internship report on sunrise bank limited

TRANSCRIPT

INTERNSHIP REPORT ON SUNRISE BANK LTD

GAIRIDHARA BRANCH

By

Rojej Shrestha

Roll no: 14450052

P.U Registration No: 2013- 2- 45-0196

A Internship Report Submitted to:

Ace Institute of Management

Pokhara University (P.U)

Submitted for the partial fulfillment of the degree of

Bachelor in Business Administration - Banking and Insurance (BBA - BI)

Date: 28th October, 2016

INTERNSHIP REPORT II

DECLARATION

This internship Report entitled “An Internship report on Sunrise Bank”, submitted by

Rojej Shrestha in partial fulfillment of the requirements for the award of BBA-BI degree

of Pokhara University submitted to Ace Institute of Management comprises only my

work due acknowledgments have been made to materials used in the report under the

supervision of Mrs Sharmila Maharjan, the Facilitator of Ace and Mr. Ram Kumar Giri,

Branch Manager, Suresh Parajuli, Prakriti Giri, Somi Malla of Sunrise Bank.

………………………….

Signature

Rojej Shrestha

Date : 28th October, 2016

INTERNSHIP REPORT III

BONAFIDE CERTIFICATE

This is to certify that this project report titled “An Internship report on Sunrise Bank

Ltd.” submitted by Rojej Shrestha for the partial fulfillment of the requirement of BBA-

BI embodies the bonafide work done by her under my supervision.

…………………………. ……………………………

Signature Signature

Sharmila Maharjan Ramesh Kumar Chauhan

Supervisor Program Director

Ace Institute of Management Ace Institute of Management

……………………………..

Signature

Name of the External Examiner:

Date:

INTERNSHIP REPORT IV

ACKNOWLEDGMENT

This report is set up under the extraordinary arrangement of the commonsense field

learning which is set up to satisfy the necessity of Bachelor in Business Administration

Banking and Insurance. This sort of work is key for any administration understudies that

give us chances to get presented to practical information and implications, giving

ongoing critical thinking circumstances. I might want to thank our school colleague for

their support and encrouagement.

A genuine thank to our venture counsel Mrs.Sharmila Maharjan for her valuable direction

and eagerness in readiness of this temporary position report and my field boss Ms.

Prakriti Giri, Mr. Suresh Parajuli, Ms. Somi Malla.

Further, I would like to express my sincere thanks to Pokhara University and Ace

Institute of Management, for providing the opportunity of internship.

Lastly, I would like to thank all other supervisors and senior interns, who guided me

throughout the internship program in SBL. The guidances that I received, helped me to

perform my best and learn things that will surely prove to be helpful in my career.

INTERNSHIP REPORT V

LIST OF ABBREVIATION

SBL SUNRISE BANK LIMITED

NRB NEPAL RASTRA BANK

CRD CREDIT DEPARTMENT

CAP CREDIT APPROVAL PACKAGE

CFOL CREDIT FACILITIY OFFER LETTER

ATM AUTOMATED TELLER MACHINE

LC LETTER OD CREDIT

CSD CUSTOMER SERVICE DEPARTMENT

SCT SMART CHOICE TECHNOLOGY

INTERNSHIP REPORT VI

Contents

CHAPTER I ........................................................................................................................ 1

ORGANIZATION PROFILE ............................................................................................. 1

1.1 Introduction ............................................................................................................... 1

1.2 Organization’s Missions and Objectives ................................................................... 2

1.3Major Markets and Customers: .................................................................................. 2

1.4 Product and Services ................................................................................................. 3

1.4.1 Deposits .............................................................................................................. 3

1.4.2 Loan .................................................................................................................... 5

1.4.3 Suryodaya Remit ................................................................................................ 6

1.4.4 Locker ................................................................................................................. 6

1.4.5 Branchless banking ............................................................................................. 6

1.4.6 Internet banking ............................................................................................ 7

1.4.7 Mobile banking ................................................................................................... 7

1.4.8 Extension counter ............................................................................................... 7

1.5 Board of Directors ..................................................................................................... 8

1.7 Capital Strucutre ........................................................................................................ 9

1.9 Deposits ..................................................................................................................... 9

1.9.1 Expenses ........................................................................................................... 10

1.9.2 Organizational Performance ............................................................................. 12

CHAPTER 2 ..................................................................................................................... 14

JOB PROFILE AND ACTIVITIES PERFORMED......................................................... 14

2.1 Activities performed in the organization:................................................................ 14

2.2 Learnings: ................................................................................................................ 14

2.3 Major activities:....................................................................................................... 15

INTERNSHIP REPORT VII

2.3.1 Customer Handling ........................................................................................... 15

2.3.2 Credit Approval Package, CFOL...................................................................... 15

2.3.3 Collateral Site Visit .......................................................................................... 15

2.3.4 Credit Documents Handling ............................................................................. 15

2.3.4 Document Uploading on Bank Server .............................................................. 16

2.3.5 T24 Software .................................................................................................... 16

2.4 Problem solved: ....................................................................................................... 16

2.5 Interns key observation: .......................................................................................... 17

CHAPTER 3 ..................................................................................................................... 18

