intrntnl rdt rt nntn pl nd dpl ntntl, rtn plx b f/media/publications/economic... · pltd, bt nt...

TRANSCRIPT

International credit

Some test cases show how credit markets

market connections couple and decouple constantly,

creating a complex web ofinternational financial relationships

Steven Strongin

International credit marketscreate a sense of mystery thatfew economic institutions canmatch. As the old joke goes,"Only two economists under-

stand international finance—and they dis-agree." Today that sense of mystery has be-come more frustrating. International eventsnow generate immediate and obvious conse-quences in U.S. markets on a daily basis.Early morning business broadcasts report over-night events in foreign markets in detail andwith an urgency that a decade ago would havebeen reserved for wars or diplomatic crises.

While it is easy to see that events movearound the globe through the internationalmarkets as one market closes and the next oneopens, it seems to work differently every time.One time, Japanese rates go up and U.S. ratesgo up in lockstep and the analysts discuss howworld credit markets have become "a singlemarket, each market tightly coupled with itsinternational counterparts." The next day,Japanese rates go up while U.S. rates fall andthe analysts talk about shifts in investor prefer-ences and political uncertainties and theorizewhy the markets have become "decoupled."

The importance of the links between theinternational credit markets are self-evident intoday's highly integrated financial world.Every two weeks on the CHIPS wire, the fi-nancial link between London and New York,there are enough credit flows between the twocountries to purchase the combined GNPs ofboth countries. However, these links are slip-pery, appearing to defy normal notions of logic

and consistency. It sometimes seems as if theinternational markets have a will of their own.Indeed, analysts often talk of the market doingsuch and such as though it were a sentientbeing instead of an organized exchange whereinvestors buy and sell.

In truth, there is very little mystery andthe mechanisms that control the linkages be-tween markets are actually quite simple. Sup-ply and demand work much the same way ininternational credit markets as they do in anyother market. The impression that the marketsare mysterious is an illusion created by thelarge number of things going on at any onetime. Press explanations of international creditmarkets, perhaps due to some misguided no-tion of simplicity, often leave out key detailsand baffle the observer. Much like the magi-cian, the pundit, by keeping part of the actionobscured, leaves the audience open-mouthedwith disbelief at the conclusion.

This article explores the relationship ofhighly integrated credit markets to provide abetter understanding of exactly what is goingon in international credit markets. It does soby examining four cases that are constructedwith only one factor changing. It then showsthat by mixing the four types of events ana-lyzed it is possible to understand more fullyhow international markets' linkages operateand why those linkages often produce seem-ingly inconsistent outcomes across time. The

Steven Strongin is an assistant vice president andsenior economist at the Federal Reserve Bank ofChicago. The author thanks Kenneth Kuttner andHesna Genay for their helpful comments.

2 ECONOMIC PERSPECTIVES

cases are similar to current events, but are sim-plified to make the analysis clearer.

Some readers may find that the hypotheti-cal cases presented both oversimplify the pres-ent structure of international markets and over-state the degree of integration that actuallyexists. This is done on purpose. The point isthat even in such a hypothetical world, wheremarkets are completely integrated and efficient,international markets will still not march inlockstep and that important information is lostby reducing our world view to "one worldmarket." However, after the four cases arepresented, it is argued that almost any real-world international credit shock can be viewedas a combination of the four presented.

In each case the question asked is, how areU.S. markets affected by foreign events? Ineach case a specific country is treated as therest of the world. In the first case, for example,Japan is so designated. This in no way affectsthe analysis. It does, however, simplify theexposition.

A short note on jargon

Writing on international markets is filledwith terms that seem to shift meanings withthe seasons. In this article, jargon is kept to aminimum, but some of the most overused termsare kept in order to provide the reader withsome notion of how these terms may or maynot apply to actual events. The definitions ofthe slipperiest terms follow.

