investment appraisal & company valuation for beginners

TRANSCRIPT

Learning

Company

VALUATIONSwww.antonioalcocer.com@antonioalcocer

www.antonioalcocer.com

PRESENTS

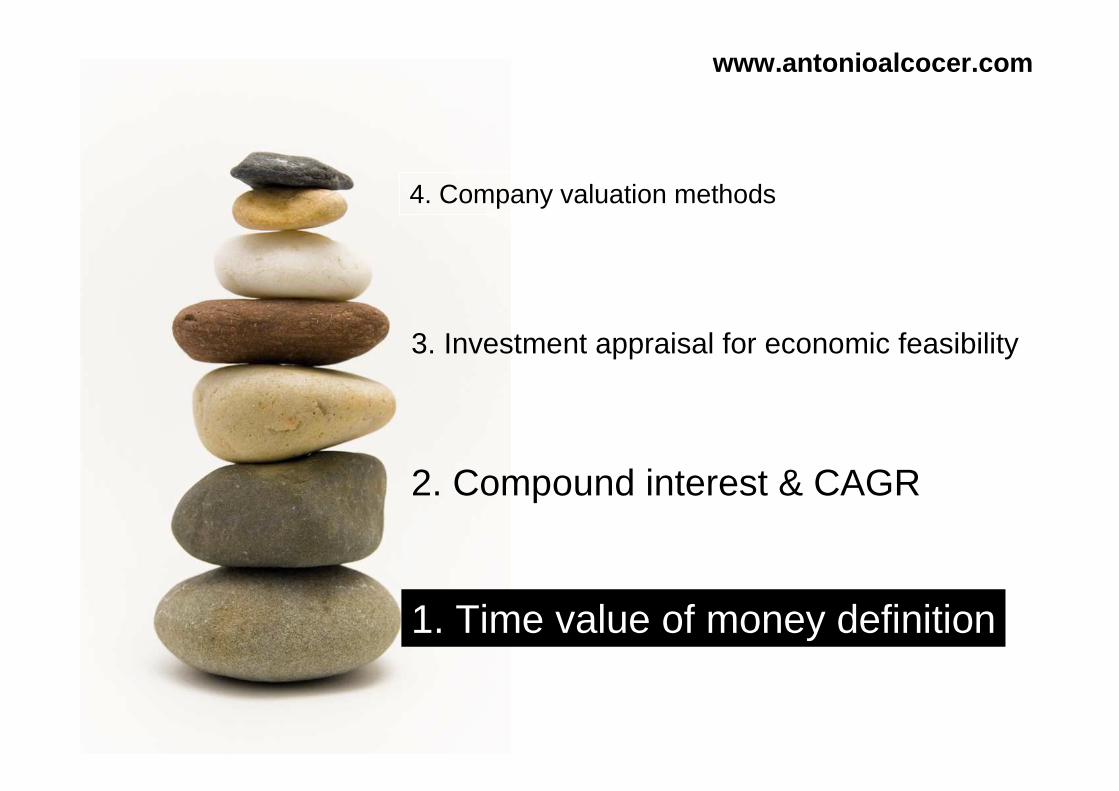

4. Company valuation methods

1. Time value of money definition

2. Compound interest & CAGR

3. Investment appraisal for economic feasibility

Why ($100, today) are not equivalent to($100, when I was younger)?

www.antonioalcocer.com

TIME VALUE OF

MONEY

www.antonioalcocer.com

*!$%?

www.antonioalcocer.com

TIME VALUE OF

MONEY

TIME VALUE OF MONEY

TIME VALUE OF MONEY

OPPORTUNITY COST

www.antonioalcocer.com

“Money can be investedtoday in different options

with a different returnovetime”

Opportunity cost

www.antonioalcocer.com

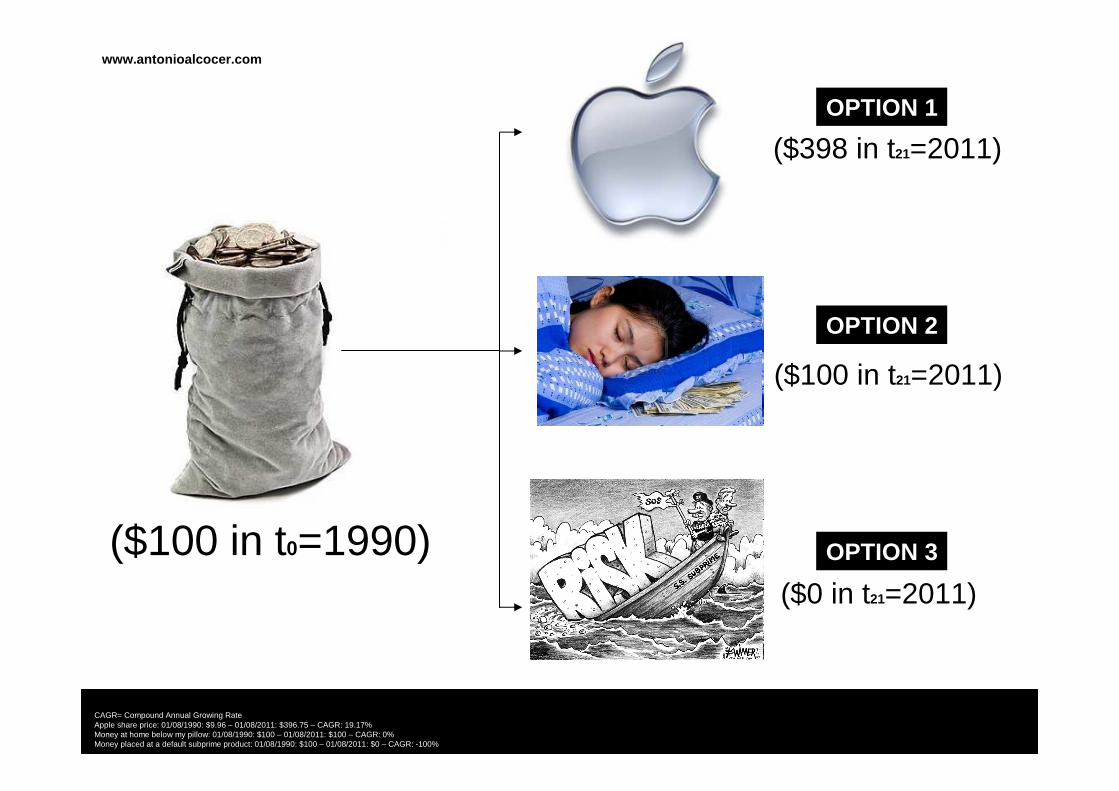

($100 in t0=1990)

CAGR= Compound Annual Growing RateApple share price: 01/08/1990: $9.96 – 01/08/2011: $396.75 – CAGR: 19.17%Money at home below my pillow: 01/08/1990: $100 – 01/08/2011: $100 – CAGR: 0%Money placed at a default subprime product: 01/08/1990: $100 – 01/08/2011: $0 – CAGR: -100%

($398 in t21=2011)

($100 in t21=2011)

($0 in t21=2011)

OPTION 1

OPTION 2

OPTION 3

www.antonioalcocer.com

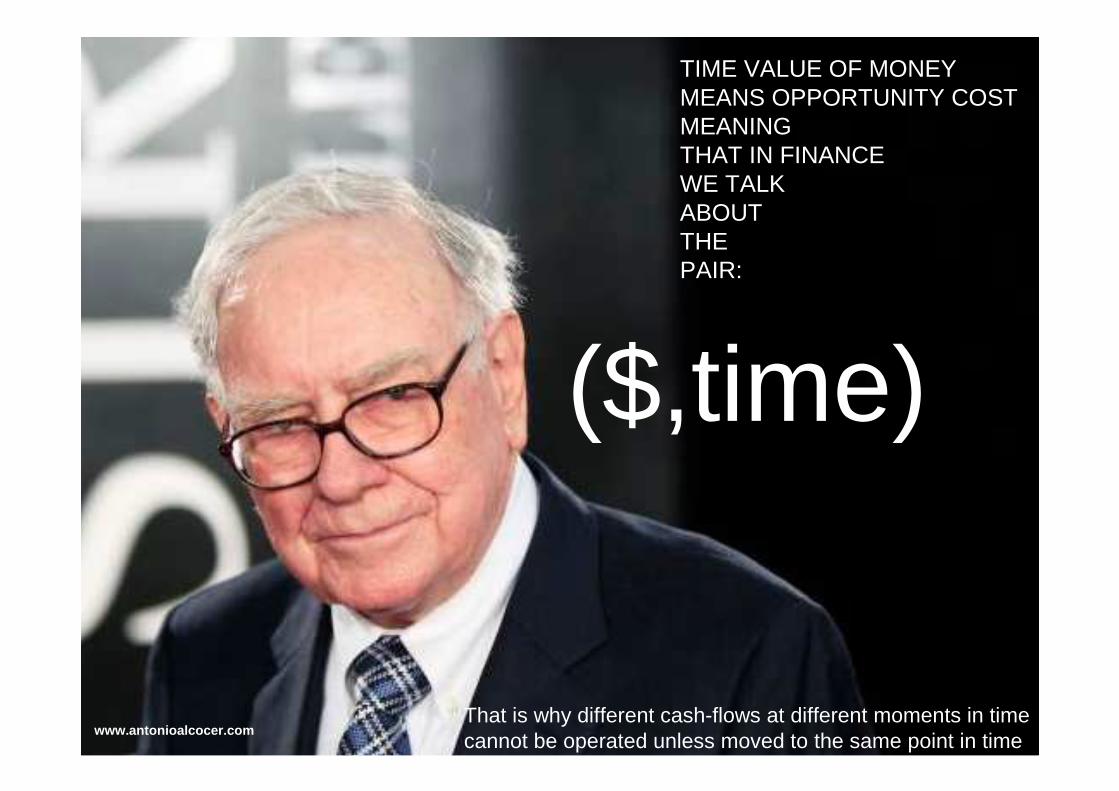

TIME VALUE OF MONEYMEANS OPPORTUNITY COSTMEANINGTHAT IN FINANCE WE TALKABOUT THEPAIR:

($,time)

That is why different cash-flows at different moments in time cannot be operated unless moved to the same point in time

www.antonioalcocer.com

How can be cash-flows

moved in time?

www.antonioalcocer.com

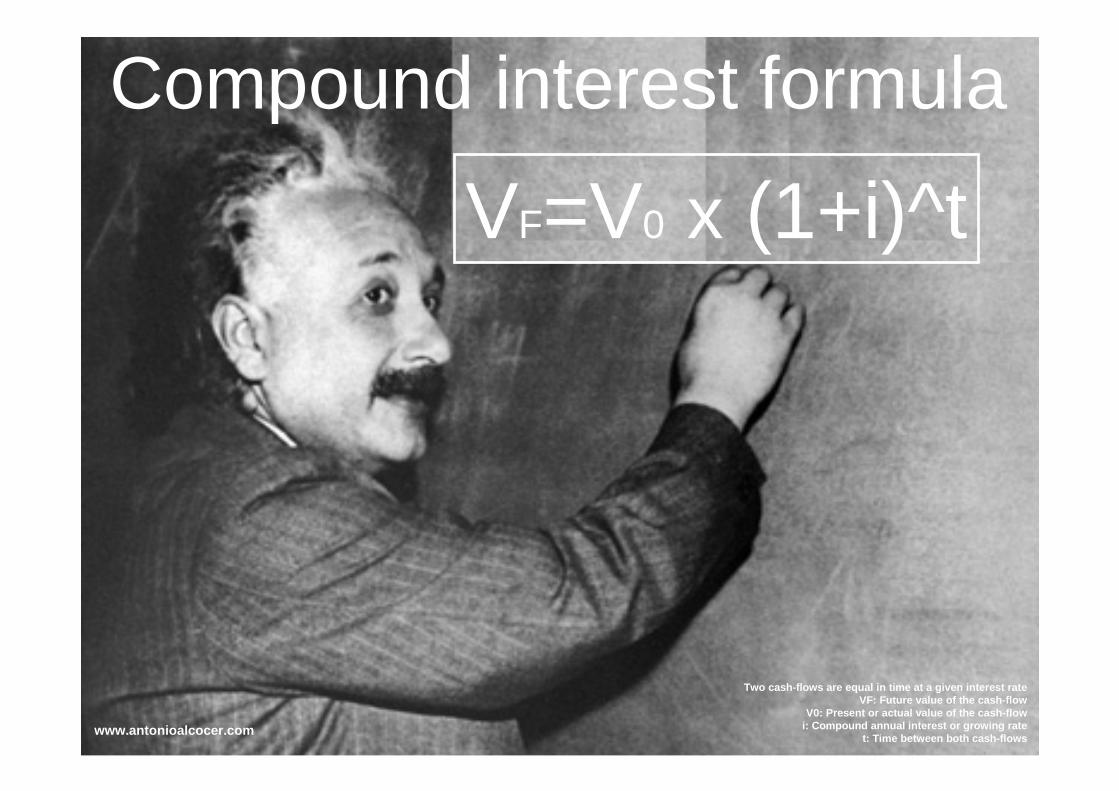

VF=V0 x (1+i)^t

Compound interest formula

Two cash-flows are equal in time at a given interest rat eVF: Future value of the cash-flow

V0: Present or actual value of the cash-flowi: Compound annual interest or growing rate

t: Time between both cash-flowswww.antonioalcocer.com

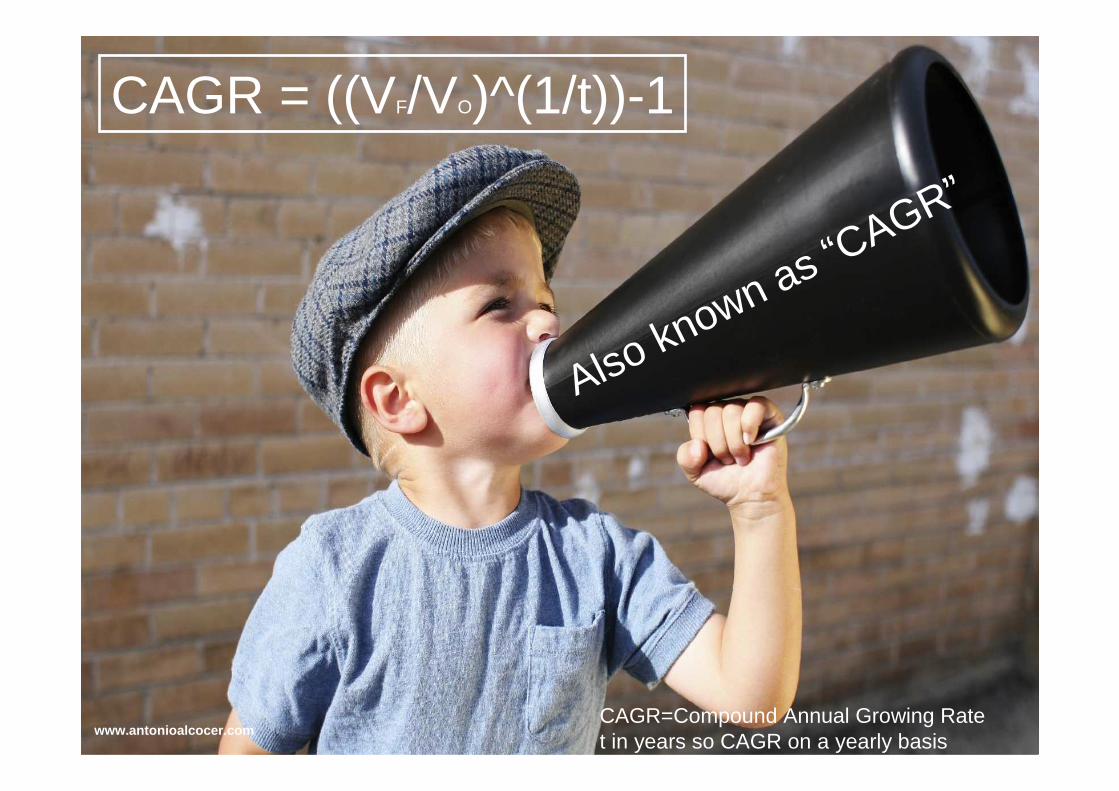

Also known as “CAGR”

CAGR=Compound Annual Growing Ratet in years so CAGR on a yearly basis

CAGR = ((VF/VO)^(1/t))-1

www.antonioalcocer.com

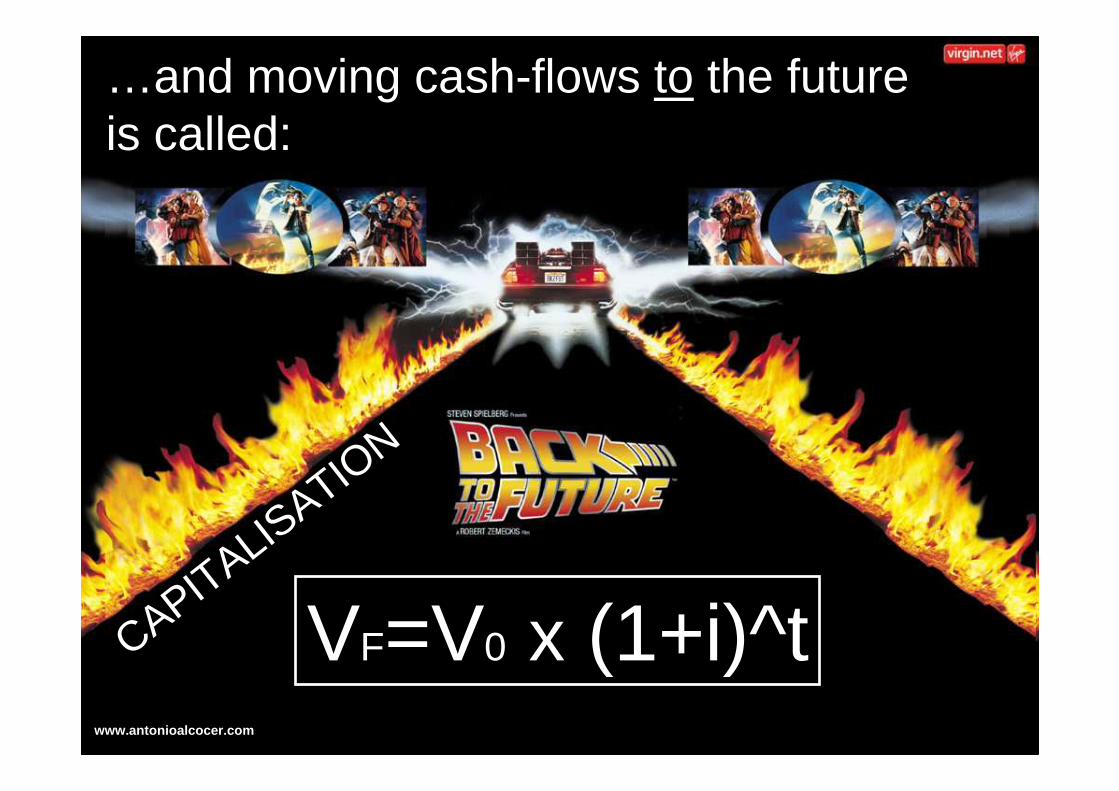

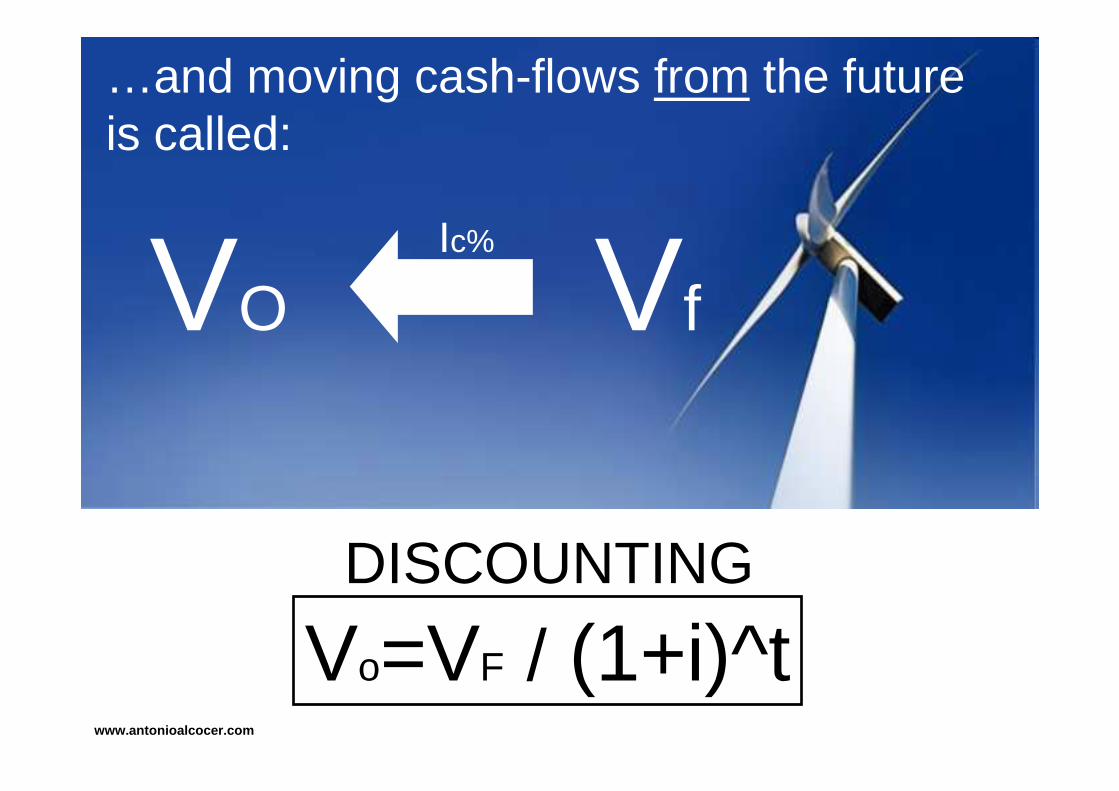

…and moving cash-flows to the futureis called:

CAPITALISATIO

N

VF=V0 x (1+i)^twww.antonioalcocer.com

VOIc%

Vo=VF / (1+i)^t

Vf

DISCOUNTING

…and moving cash-flows from the futureis called:

www.antonioalcocer.com

And what about simple interest?