LESSON LEARNT AND FEEDBACK ........................................................................... 18

3.1 Key skills and attitude learnt: ............................................................................. 18

3.2 Feedback to the organization: ............................................................................ 18

3.3 Feedback to the college: ..................................................................................... 19

ANNEXES ........................................................................................................................ IX

INTERNSHIP REPORT VIII

LIST OF TABLE

Table 1 Fixed Deposit Schedule ......................................................................................... 4

Table 2 Capital Structure .................................................................................................... 9

Table 3. product and services ........................................................................................... XII

INTERNSHIP REPORT IX

LIST OF FIGURES

Figure 1 Board of Directors ................................................................................................ 8

Figure 2 Comparison between the deposits of present and last fiscal year ...................... 10

Figure 3 Expenses of the Bank ......................................................................................... 11

Figure 4: Balanced Scorecard ........................................................................................... 12

INTERNSHIP REPORT 1

CHAPTER I

ORGANIZATION PROFILE

1.1 Introduction

A bank is a financial institution that primarily accepts deposits and creates credit. Banks

also provide financial services, such as wealth management, foreign currency exchange

and safe deposit lockers. There are two types of banks: Commercial Banks and

Investment Banks. Generally, Banks are regulated by the national government or central

bank.

The major objectives of Central Banks are Currency Stability, Inflation control and

Monetary policy and control of money supply in an economy. Some of the world’s major

central banks are U.S Federal Reserve Bank, the European Central Bank, the bank of

England, and the bank of japan the Swiss National Bank and the people’s Bank of China.

In an economy driven by appetite for success, Sunrise Bank Limited is "Rising to Serve"

by defining new levels of services and products. As a bank founded by reputed

entrepreneurs, they understand the needs of a growing economy and are well equipped to

serve.

Their team of seasoned banking and management professionals has dedicated themselves

to establishing an institution determined to cater to the needs of all, be it big or small. Our

aspirations are their benchmarks and we will always be "Rising to serve".

Sunrise Bank Nepal Ltd. provides personal and business banking products and services.

Its personal banking products and services include savings deposits, fixed deposits, and

loans; and business banking products and services include loans and advances, demand

loans, fixed term loans, import loans, overdraft loans, short term pledge loans, export

financing, hire purchase, deprived sector loans, SME loans, loan against bank guarantee,

loan against government bonds, loan against shares, loan against fixed deposits of other

banks, consortium loans, and gold loans. The company also provides locker, Internet

banking, remit, and mobile banking services, as well as Visa debit cards.

INTERNSHIP REPORT 2

1.2 Organization’s Missions and Objectives

Sunrise bank visions to “you and us …..Together we built”. And missions to Establish

Sunrise bank as a lead bank in all places of their branch location national wide.

Objectives of Sunrise Bank Ltd:

To continuously expand Bank's operation in systematic manner,

To become a major innovative Bank and provide top of the line services,

To build an HR team that continuously supplements the growth of the

organization,

To be vigilant to the evolving economy and align our operations accordingly.

1.3Major Markets and Customers:

Sunrise Bank Ltd. is an “A” class commercial bank classified by Central Bank of Nepal.

Sunrise Bank has been able to expand its services through establishment of branches

throughout the country. People of Nepal from various geographic regions are able to

purchase the products and use the services provided by the bank. The market for the bank

is widespread over the places of Nepal.

As per bank they say the bank understand that banking is no longer a numbers game.

“success” for us is not just a margin. We understand that you are looking for a friend. A

friend to understand, evaluate and invest in your dreams and aspirations. A friend who

will safe guard your savings and give you the best value for it. For us success is your

hand in friendship.

I was deployed in Credit Department of Main Branch. It is one of the most important

department of a bank that generates the major source of income for bank i.e. Interest

Income. The Credit Department of Main Branch provides different loan products not less

than NRs. 5.00 Lakhs. It has large customer base and good position of Credit portfolio.

People purchase different loan products such as SME Loan (Small Medium Enterprises),

Overdraft, Margin Lending and so on. Sunrise Bank Ltd has large customer base from

low income to high income earning people.

INTERNSHIP REPORT 3

1.4 Product and Services

SBL generates significant revenues through credit creation and the funds from deposits

are used for credit creation. As such, the major products of SBL are

Deposits

Loans and Advances

Along with these products, other services that significantly contribute for SBL’s revenue

generation and customer retention include:

Suryodaya Remit

Locker

Branchless Banking

Internet Banking

Mobile Banking

Sunrise Visa Debit Card

Extension Counter

1.4.1 Deposits

Deposits are the major sources of fund in SBL. Deposit is the amount placed by

individuals and corporate groups in the bank for safekeeping and is subject to

withdrawal on the demand of the depositor or at the time of maturity of stated period.

Deposits are the major liability for any banks and in case of liquidation, deposits are

settled first and foremost. Deposits are facilitated through variety of accounts and

they are:

a) Fixed Account

A fixed account requires the depositor to deposit a fixed sum of money for a fixed

period of time. A penal interest is charged in case of withdrawal of fixed deposit

prior maturity. The interest is paid on quarterly basis. Fixed account can be

opened by individuals, minors, clubs, societies, associations and trusts.

