interpreting current packaging trends & future consumer behaviour · ·...

TRANSCRIPT

1Arena PACE Forum Europe | March 2018

Interpreting Current Packaging Trends & Future Consumer Behaviour

Dominic Cakebread, Head of Packaging Consulting

Arena PACE Forum Europe 6 March 2018

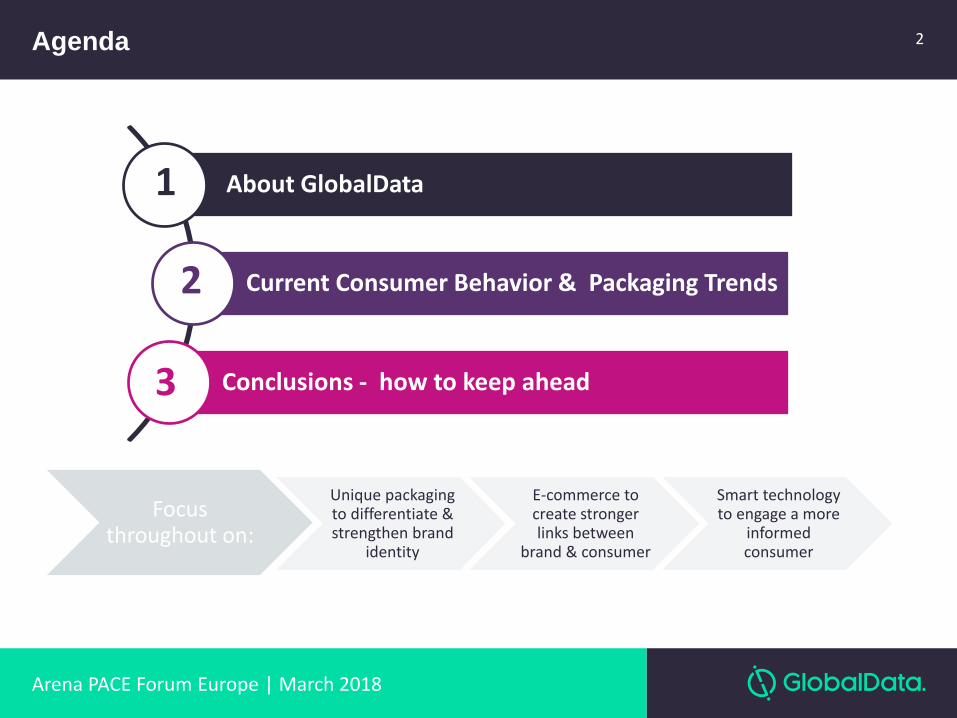

Agenda

Arena PACE Forum Europe | March 2018

2

About GlobalData

Current Consumer Behavior & Packaging Trends

Conclusions - how to keep ahead

1

2

3

Focus throughout on:

Unique packaging to differentiate & strengthen brand

identity

E-commerce to create stronger links between

brand & consumer

Smart technology to engage a more

informed consumer

Agenda

Arena PACE Forum Europe | March 2018

3

About GlobalData

Current Consumer Behavior & Packaging Trends

Conclusions - how to keep ahead

1

2

3

Arena PACE Forum Europe | March 2018

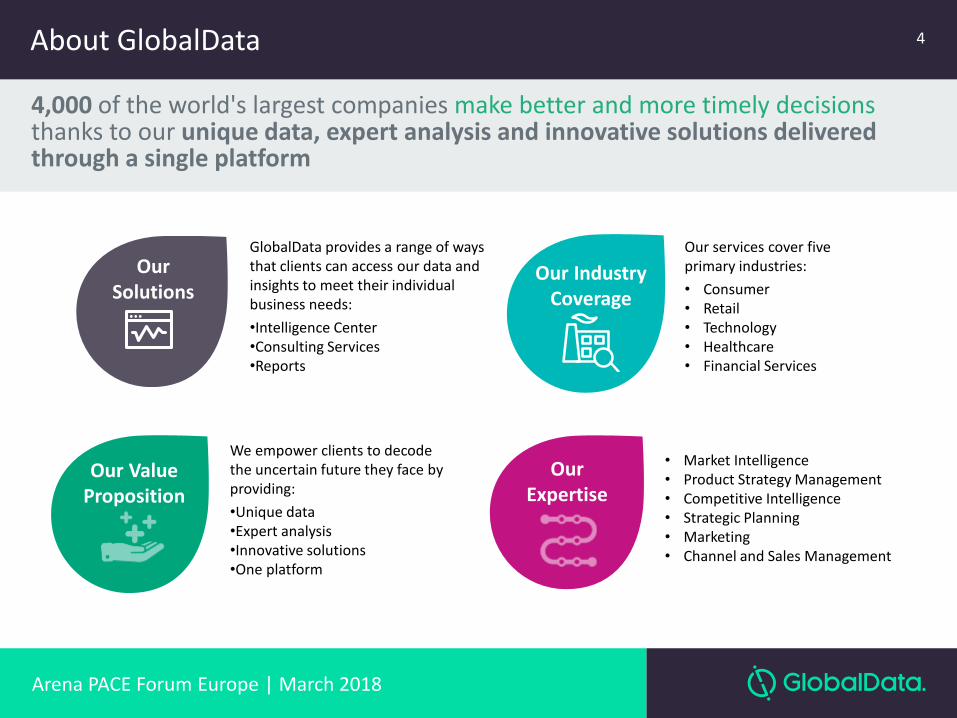

GlobalData provides a range of ways that clients can access our data and insights to meet their individual business needs:

•Intelligence Center•Consulting Services•Reports

• Market Intelligence• Product Strategy Management• Competitive Intelligence• Strategic Planning• Marketing• Channel and Sales Management

We empower clients to decode the uncertain future they face by providing:

•Unique data•Expert analysis •Innovative solutions•One platform

Our services cover five primary industries:

• Consumer• Retail• Technology• Healthcare• Financial Services

4,000 of the world's largest companies make better and more timely decisions thanks to our unique data, expert analysis and innovative solutions delivered through a single platform

