investment portfolio quarterly - winter 2014

DESCRIPTION

For more discussion and/or questions, please contact us at www.beltramewealthmanagement.comTRANSCRIPT

Investment Portfolio Quarterly

Insightful PerspectivesWinter 2014

Contents Page Executive Summary

Q4/13 Quarterly Comments 1 Portfolio Strategy

Normalization Year 3

Economic Outlook

U.S. Economic Outlook: Enter the Bear Flattener 11

Equity Strategy

Top 10 Canadian and U.S. Stocks Picks for 2014 18

Investment Strategy

Emerging Markets: One Step Forward, Two Steps Back? 34

Guided Portfolios

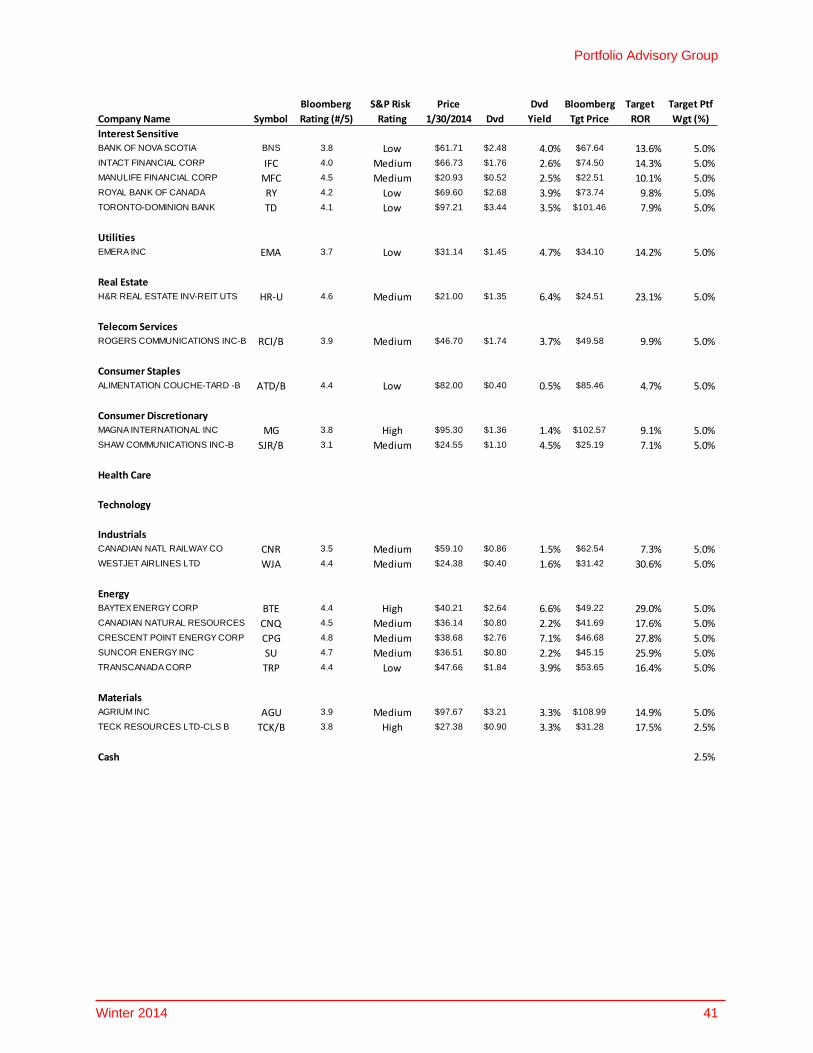

Canadian Core 38

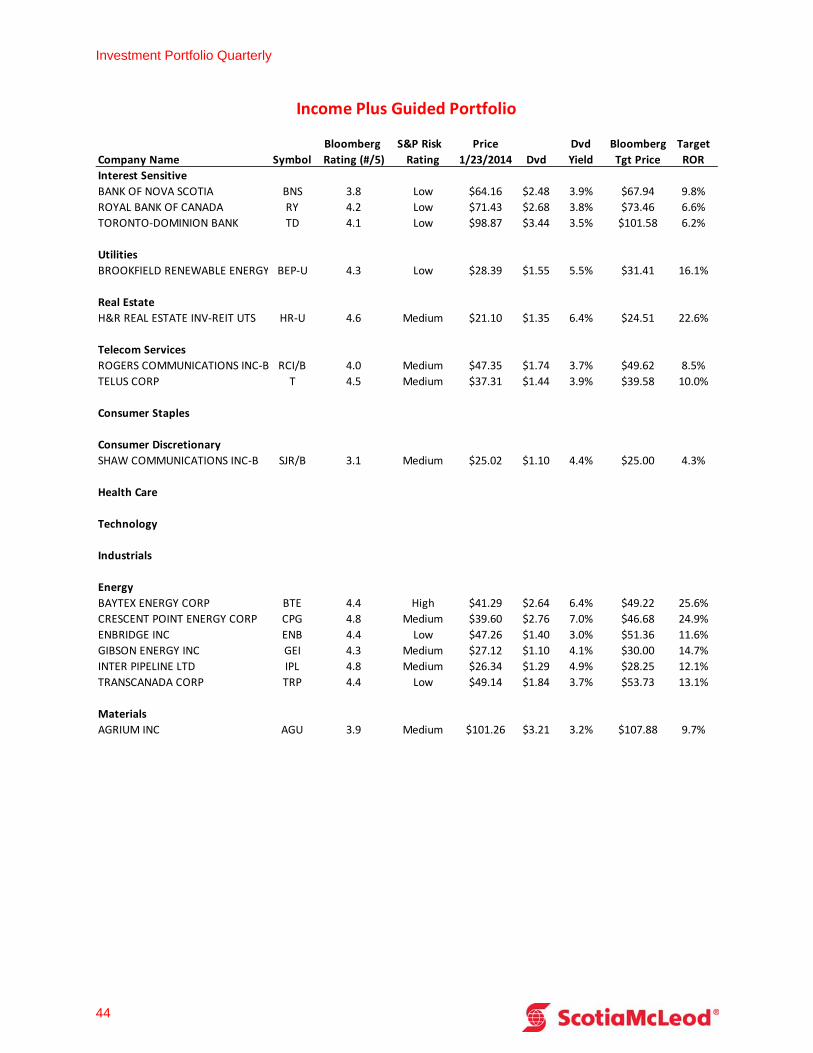

Canadian Income Plus 42

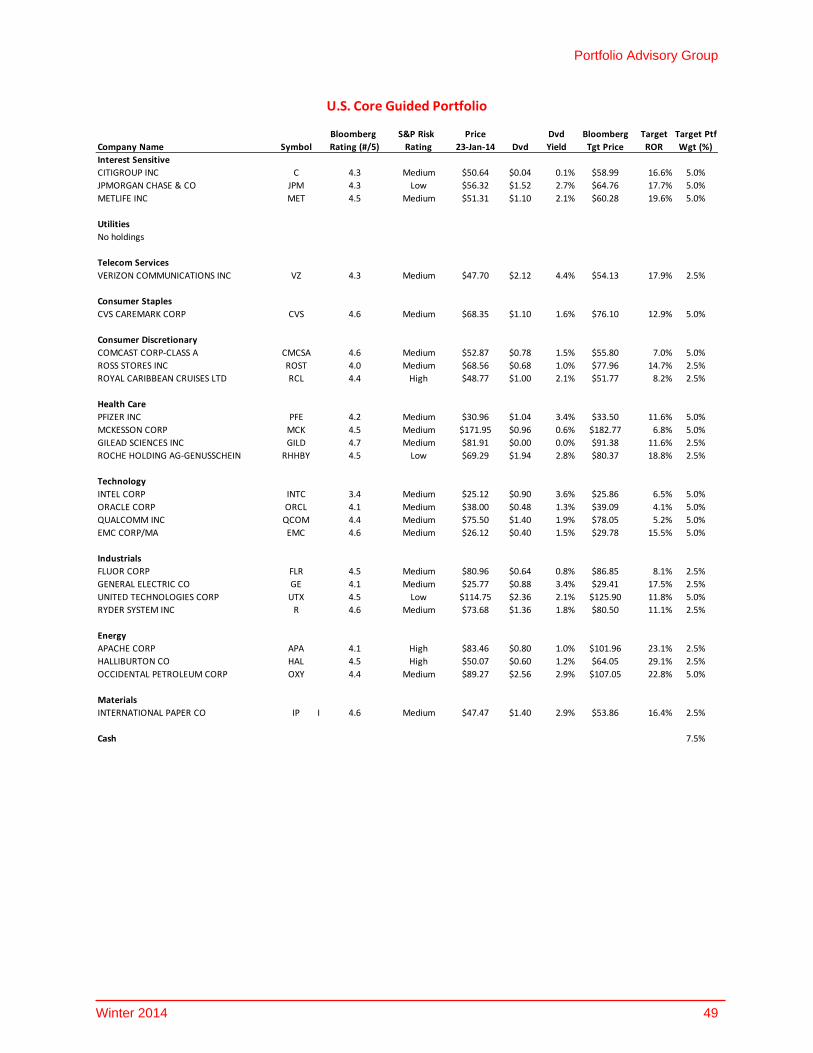

U.S. Core 45

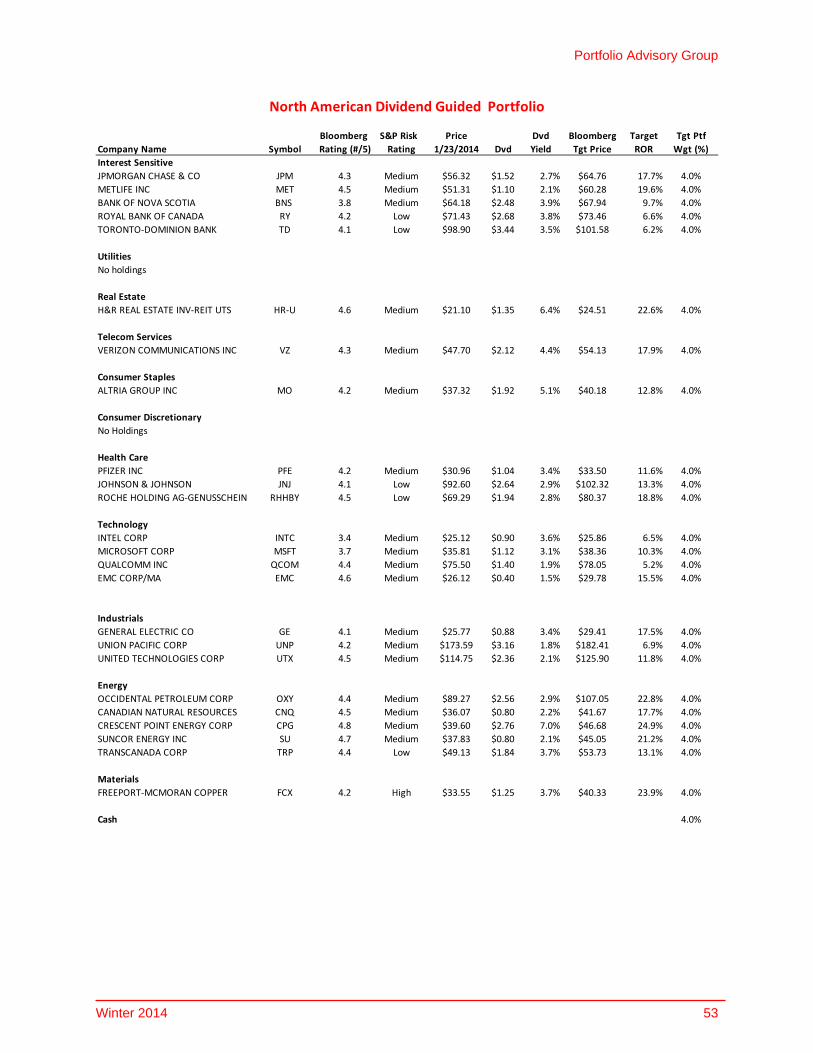

North American Core 50

Core-Plus Fixed Income 54

Portfolio Advisory Group

Winter 2014 1

Executive Summary Q4/13 Quarterly Comments Shane Jones — Chief Investment Officer & Co-Head, Portfolio Advisory Group

The fourth quarter of 2013 was an excellent quarter in equity markets although markets are typically strong as we head into the year-end period, this one was very strong. Mr. Bernanke finally put the pin in and started the highly anticipated “tapering of QE3” with a reduction in bond purchases from $85 billion per month to $75 billion per month. At the present time it is expected that the Federal Reserve will reduce at $10 billion per meeting which are every 6 weeks and this will then bring the quantitative easing to an end in the latter part of 2014. However, economic conditions will drive these decisions so any further tapering will be data dependent. Economic statistics picked up pace in the fourth quarter with job creation better than expected and an increase in Gross Domestic Output, these stronger than expected numbers were critical in the Federal Reserve decisions although inflation does remain subdued. After many quarters of low volume trading we actually saw a decent increase in market volumes which were a catalyst for the better tone in the markets as Fund Managers positioned their portfolios to be overweight equities and underweight bonds as the equity markets continued to produce outstanding results. Bond Markets also put in a decent performance for the quarter considering the market environment as markets remained volatile around the potential for the aforementioned tapering of QE3. 10 Year US Treasury Bonds appear to be capped at around the 3% level at the present time and remain in a very tight trading range of 2.8% to 3.0%. As we enter the 1st quarter of the New Year we finally have a long awaited budget agreement however the parties still have to agree on the debt ceiling issue which comes up for debate in February and could cause further disruption in the markets.

Looking at North American Equity markets both Canada and the US performed very well with Total Returns of 7.28% and 10.33% respectively. As mentioned volumes improved dramatically throughout the quarter with equities being purchased at a healthy pace pushing US stock valuations to very high levels. When looking at the breakdown of sectors on the S&P500 that gained or lost in the quarter the gains were paced by an almost 40% return in the Oil and Gas refinery stocks followed by a 30% gain in Aluminum stocks. On the opposite end we saw big losses for Gold stocks of -18% as the precious metal continued to lose faith with investors. Looking at the same statistics for Canada and using the 10 sectors Industrials, Healthcare and Financials led the groups with gains of 15.8%, 13.8% and 9.1% respectively, in fact all sub-sectors produced positive performance with the exception of Materials which was dragged lower by the continuing poor performance of Gold stocks. In North American fixed income markets the focus remained on the Federal Reserve and their tapering of QE3 policy (when, why and how much), this kept markets uncertain and we saw yields trade in a tight range between 2.75% and 3%. Tapering did start in December and the announcement of further tapering is expected in late January. However, any further tapering of bond purchases will become very data dependent and the Federal Reserve will be looking for better economic statistics in the coming months such as lower unemployment and GDP growth to signal that the US economy is on track for a full recovery. We do not expect any changes to official interest rates in North America in 2014.

In Europe, equity markets performed very well as signs of a recovery are beginning to take shape across the EuroZone with the exception of France whose high tax rates are beginning to really hurt economic growth. We are starting to slow but sure gains in Spain and Italy while Germany and the Benelux countries continue to perform well from an economic standpoint. The UK is also seeing stronger than expected economic growth but most of the gains appear to be in the Southern regions of the country which has a very close proximity to the recovering European markets. The DAX in Germany gained 11.1%, the CAC in France added 3.7% while the FTSE in the UK added 4.4%. Ireland has emerged from its IMF/European austerity controls and the hope is that Portugal will emerge from under the same measures in the next few years as the economic recovery there takes shape. European markets are poised to perform well in 2014 and it’s an area of focus for many investors including ourselves.

Investment Portfolio Quarterly

2

As we look at Asia markets we see very different performance in the 2 major markets as Japan performed extremely well gaining 12.7% on a weak currency that really helping this exporting nation. In contrast we saw the Shanghai Market lose 2.7% as the economy struggles to gain traction and move back above the 8% growth level. Overnight money rates have also been a drag on economic growth and the markets as liquidity conditions remain very tight and the shadow banking market continues to be problematic. We still believe that with the US economy grinding higher and the European economy looking to have bottomed that this will bode well for the Chinese economy as we move further into 2014. If we are correct we expect that this will have a positive impact on Commodity markets and the Canadian equity markets.

In Commodities and Currencies we have once again had quite the mixed picture with Gold and Oil performing poorly while Natural Gas and the US Dollar performed better than expected especially Nat Gas as colder than expected weather conditions drove the price 24% higher in the US. Copper gained marginally while agricultural commodities were weak due to a stronger than expected crop yield especially Corn and Wheat. The US Dollar gained against most other major currencies (Japanese Yen was the exception) as the uncertainty around the Federal Reserve actions and the debt ceiling debates lifted the weight on the currency. The Canadian Dollar had a poor quarter as expectations of a move in official interest rates from the Bank of Canada has played into many speculators minds. We will await the economic update from Mr. Poloz in late January to see if there is a shift in policy from the central bank. This weakness in the Canadian Dollar has gathered momentum in early January and the currency is pushing towards $0.90 to the US Dollar. Oil has weakened from its recent highs on an agreement with Iran to reduce sanctions and some easing of tensions in Egypt and Libya. The Syria situation is still evolving with peace talks expected soon.