Coupled markets are markets which movetogether in lockstep; for example, if Japaneserates go up by 2 percentage points, then U.S.rates will go up by 2 percentage points.Weakly coupled markets are those that alwaysmove in the same direction, both up or bothdown, but not necessarily in the same incre-ments. Decoupled markets are markets thatsomeone once claimed were coupled, but movein opposite directions in response to some spe-cific event or over some period of time.

The market refers to the short-term debtmarket of the given country. Thus, the U.S.market would be the market for short-termdebt denominated in dollars and sold in theU.S. The German market would be the mar-ket for short-term debt denominated in marksand sold in Germany. The special require-ments for comparing markets denominatedin different currencies is discussed in an ac-companying box.

Case 1: Japan tightens credit

Assume an action by the Bank of Japanthat restricts credit in Japanese markets. Theresult: World interest rates rise, in response toa reduction in world credit supplies. This keyoutcome can be seen in Figure 1.

The economics of this are simple supplyand demand. The world supply of credit issimply the sum of the credit supplied by eachcountry at a given rate of return. In this case,

Supply world = Supply us Supply japan'.

World demand is the sum of the demandwithin each country:

Demand world = Demand us Demand,„.

Viewed as a single world market, a reduc-tion in Japan's supply of credit directly re-duces the world supply of credit. It should benoted at this point that the r in Figure 1 and allsubsequent figures is the risk-adjusted (includ-ing exchange-rate risk) real return on capital.It must, thus, be equal or nearly equal acrossnations. At various points, it will be importantto draw a distinction between this rate and theobserved nominal rate which is affected bycountry-specific risks and inflation expecta-tions. The use of r in this form is really anassumption that international markets are well-integrated and efficient. For the countries inquestion, this is probably a reasonable assump-tion (see accompanying box for a more in-depth analysis of this issue).

FEDERAL RESERVE BANK OF CHICAGO

Adding up quantities of credit across nations

There are a number of ways of thinking aboutinternational markets that look very different for-mally, but are actually the same once you brave themathematics. In the accompanying analysis sub-stantial use is made of supply and demand analysis.Supply and demand has a long and venerable tradi-tion in economics, but in the international case itglosses over two fairly important issues. First, howdo you add quantities of credit that are valued inboth yen and dollars, sometimes hedged, some-times not? Second, how do you compare interestrates across countries when the debt instruments arevalued in different currencies and subject to differ-ent risks and taxes? The full answer to these ques-tions is clearly beyond the scope of this article, butthe problems, at least for the cases discussed in thisarticle, are not that difficult.

International finance typically concerns itselfwith questions about the efficiency of internationalcredit markets, where very exact and precise treat-ment of inflation and tax differentials are neces-sary, and measurement of risk is the keystone of theanalysis. In this article, we are trying to understandhow events in one country's credit market canaffect the credit market in another, and howchanges in relative risk affect international markets.Thus, we can deal with these very difficult issues ofinternational finance by assuming that internationalmarkets are efficient and by reducing the problemto the essentials of changes in the cost of capitaland real flows of capital. Nevertheless, some ex-planation of how this is done is appropriate.

Central to understanding how we can add yenmarkets and dollar markets together without gettingdeeply mired in issues of currency valuation is theobservation that credit markets are actually goodsmarkets seen though the veil of money. Creditrelates directly to the goods that are purchased.You supply credit if you consume less than youmake. You demand credit if you consume morethan you make. Anything more complicated can-cels out when the accountants finish counting.

Thus, from an international perspective acountry that produces more than it consumes is anet exporter of goods as well as credit and a coun-try that produces less than it consumes will be botha net importer of goods and capital. The supply ofcredit can be thought of as the excess supply ofgoods and the demand for credit as the excessdemand for goods. So when we add up the creditdemands in two countries we are adding up theexcess demand for goods and the excess supply ofgoods. It doesn't really matter if a ton of steel isvalued in yen or in dollars, it is still a ton of steel.