Our Solutions

Our ValueProposition

Our Expertise

Our Industry Coverage

About GlobalData 4

Arena PACE Forum Europe | March 2018

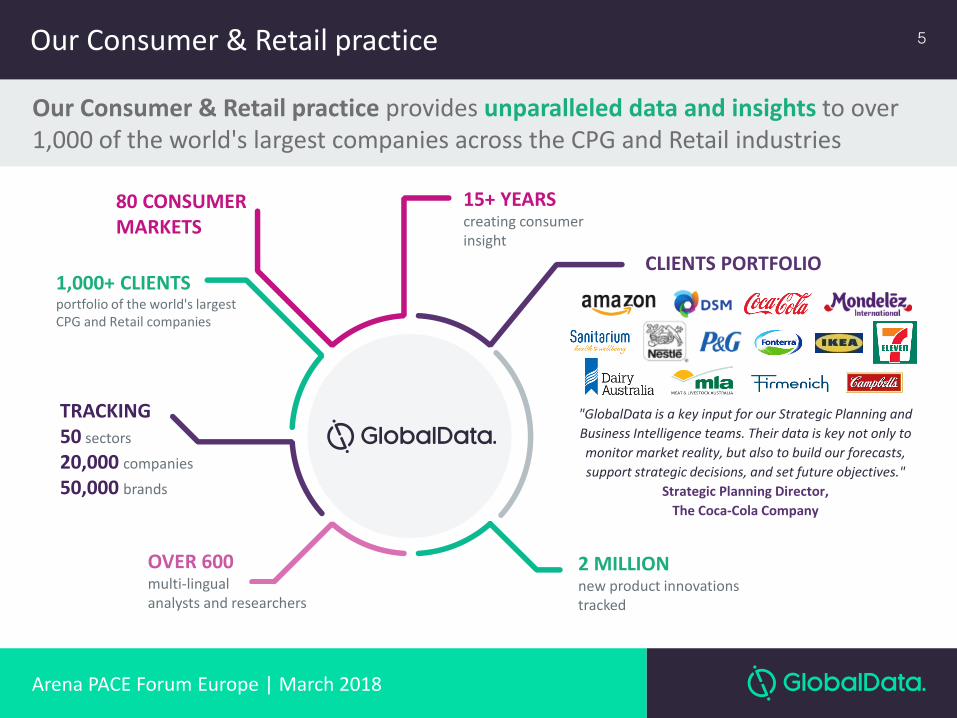

Our Consumer & Retail practice 5

15+ YEARScreating consumer insight

2 MILLIONnew product innovations tracked

OVER 600multi-lingual analysts and researchers

80 CONSUMERMARKETS

1,000+ CLIENTSportfolio of the world's largest CPG and Retail companies

CLIENTS PORTFOLIO

TRACKING50 sectors

20,000 companies

50,000 brands

"GlobalData is a key input for our Strategic Planning and

Business Intelligence teams. Their data is key not only to

monitor market reality, but also to build our forecasts,

support strategic decisions, and set future objectives."

Strategic Planning Director,

The Coca-Cola Company

Our Consumer & Retail practice provides unparalleled data and insights to over 1,000 of the world's largest companies across the CPG and Retail industries

© 2018 | Arena PACE Forum EuropeArena PACE Forum Europe | March 2018

6

Our CONSULTING offering provides tailored solutions to help clients identify new growth opportunities, minimize risk, gain competitive advantage, and improve profitability.

Consulting Services

INNOVATION & INSIGHT

OPPORTUNITY ASSESSMENT

MARKET & PRODUCT STRATEGY

MARKETING COMMUNICATIONS

FINANCIAL ANALYSIS

COMPETITIVE & COMPANYANALYSIS

REGULATORY, TRADE & INDUSTRY

FORECASTING

GLOBAL REACH, LOCAL INSIGHT

OUR CLIENTSWorking with the world’s leading consumer goods

manufacturers and retailers

OUR PROJECTS150 completed projects in

the last two years

OUR GLOBAL REACH Delivering value for

companies across all regions globally

OUR PEOPLEA team of 40

consultants specialising in diverse sectors

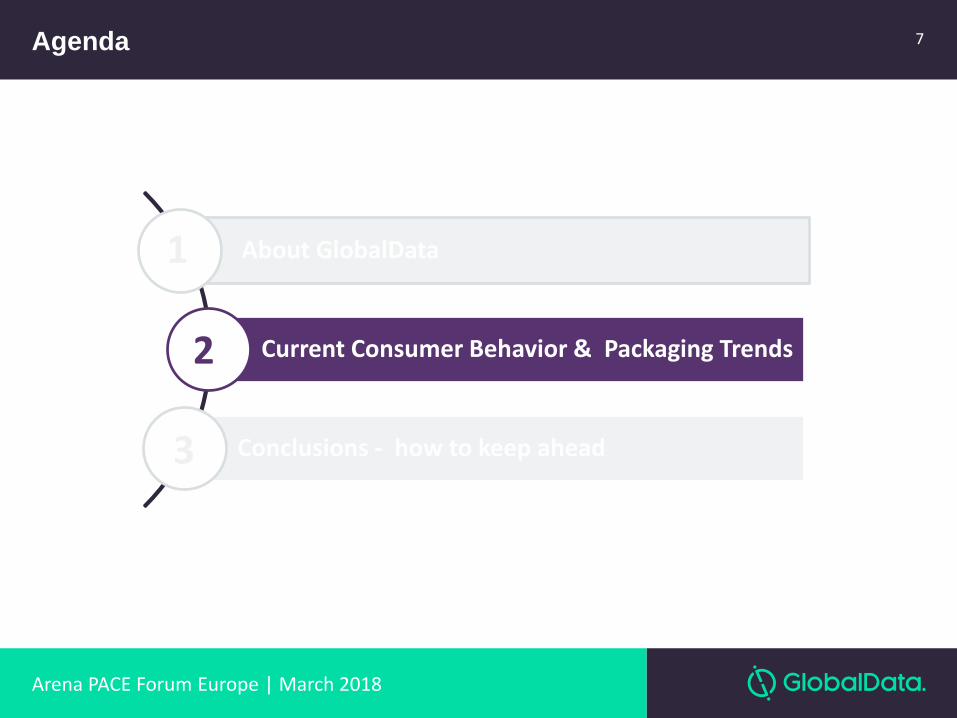

Agenda

Arena PACE Forum Europe | March 2018

7

About GlobalData

Current Consumer Behavior & Packaging Trends

Conclusions - how to keep ahead

1

2

3

Arena PACE Forum Europe | March 2018

8Key Consumer Behavior & Packaging Trends

1. Demographic & Economic Growth

2. Sustainability & Environment

3. Multichannel Distribution & E-Commerce

4. Smart Packaging and the Connected Consumer

5. Personalization and Individualization

6. Digital print

7. Differentiation in Shape & Design

© 2018 | Arena PACE Forum EuropeArena PACE Forum Europe | March 2018

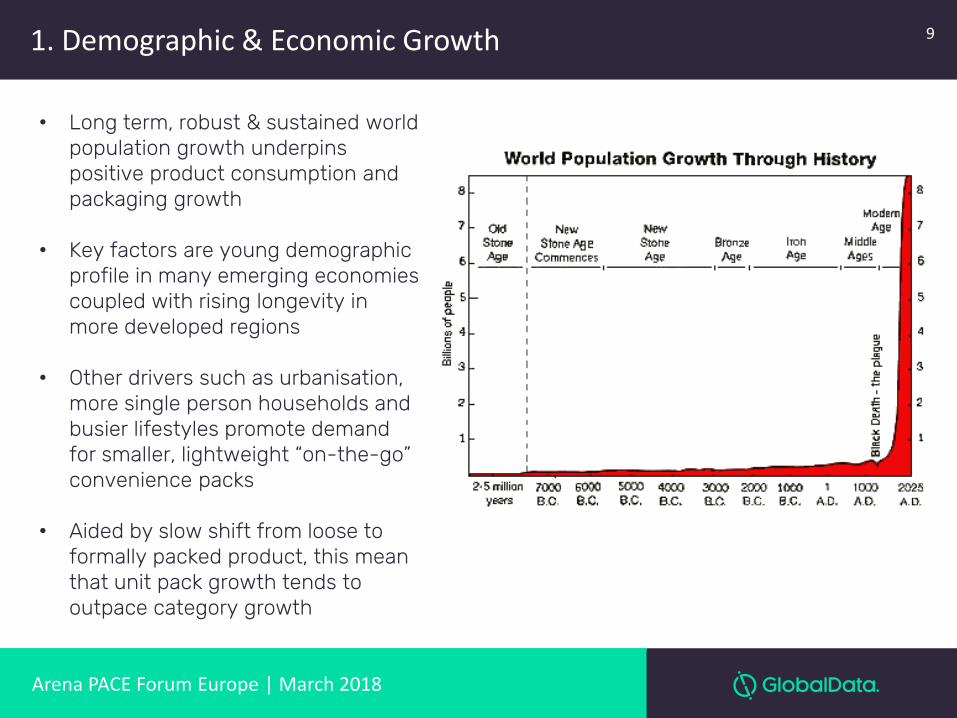

• Long term, robust & sustained world population growth underpins positive product consumption and packaging growth

