investment ...................................................................29

IX. Post-Closing Initiatives ................................................................................35

X. Transaction ...................................................................................................37

XI. Projections and Returns ..............................................................................38

XII. Recommendation .........................................................................................47

XIII. Appendix .......................................................................................................48

3

I. Transaction Summary

On August 2, 2011, Sterling completed the acquisition of Powertrain (“Powertrain” or the

“Company”), a leading supplier of engine and transmission oil pumps and powdered metal

components to major automotive original equipment manufacturers. The entities constituting

Powertrain are principally owned by Gates Corporation (“Gates”), a wholly owned subsidiary of

Tomkins Ltd (“Tomkins”), and a leading manufacturer of industrial and automotive products,

systems and components. Gates is exiting the business as Powertrain falls outside of Gates’

focus on aftermarket belts, hoses and hydraulics. RBC and UBS jointly represented Tomkins

and Gates on the sale.

Powertrain designs, manufactures and sells oil pumps and powdered metal components used in

engines and transmissions ultimately used in approximately 400 nameplate vehicle platforms.

Headquartered in Ancaster, Ontario, the Company serves its North American customers from

five manufacturing facilities in Ontario, Canada. Additionally, the Company has a technical

center in Aachen, Germany and recently started manufacturing operations in Izmir, Turkey to

serve the European pump market. Through a 30% interest in a JV with Halla Corporation, a

Korean conglomerate, the Company serves the Asian powered metal components market.

Powertrain is in the process of expanding its technical center in Changzhou, China to include

manufacturing to support recently awarded pump business in China. During the trailing twelve

month period ending 5/31/2011, Powertrain generated sales and adjusted EBITDA of $285.8

million and $50.3 million, respectively. Based on management volume forecast (in aggregate, an

approximate 10% discount to CSM volume forecasts), the Company has more than $2.0 billion

in “booked” sales between 2011 and 2015, representing 98% of projected sales over the period.

We conducted considerable due diligence on the Company, including detailed platform level

reviews (customer, competitors, volumes, margins), numerous calls with management, a number

of in-person sessions with management in Toronto, primary diligence calls and meetings with

industry experts arranged through Kingfish and Jon Foster at Current Capital and calls with all

major customers and suppliers. Mr. Foster is a director for Lear Corporation, a global

automotive components manufacturer and Mr. Foster will join Sterling on the board of

Powertrain. Given our exposure to management, we have had a fair chance to evaluate

management and have concluded that the Powertrain management team is professional, quite

sophisticated, detail oriented and results driven. The management team currently has no equity

in Powertrain; we believe that, with appropriate incentives, they would be even more value

creation oriented.

The Powertrain opportunity is attractive for a number of reasons, including: (i) North American

market leader; (ii) substantial revenue visibility; (iii) significant barriers to entry; (iv) strong

management team; (v) significant international growth opportunities; (iv) limited auction with

complexities; and (v) clear opportunity for Sterling value creation. The main risks to this

investment include: (i) Customer concentration; (ii) volume volatility in automotive market; (iii)

high capital expenditure requirements; (iv) raw material variability; (v) Exposure to $CAD/USD

exchange rate; and (vi) technology exposure.

4

We originally submitted an indication of interest on March 4, 2011 of $300 - $320 million,

implying a transaction multiple of 6.5x to 6.9x LTM EBITDA (as of 12/31/10) of $46.3 million,

assuming the CIM forecast included appropriate standalone costs. Through 5/31/11, LTM

Adjusted EBITDA had increased to $50.3. We acquired Powertrain for $290.7 million ($285

million cash + $5.7 million of assumed pension liabilities) or 5.8x 5/31/11 LTM Adjusted

EBITDA / 7.2x 5/31/11 LTM Adjusted EBITDA less an assumed $10.0 million annual

maintenance and replacement CapEx. Pro forma for the NPV of tax benefits associated with the

tax basis step-up of approximately $23 million, the purchase price is equivalent to $267.7

million, or 5.3x LTM Adjusted EBITDA. Total equity for the transaction was $117 million, with

Fund III investing approximately $107 million at close and the balance coming from co-

investors.

II. Company

Overview

Gates Corporation’s Powertrain division (“Powertrain” or the “Company”), headquartered in

Ancaster, Ontario, is a leading supplier of engine and transmission oil pumps and powdered

metal (“PM”) components for automotive powertrains to original equipment (“OEM”)

manufacturers. With eight manufacturing facilities in North America, Europe, China and Korea,

the company serves its core markets and customers with regional and/or local manufacturing,

design, development, and customer service capabilities. Powertrain’s OEM customers rely on the

Company’s ability to design and produce highly durable components for their most important

and widely marketed platforms. The Company’s products are specified into specific powertrain

(engine and transmission) platforms that have an average life of 10 – 15 years with some lasting

as long as 20 years. Currently the Company provides products to 20 such platforms. In turn,

each platform is used across multiple vehicle platforms, resulting in exposure to 400+ nameplate

vehicles.

Powertrain is a market leader in both of its two distinct product segments: oil pumps and PM

components.

Oil Pumps – Representing 51% of Powertrain’s 2010 revenue, these are fixed and variable

displacement oil pumps used in engines and transmissions. The Company is one of the top three

non-captive (70% of the market) automotive oil pump producers in the world. The Company

pioneered the development of variable vane oil pump technology and is the largest variable

displacement pump producer in the world with 21 million installed units. This variable vane oil

pump technology is proven to improve an automobile’s fuel efficiency by 1–2% over fixed

displacement technology and is expected by management to be a driver of future sales growth.

PM Parts – Representing 49% of Powertrain’s 2010 revenue, these are complex fabricated

components, gears, sprockets, assemblies and pump components. The Company is the second

largest automotive PM producer in North America.

5

Overview of Platform Lifecycle

The lifecycle for engine and transmission platforms can range between ten and twenty years,

depending on the specific platform. This lifecycle is substantially longer than for interior

components and systems, which have lifecycles of less than five years. The engine and

transmission platform lifecycle begins with a design phase, followed by the selection of one or

more suppliers (for pumps), initial capital expenditure outlays by the supplier, ramp up, peak

revenues, declining revenues and the end of the platform. The following table outlines the

lifecycle stages for a typical powertrain platform:

Platform Lifecycle Analysis

Year Stage

Year 1 Initial Discussions

Year 2 Prototype Design and Supplier Selection

Year 3 Specification Process and Initial CapEx

Year 4 Initial Ramp; Revenue = X

Year 5 Ramp; Revenue = 2X

Year 6 Ramp; Revenue = 3X

Year 7 Peak Revenue; Revenue = 4X

Year 8 Peak Revenue; Revenue = 4X

Year 9 Peak Revenue; Revenue = 4X

Year 10 Peak Revenue; Revenue = 4X

Year 11 Peak Revenue; Revenue = 4X

Year 12 Decline; Revenue = 3X

Year 13 Decline; Revenue = 2X

Year 14 Decline; Revenue = X

Year 15 End of Program

Powertrain will typically begin discussions for the next generation of a given platform three to

five years before the end of the current generation. Powertrain is well-positioned to win the next

generation of business with existing customers due to the track record and relationships that are

built during the long lifecycle of the existing platforms.

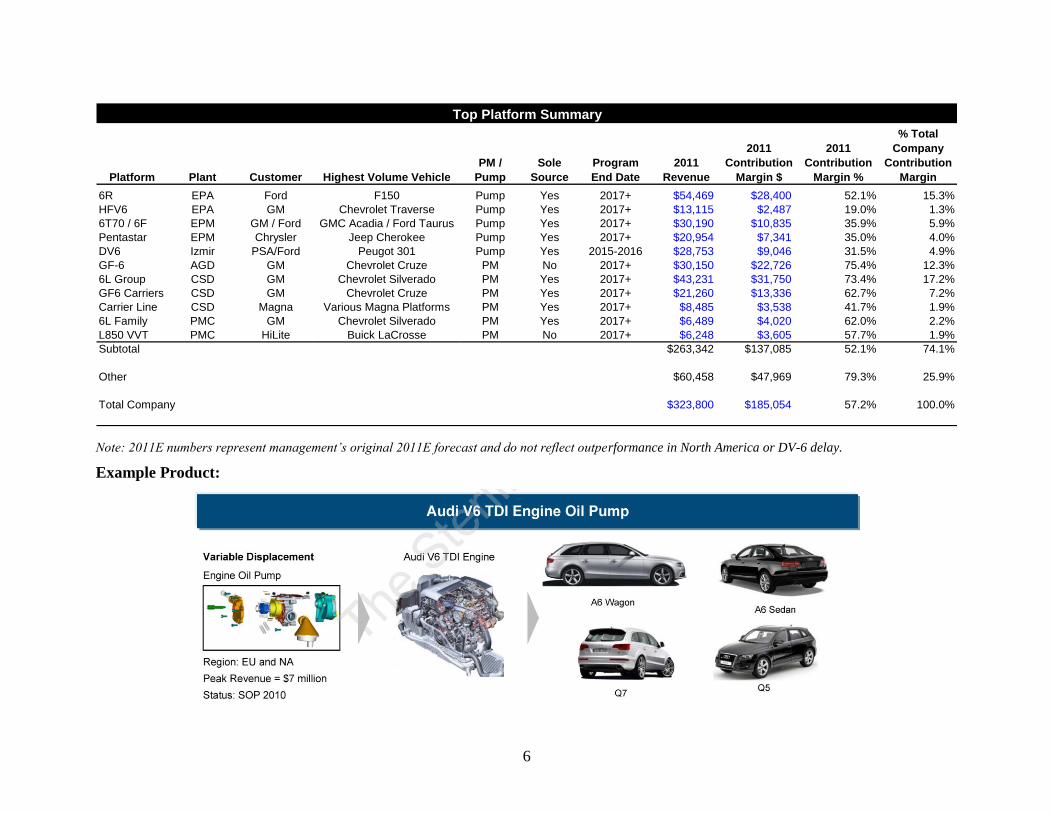

Products

Powertrain’s product portfolio consists of oil pumps and powdered metal products that are sold

into a variety of platforms and then vehicles for OEM’s. The following table summarizes the