www.antonioalcocer.com

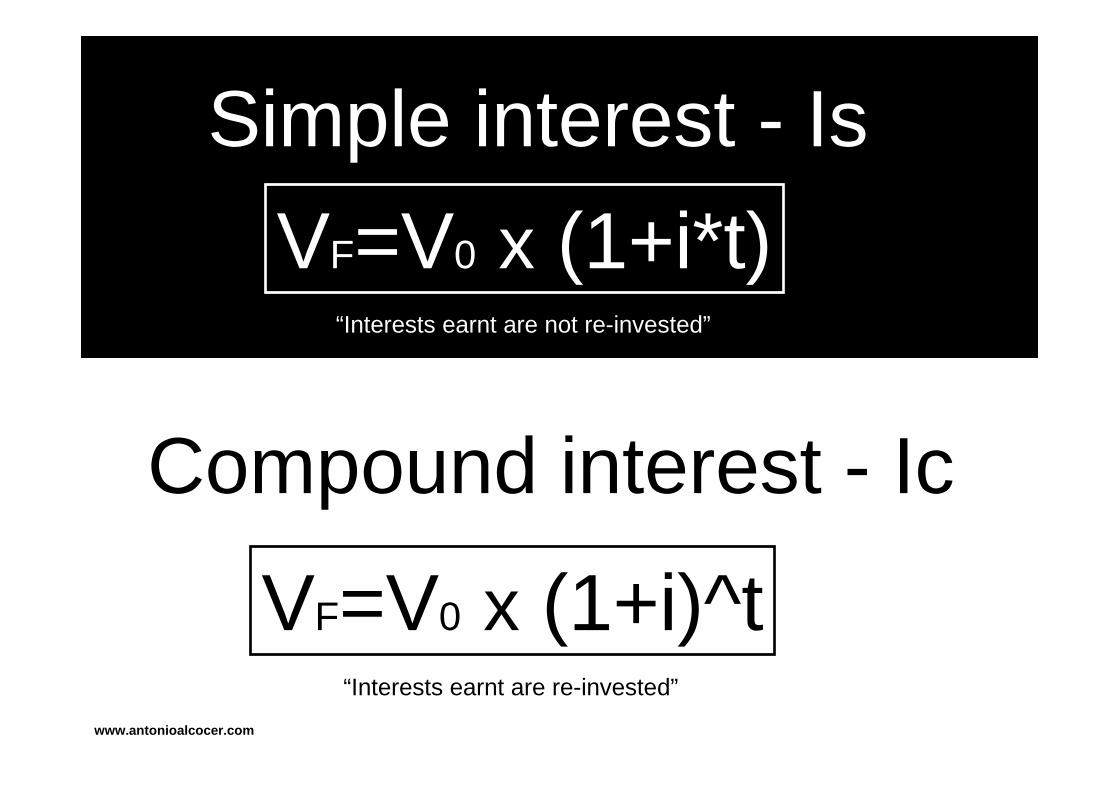

TIME VALUE OF MONEYCompound interest - Ic

VF=V0 x (1+i*t)

Simple interest - Is

VF=V0 x (1+i)^t

“Interests earnt are not re-invested”

“Interests earnt are re-invested”

www.antonioalcocer.com

www.antonioalcocer.com

Yield[annual]=12%

I12=1% I4=3%I6=2% I2=6%MONTHLY BI-MONTHLY QUARTERLY SEMI-ANNUALLY

IsBy convention yields are provided in a yearly basis IF NOT SPECIFIED

NO REINVESTMENT REINVESTMENT

Ic

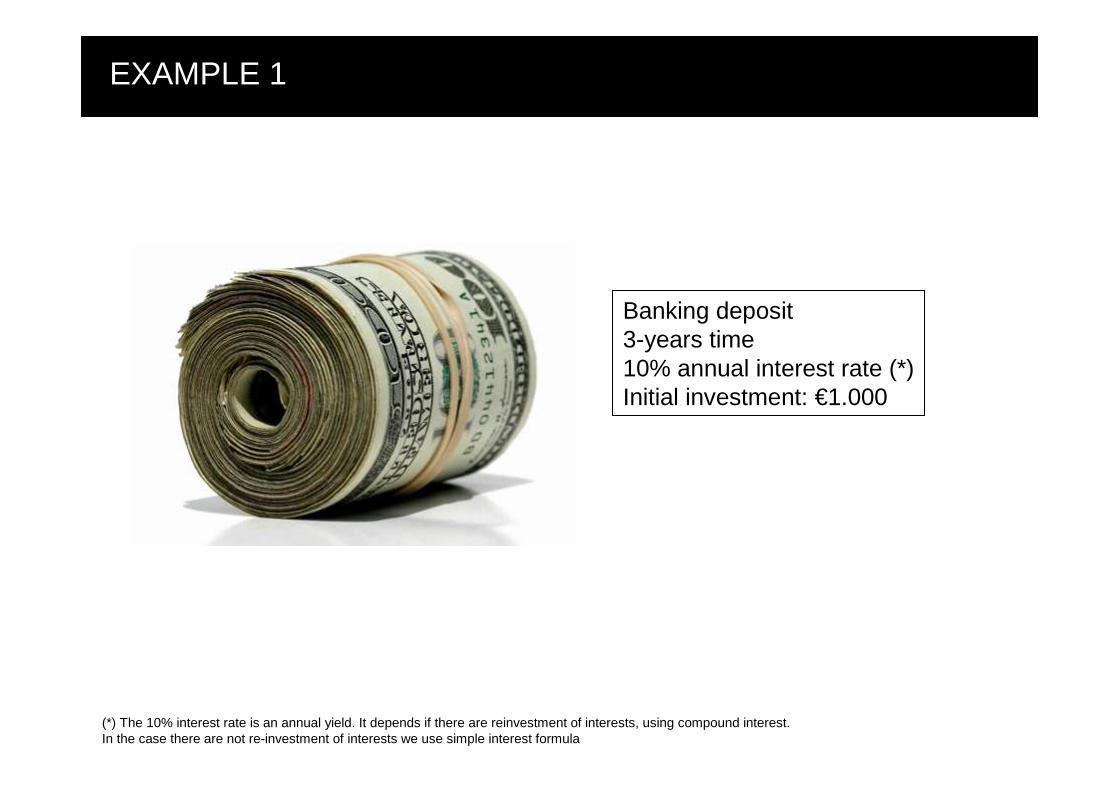

EXAMPLE 1

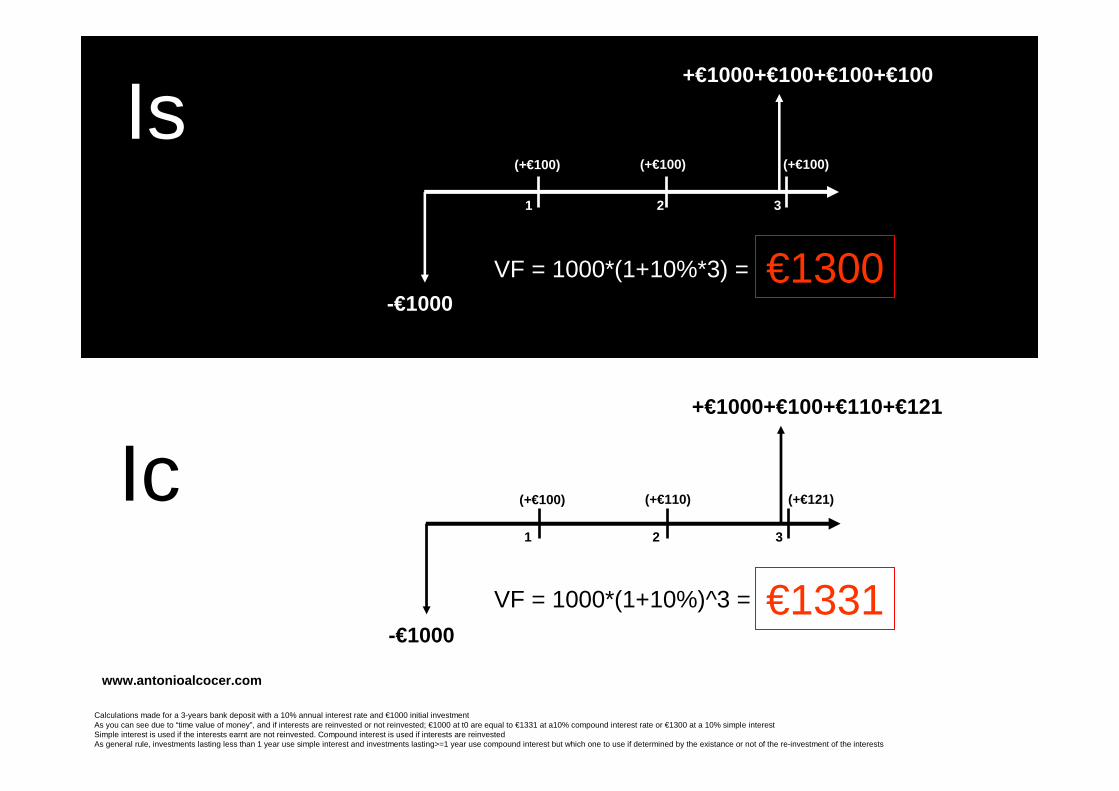

Banking deposit3-years time10% annual interest rate (*)Initial investment: €1.000

(*) The 10% interest rate is an annual yield. It depends if there are reinvestment of interests, using compound interest.In the case there are not re-investment of interests we use simple interest formula

1 2 3

-€1000

+€1000+€100+€100+€100

VF = 1000*(1+10%*3) =

Is

Ic1 2 3

-€1000

(+€100) (+€110)

+€1000+€100+€110+€121

VF = 1000*(1+10%)^3 =

Calculations made for a 3-years bank deposit with a 10% annual interest rate and €1000 initial investmentAs you can see due to “time value of money”, and if interests are reinvested or not reinvested; €1000 at t0 are equal to €1331 at a10% compound interest rate or €1300 at a 10% simple interestSimple interest is used if the interests earnt are not reinvested. Compound interest is used if interests are reinvestedAs general rule, investments lasting less than 1 year use simple interest and investments lasting>=1 year use compound interest but which one to use if determined by the existance or not of the re-investment of the interests

www.antonioalcocer.com

€1331

€1300

(+€121)

(+€100) (+€100) (+€100)

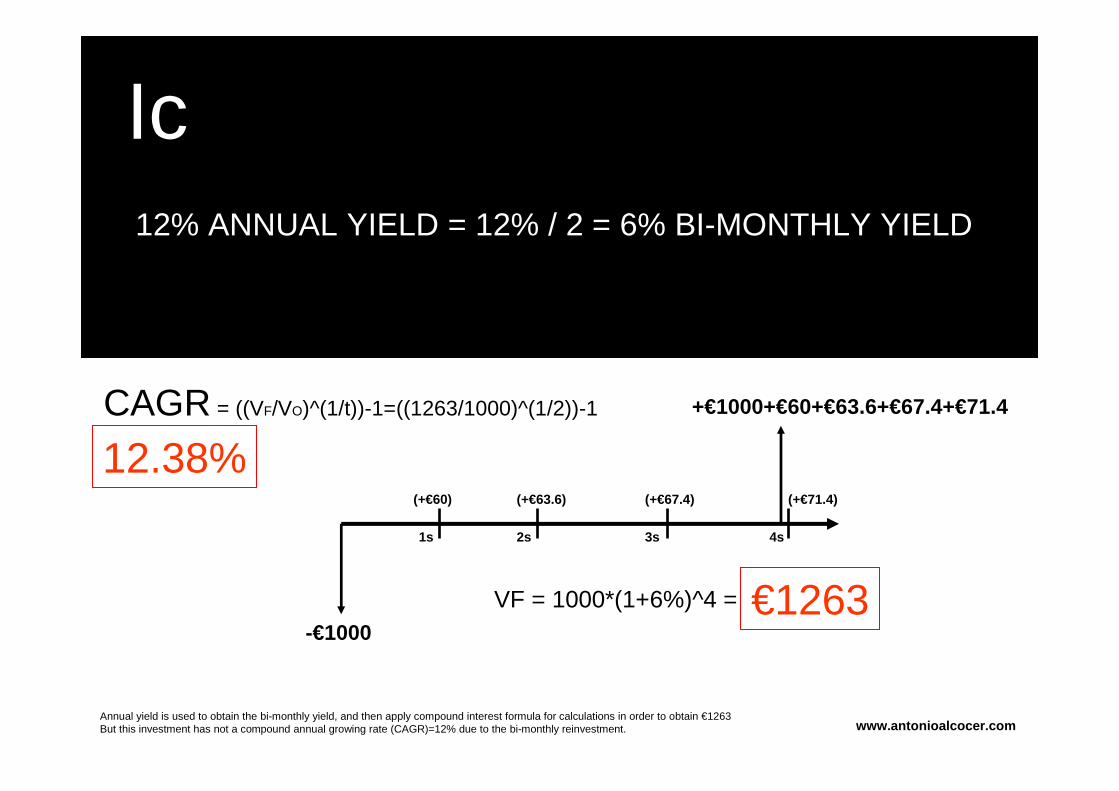

EXAMPLE 2

Banking deposit2-years time10% annual interest rateBi-monthly re-investment of interests4 semestersInitial investment: €1.000

Ic

1s 2s 3s

-€1000

(+€63.6) (+€67.4)

+€1000+€60+€63.6+€67.4+€71.4

VF = 1000*(1+6%)^4 =

www.antonioalcocer.com

€1263

(+€71.4)

4s

12% ANNUAL YIELD = 12% / 2 = 6% BI-MONTHLY YIELD

(+€60)

Annual yield is used to obtain the bi-monthly yield, and then apply compound interest formula for calculations in order to obtain €1263But this investment has not a compound annual growing rate (CAGR)=12% due to the bi-monthly reinvestment.

CAGR = ((VF/VO)^(1/t))-1=((1263/1000)^(1/2))-1

12.38%

but as a general rule in finance we assume…

www.antonioalcocer.com

…reinvestment of interests& use compound interest!

www.antonioalcocer.com

www.antonioalcocer.com

Compound interest’s power it’s oneof the strongest powers on EarthAlbert Einstein

www.antonioalcocer.com

t0=30

Vf$337.494

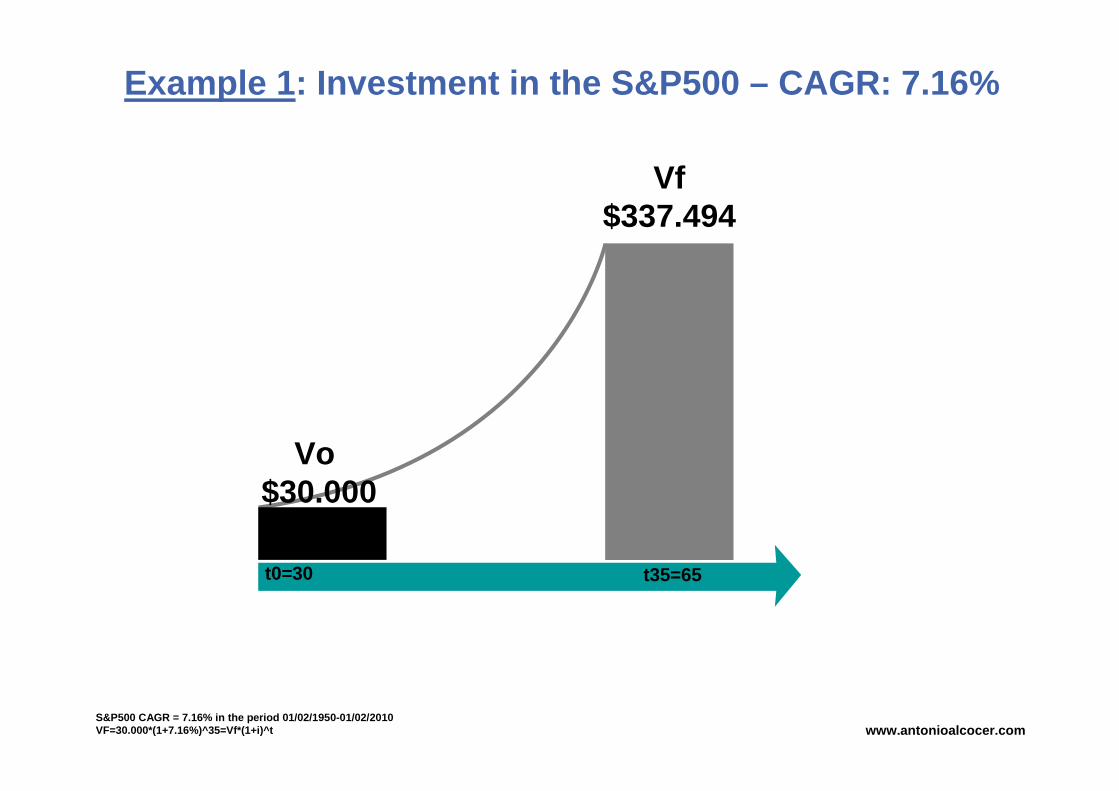

Example 1 : Investment in the S&P500 – CAGR: 7.16%

Vo $30.000

t35=65

S&P500 CAGR = 7.16% in the period 01/02/1950-01/02/201 0VF=30.000*(1+7.16%)^35=Vf*(1+i)^t www.antonioalcocer.com

You better wouldhave invested in Berkshire Hathway- Oracle of Omaha’s word -

www.antonioalcocer.com

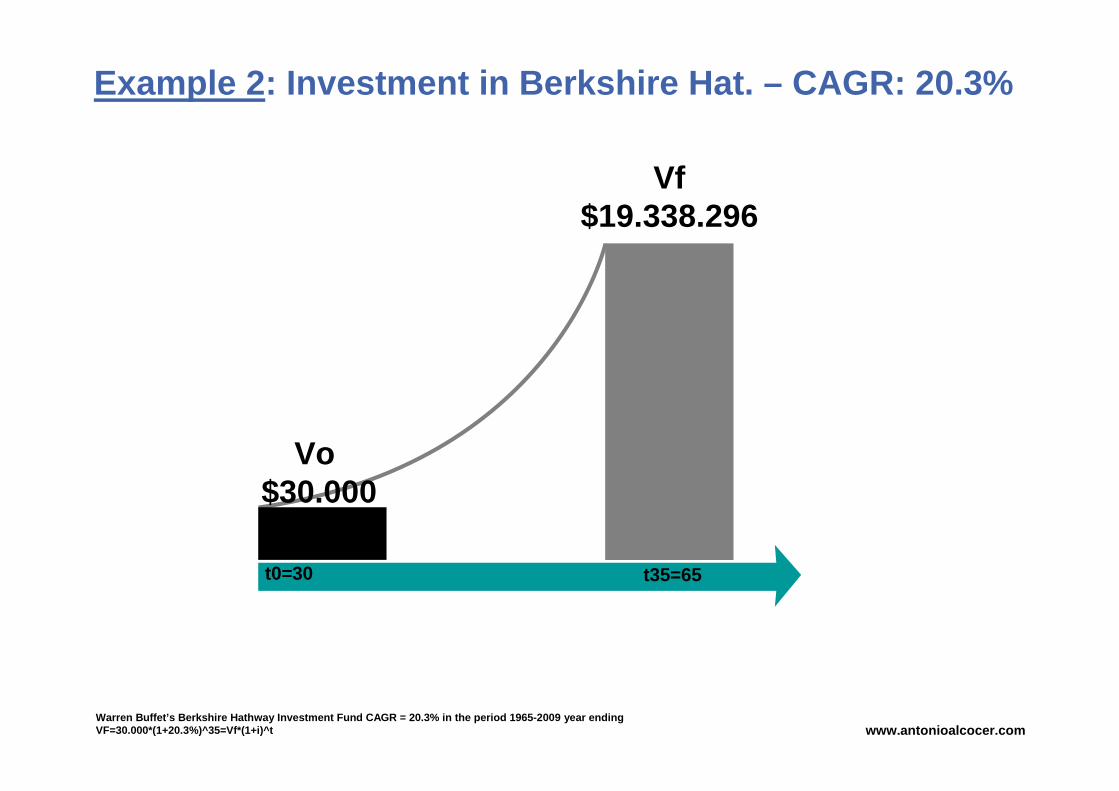

t0=30

Vf$19.338.296

Example 2 : Investment in Berkshire Hat. – CAGR: 20.3%

Vo $30.000

t35=65

Warren Buffet’s Berkshire Hathway Investment Fund CAGR = 20.3% in the period 1965-2009 year endingVF=30.000*(1+20.3%)^35=Vf*(1+i)^t www.antonioalcocer.com

I rather go for Apples

- Get back soon Steve! -www.antonioalcocer.com

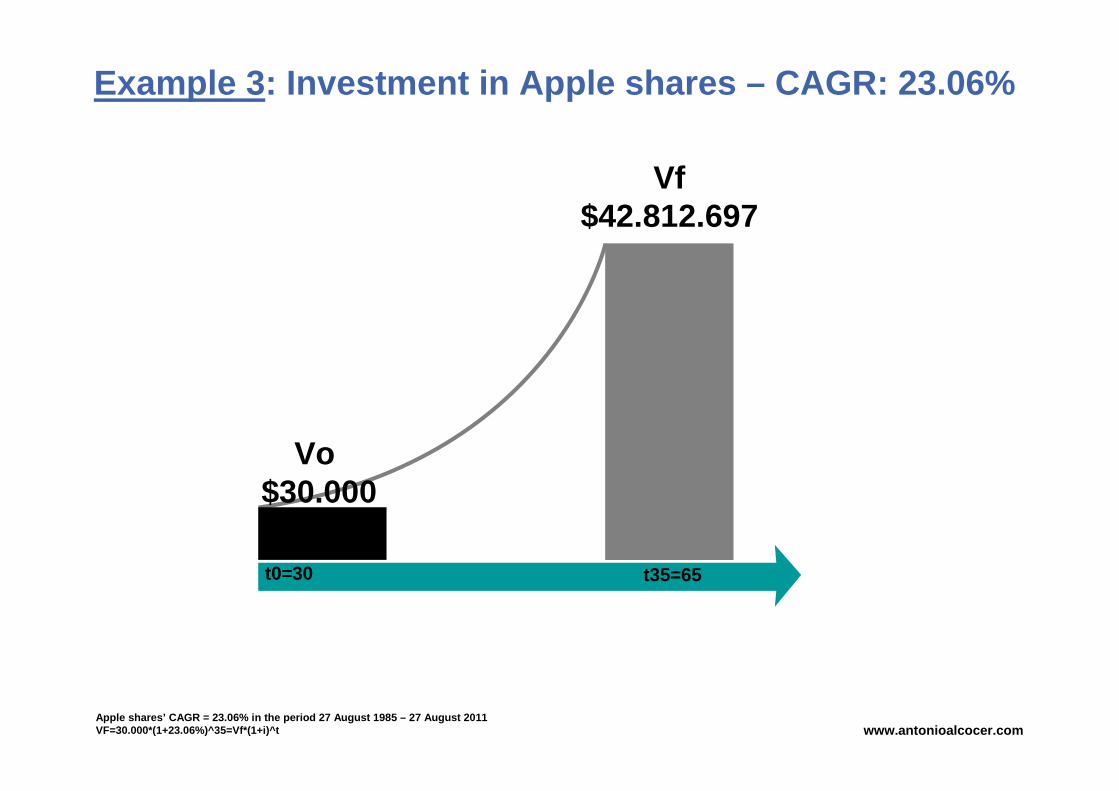

t0=30

Vf$42.812.697

Example 3 : Investment in Apple shares – CAGR: 23.06%

Vo $30.000

t35=65

Apple shares’ CAGR = 23.06% in the period 27 August 19 85 – 27 August 2011VF=30.000*(1+23.06%)^35=Vf*(1+i)^t www.antonioalcocer.com

*!$%?

