inventory valuation

DESCRIPTION

Solution to Inventory Valuation problems.TRANSCRIPT

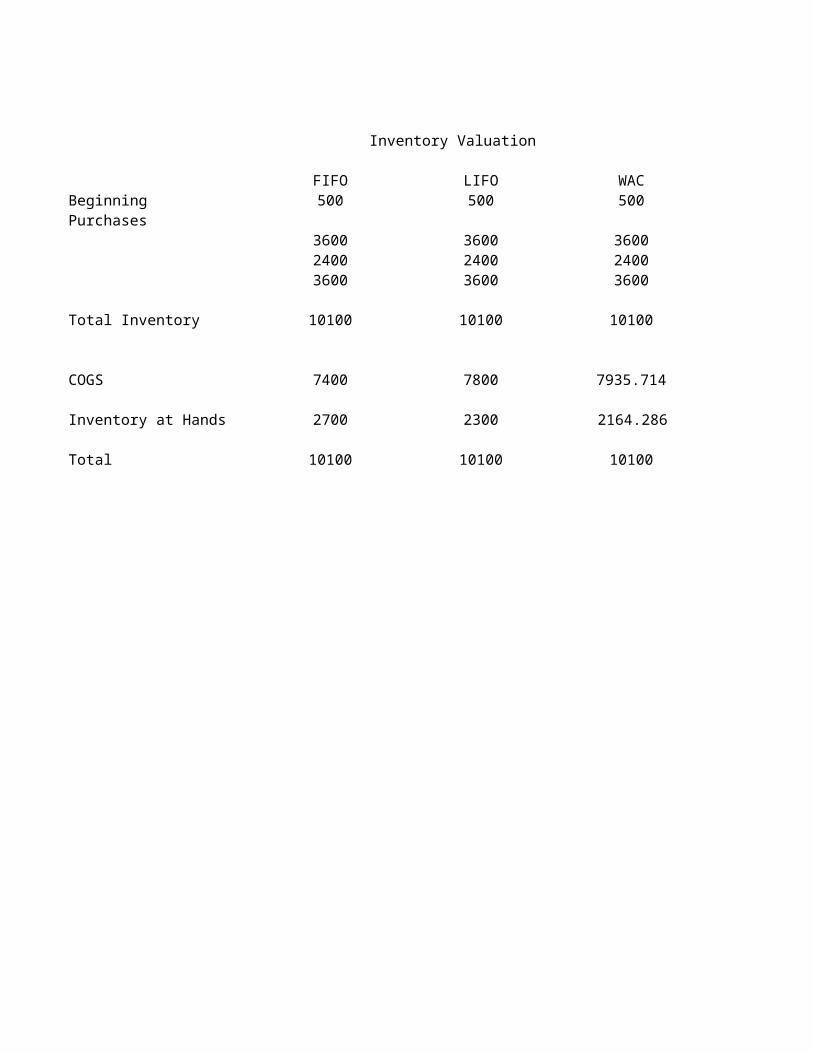

Inventory Valuation

FIFO LIFO WACBeginning 500 500 500Purchases

3600 3600 36002400 2400 24003600 3600 3600

Total Inventory 10100 10100 10100

COGS 7400 7800 7935.714

Inventory at Hands 2700 2300 2164.286

Total 10100 10100 10100

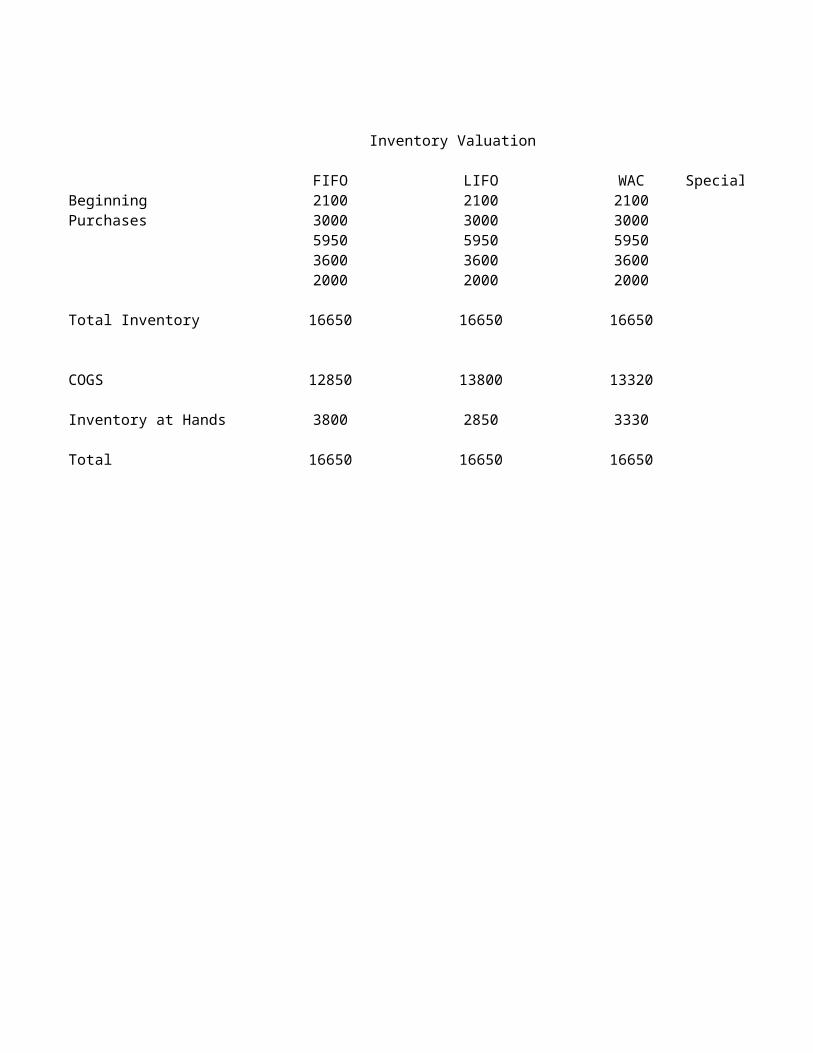

Inventory Valuation

FIFO LIFO WAC Special IdentificationBeginning 2100 2100 2100 2100Purchases 3000 3000 3000 3000

