introduction 3 - mpc€¦ · malaysia and top 10 countries 8 competitiveness ... second among asean...

TRANSCRIPT

1

2

Introduction 3

WEF’s Assessment of Malaysia’s Competitiveness Performance 3

Measuring Competitiveness 4

Highlights: Malaysia’s Competitiveness Strengths and Areas for Improvement 6

Malaysia and Top 10 Countries 8

Competitiveness Performance in the Asia Pacific and ASEAN 9

Malaysia’s Performance in the Global Competitiveness Index 2013-2014 11

Institutional Strengths 12

Ensuring Integrated and Efficient Infrastructure 14

The Macroeconomic Environment 16

Keeping Healthcare and Primary Education in Perspective 17

Quality Workforce through Higher Education & Training 19

Promoting A Better Goods Market Through Efficiency 21

Competitive Labour Market 22

Financially Effective 24

Advancing Technological Readiness 25

Going for Global Markets 27

Bringing Sophistication to Business 28

Empowering Innovation 29

Evolution in Malaysia's Competitiveness Performance 31

Competitiveness Enhancement Initiatives 32

Committed to Transform the Nation 32

Appendices

1. Global Competitiveness Index 2013-2014 Rankings and 2012-2013 Comparisons 33

2. The Global Competitiveness Index 2013-2014 Rankings for the Asia Pacific and

ASEAN Countries 37

3. List of Countries/Economies at Each Stage of Development 38

4. ASEAN’s Competitiveness Landscape: A mixed picture with encouraging trends 39

3

PERFORMANCE OF MALAYSIA IN THE GLOBAL COMPETITIVENESS

REPORT 2013-2014

INTRODUCTION

Malaysia moved up one position and maintains its top position among countries in the

transition stage of development from an efficiency-driven to innovation-driven stage.

1. The Global Competitiveness Report 2013-2014 (GCR 2013-2014) by the World

Economic Forum (WEF) based in Geneva, Switzerland covers 148 countries (GCR 2012-

2013: 144 countries). In the Report which was released to the public on 4th

September 2013,

Malaysia ranked at 24th

position (GCR 2012-2013: ranked 25th) and is among the top 20%

of the most competitive economies globally.

2. Malaysia has sustained its position in the transition stage of development from an

efficiency-driven to innovation-driven stage with an increase in GDP per capita to

USD10,304 in 2012 from USD9,700 previously.

3. Malaysia advances one position to 24th. Second among ASEAN countries, behind

Singapore, Malaysia ranks no lower than 51st in any of the 12 pillars of the GCI and features in

the top of two of them. Its most notable advantages are its efficient and competitive

market for goods and services (10th

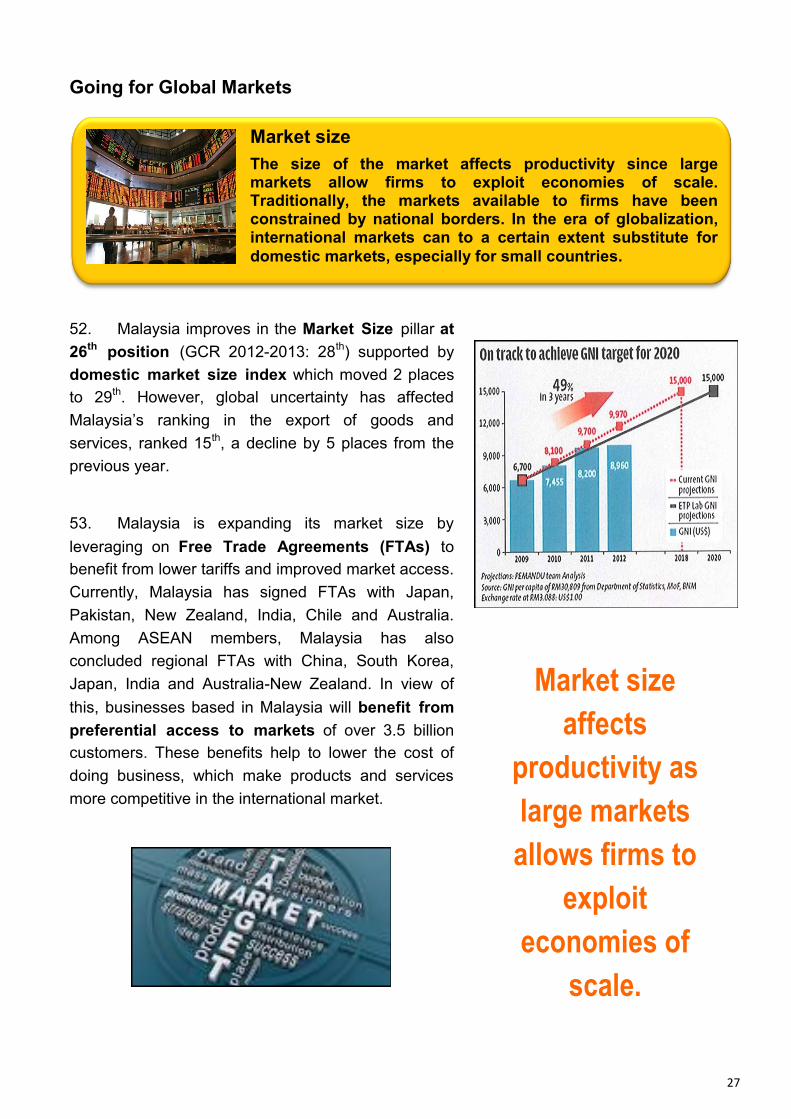

), its well-developed and sound financial markets

(6th

), and its business-friendly institutional framework (29th

).

Table 1: Sub-index Weights and Income Thresholds for Stages of Development

WEF’s Assessment of Malaysia’s Competitiveness Performance

Stages of Development

Stage 1: Transition from Stage 2: Transition from

stage 2 to stage 3

Stage 3:

Factor Driven stage 1 to stage 2 Efficiency-driven Innovation-driven

GDP per capita (US$) thresholds*

<2,000 2,000-2,999 3,000-8,999 9,000-17,000 >17,000

Weight for basic requirements sub-index

60% 40-60% 40% 20-40% 20%

Weight for efficiency enhancers sub-index

35% 35-50% 50% 50% 50%

Weight for innovation and sophistication factors sub-index 5% 5-10% 10% 10-30% 30%

Source: GCR 2013-2014, WEF

4

4. In a region plagued by corruption and red tape, Malaysia stands out as one of the

very few countries that have been relatively successful at tackling these two issues, as

part of its economic and government transformation programmes. The country, for

instance, ranks an impressive 8th

for the burden of government regulation, although the

score differential with the leader, Singapore, remains large. Malaysia ranks a satisfactory

33rd

in the ethics and corruption component of the Index, but room for improvement

remains. Furthermore, Malaysia ranks 15th

for the quality of its transport infrastructure,

a remarkable feat in this part of the world, where insufficient infrastructure and poor

connectivity are major obstacles to development for many countries.

5. Malaysia’s private sector is highly sophisticated (20th

) and already fairly

innovative (25th

). All this bodes well for a country that aims to become a high-income,

knowledge-based economy by the end of the decade. Amid this largely positive

assessment, the government budget deficit, (103rd

) at 4.3% of GDP in 2012; the low

level of female participation in the workforce (121st

); and the consistently low

technological readiness (51st

), stand out as some major weaknesses of Malaysia’s

competitiveness.

Measuring Competitiveness

6. The GCR 2013-2014 uses 30% statistical data (34 criteria) and 70% survey data

(80 criteria) from the Executive Opinion Survey. The report examines factors enabling

national economies to achieve sustained economic growth and long term prosperity

through its 12 pillars of competitiveness involving 114 indicators. The pillars are:

Institutions

Infrastructure

Macroeconomic Environment

Health & Primary Education

Higher Education & Training

Goods Market Efficiency

Labour Market Efficiency

Financial Market Development

Technological Readiness

Market Size

Business Sophistication

Innovation

5

7. Although the pillars are aggregated into a single index, measures are reported for

the 12 pillars separately because such details provide a sense of the specific areas in

which a particular country needs to improve. The GCI takes the stages of development

into account by attributing higher relative weights to those pillars that are more

relevant for an economy given its particular stage of development. That is, although

all 12 pillars matter to a certain extent for all countries, the relative importance of each one

depends on a country’s particular stage of development.