REDBUBBLE.COM

$42.812.697?

www.antonioalcocer.com

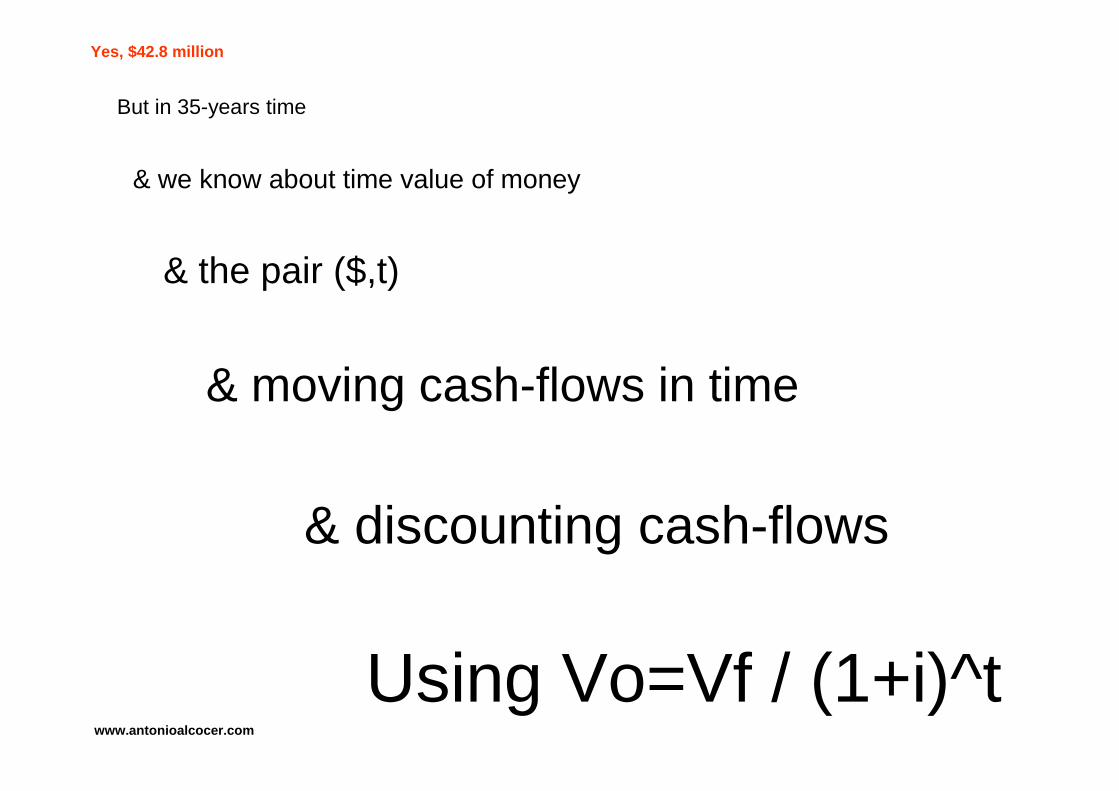

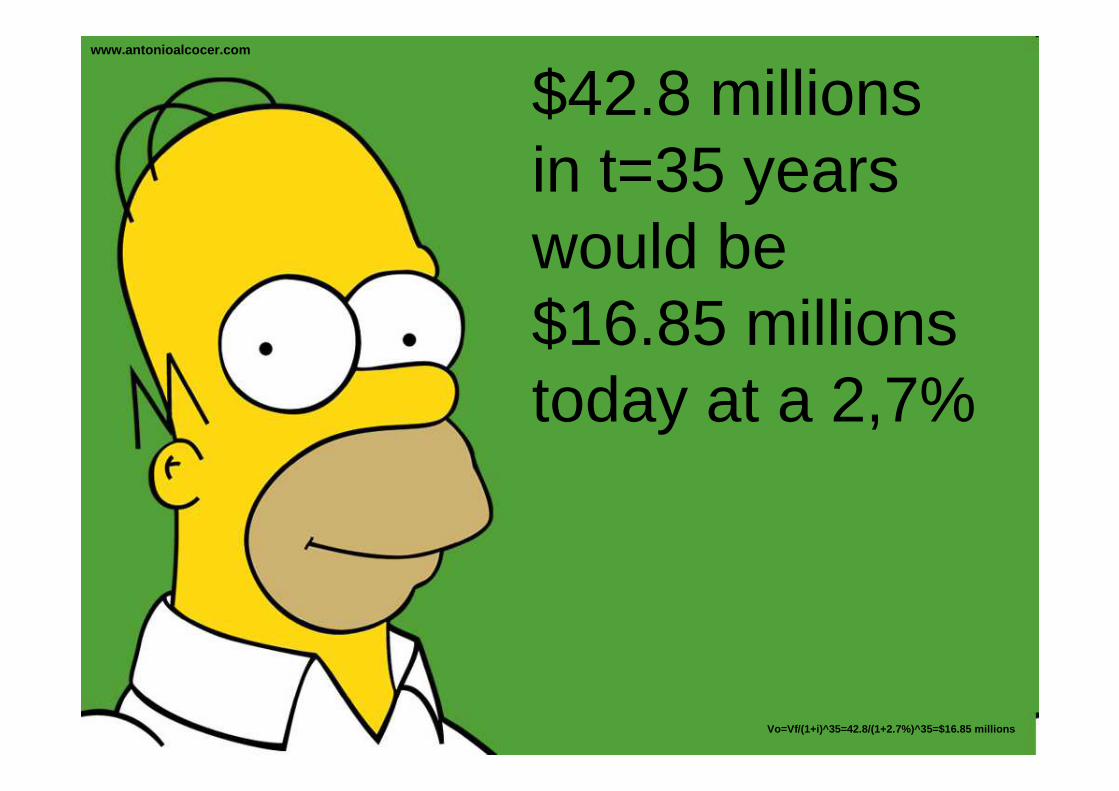

Yes, $42.8 million

But in 35-years time

& we know about time value of money

& the pair ($,t)

& moving cash-flows in time

& discounting cash-flows

Using Vo=Vf / (1+i)^twww.antonioalcocer.com

So you are telling me that today I would not beworthy $42.8 million?

www.antonioalcocer.com

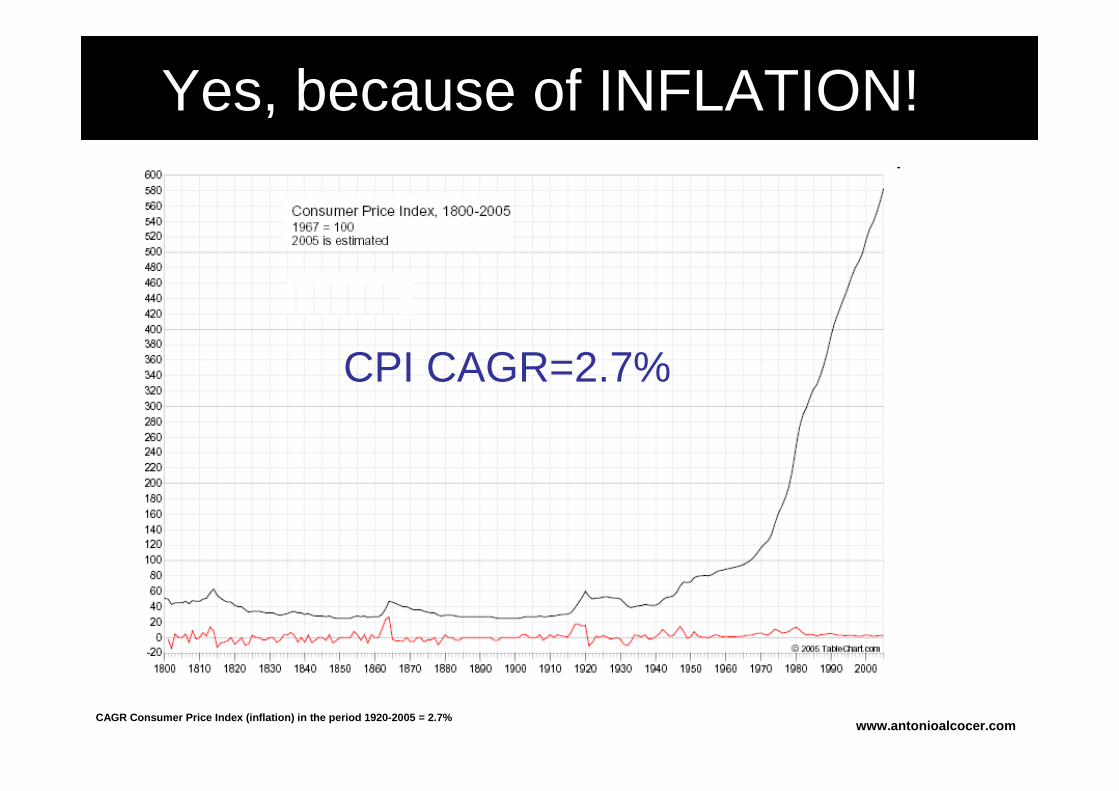

Yes, because of INFLATION!

CAGR Consumer Price Index (inflation) in the period 192 0-2005 = 2.7%

CPI CAGR=2.7%

www.antonioalcocer.com

$42.8 millionsin t=35 yearswould be$16.85 millionstoday at a 2,7%

Vo=Vf/(1+i)^35=42.8/(1+2.7%)^35=$16.85 millions

www.antonioalcocer.com

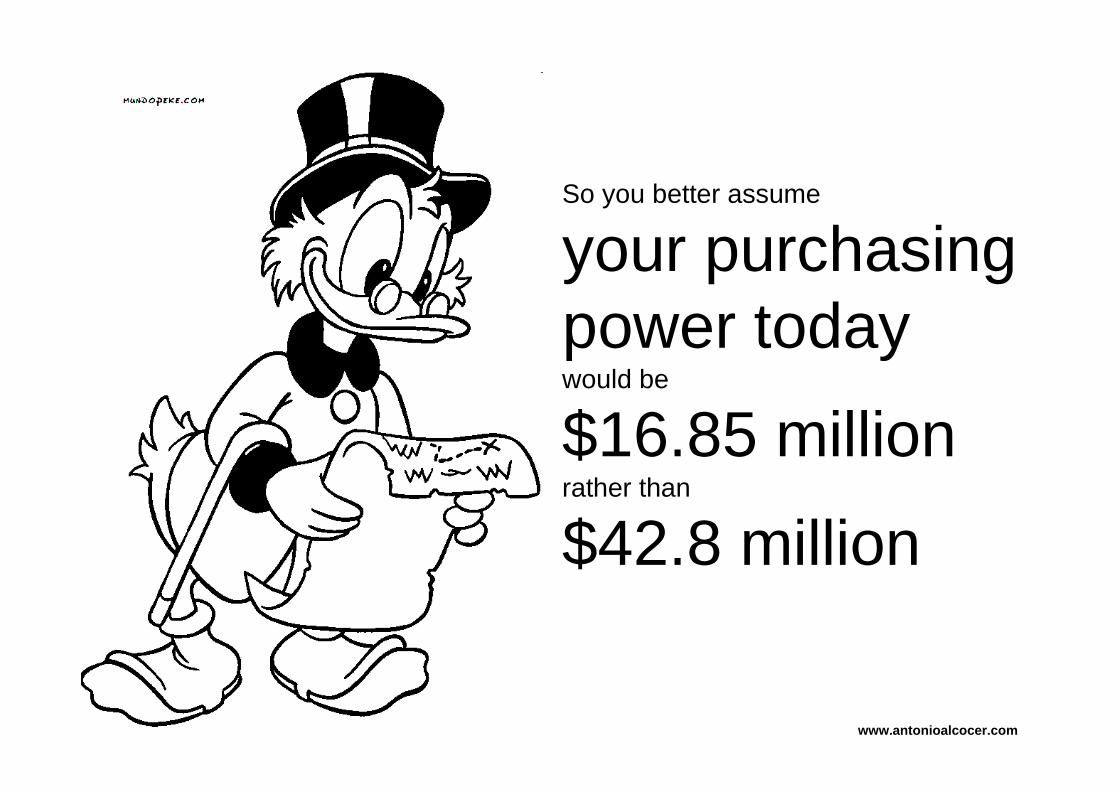

So you better assume

your purchasingpower todaywould be

$16.85 millionrather than

$42.8 million

www.antonioalcocer.com

Yes, if you would have invested in Apples

HAVE YOU?www.antonioalcocer.com

NowWe are ready to understandInvestment appraisal methodsUsed in Finance to studyThe economic feasibilityOf a project

www.antonioalcocer.com

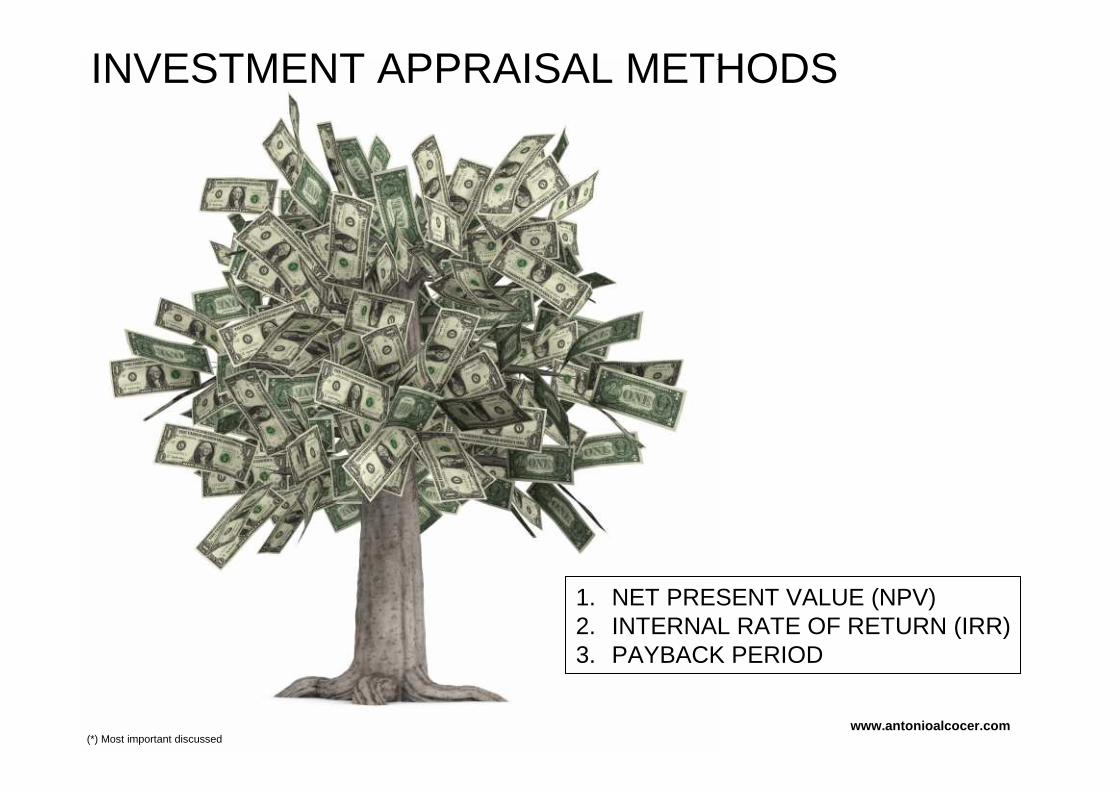

INVESTMENT APPRAISAL METHODS

1. NET PRESENT VALUE (NPV)2. INTERNAL RATE OF RETURN (IRR)3. PAYBACK PERIOD

(*) Most important discussedwww.antonioalcocer.com

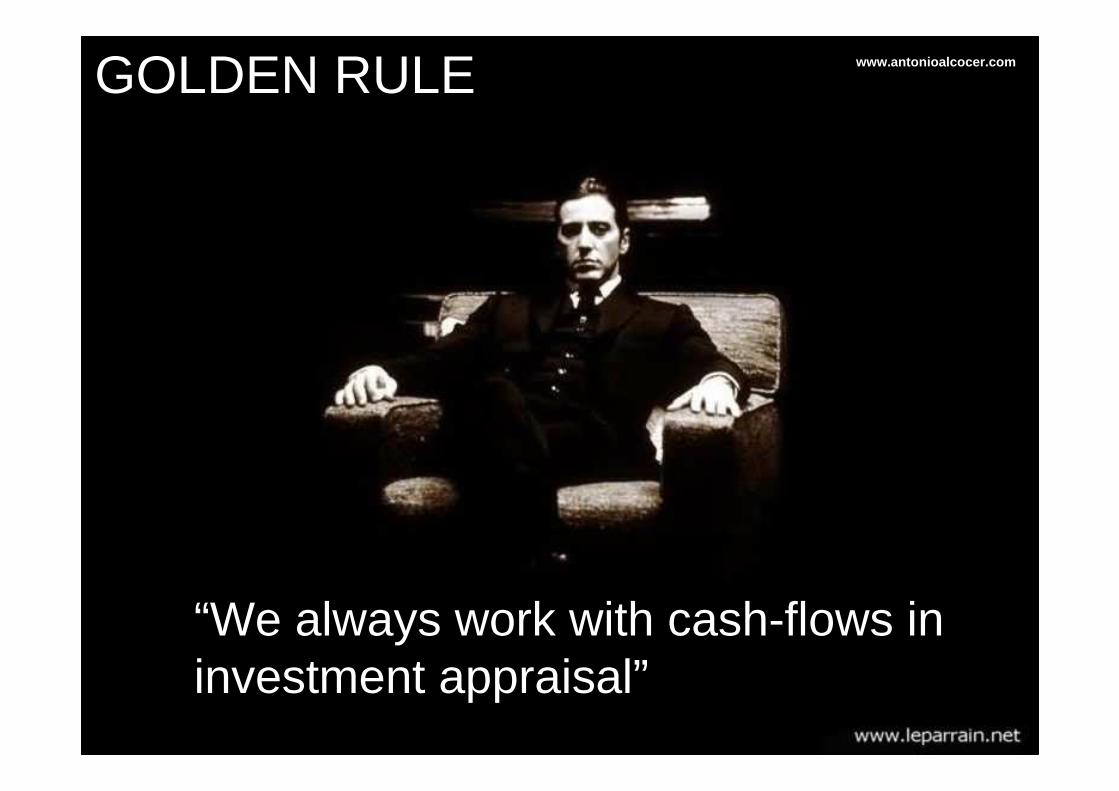

“We always work with cash-flows in investment appraisal”

GOLDEN RULE www.antonioalcocer.com

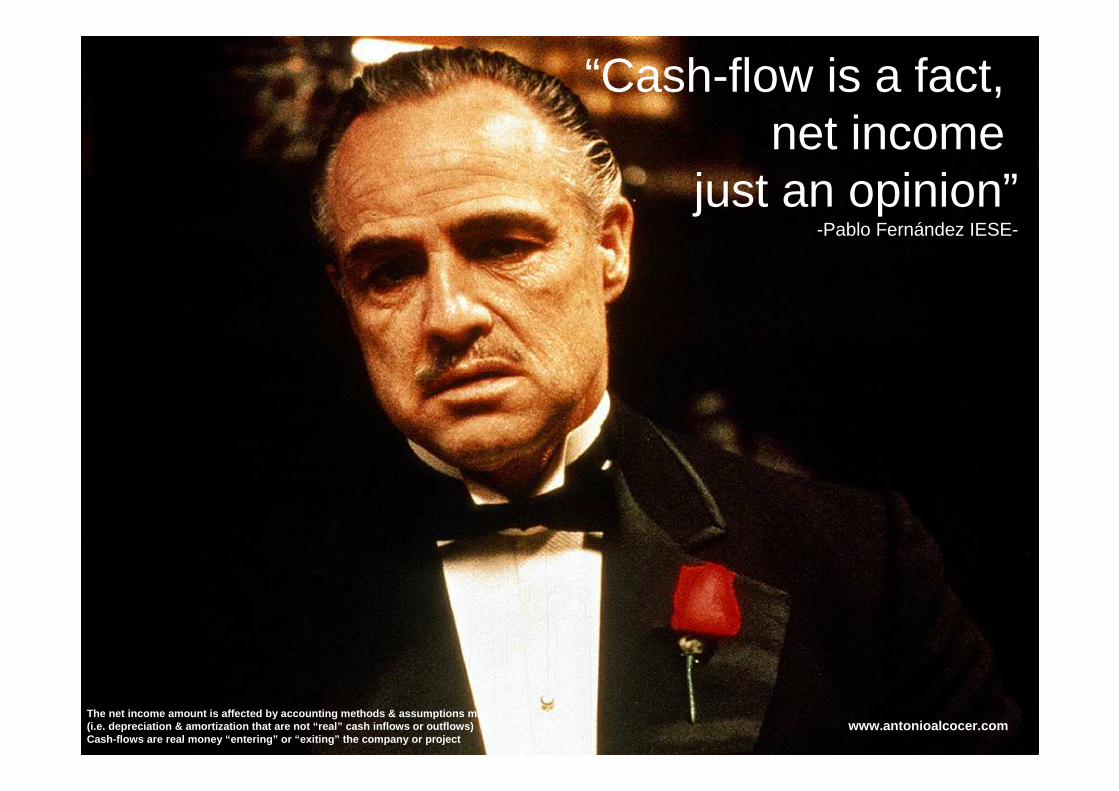

“Cash-flow is a fact, net income

just an opinion”-Pablo Fernández IESE-

The net income amount is affected by accounting methods & a ssumptions made(i.e. depreciation & amortization that are not “real” ca sh inflows or outflows)Cash-flows are real money “entering” or “exiting” the com pany or project

www.antonioalcocer.com

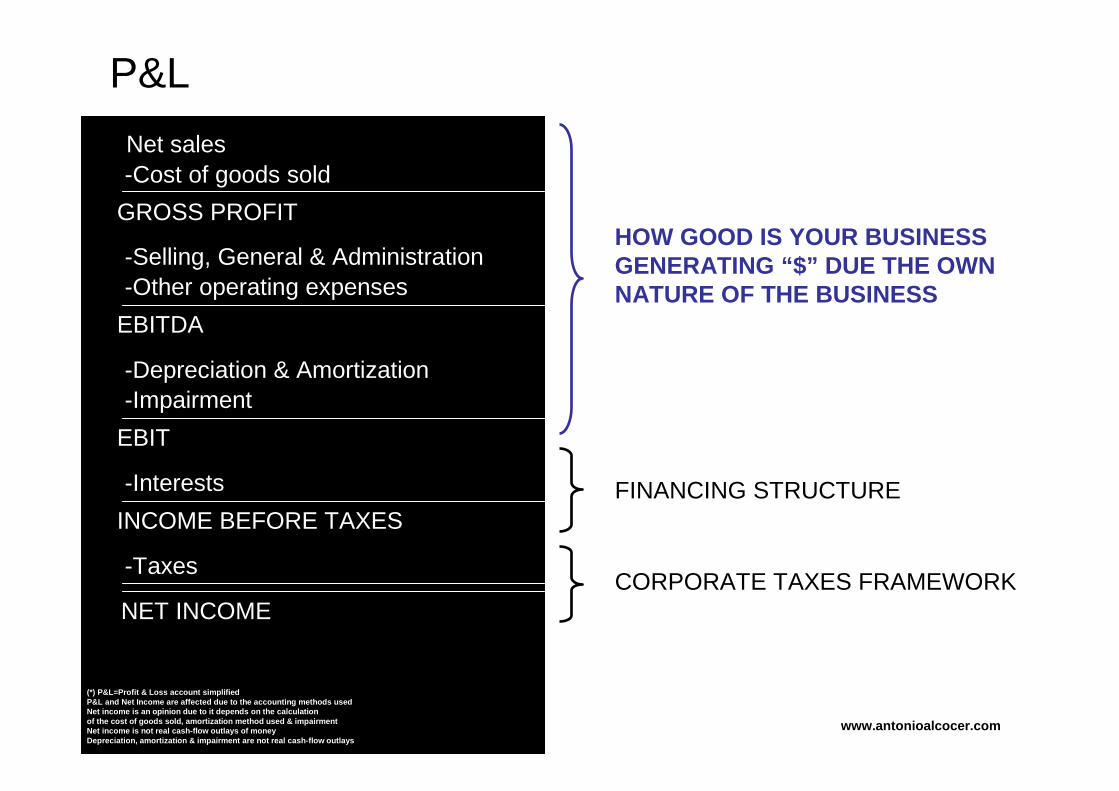

P&L (*)