Company’s key platforms:

6

Top Platform Summary

Platform Plant Customer Highest Volume Vehicle

PM /

Pump

Sole

Source

Program

End Date

2011

Revenue

2011

Contribution

Margin $

2011

Contribution

Margin %

% Total

Company

Contribution

Margin

6R EPA Ford F150 Pump Yes 2017+ $54,469 $28,400 52.1% 15.3%

HFV6 EPA GM Chevrolet Traverse Pump Yes 2017+ $13,115 $2,487 19.0% 1.3%

6T70 / 6F EPM GM / Ford GMC Acadia / Ford Taurus Pump Yes 2017+ $30,190 $10,835 35.9% 5.9%

Pentastar EPM Chrysler Jeep Cherokee Pump Yes 2017+ $20,954 $7,341 35.0% 4.0%

DV6 Izmir PSA/Ford Peugot 301 Pump Yes 2015-2016 $28,753 $9,046 31.5% 4.9%

GF-6 AGD GM Chevrolet Cruze PM No 2017+ $30,150 $22,726 75.4% 12.3%

6L Group CSD GM Chevrolet Silverado PM Yes 2017+ $43,231 $31,750 73.4% 17.2%

GF6 Carriers CSD GM Chevrolet Cruze PM Yes 2017+ $21,260 $13,336 62.7% 7.2%

Carrier Line CSD Magna Various Magna Platforms PM Yes 2017+ $8,485 $3,538 41.7% 1.9%

6L Family PMC GM Chevrolet Silverado PM Yes 2017+ $6,489 $4,020 62.0% 2.2%

L850 VVT PMC HiLite Buick LaCrosse PM No 2017+ $6,248 $3,605 57.7% 1.9%

Subtotal $263,342 $137,085 52.1% 74.1%

Other $60,458 $47,969 79.3% 25.9%

Total Company $323,800 $185,054 57.2% 100.0%

Note: 2011E numbers represent management’s original 2011E forecast and do not reflect outperformance in North America or DV-6 delay.

Example Product:

7

Oil Pumps (51% of 2010 net sales)

Overview

The Company’s oil pump products are an important component in the operation of automotive

engines and transmissions, ensuring that there is adequate lubrication within these systems

throughout all ranges of the drive cycle. The Company designs and manufactures transmission

and engine oil pumps based on the engineering requirements of the original equipment

manufacturers. The Company has shipped more than 21 million variable displacement oil pumps

globally and currently produces 17,000 fixed and variable oil pumps per day in North America,

making it one of the largest non-captive oil pump producers in the region and one of the top three

players in the world.

Product Differentiation

Powertrain developed the industry’s first variable vane displacement oil pump. While fixed

displacement pumps provide capacity in direct proportion to engine speed and tend to

overproduce at higher engine speeds, variable displacement pumps adjust output flow according

to actual needs. This technology costs approximately $20 more per pump than a traditional fixed

displacement pump, but improves fuel efficiency by 1-2%. OEM’s have historically paid $60+

for similar improvements in fuel efficiency, implying that the value-proposition for variable vane

displacement pumps is very attractive. Currently, variable vane displacement pumps represent

just 12% of the North American pump market, but are expected to reach 45% of the North

American pump market by 2015, according to CSM and management estimates. The relatively

low variable vane penetration today reflects the long platform lifecycles of existing fixed

displacement technology. The following chart shows the expected increase in variable vane

penetration in North America:

Projected Variable Vane Penetration

North America

12.0%

45.0%

88.0%

55.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

2011 2015

Variable Vane Fixed Displacement

Source: CSM and management estimates.

8

Top Three Oil Pump Platforms

Powertrain’s three largest oil pump platforms are the 6R, the 6T70-6F and the DV-6:

6R Platform: The 6R platform represents a large, highly complex oil pump sold to Ford.

Management projects units for the 6R to reach 800K units by 2015 versus 570K units in

2011 (reflecting a discount to CSM projections). The Ford F150 truck, the world’s most

popular light truck, is expected to represent 500K of these units. Due to the complex

nature of the pump, the 6R receives a premium price of $95 per pump versus prices of

$30 and below for other pumps. This program is expected to continue beyond 2017.

Powertrain is the sole supplier.

6T70-6F Platform: The 6T70-6F platform represents an oil pump that is sold both to

GM and Ford. The 6T70 is sold to GM, with key vehicles including the Buick LaCrosse,

the Cadillac SRX and the GMC Acadia. The 6F is sold to Ford, with key vehicles

including the Ford Edge, the Ford Explorer and the Ford Taurus. The average selling

price for the 6T70-6F is $30. This platform has reached its peak volume and is projected

to remain at approximately 1,000,000 units per year during the projection period. This

program is expected to continue beyond 2017. It is unusual to be on a platform that

serves two major OEM’s, but this is indicative of Powertrain’s important presence in the

market. Powertrain is the sole supplier.

DV-6 Platform: The DV-6 represents an oil pump platform sold to both PSA and Ford

from the Izmir facility based in Turkey. Units for 2011 originally projected by

management to be 1.25 million. This program is expected to end in 2015/2016, when

volumes will decline from 1.2 million units in 2014 to 500K units in 2015 and then zero

units in 2016. Powertrain is the sole supplier.

9

Powdered Metals (49% of 2010 net sales)

Overview

Powertrain has been a leader in the North American powdered metal manufacturing industry for

more than fifty years. The Company has strong engineering and manufacturing capabilities and

is recognized by its customers as a high-quality, high service-level supplier of powdered metal

components.

Powertrain specializes in products that are used primarily in transfer cases, automatic and manual

transmissions, and engines. These include:

Gears and sprockets

Synchronizer Assemblies

Planetary Carriers

Clutch Components

Pump Components

Engine Components

Product Differentiation

Powertrain services all of the major North American automotive original equipment

manufacturers and has been supplying powdered metal components for more than 50 years.

Industry experts refer to this form of metallurgy as a “black art” and it is our understanding that

competitors have had trouble replicating Powertrain’s capabilities. Advantages of Powertrain’s

powdered metals include:

Superior tensile strength

10% reduction in weight vs. cast/wrought iron parts

20-30% reduction in material wastage

Top Three Powdered Metal Platforms

The three largest powdered metal platforms are the 6L Group / 6L Family, the GF-6 and the GF-

6 Carriers:

10

6L Group / 6L Family: The OEM’s are increasingly outsourcing components and

systems that are not directly related to vehicle design. Powertrain currently manufactures

powdered metals for approximately 1/3 of all GM’s North American vehicle production

through the 6L Group / 6L Family. The only difference between the 6L Group and 6L

Family is that the 6L Group powdered metals are produced at the CSD plant and the 6L

Family powdered metals are produced at the PMC plant. These two platforms are

generally going into the same GM vehicles, which include the Chevrolet Silverado, the

GMC Sierra and the Chevrolet Tahoe. These platforms are expected to continue beyond

2017+. Management expects 2011 units to total 4.1 million units for the 6L Group and

Family combined, ramping to 4.7 million units by 2015.

GF-6: The GF-6 represents an automotive sprocket sold to GM. Powertrain shut down

the automotive gear division in 2009 because the per unit price of $13 for the GF-6 was

not economical at the AGD plant. However, GM then asked Powertrain to reopen the

AGD plant in 2010 to produce the GF-6. A higher price of $22 per unit was contracted

such that the GF-6 would be profitable even while covering 100% of AGD’s overhead.

AGD currently runs at about 25% utilization (to be filled with future volumes). While

Powertrain is currently handling nearly 100% of GM’s GF-6 sprocket needs, there is

currently another supplier ramping up that will share this volume starting in 2013 / 2014.

There are other opportunities being addressed to add utilization to AGD. This program is

expected to continue beyond 2017+. Management expects 2011 units to total 1.3 million

units and remain at this level throughout this projection periods.

GF-6 Carriers: Powertrain has been producing the GF-6 Carriers in the CSD plant since

before 2008. While the GF-6 sprocket is dual-sourced, the GF-6 carriers are sole-sourced

by GM through Powertrain. The GF-6 Carriers are sold into the same vehicles as the GF-

6 sprockets – each respective vehicle uses one sprocket and two carriers. The largest

volume vehicles for the GF-6 (both sprockets and carriers) are the Chevrolet Cruze, the

Chevrolet Malibu and the Chevrolet Equinox. This program is expected to continue

beyond 2017+. Management expects 2011 units to total 1.6 million units, ramping to 2.8

million units by 2015.

