investment and institutions stijn claessens, kenichi ueda, and yishay yafeh international monetary...

TRANSCRIPT

Investment and Institutions

Stijn Claessens, Kenichi Ueda, and Yishay YafehInternational Monetary Fund and University of Amsterdam, International Monetary Fund, andHebrew University

16th Dubrovnik Economic Conference, June 24, 2010

The views expressed in this paper are those of the authors and should not be attributed to the International Monetary Fund, its Executive Board or its management.

2

MotivationMotivation

Capital is not always allocated efficiently (Hsieh and

Klenow, 2009; Abiad, Oomes, and Ueda, 2008)

TFP is the most important factor for growth.

Does the institutional environment affect the cross-

country differences in investment efficiency, and, if so,

which institutions and how?

How should we judge the cross-country differences in

investment efficiency?

3

Our ConjectureOur Conjecture

Tobin’s Q is a measure of investment

efficiency.

Tobin’s Q should be 1 in a perfect world.

If not, it should approach 1 over time.

This adjustment may be slower in countries

with worse institutions.

4

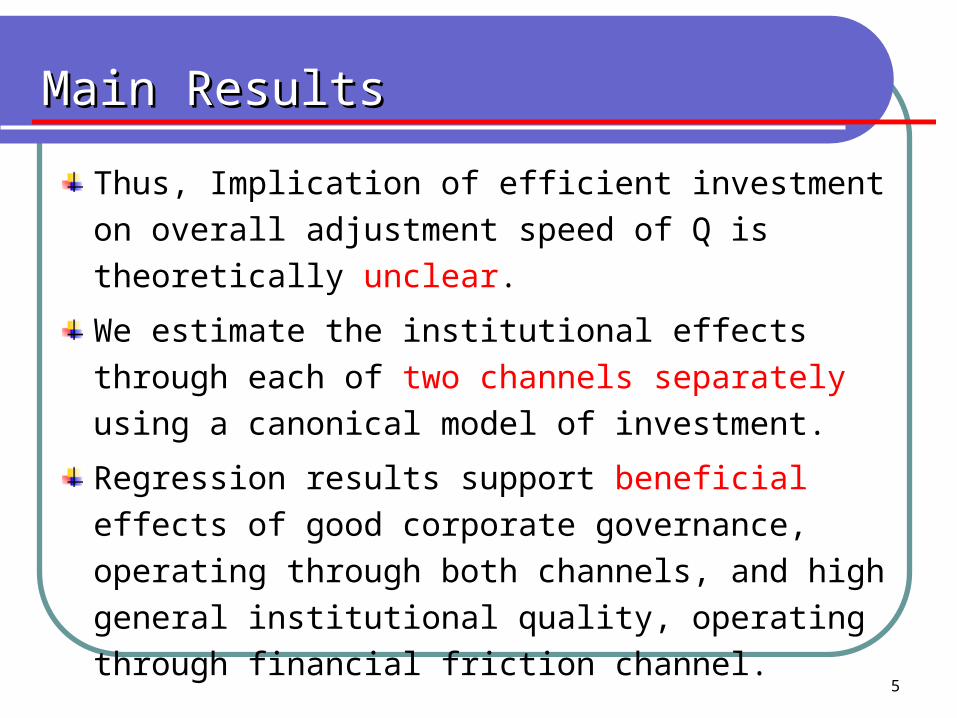

Main ResultsMain Results

Good institutions can affect the investment

efficiency through two channels:

Lower required return allows a larger adjustment

in Q (from above) as the required capital gain (given

current profits) is less.

Less financial frictions create less divergence of

Tobin’s Q from its steady state to begin with,

implying slower adjustment in Q.

5

Main ResultsMain Results

Thus, Implication of efficient investment on overall

adjustment speed of Q is theoretically unclear.

We estimate the institutional effects through each of

two channels separately using a canonical model of

investment.

Regression results support beneficial effects of good

corporate governance, operating through both

channels, and high general institutional quality,

operating through financial friction channel.

6

Literature: Finance-Efficiency LinkLiterature: Finance-Efficiency Link

Efficiency of allocating capital across sectors has

been estimated using a variety of measures

GDP growth or TFP growth (e.g., Beck, Loayza, and

Levine, 2000; De Nicolo, Laeven, and Ueda, 2008)

Industry growth (e.g., Rajan and Zingales, 1998, and

Wurgler, 2000).