• Key factors are young demographic profile in many emerging economies coupled with rising longevity in more developed regions

• Other drivers such as urbanisation, more single person households and busier lifestyles promote demand for smaller, lightweight “on-the-go” convenience packs

• Aided by slow shift from loose to formally packed product, this mean that unit pack growth tends to outpace category growth

1. Demographic & Economic Growth 9

© 2018 | Arena PACE Forum EuropeArena PACE Forum Europe | March 2018

Economic Growth Drivers :

• GDP Growth and rising consumer disposable income• Movement from Export to Consumption Economies• More working women • Rapid Growth in eCommerce & Online Shopping• Growth in global trade

All Leading to increased demand for:

• Smaller, lighter single serve, on-the go packaging • Lighter weight packaging – plastics & flexible pouches• More multi-packaging• More convenience features• Easier to open and recloseable packs• More products brands & competition leading to..• Need for individualisation of pack design to differentiate

Ageing populations and longevity is also driving need fro better easy to open and convenience packs

1. Demographic & Economic Growth 10

© 2018 | Arena PACE Forum EuropeArena PACE Forum Europe | March 2018

2. Sustainability and the Environment

• As total and per capita product and packaging consumption has increased, so too has concern to reduce packaging waste

• Consumer concern is rising rapidly and spreading geographically such that “Sustainability” is now a fundamental aspect of packaging’s DNA and built into many major corporate and brand development plans

• In consequence we see more use of:

- Stronger, but lighter weight, less resource-hungry materials- More use of recyclable and renewable materials- More responsibly sourced materials (e.g. FSC)- More use of barrier coatings for shelf life and better print- Rising interest in bio-derived and biodegradable polymers

• The sustainability debate is also increasingly moving from land-fill to ocean waste with a recent strong focus on plastics

11

© 2018 | Arena PACE Forum EuropeArena PACE Forum Europe | March 2018

Light-weighting – has been an ongoing packaging industry mega-trend for a decade –is still spreading globally and across CPG categories and countries

Driven as much by pressures to save costs & the desire for efficiency improvements in supply chain as environmental concerns

Are we possibly reaching limits of

technical feasibility in some key applications (beverage cans, PET bottled water, glass

bottles)?

But in the general packaging market, light-weighting is still

driving a strong trend from rigid to lower weight rigid plastics bottle and flexible

packaging (especially stand up pouches)

2. Sustainability and the Environment 12

Arena PACE Forum Europe | March 2018

13

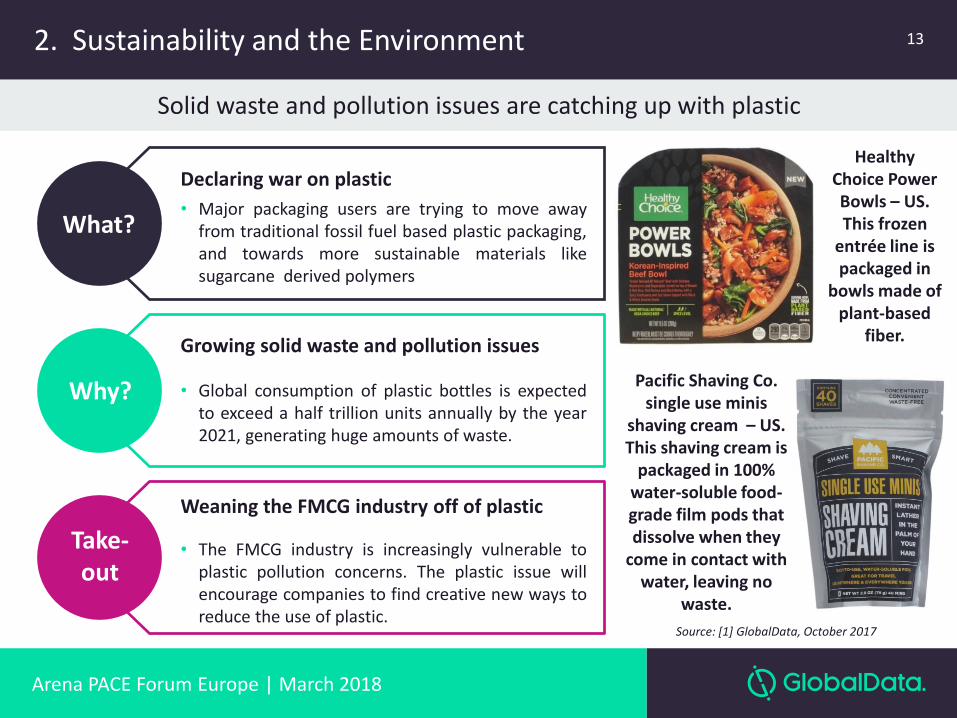

Solid waste and pollution issues are catching up with plastic

What?

Why?

Take-out

Declaring war on plastic

• Major packaging users are trying to move awayfrom traditional fossil fuel based plastic packaging,and towards more sustainable materials likesugarcane derived polymers

Growing solid waste and pollution issues

• Global consumption of plastic bottles is expectedto exceed a half trillion units annually by the year2021, generating huge amounts of waste.

Weaning the FMCG industry off of plastic

• The FMCG industry is increasingly vulnerable toplastic pollution concerns. The plastic issue willencourage companies to find creative new ways toreduce the use of plastic.

Healthy Choice Power Bowls – US. This frozen

entrée line is packaged in

bowls made of plant-based

fiber.

Pacific Shaving Co. single use minis

shaving cream – US. This shaving cream is

packaged in 100% water-soluble food-grade film pods that dissolve when they

come in contact with water, leaving no

waste.

Source: [1] GlobalData, October 2017

2. Sustainability and the Environment

Arena PACE Forum Europe | March 2018

14

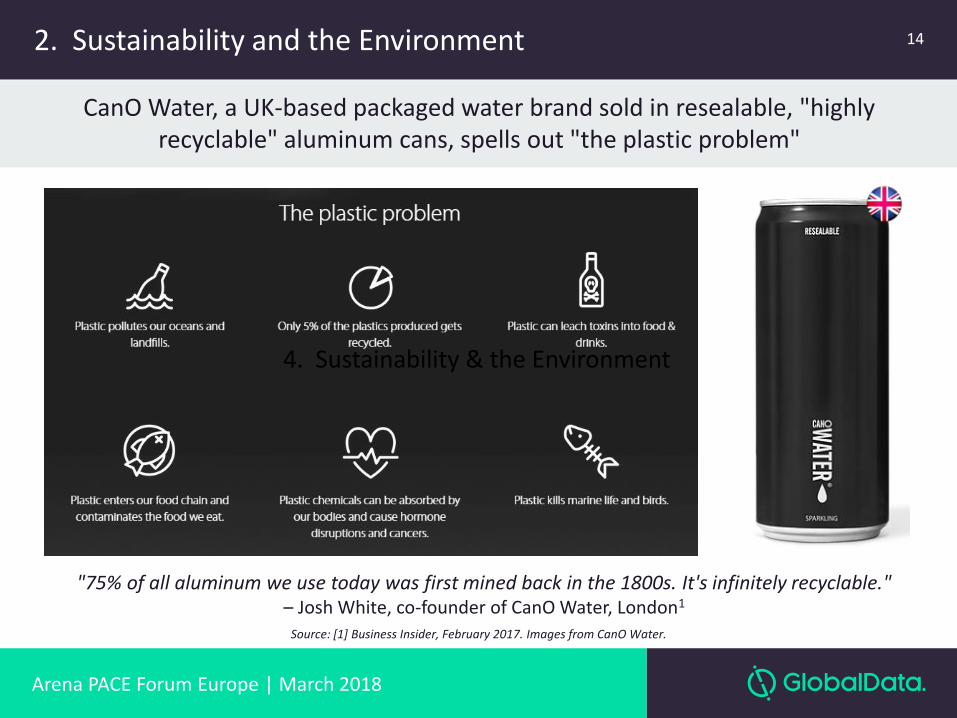

CanO Water, a UK-based packaged water brand sold in resealable, "highly recyclable" aluminum cans, spells out "the plastic problem"

Source: [1] Business Insider, February 2017. Images from CanO Water.

