investment fundamentals forum - cfa institute v21jan...what are specified investment products? •...

TRANSCRIPT

Investment Fundamentals Forum21 January 2013

Understanding and Trading Equity &Related Products in Singapore

Th’ng Beng Hooi, CFA

1

Speaker BiographyTh’ng Beng Hooi, CFA

2

DisclaimerPlease note that the information is provided for you by way of information only. All theinformation, report and analysis were and should be taken as having been prepared for thepurpose of general circulation and that none were made with regard to any specific investmentobjectives, financial situation and particular needs of any particular person who may receive theinformation, report or analysis (including yourself).

Any recommendation or advice that maybe expressed in or inferred from such information,reports or analysis therefore does not take into account and may not be suitable for yourinvestment objectives, financial situation and particular needs. You understand that you buyand/or sell and/or take any position in/or on the market, in any of the stocks, shares, products orinstruments etc. based on your own decision(s). This is regardless of whether the information isanalysed or not, regardless of the details or information related to price levels,support/resistance levels and any information based on technical or fundamental analysis. Youunderstand and accept that nothing told or provided to you whether directly or indirectly is tobe a basis for your decision(s) in relation to the market or your trades or transaction(s).

Please see a registered trading representative or financial adviser for formal advise.

3

WHAT’S AVAILABLE?

4

5

What AreSpecified Investment Products?

• Some products listed on SGX may have termsand features that are not as well known andwidely understood as others.

• These are referred to as “Specified InvestmentProducts”.

6

What AreSpecified Investment Products?

• Specified investment products (Listed) include:– Certificates– Exchange Traded Funds (ETFs)– Exchange Traded Notes (ETNs)– Extended Settlement Contracts– Structured Warrants– Callable Bull / Bear Contracts (CBBCs)

• Not yet launched

7

What AreSpecified Investment Products?

• Specified investment products (Unlisted) include:– CFDs– Leveraged FX– Equity Linked Notes– Other Structured Products

8

What AreSpecified Investment Products?

• Specified investment products (Unlisted) include:– CFDs– Leveraged FX– Equity Linked Notes– Other Structured Products

9

What AreExcluded Investment Products?

• Shares• Fully paid depository receipts representing shares• Subscription rights pursuant to rights issues• Company issued warrants/derivatives• Units in business trusts• Units in real estate investment trusts• Debentures (other than asset backed securities & structured notes

• All above must be listed10

AMERICAN DEPOSITORY RECEIPTS

11

Risks

• Market & Company Specific Risk• Foreign Currency Risk• Foreign Political, Social and Economic Risk• Price Risk (tracking error)

12

INTRODUCTION TOEXCHANGE TRADED FUNDS

13

What Are Exchange Traded Funds?• An investment vehicle traded on the SingaporeExchange (SGX) like any other security (e.g. stocks).

• The ETF invests in a basket of securities in order totrack a stated index.

• For example: the STI ETF tracks the STI index.

14

What Are Exchange Traded Funds?• ETFs exist for many asset types: stocks, bonds,commodities and currencies.

• ETFs that track certain stock sectors or geographicalmarkets are also available.

• For example: the iShares Dow Jones US TechnologySector Index Fund tracks the tech sector of the DJIA.

15

What Are Exchange Traded Funds?

• An ETF is like a unit trust fund with the followingfeatures:– Invests in assets of your choice.– Listed on SGX.– Traded like any other stock.– Brokerage fees similar to any other stock.– Low annual management fees.

16

Direct Replication (Cash Based)

• ETF holds same constituent stocks in the same weightage as the stated index.• Higher tracking error due to expenses and tax withholdings on dividendpayments.

• No counter party risk.

Full Replication

• ETF holds only selected constituent stocks that have high correlation with statedindex.

• Higher tracking error due to expenses and tax withholdings on dividendpayments.

• No counter party risk.

Representative Sample

17

Synthetic Replication

• Use swaps to gain performance similar to the stated index.• Swaps used may not even be the same constituent stocks.• Lower tracking error as swaps give more precise tracking to the stated index.• Counter party risk arising from swap agreement.

Swap Based

• Use derivatives to replicate the stated index.• Derivatives used are warrants and participatory notes.• Higher tracking error due to higher cost of derivatives.• Counter party risk arising from possibility of default.

Derivative Embedded

18

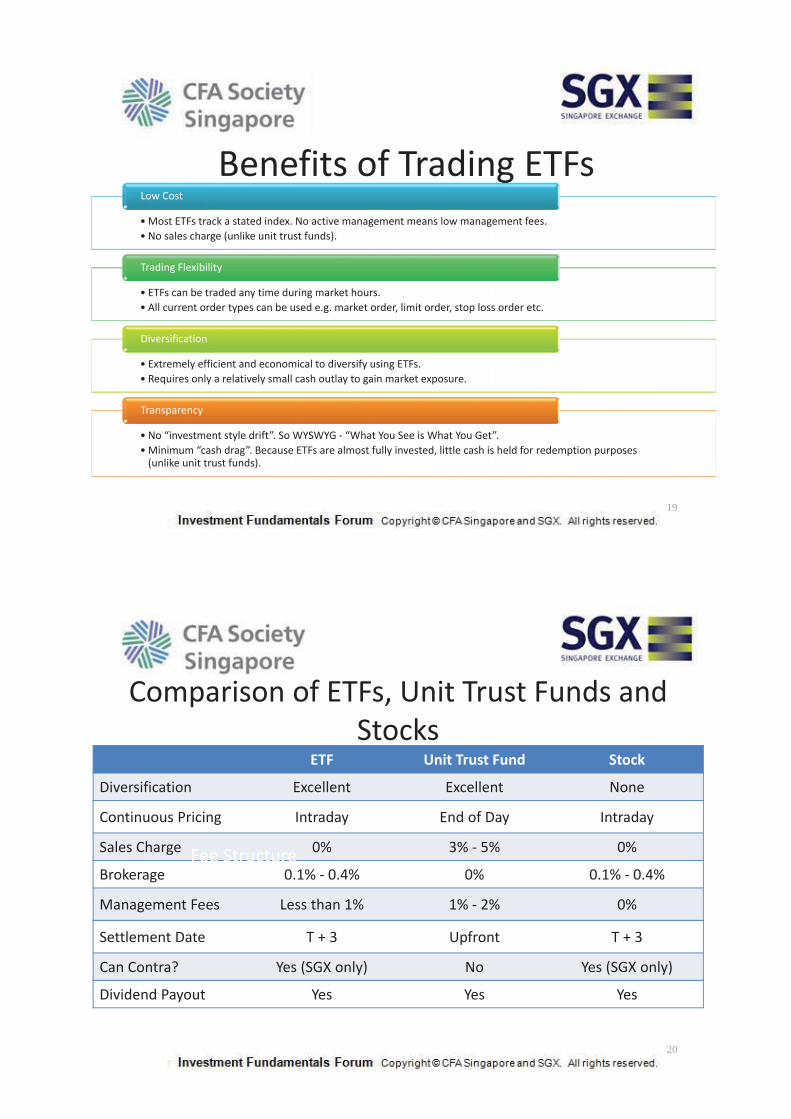

Benefits of Trading ETFs•Most ETFs track a stated index. No active management means low management fees.• No sales charge (unlike unit trust funds).

Low Cost

• ETFs can be traded any time during market hours.• All current order types can be used e.g. market order, limit order, stop loss order etc.

Trading Flexibility

• Extremely efficient and economical to diversify using ETFs.• Requires only a relatively small cash outlay to gain market exposure.

Diversification

• No “investment style drift”. So WYSWYG “What You See is What You Get”.• Minimum “cash drag”. Because ETFs are almost fully invested, little cash is held for redemption purposes(unlike unit trust funds).