Dispersion of firm-level productivity (e.g., Hsieh and

Klenow, 2009, and Abiad, Oomes, and Ueda, 2008).

7

Literature: Tobin’s QLiterature: Tobin’s Q

Tobin's Q measures efficiency in the use of capital (Tobin, 1969)

Speed of investment adjustment relates to Q (Mussa, 1977).

Because of adjustment costs, investment and Tobin’s Q relate in

non-linear ways (Abel and Eberly, 1994) without financial

frictions.

With financial frictions, the sign of cash-flow sensitivity of

investment becomes difficult to predict (Gomes, 2000).

Moreover, market imperfections and varying discount factors

affect movements in Q (Abel and Eberly, 2008).

(Measurement error issues are discussed later.)

8

Literature: Measures of SystemsLiterature: Measures of Systems

Many measures have been developed/collected for

institutional and financial development (e.g.,

Demirguc-Kunt and Levine, 2001, Morck et al, 2000,

La Porta et al., 2008).

These allow comparisons of financial and governance

systems around the world.

9

ModelModel

Develop a canonical model of Tobin’s Q with both adjustment cost of investment and financial frictions (Abel and Blanchard (1986), Abel and Eberly (1994, 2008), Gomes (2000), and Hennessy et al. (2007)).

10

TimingTiming

Given K– and revealed current productivity ε at the

beginning of the current period:

Investment I is determined

Adjustment costs ϕ are wasted on investment

New capital K is formed and usable immediately

Using K, goods are produced with productivity ε

Fees λ paid for external financing (over-the-period)

11

ModelModel

( , ) ( , )t t t t t t tK f K L w L

1(1 ) tt tIK K

1 1, , ( , ) (1 ) ( , )t t t t tt t t t tB K K I K K K K ò

max , ) ( , ; , , )

( , ; ,

1( ; ) (

1

) ( ;, )

KI K X W

B K X

V

K

r

V

K K

EW

12

TimingTiming

First-order condition

Envelope condition

Combined together and use

1 1 1 1 11 2 2 E V

1 1 1(1 )(1 )r V

1Q V

1 1 2 2(1 (1 ))E Q r Q

13

Adjustment Speed of QAdjustment Speed of Q

Adjustment in Q depends on required return and frictions

Lower required return allows a larger adjustment in Q

(from above) as the required capital gain (given current

profits) is less.

Less financial frictions creates less divergence of Tobin’s Q

from its steady state to begin with, implying slower

adjustment in Q.

1 2 21) (1(1 )()

)(

E Qr

Q

Q

Q

14

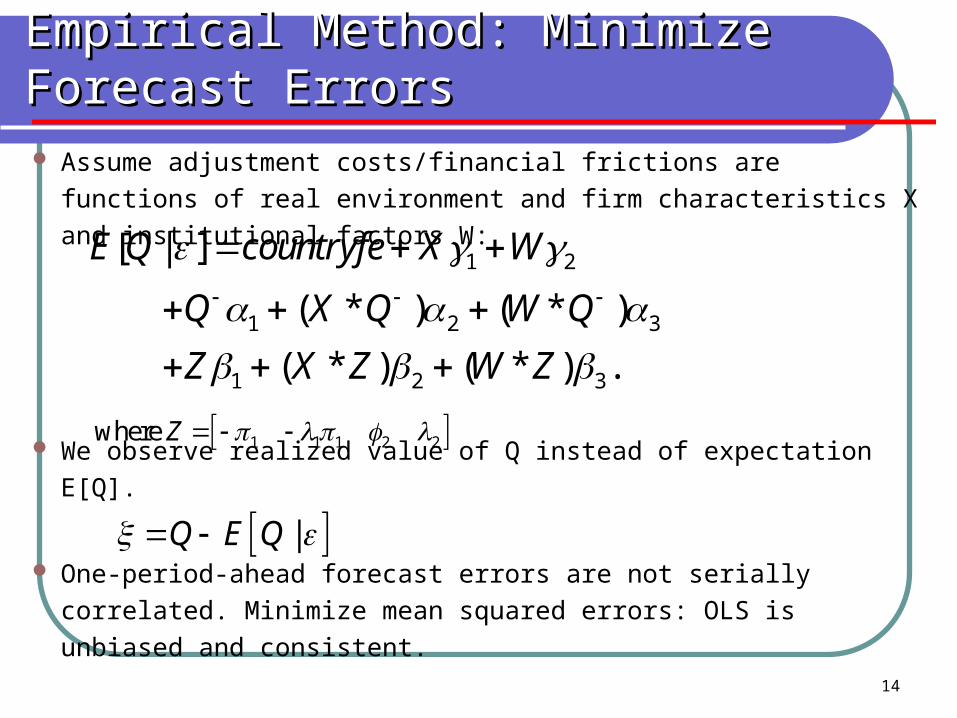

Empirical Method: Minimize Forecast ErrorsEmpirical Method: Minimize Forecast Errors

Assume adjustment costs/financial frictions are functions of real

environment and firm characteristics X and institutional factors W:

We observe realized value of Q instead of expectation E[Q].