Clearly, countries produce and demand differ-ent goods. Some goods are only internal to thecountry, such as land, and some goods are difficultto move from one country to another, such as legalservices. Nevertheless, from the standpoint ofinternational trade the adding up is valid. It is,after all, only the unconsumed traded goods thatmove between countries and match to the interna-tional credit flows. These other technical issuessimply demonstrate why currency valuation is socomplicated, since it is in the process of currencyvaluation that all technical issues are balanced outwith movements in the international goods markets.They also show why simple notions of purchasingpower parity seldom work.

In the end, international credit flows matchinternational goods flows. Nobody borrows moneyjust to hold it. If the foreign credit is used to buyimported goods, this is obvious. If the foreigncredit is used to buy securities (Japanese purchasesof U.S. Treasury bills for example) or domesticgoods, then they are supplying cash or credit tosomeone who will buy other goods. If the countryas a whole is consuming more than it makes, even-tually those borrowed funds will be used to buyforeign goods. ("Goods" here is used in a generalsense of all goods and services, as well as sales ofassets.) In other words, you make what you can.You trade for what you cannot make. And onlythen do you borrow. And then it can only be to buysomething that someone else makes.

In the official trade accounts, there is a differ-ence between the current account in goods andservices and the capital account. This number islabeled statistical discrepancy and represents thelimitations of the trade statistics, not any real eco-nomic phenomenon.

Comparing interest rates across nationsTo examine comparable interest rates, you

have to reduce the price of credit to the opportunitycost of capital in international markets. In terms ofreal performance, the important question is the costof investing in new capital. So the r in a supplyand demand context is the cost of buying credit inorder to finance capital acquisitions in a givenmarket. What is the relationship between the do-mestic nominal rates we observe in the market andthe opportunity cost of capital? The answer iscomplicated, but not hopelessly obscure.

Risk factors, taxes, and inflation all play a rolein comparing debt instruments across countries.Inflation and taxes are conceptually the simplestproblems to address. Rates should be compared onan after-tax basis. After all, the real cost of capital

4 ECONOMIC PERSPECTIVES

is what is costs after the government has taken itsshare of the profits.

Unfortunately, it is rarely possible to calculatean after-tax return because the tax codes are suffi-ciently complicated that the after-tax rates differfrom individual to individual, let alone country tocountry. Luckily, for most purposes we can ignorethe tax effects, because there are no differencesbetween funds raised domestically and those raisedin foreign markets. Interest costs may be deductedfrom income regardless of the source of funds. Soas long as the tax codes are not changing, the taxeffects act as a constant or nearly constant distor-tion between observed U.S. rates and foreign rates,a kind of slow-moving fudge factor. Taxes can beextremely important over the long haul, but arerarely important over the short spans of time inwhich credit markets typically operate. Largechanges in tax laws are an exception, but theyluckily do not happen often and usually cause onlya short-term breakdown in the relationships dis-cussed in this article while the markets adjust.

Inflation needs to be dealt with more directly.Investors care about real returns, not nominal ones.Since the actual return on investment is the returnafter taxes and inflation, investors are interested inthe expected return net of inflation and taxes.Thus, in a very simple world of constant marginaltaxes and constant inflation, a country's real rate ofinterest must be adjusted for its rate of taxation andinflation by the following formula:

r = (1-0(i-rc)where r is the real after-tax rate of interest; i is

the observed nominal rate of interest; TC is the rateof inflation; and t is the tax rate. In the real world,taxation is much more complicated although it canusually be ignored for our purposes. Expectedinflation is much more volatile and unfortunatelynot directly observable. Nevertheless, there is abroad notion in the equation that, as long as nomi-nal rates increase to fully reflect expected inflation,there is no effect on real rates. This is a good start-ing place for analysis. Put simply, if the inflationin one country goes up and nominal rates also go upby the same amount, the actual cost of capital isunaffected and there are no real economic effects.Mathematically, if i and it go up the same amount,r is unaffected. Depending on tax issues and otherfactors this may not always be strictly true, but,given the general level of precision in these models,it is a good working assumption and for most of theobserved inflation rates in major industrializedcountries fairly accurate.