Transparency

19

Comparison of ETFs, Unit Trust Funds andStocks

ETF Unit Trust Fund Stock

Diversification Excellent Excellent None

Continuous Pricing Intraday End of Day Intraday

Sales Charge 0% 3% 5% 0%

Brokerage 0.1% 0.4% 0% 0.1% 0.4%

Management Fees Less than 1% 1% 2% 0%

Settlement Date T + 3 Upfront T + 3

Can Contra? Yes (SGX only) No Yes (SGX only)

Dividend Payout Yes Yes Yes

Fee Structure

20

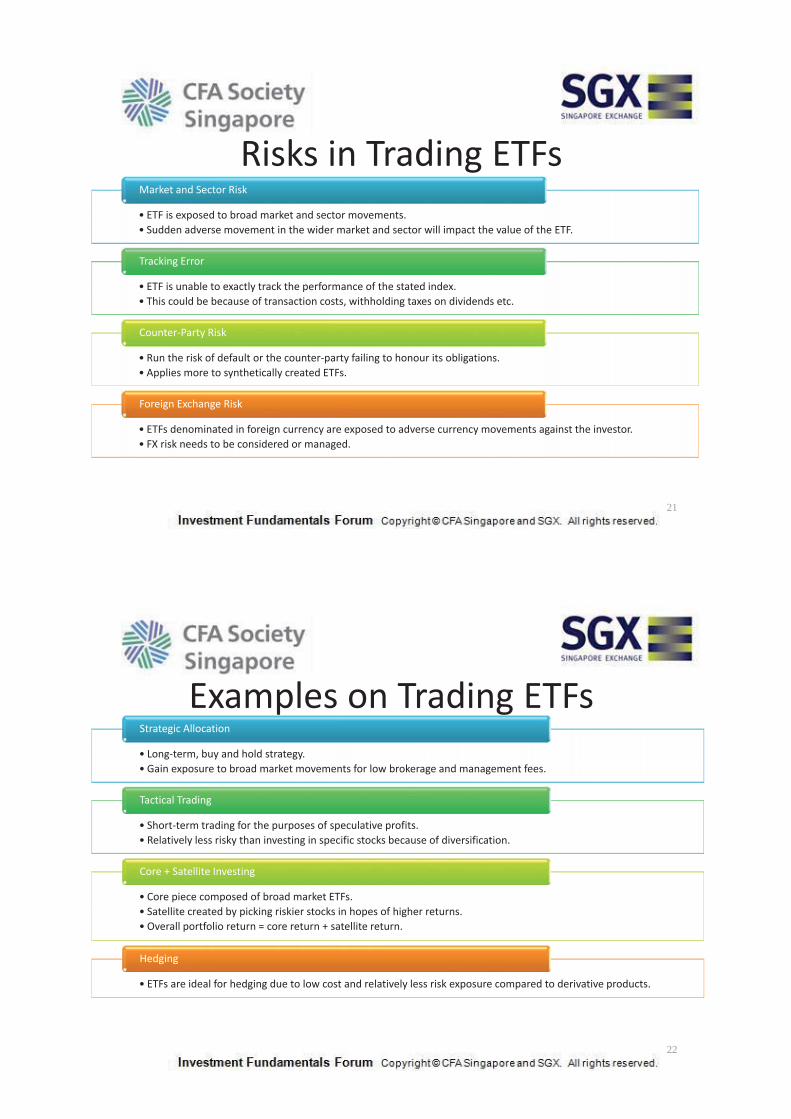

Risks in Trading ETFs•ETF is exposed to broad market and sector movements.• Sudden adverse movement in the wider market and sector will impact the value of the ETF.

Market and Sector Risk

• ETF is unable to exactly track the performance of the stated index.• This could be because of transaction costs, withholding taxes on dividends etc.

Tracking Error

• Run the risk of default or the counter party failing to honour its obligations.• Applies more to synthetically created ETFs.

Counter Party Risk

• ETFs denominated in foreign currency are exposed to adverse currency movements against the investor.• FX risk needs to be considered or managed.

Foreign Exchange Risk

21

Examples on Trading ETFs•Long term, buy and hold strategy.• Gain exposure to broad market movements for low brokerage and management fees.

Strategic Allocation

• Short term trading for the purposes of speculative profits.• Relatively less risky than investing in specific stocks because of diversification.

Tactical Trading

• Core piece composed of broad market ETFs.• Satellite created by picking riskier stocks in hopes of higher returns.• Overall portfolio return = core return + satellite return.

Core + Satellite Investing

• ETFs are ideal for hedging due to low cost and relatively less risk exposure compared to derivative products.

Hedging

22

INTRODUCTION TOSTRUCTUREDWARRANTS

23

What Are Structured Warrants?• An investment vehicle issued by financial institutions(issuers) which enable investors to:– Participate in the performance of the underlying stock.– At a fraction of its price.

• Investor’s capital is freed up for other investing ortrading purposes.

24

Types of Structured Warrants• A call warrant gives the holder the right but not theobligation to buy the underlying asset at the exerciseprice.– Increases in value if the price of the underlying goes up.

• A put warrant gives the holder the right but not theobligation to sell the underlying asset at the exerciseprice.– Increases in value if the price of the underlying drops.

25

Structured Warrant Features• Exercise price

– The predetermined price which is fixed before the warrantis listed.

• Exercise style– Structured warrants listed on SGX ST are primarilyEuropean style.

– Meaning the warrants can only be exercised on expirydate.

26

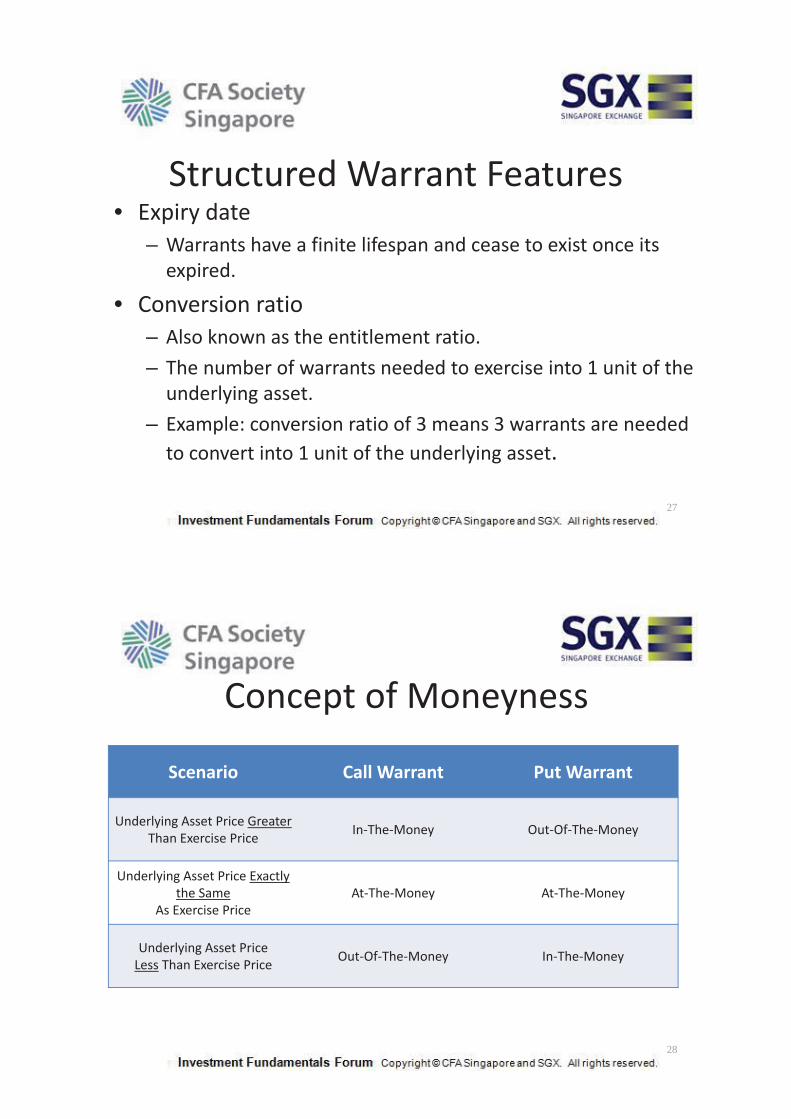

Structured Warrant Features• Expiry date

– Warrants have a finite lifespan and cease to exist once itsexpired.

• Conversion ratio– Also known as the entitlement ratio.– The number of warrants needed to exercise into 1 unit of theunderlying asset.

– Example: conversion ratio of 3 means 3 warrants are neededto convert into 1 unit of the underlying asset.