"75% of all aluminum we use today was first mined back in the 1800s. It's infinitely recyclable." – Josh White, co-founder of CanO Water, London1

4. Sustainability & the Environment

2. Sustainability and the Environment

Arena PACE Forum Europe | March 2018

15

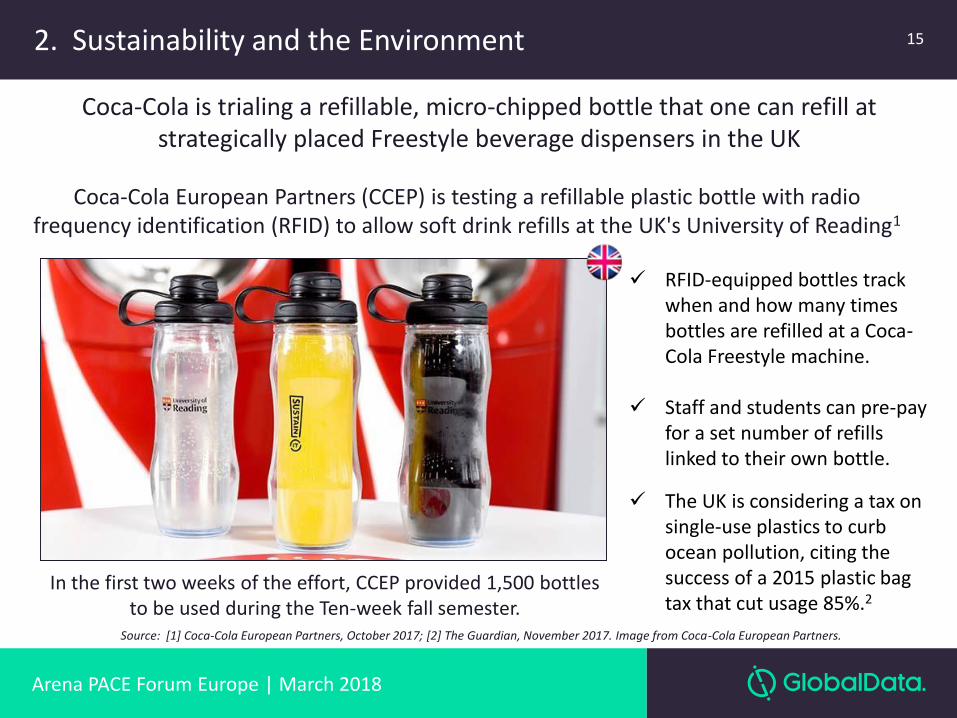

Coca-Cola is trialing a refillable, micro-chipped bottle that one can refill at strategically placed Freestyle beverage dispensers in the UK

Source: [1] Coca-Cola European Partners, October 2017; [2] The Guardian, November 2017. Image from Coca-Cola European Partners.

Coca-Cola European Partners (CCEP) is testing a refillable plastic bottle with radio frequency identification (RFID) to allow soft drink refills at the UK's University of Reading1

RFID-equipped bottles track when and how many times bottles are refilled at a Coca-Cola Freestyle machine.

Staff and students can pre-pay for a set number of refills linked to their own bottle.

The UK is considering a tax on single-use plastics to curb ocean pollution, citing the success of a 2015 plastic bag tax that cut usage 85%.2

In the first two weeks of the effort, CCEP provided 1,500 bottles to be used during the Ten-week fall semester.

2. Sustainability and the Environment

© 2018 | Arena PACE Forum EuropeArena PACE Forum Europe | March 2018

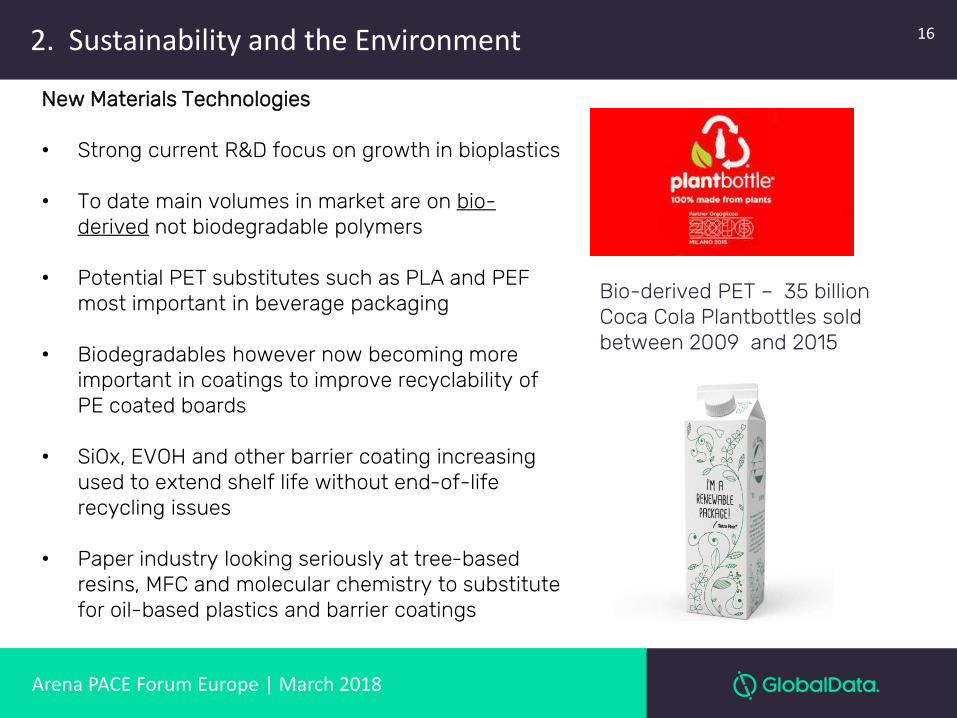

Bio-derived PET – 35 billion Coca Cola Plantbottles sold between 2009 and 2015

New Materials Technologies

• Strong current R&D focus on growth in bioplastics

• To date main volumes in market are on bio-derived not biodegradable polymers

• Potential PET substitutes such as PLA and PEF most important in beverage packaging

• Biodegradables however now becoming more important in coatings to improve recyclability of PE coated boards

• SiOx, EVOH and other barrier coating increasing used to extend shelf life without end-of-life recycling issues

• Paper industry looking seriously at tree-based resins, MFC and molecular chemistry to substitute for oil-based plastics and barrier coatings

162. Sustainability and the Environment

© 2018 | Arena PACE Forum EuropeArena PACE Forum Europe | March 2018

3. Channels of DistributionTraditional Retail

• Growth and change in self service modern retail infrastructure still remains a primary driver of packaging demand around the world

• Retail, e-Commerce and Online Shopping all changing fast & packaging needs to adapt to this

• In a more crowded environment and online the pack need to perform better to stand out, attract consumer to sell the product in all channels:

• Interest can be being boosted by:• Innovative Pack Shape, Print & Design• Use of Multi-packaging & Shelf ready outers• Better in store display and merchandising

Food Service

• Often overlooked , but growing at twice retail in many countries• Greater margin opportunity with smaller lighter, ‘on the go’ packs• Attention currently on waste from disposable drinks cups -

3. Multichannel Distribution and E-Commerce 17

© 2018 | Arena PACE Forum EuropeArena PACE Forum Europe | March 2018

E-Commerce

• Growth in online shopping has been accelerated rapidly in recent years as consumers have switched from ordering by computers to Smart phone apps

• Most online packaging is still far from optimised however; often standard, unprinted boxes, oversized, do not fit products, distribution system, delivery vehicle or letter boxes

• Longer term packs will be more purpose-designed to match products or even turned in to moving adverts (Minion Movie)

• Advertising potential of packaging in this area is under exploited- even online it is the packaging that the consumer sees not the product!