Risk is a more subtle problem. Taxes, cur-rency valuations, and inflation do not stay the same.

As a result, investors require compensation for therisk they assume in a given debt instrument. Inter-national rates can only be compared when the dif-ferences in relative risk have been taken into ac-count. A country where risks are greater will haveto pay more for international funds. Risk can takemany forms: worries about central bank behavior,taxes, or simple liquidity worries.

The key thing to understand about these poten-tial problems is their effects on credit flows. An-ticipated inflation, for example, will raise nominalrates and leave real rates unchanged producing noeffect whatsoever on the graphs in the article. Therisk of a sudden increase in inflation, on the otherhand, will raise real rates and scare away credit,since the suppliers of credit will demand compen-sation for the potential of inflation.

If there is a chance that there will be a suddenincrease in the price level due, for example, to acurrency conversion as is occuring in Germany in1990, nominal rates will rise to reflect the expecta-tion of higher inflation. If the inflation does notoccur, lenders will profit and borrowers lose. If theinflation does occur the opposite takesplace—borrowers gain and lenders lose. The un-certainty about inflation makes debt contracts inthat particular currency more risky. As a result,investors will prefer other currencies at the margin,regardless of which side of the contract they intendto be on. Moreover, since lenders tend to be moremobile in terms of switching from market to mar-ket, this will cause rates to rise in the riskier mar-ket. From the standpoint of the borrower, one wayto think of this is that in order to achieve the samelevel of risk, it would be necessary to pay both forthe expected inflation and for a currency hedgewhere the cost of the currency hedge is directlyrelated to the amount of uncertainty.

In general, the way to separate events thataffect international credit markets from those thatdo not is to examine the risk faced by internationalinvestors in a debt contract denominated in onecurrency relative to another. If the event raises therelative risk, then real effects on internationalcredit flows are likely to follow.

Risk-induced changes cause investors to favorone country over another and create real changes inthe relative cost of capital. In the pure inflationcase, investors simply require an adjustment in theinterest rate to compensate for inflation. This isexactly offset by the borrowers' ability to pay backtheir debts with cheaper inflated currencies. Infla-tion only causes a change in the units of measurebut risk of inflation changes the actual costs. Thisis made more explicit in Cases 3 and 4.