Pricing

For the majority of Powertrain’s platforms, the selling price per unit is locked in with the

customer for three to five years. The contracts generally start with a higher initial price that then

decreases by 3% per year, typically for the first three years, to account for the ramping volumes.

Given the interdependency between Powertrain and its customers, it is our understanding that

there is limited pricing pressure once the initial contract has been negotiated and the program has

begun. However, the pricing negotiations resume when Powertrain attempts to win the next

generation of the platform.

Facility Overview

The majority of Powertrain’s facilities and operations are based in Ontario, Canada. While

Canada has higher labor costs than Asia, the Company’s manufacturing footprint does not

provide a significant competitive disadvantage due to the highly automated nature of its

manufacturing operations and customer’s preference to source from regional suppliers. During

11

the site visit, it was clear that the facilities are relatively new and very well-organized and

maintained. Management is comfortable that the existing facilities will be able to accommodate

future growth in North America. Capacity utilization across the oil pump facilities is

approximately 80% and capacity utilization across the powdered metal facilities is approximately

70%. The following chart provides an overview of Powertrain’s facilities:

Facilities Overview

Owned / No. of 2011E Plant % of

Location Division Product Sq. Ft. Leased Employees EBITDA Total(1)

Stratford, Ontario Carrier Systems ("CSD") PM 210,000 Owned 504 $25,168 40.9%

Ancaster, Ontario PM Components ("PMC") PM 140,440 Owned 307 $6,193 10.1%

Mississauga, Ontario Automotive Gears ("AGD") PM 120,000 Owned 244 $1,511 2.5%

Mississauga, Ontario Engineered Products ("EPM") Pumps 100,000 Owned 182 $11,786 19.1%

Ancaster, Ontario Engineered Products ("EPA") Pumps 86,358 Owned 203 $14,056 22.8%

Izmir, Turkey Engineered Products Pumps 130,974 Owned 162 $3,178 5.2%

Ochang, Korea Halla Stackpole JV PM 174,650 Owned 255 $1,869 3.0%

Changzhou, China Engineered Products ("EPC") Pumps TBD TBD TBD ($2,172) (3.5%)

(1) % of Total Plant EBITDA, before corporate overhead.

Europe and Asia Strategy

Currently, the large majority of the Company’s revenue and EBITDA is generated in North

America. In 2010, the Company generated just $8 million of sales in Europe and no sales in

Asia. However, Europe and Asia will represent important sources of future growth for the

Company. The Asia automotive market is growing substantially faster than both the North

America and Europe markets. In terms of exit planning, we believe that developing a presence

in Asia would increase strategic interest in the Company as well as positively impact the exit

multiple. The following table illustrates the Company’s current geographic mix and the projected

geographic mix in 2015 based on management’s projections:

Geographic Mix 2010A-2015E

97.0%

77.0%

3.0%

15.0%

0.0% 8.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

2010A 2015E

North America Europe Asia

12

Europe Business

Over the last three years, the Company has invested more than $20 million in capital

expenditures in a new plant in Izmir, Turkey. Sterling will benefit from these large upfront

capital expenditures as the new business begins to ramp up during the ownership period. For

example, the Izmir plant includes the DV6 platform, which represented 359 units in 2010, but is

expected to reach 1,250,150 units in 2011. Of the six platforms on which the Company has

positions in Europe, three started production in 2010. Five additional platforms have been

awarded and are scheduled to begin production in 2011-2012.

Asia Business

Asia is forecasted to embrace the variable vane pump technology over the next five years and

Powertrain should be well-positioned from a technological perspective to share in this growth.

The following chart shows the projected variable vane oil pump volumes for the Asia market

from 2010 to 2015:

Projected Variable Displacement Volume in Asia

(millions of units)

1

2

4

5

7

9

0

1

2

3

4

5

6

7

8

9

10

2010A 2011E 2012E 2013E 2014E 2015E

While Powertrain currently does not generate any volume in Asia, the company has booked five

substantial platforms that, in total, are expected to reach approximately 1.5 million units by 2015.

The customers for these platforms are Chery, PSA and SGM. However, Asia is expected to

generate negative EBITDA in 2011 and 2012 and will require significant upfront capital

investment in order to reach these volumes.

13

Customers

Powertrain’s top three customers account for 78% of 2011E revenue and the top eight customers

account for 97% of 2011E revenue. However, within each “customer” are numerous platforms

and vehicles.

Powertrain Customer Concentration

Length of Key % of

Relationship Platforms 2011 Revenue

GM 35 6L, 6T70, SGE, GF6, HFV6 41%

Ford 27 6R, 6F, HF35 25%

Chrysler 22 Pentastar, 68RFE, 45RFE, 62TE 12%

Magna 10 X2T 6%

PSA Peugot Citroen 3 DV EUR5, EB 6%

Audi 5 V6, V8 (several variants) 4%

Hilite 8 L850 VVT 2%

Whirlpool 14 Components for blenders 1%

Others n/a Chery I3, I4 TDGi 3%

For the oil pump division, Ford accounts for 48% of total oil pump revenue, GM accounts for

17% of total oil pump revenue and Chrysler accounts for 15% of total oil pump revenue.

Top 5 Oil Pump Customers

% of Key

Customer Pump Revenue Platforms

Ford 47.9% 6R, 6F

GM 16.9% 6T70, HFV6

Chrysler 15.1% Pentastar

PSA Peugeot Citroen 11.0% DV6

Audi 8.1% V6i, V8

Total 99.0%

For the powdered metal division, GM accounts for 66% of PM sales, Magna accounts for 12% of

PM sales and Chrysler accounts for 8.6% of PM sales. Ford Motor Company is aligned with

other powdered metal suppliers and therefore does not use Powertrain for powdered metals.

Ford aims to maintain a diversified supplier base for its components in order to avoid supply

disruptions as well as to avoid providing one supplier with excess pricing leverage.

14

Top 5 Powdered Metal Customers

% of Key

Customer Pump Revenue Platforms

GM 65.9% 6L, GF6

Magna 12.2% X2T and Trilobe

Chrysler 8.6% Clutch plates

HiLite 3.9% L850

Whirlpool 2.6% n/a

Total 93.2%

Customer Contracts

Powertrain’s customer contracts generally last between 3-5 years and provide for contracted

pricing during the term. Given that the platform lifecycles average in excess of ten years,

Powertrain will undergo multiple contract renewal discussions with customers during the course

of the platform’s lifecycle. The Ford contracts are different than for GM and the other customers

– the contract is only one-year in length with automatic rollovers, but pricing is locked in for 3-5

years through a separate LTA agreement. Finally, it’s important to note that the contracts allow

for customers to switch platform providers if there is an issue with quality or execution.

However, historically, a switch during a platform lifecycle has never happened and would be

highly unlikely unless there was a serious quality or safety issue with the product due to

substantial time and costs of testing and qualifying a new supplier. The following table

summarizes the contract terms for our eleven major platforms:

Top Customer Contract Summary

Pass Expiration

Platform Customer Through Date Comments

6R Ford Yes LTA - 2015 Annual contract w/ rollover. Program extends beyond 2017+

HFV6 GM No 2015 Program extends beyond 2017+

6T70 / 6F GM / Ford Yes 2014 Program extends beyond 2017+

Pentastar Chrysler Yes 2014 Program extends beyond 2017+

DV6 PSA/Ford Yes 2015 Program ends 2015-2016

GF-6 GM Yes 2013 Partial renewals expected. Program extends beyond 2017+

6L GM No 2014 Program extends beyond 2017+

GF-6 Carriers GM Yes 2016 Program extends beyond 2017+

Carrier Line Magna Yes 2014 Program extends beyond 2017+

L850 VVT HiLite Yes 2010 Contract renewal underway. Program extends beyond 2017+

15

Vehicles Served

Powertrain’s products are used in a diverse range of vehicles and no one vehicle accounts for

more than 7% of sales. The Ford 150, which uses the 6R platform, represents Powertrain’s top

vehicle. The following table outlines Powertrain’s top 20 vehicle exposure:

Vehicle Concentration (% of Total 2011-2015 Production)

# Top Names Category %

1 Ford F-150 LT - Pickup 6.5%

2 Chevrolet-Malibu Car - Mid-Size 6.3%

3 Chevrolet-Equinox LT - SUV Mid/Full Size 4.8%

4 Chevrolet-Silverado LT - Pickup 3.9%

5 Buick-LaCrosse Car - Mid-Size 3.5%

6 Chevrolet-Cruze Car - Compact 3.3%

7 Buick-Regal Car - Mid-Size 2.6%

8 GMC-Terrain LT - Compact/Crossover 2.2%

9 Chevrolet-Impala Car - Full-Size 1.8%

10 Ford-Focus Car - Compact 1.8%

11 Ford-Explorer LT - SUV Mid/Full Size 1.7%

12 Dodge-Caravan LT - Other 1.7%

13 Cadillac-SRX LT - SUV Mid/Full Size 1.7%

14 Chevrolet-Camaro Car - Full-Size 1.6%

15 Chevrolet-Traverse LT - SUV Mid/Full Size 1.6%

16 Ford-Edge LT - SUV Mid/Full Size 1.5%

17 GMC-Sierra LT - Pickup 1.5%

18 Chrysler-Town & Country LT - Other 1.4%

19 Jeep-Grand Cherokee LT - SUV Mid/Full Size 1.4%

20 Ford-Taurus Car - Full-Size 1.4%

Total 52.2%

While Powertrain is diversified by vehicle, the Company’s vehicle mix does tend toward larger

vehicles. As shown in the chart below, SUV’s and Pickup Trucks comprise approximately 41%

of Powertrain’s total volume sales in 2011. It should be noted that the Company’s pumps are

also used on smaller engine platforms, for example the Chery 3 cylinder engine for the Chinese

market. We have considered the potential impacts of higher gasoline prices on vehicle mix in

our downside model scenarios.

