international financial integration and crisis intensity andrew k. rose uc berkeley, nber and cepr...

Post on 20-Dec-2015

217 views

TRANSCRIPT

International Financial Integration and Crisis Intensity

Andrew K. RoseUC Berkeley, NBER and CEPR

(collaborator with Mark Spiegel)

1ASEAN Presentation, Seoul December 2010

What Caused the 2008-09 Crisis?

• Defining macroeconomic event of generations– A recent “Natural Experiment”

• Did International Financial Integration play any significant role?– If so, multilateral or bilateral ties matter most?– If bilateral, which country matters most for

exposure/insurance?• Big Asian Economies: China; Japan; Korea.• United States

ASEAN Presentation, Seoul December 2010 2

Non-Structural Methodology

• MIMIC (multiple-indicator, multiple cause) model explicitly incorporate difficulties in observing relative crisis severity– Treats crisis as a latent variable– Observed with error as function of observable

manifestations– Also do OLS, graphical analysis

• Sample is cross-section of 85 countries

3ASEAN Presentation, Seoul December 2010

Crisis Performance is Latent Variable Mapping Observable Causes to

Observable Manifestations• 4 Manifestations from 2008-09: equity market

collapse, exchange rate devaluation, economic growth, and change in creditworthiness

• Compare to 2006 vulnerabilities (causes)– National causes– International financial linkages

4ASEAN Presentation, Seoul December 2010

Results, 1

• Plausible estimates of relative severity of crisis– Ex: Iceland and Latvia identified as exceptionally bad– Most Asians have mild crises

• Use literature to find three “national” crisis causes (determinants from 2006)1.Real Income (negative “progressive” effect”)2.Financial Market Regulation (looser → worse crisis)3.Current Account (% GDP) (deficit → worse)

5ASEAN Presentation, Seoul December 2010

Results, 2

• Less success linking crisis to integration variables– No multilateral variables consistently enter at

statistically significant levels– Most bilateral variables irrelevant too

– Little effect of: a) banking exposure; b) debt denomination; c) Fed swap lines

– Asset exposure (CPIS) matters, but not strong– More exposure to US → more mild crisis!

ASEAN Presentation, Seoul December 2010 6

Data

7ASEAN Presentation, Seoul December 2010

Empirical Strategy

• Exploit recent international cross section– “Great Recession” a “natural experiment”

• Don’t have to rely on time-series/panel data

– All information country-specific initially– Then add linkages between countries

– National characteristics may influence vulnerability to foreign shocks

• Medical analogy: common shocks vs. contagion

8ASEAN Presentation, Seoul December 2010

Data Span

• As crisis hit all types of countries, include both developed and EMEs– All countries >$10,000 per capita GDP– All countries >$4,000 per capita GDP, plus

population > 1 million (WB: upper middle income)– Maximum of 85 countries in sample

• Use only publicly-available series available for reasonable span of countries

9ASEAN Presentation, Seoul December 2010

Sample of CountriesArgentina Chinaa Finland Ireland Lithuania Norway Singaporea Trinidad &

TobagoArmeniaa Colombia France Israel Luxembourg Oman Slovakia Tunisia

Australiaa Costa Rica Georgiaa Italy Macedonia Panama Slovenia Turkeya

Austria Croatia Germany Jamaica Malaysiaa Papua New Guineaa

South Africa UK

Barbados Cyprus Greece Japana Malta Paraguay Spain Ukraine

Belgium Czech Rep Guyana Kazakhstana Mauritius Peru Sri Lankaa United Statesa

Botswana Denmark Hong Konga Koreaa Mexico Poland St. Kitts & Nevis

Uruguay

Brazil Ecuador Hungary Kuwait Morocco Portugal Swaziland Venezuela

Bulgaria Egypt Iceland Kyrgyzstana Namibia Romania Sweden

Canada El Salvador Indonesiaa Latvia Netherlands Russia Switzerland

Chile Estonia Iran Lebanon New Zealanda Saudi Arabia Thailanda a = Asian

ASEAN Presentation, Seoul December 2010 10

Differences in Crisis Severity (Manifestations/Consequences)

• Crisis intensity only observed with error [e.g. Berg, et al (2004)]– Abundant measurement error likely