One-period-ahead forecast errors are not serially correlated.

Minimize mean squared errors: OLS is unbiased and consistent.

|Q E Q

1 2

1

2 3

2 3

1

[ | ]

( ) )* ( *

( * ) ( * ) .

E Q

Q Q Q

countryfe X W

X W

X Z W ZZ

1 1 1 2 2where Z

15

Estimation: Parameterization of CostsEstimation: Parameterization of Costs

1 2

2

3( , , )2

b Bb B b K K

KB K

2

32 2 2

a I

Ka

32

2

1( , , )2

aa I a KK

KK

II

11 3

Bb b

K

3

2

2 2 2

b Bb

K

16

Assumptions on Parameters and VariablesAssumptions on Parameters and Variables

Each coefficient (a2, a3, b1, b2, and b3) of

adjustment cost and financial friction functions

are assumed to be linear functions of real

environment and characteristics (X) and

institutional factors (W).

Make similar assumption for the required return

r, which constitute a coefficient c on lagged Q.

c(X, W)

17

Equation to be EstimatedEquation to be Estimated

, ,

, , , , , 1

, , , , ,

2 , , , , ,

2

, , , , , ,3 , ,

, , , 1, , , ,

1 1, , , ,

1, , , , ,, , , , , ,

,

,

,

2

,

,

,

,

1,

2

i j k t i

j k t k

j k t k i j k t

j k t k i j k t

j k t k i j k t

i j k t i j k tj k t k i j k t

i

j k t

i

j k t i j

j k t

i jt

j

tk

k

Q

a Q

b

b

B

X W

X W

X W

X W

X WB

bA A

c X

,

, ,3 , ,

, ,

, , ,

2

, ,

,

,,

, , ,

k t

i j kj k t

i j

i j k t

i j k t

i j k t

k t

IXc

A

18

Firm Level Data

Firm level data: Worldscope, 1990-2007, 48

countries.

Before tax income / After tax income

Capital investment / Capex + security investment

RZ external finance / Increase in debt + equity fin.

19

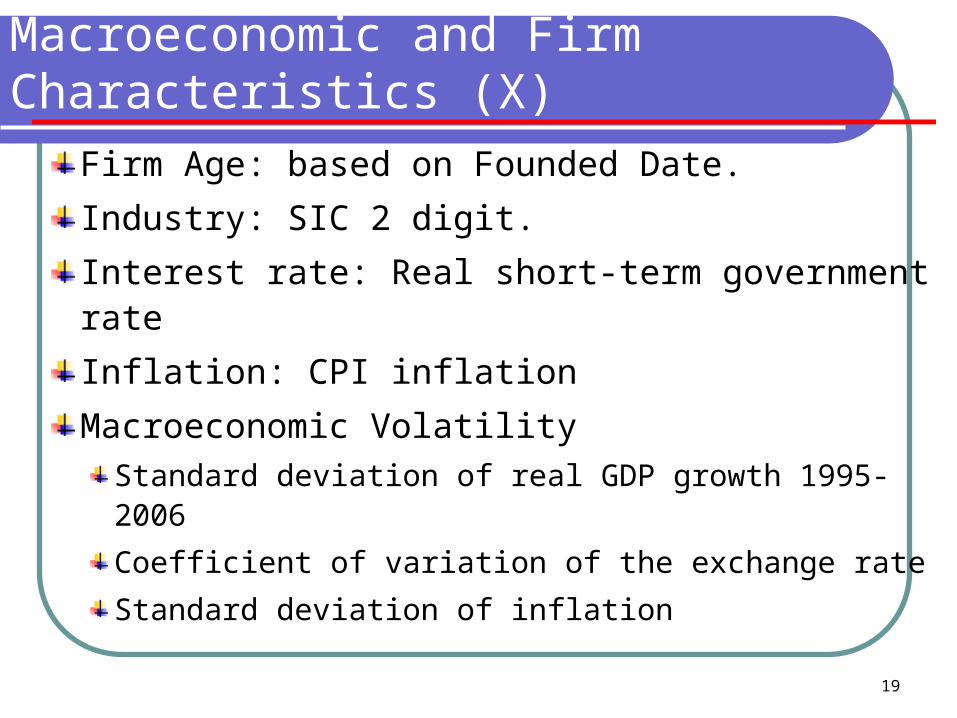

Macroeconomic and Firm Characteristics (X)

Firm Age: based on Founded Date.