Breakdown by Size of Vehicle

% of Total 2011P

Car - Compact 13.3%

Car - Mid-Size 18.1%

Car - Full-Size 7.4%

Car - Luxury 2.7%

LT - Compact/Crossover 7.0%

LT - SUV Mid/Full Size 26.2%

LT - Pickup 14.5%

LT - Other 10.8%

Total 100.0%

16

Suppliers

Powertrain’s supplier base is diversified with no one supplier accounting for more than 10% of

purchases in 2010. Powertrain’s largest raw material purchases include steel and aluminum

castings for oil pumps and iron for powdered metals. Due to the commodity nature of these raw

materials, Powertrain has alternate suppliers for all of its major purchases and did not experience

supply constraints in 2010, even when sales increased significantly beyond the initial budget.

The Company is in the process of locking down additional suppliers to support future growth in

China.

Powertrain - Summary of Top 30 Vendors

For the year ended 2010 % of

Vendor Name Curr Year 2010 2010

QUEBEC METAL POWDERS LIMITED US 12,548,715$ 9.9%

ACCURCAST INC CA 10,598,624$ 8.4%

IMCG GLOBAL INC US 4,925,915$ 3.9%

AMT DIE CASTINGS CA 4,434,026$ 3.5%

NORTH AMERICAN HOGANAS INC US 3,942,801$ 3.1%

PREMIER TOOL AND DIE CAST CORP US 3,871,002$ 3.1%

ACUPOWDER INTERNATIONAL, LLC US 3,178,003$ 2.5%

KOYO BEARINGS CANADA INC. CA 3,038,464$ 2.4%

HYDRO ONE CA 2,834,034$ 2.2%

LITTLE LAKES MACHINE CA 2,734,071$ 2.2%

Brome Financial Corp. Inc. CA 2,669,700$ 2.1%

ADECCO CA 2,588,681$ 2.0%

SPARTAN LIGHT METAL PRODUCTS US 2,471,758$ 2.0%

WEBER SUPPLY COMPANY INC. CA 2,345,591$ 1.9%

UPS SCS INC - MONTREAL CA 2,166,034$ 1.7%

PMG INDIANA CORPORATION US 2,097,009$ 1.7%

Revstone Industries Burlington CA 2,008,376$ 1.6%

THE STAFFING EDGE INC. CA 1,905,177$ 1.5%

RBC DEXIA INVESTOR SERVICES CA 1,865,382$ 1.5%

TRU-DIE LIMITED CA 1,826,491$ 1.4%

SHELL ENERGY NORTH AMERICA CA 1,814,285$ 1.4%

HUSCO AUTOMOTIVE PRODUCTS LLC US 1,810,727$ 1.4%

INA USA CORP US 1,778,143$ 1.4%

STEVENS RESOURCE GROUP INC CA 1,761,340$ 1.4%

GREAT-WEST LIFE ASSURANCE CO. CA 1,727,741$ 1.4%

WORKPLACE SAFETY & INS. BOARD CA 1,644,118$ 1.3%

NIAGARA TOOLS CA 1,512,166$ 1.2%

SYSTEMATIX INC. CA 1,380,681$ 1.1%

FERRO TECHNIQUE LIMITED. US 1,357,184$ 1.1%

AIR PRODUCTS CANADA LIMITED CA 1,342,645$ 1.1%

Total for Top 30 90,178,883$ 71.2%

Total 2010 Purchases 126,600,000$ 100.0%

17

Competitors

Powertrain competes on a number of dimensions: quality, price, execution and global reach.

Powertrain’s most significant competitor is Magna International. Magna is a global, diversified

automotive components supplier based in Ontario, Canada. Magna manufactures both a fixed

displacement and a variable vane oil pump that are of comparable quality and price points to

Powertrain’s products. However, according to management, Powertrain outperforms Magna

when it comes to execution. According to Robert Mooy, the head of Powertrain’s oil pump

division, “It’s one thing to manufacture one pump successfully during the prototype phase, but

it’s an entirely different challenge to manufacture one million pumps each year for the customer

with 100% on-time delivery.” We expect to confirm our belief that Powertrain is viewed as a top

tier supplier through customer calls during confirmatory diligence. Other key competitors

include SHW, Pierburg and Mahle. SHW and Pierburg have a limited presence in North

America, but have been successful in Europe and Asia. Mahle has been very aggressive on

price, but has had trouble competing with Powertrain and Magna on the quality and execution

dimensions. The following table outlines current market share by region for fixed and variable

displacement pumps for the top competitors in the space:

2011 Market Share AnalysisTransmission Engine

NA Eu Asia NA Eu Asia

Non-captive Fixed Pumps:

Powertrain 37.0% 0.0% 0.0% 16.0% 0.0% 0.0%

Magna International 25.0% 5.0% 5.0% 21.0% 15.0% 5.0%

SHW 0.0% 20.0% 0.0% 2.0% 30.0% 5.0%

Pierburg 0.0% 20.0% 0.0% 2.0% 30.0% 5.0%

Mahle 0.0% 10.0% 0.0% 0.0% 0.0% 0.0%

Non-captive Variable Pumps:

Powertrain 100.0% 0.0% 0.0% 40.0% 15.0% 0.0%

Magna International 0.0% 0.0% 0.0% 44.0% 10.0% 0.0%

SHW 0.0% 0.0% 0.0% 6.0% 35.0% 85.0%

Pierburg 0.0% 0.0% 0.0% 0.0% 15.0% 0.0%

Mahle 0.0% 0.0% 0.0% 0.0% 3.0% 0.0%

Source: CSM data and management estimates.

According to management estimates, Powertrain will gain market share in Europe and Asia by

2015 through variable vane pump business that has already been booked. Powertrain’s current

presence in Europe and Asia is small, as those programs are in the early stages of the platform

lifecycle.

18

III. Industry Overview

Production Volumes

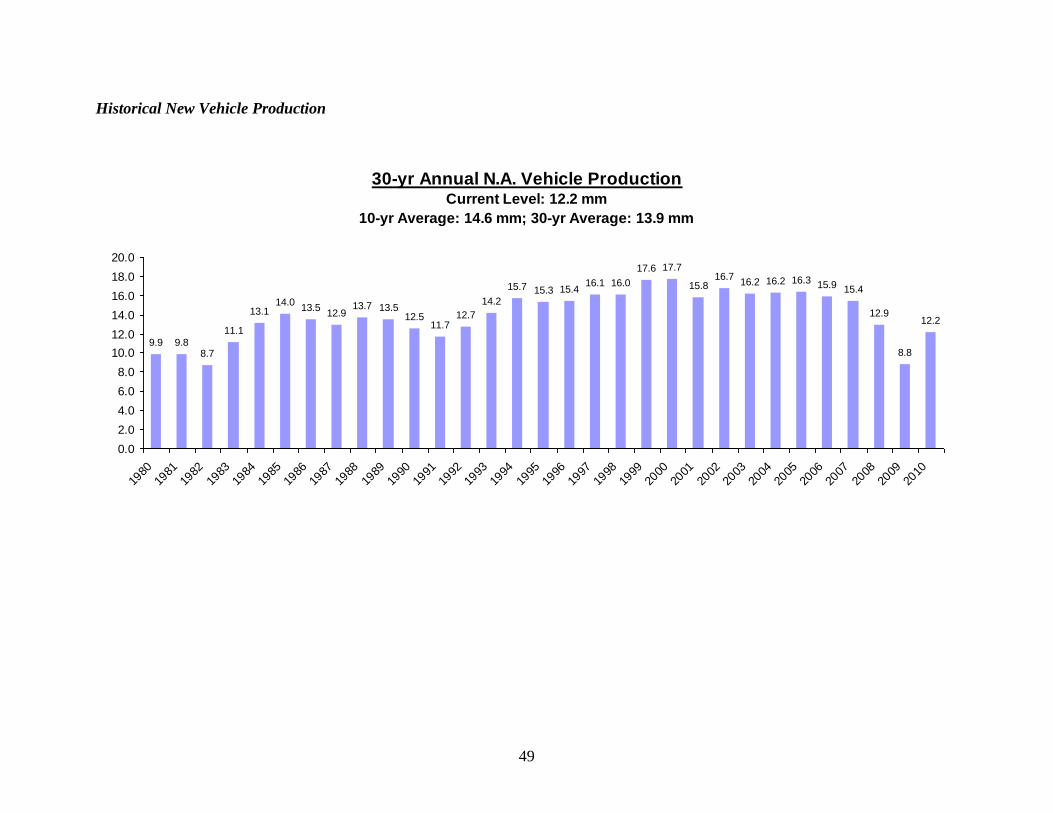

The global automotive market experienced one of the most severe contractions in its history

during the last economic recession. Annualized light vehicle production declined from 15.8

million units in Q2 of 2007 to 6.8 million units in Q1 of 2009. While light vehicle production

remains lower than historic averages, it has improved significantly relative to 2009. This

positive momentum is expected to continue in 2011 due to the increasing age of cars on the road

and the return of consumer confidence and credit availability.

