investment management committee

TRANSCRIPT

INVESTMENT MANAGEMENT COMMITTEE

December 2017

TEACHER RETIREMENT SYSTEM OF TEXAS MEETING BOARD OF TRUSTEES

AND INVESTMENT MANAGEMENT COMMITTEE

(Committee Chair and Members are Subject to Change at the December Board Meeting: Mr. Colonnetta, Chair; Mr. Corpus, Mr. Moss, and Ms. Ramirez,)

All or part of the December 14, 2017, meeting of the TRS Investment Management Committee and Board of Trustees may be held by telephone or video conference call as authorized under Sections 551.130 and 551.127 of the Texas Government Code. The Board intends to have a quorum and the presiding officer of the meeting physically present at the following location, which will be open to the public during the open portions of the meeting: 1000 Red River, Austin, Texas 78701 in the TRS East Building, 5th Floor, Boardroom.

AGENDA

December 14, 2017 – 1:30 p.m. TRS East Building, 5th Floor, Boardroom

1. Call roll of the Committee Members.

2. Consider the approval of the proposed minutes of the September 21, 2017,committee meeting – Committee Chair.

3. Review the Multi-Asset Strategies Group – Mohan Balachandran, Ashley Baum,Kyle Schmidt and Matt Talbert.

4. Review the Risk Group Annual Update – James Nield and Mark Telschow.

NOTE: The Board of Trustees (Board) of the Teacher Retirement System of Texas will not consider or act upon any item before the Investment Management Committee (Committee) at this meeting of the Committee. This meeting is not a regular meeting of the Board. However, because the full Investment Management Committee constitutes a quorum of the Board, the meeting of the Committee is also being posted as a meeting of the Board out of an abundance of caution.

Minutes of the Investment Management Committee

September 21, 2017

The Investment Management Committee of the Board of Trustees of the Teacher Retirement System of Texas met on September 21, 2017, in the boardroom located on the fifth floor of the TRS East Building offices at 1000 Red River Street, Austin, Texas.

Committee Members present: Mr. Joe Colonnetta, Chair Mr. David Corpus Mr. David Kelly Mr. Chris Moss Ms. Dolores Ramirez Other Board Members present: Ms. Karen Charleston Mr. John Elliott Dr. Greg Gibson Others present: Brian Guthrie, TRS Steve Huff, Fiduciary Counsel, Reinhart Boerner Van Deuren s.c. Ken Welch, TRS Steve Voss, Aon Hewitt Carolina de Onis, TRS Mike Comstock, Aon Hewitt Jerry Albright, TRS Michael McCormick, Aon Hewitt Jase Auby, TRS Ted Melina Raab, Texas AFT James Nield, TRS Ann Fickel, TCTA Mike Pia, TRS J.B Daumerie, TRS Dale West, TRS Susanne Gealy, TRS Brad Gilbert, TRS Heather Traeger, TRS Katherine Farrell, TRS Dr. Keith Brown, Investment Advisor Investment Management Committee Chair Mr. Colonnetta called the meeting to order at 1:00 p.m.

1. Call roll of Committee members.

Ms. Farrell called the roll. A quorum was present.

2. Consider the approval of the proposed minutes of the June 1, 2017 committee meeting – Committee Chair Joe Colonnetta.

On a motion by Mr. Corpus, seconded by Mr. Kelly, the committee voted to approve the proposed minutes for the June 1, 2017, Investment Management Committee meeting as presented.

3. Review the External Public Markets Portfolio – Dale West.

Mr. Dale West explained the external public markets group is charged with hiring external managers, both in traditional long oriented fashion and hedge funds in the public markets. Mr. West provided a summary of the results for the year. He stated the year began right after Brexit. He stated in essence they were starting at the bottom and rebounded – the absolute returns from both portfolios were extremely strong. Mr. West reported the external public market portfolios were just under $40 billion as of June 30th, representing about 28 percent of the Trust. He said the portfolios in aggregate returned 18.3 percent over the one-year period; 4 percent annualized over three years and 9 percent annualized over five years. Mr. West reported that all six asset class portfolios outperformed their benchmarks in the 12-month period with five of six ahead of the benchmark for five years. He said the U.S. portfolios is the exception over the long term. . Ms. Susanne Gealy reported on the global equity external manager program. She stated the total global equity portfolio of $27.8 billion returned 22.3 percent and 161 basis points of excess return beyond the benchmark over the last year. This portfolio is broken out into four equity asset class mandates: US portfolio, non- US developed, emerging market and world equity. Ms. Gealy said the three international portfolios were reporting significant success and results. Ms. Gealy discussed the critical process of reunderwriting underperforming managers of external public markets. She said while underperforming managers, while regrettable and not preferred are a natural course of the investment cycle and the investment opportunity set. She said as soon as a CUSUM risk signal is triggered, they move into re-underwriting the manager. A CUSUM risk signal is the statistical description of cumulative sum, which comes from industry or manufacturing. Ms. Gealy said in this application, it is used to identify when a manager’s information ratio is beyond or below what is expected to occur. Mr. Brad Gilbert stated on the hedge fund side, both portfolios outperformed their benchmarks. He said the two separate hedge fund portfolios equate to 8 percent of Trust assets and 2 percent of risk. He reported the directional portfolio returned 11.7 percent, which is 538 basis points ahead of its benchmark. He also reported the stable value portfolio returned 7 percent, which is 168 basis points ahead of its benchmark. Mr. Gilbert discussed why they were investing in hedge funds and what they are looking to create with this allocation. He said the directional portfolio is named so because it tends to move directionally with equity markets but has less than one-half the volatility of equities. The stable value portfolio, he said, has outperformed Treasuries by 80 basis points each year since inception, with about one-fifth of the volatility in Treasuries. Mr. Gilbert discussed other methods of viewing the performance of the two portfolios. Mr. Gilbert then discussed the work on hedge fund fees over the last year, implementing one or thirty structure which began in the fourth quarter of 2016. Mr. West described the fee savings for the Trust. Mr. Gilbert reported Credit Suisse did a midyear survey stating 14 percent of investors

and 18 percent of pensions are now either implementing or looking to implement the one or 30 structure.