• Initially model severity as a latent variable linked to four observable indicators for 2008-091.GDP growth (%)2.Change in National Equity Markets (stocks, %)3.Change in multilateral SDR exchange rate (%)4.Change in Euromoney country credit rating

• March 2008 - March 2010

11ASEAN Presentation, Seoul December 2010

Table 1: Crisis Manifestations2008-09

changes in:Stock

Market Euromoney

Credit RatingPrice of

SDRReal GDP

1 Iceland -91.4 -23.4 100.3 -5.6

2 Russia -81.2 -1.6 22.2 -2.7

3 Bulgaria -75.8 -6.4 1.7 .7

4 UAE -69.9 -4.4 -.8 4.5

5 Cyprus -66.9 -1.0 1.4 1.8

6 Macedonia -64.3 -3.7 1.6 4.1

7 Slovenia -64.1 -4.0 1.4 -4.6

8 Croatia -61.7 5.2 1.3 -3.5

9 Greece -58.3 -9.8 1.4 -.0

10 Bermuda -57.3 -15.3 -.8 .4

ASEAN Presentation, Seoul December 2010 12

Methodology

13ASEAN Presentation, Seoul December 2010

MIMIC model

• MIMIC model consists of two sets of equations: (1)

(2)

where is crisis indicator, is an observation for potential crisis cause; is latent variable representing severity of the crisis (or lack thereof in our case), and and are well-behaved disturbances

• Equation (1) links observable (2008-09) manifestations of the crisis to latent variable

• Equation (2) links latent variable to (2006) crisis causes

, ii j j iy

,i k i k ix

,i jy ,i kxi

i i

14ASEAN Presentation, Seoul December 2010

Characteristics of MIMIC Model• Substitute (2) into (1), eliminate latent variable• MIMIC model is then a system of J (=4) equations

with right hand sides restricted to be proportional

• With normalization, system is identified– Normalize on equity returns (Breusch)

• Desirable feature of MIMIC model is ability to systematically address measurement error

• Estimate with STATA using GLLAMM model [Rebe-Hesketh, et al (2004)]

15ASEAN Presentation, Seoul December 2010

What Determinants are Associated with Crisis Incidence?

• Survey literature (Rose and Spiegel 2009a, 2009b, 2010), find three determinants

• Use these as national controls throughout1. Real Income (negative effect)2. Credit Market Regulation (looser is worse)3. Current Account, % GDP (higher is better)

ASEAN Presentation, Seoul December 2010 16

Sensitivity Analysis

1. Drop Exchange Rate Consequences2. Restrict to Asian/Pacific Countries (and USA)3. OLS with growth as dependent variable4. OLS with stock market change as regressand

ASEAN Presentation, Seoul December 2010 17

MIMIC Estimates with ControlsControl MIMIC

DefaultDrop

ExchangeRate

Conseq.

Asian/Pacific

OLS, Growth

OLS, Stocks

Log 2006 real GDP pc

-12.6**(4.36)

-13.5**(4.4)

-6.0(3.2)

-3.0**(.8)

-13.2**(3.9)

2006 Credit Market Regulation

-2.5(3.5)

-2.0(3.5)

-.4(3.1)

-2.2**(.7)

-1.4(2.8)

2006 Current Account, %GDP

.56*(.26)

.53*(.26)

-.22(.27)

.21**(.06)

.53*(.25)

ASEAN Presentation, Seoul December 2010 18

Findings consistent with Literature

• Real GDP per capita has negative, significant effect (the “progressive” crisis)

• More Credit Market Regulation associated with milder crisis (Giannone et al), but rarely significant