27

Concept of Moneyness

Scenario Call Warrant Put Warrant

Underlying Asset Price GreaterThan Exercise Price In The Money Out Of The Money

Underlying Asset Price Exactlythe Same

As Exercise PriceAt The Money At The Money

Underlying Asset PriceLess Than Exercise Price Out Of The Money In The Money

28

Determining the Price of a Warrant• The price of a warrant has two components:

– Intrinsic value– “Time value”

Warrant Price = Intrinsic Value + “Time Value”

29

Determining the Price of a Warrant• What is Intrinsic Value?

– Difference between the price of the underlying assetand the warrant’s exercise price when the warrant isin the money.

30

Determining the Price of a Warrant• What is “Time Value”?

– The warrant has value only when it has not reachedits expiry date.

– At expiry date, the warrant expires and is worthless.

TimeValue

Maturity

Rate of Time Decay

31

Price of a Call Warrant• For example,

– Current price of underlying asset is $4.80– Call warrant’s exercise price is $4.50– Time value of warrant is $0.40

• Intrinsic value is $0.30 ($4.80 $4.50)• Warrant price is then $0.70 ($0.40 + $0.30)

32

Price of a Put Warrant• For example,

– Current price of underlying asset is $3.00– Put warrant’s exercise price is $3.20– Time value of warrant is $0.20

• Intrinsic value is $0.20 ($3.20 $3.00)• Warrant price is then $0.40 ($0.20 + $0.20)

33

Structured Warrant Names

• Warrant name: HSI18400MBECW111129Item Term Explanation

Underlying asset HSI Hang Seng Index

Exercise price 18400 Warrant is exercisable when theHSI reaches 18,400 points.

Issuer MB Macquarie Bank

Type ECW European style Call warrant.

Expiry date 111129In YYMMDD format. The expirydate for this warrant is Nov 29th2011.

34

Benefits of Trading Structured Warrants

•Gain exposure to an underlying asset at only a fraction of its price.• Investors have complete flexibility in deciding how much leverage or gearing they need.•The greater the amount of leverage, the greater the percentage change in the warrant pricewhen the price of the underlying changes.

Leverage

•For the same amount of exposure, investors only need to pay for a fraction of underlying’sprice.

• Investor’s capital is freed up for other investing or trading purposes.

Cash Extraction

•Limited only to the amount paid for the warrants.•Potential losses from investing in the underlying asset can be much higher.•However, potential gains from call warrants are unlimited.

Limited Downside Losses

35

Benefits of Trading Structured Warrants

•Put warrants can be used as a hedge.• Especially useful for investors with long term long positions or portfolios.

Portfolio Protection

• Good selection of warrants for local and foreign stocks and indices.

Diverse Market Access

• There are no margin calls.• Cash top up is unnecessary unlike Contract for Differences (CFDs) or Options.

No Margin Calls

• No special stock picking skills needed.• Take a macro view of overall market instead.• Only exposed to market risk and not stock specific risk.• Useful for hedging purposes.

Index Warrants

36

Risks in Trading Structured Warrants

• Structured warrants have limited lifespans.• Potential gains are only realized if the warrants are in the money on the expiry date.• Investors will lose the what they had paid for the warrants if they expire at the moneyor out of the money.

Limited Lifespan

• Both potential gains and losses are magnified by the use of leverage.• However losses are only limited to what the investor had paid for the warrants.

Leverage

• Warrants are issued by financial institutions as unsecured financial instruments.• Warrant holders do not have additional protection and will be treated as any othercreditor in the event that the financial institution is unable to fulfill its obligations.

Issuer Risk

37

Risks in Trading Structured Warrants

•Investors bear the FX risk for warrants denominated in foreign currencies.• Some issuers may offer warrants “localized” into SGD on a notional 1 for 1 basis. This shieldsinvestors from FX risk.

Currency Risk

• Similar to all other types of securities, warrants are exposed to market risk.•Movements in broader market may impact the price of the underlying asset and hence the value ofthe warrants.

•Market risk also includes market forces such as the demand and supply of warrants.

Market Risk

• If the underlying asset is suspended or halted from trading, SGX may impose a similar suspension orhalt in the trading of its warrants.

•Warrant holders may not be able to exit their positions at a time of their choosing or may have toexit at a loss.

Suspension from Trading

38

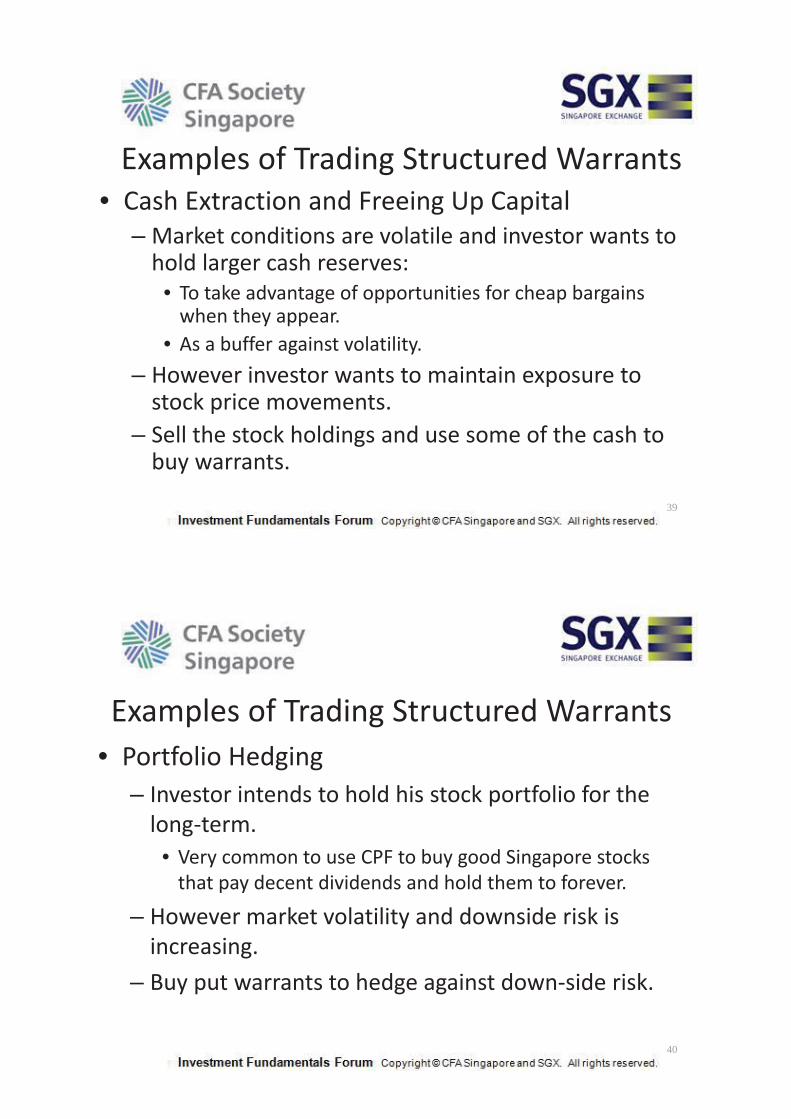

Examples of Trading Structured Warrants• Cash Extraction and Freeing Up Capital

– Market conditions are volatile and investor wants tohold larger cash reserves:

• To take advantage of opportunities for cheap bargainswhen they appear.

• As a buffer against volatility.– However investor wants to maintain exposure tostock price movements.

– Sell the stock holdings and use some of the cash tobuy warrants.

39

Examples of Trading Structured Warrants• Portfolio Hedging

– Investor intends to hold his stock portfolio for thelong term.

• Very common to use CPF to buy good Singapore stocksthat pay decent dividends and hold them to forever.

– However market volatility and downside risk isincreasing.

– Buy put warrants to hedge against down side risk.

40

INTRODUCTION TOFUTURES

41

What Is A Futures Contract?• A futures contract is an agreement to buy or sell anasset at a specified price to be delivered at somespecified future time.

• Broad categories of futures contracts:– Commodity futures

• Example: Metals, agriculture and energy related.

– Financial futures• Example: Stock indices and interest rates.