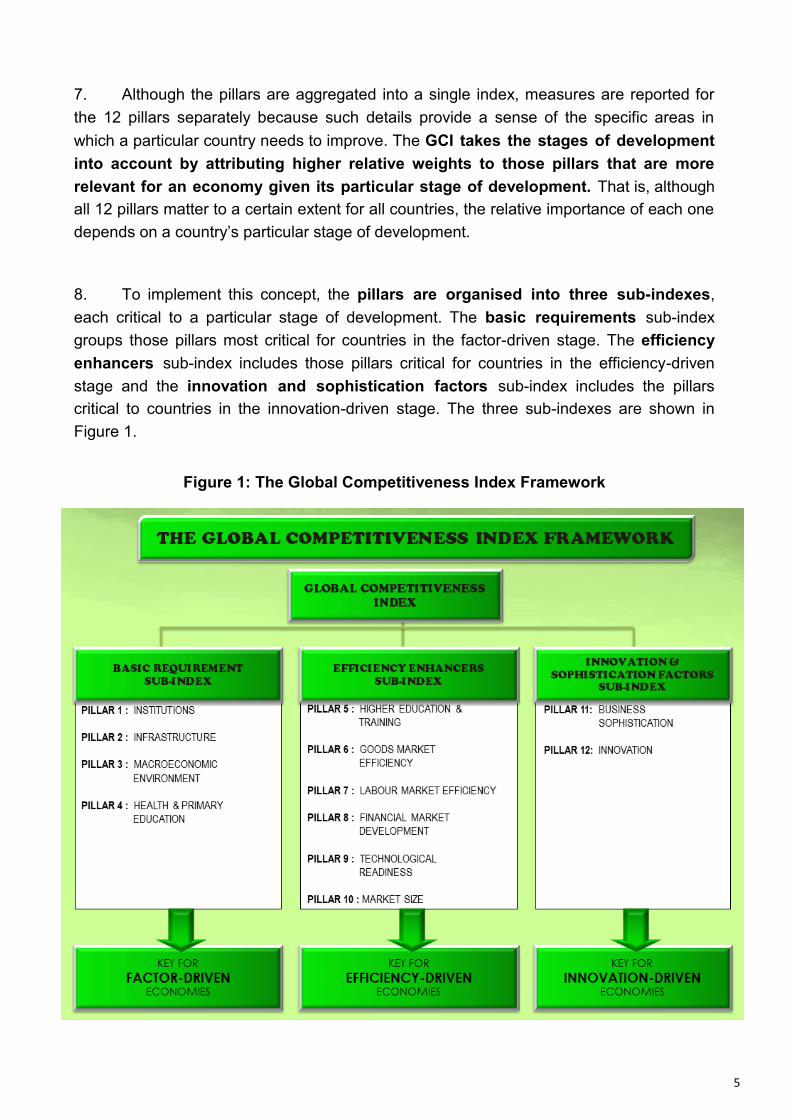

8. To implement this concept, the pillars are organised into three sub-indexes,

each critical to a particular stage of development. The basic requirements sub-index

groups those pillars most critical for countries in the factor-driven stage. The efficiency

enhancers sub-index includes those pillars critical for countries in the efficiency-driven

stage and the innovation and sophistication factors sub-index includes the pillars

critical to countries in the innovation-driven stage. The three sub-indexes are shown in

Figure 1.

Figure 1: The Global Competitiveness Index Framework

6

Malaysia’s Competitiveness Strengths and Areas for Improvement

9. At 24th

, Malaysia maintains its position at the top 20% among 148 countries

ahead of Korea (25th), Brunei Darussalam (26

th), Israel (27

th), Ireland (28

th) and People’s

Republic of China (29th). Malaysia reaffirms once again its top position among 22

countries in the transition stage from an efficiency-driven to innovation-driven, with an

increase in GDP per capita from USD9,700 to USD10,304 in 2012. At this position,

Malaysia’s aspiration to become a high-income, knowledge-based economy by the end of

the decade is achievable.

10. Among the criteria which recorded top 10 positions include:

(i) Malaysia’s inflation rate at 1.7% placed the country in the first spot together with 43

other economies which recorded low inflation rates of between 0.5% - 2.9%. The

legal rights index which measures the extent of protection towards lenders and

borrowers also remained at 1st position;

(ii) Two perception-based criteria attained 2nd

position which are pay and productivity,

(GCR 2012-2013: 3rd

) and the agricultural policy costs (GCR 2012-2013: 4th);

(iii) The strength of investor protection and government procurement of advanced

technological products remained at 4th position;

(iv) Perception on ease of access to loans attained 5th position (GCR 2012-2013: 8

th);

(v) Perception on venture capital availability, ranked 7th (GCR 2012-2013: 11

th);

(vi) Perception on burden of government regulation maintained its 8th position;

(vii) Perception on financing through local equity market maintained its 9th position; and

(viii) Perception on the effect of taxation on incentives to work, ranked 10th.

MALAYSIA’S COMPETITIVENESS BASED ON

GLOBAL COMPETITIVENESS REPORT

2013-2014

HIGHLIGHTS

7

11. Among the criteria to be given continuous emphasis include:

(i) Ratio of women to men in labour force, ranked 121st (GCR 2012-2013: 119

th);

(ii) Redundancy costs which refers to the advance notice requirements, severance

payments and penalties due when terminating a redundant worker expressed as 23.9

salaried weeks, ranked at 110th position (GCR 2012-2013: 108

th);

(iii) Secondary education enrollment, ranked 105th

position (GCR 2012-2013: 103rd

);

(iv) General government debt as a percentage of GDP, ranked 105th

(GCR 2012-2013: 100th).

(v) Perception on the impact of business cost of terrorism, ranked 85th (GCR 2012-2013:

58th);

(vi) The number of mobile broadband subscription for every 100 population, ranked 79th

(GCR 2012-2013: 64th); and

(vii) Tuberculosis incidence per 100,000 population, ranked 90th (GCR 2012-2013: 86

th);

and

(viii) Business impact of tuberculosis, ranked 87th (GCR 2012-2013: 86

th).

12. Several criteria recorded improvements in ranking. Nevertheless continuous efforts

are necessary to improve the criteria further. They are :

(i) General government budget balance as a percentage of GDP, ranked 103rd

(GCR 2012-2013: 110th);

(ii) International internet bandwidth (kb/s) per internet user, ranked 77th (GCR 2012-

2013: 83rd

);

(iii) Malaria cases for every 100,000 population, ranked 96th (GCR 2012-2013: 97

th)

while business impact of malaria, ranked 96th (GCR 2012-2013: 99

th);

(iv) Perception on business impact of HIV/AIDS, ranked 88th (GCR 2012-2013: 91

st) and

HIV prevalence as a percentage of adults, ranked 78th

(GCR 2012-2013: 87th).

8

Malaysia and Top Ten Countries

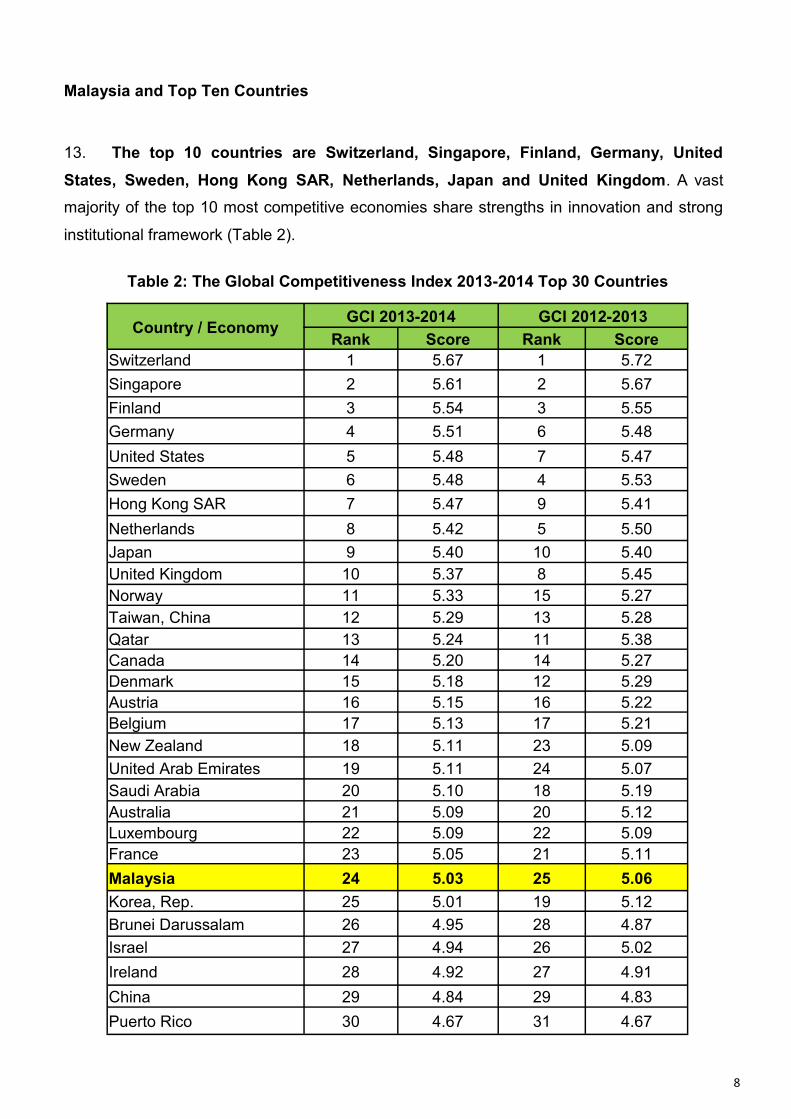

13. The top 10 countries are Switzerland, Singapore, Finland, Germany, United

States, Sweden, Hong Kong SAR, Netherlands, Japan and United Kingdom. A vast

majority of the top 10 most competitive economies share strengths in innovation and strong

institutional framework (Table 2).