INTERNSHIP REPORT 4

TIME Interest Rate

Individual

6 Months 4.00%

1 Year 5.00%

18 Months and above 5.25%

Corporate

1 year 4.00%

18 months and above 4.25%

Interest payable on quarterly basis*

Table 1 Fixed Deposit Schedule

b) Saving Account

A saving account is an interest bearing account. In SBL, interest is calculated on

daily balance and credited to the account on quarterly basis. The minimum

balance for saving account depends on the nature of saving account. Such balance

is subject to any incidental charges that SBL specifies during the period. To keep

the records of savings and transactions as well as to be updated with the status of

the account, a passbook is provided to the depositor. The types of saving account

in SBL are:

Normal Savings

Sunrise Payroll Savings

Sunrise Fat Savings

Sunrise Exclusive Bachat

Sunrise Bal Bachat

Sunrise Share Dhani

Sunrise Pink Bachat

Sunrise Remit Bachat

USD/GBP Saving

INTERNSHIP REPORT 5

Sunrise Senior Citizen

Sunrise Super Savings

Sunrise Krishi Karja Saving

Sunrise Disability Saving

Sunrise Share Lagani Khata

Sunrise Bisesh Bachat

Euro Saving Account

c) Current Account

A current account is non-interest bearing account. Only the corporate bodies can

open a current account. It is especially designed for corporate bodies that are

indulged in frequent transactions. SBL provides the current account holder with

cheque book. A semiannual statement is sent to keep track of the transactions

carried out by the account holder. Additionally, the bank may provide the

statement daily, weekly or monthly as per the request made.

1.4.2 Loan

SBL provides wide range of loan products for both individual and corporate. It is the

major source for income earning of the bank. Dome of the loan products are

a) Sunrise Ghar Karja

This loan is basically focused for those who dreams to own their home. The

interest are highly competitive. The interest rate ranges from 8.50% to 13%.

b) Sunrise Sajilo Karja

Sunrise Sajilo Karja can be disbursed for social, personal, business purposes.

This flexible loan allows the borrower to fulfill all personal financial

requirements. We offer loans in line with the clients' repayment capacity and

the usage of the loan.

c) Term Loan

INTERNSHIP REPORT 6

d) Sunrise Surakshit Ghar Karja

A home loan product tied up with endowment life insurance policy--this is

a unique loan product being offered to the customers for the first time in the

Nepalese banking sector. The loan limit ranges from 0.5 million to 10 Million.

Under this scheme, each borrower will have life insurance policy commensurate

with the loan amount and tenure of the house loan. Insurance company will pay

full loan amount to the bank on behalf of the borrower within the loan tenure.

Therefore the borrower will bear say interest portion only making the EMI

significantly lower than in normal home loan.

1.4.3 Suryodaya Remit

It is an electronic online cash exchange result of the bank intended to encourage

exchange of assets by Nepalese exiles working/living in remote nations and in

addition for residential exchange of assets. Suryodaya transmit is secured by

method for VeriSign and computerized authentications mapped to every client

independently. It is quick, moderate and secure.

1.4.4 Locker

Sunrise Safe Deposit Locker is facility furnished to the individual and

institutional customers who prefer to safe deposit precious gems & jewelries and

important documents to evade the probability of increasing theft, burglary and

fire. The Safe Deposit Locker has been the first choice for the safest custody of

the valuable goods with flexibility of time to store and take away when required.

The Bank has varied sizes of Safe Deposit Locker to select from. Lockers facility

can be availed from selective Branches of the Bank.

1.4.5 Branchless banking

Branchless saving money is a practical channel for conveying budgetary

administrations without depending on the customary bank branches. Branchless

managing an account gives essential keeping money benefits through NIBL

specialists having Bio-metric POS devices(with unique mark scanner).

INTERNSHIP REPORT 7

1.4.6 Internet banking

Web based keeping money otherwise called web saving money e-managing an

account or virtual banking, E-saving money or virtual saving money, is an

electronic installment framework that empowers clients of bank or other monetary

organization to lead a scope of budgetary exchanges through the monetary

institution’s site.

1.4.7 Mobile banking

Mobile banking is a service provided by a bank or other financial institution that

allows its customers to conduct a range of financial transactions remotely using a

mobile device such as a mobile phone or tablet, and using software usually called

an app, provided by the financial instutions for the purpose. Mobile banking is

usually available on 24hour basis.some financial institutions have restrictions on

which accounts may be accessed through mobile banking as well as a limit on the

amount that can be transacted

1.4.8 Extension counter

There are no inflexible rules, but banks for the most part open augmentation

counters in spots like colleges, large government or private foundations and so on

with the end goal of conveying fundamental saving money administrations at their

doorstep, even however opening a branch may not be a feasible proposition.

Therefore, the expansion counters would by and large capacity from littler

premises and with less number of representatives, for rendering just essential

keeping money services.so, as a rule the accompanying administrations for the

most part would not be accessible:

o Credit Products

o Safe Deposit Lockers

o Foreign exchange services etc.

INTERNSHIP REPORT 8

1.5 Board of Directors

Figure 1 Board of Directors

The Board of Directors consists of 9 members. As per the directives of NRB, there are 3

Public Directors and 6 Director. Mr. Motilal Dugar is the chairman of SBL.