42

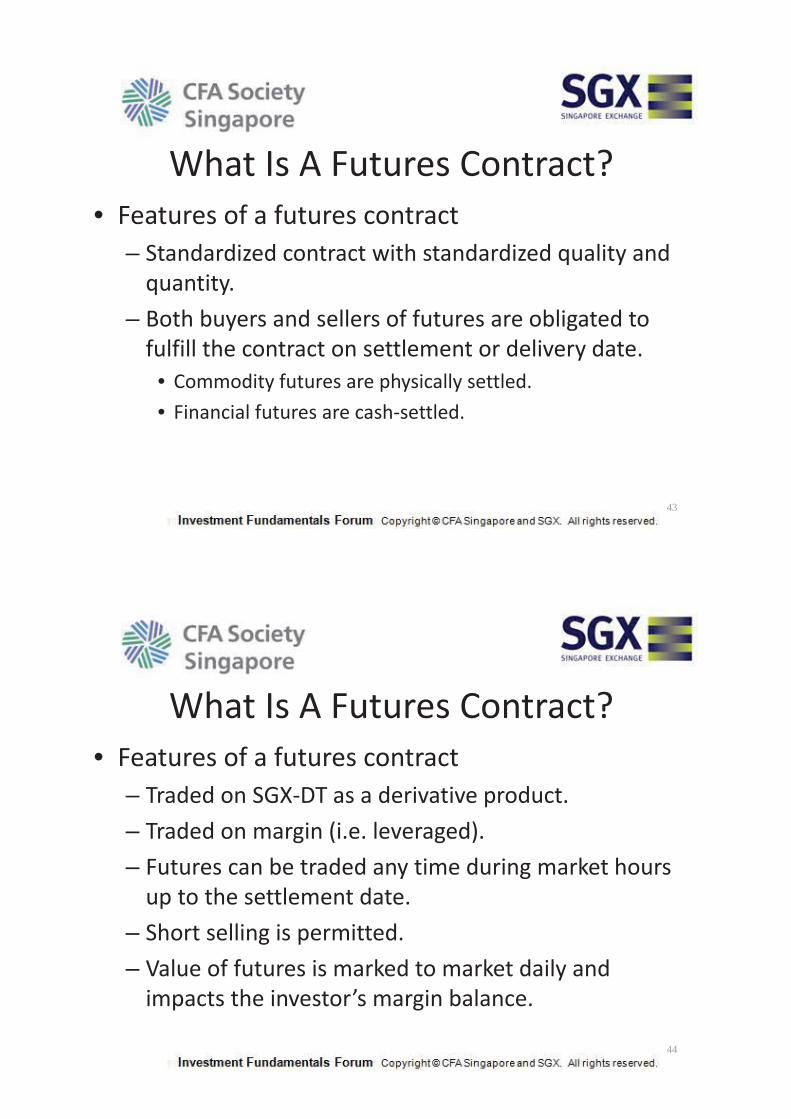

What Is A Futures Contract?• Features of a futures contract

– Standardized contract with standardized quality andquantity.

– Both buyers and sellers of futures are obligated tofulfill the contract on settlement or delivery date.

• Commodity futures are physically settled.• Financial futures are cash settled.

43

What Is A Futures Contract?• Features of a futures contract

– Traded on SGX DT as a derivative product.– Traded on margin (i.e. leveraged).– Futures can be traded any time during market hoursup to the settlement date.

– Short selling is permitted.– Value of futures is marked to market daily andimpacts the investor’s margin balance.

44

Benefits of Trading Futures Contracts•Users of the actual commodity can hedge against adverse supply situations.• For example• A maker of shoes needs to secure a steady supply of rubber for next year.• Buying a SICOM rubber futures contract ensures rubber delivery is not disrupted regardless of marketconditions in the next year.

Hedging with Commodity Futures

• Investors can take a futures position that is opposite from what they are holding.• In a perfect hedge, gains on one position will be net off by losses on the other position regardless of howthe market moves.

• Example: Sell STI index futures contracts as a hedge to a portfolio of STI component stocks.

Hedging with Financial Futures

• Buy and sell futures contracts for capital gains.• Investor buys futures if he believes prices of the underlying asset will rise.• Investor sells futures if he believes prices of the underlying asset will fall.

Speculative Trading

45

Risks in Trading Futures Contracts•Price movements in the underlying asset of a futures contract may not move closely to thevalue of shares being hedged.

•The value of the shares being hedged may not exactly equal the value of the futurescontracts.

•The hedge may then over or undershoot.

Hedging Imperfections

•Liquidity can dry up in a rapidly rising or falling market.•For example, a futures contract has risen or fallen by the maximum allowable daily limit. Nocounter party is available for investors to offset their positions.

Liquidity Risk

•Futures are traded using margins.•Both losses and gains are magnified through the leverage effect.

Leveraged Losses

46

Examples of Trading Futures Contracts• Hedging a Stock Portfolio

– An investor is holding a long term portfolio of STI componentstocks.

– The portfolio’s value is about $550,000 and the current STIindex level is 2,760.

– The investor shorts 20 contracts of the STI index futures as ahedge.

– The market corrects and on settlements date, the STI indexlevel is 2,600.

47

Examples of Trading Futures Contracts• Hedging a Stock Portfolio

– Investor’s stock portfolio has lost about $31,884 (160/ 2760 x $550,000).

– However, her futures position has gained $32,000(160 x 20 x $10).

– Investor’s net position is $116.

48

INTRODUCTION TOOPTIONS

49

What Is An Option?

• An investment vehicle developed by SGXwhich enable investors to:– Participate in the performance of the underlyingasset.

– At a fraction of its price.

• Options are similar to structured warrants butwith some key differences.

50

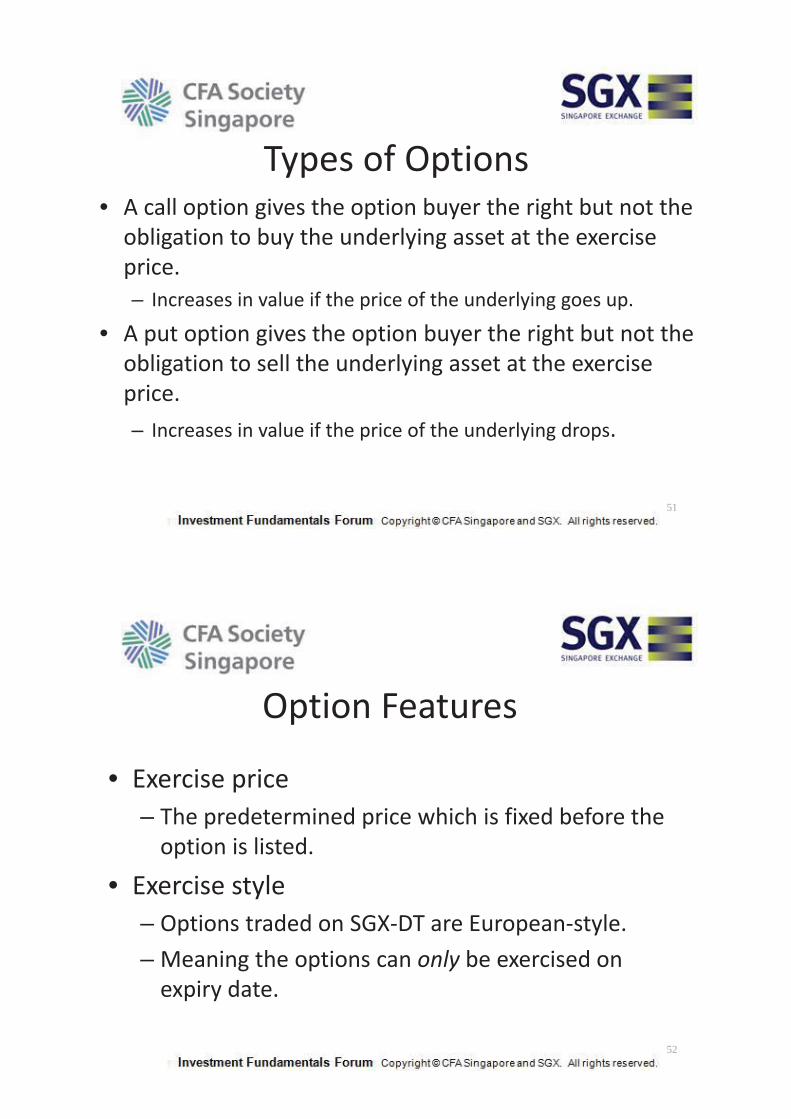

Types of Options• A call option gives the option buyer the right but not theobligation to buy the underlying asset at the exerciseprice.– Increases in value if the price of the underlying goes up.