Table 2: The Global Competitiveness Index 2013-2014 Top 30 Countries

Country / Economy GCI 2013-2014 GCI 2012-2013

Rank Score Rank Score

Switzerland 1 5.67 1 5.72

Singapore 2 5.61 2 5.67

Finland 3 5.54 3 5.55

Germany 4 5.51 6 5.48

United States 5 5.48 7 5.47

Sweden 6 5.48 4 5.53

Hong Kong SAR 7 5.47 9 5.41

Netherlands 8 5.42 5 5.50

Japan 9 5.40 10 5.40

United Kingdom 10 5.37 8 5.45

Norway 11 5.33 15 5.27

Taiwan, China 12 5.29 13 5.28

Qatar 13 5.24 11 5.38

Canada 14 5.20 14 5.27

Denmark 15 5.18 12 5.29

Austria 16 5.15 16 5.22

Belgium 17 5.13 17 5.21

New Zealand 18 5.11 23 5.09

United Arab Emirates 19 5.11 24 5.07

Saudi Arabia 20 5.10 18 5.19

Australia 21 5.09 20 5.12

Luxembourg 22 5.09 22 5.09

France 23 5.05 21 5.11

Malaysia 24 5.03 25 5.06

Korea, Rep. 25 5.01 19 5.12

Brunei Darussalam 26 4.95 28 4.87

Israel 27 4.94 26 5.02

Ireland 28 4.92 27 4.91

China 29 4.84 29 4.83

Puerto Rico 30 4.67 31 4.67

9

Competitiveness Performance in the Asia Pacific and ASEAN

14. Among 25 Asia Pacific countries, Malaysia improved to 7th

position from 8th in

2012 after Singapore, Hong Kong SAR, Japan, Taiwan, New Zealand and Australia.

Malaysia is ahead of Korea (8th), Brunei Darussalam (9

th), People’s Republic of China (10

th),

Thailand (11th), Indonesia (12

th), Philippines (13

th), India (14

th) and Sri Lanka (15

th).

15. Asia Pacific is home to some of the most competitive nations including three from

the top 10 countries namely Singapore, Hong Kong SAR, and Japan and is among the

dynamic and rapidly improving economies in terms of competitiveness such as Indonesia

and the Philippines. The Philippines (59th) moves up 6 places while Indonesia (38

th) made

significant strides moving up 12 places. Vietnam (70th) also moved up the ladder by 5

places however Cambodia (88th) dropped in ranking by 3 places.

16. The WEF news release reported that “Among the Asian economies, Indonesia jumps

to 38th, making it the most improved of the G20 economies since 2006, while Korea (25

th)

falls by six places. Behind Singapore, Hong Kong SAR, Japan, and Taiwan (China) all

remain in the top 20. Developing Asian nations display very mixed performances and

trends: Malaysia places 24th

while countries such as Nepal (117th), Pakistan (133

rd) and

Timor-Leste (138th) are near the bottom of the ranking. Bhutan (109

th), Lao PDR (81

st) and

Myanmar (139th) join the index for the first time”.

17. Among ASEAN countries, Malaysia remained at 2nd

position after Singapore and is

ahead of Brunei Darussalam (3rd

), Thailand (4th), Indonesia (5

th), Philippines (6

th),

Vietnam (7th), Lao PDR (8

th), Cambodia (9

th), and Myanmar (10

th) as shown in Figure 2.

10

Figure 2: Competitiveness Performance of Asia Pacific and ASEAN

11

Malaysia’s Performance in The Global Competitiveness Index

2013-2014

18. Malaysia’s performance in the 12 pillars is as shown in Table 3.

Table 3: Malaysia’s Performance in the 12 Pillars

OVERALL

Ranked 24th

/148 (GCR 2012-2013: 25th

/144)

Basic Requirements

Ranked 27th

(GCR 2012-2013: 27

th)

Efficiency Enhancers

Ranked 25th

(GCR 2012-2013: 23

rd)

Innovation Factors

Ranked 23rd

(GCR 2012-2013: 23

rd)

Pillar 1 Institutions

Ranked 29th

(GCR 2012-2013: 29th)

Pillar 5 Higher Education &

Training

Ranked 46th

(GCR 2012-2013: 39

th)

Pillar 11 Business

Sophistication

Ranked 20th

(GCR 2012-2013: 20

th)

Pillar 2 Infrastructure

Ranked 29th

(GCR 2012-2013: 32nd

)

Pillar 6 Goods Market

Efficiency

Ranked 10th

(GCR 2012-2013: 11

th)

Pillar 12 Innovation Ranked 25

th

(GCR 2012-2013: 25th)

Pillar 3

Macroeconomic Environment

Ranked 38th

(GCR 2012-2013: 35

th)

Pillar 7

Labour Market Efficiency

Ranked 25th

(GCR 2012-2013: 24

th)

Pillar 4

Health & Primary Education

Ranked 33rd

(GCR 2012-2013: 33rd

)

Pillar 8

Financial Market Development

Ranked 6th

(GCR 2012-2013: 6th)

Pillar 9 Technological Readiness

Ranked 51st

(GCR 2012-2013: 51

st)

Pillar 10 Market Size

Ranked 26th

(GCR 2012-2013: 28

th)

12

Institutional Strengths

19. Malaysia maintains its 29th

position in the

Institutions pillar in the GCR 2013-2014 report.

Among the notable indicators that have improved

in rankings are irregular payments and bribes,

ethical behavior of firms and strength of auditing

and reporting standards. The formation of 700

integrity units throughout various ministries and

agencies is expected to enhance the culture of

higher work quality and response in order to

improve public trust of government institutions and its

mandated duties.

20. To further strengthen public confidence in the

Government, new initiatives are being undertaken to

combat crime and restore public peace and

confidence. A new anti-crime legislation that is

being proposed would strengthen the capability of

Institutions

The institutional environment is determined by the legal and

administrative framework within which individuals, firms and

governments interact to generate wealth.

13

the police to act against serious and organised

crimes and will be tabled in Parliament to replace the

repealed Emergency Ordinance Act. More action is

also being undertaken which include the introduction

of Electronic Monitoring Device (EMD) to track the

organised and violent crime suspects to ensure they

would not commit other crimes while out on bail. The

Home Ministry is also making public the list of

illegal organisations linked to gangsterism in the

country. This move indicates the Government is

committed and serious in fighting crime and

safeguarding public safety.

21. Under the Government Transformation

Program (GTP) 1.0, Malaysia has succeeded in

reducing the number of corruption cases through

sustained efforts by the National Key Result Areas

(NKRA) which includes the establishment of 14

Special Corruption Courts, Corporate Integrity

Pledges and a Name and Shame Database. These

initiatives have helped to further improve public

perception on bribery and irregular payments within

government agencies and ministries. Subsequently,

GTP 2.0 has outlined Enforcement Agency,

Combating Grand Corruption, Government

Procurement and Education & Public Support as

its initiatives.

The criteria that have contributed to Institutions

pillar include:

Strength of investor protection at 4th position; and

Burden of government regulation at 8th position.

Among the areas for improvement under the

Institutions pillar include perception on:

Business costs of terrorism, ranked at 85th;

Business costs of crime and violence, ranked at

75th; and

Organised crime, ranked at 63rd

.

The formation of

700 integrity

units

throughout

various

ministries and

agencies is

expected to

enhance the

culture of higher

work quality.