NET INCOME

-Cost of goods sold

GROSS PROFIT

-Selling, General & Administration-Other operating expenses

-Impairment

Net sales

-Taxes

EBITDA

-Depreciation & Amortization

EBIT

-Interests

INCOME BEFORE TAXES

(*) P&L=Profit & Loss account simplifiedP&L and Net Income are affected due to the accounting metho ds usedNet income is an opinion due to it depends on the calculatio nof the cost of goods sold, amortization method used & impai rmentNet income is not real cash-flow outlays of moneyDepreciation, amortization & impairment are not real c ash-flow outlays

HOW GOOD IS YOUR BUSINESSGENERATING “$” DUE THE OWNNATURE OF THE BUSINESS

FINANCING STRUCTURE

CORPORATE TAXES FRAMEWORK

www.antonioalcocer.com

“So nowI understandin investment appraisalwe useCASH-FLOWS”

www.antonioalcocer.com

But how manycash-flows exist?

www.antonioalcocer.com

Available “$” for the funds providers:_BANKS_SHAREHOLDERS

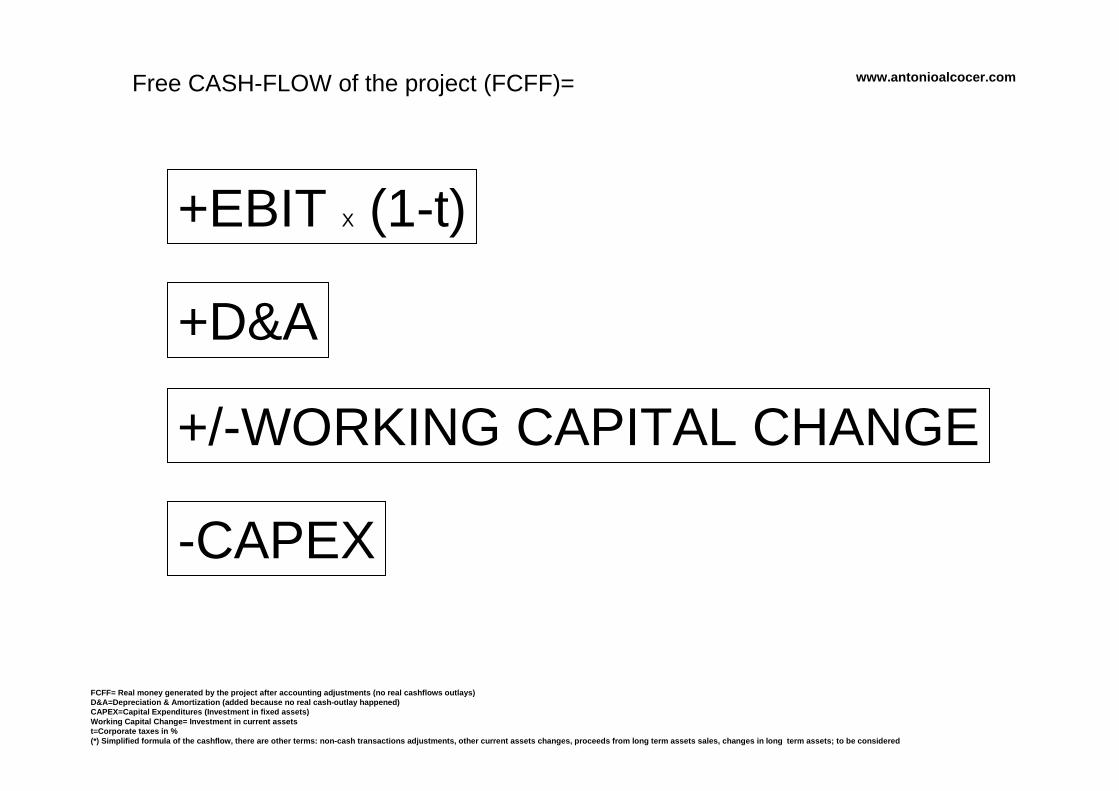

Free CASH-FLOW of the project (FCFF)=

www.antonioalcocer.com

Free CASH-FLOW of the project (FCFF)=

+EBIT X (1-t)

+D&A

+/-WORKING CAPITAL CHANGE

-CAPEX

FCFF= Real money generated by the project after accounti ng adjustments (no real cashflows outlays)D&A=Depreciation & Amortization (added because no real cash-outlay happened)CAPEX=Capital Expenditures (Investment in fixed assets )Working Capital Change= Investment in current assetst=Corporate taxes in %(*) Simplified formula of the cashflow, there are other terms: non-cash transactions adjustments, other curre nt assets changes, proceeds from long term assets sales, changes in long term assets; to be considered

www.antonioalcocer.com

Available “$” for theequity providers:_SHAREHOLDERS

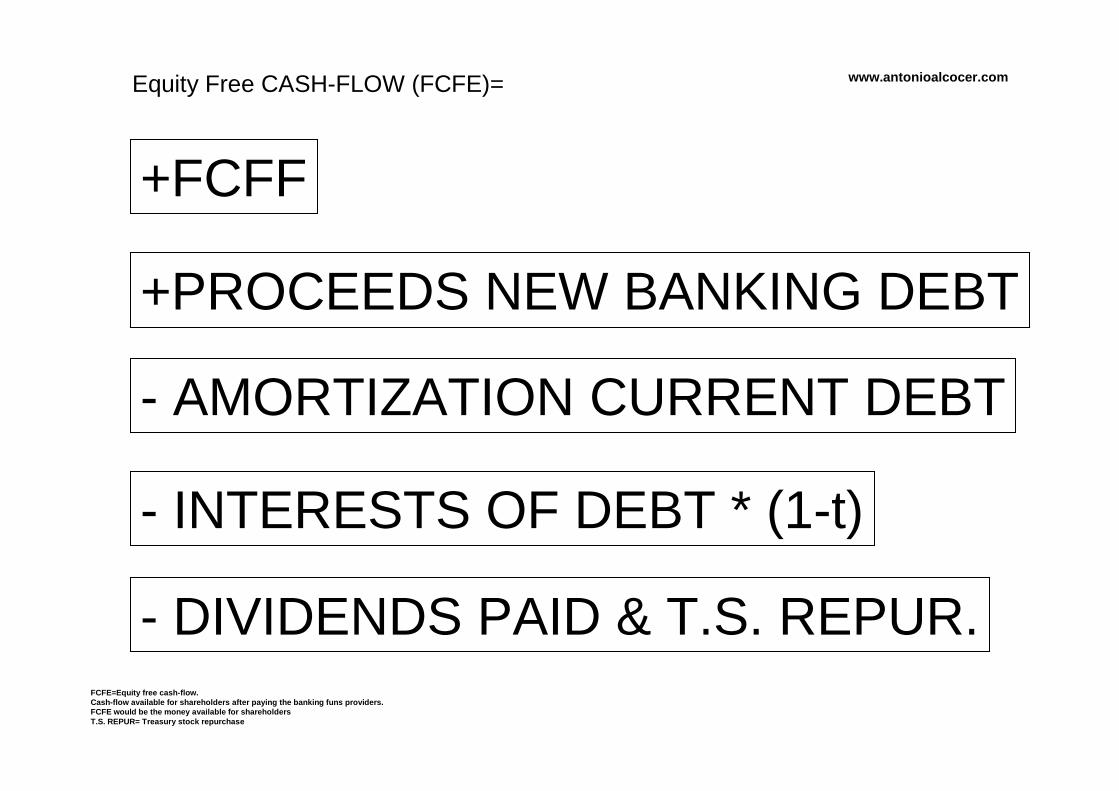

Equity Free CASH-FLOW (FCFE)=

www.antonioalcocer.com

Equity Free CASH-FLOW (FCFE)=

+FCFF

+PROCEEDS NEW BANKING DEBT

- AMORTIZATION CURRENT DEBT

- INTERESTS OF DEBT * (1-t)

FCFE=Equity free cash-flow.Cash-flow available for shareholders after paying the bank ing funs providers.FCFE would be the money available for shareholdersT.S. REPUR= Treasury stock repurchase

- DIVIDENDS PAID & T.S. REPUR.

www.antonioalcocer.com

…and many others

www.antonioalcocer.com

NOW

WE ARE READY

FOR AN EXAMPLE!

www.antonioalcocer.com

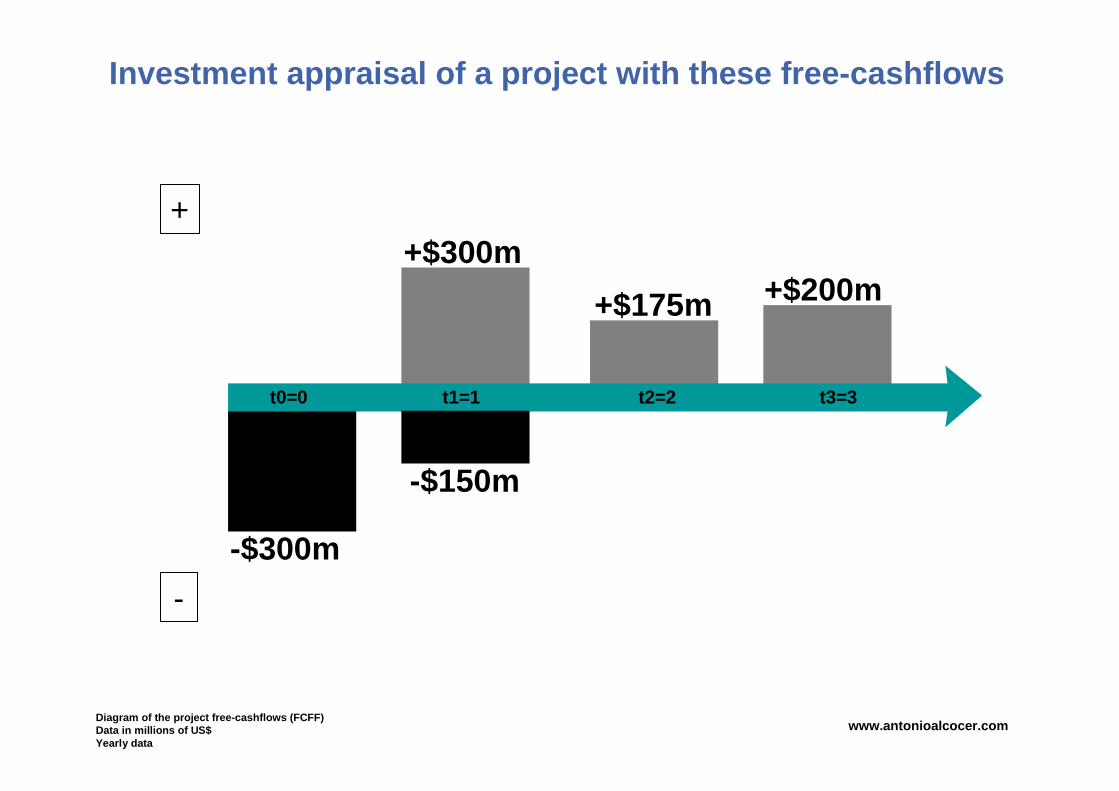

Investment appraisal of a project with these free-cashflo ws

-$300m

t0=0

Diagram of the project free-cashflows (FCFF)Data in millions of US$Yearly data

t1=1 t2=2 t3=3

-$150m

+$175m

+$300m+$200m

+

-

www.antonioalcocer.com

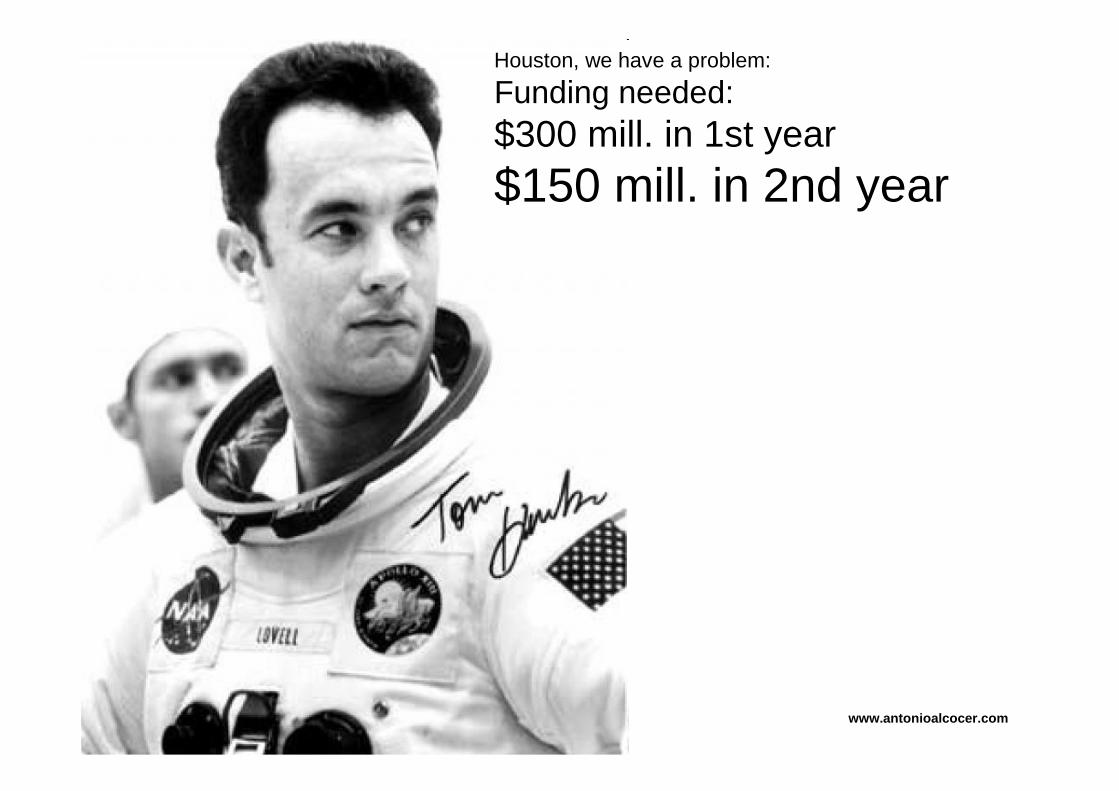

Houston, we have a problem:

Funding needed:$300 mill. in 1st year

$150 mill. in 2nd year

www.antonioalcocer.com

Don’t worry

Funds providers:_banks_shareholders

will gently disposethem

www.antonioalcocer.com

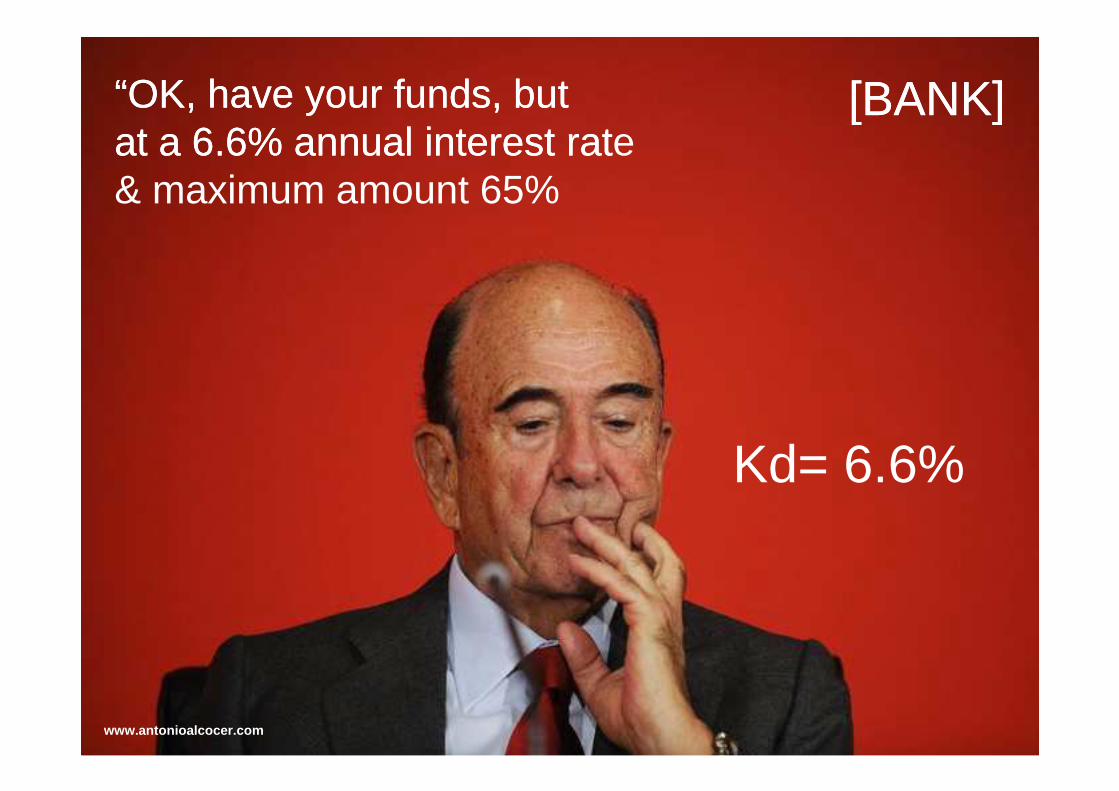

[BANK]“OK, have your funds, butat a 6.6% annual interest rate& maximum amount 65%

[BANK]“OK, have your funds, butat a 6.6% annual interest rat

Kd= 6.6%

www.antonioalcocer.com

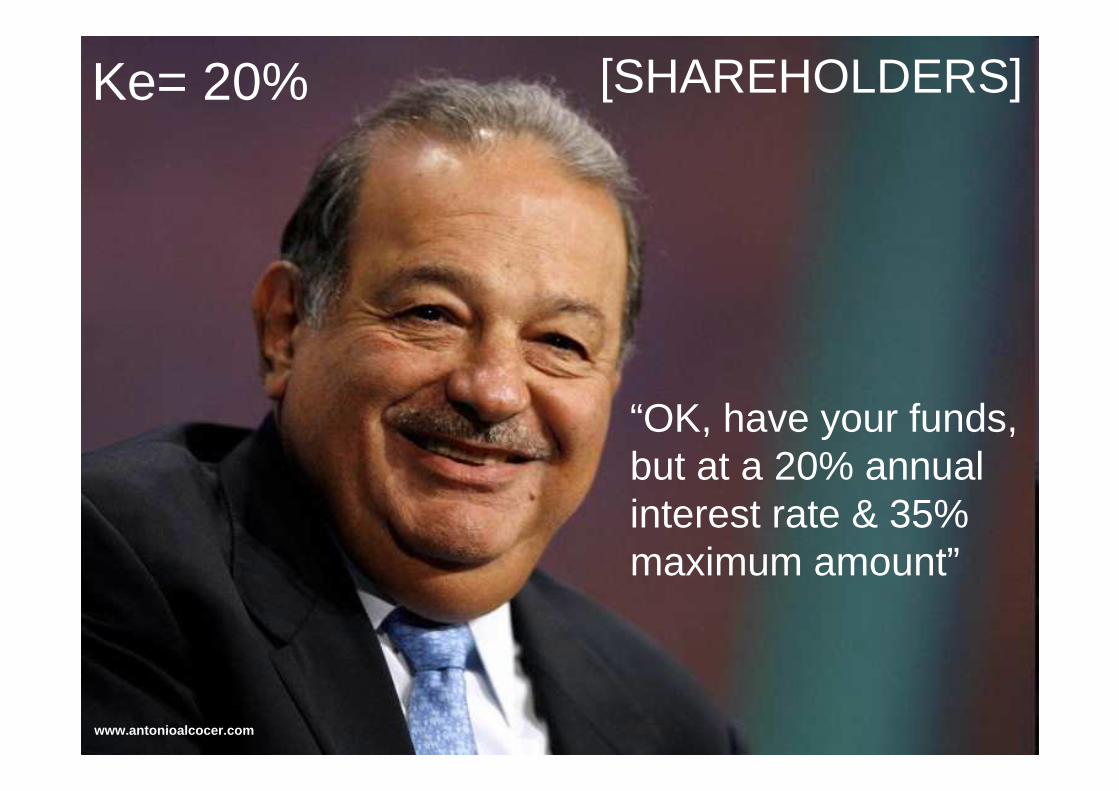

[SHAREHOLDERS]

“OK, have your funds, but at a 20% annualinterest rate & 35% maximum amount”

Ke= 20%

www.antonioalcocer.com

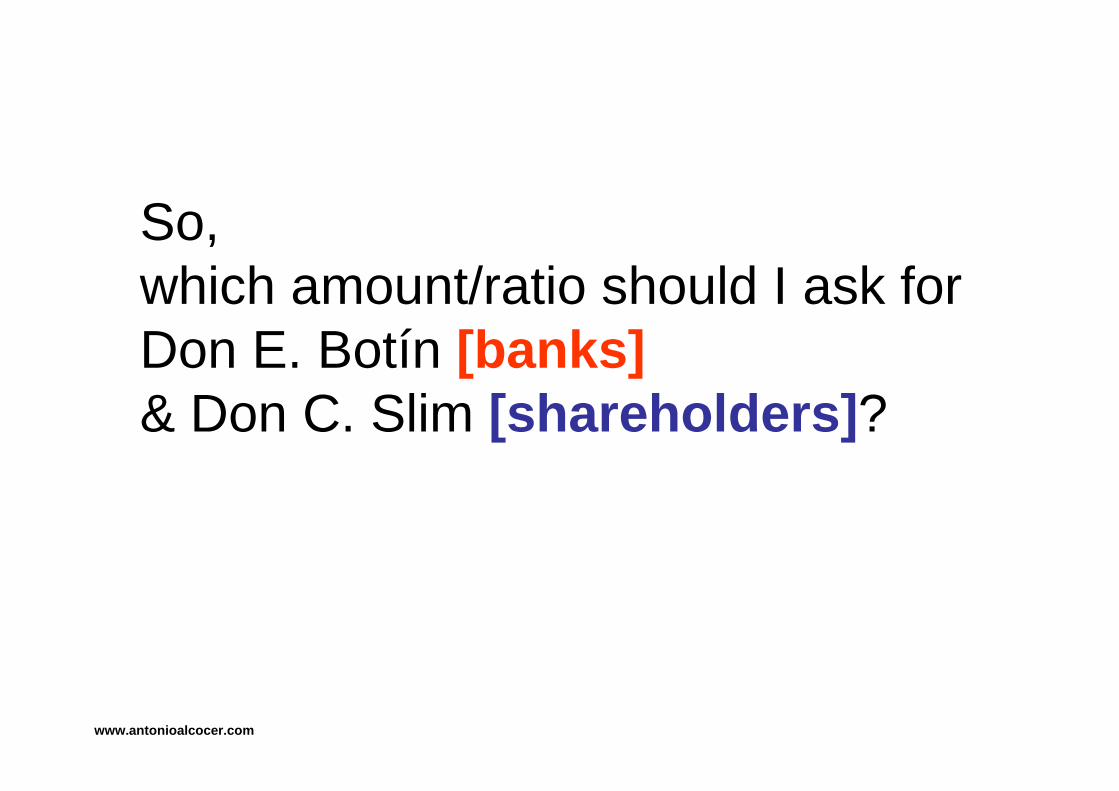

So, which amount/ratio should I ask forDon E. Botín [banks ]& Don C. Slim [shareholders ]?

www.antonioalcocer.com

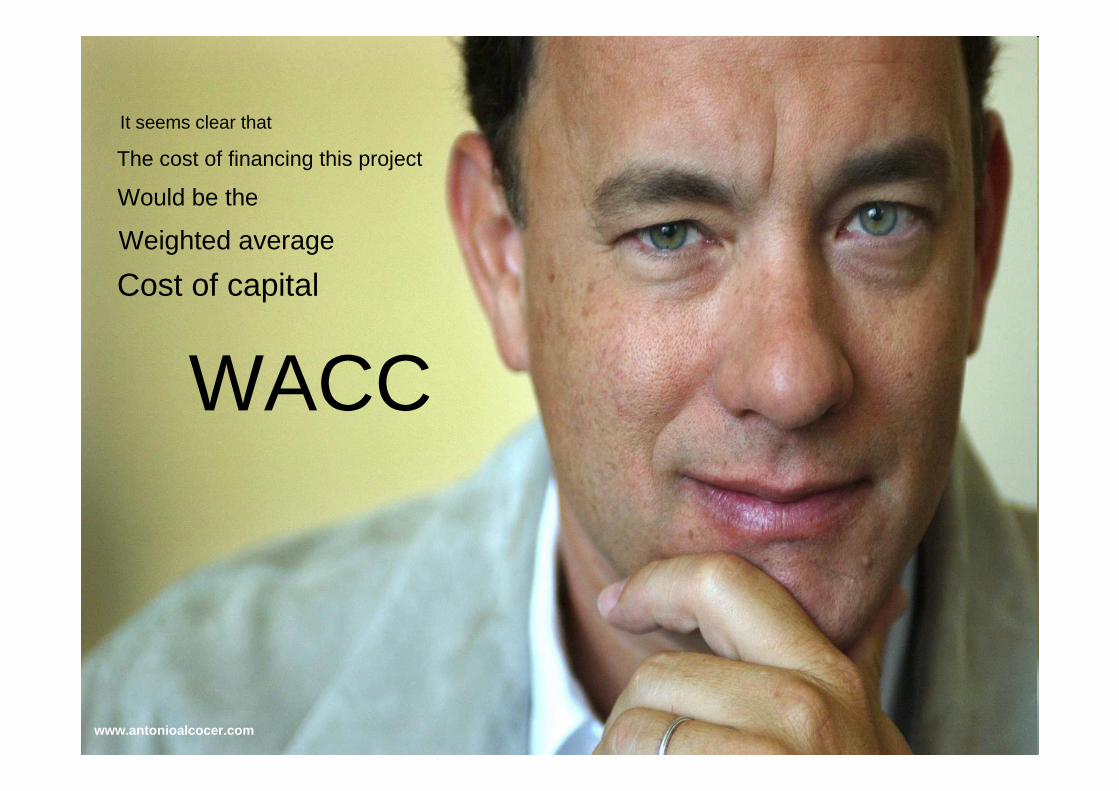

It seems clear that

The cost of financing this project

Would be the

Weighted average

Cost of capital

WACC

www.antonioalcocer.com

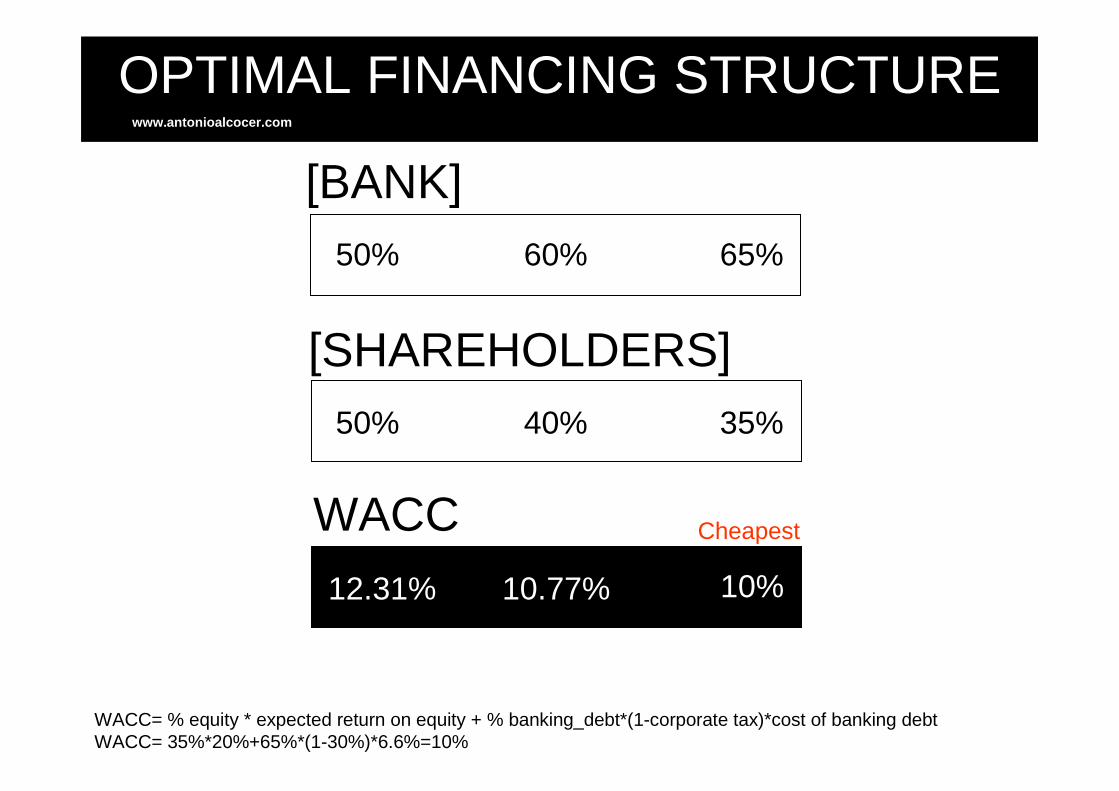

OPTIMAL FINANCING STRUCTURE

[BANK]

[SHAREHOLDERS]

WACC

50% 60% 65%

50% 40% 35%

12.31% 10.77% 10%

WACC= % equity * expected return on equity + % banking_debt*(1-corporate tax)*cost of banking debtWACC= 35%*20%+65%*(1-30%)*6.6%=10%

Cheapest

www.antonioalcocer.com

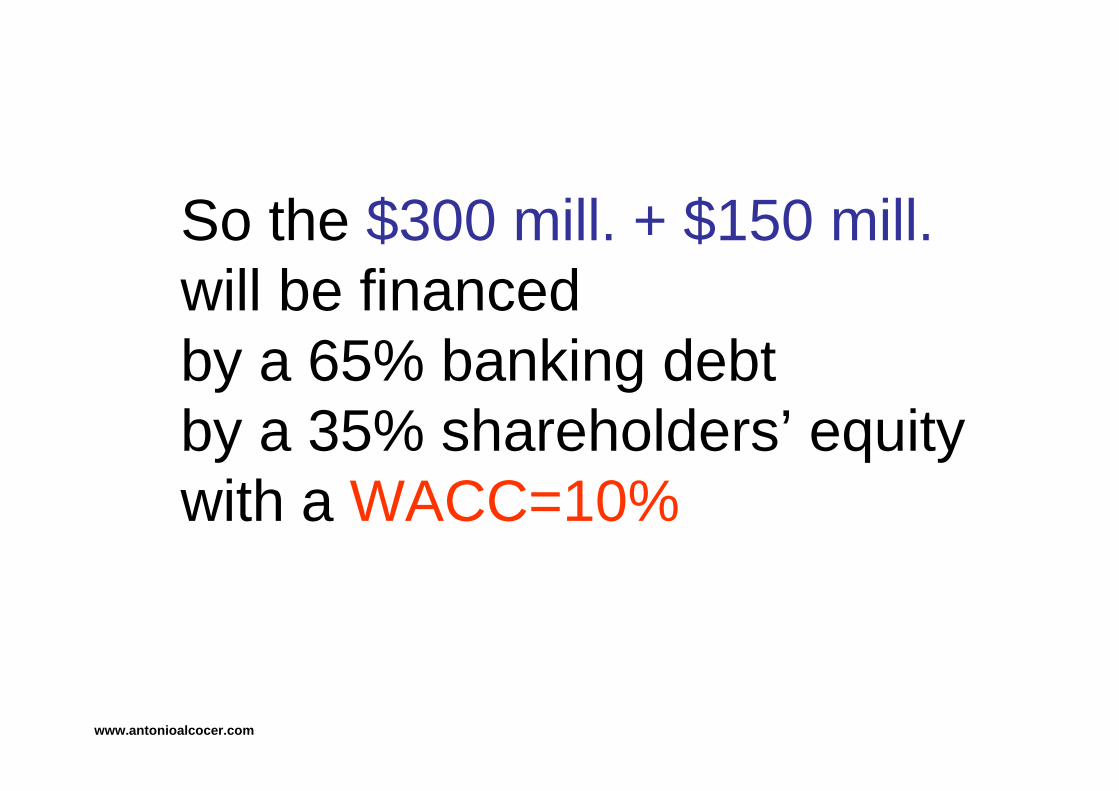

So the $300 mill. + $150 mill.will be financedby a 65% banking debtby a 35% shareholders’ equitywith a WACC=10%

www.antonioalcocer.com

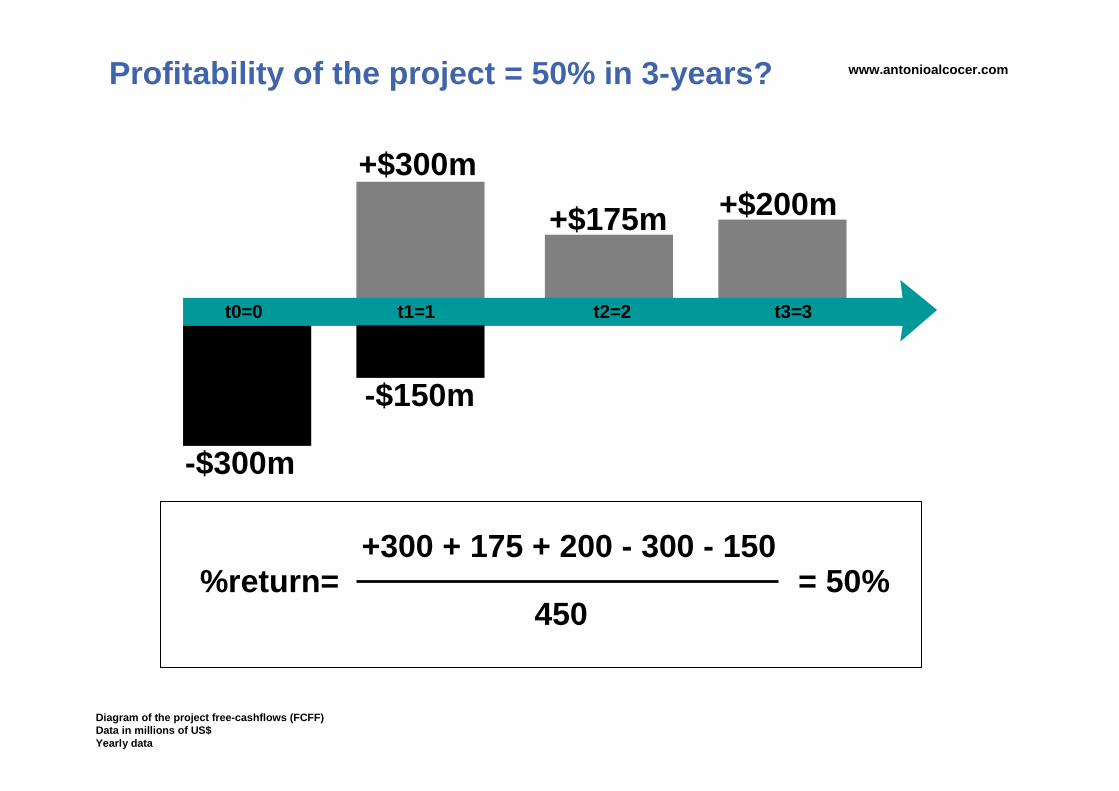

Profitability of the project = 50% in 3-years?

-$300m

t0=0

Diagram of the project free-cashflows (FCFF)Data in millions of US$Yearly data

t1=1 t2=2 t3=3

-$150m

+$175m

+$300m+$200m

%return= +300 + 175 + 200 - 300 - 150

450= 50%

www.antonioalcocer.com

Noooooo!!!!!!!!!

TIMEVALUE

OF MONEY

www.antonioalcocer.com

INVESTMENT APPRAISAL METHODS

1. NET PRESENT VALUE (NPV)2. INTERNAL RATE OF RETURN (IRR)3. PAYBACK PERIOD

(*) Most important discussed www.antonioalcocer.com

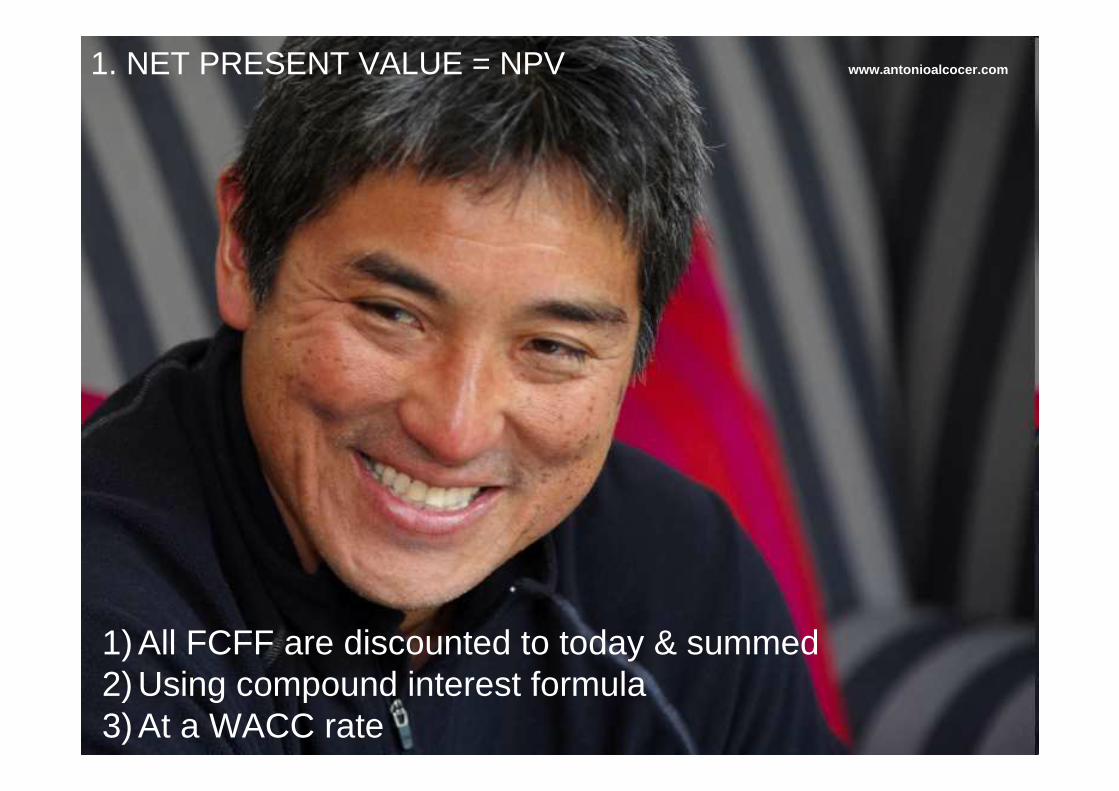

1. NET PRESENT VALUE = NPV

1) All FCFF are discounted to today & summed2) Using compound interest formula3) At a WACC rate

www.antonioalcocer.com

1. NET PRESENT VALUE=$0

Cash-flows generated exactly pay the cash-flows expectations requested by the banking & shareholders (funds providers)

[Undertake project]

www.antonioalcocer.com

1. NET PRESENT VALUE>$0

Cash-flows generated pay all the cash-flows requested by fund providers in order to meet their profit expectations (NPV=0) & additional cash-flow=NPV goes as excess profit for shareholders

[Undertake project]

www.antonioalcocer.com

1. NET PRESENT VALUE<$0[Do not undertake project]

Cash-flows generated are not enoughto pay the cash-flows demmands by funds providers according to theirprofit expectations (=WACC)

www.antonioalcocer.com

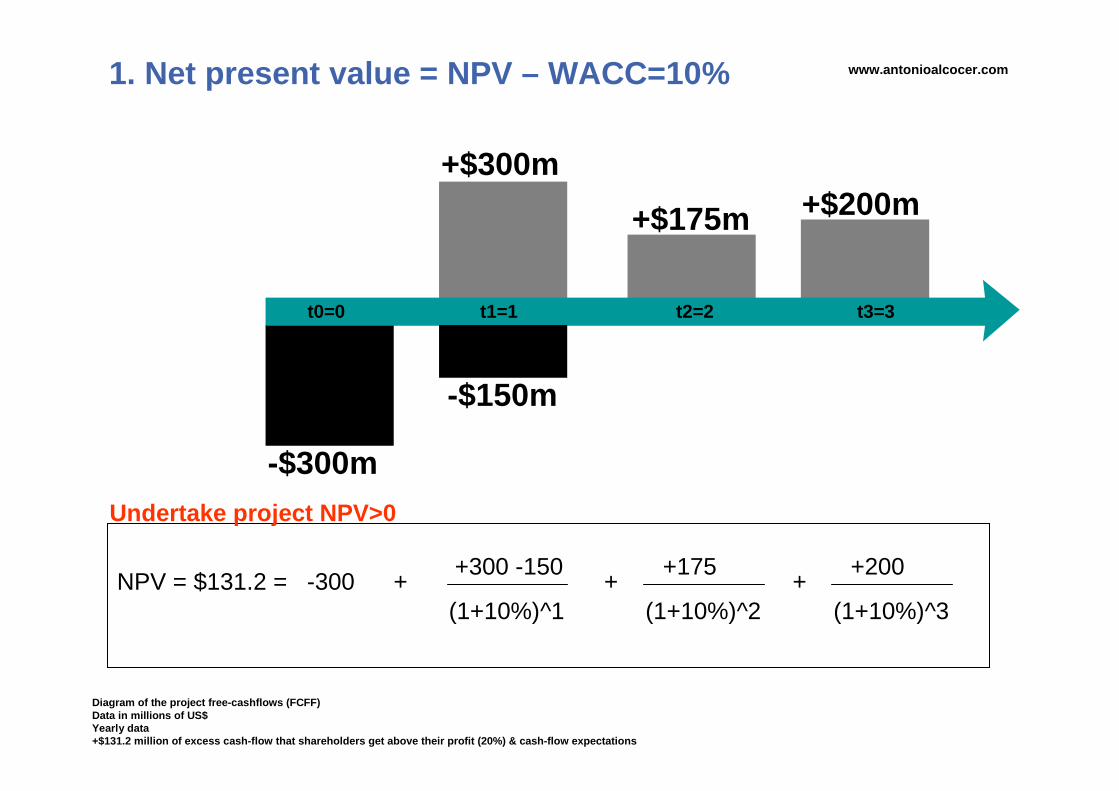

1. Net present value = NPV – WACC=10%

-$300m

t0=0

Diagram of the project free-cashflows (FCFF)Data in millions of US$Yearly data+$131.2 million of excess cash-flow that shareholders get above their profit (20%) & cash-flow expectations

t1=1 t2=2 t3=3

-$150m

+$175m

+$300m+$200m

NPV = $131.2 = -300 ++300 -150

(1+10%)^1+

+175

(1+10%)^2

+200

(1+10%)^3+

Undertake project NPV>0

www.antonioalcocer.com

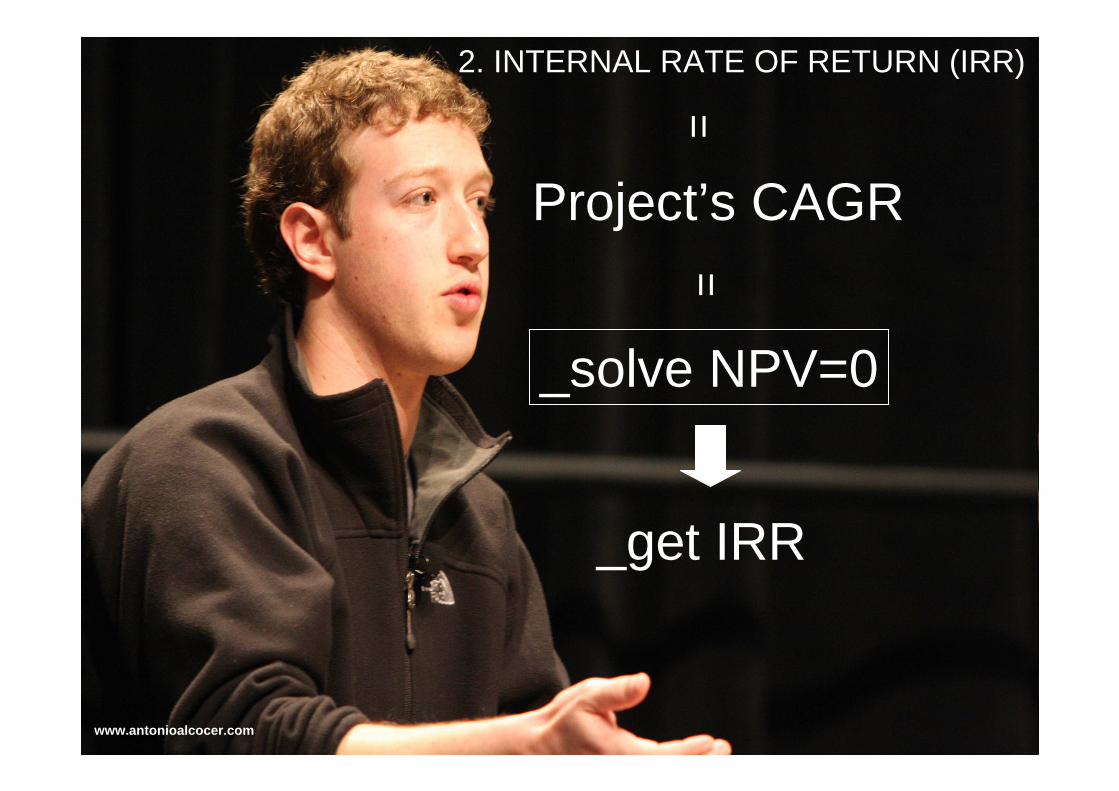

2. INTERNAL RATE OF RETURN (IRR)

=

Project’s CAGR

=_solve NPV=0

_get IRR

www.antonioalcocer.com

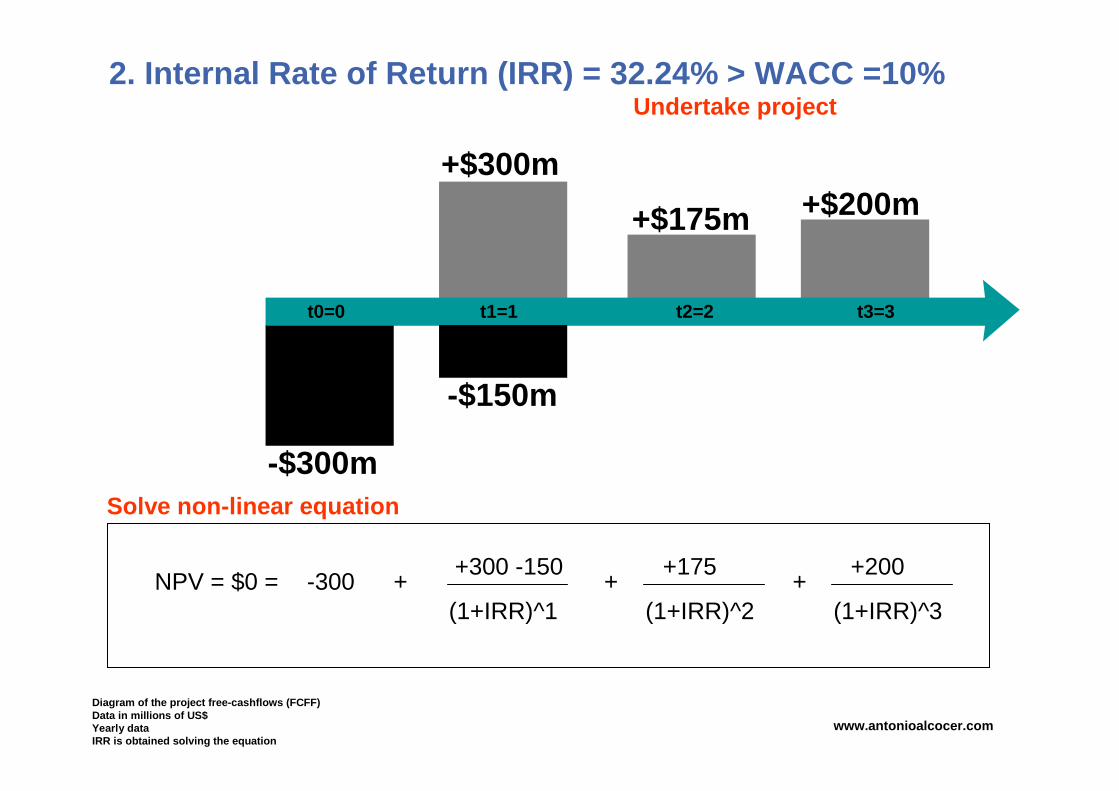

2. Internal Rate of Return (IRR) = 32.24% > WACC =10%

-$300m

t0=0

Diagram of the project free-cashflows (FCFF)Data in millions of US$Yearly dataIRR is obtained solving the equation

t1=1 t2=2 t3=3

-$150m

+$175m

+$300m+$200m

NPV = $0 = -300 ++300 -150

(1+IRR)^1+

+175

(1+IRR)^2

+200

(1+IRR)^3+

Undertake project

www.antonioalcocer.com

Solve non-linear equation

NPV=0

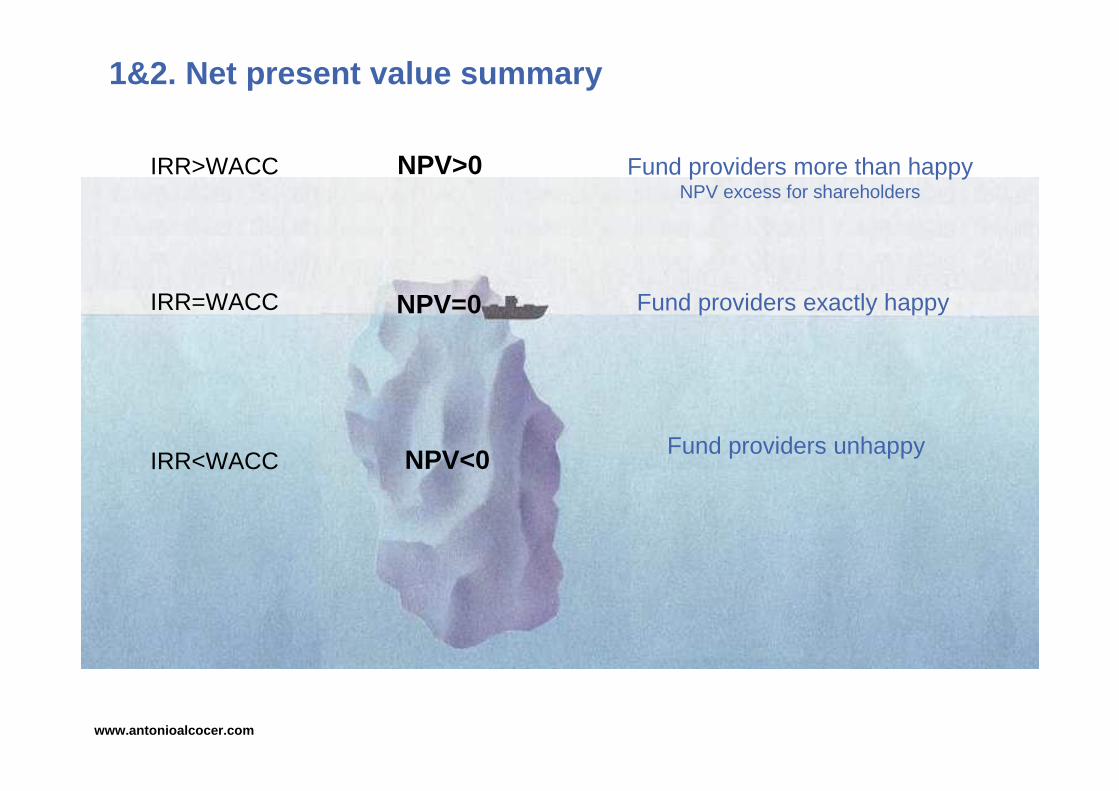

NPV<0

NPV>0

Fund providers unhappy

Fund providers exactly happy

Fund providers more than happyNPV excess for shareholders

1&2. Net present value summary

IRR<WACC

IRR=WACC

IRR>WACC

www.antonioalcocer.com

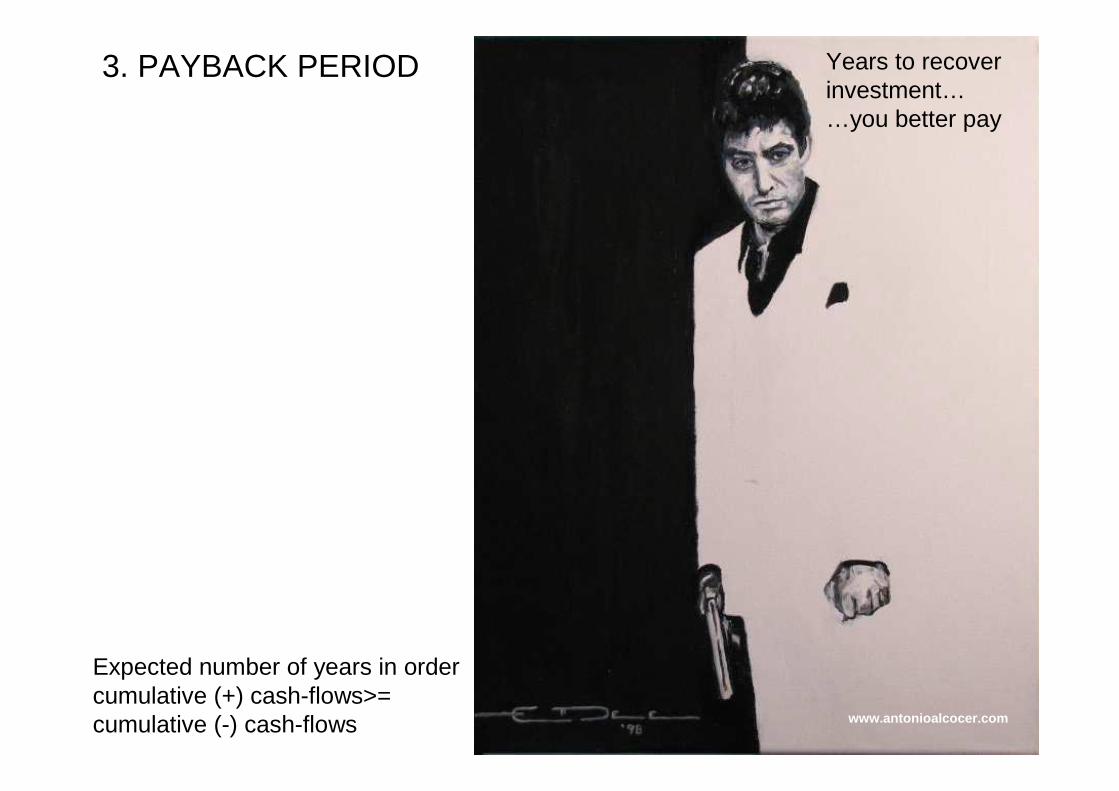

3. PAYBACK PERIOD

Expected number of years in ordercumulative (+) cash-flows>=cumulative (-) cash-flows

Years to recoverinvestment……you better pay

www.antonioalcocer.com

3. Payback period= 1.85 years

-$300m

t0=0

Payback period does not take into account time value of mone y, so it should not be used in a stand alone basis but as complementary info to NPV and IRRDiagram of the project free-cashflows (FCFF)Data in millions of US$Yearly dataPayback period: Positive cumulative cashflows are > ne gative cumulative cashflows in year 1-2175/12=14.58-150/14.58=10.29 months = 10.29/12= 0.85 years

t1=1 t2=2 t3=3

-$150m

+$175m

+$300m+$200m

-300 -300+300-150 -300+300-150+175 -300+300-150+175+200

-300 -150 +25 +225

Cumulative

www.antonioalcocer.com

RE

We have learnt:

Time value of moneyCompound interestMoving cash-flows in timeInvestment appraisal methodsProject free cashflowsWACCNPV+IRR+Payback

www.antonioalcocer.com

[now we can strike back the Empire!]

[and go for company valuations…]

www.antonioalcocer.com

WHAT IS THE

VALUE OF A COMPANY?

www.antonioalcocer.com

THIS ONE MUST BE INFINITE

www.antonioalcocer.com

THIS ONE…

www.antonioalcocer.com

∞

^∞

∞Infinite=

www.antonioalcocer.com

HEY!!!!WHAT IS THEVALUE OF ACOMPANY?

= Enteprise value [EV]

www.antonioalcocer.com

“But

in company’s valuation

we need

to calculate

the “intrinsic” or “fair value”

of the company’s equity

“updated”

based on its

future performance=

cashflows”www.antonioalcocer.com

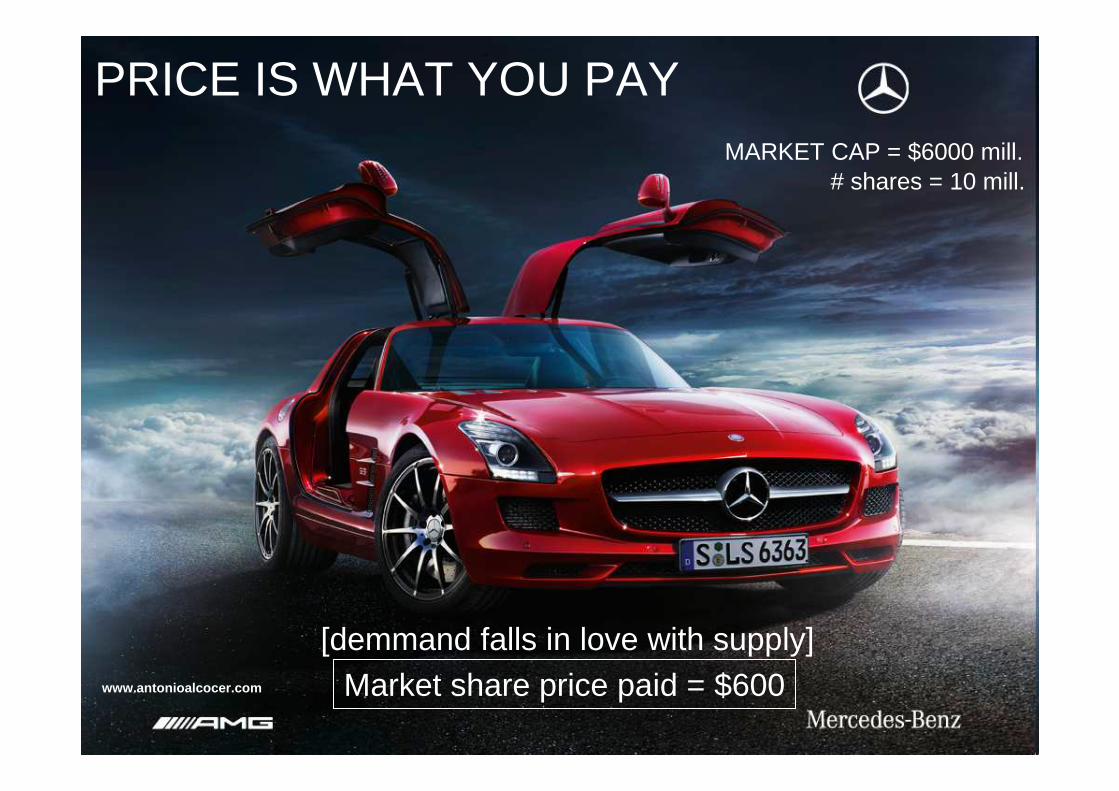

But before we start remember the 2nd GOLDEN RULE:

PRICE IS WHAT YOU PAY

[demmand falls in love with supply]

www.antonioalcocer.com

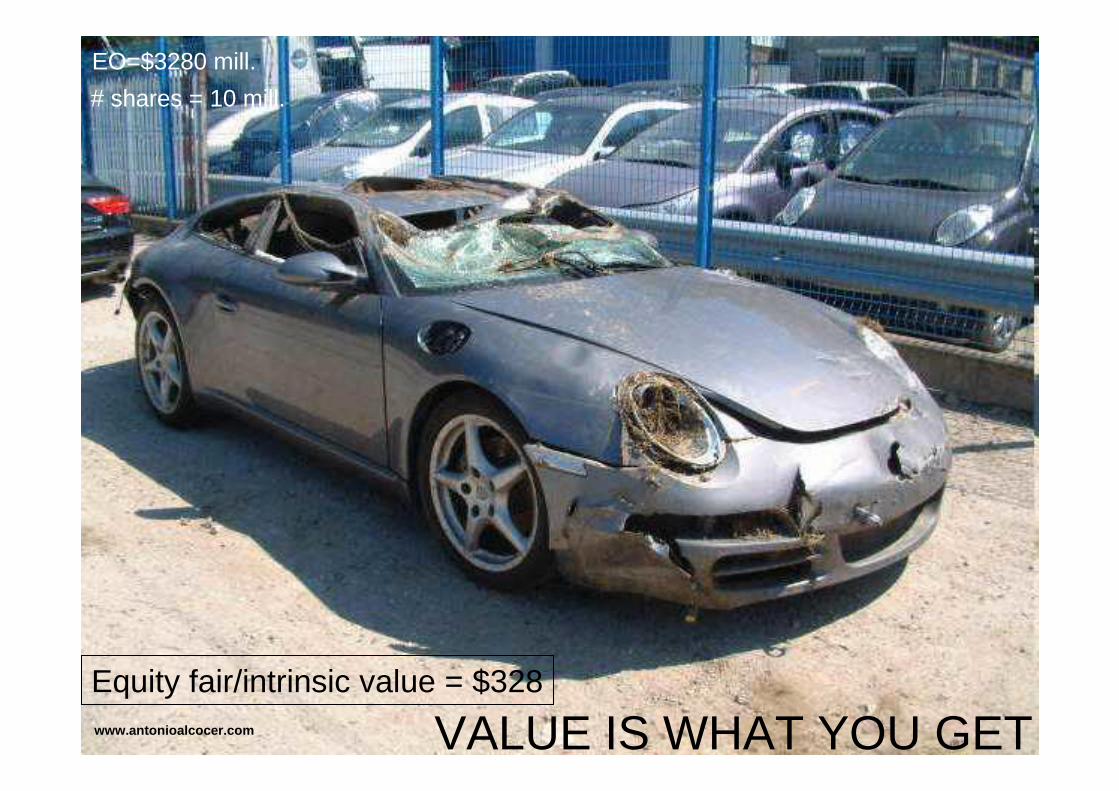

VALUE IS WHAT YOU GET www.antonioalcocer.com

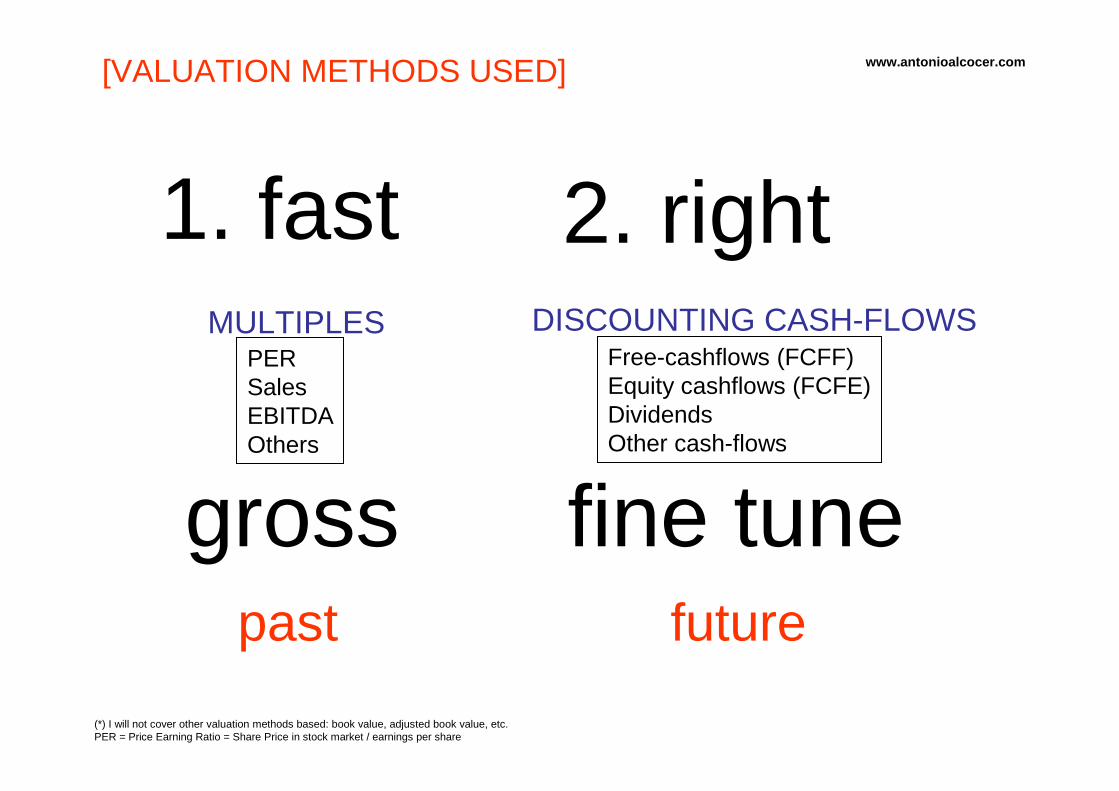

PERSalesEBITDAOthers

Free-cashflows (FCFF)Equity cashflows (FCFE)DividendsOther cash-flows

DISCOUNTING CASH-FLOWS

(*) I will not cover other valuation methods based: book value, adjusted book value, etc.PER = Price Earning Ratio = Share Price in stock market / earnings per share

[VALUATION METHODS USED]

MULTIPLES

1. fast 2. right

gross fine tunepast future

www.antonioalcocer.com

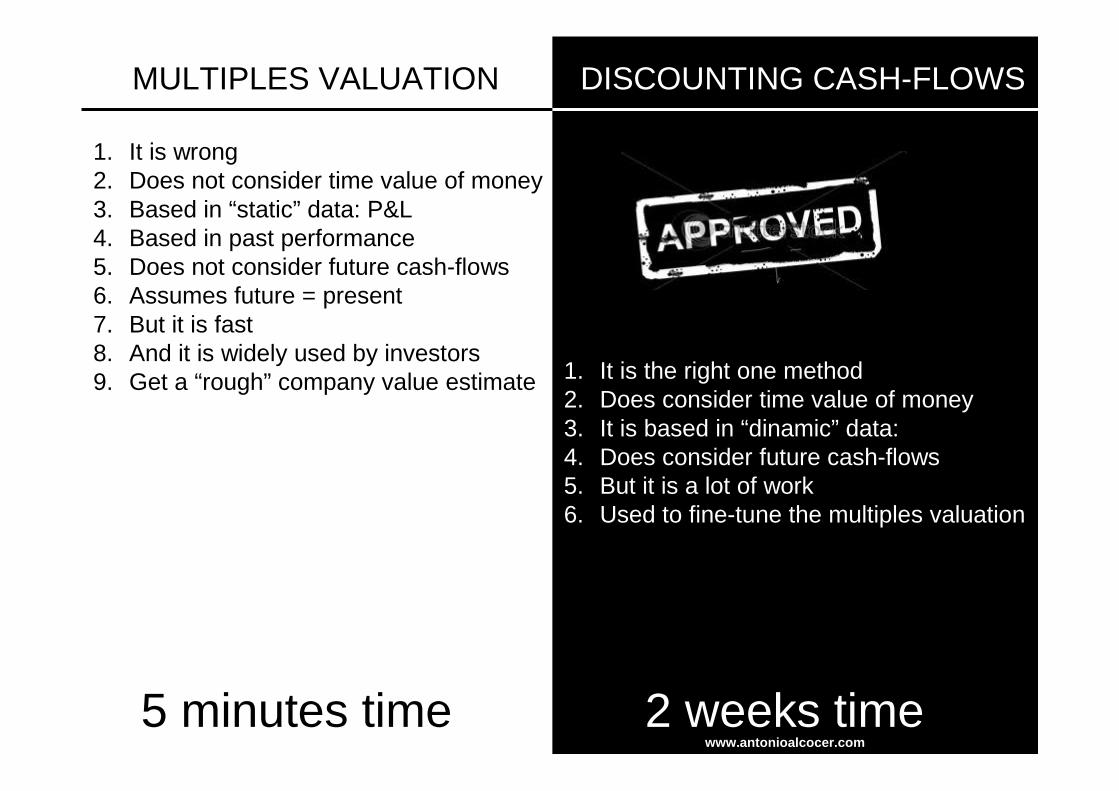

MULTIPLES VALUATION

1. It is wrong2. Does not consider time value of money3. Based in “static” data: P&L4. Based in past performance5. Does not consider future cash-flows6. Assumes future = present7. But it is fast8. And it is widely used by investors9. Get a “rough” company value estimate

DISCOUNTING CASH-FLOWS

1. It is the right one method2. Does consider time value of money3. It is based in “dinamic” data:4. Does consider future cash-flows5. But it is a lot of work6. Used to fine-tune the multiples valuation

5 minutes time 2 weeks timewww.antonioalcocer.com

I was captured by the dark side, and although I know it is WRONG…

…explain me the MULTIPLES VALUATION methodwww.antonioalcocer.com

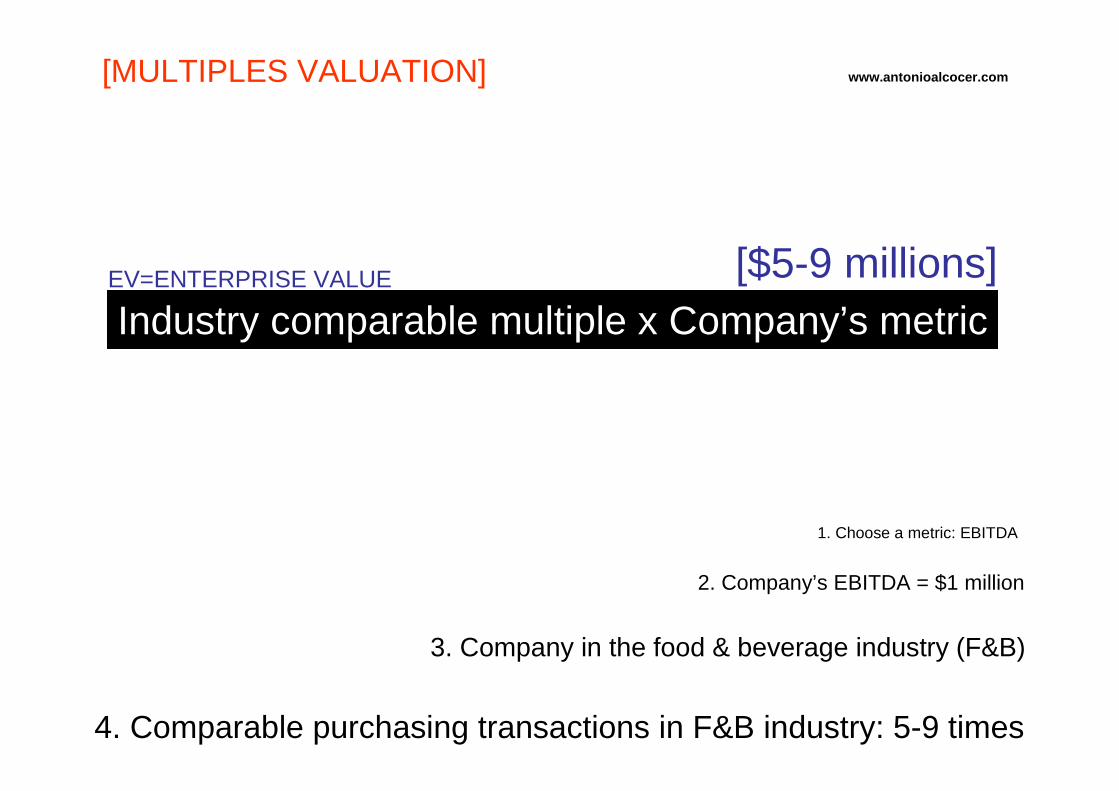

[MULTIPLES VALUATION]

2. Company’s EBITDA = $1 million

3. Company in the food & beverage industry (F&B)

4. Comparable purchasing transactions in F&B industry: 5-9 times

Industry comparable multiple x Company’s metric

1. Choose a metric: EBITDA

EV=ENTERPRISE VALUE [$5-9 millions]

www.antonioalcocer.com

[DISCOUNTING CASH-FLOWS VALUATION METHOD]

WHAT IS THE VALUE OF A COMPANY?

www.antonioalcocer.com

HOW much would you pay for a cow?

Depends on the future milkthat it can provide[& not the milk that provided in the past]

www.antonioalcocer.com

What is the value of a company?

Depends on the future cash-flows it can generate[you decide using either FCFF or FCFE_it’s up to you]

www.antonioalcocer.com

& the annual growing rate “g”(%)of these future cash-flows

[Should not be greater than a economy’s GDP in the long run <3%][In the short term cash-flows growth can exceed long term trend]

www.antonioalcocer.com

Assuming the company will last forever [=infinite]

www.antonioalcocer.com

& the company’s financing structure: WACC

%L banking debt [59%]

%E equity [41%]Ke(%) profit expectations: 9.7%

Kd(%) cost of debt 6.3%

www.antonioalcocer.com

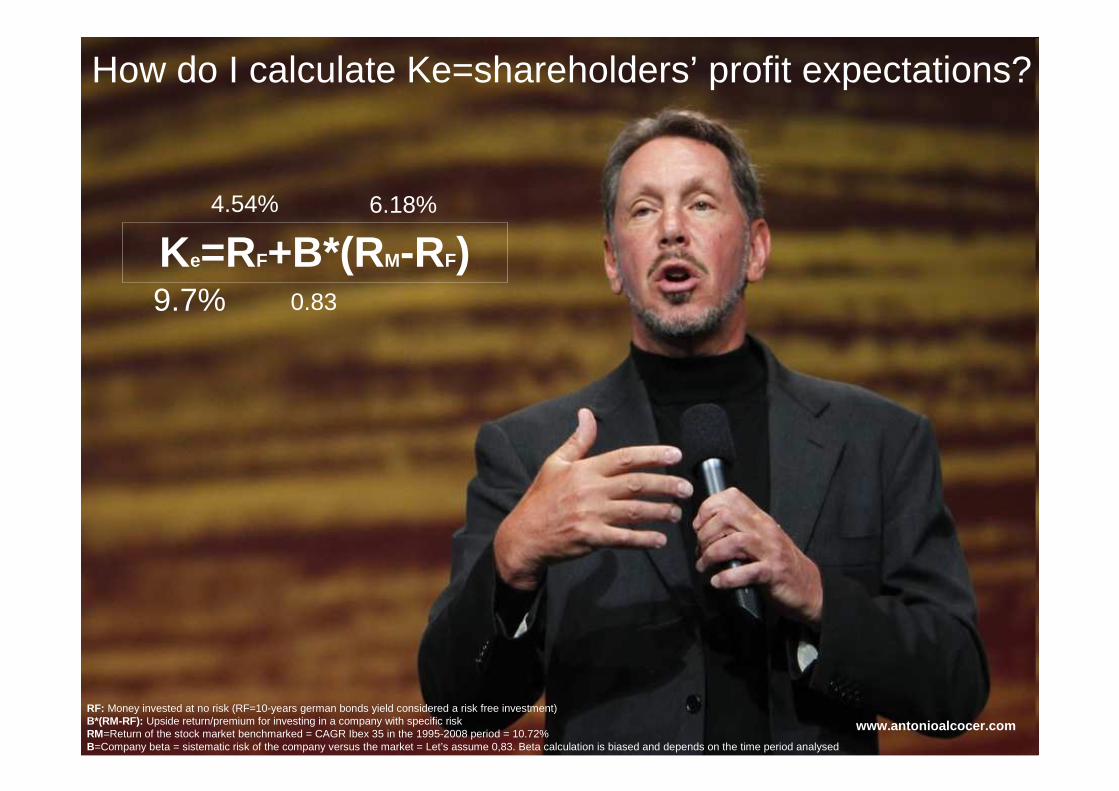

How do I calculate Ke=shareholders’ profit expectations?

RF: Money invested at no risk (RF=10-years german bonds yield considered a risk free investment)B*(RM-RF): Upside return/premium for investing in a company with specific riskRM=Return of the stock market benchmarked = CAGR Ibex 35 in the 1995-2008 period = 10.72%B=Company beta = sistematic risk of the company versus the market = Let’s assume 0,83. Beta calculation is biased and depends on the time period analysed

4.54%

Ke=RF+B*(RM-RF)6.18%

0.839.7%

www.antonioalcocer.com

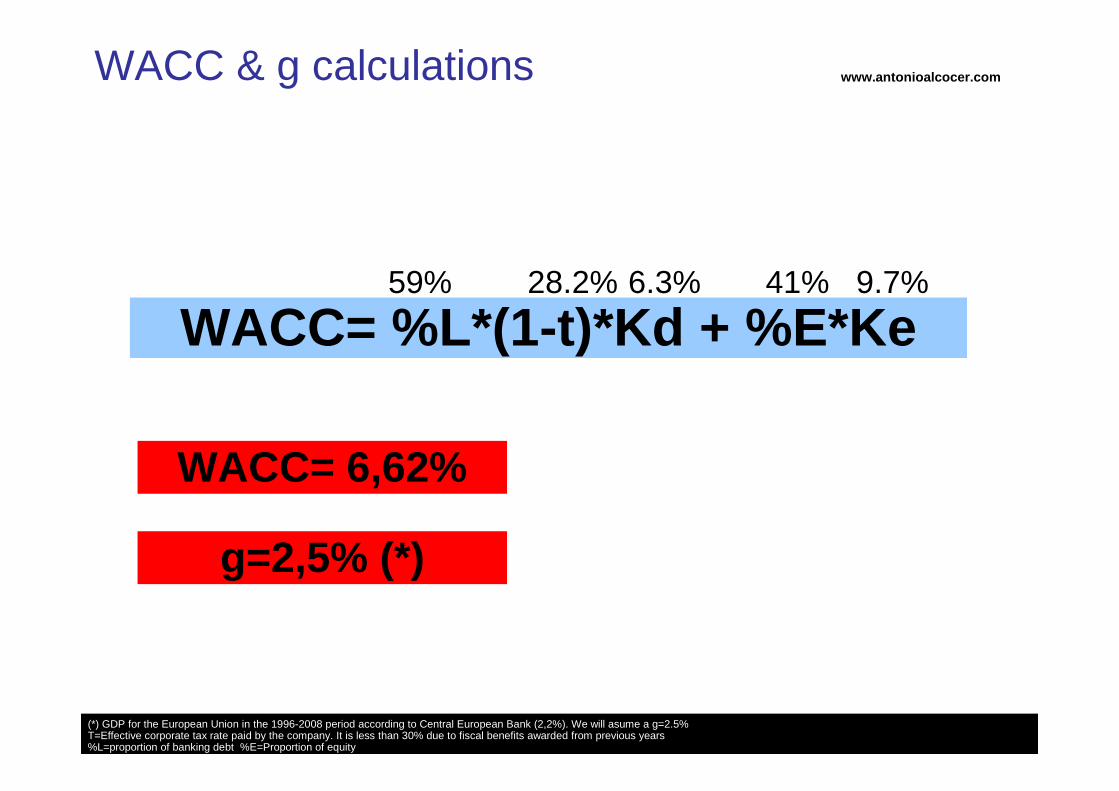

WACC= %L*(1-t)*Kd + %E*Ke

WACC= 6,62%

g=2,5% (*)

(*) GDP for the European Union in the 1996-2008 period according to Central European Bank (2,2%). We will asume a g=2.5%T=Effective corporate tax rate paid by the company. It is less than 30% due to fiscal benefits awarded from previous years%L=proportion of banking debt %E=Proportion of equity

WACC & g calculations

59% 41%28.2% 6.3% 9.7%

www.antonioalcocer.com

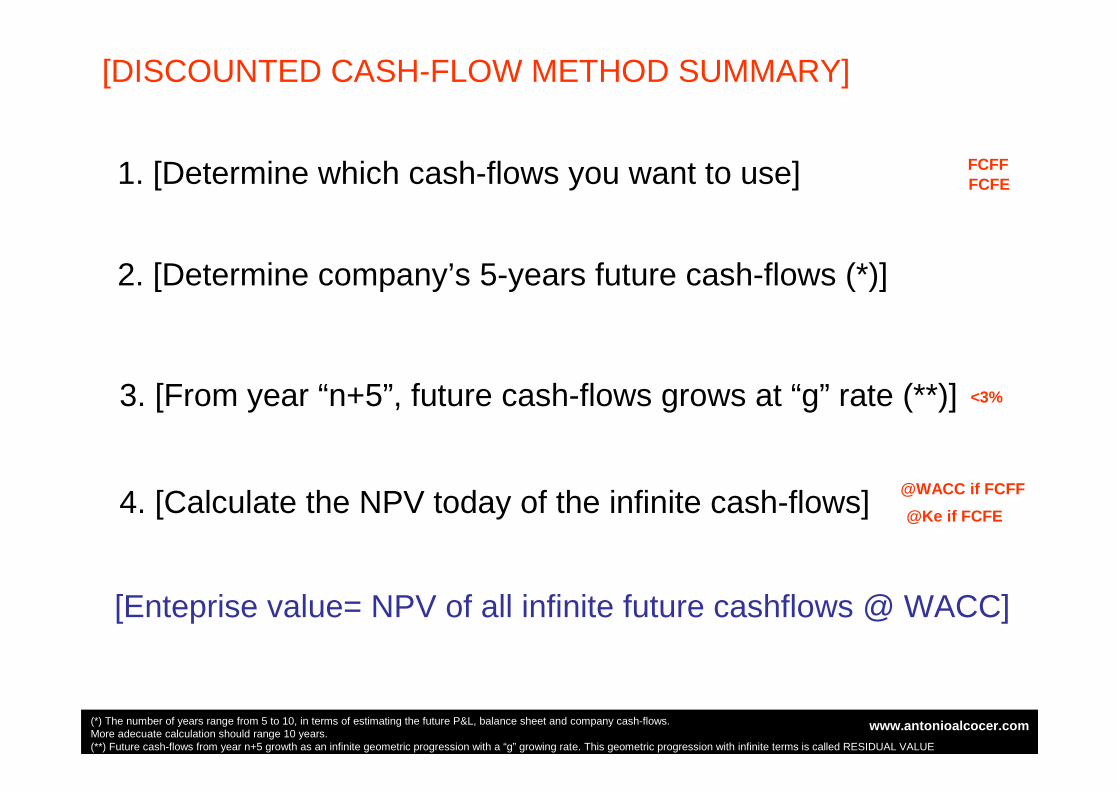

[DISCOUNTED CASH-FLOW METHOD SUMMARY]

2. [Determine company’s 5-years future cash-flows (*)]

3. [From year “n+5”, future cash-flows grows at “g” rate (**)]

4. [Calculate the NPV today of the infinite cash-flows]

[Enteprise value= NPV of all infinite future cashflows @ WACC]

@Ke if FCFE

1. [Determine which cash-flows you want to use]

@WACC if FCFF

FCFFFCFE

<3%

(*) The number of years range from 5 to 10, in terms of estimating the future P&L, balance sheet and company cash-flows.More adecuate calculation should range 10 years.(**) Future cash-flows from year n+5 growth as an infinite geometric progression with a “g” growing rate. This geometric progression with infinite terms is called RESIDUAL VALUE

www.antonioalcocer.com

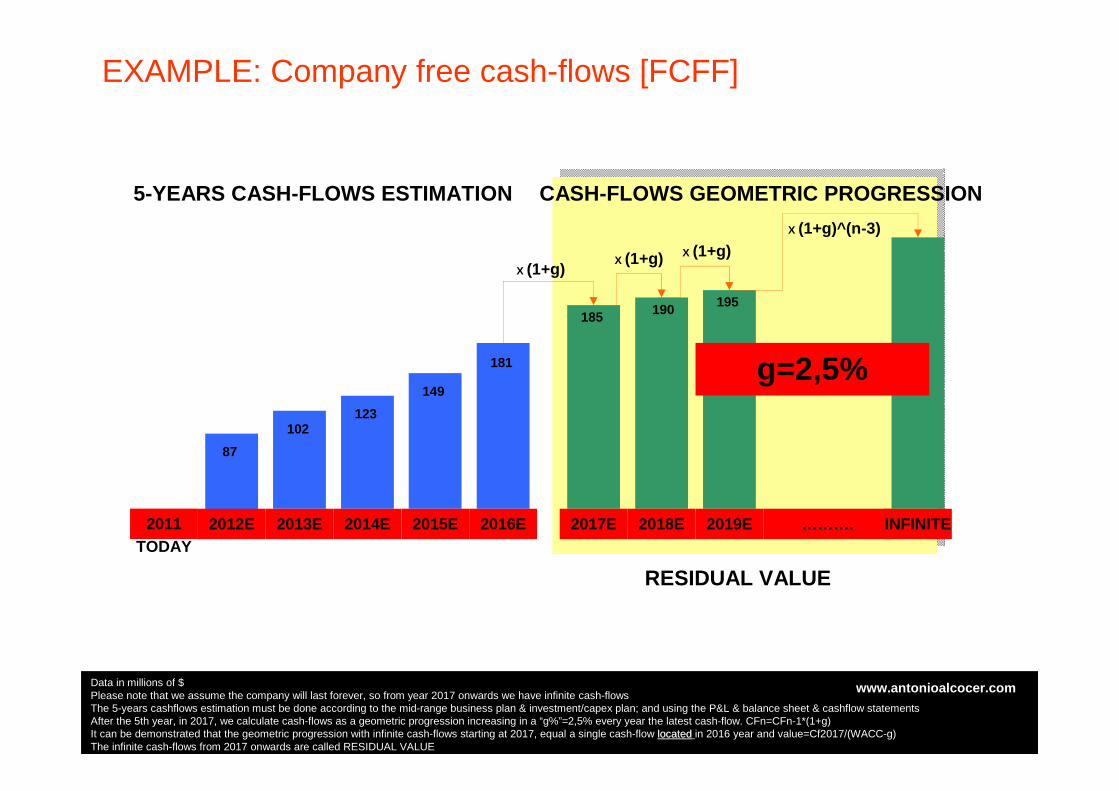

87

102123

149

181

2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E ………. INFINITE

5-YEARS CASH-FLOWS ESTIMATION

X (1+g)X (1+g) X (1+g)

X (1+g)^(n-3)

185 190 195

CASH-FLOWS GEOMETRIC PROGRESSION

2011

g=2,5%

EXAMPLE: Company free cash-flows [FCFF]

Data in millions of $Please note that we assume the company will last forever, so from year 2017 onwards we have infinite cash-flowsThe 5-years cashflows estimation must be done according to the mid-range business plan & investment/capex plan; and using the P&L & balance sheet & cashflow statementsAfter the 5th year, in 2017, we calculate cash-flows as a geometric progression increasing in a “g%”=2,5% every year the latest cash-flow. CFn=CFn-1*(1+g)It can be demonstrated that the geometric progression with infinite cash-flows starting at 2017, equal a single cash-flow locatedlocated in 2016 year and value=Cf2017/(WACC-g)The infinite cash-flows from 2017 onwards are called RESIDUAL VALUE

RESIDUAL VALUE

TODAY

www.antonioalcocer.com

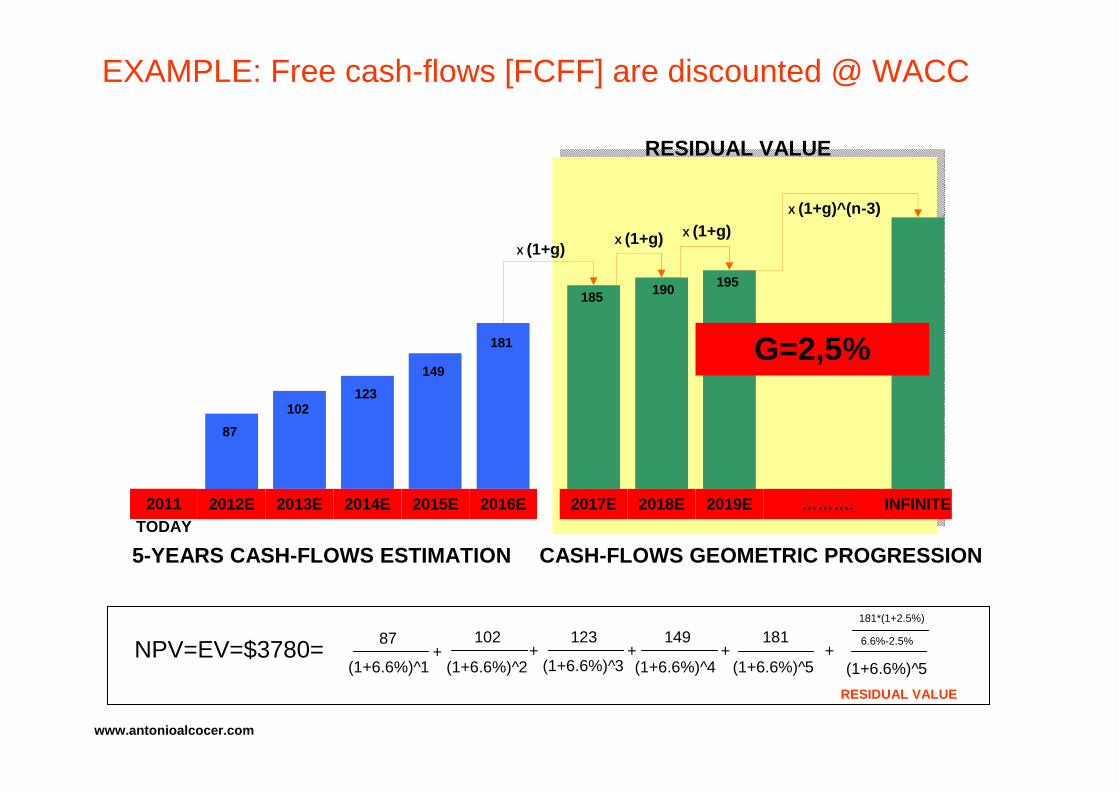

87

102123

149

181

2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E ………. INFINITE

5-YEARS CASH-FLOWS ESTIMATION

X (1+g)X (1+g) X (1+g)

X (1+g)^(n-3)

185 190 195

CASH-FLOWS GEOMETRIC PROGRESSION

2011

G=2,5%

EXAMPLE: Free cash-flows [FCFF] are discounted @ WACC

RESIDUAL VALUE

TODAY

NPV=EV=$3780=87

+(1+6.6%)^1

102+

(1+6.6%)^2

123+

(1+6.6%)^3

149+

(1+6.6%)^4

181+

(1+6.6%)^5

181*(1+2.5%)

6.6%-2.5%

(1+6.6%)^5

RESIDUAL VALUE

www.antonioalcocer.com

COMPANY’S EV$3780 millions

Have I done this?

www.antonioalcocer.com

COMPANY’S ENTERPRISE VALUE=

What is the meaning?

www.antonioalcocer.com

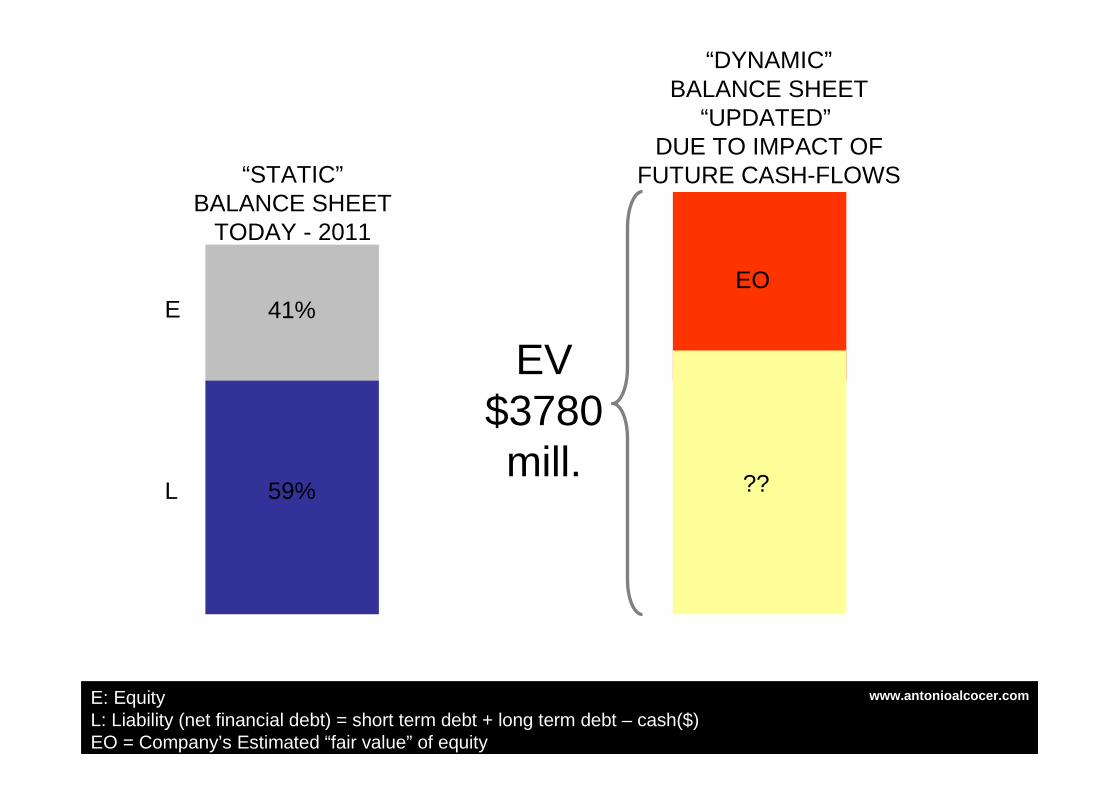

“STATIC”BALANCE SHEET

TODAY - 2011

41%

59%

E

L

“DYNAMIC”BALANCE SHEET

“UPDATED”DUE TO IMPACT OF

FUTURE CASH-FLOWS

EO

E: EquityL: Liability (net financial debt) = short term debt + long term debt – cash($)EO = Company’s Estimated “fair value” of equity

??

EV$3780mill.

www.antonioalcocer.com

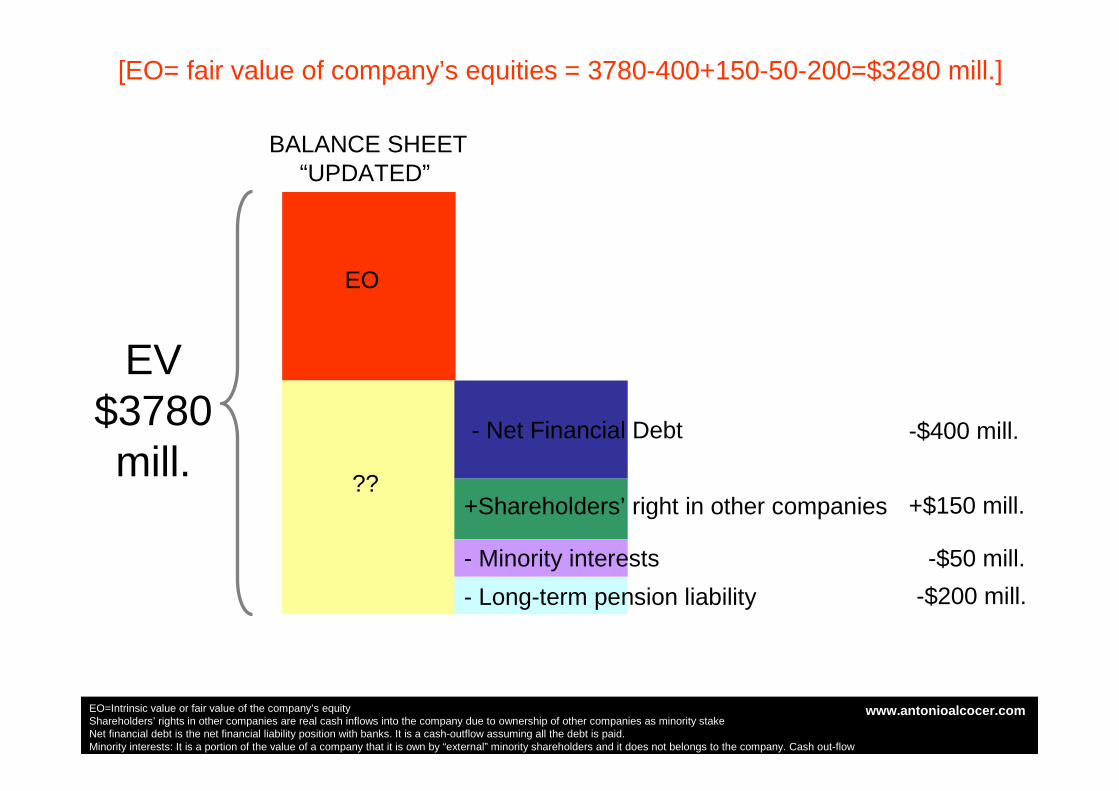

BALANCE SHEET“UPDATED”

EO

??

EV$3780mill.

- Net Financial Debt

- Long-term pension liability

- Minority interests

+Shareholders’ right in other companies

-$400 mill.

+$150 mill.

-$50 mill.

-$200 mill.

[EO= fair value of company’s equities = 3780-400+150-50-200=$3280 mill.]

EO=Intrinsic value or fair value of the company’s equityShareholders’ rights in other companies are real cash inflows into the company due to ownership of other companies as minority stakeNet financial debt is the net financial liability position with banks. It is a cash-outflow assuming all the debt is paid.Minority interests: It is a portion of the value of a company that it is own by “external” minority shareholders and it does not belongs to the company. Cash out-flowLong term pension liability & other liabilities correspond to future cash-outflows to be paid by the company.

www.antonioalcocer.com

Fair value>market value

Fair value<market value

BUY?

SELL?

www.antonioalcocer.com

PRICE IS WHAT YOU PAY

[demmand falls in love with supply]

MARKET CAP = $6000 mill.# shares = 10 mill.

Market share price paid = $600www.antonioalcocer.com

VALUE IS WHAT YOU GET

EO=$3280 mill.

# shares = 10 mill.

Equity fair/intrinsic value = $328www.antonioalcocer.com

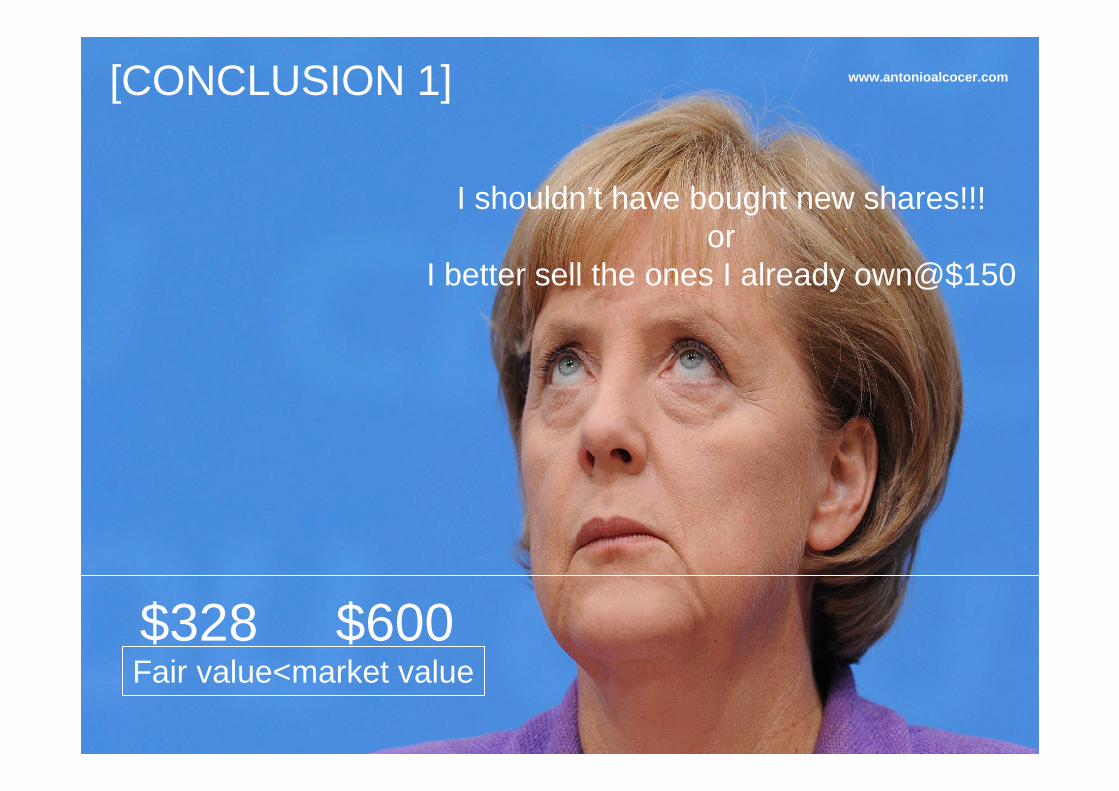

[CONCLUSION 1]

Fair value<market value$328 $600

I shouldn’t have bought new shares!!!or

I better sell the ones I already own@$150

www.antonioalcocer.com

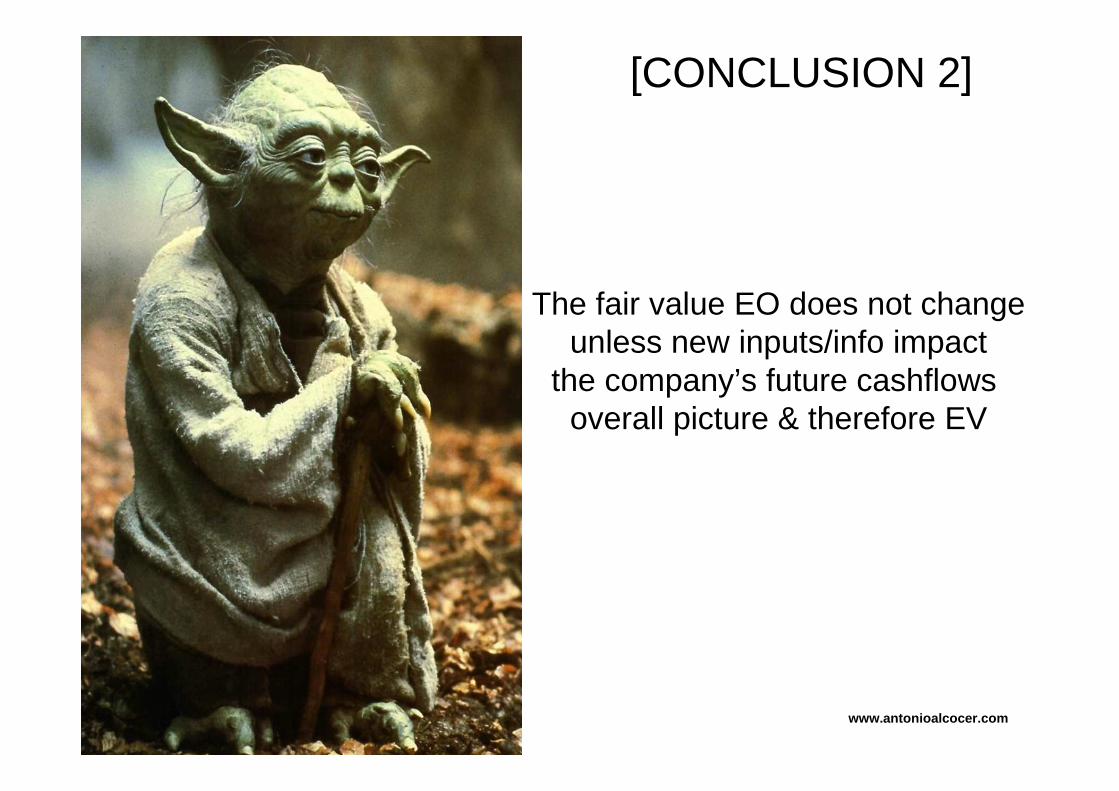

[CONCLUSION 2]

The fair value EO does not changeunless new inputs/info impact

the company’s future cashflowsoverall picture & therefore EV

www.antonioalcocer.com

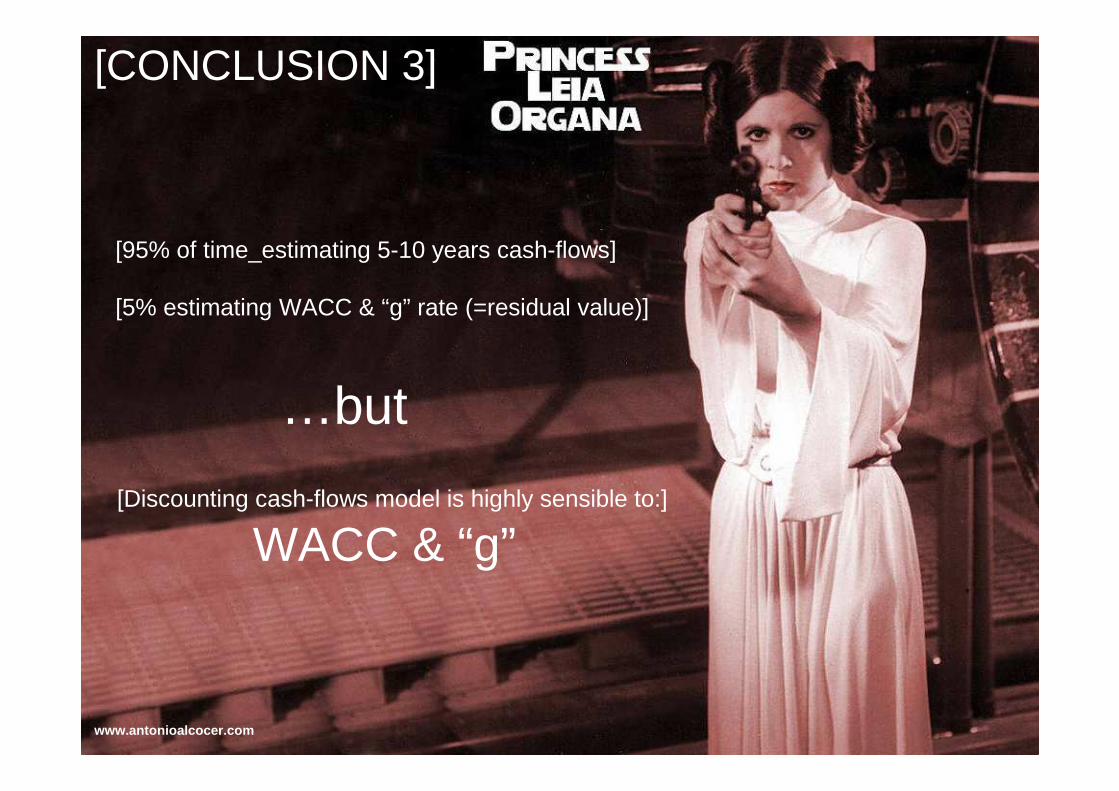

[95% of time_estimating 5-10 years cash-flows]

[5% estimating WACC & “g” rate (=residual value)]

[CONCLUSION 3]

…but

[Discounting cash-flows model is highly sensible to:]

WACC & “g”

www.antonioalcocer.com

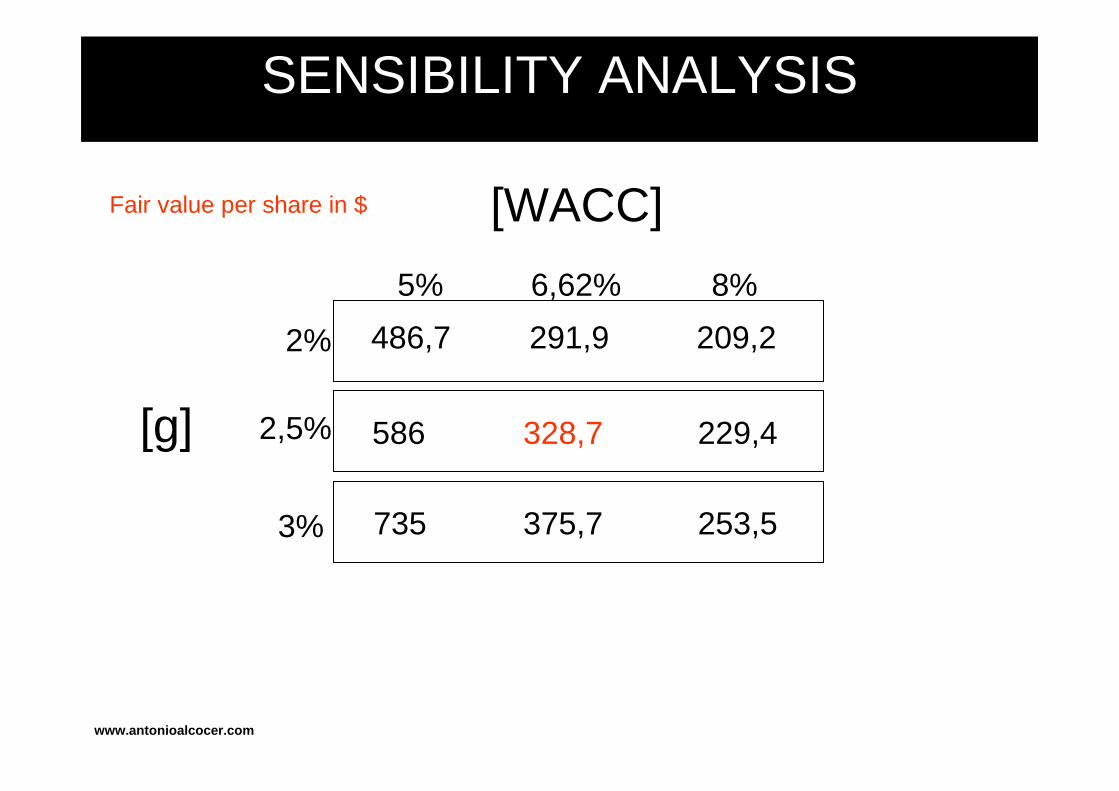

SENSIBILITY ANALYSIS

[WACC]

5% 6,62% 8%

486,7

[g]

2%

2,5%

3%

Fair value per share in $

291,9 209,2

586

735

328,7 229,4

375,7 253,5

www.antonioalcocer.com

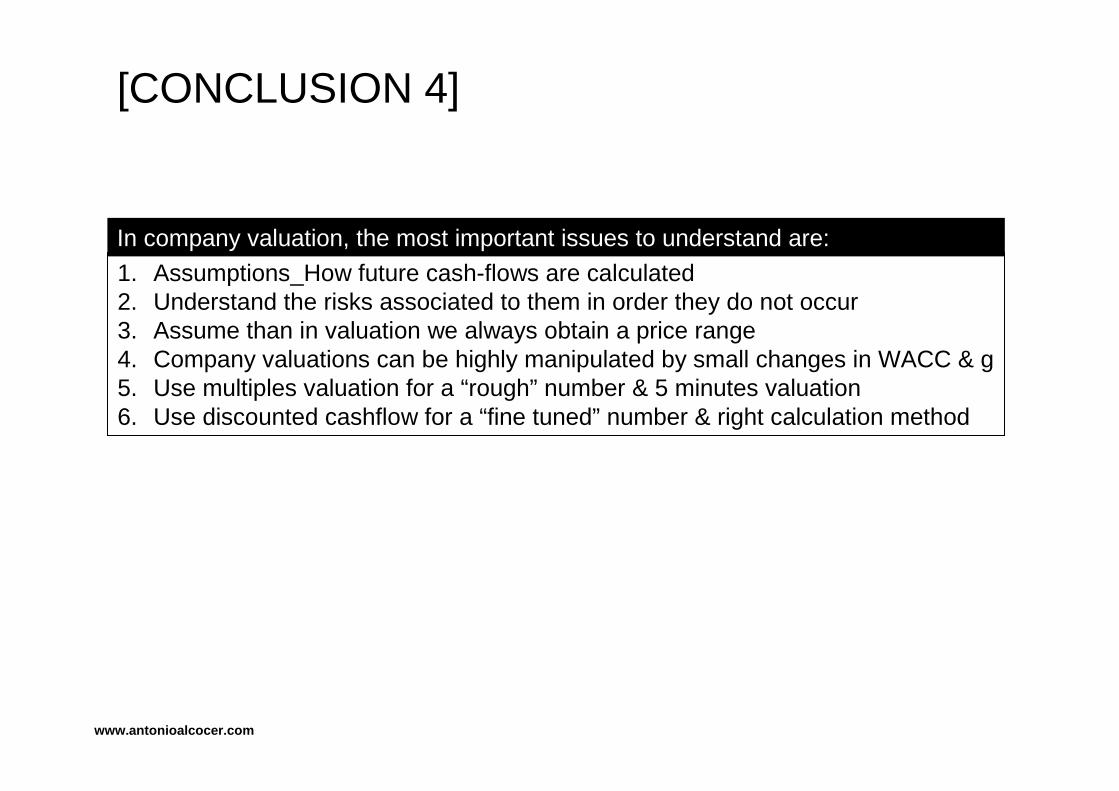

[CONCLUSION 4]

In company valuation, the most important issues to understand are:

1. Assumptions_How future cash-flows are calculated2. Understand the risks associated to them in order they do not occur3. Assume than in valuation we always obtain a price range4. Company valuations can be highly manipulated by small changes in WACC & g5. Use multiples valuation for a “rough” number & 5 minutes valuation6. Use discounted cashflow for a “fine tuned” number & right calculation method

www.antonioalcocer.com

Thank you very much for you time!Any comment, suggestion is more than welcome:

www.antonioalcocer.com@antonioalcocer