• A put option gives the option buyer the right but not theobligation to sell the underlying asset at the exerciseprice.– Increases in value if the price of the underlying drops.

51

Option Features

• Exercise price– The predetermined price which is fixed before theoption is listed.

• Exercise style– Options traded on SGX DT are European style.– Meaning the options can only be exercised onexpiry date.

52

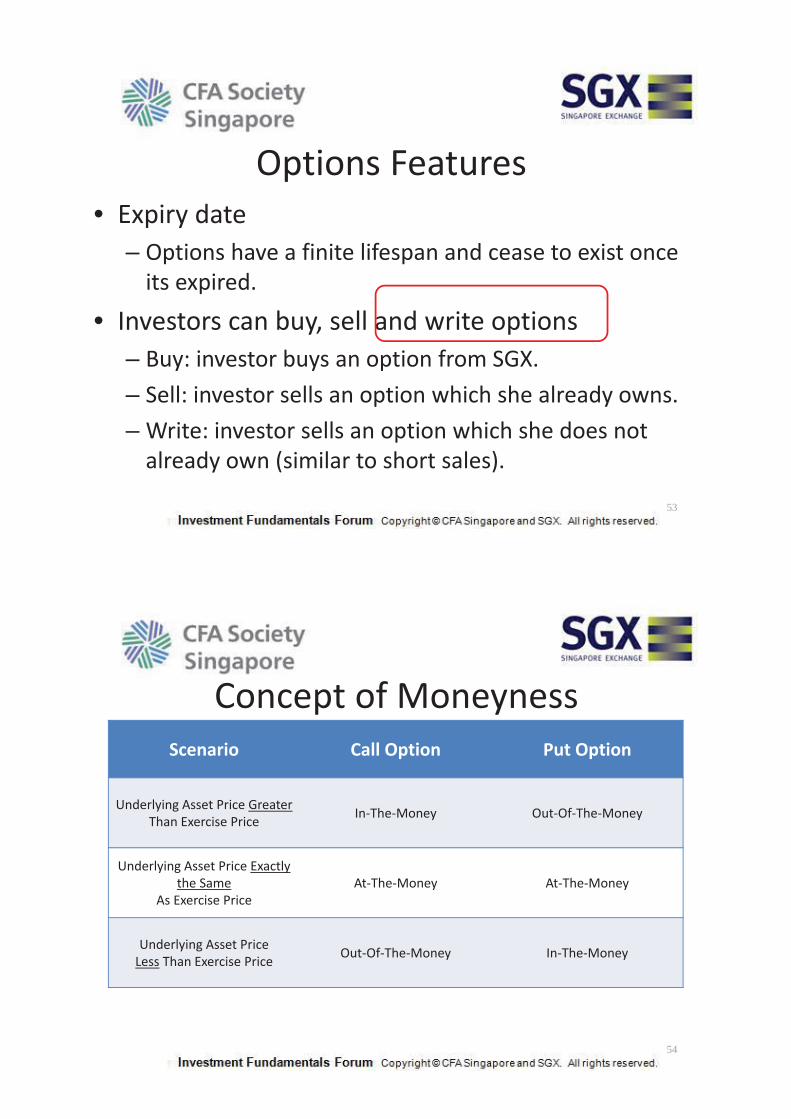

Options Features• Expiry date

– Options have a finite lifespan and cease to exist onceits expired.

• Investors can buy, sell and write options– Buy: investor buys an option from SGX.– Sell: investor sells an option which she already owns.– Write: investor sells an option which she does notalready own (similar to short sales).

53

Concept of MoneynessScenario Call Option Put Option

Underlying Asset Price GreaterThan Exercise Price In The Money Out Of The Money

Underlying Asset Price Exactlythe Same

As Exercise PriceAt The Money At The Money

Underlying Asset PriceLess Than Exercise Price Out Of The Money In The Money

54

Determining the Price of an Option• The price of an option has two components:

– Intrinsic value– Time value

Option Price = Intrinsic Value + Time Value

55

Determining the Price of an Option• What is Intrinsic Value?

– Difference between the price of the underlying assetand the option’s exercise price when the option is inthe money.

56

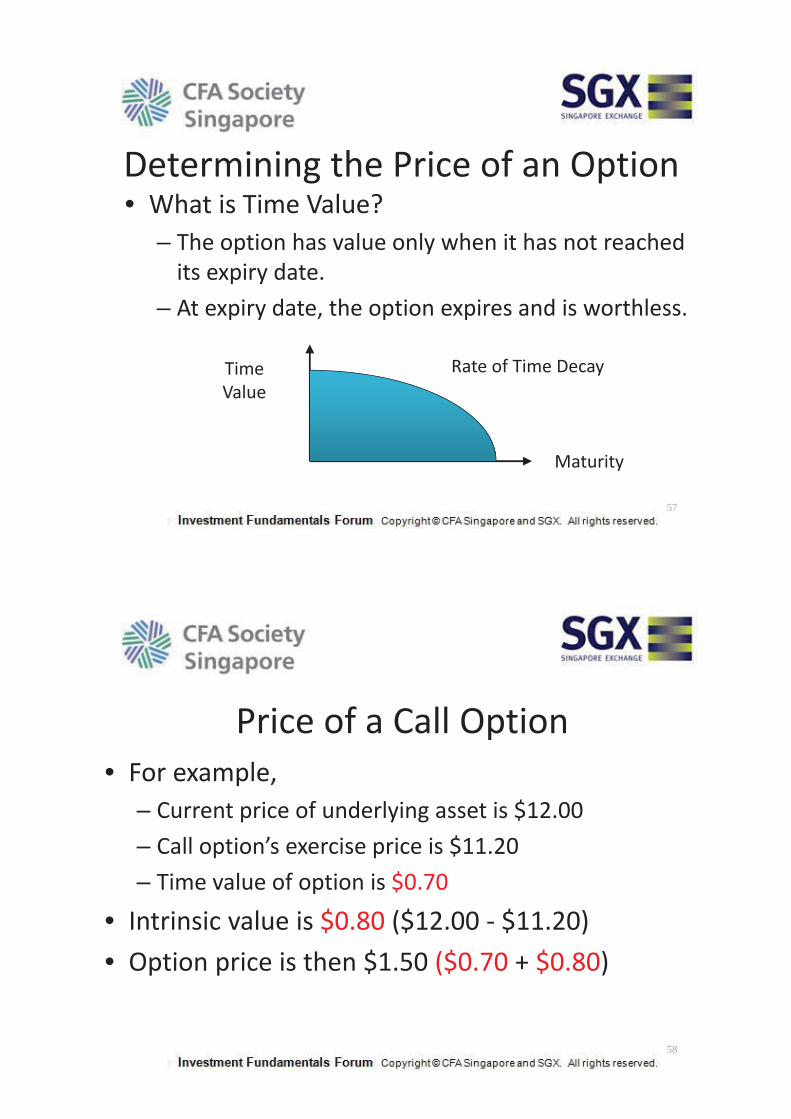

Determining the Price of an Option• What is Time Value?

– The option has value only when it has not reachedits expiry date.

– At expiry date, the option expires and is worthless.

TimeValue

Maturity

Rate of Time Decay

57

Price of a Call Option• For example,

– Current price of underlying asset is $12.00– Call option’s exercise price is $11.20– Time value of option is $0.70

• Intrinsic value is $0.80 ($12.00 $11.20)• Option price is then $1.50 ($0.70 + $0.80)

58

Price of a Put Option• For example,

– Current price of underlying asset is $6.30– Put option’s exercise price is $8.00– Time value of option is $0.30

• Intrinsic value is $1.70 ($8.00 $6.30)• Option price is then $2.00 ($0.30 + $1.70)

59

Benefits of Trading Options•Gain exposure to an underlying asset at only a fraction of its price.• Investors have complete flexibility in deciding how much leverage or gearing they need.•The greater the amount of leverage, the greater the percentage change in the Option pricewhen the price of the underlying changes.