Industry: SIC 2 digit.

Interest rate: Real short-term government rate

Inflation: CPI inflation

Macroeconomic Volatility

Standard deviation of real GDP growth 1995-2006

Coefficient of variation of the exchange rate

Standard deviation of inflation

20

Institutions (W)

Corporate Governance (Shareholder Protection)

Anti-director index (La Porta, et al., 1998; Spamann, 2009)

Self-dealing index (Djankov, et al., 2008)

CGQ index (De Nicolo, Laeven and Ueda, 2008)

Creditor Rights

Strength of Legal Rights (for creditors/borrowers) (Doing

Business)

Creditor Rights (Djankov, McLeish, and Shleifer, 2007)

Efficiency in Bankruptcy (World Economic Forum, 2004)

21

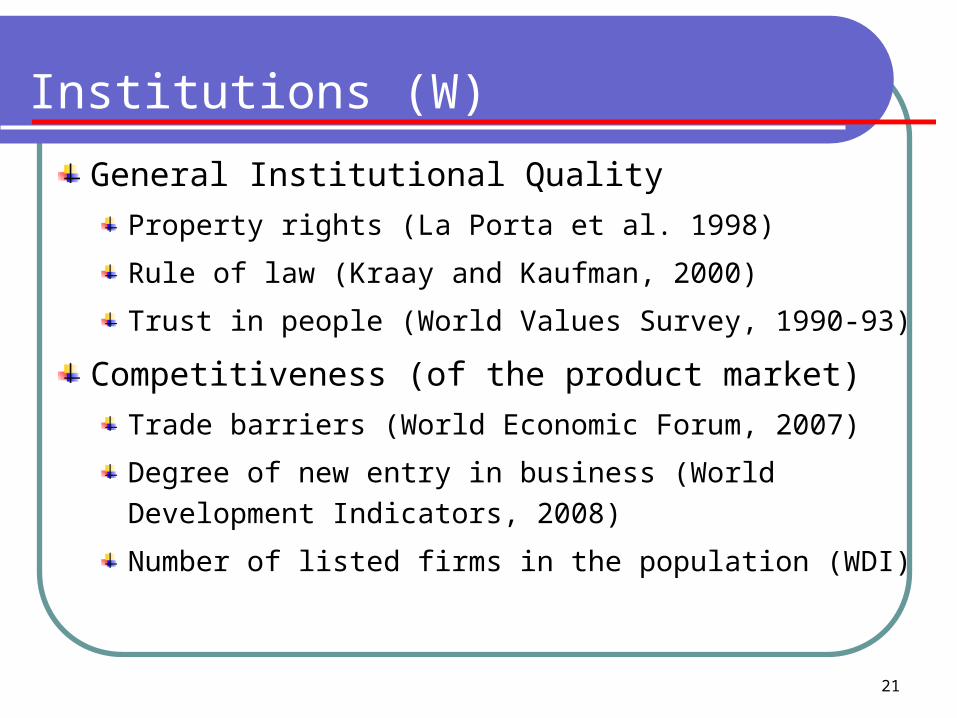

Institutions (W)

General Institutional Quality

Property rights (La Porta et al. 1998)

Rule of law (Kraay and Kaufman, 2000)

Trust in people (World Values Survey, 1990-93)

Competitiveness (of the product market)

Trade barriers (World Economic Forum, 2007)

Degree of new entry in business (World Development

Indicators, 2008)

Number of listed firms in the population (WDI)

22

Institutions (W)

Financial Market Development

Stock market-capitalization-to-GDP ratio

(International Financial Statistics)

Private credit (stocks + debt) to GDP ratio

(International Financial Statistics)

Lack of foreign ownership restrictions (World

Economic Forum)

23

Benchmark All TogetherRequired Return

(-) Fin. Friction Coeff. Ext. Fin.