As we start the New Year of 2014 things appear to be a little calmer around the world. We have a budget agreement in Washington but still face a debt ceiling debate. In Europe, Germany has formed a grand coalition which should help keep that economy on track and help others in the region. In the Middle-East tensions appeared to have eased a little in the region with the exception of Syria and we have an agreement with Iran on Uranium enrichment. Asia economies are still slower than expected however we feel that there will be a pick-up in Chinese economic activity post the Chinese New Year in early February which should have a positive impact on the whole region. Having said all that and we move back to more fundamental investing rather than looking at geopolitical events we could see more volatility than expected as Fund Managers look to position themselves in the right markets and right stocks for 2014.

Here are some of the highlights of what our Winter 2014 Investment Portfolio Quarterly (IPQ) offers:

Scotiabank GBM Portfolio Strategy Team provides their Portfolio Strategy Outlook for 2014 report.

Scotiabank Economist Derek Holt discusses his outlook for the US economy and his view that this recovery has just begun and believes in a fairly bullish outlook.

Himalaya Jain and Warren Hastings provide their Top 10 Canadian Stock Picks for 2014 and provide an overview of the performance of the Top Picks from 2013.

Marco Martin and Caroline Escott provide their Top 10 US Stock Picks for 2014 and also an overview of the performance of the top picks from 2013.

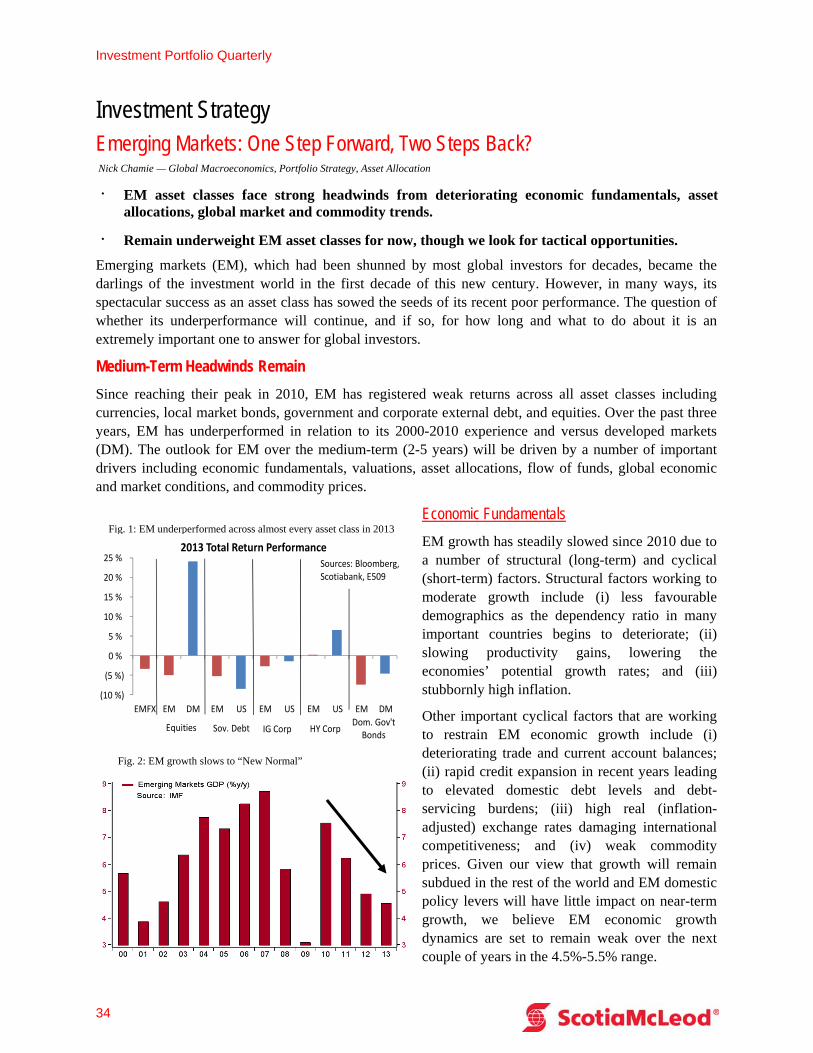

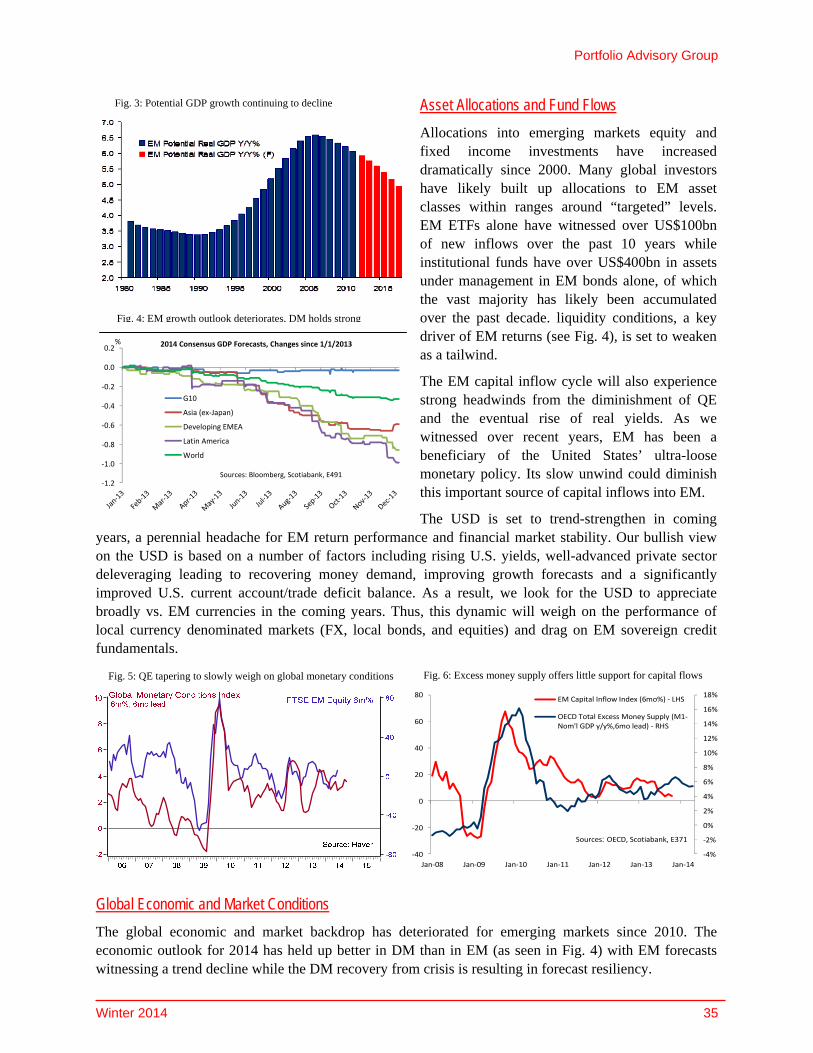

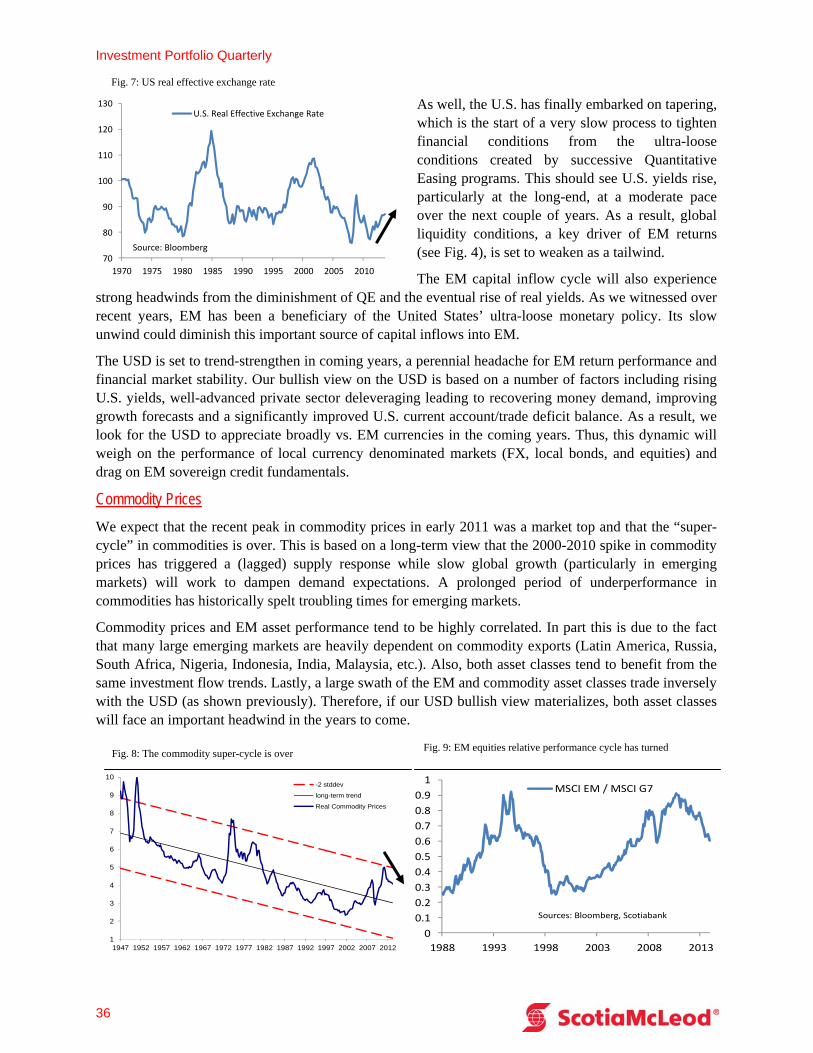

Nick Chamie, IPAG, provides his outlook for emerging markets.

Caroline Escott, Warren Hastings, Tim Vlahopoulos and Andrew Mystic provide their quarterly review and commentary on the performance of the Guided Portfolios.

We hope you all enjoy the Winter 2014 version of the IPQ and recommend you contact your ScotiaMcLeod Advisor with regard to any ideas presented here which interest you, or to review your investment portfolio

Portfolio Advisory Group

Winter 2014 3

Exhibit 1: Global Equity Returns (CAD) – December & 2013 (price only)

-20% -10% 0% 10% 20% 30% 40% 50%

-20% -10% 0% 10% 20% 30% 40% 50%

U.S. (S&P 500)

Germany (DAX)

Japan (Topix)

MSCI AC World

U.K. (FTSE)

Hong Kong

Canada (TSX)

MSCI China

Australia (ASX)

MSCI Mexico

MSCI EM

MSCI India

MSCI LatAm

MSCI Brazil

December

2013

Source: Scotiabank GBM Portfolio Strategy, Bloomberg.

Exhibit 2: Global Equity Returns (USD) – December & 2013 (price only)

-30% -20% -10% 0% 10% 20% 30% 40%

-30% -20% -10% 0% 10% 20% 30% 40%

U.S. (S&P 500)

Germany (DAX)

Japan (Topix)

MSCI AC World

U.K. (FTSE)

Hong Kong

Canada (TSX)

MSCI China

Australia (ASX)

MSCI Mexico

MSCI EM

MSCI India

MSCI LatAm

MSCI Brazil

December

2013

Source: Scotiabank GBM Portfolio Strategy, Bloomberg.

Portfolio Strategy Normalization Year Vincent Delisle, CFA — Portfolio Strategist, Scotiabank Global Banking and Markets.

Hugo Ste-Marie, CFA – Portfolio Strategist, Scotiabank Global Banking and Markets.

A BANNER YEAR FOR DM IN 2013, LACKLUSTRE FOR EM

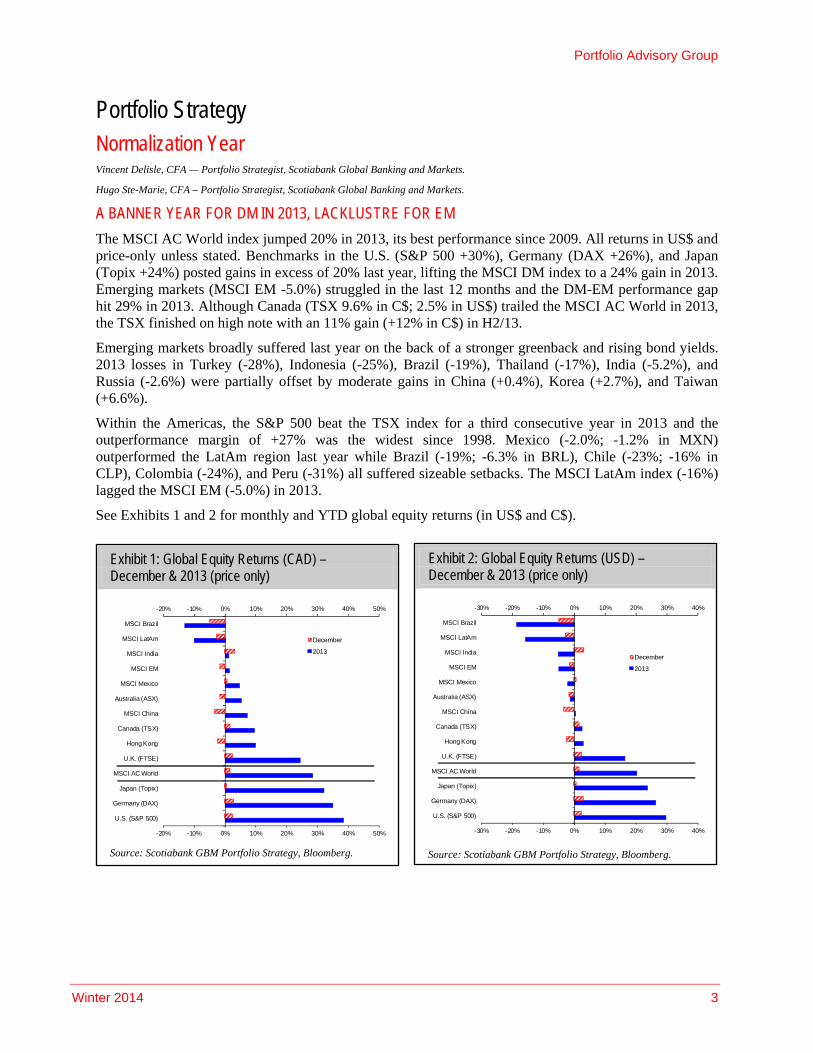

The MSCI AC World index jumped 20% in 2013, its best performance since 2009. All returns in US$ and price-only unless stated. Benchmarks in the U.S. (S&P 500 +30%), Germany (DAX +26%), and Japan (Topix +24%) posted gains in excess of 20% last year, lifting the MSCI DM index to a 24% gain in 2013. Emerging markets (MSCI EM -5.0%) struggled in the last 12 months and the DM-EM performance gap hit 29% in 2013. Although Canada (TSX 9.6% in C$; 2.5% in US$) trailed the MSCI AC World in 2013, the TSX finished on high note with an 11% gain (+12% in C$) in H2/13.

Emerging markets broadly suffered last year on the back of a stronger greenback and rising bond yields. 2013 losses in Turkey (-28%), Indonesia (-25%), Brazil (-19%), Thailand (-17%), India (-5.2%), and Russia (-2.6%) were partially offset by moderate gains in China (+0.4%), Korea (+2.7%), and Taiwan (+6.6%).

Within the Americas, the S&P 500 beat the TSX index for a third consecutive year in 2013 and the outperformance margin of +27% was the widest since 1998. Mexico (-2.0%; -1.2% in MXN) outperformed the LatAm region last year while Brazil (-19%; -6.3% in BRL), Chile (-23%; -16% in CLP), Colombia (-24%), and Peru (-31%) all suffered sizeable setbacks. The MSCI LatAm index (-16%) lagged the MSCI EM (-5.0%) in 2013.

See Exhibits 1 and 2 for monthly and YTD global equity returns (in US$ and C$).

Investment Portfolio Quarterly

4

Exhibit 3: Currencies & Commodities: December & 2013

-40% -30% -20% -10% 0% 10% 20% 30%

-40% -30% -20% -10% 0% 10% 20% 30%

WTI

Brent

Natural Gas

Gasoline

Gold

Silver

CRB Index

Copper

US$ per C$

US$ per A$

US$ per Real

US$ per PesoDecember

2013

Source: Scotiabank GBM Portfolio Strategy, Bloomberg.

Exhibit 4: Bonds, Yields & Currencies: December & 2013

-75 -50 -25 0 25 50 75 100 125

-30% -20% -10% 0% 10% 20% 30% 40% 50%

US$ per Euro

US$ per Pound

US$ per Yen

US$ per Swiss Franc

DXY Index

U.S. LT Bonds Return

CDA LT Bonds Return

DEX Universe Index

Can. Yield Curve

Can. 10-yr

U.S. Yield Curve

U.S. 10-yr

U.S. Spreads (BAA)

December

2013

Source: Scotiabank GBM Portfolio Strategy, Bloomberg.