Leverage

•For the same amount of exposure, investors only need to pay for a fraction of underlying’sprice.

• Investor’s capital is freed up for other investing or trading purposes.

Cash Extraction

•Limited only to the amount paid for the options.•Potential losses from investing in the underlying asset can be much higher.•However, option writers face unlimited liabilities and much higher potential losses.

Limited Downside Losses (Does not apply to option writers)

60

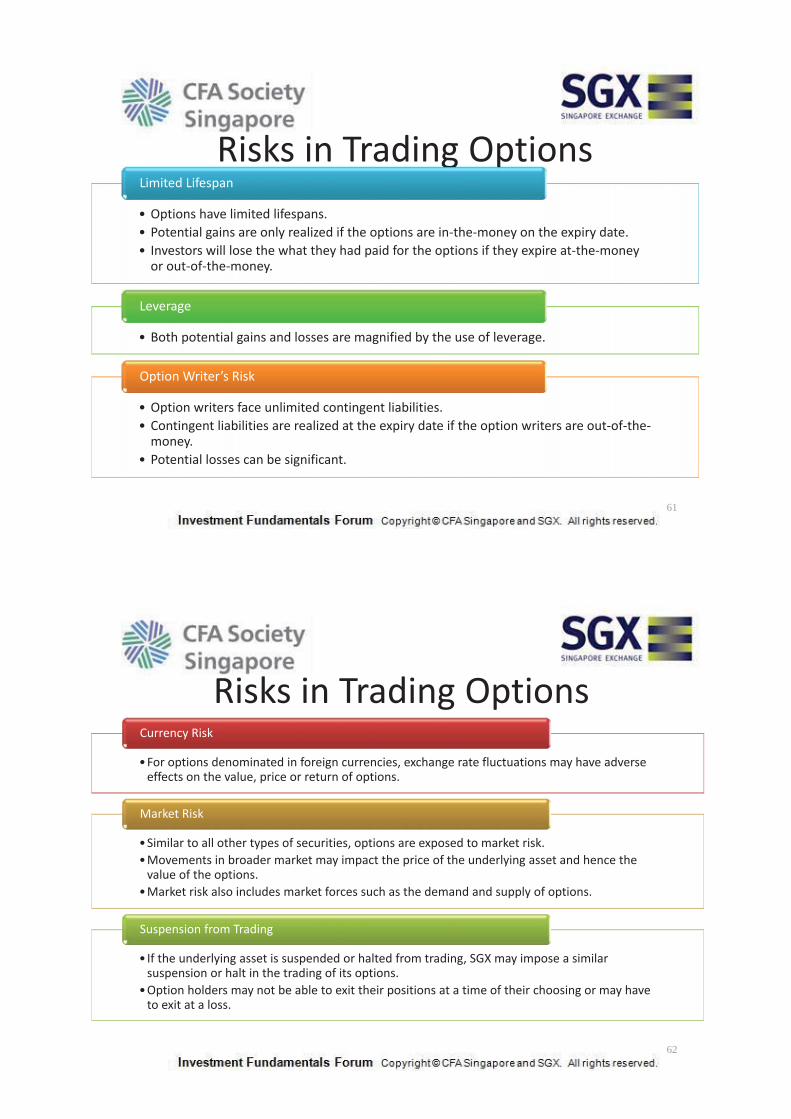

Risks in Trading Options• Options have limited lifespans.• Potential gains are only realized if the options are in the money on the expiry date.• Investors will lose the what they had paid for the options if they expire at the moneyor out of the money.

Limited Lifespan

• Both potential gains and losses are magnified by the use of leverage.

Leverage

• Option writers face unlimited contingent liabilities.• Contingent liabilities are realized at the expiry date if the option writers are out of themoney.

• Potential losses can be significant.

Option Writer’s Risk

61

Risks in Trading Options

•For options denominated in foreign currencies, exchange rate fluctuations may have adverseeffects on the value, price or return of options.

Currency Risk

•Similar to all other types of securities, options are exposed to market risk.•Movements in broader market may impact the price of the underlying asset and hence thevalue of the options.

•Market risk also includes market forces such as the demand and supply of options.

Market Risk

•If the underlying asset is suspended or halted from trading, SGX may impose a similarsuspension or halt in the trading of its options.

•Option holders may not be able to exit their positions at a time of their choosing or may haveto exit at a loss.

Suspension from Trading

62

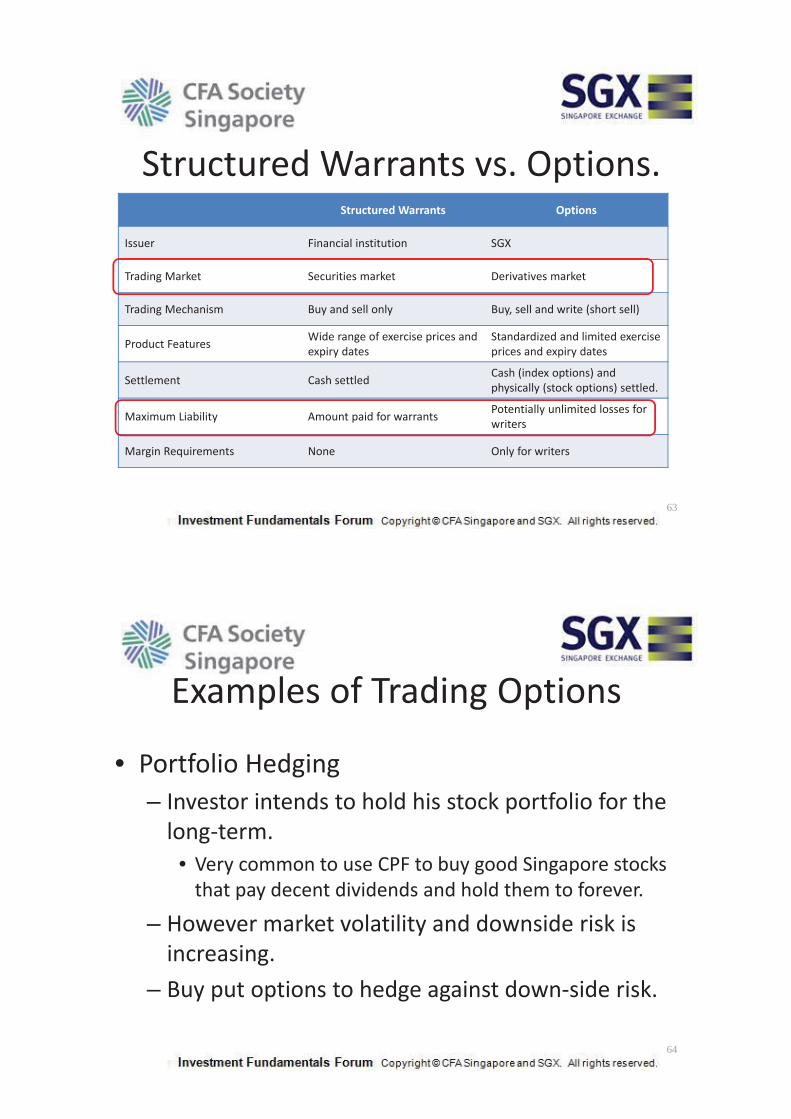

Structured Warrants vs. Options.Structured Warrants Options

Issuer Financial institution SGX

Trading Market Securities market Derivatives market

Trading Mechanism Buy and sell only Buy, sell and write (short sell)

Product Features Wide range of exercise prices andexpiry dates

Standardized and limited exerciseprices and expiry dates

Settlement Cash settled Cash (index options) andphysically (stock options) settled.

Maximum Liability Amount paid for warrants Potentially unlimited losses forwriters

Margin Requirements None Only for writers

63

Examples of Trading Options

• Portfolio Hedging– Investor intends to hold his stock portfolio for thelong term.

• Very common to use CPF to buy good Singapore stocksthat pay decent dividends and hold them to forever.

– However market volatility and downside risk isincreasing.

– Buy put options to hedge against down side risk.