Fin. Friction Coeff. Capital

(-) Fin. Friction Curvature

[1] [2] [3] [4]

Institutional Factors

Corporate Governance -0.0433 -0.0028 0.0200 0.0230

[-2.403]** [-1.778]* [2.639]*** [1.167]

Creditor Rights -0.0099 -0.0042 -0.0102 0.0399

[-0.454] [-1.119] [-1.673]* [1.148]

Institution -0.0007 0.0091 0.0639 -0.2282

[-0.016] [0.734] [3.683]*** [-1.750]*

Competitiveness 0.0772 0.0003 -0.0071 -0.0950

[1.864]* [0.045] [-0.423] [-0.858]

Financial Markets 0.0001 0.0000 0.0001 -0.0004

[0.357] [-0.167] [0.414] [-0.508]

24

One-by-One: Almost the same resultsa -b1 b2 -b3

Required Return (-) Fin. Friction Coeff. Ext. Fin.

Fin. Friction Coeff. Capital

(-) Fin. Friction Curvature

[1] [2] [3] [4]

Corporate Governance -0.0494 -0.0037 0.0222 0.0335

[-2.665]*** [-1.603] [2.964]*** [1.443]

Creditor Rights -0.0184 -0.0039 0.0077 0.0002

[-1.144] [-1.587] [1.340] [0.010]

Institution -0.0632 -0.0062 0.0535 -0.0794

[-1.534] [-0.893] [3.299]*** [-1.187]

Competitiveness 0.0858 0.0041 -0.0264 -0.0775

[2.154]** [0.737] [-1.814]* [-0.965]

Financial Market -0.0003 -0.0001 0.0002 0.0009

[-0.920] [-1.782]* [1.494] [1.684]*

25

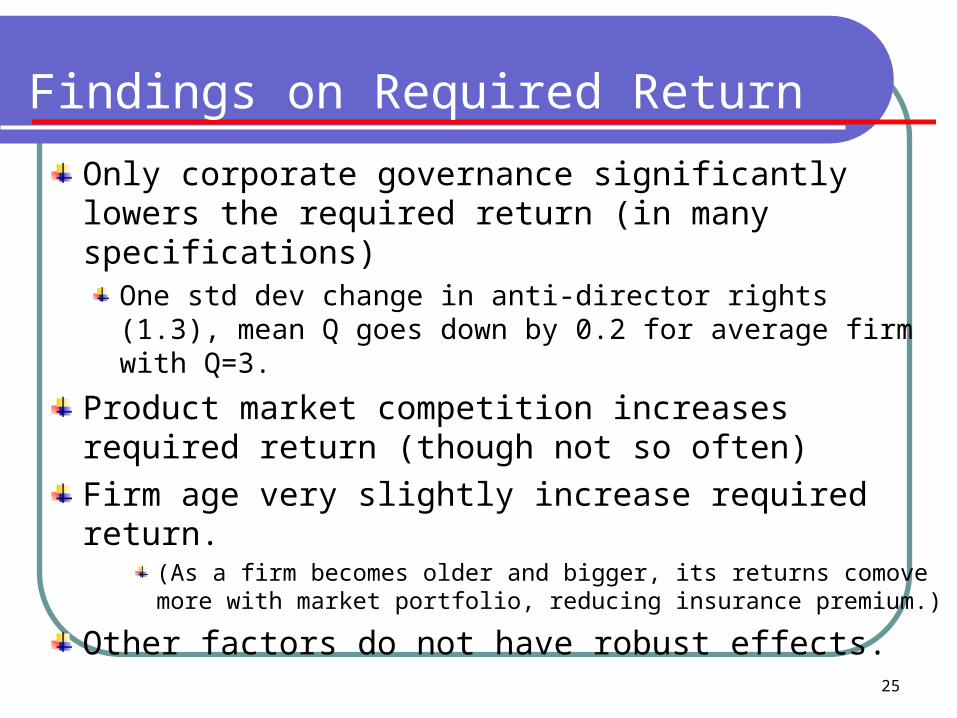

Findings on Required Return

Only corporate governance significantly lowers the required return (in many specifications)

One std dev change in anti-director rights (1.3), mean Q goes down by 0.2 for average firm with Q=3.

Product market competition increases required return (though not so often)

Firm age very slightly increase required return.(As a firm becomes older and bigger, its returns comove more with market portfolio, reducing insurance premium.)