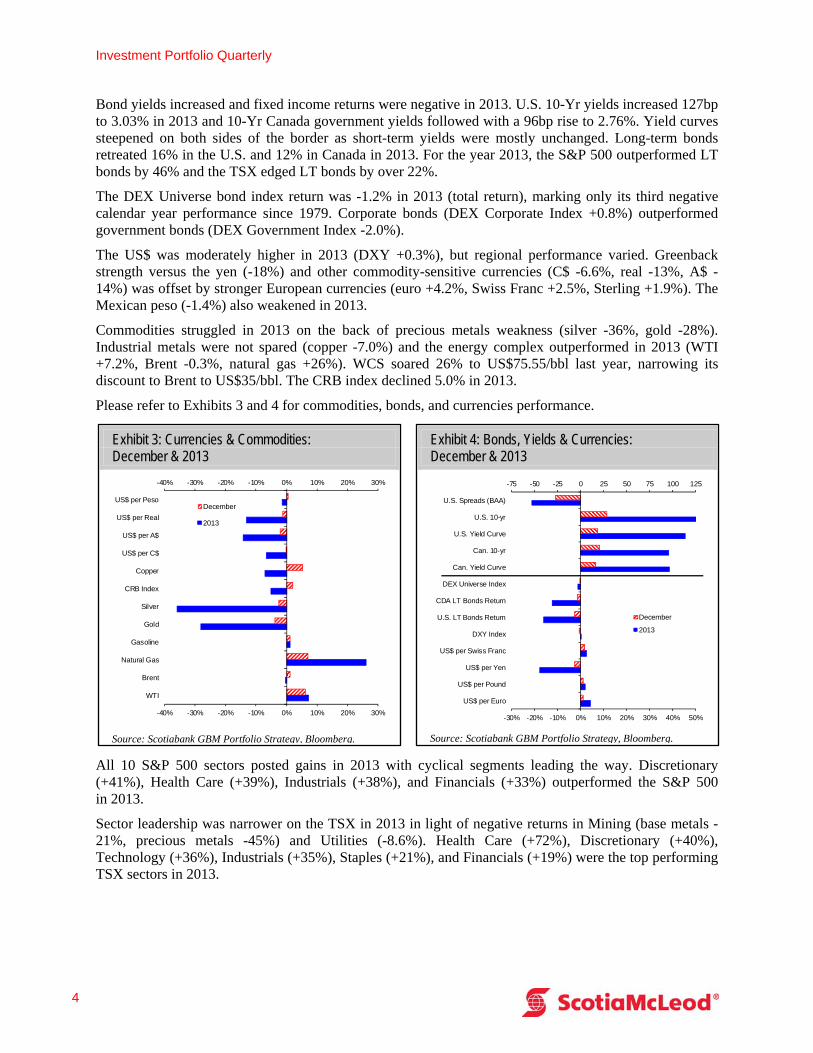

Bond yields increased and fixed income returns were negative in 2013. U.S. 10-Yr yields increased 127bp to 3.03% in 2013 and 10-Yr Canada government yields followed with a 96bp rise to 2.76%. Yield curves steepened on both sides of the border as short-term yields were mostly unchanged. Long-term bonds retreated 16% in the U.S. and 12% in Canada in 2013. For the year 2013, the S&P 500 outperformed LT bonds by 46% and the TSX edged LT bonds by over 22%.

The DEX Universe bond index return was -1.2% in 2013 (total return), marking only its third negative calendar year performance since 1979. Corporate bonds (DEX Corporate Index +0.8%) outperformed government bonds (DEX Government Index -2.0%).

The US$ was moderately higher in 2013 (DXY +0.3%), but regional performance varied. Greenback strength versus the yen (-18%) and other commodity-sensitive currencies (C$ -6.6%, real -13%, A$ -14%) was offset by stronger European currencies (euro +4.2%, Swiss Franc +2.5%, Sterling +1.9%). The Mexican peso (-1.4%) also weakened in 2013.

Commodities struggled in 2013 on the back of precious metals weakness (silver -36%, gold -28%). Industrial metals were not spared (copper -7.0%) and the energy complex outperformed in 2013 (WTI +7.2%, Brent -0.3%, natural gas +26%). WCS soared 26% to US$75.55/bbl last year, narrowing its discount to Brent to US$35/bbl. The CRB index declined 5.0% in 2013.

Please refer to Exhibits 3 and 4 for commodities, bonds, and currencies performance.

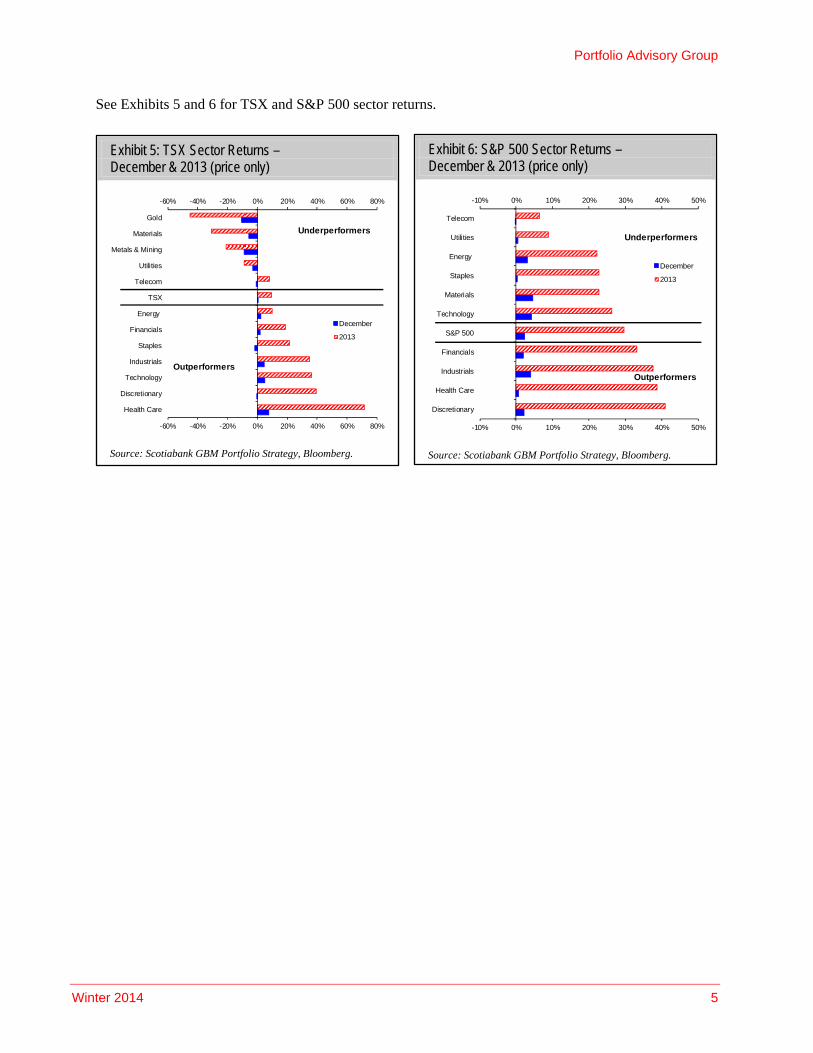

All 10 S&P 500 sectors posted gains in 2013 with cyclical segments leading the way. Discretionary (+41%), Health Care (+39%), Industrials (+38%), and Financials (+33%) outperformed the S&P 500 in 2013.

Sector leadership was narrower on the TSX in 2013 in light of negative returns in Mining (base metals -21%, precious metals -45%) and Utilities (-8.6%). Health Care (+72%), Discretionary (+40%), Technology (+36%), Industrials (+35%), Staples (+21%), and Financials (+19%) were the top performing TSX sectors in 2013.

Portfolio Advisory Group

Winter 2014 5

Exhibit 5: TSX Sector Returns – December & 2013 (price only)

-60% -40% -20% 0% 20% 40% 60% 80%

-60% -40% -20% 0% 20% 40% 60% 80%

Health Care

Discretionary

Technology

Industrials

Staples

Financials

Energy

TSX

Telecom

Utilities

Metals & Mining

Materials

Gold

December

2013

Underperformers

Outperformers

Source: Scotiabank GBM Portfolio Strategy, Bloomberg.

Exhibit 6: S&P 500 Sector Returns – December & 2013 (price only)

-10% 0% 10% 20% 30% 40% 50%

-10% 0% 10% 20% 30% 40% 50%

Discretionary

Health Care

Industrials

Financials

S&P 500

Technology

Materials

Staples

Energy

Utilities

Telecom

December

2013

Underperformers

Outperformers

Source: Scotiabank GBM Portfolio Strategy, Bloomberg.

See Exhibits 5 and 6 for TSX and S&P 500 sector returns.

Investment Portfolio Quarterly

6

Exhibit 7: World Manufacturing PMI and GDP Growth (1997-2013)

2.9%

3.5%3.6%

-1%

0%

1%

2%

3%

4%

5%

6%

35

40

45

50

55

60

65

70

Dec

-97

Dec

-98

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Global Manufacturing PMI - LHS

IMF World Real GDP Growth - RHS

Source: Scotiabank GBM Portfolio Strategy; Bloomberg; Scotiabank Economics estimates.

Exhibit 8: Global Manufacturing PMI

53.3

57.0

52.7

54.3

57.3

55.2

50.8 50.5

46

48

50

52

54

56

58

World U.S. Eurozone Germany U.K. Japan China* Brazil

2012 Average

H1/13 Average

H2/13 Average

December

* China PMI: Average of Government PMI and Markit/HSBC PMI. Source: Scotiabank GBM Portfolio Strategy; Bloomberg.

Global Portfolio Strategy Outlook – 2014 THE 2014 GAME PLAN

As we table our 2014 investment strategy outlook, we expect most of the themes that helped investors outperform in recent years (i.e., equity overweight since 2009; DM over EM and underweight resources since 2011; and interest-sensitive underweight since Q2/13) will play out in 2014. However, considering how overextended some of these trades have become, our focus in coming months will be on identifying potential shifts that could trigger a leadership change. For now, our macroeconomic thesis and our tactical indicators point to extending the 2013 game plan into 2014. Asset mix is a dynamic process and investors should be on the lookout for reversals once U.S. Federal Reserve tapering goes from fear to reality. Five years after the end of the global recession and with the S&P 500 up 173% since Q1/09, many segments of the market have not fully normalized. Sector correlations remain elevated, consumer confidence is hovering around 16% below the historical average, public equity weightings are at the low end of their 18-year range, and real interest rates remain low. With the pending shift in Fed policy, the normalization trend could accelerate in 2014.

THE MACRO VIEW FOR 2014

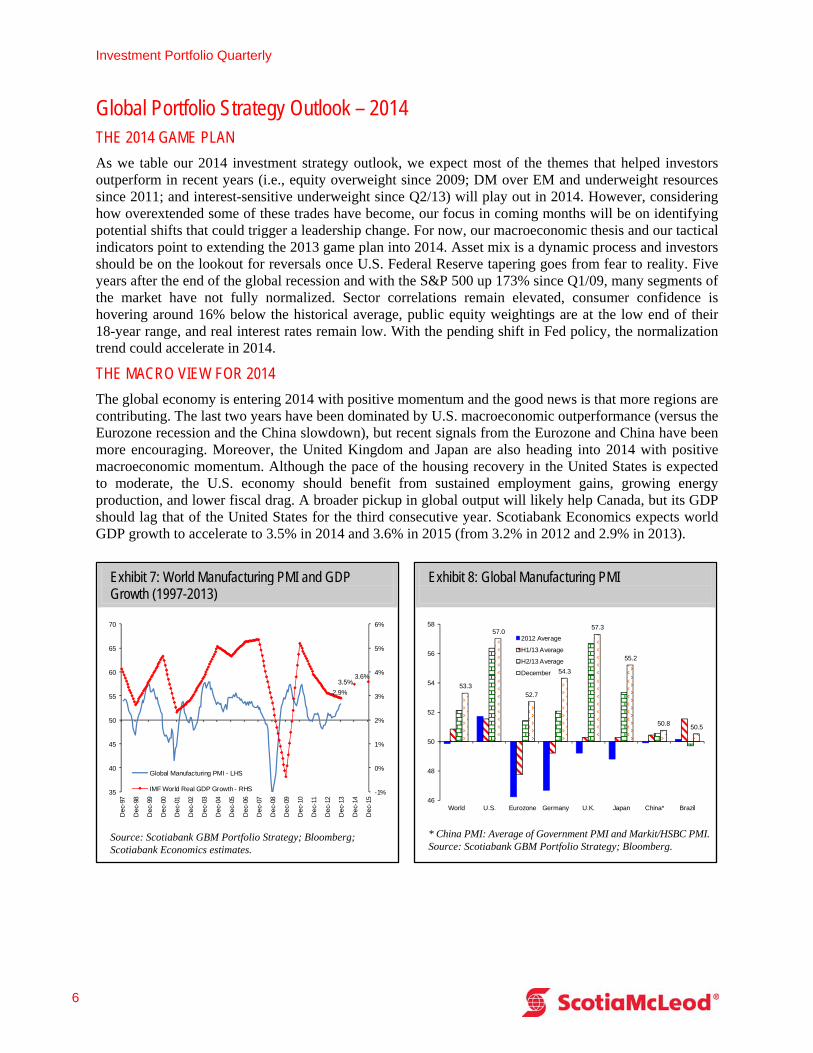

The global economy is entering 2014 with positive momentum and the good news is that more regions are contributing. The last two years have been dominated by U.S. macroeconomic outperformance (versus the Eurozone recession and the China slowdown), but recent signals from the Eurozone and China have been more encouraging. Moreover, the United Kingdom and Japan are also heading into 2014 with positive macroeconomic momentum. Although the pace of the housing recovery in the United States is expected to moderate, the U.S. economy should benefit from sustained employment gains, growing energy production, and lower fiscal drag. A broader pickup in global output will likely help Canada, but its GDP should lag that of the United States for the third consecutive year. Scotiabank Economics expects world GDP growth to accelerate to 3.5% in 2014 and 3.6% in 2015 (from 3.2% in 2012 and 2.9% in 2013).

Portfolio Advisory Group

Winter 2014 7

Exhibit 9: U.S. 10-Year Yield, Jobless Claims, and Consumer Confidence (1998-2013)

0

20

40

60

80

100

120

140

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

Jan-

15

U.S. 10-Yr Yield - LHS

Initial Jobless Claims (Inverted,Normalized) - RHS

Consumer Confidence(Normalized) - RHS

%

Source: Scotiabank GBM Portfolio Strategy; Bloomberg.

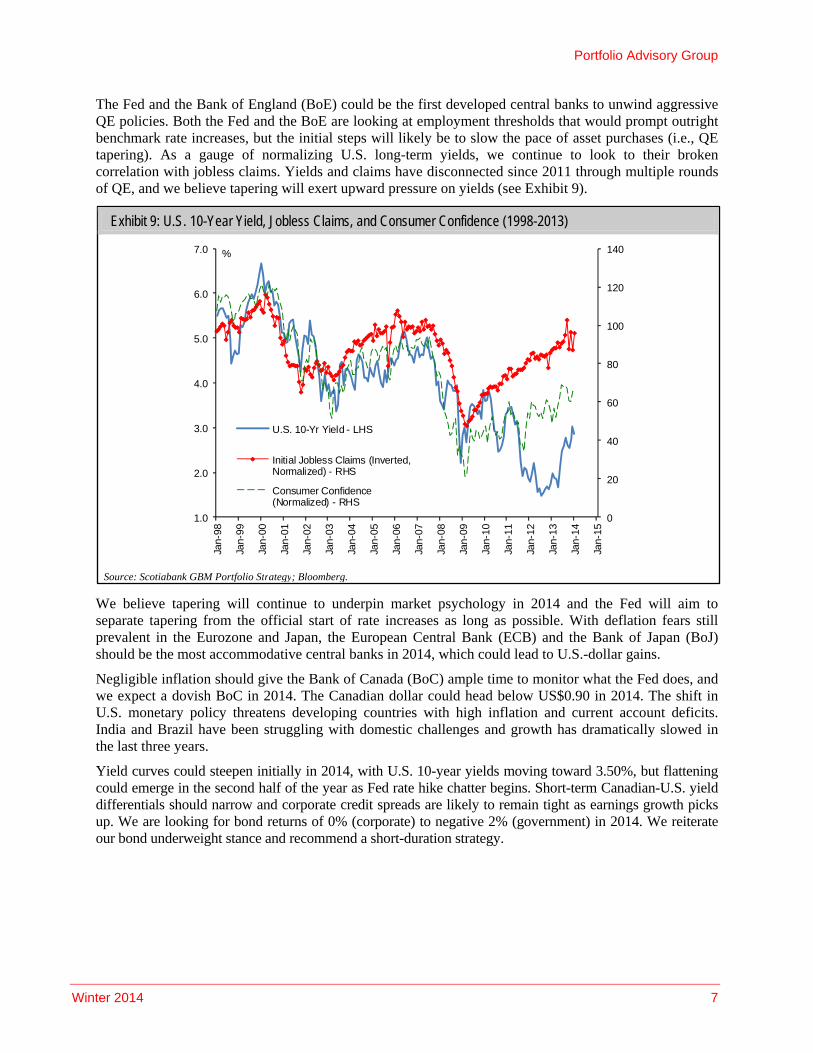

The Fed and the Bank of England (BoE) could be the first developed central banks to unwind aggressive QE policies. Both the Fed and the BoE are looking at employment thresholds that would prompt outright benchmark rate increases, but the initial steps will likely be to slow the pace of asset purchases (i.e., QE tapering). As a gauge of normalizing U.S. long-term yields, we continue to look to their broken correlation with jobless claims. Yields and claims have disconnected since 2011 through multiple rounds of QE, and we believe tapering will exert upward pressure on yields (see Exhibit 9).