• Tactical use of digital print to address this is a likely to be expanded in future years

3. Multichannel Distribution and E-Commerce 18

Arena PACE Forum Europe | March 2018

19

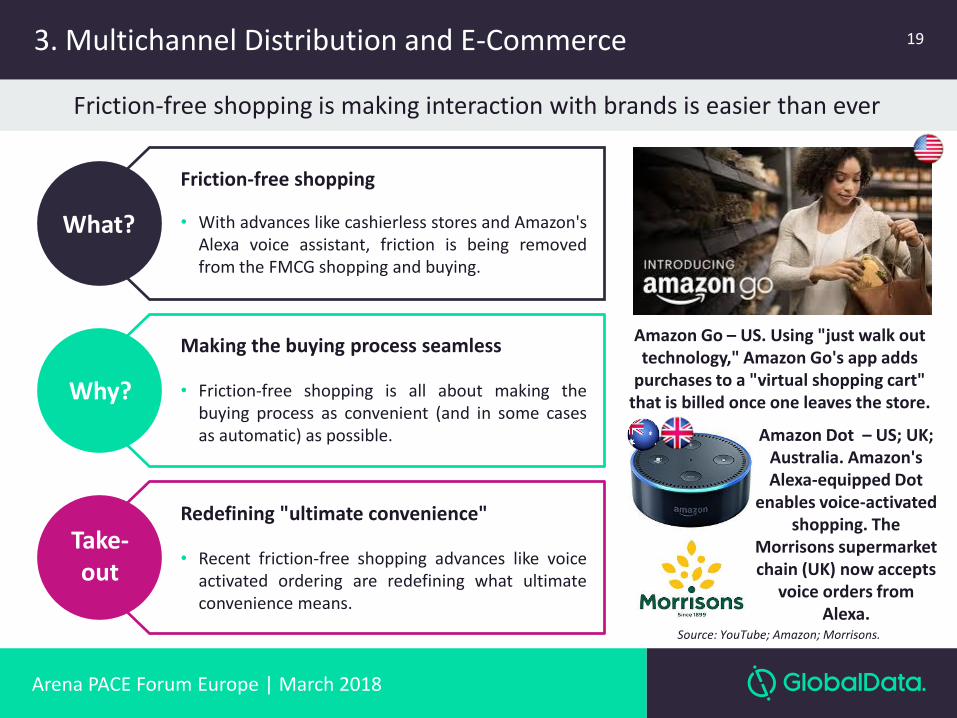

Friction-free shopping is making interaction with brands is easier than ever

What?

Why?

Take-out

Friction-free shopping

• With advances like cashierless stores and Amazon'sAlexa voice assistant, friction is being removedfrom the FMCG shopping and buying.

Making the buying process seamless

• Friction-free shopping is all about making thebuying process as convenient (and in some casesas automatic) as possible.

Redefining "ultimate convenience"

• Recent friction-free shopping advances like voiceactivated ordering are redefining what ultimateconvenience means.

Amazon Go – US. Using "just walk out technology," Amazon Go's app adds

purchases to a "virtual shopping cart" that is billed once one leaves the store.

Source: YouTube; Amazon; Morrisons.

Amazon Dot – US; UK; Australia. Amazon's Alexa-equipped Dot

enables voice-activated shopping. The

Morrisons supermarket chain (UK) now accepts

voice orders from Alexa.

3. Multichannel Distribution and E-Commerce

Arena PACE Forum Europe | March 2018

20

Rapid acceleration in developments – the future is nearly here!

What?

Why?

Take-out

Multiple and varied new technologies are leading fast, radical, and lasting change

• Big data, CRM, artificial intelligence, automation,virtual/augmented reality, smart homes, socialmedia… the list seems endless - and growing!

We are already in the new digital age

• Concept-to-market times are getting shorter whileconsumer acceptance and adoption of newtechnology is faster and more widespread.

Act now to futureproof your business

• Seek to understand and master the ever-changingdigital landscape.

• Take risks: experiment or fall behind.