14

Ensuring Integrated and Efficient

Infrastructure

22. Malaysia advances 3 places to be ranked at

29th

in the Infrastructure pillar (GCR 2012-2013:

32nd

). Overall, Malaysia ranks 15th

for the quality of

its transport infrastructure, a remarkable feat in this

part of the world, where insufficient infrastructure and

poor connectivity are major obstacles to development

for many countries. Notable improvements include

quality of overall infrastructure, quality of roads,

quality of air transport infrastructure and mobile

telephone subscriptions.

23. One of the prominent government initiatives

under the ETP is the Greater Kuala Lumpur/Klang

Valley project. This project along with other projects

such as the Klang Valley Mass Rapid Transit

(KVMRT) and the Kuala Lumpur International

Airport 2 (KLIA 2) are expected to spur growth in

which the KVMRT is expected to create 130,000 jobs.

The completed tracks are expected to generate

between RM3 billion and RM4 billion in Gross

National Income (GNI) per annum. The first phase,

the Sungai Buloh-Kajang line, will connect Sungai

Buloh to the city centre. A positive ripple effect would

include more property developments as well as

improved accessibility and amenities.

24. The KLIA 2 is the expansion of the current

KLIA and is said to be ready by mid 2014. It will

increase the base capacity of KLIA to handle over

100 international destinations and more than 50

international flight connections. The airport is

Infrastructure

Extensive and efficient infrastructure is critical for ensuring the effective functioning of the economy, as it is an important factor in determining the location of economic activity and the kinds of activities or sectors that can develop in a particular instance.

15

expected to serve over 37 million passengers and will

capitalise on the increased traffic through KLIA's retail

potential. A shopping hub will be created alongside

the new KLIA2 low-cost terminal.

25. To further develop infrastructure for rural

project developments, the Government in its 2013

budget, had allocated RM4.5 billion in which RM1.2

billion is specifically allocated for the development

of 441km of rural roads that link villages especially

within the interiors of Sabah and Sarawak.

26. Port facilities are also being improved to

enhance the value chain especially that of

downstream oil and gas activities in Johor. Ports in

Johor are expected to be the regional champion in

cargo handling volume, surpassing other terminals in

Singapore with the support of the massive

development of “Pengerang Integrated Petroleum

Complex” (PIPC) by 2025.

Among the criteria that have contributed to

Infrastructure pillar include:

Quality of railroad infrastructure, ranked 18th; and

Quality of air transport infrastructure, ranked 20th.

Among the areas for improvement required for

Infrastructure pillar are:

Fixed telephone lines/100 population, ranked 79th;

and

Quality of electricity supply, ranked 37th.

A combination of

ground (KVMRT,

Rural Roads), air

(KLIA2) and port

facilities are

expected to

support and boost

Malaysia’s

infrastructure

towards better

connectivity,

efficiency and

productivity.

16

The Macroeconomic Environment

27. Malaysia is ranked slightly lower by 3

places at 38th

(GCR 2012-2013:35th) for the

Macroeconomic Environment adversely affected

by the government budget balance and general

government debt. However, significant

improvement was recorded in the annual

percentage change for Inflation at 1.7% in 2012

resulting in a surge to 1st

position from 33rd

. In the

first five months of 2013, inflation remained low at

1.6%. While it is expected to rise in the

second half of the year due to domestic supply and

cost factors, it is projected to remain modest.

Malaysia’s monetary policy in 2013 focuses on

sustainable growth and addresses potential risk to

inflation.

28. Malaysia continues to recover from its deficit

as it sees the benefits of the Economic

Transformation Program (ETP). Within a year of

the ETP’s implementation, Malaysia experienced a

reduced deficit of 1.8% from 6.6% to 4.8%. The

trend of reduction continued in 2012 which saw a

reduction to 4.3% and is on track to hit the 4%

target in 2014 and the 3% target by 2015. Measures

such as subsidy rationalisation goods and services

tax and a review of the real property gains tax

(RPGT) are being considered.

29. General government debt as a percentage

of GDP improved by 7 positions. Even though the

performance improved, Bank Negara is taking

measures to curb excessive households debts and

reinforce responsible lending practices by key credit

providers.

“Our target is to

achieve a fiscal

deficit of 3% of GDP by

2015 and a balanced

budget by 2020”

- Datuk Seri Najib Tun Razak, PM

Macroeconomic environment

The stability of the macroeconomic environment is important for business and therefore is significant for the overall competitiveness of a country.

17

The areas under Macroeconomic Environment

pillar that need to be addressed are:

General government debt, % GDP, ranked 105th;

and

Government budget balance, % GDP, ranked

103rd

.

Keeping Healthcare and Primary

Education in Perspective

30. Malaysia retains the overall ranking of 33rd

in

the Health and Primary Education pillar. The

criteria that improved in this pillar includes the HIV

prevalence, up by 9 places to 78th

place (GCR 2012

-2013: 87th).

31. The healthcare industry has become a powerful

engine of economic growth. Malaysia's spending on

healthcare, at 5% of GDP, is above regional peers

and contributes RM15 billion in GNI. The

Government has also allocated RM19.3 billion for

healthcare management and development services in

the 2013 budget, an increase of 15% over the

previous year. The Government has also promoted

healthcare through its 1Malaysia Healthy

Community Programme which has seen 245 Klinik

1Malaysia established with another 70 expected by

the end of 2013.

32. The Government is also serious about tackling

AIDS. In view of this, Malaysia has launched the new

Human Immunodeficiency Virus (HIV) treatment

guidelines as recommended by the World Health

Health and primary education

A healthy workforce is vital to a country’s competitiveness and productivity while lack of basic education can become a constraint on business development, with firms finding it difficult to move up the value chain.

18

Organisation (WHO). With the offering of

anti-retroviral therapy (ART) at an earlier stage, 3

million deaths can be prevented and 3.5 million new

HIV infections between now and 2025 could be

averted. A survey by Bloomberg reported that

Malaysia is among the world’s top 20 countries

with the most efficient healthcare system, which

results in a longer life expectancy for its citizens.

According to the survey, Malaysia was ranked 18th,

placing it ahead of France, Thailand and the United

States.

33. The government is also relentless in pursuing

for a better national education system that enables

students to overcome and face challenges. In this

regard, the Malaysia Education Blueprint 2013-

2025, has been developed to transform the

education system. It is aimed at improving the

education system and encapsulating quality and

holistic empowerment of teachers, students and the

education system.

Among the areas that require improvement in Health

and Primary Education pillar include:

Business impact of malaria, ranked 96th;

Malaria cases/100,000 population, ranked, 96th;

Tuberculosis cases/100,000 population, ranked

90th.

Business impact of HIV/AIDS, ranked 88th;

Business impact of tuberculosis, ranked 87th; and

HIV prevalence, % adults aged, 15 to 49 years,

ranked 78th.

Malaysia Education

Blueprint 2013-2025, has

been developed to

transform the education

system. It is aimed at

improving the education

system and encapsulating

quality and holistic

empowerment of teachers,

students and the

education system.

19

Quality Workforce through Higher

Education and Training

34. Higher Education and Training pillar

declines 7 places to 46th

position in 2013 (GCR

2012-2013: 39th). The performance was largely

influenced by perception based indicators that

include the quality of management schools, quality

of math and science education and the quality of

education system.

35. In this regard, the Government is committed in

its quest to transform the education system towards

“a first class society in a first class nation” by

2020. Under the 2013 budget, RM11.1 billion has

been allocated to the social sector which includes

education and training. The Graduate Employability

Taskforce, set up under a RM200 million fund is

expected to enable students to develop soft skills and

Higher education and training

Quality higher education and training is particularly crucial for economies that want to move up the value chain beyond simple production processes and products.

20

improve their marketability. The vocational education

transformation implemented under the Malaysia

Education Blueprint 2013-2025 which also looks into

the higher education aspect, is giving emphasis

on vocational training and is expected to transform

traditional blue collar businesses into high-skill,

high-income industries. A total of 117,000

applications to enroll in vocational colleges for this

year’s intake had been received despite the fact that

only 21,000 placements were available.

36. The Government envisions the creation of a

regional hub for education excellence in

Malaysia where the best minds of the world

converge. As an education hub, Malaysia stands to

gain not only from the inflow of international students

but also from the establishment of top-notch

universities and international colleges. An example is

the Educity@Iskandar where globally recognised

institutions such as Newcastle University of Medicine

Malaysia, Netherlands Maritime Institute of

Technology, Raffles University Iskandar, University of

Southampton Malaysia and University of Reading

Malaysia have set up campuses, not only transform

education into a vibrant economic sector but will also

provide the required training to meet industry needs.

The criteria that require improvement in Higher

Education and Training pillar are:

Secondary education enrollment, gross %, ranked

105th; and

Tertiary education enrollment, gross %, ranked

62nd

.