CHAIRMAN

(Mr. Motilal Dugar)

DIRECTOR

(Mr. Malchand

Dugar)

DIRECTOR

(Mr. Bachh Raj Tater)

DIRECTOR

(Mr. Motilal Dugar)

DIRECTOR

(Dr. Bhogendra Guragain)

DIRECTOR

(Mr. R.K. Manandhar)

PUBLIC DIRECTOR

(Mr. Deepak Pd,

Bhattarai

PUBLIC DIRECTOR

(Mr. Deepak Nepal)

PUBLIC DIRECTOR(Mr. Jyoti

Kumar Begani)

INTERNSHIP REPORT 9

1.7 Capital Strucutre

AUTHORIZED CAPITAL 5 BILLION

PAID UP CAPITAL 3.98 BILLION

Table 2 Capital Structure

At present, the authorized share capital of SBL is NRs. 5.00 Billion whereas the paid-up

capital is 3.98 Billion. 51% of paid-up capital is held by promoter shares whereas 49% is

held by public shares. The pie-chart diagram is presented in Annexes.

As per the directives of NRB, every “A” Class commercial bank must maintain its paid-

up capital to NRs. 8.00 Billion by fiscal year 2073/74. SBL has its capital plan to reach

the directive through the merger and issuance of rights and bonus shares.

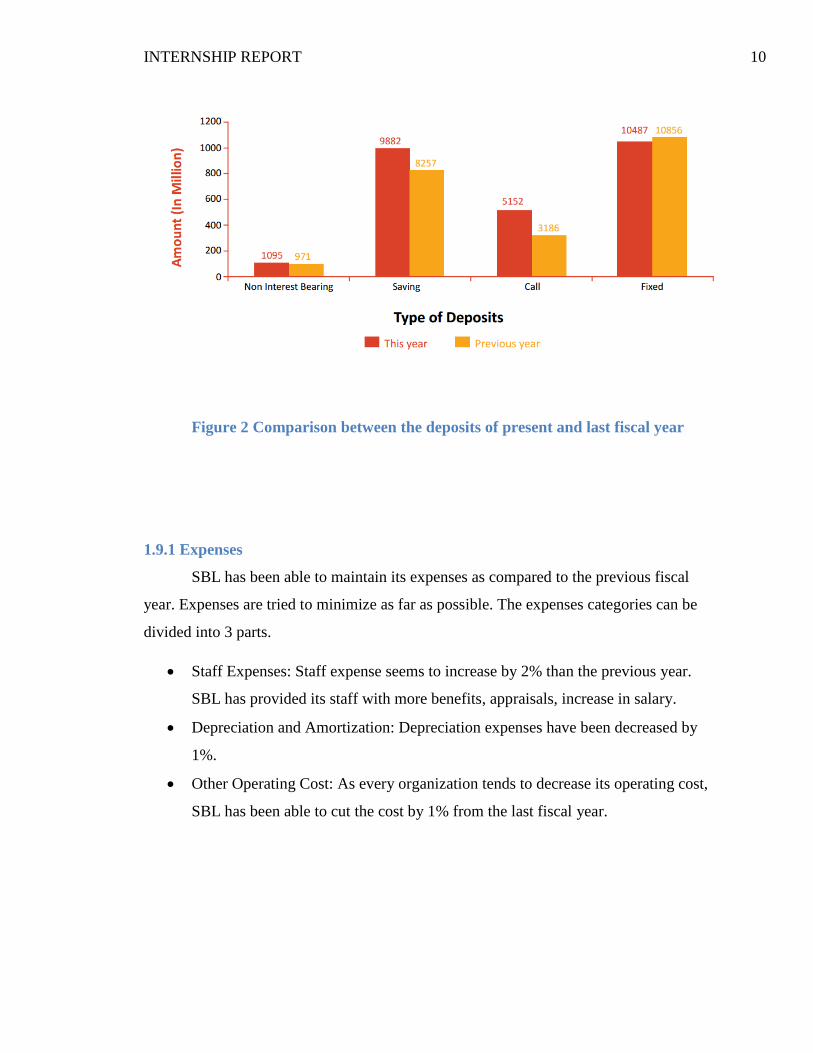

1.9 Deposits

At the mid July 2014, the deposit of Sunrise Bank Ltd. increased by 14% and reached Rs

26.2 Billion. The bank has offered need to low enthusiasm bearing stores as opposed to

the high enthusiasm bearing deposits.Hence,the add up to altered stores diminished by

3% to NPR 10.48 billion while the aggregate sparing Deposits of the bank expanded by

20% to NPR 9.88 billion. The interest bearing accounts have increased by 13% while the

total deposits have increased by 14%

The following bar-diagram shows the changes in deposits at the end of the fiscal year

2013/14.