One-tap ordering

Automated delivery

Smart homes and appliances

Wearable devices

3. Multichannel Distribution and E-Commerce

Arena PACE Forum Europe | March 2018

21

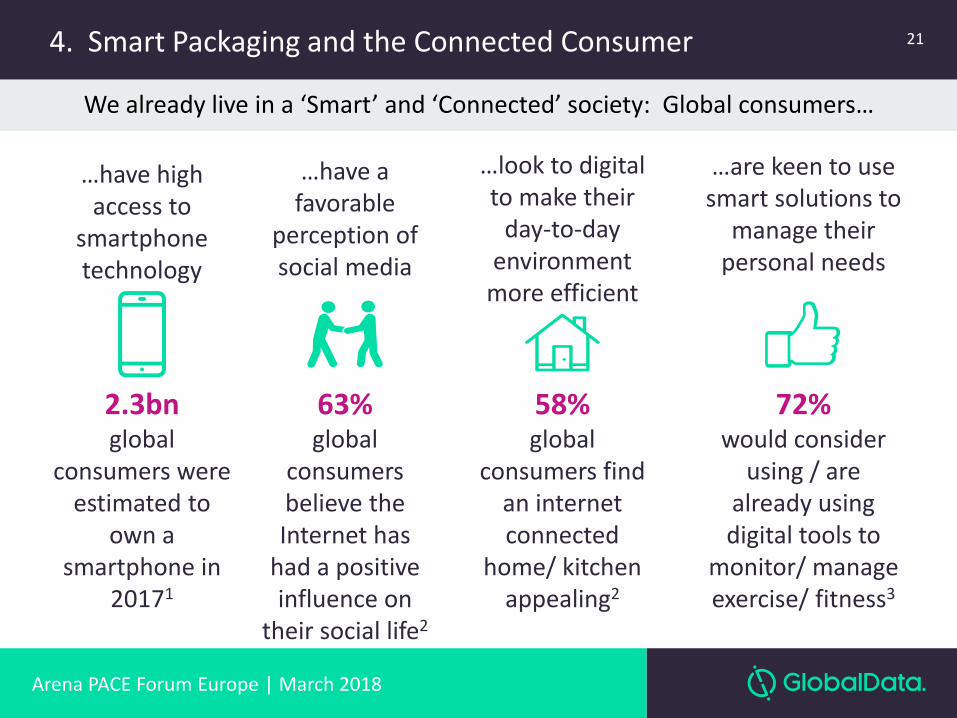

We already live in a ‘Smart’ and ‘Connected’ society: Global consumers…

…have high access to

smartphone technology

…look to digital to make their

day-to-day environment

more efficient

…have a favorable

perception of social media

…are keen to use smart solutions to

manage their personal needs

2.3bn global

consumers were estimated to

own a smartphone in

20171

63% global

consumers believe the Internet has

had a positive influence on

their social life2

58% global

consumers find an internet connected

home/ kitchen appealing2

72% would consider

using / are already using digital tools to

monitor/ manage exercise/ fitness3

4. Smart Packaging and the Connected Consumer

Arena PACE Forum Europe | March 2018

22

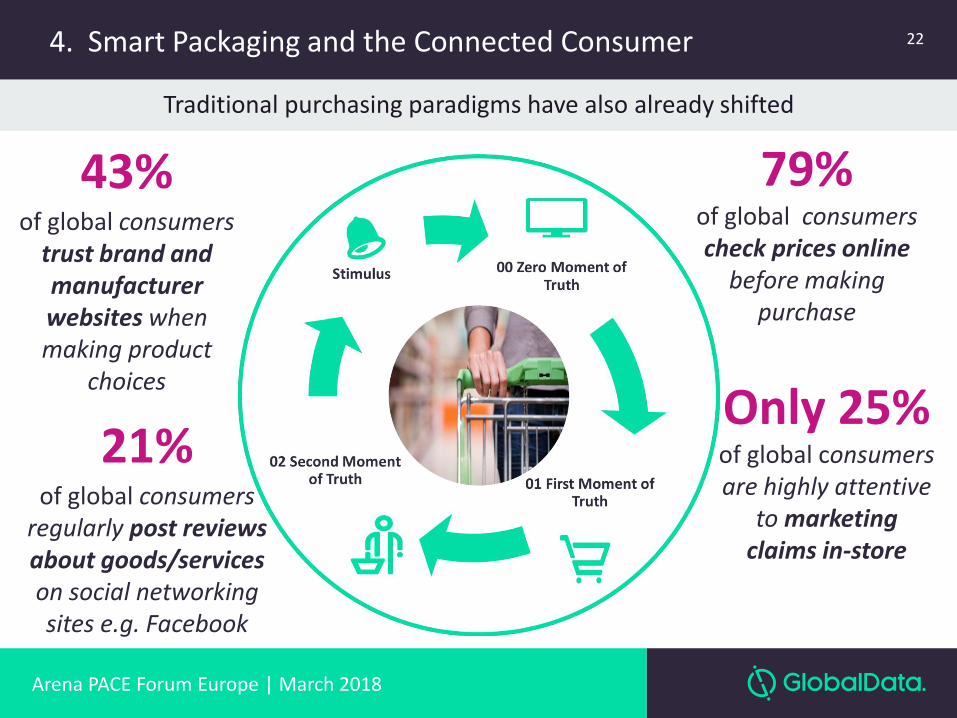

Traditional purchasing paradigms have also already shifted

79% of global consumers check prices online

before making purchase

Only 25% of global consumers are highly attentive

to marketing claims in-store

43%of global consumers

trust brand and manufacturer websites when making product

choices

21%of global consumers

regularly post reviews about goods/services on social networking sites e.g. Facebook

4. Smart Packaging and the Connected Consumer

© 2018 | Arena PACE Forum EuropeArena PACE Forum Europe | March 2018

• Explosion in Smart phone ownership means that more and more consumers are now “digitally connected” and “always on”

• Smart packaging systems have been widely used in modern distribution, warehousing and logistics for a some time

• But RFID, NFC and similar system can engage the consumer more directly but are in their infancy in consumer packaging applications

• Main current focus on high end products where brand authentication or theft protection are higher needs (wines & spirits, pharmaceuticals, cosmetic)

• However 47% of consumers find interactive packaging an “exciting” or “nice to have” packaging feature (GlobalData Survey, 2015)

• Smart Packaging systems can also be used communicate meaningful data to consumer such as Spoilage, Tamper Evidence, Temperature Change & Product Authentication

4. Smart Packaging and the Connected Consumer 23

© 2018 | Arena PACE Forum EuropeArena PACE Forum Europe | March 2018

Outlook

• The use of QR Codes, RFID, NFC. AR and printed electronics will increase as lower cost printed electronics remove current price limitations

• But it is not just these technologies – there is a huge array of related and unrelated technologies are currently at R&D stage including active and intelligent packaging systems, mass serialization, thermochromic inks, track ’n’ trace systems.

• Some fusion of technologies likely in future years as the most simple, pragmatic and cost-effective solutions emerge as winners

• Many systems are still too expensive for primary packaging applications and difficult to incorporate in high speed filling lines

• Smart Packaging can also provide a real world link to Big Data Stores and data mining facilities

• Anti –counterfeiting remains a key driver of current Smart Packaging adoption

4. Smart Packaging and the Connected Consumer 24

Arena PACE Forum Europe | March 2018

25

A complex area – need to identify where and when to play in the digital landscape

Location-Based Technology

CRM Systems Big Data Handling

Contactless Retail

Social Media Gamification Smart Appliances Virtual Reality

Influencers Wearable Technology

Voice-Activated Augmented Reality

Traditional E-Commerce Apps Smart Delivery Systems

Artificial Intelligence

Smart Labels / Packaging

In-Store Smart Tech Smart Homes

Automation 2.0

Easy

Difficult

Now Future

4. Smart Packaging and the Connected Consumer

© 2018 | Arena PACE Forum EuropeArena PACE Forum Europe | March 2018

“Selfie” Culture

• As developed markets have become more saturated, consumers increasingly looking for differentiation and individualisation

• Manifest for example in growing trend for craft beers and spirits and tailored high end premium & luxury packaging

• Difficulty is to be able to achieve this individualisation without compromising filling lines speeds

• Future of more diverse products - individually tailored but at faster filling speeds

5. Personalisation and Individualisation 26

Arena PACE Forum Europe | March 2018

27

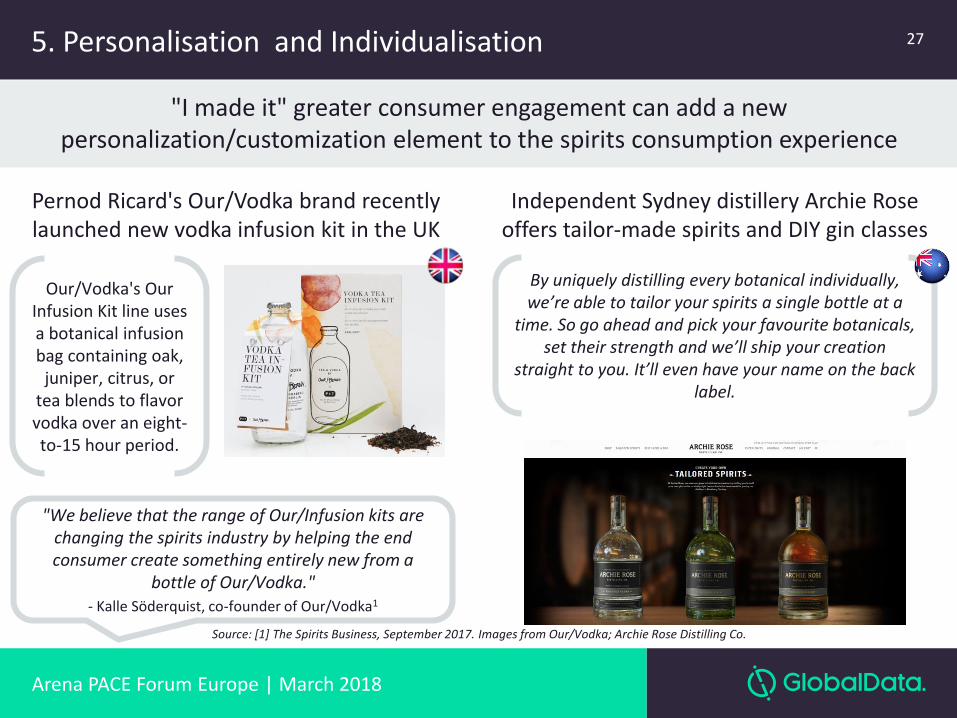

"I made it" greater consumer engagement can add a new personalization/customization element to the spirits consumption experience

Pernod Ricard's Our/Vodka brand recently launched new vodka infusion kit in the UK

Source: [1] The Spirits Business, September 2017. Images from Our/Vodka; Archie Rose Distilling Co.