North American Light Vehicle Production

From a historical perspective, the automotive industry has been relatively stable over the last

thirty years. Over the last ten years, production has averaged 14.6 million vehicles per year.

Over the last thirty years, production has averaged 13.9 million vehicles per year. In addition, as

a percentage of the U.S. population, vehicle production levels in 2010 were the second lowest

they have been in thirty years – 3.9% versus a ten-year average of 4.9% and a 30-year average of

5.2%. Additional historical vehicle production data can be found in the Appendix.

Currently, 70% of the market for automotive pumps and powdered metal components is non-

captive and this percentage is projected to grow to 80% by 2015 as automotive manufacturers

continue to outsource to reduce cost, enhance flexibility and benefit from product innovation

driven by specialized expertise.

Underlying Drivers

Underlying drivers of automotive demand include consumer sentiment and vehicle aging.

Consumer confidence has historically been a very good predictor of auto sales, and these

two variables have tracked each other closely:

19

Note: Light blue = auto sales; Dark blue = consumer confidence.

The average age of a car on the road is over 10 years, the highest it has ever been

(according to RL Polk, the average age of a car hit 11 years in 2010), with an average

mileage of 120,000-150,000 thus approaching the point where repairs typically exceed

the cost of buying a new vehicle. Annual vehicle aging is shown in the chart below:

20

CSM Projections

CSM, which was acquired by IHS Automotive in May of 2010, is the most widely used and

trusted independent source of automotive forecasting data. CSM employs over 130 automotive

experts to produce extremely detailed auto production forecasts (down to the vehicle level), and

its customers include 85% of the largest OEMs.

CSM provides independent unit projections for each of Powertrain’s platforms. As evidenced in

the table below, management’s projections are generally in-line with CSM:

Key Pump Platforms - CSM vs. Management

CAGR

2011 2012 2013 2014 2015 '11-'15

6R Platform:

CSM 649,137 694,354 770,687 900,826 934,072 9.5%

Management 572,600 634,500 799,000 799,940 799,940 8.7%

% of CSM 88.2% 91.4% 103.7% 88.8% 85.6%

Pentastar Platform:

CSM 759,382 773,470 779,390 787,625 711,882 (1.6%)

Management 545,250 634,500 681,500 744,245 720,510 7.2%

% of CSM 71.8% 82.0% 87.4% 94.5% 101.2%

HFV6 Platform:

CSM 815,018 1,000,906 913,843 885,298 892,585 2.3%

Management 816,800 1,010,500 971,960 953,395 926,840 3.2%

% of CSM 100.2% 101.0% 106.4% 107.7% 103.8%

6T70-6F Platform:

CSM 1,060,451 1,228,191 1,072,629 1,027,088 990,609 (1.7%)

Management 1,006,400 1,057,500 1,057,500 971,490 971,490 (0.9%)

% of CSM 94.9% 86.1% 98.6% 94.6% 98.1%

DV6 Platform:

CSM 1,657,279 1,734,045 1,850,743 1,943,465 1,779,327 1.8%

Management 1,250,150 1,681,300 1,731,400 1,221,450 500,000 (20.5%)

% of CSM 75.4% 97.0% 93.6% 62.8% 28.1%

Total Major Pumps:

CSM 4,941,267 5,430,966 5,387,292 5,544,302 5,308,475 1.8%

Management 4,191,200 5,018,300 5,241,360 4,690,520 3,918,780 (1.7%)

% of CSM 84.8% 92.4% 97.3% 84.6% 73.8%

Conclusion: Now is an opportunistic time to invest in the automotive sector, when production

volumes are near cyclical lows and the industry is in the early stages of emerging from the last

economic recession. In addition, the availability of detailed, product-level projections from

independent research analysts provides a valuable resource to sanitize management’s

projections.

21

IV. Historical Financials

Summary of Historical Financial Performance

Year Ending December 31,

($ in millions) 2008 2009 2010 LTM 5/31/11

Revenue

Oil Pump $91.6 $82.9 $127.0 $152.5

Powdered Metal 99.0 89.1 135.8 164.0

Corporate and Other Adjustments (1)

(15.4) (9.6) (14.6) (30.7)

Total Revenue $175.2 $162.4 $248.2 $285.8

Oil Pump Revenue % Growth (9.5%) 53.2% NM

Powdered Metal Revenue % Growth (10.0%) 52.4% NM

Total Revenue % Growth (7.3%) 52.8% NM

Total Gross Profit $31.5 $35.1 $56.4 $58.9

% Margin 18.0% 21.6% 22.7% 20.6%

Adj. EBITDA (2)

$19.8 $18.4 $46.1 $50.3

% Margin 11.3% 11.3% 18.6% 17.6%

Capital Expenditures $17.4 $10.2 $25.3 $28.1

% Revenue 9.9% 6.3% 10.2% 9.8%

Key Balance Sheet Items:

Inventory $11.2 $8.0 $15.8 NA

Accounts Receivable 26.3 34.5 43.9 NA

Net PP&E 134.1 152.0 163.4 NA

$0$100$200$300$400$500$600$700

2008

(1) Primarily relates to intercompany sales from PM to pump division.

(2) Includes pro forma standalone costs and KMPG QofE adjustments.

Despite the severe economic downturn, Powertrain’s revenue grew from $175.2 million in 2008

to 248.2 million in 2010, representing a CAGR of 19%.

In 2009, revenue declined by just 7% versus revenue declines by Ford of 19% and GM of 29.8%.

The outperformance was driven by market share gains resulting from new program wins signed

up prior to the recession. These programs were ramping during the early stages of their

lifecycles and helped offset some of the impact of the overall downward economic pressure of

unit volumes.

Revenues in each of Powertrain’s Powdered Metal and Pumps Divisions rebounded in 2010,

with growth of ~50%. This rebound was driven by:

i) Industry Rebound. North American new vehicle production increased from 8.5

million units in 2009 to 11.9 million units in 2010. Ford sales were up 10.9% in 2010

and GM sales were up 29.6% in 2010. The improved vehicle demand provided a

significant industry tailwind for Powertrain.

ii) Existing Business Ramp. Key platforms including the 6R, the HFV6, the 6T70-6F

and the 6L ramped considerably from 2009 to 2010, as they moved closer towards

their peak volume levels.

22

iii) New Business Wins. The Company won considerable new business that began to

show volumes in 2010 including the Pentastar for Chrysler and a variety of other

smaller platforms.

In addition to revenue gains, Powertrain improved gross margins and EBITDA margins in both

2009 and 2010. This improvement was driven by three primary factors:

i) Improved Business Mix. High margin programs, including the 6R and the 6L,

ramped considerably from 2008 to 2010.

ii) Fixed Cost Leverage. The Company’s plant level SG&A and P&PD costs are

almost entirely fixed. Therefore, the Company benefits from improved margins when

volumes increase.

iii) Cost Initiatives. The most significant cost improvements have been generated by

automation. The Company has made substantial capital expenditures to add machines

and reduce headcount.

The cumulative impact of these improvements in revenue and margins is reflected in the

historical growth in EBITDA from $19.8 million in 2008 to $46.1 million in 2010,

representing a CAGR of 52.6%.

23

V. Standalone Cost Analysis

Powertrain currently operates largely on a standalone basis and there are relatively few shared

services with the larger Tompkins organization. For example, when preparing the 2010 audit

for this division, the auditors were required to make very limited carve-out assumptions because

so much of the business was already being operated independently of Tompkins. Management

estimates that the incremental expense to operate the business on a standalone basis would be

$1.5 million. Sterling and KPMG estimate that the incremental expenses to run the business on

a standalone basis would be $2.4 million, reflecting additional amounts in insurance as well as

audit and legal expenses. KPMG has conducted a quality of earnings analysis of the Adjusted

EBITDA as well as an analysis of the standalone cost assumptions, confirming the numbers in

the table below:

Standalone Cost Analysis($ in thousands)

Current Standalone Standalone

Costs Mgmt Estimate Sterling Estimate

North America:

Salaries $6,054 $6,134 $6,134

Benefits 989 1,145 1,145

Insurance 1 106 750

Information Technology 215 371 371

Audit / Legal Fees 320 340 550

Travel / Meals / Entertainment 393 428 428

Outside Services 333 328 328

Miscellaneous 1,101 1,212 1,212

Total North America $9,406 $10,064 $10,918

Europe $2,848 $3,712 $3,712

Total Overhead Costs $12,254 $13,776 $14,630

Standalone Adjustment $1,522 $2,376

LTM 5/31/2011 Adj. EBITDA, pre-Standalone $52,691

Less: Sterling Standalone Costs ($2,376)

LTM 5/31/2011 Adj. EBITDA, post-Standalone $50,315

24

VI. Management

The Sterling investment team has been impressed with the management team at Powertrain. The

experience, depth and sophistication of the management team are stronger than we would

typically expect for a small division of a large, multinational corporation. Powertrain’s

management team has an average of 21 years of experience in the oil pump and powdered metal

components industries. In addition, the management team is excited about the potential benefits

from operating on a standalone basis. On a scale of 1-10 (relative to other Sterling portfolio

companies), we would rank the Powertrain team an 8 or 9.