INTERNSHIP REPORT 10

Figure 2 Comparison between the deposits of present and last fiscal year

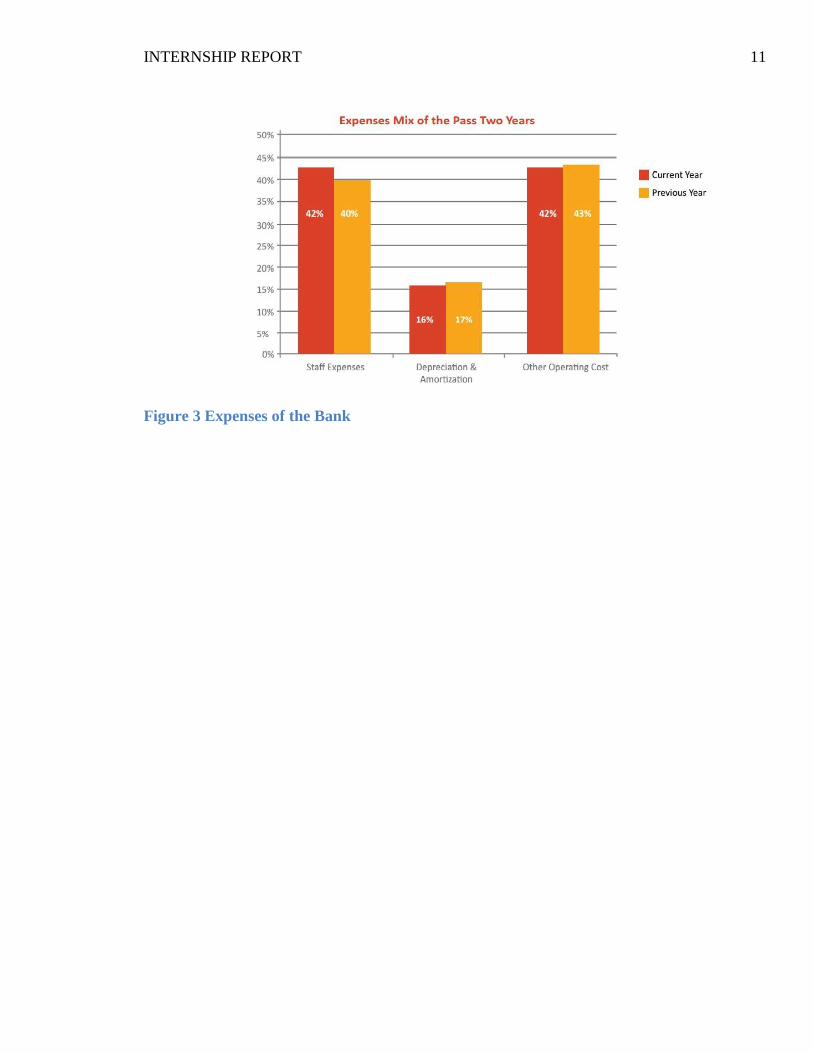

1.9.1 Expenses

SBL has been able to maintain its expenses as compared to the previous fiscal

year. Expenses are tried to minimize as far as possible. The expenses categories can be

divided into 3 parts.

Staff Expenses: Staff expense seems to increase by 2% than the previous year.

SBL has provided its staff with more benefits, appraisals, increase in salary.

Depreciation and Amortization: Depreciation expenses have been decreased by

1%.

Other Operating Cost: As every organization tends to decrease its operating cost,

SBL has been able to cut the cost by 1% from the last fiscal year.

INTERNSHIP REPORT 11

Figure 3 Expenses of the Bank

INTERNSHIP REPORT 12

1.9.2 Organizational Performance

SBL has been able to perform the best organizational performances. It has been earning

profit in increasing trend. SBL focuses on its customer by launching various flexible

products. . The job responsibilities for each designation are clearly described so that the

employees clearly understand their responsibilities and accountabilities. SBL focuses on

job rotation and job enrichment to reduce the monotony.