We believe tapering will continue to underpin market psychology in 2014 and the Fed will aim to separate tapering from the official start of rate increases as long as possible. With deflation fears still prevalent in the Eurozone and Japan, the European Central Bank (ECB) and the Bank of Japan (BoJ) should be the most accommodative central banks in 2014, which could lead to U.S.-dollar gains.

Negligible inflation should give the Bank of Canada (BoC) ample time to monitor what the Fed does, and we expect a dovish BoC in 2014. The Canadian dollar could head below US$0.90 in 2014. The shift in U.S. monetary policy threatens developing countries with high inflation and current account deficits. India and Brazil have been struggling with domestic challenges and growth has dramatically slowed in the last three years.

Yield curves could steepen initially in 2014, with U.S. 10-year yields moving toward 3.50%, but flattening could emerge in the second half of the year as Fed rate hike chatter begins. Short-term Canadian-U.S. yield differentials should narrow and corporate credit spreads are likely to remain tight as earnings growth picks up. We are looking for bond returns of 0% (corporate) to negative 2% (government) in 2014. We reiterate our bond underweight stance and recommend a short-duration strategy.

Investment Portfolio Quarterly

8

Exhibit 10: S&P 500 Earnings Growth and Yield Curve (1954-2013)

-50%

-25%

0%

25%

50%

75%

100%

125%

-200

-100

0

100

200

300

400

500

Q1 1

954

Q1 1

957

Q1 1

960

Q1 1

963

Q1 1

966

Q1 1

969

Q1 1

972

Q1 1

975

Q1 1

978

Q1 1

981

Q1 1

984

Q1 1

987

Q1 1

990

Q1 1

993

Q1 1

996

Q1 1

999

Q1 2

002

Q1 2

005

Q1 2

008

Q1 2

011

Q1 2

014

NBER Recessions

Yield Curve (U.S. Gov. 10-Yrless 3-M) - LHSS&P 500 YoY EPS Growth(T+18M) - RHS

Source: Scotiabank GBM Portfolio Strategy; Bloomberg; S&P.

Exhibit 11: U.S.-Canada Bond Yield Spreads

-90

-60

-30

0

30

60

90

120

-90

-60

-30

0

30

60

90

120

Jan

-07

Jul-0

7

Jan

-08

Jul-0

8

Jan

-09

Jul-0

9

Jan

-10

Jul-1

0

Jan

-11

Jul-1

1

Jan

-12

Jul-1

2

Jan

-13

Jul-1

3

Jan

-14

Jul-1

4

10-Yr Bond Spread U.S. less Canada (bp)

2-Yr Bond Spread U.S. less Canada (bp)

Source: Scotiabank GBM Portfolio Strategy; Bloomberg.

Exhibit 12: Scotiabank GBM Financial Forecasts

Forecasts 2011 2012 2013E 2014E 2015E

S&P/TSX 11,955 12,434 13,622 14,200

EPS 833 818 833 900 950

S&P 500 1,258 1,426 1,848 1,950

EPS 96 99 108 117 125Mexico Bolsa 37,078 43,706 42,727 45,000

Brazil Bovespa 56,754 60,952 51,507 56,000

Chile IPSA 4,178 4,301 3,699 4,100

Equity

Source: Scotiabank GBM Portfolio Strategy estimates.

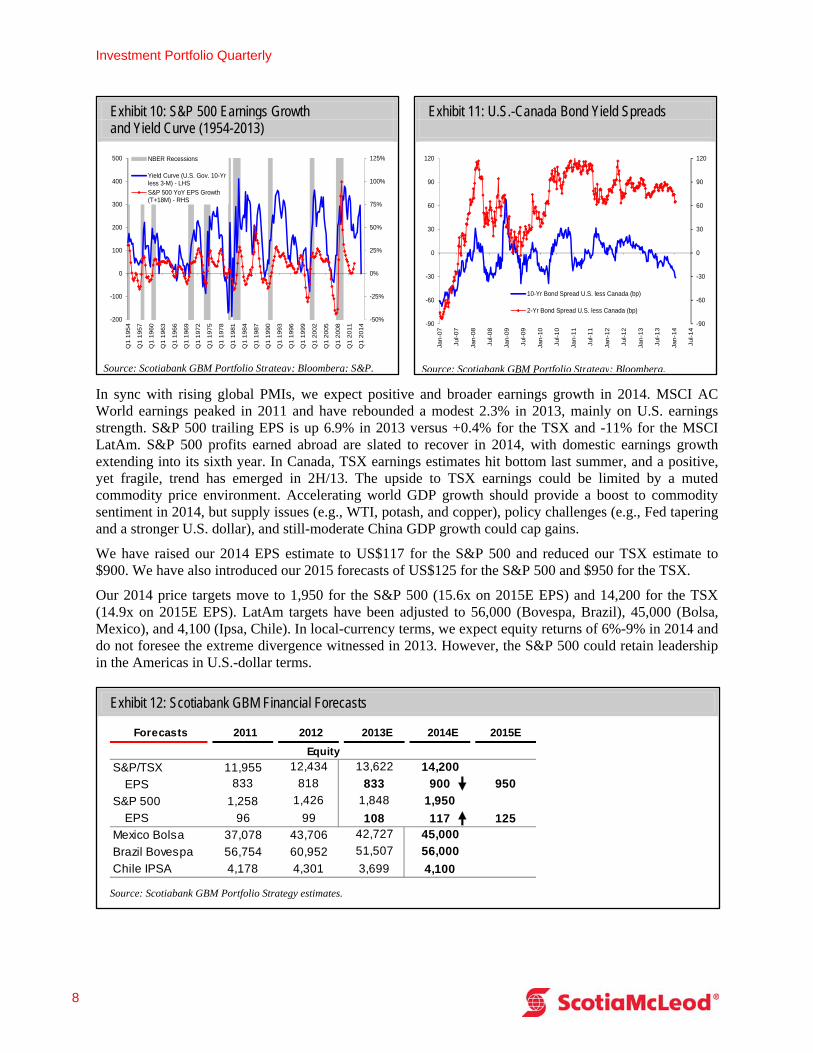

In sync with rising global PMIs, we expect positive and broader earnings growth in 2014. MSCI AC World earnings peaked in 2011 and have rebounded a modest 2.3% in 2013, mainly on U.S. earnings strength. S&P 500 trailing EPS is up 6.9% in 2013 versus +0.4% for the TSX and -11% for the MSCI LatAm. S&P 500 profits earned abroad are slated to recover in 2014, with domestic earnings growth extending into its sixth year. In Canada, TSX earnings estimates hit bottom last summer, and a positive, yet fragile, trend has emerged in 2H/13. The upside to TSX earnings could be limited by a muted commodity price environment. Accelerating world GDP growth should provide a boost to commodity sentiment in 2014, but supply issues (e.g., WTI, potash, and copper), policy challenges (e.g., Fed tapering and a stronger U.S. dollar), and still-moderate China GDP growth could cap gains.

We have raised our 2014 EPS estimate to US$117 for the S&P 500 and reduced our TSX estimate to $900. We have also introduced our 2015 forecasts of US$125 for the S&P 500 and $950 for the TSX.

Our 2014 price targets move to 1,950 for the S&P 500 (15.6x on 2015E EPS) and 14,200 for the TSX (14.9x on 2015E EPS). LatAm targets have been adjusted to 56,000 (Bovespa, Brazil), 45,000 (Bolsa, Mexico), and 4,100 (Ipsa, Chile). In local-currency terms, we expect equity returns of 6%-9% in 2014 and do not foresee the extreme divergence witnessed in 2013. However, the S&P 500 could retain leadership in the Americas in U.S.-dollar terms.

Portfolio Advisory Group

Winter 2014 9

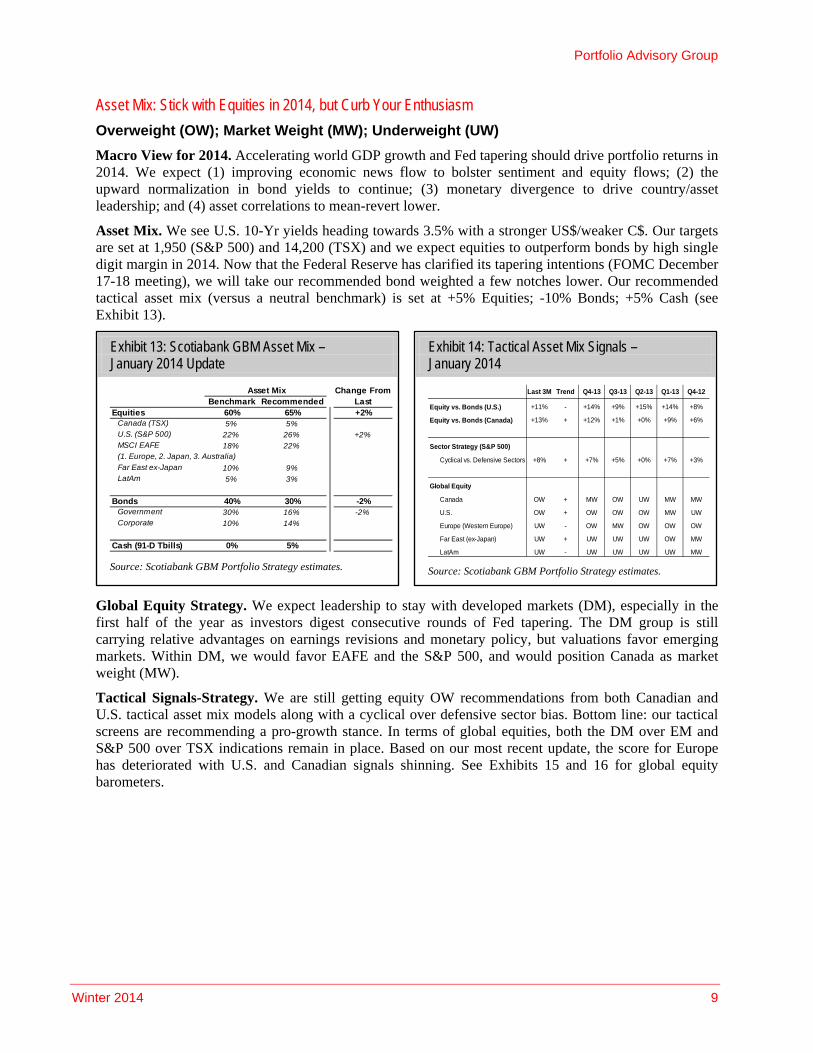

Exhibit 13: Scotiabank GBM Asset Mix – January 2014 Update

Change FromBenchmark Recommended Last

Equities 60% 65% +2% Canada (TSX) 5% 5% U.S. (S&P 500) 22% 26% +2% MSCI EAFE 18% 22% (1. Europe, 2. Japan, 3. Australia)

Far East ex-Japan 10% 9% LatAm 5% 3%

Bonds 40% 30% -2% Government 30% 16% -2% Corporate 10% 14%

Cash (91-D Tbills) 0% 5%

Asset Mix

Source: Scotiabank GBM Portfolio Strategy estimates.

Exhibit 14: Tactical Asset Mix Signals – January 2014

Last 3M Trend Q4-13 Q3-13 Q2-13 Q1-13 Q4-12

Equity vs. Bonds (U.S.) +11% - +14% +9% +15% +14% +8%

Equity vs. Bonds (Canada) +13% + +12% +1% +0% +9% +6%

Sector Strategy (S&P 500)

Cyclical vs. Defensive Sectors +8% + +7% +5% +0% +7% +3%

Global Equity

Canada OW + MW OW UW MW MW

U.S. OW + OW OW OW MW UW

Europe (Western Europe) UW - OW MW OW OW OW

Far East (ex-Japan) UW + UW UW UW OW MW

LatAm UW - UW UW UW UW MW

Source: Scotiabank GBM Portfolio Strategy estimates.

Asset Mix: Stick with Equities in 2014, but Curb Your Enthusiasm

Overweight (OW); Market Weight (MW); Underweight (UW)

Macro View for 2014. Accelerating world GDP growth and Fed tapering should drive portfolio returns in 2014. We expect (1) improving economic news flow to bolster sentiment and equity flows; (2) the upward normalization in bond yields to continue; (3) monetary divergence to drive country/asset leadership; and (4) asset correlations to mean-revert lower.

Asset Mix. We see U.S. 10-Yr yields heading towards 3.5% with a stronger US$/weaker C$. Our targets are set at 1,950 (S&P 500) and 14,200 (TSX) and we expect equities to outperform bonds by high single digit margin in 2014. Now that the Federal Reserve has clarified its tapering intentions (FOMC December 17-18 meeting), we will take our recommended bond weighted a few notches lower. Our recommended tactical asset mix (versus a neutral benchmark) is set at +5% Equities; -10% Bonds; +5% Cash (see Exhibit 13).

Global Equity Strategy. We expect leadership to stay with developed markets (DM), especially in the first half of the year as investors digest consecutive rounds of Fed tapering. The DM group is still carrying relative advantages on earnings revisions and monetary policy, but valuations favor emerging markets. Within DM, we would favor EAFE and the S&P 500, and would position Canada as market weight (MW).

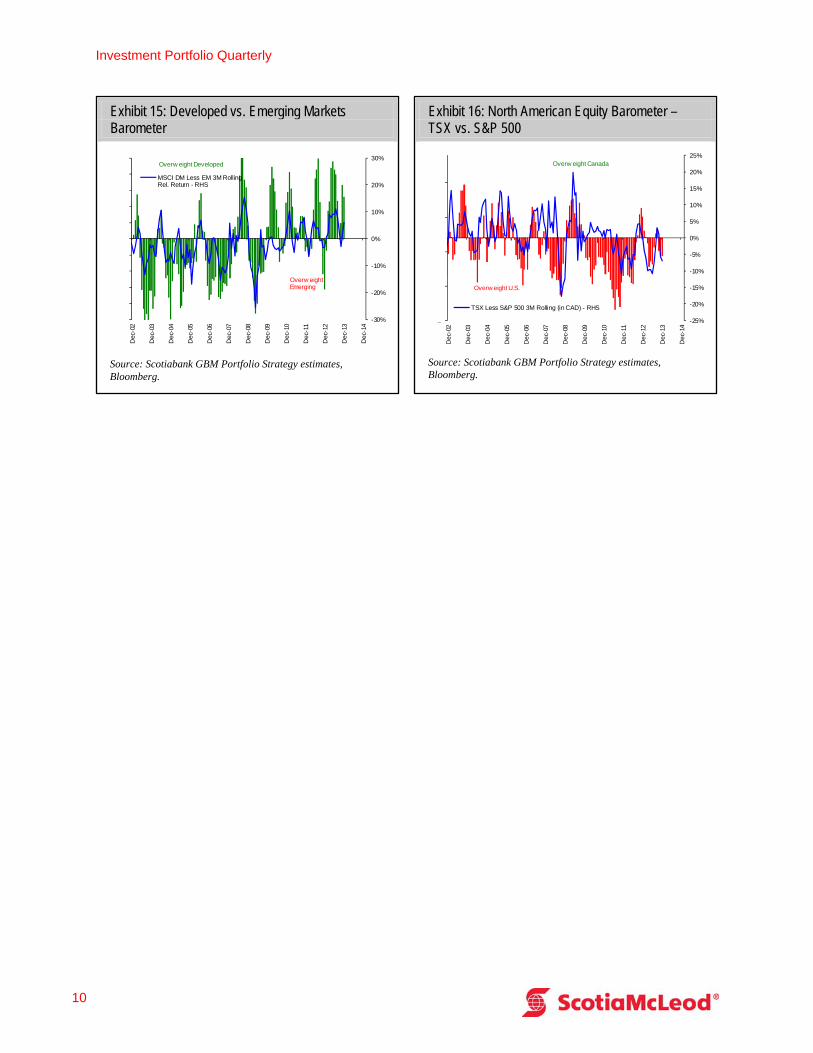

Tactical Signals-Strategy. We are still getting equity OW recommendations from both Canadian and U.S. tactical asset mix models along with a cyclical over defensive sector bias. Bottom line: our tactical screens are recommending a pro-growth stance. In terms of global equities, both the DM over EM and S&P 500 over TSX indications remain in place. Based on our most recent update, the score for Europe has deteriorated with U.S. and Canadian signals shinning. See Exhibits 15 and 16 for global equity barometers.

Investment Portfolio Quarterly

10

Exhibit 15: Developed vs. Emerging Markets Barometer

-30%

-20%

-10%

0%

10%

20%

30%

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

MSCI DM Less EM 3M RollingRel. Return - RHS

Overw eight Emerging

Overw eight Developed

Source: Scotiabank GBM Portfolio Strategy estimates, Bloomberg.