Peter Ballantyne, President – Peter has served as President of Powertrain since 2010. He

joined Tomkins as VP Business Improvement in 2009. Prior to joining Powertrain, Peter

worked for Magna International as Group General Manager since 2007 and VP

Operations, Managing Director since 2003. Peter has over 25 years of experience in the

automotive industry. He graduated from Queen’s University with a B.Sc. in Engineering

and holds a business diploma from Wilfrid Laurier University.

Rahim Suleman, Director Finance – Rahim has served as the Director Finance since

joining Powertrain in July 2010. Prior to joining Powertrain, Rahim was the Global

Finance Manager for GE Digital Energy. He has served as Corporate Controller and VP

Finance for various organizations and has experience in the manufacturing, information

technology and real estate industries. He has over seven years of experience in the

automotive industry. Rahim is a Chartered Accountant (CA) and holds a Master of

Accountancy and a Bachelor of Arts (Accountancy) from the University of Waterloo.

Andrew Dempsey, Director Engineering – Andrew has served as Director Engineering

since November 2008. He joined Powertrain in November 1998 and has held several

roles of increasing responsibility in the engineering organization. Prior to joining

Powertrain, Andrew served in technical roles of increasing responsibility with several PM

manufacturers. Andrew holds an M.A.Sc. in Metallurgy and Materials Science and a

B.A.Sc. in Metallurgical Engineering and is a member of the Professional Engineers of

Ontario.

Robert Mooy, Vice President Engineered Products Division – Rob has served as VP

Engineered Products Division since April 2008. He joined Powertrain in 2002 as Director

of Product Development and was promoted to VP of Product/Business Development in

2005. Prior to joining Powertrain, Rob held several management and engineering roles of

increasing responsibility in the Tier one automotive supplier segment. He holds a

Bachelors Degree in Mechanical Engineering and is a member of the Professional

Engineers of Ontario.

25

Mohamad El-Mahmoud, Business Unit Director, Asia – Mohamad entered Gates GmbH

Aachen as a Mechanical Designer in 2000. In 2002 he was promoted to Systems

Engineering Manager, a position he kept until July 2004 when he was dispatched to Asia

on an assignment as Engineering Manager with target to build up and expand the

technical organization in China, Korea and India. He later served as Asia Business

Development Director until August 2008 when he became responsible for Engineered

Products Asia activities with a focus on variable vane oil pumps. Prior for working with

Gates, Mohamad was a mechanical designer with PH-Mechanik, an automation company

based in Aachen, Germany. He has eleven years of automotive experience and holds BS

in Mechanical Engineering and Aeronautics from Aachen University of Applied Science.

26

VII. Attractiveness and Opportunities of Investment

Market leader in North America

Powertrain has manufactured powdered metal components for 55 years and has manufactured oil

pumps for 20 years. Powertrain is one of the top three powertrain component suppliers on a

global basis. In North America, Powertrain is the market share leader in fixed

displacement pumps with an approximate market share of 26% of the non-captive market

and variable displacement pumps with an approximate market share of 64% of the non-

captive market. Powertrain developed the industry’s first variable displacement pump and

therefore is well-positioned to maintain leadership as variable vane penetration increases.

Powertrain is also the second largest powdered metal supplier in North America. Powertrain’s

market leadership stems from a long history and track record with GM (35 years), Ford (27

years) and Chrysler (22 years).

Substantial Revenue Visibility

The Company typically starts working with an OEM 2-3 years in advance of initial production

volumes and Powertrain and its customers plan capacity requirements in multiple phases across a

seven to ten year volume planning window – each phase being an incremental uplift in

production volumes. For example, Powertrain started working with Chrysler in 2004 on

Pentastar, a new variable displacement engine oil pump. The Company was awarded the

business in 2006 and started shipping units in 2009 at very low volumes. As various vehicle

platforms have migrated to the new engine platform (as planned), volumes have ramped to more

than 500,000 units in 2011 and expected to grow to more than 700,000 units by 2015. The

underlying vehicle migration timing is planned by Chrysler and underlying vehicle demand is

diversified across multiple nameplates. For example, Pentastar will be used on 28 nameplate

vehicles.

Using these long-term volume projections, the company’s forecasted sales between 2011 and

2015 are based on: 1) the known ramping of existing platforms as additional vehicles are moved

onto new powertrain platforms, plus; 2) the startup of new booked platforms, plus; 3) projected

“blue sky” business, less; 4) the decline older platforms. The combination of 1) and 2) is

generally referred to as “contracted” as the unit prices for these volumes are contracted with the

customer. Thus, the long lead time planning, underlying nameplate diversification and

contracted pricing provides a high level of visibility to future sales related to “contracted”

business. Based on management volume forecast (in aggregate, an approximate 10% discount to

CSM volume forecasts), the Company has more than $2.0 billion in “booked” sales between

2011 and 2015, representing 98% of projected sales over the period.

High Switching Costs and Barriers to Entry

Once a powertrain program is underway, it is very difficult for an original equipment

manufacturer to switch powertrain component suppliers due to:

27

High Upfront CapEx. Both Powertrain and the customer make substantial upfront

capital expenditures to support a given platform and vehicle design. Changing the key

components of an engine or transmission would have ripple effects throughout the design

that would be costly for the original equipment manufacturer

Specification Process. Powertrain’s products undergo substantial upfront testing and

validation before being specified into an engine or transmission. In order to switch

products during the cycle, the customer would need to conduct an eight month long

validation process of the alternative product, which is expensive and would be disruptive

to the customer’s production cycle

Black Box. Powertrain owns the technology for the majority of its automotive oil pump

platforms. The “black box” nature of the product from the customer’s perspective makes

it difficult for the customer to switch suppliers mid-cycle to fulfill the same requirements

In addition, the powertrain industry is well-protected against new entrants due to:

Proven durability and delivery. The powertrain is the centerpiece of the vehicle

platforms. As OEM’s migrate to more global powertrain platforms (for example, the GF-

6) and add an increasing number of vehicles to each platform, the powertrain’s system

components and the supply chain supporting the powertrain have become more critical.

OEM’s want proven technologies from proven suppliers.

Products involve proprietary technologies that have evolved over many years

Entry would require large upfront capital expenditures with 2-3 year lag before any cash

flows are realized

The high switching costs and barriers to entry for this business should support margin

sustainability and sticky cash flows throughout the projection period.

Management Team

The deal team has been impressed with the management team of Powertrain, including Peter

Ballantyne, the President who joined the team in 2010 from Magna International, Robert Mooy,

the head of the oil pumps business, and Rahim Suleman, the CFO who joined the team in 2010

from General Electric. The quality of the team also extends beyond these three top executives –

the other key regional heads and divisional managers know their business well. As a whole, the

management team has an average of 21 years in the oil pump and powdered metal industry.

The management team overall is excited about the opportunity to grow the business as a

standalone entity. Management describes the organization as more nimble and responsive before

being acquired by Tompkins in 2003. Management believes the carve-out will help create an

energized culture within Powertrain. The management team is not expected to receive a large

pay-out in conjunction with this transaction and therefore will be highly aligned with Sterling

through their options package. A focused, hungry management team will be a critical

component of our investment success, as Powertrain executes on existing booked business while

also expanding its foothold in Europe and Asia.

28

Europe and Asia Growth Opportunity

As discussed earlier in the memo, Powertrain currently has a small presence in Europe and Asia,

but these regions represent attractive future growth opportunities. Management sees significant

opportunities to grow in these markets both by winning new customers and by following existing

customers. Europe and Asia are projected to grow from 3% of sales in 2010 to 23% of sales in

2015. In support of this projected revenue growth, Powertrain has already been awarded 11

platforms in Europe and five in China. Prior to closing the acquisition, Powertrain was also

awarded an oil pump contract with Hyundai, representing the first oil pump sourced to a "non-

Korean" supplier by Hyundai. This new platform will result in upside beyond the base case

projections and could result in future opportunities with Hyundai in North America. From an

exit planning perspective, by developing a presence in Asia, the Company may attract increased

strategic interest and the improved growth profile could merit a higher valuation multiple. China

is now the largest automotive market in the world ahead of Europe and the U.S.

Limited Auction Effectiveness with Complexities

A limited number of parties were actively involved in the auction process run by RBC and UBS.

The number of parties in the process was limited for a variety of factors, including:

The CIM did a particularly weak job presenting three significant investment attributes – the

largely contracted nature of a substantial amount of the Company’s sales, the significant tax

attributes associated with the transaction and the discretionary nature of growth capital

expenditures. Our team’s IOI was submitted on behalf of Sterling and Current Capital and

Sterling would likely not have submitted an IOI, was it not for Mr. Foster’s knowledge of the

auto industry.

The dual-bank process (UBS/RBC) created confusion and was generally ill-coordinated

during the early stages of the process.