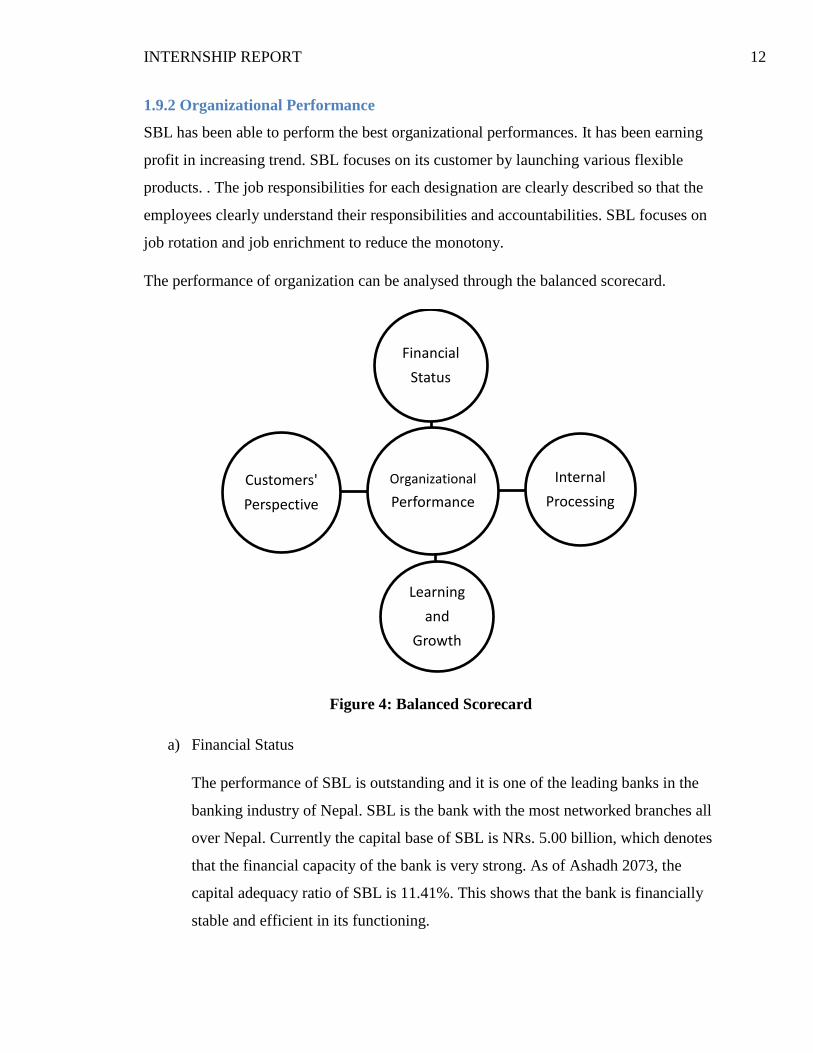

The performance of organization can be analysed through the balanced scorecard.

Figure 4: Balanced Scorecard

a) Financial Status

The performance of SBL is outstanding and it is one of the leading banks in the

banking industry of Nepal. SBL is the bank with the most networked branches all

over Nepal. Currently the capital base of SBL is NRs. 5.00 billion, which denotes

that the financial capacity of the bank is very strong. As of Ashadh 2073, the

capital adequacy ratio of SBL is 11.41%. This shows that the bank is financially

stable and efficient in its functioning.

Organizational

Performance

Financial

Status

Internal

Processing

Learning

and

Growth

Customers'

Perspective

INTERNSHIP REPORT 13

b) Customer Perspective

Creation of customer satisfaction and customer delight is of utmost importance

for SBL. It deals with various natures of customers ranging from individuals to

corporate groups. SBL continually comes up with various customized products

that are tailored as per the need of the customers. For an instance, earthquake

relief loan for earthquake victims at 2% interest rate, women’s saving account

with various discount schemes, etc. However, according to the customers, there is

more scope for improvement in the service provided by SBL.

c) Internal Processing

The processes of SBL are systematized for better services and effectiveness of the

bank. Every member of the bank knows his/her responsibility and duties toward

the organization as the responsibilities and authority to each designation is clearly

spelled. The channel for flow of information is also clear. With effective

communication and clear lines of authority, the internal processing is free from

mismanagement.

d) Learning and Growth

SBL strongly focuses on strengthening the potential of its employees. It has a

continuous learning culture for every employee. The employees are rotated in

their jobs with the purpose of providing better understanding of the impact and

contribution of every activity carried out in the bank. It also makes the employees

more cooperative and understanding of each other which promotes their bonding.

SBL also enriches the job by attaching several responsibilities to a single job

designation. This helps the employees to develop the skills of multitasking. To

develop the competencies among the employees and improve their productivity,

SBL provides its employees with numerous training opportunities related to their

field. This makes them ready and confident for their job responsibilities.

INTERNSHIP REPORT 14

CHAPTER 2

JOB PROFILE AND ACTIVITIES PERFORMED

My Internship tenure in Sunrise Bank Ltd. was of 7 weeks in Main Branch, Gairidhara. I

got the wonderful opportunity to work in Credit Department. Through this department, I

was able to acquire the very essential banking knowledge as I want to see myself as a

banker in future. I primarily learned the Credit products such as Loan, Overdraft,

LC/Guarantee etc. In my tenure, I was able to deal with customers and disseminate the

information to them. Not only Credit related tasks, I was able to gain knowledge about all

the other banking task.

2.1 Activities performed in the organization:

During 7 weeks of my internship tenure, I was deployed in Credit Department. CRD is

one of the most important and essential department for each and every bank as it

generates the major income source for a bank i.e. interest income. As the main branch

and the head corporate office are in same building, I got the opportunity to watch the

coordination between the branch and the corporate office. SBL has its tradition to

celebrate their staffs birthday, “Daar” Party and so on. The activities I performed within

7 weeks were based on my acquired knowledge and intuition. It allowed me to relate my

studies in the practical working environment.

2.2 Learnings:

Coordination and respect among staffs.

Listen and understand the customers.

Two-way communication is very vital.

Dealing with the customer through psycho-analysis

Brain Storming and Team Work.

Positive Organizational Behavior.

Motivation and Self motivational techniques.

Decision making, cognitive learning.

Following and respecting the work ethics.

INTERNSHIP REPORT 15

2.3 Major activities:

I was very thankful that I got the opportunity to work in Credit Department. In Credit

Department there are lots of paper work involved. It has very well managed system to

record the documents in a specific procedure. Documents were recorded in printed as

well as in digital format.

2.3.1 Customer Handling

CRD department is the first place where a potential customer approaches to the

bank. It is the primary duty and responsibility of the bank to provide the information of

availing credit products and their interest rates. As the first thing I learnt was different

types of loans and credit facilities, I provided necessary information about the products

and I often provided the essential suggestions as per my capacity to the customer.

2.3.2 Credit Approval Package, CFOL

CAP is the most important document prepared in CRD. It consist all the analysis

and customer’s background, credit history, proposed terms and condition, interest rates. I

was very fortunate learn how to prepare them. I assisted my immediate supervisor to

prepare CAP. I was also given the responsibility to coordinate with the Branch Manager

and report if any extra essential comments.