FEDERAL RESERVE BANK OF CHICAGO 5

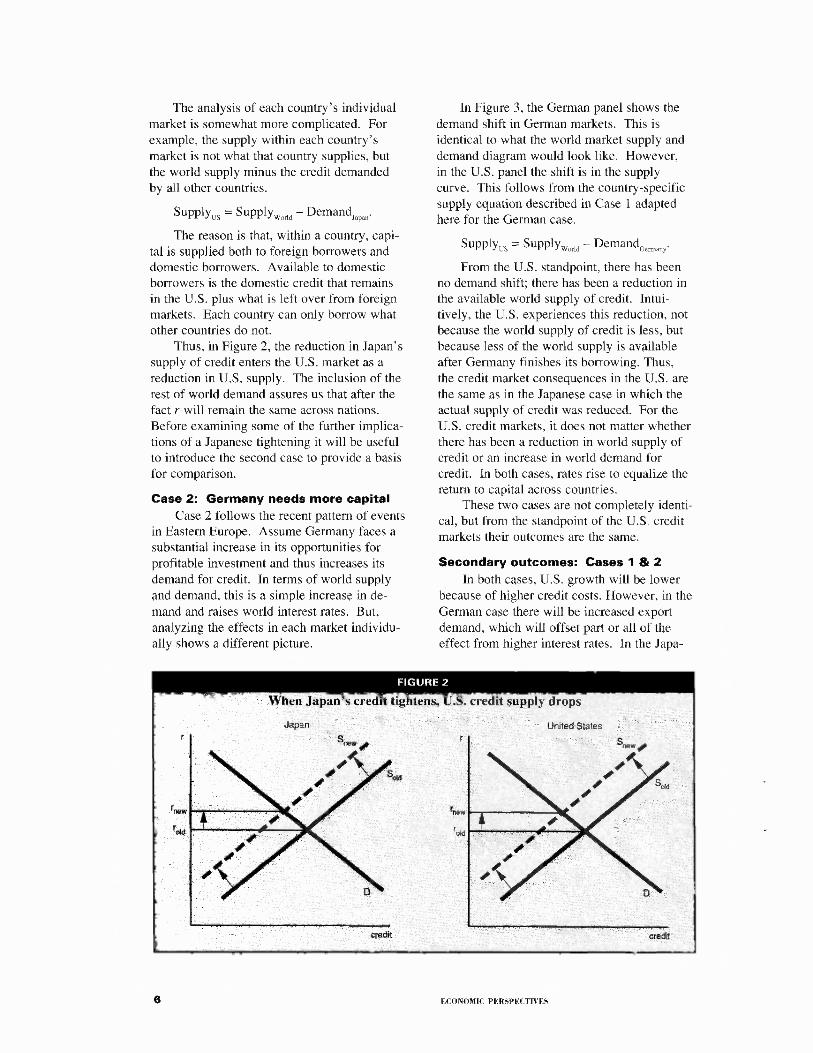

When Japan's credit tightens, U.S. credit supply drops

!Japan United States

The analysis of each country's individualmarket is somewhat more complicated. Forexample, the supply within each country'smarket is not what that country supplies, butthe world supply minus the credit demandedby all other countries.

Supply us = Supply world — Demand japan

The reason is that, within a country, capi-tal is supplied both to foreign borrowers anddomestic borrowers. Available to domesticborrowers is the domestic credit that remainsin the U.S. plus what is left over from foreignmarkets. Each country can only borrow whatother countries do not.

Thus, in Figure 2, the reduction in Japan'ssupply of credit enters the U.S. market as areduction in U.S, supply. The inclusion of therest of world demand assures us that after thefact r will remain the same across nations.Before examining some of the further implica-tions of a Japanese tightening it will be usefulto introduce the second case to provide a basisfor comparison.

Case 2: Germany needs more capital

Case 2 follows the recent pattern of eventsin Eastern Europe. Assume Germany faces asubstantial increase in its opportunities forprofitable investment and thus increases itsdemand for credit. In terms of world supplyand demand, this is a simple increase in de-mand and raises world interest rates. But,analyzing the effects in each market individu-ally shows a different picture.

In Figure 3, the German panel shows thedemand shift in German markets. This isidentical to what the world market supply anddemand diagram would look like. However,in the U.S. panel the shift is in the supplycurve. This follows from the country-specificsupply equation described in Case 1 adaptedhere for the German case.

Supply„ = Supply world — Demand Germany.

From the U.S. standpoint, there has beenno demand shift; there has been a reduction inthe available world supply of credit. Intui-tively, the U.S. experiences this reduction, notbecause the world supply of credit is less, butbecause less of the world supply is availableafter Germany finishes its borrowing. Thus,the credit market consequences in the U.S. arethe same as in the Japanese case in which theactual supply of credit was reduced. For theU.S. credit markets, it does not matter whetherthere has been a reduction in world supply ofcredit or an increase in world demand forcredit. In both cases, rates rise to equalize thereturn to capital across countries.

These two cases are not completely identi-cal, but from the standpoint of the U.S. creditmarkets their outcomes are the same.

Secondary outcomes: Cases 1 & 2

In both cases, U.S. growth will be lowerbecause of higher credit costs. However, in theGerman case there will be increased exportdemand, which will offset part or all of theeffect from higher interest rates. In the Japa-

6 ECONOMIC PERSPECTIVES

When Germany demands more credit, U.S.

Germany

FIGURE 3

nese case export demand will fall, which willreinforce the higher interest-rate effects.

The differences in the two cases arisefrom the fact that world supply and demandfor goods and services are different in eachcase. In the German case world demand forgoods is higher, while in the Japanese caseworld demand for goods is lower. As a result,world and country-specific inflation pressureswill be higher in the German case, while in theJapanese case inflation pressures will be lower.