5950 5950 5950 59503600 3600 3600 36002000 2000 2000 2000

Total Inventory 16650 16650 16650 16650

COGS 12850 13800 13320 13310

Inventory at Hands 3800 2850 3330 3340

Total 16650 16650 16650 16650

Special Identification

Inventory Valuation

FIFO LIFOBeginning 80 80Purchases 200 200

350 350180 180

Total Inventory 810 810

COGS 560 605

Inventory at Hands 250 205

Total 810 810

Inventory Valuation

FIFO LIFO

Purchases 200 200350 350180 180

Total Inventory 730 730

COGS 480 525

Inventory at Hands 250 205

Total 730 730

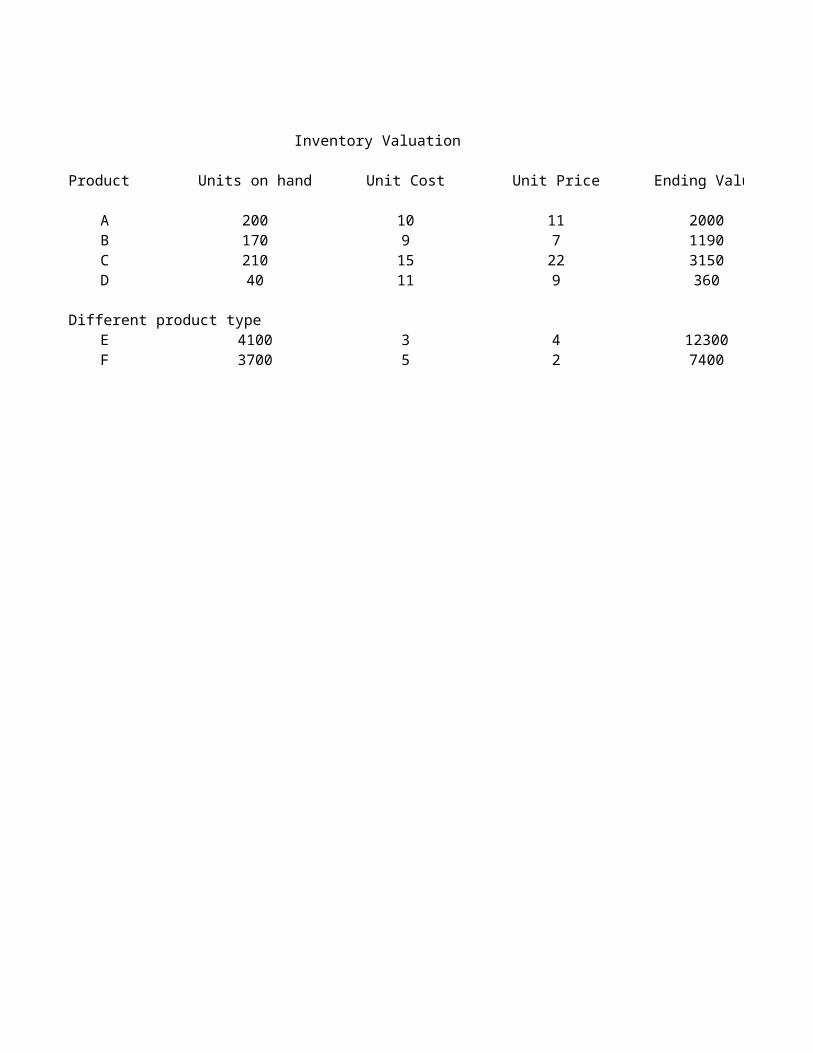

Inventory Valuation

Product Units on hand Unit Cost Unit Price Ending Value

A 200 10 11 2000B 170 9 7 1190C 210 15 22 3150D 40 11 9 360

Different product typeE 4100 3 4 12300F 3700 5 2 7400

Fairdeal Income statement

2007 2008

Net Sales 22860 Net Sales 24500

Inventory InventoryBeginning 4790 Beginning 4810Purchases 18300 Purchases 19580

23090 24390

Ending Inventory 4650 Ending Inventory 5320

COGS 18440 COGS 19070Gross Profit 4420 Gross Profit 5430Expenses 2310 Expenses 2310Net profit 2110 Net profit 3120