I also learnt to prepare CFOL (Credit Facility Offer Letter). However, I was no

the authorize concern to prepare CFOL, I was able to prepare it by the end of my

internship tenure.

2.3.3 Collateral Site Visit

For any kind of loans, collateral is a very important part as it is the best way to

cover the bad debts. I was provided the opportunity to visit the collateral site property by

my supervisors. I learnt what things look for, genuinity of the customer, feasible analysis.

I also assisted my supervisor to prepare CSVR (Collateral Site Visit Report).

2.3.4 Credit Documents Handling

In Credit Department, there are lots of paperwork. Documents can be classified as

Credit, Legal and Approval/Recommendation documents. While handling these

INTERNSHIP REPORT 16

documents, I enjoyed learning the new terms, technical words and so on. I learnt to scan

the documents, print them and Xerox them.

2.3.4 Document Uploading on Bank Server

Banks keep their documents in both printed and in digital form. There are

procedures to upload the documents into the bank server. I was very thankful to use such

technology in organizational work settings.

2.3.5 T24 Software

However, I was no fully authorized to operate it. I learnt to use T-24 banking

Software, the latest of its kind. Generally, I had to use it for balance inquiry and bank

statement of customers.

2.4 Problem solved:

Working in SBL, I was exposed to real life experience as a professional. As an intern, I

was given responsibilities with expectations of better performance. I learnt many things

as I tackled with the tasks I undertook. During my internship tenure, I performed my best

and solved problems such as:

Provided necessary information to the customer when confused.

Managed the paperwork load of the department.

Help Relationship Managers and Branch Manager to correct communication

error.

Report the complaints and messages of customer to the concerned authority.

Assisted Relationship Managers to clarify the related issues.

Provided the knowledge I acquired from college to the bank which may increase

the efficiency. For example: Use of Google Drive or Cloud Servers.

Assisted filling up the different forms, especially to those who could not read and

write.

Gave feedbacks to supervisors.

INTERNSHIP REPORT 17

2.5 Interns key observation:

There were numerous things I observed as an intern while working at sunrise commercial

bank which I otherwise would not have known. As I select bank for my intern the most

things I observe are the processes of the banking the functions which are as follow:

Interns must be assigned with the responsibility as per their potentialities.

The coordination between the staffs are good but still needs to smoothen it from

time to time.

Theoretical knowledge is equally important as every works and tasks needs

theoretical base.

Branch Manager regularly inspects the staff, listen to their problems, supervises

etc.

The employees of SBL are friendly and equally helpful. They do not disturb or

irritate if the work load is heavy.

In credit department, Relationship Officers brainstorms, discuss and solves the

problem as we had studied in Principle of Management and Organizational

Behaviour.

The technology has become old and is slower which slows down the processes.

This also results in slower delivery of service to the customers.

Every employee was given certain duties for which they could be held

accountable. As such, there was defined authority and responsibility.

Flexible Lunch hours so that the branch is not empty.

Failure in effective communication makes customer angry.

Celebration of birthday parties and farewell parties.

On-the-job training and Job rotation are more focused to reduce the monotony.

INTERNSHIP REPORT 18

CHAPTER 3

LESSON LEARNT AND FEEDBACK

3.1 Key skills and attitude learnt:

An internship is an opportunity offered by employers, both in the non-profit and for-

profit sectors, to students interested in the industry. An intern works at the company for a

fixed period of time, usually three to six months. Some students will have a part-time

internship, where they work at the office for just a few days or hours a week. Others will

have full-time internships, meaning they work the same hours as the company's full-time

employees. At SBL, my internship tenure of 7 weeks provided me the wonderful

opportunities to know about the professional banking world. I knew what is to work in

organizational work settings.

Reality of professional organizational settings.

Importance of punctuality and completion of tasks.

Responsibilities.

Importance of team work that helps to solve problems.

Deal with customers in polite and friendly way.

About banking system and corporate work culture.

Laws and directives of regulatory body i.e. NRB.

3.2 Feedback to the organization:

As the organization is categorized in class A bank and is running smoothly some points I

would like to state as feedback are as follows:

Flexibility in Products: However, SBL has been able to launch products

according to the time. More flexibility is to be brought up. This will help

customers to utilize the product to the fullest.

Advertisement: SBL must consider the latest media of advertisement. Use of

social networking sites such as Facebook, Instagram, and Twitter etc must be

boosted. Customer’s query must be replied instantly in Facebook pages.

Maintain good PR: Sunrise Bank ought to focus on the advertising and ought to

make a symphonious association with the clients. Media is the essential weapon

INTERNSHIP REPORT 19

for a wide range of publicizing and organization ought to keep a nearby tie with

the business.

The staffs whose job role requires frequent contacts with the customers should be

trained to deal in a patient and polite manner.

The willingness to work should be developed among the employees through

effective incentive plans

The technologies should be updated as the existing technologies are slowing the

processes.

3.3 Feedback to the college:

The school ought to give the essential information about every one of the divisions, its

extension, and so forth. Prior to the temporary position so that the understudies would

think that its simple to choose the association where they might want to assistant. The day

and age for searching for the entry level position was too short for legitimate assessment

of decisions.

Understudies needed to pick the less good alternative because of time limitations.

The 6/8 weeks’ time span for temporary position is insufficient for an understudy.