But, in terms of nominal interest rates, theGerman case will cause a somewhat greaterrise in U.S. interest rates. This occurs becauseinflation, due to increased world demand forgoods, and the real cost of capital are movingin the same direction. In the Japanese case,the reduced inflationary pressures will slightlyoffset the real interest-rate increases.

The effects on profits and the stock mar-ket are also different. In both cases higherrates cause future profits to be discountedmore heavily, but in the German case this isoffset (perhaps more than offset) by higherexpected profits. In the Japanese case ex-pected declines in profits cause an even deeperdecline in stock values.

Exchange-rate effects are the same inCases 1 and 2, but the mechanisms are quitedifferent. If exchange rates are viewed as therelative price of two currencies, then in theGerman case the mark rises because there isgreater demand for marks, due to higher realgrowth and the subsequent increase in demand

for transactions deposits in Germany. In theJapanese case, the yen rises because its supplyhas been reduced. So, despite the fact that thechannel is quite different in each case, a rise inrates causes the foreign currency to appreciate.(It should be noted that in both cases U.S.interest rates rise and the dollar falls. Thepositive interest-rate-to-currency effects arelimited to the originating country. They areexactly opposite for the receiving country—the U.S.)

This interest-rate-to-exchange-rate rela-tionship, which could be called the "normal"relationship, is reversed in Case 3.

Case 3: Investors lose faith in Japan

Assume that international investors losefaith in the ability of Japan to maintain thesteady growth and generally orderly markets itis famous for. Such a loss would in turn causeinvestors to demand higher risk premiums forinvesting in Japan. In terms of the previousdiagrams, the original equilibrium in bothcountries is the same, but now the supply ofcredit in Japan falls while the supply of creditin the U.S. increases, as in Figure 4.

As a result, r is no longer the same in bothcountries, but is lower in the U.S. than in Ja-pan. The reason for this has to do with theway r is constructed. In the previous cases, rwas adjusted for all risk factors so that returnswere equalized across nations. In this case,the adjustments are made for conditions priorto the shock, but afterwards an additional

FEDERAL RESERVE BANK OF CHICAGO 7

credit credit

Japan

FIGURE 4

Loss of confidence in Japan produces credit rate differential

premium is necessary to adjust for the nowhigher risk in Japan. Quantitatively, the newrisk in Japan makes investors want a higherreturn for bearing that risk. The exact pre-mium is the difference between the new U.S.rate and the new Japanese rate, (1) percentagepoints in Figure 4.

Operationally, investors' willingness tolend to Japan is reduced by relative to theirnew willingness to lend to the U.S., that is,previously they would lend to Japan if r washigher in Japan and to the U.S. if r was higherin the U.S. Now they will lend to Japan onlyif r in Japan is at least percentage pointshigher than in the U.S.

In order to examine later events, both theJapanese supply and demand curves wouldboth need to be shifted straight up by (I) tomatch the U.S. curves in terms of r. Thisupward shift will then re-equalize the riskfactors and incorporate the market's currentassessment of the relative risks of Japaneseversus U.S. securities. This is, in essence, ex-actly how the risk-adjusted curves are derivedin the first place.

As a result of the shift in relative realrates, a number of consequences occur whichare quite different qualitatively from the previ-ous cases of increases in foreign rates. LowerU.S. rates cause U.S. growth to increase.Higher Japanese rates make Japanese growthfall. The increased growth in the U.S. causesan increase in the demand for money in theU.S., while reduced Japanese growth lowersthe Japanese demand for yen. Thus, while

Japanese interest rates rise and U.S. interestrates fall, the dollar appreciates. This is ex-actly contrary to the previous two cases, butmakes perfect sense. If Japan is seen as risk-ier, it both devalues the yen and raises Japa-nese interest rates.