There is a difference of Rs.70 due to the mistakes committed in the inventory

5230

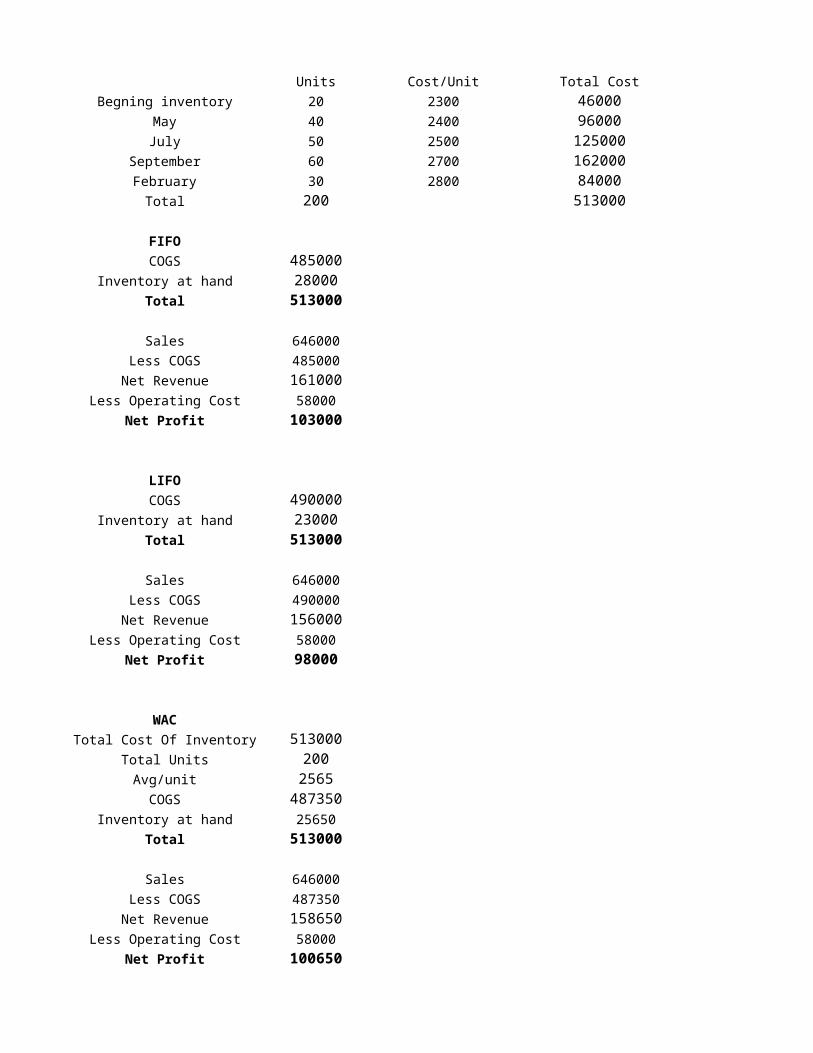

Units Cost/Unit Total Cost

Begning inventory 20 2300 46000May 40 2400 96000July 50 2500 125000

September 60 2700 162000February 30 2800 84000

Total 200 513000

FIFO

COGS 485000Inventory at hand 28000

Total 513000

Sales 646000

Less COGS 485000

Net Revenue 161000Less Operating Cost 58000

Net Profit 103000

LIFO

COGS 490000Inventory at hand 23000

Total 513000

Sales 646000

Less COGS 490000

Net Revenue 156000Less Operating Cost 58000

Net Profit 98000

WAC

Total Cost Of Inventory 513000Total Units 200

Avg/unit 2565COGS 487350

Inventory at hand 25650

Total 513000

Sales 646000

Less COGS 487350

Net Revenue 158650Less Operating Cost 58000

Net Profit 100650

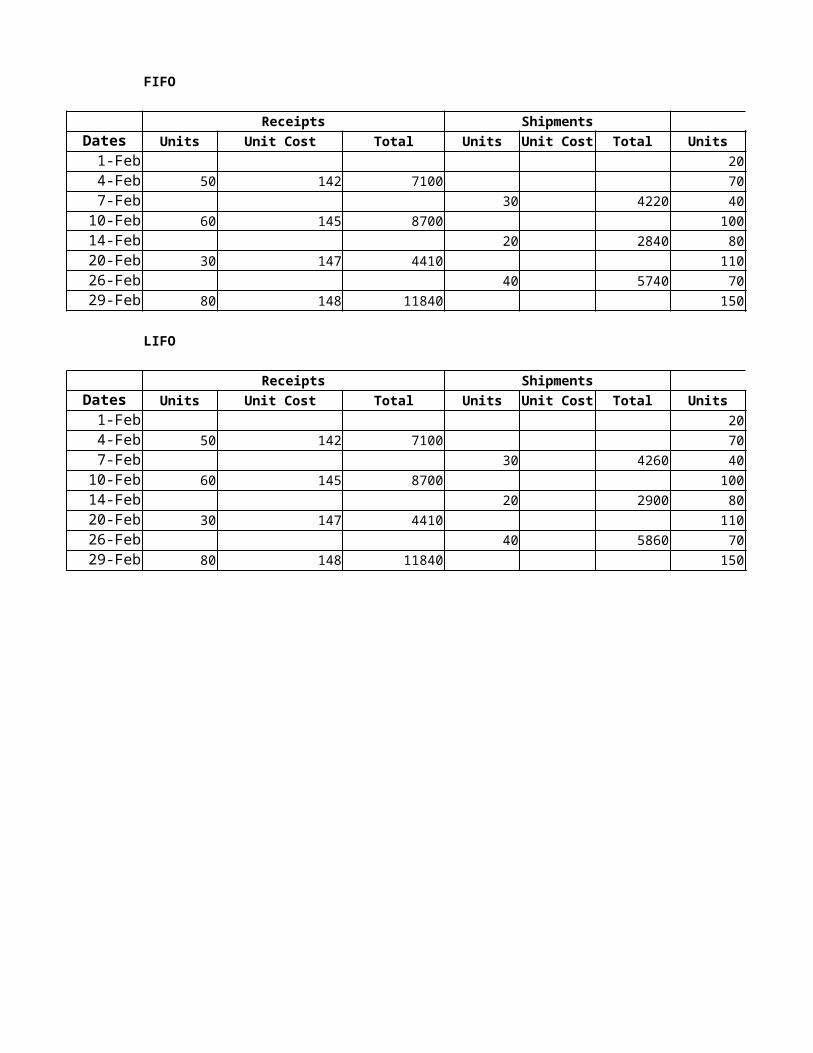

FIFO

Receipts Shipments Balance

Dates Units Unit Cost Total Units Unit Cost Total Units Unit Cost

1-Feb 20 140

4-Feb 50 142 7100 70

7-Feb 30 4220 40

10-Feb 60 145 8700 100

14-Feb 20 2840 80

20-Feb 30 147 4410 110

26-Feb 40 5740 70

29-Feb 80 148 11840 150

LIFO

Receipts Shipments Balance

Dates Units Unit Cost Total Units Unit Cost Total Units Unit Cost

1-Feb 20 140

4-Feb 50 142 7100 70

7-Feb 30 4260 40

10-Feb 60 145 8700 100

14-Feb 20 2900 80

20-Feb 30 147 4410 110

26-Feb 40 5860 70

29-Feb 80 148 11840 150

Balance

Total

2800

9900

5680

14380

11540

15950

10210

22050

Balance

Total