Exhibit 16: North American Equity Barometer – TSX vs. S&P 500

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

-1

-1

0

0

1

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

TSX Less S&P 500 3M Rolling (in CAD) - RHS

Overw eight U.S.

Overw eight Canada

Source: Scotiabank GBM Portfolio Strategy estimates, Bloomberg.

Portfolio Advisory Group

Winter 2014 11

Exhibit 2: Still A Young Expansion

Source: NBER, Scotiabank Economics.

Economic and Market Outlook

U.S. Economic Outlook: Enter the Bear Flattener Derek Holt, MA, MBA, CFA – Vice-President, Scotiabank Economics

Dov Zigler, MA – Scotiabank Economics

We view this recovery as having only just begun in earnest and believe in a fairly bullish outlook with upside risks to our growth and interest rate forecasts. In contrast to the tail risk offered up within the range of consensus opinions that the expansion is already growing old and threatens to turn south, we think the bigger tail risk to consensus forecast opinions over 2014-15 lies in the direction of a stronger-

than-expected U.S. recovery with Bloomberg’s consensus at 2.6% in 2014 and 3% growth in 2015.

As a consequence, whereas the past couple of years have been all about Treasury curve steepening to among the wider 10s minus 2s spreads on record, we view the next two years as being about a shift toward a bear flattener environment (Exhibit 1). Because we think the Fed’s forward rate guidance will be more directly challenged by markets going forward, we see the flatteners shown in Exhibit 1 as facing the risk of greater than forecast curve flattening.

Still A Young Expansion...

We start by rejecting the argument that this is becoming a lengthy expansion that risks running out of gas. True, at 55 months, the current U.S. economic expansion is already longer than any pre-WWII economic expansion and lies just a few months away from the average post-WWII expansion, but averages can be misleading.

There is no hard science on defining the lengths of business cycles such that citing the length of the current one as necessarily begetting weakness ahead is far too simplistic. Recall the famous quip from former Fed Chairman Alan Greenspan and pending Fed Chair Janet Yellen in the 1990s that “expansions don’t die of old age” as the expansion then continued until March 2001. The theory on business cycles will probably never be advanced enough to give us any hard and fast rules of thumb on factors driving the length of economic expansions.

It is also important to note that some of the expansions over the post-war period were uninspiring and skewed the sample lower. Take, for example, the brief expansion from August 1980 ending in June 1981 as the U.S. experienced back-to-back recessions in the early 1980s. Or take the recession of

April 1960 until February 1961 that followed the recession that ended in 1958. As Exhibit 2 demonstrates, however, no fewer than five expansion periods were longer than the current one to date. The granddaddy of them all was the one that ended in February 2001 and which lasted for 120 months — or more than twice as long as the current expansion — and before excessive leverage really distorted the next cycle. By comparison to these periods, we could easily have a long way to go yet.

Exhibit 1: On To The Bear Flattener?

Source: Bloomberg, Scotiabank Economics.

Investment Portfolio Quarterly

12

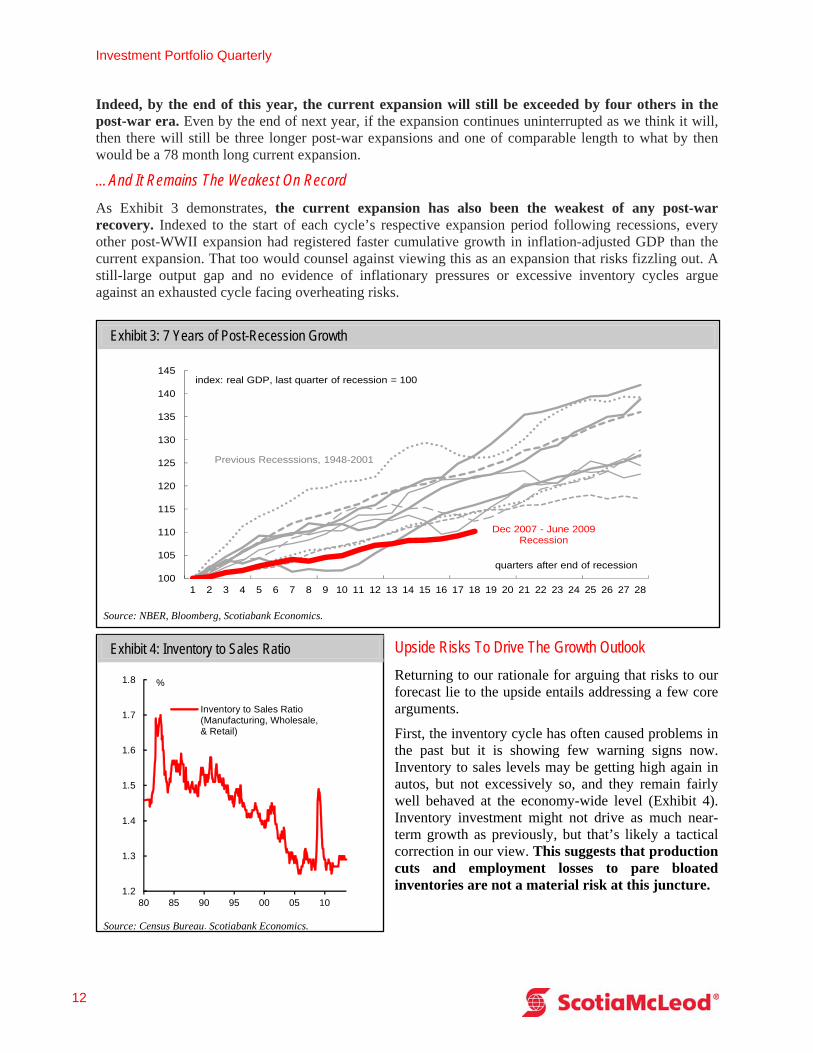

Exhibit 3: 7 Years of Post-Recession Growth

100

105

110

115

120

125

130

135

140

145

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28

index: real GDP, last quarter of recession = 100

Dec 2007 - June 2009 Recession

quarters after end of recession

Previous Recesssions, 1948-2001

Source: NBER, Bloomberg, Scotiabank Economics.

Exhibit 4: Inventory to Sales Ratio

1.2

1.3

1.4

1.5

1.6

1.7

1.8

80 85 90 95 00 05 10

Inventory to Sales Ratio(Manufacturing, Wholesale,& Retail)

%

Source: Census Bureau, Scotiabank Economics.

Indeed, by the end of this year, the current expansion will still be exceeded by four others in the post-war era. Even by the end of next year, if the expansion continues uninterrupted as we think it will, then there will still be three longer post-war expansions and one of comparable length to what by then would be a 78 month long current expansion.

…And It Remains The Weakest On Record

As Exhibit 3 demonstrates, the current expansion has also been the weakest of any post-war recovery. Indexed to the start of each cycle’s respective expansion period following recessions, every other post-WWII expansion had registered faster cumulative growth in inflation-adjusted GDP than the current expansion. That too would counsel against viewing this as an expansion that risks fizzling out. A still-large output gap and no evidence of inflationary pressures or excessive inventory cycles argue against an exhausted cycle facing overheating risks.

Upside Risks To Drive The Growth Outlook

Returning to our rationale for arguing that risks to our forecast lie to the upside entails addressing a few core arguments.

First, the inventory cycle has often caused problems in the past but it is showing few warning signs now. Inventory to sales levels may be getting high again in autos, but not excessively so, and they remain fairly well behaved at the economy-wide level (Exhibit 4). Inventory investment might not drive as much near-term growth as previously, but that’s likely a tactical correction in our view. This suggests that production cuts and employment losses to pare bloated inventories are not a material risk at this juncture.

Portfolio Advisory Group

Winter 2014 13

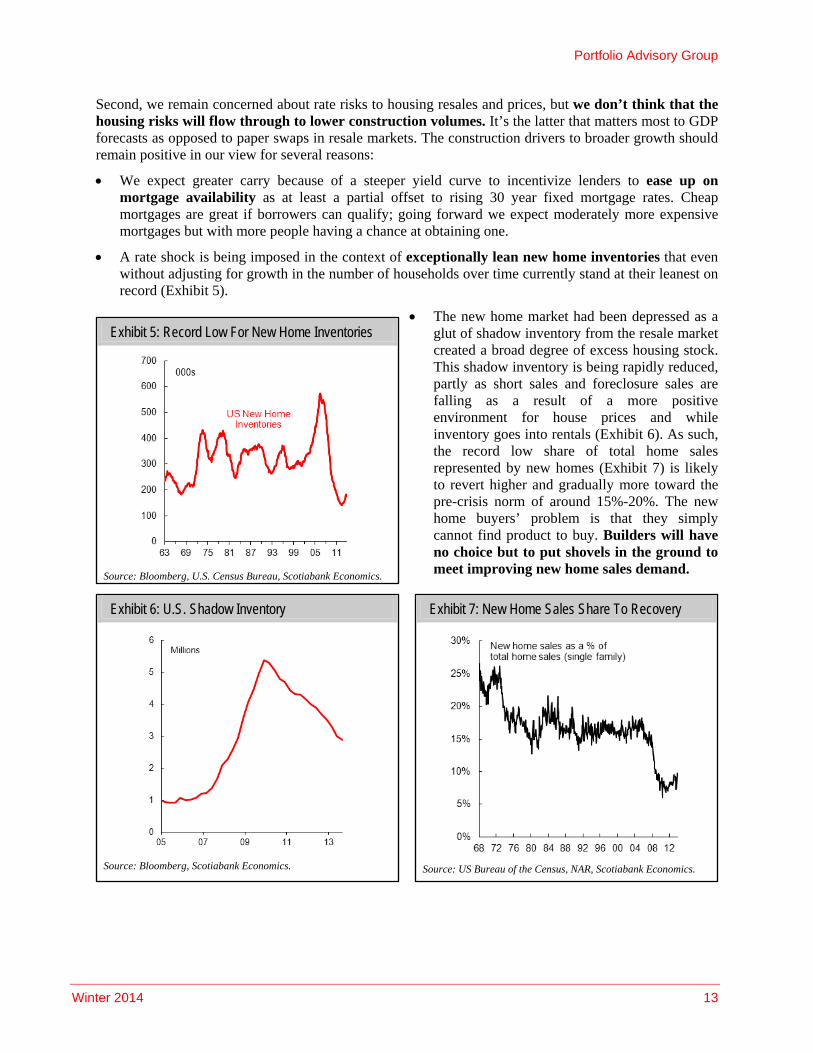

Exhibit 5: Record Low For New Home Inventories

Source: Bloomberg, U.S. Census Bureau, Scotiabank Economics.

Exhibit 6: U.S. Shadow Inventory

Source: Bloomberg, Scotiabank Economics.

Exhibit 7: New Home Sales Share To Recovery

Source: US Bureau of the Census, NAR, Scotiabank Economics.

Second, we remain concerned about rate risks to housing resales and prices, but we don’t think that the housing risks will flow through to lower construction volumes. It’s the latter that matters most to GDP forecasts as opposed to paper swaps in resale markets. The construction drivers to broader growth should remain positive in our view for several reasons:

We expect greater carry because of a steeper yield curve to incentivize lenders to ease up on mortgage availability as at least a partial offset to rising 30 year fixed mortgage rates. Cheap mortgages are great if borrowers can qualify; going forward we expect moderately more expensive mortgages but with more people having a chance at obtaining one.

A rate shock is being imposed in the context of exceptionally lean new home inventories that even without adjusting for growth in the number of households over time currently stand at their leanest on record (Exhibit 5).

The new home market had been depressed as a glut of shadow inventory from the resale market created a broad degree of excess housing stock. This shadow inventory is being rapidly reduced, partly as short sales and foreclosure sales are falling as a result of a more positive environment for house prices and while inventory goes into rentals (Exhibit 6). As such, the record low share of total home sales represented by new homes (Exhibit 7) is likely to revert higher and gradually more toward the pre-crisis norm of around 15%-20%. The new home buyers’ problem is that they simply cannot find product to buy. Builders will have no choice but to put shovels in the ground to meet improving new home sales demand.

Investment Portfolio Quarterly

14

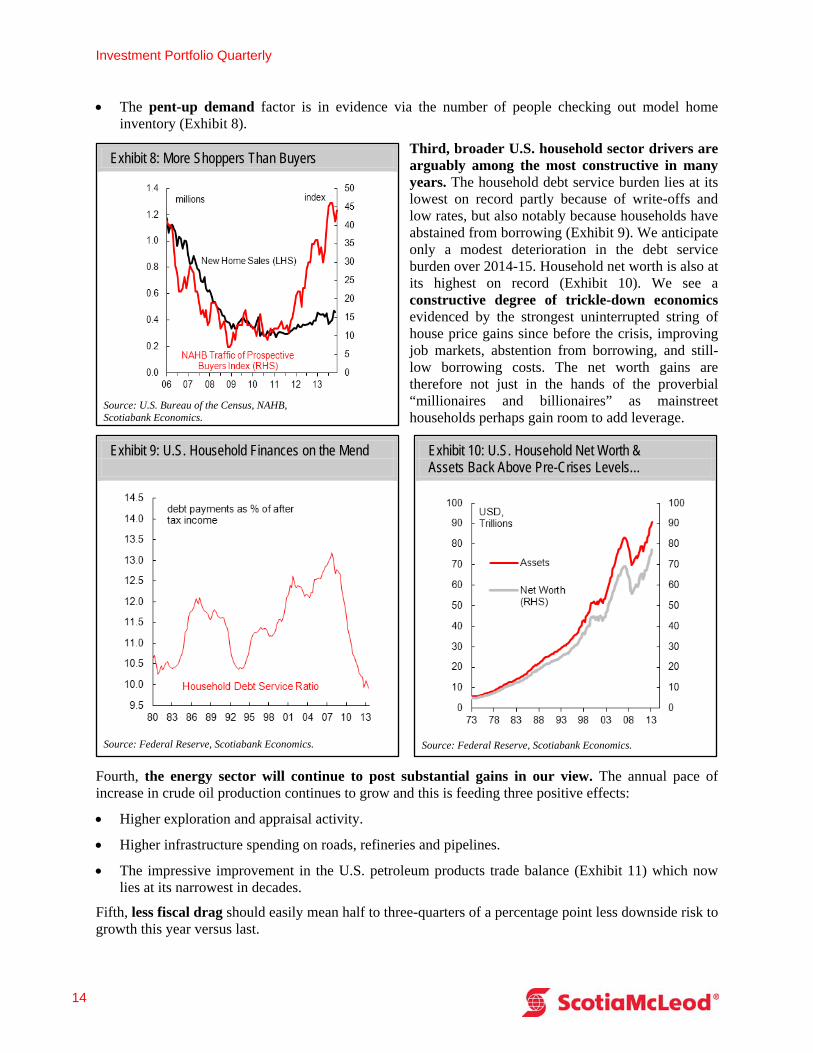

Exhibit 8: More Shoppers Than Buyers

Source: U.S. Bureau of the Census, NAHB, Scotiabank Economics.

Exhibit 10: U.S. Household Net Worth & Assets Back Above Pre-Crises Levels…

Source: Federal Reserve, Scotiabank Economics.

Exhibit 9: U.S. Household Finances on the Mend

Source: Federal Reserve, Scotiabank Economics.

The pent-up demand factor is in evidence via the number of people checking out model home inventory (Exhibit 8).

Third, broader U.S. household sector drivers are arguably among the most constructive in many years. The household debt service burden lies at its lowest on record partly because of write-offs and low rates, but also notably because households have abstained from borrowing (Exhibit 9). We anticipate only a modest deterioration in the debt service burden over 2014-15. Household net worth is also at its highest on record (Exhibit 10). We see a constructive degree of trickle-down economics evidenced by the strongest uninterrupted string of house price gains since before the crisis, improving job markets, abstention from borrowing, and still-low borrowing costs. The net worth gains are therefore not just in the hands of the proverbial “millionaires and billionaires” as mainstreet households perhaps gain room to add leverage.