The carve-out nature creates complications related to evaluating stand alone costs (and the

risks related thereto) and negotiating and managing transition services which will be needed.

Many private equity firms and financing sources are not interested in automotive-related

opportunities given the performance during the downturn.

The recent recession stressed most tier-1 automotive suppliers severely. Based on

discussions with industry participants, most suppliers are cautious about acquisitions and

continue to be internally focused on initiative and/or ramping capacity to support the rebound

in demand. Further, equity analysts suggest most larger suppliers are focused on deploying

capital in faster growing emerging markets. Industry experts expect more corporate

acquisition activity in a few years.

Clear opportunity for Sterling Value Creation

Although management has made significant headway winning new platforms and ramping

volumes over the last several years, we believe there are several areas where Sterling can help

management further develop its growth strategy as well as add more focus to specific operational

initiatives. The main areas of Sterling impact are expected to be (detailed further in post-closing

initiatives):

29

Transition to a stand alone enterprise

Enhanced alignment between management incentives and shareholder value creation

Improved rigor around capital expenditures

Execution of ramp of early stage North American programs

Execution of European and Asian growth plans

Expansion into New Product Markets

VIII. Issues and Risks of Investment

High Customer Concentration

As is often the case in the North American automotive components industry, Powertrain has a

high level of exposure to the big three U.S. automotive manufacturers – Ford, General Motors

and Chrysler. Together, these three companies are expected to represent 78% of Powertrain’s

2011E sales. A loss of one of the Big Three as customers would significantly damage the cash

flows of the Company. In addition, the customer concentration may result in pricing pressure

during the front-end of new program negotiations when there is another viable supplier such as

Magna included in the bidding process.

Risk Mitigants:

Nature and timing of platforms – As discussed earlier, Powertrain is integrated across a

number of key platforms for these customers and it would be very difficult and costly for the

OEM’s to switch suppliers. Both parties have a fair amount of leverage over each other

Long relationships – 35 year relationship with GM, 27 year relationship with Ford and 22

year relationship with Chrysler

Contracts in place – prices locked in for 3-5 years

For each major automotive manufacturer, sell to a number of platforms and many vehicles

We’ve received positive feedback on the deal from former GM and Ford powertrain

executives. Customer calls will be completed during the exclusivity period

Volatile Nature of the Automobile Industry

The automotive industry has historically been volatile and highly cyclical in nature. For

example, during the last recession, Ford Motor Company’s sales dropped 17.3% in 2008 and

18.6% in 2009. Annualized light vehicle production declined from 15.8 million units in Q2 of

2007 to 6.8 million units in Q1 of 2009. General Motors and Chrysler both required capital

infusions from the government as part of a federally assisted bankruptcy process. A “double-dip”

recession or future automotive downturn could have a negative impact on the financial

performance of Powertrain. Given the high fixed cost nature of the business, a decline in

Powertrain’s sales would likely be coupled with declines in gross margin and EBITDA margin

percentages as well.

Risk Mitigants:

30

With annualized production of new vehicles near trough levels, our timing in the cycle may

provide downside protection. 2011E North America new vehicle production is 13 million

cars versus historical levels during more normal economic conditions of between 15-16

million units

The ramp up in booked business over the next two years could largely offset a decline in

industry volumes. For example, because of the ramp in 2009, the Company increased

EBITDA despite very weak end-market conditions.

High Capital Expenditure Requirements

Between 2008 and 2010, the Company invested on average $17.6 million in capital expenditures

a year, or 58% of cumulative EBITDA over the three year period. While management has

indicated that the business needs approximately $3.0 to $4.5 million in maintenance capital

expenditures per year (approximately 7% of 2011 EBITDA), the historical trends suggests the

business is very capital intensive and management’s definition of maintenance capital

expenditure may not adequately reflect the capital needs going forward. Further, the recent

ramping of new platforms (new phases), limited historical stand alone financial information and

ongoing expenditures related to continuous improvement (“CI”) projects add uncertainty to our

estimates of maintenance versus growth capital expenditures.

After several discussions with management on capital expenditures and evaluating historical

investments at the platform level, we have concluded that the majority of the recent capital

investments have been on growth projects, as listed below.

Capital Expenditures Contribution Margin Capex /

2008 2009 2010 2011 2012 2008 2012 Delta Margin

6R $ 0.9 $ 2.0 $ 2.6 $ 3.5 $ 1.1 $ 6.3 $ 31.1 $ 24.8 0.4x

Pentastar 0.3 2.7 0.5 0.6 0.5 - 8.1 8.1 0.6x

DV6 - 0.2 8.3 0.9 - - 11.0 11.0 0.9x

6L Group 4.7 0.5 0.9 0.5 1.0 20.4 33.5 13.0 0.6x

GF6 Carriers 4.1 0.5 2.6 2.6 2.8 1.3 19.2 17.9 0.7x

Asia + Europe Facility (excluding DV6) 1.4 2.0 5.0 5.9 6.2 2.1 6.3 4.3 4.8x

Sub total Major Platforms / Plants Growth $ 11.3 $ 7.9 $ 19.9 $ 14.1 $ 11.5 $ 30.1 $ 109.2 $ 79.1 0.8x

Other Platform Specific Growth 2.1 0.4 2.0 6.1 6.7 67.8 102.3 34.6 0.5x

Total Growth $ 13.4 $ 8.3 $ 21.9 $ 20.2 $ 18.2 $ 97.9 $ 211.5 $ 113.6 0.7x

(Growth as a % of Total) 76.6% 80.6% 86.6% 85.7% 80.9%

Plus: Maintenance 4.1 2.0 3.4 3.4 4.3

Total Capex $ 17.5 $ 10.3 $ 25.3 $ 23.6 $ 22.5

Based on the above data, the growth capital spent to support the top 5 platforms has obviously

generated excellent returns for Powertrain. On the other hand, the growth capital spent to

support Asia and Europe has not generated significant cash flows and therefore the expected

return on this capital is less certain.

On a consolidated basis, between 2008 and 2012, powertrain will have invested more than $82

million in growth capital and close to $100 million in total capital. Over this time frame

EBITDA is expected to increase by more than $50 million on a run rate basis ($26 has already

occurred), implying a very attractive return on the growth capital expenditures in total. While

attractive historically, the substantial capital requirements put the Company at risk of significant

capital outlays prior to platform ramp ups. Nevertheless, the business will continue to need to

31

take on expenditures to support platform renewals and launches, as this is simply the nature of

the automotive supplier’s business.

Further, while more than 80% of the capital expenditures between 2008 and 2012 have been or

will be for platform/facility specific growth projects, given the finite life of a platform and the

requirement to invest in dedicated capital for each platform, we have further differentiated

growth capital expenditures into “generic capital” and “dedicated capital”. In general, generic

capital investments are made in flexible equipment (CNC mills, lathes, grinders, cleaners,

robots…) that can be reconfigured to future uses with minimal investment, with assets often

outliving a specific program. Dedicated capital investments on the other hand, (custom assembly

cells, specialty test fixtures) require significant investment to redeploy and are often designed for

the life of the program. Based on our review of multiple large and small platforms,

approximately 35-40% of the growth capital invested for a platform is dedicated capital,

requiring “replenishment”. The table below shows the replenishment capital required for a

number of the Company’s platforms.

Sample

Sample Platforms 6R 6T70 HFV6 Penta DV6 Mean

Peak Sales $ 70.0 $ 31.0 $ 16.0 $ 26.0 $ 37.0 $ 180.0

Total Capital 32.3 9.1 6.0 7.1 9.5 $ 64.0

Capex / Peak Sales 0.46x 0.29x 0.38x 0.27x 0.26x 0.36x

Dedicated Capital $ 5.5 $ 4.0 $ 2.5 $ 3.0 $ 4.0 $ 19.0

Dedicated (% of total Capex) 17.0% 44.0% 41.7% 42.3% 42.1% 37.4%

Life 15.0 12.0 16.0 11.0 5.0 11.8

Replinishment Capital (% of Sales)1

0.7% 1.5% 1.4% 1.5% 3.1% 1.6%

1 Average annual sales is used to calculate this metric as at any point in time muliple platforms are in

various stages of ramping up or down. The average gives a better % of sales metric to aplpy to

an aggregate sales figure.

The combination of regular-way maintenance capital and replenishment capital results in a

higher ongoing steady state capital requirement for the business. Thus, while we do think

management has budgeted adequate future capital expenditures for the forecast period in

aggregate, we would expect capital requirements to be quite a bit higher than pure maintenance

capital should the business enter a slower growth phase. When applied to 2011 forecasted sales,

we believe a more appropriate recurring capital requirement is $8.6 million, which represents

approximately 17% of 2011 EBITDA. However, for valuation purposes, we are assuming

annual maintenance and replacement capital expenditures to support the current earnings

would be approximately $10 million.

Rising Raw Material Costs

With $140 million in annual material purchases, Powertrain must actively manage its raw

material exposure. The largest material buys for the oil pump division are aluminum and steel

castings. The largest material buy for the powdered metal division is powdered iron. The deal

team believes that Powertrain’s net EBITDA exposure to rising raw material costs is generally

32

limited due to contracted material pass-throughs included in its oil pump and powdered metal

customer contracts as well as LTA arrangements with its suppliers. While aluminum, steel and

iron prices increased substantially in 2010, Powertrain’s material costs as a percentage of sales

have remained flat at approximately 34% since 2008. As detailed below, we have calculated that

a ten percentage increase in overall raw material costs would result in an ~$887K drop in

EBITDA.