The Government

is committed to

transform the

education

system towards

“a first class

society in a first

class nation” by

2020.

21

Promoting A Better Goods Market Through

Efficiency

37. Malaysia improves its ranking to be among the

top 10 (GCR 2012-2013: 11th) in the Goods Market

Efficiency pillar. Significant improvements were in

total tax rate (20th

), indicating a jump of 30 places;

number of procedures to start a business which

attained 10th

position; trade tariffs moving up 8

spots and prevalence of foreign ownership

improved 5 rungs.

38. Malaysia needs to further diversify its source of

income to reposition itself on track towards a stable

economic growth. Implementation of GST would help

the country to broaden its tax base and strengthen

public finances.

39. Among the efficiency improvements in starting

a business undertaken was the development of the

MyCoID Gateway System which enables services to

be transacted online. The Malaysian Corporate

Identity Number (MyCoID), a unique company

incorporation number for registering and dealing with

relevant government agencies to start a business

helps to save time, bureaucratic red tape and

improve efficiency of the process. MyCoID has

been expanded to Phase 3 to include other

government agencies and local authorities directly

involved in the ease of doing business.

Goods market efficiency

Countries with efficient goods markets are well positioned to produce the right mix of products and services given their particular supply-and-demand.

The criteria that supported

Goods Market Efficiency:

Agricultural policy

costs (2nd),

Buyer sophistication (11th),

Effect of taxation on

incentives to invest (12th),

and Business impact of

rules on FDI (14th) .

22

40. PEMUDAH — The Special Taskforce to

Facilitate Business continues to undertake initiatives

to improve the business environment. These include

business process re-engineering in various licensing

processes and procedures; implementation of

web-based e-payment facilities for online payments

nationwide; and fine tuning the one-stop center

approval processes.

The area that needs improvement in Goods Market

Efficiency pillar is:

Trade tariffs, % duty, ranked 68th.

Competitive Labour Market

41. Malaysia is ranked 25th

in the Labour Market

Efficiency pillar (GCR 2012-2013: 24th), indicating a

decline by 1 position. Perception on flexibility of wage

determination and cooperation in labor-employer

relations are among the criteria that contributed to the

decline in ranking. However, hiring and firing

practices went up 8 positions to 26th (GCR 2012-2013:

34th), while pay and productivity ranked among the top

10 criteria attaining 2nd

position.

42. With the implementation of Minimum Wage

Policy on 1st January 2013, it is envisaged that

inefficiencies in the labour market can be addressed

and overcome. The purpose of a minimum wage is to

improve the social wellbeing of low paid workers

and to incentivise firms to move up the value chain

thus transforming the economy into one with high

productivity and high income. The Productivity-

Labour market efficiency

The efficiency and flexibility of the labor market are critical for ensuring that workers are allocated to their most effective use in the economy and provided with incentives to give their

best effort in their jobs.

The

implementation

of minimum

wage will

address

inefficiencies in

the labour

market.

23

linked Wage System which links wage increases to

performance will complement the Minimum Wage

Policy.

43. To propel Malaysia into an innovation-driven

nation is to retain or attract high value talents in the

country. Through the Talent Corporation program,

Malaysia has seen positive results by succeeding to

attract 2,015 Malaysians back into Malaysia to serve

the country since 2001. A total of RM65 million has

been allocated to Talent Corp to develop attractive

programs to further attract and nurture interest among

talented Malaysians abroad to return as well as to

promote a greater diversity of job choices for fresh

graduates to explore.

44. The Government has committed several

initiatives to boost the representation of women

participation in an enabling environment. The

Women’s Directors program has a total of 500 women

who are being trained as board members. The

Government has also urged private and public

corporations to facilitate a childcare centre at the

workplace using federal incentives to

accommodate the female employee’s work life

balance. At present there are a total of 47.9% women

participating in the labour force.

The criteria that had contributed to the performance of

Labour Market Efficiency are:

Pay and productivity, ranks 2nd

; and

Effect of taxation on incentives to work, ranks 10th.

Among the criteria required for improving Labour

Market Efficiency are:

Women in labour force, ranked 121st; and

Redundancy costs, weeks of salary, ranked 110th.

The Government

has committed

several

initiatives to boost

the representation

of women

participation in an

enabling

environment. At

present there are a

total of 47.9%

women

participating in the

labour force.

24

Financially Effective

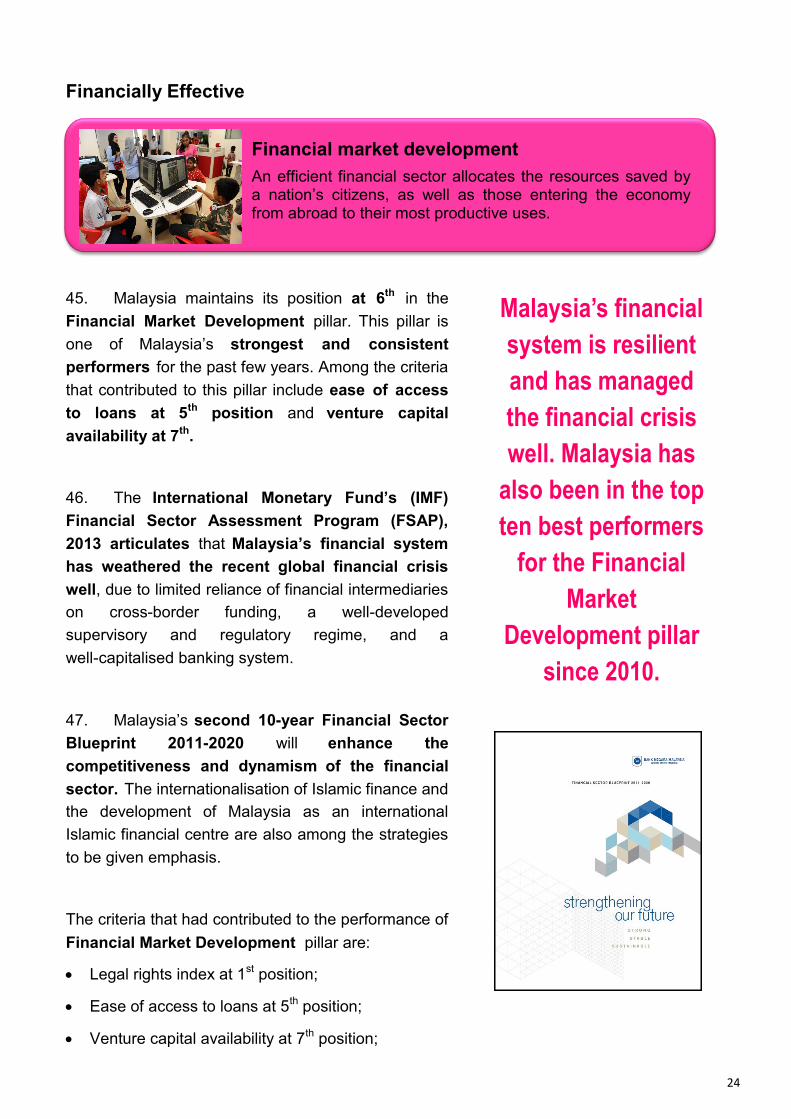

45. Malaysia maintains its position at 6th

in the

Financial Market Development pillar. This pillar is

one of Malaysia’s strongest and consistent

performers for the past few years. Among the criteria

that contributed to this pillar include ease of access

to loans at 5th

position and venture capital

availability at 7th

.

46. The International Monetary Fund’s (IMF)

Financial Sector Assessment Program (FSAP),

2013 articulates that Malaysia’s financial system

has weathered the recent global financial crisis

well, due to limited reliance of financial intermediaries

on cross-border funding, a well-developed

supervisory and regulatory regime, and a

well-capitalised banking system.

47. Malaysia’s second 10-year Financial Sector

Blueprint 2011-2020 will enhance the

competitiveness and dynamism of the financial

sector. The internationalisation of Islamic finance and

the development of Malaysia as an international

Islamic financial centre are also among the strategies

to be given emphasis.

The criteria that had contributed to the performance of

Financial Market Development pillar are:

Legal rights index at 1st position;

Ease of access to loans at 5th position;

Venture capital availability at 7th position;

Financial market development

An efficient financial sector allocates the resources saved by a nation’s citizens, as well as those entering the economy from abroad to their most productive uses.

Malaysia’s financial

system is resilient

and has managed

the financial crisis

well. Malaysia has

also been in the top

ten best performers

for the Financial

Market

Development pillar

since 2010.

25

Financing through local equity market at 9th

position; and

Affordability of financial services at 15th position.