Other factors do not have robust effects.

26

Findings on Internal Fin Frictions (2)-(4)

Slope and curvature of costs associated with the size of

external finance is little affected by any institutional

factors.

Better general institutional quality sometimes worsen the

curvature but not robust.

27

Findings on Internal Fin Frictions (2)-(4)

Extra costs that small firms need to pay (small-firm

premium) are less in country with better corporate

governance and general institutional quality (column 3).

One std dev improvements in CG lowers the premium by

about 3 cents per dollar asset.

One std dev improvements in institutional quality lowers

premium by about 4 cents per dollar assets.

Other factors do not have robust effects on

financial frictions.

28

Real Adj. Cost of Investment

Real adjustment cost of investment are not affected by X.

How about institutional factors W?

Entrenchment of managers under private information (Myers and Majluf

(1984) and workers’ sabotage (Parente and Prescott, 2000)

We find:

Better corporate governance and general institutional quality reduce

technological/managerial diseconomy of scale.

But somewhat offset by increased curvature.

Without coeff on investment, overall effect is unidentified.

Other institutional factors do not have significant effects.

All effects on financial frictions and required returns are unchanged.

29

Real Adj. Cost of Investment – CG lowers

Required Return (-) Fin. Friction Coeff. Ext. Fin.

Fin. Friction Coeff. Capital

(-) Fin. Friction Curvature

Inv. Adj. Cost Coeff. Capital

(-) Inv. Adj. Cost Curvature

[1] [2] [3] [4] [5] [6]

Institutional Factors

Corporate Governance -0.0424** -0.0027* 0.0249*** 0.0220 -0.1738*** -0.9204**

[-2.346] [-1.759] [3.193] [1.117] [-3.300] [-2.060]

Creditor Rights -0.0102 -0.0042 -0.0100 0.0411 0.0324 -0.0422

[-0.465] [-1.142] [-1.571] [1.187] [0.503] [-0.185]

Institution 0.0010 0.0094 0.0638*** -0.2332* -0.2343* -0.1380

[0.023] [0.761] [3.584] [-1.786] [-1.663] [-0.238]

Competitiveness 0.0782* 0.0005 -0.0013 -0.1008 0.1335 -0.9498

[1.885] [0.076] [-0.074] [-0.903] [0.852] [-1.633]

Financial Markets 0.0001 0.0000 0.0000 -0.0003 0.0029 0.0063

[0.356] [-0.158] [0.252] [-0.498] [1.291] [0.586]

30

Measurement Error IssuesMeasurement Error Issues

Stock Price Movements may not always reflect

fundamental values:

Abel and Blanchard (1986), Blanchard, Rhee, and

Summers (1994), Phillippon (2009) – need long time

series

Accounting Issues:

Difference between marginal and average Q Hayashi’s

(1982) assumptions make them the same; we also allow

for industry and age specific effects.

Blanchard, Rhee, and Summers (1994): market valuation

in debt and the replacement cost of capital—need long T.