4. Review the Public Strategic Partnership Network – Michael Pia and J.B. Daumerie.

Mr. Mike Pia provided the annual report on the public SPN. He reported the public SPN portfolio is a $7.5 billion portfolio with four global firms. He said the portfolio exceeded its alpha target of 200 basis points, by returning 214 basis points on a one-year basis. He stated the tracking error has been muted at 84 basis points.

Mr. J.B. Daumerie provided greater detail as to the public SPN performance. He said there was a politically driven bull market, which helped partners have a negative view on bonds. He reported relative valuations and easing monetary policies internationally, provided opportunities for the partners to capitalize on themes.

Mr. Daumerie discussed one of the key strengths of the partnership is the key force multiplier on the Trust. He stated the partners are not just an external allocation of capital but they also serve the Trust in a variety of avenues. The partners share insights on specific market events and investment problems and collaborate on research projects.

5. Global Equity Best Practices Update – Jase Auby and Dale West.

Mr. Jase Auby discussed the global equity best practices examination within the global equity portfolio. He said this was the third and final presentation. The first presentation covered phase one where the best practices across the industry were reviewed. Phase two begain to focus in on what alpha streams we had and how to optimize the portfolio. And for the final phase, phase three is the implementation of the plan. Mr. Auby characterized the strategy as rather than trying to do all things in the US market and cover all the bases, they are going to be much more selective. He said they have moved some of the money into passive and are focusing on smaller, more niche strategies.

Mr. Auby reported there are four areas of focus. The first is to improve the organization and have it focused on the overall result of the portfolio. The second area of focus is to potentially increase the newer internal quantitative portfolios, scaling up innovation. The third area of focus is to address the challenge of negative alpha in the US portfolios. And the fourth area is increasing the focus on the management of compensated risk premium.

Mr. West reported that in looking across the Trust, the international alpha streams have consistently generated positive returns and added value while the US alpha streams have been a consistent drag. He said they were also able to identify some that were duplicative and not necessary. As a result, he said, a handful of external managers were terminated over the last couple of months, as redundant.

Mr. West stated the preference is for internal portfolios when there is the internal capability. He said after allocation to internal portfolios then they complete the rest of the target asset allocation with external portfolios. He said a risk model is used to review the stocks in each portfolio to

determine the risk footprint of a given strategy. Mr. West said the risk model is to make sure the exposures are what they want in terms of targeted and compensated risk premiums. Without further discussion, the meeting adjourned at 2:12 p.m. APPROVED BY THE INVESTMENT MANAGEMENT COMMITTEE OF THE BOARD OF TRUSTEES OF THE TEACHER RETIREMENT SYSTEM OF TEXAS ON THE 14TH DAY OF DECEMBER 2017.

______________________________ _________________ Katherine H. Farrell Date Secretary of the TRS Board of Trustees

Multi-Asset Strategies GroupMohan Balachandran, Senior Managing DirectorAshley Baum, Senior Investment ManagerMatt Talbert and Kyle Schmidt, Investment Manager

December 2017

2

Agenda

I. Mandate

II. Multi-Asset Strategies Group Organization

III. Performance

IV. Team Overviews• Quantitative Equity Strategies Team• Fixed Income Team• Alternative Risk Premia Team• Special Opportunities Team

3

S t a b l e Va l u e1 6 %

G l o b a l E q u i t y5 7 %

R e a l R e t u r n2 2 %

Category:

Asset Class:

Economic Conditions:

The Trust is allocated across the following groups:

Multi-Asset Strategies Mandate

•GDP surprises are negative•Inflation surprisingly low with weak demand•Negative earnings surprises•Out of line valuations•Flight to quality

•Positive GDP surprises•Inflation surprises not dramatic•Positive earnings surprises•Reasonable valuations•Political stability

•Real GDP growth too low•Inflation surprises on the high side•Real earnings too low•Commodity-oriented demand exceeds supply by an above normal margin

Treasuries 11%Stable Value Hedge Funds 4%

Cash 1%Absolute Return 0%

44% Public Equities:USA18%

Non-US Developed 13%Emerging Markets 9%

Directional Hedge Funds 4%

13% Private Equity

Global TIPS 3%Real Estate & Other Real Assets 14%

Energy & Natural Resources 5%Commodities 0%

REITS 0%

Risk Parity 5%

4

Multi-Asset Strategies Mandate

• Alternative Risk Premia: Harvest systematic, empirically tested sources of return through dynamic long-short multi-asset strategiesARP

• Special Opportunities: Access opportunistic investments that are accretive to the overall Trust not targeted in other areas

Spec Opps

• Quantitative Equity Strategies: Manage systematic active equity portfolios using alpha models and risk premiaQES

• Treasury: Manage Trust liquidity, rebalancing process and securities lendingTreasury

• Fixed Income: Manage US Treasury, cash and global inflation-linked portfolios with a low tracking errorFixed Income

SAA

• Multi-Asset Research & Development: Conduct research and development across equities, fixed income, credit and commoditiesR&D

Manage the Trust’s multi-asset exposures and develop alpha strategies

Alph

aBe

taTr

ust

• Strategic Asset Allocation: Develop and implement Trust-wide strategic asset allocation based on long-term risk, return and diversification expectations