Advancing Technological Readiness

48. Technological Readiness which focuses on

the availability and adoption of technology as well as

internet usage within the country maintains its

ranking at 51st

place, a comparatively low ranking

compared to Malaysia’s performance in the other 11

pillars. Under this pillar, international internet

bandwidth went up by 6 rungs to 77th

position.

49. 65.8% Malaysians were found to be

using the internet, with every 8 out of 100

population subscribing it through fixed broadband

services. The Government’s rebate program of

RM200 under the Youth Communication Package

to purchase smartphones is one of the initiatives to

access knowledge and information through the

internet.

50. To help promote greater adoption of ICT and

the usage of the internet for businesses, the

Government has launched the "Get Malaysia

Business Online" (GMBO) to encourage SMEs to

build their online presence. In the 2013 budget,

GMBO plans to assist 50,000 small entrepreneurs

particularly women to promote their business online

with a RM1,000 grant.

Technological readiness

The technological readiness pillar measures the agility with which an economy adopts existing technologies to enhance the productivity of its industries, with specific emphasis on its capacity to fully leverage information and communication technologies (ICT) in daily activities and production processes for increased efficiency and enabling innovation for competitiveness.

Get Malaysia

Business Online

(GMBO)

encourages SMEs

to build their

online presence.

26

51. The Digital Malaysia, a national programme

that is currently ongoing would advance Malaysia’s

digital economy as it creates an ecosystem that will

allow Malaysians to connect globally and interact

in real time, increase productivity, gross national

income and empower government, businesses

and citizens. To enable rural students to benefit from

ICT and the usage of the internet, the 1Malaysia

Internet Centre (PI1M), an initiative by the Malaysian

Communications and Multimedia Commission

(MCMC), has helped rural students to be literate in IT.

The criteria that had contributed to the performance of

Technological Readiness is FDI and technology

transfer, ranked 13th

.

Among the areas for improvement required for

Technological Readiness pillar are:

Mobile broadband subscriptions/100 population,

ranked 79th;

International internet bandwidth, kb/s per user,

ranked 77th; and

Fixed broadband internet subscriptions/100

population, ranked 66th.

The Digital

Malaysia

programme

aims to develop

and connect the

economy to a

digital business

age for all

Malaysians

digitally through

the internet by

2020.

27

Going for Global Markets

52. Malaysia improves in the Market Size pillar at

26th

position (GCR 2012-2013: 28th) supported by

domestic market size index which moved 2 places

to 29th. However, global uncertainty has affected

Malaysia’s ranking in the export of goods and

services, ranked 15th, a decline by 5 places from the

previous year.

53. Malaysia is expanding its market size by

leveraging on Free Trade Agreements (FTAs) to

benefit from lower tariffs and improved market access.

Currently, Malaysia has signed FTAs with Japan,

Pakistan, New Zealand, India, Chile and Australia.

Among ASEAN members, Malaysia has also

concluded regional FTAs with China, South Korea,

Japan, India and Australia-New Zealand. In view of

this, businesses based in Malaysia will benefit from

preferential access to markets of over 3.5 billion

customers. These benefits help to lower the cost of

doing business, which make products and services

more competitive in the international market.

Market size

The size of the market affects productivity since large markets allow firms to exploit economies of scale. Traditionally, the markets available to firms have been constrained by national borders. In the era of globalization, international markets can to a certain extent substitute for

domestic markets, especially for small countries.

Market size

affects

productivity as

large markets

allows firms to

exploit

economies of

scale.

28

Bringing Sophistication to Business

54. Malaysia retains its 20th

position in the

Business Sophistication pillar with improvement in

the indicator of value chain breadth in Malaysian

companies are broad, moving up to 17th

from 21st

position. This was further supported by control of

international distribution and marketing index

and willingness to delegate authority to

subordinates which increased by 1 position to 11th

and 13th respectively. It was also perceived that local

supplier quantity in Malaysia are extremely

numerous where Malaysia is ranked 17th

.

The criteria that had recorded favorable performance

in Business Sophistication pillar include:

Control of international distribution at 11th

position;

Willingness to delegate authority at 13th position;

and

State of cluster development at 14th position.

Business sophistication

There is no doubt that sophisticated business practices are conducive to higher efficiency in the production of goods and services. Business sophistication concerns two elements that are intricately linked: the quality of a country’s overall business networks and the quality of individual firms’ operations and strategies.

29

Empowering Innovation

55. The Innovation pillar maintains its rank at

25th

, with the criteria for both capacity for

innovation and university-industry collaboration in

R&D moving up 2 places to 15th

and 16th

respectively.

56. Malaysia continues to place innovation at the

centre of its transformation programmes through

various initiatives. Among them is the Innovation

Business Opportunities (IBO) programme, a

collaboration between the Performance

Management and Delivery Unit (PEMANDU) and the

Agensi Inovasi Malaysia (AIM) to provide a steady

pipeline of opportunities for the business community.

The programmes is already attracting “bids” from

interested companies to take new products and

services to market in fields such as agriculture,

education, the electronics and electrical sector and

financial services. As of May 2013, the 92 IBO

projects were already projected to contribute RM2

billion of gross national income. The 1 Malaysia

Biomass Strategy (1MBAS) is also expected to

contribute up to RM30 billion.

57. Patents are important as they help to secure a

form of economic wealth and branding for the various

businesses in Malaysia through licensing and royalty

incomes. Malaysia recorded an improvement for its

PCT patents per million population indicator to 31st

from 34th

previously. On-going initiatives in promot-

ing the use of patenting ideas and inventions are

being undertaken by the Intellectual Property

Corporation of Malaysia (MyIPO).

Innovation

Innovation can emerge from new technological and non-technological knowledge. Non-technological innovations are closely related to the know-how, skills, and working conditions that are embedded in organizations. In the long run, standards of living can be largely enhanced by technological innovation and technological breakthroughs.

Innovation is the

key towards

propelling

Malaysia towards

a high income

economy by 2020.

30

58. The Ministry of Science, Technology and

Innovation (MOSTI) has to conducted over 63

science awareness programmes with the help of the

private sector aimed at sharing scientific knowledge,

technology and innovation with the goal of aspiring the

future generations to look towards creating their own

innovations.

Among the criteria that had a positive impact on

Innovation include:

Government procurement of advanced

technological products at 4th position;

Capacity for innovation at 15th position;

University-industry collaboration in R&D at 16th

position;

Companies spending on R&D at 17th position; and

Availability of scientists and engineers at 19th

position.

Innovation

Business

Opportunities

(IBO)

programme

provides

opportunities

for the

business

community.

31

Evolution in Malaysia’s Competitiveness Performance

Figure 3 indicates the evolution of Malaysia’s competitiveness performance in the 12 pillars

from GCR 2010-2011 to GCR 2013-2014. To enhance national competitiveness and moving

Malaysia into the next stage of development, more emphasis is needed in the

Macroeconomic Environment (pillar 3), Higher Education & Training (pillar 5) and

Technological Readiness (pillar 9).

.

Best Average Worst

Figure 3: Evolution in Malaysia’s Competitiveness Performance by Rank

Evolution

in

Malaysia's

Rank

Glo

ba

l C

om

pe

titi

ve

ne

ss

Ind

ex

20

13

-20

14

1s

t p

illa

r: In

sti

tuti

on

s

2n

d p

illa

r: In

fra

str

uc

ture

3rd

pilla

r:

Ma

cro

ec

on

om

ic

En

vir

on

me

nt

4th

pilla

r: H

ea

lth

an

d

pri

ma

ry e

du

ca

tio

n

5th

pilla

r: H

igh

er

ed

uc

ati

on

an

d t

rain

ing

6th

pilla

r: G

oo

ds

ma

rke

t

eff

icie

nc

y

7th

pilla

r: L

ab

ou

r

ma

rke

t e

ffic

ien

cy

8th

pilla

r: F

ina

nc

ial

ma

rke

t d

ev

elo

pm

en

t

9th

pilla

r: T

ec

hn

olo

gic

al

rea

din

es

s

10

th p

illa

r: M

ark

et

siz

e

11

th p

illa

r: B

us

ine

ss

so

ph

isti

ca

tio

n

12

th p

illa

r: In

no

va

tio

n

GCI Edition

2013-2014

(n=148)24 29 29 38 33 46 10 25 6 51 26 20 25

2012-2013

(n=144)25 29 32 35 33 39 11 24 6 51 28 20 25

2011-2012

(n=142)21 30 26 29 33 38 15 20 3 44 29 20 24

2010-2011

(n=139)26 42 30 41 34 49 27 35 7 40 29 25 24

Rank

32

Competitiveness Enhancement Initiatives

To create enabling environment to foster innovation through collaboration and in

particular develop appropriate educational systems;

Continue efforts on structural reforms and critical investments required to ensure a

prosperous environment and employment for citizens and complement these with

transformation programmes that will drive further economic growth; and

Address perception issues among the business community and the public at large for a

better and more objective assessment of various information and facts on

competitiveness.