2800

9900

5640

14340

11440

15850

9990

21830

Sanu CompanyInventory Valuation

Units on hand Unit Cost Unit Price After Commission & Del.Product Group 1A 134 210 450 480 495A 156 140 530 670 583N 278 65 480 520 528P 345 83 510 360 561

Product Group 2R 098 13 650 800 800R 112 17 750 760 900T 034 26 680 740 816T 041 19 610 780 732

After Commission & Del. Ending Value

100800816203380029880

10400129201924013908

Units Cost/Unit Total Cost

Begning inventory 10000 18 180000Purchases 15000 19 285000

10000 21 21000020000 22 44000010000 23 230000

Total 65000 1345000

FIFO

COGS 1005000Inventory at hand 340000Total 1345000

Sales 1400000

Less COGS 1005000

Gross Revenue 395000Less Operating Cost 185000

Revenue 210000Income Taxes 84000

Net Profit 126000

LIFO

COGS 1070000Inventory at hand 275000Total 1345000

Sales 1400000

Less COGS 1070000

Gross Revenue 330000Less Operating Cost 185000

Revenue 145000Income Taxes 58000

Net Profit 87000

2. The company is benefitted by LIFO method when it comes to income tax reporting as we can see the NET Profit is down by $ 39000 and the Income tax is reduced by $ 26000, but there is a trade-off between the

Shareholder's reporting as we need to more liquidity for investor confidence.

Units Cost/Unit Total Cost

Begning inventory 10000 18 180000Purchases 15000 19 285000

10000 21 21000020000 22 44000010000 23 23000015000 25 375000

Total 80000 1720000

FIFO

COGS 1005000Inventory at hand 715000Total 1720000