Thus, it begins to be clear how the link-ages between markets can create very differentresults at different times. Events such as thosein the first two cases, when the supply anddemand for credit within one country change,cause rates to move together world-wide andthe currency of the country whose rates wentup first to appreciate. In this third case whereinvestor preferences between countries change,the exact opposite happens. Rates move in op-posite directions and the currency of the coun-try whose rates increase actually depreciates,contrary to the normal notion of higher ratesmeaning higher values for currency. An inter-esting irony is that so-called domestic eventssuch as those in Cases 1 and 2 produce whatappears to be tightly coupled world capitalmarkets, while truly international events suchas those in the third case produce the appear-ance of decoupling.

Just within the context of these three verysimple cases it is clear that strong internationallinkages are consistent with almost any patternof interest rate and currency movements de-pending on what type of events precipitate thechanges. It isn't that the rules change, it's thatdifferent types of events lead to different out-comes. Hardly a surprising result.

8

ECONOMIC PERSPECTIVES

Case 4: Country-specific inflationThe cases until now have covered basic

ways in which changes in one country or in-vestors' views of that country can have effectson other countries. The last case spends alittle time on a change that does not have im-portant international implications but that isoften thought to be very important.

Assume that, due to reunification, Ger-many will have an increase in its price level of10 percent over 5 years. Obviously there willbe some risk associated with this that willcause effects similar to those analyzed in Case3. Beyond the risk effect, however, there isvery little effect in terms of international capi-tal flows.

In the supply and demand diagrams usedin this article, r is adjusted for known differ-ences in inflation and expected changes inexchange rates. In the case of a perfectlyanticipated increase in inflation as assumed inthe present case, all that happens is that nomi-nal rates in Germany rise by an average of 2percentage points a year for 5 years to coverthe additional inflation (Forward exchangerates will incorporate an additional average 2percent a year depreciation to adjust futureexchange rates to the greater inflation as well.)Nothing else changes. Therefore, the diagramsdo not change.

The reason for this is that investors careabout the purchasing power of their invest-ments, not about the number of pieces of paperthey have at the end of the day. As a result, aslong as nominal rates rise enough to coverinflation, nobody cares. Investors are compen-sated by the higher rates, borrowers are willingto pay the new higher rates because they willpay off their loan with cheaper currency. It allcancels out. Nominal rates in Germanychange and the mark depreciates in the futurewhen the inflation actually occurs, but that'sall that happens as long as German rates adjustto compensate fully for inflation.

To the extent that German monetary au-thorities do not fully adjust short-term rates toaccommodate the increase in inflation therewill be some additional consequences. This isexactly the mirror image of Case 1 whereJapan tightens credit. The failure to let ratesfully reflect the rise in inflation is the equiva-lent to lowering rates by easing the supply ofcredit and real rates fall. Thus, the value ofthe mark would fall and world real rates would

decline. This is a simple illustration of thefact that constant short-term rates do not al-ways mean constant policy.

Putting it all togetherThe four cases examined were each de-

signed to highlight specific aspects of thetransmission of credit market shocks throughinternational markets. The real world is, ofcourse, far more complicated. However, bytaking the examples described above and ap-plying them to a real-world case, it shouldbecome clear why the descriptions of interna-tional market behavior in the business presscan often be seriously misleading and seem-ingly inconsistent.

Take the case of the release of new CPInumbers in the U.S. Suppose those numberscome in below expectations and this is takenas a sign that inflationary pressures are lessthan had previously been assumed. The analy-sis in Case 4 would suggest that this wouldcause U.S. nominal rates to fall by preciselythe reduction in inflationary expectations.Real rates would remain the same both in theU.S. and in foreign markets as well. The dol-lar would remain steady as neither the supplynor demand for money in the U.S. or anywhereelse would have changed. (There could evenpotentially be a small rise in the dollar becauseinflation acts as a small tax on non-interestbearing types of money and the reduction ininflation would generate a small increase inthe demand for U.S. currency.) With U.S.interest rates falling, foreign rates steady, andthe dollar steady or rising, the markets wouldbe said to be decoupled.