• Current Account surpluses associated with milder crises

ASEAN Presentation, Seoul December 2010 19

Crisis was Progressive

ASEAN Presentation, Seoul December 2010 20

-10

0-50

050

10

0

7 8 9 10 11

Stock Market Change

-50

050

10

0

7 8 9 10 11

Depreciation against SDR-2

0-1

00

10

20

7 8 9 10 11

Country Credit Rating Change

-20

-10

010

20

7 8 9 10 11

GDP Growth Rate

Log Real GDP per capita 2006

2008-09 Crisis Manifestations against Real Income

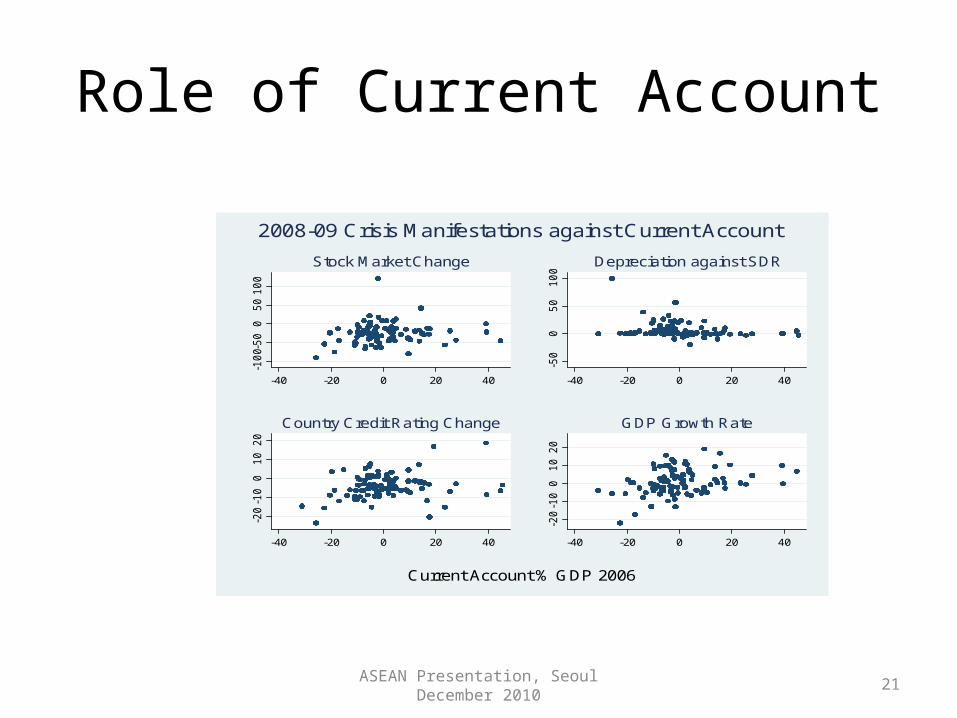

Role of Current Account

ASEAN Presentation, Seoul December 2010 21

-10

0-50

050

10

0

-40 -20 0 20 40

Stock Market Change

-50

050

10

0

-40 -20 0 20 40

Depreciation against SDR-2

0-1

00

10

20

-40 -20 0 20 40

Country Credit Rating Change

-20

-10

010

20

-40 -20 0 20 40

GDP Growth Rate

Current Account % GDP 2006

2008-09 Crisis Manifestations against Current Account

International Financial Integration

22ASEAN Presentation, Seoul December 2010

Multilateral Financial Linkages

• Examine (6) imperfect multilateral proxies for 2006 financial integration, a)-e) as %GDP– a) net foreign assets; – b) external debt; – c) short-term external debt; – d) financing via international capital markets; – e) international reserves. – f) currency union dummy

23ASEAN Presentation, Seoul December 2010

Unchanged Methodology

• Always include (3) national causes• Same sensitivity analysis

ASEAN Presentation, Seoul December 2010 24

Role of MultilateralFinancial Linkages

Multilateral Linkages2006, %GDP

MIMICDefault

Drop Exch.Rate

Conseq.

Asian/Pacific

OLS,Growth

OLS,Stocks

Net Foreign Assets

-8.3(6.3)

-8.6(6.3)

3.9(4.8)

.29(1.28)

-9.0(8.0)

Debt .11(.31)

.03(.32)

.05(.10)

.00(.04)

.01(.31)

Short-Term Ext. Debt

-1.0(.8)

-1.0(.8)

-5.6**(1.4)

-.36*(.14)

-.98(.55)

Fin via Int’lCapital Mkts

-.9(1.1)

-1.0(1.1)

-1.8*(.8)

.12(.18)

-1.11(.86)

Reserves -.2(.2)

-.2(.2)

.3(.2)

-.00(.03)

-.18(.16)

Currency Union

-3.9(7.5)

-4.6(7.5)

n/a -.48(1.41)

-4.3(4.4)