Material Cost Analysis

($ in millions)

2011

Oil Pumps:

Total Material Buy $104,506

% Commodity-based 45.0%

Total Aluminum / Steel Buy $47,028

% Tied to Commodity Price 60.0%

Total Tied to Commodity Price $28,217

% Not Covered by Material Pass-throughs 10.0%

Total Oil Pump Purchases Exposed $2,822

Powdered Metals:

Total Material Buy $35,929

% Commodity-based 85.0%

Total Iron Buy $30,540

% Tied to Commodity Price 33.0%

Total Tied to Commodity Price $10,078

% Not Covered by Material Pass-throughs 60.0%

Total PM Purchases Exposed $6,047

Total Material Purchases Exposed $8,869

EBITDA Impact from 10% Rise in Raw Material Costs ($887)

Lack of Currency Parity Between Purchases and Revenue

The Company purchases approximately $40 million in net USD inputs while the revenues are

collected in Canadian dollars. The CFO believes and our analysis supports, that every $0.01

change in exchange rate has a $400,000 impact to EBITDA. However, the Canadian economy is

generally a commodity-based economy – in 2009, agricultural, forestry, energy and mining

exports accounted for 58% of Canada’s total exports. Therefore, there is a high correlation

between movements in the Canadian dollar and movements in raw material costs. These two

movements have historically had offsetting impacts for Powertrain, with a cumulative total

EBITDA impact of currency and raw material costs from 2002-2010 of just $1.8 million and an

average impact of just $0.2 million. The following table shows the historical net impact of

movements in the CAD / USD exchange rate and Powertrain’s primary raw material costs:

33

Material Cost and Currency Impact Analysis

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Aluminum $1,446.7 $1,351.1 $1,432.8 $1,718.5 $1,900.5 $2,573.1 $2,639.9 $2,577.9 $1,669.2 $2,173.0

% Growth (6.6%) 6.1% 19.9% 10.6% 35.4% 2.6% (2.3%) (35.3%) 30.2%

EBITDA $ Impact $0.1 ($0.1) ($0.3) ($0.1) ($0.5) ($0.0) $0.0 $0.5 ($0.4)

Steel $299.1 $328.3 $444.6 $607.1 $733.3 $693.8 $650.0 $965.6 $783.3 $815.6

% Growth 9.8% 35.4% 36.6% 20.8% (5.4%) (6.3%) 48.6% (18.9%) 4.1%

EBITDA $ Impact ($0.1) ($0.5) ($0.5) ($0.3) $0.1 $0.1 ($0.7) $0.3 ($0.1)

Iron / Scrap Steel $88.7 $80.5 $133.0 $222.6 $216.6 $234.6 $280.1 $439.0 $248.5 $345.9

% Growth (9.2%) 65.2% 67.4% (2.7%) 8.3% 19.4% 56.7% (43.4%) 39.2%

EBITDA $ Impact $0.6 ($3.9) ($4.1) $0.2 ($0.5) ($1.2) ($3.4) $2.6 ($2.4)

CAD / USD $0.65 $0.64 $0.72 $0.77 $0.83 $0.88 $0.94 $0.94 $0.88 $0.97

% Growth (1.4%) 12.4% 7.5% 7.3% 6.8% 6.1% 0.8% (6.7%) 10.4%

EBITDA $ Impact ($0.4) $3.2 $2.2 $2.2 $2.2 $2.1 $0.3 ($2.5) $3.6

NET EBITDA $ Impact $0.2 ($1.4) ($2.7) $2.0 $1.3 $1.0 ($3.8) $0.9 $0.8

Cumulative 2002-2010 ($1.8)

Average 2002-2010 ($0.2)

34

USD Equity Investment Is Exposed to Changes in the CAD/USD Exchange Rate

For the debt portion of the capital structure, we executed a hedge to protect us from movements

in the exchange rate. For the $140 million first lien term loan, we locked in a fixed rate of

9.69%, with interest payments to be made in Canadian dollars. Similarly, for the $45 million

mezzanine debt, we locked in a fixed, Canadian rate of 13.60% cash and 2% PIK. In addition,

our covenants are to be calculated in Canadian dollars. However our equity investment will be

exposed to changes in CAD/USD exchange rates. An additional hedge for the equity would have

been prohibitively expensive, as Sterling similarly concluded when it acquired Canadian-based

North American Construction Group.

Changes in Technology or Consumer Preferences

Powertrain’s products are potentially at risk from technological obsolescence or changes in

consumer vehicle preferences. This risk could manifest itself in the form of a consumer shift

towards more fuel-efficient vehicles or through a competitor’s development of a superior

automotive oil pump or powdered metal technology:

Shift Towards More Fuel-Efficient Vehicles: 41% of Powertrain’s 2011E sales are

from SUV’s and trucks. A consumer shift away from large vehicles towards small

vehicles in response to high energy prices could negatively impact Powertrain. In

addition, a viable and affordable electric car could eliminate the need for oil pumps

Product Technology Shifts: Powertrain’s business model revolves around offering the

best oil pump and powdered metal technology at a premium price relative to most

competitors. There exists the possibility that a competitor will develop a superior oil

pump or powdered metal technology, resulting in market share losses for Powertrain

Risk Mitigants:

Technological changes in the automotive industry have historically had long lead times, due

to the long lifecycles of existing products and the substantial upfront investment made in the

existing technologies

We modeled sensitivities around vehicle size categories in order to ensure that the returns

would be acceptable even in the case that consumer vehicle preferences changed materially

Relative to other efficiency improvement options for OEM’s, variable displacement pumps

are a very cost effective way to increase fuel economy by 1-2%. Variable vane pump

penetration is still in infancy. The migration from fixed pumps to variable vane should

significantly benefit Powertrain

35

IX. Post-Closing Initiatives

Transition to a Standalone Enterprise and Onboard to Sterling Processes

Post-closing, the first initiative will be to smoothly transition the Powertrain business out of

Gates. This will involve a list of small items (audit, tax, legal, insurance…) for the Canadian

operations and some more material items for the European operations, for example a new ERP

system (albeit anticipated to be a very small project).

We will also quickly onboard the business to a monthly financial operating and management

review schedule. The Company closes its books (using the same process it uses at year end)

each month within 20 days of month end and generates a series of variance analysis and other

operating reports. Given the strength of the existing financial reporting packages and the

capacity of the CFO, we expect to quickly move to incorporate additional operational targets and

metrics into our operating reviews, which the Company does not currently highlight, for

example: key equipment utilization, platform level material/direct variances, return on

investment YTD for select platforms, and platform contribution margin analysis.

Establish Sterling Employee Incentive Programs and Implement the Board of Directors

Currently, a select group of senior managers participate in a weakly defined bonus plan. There is

no ownership of Powertrain equity by any of the employees and only Peter Ballantyne has

options in the larger Tomkins parent. For 2010, the total bonus pool was $0.8 million across 16

people. Despite the significant improvement in EBITDA (from $25 million to $46 million

between 2009 and 2010), bonuses have been held below 2% of Adjusted EBITDA . To properly

align the interest of the entire organization with those of Sterling, we will encourage broader

equity participation, both through direct equity ownership and stock options, and a clearly

defined incentive bonus program.

Establish More Rigorous Capital Investment Review and Tracking

The Company currently uses Gates’ capital review process and tools. While these are useful for

generic capital investment decisions they have been tweaked to fit Powertrain’s needs on an as

needed basis. They do not differentiate generic versus dedicated capital requirements and do not

evaluate sensitivities around ramp timing or volumes. We believe Sterling can help management

refine the investment process (model, review, approval) and ultimately make more optimal

capital investment decisions.

36

Further Develop and Execute Europe, Asia and New Product Market Expansion Plans

European Expansion

The start up and ramp of the Izmir, Turley operation will be well underway by the time of close,

primarily supporting two primary customers – PSA and Audi. Beyond these accounts,

management categorizes additional growth as “blue sky” or yet to be specifically determined.

And while the European market on the surface looks attractive (shift to variable vane technology,

highly emissions focused), based on our discussions with management and industry experts,

Europe is clearly a mature and highly competitive market. We believe further growth in Europe

will be challenging and as such expect to invest significant resources into managing the

development of that region. To date, the management team and Gates have developed a detailed

European growth plan and made substantial progress towards that plan. However, the Company

needs to further evaluate the longer term market opportunity and we expect Sterling to be

substantially involved and helpful towards that objective.

Asian Expansion

The successful execution of the Asian business development facility is a major component of the

upside in the Powertrain investment. The management team has been working on the China

development plan for several years and has prior experience operating in China (through the

prior Halla JV) and has developed a detailed business plan for a new China facility. We have

completed a preliminary review of the plan and based on conversations with management, the

plan is well thought out from an operational perspective but requires further evaluation of the

market opportunity. Sterling (and Sterling third party partners) would play a central role in the

assessment, development and ongoing support of the final plan. Like the other initiatives, the

management team is open to active involvement by Sterling.

Expansion Into New Product Markets