Committed to Transform the Nation

Despite the challenging external environment, Malaysia’s economic and financial

fundamentals remain sound, a reflection of our economic management, enhanced

productivity, emphasis on being more innovative, supported by strong transformation

initiatives. The Government is committed to building a resilient, dynamic and innovative

economy; enhancing security and public safety; strengthening women’s participation;

fighting corruption as well as enhancing good governance.

33

Appendix I

Global Competitiveness Index 2013-2014 Rankings and

2012-2013 Comparisons

Country / Economy GCI 2013-2014 GCI 2012-2013

Rank Score Rank Score

Switzerland 1 5.67 1 5.72

Singapore 2 5.61 2 5.67

Finland 3 5.54 3 5.55

Germany 4 5.51 6 5.48

United States 5 5.48 7 5.47

Sweden 6 5.48 4 5.53

Hong Kong SAR 7 5.47 9 5.41

Netherlands 8 5.42 5 5.50

Japan 9 5.40 10 5.40

United Kingdom 10 5.37 8 5.45

Norway 11 5.33 15 5.27

Taiwan, China 12 5.29 13 5.28

Qatar 13 5.24 11 5.38

Canada 14 5.20 14 5.27

Denmark 15 5.18 12 5.29

Austria 16 5.15 16 5.22

Belgium 17 5.13 17 5.21

New Zealand 18 5.11 23 5.09

United Arab Emirates 19 5.11 24 5.07

Saudi Arabia 20 5.10 18 5.19

Australia 21 5.09 20 5.12

Luxembourg 22 5.09 22 5.09

France 23 5.05 21 5.11

Malaysia 24 5.03 25 5.06

Korea, Rep. 25 5.01 19 5.12

Brunei Darussalam 26 4.95 28 4.87

Israel 27 4.94 26 5.02

Ireland 28 4.92 27 4.91

China 29 4.84 29 4.83

Puerto Rico 30 4.67 31 4.67

Iceland 31 4.66 30 4.74

Estonia 32 4.65 34 4.64

Oman 33 4.64 32 4.65

Chile 34 4.61 33 4.65

Spain 35 4.57 36 4.60

Kuwait 36 4.56 37 4.56

Thailand 37 4.54 38 4.52

Indonesia 38 4.53 50 4.40

34

Country / Economy GCI 2013-2014 GCI 2012-2013

Rank Score Rank Score

Azerbaijan 39 4.51 46 4.41

Panama 40 4.50 40 4.49

Malta 41 4.50 47 4.41

Poland 42 4.46 41 4.46

Bahrain 43 4.45 35 4.63

Turkey 44 4.45 43 4.45

Mauritius 45 4.45 54 4.35

Czech Republic 46 4.43 39 4.51

Barbados 47 4.42 44 4.42

Lithuania 48 4.41 45 4.41

Italy 49 4.41 42 4.46

Kazakhstan 50 4.41 51 4.38

Portugal 51 4.40 49 4.40

Latvia 52 4.40 55 4.35

South Africa 53 4.37 52 4.37

Costa Rica 54 4.35 57 4.34

Mexico 55 4.34 53 4.36

Brazil 56 4.33 48 4.40

Bulgaria 57 4.31 62 4.27

Cyprus 58 4.30 58 4.32

Philippines 59 4.29 65 4.23

India 60 4.28 59 4.32

Peru 61 4.25 61 4.28

Slovenia 62 4.25 56 4.34

Hungary 63 4.25 60 4.30

Russian Federation 64 4.25 67 4.20

Sri Lanka 65 4.22 68 4.19

Rwanda 66 4.21 63 4.24

Montenegro 67 4.20 72 4.14

Jordan 68 4.20 64 4.23

Colombia 69 4.19 69 4.18

Vietnam 70 4.18 75 4.11

Ecuador 71 4.18 86 3.94

Georgia 72 4.15 77 4.07

Macedonia, FYR 73 4.14 80 4.04

Botswana 74 4.13 79 4.06

Croatia 75 4.13 81 4.04

Romania 76 4.13 78 4.07

Morocco 77 4.11 70 4.15

Slovak Republic 78 4.10 71 4.14

Armenia 79 4.10 82 4.02

Seychelles 80 4.10 76 4.10

Lao PDR* 81 4.08 - -

35

Country / Economy GCI 2013-2014 GCI 2012-2013

Rank Score Rank Score

Iran, Islamic Republic 82 4.07 66 4.22

Tunisia* 83 4.06 - -

Ukraine 84 4.05 73 4.14

Uruguay 85 4.05 74 4.13

Guatemala 86 4.04 83 4.01

Bosnia and Herzegovina 87 4.02 88 3.93

Cambodia 88 4.01 85 4.01

Moldova 89 3.94 87 3.94

Namibia 90 3.93 92 3.88

Greece 91 3.93 96 3.86

Trinidad and Tobago 92 3.91 84 4.01

Zambia 93 3.86 102 3.80

Jamaica 94 3.86 97 3.84

Albania 95 3.85 89 3.91

Kenya 96 3.85 106 3.75

El Salvador 97 3.84 101 3.80

Bolivia 98 3.84 104 3.78

Nicaragua 99 3.84 108 3.73

Algeria 100 3.79 110 3.72

Serbia 101 3.77 95 3.87

Guyana 102 3.77 109 3.73

Lebanon 103 3.77 91 3.88

Argentina 104 3.76 94 3.87

Dominican Republic 105 3.76 105 3.77

Suriname 106 3.75 114 3.68

Mongolia 107 3.75 93 3.87

Libya 108 3.73 113 3.68

Bhutan* 109 3.73 - -

Bangladesh 110 3.71 118 3.65

Honduras 111 3.70 90 3.88

Gabon 112 3.70 99 3.82

Senegal 113 3.70 117 3.66

Ghana 114 3.69 103 3.79

Cameroon 115 3.68 112 3.69

Gambia, The 116 3.67 98 3.83

Nepal 117 3.66 125 3.49

Egypt 118 3.63 107 3.73

Paraguay 119 3.61 116 3.67

Nigeria 120 3.57 115 3.67

Kyrgyz Republic 121 3.57 127 3.44

Cape Verde 122 3.53 122 3.55

Lesotho 123 3.52 137 3.19

36

Country / Economy GCI 2013-2014 GCI 2012-2013

Rank Score Rank Score

Swaziland 124 3.52 135 3.28

Tanzania 125 3.50 120 3.60

Côte d’Ivoire 126 3.50 131 3.36

Ethiopia 127 3.50 121 3.55

Liberia 128 3.45 111 3.71

Uganda 129 3.45 123 3.53

Benin 130 3.45 119 3.61

Zimbabwe 131 3.44 132 3.34

Madagascar 132 3.42 130 3.38

Pakistan 133 3.41 124 3.52

Venezuela 134 3.35 126 3.46

Mali 135 3.33 128 3.43

Malawi 136 3.32 129 3.38

Mozambique 137 3.30 138 3.17

Timor-Leste 138 3.25 136 3.27

Myanmar* 139 3.23 - -

Burkina Faso 140 3.21 133 3.34

Mauritania 141 3.19 134 3.32

Angola* 142 3.15 - -

Haiti 143 3.11 142 2.90

Sierra Leone 144 3.01 143 2.82

Yemen 145 2.98 140 2.97

Burundi 146 2.92 144 2.78

Guinea 147 2.91 141 2.90

Chad 148 2.85 139 3.05

Note: *New entrants / Re-instated

37

Appendix 2

The Global Competitiveness Index 2013-2014 Rankings for

Asia Pacific Countries

The Global Competitiveness Index 2013-2014 Rankings for

ASEAN Countries

Country / Economy GCI 2013-2014

Rank Score

Singapore 1 5.61

Hong Kong SAR 2 5.47

Japan 3 5.40

Taiwan, China 4 5.29

New Zealand 5 5.11

Australia 6 5.09

Malaysia 7 5.03

Korea, Rep. 8 5.01

Brunei Darussalam 9 4.95

China 10 4.84

Thailand 11 4.54

Indonesia 12 4.53

Philippines 13 4.29

India 14 4.28

Sri Lanka 15 4.22

Vietnam 16 4.18

Lao PDR* 17 4.08

Cambodia 18 4.01

Mongolia 19 3.75

Bhutan* 20 3.73

Bangladesh 21 3.71

Nepal 22 3.66

Kyrgyz Republic 23 3.57

Pakistan 24 3.41

Myanmar* 25 3.23

Country / Economy GCI 2013-2014

Rank Score

Singapore 1 5.61

Malaysia 2 5.03

Brunei Darussalam 3 4.95

Thailand 4 4.54

Indonesia 5 4.53

Philippines 6 4.29

Vietnam 7 4.18

Lao PDR* 8 4.08

Cambodia 9 4.01

Myanmar* 10 3.23

38

Appendix 3

List of Countries/ Economies at Each Stage of Development

Stage 1 Transition from

1 to 2 Stage 2

Transition from

2 to 3 Stage 3

(38 economies) (20 economies) (31 economies) (22 economies) (37 economies)