ASEAN Presentation, Seoul December 2010 25

Poor Multilateral Results

• Little effect of international financial integration, after taking into account (3) domestic factors– 30 coefficients; one significantly different from

zero at 1%; two more at 5%.– Short-Term External Debt/GDP consistently

negative effect (Blanchard et al)• Significant 2/5 times

ASEAN Presentation, Seoul December 2010 26

Proceed on to Bilateral Linkages

• Exposure to Individual Countries• Different Sectors:

– All External Assets (CPIS)• Debt, Long-Term Debt as well

– Bank Loans (BIS)– Debt Denomination (WB)– Fed swap-lines

ASEAN Presentation, Seoul December 2010 27

(17) Measures of Bilateral Financial Linkages

• Share of overseas assets held in USA (as proportion of all overseas wealth)– Also consider China, Japan, Korea

• Also consider debt, long-term debt

– BIS Consolidated banking data• Available for Japan, USA

– PPG debt denominated in yen/$– Finally, (endogenous) existence of Fed swapline

28ASEAN Presentation, Seoul December 2010

CPIS: American Exposure Helps!Bilateral Linkages(2006)

Exposure to

MIMICDefault

Drop Exchange

Rate Conseq.

Asian/Pacific

OLS,Growth

OLS,Stocks

CPIS AssetShare

USA .44**(.12)

.48**(.12)

.10(.12)

.02(.03)

.48**(.10)

CPIS AssetShare

Japan 1.5(1.2)

1.9(1.2)

.11(.61)

.36(.20)

1.9(1.5)

CPIS AssetShare

Korea .26(2.80)

.3(3.1)

4.7(2.6)

-.18(.61)

.5(2.9)

CPIS AssetShare

China 4.7(7.8)

4.7(7.8)

1.5(2.8)

2.79**(.56)

4.7(4.2)

29ASEAN Presentation, Seoul December 2010

Special Role of US

• Crisis originated in US• Provider of International Reserves• Monetary Anchor (especially in Asia)• Dollar Appreciation in 2008• But exposure to US assets associated with

more mild crises

ASEAN Presentation, Seoul December 2010 30

Robust to Exact Asset ConsideredBilateral Linkages

Exposure to MIMICDefault

Drop ExchRate

Asian/Pacific

OLS,Growth

OLS,Stocks

CPIS DebtShare

USA .39**(.11)

.43**(.11)

.17(.14)

.02(.03)

.44**(.09)

CPIS DebtShare

Japan -.62(1.27)

-.59(1.34)

.0002(.0007)

.39(.22)

-.60(1.52)

CPIS DebtShare

Korea -.38(2.56)

-.27(2.54)

2.3(2.1)

-.10(.41)

-.2(2.2)

CPIS DebtShare

China 1.0(1.2)

1.0(1.2)

.4(1.0)

.40**(.08)

1.06*(.44)

CPIS LongDebt Share

USA .38**(.12)

.44**(.12)

.26(.19)

.02(.03)

.45**(.10)

CPIS LongDebt Share

Japan -1.74(1.5)

-1.6(1.6)

.0001(.0009)

.16(.22)

-1.6(1.7)

CPIS LongDebt Share

Korea .17(2.05)

.30(2.04)

2.4(1.7)

-.08(.30)

.3(1.6)

CPIS LongDebt Share

China 1.1(1.1)

1.0(1.1)

2.0(3.4)

.43(.07)

.98*(.47) 31ASEAN Presentation, Seoul December 2010

Graphical Evidence: US Exposure

ASEAN Presentation, Seoul December 2010 32

-10

0-50

050

10

0

0 20 40 60 80

Stock Market Change

-50

050

10

0

0 20 40 60 80

Depreciation against SDR-2

0-1

00

10

20

0 20 40 60 80

Country Credit Rating Change

-20

-10

010

20

0 20 40 60 80

GDP Growth Rate

Percentage External Assets in USA, CPIS 2006

2008-09 Crisis Manifestations against Asset Exposure to USA

Japanese Exposure(note x-scales)

ASEAN Presentation, Seoul December 2010 33

-10

0-50

050

10

0

0 2 4 6 8 10

Stock Market Change

-50

050

10

0

0 2 4 6 8 10

Depreciation against SDR-2

0-1

00

10

20

0 2 4 6 8 10

Country Credit Rating Change

-20

-10

010

20

0 2 4 6 8 10

GDP Growth Rate

Percentage External Assets in Japan, CPIS 2006

2008-09 Crisis Manifestations against Asset Exposure to Japan

Korea (note x-scales)