It would have been exceptional if the related University and College can give

such temporary job program in the last semester of BBA-BI educational modules

with legitimate introduction program.

Appropriate directing to the understudies amid their entry level position ought to

be given so that the understudies would know whether whatever they have been

learning at their work coordinate their temporary job targets or not.

The college ought to consider making school time adaptable for understudies after

the Internship is over in light of the fact that working and increasing pragmatic

learning is similarly essential as hypothetical information.

Inspite of all I would like to thank to Pokhara University and Ace establishment

of Management, for giving such mind blowing course structure, extremely ace

indicating teachers, and better school environment and giving such passage level

position undertakings to get the learning of organization understudies.

INTERNSHIP REPORT VIII

REFERENCE

Annual Report of 2071/2072

http://wwww.sunrisebank.com.np/

INTERNSHIP REPORT IX

ANNEXES

Figure 3.Organizational Structure

INTERNSHIP REPORT X

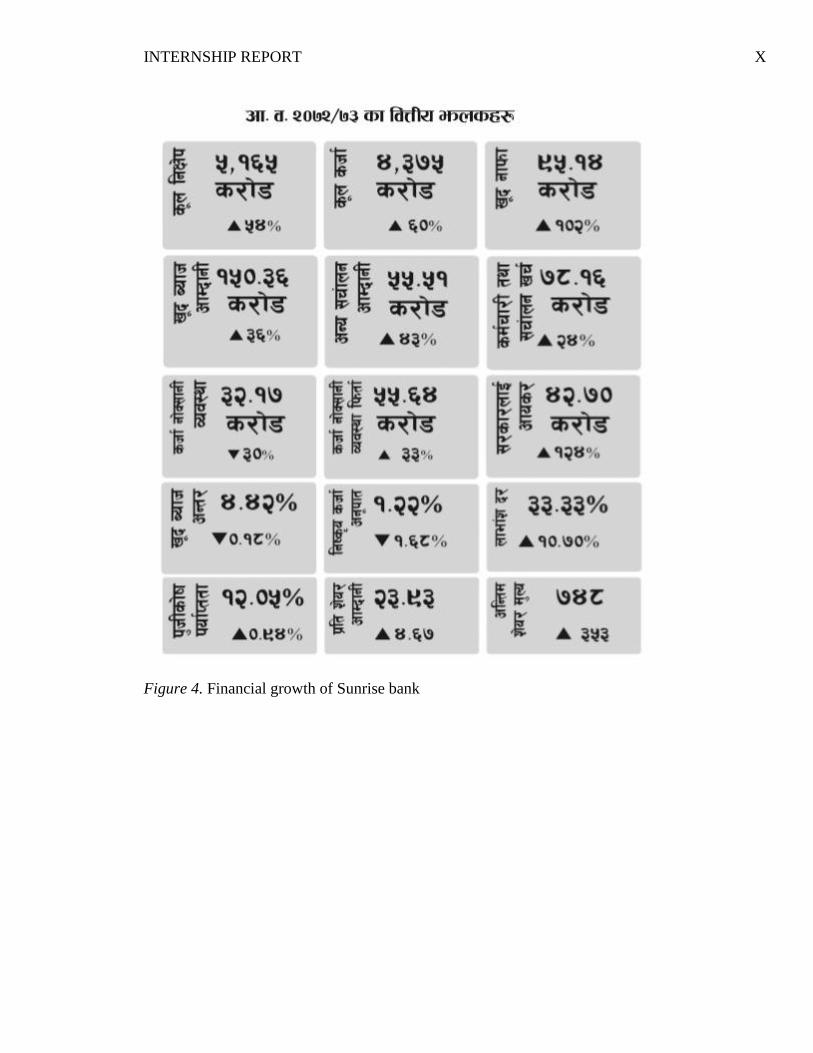

Figure 4. Financial growth of Sunrise bank

INTERNSHIP REPORT XI

Figure 5. Analysis Of Bank’s Progress

INTERNSHIP REPORT XII

NORMAL SAVINGS

Minimum Balance-NRs. 0.00

Interest Scheme: Monthly Minimum

Balance

Current Interest Rate: 6.50 % p.a.

SUNRISE BAL BACHAT KOSH

Minimum Balance

Up to NRs 25,000.00 (5% p.a)

NRs 25,001.00 to NRs

100,000.00 (5.25% p.a)

NRs.100,001.00 to NRs.

200,000.00 (6.00% p.a)

Above NRs 200,001.00 (6.50%

p.a)

USD SAVINGS ACCOUNT

Minimum Balance: USD 10.00

Interest Rate: 0.25%

SUNRISE SUPER SAVING

Minimum Balance-NRs. 10,000.00

Interest Scheme: Daily Balance

Interest Rate

5.25 % interest on daily

Minimum Balance of NRs.

10,000.00

6.10 % interest on daily Balance

upto NRs. 500,000.00

6.35% interest on daily Balance

upto NRs. 5 Million

6.60% interest on daily Balance

above NRs. 5 Million

FIXED DEPOSITS

Minimum balance: NRs 10,000.00

Minimum Interest Rate

14 days 3%

1 month 3.50%

3 months 4.00%

6 months 4.50%

1 year 5.75%

13 - 24 Months 6.25%

Table 3: Product and services