Sales 1400000

Less COGS 1005000

Gross Revenue 395000Less Operating Cost 185000

Revenue 210000Income Taxes 84000

Net Profit 126000

LIFO

COGS 1150000Inventory at hand 570000Total 1720000

Sales 1400000

Less COGS 1150000

Gross Revenue 250000Less Operating Cost 185000

Revenue 65000Income Taxes 26000

Net Profit 39000

3. When the company is buying additional 15000 CDs by LIFO method its margins & profits are further reduced and the NET profit comes

down to $39000

Goodwill

2007 2008

Net Sales 547200 Net Sales 434000

Inventory InventoryBeginning 73200 Beginning 65900Purchases 481700 Purchases 398100

554900 446000

Ending Inventory 65900 Ending Inventory 51900

COGS 489000 COGS 412100Gross Profit 58200 Gross Profit 21900Expenses 28700 Expenses 31200Net profit 29500 Net profit -9300

There is a difference of Rs.20200 due to the mistakes committed in the inventory

20200

Mohan FurnitureUnits Cost/Unit Total Cost

Begning inventory 20 1000 20000March 20 1100 22000June 10 1200 12000August 30 1300 39000November 20 1400 28000Total 100 121000

FIFO

COGS 107000Inventory at hand 14000Total 121000

Sales 144000

Less COGS 107000

Net Revenue 37000Less Operating Cost 16000

Net Profit 21000

LIFO

COGS 111000Inventory at hand 10000Total 121000

Sales 144000

Less COGS 111000

Net Revenue 33000Less Operating Cost 16000

Net Profit 17000

WAC

Total Cost Of Inventory 121000Total Units 100Avg/unit 1210COGS 108900Inventory at hand 12100