5

Multi-Asset Strategies Group

Mohan Balachandran, PhDSr. Managing DirectorPhD, Physics, Brown University

Wayne Speer, CFASr. Investment ManagerMBA, SMU

Don StanleyAssociateBBA, Finance UT Austin

Shruti SureshContractorMS, StatisticsColumbia University

Solomon GoldInvestment ManagerMS, Economics, UT Austin

Hasim MardinSr. AssociateMS, Economics, UT Austin

Jingshan Fu, PhDInvestment ManagerPhD, Demography, Harvard University

ANALYTICS/ RESEARCH

Mark Albert, CFASr. DirectorMBA, University of Michigan

Ashley Baum, CFA, CPASr. Investment ManagerMPA Accounting, UT Austin

Matt Talbert, PhDInvestment Manager PhD, Economics, UT Austin

Multi-Asset Strategies Group HighlightsFour PhDs

Eleven Masters DegreesSix CFAs

Patrick Zerda, CFASr. AssociateMPA Accounting, UT Austin

Sibei Wen, CFAContractorMS, Statistics UT Austin

Ryan LearySr. AssociateMBA, Rice University

Paul WaclawskyAdministrativeBS, AccountingUniversity of Maryland

Eric Morris, CFAAssociateMBA, UT Austin

Gabriel Salinas, PhDSr. AssociatePhD, Economics UT Austin

Kyle SchmidtInvestment ManagerMBA, SMU

QES Spec Opps ARP ARP/QES

6

Performance Executive SummaryAs of September 30, 2017

Source: State Street Bank, TRS IMD1The Special Opportunities benchmark is a blend of the underlying trust benchmarks weighted by the NAV of the underlying investments against the relevant benchmark (a combination of the Trust’s US equity benchmark and Absolute Return (LIBOR plus 200 bp) benchmark). Historically, the benchmark has also included weighted contributions from the real estate and energy and natural resources benchmarks. 2 Returns on overlay portfolio scaled to 12% volatility on $284MM NAV, equivalent to 2.5 bps of Trust risk3Portfolio live since 9/30/15

Multi-Asset Strategies Group

PortfolioTotal Assets Return Alpha (bp)

$, bn % Trust 1-Year 3-Year 1-Year 3-Year

Global Equity $4.0 2.8%

Quantitative Equity Strategies 3.1 2.1% 22.4% 8.4% +330 +60

Low Volatility 0.9 0.6% 19.3% 15.9% +13 +456

Stable Value $14.2 9.7%

Treasury 13.6 9.3% -6.0% 5.1% +33 +21

Special Opportunities 0.7 0.4% 7.7% 6.1% +141 1 +176 1

Real Return

TIPS $4.3 3.0% -0.4% 1.9% +31 +26

Overlay

Alternative Risk Premia $0 2 0% 2 11.3% 10.1% 3 +1128 +1006 3

Total $22.6 $15.4%

7

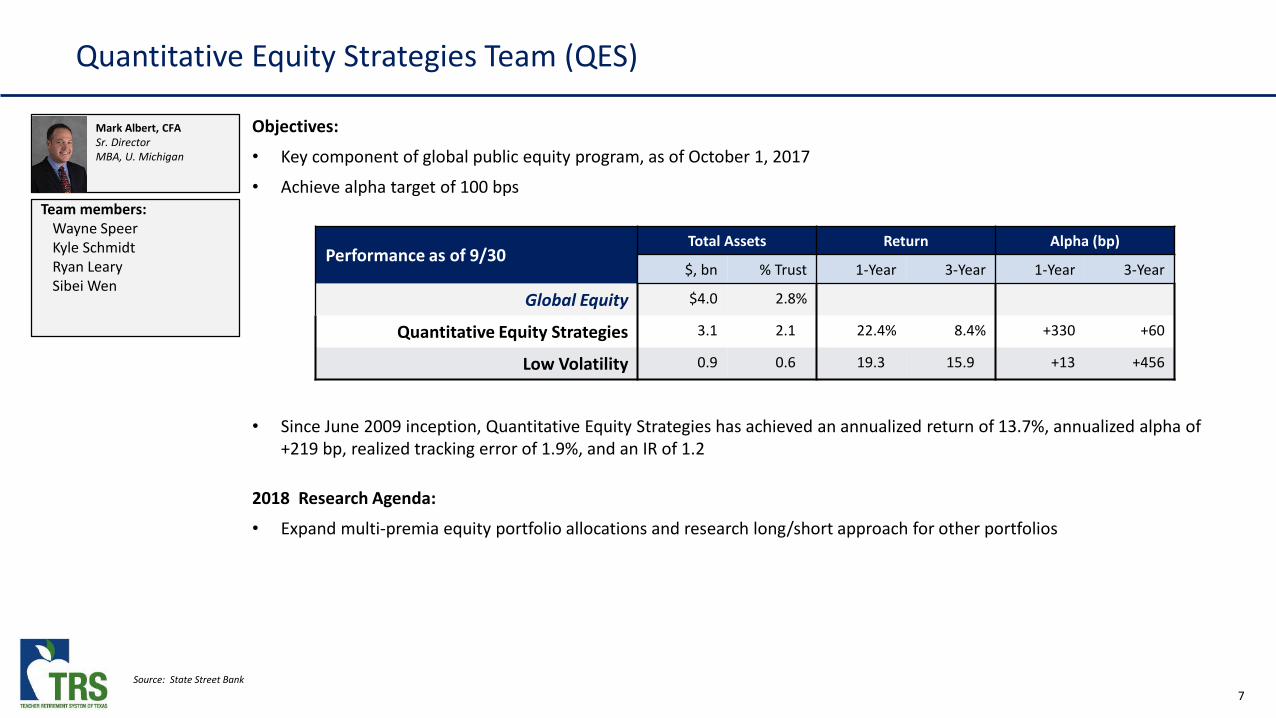

Quantitative Equity Strategies Team (QES)

Objectives:

• Key component of global public equity program, as of October 1, 2017

• Achieve alpha target of 100 bps

• Since June 2009 inception, Quantitative Equity Strategies has achieved an annualized return of 13.7%, annualized alpha of +219 bp, realized tracking error of 1.9%, and an IR of 1.2

2018 Research Agenda:

• Expand multi-premia equity portfolio allocations and research long/short approach for other portfolios

Mark Albert, CFASr. DirectorMBA, U. Michigan

Team members:Wayne SpeerKyle SchmidtRyan LearySibei Wen

Source: State Street Bank

Performance as of 9/30Total Assets Return Alpha (bp)

$, bn % Trust 1-Year 3-Year 1-Year 3-Year

Global Equity $4.0 2.8%

Quantitative Equity Strategies 3.1 2.1% 22.4% 8.4% +330 +60

Low Volatility 0.9 0.6% 19.3% 15.9% +13 +456

8

Fixed Income Team

Objectives:

• Manage total Trust asset allocation of $17.9 billion in internal US treasury and global inflation-linked portfolios

• Oversee and communicate SAA implementation

• Manage global inflation-linked bond allocation for Risk Parity portfolio

2018 Research Agenda:

• Research global sovereign bond portfolio

• Develop emerging market debt portfolio capabilities

Mohan Balachandran, PhDSr. Managing DirectorPhD, Physics, Brown University

Team members:Hasim MardinPatrick ZerdaEric Morris

Source: State Street Bank

Performance as of 9/30Total Assets Return Alpha (bp)

$, bn % Trust 1-Year 3-Year 1-Year 3-Year

Treasury $13.6 9.3% -6.0% 5.1% +33 +21

TIPS $4.3 3.0% -0.4% 1.9% +31 +26

9

Alternative Risk Premia Team

Objectives:

• Use overlay strategies to generate excess return for Public Markets

• Achieve portfolio returns through a diversified set of risk premia targeting a Sharpe ratio of 0.7

2018 Research Agenda:

• Right size the ARP portfolio

• Investigate new strategies and applications for risk premia investing

Matt Talbert, PhDInvestment ManagerPhD, Economics, University of Texas

Team members:Jingshan FuSolomon GoldKyle SchmidtGabriel SalinasRyan Leary

Source: State Street Bank, TRS IMD1 Returns on overlay portfolio scaled to 12% volatility on $284 million NAV, equivalent to 2.5 bps of Trust risk2Portfolio live since 9/30/15

Performance as of 9/301Total Assets Return Alpha (bp)

$, bn % Trust 1-Year 3-Year 1-Year 3-Year

Alternative Risk Premia $0 1 0% 1 11.3% 10.1% 2 +1128 +1006 2

10

This slide was intentionally left blank.

11

This slide was intentionally left blank.

12

Special Opportunities Team

Objectives:• Capture unique opportunities from TRS’ external network that are accretive to the overall Trust with acceptable risk and

liquidity• Outperform allocated funding source over a three year period

Accomplishments:• Increased Special Opportunities platform co-investment capacity, including two new partners to now total six relationships• Reviewed 65 unique opportunities over the last 12 months• Invested in 9 co-investments in the last 12 months totaling $432 million• Launched direct lending mandate for $600 million across corporate, senior, mezzanine and real estate credits (legal pending)

2018 Research Agenda:• Support and implement Illiquid Credit initiative• Continue building Special Opportunities external network

Source: StateStreet Bank1 Inception date is June 4, 20122 The Special Opportunities benchmark is a blend of the underlying trust benchmarks weighted by the NAV of the underlying investments against the relevant benchmark (a combination of the Trust’s US equity benchmark and Absolute Return (LIBOR plus 200 bp) benchmark). Historically, the benchmark has also included weighted contributions from the real estate and energy and natural resources benchmarks.

Ashley Baum, CFA, CPASr. Investment ManagerMPA and BBA, UT Austin

Team members:Don StanleyShruti Suresh

Performance as of 9/30Total Assets Return Alpha (bp) SI

IRR1SI

MOIC$, bn % Trust 1-Year 3-Year 1-Year 3-Year

Special Opportunities $0.7 0.4% 7.7% 6.1% +141 2 +176 2 11.8% 1.1x

13

This slide was intentionally left blank.

14

This slide was intentionally left blank.

15

This slide was intentionally left blank.

16

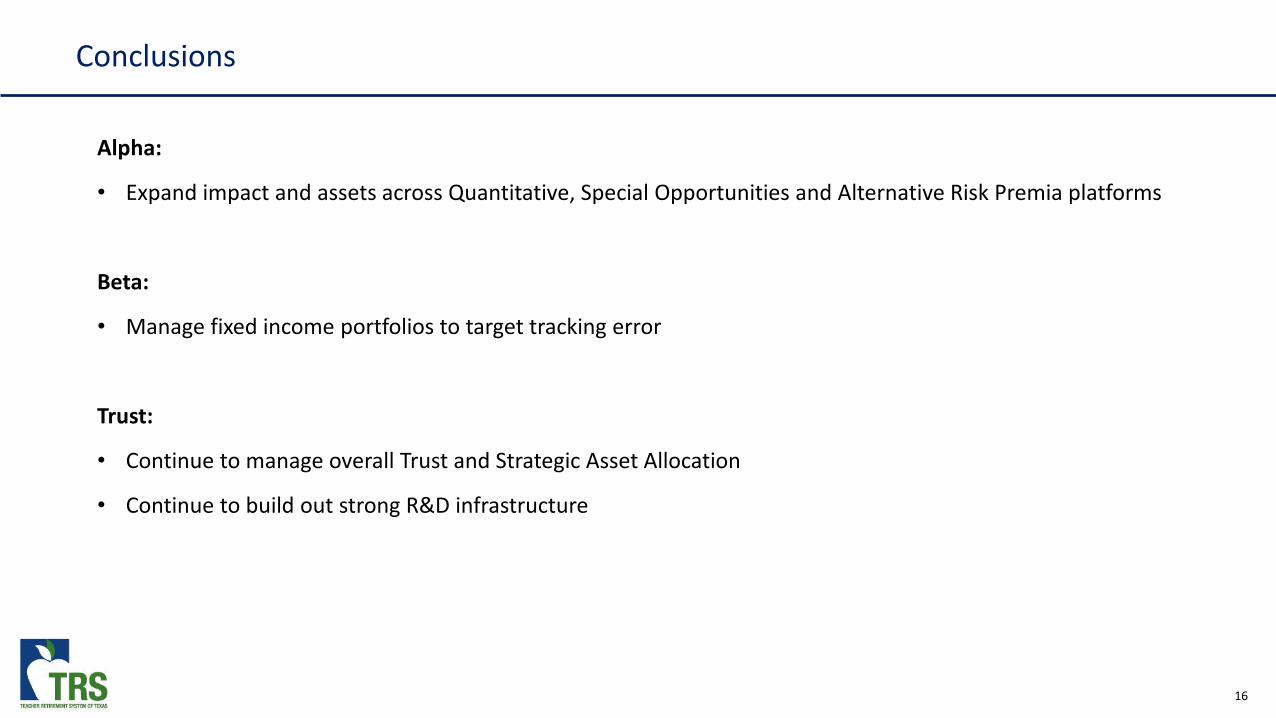

Conclusions

Alpha:

• Expand impact and assets across Quantitative, Special Opportunities and Alternative Risk Premia platforms

Beta:

• Manage fixed income portfolios to target tracking error

Trust:

• Continue to manage overall Trust and Strategic Asset Allocation

• Continue to build out strong R&D infrastructure

APPENDIX

18

This slide was intentionally left blank.

19

This slide was intentionally left blank.

Risk Group Annual UpdateJames Nield, Chief Risk OfficerMark Telschow, Senior Investment Manager

December 2017

2

Agenda

I. Mandate: Enable Efficient Risk Usage

II. Risk Group Organization

III. Risk Management• Identify, Prepare, Act

IV. Risk Strategies• Performance• Strategy Overview

3

Risk Mandate

Source: State Street

• Enable efficient risk usage through Risk Management and Risk Strategies

Risk Strategies

Risk Parity Low Volatility

Tilts

Dynamic FX Reinsurance

Risk Management

MacroTotal Trust Portfolios

• One-year and three-year returns of 9.1% and 6.1%• One-year and three-year alpha of +49 bp and +140 bp

• Systematically monitor over 300 signals each day• “Identify, Prepare, Act” approach to Risk Management

4

Risk Group Organization

James Nield, CFA, FRMChief Risk OfficerMBA, Finance, New York UniversityBS, Finance, Pennsylvania State University

Mark Telschow, CFASenior Investment ManagerBS, Civil Engineering, University of Texas

Mike Simmons, CFA Senior AssociateMPA, Accounting, University of TexasBBA, Finance,Texas A&M University

Steven LambertAssociateBS, Business Management,Saint Joseph’s College

Stephen Kim State Street EmployeeMBA, Finance, University of TexasBS, Computer Science,Dartmouth College

Josiah StevensonSenior AnalystMS, Economics, University of TexasBS, Economics, Texas A&M University

Paul WaclawskyAdministrativeBS, Accounting,University of Maryland

Risk Group Highlights

Five Advanced DegreesThree CFAsOne FRM

Elona RikaContractorPhD Economics & Finance,Brandeis University

Pierre PfarrAnalystBA, Economics,University of Texas

5

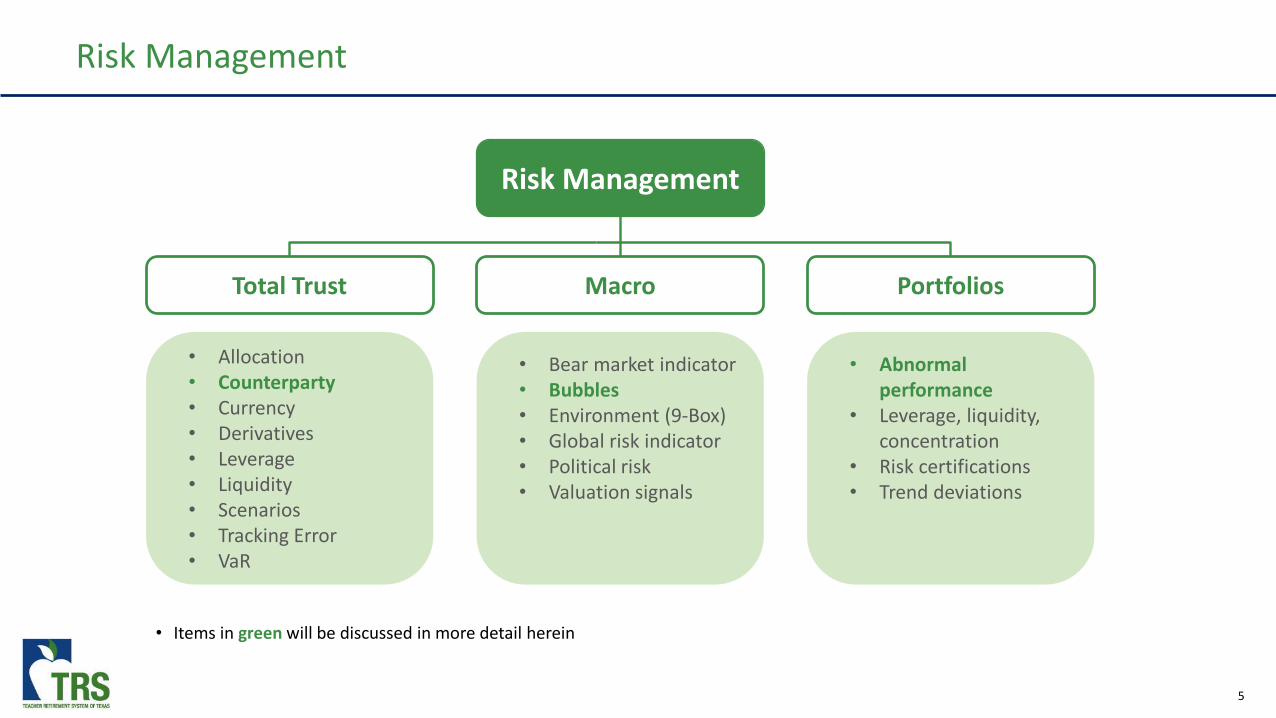

• Allocation• Counterparty• Currency• Derivatives• Leverage• Liquidity• Scenarios• Tracking Error• VaR

Risk Management

Risk Management

MacroTotal Trust Portfolios

• Bear market indicator• Bubbles• Environment (9-Box)• Global risk indicator• Political risk• Valuation signals

• Abnormal performance

• Leverage, liquidity, concentration

• Risk certifications• Trend deviations

• Items in green will be discussed in more detail herein

6

Identify, Prepare, Act

• Counterparty Risk

• Reduce trade duration• Limit types of trades• Cease trading• Move trades

• Diversify exposures• Multiple counterparties• Daily margin• Internal and policy credit limits

Risk Management

Total Trust PortfoliosMacro

Identify

Prepare

Act

7

Counterparty RiskIdentify, Prepare, Act

• Metrics we follow:1. CDS Spreads2. Capital Ratio3. Common Ratio

Risk Management

MacroTotal Trust Portfolios

4. Equity Returns5. Ratings / Changes6. Rating Outlook

3

3

1 2

1 2

3

3

2 1

1 2

2 1

3

1 2

3

3

1 2

0 10 31 1 0

TD

UBS

Tot.

DB

GS

JPM

Mac

MS

SG

CS

Credit Ratings

AAA

AA A BBB

BB

BoA

Bar

BNP

CIBC

CitCounterparty Rating Trend

Source: TRS IMD, Bloomberg

0

2

4

6

8

10

12

Oct-14 Apr-15 Oct-15 Apr-16 Oct-16 Apr-17 Oct-17

Upgrades Downgrades Net

8

Identify, Prepare, Act

• Bubble Risk

• Reduce any overweight• Evaluate stop loss limits

• Bubble Signalo Absolute returno Relative return

• Valuation Check

Risk Management

Total Trust PortfoliosMacro

Identify

Prepare

Act

9

Bubble RiskIdentify, Prepare, Act

• No bubble signals as of September 2017o We track over one hundred assets across five different asset classeso Currently in the longest time period without a bubble signalo This is consistent with an expansion cycle that has been longer than most cycles

Risk Management

Total Trust PortfoliosMacro

Monthly bubble signals by asset class

-

2

4

6

8

10

12

14

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Num

ber o

f Sig

nals

Equities Fixed Income Commodities Currencies Alternatives

Source: TRS IMD

10

Bubble RiskIdentify, Prepare, Act

Criteria: Over the past 7 years:

1. Has asset value doubled from a low?

2. How different is current price from the asset’s average price?

3. Are the asset returns similar or different from a basket of asset returns?

Risk Management

Total Trust PortfoliosMacro

Has asset doubled?

How different is current price?

0%

50%

100%

150%

200%

S&P EAFE+C EM DIR. HF PVT EQ. TRSRY SV HF H. YLD TIPS ENRI R. ASSETS COMDTY

7 Yr

. Ret

urn

% Increase from Trough (Past 7 Yrs) Criteria #1: Has Asset Doubled?

-3

-2

-1

0

1

2

3

S&P EAFE+C EM DIR. HF PVT EQ. TRSRY SV HF H. YLD TIPS ENRI R. ASSETS COMDTY

Std.

Dev

iatio

n# Standard Deviations from Average (Past 7 Yrs) Criteria #2: 2.75 Std Dev from Avg

Source: TRS IMDNote: criteria #1 and #2 are considered super criteria and both criteria must be met to generate a bubble signal. Criteria #3 only impacts the magnitude of the signal

11

Identify, Prepare, Act

• Abnormal performance

• Mandatory re-underwriting• Buy or sell rating

• Manager limits• Trend deviation signal• CUSUM (Cumulative sum of Information Ratio)

Risk Management

Total Trust PortfoliosMacro

Identify

Prepare

Act

12

$

$

• CUSUM: Systematic sampling process to determine if our public market portfolios are producing the desired alphao Objective is to quickly detect any errors in the processo CUSUM signal triggers a mandatory re-underwriting of the investment

CUSUMIdentify, Prepare, Act

Normal Variation

Abnormal Variation

$ $$ $ $ $ $

$ $$ $ $ $ $

Risk Management

Total Trust PortfoliosMacro

13

CUSUMIdentify, Prepare, Act

• Since 2010, we have evaluated 115 CUSUM signalso “Buy” recommendation 80% of the time o CUSUM decisions have a hit rate of 57%

• In total, this process has produced an incremental $530 million in alpha since inception

Risk Management

Total Trust PortfoliosMacro

-$300

$0

$300

$600

$900

$1,200

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

$ m

illio

ns

$ Impact of CUSUM Process

Source: TRS IMD, CUSUM dollar impact based on 3-year performance following CUSUM signal. Signals with less than 12 months of data are excluded from analysis

14

Risk Strategies

Risk Strategies

Risk Parity Low Volatility

Tilts

Dynamic FX Reinsurance

15

Risk Strategies Overview

Investing in a diversified portfolio that uses leverage to target a desired risk level

• Items in blue will be discussed in more detail herein

Tilts

Generating equity-like returns with less market risk (beta) by capitalizing on behavioral biases

Hedging unwanted currency exposure to generate risk budget that can be used elsewhere

Reinsurance Adding a non-correlated return stream to further diversify the Trust

Portfolio: Enable efficient risk usage by....

Low Vol

Risk Parity

Dynamic FX

Adjusting Risk Parity positions based on market conditions

16

• One-year and three-year returns of 9.1% and 6.1%• One-year and three-year alpha of +49 bp and +140 bp• Three-year return of $1.3 billion and three-year alpha of $181 million

Risk Strategies PerformanceAs of September 30, 2017

Risk Strategies

PortfolioTotal Assets Returns (%) Alpha (bp)

$, millions % Trust 1-Year 3-Year 1-Year 3-Year

Risk Parity $7,301 5.0% 8.5% 4.9% +97 +98

Low Volatility 2,020 1.4% 19.3% 15.9% +13 +456

Reinsurance 300 0.2% -7.5% 4.9% -1167 +312

Dynamic Currency 1 0 0.0% 0.1% -0.3% +11 -29

Total $9,620 6.6% 9.1% 6.1% +49 +140

Source: State Street Bank; currency return equals contribution to Risk Group performance1 Dynamic Currency hedging portfolio was launched in February 2015

17

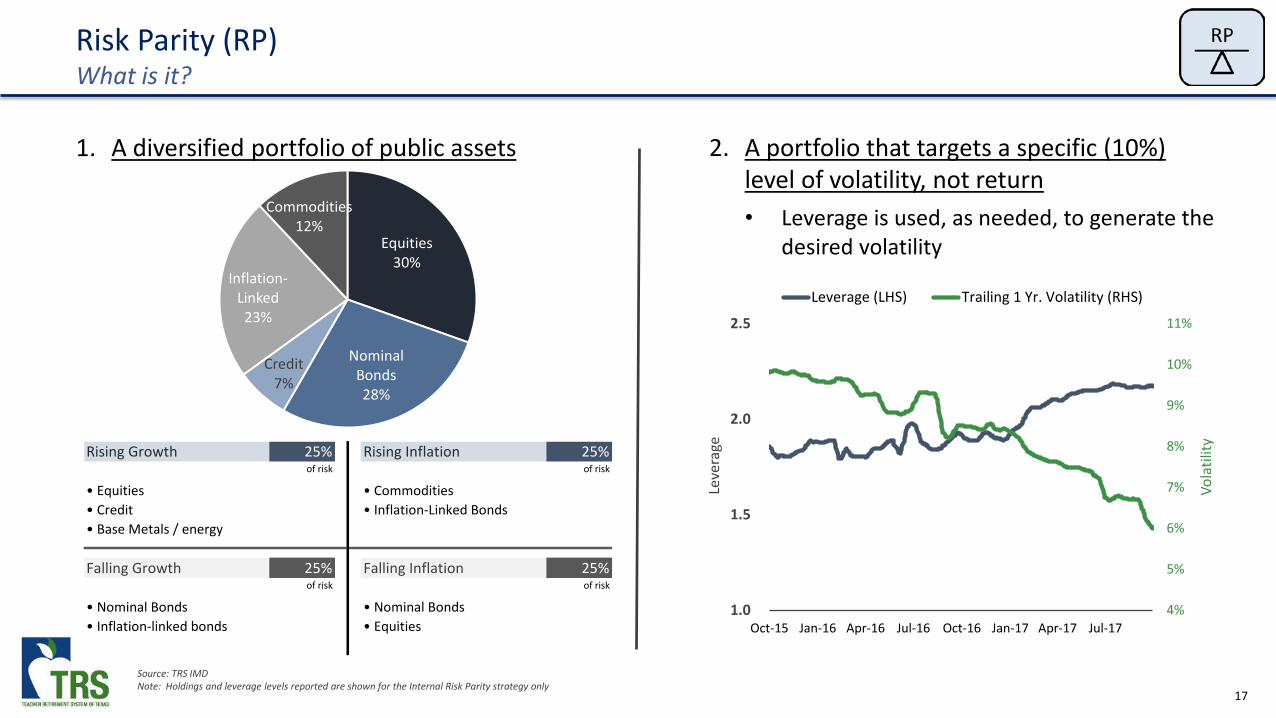

Risk Parity (RP)What is it?

1. A diversified portfolio of public assets 2. A portfolio that targets a specific (10%) level of volatility, not return• Leverage is used, as needed, to generate the

desired volatility

Rising Growth 25% Rising Inflation 25%of risk of risk

• Equities • Commodities• Credit • Inflation-Linked Bonds• Base Metals / energy

Falling Growth 25% Falling Inflation 25%of risk of risk

• Nominal Bonds • Nominal Bonds• Inflation-linked bonds • Equities

4%

5%

6%

7%

8%

9%

10%

11%

1.0

1.5

2.0

2.5

Oct-15 Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17

Vola

tility

Leve

rage

Leverage (LHS) Trailing 1 Yr. Volatility (RHS)

Equities30%

Nominal Bonds28%

Credit7%

Inflation-Linked23%

Commodities12%

Source: TRS IMDNote: Holdings and leverage levels reported are shown for the Internal Risk Parity strategy only

18

Equities58%

Bonds4%

IL12%

Commod.21%

Credit5%Equities

97%

Bonds3%

RP60/40

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 10 Yr. Avg

RP

Treasury RP RP TIP RP Credit Treasury Credit Credit Global Eq. RP

TIPS Global Eq. TIPS Treasury TIPS Global

Eq. RP Treasury RP Credit TIPS

RP TIPS Credit RP Credit RP TIPS Global Eq. TIPS RP Credit

Credit Comdty Comdty Global Eq.