In reality, the response would be morecomplicated. The reduction in inflationaryexpectations would have an impact on ex-pected monetary policy. Depending on currentpolicy, it would either reduce the pressure totighten or generate some expectation of lowerrates. In either case it would create the expec-tation of a larger-than-expected supply ofcredit in U.S. markets. This would generateeffects that mirror those in Case 1. Worldrates would fall as easier U.S. monetary policywould increase the world supply of credit.Thus, rates would fall everywhere, althoughnominal rates would fall more in the U.S. thanin foreign markets due to the lower inflation.In addition, the dollar would fall due to anexpected increase in the supply of dollars

FEDERAL RESERVE BANK OF CHICAGO 9

relative to foreign currencies. Thus, if theCase 1 effects dominate, the markets would besaid to be weakly coupled.

If, for political reasons, the lower inflationmade it likely that many of the world's centralbanks would engage in a coordinated easing,then both foreign and domestic rates wouldfall together and the markets would be said tobe tightly coupled. The dollar would riserather than fall because other central bankswould also be increasing the supply of theircurrencies, but only the U.S. would have lowerinflation expectations to offset this effect.

Further complicating this situation, if thecoordinated actions were viewed as inappro-priate by the markets because of the substan-tial inflationary pressures that might, for ex-ample, occur in Germany, German rates couldactually rise due to the increased risk in hold-ing German securities, as described in Case 3.In such a case, Germany would be said to havebecome decoupled from the rest of the interna-tional market.

Yet, in all of these possibilities interna-tional markets have been treated throughout asone integrated market. The problem with allthis talk of coupling and decoupling is that itmisses the richness of the dynamics of theinternational credit markets. The four simplecases presented in this article are capable ofdisplaying an enormous range of outcomesdepending on how they are mixed. It is notthat what is going on in international creditmarkets is so complicated; it is that so manydifferent things can happen at the same timethat disentangling the effects of a specificevent is nearly impossible.

ConclusionWhile it is not possible fully to discern

what effects international events will have onU.S. markets, the surface randomness of marketresponses should not be all that disturbing. It isimportant not only to keep track of what themarkets are doing, but why they are doing it.

Almost any specific international financialmarket shift in exchange rates or interest ratescan be explained by more than one combinationof the cases described above, which coverchanges in both the supply and demand forcredit as well as changes in relative preferencesof investors between countries and the effectsof inflation. However, the real economic conse-quences differ significantly depending onsources of the international disturbances. Thus,while international markets have become in-creasingly important for our economy and forthe process of policy formation, the lack of aclear simple relationship between events in for-eign markets and our own economy means thatforeign developments have to be analyzed interms of their likely sources and consequencesand do not, in themselves, tell us very much.

Unfortunately for proponents of interna-tional coordination of monetary policy, thismeans that international market movements donot map smoothly into policy actions. Seem-ingly equivalent market movements can haveradically different implications for individualeconomies and thus require substantially differ-ent policy actions. It is only by examiningthe sources of international developments andprojecting their effect on the various affectedeconomies that policy implications can bedetermined.

REFERENCES

Caves, R.E., and R.W. Jones, World tradeand payments, Little Brown, Boston, 1973.

Dornbush, R., "Money, devaluation, and non-traded goods," Scandinavian Journal of Eco-nomics, Vol. 78, No. 2, May 1976, pp. 255-275.

Frenkel J., and H.G. Johnson, The monetaryapproach to the balance of payments, GeorgeAllen and Unwin, 1975.

Hodrick, Robert J., "An empirical analysisof the monetary approach to the determination

of the exchange rate," in The economics ofexchange rates, Jacob A. Frenkel and Harry G.Johnson (eds.), Addison-Wesley PublishingCompany, Reading, PA, 1978, pp. 97-116.

Mussa, Michael, "The exchange rate, thebalance of payments, and monetary and fiscalpolicy under a regime of controlled floating,"Scandinavian Journal of Finance, Vol. 78, No.2, May 1976, pp. 229-248.

10 ECONOMIC PERSPECTIVES