ASEAN Presentation, Seoul December 2010 34

-10

0-50

050

10

0

0 1 2 3 4 5

Stock Market Change

-50

050

10

0

0 1 2 3 4 5

Depreciation against SDR-2

0-1

00

10

20

0 1 2 3 4 5

Country Credit Rating Change

-20

-10

010

20

0 1 2 3 4 5

GDP Growth Rate

Percentage External Assets in Korea, CPIS 2006

2008-09 Crisis Manifestations against Asset Exposure to Korea

China (note x-scales)

ASEAN Presentation, Seoul December 2010 35

-10

0-50

050

10

0

0 .5 1 1.5 2

Stock Market Change

-50

050

10

0

0 .5 1 1.5 2

Depreciation against SDR-2

0-1

00

10

20

0 .5 1 1.5 2

Country Credit Rating Change

-20

-10

010

20

0 .5 1 1.5 2

GDP Growth Rate

Percentage External Assets in China, CPIS 2006

2008-09 Crisis Manifestations against Asset Exposure to China

BIS Consolidated Banking Claims,Debt Denomination, Fed Swaplines

Linkage(2006)

Exposure to Default Drop Exchange Rate

Consequence

Euromoney, not II

Condition on C/acc (%GDP),

not size

Condition on NFA (%GDP), not size

BIS ConsolidatedBanking Share

USA 191.(122.)

202.(122.)

-224.(212.)

-13.6(18.8)

207.**(69.)

BIS ConsolidatedBanking Share

Japan 59.(48.)

57.(49.)

-18.(33.)

10.0**(3.8)

57**(18.)

% PPG Debtin $

USA .11(.24)

.08(.23)

n/a -.01(.04)

.07(.25)

% PPG Debtin yen

Japan .15(.50)

.12(.50)

-.11(.27)

.10(.09)

.10(.28)

Federal ReserveSwap Line

USA 7.2(8.1)

7.2(8.2)

-1.7(7.0)

-.8(1.6)

7.5(6.7)

36ASEAN Presentation, Seoul December 2010

Outliers Important for Japanese BIS consolidated banking data

ASEAN Presentation, Seoul December 2010 37

-10

0-50

050

10

0

0 10 20 30 40 50

Stock Market Change

-50

050

10

0

0 10 20 30 40 50

Depreciation against SDR-2

0-1

00

10

20

0 10 20 30 40 50

Country Credit Rating Change

-20

-10

010

20

0 10 20 30 40 50

GDP Growth Rate

Percentage Banking Assets in Japan, BIS 2006

2008-09 Crisis Manifestations against Bank Exposure to Japan

American Analogue

ASEAN Presentation, Seoul December 2010 38

-10

0-50

050

10

0

0 5 10 15 20

Stock Market Change

-50

050

10

0

0 5 10 15 20

Depreciation against SDR-2

0-1

00

10

20

0 5 10 15 20

Country Credit Rating Change

-20

-10

010

20

0 5 10 15 20

GDP Growth Rate

Percentage Banking Assets in USA, BIS 2006

2008-09 Crisis Manifestations against Bank Exposure to USA

Some Sensitivity, Bigger Mystery

• Why does exposure to America (most likely epi-center of 2008 crisis) seem to help?– Special Advantage of “Exorbitant Privilege”?– Interesting Future Research topic

• Still, results not very strong– Most measures insignificant

• No evidence that Asian links helped in crisis

39ASEAN Presentation, Seoul December 2010

Summary and Conclusion

40ASEAN Presentation, Seoul December 2010

Examine causes and consequences of 2008-09 Financial Crisis

• MIMIC Methodology explicitly confronts fact that “crisis severity” observed with error

• Account for national crisis causes that work in literature

• Cross-sectional focus: only trying to explain relative incidence, not timing

41ASEAN Presentation, Seoul December 2010

Message

• Financial Integration across countries not very important in understanding crisis incidence

• Seems to provide little insurance (though may also limit contagion)

• Multilateral measures especially weak• Bilateral American Financial Influence:

Enduring Impact

ASEAN Presentation, Seoul December 2010 42