Our/Vodka's Our Infusion Kit line uses a botanical infusion bag containing oak,

juniper, citrus, or tea blends to flavor vodka over an eight-to-15 hour period.

"We believe that the range of Our/Infusion kits are changing the spirits industry by helping the end consumer create something entirely new from a

bottle of Our/Vodka."- Kalle Söderquist, co-founder of Our/Vodka1

Independent Sydney distillery Archie Rose offers tailor-made spirits and DIY gin classes

By uniquely distilling every botanical individually, we’re able to tailor your spirits a single bottle at a

time. So go ahead and pick your favourite botanicals, set their strength and we’ll ship your creation

straight to you. It’ll even have your name on the back label.

5. Personalisation and Individualisation

© 2018 | Arena PACE Forum EuropeArena PACE Forum Europe | March 2018

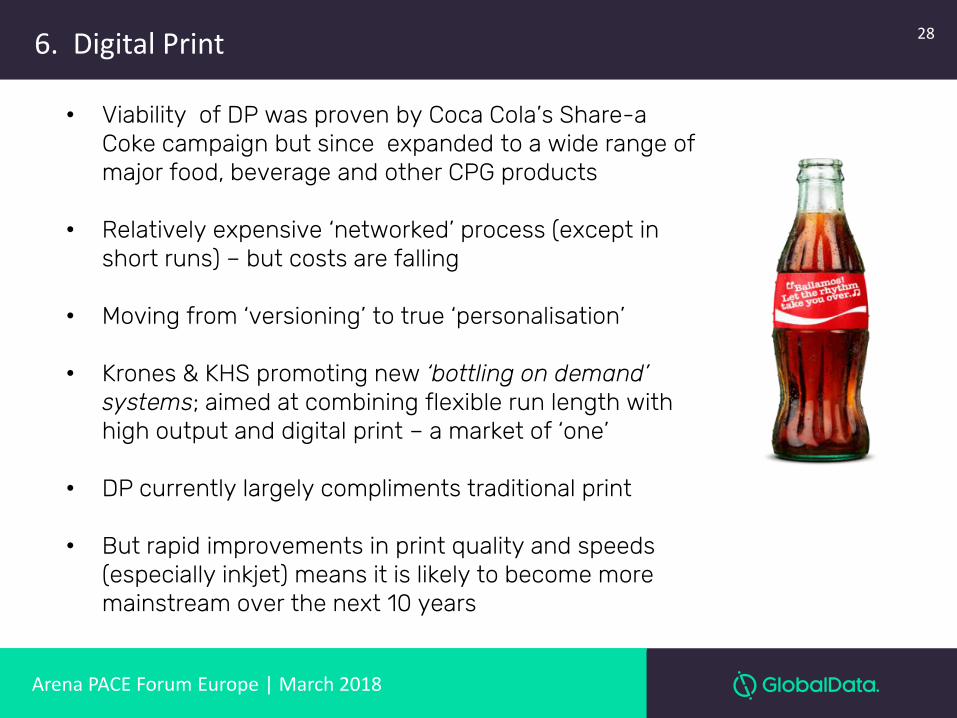

• Viability of DP was proven by Coca Cola’s Share-a Coke campaign but since expanded to a wide range of major food, beverage and other CPG products

• Relatively expensive ‘networked’ process (except in short runs) – but costs are falling

• Moving from ‘versioning’ to true ‘personalisation’

• Krones & KHS promoting new ‘bottling on demand’ systems; aimed at combining flexible run length with high output and digital print – a market of ‘one’

• DP currently largely compliments traditional print

• But rapid improvements in print quality and speeds (especially inkjet) means it is likely to become more mainstream over the next 10 years

6. Digital Print 28

© 2018 | Arena PACE Forum EuropeArena PACE Forum Europe | March 2018

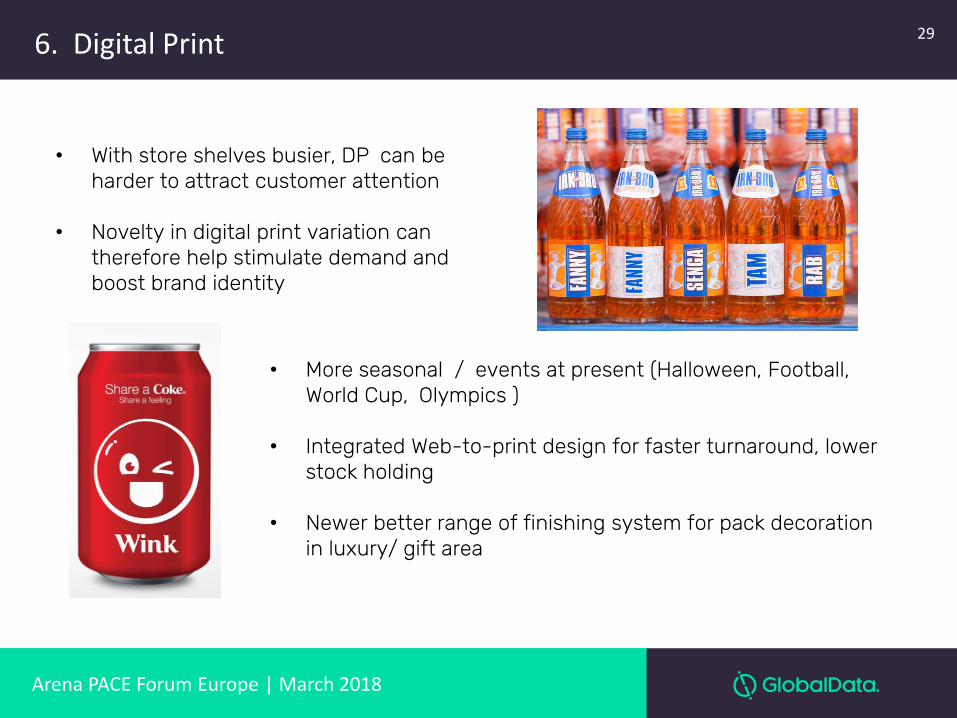

• With store shelves busier, DP can be harder to attract customer attention

• Novelty in digital print variation can therefore help stimulate demand and boost brand identity

• More seasonal / events at present (Halloween, Football, World Cup, Olympics )

• Integrated Web-to-print design for faster turnaround, lower stock holding

• Newer better range of finishing system for pack decoration in luxury/ gift area