64

Examples of Trading Options• Speculative Trading

– Selected basic option strategiesRising Volatility Falling Volatility

Bullish Long call option Short put option

Bearish Long put option Short call option

Undecided Long straddle Short straddle

65

INTRODUCTIONTO

CERTIFICATES

66

Discount CertLong Note + short Put

What Is A Certificate?

• A certificate is an investment product issued by athird party financial institution, offering investmentopportunities based on different market themes andexpectations.

• Requires minimal capital as compared to investingdirectly in the underlying assets.

• Price movement of certificates is transparent toinvestors.

67

Discount Certificates• Allows an investor to buy into the performance of anunderlying asset at a discount to its actual price.

• The potential gain to the investor is limited to amaximum amount called the cap strike.

• The cap strike is predetermined at the time of issueand remains constant till the expiry date.

• Discount certificates are also known as call spreadwarrants.

68

How Do Discount Certificates Work?

• Shares of OCBC Bank are trading at $8.00.• A 6 month discount certificate on OCBC with acap strike of $7.50 costs $7.00.

• So investors may get the share at $7.00 whichrepresents a discount of 12.5%.

• At the expiry date, there are 3 possiblescenarios.

69

How Do Discount Certificates Work?

• Scenario 1– Price of OCBC share is above cap strike.– Regardless of actual share price, discountcertificate is settled in cash.

– Investor is paid $7.50 (the cap strike).– Return is 7.14% ($7.50/$7.00 1)

70

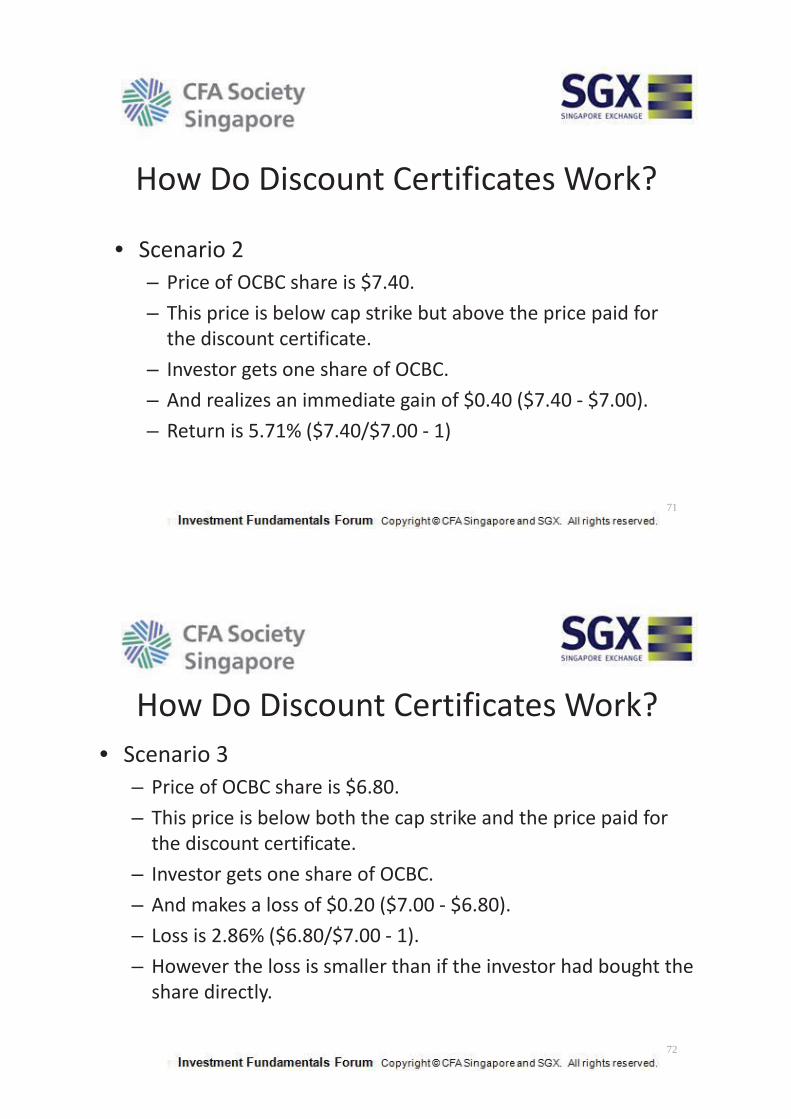

How Do Discount Certificates Work?

• Scenario 2– Price of OCBC share is $7.40.– This price is below cap strike but above the price paid forthe discount certificate.

– Investor gets one share of OCBC.– And realizes an immediate gain of $0.40 ($7.40 $7.00).– Return is 5.71% ($7.40/$7.00 1)

71

How Do Discount Certificates Work?• Scenario 3

– Price of OCBC share is $6.80.– This price is below both the cap strike and the price paid forthe discount certificate.

– Investor gets one share of OCBC.– And makes a loss of $0.20 ($7.00 $6.80).– Loss is 2.86% ($6.80/$7.00 1).– However the loss is smaller than if the investor had bought theshare directly.

72

Participation Certificates

• Essentially zero strike warrants.• Tracks the performance of the underlyingasset with no leverage.

• Enables investors to overcome foreign markettrading restrictions and settlement processes.

• All trades are settled through SGX.

73

Participation Certificates

• No time decay and no premium payments.• Investor’s gain or loss roughly equivalent to

– Gain or loss on the underlying asset and– Gain or loss on the FX rate

74

How Do Participation Certificates Work?• Value of participation certificate at any time

Value = Underlying index value x Forex rateExercise amount

• Exercise amount is a predetermined number set bythe issuer.– Remains fixed until certificate matures.

75

Daily Lock In Certificates• Daily Lock In Certificates is a structured productwith a daily accrual feature.

• Investor accumulates a lock in amount if theunderlying shares or indices perform within astipulated range.

• No accumulation of any return otherwise.

76

How Do Daily Lock In CertificatesWork?

• “Knock Out Level”– Issuer sets a pre determined level for certificates toknock out.

– Essentially means that the issuer has the right to callthe certificate.

– If this occurs, investor will get initial investment backplus any accrued lock in amount.

77

How Do Daily Lock In Certificates Work?• “Knock In Strike Level”

– Is a pre determined level set by the issuer.– On valuation date (i.e. maturity),

• If the price of the underlying asset is above the knock in strikelevel, investor gets initial investment back plus any accrued lock inamount.

• Otherwise, investor loses some of initial investment but stillreceives any accrued lock in amount.

• Investor loses all of initial investment if price of underlying falls tozero.

78

Double Chance Certificates• Double Chance Certificates is a short term investmentproduct.

• Its payout is dependent on the performance of theunderlying asset at expiry.

• Same amount of risk compared to directly investing inthe underlying stocks.

• May offer investors the chance of doubling theirinvestment returns, if held to expiry.

79

How Do Double ChanceCertificates Work?

• Determination Price– Issuer sets a pre determined level as theDetermination Price.

– At expiry,• Investor makes a return if price of underlying is above theDetermination Price.

• Otherwise, investor will receive one share of theunderlying instead.

80

How Do Double ChanceCertificates Work?

• Cap Strike– At expiry,

• If price of underlying is above Determination Price butbelow the Cap Strike, investor’s return is:

Gain = 2 x (Price of underlying – Purchase Price)

81

How Do Double ChanceCertificates Work?

• Cap Strike– At expiry,

• If price of underlying is above Determination Price andabove the Cap Strike, investor’s return is:

Gain = 2 x (Cap Strike – Purchase Price)

82

Benefits of Trading Certificates•Access to foreign markets and instruments without restrictions of foreign jurisdiction or potential high costof trading.

Diversification

• Able to increase potential returns in a flat or sideways moving market.

Yield Enhancing

•Market maker is obligated to provide liquidity at competitive bid and ask prices.• Investors can trade at any time during market hours.• Only 1 lot (1,000 units) as minimum investment.

Liquidity and Low Minimum Investment

• Cost of trading is only the brokerage fee plus a bid ask spread.• No sales charge or management fee (unlike a unit trust fund).• However, dividends on stocks is absorbed by issuers (only for participation certificates).