31

Measurement Error IssuesMeasurement Error Issues

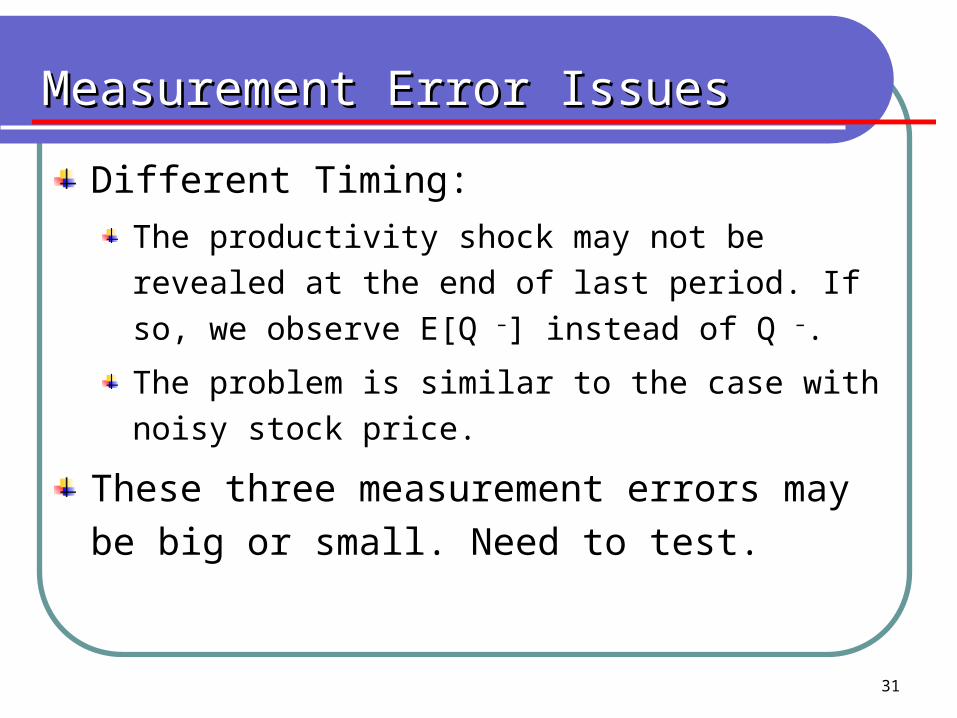

Different Timing:

The productivity shock may not be revealed at the end of

last period. If so, we observe E[Q –] instead of Q –.

The problem is similar to the case with noisy stock price.

These three measurement errors may be big or small.

Need to test.

32

Testing Measurement ErrorsTesting Measurement Errors

With measurement errors, the OLS errors are serially

correlated (even if measurement errors are not).

Cannot reject Ho (zero autocorrelation) in OLS errors.

* * 'OLS OLSu X W ' ' '( * ) '( * )OLS OLS OLSE u u E v v E v X v E v W v

33

IV EstimationIV Estimation

Measurement errors turns out small, if any, relative

to one-period-ahead forecast errors.

Still, to check robustness, we run IV estimation.

Note that, if any, there is little autocorrelation in

measurement errors. Large swings in stock prices is

likely to dominate the other sources.

We use twice-lagged Q as an instruments for lagged

Q (and fitted cross-terms as IV for cross-terms).

TSLS results are similar to the OLS-FE estimation.

34

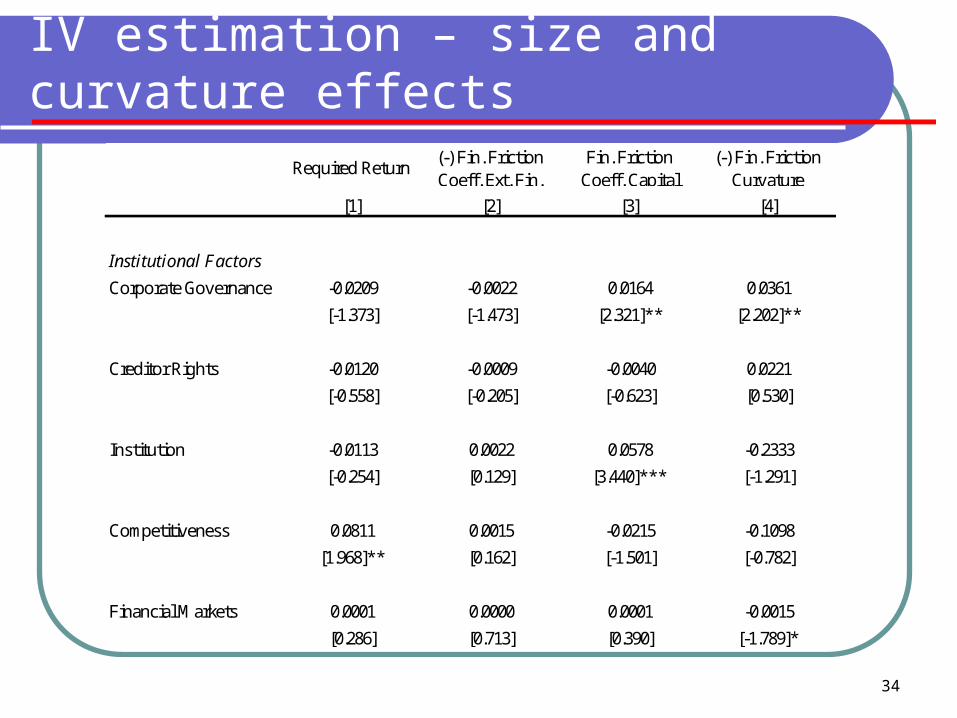

IV estimation – size and curvature effects Required Return

(-) Fin. Friction Coeff. Ext. Fin.