Total 121000

Sales 144000

Less COGS 108900

Net Revenue 35100Less Operating Cost 16000

Net Profit 19100

Swimming Caps CompanyFIFO

Receipts Shipments Balance

Dates Units Unit Cost Total Units Unit Cost Total Units Unit Cost Total

1-Nov 40 70 2800

3-Nov 80 71 5680 120 8480

8-Nov 100 7060 20 1420

15-Nov 40 73 4380 60 5800

17-Nov 50 3610 10 2190

21-Nov 30 74 2220 40 4410

26-Nov 30 76 2280 70 6690

28-Nov 20 1470 50 5220

LIFO

Receipts Shipments Balance

Dates Units Unit Cost Total Units Unit Cost Total Units Unit Cost Total

1-Nov 40 70 2800

3-Nov 80 71 5680 120 8480

8-Nov 100 7080 20 1400

15-Nov 40 73 4380 60 5780

17-Nov 50 4320 10 1460

21-Nov 30 74 2220 40 3680

26-Nov 30 76 2280 70 5960

28-Nov 20 1520 50 4440

Mario CompanyInventory Valuation

Units on hand Unit Cost Unit Price After Commission & Del.Product Group 1A 087 130 210 280 231C 134 170 230 300 253F 169 100 250 260 275J 314 120 220 200 242

Total Inventory

Product Group 2P 518 10 890 920 1078S 098 20 850 970 1030U 126 35 720 840 874Y 376 10 780 800 946

Total Inventory

After Commission & Del. Ending Value

30030430102600024000

123040

920019400294008000

66000

Units Cost/Unit Total Cost

Begning inventory 1000 70 70000 Begning inventory

Purchases 5000 75 375000 Purchases

8000 76 6080009000 80 720000

Total 23000 1773000Total

FIFO

COGS 1533000 FIFO

Inventory at hand 240000 COGS

Total 1773000 Inventory at hand

Total

Sales 2400000

Less COGS 1533000 Sales

Gross Revenue 867000 Less COGS

Less Operating Cost 365000 Gross Revenue

Revenue 502000 Less Operating Cost

Income Taxes 150600 Revenue

Income Taxes

Net Profit 351400Net Profit

LIFO

COGS 1553000 LIFO

Inventory at hand 220000 COGS

Total 1773000 Inventory at hand

Total

Sales 2400000

Less COGS 1553000 Sales

Gross Revenue 847000 Less COGS

Less Operating Cost 365000 Gross Revenue

Revenue 482000 Less Operating Cost

Income Taxes 144600 Revenue

Income Taxes

Net Profit 337400Net Profit

2. The company is benefitted by LIFO method when it comes to income tax reporting as we can see the NET Profit is down

by $ 14000 and the Income tax is reduced by $ 6000, but there is a trade-off between the Shareholder's reporting as we need

to more liquidity for investor confidence.

3. When the company is buying additional 4000 CDs by LIFO method its margins & profits are further

reduced and the NET profit comes down to $41300

Units Cost/Unit Total Cost

1000 70 700005000 75 3750008000 76 6080009000 80 7200004000 85 340000

27000 2113000

1533000580000

2113000

2400000

1533000

867000365000

502000150600

351400

1592000521000

2113000

2400000

1592000

808000365000

443000132900

310100

3. When the company is buying additional 4000 CDs by LIFO method its margins & profits are further

reduced and the NET profit comes down to $41300

Assesment of Damage

Girdhar Clothing Company

Starting 17200Purchased 145200Goods available 162400

Sales 196500COGS 157200Expense 8100Profit Margin 149100

Loss Due to fire 5200

In event of rise of 2% in selling price

Girdhar Clothing Company

Starting 17200Purchased 145200Goods available 162400

Sales 200430COGS 157200Expense 8100Profit Margin 149100

Loss Due to fire 5200

In event of of rise of 2% in selling price the cost of goods damaged remains same

Ans 17 (i)

Ans 17 (ii)Noble Crus definitely uses LIFO

Ans 17 (iii)

The Wine Investment fund accounts for portflio consisting companies that use the LIFO method which shows profits even during the bearish market. This will help in pricing the funds costlier than general Index

The defense clearly states that they are not using genuine method of accounting and shall place the proper accounting in the coming year.