Bangladesh Algeria Albania Argentina Australia

Benin Angola* Bosnia and

Herzegovina Barbados Austria

Burkina Faso Armenia Bulgaria Brazil Bahrain

Burundi Azerbaijan Cape Verde Chile Belgium

Cambodia Bhutan* China Costa Rica Canada

Cameroon Bolivia Colombia Croatia Cyprus

Chad Botswana Dominican

Republic Estonia Czech Republic

Côte d'Ivoire Brunei Darussalam Ecuador Hungary Denmark

Ethiopia Gabon Egypt Kazakhstan Finland

Gambia, The Honduras El Salvador Latvia France

Ghana Iran, Islamic Rep. Georgia Lebanon Germany

Guinea Kuwait Guatemala Lithuania Greece

Haiti Libya Guyana Malaysia Hong Kong SAR

India Moldova Indonesia Mexico Iceland

Kenya Mongolia Jamaica Oman Ireland

Kyrgyz Republic Morocco Jordan Panama Israel

Lao PDR* Philippines Macedonia, FYR Poland Italy

Lesotho Saudi Arabia Mauritius Russian Federation Japan

Liberia Sri Lanka Montenegro Seychelles Korea, Rep.

Madagascar Venezuela Namibia Slovak Republic Luxembourg

Malawi Paraguay Turkey Malta

Mali Peru Uruguay Netherlands

Mauritania Romania New Zealand

Mozambique Serbia Norway

Myanmar* South Africa Portugal

Nepal Suriname Puerto Rico

Nicaragua Swaziland Qatar

Nigeria Thailand Singapore

Pakistan Timor-Leste Slovenia

Rwanda Tunisia* Spain

Senegal Ukraine Sweden

Sierra Leone Switzerland

Tanzania Taiwan, China

Uganda Trinidad and Tobago

Vietnam United Arab

Emirates

Yemen United Kingdom

Zambia United States

Zimbabwe

Note: *New entrants / Re-instated

39

ASEAN’s Competitiveness Landscape:

A mixed picture with encouraging trends

To any observer of the region, the developmental gap within the Association of Southeast Asian

Nations (ASEAN) is striking. No other regional integration initiative has deeper disparities among

participating members. Founded in 1967 by Indonesia, Malaysia, Singapore, Thailand, and the

Philippines, the subsequent accession of Brunei Darussalam, Vietnam, Lao PDR, Myanmar, and

Cambodia have made ASEAN’s developmental landscape even more disparate. For example,

Singapore is 80 times richer than Myanmar, where infant mortality rate is 25 times higher.

Singapore’s population also lives 20 years longer than Cambodia’s.

Despite this diversity, ASEAN has embarked on an ambitious journey toward regional integration.

The ASEAN Economic Community (AEC) is one of the three pillars of this integration effort,

alongside the ASEAN Political-Security Community and the ASEAN Socio-Cultural Community.

The AEC vision is for ASEAN to become, by 2015, a single market and production base, a highly

competitive economic region, a region of equitable economic development, and a region fully

integrated into the global economy. Progress is real. By its own account, ASEAN has implemented

nearly 80 percent of the measures set out in the AEC Blueprint of 2007.

Although it remains to be seen whether the AEC vision will be fully realised by 2015, the

fast-approaching deadline should motivate ASEAN leaders, and boosting competitiveness should

be a priority. Competitiveness will foster economic development, which in turn will reduce

disparities and accelerate regional and global integration—the other goals of the AEC.

This year for the first time, with the inclusion of Lao PDR and Myanmar, the Global

Competitiveness Index (GCI) offers a complete picture of ASEAN’s competitiveness landscape,

and it is a landscape that demonstrates much greater contrast than exhibited in earlier GCI

editions. Lao PDR comes in 81st and Myanmar ranks 139th, some 50 places behind Cambodia,

which at 88th place is ranked second lowest in ASEAN. Table 1 allows for a more granular analysis

of the GCI results by reporting the rank achieved by ASEAN Member States in the overall GCI and

its 12 pillars. The different shadings allow for a ready identification of strengths and weaknesses

and of regional patterns.

Malaysia performs consistently well, although room for improvement remains. Myanmar is

ASEAN’s lowest ranked nation on all the pillars except market size. In technological readiness, it

even ranks last among the 148 economies studied. The table also reveals that the competitiveness

of most ASEAN countries is still impeded by poor transport, inadequate energy and communication

infrastructures, low enrollment rates and/or mediocre quality in education, and low levels of

technological readiness.

With the exception of Singapore and Myanmar, performance tends to be inconsistent across the

different pillars of the Index. Finally, the macroeconomic environment is rather sound in a majority

Appendix 4

40

of ASEAN countries, much more so than in many troubled advanced economies. In fact, Brunei

Darussalam—an oil-rich economy—tops this pillar. More prudent and sustainable macroeconomic

management is probably one of the positive consequences of the 1997 Asian financial crisis, which

created havoc across ASEAN nations and inspired reforms.

All in all, the assessment is very mixed. Much remains to be done for ASEAN to become a more

competitive, prosperous, and harmonious group. Although ASEAN economies have enjoyed brisk

economic growth over the past decade, the foundations remain relatively shaky for a number of

countries. Yet there is reason for optimism.

Since the 2006–2007 edition of the GCI, the competitiveness trends for ASEAN have been

overwhelmingly positive, as seen in Figure 1, which depicts the evolution in rank of selected

developing Asian countries within a constant sample of 118 economies. The seven ASEAN members

(identified by solid blue lines) covered since 2006 have either improved or maintained their standing

over the eight-year period to 2013. Cambodia has leapfrogged 23 ranks, the fourth largest gain within

the entire sample. Indonesia and the Philippines each progress 19 places. Indonesia posts the

biggest progression among the group of 20 major economies (G20). It is all the more encouraging

that these two nations are also the most populous in ASEAN, accounting for more than half of the

group’s population.

Furthermore, Singapore has improved steadily from 8th in 2006 to 2nd in 2011—behind

Switzerland—and has retained its rank since then. Malaysia and Thailand have slightly declined,

losing four and five places, respectively, but they have done so from a relatively high base and both

countries have progressed in the last year.

The fact that ASEAN membership spans the entire development ladder and includes competitiveness

champions can benefit the less competitive countries in the group. Indeed, there are many stories of

member countries successfully addressing key competitiveness issues in ways that could be

emulated by others. For instance, Singapore is a competitiveness champion. Its administration is one

of the world’s least corrupt and most efficient.

Malaysia has been tackling excessive regulation as part of its Government Transformation

Programme, and the Philippines—where a national competitiveness council was set up in 2006—has

made significant strides against corruption. Furthermore, a number of regional initiatives, launched in

the 1990s following the accession of less developed members and aimed at reducing the

developmental gap, have proven quite effective. These include the Initiative for ASEAN Integration

and the Master Plan on ASEAN connectivity. Although the responsibility for addressing the structural

issues described above lies primarily with national actors, regional cooperation is critical. Efforts at

the country and regional levels are complementary and reinforce each other. They enable Member

States to leverage growth opportunities and strengthen their respective competitive advantages to

move up the value chain, thus reducing the intra-ASEAN developmental gap.

41

Table 1: Performance of ASEAN members in the 2013 - 2014 GCI and the 12

composing pillars, rank out of 148 economies

Best Median Worst

Source: Extracted from the Global Competitiveness Report 2013-2014, World Economic Forum (WEF)

42

For further information on the

Global Competitiveness Report 2013-2014

(GCR 2013-2014), please contact:

Global Competitiveness Department (GCD)

Malaysia Productivity Corporation (MPC)

A-06-01 Tingkat 6, Blok A PJ8,

No.23 Jalan Barat,

Seksyen 8

46050 Petaling Jaya,

Selangor Darul Ehsan,

Malaysia.

Tel: 603-7960 0173

Fax: 603-7960 0206

Email: [email protected]

1800 88 1140

www.mpc.gov.my