Fin. Friction Coeff. Capital

(-) Fin. Friction Curvature

[1] [2] [3] [4]

Institutional Factors

Corporate Governance -0.0209 -0.0022 0.0164 0.0361

[-1.373] [-1.473] [2.321]** [2.202]**

Creditor Rights -0.0120 -0.0009 -0.0040 0.0221

[-0.558] [-0.205] [-0.623] [0.530]

Institution -0.0113 0.0022 0.0578 -0.2333

[-0.254] [0.129] [3.440]*** [-1.291]

Competitiveness 0.0811 0.0015 -0.0215 -0.1098

[1.968]** [0.162] [-1.501] [-0.782]

Financial Markets 0.0001 0.0000 0.0001 -0.0015

[0.286] [0.713] [0.390] [-1.789]*

35

ConclusionConclusion

We have investigated how institutional environment

affect investment efficiency.

Good corporate governance and general institutional

quality, though less robust, are the main driving forces

to lower financial frictions, in particular, the small-firm

premium.

Also, better corporate governance lowers the required

return in many specifications.

36

ConclusionConclusion

Why is corporate governance, not creditor rights,

important? Our interpretation:

At the margin, the cost of equity finance determines the cost

of borrowing.

Cost of external finance implicitly measures investors’ fear

on mismanagement of injected cash.

37

AppendixAppendix

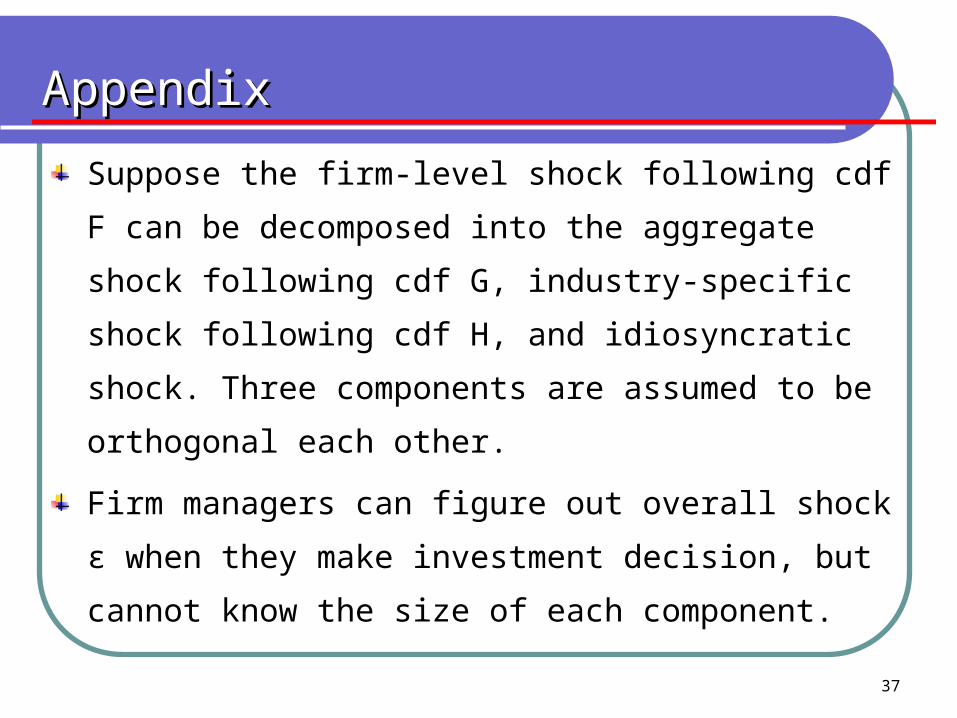

Suppose the firm-level shock following cdf F can be

decomposed into the aggregate shock following cdf G,

industry-specific shock following cdf H, and idiosyncratic

shock. Three components are assumed to be orthogonal each

other.

Firm managers can figure out overall shock ε when they make

investment decision, but cannot know the size of each

component.

38

AppendixAppendix

max , ; , ) , ) ( , ; , , )

( , ; , , ) ( )

max , ; , ) ,

( ; , ,

) ( , ; , , )

( , ; , , ) ( )

ma

)

( (

; , ,

( (

; , ,

1(

1 [ ],x , ) ( , ; , , )

( ;

,

, ,

K

K

K

X W I K X W

B K X W V K dF dGdH

X W dGdH I K X W

B K X W V K d

V K X W

m K

X W

m K

X W

K

F

I K X Wr E X W

B K X

; ,, ) ( ) .,X WW V K dF