Low and Transparent Costs

83

Risks in Trading Certificates•Certificates are issued by third party financial institutions.• There is a risk that these institutions are unable to fulfill their obligations to settle the transactions.

Credit Risk

• Rapidly rising or falling markets may lead to a possibility of certificates holders being unable to sell hiscertificates at a reasonable price.

Liquidity Risk

• Similar to all other types of securities, certificates are exposed to market risk.• Movements in the broader market may impact the price of the underlying asset and hence the value of thecertificates.

Market Risk

• For certificates denominated in foreign currencies, exchange rate fluctuations may have adverse effects onthe value, price or return of certificates.

Exchange Rate Risk

84

INTRODUCTION TOEXCHANGE TRADED NOTES

85

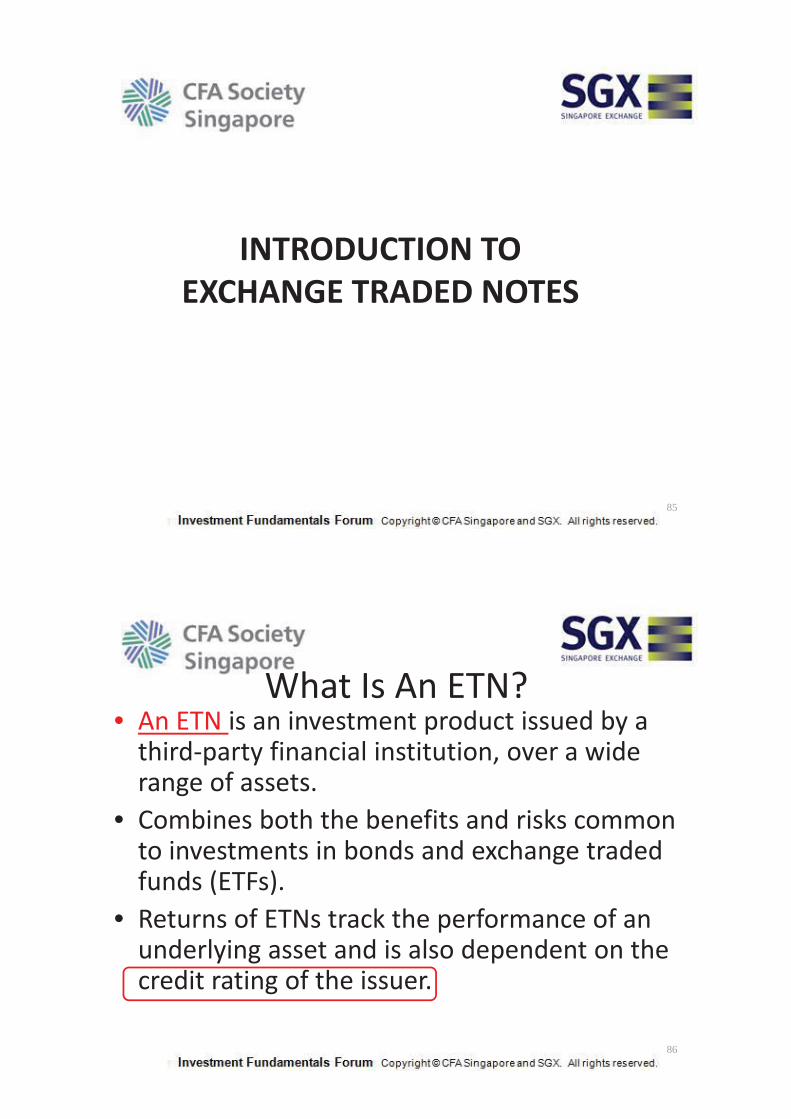

What Is An ETN?• An ETN is an investment product issued by athird party financial institution, over a widerange of assets.

• Combines both the benefits and risks commonto investments in bonds and exchange tradedfunds (ETFs).

• Returns of ETNs track the performance of anunderlying asset and is also dependent on thecredit rating of the issuer.

86

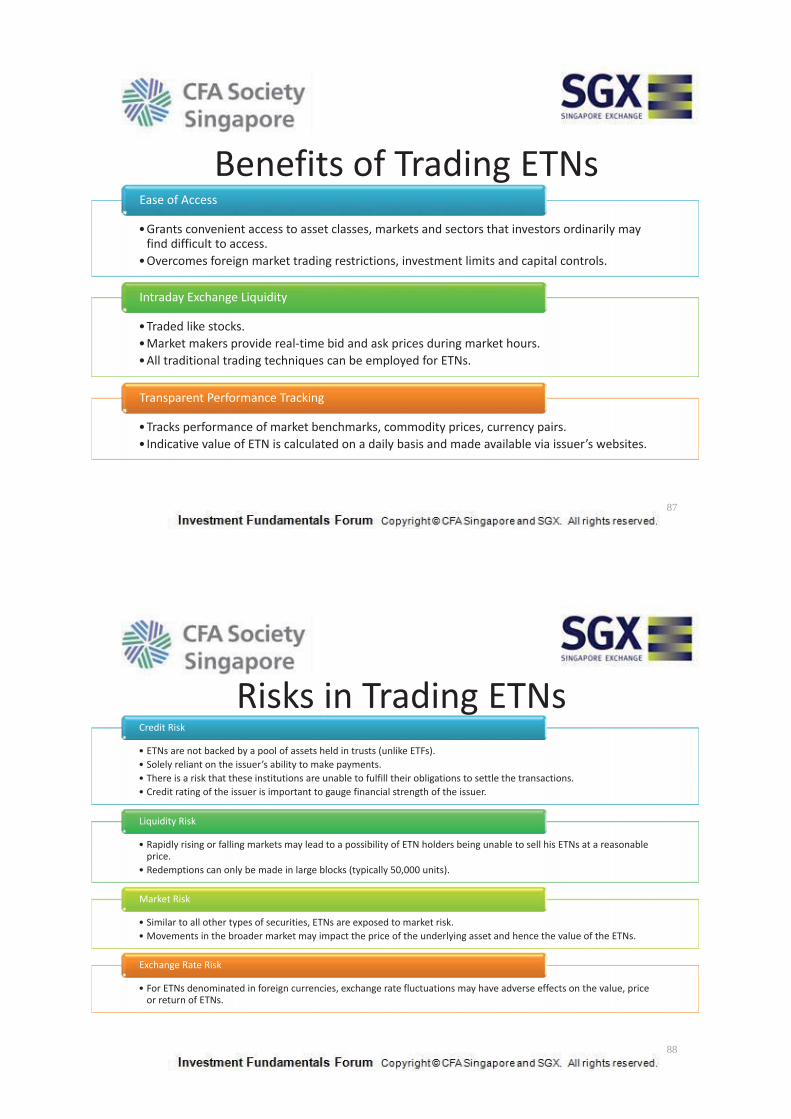

Benefits of Trading ETNs•Grants convenient access to asset classes, markets and sectors that investors ordinarily mayfind difficult to access.

•Overcomes foreign market trading restrictions, investment limits and capital controls.

Ease of Access

•Traded like stocks.•Market makers provide real time bid and ask prices during market hours.•All traditional trading techniques can be employed for ETNs.

Intraday Exchange Liquidity

•Tracks performance of market benchmarks, commodity prices, currency pairs.• Indicative value of ETN is calculated on a daily basis and made available via issuer’s websites.

Transparent Performance Tracking

87

Risks in Trading ETNs• ETNs are not backed by a pool of assets held in trusts (unlike ETFs).• Solely reliant on the issuer’s ability to make payments.• There is a risk that these institutions are unable to fulfill their obligations to settle the transactions.• Credit rating of the issuer is important to gauge financial strength of the issuer.

Credit Risk

• Rapidly rising or falling markets may lead to a possibility of ETN holders being unable to sell his ETNs at a reasonableprice.

• Redemptions can only be made in large blocks (typically 50,000 units).

Liquidity Risk

• Similar to all other types of securities, ETNs are exposed to market risk.• Movements in the broader market may impact the price of the underlying asset and hence the value of the ETNs.

Market Risk

• For ETNs denominated in foreign currencies, exchange rate fluctuations may have adverse effects on the value, priceor return of ETNs.

Exchange Rate Risk

88

End of the Session

Questions?

89