Global Eq. Comdty Global

Eq. TIPS Comdty Treasury Treasury

Comdty Credit Treasury Credit Treasury Treasury Credit RP Global Eq. TIPS Global

Eq.

Global Eq. Treasury Global

Eq. Comdty Comdty TIPS Comdty Comdty Treasury Comdty Comdty

Risk Parity (RP)Why do we like it?

1. Diversifying to Trust

2. Diversified exposures within the portfolio

3. Balance through time

3.5%

5.0%

0% 1% 2% 3% 4% 5% 6%

Risk Contribution

$ Allocation

• Rank of Return/Risk ratio by asset shown below

Source: TRS IMD; State Street ; Bloomberg

• Past 10 year portfolio risk contributions:

19

Risk Parity (RP)How does it efficiently use risk?

1. Diversification enables higher returns for the same level of volatility

2. Further efficiencies achieved by implementing half of the portfolio internally• Estimated annual fee savings of $12 million (at current size)• Internal Risk Parity has outperformed the Risk Parity benchmark by +340 bp on a three-year basis

retuning an incremental $142 million in returns

-40%

-20%

0%

20%

40%

60%

80%

100%

Sep-07 Sep-08 Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 Sep-15 Sep-16 Sep-17

Cum

ulat

ive

Retu

rn

Risk Parity (10 Vol.) 60/40 (10 Vol.)

Source: TRS IMD, Bloomberg (HFR Risk Parity 10 Vol Benchmark used for Risk Parity; ACWI and US Aggregate indices used for 60/40 portfolio); fee savings calculated using estimated management fee of 35 bp

20

Low Volatility (LV)What is it?

1. A portfolio of low volatility stocks...• Research shows that low

volatility stocks tend to outperform due to leverage aversion and behavioral biases

2. That provides defensive factor exposure• Defensive exposure is

diversifying to the total Global Equity portfolio

21

Low Volatility (LV)Why do we like it?

0.86

0.92

0.88

0 1

USA

EAFE+C

EM

Realized Beta

1. Defensive Beta 2. Diversifying Alpha

-0.2

-0.5

-0.1

-1.0-0.50.00.51.0

USA

EAFE+C

EM

Correlation to Total Public Equity Alpha

Source: TRS IMD, Beta and correlation shown since funding

More Diversifying Alpha(low correlations are more diversifying)

22

Low Volatility (LV)How does it efficiently use risk?

1. Defensive beta plus diversifying alpha produces benchmark or better returns at lower risk

2. Further efficiencies achieved by implementing the portfolio internally• Estimated annual fee savings of $10 million (at current size)• Low Volatility has outperformed the benchmark by +456 bp on a three-year annualized basis retuning an

incremental $52 million in returns

0%

20%

40%

60%

80%

100%

120%

140%

Dec-12 Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Jun-16 Dec-16 Jun-17

Cum

ulat

ive

Retu

rn

Total LowVol Benchmark

Source: TRS IMDNote: Fee savings calculated using an estimated management fee of 50 bp

23

Risk GroupAccomplishments and Priorities

2017 Accomplishments

• Executed our mandate to enable efficient risk usage

• Produced positive alpha over both a 1 year (+49 bp) and 3 year (+140 bp) basis

• Delivered on key priorities which include:1. Contributed to development of Global Equity

Best Practices2. Launched Risk Parity Tilts portfolio3. Supported Real Assets currency hedging4. Created a new internal risk event report 5. Expanded Low Volatility portfolio

2018 Priorities (Preliminary)

• Continue to execute mandate to enable efficient risk usage

• Further apply “Identify, Prepare, Act” process across key risks

• Enhance Tilts portfolio

• Rebalance Risk Parity portfolio

• Develop additional Risk Strategies to support Trust performance through the business cycle

• Support update of 2018 Investment Policy Statement (IPS)

Note: Sample internal risk event report in appendix

24

Risk Group Key Points

1. Efficient risk usage = Risk Management + Risk Strategies

2. “Identify, Prepare, Act” is the process we employ to manage risk

3. Risk Strategies generated strong performance

APPENDIX

26

ReinsurancePortfolio Overview

Size: $0.3 billion

Start Date: October 2013

Team: Risk, Hedge Funds

Benchmark: HFRI Fund of Funds Conservative

Objective: Capture premium of providing capital to insurance companies. Provide diversified returns to TRS

Update: Portfolio was negatively impacted by Hurricanes Harvey, Irma, and Maria along with California wildfires• Losses were in-line with expectations given

events• We do see some improved opportunity for 2018

which we are evaluating• Since inception returns of 7.9%

TRS Portfolio Impact: Historical / Simulated Events

Andrew 1:100 QuakeKatrina 1:100 HurricaneWTC - 9/11 1:250 Quake1906 SF Quake 1:250 Hurricane

Rtn.

-17.1% -53.4%

Rtn.-9.2% -23.4%

-5.1% -36.3%-37.8% -66.7%

Cumulative Performance:

RE

0%

10%

20%

30%

40%

50%

Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Jun-16 Dec-16 Jun-17

TRS Re Benchmark

Source: TRS IMD, Bloomberg, State Street

27

This slide was intentionally left blank.

28

Risk Signals

• Signals highlight key metrics for further evaluation• Generate 174 signals on average each month

Example: • Metric: US Economic Surprise• Ticker: CESIUSD• Threshold: Down, -50

-

100

200

300

400

500

600

Aug-15 Nov-15 Feb-16 May-16 Aug-16 Nov-16 Feb-17 May-17 Aug-17

Liquidity Leverage Relative Weight Market Return

Counterparty Exposure Economic Market Signal Credit Ratings

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

-100

-80

-60

-40

-20

0

20

40

60

80

Dec-14 Jun-15 Dec-15 Jun-16 Dec-16 Jun-17

Signal US Econ. Surp Threshold

Source: TRS IMD