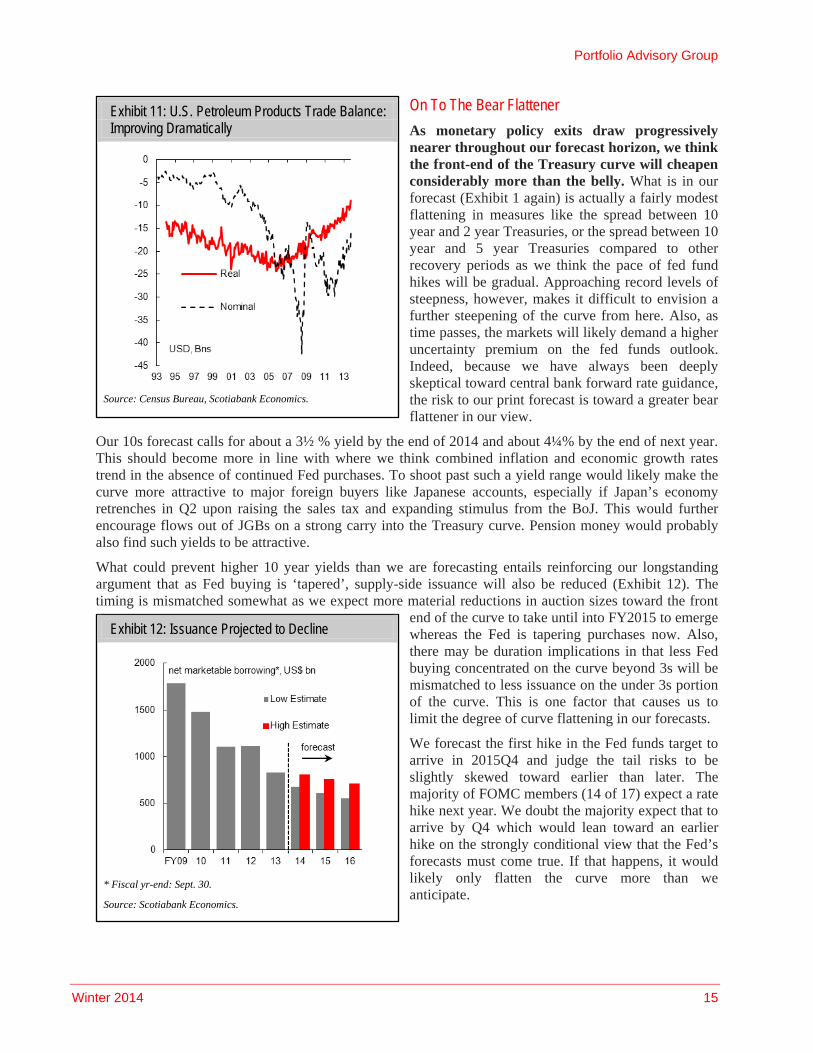

Fourth, the energy sector will continue to post substantial gains in our view. The annual pace of increase in crude oil production continues to grow and this is feeding three positive effects:

Higher exploration and appraisal activity.

Higher infrastructure spending on roads, refineries and pipelines.

The impressive improvement in the U.S. petroleum products trade balance (Exhibit 11) which now lies at its narrowest in decades.

Fifth, less fiscal drag should easily mean half to three-quarters of a percentage point less downside risk to growth this year versus last.

Portfolio Advisory Group

Winter 2014 15

Exhibit 11: U.S. Petroleum Products Trade Balance: Improving Dramatically

Source: Census Bureau, Scotiabank Economics.

Exhibit 12: Issuance Projected to Decline

* Fiscal yr-end: Sept. 30.

Source: Scotiabank Economics.

On To The Bear Flattener

As monetary policy exits draw progressively nearer throughout our forecast horizon, we think the front-end of the Treasury curve will cheapen considerably more than the belly. What is in our forecast (Exhibit 1 again) is actually a fairly modest flattening in measures like the spread between 10 year and 2 year Treasuries, or the spread between 10 year and 5 year Treasuries compared to other recovery periods as we think the pace of fed fund hikes will be gradual. Approaching record levels of steepness, however, makes it difficult to envision a further steepening of the curve from here. Also, as time passes, the markets will likely demand a higher uncertainty premium on the fed funds outlook. Indeed, because we have always been deeply skeptical toward central bank forward rate guidance, the risk to our print forecast is toward a greater bear flattener in our view.

Our 10s forecast calls for about a 3½ % yield by the end of 2014 and about 4¼% by the end of next year. This should become more in line with where we think combined inflation and economic growth rates trend in the absence of continued Fed purchases. To shoot past such a yield range would likely make the curve more attractive to major foreign buyers like Japanese accounts, especially if Japan’s economy retrenches in Q2 upon raising the sales tax and expanding stimulus from the BoJ. This would further encourage flows out of JGBs on a strong carry into the Treasury curve. Pension money would probably also find such yields to be attractive.

What could prevent higher 10 year yields than we are forecasting entails reinforcing our longstanding argument that as Fed buying is ‘tapered’, supply-side issuance will also be reduced (Exhibit 12). The timing is mismatched somewhat as we expect more material reductions in auction sizes toward the front

end of the curve to take until into FY2015 to emerge whereas the Fed is tapering purchases now. Also, there may be duration implications in that less Fed buying concentrated on the curve beyond 3s will be mismatched to less issuance on the under 3s portion of the curve. This is one factor that causes us to limit the degree of curve flattening in our forecasts.

We forecast the first hike in the Fed funds target to arrive in 2015Q4 and judge the tail risks to be slightly skewed toward earlier than later. The majority of FOMC members (14 of 17) expect a rate hike next year. We doubt the majority expect that to arrive by Q4 which would lean toward an earlier hike on the strongly conditional view that the Fed’s forecasts must come true. If that happens, it would likely only flatten the curve more than we anticipate.

Investment Portfolio Quarterly

16

Exhibit 13: It Takes a Recession… A Falling Stock Market Typically Needs a Recession

-60

-40

-20

0

20

40

60

80

65 70 75 80 85 90 95 00 05 10

y/y % changeS&P 500 Index

Grey bars represent recession periods.

Source: Bloomberg, Scotiabank Economics.

Exhibit 14: Multiple Expansion Drove Gains in 2011-2013…But Equities Aren’t Over-Valued

10

11

12

13

14

15

16

17

18

19

05 06 07 08 09 10 11 12 13

S&P 500P/E Ratio,12-monthsahead

Source: Bloomberg, Scotiabank Economics.

Stronger Economy = Stronger Equities

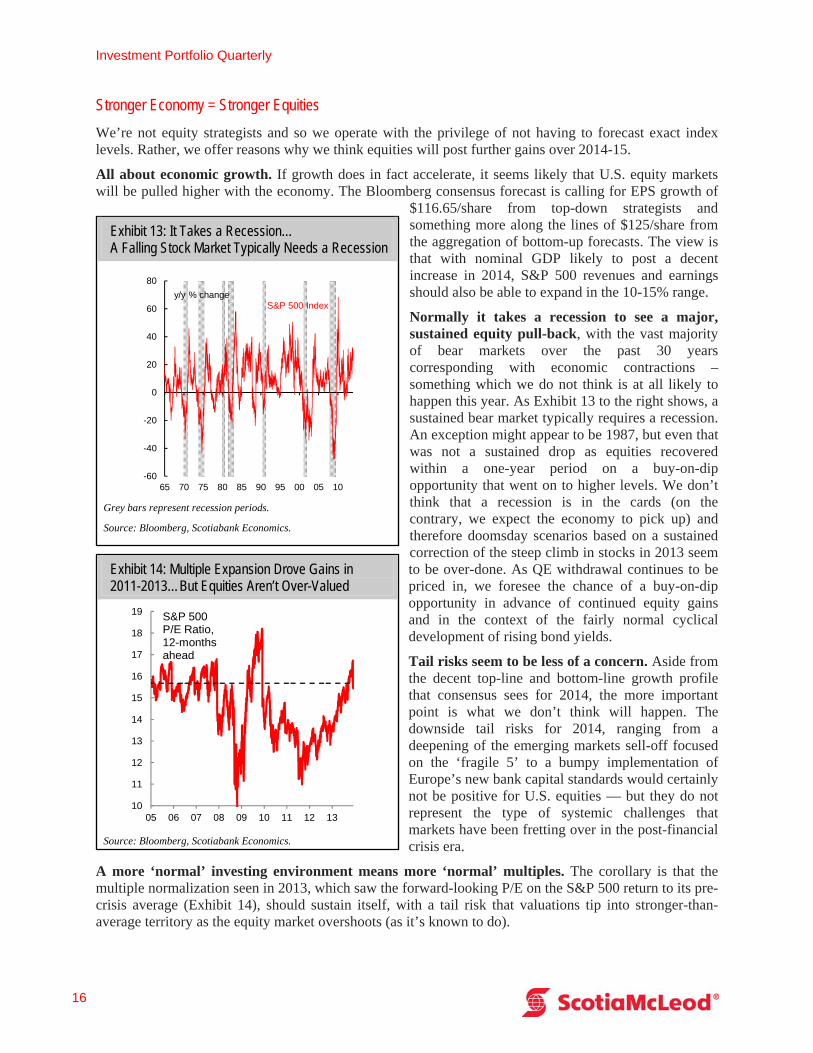

We’re not equity strategists and so we operate with the privilege of not having to forecast exact index levels. Rather, we offer reasons why we think equities will post further gains over 2014-15.

All about economic growth. If growth does in fact accelerate, it seems likely that U.S. equity markets will be pulled higher with the economy. The Bloomberg consensus forecast is calling for EPS growth of

$116.65/share from top-down strategists and something more along the lines of $125/share from the aggregation of bottom-up forecasts. The view is that with nominal GDP likely to post a decent increase in 2014, S&P 500 revenues and earnings should also be able to expand in the 10-15% range.

Normally it takes a recession to see a major, sustained equity pull-back, with the vast majority of bear markets over the past 30 years corresponding with economic contractions – something which we do not think is at all likely to happen this year. As Exhibit 13 to the right shows, a sustained bear market typically requires a recession. An exception might appear to be 1987, but even that was not a sustained drop as equities recovered within a one-year period on a buy-on-dip opportunity that went on to higher levels. We don’t think that a recession is in the cards (on the contrary, we expect the economy to pick up) and therefore doomsday scenarios based on a sustained correction of the steep climb in stocks in 2013 seem to be over-done. As QE withdrawal continues to be priced in, we foresee the chance of a buy-on-dip opportunity in advance of continued equity gains and in the context of the fairly normal cyclical development of rising bond yields.

Tail risks seem to be less of a concern. Aside from the decent top-line and bottom-line growth profile that consensus sees for 2014, the more important point is what we don’t think will happen. The downside tail risks for 2014, ranging from a deepening of the emerging markets sell-off focused on the ‘fragile 5’ to a bumpy implementation of Europe’s new bank capital standards would certainly not be positive for U.S. equities — but they do not represent the type of systemic challenges that markets have been fretting over in the post-financial crisis era.

A more ‘normal’ investing environment means more ‘normal’ multiples. The corollary is that the multiple normalization seen in 2013, which saw the forward-looking P/E on the S&P 500 return to its pre-crisis average (Exhibit 14), should sustain itself, with a tail risk that valuations tip into stronger-than-average territory as the equity market overshoots (as it’s known to do).

Portfolio Advisory Group

Winter 2014 17

A market without major macro-shocks was quite benign for stock multiples in 2013. To remind readers, the major hiccups in 2013 were: a) a ‘fiscal cliff’ scenario that was much less bad than advertised, b) a bank panic in Cyprus that failed to spill over to the rest of the world, and c) fears of Fed tapering which turned out to be somewhat of a non-event for equities by the time the taper actually happened. U.S. equity markets were able to weather moderate shocks, including tail risks that had profound implications for particular assets (Greek and Cypriot banks, defense stocks, 10-year bonds, etc.) but not for the market as a whole. We expect more of the same this year.

Investment Portfolio Quarterly

18

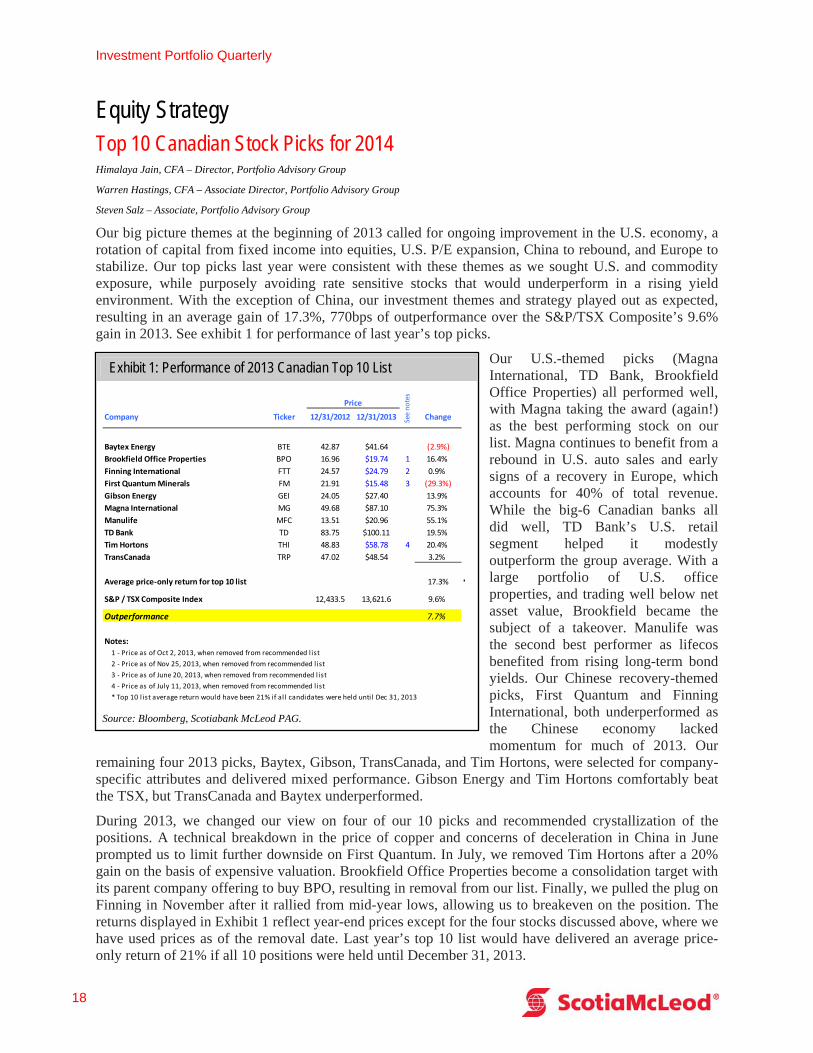

Exhibit 1: Performance of 2013 Canadian Top 10 List

Company Ticker 12/31/2012 12/31/2013 Change

Baytex Energy BTE 42.87 $41.64 (2.9%)

Brookfield Office Properties BPO 16.96 $19.74 1 16.4%

Finning International FTT 24.57 $24.79 2 0.9%

First Quantum Minerals FM 21.91 $15.48 3 (29.3%)

Gibson Energy GEI 24.05 $27.40 13.9%

Magna International MG 49.68 $87.10 75.3%

Manulife MFC 13.51 $20.96 55.1%

TD Bank TD 83.75 $100.11 19.5%

Tim Hortons THI 48.83 $58.78 4 20.4%

TransCanada TRP 47.02 $48.54 3.2%

Average price‐only return for top 10 list 17.3% *

S&P / TSX Composite Index 12,433.5 13,621.6 9.6%

Outperformance 7.7%

Notes:

1 ‐ Price as of Oct 2, 2013, when removed from recommended l ist

2 ‐ Price as of Nov 25, 2013, when removed from recommended l ist

3 ‐ Price as of June 20, 2013, when removed from recommended l ist

4 ‐ Price as of July 11, 2013, when removed from recommended l ist

* Top 10 l ist average return would have been 21% if all candidates were held until Dec 31, 2013

PriceSee notes

Source: Bloomberg, Scotiabank McLeod PAG.

Equity Strategy Top 10 Canadian Stock Picks for 2014 Himalaya Jain, CFA – Director, Portfolio Advisory Group

Warren Hastings, CFA – Associate Director, Portfolio Advisory Group

Steven Salz – Associate, Portfolio Advisory Group

Our big picture themes at the beginning of 2013 called for ongoing improvement in the U.S. economy, a rotation of capital from fixed income into equities, U.S. P/E expansion, China to rebound, and Europe to stabilize. Our top picks last year were consistent with these themes as we sought U.S. and commodity exposure, while purposely avoiding rate sensitive stocks that would underperform in a rising yield environment. With the exception of China, our investment themes and strategy played out as expected, resulting in an average gain of 17.3%, 770bps of outperformance over the S&P/TSX Composite’s 9.6% gain in 2013. See exhibit 1 for performance of last year’s top picks.

Our U.S.-themed picks (Magna International, TD Bank, Brookfield Office Properties) all performed well, with Magna taking the award (again!) as the best performing stock on our list. Magna continues to benefit from a rebound in U.S. auto sales and early signs of a recovery in Europe, which accounts for 40% of total revenue. While the big-6 Canadian banks all did well, TD Bank’s U.S. retail segment helped it modestly outperform the group average. With a large portfolio of U.S. office properties, and trading well below net asset value, Brookfield became the subject of a takeover. Manulife was the second best performer as lifecos benefited from rising long-term bond yields. Our Chinese recovery-themed picks, First Quantum and Finning International, both underperformed as the Chinese economy lacked momentum for much of 2013. Our

remaining four 2013 picks, Baytex, Gibson, TransCanada, and Tim Hortons, were selected for company-specific attributes and delivered mixed performance. Gibson Energy and Tim Hortons comfortably beat the TSX, but TransCanada and Baytex underperformed.

During 2013, we changed our view on four of our 10 picks and recommended crystallization of the positions. A technical breakdown in the price of copper and concerns of deceleration in China in June prompted us to limit further downside on First Quantum. In July, we removed Tim Hortons after a 20% gain on the basis of expensive valuation. Brookfield Office Properties become a consolidation target with its parent company offering to buy BPO, resulting in removal from our list. Finally, we pulled the plug on Finning in November after it rallied from mid-year lows, allowing us to breakeven on the position. The returns displayed in Exhibit 1 reflect year-end prices except for the four stocks discussed above, where we have used prices as of the removal date. Last year’s top 10 list would have delivered an average price-only return of 21% if all 10 positions were held until December 31, 2013.

Portfolio Advisory Group

Winter 2014 19

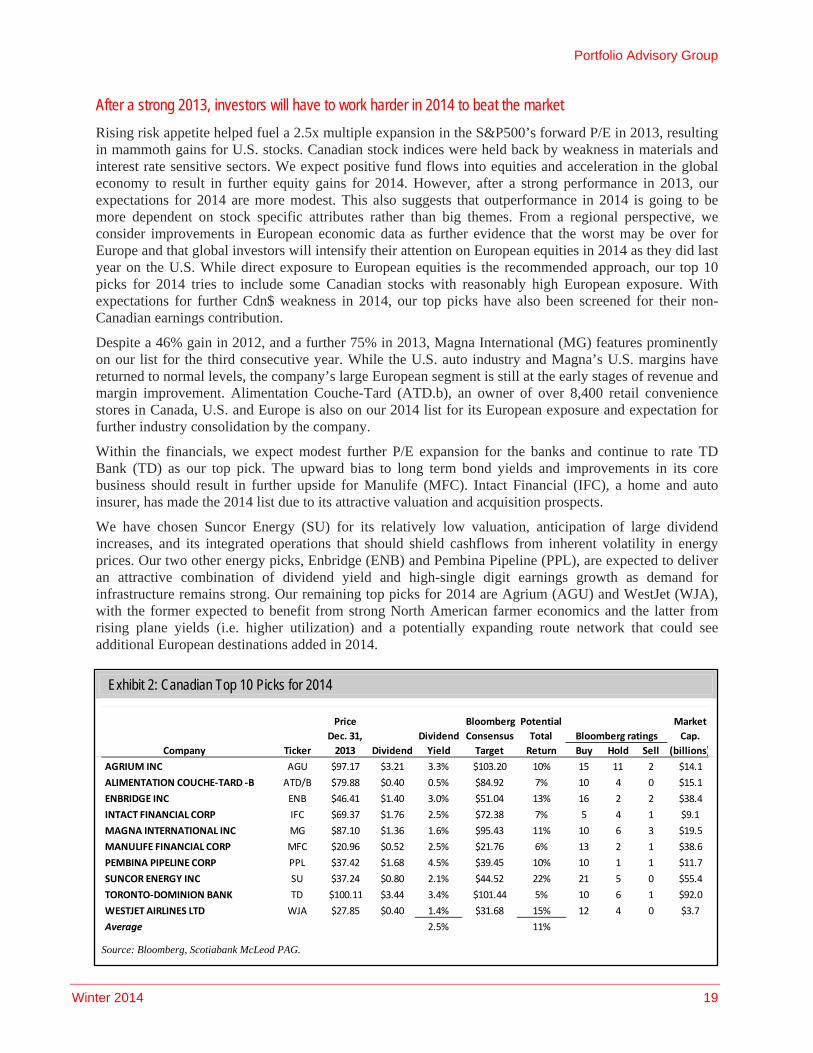

Exhibit 2: Canadian Top 10 Picks for 2014

Price

Dec. 31, Dividend

Bloomberg

Consensus

Potential

Total

Market

Cap.

Company Ticker 2013 Dividend Yield Target Return Buy Hold Sell (billions)

AGRIUM INC AGU $97.17 $3.21 3.3% $103.20 10% 15 11 2 $14.1

ALIMENTATION COUCHE‐TARD ‐B ATD/B $79.88 $0.40 0.5% $84.92 7% 10 4 0 $15.1

ENBRIDGE INC ENB $46.41 $1.40 3.0% $51.04 13% 16 2 2 $38.4

INTACT FINANCIAL CORP IFC $69.37 $1.76 2.5% $72.38 7% 5 4 1 $9.1

MAGNA INTERNATIONAL INC MG $87.10 $1.36 1.6% $95.43 11% 10 6 3 $19.5

MANULIFE FINANCIAL CORP MFC $20.96 $0.52 2.5% $21.76 6% 13 2 1 $38.6

PEMBINA PIPELINE CORP PPL $37.42 $1.68 4.5% $39.45 10% 10 1 1 $11.7

SUNCOR ENERGY INC SU $37.24 $0.80 2.1% $44.52 22% 21 5 0 $55.4

TORONTO‐DOMINION BANK TD $100.11 $3.44 3.4% $101.44 5% 10 6 1 $92.0

WESTJET AIRLINES LTD WJA $27.85 $0.40 1.4% $31.68 15% 12 4 0 $3.7

Average 2.5% 11%

Bloomberg ratings

Source: Bloomberg, Scotiabank McLeod PAG.

After a strong 2013, investors will have to work harder in 2014 to beat the market

Rising risk appetite helped fuel a 2.5x multiple expansion in the S&P500’s forward P/E in 2013, resulting in mammoth gains for U.S. stocks. Canadian stock indices were held back by weakness in materials and interest rate sensitive sectors. We expect positive fund flows into equities and acceleration in the global economy to result in further equity gains for 2014. However, after a strong performance in 2013, our expectations for 2014 are more modest. This also suggests that outperformance in 2014 is going to be more dependent on stock specific attributes rather than big themes. From a regional perspective, we consider improvements in European economic data as further evidence that the worst may be over for Europe and that global investors will intensify their attention on European equities in 2014 as they did last year on the U.S. While direct exposure to European equities is the recommended approach, our top 10 picks for 2014 tries to include some Canadian stocks with reasonably high European exposure. With expectations for further Cdn$ weakness in 2014, our top picks have also been screened for their non-Canadian earnings contribution.

Despite a 46% gain in 2012, and a further 75% in 2013, Magna International (MG) features prominently on our list for the third consecutive year. While the U.S. auto industry and Magna’s U.S. margins have returned to normal levels, the company’s large European segment is still at the early stages of revenue and margin improvement. Alimentation Couche-Tard (ATD.b), an owner of over 8,400 retail convenience stores in Canada, U.S. and Europe is also on our 2014 list for its European exposure and expectation for further industry consolidation by the company.

Within the financials, we expect modest further P/E expansion for the banks and continue to rate TD Bank (TD) as our top pick. The upward bias to long term bond yields and improvements in its core business should result in further upside for Manulife (MFC). Intact Financial (IFC), a home and auto insurer, has made the 2014 list due to its attractive valuation and acquisition prospects.

We have chosen Suncor Energy (SU) for its relatively low valuation, anticipation of large dividend increases, and its integrated operations that should shield cashflows from inherent volatility in energy prices. Our two other energy picks, Enbridge (ENB) and Pembina Pipeline (PPL), are expected to deliver an attractive combination of dividend yield and high-single digit earnings growth as demand for infrastructure remains strong. Our remaining top picks for 2014 are Agrium (AGU) and WestJet (WJA), with the former expected to benefit from strong North American farmer economics and the latter from rising plane yields (i.e. higher utilization) and a potentially expanding route network that could see additional European destinations added in 2014.

Investment Portfolio Quarterly

20

Two bonus picks:

Two additional picks that are not formally part of our top 10 list, but nevertheless reflect our current views, include ETFs that provide exposure to European equities and offer some protection against rising bond yields. While there are many options, Vanguard FTSE Europe ETF (VGK-NYSE) and WisdomTree Europe Hedged Equity Fund (HEDJ-NYSE) provide exposure to European large caps, with the latter hedged to the U.S. dollar. From a shorter-term perspective, ProShares UltraShort 20+ Year Treasury ETF (TBT-NYSE) is positively correlated to long-term Treasury yields and should provide downside protection against a disorderly sell-off in the bond market. As with all investments, these ETFs should be considered in the context of individual investor objectives and risk tolerance.

Agrium Inc. (AGU – TSX, $97.17)

Description:

Agrium is a major retail supplier of agricultural products and services in North and South America and a leading global producer and marketer of agricultural nutrients and industrial products. AGU produces and markets three primary groups of nutrients: nitrogen, phosphate and potash, plus controlled-release fertilizers and micronutrients.

Investment Thesis:

We like AGU’s 2014 prospects given strong farmer economics, expected strong retail results, and attractive nitrogen fundamentals. With respect to the first point, use of crop inputs, including those AGU produces, is supported by record high U.S. net farm income and record low farm debt/equity ratios based on U.S. Department of Agriculture estimates for 2013.

AGU should also benefit from continued growth of its strategically important retail segment, supported by integration of Viterra (acquired Oct. 1, 2013), further tuck-in acquisitions, and ongoing operational improvements.

Based on 2012 results, nitrogen represented 63% of AGU gross profit. Fundamentals for nitrogen appear stronger than those for phosphate and potash, driven by higher nitrogen/urea feedstock prices in China and lower Chinese urea exports.

On NTM consensus estimates, AGU shares trade at 7.4x forward EV/EBITDA, a premium to the long-term average of 6.7x but supported by estimated EBITDA and EPS growth of 5% and 7%, respectively, in F14. Agrium shares currently yield 3.3% and we believe the dividend is sustainable given AGU’s 37% F14E payout ratio.

The Bloomberg consensus comprises 15 Buys, 11 Holds, and 2 Sells, with a $103.20 average 12-month target price.

Alimentation Couche-Tard Inc. (ATD/B – TSX, $79.88)

Description:

Alimentation Couche-Tard Inc. (“Couche-Tard”) is a convenience store and fuel station operator in North America, Europe and ten other countries worldwide under the Circle K banner. The company has approximately 6,200 convenience stores in its North American network, nearly 2,300 in Europe, and 4,200 under the Circle K banner.

Portfolio Advisory Group

Winter 2014 21

Investment Thesis:

Couche-Tard made our list given its exposure to the recovering European economy and an improving balance sheet potentially supportive of another large acquisition.

In Europe, Couche-Tard owns Statoil Fuel & Retail (SFR), which operates nearly 2,300 stores in Scandinavia, Poland, the Baltics, and Russia. For the four quarters ended October 13, 2013, Europe represented approximately 35% of Couche-Tard’s revenue and gross profit.

Couche-Tard has an acquisition growth strategy, and with its adjusted leverage ratio having declined from 3.6x following the SFR acquisition in June, 2012 to 2.6x at the end of Q2F14, the company may be in a position to pursue another large acquisition and further consolidate its industry. According to recent analyst commentary, one possible consolidation target may be the retail network of U.S. oil and gas exploration and development company Hess Corp.

ATD/B shares currently trade at 15.7x F15E EPS, a premium to the 10-year average of approximately 13.5x likely reflecting strong expected EPS growth of 27% and 11% in F14 and F15, respectively. Couche-Tard’s dividend yield is currently just 0.5% and the company pays out less than 10% of EPS, suggesting plenty of room for dividend growth. Indeed the company hiked its dividend in each of the past two quarters.

The Bloomberg consensus currently comprises 10 Buys, 4 Holds, and no Sells, with an average 12-month share price target of $84.92.

Enbridge Inc. (ENB – TSX, $46.41)

Description:

Enbridge operates the world's longest crude oil and liquids transportation system. The company also has a significant presence in natural gas gathering, transmission and distribution, and an increasing involvement in power transmission and renewable/alternative energy production.

Investment Thesis:

We expect ENB to deliver an attractive combination of dividend yield and high-single digit earnings growth as demand for energy infrastructure remains strong. In December, ENB raised its dividend 11% and the shares currently yield 3.0%, and consensus estimates point to EPS growth of 9.5% in F14.

Earnings and dividend growth is supported by the company’s $36B growth plan, of which $29B+ is commercially secured and expected to enter service in the 2013-2017 time frame. These highly visible growth prospects underpin the company’s annual EPS and dividend growth guidance of 10%-12% (CAGR) from 2012-2017.

ENB shares trade at 13.9x NTM EV/EBITDA on consensus estimates versus a one-year average of 14.3x. The Bloomberg consensus currently comprises 16 Buys, 2 Holds, and 2 Sells, with an average 12-month share price target of $51.04.

Intact Financial Corporation (IFC – TSX, $69.37)

Description:

Intact provides property and casualty (P&C) insurance in Canada and is the country’s largest provider of home, auto, and business insurance.

Investment Portfolio Quarterly

22

Investment Thesis:

Based on 2014 consensus EPS, IFC is trading at a reasonable 11.0x P/E, particularly in view of strong expected F14 YOY growth of 63%.

We see further share price upside as investors grow more confident that expected Ontario auto insurance rate reductions should be gradual (averaging 15% over 2 years) and margin-neutral, with management expecting the Ontario government to announce offsetting cost reduction measures in the coming months. Additionally, IFC indicated it is targeting home insurance premium rate increases of 15%-23% on renewal, up from prior rate hikes of 6%-7%.

IFC could also benefit from potential industry M&A. Management believes 20 percentage points of Canadian P&C Insurance industry market share could change hands over the next five years. IFC has a track record of successfully integrating acquisitions, and management foresees growing its market share from 17% currently to 30% (before facing issues with competition regulators). The Scotiabank GBM analyst believes this growth likely will be achieved via acquisitions and estimates it could add as much as $25-$30 to IFC’s share price.

The Bloomberg consensus comprises 5 Buys, 4 Holds, and 1 Sell, with a $72.38 average 12-month target price.

Magna International Inc. (MG – TSX, $87.10)

Description:

Magna International Inc. is the most diversified automotive supplier in the world. It designs, develops and manufactures automotive systems, assemblies, modules and components, as well as engineers and assembles complete vehicles, primarily for sale to original equipment manufacturers (OEMs) of cars and light trucks in its three geographic segments – North America, Europe, and Rest of World (primarily Asia, South America and Africa). The company has 312 manufacturing operations and 87 product development, engineering and sales centres in 29 countries on five continents as of Q3 2013.

Investment Thesis:

Magna continues to grow its North American operations (52% of sales) modestly above industry growth rates while maintaining operating margins at ~9.0%. We believe this growth will be supported by a recovering U.S. auto industry (North American Vehicle sales gaining +12% on an annualized basis since 2009 lows) and improving consumer confidence.

Magna’s large European segment (41% of sales) has sustained bottom line growth despite a depressed economic backdrop. The company is on track to improve European operating margins to its target of 50% of North American levels. As Eurozone consumer confidence, unemployment, and PMI continues to improve, we believe Magna is well positioned to capitalize in this geographic segment, complemented by the possible exit from underperforming, non-core operations.

Magana has ~$0.7B in excess cash to be deployed, with a focus on new programs, targeted acquisitions, another possible share buyback, and potential dividend increases, which are all supportive of further share price appreciation.

Despite remarkable share price performance over the past two years, Magna trades at NTM EV/EBITDA of 5.5x vs. the peer average of 6.1x. Given Magna’s macroeconomic resilience, fiscal flexibility, firm 2014E earnings outlook, and prudent management, we believe the stock deserves to trade in-line or even a small premium to its peers. We also like the foreign currency exposure (to the USD and EUR) provided by Magna’s global operations.

Bloomberg consensus: 10 buys, 6 holds, 3 sells; average 12-month target price = $95.43

Portfolio Advisory Group

Winter 2014 23

Manulife Financial Corporation (MFC – TSX, $20.96)

Description:

Manulife Financial is a financial services group with principal operations in Asia, Canada and the United States. Manulife’s products and services include individual life insurance, group life and health insurance, long-term care services, pension products, annuities, mutual funds and banking products. Manulife also provides asset management services to institutional customers worldwide and offers reinsurance solutions.

Investment Thesis:

The upward bias to long term bond yields and improvements in its core business, driven by price increases and ongoing cost savings, should result in further upside for Manulife. In Q3F13, the company indicated earnings sensitivity of +$300M for a 100 bps increase in interest rates, and noted its efficiency initiatives could deliver $100M in after-tax savings in 2014 and higher amounts in 2015 and 2016.

The company’s exposure to fast-growing Asian emerging markets, which is higher than many of its North American peers, should also support continued earnings growth in 2014. Indeed, based on Scotiabank GBM F14 estimates, MFC’s Asia segment is expected to be the company’s most profitable, generating $1.1B in net income (before corporate eliminations) versus $635M-$971M at each of the three North American segments.

Based on consensus estimates, MFC trades at 13.0x F14 EPS, versus Canadian peers GWO, SLF, and IAG at 12.8x, 13.4x, and 13.1x, respectively. However, MFC is expected to deliver EPS growth of approximately 19% in F14, ahead of its peers at 13%, 2%, and 6%, respectively. It should also be noted MFC’s Q3F13 capital ratio at 229% was highest amongst its Canadian peers (216%-227%).

The Bloomberg consensus comprises 13 Buys, 2 Holds, and 1 Sell, with a $21.76 average 12-month target price.

Pembina Pipeline Corporation (PPL – TSX, $37.42)

Description:

Pembina is an energy transportation and midstream service provider that owns and operates pipelines in western Canada and related infrastructure in eastern and western Canada and the U.S.

Investment Thesis:

Underscoring ongoing strong demand for energy infrastructure, the company recently announced a $2 billion expansion of its pipeline system after reaching binding commercial agreements that are expected to provide a long-term annual EBITDA stream of $270M-$300M.

While valuation has increased to 16.8x NTM EV/EBITDA versus a five-year average of 13.4x, this arguably is justified by EBITDA estimates that have steadily moved higher over the course of 2013 and now imply 11%-12% YOY growth in both F14 and F15.

This should support YOY dividend growth of 4%-5% in both F14 and F15, complementing PPL shares’ current attractive dividend yield of 4.5%.

PPL’s balance sheet has improved significantly over six quarters, with leverage declining to 2.9x net debt / EBITDA from 5.6x following the Q2F12 acquisition of Provident Energy Ltd.

The current Bloomberg consensus comprises 10 Buys, 1 Hold, and 1 Sell, with an average 12 month target price of $39.45.

Investment Portfolio Quarterly

24

Suncor Energy Inc. (SU – TSX, $37.24)

Description:

Suncor Energy Inc.'s asset base is dominated by its oil sands operations in Fort McMurray in northeast Alberta, which produces about 400,000 bbl/d of refinery feedstock. In 2009, the company amalgamated with its former rival, Petro Canada, to form the largest Canadian-based integrated oil company. Suncor also has operations on the east coast of Canada and in Libya, Syria, and the United Kingdom. Suncor's downstream operations include refineries in Canada and the United States and a large network of retail service stations in Canada under the Sunoco and Petro Canada brands.

Investment Thesis:

The company’s oil sands operations have transitioned to a positive free cash flow (FCF) status, with the company prioritizing dividend increases, upstream and downstream growth projects, share repurchases, debt reduction, and opportunistic acquisitions.

Against a substantial FCF generation backdrop, and given a current dividend yield of 2.1%, below its two major integrated peers Cenovus and Husky at 3.2% and 3.6% respectively, we expect Suncor to continue raising its dividend at an above-average rate. The company also signaled at its most recent investor day that it would be comfortable repurchasing stock at present levels.

Clean balance sheet to support growth initiatives and FCF deployment. Suncor has a 2014E net debt to cash flow ratio of 0.6x and 2015E of 0.5x vs. the integrated peer-average of 1.1x. Additionally, the company has a net debt to capital ratio of 11.1% as of Q3/13 vs. 18.5% for its peers.

Suncor’s integrated business model and importantly its broad market access (E&P in Norway, UK, Libya, Canada) provides the company with increasingly competitive world oil price exposure over its peers. Access to North American markets is expected to improve over the next several years from its commitments to TransCanada’s Keystone XL pipeline and Enbridge’s Line 9 reversal.

Triggered by Berkshire Hathaway’s ownership filing in August, Suncor has begun to narrow its valuation gap relative to peers. The stock is trading at 6.2x 2014E EV/DACF vs. the sub-sector average of 7.4x. We believe that Suncor’s notable FCF generation, de-risked balance sheet, potential dividend increase, and integrated business model should contribute to higher relative valuation multiple.

Bloomberg consensus: 21 buys, 5 holds, 0 sells; average 12-month target price = $44.52

The Toronto-Dominion Bank (TD – TSX, $100.11)

Description:

Toronto-Dominion Bank (TD) is the largest Canadian chartered bank based on assets and the second-largest by market capitalization. It is one of the ten largest banks in the U.S. based on deposits after completing the purchase of TD Banknorth in 2007, Commerce Bank on March 31, 2008, and the South Financial Group on September 30, 2010. The bank also holds a 42% interest in TD Ameritrade.

Investment Thesis:

We continue to rate TD as our top bank pick owing to expected modest further P/E expansion for Canadian banks, exposure to the recovering U.S. economy, and above-average earnings growth.

On F14 consensus EPS estimates the P/E ratio for the Canadian bank group has expanded by 2.0 multiple points since June to 11.7x, driven by increasing comfort in a soft landing scenario for housing. This compares with a trading range of 12x-13x under normal conditions, suggesting another point of possible multiple expansion for the group.

Portfolio Advisory Group

Winter 2014 25

With U.S. personal and commercial (P&C) banking representing 23% of TD’s consolidated 2013 adjusted earnings, TD stands to benefit from a strengthening U.S. economy.

TD’s F14E EPS growth of +12.7% YOY ranks it ahead of all other Canadian banks. TD is one of only two Canadian banks expected to generate double-digit EPS growth in F14 (the other being CWB).

TD shares trade at 11.9x NTM consensus EPS estimates versus a ten-year average of 11.6x. The Bloomberg consensus currently comprises 10 Buys, 6 Holds, and 1 Sell, with an average 12-month share price target of $101.44.

WestJet Airlines (WJA – TSX, $27.85)

Description:

Founded in 1996 by a team of Calgary entrepreneurs, WestJet has grown from being a regional carrier with three aircraft and five destinations, to become Canada’s leading value-oriented airline offering scheduled service to 76 destinations in Canada, United States, Mexico and Caribbean, with its fleet of 98 Boeing Next-Generation 737 aircraft. Based on the Southwest Airlines’ model (which has resulted in 40 consecutive years of profitability for Southwest) of single aircraft type, high employee and aircraft productivity, low unit cost, and reduced frills, WestJet has become one of the most profitable airlines in North America.

Investment Thesis:

In recent years, the Canadian airline industry has benefited from limited capacity additions and increased demand, resulting in higher plane utilization and improved margins.

The introduction of Plus and Encore this year should complement earnings growth for 2014 and 2015 (11% forecast EBITDAR growth for each year). Plus is a business class equivalent, while Encore will provide regional connections serviced by Q400 turboprop planes.

WestJet also recently announced its first European destination (Dublin) and will decide on additional European destinations later in 2014. Given limited current customer options and WestJet’s value proposition, expanded European service could prove profitable for the Company.

WJA is trading at a reasonable 12x 2014E EPS (historical average of 12.3x), with a 2014E PEG ratio of 0.81. The company maintains a conservative balance sheet (net debt/EBITDA of -0.76x, i.e. net cash position).

Bloomberg consensus: 12 buys, 4 holds, 0 sells; average 12-month target price = $31.68

Investment Portfolio Quarterly

26

Exhibit 3: Performance of 2013 U.S. Top 10 List

Company Ticker 12/31/2012 12/31/2013 Change

APPLE INC AAPL 532.17 $561.02 5.4%

CATERPILLAR INC CAT 89.61 $90.81 1.3%

DIRECTV DTV 50.16 $69.06 37.7%

EMC CORP/MA EMC 25.30 $25.15 (0.6%)

FLUOR CORP FLR 58.74 $80.29 36.7%

JPMORGAN CHASE & CO JPM 43.97 $58.48 33.0%

MCKESSON CORP MCK 96.96 $161.40 66.5%

KROGER CO KR 26.02 $41.91 1 61.1%

MICROSOFT CORP MSFT 26.71 $37.41 40.1%

VALERO ENERGY CORP VLO 28.46 $50.40 2 77.1%

Average price‐only return for top 10 list 35.8% *

S&P 500 Index 1,426.2 1,848.4 29.6%

Outperformance 6.2%

Notes:

1 ‐ Price as of Oct 2, 2013, when removed from recommended l ist

2 ‐ VLO cost adjusted for spin‐off by factor .913472

* Top 10 l ist average return would have been 34.9% if all candidates held until Dec 31, 2013

See notes

Price

Source: Bloomberg, Scotiabank McLeod PAG.

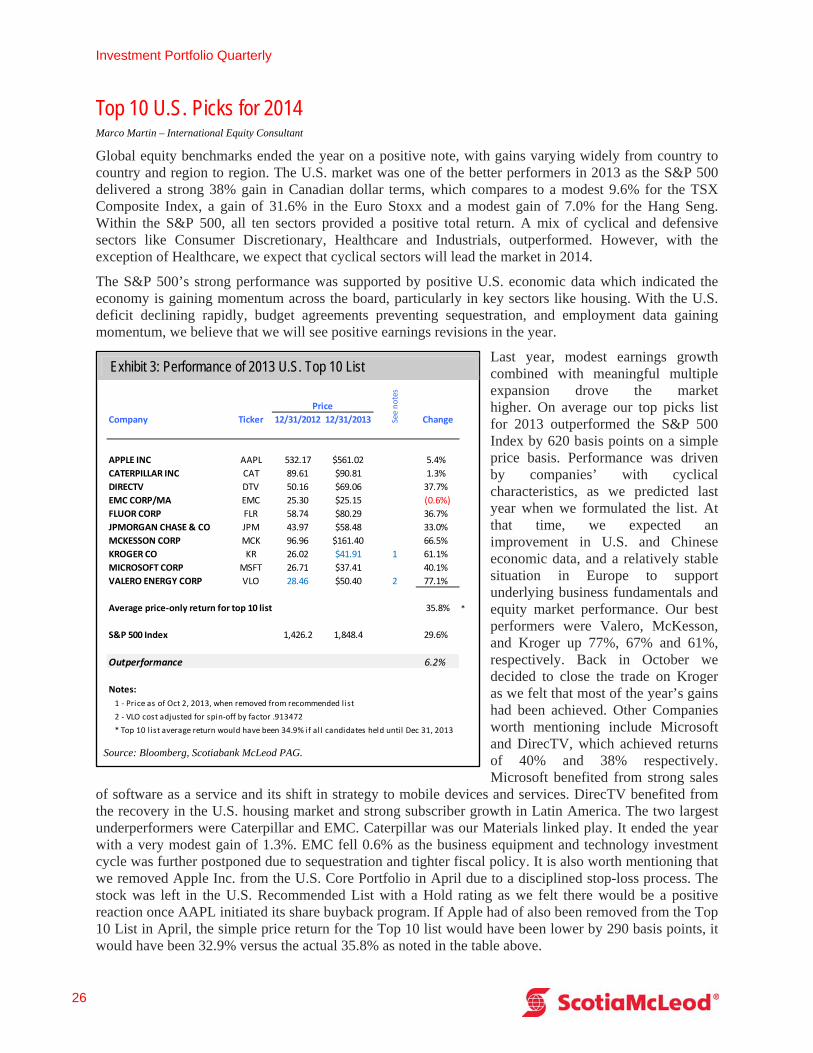

Top 10 U.S. Picks for 2014 Marco Martin – International Equity Consultant

Global equity benchmarks ended the year on a positive note, with gains varying widely from country to country and region to region. The U.S. market was one of the better performers in 2013 as the S&P 500 delivered a strong 38% gain in Canadian dollar terms, which compares to a modest 9.6% for the TSX Composite Index, a gain of 31.6% in the Euro Stoxx and a modest gain of 7.0% for the Hang Seng. Within the S&P 500, all ten sectors provided a positive total return. A mix of cyclical and defensive sectors like Consumer Discretionary, Healthcare and Industrials, outperformed. However, with the exception of Healthcare, we expect that cyclical sectors will lead the market in 2014.

The S&P 500’s strong performance was supported by positive U.S. economic data which indicated the economy is gaining momentum across the board, particularly in key sectors like housing. With the U.S. deficit declining rapidly, budget agreements preventing sequestration, and employment data gaining momentum, we believe that we will see positive earnings revisions in the year.

Last year, modest earnings growth combined with meaningful multiple expansion drove the market higher. On average our top picks list for 2013 outperformed the S&P 500 Index by 620 basis points on a simple price basis. Performance was driven by companies’ with cyclical characteristics, as we predicted last year when we formulated the list. At that time, we expected an improvement in U.S. and Chinese economic data, and a relatively stable situation in Europe to support underlying business fundamentals and equity market performance. Our best performers were Valero, McKesson, and Kroger up 77%, 67% and 61%, respectively. Back in October we decided to close the trade on Kroger as we felt that most of the year’s gains had been achieved. Other Companies worth mentioning include Microsoft and DirecTV, which achieved returns of 40% and 38% respectively. Microsoft benefited from strong sales

of software as a service and its shift in strategy to mobile devices and services. DirecTV benefited from the recovery in the U.S. housing market and strong subscriber growth in Latin America. The two largest underperformers were Caterpillar and EMC. Caterpillar was our Materials linked play. It ended the year with a very modest gain of 1.3%. EMC fell 0.6% as the business equipment and technology investment cycle was further postponed due to sequestration and tighter fiscal policy. It is also worth mentioning that we removed Apple Inc. from the U.S. Core Portfolio in April due to a disciplined stop-loss process. The stock was left in the U.S. Recommended List with a Hold rating as we felt there would be a positive reaction once AAPL initiated its share buyback program. If Apple had of also been removed from the Top 10 List in April, the simple price return for the Top 10 list would have been lower by 290 basis points, it would have been 32.9% versus the actual 35.8% as noted in the table above.

Portfolio Advisory Group

Winter 2014 27

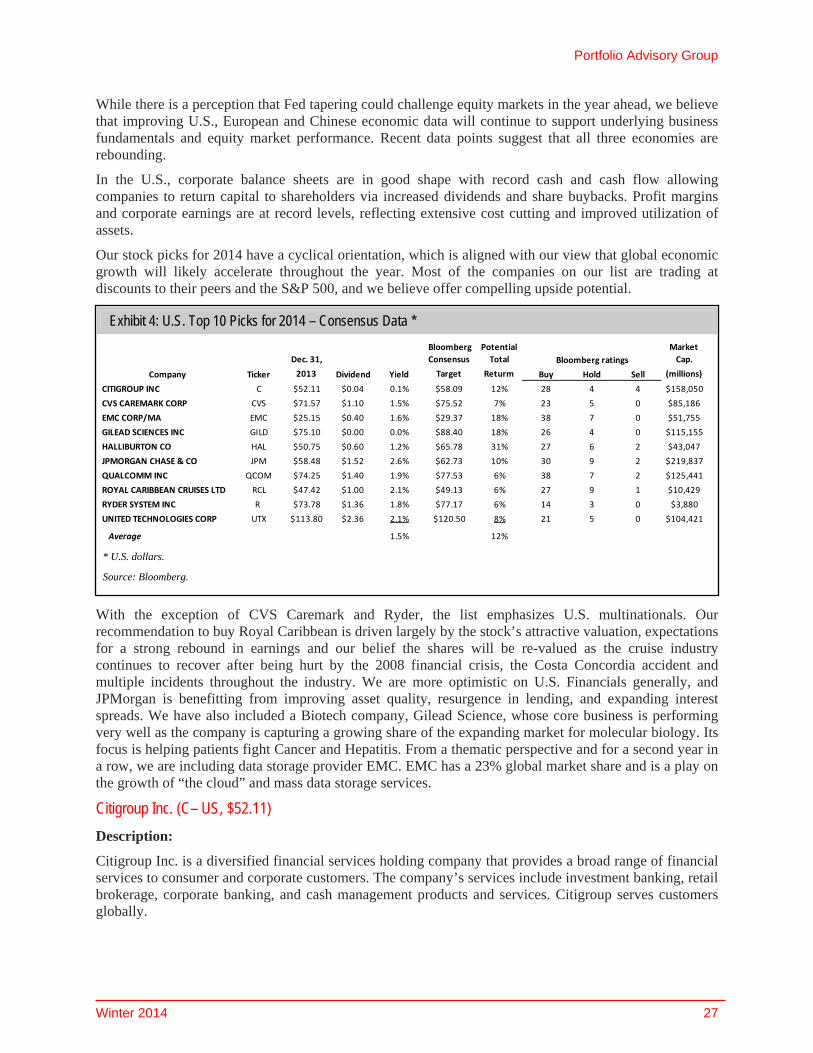

Exhibit 4: U.S. Top 10 Picks for 2014 – Consensus Data *

Dec. 31,

Bloomberg

Consensus

Potential

Total

Market

Cap.

Company Ticker 2013 Dividend Yield Target Returm Buy Hold Sell (millions)

CITIGROUP INC C $52.11 $0.04 0.1% $58.09 12% 28 4 4 $158,050

CVS CAREMARK CORP CVS $71.57 $1.10 1.5% $75.52 7% 23 5 0 $85,186

EMC CORP/MA EMC $25.15 $0.40 1.6% $29.37 18% 38 7 0 $51,755

GILEAD SCIENCES INC GILD $75.10 $0.00 0.0% $88.40 18% 26 4 0 $115,155

HALLIBURTON CO HAL $50.75 $0.60 1.2% $65.78 31% 27 6 2 $43,047

JPMORGAN CHASE & CO JPM $58.48 $1.52 2.6% $62.73 10% 30 9 2 $219,837

QUALCOMM INC QCOM $74.25 $1.40 1.9% $77.53 6% 38 7 2 $125,441

ROYAL CARIBBEAN CRUISES LTD RCL $47.42 $1.00 2.1% $49.13 6% 27 9 1 $10,429

RYDER SYSTEM INC R $73.78 $1.36 1.8% $77.17 6% 14 3 0 $3,880

UNITED TECHNOLOGIES CORP UTX $113.80 $2.36 2.1% $120.50 8% 21 5 0 $104,421

Average 1.5% 12%

Bloomberg ratings

* U.S. dollars.

Source: Bloomberg.

While there is a perception that Fed tapering could challenge equity markets in the year ahead, we believe that improving U.S., European and Chinese economic data will continue to support underlying business fundamentals and equity market performance. Recent data points suggest that all three economies are rebounding.

In the U.S., corporate balance sheets are in good shape with record cash and cash flow allowing companies to return capital to shareholders via increased dividends and share buybacks. Profit margins and corporate earnings are at record levels, reflecting extensive cost cutting and improved utilization of assets.