6. Digital Print 29

© 2018 | Arena PACE Forum EuropeArena PACE Forum Europe | March 2018

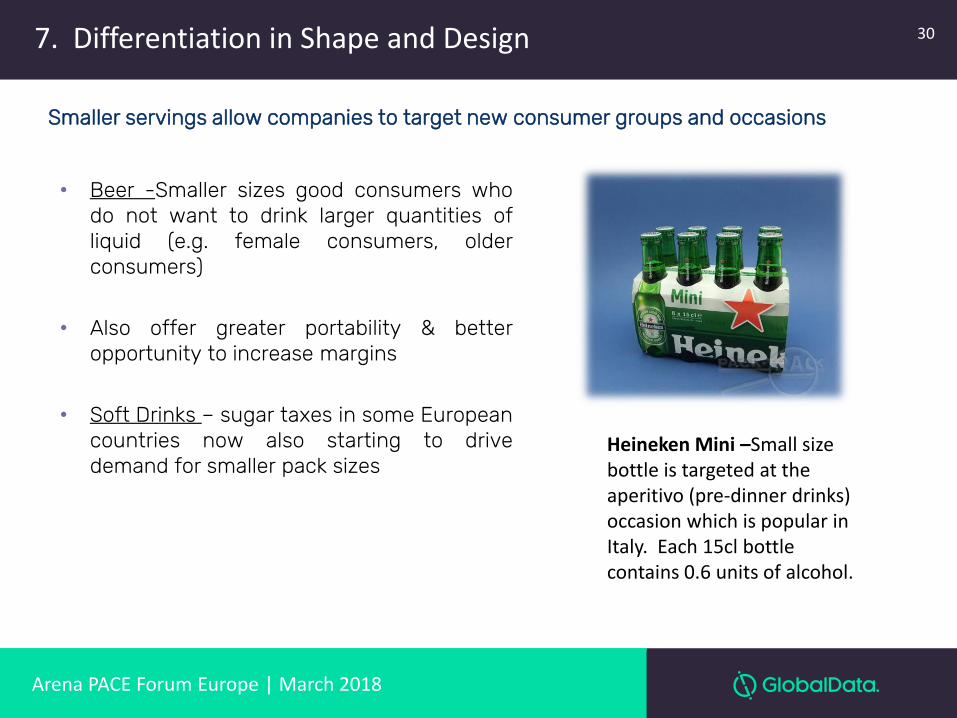

Heineken Mini –Small size bottle is targeted at the aperitivo (pre-dinner drinks) occasion which is popular in Italy. Each 15cl bottle contains 0.6 units of alcohol.

Smaller servings allow companies to target new consumer groups and occasions

• Beer -Smaller sizes good consumers whodo not want to drink larger quantities ofliquid (e.g. female consumers, olderconsumers)

• Also offer greater portability & betteropportunity to increase margins

• Soft Drinks – sugar taxes in some Europeancountries now also starting to drivedemand for smaller pack sizes

7. Differentiation in Shape and Design 30

© 2018 | Arena PACE Forum EuropeArena PACE Forum Europe | March 2018

• Unique convenience features are increasingly a key differentiator for brand identity

• The main focus in still largely on easy opening , closing, dispensing and tamper evidence system (e.g. low torque and wide-mouth closures)

• Full aperture drinks cans are rare but offer better option to drink from can

• Also a strong focus at the moment on improving closures/dispensing systems for stand-up pouches

• For food products resealable closures, lidding and zippers are also becoming more prevalent to differentiate the brand and add value

• Cash rich, time poor consumers driving demand for quick preparation ready meals and ‘on the go ‘ packaging

Convenience and On-the-Go

317. Differentiation in Shape and Design

© 2018 | Arena PACE Forum EuropeArena PACE Forum Europe | March 2018

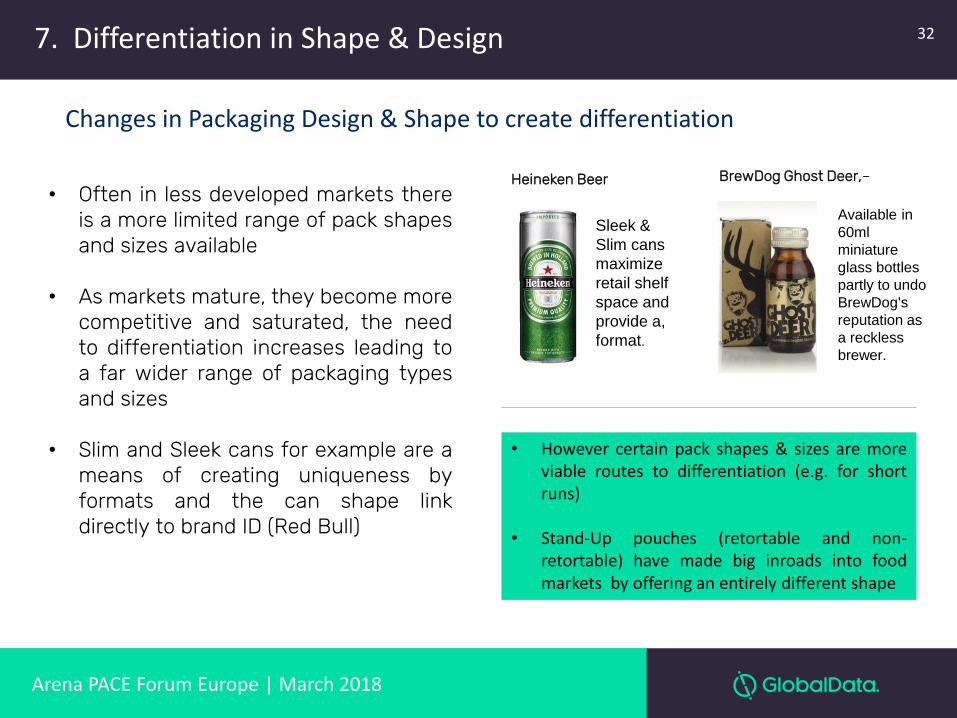

• Often in less developed markets thereis a more limited range of pack shapesand sizes available

• As markets mature, they become morecompetitive and saturated, the needto differentiation increases leading toa far wider range of packaging typesand sizes

• Slim and Sleek cans for example are ameans of creating uniqueness byformats and the can shape linkdirectly to brand ID (Red Bull)

Sleek &

Slim cans

maximize

retail shelf

space and

provide a,

format.

BrewDog Ghost Deer,–

Available in

60ml

miniature

glass bottles

partly to undo

BrewDog's

reputation as

a reckless

brewer.

Changes in Packaging Design & Shape to create differentiation

• However certain pack shapes & sizes are moreviable routes to differentiation (e.g. for shortruns)

• Stand-Up pouches (retortable and non-retortable) have made big inroads into foodmarkets by offering an entirely different shape

7. Differentiation in Shape & Design

Heineken Beer

32

Agenda

Arena PACE Forum Europe | March 2018

33

About GlobalData

Current Consumer Behavior & Packaging Trends

Conclusions - how to keep ahead

1

2

3

Arena PACE Forum Europe | March 2018

Conclusions

Traditional Retail is no longer the core driver of category or packaging growth

34

Consumer behaviours are being influenced

increasingly by rapidly changing personal and

societal changes and are less driven by traditional advertising and media

Digital lifestyles are changing consumer

behaviours –understanding the

personal and individual drivers of consumers will

be critical to future business success

In an age where digital media and online

purchasing is becoming the norm, packaging

needs to be more versatile, interactive and central to

the brand identity – a primary sales vehicle and means of communication not just a cost and means

of delivery

© 2018 | Arena PACE Forum EuropeArena PACE Forum Europe | March 2018

www.globaldata.com/consumer/

Thank you!

twitter.com/globaldata

+44 7488 599528

www.linkedin.com/company/globaldata

Further information: